togliattikhimbank - thbank.ru · togliattikhimbank 2003 consolidated financial statements contents...

TRANSCRIPT

TogliattikhimbankConsolidated Financial Statements

Year ended December 31, 2003 Together with Report of Independent Auditors

Togliattikhimbank 2003 Consolidated Financial Statements

CONTENTS

REPORT OF INDEPENDENT AUDITORS

CONSOLIDATED FINANCIAL STATEMENTS

REPORT OF INDEPENDENT AUDITORS........................................................................6CONSOLIDATED BALANCE SHEETS..............................................................................1CONSOLIDATED STATEMENTS OF INCOME...............................................................2CONSOLIDATED STATEMENTS OF CHANGES IN SHAREHOLDERS’ EQUITY .3CONSOLIDATED STATEMENTS OF CASH FLOWS.....................................................4

1. Principal Activities................................................................................................................................52. Basis of Preparation..............................................................................................................................52. Basis of Preparation (continued)........................................................................................................63. Summary of Accounting Policies ......................................................................................................64. Cash and Cash Equivalents...............................................................................................................135. Trading Securities................................................................................................................................136. Amounts Due from Credit Institutions..........................................................................................146. Amounts Due from Credit Institutions (continued)....................................................................157. Available-for-Sale Securities..............................................................................................................158. Loans to Customers ..........................................................................................................................168. Loans to Customers (continued)......................................................................................................169. Taxation................................................................................................................................................179. Taxation (continued)..........................................................................................................................1710. Investments in Associates ..............................................................................................................1810. Investments in Associates (continued)........................................................................................1811. Allowances for Losses and Provisions..........................................................................................1812. Property and Equipment.................................................................................................................2113. Amounts Due to Credit Institutions.............................................................................................2114. Amounts Due to Customers...........................................................................................................2114. Amounts Due to Customers (continued).....................................................................................2115. Amounts Due to Related Party......................................................................................................2216. Debt Securities Issued......................................................................................................................2217. Subordinated Loan...........................................................................................................................2218. Shareholders’ Equity........................................................................................................................2318. Shareholders’ Equity (continued)...................................................................................................2419. Commitments and Contingencies..................................................................................................2420. Gains Less Losses from Available-for-Sale Securities................................................................2521. Salaries and Administrative and Operating Expenses................................................................2522. Risk Management Policies...............................................................................................................2522. Risk Management Policies (continued).........................................................................................2622. Risk Management Policies (continued).........................................................................................2722. Risk Management Policies (continued).........................................................................................2922. Risk Management Policies (continued).........................................................................................3023. Fair Values of Financial Instruments............................................................................................3024. Related Party Transactions..............................................................................................................32

Togliattikhimbank 2003 Consolidated Financial Statements

25. Capital Adequacy..............................................................................................................................3326. Subsequent events.............................................................................................................................34

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

REPORT OF INDEPENDENT AUDITORS........................................................................6CONSOLIDATED BALANCE SHEETS..............................................................................1CONSOLIDATED STATEMENTS OF INCOME...............................................................2CONSOLIDATED STATEMENTS OF CHANGES IN SHAREHOLDERS’ EQUITY .3CONSOLIDATED STATEMENTS OF CASH FLOWS.....................................................4

1. Principal Activities................................................................................................................................52. Basis of Preparation..............................................................................................................................52. Basis of Preparation (continued)........................................................................................................63. Summary of Accounting Policies ......................................................................................................64. Cash and Cash Equivalents...............................................................................................................135. Trading Securities................................................................................................................................136. Amounts Due from Credit Institutions..........................................................................................146. Amounts Due from Credit Institutions (continued)....................................................................157. Available-for-Sale Securities..............................................................................................................158. Loans to Customers ..........................................................................................................................168. Loans to Customers (continued)......................................................................................................169. Taxation................................................................................................................................................179. Taxation (continued)..........................................................................................................................1710. Investments in Associates ..............................................................................................................1810. Investments in Associates (continued)........................................................................................1811. Allowances for Losses and Provisions..........................................................................................1812. Property and Equipment.................................................................................................................2113. Amounts Due to Credit Institutions.............................................................................................2114. Amounts Due to Customers...........................................................................................................2114. Amounts Due to Customers (continued).....................................................................................2115. Amounts Due to Related Party......................................................................................................2216. Debt Securities Issued......................................................................................................................2217. Subordinated Loan...........................................................................................................................2218. Shareholders’ Equity........................................................................................................................2318. Shareholders’ Equity (continued)...................................................................................................2419. Commitments and Contingencies..................................................................................................2420. Gains Less Losses from Available-for-Sale Securities................................................................2521. Salaries and Administrative and Operating Expenses................................................................2522. Risk Management Policies...............................................................................................................2522. Risk Management Policies (continued).........................................................................................2622. Risk Management Policies (continued).........................................................................................2722. Risk Management Policies (continued).........................................................................................2922. Risk Management Policies (continued).........................................................................................3023. Fair Values of Financial Instruments............................................................................................3024. Related Party Transactions..............................................................................................................3225. Capital Adequacy..............................................................................................................................3326. Subsequent events.............................................................................................................................34

REPORT OF INDEPENDENT AUDITORS

To the Shareholders and Board of Directors of Togliattikhimbank –

We have audited the accompanying consolidated balance sheet of Togliattikhimbank and subsidiary (together the “Bank”) as of December 31, 2003 and the related consolidated statements of income, changes in shareholders’ equity, and cash flows for the year then ended. These financial statements are the responsibility of the Bank’s management. Our responsibility is to express an opinion on these financial statements based on our audit.

We conducted our audit in accordance with International Standards on Auditing. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, the consolidated financial position of the Bank as of December 31, 2003 and the results of its operations and its cash flows for the year then ended in accordance with International Financial Reporting Standards.

We draw attention to Note 24 to the consolidated financial statements. The Bank is a member of a group of affiliated companies and has extensive transactions and relations with the members of this group, and, therefore, is dependent on their financial performance.

April 30, 2004

Togliattikhimbank Consolidated Financial Statements

CONSOLIDATED BALANCE SHEETS

(Thousands of Russian Rubles)

December 31,Notes 2003 2002

AssetsCash and cash equivalents 4 403,295 140,229Trading securities 5 11,288 33,011Amounts due from credit institutions 6 177,682 449,819Available-for-sale securities 7 934,906 219,757Loans to customers 8 2,194,404 1,478,280Tax assets 9 9,195 –Investments in associates 10 17,649 8,760Property and equipment 12 17,119 18,837Other assets 7,984 9,818Total assets 3,773,522 2,358,511

Liabilities Amounts due to credit institutions 13 128,710 139,496Amounts due to customers 14 1,916,794 1,111,365Amounts due to related party 15 – 124,648Debt securities issued 16 858,157 493,394Tax liabilities 9 40,699 3,115Subordinated loan 17 69,181 64,308Other liabilities 11,011 12,516Total liabilities 3,024,552 1,948,842

Minority interest 4,931 5,171

Shareholders’ equity 18Share capital 283,238 149,238Retained earnings 460,801 255,260 Total shareholders’ equity 744,039 404,498

Total liabilities, shareholders’ equity and minority interest 3,773,522 2,358,511

Financial commitments and contingencies 19 1,979,919 1,667,742

Signed and authorized for release on behalf of the Board of the Bank

___________________Alexander Popov Chairman of the Board

___________________Sergey Popov Chief Accountant

April 30, 2004

The accompanying notes on pages 5 to 26 are an integral part of these consolidated financial statements.

1

Togliattikhimbank Consolidated Financial Statements

CONSOLIDATED STATEMENTS OF INCOME

(Thousands of Russian Rubles)

Years ended December 31,Notes 2003 2002

Interest incomeLoans 320,589 296,195Securities 13,351 13,478Interbank placements 5,435 16,661

339,375 326,334Interest expense

Deposits (48,271) (79,025)Borrowings (2,085) (7,881)Debt notes issued (13,731) (10,001)

(64,087) (96,907)Net interest income 275,288 229,427Impairment of interest earning assets 11 (35,769) (5,506)Net interest income after impairment 239,519 223,921

Fee and commission income 80,445 79,872Fee and commission expense (17,840) (25,375)Fees and commissions, net 62,605 54,497

Gains less losses from trading securities, net 11,454 3,362Gains less losses from available-for-sale securities, net 20 25,638 (20,527)Gains less losses from foreign currencies:

- dealing, net 10,976 12,326- translation differences (3,624) (2,074)

Other income 6,790 2,984Non interest income 51,234 (3,929)

Salaries and benefits 21 (24,385) (48,552)Depreciation and amortisation 12 (7,062) (6,367)Other administrative and operating expenses 21 (48,686) (75,225)Other impairment and provisions 11 (941) (14,168)Non interest expense (81,074) (144,312)

Loss on net monetary position – (59,228)Income before income tax expense and minority interest 272,284 70,949

Income tax expense 9 (66,983) (17,973)Minority interest in net income (loss) 240 (990)Net income 205,541 51,986

The accompanying notes on pages 5 to 26 are an integral part of these consolidated financial statements.

