top frontier investment holdings, inc. and … financial statements.pdf · top frontier investment...

TRANSCRIPT

TOP FRONTIER INVESTMENT HOLDINGS, INC.

AND SUBSIDIARIES

CONSOLIDATED FINANCIAL STATEMENTS

August 31, 2013

and

FINANCIAL STATEMENTS

December 31, 2012, 2011 and 2010

kpmg

Manabat Sanagustin & Co., CPAs Telephone +63 (2) 885 7000

The KPMG Center, 9/F Fax +63 (2) 894 1985

6787 Ayala Avenue Internet www.kpmg.com.ph

Makati City 1226, Metro Manila, Philippines E-Mail [email protected]

Branches: Bacolod · Cebu · Iloilo · Subic

Manabat Sanagustin & Co., CPAs, a Philippine

partnership and a member firm of the KPMG network of

independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity.

PRC-BOA Registration No. 0003, Group A, valid until December 31, 2013

SEC Accreditation No. 0004-FR-3, Group A, valid until November 22, 2014

IC Accreditation No. F-0040-R, Group A, valid until September 11, 2014

BSP Accredited, Group A, valid until December 17, 2014

part

ner

shi

ind

epe

REPORT OF INDEPENDENT AUDITORS

The Board of Directors and Stockholders

Top Frontier Investment Holdings, Inc.

We have audited the accompanying consolidated financial statements of Top Frontier Investment

Holdings, Inc. and Subsidiaries, which comprise the consolidated statement of financial position

as at August 31, 2013 and the consolidated statement of comprehensive income, consolidated

statement of changes in equity and consolidated statement of cash flows for the eight months

ended August 31, 2013, and notes, comprising a summary of significant accounting policies and

other explanatory information. Also, we have audited the accompanying financial statements of

Top Frontier Investment Holdings, Inc., which comprise the statements of financial position as at

December 31, 2012 and 2011 and the statements of comprehensive income, statements of

changes in equity and statements of cash flows for the eight months ended August 31, 2012 and

for the years ended December 31, 2012, 2011 and 2010, and notes, comprising a summary of

significant accounting policies and other explanatory information.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements

in accordance with Philippine Financial Reporting Standards, and for such internal control as

management determines is necessary to enable the preparation of financial statements that are

free from material misstatement, whether due to fraud or error.

Auditors’ Responsibility

Our responsibility is to express an opinion on these financial statements based on our audits.

We conducted our audits in accordance with Philippine Standards on Auditing. Those standards

require that we comply with ethical requirements and plan and perform the audit to obtain

reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and

disclosures in the financial statements. The procedures selected depend on the auditors‟

judgment, including the assessment of the risks of material misstatement of the financial

statements, whether due to fraud or error. In making those risk assessments, the auditors consider

internal control relevant to the entity‟s preparation and fair presentation of the financial

statements in order to design audit procedures that are appropriate in the circumstances, but not

for the purpose of expressing an opinion on the effectiveness of the entity‟s internal control. An

audit also includes evaluating the appropriateness of accounting policies used and the

reasonableness of accounting estimates made by management, as well as evaluating the overall

presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a

basis for our audit opinion.

Manabat Sanagustin & Co., CPAs, a Philippine

partnership and a member firm of the KPMG network of

independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity.

PRC-BOA Registration No. 0003, Group A, valid until December 31, 2013

SEC Accreditation No. 0004-FR-3, Group A, valid until November 22, 2014

IC Accreditation No. F-0040-R, Group A, valid until September 11, 2014

BSP Accredited, Group A, valid until December 17, 2014

part

ner

shi

ind

epe

kpmg

Manabat Sanagustin & Co., CPAs Telephone +63 (2) 885 7000

The KPMG Center, 9/F Fax +63 (2) 894 1985

6787 Ayala Avenue Internet www.kpmg.com.ph

Makati City 1226, Metro Manila, Philippines E-Mail [email protected]

Branches: Bacolod · Cebu · Iloilo · Subic

REPORT OF INDEPENDENT AUDITORS

The Board of Directors and Stockholders

Top Frontier Investment Holdings, Inc.

5th Floor, ENZO Building

399 Sen. Gil J. Puyat Avenue, Makati City

We have audited the accompanying consolidated financial statements of Top Frontier Investment

Holdings, Inc. and Subsidiaries, which comprise the consolidated statement of financial position

as at August 31, 2013 and the consolidated statement of comprehensive income, consolidated

statement of changes in equity and consolidated statement of cash flows for the eight months

ended August 31, 2013, and notes, comprising a summary of significant accounting policies and

other explanatory information. Also, we have audited the accompanying financial statements of

Top Frontier Investment Holdings, Inc., which comprise the statements of financial position as at

December 31, 2012 and 2011 and the statements of comprehensive income, statements of

changes in equity and statements of cash flows for the eight months ended August 31, 2012 and

for the years ended December 31, 2012, 2011 and 2010, and notes, comprising a summary of

significant accounting policies and other explanatory information.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements

in accordance with Philippine Financial Reporting Standards, and for such internal control as

management determines is necessary to enable the preparation of financial statements that are

free from material misstatement, whether due to fraud or error.

Auditors’ Responsibility

Our responsibility is to express an opinion on these financial statements based on our audits.

We conducted our audits in accordance with Philippine Standards on Auditing. Those standards

require that we comply with ethical requirements and plan and perform the audit to obtain

reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and

disclosures in the financial statements. The procedures selected depend on the auditors‟

judgment, including the assessment of the risks of material misstatement of the financial

statements, whether due to fraud or error. In making those risk assessments, the auditors consider

internal control relevant to the entity‟s preparation and fair presentation of the financial

statements in order to design audit procedures that are appropriate in the circumstances, but not

for the purpose of expressing an opinion on the effectiveness of the entity‟s internal control. An

audit also includes evaluating the appropriateness of accounting policies used and the

reasonableness of accounting estimates made by management, as well as evaluating the overall

presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a

basis for our audit opinion.

TOP FRONTIER INVESTMENT HOLDINGS, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF FINANCIAL POSITION

(In Thousands)

