to department of marketing, faculty of ... bosah,.pdfof selected commercial banks in enugu and...

TRANSCRIPT

1

INFORMATION AND COMMUNICATION TECHNOLOGY AS A

TOOL FOR IMPROVING BANKING SERVICES: AN EVALUATION

OF SELECTED COMMERCIAL BANKS IN ENUGU AND ANAMBRA

STATE

BEING DISSERTATION REPORT SUBMITTED IN PARTIAL

FULFILLMENT OF THE REQUIREMENT FOR THE AWARD OF

MASTERS DEGREE IN BUSINESS ADMINISTRATION (MBA

MARKETING)

TO

DEPARTMENT OF MARKETING,

FACULTY OF BUSINESS ADMINISTRATION, UNIVERSITY OF NIGERIA, ENUGU CAMPUS

BY

MAUREEN BOSAH,

2

REG NO: PG/MBA/07/46607

APRIL, 2009

3

TITLE PAGE

INFORMATION AND COMMUNICATION TECHNOLOGY AS A

TOOL FOR IMPROVING BANKING SERVICES: AN

EVALUATION OF SELECTED COMMERCIAL BANKS IN

ENUGU AND ANAMBRA STATE

TO

DEPARTMENT OF MARKETING, FACULTY OF BUSINESS

ADMINISTRATION UNIVERSITY OF NIGERIA

ENUGU-CAMPUS

BY

MAUREEN BOSAH,

REG NO: PG/MBA/07/46607

4

SUPERVISOR: PROF. J.O ONAH

APRIL,2009.

5

CERTIFICATION

I hereby certify that this dissertation report was approved by the

department of marketing for Maureen Bosah with Reg. No:

PG/MBA/07/46607 and was carried out successfully under my

supervision in accordance with the regulations for the award of masters

of Business Administration Degree (MBA) in marketing, at the University

of Nigeria, Enugu Campus.

-------------------------- ------------------------

Prof. J.O. Onah Dr. (MRS.) Nnabuko

Project Supervisor Head of Department

Date:--------------------- Date:--------------------

---------------------------

MAUREEN BOSAH

PG/MBA/07/46607

6

DEDICATION

This dissertation is dedicated to God Almighty, the giver of all knowledge

and understanding and to my three children Nonso, Nwando and

Obinna.

7

ACKNOWLEDGMENT

I must not fail to acknowledge my profound gratitude to Almighty God

for the realization of this dream.

I have incurred immeasurable debt of gratitude to a number of people

without whose guidance and co-operation, my effort would have been

impeded. My appreciation goes to my supervisor, Prof. J.O. Onah, who

guided and saw this research work to its successful end.

Special thanks to my course mates who through their availability has

resulted to my consistency in the study, indeed, they have encouraged

me and I am very grateful.

I must not fail to express my appreciation to my family for their prayers,

love, advice and above all financial and moral support.

I shall forever remain grateful to God for his mercies and direction

which has always seen me through.

8

Abstract

The banking industry went neck-deep into adoption information technology as tool for improving banking services. It was in realization of this that this evaluation study was carried out, to ascertain if the adoption of ICT has actually improved banking services or not. Nigeria introduced a structural adjustment programme (SAP) in 1986 to restrict not only the foreign dependent industrial base, but also to tackle her other economic problems, the liberalization and deregulation of the banking industry. To carry out the study, data were collected through questionnaires and

analyzed the hypotheses tested. The result showed that there has

been more improvement in banking industry among the new

generation banks than the old ones. This is because many of the

new generation banks are computerized and integrated by

network. Although customers still complain because they want

banks to have automatic teller machine services and other facilities

that will enhance their services to customers.

9

TABLE OF CONTENTS

Title page:………………………………………………………………………………….i

Certification:………………………………………………………………………………ii

Dedication:………………………………………………………………………………..iii

Acknowledgement:…………………………………………………………………….iv

Abstract:…………………………………………………………………………………..v

Table of contents:………………………………………………………………………ix

List of tables:……………………………………………………………………………..x

CHAPTER ONE

Introduction

1.0 Background of the study:……………………………………………………1

1.1 Statement of the problem:………………………………………………….4

1.2 Objective of the study:……………………………………………………….6

1.3 Hypotheses:………………………………………………………………………7

1.4 Scope and limitations of the study:………………………………………8

1.5 Significance of the study:……………………………………………………8

1.6 Definition of key teams:……………………………………………………..9

Reference:……………………………………………………………………………….12

10

CHAPTER TWO

Review of related literature

2.1 Marketing philosophy and banking industry ………………………13

2.2 Definition of information and communication technology ……15

2.3 Concepts ICT:…………………………………………………………………16

2.4 Meaning of improved banking services:………………………………21

2.5 Role of ICT in the banking industry:…………………………………..22

2.6 Role of ICT in segmentation and niche marketing:………………29

Reference ………………………………………………………………………………33

CHAPTER THREE

Research design and methodology

3.1 Design ……………………………………………………………………………37

3.1.1. Banking customers:………………………………………………………38

3.1.2. Banking staff/management:………………………………………….39

3.1.3. Questionnaire design:…………………………………………………..39

3.2 Methodology:……………………………………………………………….39

3.2.1 Study population:…………………………………………………………39

3.2.2 Determination of sample size:……………………………………….41

3.2.2.1 Use of stratified sampling:…………………………………………….42

11

3.2.2.2 Use of statistical formula:……………………………………………..42

3.2.3.1 Primary data:…………………………………………………………..43

3.2.3.2 Secondary data:………………………………………………………44

3.2.4 Questionnaire administration:……………………………………44

3.2.5 Validation of research instrument:……………………………45

3.2.6 Analytical technique/tool:…………………………………………45

3.2.6.1 Hypotheses testing:…………………………………………………46

3.2.7 Decision rule:…………………………………………………………46

Reference:………………………………………………………………………………47

CHAPTER FOUR

Data presentation and analysis

4.1 Data presentation:……………………………………………………………48

4.2 Hypotheses testing:………………………………………………………….56

CHAPTER FIVE

SUMMARY OF FINDINGS, RECOMMENDATIONS AND

CONCLUSION

5.1 Summary of findings:……………………………………………………….65

5.2 Recommendations:…………………………………………………………..68

5.3 Conclusion:………………………………………………………………………71

Bibliography:……………………………………………………………………………73

12

Appendix A Disaggregated data:………………………………………………..76

Appendix B ……. Questionnaire:…………………………………………………81

Appendix C ……. Map that shows the location of study:………………..84

LIST OF TABLES

4.1 Distribution of response for instrument:…………………………… 49

4.2 Waiting time for cash withdrawal:……………………………………..50

4.3 Clearing period of in-house cheques:………………………………… 51

4.4 Waiting time for obtaining draft or manager’s cheque:…………52

4.5 Length of time for fund training:……………………………………….53

4.6 Regularity in getting statement of account:………………………..54

4.7 Unavailable banking services:………………………………………. ….55

13

QUESTIONNAIRE 1: FOR BANK CUSTOMERS

1. Are you a customer of bank? Yes No

2. How long have you been a customer bank?

Below 5 years 5-10 years more than 10 years

3. What is the name of your bank? _____________

4. What is the location of your bank Enugu Onitsha

5. Is your bank computerized? Yes No

6. Before computerization, it used to take you how long to cash your

cheque?

10-20 mins 20-40 mins 40-60 mins More than I

hour

7. After computerization it now takes you how long to cash your

cheque?

10-20 min 20-40 mins 40-60

More than I hour

8. Before computerization, it used to take you how long to clear your

in house

cheque? I day 2 days 3 days 7 days 13 days

9. After computerization, it now takes you how long to clear your in-

house

cheque? 1 day 2 days 3 days 7 days 13 days

14

10. Before computerization, it used to take you how long to obtain a

draft/bankers cheque? 1-2 hours more than 2 hours less

than 10 mins

11. Since your bank got computerized, do you now get your statement

of accounts regularly? Yes No

12. Are there other banking services that your bank is not rendering,

but which you would want from them? Yes No

QUESTIONNAIRE II: FOR BANK MANAGEMENT

1. What is the location of your bank? Enugu Onitsha

2. For how long have you been working in the banking industry?

1-5 yrs 6-10 yrs more than 10 years

3. What is your position in your bank? Supervisor Officer

Manager Executive

4. Is your bank computerized? Yes/No

5. Are you on-line? Yes/No

6. What other facets of Information Technology are available to your

bank?

i) ………………………. (ii) …………………….

iii) ………………………. (iv) ……………………

15

Appendix B

Department of Marketing

University of Nigeria Enugu Campus 6th March,2010

QUESTIONNAIRE

Dear Sir/Madam,

I am a postgraduate student of the above institution. I am

undertaking a research on information technology as a tool for improving

banking services.

Please your co-operation in giving objective answer to these

questions will depend to a very large extent the success of this study.

The information provided by you will be treated with utmost

confidentiality please answer the questions truthfully as you can and to

the best of your knowledge,

Thanks for assisting.

16

Yours faithfully,

Maureen Bosah

The areas marked with (x) indicates the state where the

researcher carried out the research work.

17

CHAPTER ONE

INTRODUCTION

1.0 BACKGROUND OF THE STUDY

It is surely beyond question that Nigeria today faces formidable

difficulties. At the forefront of public concern is the unprecedented level

of unemployment, the ever-increasing public debt and the low absorptive

capacity of the economy.