2

Togliattikhimbank Consolidated Financial Statements

CONSOLIDATED STATEMENTS OF CHANGES IN SHAREHOLDERS’ EQUITY

For the years ended December 31, 2003 and 2002

(Thousands of Russian Rubles)

Share Capital Retained earningsTotal

shareholders’ equity

December 31, 2001 149,238 211,909 361,147Dividends (8,635) (8,635)Net income 51,986 51,986December 31, 2002 149,238 255,260 404,498

Capital contributions 134,000 134,000Net income 205,541 205,541December 31, 2003 283,238 460,801 744,039

The accompanying notes on pages 5 to 26 are an integral part of these consolidated financial statements.

3

Togliattikhimbank Consolidated Financial Statements

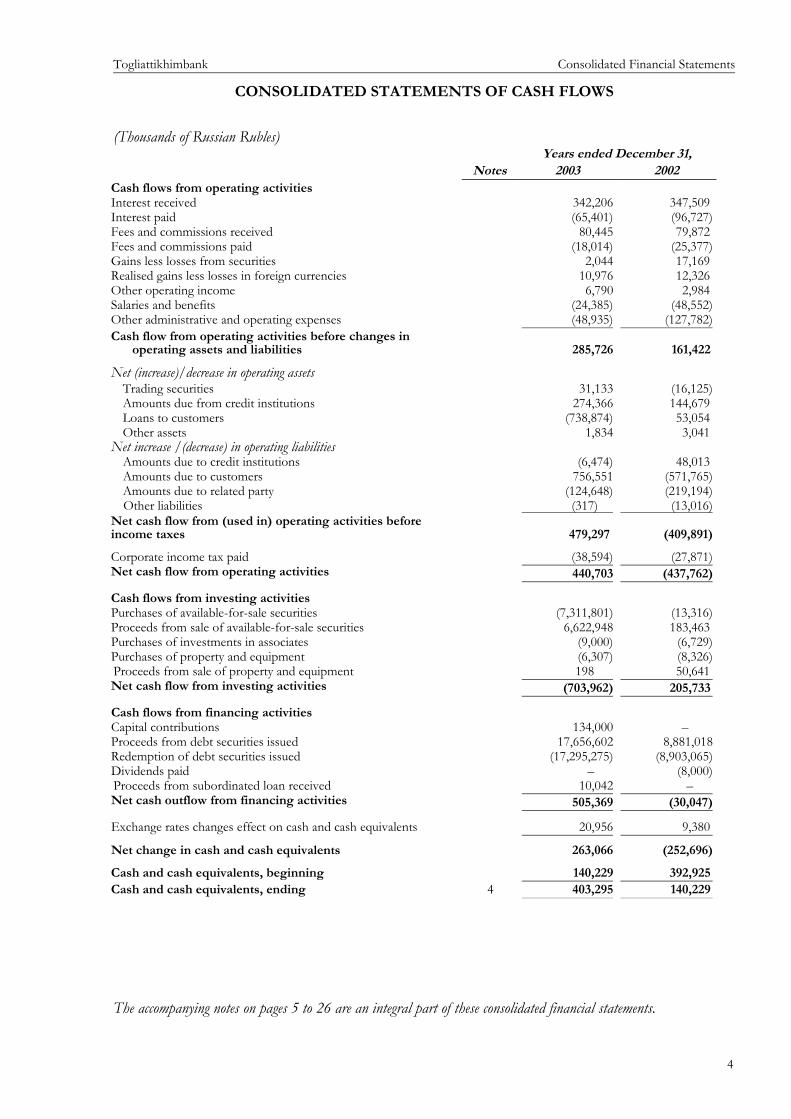

CONSOLIDATED STATEMENTS OF CASH FLOWS

(Thousands of Russian Rubles)Years ended December 31,

Notes 2003 2002Cash flows from operating activitiesInterest received 342,206 347,509Interest paid (65,401) (96,727)Fees and commissions received 80,445 79,872Fees and commissions paid (18,014) (25,377)Gains less losses from securities 2,044 17,169Realised gains less losses in foreign currencies 10,976 12,326Other operating income 6,790 2,984Salaries and benefits (24,385) (48,552)Other administrative and operating expenses (48,935) (127,782)Cash flow from operating activities before changes in

operating assets and liabilities 285,726 161,422

Net (increase)/decrease in operating assets Trading securities 31,133 (16,125)Amounts due from credit institutions 274,366 144,679Loans to customers (738,874) 53,054Other assets 1,834 3,041

Net increase /(decrease) in operating liabilitiesAmounts due to credit institutions (6,474) 48,013Amounts due to customers 756,551 (571,765)Amounts due to related party (124,648) (219,194)

Other liabilities (317) (13,016)Net cash flow from (used in) operating activities before income taxes 479,297 (409,891)Corporate income tax paid (38,594) (27,871)Net cash flow from operating activities 440,703 (437,762)

Cash flows from investing activitiesPurchases of available-for-sale securities (7,311,801) (13,316)Proceeds from sale of available-for-sale securities 6,622,948 183,463Purchases of investments in associates (9,000) (6,729)Purchases of property and equipment (6,307) (8,326)Proceeds from sale of property and equipment 198 50,641Net cash flow from investing activities (703,962) 205,733

Cash flows from financing activitiesCapital contributions 134,000 –Proceeds from debt securities issued 17,656,602 8,881,018Redemption of debt securities issued (17,295,275) (8,903,065)Dividends paid – (8,000)Proceeds from subordinated loan received 10,042 –Net cash outflow from financing activities 505,369 (30,047)

Exchange rates changes effect on cash and cash equivalents 20,956 9,380

Net change in cash and cash equivalents 263,066 (252,696)Cash and cash equivalents, beginning 140,229 392,925Cash and cash equivalents, ending 4 403,295 140,229

The accompanying notes on pages 5 to 26 are an integral part of these consolidated financial statements.

4

Togliattikhimbank Notes to 2003 Consolidated Financial Statements

(Thousands of Russian Rubles)

1. Principal Activities

Togliattikhimbank (the “Bank”) was formed on September 21, 1993 as a limited liability partnership under the laws of the Russian Federation. On June 27, 2000 the Bank was re-registered with the Central Bank of Russia (“CBR”) as a closed joint stock company. The Bank operates under a general banking license issued by the CBR on June 27, 2000. The Bank also possesses licenses for securities operations and custody services from the Federal Commission for the Securities Market granted in December 2000.

The Bank accepts deposits from the public and extends credit, transfers payments in Russia and abroad, exchanges currencies and provides banking services to its commercial and retail customers. The Bank’s registered legal address is Gorkogo str., 96, Togliatti, Russia.

As of December 31, 2003, the following shareholders owned more than 5% of the outstanding shares.

Shareholder 2003 2002OAP Togliattiazot 97.2 35.0OOO Kontaz 1.0 17.3Mr. Vladimir N. Makhlai 0.9 11.1Mr. Sergei V. Makhlai 0.9 16.3FK Tafko – 6.2Mr. Vyacheslav M. Nosov – 5.9Other – 8.2Total 100.0 100.0

As of December 31, 2003, members of the Shareholders’ Council and Management Boards controlled 1.8% shares (2002 – 20.5%) of the Bank.

The Bank had an average of 173 employees during 2003 (2002 – 254).

2. Basis of Preparation

General

These consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (“IFRS”) which comprise standards and interpretations approved by the International Accounting Standards Board, and International Accounting Standards (“IAS”) and Standing Interpretations Committee interpretations (“SIC”) approved by the International Accounting Standards Committee that remain in effect. These financial statements are presented in thousands of Russian Rubles (“RUB”), except per share amounts and unless otherwise indicated. The Ruble is utilized as the majority of the Bank’s transactions are denominated, measured, or funded in Russian Rubles. Transactions in other currencies are treated as transactions in foreign currencies.

The Bank is required to maintain its records and prepare its financial statements for regulatory purposes in Russian Rubles in accordance with Russian accounting and banking legislation and related instructions (“RAL”). These consolidated financial statements are based on the Bank’s RAL books and records, as adjusted and reclassified in order to comply with IFRS. The reconciliation between RAL and IFRS is presented later in this note.

The preparation of financial statements requires management to make estimates and assumptions that affect reported amounts. These estimates are based on information available as of the date of the financial statements. Actual results, therefore, could differ from these estimates.

Inflation Accounting

Effective from January 1, 2003, international accounting and financial reporting bodies have determined that the Russian Federation no longer meets the criteria of IAS 29 for hyperinflation. Beginning in 2003, the Bank ceased applying IAS 29 to current periods and only recognizes the cumulative impact of inflation indexing on non-monetary elements of the financial statements through December 31, 2002. Monetary items and results of operations as of and for the year ended December 31, 2003, are reported at actual, nominal amounts.

Non-monetary assets and liabilities acquired prior to December 31, 2002, and share capital transactions occurring before December 31, 2002, have been restated by applying the relevant conversion factors to the historical cost (“restated cost”) through December 31, 2002. Gains or losses on subsequent disposal are recognised based on the restated cost of the non-monetary assets and liabilities.