August 31 December 31

Note 2013 2012* 2011*

ASSETS

Current Assets

Cash and cash equivalents 5, 6, 24 P711,321 P202,681 P28,720

Receivables 5, 7, 18, 24 76,165 550,585 -

Prepaid expenses and other current assets 5, 8 90,967 9,790 8,817

Total Current Assets 878,453 763,056 37,537

Noncurrent Assets

Available-for-sale financial assets 9, 24 117,982,526 165,804,776 169,110,711

Property, plant and equipment 5 137,610 - -

Mineral rights and evaluation assets 5, 11 13,638,036 - -

Deferred tax assets 5, 22 311,833 - -

Goodwill 5 1,643,990 - -

Advances for investment in shares of stock 9, 24 - - 9,392,600

Derivative assets 10, 24 - - 16,602,012

Other noncurrent assets - net 5, 12, 24 234,931 247 370

Total Noncurrent Assets 133,948,926 165,805,023 195,105,693

P134,827,379 P166,568,079 P195,143,230

LIABILITIES AND EQUITY

Current Liabilities

Accounts payable and other current

liabilities 5, 13, 18, 24 P13,900,535 P10,895,252 P23,834,960

Loans payable - net of debt issue costs 5, 14, 24 28,716,468 - -

Total Current Liabilities 42,617,003 10,895,252 23,834,960

Noncurrent Liabilities

Premium liability 10 - - 1,842,727

Loans payable - net of debt issue costs 14, 24 - 26,098,142 -

Deferred tax liabilities 5, 22 590,032 - -

Accrual for mine rehabilitation and

decommissioning 5, 16 16,115 - -

Retirement liability 5, 21 8,485 - -

Other noncurrent liabilities 5, 15, 18, 24 14,744,077 - -

Total Noncurrent Liabilities 15,358,709 26,098,142 1,842,727

Total Liabilities 57,975,712 36,993,394 25,677,687

Equity

Equity Attributable to Equity Holders of

the Parent Company

Capital stock 17 750,000 750,000 750,000

Additional paid-in capital 17 92,500,000 92,500,000 92,500,000

Unrealized gain (loss) on available-for-sale

financial assets 9 (34,095,286) 13,726,964 26,425,499

Retained earnings 31,262,967 35,496,821 49,790,044

Treasury stock 17 (12,899,100) (12,899,100) -

77,518,581 129,574,685 169,465,543

Non-controlling Interests 5 (666,914) - -

Total Equity 76,851,667 129,574,685 169,465,543

P134,827,379 P166,568,079 P195,143,230

*Financial statements of Top Frontier Investment Holdings, Inc. since the subsidiary was consolidated effective August 30, 2013.

See Notes to the Financial Statements.

TOP FRONTIER INVESTMENT HOLDINGS, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

(In Thousands)

For the Eight Months

Ended August 31

For the Years Ended

December 31

Note 2013 2012* 2012* 2011* 2010*

REVENUES

Dividend income 9 P1,101,170 P1,564,091 P2,665,261 P1,568,321 P12,088,639

Gain on sale of available-

for-sale financial assets 9 - - - 1,137,775 -

1,101,170 1,564,091 2,665,261 2,706,096 12,088,639

OPERATING EXPENSES 19 1,526 150,211 157,214 371,996 1,134,695

INCOME FROM

OPERATIONS 1,099,644 1,413,880 2,508,047 2,334,100 10,953,944

FINANCE INCOME (COSTS)

Interest income 3,255 1,200 6,129 11,116 9,985

Foreign exchange gain (loss) 24 (3,232,113) 1,104,762 2,010,420 72,272 146,763

Financing charges 14, 20, 24 (1,838,883) (1,306,391) (2,196,791) (1,849,710) (558,541)

Gain (loss) on derivative

assets 10 - (14,759,285) (14,759,285) (11,703,190) 53,857,312

(5,067,741) (14,959,714) (14,939,527) (13,469,512) 53,455,519

INCOME (LOSS)

BEFORE INCOME TAX (3,968,097) (13,545,834) (12,431,480) (11,135,412) 64,409,463

INCOME TAX EXPENSE 22 74 1,621 1,479 868 -

NET INCOME (LOSS) (3,968,171) (13,547,455) (12,432,959) (11,136,280) 64,409,463

OTHER COMPREHENSIVE

INCOME (LOSS)

Changes in fair value of

available-for-sale financial

assets during the period that

will be reclassified to profit

or loss (47,822,250) (2,316,073) (12,698,535) (76,908,025) 120,837,704

Reclassification adjustment 9 - - - 1,448,454 -

Net change in fair value of

available-for-sale

financial assets during

the period 9 (47,822,250) (2,316,073) (12,698,535) (75,459,571) 120,837,704

TOTAL

COMPREHENSIVE

INCOME (LOSS) (P51,790,421) (P15,863,528) (P25,131,494) (P86,595,851) P185,247,167

Forward

For the Eight Months

Ended August 31

For the Years Ended

December 31

Note 2013 2012* 2012* 2011* 2010*

NET INCOME (LOSS)

ATTRIBUTABLE TO:

Equity holders of the

Parent Company (P3,968,171) (P13,547,455) (P12,432,959) (P11,136,280) P64,409,463

Non-controlling interests 5 - - - - -

(P3,968,171) (P13,547,455) (P12,432,959) (P11,136,280) P64,409,463

TOTAL

COMPREHENSIVE

INCOME (LOSS)

ATTRIBUTABLE TO:

Equity holders of the

Parent Company (P51,790,421) (P15,863,528) (P25,131,494) (P86,595,851) P185,247,167

Non-controlling interests 5 - - - - -

(P51,790,421) (P15,863,528) (P25,131,494) (P86,595,851) P185,247,167

*Financial statements of Top Frontier Investment Holdings, Inc. since the subsidiary was consolidated effective August 30, 2013.

See Notes to the Financial Statements.

TOP FRONTIER INVESTMENT HOLDINGS, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

(In Thousands, Except Per Share Data and Number of Shares)

For the Eight Months

Ended August 31

For the Years Ended

December 31

Note 2013 2012* 2012* 2011* 2010*

CAPITAL STOCK 17

Common - P1 par value in

2013, P100 par value in

2012, 2011 and 2010

Authorized - 740,000,000

shares in 2013,

7,400,000 shares in

2012, 2011 and 2010

Issued and outstanding -

490,196,000 shares in

2013, 4,901,960 in 2012,

2011 and 2010

Balance at beginning of period P490,196 P490,196 P490,196 P490,196 P250,000

Issuance - - - - 240,196

Balance at end of period 490,196 490,196 490,196 490,196 490,196

Preferred - P100 par value

Authorized - 2,600,000 shares

Issued and outstanding -

1,904,540 shares in 2013 and

2012, 2,598,040 shares in

2011 and 2010

Balance at beginning of period 259,804 259,804 259,804 259,804 -

Issuance - - - - 259,804

Balance at end of period 259,804 259,804 259,804 259,804 259,804

750,000 750,000 750,000 750,000 750,000

ADDITIONAL PAID-IN

CAPITAL 17

Balance at beginning of period 92,500,000 92,500,000 92,500,000 92,500,000 -

Issuance of common shares - - - - 44,436,260

Issuance of preferred shares - - - - 48,063,740

Balance at end of period 92,500,000 92,500,000 92,500,000 92,500,000 92,500,000

TREASURY STOCK 17 (12,899,100) (12,899,100) (12,899,100) - -

UNREALIZED GAIN

(LOSS) ON AVAILABLE-

FOR-SALE-FINANCIAL

ASSETS 9

Balance at beginning of period 13,726,964 26,425,499 26,425,499 101,885,070 (18,952,634)

Changes in fair value during

the period (47,822,250) (2,316,073) (12,698,535) (75,459,571) 120,837,704

Balance at end of period (34,095,286) 24,109,426 13,726,964 26,425,499 101,885,070

RETAINED EARNINGS

Balance at beginning of

period 35,496,821 49,790,044 49,790,044 62,013,604 (2,395,859)

Net income (loss) for the period (3,968,171) (13,547,455) (12,432,959) (11,136,280) 64,409,463

Cash dividends 17 (265,683) (1,328,898) (1,860,264) (1,087,280) -

Balance at end of period 31,262,967 34,913,691 35,496,821 49,790,044 62,013,604

EQUITY ATTRIBUTABLE TO

EQUITY HOLDERS OF THE

PARENT COMPANY 77,518,581 139,374,017 129,574,685 169,465,543 257,148,674

NON-CONTROLLING

INTERESTS 5 (666,914) - - - -

P76,851,667 P139,374,017 P129,574,685 P169,465,543 P257,148,674

*Financial statements of Top Frontier Investment Holdings, Inc. since the subsidiary was consolidated effective August 30, 2013.