Compounding these problems are regional and sectoral imbalances that

manifest the problem of workless ness, but which also extend far beyond

this as de-industrialization takes its toll? In the face of this is a deep-

seated international recession which is having the effect of tightening

competitive pressures and for which Nigeria does not seem to have

adequate response. Despite these problems Nigerians look forward to

the future with enthusiasm and an unflinching hope for better days.

Their faith is hinged on technology, especially in the area of

INFORMATION AND COMMUNICATION TECHNOLOGY (ICT)

Information and Communication Technology (ICT) as part of a low-cost

producer strategy has a number of effects. It can reduce the number of

18

clerical staff by performing the tasks, which these people do, permit

better utilization of facilities and resources and accounts receivables by

improving an organization’s ability to analyse and control these areas. It

can also provide a better utilization of materials and lower wastage. The

benefits to management in terms of having better decision-making and

better control over expenditures, and being able to correct errors quickly

are obvious. It also aids and facilitates product differentiation, which is a

good strategy that gives a marketer an edge over his competitors. It has

been used in a variety of industries and more especially in the service

industries such as the banks. Information and communication technology

can be used to differentiate products in a number of ways. It can be a

significant component of the product itself or it can provide a service

that is somehow unique and consequently can help attract consumers to

your product. It can also help differentiate products by significantly

reducing the lead-time for product development, customization or

delivery. It may also give a higher level of customers’ satisfaction. For

example, a number of banks and investment houses are now offering a

variety of investment services and portfolio management systems that

run on personal computers.

19

The history of the Nigerian banking system shows that expatriate banks

monopolized banking business up to 1928. These expatriate banks were

operated to achieve the objectives of their home offices, with little or no

regards to the needs of the local environment and entrepreneurs. To

break their monopoly and discriminatory practices, a handful of patriotic

Nigerians established indigenous banks. However, many factors which

would have ensured the soundness of the operations and effective

growth of these banks, such as adequate qualified personnel, right bank

orientation and good legal framework, among others were neither in

place nor though necessary (Ologun, 1994, p. 313). It was not surprising

that many of these banks collapsed with the rapidity with which they

were established (Adekanye, 1986, p.4).

Nevertheless, with political autonomy of the country and the

establishment of a central bank and other financial institutions, things

substantially changed as compared with the expatriate-banking era.

Consequent upon the adoption of the Structural Adjustment Programme

(SAP) in 1986, and the subsequent deregulation of the economy, there

was a phenomenal change in the banking industry in particular and the

economy as a whole. For instance, between 1986 and 1991, a total of 79

20

new banks with 824 bank branches opened for business (Oresotu, 903,

p. 11), bringing the total number of banks and their branches to 119 and

2107, respectively.

In many Nigerian banks’ branches today, people still queue up for

upwards of three hours to withdraw any amount from their accounts.

And should there be a need to obtain a draft, the request for same

should be submitted in the morning hours while collection will be in the

late afternoon hours, if not the following day. As a result of the delay in

obtaining banking services, most Nigerians still carry about huge

amounts of money for their transactions often facing the gauntlet of the

armed robbers. This is deplorable, more especially when globalization

and integration of world businesses through the use of ICT is faitly

changing the face of business transition, a race in which the Nigerian

banking industry cannot afford to be left out.

1.1 STATEMENT OF THE PROBLEM

Banking is basically a service industry operated by human beings,

for the benefit of the general public. As such it is natural that the

services provided by banks cannot be 100 percent perfect, and should

not be at zero level either. Customers’ discontentment stem most

21

especially from unending hours wasted in the banks to withdraw or

deposit their money; delayed, irregular and incorrect rendition of bank

statements of accounts; unstandardised accounting practices,

procedures, codes and classifications; delay in the clearance of cheques

lodged in by customers; and inflation of interest, charges and other

irregular charges, among others. It is in an effort to change this situation

that the Nigerian banking industry, against all odds, has gone neck deep

into the adoption of Information Communication Technology as sine qua

non for to improving banking services. Now, having adopted it for

effective and efficient service delivery, can it be arsented that the

situation has changed for the better?

The Nigerian banking industry was known for its under-development,

inexpensiveness and congestion because it was geographically

constrained. Banking services such as foreign exchange arbitration and

futures trading were all inhibited due to non-adoption of ICT. Now that it

is part and parcel of the system, has there been any change for the

better, and if not, why? This is another problem of this work. The next

problem relates to lack of effective financial intermediation, problem of

22

product differentiation and/or customization, and segmentation and

targeting. How has the adoption of it affected this?

1.2 OBJECTIVES OF THE STUDIES

The broad objective of this research, based on the statement of

the problem therefore, is to determine if IT has played any role as a tool

for improving banking services in Nigeria.

Specifically, the research seeks to achieve the following objectives:

1. To find out if the consumers of banking services feel that they

are now promptly attended to when they want to withdraw or

deposit their money than before.

2. To find out if the customer gets their statements of account

regularly and in time too.

3. To find out if there is any improvement or enhancement in the

customers’ foreign exchange transactions; especially as it

relates to remittance of foreign currencies to or from overseas

sources.

4. To find out if there are still services which customers want but

which banks cannot render.

23

1.3 HYPOTHESES

Based on the foregoing, the following hypotheses are formulated:

1. H0: Despite the adoption of ICT by the Nigerian banking industry,

customers still cannot withdraw their money in shorter period of

time than before.

Hi: With the adoption of ICT by the Nigerian banking industry,

customers can now withdraw their money in less time than before.

2 Ho: Despite the adoption of ICT by the Nigerian banking industry,

customers still cannot get their statement of accounts regularly

and timely.

Hi: With the adoption of by the Nigerian banking industry, customers

now get their statements of accounts regularly and timely.

3 Ho: Despite the introduction of ICT by the Nigerian banking

industry, bank customers still cannot remit or receive foreign

currencies to or from overseas sources in shorter period of time

than before.

Hi: With the introduction of ICT by the Nigerian banking industry, bank

customers now remit or receive foreign currencies to or from

overseas sources in less time than before.

24

1.4 SCOPE AND LIMITATIONS OF THE STUDY

The study covers only the commercial banks in Nigeria. However,

our survey is carried out on commercial banks in Enugu and Anambra

States. Emphases are on how ICT has been used as a tool to improve

banking services in Nigeria.

The main limitations of this work are cost and time resources.

This study is only surveying the banks in Enugu and Anambra States. In

as mush as the bank branches take instructions from their head offices;

there are the possibilities of regional imbalances and therefore

differences. But the cost of carrying out a countrywide survey is not a

thing that can easily be afforded by a student. In view of this limited

scope of the study. The findings of this work should .be used with

caution.

1.5 SIGNIFICANCE OF THE STUDY

This study was undertaken in partial fulfillment of the requirement

for the award of Master of Business Administration (MBA) degree of

University of Nigeria, Enugu Campus. Certainly, this study will add to

existing literature in this topic. Therefore it will serve as reference point

25

or a springboard for further research, more especially since it is changing

and introducing new facets over time?

Banking in Nigeria stands to gain immensely from this work because the

banks may become aware of their customers’ feelings about their

services. It is not just enough adopting ICT to facilitate operations and

improve banking services, but being in a position to ascertain if the

programme is poorly implemented in the face of lack of the co-operant

factors which will make the objectives of the adoption vitiated.

Therefore, the banks will gain from this work.

1.6.0 SUB-TITLE: DEFINITION OF KEY TERMS

1.6.1. ON-LINE: This is a situation where an organization has

computerized her operations and has the computers and terminals

available for use for their operations. Any information available in the

database can be assessed by any operator.

1.6.2. BATCHING: In some organizations, operations are

computerized but the computers are not available for use. In such

situations, organizations (or branch of it) go to the computer, key in their

data into the computer, process them and obtain the required

26

information on a hard copy (print outs), in the form of statements,

reports and even graphs.

1.6.3. NETWORK: This is a configuration or linking of computers

so that information available at one workstation is equally available to all

others.

1.6.4 Local Area Network: Is smaller in the area of coverage, such

as all the areas and departments of a particular office, under the same

roof. The network comes about by the fact from any particular

workstation in the office; any person can assess any information from

the data-base, subject to the person’s password level. In such a

situation, organizations, you have perhaps only one computer with many

terminals.

1.6.5 Wide Area Network, all the offices of the same organization

in the different states are linked together to .the same data-base. From

any workstation, in any state, you can assess the data in the data-base.

1.6.6 The Internet: This is a computer network of all other

networks all over the world, that coffers both data, graphics, audio and

visual opportunities to those who are hooked-on to it on-line.

27

1.6.7 The Internet-Connectivity: For internet to be worldwide

network, it must be by Transmission Control Protocol/Internet Protocol

(TCP/IP) networking protocol. The main difference between the Internet

and WAN is that with Internet, connectivity must be by TCP/IP

networking protocol.

1.6.8 ELECTRONIC BANKING: Under an electronic banking

environment, a client of a bank with a personal computer or a terminal in

his house or office, connected in a network to a computer in his bank

can without leaving his office or house, look at his account, because it

appears on his TV console. He can virtually write a cheque without

leaving his office. In the case of customers who are electronically

connected, they can transfer money to each other without involving the

bank personnel. This obviously reduces the work-load of the bank

personnel, and the number of customers who come to the bank for one

service or the other. Technically, the customer-banker ratio reduces and

their efficiency, effectiveness and service improves.