5

Togliattikhimbank Notes to 2003 Consolidated Financial Statements

(Thousands of Russian Rubles)

2. Basis of Preparation (continued)

Consolidated Subsidiaries

The consolidated financial statements include the following subsidiaries:

2003 and 2002

SubsidiaryHolding,

% Country

Date of incorporatio

n IndustryDate of

acquisitionVolga-Polis OAO 53.1% Russia December 1998 Insurance July 1999

Reconciliation of RAL and IFRS Equity and Net Income

Shareholders’ equity and net income are reconciled between RAL and IFRS as follows:

2003 2002Shareholders’

equityNet

incomeShareholders

’ equityNet

income Russian Accounting Legislation (combined) 565,927 85,153 348,569 80,271Inflation impact on non-monetary capital items 9,992 – 9,992 56,876Effect of accrued expenses 1,459 13,513 (12,054) (4,678)Effect of accrued interest 4,168 (6,496) 10,664 (11,869)Impairment of financial assets (3,323) (941) (2,382) (14,168)Provisions for losses 216,973 135,511 81,462 (35,351)Accelerated depreciation (2,141) 287 (2,428) 2,172Fair value re-measurement of securities (10,149) 19,753 (29,902) (34,825)Deferred taxation (40,699) (39,173) (1,526) 11,425Expenses recorded directly to equity (30) (1,795) (30) –Equity in undistributed earnings of subsidiaries 1,862 (271) 2,133 2,133International Financial Reporting Standards 744,039 205,541 404,498 51,986

3. Summary of Accounting Policies

Principles of consolidation

The consolidated financial statements of the Bank include Togliattikhimbank and the company that it controls (subsidiary). This control is normally evidenced when the Bank owns, either directly or indirectly, more than 50% of the voting rights of a company's share capital and is able to govern the financial and operating policies of an enterprise so as to benefit from its activities. Intercompany balances and transactions, including intercompany profits and unrealized profits and losses are eliminated. Consolidated financial statements are prepared using uniform accounting policies for like transactions and other events in similar circumstances. The equity and net profit attributable to minority shareholders' interests, if any, are shown separately in the balance sheets and statements of income, respectively.

Recognition of Financial Instruments

The Bank recognizes financial assets and liabilities on its balance sheet when, and only when, it becomes a party to the contractual provisions of the instrument. Financial assets and liabilities are recognized using trade date accounting.

Financial assets and liabilities are offset and the net amount is reported in the balance sheet when there is a legally enforceable right to set off the recognized amounts and there is an intention to settle on a net basis, or realize the asset and settle the liability simultaneously.

Financial assets and liabilities are initially recognized at cost, which is the fair value of consideration given or received, respectively, including or net of any transaction costs incurred, respectively. Any gain or loss at initial recognition is recognized in the current period’s statement of income. The accounting policies for subsequent re-measurement of these items are disclosed in the respective accounting policies set out below.

6

Togliattikhimbank Notes to 2003 Consolidated Financial Statements

(Thousands of Russian Rubles)

3. Summary of Accounting Policies (continued)

Cash and Cash Equivalents

Cash and cash equivalents consist of cash on hand, amounts due from the CBR – excluding obligatory reserves, and due from credit institutions that mature within ninety days of the date of origination and are free from contractual encumbrances.

Trading Securities

Securities purchased principally for the purpose of generating a profit from short-term fluctuations in price or dealers’ margin are classified as trading securities. Trading securities are initially recognized under the policy for financial instruments and are subsequently measured at fair value, based on market values as of the balance sheet date. Realized and unrealized gains and losses resulting from operations with trading securities are recognized in the statement of income as gains less losses from trading securities. Interest earned on trading securities is reported as interest income.

In determining estimated fair value, securities are valued at the last trade price if quoted on an exchange, or the last bid price if traded over-the-counter. When market prices are not available or if liquidating the Bank’s position would reasonably be expected to impact market prices, fair value is determined by reference to price quotations for similar instruments traded in different markets or objective and reliable management estimates of the amounts that can be realized.

Amounts Due from Credit Institutions

In the normal course of business, the Bank maintains current accounts or deposits for various periods of time with other banks. Amounts due from credit institutions with a fixed maturity term are subsequently measured at amortized cost using the effective interest method. Those that do not have fixed maturities are carried at cost. Amounts due from credit institutions are carried net of any allowance for impairment.

Repurchase and Reverse Repurchase Agreements

Repurchase and reverse repurchase agreements are utilized by the Bank as an element of its treasury management and trading business. These agreements are accounted for as financing transactions.

Securities sold under repurchase agreements are accounted for as trading or available-for-sale securities and funds received under these agreements are included in amounts due to credit institutions or amounts due to customers. Securities purchased under agreements to resell (‘reverse repos’) are recorded as amounts due from credit institutions or as loans to customers.

Securities purchased under reverse repurchase agreements are not recognized in the financial statements, unless these are sold to third parties, in which case the purchase and sale are recorded with the gain or loss included in gains less losses from trading securities. The obligation to return them is recorded at fair value as a trading liability.

Any related income or expense arising from the pricing spreads of the underlying securities is recognized as interest income or expense, accrued using the effective interest method, during the period that the related transactions are open.

Investment Securities

The Bank classifies its investment securities into two categories:

• Securities with fixed maturities and fixed or determinable payments that Management has both the positive intent and the ability to hold to maturity are classified as held-to-maturity; and

• Securities that are not classified by the Bank as held-to-maturity or trading (see above) are included in the available-for-sale portfolio.

7

Togliattikhimbank Notes to 2003 Consolidated Financial Statements

(Thousands of Russian Rubles)

3. Summary of Accounting Policies (continued)

Investment Securities (continued)

The Bank classifies investment securities depending upon the intent of management at the time of the purchase. Shares of associates and subsidiaries held by the Bank exclusively with a view to their future disposal are also classified as available-for-sale. Investment securities are initially recognized in accordance with the policy stated above and subsequently re-measured using the following policies:

1. Held-to-maturity investment securities – at amortized cost using the effective interest method. Allowance for impairment is estimated on a case-by-case basis.

2. Available-for-sale investment securities are subsequently measured at fair value, which is equal to the market value as at the balance sheet date. When debt securities with fixed maturities are non-marketable or no information is available about the market value of similar instruments, fair value has been estimated as the discounted future cash flows using current interest rates. Non-marketable securities that do not have fixed maturities are stated at cost, less allowance for diminution in value unless there are other appropriate and workable methods of reasonably estimating their fair value.

Gains and losses arising from changes in the fair value of available-for-sale investment securities are recognized in the statement of income as gains less losses from available-for-sale securities in the period that the change occurs.

Promissory Notes

The majority of promissory notes held by the Bank are, in substance, equivalent to loans, and any allowance for impairment is assessed on the same basis. For promissory notes held as trading or investment securities, the Bank applies the same accounting policies as for these categories of securities.

Loans to Customers

Loans granted by the Bank by providing funds directly to the borrower are categorized as loans originated by the Bank and are initially recorded in accordance with the recognition of financial instruments policy. The difference between the nominal amount of consideration given and the fair value of loans issued at other than market terms is recognized in the period the loan is issued as initial recognition of loans to customers at fair value in the statement of income. Loans to customers with fixed maturities are subsequently measured at amortized cost using the effective interest method. Those that do not have fixed maturities are carried at cost. Loans and advances to customers are carried net of any allowance for impairment.

Leases

i. Finance - Bank as lessee The Bank recognizes finance leases as assets and liabilities in the balance sheet at the inception of the lease at amounts equal to the fair value of the leased property or, if lower, at the present value of the minimum lease payments. In calculating the present value of the minimum lease payments the discount factor used is the interest rate implicit in the lease, when it is practicable to determine; otherwise, the Bank’s incremental borrowing rate is used. Initial direct costs incurred are included as part of the asset. Lease payments are apportioned between the finance charge and the reduction of the outstanding liability. The finance charge is allocated to periods during the lease term so as to produce a constant periodic rate of interest on the remaining balance of the liability for each period.

The costs identified as directly attributable to activities performed by the lessee for a finance lease, are included as part of the amount recognised as an asset under the lease.

ii. Operating - Bank as lessee Leases of assets under which the risks and rewards of ownership are effectively retained with the lessor are classified as operating leases. Lease payments under operating lease are recognized as expenses on a straight-line basis over the lease term and included into administrative and operating expenses.

8

Togliattikhimbank Notes to 2003 Consolidated Financial Statements

(Thousands of Russian Rubles)

3. Summary of Accounting Policies (continued)

Taxation

The current income tax charge is calculated in accordance with the regulations of the Russian Federation and of Samara region. Deferred income taxes are calculated using the liability method. Deferred taxes reflect the effects of temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for income tax purposes. Deferred tax assets are recognized when it is probable that sufficient taxable profits will be available against which the deferred tax assets can be utilized.

Russia also has various operating taxes, which are assessed on the Bank’s activities. These taxes are included as a component of administrative and operating expenses in the statement of income.

Investments in Associates

Investments in associates (investments of between 20% to 50% in a company’s equity) are carried at restated cost less any allowance for permanent diminution in value. The Bank has not accounted for investments in associates using the equity method, as the Bank has no significant influence over these associates as defined by IAS 28 “Accounting for investments in associates”.

Allowances for Impairment of Financial Assets

The Bank establishes allowances for impairment of financial assets when it is probable that the Bank will not be able to collect the principal and interest according to the contractual terms of the related loans issued and other financial assets, which are carried at cost and amortized cost. The allowances for impairment of financial assets are defined as the difference between carrying amounts and the present value of expected future cash flows, including amounts recoverable from guarantees and collateral, discounted at the original effective interest rate of the financial instrument. For instruments that do not have fixed maturities, expected future cash flows are discounted using periods during which the Bank expects to realize the financial instrument.