See Notes to the Financial Statements.

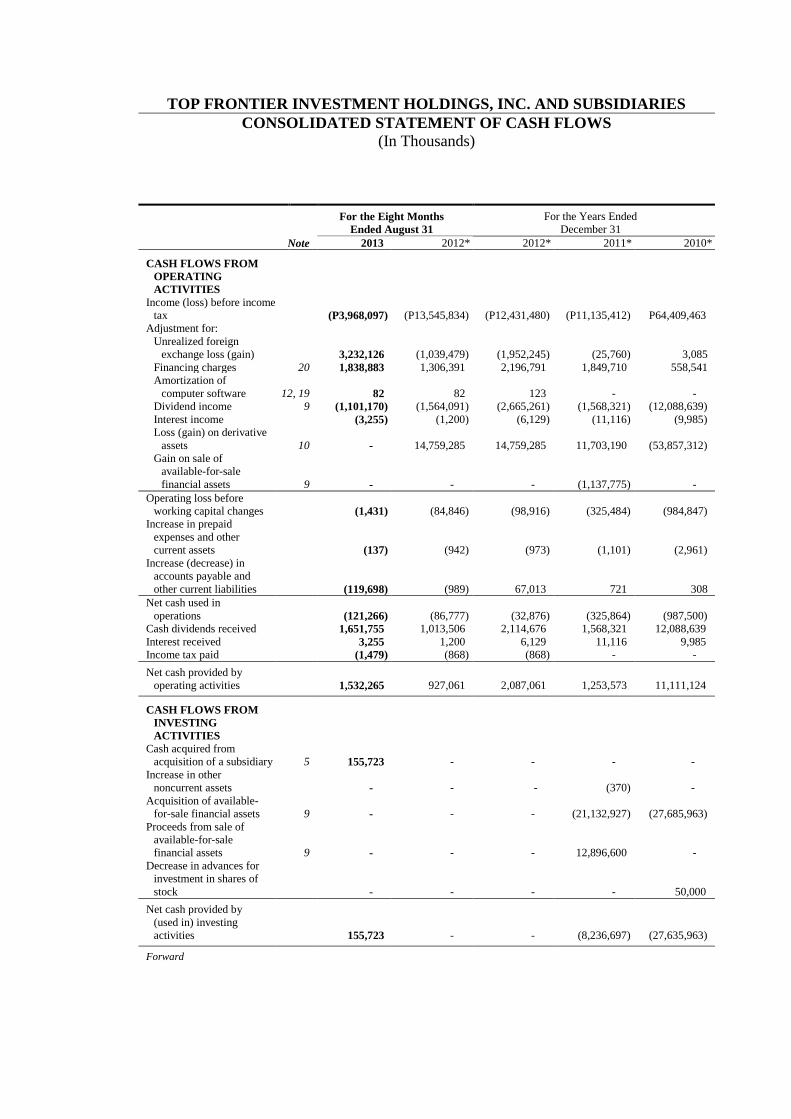

TOP FRONTIER INVESTMENT HOLDINGS, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF CASH FLOWS

(In Thousands)

For the Eight Months

Ended August 31

For the Years Ended

December 31

Note 2013 2012* 2012* 2011* 2010*

CASH FLOWS FROM

OPERATING

ACTIVITIES

Income (loss) before income

tax (P3,968,097) (P13,545,834) (P12,431,480) (P11,135,412) P64,409,463

Adjustment for:

Unrealized foreign

exchange loss (gain) 3,232,126 (1,039,479) (1,952,245) (25,760) 3,085

Financing charges 20 1,838,883 1,306,391 2,196,791 1,849,710 558,541

Amortization of

computer software 12, 19 82 82 123 - -

Dividend income 9 (1,101,170) (1,564,091) (2,665,261) (1,568,321) (12,088,639)

Interest income (3,255) (1,200) (6,129) (11,116) (9,985)

Loss (gain) on derivative

assets 10 - 14,759,285 14,759,285 11,703,190 (53,857,312)

Gain on sale of

available-for-sale

financial assets 9 - - - (1,137,775) -

Operating loss before

working capital changes (1,431) (84,846) (98,916) (325,484) (984,847)

Increase in prepaid

expenses and other

current assets (137) (942) (973) (1,101) (2,961)

Increase (decrease) in

accounts payable and

other current liabilities (119,698) (989) 67,013 721 308

Net cash used in

operations (121,266) (86,777) (32,876) (325,864) (987,500)

Cash dividends received 1,651,755 1,013,506 2,114,676 1,568,321 12,088,639

Interest received 3,255 1,200 6,129 11,116 9,985

Income tax paid (1,479) (868) (868) - -

Net cash provided by

operating activities 1,532,265 927,061 2,087,061 1,253,573 11,111,124

CASH FLOWS FROM

INVESTING

ACTIVITIES

Cash acquired from

acquisition of a subsidiary 5 155,723 - - - -

Increase in other

noncurrent assets - - - (370) -

Acquisition of available-

for-sale financial assets 9 - - - (21,132,927) (27,685,963)

Proceeds from sale of

available-for-sale

financial assets 9 - - - 12,896,600 -

Decrease in advances for

investment in shares of

stock - - - - 50,000

Net cash provided by

(used in) investing

activities 155,723 - - (8,236,697) (27,635,963)

Forward

For the Eight Months

Ended August 31

For the Years Ended

December 31

Note 2013 2012* 2012* 2011* 2010*

CASH FLOWS FROM

FINANCING

ACTIVITIES

Financing charges paid (P866,532) (P1,535,305) (P2,482,170) (P1,849,710) (P558,541)

Cash dividends paid 17 (265,683) (1,328,898) (1,860,264) (1,087,280) -

Availment (payment) of

amounts owed to related

parties 18 (47,150) (12,158,385) (12,158,423) 9,167,182 (75,563,008)

Proceeds from loan 14 - 27,488,500 27,488,500 - -

Partial redemption of

preferred shares 17 - (12,899,100) (12,899,100) - -

Proceeds from issuance of

capital stock 17 - - - - 93,000,000

Net cash provided by

(used in) financing

activities (1,179,365) (433,188) (1,911,457) 6,230,192 16,878,451

EFFECTS OF

EXCHANGE RATE

CHANGES ON CASH

AND CASH

EQUIVALENTS 17 (2,950) (1,643) 128 6,560

NET INCREASE

(DECREASE) IN

CASH AND CASH

EQUIVALENTS 508,640 490,923 173,961 (752,804) 360,172

CASH AND CASH

EQUIVALENTS AT

BEGINNING OF

PERIOD 202,681 28,720 28,720 781,524 421,352

CASH AND CASH

EQUIVALENTS AT

END OF PERIOD 6 P711,321 P519,643 P202,681 P28,720 P781,524

*Financial statements of Top Frontier Investment Holdings, Inc. since the subsidiary was consolidated effective August 30, 2013.