28

REFERENCES

Ologun, S.O. (1994) “Bank Failure in Nigeria: Genesis Effects and Remedies” in Economic and Financial Review CBN vol. 32 No. 3

Adekanye, F. (1986) Practice of Banking vol. 1 London: Collins

Oresetu, F.O. (1992) “Interest Rates Behaviour under A Programme of Financial Reform: The Nigerian Case in Economic and Financial Review CBN vol. 30 No. 2.

29

CHAPTER TWO

LITERATURE REVIEW

2.1 MARKETING PHILOSOPHY AND THE BANKING INDUSTRY

Traditionally, banking is financial intermediation, which involves

movement of funds from surplus areas to deficit areas in the system.

This activity (banking) depends entirely on public confidence in the

system’s soundness and the strength of its products and services.

Theoretically, a bank accepts deposits and grants credit. But a bank does

more than this, hence, the need to have appropriate policies in areas like

product formulation and development, market expansion, advertising,

segmentation, establishment of branches, innovation and selling

(Ezeokafor, 1996, p. 26). To enhance marketing in banking, banking

institutions must address such issues as identification of customers’

financial needs and wants, the development of products specifically

tailored towards the specific needs of a clearly identified target market,

the evolution of a pricing/fee structure suitable for specific services,

strategic expansion of branch network, intelligent research into present

and future financial market needs, and the planning and implementation

of specific marketing programme to attract funds outside the banking

30

system. Ezeokafor summarized his views by saying that marketing

concepts in banks relate to the design and delivery of customer needed

services in such a way that satisfies him, especially as there is fierce

competition between the banking industry and the non banking financial

institutions. Reasoning along the same line with Ezeokafor, Ubong (1997,

p.15) says that today’s economy makes it imperative for banks to

identify the needs and wants of their customers and be able to satisfy

same in products and services. According to him, today, customers do

not just want to save and withdraw. They expect speed, conveniences,

case of transactions, returns and accuracy. Banks, therefore, do not

have a choice for providing technology based products like cards

services, cash transfer through the satellite, tele-banking, electronic

banking and automated machines, to mention just a few products. One

does not need a microscope to see an elephant. The world is not only

fast becoming a global village through ICT, but also are already in the

era of universal banking (Bulama, 1997, p.10). Ovia (1997, p. 33),

Ogbonna (1997, p.16), Omachonn (1997, p. 23), Minima (1997, p. 20),

Adegbite (1997, p. 10) and Oladimeji (1997, p. 13) have all harped on

the indispensable role of ICT in today’s banking service delivery; pointing

31

out the fact that banks that do not adopt ICT are doing so at their own

peril. It is with ICT that banks can remain relevant in the 21st century;

and therefore, banks that refuse to adopt ICT will be left behind in the

global vogue for sophisticated customer delivery services.

Granted that it is a sine qua non in today’s and tomorrow’s banking, one

will at this juncture ask: what is ICT? What do we mean by improved

banking service? What is the role of ICT in improved banking service?

The modest attempt at highlighting what academics, professionals,

bankers and industry analysts have said or done as regards the

questions raised above is the main concern of this chapter. The chapter

will also review what others have said about how ICT can be used as

tool for market segmentation, targeting and niche marketing.

2.2 DEFINITION OF INFORMATION COMMUNICATION TECHNOLOGY

Information Communication Technology (ICT) has becomes the

anecdotal big elephant which every person describes from the angle he

sees it. Though differently described, all of them are still correct. In a

manner (ICT) has become common with its different and varied facets

that people now understand it from the perspective of the facets they

are familiar with. But generally, it has been defined by Oliver and

32

Chapman (1990, p. c10) as the technology, which supports the activities

involving the creation, storage, manipulation and communication of

information together with their related methods, management and

application. Irving and Higgins (1991, p.8) have defined it from the point

of view of the office information systems as a seamless integration of

telecommunications, data processing, and personal computing with

manual business processes; which support key business functions; and

which improves effectiveness, efficiency, and quality of working life.

2.3 CONCEPTS OF ICT AND ITS USES

it is founded on the concept of

a) Information as a major resource;

b) The use of computer-based system;

c) The development of ICT architect are for an organization; and

d) The development and operation of applications.

it is founded on the concept of information as a major resource; and an

essential basis for planning, organizing, managing, administering and

controlling the key operations and activities within a company.

Application programmes translate business requirements into technology

33

system designs, write test and install programmes using special

programming languages such as COBOL or FORTRAN.

The different sides of this elephant include the telephone, photocopier,

microfilm and the computer, to mention a few. And it is note-worthy

here to state that most people today see ICT as nothing but computers.

This view could still be adjudged right because most if not all the

features of other facets of IT-audio, visual, data, graphics are all found

in the computer. And many scholars (Pym, 1985, p. 172 and Evans,

1979, p. 9) consent to the computer being a comprehensive embodiment

of IT, and the fact that the computer is a single startling development in

technology whose impact is felt in every facet of life.

The Uses of ICT are:

a) Data Management: Data management involves the collection,

organization and storage of data required for the conduct of the

business, and the production of information in the form of report or in

response to enquiries. The key data management activities are:

i) Organizing files and records

ii) Locating data quickly in data stores (databases)

iii) Maintaining, updating, manipulating and processing data, and

34

iv) Extracting information from the database, which means carrying

out sorting, calculating and formatting (ie. arranging information in a

predetermined way) activities.

b) Application Development and Management: This is the

process of applying hardware and software to satisfy business/users

needs.

c) Communication Management: This provides for the transfer

and exchange of information between people and within computer

networks.

d) Computer Support to Operations: This is the use of a

computer system to support such activities as computer-aided design

(CAD) and computer aided manufacture (CAM).

e) Integrated Systems: This is the use of computers and

communications technology to help in running integrated systems such

as the following:

i) Computer aided engineering (CAE, also known as CADAM)-

combining computer aided design and aided manufacturing operation.

ii) Computer-integrated manufacturing (CIM)- integrating the various

activities, which together form the total manufacturing process; i.e,

35

design, production engineering, production planning and control,

production scheduling, accounting and distribution.

iii) Flexible manufacturing system (FMS), which integrates all aspects

of machining in one cell.

iv) Management information system (MIS), which provides mainly

financial and out-put or sales information or reports for planning and

control purposes.

v) Point-of-event data capture systems, which move information such

as point-of-order in manufacturing, point-of-sale transaction in retailing

and point-of-reservation in airlines and hotels to a central store where it

can be used for any centralized operation (e.g. inventory control) and

can be accessed by personal computers.

vi) Integrated business support systems, which link such activities as

invoicing, stock control, purchasing, sales and general accounting into

one overall system.

f) Decision Support: ICT supports decision making by collecting,

analyzing and manipulating data in order to model alternatives and

explore the consequences of different courses of actions. Expert systems

36

can be developed which aim to emulate the reasoning of an expert in a

particular domain (area of expertise).

g) Industrial Automation: IT is the basis of industrial automation

on the following fields.

i) Process Control: Tight control is achieved over production

processes by the rapid and continuous inspection of main variables and

the initial speed response to variations. Process control systems use real-

time processing, i.e. data is processed immediately after the event that

occasions it.

ii) Machine Tool Control: Computer numerical control (CNC)

systems prepare the information required to operate machines tools

from design information. In direct numerical control (DNC) the computer

is linked directly to the machine tool.

iii) Office Automation: Office automation involves the use of

personal computers word-processors, desktop publishers, spread sheet,

laser printers and sophisticated telecommunication links such as video

text and electronic mail. The aim is to bring these devices together into

an integrated system, which will speed up the processing and exchange

of information and streamline record keeping.

37

2.4 MEANING OF IMPROVED BANKING SERVICE: It is probably in

the service industry that the whole facets of ICT are needed more; and a

typical of such information driven service industries is the banking

industry. It is in view of this fact that, amid daunting challenges,

Nigerian banking sector has continued to be dynamic in strategic

positioning on the edge of ICT. The Nigerian banking sector has

continued, according to Badaru (1997, p. 19), to witness an aggressive

push towards the acquisition of a suite of ICT solutions to achieve

efficient banking services in the increasingly competitive market place.

Badaru went further to say that pivotal to this migration of the Nigerian

banking industry is the need to achieve an optimal service delivery,

customer satisfaction and ease of operation.

Time is money. This popular saying vis-à-vis the statement of problem

points to an insight into what improved banking service means in

Nigeria. Customers should be able to withdraw their money within few

minutes. It should not take more than fifteen minutes for a customer to

obtain such services as a draft, nor should it take more than two minutes

for a customer to get a confirmation of the balance he/she has in his/her

account. It should not take more than one day to clear in-house

38

cheques. It will not be a luxury if a customer who has an account with

an Enugu branch of a bank goes to Lagos and withdraws money from

the sister branch of his bank. Improved banking services include

remitting or receiving foreign currencies to or from foreign sources

within 24 hours in addition to getting these services courteously.