The allowances are based on the Bank’s own loss experience and management’s judgment as to the level of losses that will most likely be recognized from assets in each credit risk category by reference to the debt service capability and repayment history of the borrower. The allowances for impairment of financial assets in the accompanying consolidated financial statements have been determined on the basis of existing economic and political conditions. The Bank is not in a position to predict what changes in conditions will take place in the Russian Federation and what effect such changes might have on the adequacy of the allowances for impairment of financial assets in future periods.

Changes in allowances are reported in the statement of income of the related period. When an asset is not collectable, it is written off against the related allowance for impairment; if the amount of impairment subsequently decreases due to an event occurring after the write-down, the reversal of the related allowance is credited to the related impairment of financial assets in the statement of income.

9

Togliattikhimbank Notes to 2003 Consolidated Financial Statements

(Thousands of Russian Rubles)

Property and Equipment

Property and equipment are carried at restated cost less accumulated depreciation and any accumulated impairment for diminution in value. Depreciation of assets under construction and those not placed in service commences from the date the assets are placed into service. Depreciation is calculated on a straight-line basis over the following estimated useful lives:

YearsBuildings 40Furniture and fixtures 5

The carrying amounts of property and equipment are reviewed at each balance sheet date to assess whether they are recorded in excess of their recoverable amounts, and where carrying values exceed this estimated recoverable amount, assets are written down. An impairment is recognized in the respective period and is included in administrative and operating expenses.

Costs related to repairs and renewals are charged when incurred and included in administrative and operating expenses, unless they qualify for capitalization.

10

Togliattikhimbank Notes to 2003 Consolidated Financial Statements

(Thousands of Russian Rubles)

3. Summary of Accounting Policies (continued)

Amounts Due to Credit Institutions and to Customers

Amounts due to credit institutions and to customers are initially recognized in accordance with recognition of financial instruments policy. Subsequently, amounts due are stated at amortized cost and any difference between net proceeds and the redemption value is recognized in the statement of income over the period of the borrowings using the effective interest method.

Debt Securities Issued

Debt securities issued represent promissory notes issued by the Bank to its customers. They are accounted for according to the same principles used for amounts due to credit institutions and to customers.

Retirement and Other Benefit Obligations

The Bank does not have any pension arrangements separate from the State pension system of the Russian Federation, which requires current contributions by the employer calculated as a percentage of current gross salary payments; such expense is charged in the period the related salaries are earned. In addition, the Bank has no post-retirement benefits or significant other compensated benefits requiring accrual.

Share Capital

Share capital is recognized at restated cost. Share capital contributions made in the form of assets other than cash are stated at their fair value at the date of contribution.

External costs directly attributable to the issue of new shares, other than on a business combination, are deducted from equity net of any related income taxes.

Dividends on ordinary shares are recognized as a reduction in shareholders’ equity in the period in which they are declared. Dividends that are declared after the balance sheet date are treated as a subsequent event under IAS 10 “Events After the Balance Sheet Date” and disclosed accordingly.

Contingencies

Contingent liabilities are not recognized in the financial statements unless it is probable that an outflow of resources will be required to settle the obligation and a reliable estimate can be made. A contingent asset is not recognized in the financial statements but disclosed when an inflow of economic benefits is probable.

11

Togliattikhimbank Notes to 2003 Consolidated Financial Statements

(Thousands of Russian Rubles)

Income and Expense Recognition

Interest income and expense are recognized on an accrual basis calculated using the effective interest method. The recognition of contractual interest income is suspended when loans become overdue by more than ninety days. Commissions and other income are recognised when the related transactions are completed. Loan origination fees for loans issued to customers, when significant, are deferred (together with related direct costs) and recognized as an adjustment to the loans effective yield. Non-interest expenses are recognized at the time the transaction occurs.

Foreign Currency Translation

Foreign currency transactions are accounted for at the exchange rates prevailing at the date of transaction. Monetary assets and liabilities denominated in foreign currencies are translated into Russian Rubles at official CBR exchange rates at the balance sheet date. Gains and losses resulting from the translation of foreign currency transactions are recognized in the statement of income as gains less losses from foreign currencies - translation differences.

Differences between the contractual exchange rate of a certain transaction and the Central Bank exchange rate on the date of the transaction are included in gains less losses from foreign currencies - dealing. The official CBR exchange rates at December 31, 2003 and 2002, were 29.45 Rubles and 31.78 Rubles to 1 USD, respectively.

12

Togliattikhimbank Notes to 2003 Consolidated Financial Statements

(Thousands of Russian Rubles)

3. Summary of Accounting Policies (continued)

Reclassifications

The following reclassifications have been made to 2002 balances to conform to the 2003 presentation.

Amount Previously reported As reclassified Comment

299 Interest income from loans Interest income from securities To achieve better presentation

2,345 Gains less losses from foreign currencies

Fee and commission income To achieve better presentation

1,173 Gains less losses from Available-for-sale securities

Other impairments and provisions To achieve better presentation

4. Cash and Cash Equivalents

Cash and cash equivalents comprise:

2003 2002Cash on hand 60,486 31,667Current accounts with the Central Bank 58,754 11,003Current accounts with other credit institutions 122,006 57,993Time deposits with credit institutions up to 90 days 162,049 39,566

Cash and cash equivalents 403,295 140,229

As of December 31, 2003, RUB 156,004 (2002 – RUB 50,319) was placed on current accounts and inter-bank deposits with three (2002 – three) internationally recognized OECD banks, who are the main counter parties of the Bank in performing international settlements.

As of December 31, 2003, RUB 100,845 (2002 – RUB 27,009) was placed on current accounts and inter-bank deposits with three (2002 – one) Russian banks.

5. Trading Securities

Trading securities owned comprise:2003 2002

Corporate shares 11,288 30,787Promissory notes of banks – 2,224

Trading securities 11,288 33,011

13

Togliattikhimbank Notes to 2003 Consolidated Financial Statements

(Thousands of Russian Rubles)

Interest rates and maturity of these securities follow:

2003 2002% Maturity % Maturity

Promissory notes of banks – – 6% 2004

6. Amounts Due from Credit Institutions

Amounts due from credit institutions comprise:

2003 2002Obligatory reserve with the Central Bank 160,092 145,142Time deposits of more than 90 days or overdue 13,991 304,677Due from brokers 3,599 –

Amounts due from credit institutions 177,682 449,819

14

Togliattikhimbank Notes to 2003 Consolidated Financial Statements

(Thousands of Russian Rubles)

6. Amounts Due from Credit Institutions (continued)

The obligatory reserve with the Central Bank represents amounts deposited with the CBR relating to daily settlements and other activities. Credit institutions are required to maintain a non-interest earning cash deposit (obligatory reserve) with the CBR, the amount of which depends on the level of funds attracted by the credit institution. The Bank’s ability to withdraw such deposit is significantly restricted by the statutory legislation.

As of December 31, 2003 and 2002 included in time deposits RUB 13,911 and RUB 293,907 represent a security for open commitments placed with three and five internationally recognized OECD banks respectively. Out of these amounts RUB nil and RUB 285,058 were fully collateralised by customers’ funds at December 31, 2003 and 2002 respectively.

7. Available-for-Sale Securities

Available-for-sale securities comprise:

2003 2002Promissory notes of banks 699,668 –Bonds of the Ministry of Finance 118,345 200,340Eurobonds of the Ministry of Finance 94,290 –Corporate equities 28,275 26,526Corporate bonds 1,786 –Municipal bonds 481 –Available-for-sale securities, gross 942,845 226,866Less – Allowance for diminution in value (7,939) (7,109)

Available-for-sale securities, net 934,906 219,757

Interest rates and maturity of these securities follow:

2003 2002% Maturity % Maturity

Bonds of the Ministry of Finance 3% 2008 3% 2003 - 2008Eurobonds of the Ministry of Finance 5% 2030 – –Promissory notes of banks – 2004 – –Corporate equities – –- – –Corporate bonds 14.25 - 17% 2005 - 2006 – –Municipal bonds 12 - 16% 2004 - 2006 – –

15

Togliattikhimbank Notes to 2003 Consolidated Financial Statements

(Thousands of Russian Rubles)

Included in corporate equities at December 31, 2003 and 2002 there are shares of associates and shares of major shareholder of the Bank held for disposal which are represented by non-marketable securities. There are no appropriate or workable methods of reasonably estimating their fair value and these shares are stated at restated cost.

The Bank has recognized 100% allowance for impairment for certain of these securities aggregating RUB 7,939 (2002 – RUB 7,109).

Included in corporate equities at December 31, 2003 and 2002, are investments in major shareholder totalling RUB 16,689 and RUB 16,689, respectively.