See Notes to the Financial Statements.

TOP FRONTIER INVESTMENT HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

(Amount in Thousands, Except Per Share Data and Number of Shares)

1. Corporate Information

Top Frontier Investment Holdings, Inc. (the “Parent Company”) was incorporated and

registered with the Philippine Securities and Exchange Commission (SEC) on March 11,

2008. The Parent Company is primarily established as a holding company provided that

the Parent Company shall not engage in the business of an investment company as

defined in the Investment Company Act (R.A. 2629), as amended, without first

complying with the applicable provisions of the said statute.

The registered office address of the Parent Company is 5th Floor, ENZO Building, 399

Sen. Gil J. Puyat Avenue, Makati City.

Clariden Holdings, Inc. (Clariden)

Clariden‟s primary purpose is to acquire by purchase, exchange, assignment or otherwise,

and to sell, assign, transfer, exchange, lease, let, develop, mortgage, pledge, deal in and

operate, enjoy and dispose of, all properties of every kind and description and wherever

situated and to the extent permitted by law.

Excelon Asia Holding Corporation (EAHC)

New Manila Properties Inc. (NMPI)

Philnico Holdings, Ltd. (PHL) h

EAHC‟s primary purpose of business is to acquire by purchase, exchange or otherwise,

and to sell, assign, transfer, exchange, lease, develop, mortgage, pledge, deal in and with

otherwise operate, enjoy, and dispose of, all properties of every kind and description and

whenever situated and as to the extent permitted by law. EAHC has 46% equity interest

in PNPI.

NMPI‟s primary purpose is to purchase, hold, administer, acquire, sell, convey,

mortgage, encumber, rent, construct, lease or otherwise dispose of or deal in residential,

commercial, urban or other kinds of real property, without engaging in subdivision

business. NMPI has 46% equity interest in PNPI.

PHL is a holding company and has 8% equity interest in PNPI and 32% equity interest in

PIC.

Pacific Nickel Philippines, Inc. (PNPI)

PNPI is primarily engaged to operate coal mines and explore, mine, refine, manufacture,

buy, sell, exchange, and otherwise produce and deal in all other kinds of ores, metals,

minerals, hydrocarbons, acids and chemicals, and in the product and by-products of every

kind and description.

Philnico Industrial Corporation (PIC)

PIC‟s primary purpose is to lease, manage, construct and generally deal in industrial

estates and in any and all lands, estates, buildings, plants and other business structures.

PIC is 68% owned subsidiary of PNPI.

- 2 -

Philnico Processing Corp. (PPC)

PPC is primarily engaged to obtain, hold, explore, work, develop and lease concessions

of lands containing mines of magnesite, gold and silver and other minerals, and to

conduct and carry on the business of mining, manufacturing, and otherwise producing

and dealing in all kinds of ores, metals, minerals, precious stones and coal. In July 1986,

PPC decided to shut down its nickel refinery operations due to irreversible losses

resulting from high level of debt, soaring interest rates, prolonged low metal prices and

high oil prices. PPC is 90% owned by PIC and is 61% owned subsidiary of PNPI.

EAHC, NMPI and PHL collectively own 100% of the outstanding capital stock of PNPI

and its subsidiaries (PIC and PPC).

V.I.L Mines Incorporated (VMI)

VMI‟s primary purpose is to carry on the commercial and industrial business of

exploring, buying, selling, locating, manufacturing, processing, mining and dealing in

and with metallic and non-metallic minerals, metals, coal, the products of the earth and

soil, timber, and the products and by-products thereof.

Asia-Alliance Mining Resources Corp. (AAMRC)

AAMRC is a company primarily engaged in the business of operating iron mines, and of

prospecting, exploration and mining, milling, concentrating, smelting, treating, refining

and processing of metals for market.

Prima Lumina Gold Mining Corp. (PLGMC)

PLGMC‟s primary purpose of business is to carry on the commercial and industrial

business of prospecting, exploring, buying, selling, manufacturing, fabricating,

processing, mining and dealing in and with metallic and non-metallic minerals, metals

and ores and to purchase, exchange, sell and deal in minerals and mineral lands of all

kinds and operate and construct buildings, refineries and other business structures.

South Western Cement Corp. (SWCC)

SWCC is primarily engaged to operate, conduct and maintain the business of

manufacturing, importing, exporting, buying, selling or otherwise dealing in at wholesale

such goods as cements and other goods of similar nature, and any and all equipment,

materials, supplies, used or employed in or related to the manufacture of such finished

goods.

The accompanying consolidated financial statements as of and for the eight months

period ended August 31, 2013 comprise the financial statements of the Parent Company

and its Subsidiary (collectively referred to as the “Group”; Note 2).

2. Basis of Preparation

Statement of Compliance

The accompanying financial statements have been prepared in compliance with

Philippine Financial Reporting Standards (PFRS). PFRS are based on International

Financial Reporting Standards (IFRS) issued by International Accounting Standards

Board (IASB). PFRS consist of PFRS, Philippine Accounting Standards (PAS) and

Philippine Interpretations issued by the Financial Reporting Standards Council (FRSC).

The financial statements were prepared solely for the information and use by the

management of the Group and is not intended to be, and should not be used by anyone

other than for the specified purpose.

- 3 -

The financial statements were authorized for issue by the Board of Directors (BOD) on

September 25, 2013.

Basis of Measurement

The financial statements of the Group have been prepared on a historical cost basis of

accounting, except for the following:

derivative financial instruments and available-for-sale (AFS) financial assets that are

measured at fair value; and

defined benefit liability which is measured as the present value of the defined benefit

obligation.

Functional and Presentation Currency

The financial statements are presented in Philippine peso, which is the Parent Company‟s

functional currency. All financial information are rounded off to the nearest thousand

(P000), except when otherwise indicated.

Basis of Consolidation

The consolidated financial statements as of and for the eight months period ended

August 31, 2013 include the accounts of the Parent Company and its subsidiary. The

subsidiary includes the following:

Percentage of

Ownership

2013 Country of Incorporation

Clariden and subsidiaries, namely: (a)

100 Philippines

EAHC 100 Philippines

NMPI 100 Philippines

PHL 100 British Virgin Island

PNPI (b)

100 Philippines

PIC (b)

100 Philippines

PPC (b)

90 Philippines

VMI (e)

100 Philippines

AAMRC (e)

60 Philippines

PLGMC (d) (e)

100 Philippines

SWCC (c)

100 Philippines

(a) Consolidated effective August 30, 2013 (Note 5).

(b) Indirect subsidiary through EAHC, NMPI and PHL and has no commercial operations (Note 5).

(c) Has not yet started commercial operations. (d) Incorporated on February 21, 2013.