Improved banking services as seen from other parts of the world

include, in addition to meeting up with the conditions mentioned above,

provision of such services like electronic banking, telephone banking and

automated teller machines, among others. And these services are more

often than not provided for 24 hours in a day, and 7 days in a week. To

these views Nzepome (1997) Nwabuoku (1997), Onuoha (1997), Ezeala

(1997) and Nwosigwelem (1997); in an interview added that these

services should be provided courteously. And these facts, according to

these interviewees constitute efficient and improved banking services.

Customers get what they want in the form and time they want it,

courteously.

2.5 ROLE OF ICT IN THE BANKING INDUSTRY: And to achieve

these improved conditions in banking service delivery, ICT is required,

that the positions held by experts as contained in paragraph four above.

39

The roles of ICT as a tool for improved banking services are summarized

by the report published by the London-based centre for the study of

financial innovation (CSFI), as contained in Taylor (1997, p. 28).

According to this report, ICT achieved efficient and improved banking

service by, among other ways,

i) Stimulating more intense competition in financial service market,

for example by admitting new entrants, making pricing transparent

ad raising service expectation to new levels

ii) Empowering the customer by giving him direct access to market

information.

iii) Removing geography as a constraint on the financial business-

floor-based markets, bank branches, and national preferences.

According to this report also, because the internet (a facet of ICT)

improves the convenience and reduces the cost of financial services, the

main beneficiary of these changes should be the consumer. In an

internet world, the consumer would be able to roam through an

electronic market place, seeking out the best services and prices, and

managing his own financial affairs even being able to run his own

personal bank account. Added to this report, Ebhodage (1995,p.32), and

40

Ogbulie (1997, p. 20) have pointed out that it provides assurance for

integrity and other time honoured ethical attributes of the traditional

banking practices. It provides a huge relief over the paper work and long

queues of accounting hands with their attendant inaccuracies, thus,

increasing productivity. The ICT-driven society worldwide Inter-bank

financial Telecommunication (SWIFT), for instance makes it possible for

users to receive financial messages within 15 seconds of each

transaction (Yahaya, 1997, p.24).

As already observed, bank marketing service market-the (financial)

products are all services. While Judd (1964, pp. 58-59) defined a service

as the object of a transaction, which does not entail the transfer of

ownership of a tangible commodity, Rathmeli (1974, p.7) defined it as

any intangible product bought and sold in the market place. Olakunori

and Ejionueme (1977 p.92) defined it as products which cannot be seen

or touched. They are non-physical in nature. Although neither of these

definitions wrongfully characterizes services, a more comprehensive

definition which emphasized a number of the unique aspects of services

which make them different from (physical) products was opined by

Kenneth and Upah (1983, pp. 231-57). According to them, a service is

41

any task (work) performed for another or the provision of any facility,

product, or activity for another’s use and not ownership, which arises

from an exchange transaction. It is intangible and incapable of being

stored or transported. There may be an accompanying sale of a product.

Thomas (1978, p.161) categorized services according to whether they

are equipment-based or people-based. Equipment-based services can be

completely automated or can contain some degree of labour. Examples

include airlines, computer time-sharing, motion picture theatres, taxis,

vending machine, to mention a few. On the other hand, people-based

services are labour intensive, and workers range from unskilled labourers

to professionals. In the marketing of labour-intensive services, Kenneth

and Upah (Op cit), hold the view that major attentions is focused in the

organization’s overall capabilities, key people and their capabilities

(experience and training), the nature of methods/procedures used by the

firm and the immediate environment that can convey cues as to the

successful provision of these services.

Equipment-based services can be standardized with relative ease, but

people-based services have a high degree of variability. Services

providers should therefore automate to the extent possible and reduce

42

variability of the personal aspect of a service through selection, training

and supervision (Kinnear and Bernhardt, 1983, p.668-697). Through

substitution of equipment for people, service variability can be reduced

or nearly eliminated. In many instances it is advantageous to do this

since according to Allvine (1987, p. 782) standardization of service

quality is important to consumers. Here lies another aspect of the

robustness of the adoption of ICT as a means/tool and part (as in the

use of “smart card”) for banking service delivery. Today, in the Nigerian

banking industry, many banks are taking more “bytes for bodies”,

following the example of Nigerian International Bank (NIB) now Citibank

Nigeria Limited NIB revolutionized banking in Nigeria in 1986 with the

introduction of electronic banking when all the other banks knew nothing

but a long queue of accounting hands. But today the trend has been

reversed: less bodies (human beings) and more bytes (ICT) is now the

in-thing in the banking industry.

By way of recapitulation, quality is an essential part of service marketing,

and high quality is a big advantage in positioning a service. However, the

quality of services is harder to define and measure than is the quality of

(tangible) goods, because service is delivered. That is, quality cannot be

43

measured before the service is delivered. In this regard, Levitt

(1991,pp.194-207) opined that the system and method of service

delivery on itself constitutes an aspect of a particular service.

And to this we add the view that the means and technology with which

the service is delivered also constitute part of the service and its quality.

For instance, consider the case of the use of smart cards in operating

accounts. The card gives the holder an access to cash from the bank

(ATM) at any time of the day. Then card itself is a means of delivering

the service, while at the same time, it is a part of the services and it is

technology of its own, also. Service quality has to be defined from the

viewpoint of the customer. Five components that contribute to

customers’ perceptions of service quality have been identified by Lamb,

Hair and Mc-Daniel (1994 p.344) as tangibles, reliability, responsiveness,

assurance and empathy. Lamb et al however observed that although all

these components contribute to service quality, reliability has been found

to be the most important. To these five components, Valaire and Berry

(1990, pp. 21-22) while agreeing that reliability is the most important of

all the dimensions of service quality, added other dimensions-

competence, courtesy and credibility.

44

A service’s quality is measured by comparing performance with

customers’ expectations (which are influenced by past experience,

personal needs, and word-of-mouth communication) for each of the

performance could either be positive or negative. For example, if a

customer of Bank XYZ expects to wait for fifteen minutes in the banking

hall before receiving the money he has come to withdraw but waits ten

minutes the positive gap increases the customer’s evaluation of the

responsiveness component of service quality, and vice verse. The ability

to perform the desired service dependably, accurately and consistently

by Bank XYZ increases the customer’s opinion about the reliability of the

bank’s service. Therefore, an organization first needs to learn about

customer expectations through marketing research (Rice, 1990,pp.39-

48; and Rose, 1991, pp. 99-100). On the other hand, bad service costs

customers. Many organizations struggle with service because, according

to Bennett and Hymowitz (1992, pp. 202), they have not effectively

tracked customers satisfaction. Traditional market research departments

more often than not gather information on trends, demographic or

market segments without determining whether the customers actually

got what they wanted. A print out will tell you what service are being

45

rendered to customers, but not what service they asked for (that) you

did not have. This therefore necessitates a serious attention, as a matter

of policy for organizations, to issues concerning segmentation, targeting

and niche marketing.

2.6 ROLE OF IT IN SEGMENTATION AND NICHE MARKETING

In marketing generally, segmentation, targeting and niche

marketing tend to go together. These important marketing management

concepts depend on not only information, but on rich and up-to-date

data-bases. Segmentation is disaggregative in its effects (Udeagha,

1995, p. 86) and therefore before there can be effective segmentation

and targeting, and niche marketing there must exist data, both

qualitative and quantitative, on the basis of which the buyers that

constitute a market can be identified, differentiated and segmented.

Such a database can only be efficiently, created and maintained with

minimum redundancy with, the use of IT (Kotler, 1988, p 298; Oneh, et

al, p. 52 and Adirika, 1993, p. 116).

Originally, banks competed for customers’ interest rates on their deposits

and charge on loans. The competitive rates were generally offset by

hefty fees on various services. But many banks have now turned away

46

from strict price competition. Instead they rely on building customer

loyalty by building their services into packages and targeting them for

small segments of the population. It is perhaps when the whole market

is segmented and a bank concentrates on a particular niche that all

dimensions of service quality can be met always. Today, following the

collapse of institutional boundaries as it concerns rendering of financial

services, many a banker is worrying about local, regional and

international banks, as well as thrifts and credit unions. So, people who

were not even thinking about targeting ten years ago are now

scrambling to define their customer base. Packages that encourage

loyalty by rewarding customers for doing the bulk of their banking in one

place are now being developed (Christie, 1992 p. 25) for instance, the

Nigerian International Bank (NIB) version of electronic banking includes

the bank effectively placing a micro-computer terminal in a client’s office

and that terminal is connected to the data centre in the bank’s head

office (Somasekhar, 1988, p.14) without leaving his office a client can

look at his account because it appears on his TV console. He can virtually

write a cheque without leaving the office. Because he has certain

passwords and authorizations, the bank will honour his instructions. With

47

packages such as this, a bank will not only have segmented the market

and concentrated on a particular niche, it will also have succeeded in

providing itself with a sustainable competitive advantage by building

barriers to entry against competitors, increasing switching costs for the

customers and thereby ensuring his loyalty, and locking customers into

essential information and databases (O’ Brien, 1990, pp. 144-20). For

their troubles, the banks get a larger captive audience that is less likely

to move at the drop of a rate. The “IVY” account of Nigerian

Intercontinental Merchant Bank is a perfect example of a financial

product that is developed based on market segmentation and niche

marketing. The IVY account requires that a customer deposits a

minimum amount of one million naira (N1m) for a minimum tenor of one

year, at the interest rate of six percent (6%) per annum. Other features

of this product includes the fact that consumers of the product are

entitled to free overseas medical check-up, and hospital expenses of US

$5000=, should the need arise. A cursory look at this product shows that

it is not meant for every banking Nigeria. Infact, it is not meant for every

millionaire naira untouched for at least one year. Surely, the members of

this club must be few number, and therefore the promoters of the

48

product-NIMB- can effectively serve the group, even on personal basis.