8. Loans to Customers

Loans to customers comprise:2003 2002

Loans to customers 2,105,916 1,562,069Promissory notes 119,229 37,332Factoring 121,889 –Loans to customers, gross 2,347,034 1,699,401Less – Allowance for loan impairment (152,630) (121,121)

Loans to customers, net 2,194,404 1,478,2808. Loans to Customers (continued)

Loans are classified as non-performing when full payment of principal or interest is in doubt (a loan with principal and interest unpaid for at least ninety days). When a loan is classified as non-performing, contractual interest income is not recognized in the financial statements. A non-performing loan may be restored to performing status when principal and interest amounts contractually due are reasonably assured of timely repayment. As of December 31, 2003, the total gross amount of non-performing loans was RUB 86,983 (2002 – RUB 52,103) against which the Bank established an allowance for impairment in the amount of RUB 47,617 (2002 – RUB 37,103). Past due contractual interest related to such loans amounted to RUB 1,886 (2002 – RUB 2,360).

As of December 31, 2003, the Bank had a concentration of loans represented by RUB 1,100,245 due from related parties, which represents 47% of gross loan portfolio (2002 – RUB 1,039,968 or 61%) and RUB 886,657 due from ten third party entities, (38% of gross loan portfolio) (2002 – RUB 298,017 or 18%). As of December 31, 2003, an allowance of RUB 90,428 (2002 – RUB 65,192) was made against these loans to related parties and RUB 39,006 (2002 – RUB 20,163) was made against these loans to third parties.

Loans have been extended to the following types of customers:

2003 2002Private companies 2,316,475 1,580,531State companies 15,000 10,000Individuals 15,559 8,870

2,347,034 1,599,401

Loans are made principally within Russia in the following industry sectors:

2003 2002Manufacturing 1,070,200 1,057,812Machine-building 649,509 225,624Trading enterprises 267,642 180,477Real estate construction 191,113 –Transport 20,370 10,000Telecommunication 6,500 21,501Individuals 15,559 16,741Other 126,141 87,246

2,347,034 1,599,401

16

Togliattikhimbank Notes to 2003 Consolidated Financial Statements

(Thousands of Russian Rubles)

9. Taxation

The corporate income tax expense comprises:

2003 2002Current tax charge 27,810 31,355Deferred tax charge (benefit) 39,173 (13,382)Income tax expense 66,983 17,973

Russian legal entities must file individual tax declarations. The tax rate for banks for profits other than on state securities was 24% for 2003 and 2002. The tax rate for interest income on state securities was 15% for Federal taxes. The tax rate for companies other than banks was also 24 % for 2003 and 2002.

Tax assets and liabilities consist of the following:

2003 2002Current tax assets 9,195 –Deferred tax assets – –Tax assets 9,195 –

Current tax liabilities – (1,589)Deferred tax liabilities (40,699) (1,526)Tax liabilities (40,699) (3,115)

9. Taxation (continued)

The effective income tax rate differs from the statutory income tax rates. A reconciliation of the income tax expense based on statutory rates with actual is as follows:

2003 2002Income before tax 272,284 70,949Statutory tax rate 24% 24%

Theoretical income tax expense at the statutory rate 65,348 17,028State securities non-taxable income (1,089) (3,840)Tax exempt income – (1,129)Non –deductible expenditures 2,724 1,064Permanent element of monetary gains and losses – 4,850Other items – –Income tax expense 66,983 17,973

Deferred tax assets and liabilities as of December 31 comprise:

2003 2002Tax effect of deductible temporary differences:Fair value measurement of securities – 6,158Accrued expenses 267 2,216Accrued income – 1,537Gross deferred tax assets 267 9,911Unrecognized deferred tax assets – –Deferred tax asset 267 9,911

Tax effect of taxable temporary differences:Release of allowances for impairment and provisions for other losses (38,616) (8,485)Fair value measurement of securities (524) –Property and equipment (1,826) (2,952)Deferred tax liability (40,966) (11,437)Deferred tax liability (40,699) (1,526)

17

Togliattikhimbank Notes to 2003 Consolidated Financial Statements

(Thousands of Russian Rubles)

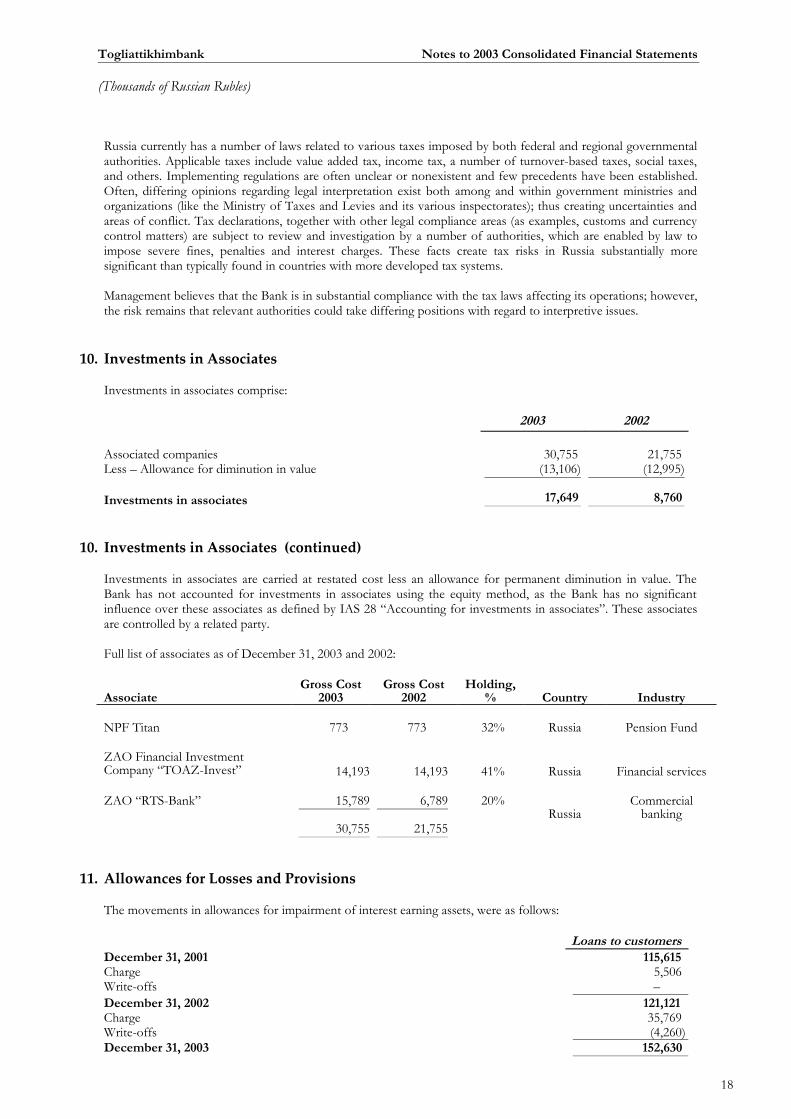

Russia currently has a number of laws related to various taxes imposed by both federal and regional governmental authorities. Applicable taxes include value added tax, income tax, a number of turnover-based taxes, social taxes, and others. Implementing regulations are often unclear or nonexistent and few precedents have been established. Often, differing opinions regarding legal interpretation exist both among and within government ministries and organizations (like the Ministry of Taxes and Levies and its various inspectorates); thus creating uncertainties and areas of conflict. Tax declarations, together with other legal compliance areas (as examples, customs and currency control matters) are subject to review and investigation by a number of authorities, which are enabled by law to impose severe fines, penalties and interest charges. These facts create tax risks in Russia substantially more significant than typically found in countries with more developed tax systems.

Management believes that the Bank is in substantial compliance with the tax laws affecting its operations; however, the risk remains that relevant authorities could take differing positions with regard to interpretive issues.

10. Investments in Associates

Investments in associates comprise:

2003 2002

Associated companies 30,755 21,755Less – Allowance for diminution in value (13,106) (12,995)

Investments in associates 17,649 8,760

10. Investments in Associates (continued)

Investments in associates are carried at restated cost less an allowance for permanent diminution in value. The Bank has not accounted for investments in associates using the equity method, as the Bank has no significant influence over these associates as defined by IAS 28 “Accounting for investments in associates”. These associates are controlled by a related party.

Full list of associates as of December 31, 2003 and 2002:

AssociateGross Cost

2003Gross Cost

2002Holding,

% Country Industry

NPF Titan 773 773 32% Russia Pension Fund

ZAO Financial Investment Company “TOAZ-Invest” 14,193 14,193 41% Russia Financial services

ZAO “RTS-Bank” 15,789 6,789 20%Russia

Commercial banking

30,755 21,755

11. Allowances for Losses and Provisions

The movements in allowances for impairment of interest earning assets, were as follows:

Loans to customersDecember 31, 2001 115,615Charge 5,506Write-offs –December 31, 2002 121,121Charge 35,769Write-offs (4,260)December 31, 2003 152,630

18

Togliattikhimbank Notes to 2003 Consolidated Financial Statements

(Thousands of Russian Rubles)

19

Togliattikhimbank Notes to 2003 Consolidated Financial Statements

(Thousands of Russian Rubles)

The movements in allowances for other losses and provisions, were as follows:

Investment securities

Associates Available-for-sale

(equity) TotalDecember 31, 2001 – 5,936 5,936Charge 12,995 1,173 14,168Write- offs – – –December 31, 2002 12,995 7,109 20,104Charge 111 830 941Write-offs – – –December 31, 2003 13,106 7,939 21,045

Allowances for impairment of assets are deducted from the related assets. In accordance with the Russian legislation, loans may only be written off with the approval of the Shareholders’ Council and, in certain cases, with the respective decision of the Court.