(e) Has not yet started commercial operations and is in exploratory and development stage of its mining

activities.

A subsidiary is an entity controlled by the Group. The Group controls an entity when it

is exposed to, or has rights to, variable returns from its involvement with the entity and

has the ability to affect those returns through its power over the entity. The financial

statements of the subsidiaries are included in the consolidated financial statements from

the date when the Group obtains control, and continue to be consolidated until the date

when such control ceases.

The consolidated financial statements are prepared for the same reporting period as the

Parent Company, using uniform accounting policies for like transactions and other events

in similar circumstances. Intergroup balances and transactions, including intergroup

unrealized profits and losses, are eliminated in preparing the consolidated financial

statements.

- 4 -

Non-controlling interests represent the portion of profit or loss and net assets not held by

the Group and are presented in the consolidated statement of comprehensive income and

within equity in the consolidated statement of financial position, separately from the

Group‟s equity attributable to equity holders of the Parent Company.

Non-controlling interests include the interests not held by the Group in AAMRC and

PPC in 2013 (Note 5).

3. Significant Accounting Policies

The accounting policies set out below have been applied consistently to all periods

presented in the financial statements, except for the changes in accounting policies as

explained below.

Adoption of New or Revised Standards, Amendments to Standards and Interpretations

The FRSC approved the adoption of a number of new or revised standards, amendments

to standards and interpretations as part of PFRS.

Adopted Effective 2013

The Group has adopted the following PFRS starting January 1, 2013 and accordingly,

changed its accounting policies in the following areas:

Presentation of Items of Other Comprehensive Income (Amendments to PAS 1,

Presentation of Financial Statements). The amendments: (a) require that an entity

presents separately the items of other comprehensive income that would be

reclassified to profit or loss in the future, if certain conditions are met, from those

that would never be reclassified to profit or loss; (b) do not change the existing

option to present profit or loss and other comprehensive income in two statements;

and (c) change the title of the statements of comprehensive income to statements of

profit or loss and other comprehensive income. However, an entity is still allowed to

use other titles. The amendments do not address which items are presented in other

comprehensive income or which items need to be reclassified. The requirements of

other PFRS continue to apply in this regard. The amendments are effective for

annual periods beginning on or after January 1, 2013.

As a result of the adoption of the amendments to PAS 1, the Group has modified the

presentation of items of other comprehensive income in the statements of

comprehensive income, to present separately items that would be reclassified to

profit or loss from those that would never be. Comparative information has been re-

presented accordingly.

Disclosures: Offsetting Financial Assets and Financial Liabilities (Amendments to

PFRS 7, Financial Instruments: Disclosures). These amendments include minimum

disclosure requirements related to financial assets and financial liabilities that are:

(a) offset in the statements of financial position; or (b) subject to enforceable master

netting arrangements or similar agreements. They include a tabular reconciliation of

gross and net amounts of financial assets and financial liabilities, separately showing

amounts offset and not offset in the statements of financial position. The amendments

are applied retrospectively for annual periods beginning on or after January 1, 2013.

The adoption of these amendments did not have significant effect on the financial

statements.

- 5 -

PFRS 10, Consolidated Financial Statements, introduces a new approach to

determining which investees should be consolidated and provides a single model to

be applied in the control analysis for all investees. An investor controls an investee

when: (a) it is exposed or has rights to variable returns from its involvement with that

investee; (b) it has the ability to affect those returns through its power over that

investee; and (c) there is a link between power and returns. Control is reassessed as

facts and circumstances change. PFRS 10 supersedes PAS 27 (2008), Consolidated

and Separate Financial Statements, and Philippine Interpretation Standards

Interpretation Committee (SIC) 12, Consolidation - Special Purpose Entities. The

new standard is effective for annual periods beginning on or after January 1, 2013.

In accordance with the transitional provisions of PFRS 10, the Group reassessed

control over its investees effective January 1, 2013 based on the new control model.

The adoption of the new standard did not result to changes in consolidation

conclusion in respect of the Group‟s investees and in the current accounting for these

investees.

PFRS 12, Disclosure of Interests in Other Entities, contains the disclosure

requirements for entities that have interests in subsidiaries, joint arrangements

(i.e., joint operations or joint ventures), associates and/or unconsolidated structured

entities. The new standard provides information that enables users to evaluate:

(a) the nature of, and risks associated with, an entity‟s interests in other entities; and

(b) the effects of those interests on the entity‟s financial position, financial

performance and cash flows. The new standard is effective for annual periods

beginning on or after January 1, 2013.

As a result of the adoption of PFRS 12, the Group has expanded its disclosures about

its interests in subsidiaries (Note 5).

PFRS 13, Fair Value Measurement, replaces the fair value measurement guidance

contained in individual PFRS with a single source of fair value measurement

guidance. It defines fair value, establishes a framework for measuring fair value and

sets out disclosure requirements for fair value measurements. It explains how to

measure fair value when it is required or permitted by other PFRS. It does not

introduce new requirements to measure assets or liabilities at fair value nor does it

eliminate the practicability exceptions to fair value measurements that currently exist

in certain standards. The new standard is effective for annual periods beginning on

or after January 1, 2013. The adoption of the new standard did not have a significant

effect on the measurement of the Group‟s assets and liabilities.

In accordance with the transitional provisions of PFRS 13, the Group has applied the

new fair value measurement guidance prospectively, and has not provided any

comparative information for new disclosures. The adoption of the new standard did

not have a significant effect on the measurements of the Group‟s assets and

liabilities.

PAS 19, Employee Benefits (Amended 2011), includes the following requirements:

(a) actuarial gains and losses are recognized immediately in other comprehensive

income; this change will remove the corridor method and eliminate the ability of

entities to recognize all changes in the defined benefit obligation and in plan assets in

profit or loss, which is currently allowed under PAS 19; and (b) expected return on

plan assets recognized in profit or loss is calculated based on the rate used to discount

the defined benefit obligation. The amendments are applied restrospectively and are

effective for annual periods beginning on or after January 1, 2013. The adoption of

these amendments did not have a significant effect on the financial statements.