Customers of this product receive the best of banking services, and this

has been made possible by the adoption of IT.

The IVY account was developed from an analysis of a previous product

of the same bank the “IDF” (Intercontinental Diamond Fund). This IDF

account required a minimum deposit of fifty thousand naira

(N50,000.00) for a minimum tenor of 180 days. This analysis, and

market forecast, was made simple by use of IT.

49

REFERENCES

Ezeokafor, U.B. (1996) “Marketing In Banking Industry” in The Journal of Marketing. Department of Marketing, UNEC.

Ubong, N. (1997) “How Banks Meet Today’s Customers’ Needs” in The Vanguard. November, 17.

Bulama, M. (1997) “Coping With Challenges In Financial Sector” in Business Times. Monday, June 23

Ovia, J. (1997) “Case For Electronic Clearing System” in Business Times. Monday, June 23

Ogbonna, C.I. (1997) “Hiccups In Nigeria’s Internet Connectivity” in The

Guardian. Thursday, May1

Omachonu, J. (1997) “Banking Robed With New Challenges” in The Guardian. Wednesday, September 17.

Minima, C. (1997) “Internet: Can Banks Foot. The Bill? In This Day vol. 3,

No. 809. Wednesday July 9

Adegbite, S.I (1997) “Information Technology By Wema Bank” in The Guardian. Wednesday September 17

Oladimeji, A. (1997) “FITC Boss Wants Banks To Computerize Operations” in Vanguard. Thursday October 30.

Oliver, E.C. and R.J. Chapman (1990), Data Processing and Information Technology. London: DP Publications.

Irving, R.H., and C.A. Higgins (1991), Office Information Systems: Management Issues and Methods. England: John Willey and Sons Limited.

50

Pym, F. (1985) The Politics of Consent. London: Sphere.

Evans, C. (1997), The Mighty Micro: The Impact of the Computer Revolution. London: Gollanez.

Badaru, S. (1997) “Banking for the Future” in This Day Vol. 3, No. 809, Wednesday, July 9.

Tayor, p. (1997) “Across the Globe … The Race Is On” in This Day vol. 3 No, 809, Wednesday, July 9.

Ogbulie, N. (1997)” Internet: can Banks Foot The Bill?” in This Day Vol. 3

No. 089, Wednesday 9. Yahaya, M.I. (1997) “Key Players For Bigger Bytes” in This Day Vol. 3

809, Wednesday, July 9. Udeagha, A.O (1995), Principles and Processes of Marketing. Enugu:

J.T.C. and Company. Kotler, P. (1988) Marketing Management: Analysis. Planning,

Implementation and Control. New Jersey: Prentice-Hall.

Onah, J.O and M.J. Thomas (1993) “Marketing Management”. Onitsha: Pacific Publishers.

Adirika, E.O. (1993) “Segmentation, Product Position and Effective Niche Marketing”: in Principles of Marketing by Udeagha, A.O. and C.I. Okeke. Enugu: New Generation Books.

Levitt, T. (1991) “Marketing Success Though Differentiation of Anything” in Dolan RJ. Strategic Marketing Management. USA Harvard Business School.

Lamb, C.W. et al (1994) Principles of Marketing Ohio: South-Western Publishing Co.

51

Valarie A.Z and L.L Berry (1990) Delivery Quality Service. New York: Free Press.

Rice, F. (1990) “How to Deal with Tougher Customers”. In Fortune, April,22.

Benneth A and C. Hymowitz (1992) “For Customers, More than Lip Service” in McCarthy E.J. and W.D Parreault Jr. Application in Basic Marketing. Homewood, IL: Richard D. Irwin Inc.

Judd, R.C. (1994) “The Case For Redefining Services” Journal of Marketing. January 28.

Olakunori, O.K and N.G Ejionueme (1997) Introduction To Marketing Enugu: Amazing Grace Publishers.

Kenneth, P.U and G.D Upah (1983) “The Marketing of Services: Why and How is it different” in Research in Marketing Vol. 6 JAI press INC.

Thomas D.R.E (1978) “Strategy is Different In Service Business” in Harvard Business Review. July August.

Kinnear T.C. and K.L Bernhardt (1983) Principles of Marketing, Glenview llinois: Scott, Foresman and Company.

Allvine, F.C (1987) Marketing New York: Harcourt Brace Jouvaborich Publishers.

Christie R. (1992) “Making Change For A Segmented Market: Banaks Package Services To Woo Target Groups” in MMcCarthy, E.J and W.D Parreault, Jr. Applications In Basic Marketing. Homewood IL, Richard D. Irwin, Inc.

Somasekhar, A. (1988) “We Run NIB To Citicorp Standards” in Financial Post, October 16.

52

O’ Brien, J.A (1990) Management Information Systems. Homewood: Richard D. Irwin.

Konsynski, B.R and F.W Mctarian (1990) “Information Partnerships-Shared Sata, Shared Scale”, in Harvard Business Review, Sept-oct.

Gunton, T (1992) The Penguin Dictionary of Information Technology and Computer Science. Harmondsworth: Penguin Books.

Armstrong, M. (1993) A Handbook of Management Techniques. New Jersey: Nichols Publishing.

53

CHAPTER THREE

RESEARCH DESIGN AND METHODOLOGY

The essence of this chapter is to highlight not only the analytical method

used for this research, but also to explain the reasons why they were

used. This explanation is informed by the fact there are many other

methods and test statistics that could be used for this same research.

3.1: DESIGN This work is a survey research; designed to evaluate the

effectiveness of ICT as a tool for improving banking services. The survey

was carried out on selected commercial banks in Enugu and Anambra

States. The measurement technique or test instrument used was

questionnaire; which was a formalized instrument for getting information

directly from a respondent concerning behaviour, level of knowledge,

and/or attitudes, belief and feelings (Donald and Hawkins, 1987, p. 35).

The questionnaire was chosen rather than observation because of the

impossibility of carrying out the observation in about eight different

banks in Enugu and Anambra States, simultaneously without surveillance

equipment. A simultaneous observation is necessary because customers’

arrival at their banks is not normally distributed over the days of the

week. In fact it is not even normally distributed over the whole day. And

54

because of the cost implications, and the associated personal biases, it

was not possible to recruit freelance field workers to help in the direct

observation.

The questionnaire has, as a result, become the best alternative in this

circumstance. Questionnaires were therefore, designed for:

(A) Bank customers, and

(B) Bank Management/Staff

3.1.1: BANK CUSTOMERS: Questionnaires were given to the

customers to capture their feeling about their banks’ efficiency in

services delivery now, compared with the years gone-bye; in addition

information were sought as to know if there were other services which

they would expect their banks to render to them but which the banks

had not been able to do so. This work attempted to look at improved

banking service from the customers’ point of view just because the

banking industry is a customer service driven industry. To be in business,

the banks just have to satisfy the customers’ view first of all and then

compare them with the views of the banks where need be. These

questionnaires were designed in such a way as to collect the necessary

data to test all the hypotheses.

55

3.1.2: BANK STAFF/MANAGEMENT: The set of questionnaire that

were administered on the Bank staff management was to elicit from

them responses as to whether their services .and service delivery have

improved, and if this improvement is due to the adoption of ICT. Their

response is only to help in analyzing, collaborating or refuting the

responses from the customers.

3.1.3: QUESTIONNAIRE DESIGN: The questionnaires were designed

in such a way to accommodate the main objective of the subject matter

under study. Two sets of questionnaires were administered. The first set

of questionnaires covered the (banks) customers, while the second set of

questionnaires covered the bank’s staff/management. Each set of

questionnaire has an introduction, which briefed the respondents on the

purpose of the research and assured them of the confidentiality of any

information provided. The second part of the questionnaire dealt with

the general questions intended to obtain the particular opinion of the

respondents based on the research questions of the study.

3.2 Methodology

3.2.1.1 STUDY POPULATION (COVERAGE) This research is

intended to concentrate on commercial banks in Enugu and Anambra

56

States, together with customers. The researcher however has

concentrated on the banks that are computerized. There are 25

commercial banks in the area under study. The choice of commercial

banks, in Enugu and Anambra States was not without reason. The

researcher is not oblivious of the fact that when we talk of financial

institutions in Nigeria, we mean more than the insured Banks. In that

case, finance houses, mortgage banks, community banks, development

banks, discount houses and insurance companies are all included. In as

much as that is the case, the researcher concentrated the survey on the

insured commercial banks. The reason for concentrating o n the

commercial banks include the following:

(i) Of the total deposit liability of insured banks in Nigeria totaling N255

billion as at end of December,1996 commercial banks mobilized

N225.3 billion, representing 88.4 percent.

(ii) Commercial banks accounted for N536.1 billion or 82.8 percent of

total assets of insured banks of N647.6 billion as at end of December,

96.