20

Togliattikhimbank Notes to 2003 Consolidated Financial Statements

(Thousands of Russian Rubles)

12. Property and Equipment

The movements of property and equipment, were as follows:

BuildingFurniture and

fixturesConstruction in

progress TotalCost

December 31, 2002 2,524 50,762 610 53,896Additions – 6,307 – 6,307Disposals – (2,162) (610) (2,772)December 31, 2003 2,524 54,907 – 57,431

Accumulated depreciationDecember 31, 2002 447 34,612 – 35,059Charge 133 6,929 – 7,062Disposals – (1,809) – (1,809)December 31, 2003 580 39,732 – 40,312

Net book value:December 31, 2002 2,007 16,150 610 18,837December 31, 2003 1,944 15,175 – 17,119

13. Amounts Due to Credit Institutions

Amounts due to credit institutions comprise:

2003 2002Current accounts 128,710 41,520Time deposits and loans – 97,976Amounts due to credit institutions 128,710 139,496

Included into current accounts is a balance of RUB 121,910 (2002 - RUB 41,156) with a single Russian bank.

At December 31, 2002, deposits of RUB 34,694 and RUB 30,000 were received from one Russian and one OECD-based bank accordingly.

14. Amounts Due to Customers

The amounts due to customers included balances in customer current accounts, term deposits, and certain other liabilities, and include the following:

2003 2002Current accounts 1,274,215 675,469Time deposits 642,579 435,896Amounts due to customers 1,916,794 1,111,365

Held as security against letters of credit – 285,058

At December 31, 2003 amounts due to customers included RUB 473,246 (or 25% of total amount due to customers) due to related parties (2002 - RUB 369,191 or 33%) and RUB 1,000,227 (or 52% of total amount due to customers) due to four third party customers (2002 - RUB 149,187 or 13%).

Amounts due to customers include accounts with the following types of customers:

2003 2002State and budgetary organisations 33,120 –Private enterprises 1,509,423 690,995Individuals 363,120 405,388Employees 11,131 14,982Amounts due to customers 1,916,794 1,111,365

14. Amounts Due to Customers (continued)

21

Togliattikhimbank Notes to 2003 Consolidated Financial Statements

(Thousands of Russian Rubles)

An analysis of customer accounts by sector follows:

2003 2002Trading enterprises 1,133,650 294,540Manufacturing 228,636 146,901Financial services 123,806 233,637Public services 33,120 –Insurance – 15,917Individuals 374,251 420,370Other 23,331 –Amounts due to customers 1,916,794 1,111,365

15. Amounts Due to Related Party

At December 31, 2002 amounts due to related party represent settlements for the purchase of investment securities which were subsequently settled.

16. Debt Securities Issued

As of December 31, 2003 and 2002 debt securities issued consisted of the promissory notes.

As of December 31, 2003, the Bank had issued non-interest-bearing promissory notes having an aggregate nominal value of RUB 624,154 (2002 – 438,037) maturing within three months after respective balance sheet date. Other debt securities issued by the Bank as of December 31, 2003, bear annual interest rates ranging from 5% to 16% (2002 – from 7% to 14%) and mature within six months after respective balance sheet date.

As of December 31, 2003 and 2002, debt securities issued to related parties amounted to RUB 660,561 (or 80% of total debt securities issued) and RUB 261,340 (or 53% of total debt securities issued), respectively.

17. Subordinated Loan

In November 2001 the Bank obtained US$-denominated subordinated loan, totalling US$ 2,000,000, from a foreign related party which matures in May 2007 and carries interest LIBOR + 6% p.a. payable annually and at redemption. The balance outstanding at December 31, 2003 and 2002 was RUB 59,587 and 64,308, respectively, including accrued interests.

In April and May 2003 the Bank obtained two US$-denominated subordinated loans, totalling US$ 320,000, from another foreign related party which mature in May and June 2008 accordingly and both carry interest LIBOR + 1% p.a. payable semi-annually and at redemption. The balance outstanding at December 31, 2003 was RUB 9,594, including accrued interests.

22

Togliattikhimbank Notes to 2003 Consolidated Financial Statements

(Thousands of Russian Rubles)

18. Shareholders’ Equity

At December 31, 2002 authorized, issued and fully paid share capital consisted of 160,000 RUB-denominated ordinary shares with equal voting rights. All shares have a nominal value of 50 Russian Roubles.

The share capital of the Bank was contributed by the shareholders in Russian Rubles and they are entitled to dividends and any capital distribution in Russian Rubles.

On February 2003 amendments to the share capital of the Bank were approved by shareholders as follows: the share capital was increased through 2nd share emission by 2,680,000 number of shares of Ruble 50 each. All shares were issued, paid in and registered by the Central Bank of Russian Federation on July 15, 2003, therefore at December 31, 2003 authorized, issued and fully paid capital consisted of 2,840,000 shares.

23

Togliattikhimbank Notes to 2003 Consolidated Financial Statements

(Thousands of Russian Rubles)

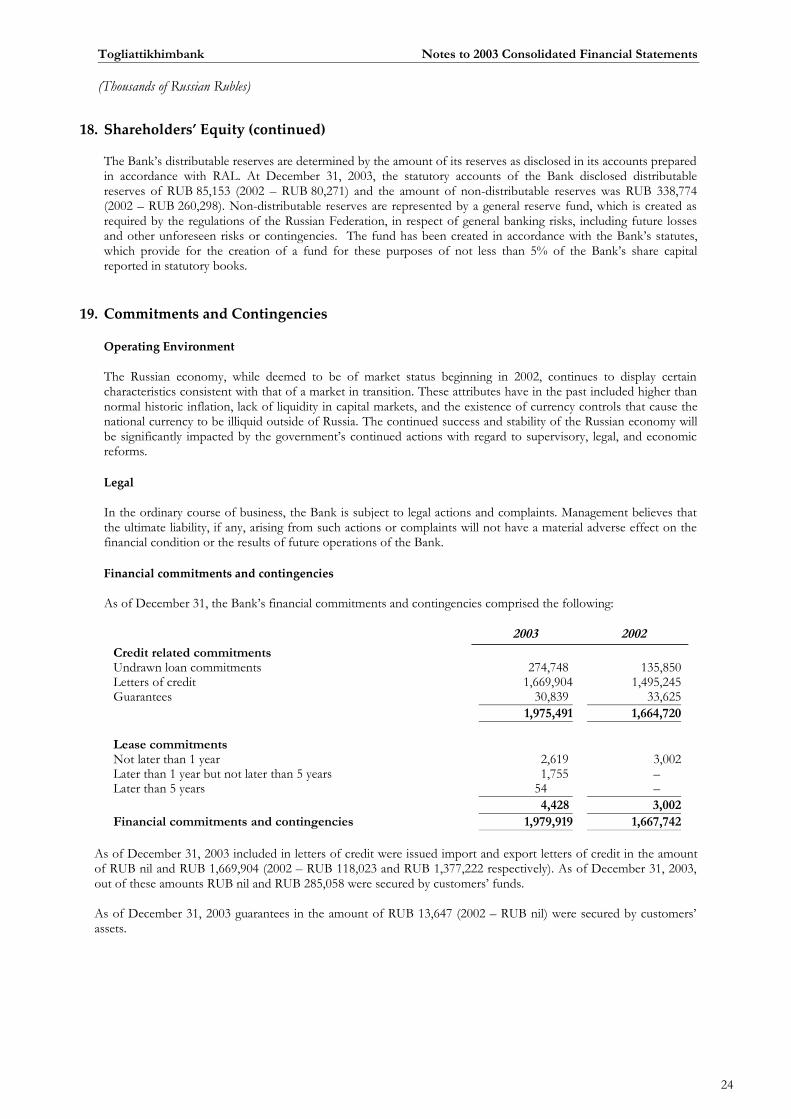

18. Shareholders’ Equity (continued)

The Bank’s distributable reserves are determined by the amount of its reserves as disclosed in its accounts prepared in accordance with RAL. At December 31, 2003, the statutory accounts of the Bank disclosed distributable reserves of RUB 85,153 (2002 – RUB 80,271) and the amount of non-distributable reserves was RUB 338,774 (2002 – RUB 260,298). Non-distributable reserves are represented by a general reserve fund, which is created as required by the regulations of the Russian Federation, in respect of general banking risks, including future losses and other unforeseen risks or contingencies. The fund has been created in accordance with the Bank’s statutes, which provide for the creation of a fund for these purposes of not less than 5% of the Bank’s share capital reported in statutory books.

19. Commitments and Contingencies

Operating Environment

The Russian economy, while deemed to be of market status beginning in 2002, continues to display certain characteristics consistent with that of a market in transition. These attributes have in the past included higher than normal historic inflation, lack of liquidity in capital markets, and the existence of currency controls that cause the national currency to be illiquid outside of Russia. The continued success and stability of the Russian economy will be significantly impacted by the government’s continued actions with regard to supervisory, legal, and economic reforms.

Legal

In the ordinary course of business, the Bank is subject to legal actions and complaints. Management believes that the ultimate liability, if any, arising from such actions or complaints will not have a material adverse effect on the financial condition or the results of future operations of the Bank.