- 6 -

Improvements to PFRS 2009-2011 contain amendments to 5 standards with

consequential amendments to other standards and interpretations, of which, only the

following are applicable to the Group:

o Comparative Information beyond Minimum Requirements (Amendments to

PAS 1). These amendments clarify the requirements for comparative information

that are disclosed voluntarily and those that are mandatory due to retrospective

application of an accounting policy, or retrospective restatement or

reclassification of items in the financial statements. An entity must include

comparative information in the related notes to the financial statements when it

voluntarily provides comparative information beyond the minimum required

comparative period. The additional comparative period does not need to contain

a complete set of financial statements. On the other hand, supporting notes for

the third balance sheet (mandatory when there is a retrospective application of an

accounting policy, or retrospective restatement or reclassification of items in the

financial statements) are not required. The amendments are effective for annual

periods beginning on or after January 1, 2013. The adoption of these

amendments did not have an effect on the financial statements.

o Presentation of the Opening Statement of Financial Position and Related Notes

(Amendments to PAS 1). The amendments clarify that: (a) the opening statement

of financial position is required only if there is: (i) a change in accounting policy;

(ii) a retrospective restatement; or (iii) a reclassification which has a material

effect upon the information in that statement of financial position; (b) except for

the disclosures required under PAS 8, Accounting Policies, Changes in

Accounting Estimates and Errors, notes related to the opening statement of

financial position are no longer required; and (c) the appropriate date for the

opening statement of financial position is the beginning of the preceding period,

rather than the beginning of the earliest comparative period presented. This is

regardless of whether an entity provides additional comparative information

beyond the minimum comparative information requirements. The amendments

explain that the requirements for the presentation of notes related to additional

comparative information and those related to the opening statement of financial

position are different, because the underlying objectives are different. The

amendments are effective for annual periods beginning on or after January 1,

2013. The adoption of these amendments did not have an effect on the financial

statements.

o Income Tax Consequences of Distributions (Amendments to PAS 32, Financial

Instruments Presentation). The amendments clarify that PAS 12, Income Taxes

applies to the accounting for income taxes relating to: (a) distributions to holders

of an equity instrument; and (b) transaction costs of an equity transaction. This

amendment removes a perceived inconsistency between PAS 32 and PAS 12.

Before the amendment, PAS 32 indicated that distributions to holders of an

equity instrument are recognized directly in equity, net of any related income tax.

However, PAS 12 generally requires the tax consequences of dividends to be

recognized in profit or loss. A similar consequential amendment has also been

made to Philippine Interpretation IFRIC 2, Members’ Share in Co-operative

Entities and Similar Instruments. The amendments are effective for annual

periods beginning on or after January 1, 2013. The adoption of these

amendments did not have an effect on the financial statements.

- 7 -

o Classification of Servicing Equipment (Amendments to PAS 16, Property, Plant

and Equipment). The amendments clarify the accounting of spare parts, stand-by

equipment and servicing equipment. The definition of „property, plant and

equipment‟ in PAS 16 is now considered in determining whether these items

should be accounted for under this standard. If these items do not meet the

definition, then they are accounted for using PAS 2, Inventories. The

amendments are required for annual periods beginning on or after January 1,

2013. The adoption of these amendments did not have an effect on the financial

statements.

Additional disclosures required by the revised standards, amendments to standards and

interpretations were included in the financial statements, where applicable.

New or Revised Standards and Amendment to Standards Not Yet Adopted

A number of new or revised standards, amendments to standards and interpretations are

effective for annual periods beginning after January 1, 2013, and have not been applied in

preparing the financial statements. Except as otherwise indicated, none of these is

expected to have a significant effect on the financial statements of the Group.

The Group will adopt the following new or revised standards, and amendments to

standards on the respective effective dates:

Recoverable Amount Disclosures for Non-Financial Assets (Amendments to PAS 36,

Impairment of Assets). The amendments clarify that the recoverable amount

disclosure only applies to impaired assets (or cash-generating unit) and require

additional disclosures to be made on the fair value measurement on impaired assets

when the recoverable amount is based on fair value less cost of disposal. The

amendments harmonize the disclosure requirements for fair value less cost of

disposal and value in use when the present value techniques are used to measure the

recoverable amount of impaired assets. The adoption of the amendments is required

to be retrospectively applied for annual period beginning on or after January 1, 2014.

The Group does not plan to adopt these amendments early.

Offsetting Financial Assets and Financial Liabilities (Amendments to PAS 32). These

amendments clarify that: (a) an entity currently has a legally enforceable right to

set-off if that right is: (i) not contingent on a future event; and (ii) enforceable both in

the normal course of business and in the event of default, insolvency or bankruptcy

of the entity and all counterparties; and (b) gross settlement is equivalent to net

settlement if and only if the gross settlement mechanism has features that:

(i) eliminate or result in insignificant credit and liquidity risk; and (ii) process

receivables and payables in a single settlement process or cycle. The adoption of the

amendments is required to be retrospectively applied for annual periods beginning on

or after January 1, 2014. The Group does not plan to adopt these amendments early.

PFRS 9, Financial Instruments (2010) and (2009). PFRS 9 (2009) introduces new

requirements for the classification and measurement of financial assets. Under

PFRS 9 (2009), financial assets are classified and measured based on the business

model in which they are held and the characteristics of their contractual cash flows.

PFRS 9 (2010) introduces additions relating to financial liabilities. The IASB

currently has an active project to make limited amendments to the classification and

measurement requirements of PFRS 9 and add new requirements to address the

impairment of financial assets and hedge accounting. PFRS 9 (2010 and 2009) is

effective for annual periods beginning on or after January 1, 2015.

- 8 -

The Group conducted an evaluation on the possible financial impact of the adoption

of PFRS 9 and does not plan to adopt this standard early.

Financial Assets and Financial Liabilities

Date of Recognition. The Group recognizes a financial asset or a financial liability in the

statements of financial position when it becomes a party to the contractual provisions of

the instrument. In the case of a regular way purchase or sale of financial assets,

recognition is done using settlement date accounting.

Initial Recognition of Financial Instruments. Financial instruments are recognized

initially at fair value of the consideration given (in case of an asset) or received (in case

of a liability). The initial measurement of financial instruments, except for those

designated as at fair value through profit or loss (FVPL), includes transaction costs.

The Group classifies its financial assets in the following categories: held-to-maturity

(HTM) investments, AFS financial assets, financial assets at FVPL and loans and

receivables. The Group classifies its financial liabilities as either financial liabilities at

FVPL or other financial liabilities. The classification depends on the purpose for which

the investments are acquired and whether they are quoted in an active market.

Management determines the classification of its financial assets and financial liabilities at

initial recognition and, where allowed and appropriate, re-evaluates such designation at

every reporting date.

Determination of Fair Value. The fair value for financial instruments traded in active

markets at the reporting date is based on their quoted market price or dealer price

quotations (bid price for long positions and ask price for short positions), without any

deduction for transaction costs. When current bid and ask prices are not available, the

price of the most recent transaction provides evidence of the current fair value as long as

there is no significant change in economic circumstances since the time of the

transaction.

For all other financial instruments not listed in an active market, the fair value is

determined by using appropriate valuation techniques. Valuation techniques include the

discounted cash flow method, comparison to similar instruments for which market

observable prices exist, options pricing models and other relevant valuation models.

‘Day 1’ Profit. Where the transaction price in a non-active market is different to the fair

value from other observable current market transactions in the same instrument or based

on a valuation technique whose variables include only data from observable market, the

Group recognizes the difference between the transaction price and the fair value

(a „Day 1‟ profit) in profit or loss unless it qualifies for recognition as some other type of

asset. In cases where data used is not observable, the difference between the transaction

price and model value is only recognized in profit or loss when the inputs become

observable or when the instrument is derecognized. For each transaction, the Group

determines the appropriate method of recognizing the „Day 1‟ profit amount.

Financial Assets

Financial Assets at FVPL. A financial asset is classified as at FVPL if it is classified as

held for trading or is designated as such upon initial recognition. Financial assets are

designated as at FVPL if the Group manages such investments and makes purchase and

sale decisions based on their fair value in accordance with the Group‟s documented risk

management or investment strategy. Derivative instruments (including embedded

derivatives), except those covered by hedge accounting relationships, are classified under

this category.