57

(iii) Aggregate credit to the economy stood at N266.5 billion and the

commercial banks accounted for N216.8 billion. This represents 81.4

percent.

(iv) The area (Anambra and Enugu States) has consistently been

ranked second only to Lagos since 1991 in the distribution of insured

banks offices and branches in Nigeria. This means that results

obtained from them can safely be used to make generalizations about

the entire industry in Nigeria.

(v) The branch banking system adopted by insured banks in Nigeria

implies that all the branches of any particular bank are governed by

the same policy from head office.

(vi) Onitsha being the commercial nerve centre of Nigeria, virtually all

the major banks in Nigeria has branches there. On the other hand,

the administrative headquarters or area offices of basically the first

generation banks are found in Enugu.

3.2.2 DETERMINATION OF SAMPLE SIZE: Two things are involved

in this sub section. The first is the determination of the banks to be

covered by the survey, while the second is the number of customers to

be surveyed from each bank.

58

3.2.2.1A USE OF STRATIFIED SAMPLING: To be fair enough to all

banks, the researcher has first of all used a stratified sampling method to

regiment the banks under two broad headings –old generation and new

generation banks.

Old generation banks in this context means those banks that been in

operation for fifteen years and above. The new generation banks on the

other hand are those that have not been in operation for up to fifteen

years. From these two categorization, the researcher covered eight

banks under the survey-five from the old generation banks and three

from the new generation banks. In choosing which banks to be covered

under the survey, .the researcher used a judgmental sampling technique

since he could only work with the banks that were willing to co-operate

with him.

3.2.2.2 USE OF STATISTICAL FORMULA: Having decided on the

number of banks, and the banks to be covered under the survey, the

researcher went round the banks to obtain the number of customers

they have. With this number and the statistical formula below, the

researcher went ahead to select the number of respondents thus:

S = N 1+N (e)2

59

Where S = sample size

N= Population size (in this case the number of customers from the

five selected banks) e = Margin of error (assumed to be 5%) Thus, we

have

S= 115,000

1+115000 (0.05)2

= 11,5000

288.5

= 398.6 = 400

This gives us approximately four hundred copies of the questionnaires,

which were administered to the customers or respondents.

3.2.3 SOURCES OF DATA: Both primary and secondary saucers were

used in collecting data for this work.

3.2.3.1 PRIMARY DATA: The main sources of data for this work

are the administered questionnaires, and oral interviews. The

questionnaires which formed the main source of data were structured

and distributed among customers of the selected banks, and senior or

management staff of the affected banks.

60

As a corollary, the interviews covered those areas that were not taken

care of by the questionnaires.

3.2.3.2 SECONDARY DATA: Secondary data, were sourced from

textbooks, magazines and newspapers, and journals including

government agencies’ publications.

3.2.4 QUESTIONNAIRE ADMINISTRATION: Having determined a

research sample size of approximately 400, which requires 400 copies of

the questionnaires to be distributed to the banks’ customers the

procedure adopted in distributing the questionnaire was personal

administration. In view of the associated problems of poor response

rate, the researcher got the banks (branch) management convinced and

involved by letting them understand that the work is for academic

purpose only. Outside this, the surveyed banks stand to benefit

immensely from the research since they will know to their customers

feelings about their services. And to get the customers moved to

respond to the questionnaires the researcher convinced the banks to use

negative re-enforcement: withholding the money they have come to

withdraw, (while appealing to them to help us fill out the questionnaires)

61

until they returned the questionnaires. This hopefully increased the

response rate, and facilitated early returns.

In administering the questionnaires to the customers, the researcher

used a systematic sampling technique; every third customer that came

for withdraw was issued with a questionnaire. And for the bank staff, the

researcher was convinced that any senior or management staff of the

banks is in a position to supply the required information.

3.2.5 VALIDATION OF RESEARCH INSTRUMENTS: The research

instruments were validated by pre-testing the questionnaires. The aim of

this validation clearly, was to ensure that the intended respondents

understood the questions clearly, without any ambiguity, and hoping to

fine-tune the questionnaires should the need arise. For pre-testing, the

questionnaires were administered to three senior staff of three banks

here in Enugu, and for the customers, ten student customers of different

banks, here in Enugu.

3.2.6 ANALYTICAL TECHNIQUE/TOOL: The following analytical

techniques were used:

Percentage analysis

Cross tabulation

62

Logical deductions

Z-test statistics (for difference of two means)

Z-test statistics (test for proportion)

3.2.7 HYPOTHESES TESTING

Ho = Null hypotheses HI = Alternative hypotheses

At 0.05 level of significance

The testing of the hypotheses was carried out by first for the old

generation banks, second, for the new generation banks, and thirdly, for

the whole banks combined. The disaggregated test are expected to

reveal any differences between the effectiveness of ICT in the two

categories of banks, while the aggregated test is expected to reveal

effectiveness of ICT in the industry as a whole.

3.2.8 DECISION RULE: If, Z> critical value, reject the null

hypothesis, and accept the alternative hypothesis. If Z< critical value,

accept the null hypothesis, and reject the alternative hypothesis.

FORMULA

Z-test

1. Difference Between two Means

Z= (X1=X2)

S21 + S2

2

N1 n1

2. Test for Proportion

Z = (P – Po)

Po (1-Po)/n

63

REFERENCES

Ovesetu, F.O. (1992) “Interest Rate Behaviour under a

Programme of financial reforms: The Nigerian case in Economics and Financial Review CBN Vol. 30 No.2

Irving, R.H; and C.A. Higgins (1991), Office Information System Management Issues and Methods. England: John Willey and Sons Limited.

Kotler, P (1988) Marketing Management: Analysis, Planning,

Implementation and control. New Jersey: Prentice-Hall. Advika, E.O. (1993) “Segmentation Product Position and Effective Niche

Marketing: in principle of marketing by Udeagha, A.O and C.I Okeke. Enugu: New Generation Books.

Lamb, C.W. et al (1994) Principles of Marketing Management.

U.S.A. Harvard Business School. Rose, F. (1991) “New Quality Means Service 100 = “In fortune, April

22. Gumton, T. (1992) The Penguin Dictionary of Information

Technology and Computer science Ezeokafor, U.B. (1996) “Marketing in Banding Industry in Journal of

marketing department UNEC Rose, F. (1991) New Quality Means Service Too in Fortune April 22.

64

CHAPTER FOUR

DATA PRESENTATION AND ANALYSIS

In the chapter, the data collected from the respondents through the

questionnaires administered to them are presented and analyzed; using

the procedures and tools stated in chapter three. In the course of this

chapter, all the test tools as mentioned in chapter one are used where

(each is) most appreciate. In carrying out the testing of the hypotheses,

the data for old generation and new generation bank were first of all

disagregated before aggregating same.

The intention as stated in chapter three, is to observe if there is

any (significant) difference in the effectiveness of ICT between the old

generation and new generation banks. And to determine if there is any

improvement in banking service delivery.

4.1 Data Presentation

Without prejudice to the disaggregated testing of the hypotheses,

the data presented hereunder is aggregated. In presenting the data,

responses to similar questions, that have different time frames (before

and after computerization) are presented on the sample table.

65

Consequent upon the size, 400 copies of the questionnaire for customers

were administered. Eventually, only 320 copies were returned, despite

the negative re-enforcement employed to elicit a high response rate.

This response rate of 80% was encouraging though and therefore the

research proceeded with the analysis of the data. However, 10 out of the

320 copies of the questionnaire returned were invalid. Of these invalid

responses, 3 are from the new generation banks group while the

remaining 7 were from the old generation banks groups. These ten

copies of the questionnaire were invalidated on the grounds of

inconsistency in response. At the final analysis, the net rate of return

was 77.5%

TABLE 4.1 DISTRIBUTION OF RESPONSE FOR INSTRUMENT

No of questionnaires No of questionnaires Return rate

250 193 48.25

150 127 31.75

400 320 80%

Source: Field Survey

66

Questions 6 and 7: Time spent in the banks to withdraw money.

Table 4.2: Waiting Time for Cash Withdrawal.

Before

Computerization

After

computerization

X 2f

No of

minutes

(X1)

No of respondents

(f)

X1 f No of minutes

(X2)

No

respondents (f)

15 16 240 15 153 2295

30 55 2650 30 111 3330

50 72 3600 50 25 1250

60 164 9840 60 16 960

Total

155

307 15330 155 305 7835

Source: Field Survey

Mean time (X1) Mean time (X2)

X1 = Exf = 15330 X2 = Exf = 7835

307 Ef 305

=49.93 mins. = 25.69 mins

The table above shows the distribution of waiting time to withdraw

money by Nigerians from their accounts with their banks, both before

and after computerization. From the table, average or mean time spent

to withdraw money before computerization was 49.93 minutes, while

after computerization, it was 25.69 minutes.