Financial commitments and contingencies

As of December 31, the Bank’s financial commitments and contingencies comprised the following:

2003 2002Credit related commitmentsUndrawn loan commitments 274,748 135,850Letters of credit 1,669,904 1,495,245Guarantees 30,839 33,625

1,975,491 1,664,720

Lease commitmentsNot later than 1 year 2,619 3,002Later than 1 year but not later than 5 years 1,755 –Later than 5 years 54 –

4,428 3,002Financial commitments and contingencies 1,979,919 1,667,742

As of December 31, 2003 included in letters of credit were issued import and export letters of credit in the amount of RUB nil and RUB 1,669,904 (2002 – RUB 118,023 and RUB 1,377,222 respectively). As of December 31, 2003, out of these amounts RUB nil and RUB 285,058 were secured by customers’ funds.

As of December 31, 2003 guarantees in the amount of RUB 13,647 (2002 – RUB nil) were secured by customers’ assets.

24

Togliattikhimbank Notes to 2003 Consolidated Financial Statements

(Thousands of Russian Rubles)

20. Gains Less Losses from Available-for-Sale Securities

Gains less losses from available-for-sale securities comprise:

2003 2002Unrealized gains (losses) 27,592 (29,902)Sales and redemptions (1,954) 9,375Gains less losses from available-for-sale securities 25,638 (20,527)

21. Salaries and Administrative and Operating Expenses

Salaries and benefits, administrative and operating expenses comprise:

2003 2002Salaries and bonuses 18,695 40,673Social security costs 5,690 7,879Salaries and benefits 24,385 48,552

Repair and maintenance of property and equipment 5,230 18,908Data processing 949 3,930Occupancy and rent 3,438 1,251Office supplies 1,105 1,843Operating taxes 8,332 12,271Security 365 1,248Communications 9,332 11,578Marketing and advertising 6,624 –Charity 60 –Insurance 1,583 1,202Legal and consultancy 2,405 1,365Business travel and related 935 1,096Loss on property and equipment disposals 1,197 8,382Penalties incurred 186 85Other 6,945 8,386Administrative and operating expenses 48,686 75,225

The aggregate remuneration and other benefits paid to members of the Shareholders’ Council and Management Boards for 2003 was RUB 1,533 (2002 – RUB 1,322).

22. Risk Management Policies

Management of risk is fundamental to the banking business and is an essential element of the Bank’s operations. The main risks inherent to the Bank’s operations are those related to credit, liquidity and market movements in interest and foreign exchange rates. A summary description of the Bank’s risk management policies in relation to those risks follows.

Credit Risk

The Bank is exposed to credit risk which is the risk that a counter party will be unable to pay amounts in full when due. The Bank structures the levels of credit risk it undertakes by placing limits on the amount of risk accepted in relation to one borrower, or groups of borrowers, and to industry segments. Limits on the level of credit risk by borrower and product are approved by the Credit Committee. Where appropriate, and in the case of most loans, the Bank obtains collateral. Such risks are monitored on a continuous basis and subject to annual or more frequent reviews.

The exposure to any one borrower including banks and brokers is further restricted by sub-limits covering on and off-balance sheet exposures which are set by the Credit Committee. The maximum credit risk exposure, ignoring the fair value of any collateral, in the event other parties fail to meet their obligations under financial instruments is equal to the carrying value of financial assets as presented in the accompanying financial statements and the disclosed financial commitments.

25

Togliattikhimbank Notes to 2003 Consolidated Financial Statements

(Thousands of Russian Rubles)

22. Risk Management Policies (continued)

Concentration

The geographical concentration of Bank’s assets and liabilities is set out below:

2003 2002Russia OECD Total Russia OECD Total

Assets:Cash and cash equivalents 244,599 158,696 403,295 87,587 52,642 140,229Trading securities 11,288 – 11,288 33,011 – 33,011Due from credit institutions 163,691 13,991 177,682 152,337 297,482 449,819Available-for-sale securities 934,906 – 934,906 219,757 – 219,757Loans to customers 2,194,404 – 2,194,404 1,478,280 – 1,478,280Tax assets 9,195 9,195 – – –Other assets 7,984 – 7,984 9,818 – 9,818

3,566,067 172,687 3,738,754 1,980,790 350,124 2,330,914Liabilities:Amounts due to other banks 128,710 – 128,710 71,520 67,976 139,496Amounts due to customers 1,610,157 306,637 1,916,794 907,963 203,402 1,111,365Amounts due to related party – – – 124,648 – 124,648Debt securities issued 858,157 – 858,157 493,394 – 493,394Tax liability 40,699 – 40,699 3,115 – 3,115Subordinated loan – 69,181 69,181 – 64,308 64,308Other liabilities 11,011 – 11,011 12,516 – 12,516

2,648,734 375,818 3,024,552 1,613,156 335,686 1,948,842Net balance sheet position 917,333 (203,131) 714,202 367,634 14,438 382,072

Net off balance sheet position 1,979,919 – 1,979,919 1,667,742 – 1,667,742

Market Risk

The Bank takes on exposure to market risks. Market risks arise from open positions in interest rate and currency products, all of which are exposed to general and specific market movements. The Bank manages market risk through periodic estimation of potential losses that could arise from adverse changes in market conditions and establishing and maintaining appropriate stop-loss limits and margin and collateral requirements.

With respect to undrawn loan commitments the Bank is potentially exposed to loss in an amount equal to the total amount of such commitments. However, the likely amount of loss is less than that, since most commitments are contingent upon certain conditions set out in the loan agreements.

26

Togliattikhimbank Notes to 2003 Consolidated Financial Statements

(Thousands of Russian Rubles)

22. Risk Management Policies (continued)

27

Togliattikhimbank Notes to 2003 Consolidated Financial Statements

(Thousands of Russian Rubles)

Currency Risk

The Bank is exposed to effects of fluctuation in the prevailing foreign currency exchange rates on its financial position and cash flows. The Board of Directors sets limits on the level of exposure by currencies (primarily USD). These limits also comply with the minimum requirements of the Central Bank of Russia. The Bank’s exposure to foreign currency exchange rate risk follows:

2003 2002

Rubles

Freely convertibl

eNon

convertible Total Rubles

Freely convertibl

e

Non convertibl

e TotalAssets:Cash and cash equivalents 140,593 262,645 57 403,295 58,991 79,842 1,396 140,229Trading securities 11,288 – – 11,288 33,011 – – 33,011Due from credit

institutions 163,691 13,991 – 177,682 145,142 304,677 – 449,819Available-for-sale

securities 722,271 212,635 – 934,906 19,417 200,340 – 219,757Loans to customers 1,999,888 194,516 – 2,194,404 1,004,487 473,793 – 1,478,280Tax assets 9,195 9,195 – – – –Other assets 7,395 589 – 7,984 9,818 – – 9,818

3,054,321 684,376 57 3,738,754 1,270,866 1,058,652 1,396 2,330,914Liabilities:Due to other banks 128,284 426 – 128,710 71,158 68,338 – 139,496Due to customers 1,209,251 707,486 57 1,916,794 298,120 811,936 1,309 1,111,365Due to related party – – – – – 124,648 – 124,648Debt securities issued 837,325 20,832 – 858,157 472,389 21,005 – 493,394Tax liability 40,699 – – 40,699 3,115 – – 3,115Subordinated loan – 69,181 – 69,181 – 64,308 – 64,308Other liabilities 11,011 – – 11,011 12,516 – – 12,516

2,226,570 797,925 57 3,024,552 857,298 1,090,235 1,309 1,948,842Net balance sheet

position 827,751 (113,549) – 714,202 413,568 (31,583) 87 382,072

Net off balance sheet position 283,413 1,669,184 27,322 1,979,919 84,224 1,583,518 – 1,667,742

Freely convertible currencies represent mainly USD amounts, but also include currencies from other OECD countries. Non-freely convertible amounts relate to currencies of CIS countries, excluding Russia.

The Bank’s principal cash flows (revenues, operating expenses) are largely generated in Russian Rubles. As a result, future movements in the exchange rate between the Russian Rubles and USD will affect the carrying value of the Bank’s USD denominated monetary assets and liabilities.

28

Togliattikhimbank Notes to 2003 Consolidated Financial Statements

(Thousands of Russian Rubles)

22. Risk Management Policies (continued)

Interest Rate Risk

Interest rate risk arises from the possibility that changes in interest rates will affect the value of the financial instruments. The Bank’s interest rate policy is reviewed and approved by the Bank’s Financial Committee.

As of December 31, the average interest rates by currencies and comparative market rates for interest generating/ bearing monetary financial instruments were as follows:

2003 2002

Rubles USD

Other foreign

currencies Rubles USD

Other foreign

currenciesBank ratesDue from credit institutions – 0.01% 5% – 1.54 – 9.5% –Trading securities – – – 6% – –Available-for-sale securities 1 - 16% 3 - 5% – – 3% –Loans to customers 6 - 24% 4.81 - 15% – 9.8 - 30% 9.7 - 17% –Due to credit institutions – – – 14.25% 8% –Customer deposits 7 - 17% 2.5 - 8% 5% 9 - 15% 7.4 - 8% –Debt securities issued 5 - 16% 8% – 7 - 14% – –Subordinated loans – 2.22 - 7.22% – – 7.4% –

The majority of the Bank’s loan contracts and other financial assets and liabilities that bear interest are either variable or contain clauses enabling the interest rate to be changed at the option of the lender. The Bank monitors its interest rate margin and consequently does not consider itself exposed to significant interest rate risk or consequential cash flow risk.