- 9 -

Financial assets are classified as held for trading if they are acquired for the purpose of

selling in the near term.

Financial assets may be designated by management at initial recognition at FVPL, when

any of the following criteria is met:

the designation eliminates or significantly reduces the inconsistent treatment that

would otherwise arise from measuring the assets or recognizing gains or losses on a

different basis;

the assets are part of a group of financial assets which are managed and their

performances are evaluated on a fair value basis, in accordance with a documented

risk management or investment strategy; or

the financial instrument contains an embedded derivative, unless the embedded

derivative does not significantly modify the cash flows or it is clear, with little or no

analysis, that it would not be separately recognized.

The Group carries financial assets at FVPL using their fair values. Attributable

transaction costs are recognized in profit or loss as incurred. Fair value changes and

realized gains or losses are recognized in profit or loss. Fair value changes from

derivatives accounted for as part of an effective accounting hedge are recognized in other

comprehensive income and presented in the statements of changes in equity. Any

interest earned shall be recognized as part of “Interest income” account in the statements

of comprehensive income. Any dividend income from equity securities classified as at

FVPL shall be recognized in profit or loss when the right to receive payment has been

established.

The Group‟s derivative assets are classified under this category (Notes 10 and 24).

Loans and Receivables. Loans and receivables are non-derivative financial assets with

fixed or determinable payments and maturities that are not quoted in an active market.

They are not entered into with the intention of immediate or short-term resale and are not

designated as AFS financial assets or financial assets at FVPL.

Subsequent to initial measurement, loans and receivables are carried at amortized cost

using the effective interest rate method, less any impairment in value. Any interest

earned on loans and receivables shall be recognized as part of “Interest income” account

in the statements of comprehensive income on an accrual basis. Amortized cost is

calculated by taking into account any discount or premium on acquisition and fees that

are an integral part of the effective interest rate. The periodic amortization is also

included as part of “Interest income” account in the statements of comprehensive income.

Gains or losses are recognized in profit or loss when loans and receivables are

derecognized or impaired, as well as through the amortization process.

Cash includes cash on hand and in banks which are stated at face value. Cash

equivalents are short-term, highly liquid investments that are readily convertible to

known amounts of cash and are subject to an insignificant risk of changes in value.

The Group‟s cash and cash equivalents, receivables, advances for investment in shares of

stock and restricted cash (included under “Other noncurrent assets” account) are included

under this category (Notes 6, 7, 9, 12 and 24).

- 10 -

HTM Investments. HTM investments are quoted non-derivative financial assets with

fixed or determinable payments and fixed maturities for which the Group‟s management

has the positive intention and ability to hold to maturity. Where the Group sells other

than an insignificant amount of HTM investments, the entire category would be tainted

and reclassified as AFS financial assets. After initial measurement, these investments are

measured at amortized cost using the effective interest rate method, less impairment in

value. Any interest earned on the HTM investments shall be recognized as part of

“Interest income” account in the statements of comprehensive income on an accrual

basis. Amortized cost is calculated by taking into account any discount or premium on

acquisition and fees that are an integral part of the effective interest rate. The periodic

amortization is also included as part of “Interest income” account in the statements of

comprehensive income. Gains or losses are recognized in profit or loss when the HTM

investments are derecognized or impaired, as well as through the amortization process.

The Group has no investments accounted for under this category as of August 31, 2013

and December 31, 2012 and 2011.

AFS Financial Assets. AFS financial assets are non-derivative financial assets that are

either designated in this category or not classified in any of the other financial asset

categories. Subsequent to initial recognition, AFS financial assets are measured at fair

value and changes therein, other than impairment losses and foreign currency differences

on AFS debt instruments, are recognized in other comprehensive income and presented

in equity. The effective yield component of AFS debt securities is reported as part of

“Interest income” account in the statements of comprehensive income. Dividends earned

on holding AFS equity securities are recognized as dividend income when the right to

receive payment has been established. When individual AFS financial assets are either

derecognized or impaired, the related accumulated unrealized gains or losses previously

reported in equity are transferred to and recognized in profit or loss.

AFS financial assets also include unquoted equity instruments with fair values which

cannot be reliably determined. These instruments are carried at cost less impairment in

value, if any.

Financial Liabilities

Financial Liabilities at FVPL. Financial liabilities are classified under this category

through the fair value option. Derivative instruments (including embedded derivatives)

with negative fair values, except those covered by hedge accounting relationships, are

also classified under this category.

The Group carries financial liabilities at FVPL using their fair values and reports fair

value changes in profit or loss. Fair value changes from derivatives accounted for as part

of an effective accounting hedge are recognized in other comprehensive income and

presented in the statements of changes in equity. Any interest expense incurred is

recognized as part of “Financing charges” account in the statements of comprehensive

income.

The Group has no liabilities accounted for under this category as of August 31, 2013 and

December 31, 2012 and 2011.

Other Financial Liabilities. This category pertains to financial liabilities that are not

designated or classified as at FVPL. After initial measurement, other financial liabilities

are carried at amortized cost using the effective interest rate method. Amortized cost is

calculated by taking into account any premium or discount and any directly attributable

transaction costs that are considered an integral part of the effective interest rate of the

liability.

- 11 -

The Group‟s liabilities arising from its trade or borrowings such as accounts payable and

other current liabilities, loans payable and other noncurrent liabilities are included under

this category (Notes 13, 14, 15, 18 and 24).

Derivative Financial Instruments and Hedging

Freestanding Derivatives

For the purpose of hedge accounting, hedges are classified as either: a) fair value hedges

when hedging the exposure to changes in the fair value of a recognized asset or liability

or an unrecognized firm commitment (except for foreign currency risk); b) cash flow

hedges when hedging exposure to variability in cash flows that is either attributable to a

particular risk associated with a recognized asset or liability or a highly probable forecast

transaction or the foreign currency risk in an unrecognized firm commitment; or

c) hedges of a net investment in foreign operations.

At the inception of a hedge relationship, the Group formally designates and documents

the hedge relationship to which the Group wishes to apply hedge accounting and the risk

management objective and strategy for undertaking the hedge. The documentation

includes identification of the hedging instrument, the hedged item or transaction, the

nature of the risk being hedged and how the entity will assess the hedging instrument‟s

effectiveness in offsetting the exposure to changes in the hedged item‟s fair value or cash

flows attributable to the hedged risk. Such hedges are expected to be highly effective in

achieving offsetting changes in fair value or cash flows and are assessed on an ongoing

basis to determine that they actually have been highly effective throughout the financial

reporting periods for which they were designated.

Fair Value Hedge. Derivatives classified as fair value hedges are carried at fair value

with corresponding change in fair value recognized in profit or loss. The carrying

amount of the hedged asset or liability is also adjusted for changes in fair value

attributable to the hedged item and the gain or loss associated with that remeasurement is

also recognized in profit or loss.

When the hedge ceases to be highly effective, hedge accounting is discontinued and the

adjustment to the carrying amount of a hedged financial instrument is amortized

immediately.