67

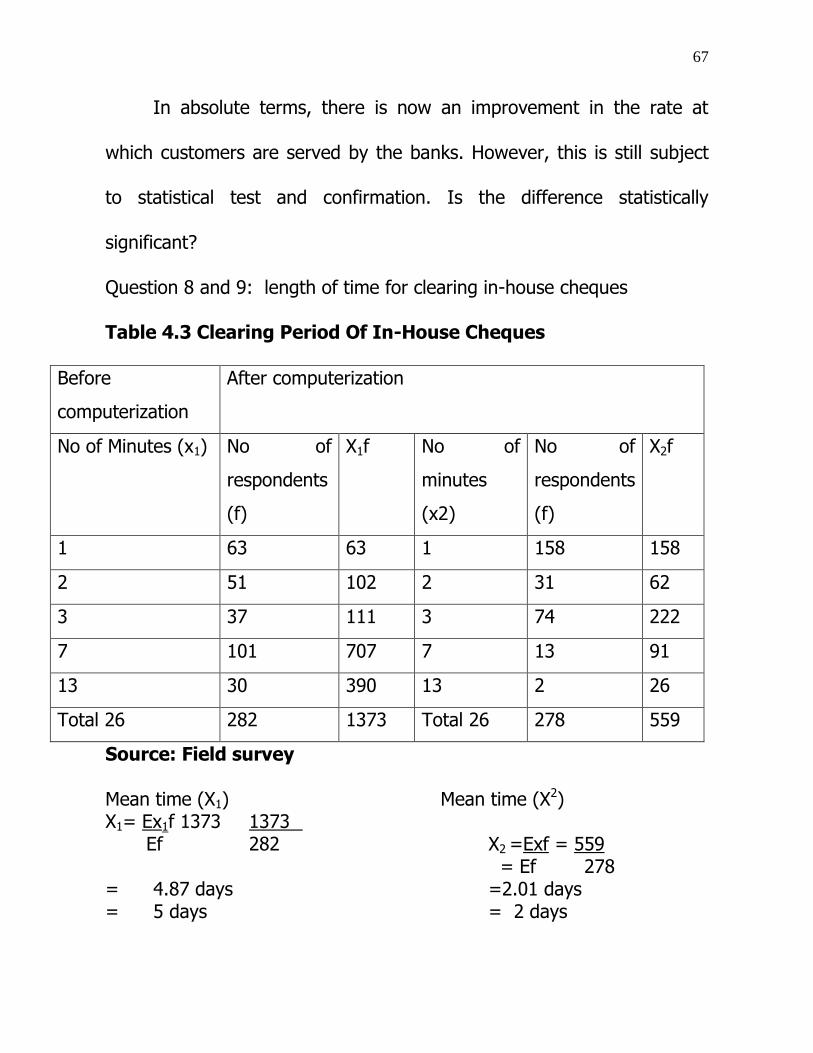

In absolute terms, there is now an improvement in the rate at

which customers are served by the banks. However, this is still subject

to statistical test and confirmation. Is the difference statistically

significant?

Question 8 and 9: length of time for clearing in-house cheques

Table 4.3 Clearing Period Of In-House Cheques

Before

computerization

After computerization

No of Minutes (x1) No of

respondents

(f)

X1f No of

minutes

(x2)

No of

respondents

(f)

X2f

1 63 63 1 158 158

2 51 102 2 31 62

3 37 111 3 74 222

7 101 707 7 13 91

13 30 390 13 2 26

Total 26 282 1373 Total 26 278 559

Source: Field survey

Mean time (X1) Mean time (X2) X1= Ex1f 1373 1373 Ef 282 X2 =Exf = 559 = Ef 278 = 4.87 days =2.01 days = 5 days = 2 days

68

As evident by the information in table 4.3 above, before computerization,

the average clearing period for in-house cheques was 5 days.

Consequent upon computerization, the average clearing period of in-

house cheques declined to 2 days. The difference between these

absolute figures will still be subjected to statistical test for difference

between two means.

Questions 10 and 11: time spent to obtain bank draft or manger’s

cheque.

Table 4:4 Waiting Time for Obtaining Draft or Manager’s Cheque

Before

computerization

After computerization

No of Minutes

(X1)

No of

respondents

(f)

X1f No of

minutes

(X2)

No of

respondents

(f)

X2f

5 2 10 5 45 225

20 22 440 20 123 3735

45 25 1125 45 83 3735

90 80 7200 90 54 4050

120 175 21000 120 4 480

Total 280 304 29775 280 300 10950

Source: Field Survey

69

Mean time X1 Mean time X2

X1= Exf 29775 X2 = Exf = 10950

Ef 304 Ef 300

= 97.94 mins. =36.5mins.

From table 4.4 above, we can deduce that before computerization in the

Nigerian banking industry, customers used to spend an average of 97.94

minutes before they could obtain a draft or managers cheque. But with

computerization, it now takes an average of 36.5 minutes to obtain the

same service, the difference between these two means will still be

subjected to test while testing the hypothesis.

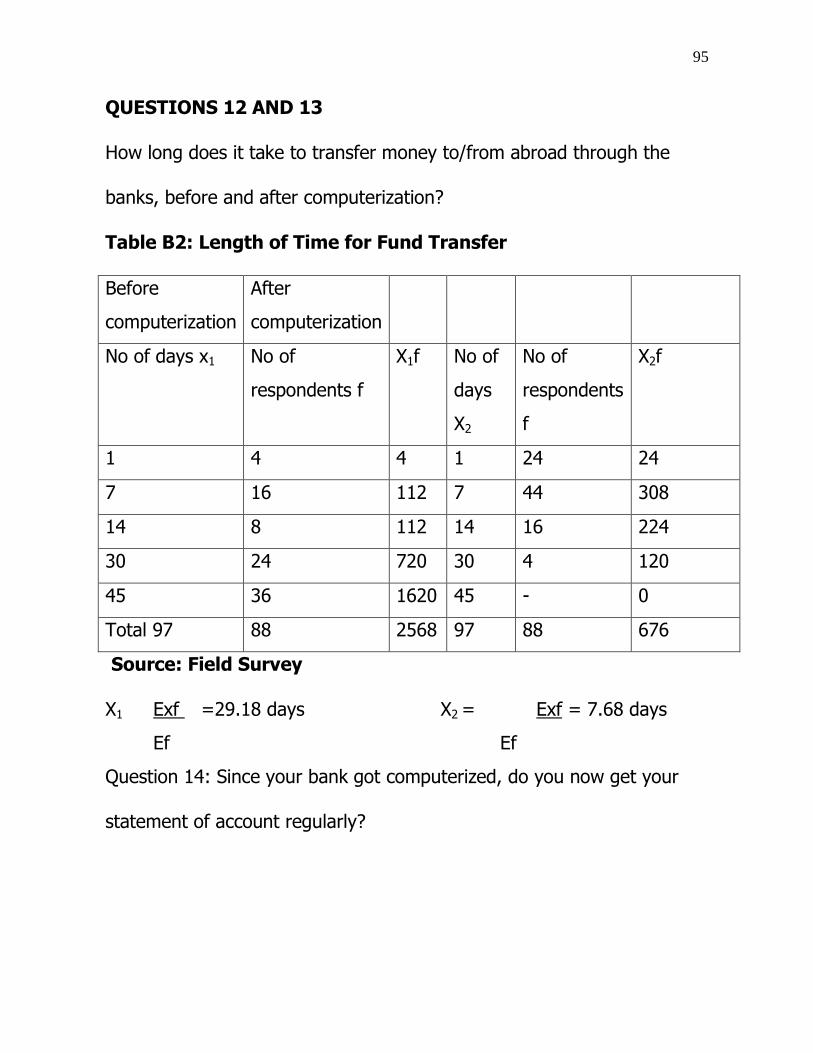

Questions 12 and 13:

Duration it take to transfer money to and from abroad through the

banks.

Table 4.5: Length of Time for Fund Training

No of

minutes

(X1)

No of

respondents

(s)

X1f No of

minutes

(x2)

No of

respondents

X2f

1 8 8 1 49 49

7 26 182 7 102 714

14 38 532 14 35 490

30 47 1410 30 12 360

70

45 92 4140 45 2 90

Total 97 211 6272 97 200 1703

Source: Field Survey

Mean time (X1) Mean time (X2)

X1 = Exf = 6272 X2 = Exf = 1703

Ef 211 Ef 200

= 29.73 days = 8.52 days

From table 4.5, it can be deduced that customers needed to wait for

about 30 days to effect a transfer of money to or from overseas, using

the banks; before computerization. However, with computerization, it

can be done the same day if your requirements are complete.