Liquidity Risk

Liquidity risk refers to the availability of sufficient funds to meet deposit withdrawals and other financial commitments associated with financial instruments as they actually fall due. In order to manage liquidity risk, the Bank performs daily monitoring of future expected cash flows on clients’ and banking operations, which is a part of assets/liabilities management process. The Board sets limits on the minimum proportion of maturing funds available to meet deposit withdrawals and on the minimum level on interbank and other borrowing facilities that should be in place to cover withdrawals at unexpected levels of demand.The tables on the following page provide an analysis of banking assets and liabilities grouped on the basis of the remaining period from the balance sheet date to the contractual maturity date.

2003

On demand

Less than1 month

1 to 3 months

3 months to 1 year

1 to 5 years Total

Assets:Cash and cash equivalents 241,246 162,049 – – – 403,295Trading securities 11,288 – – – – 11,288Due from credit institutions 115,490 9,123 9,173 30,177 13,719 177,682Available-for-sale securities – 699,668 140,948 – 94,290 934,906Loans to customers – 1,261,622 503,247 420,654 8,881 2,194,404Tax assets – 9,195 – – – 9,195Other assets – 7,984 – – – 7,984

368,024 2,149,641 653,368 450,831 116,890 3,738,754Liabilities:Amounts due to other banks 128,710 – – – – 128,710Amounts due to customers 1,382,762 66,143 109,830 344,998 13,061 1,916,794Debt securities issued 18,013 481,939 227,698 130,207 300 858,157Tax liability – – – 40,699 – 40,699Subordinated loan – – 847 68,334 69,181Other liabilities – 11,011 – – – 11,011

29

Togliattikhimbank Notes to 2003 Consolidated Financial Statements

(Thousands of Russian Rubles)

1,529,485 559,093 337,528 516,751 81,695 3,024,552Net position (1,161,461) 1,590,548 315,840 (65,920) 35,195 714,202Accumulated gap (1,161,461) 429,087 744,927 679,007 714,202

22. Risk Management Policies (continued)

Liquidity Risk (continued)

2002

On demand

Less than

1 month1 to

3 months3 months to

1 year1 to

5 years TotalAssets:Cash and cash equivalents 100,663 36,400 3,166 – – 140,229Trading securities 33,011 – – – – 33,011Due from credit institutions 60,545 38,628 104,136 244,551 1,959 449,819Available-for-sale securities – 19,417 – 88,322 112,018 219,757Loans to customers – 174,549 346,284 954,441 3,006 1,478,280Other assets – 9,818 – – – 9,818

194,219 278,812 453,586 1,287,314 116,983 2,330,914Liabilities:Amounts due to other banks 139,496 – – – – 139,496Amounts due to customers 463,598 148,121 117,686 369,564 12,396 1,111,365Amounts due to related party – 124,648 – – – 124,648Debt securities issued 397,241 43,947 39,085 13,121 – 493,394Income tax liability 1,589 – – 1,526 – 3,115Subordinated loan – – – – 64,308 64,308Other liabilities – 9,022 3,494 – – 12,516

1,001,924 325,738 160,265 384,211 76,704 1,948,842Net position (807,705) (46,926) 293,321 903,103 40,279 382,072Accumulated gap (807,705) (854,631) (561,310) 341,793 382,072

The Bank’s capability to discharge its liabilities relies on its ability to realise an equivalent amount of assets within the same period of time. There is a significant deficit at December 31, 2002 in the period less than 3 months, resulting from a significant concentration of deposits from customers.

Long-term credits and overdraft facilities are generally not available in Russia. However, the Bank practices to grant short-term loans which are usually renewed by clients at maturity. As such, the ultimate maturity of assets may be different from the analysis presented above. In addition, the maturity gap analysis does not reflect the historical stability of current accounts. Their liquidation has historically taken place over a longer period than indicated in the tables above. These balances are included in amounts at demand in the tables above. While trading securities are shown at demand, realizing such assets upon demand is dependent upon financial market conditions (see Note 2). Significant security positions may not be liquidated in a short period of time without adverse price effects.

23. Fair Values of Financial Instruments

The following disclosure of the estimated fair value of financial instruments is made in accordance with the requirements of IAS 32 “Financial Instruments: Disclosure and Presentation”. Fair value is defined as the amount at which the instrument could be exchanged in a current transaction between knowledgeable willing parties on arm’s length conditions, other than in forced or liquidation sale. As no readily available market exists for part of the Bank’s financial instruments, judgment is necessary in arriving at fair value, based on current economic conditions and the specific risks attributable to the instrument. The estimates presented herein are not necessarily

30

Togliattikhimbank Notes to 2003 Consolidated Financial Statements

(Thousands of Russian Rubles)

indicative of the amounts the Bank could realize in a market exchange from the sale of its full holdings of a particular instrument.

The following methods and assumptions are used by the Bank to estimate the fair value of these financial instruments:

Amounts Due from and to Credit Institutions

For assets maturing within one month, the carrying amount approximates fair value due to the relatively short- term maturity of these financial instruments. For longer-term deposits, the interest rates applicable reflect market rates and, consequently, the fair value approximates the carrying amounts.

31

Togliattikhimbank Notes to 2003 Consolidated Financial Statements

(Thousands of Russian Rubles)

23. Fair Values of Financial Instruments (continued)

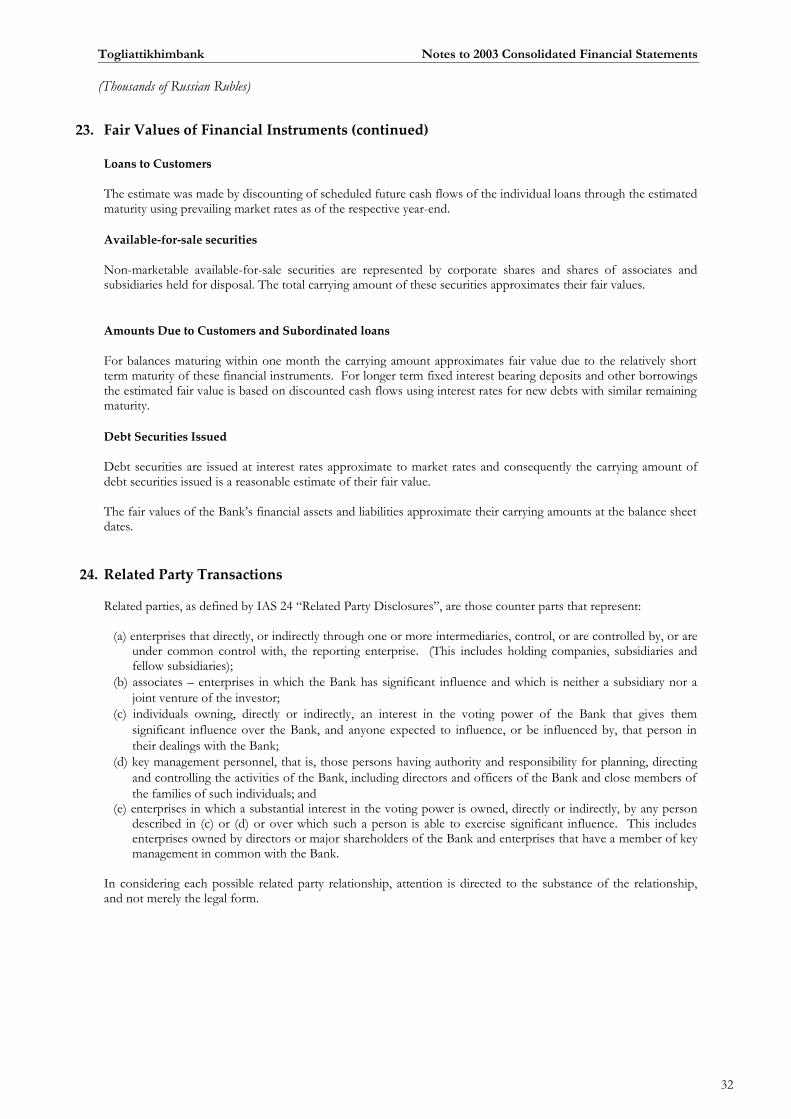

Loans to Customers

The estimate was made by discounting of scheduled future cash flows of the individual loans through the estimated maturity using prevailing market rates as of the respective year-end.

Available-for-sale securities

Non-marketable available-for-sale securities are represented by corporate shares and shares of associates and subsidiaries held for disposal. The total carrying amount of these securities approximates their fair values.

Amounts Due to Customers and Subordinated loans

For balances maturing within one month the carrying amount approximates fair value due to the relatively short term maturity of these financial instruments. For longer term fixed interest bearing deposits and other borrowings the estimated fair value is based on discounted cash flows using interest rates for new debts with similar remaining maturity.

Debt Securities Issued

Debt securities are issued at interest rates approximate to market rates and consequently the carrying amount of debt securities issued is a reasonable estimate of their fair value.