Question 14:

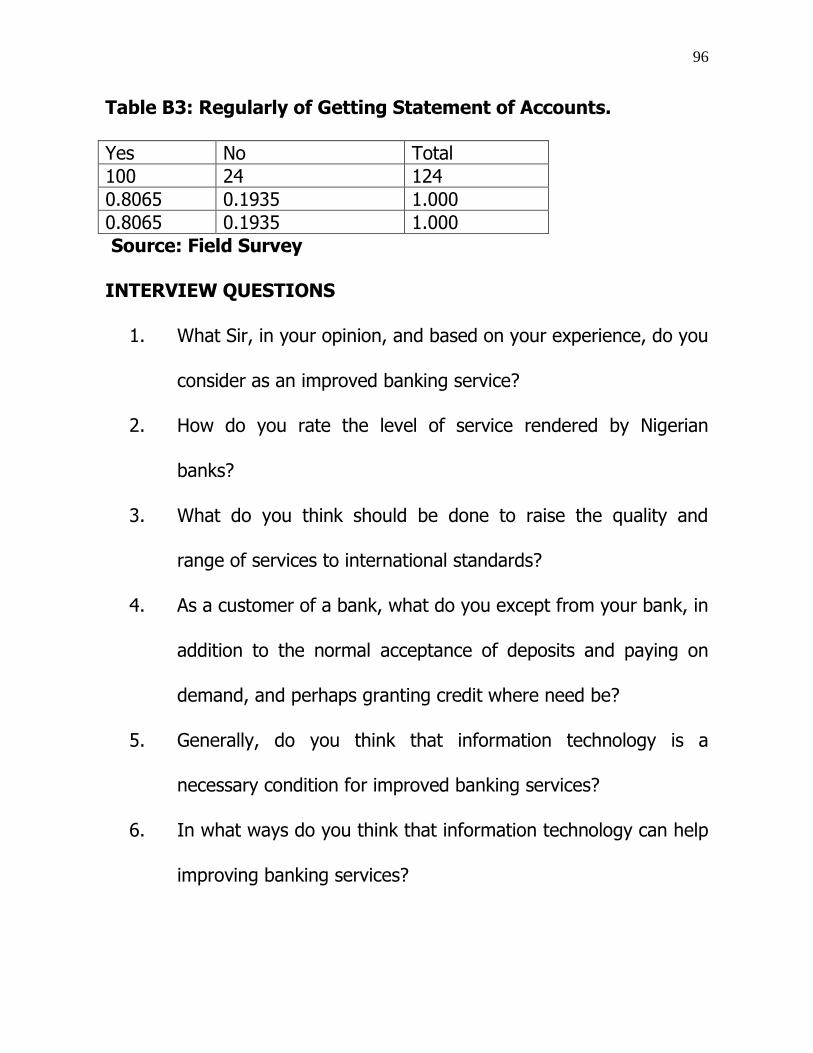

Now that your bank got computerized; do you now get your statement

of account regularly?

Table 4:6: Regularity in Getting Statement of Account

Response No of respondents Proportion

Yes 250 0.8306

No 51 0.1694

Total 301 1.0000

Source: Field Survey

71

From the above table, we can see that 83.06% of the respondents

said that they now get their statements of account regularly. Only

16.94% of the 301 respondents said otherwise. In view of these

facts, we can conclude that the adoption of it by the banking industry

has facilitated the rendition of statement of accounts by banks.

Question 5

Which are the other banking services, which the customer would want

your bank to render to them?

Table 4.7 Unavailable Banking Services

Response No of respondents Proportion

Yes 125 0.4266

No 168 0.5734

Total 293 1.0000

Source: Field Survey

Table 4.7 shows the ratio of those customers who would other banking

services, which their banks have not been able to provide.

Of the 293 respondents who answered this question, 125 or

42.66% know of, and want, extra services, which their banks are,

72

meanwhile, not providing. 57.45% neither knows of other services nor

want any other.

4.2 HYPOTHESES TESTING

In chapter one of this work, three testable hypotheses were

presented. These hypotheses are here-under tested, using the data as

presented in tables 4.2, table 4.5 and table 4.6 However, the data for

the disaggregated test, are only presented in the appendix.

A cursory look at the three hypotheses in chapter one reveals that

while the Z-test statistics (for difference between two means) is

appropriate for testing hypothesis numbers one and three, hypothesis

number two can only be tested using simple percentage or the Z-test for

proportion. Because of the standard expected of this work, the Z-test for

proportion will be used. All tests are conducted at the 5% level of

significance.

TEST TECHINQUE

Z-test (for difference between two means)

FORMULA FOR TEST TECHINQUE Z = (X1-X2) S2

1 + S22

n1 n2

73

Where

X1 = Mean time in period 1 (before computerization)

X2 = Mean time in period 2 (after computerization)

S21 = Simple variance for sample 1 (before computerization)

S22 = Simple variance for simple 2 (after computerization)

n1 n2 = Number of respondents for period 1 and 2

DECISION RULE

If (Calculated value) > Z& (theoretical value) reject the null hypothesis,

and accept the alternative hypothesis.

If Z (calculated) < Z& (theoretical value) accept the null hypothesis, and

reject the alternative hypothesis.

Testing Ho: X1 – X2 = 0 versus H1: X1-X2 = 0

HYPOTHESIS 1

Ho: Despite the adoption of ICT by the Nigerian banking industry,

customers still cannot withdraw their money in less time than before

H1: With the adoption of ICT by the Nigerian banking industry,

customers cannot withdraw their money in less than before.

74

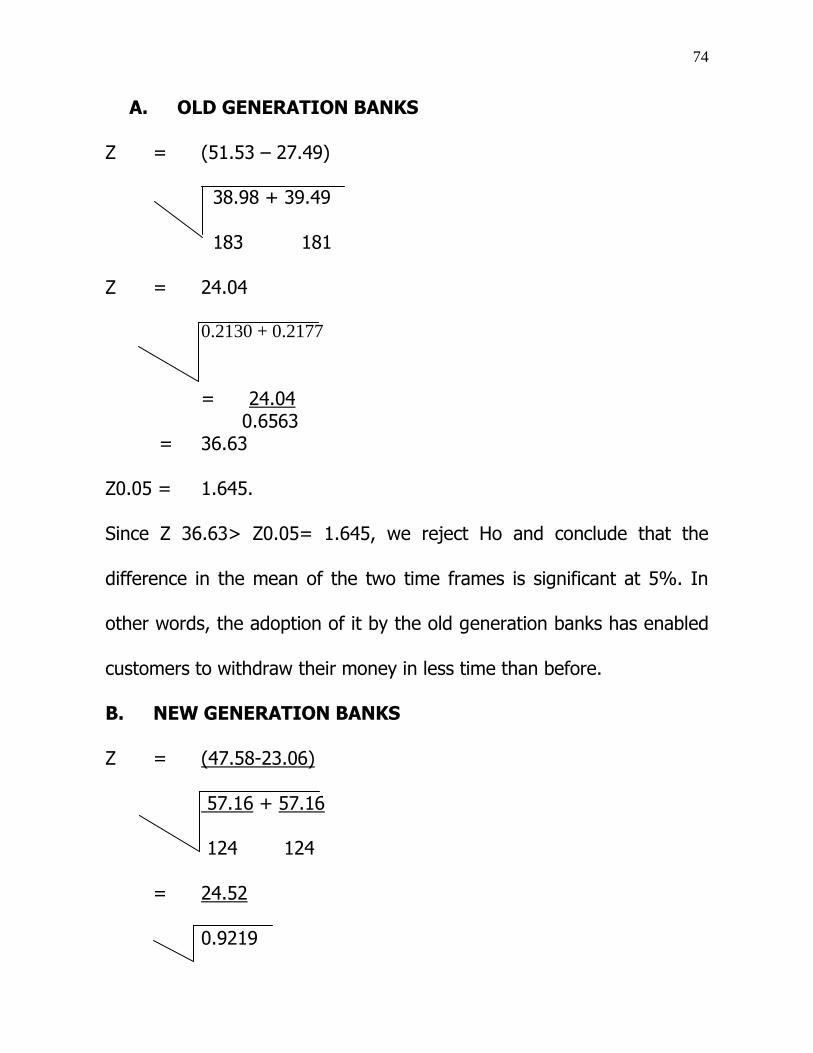

A. OLD GENERATION BANKS

Z = (51.53 – 27.49)

38.98 + 39.49

183 181

Z = 24.04

0.2130 + 0.2177

= 24.04 0.6563 = 36.63

Z0.05 = 1.645.

Since Z 36.63> Z0.05= 1.645, we reject Ho and conclude that the

difference in the mean of the two time frames is significant at 5%. In

other words, the adoption of it by the old generation banks has enabled

customers to withdraw their money in less time than before.

B. NEW GENERATION BANKS

Z = (47.58-23.06)

57.16 + 57.16

124 124

= 24.52

0.9219

75

= 25.54

Since Z = 25.54 > Z0.05 = 1.645, we reject Ho and conclude that the

difference in the mean of the two time frames is significant at 5%. In

other words, the adoption of it by the new generation banks has enabled

customers of new generation banks to withdraw their money in less time

than before.

C. AGGREGATE TEST (FOR THE WHOLE INDUSTRY)

Z. = (49.93 – 25.69)

23.36 + 23.51

307 304

= 24.24

0.761 + 0.0773

= 24.24 0.3917 = 61.88

Since Z = 61.88 > z0.05, we reject Ho and conclude that the adoption of

it the Nigerian banking industry has enabled customers to withdraw their

money in less time than before.

76

HYPOTHESIS 3

Ho: Despite the introduction of ICT by the Nigerian Banking Industry,

bank customers still cannot remit or receive foreign currencies to or from

overseas sources in less time than before.

H1: With the introduction of it by the Nigerian banking industry, bank

customers now remit of receive foreign currencies to or from overseas

sources in less time than before.

A. OLD GENERATION BANK

(30.11-9.17)

Z. = 31.98 + 39.4

123 112

= 20.94

0.26 + 0.3518

= 20.94

0.7822

= 27.38

At the same 5% level of significance, Zo.05 = 1.645. Since Z = 27.38 >

Z0.05 = 1.645, we reject the null hypothesis and accept that with the

77

introduction of ICT, old generation bank customers now remit or receive

foreign currencies to or from overseas sources in less time than before

B. NEW GENERATION BANKS

Z (29.18-7.68 )