The Group discontinues fair value hedge accounting if the hedging instrument expired,

sold, terminated or exercised, the hedge no longer meets the criteria for hedge accounting

or the Group revokes the designation.

The Group has no outstanding derivatives accounted for as fair value hedges as of

August 31, 2013 and December 31, 2012 and 2011.

Cash Flow Hedge. Changes in the fair value of a hedging instrument that qualifies as a

highly effective cash flow hedge are recognized in other comprehensive income and

presented in the statements of changes in equity. The ineffective portion is immediately

recognized in profit or loss.

If the hedged cash flow results in the recognition of an asset or a liability, all gains or

losses previously recognized directly in equity are transferred from equity and included

in the initial measurement of the cost or carrying amount of the asset or liability.

Otherwise, for all other cash flow hedges, gains or losses initially recognized in equity

are transferred from equity to profit or loss in the same period or periods during which

the hedged forecasted transaction or recognized asset or liability affects profit or loss.

- 12 -

When the hedge ceases to be highly effective, hedge accounting is discontinued

prospectively. The cumulative gain or loss on the hedging instrument that has been

reported directly in equity is retained in equity until the forecasted transaction occurs.

When the forecasted transaction is no longer expected to occur, any net cumulative gain

or loss previously reported in equity is recognized in profit or loss.

The Group has no outstanding derivatives accounted for as a cash flow hedge as of

August 31, 2013 and December 31, 2012 and 2011.

Net Investment Hedge. The Group has no hedge of a net investment in a foreign

operation as of August 31, 2013 and December 31, 2012 and 2011.

For derivatives that do not qualify for hedge accounting, any gains or losses arising from

changes in fair value of derivatives are taken directly to profit or loss during the year

incurred.

Embedded Derivatives

The Group assesses whether embedded derivatives are required to be separated from host

contracts when the Group becomes a party to the contract.

An embedded derivative is separated from the host contract and accounted for as a

derivative if all of the following conditions are met: a) the economic characteristics and

risks of the embedded derivative are not closely related to the economic characteristics

and risks of the host contract; b) a separate instrument with the same terms as the

embedded derivative would meet the definition of a derivative; and c) the hybrid or

combined instrument is not recognized as at FVPL. Reassessment only occurs if there is

a change in the terms of the contract that significantly modifies the cash flows that would

otherwise be required.

Derecognition of Financial Assets and Financial Liabilities

Financial Assets. A financial asset (or, where applicable, a part of a financial asset or

part of a group of similar financial assets) is derecognized when:

the rights to receive cash flows from the asset have expired;

the Group retains the right to receive cash flows from the asset, but has assumed an

obligation to pay them in full without material delay to a third party under a

“pass-through” arrangement; or

the Group has transferred its rights to receive cash flows from the asset and either:

(a) has transferred substantially all the risks and rewards of the asset; or (b) has

neither transferred nor retained substantially all the risks and rewards of the asset, but

has transferred control of the asset.

When the Group has transferred its rights to receive cash flows from an asset and has

neither transferred nor retained substantially all the risks and rewards of the asset nor

transferred control of the asset, the asset is recognized to the extent of the Group‟s

continuing involvement in the asset. Continuing involvement that takes the form of a

guarantee over the transferred asset is measured at the lower of the original carrying

amount of the asset and the maximum amount of consideration that the Group could be

required to repay.

- 13 -

Financial Liabilities. A financial liability is derecognized when the obligation under the

liability is discharged, cancelled or expired. When an existing financial liability is

replaced by another from the same lender on substantially different terms, or the terms of

an existing liability are substantially modified, such an exchange or modification is

treated as a derecognition of the original liability and the recognition of a new liability.

The difference in the respective carrying amounts is recognized in profit or loss.

Impairment of Financial Assets

The Group assesses at the reporting date whether a financial asset or group of financial

assets is impaired.

A financial asset or a group of financial assets is deemed to be impaired if, and only if,

there is objective evidence of impairment as a result of one or more events that have

occurred after the initial recognition of the asset (an incurred loss event) and that loss

event has an impact on the estimated future cash flows of the financial asset or the group

of financial assets that can be reliably estimated.

Assets Carried at Amortized Cost. For assets carried at amortized cost such as loans and

receivables, the Group first assesses whether objective evidence of impairment exists

individually for financial assets that are individually significant, or collectively for

financial assets that are not individually significant. If no objective evidence of

impairment has been identified for a particular financial asset that was individually

assessed, the Group includes the asset as part of a group of financial assets pooled

according to their credit risk characteristics and collectively assesses the group for

impairment. Assets that are individually assessed for impairment and for which an

impairment loss is, or continues to be, recognized are not included in the collective

impairment assessment.

Evidence of impairment for specific impairment purposes may include indications that

the borrower or a group of borrowers is experiencing financial difficulty, default or

delinquency in principal or interest payments, or may enter into bankruptcy or other form

of financial reorganization intended to alleviate the financial condition of the borrower.

For collective impairment purposes, evidence of impairment may include observable data

on existing economic conditions or industry-wide developments indicating that there is a

measurable decrease in the estimated future cash flows of the related assets.

If there is objective evidence of impairment, the amount of loss is measured as the

difference between the asset‟s carrying amount and the present value of estimated future

cash flows (excluding future credit losses) discounted at the financial asset‟s original

effective interest rate (i.e., the effective interest rate computed at initial recognition).

Time value is generally not considered when the effect of discounting the cash flows is

not material. If a loan or receivable has a variable rate, the discount rate for measuring

any impairment loss is the current effective interest rate, adjusted for the original credit

risk premium. For collective impairment purposes, impairment loss is computed based

on their respective default and historical loss experience.

The carrying amount of the asset shall be reduced either directly or through the use of an

allowance account. The impairment loss for the period shall be recognized in profit or

loss. If, in a subsequent period, the amount of the impairment loss decreases and the

decrease can be related objectively to an event occurring after the impairment was

recognized, the previously recognized impairment loss is reversed. Any subsequent

reversal of an impairment loss is recognized in profit or loss, to the extent that the

carrying amount of the asset does not exceed its amortized cost at the reversal date.

- 14 -

AFS Financial Assets. For equity instruments carried at fair value, the Group assesses

whether objective evidence of impairment exists. Objective evidence of impairment

includes a significant or prolonged decline in the fair value of an equity instrument below

its cost. In evaluating whether the period of a decline in the fair value of equity

instruments is prolonged, the period of the decline is the entire period for which fair

value has been below cost. The Group generally regards fair value decline as being

significant' when decline exceeds 25%. A decline in a quoted market price that persists

for 12 months is generally considered to be prolonged.

If an AFS financial asset is impaired, an amount comprising the difference between the

cost (net of any principal payment and amortization) and its current fair value, less any

impairment loss on that financial asset previously recognized in profit or loss, is

transferred from equity to profit or loss. Reversals in respect of equity instruments

classified as AFS financial assets are not recognized in profit or loss. Reversals of

impairment losses on debt instruments are recognized in profit or loss, if the increase in

fair value of the instrument can be objectively related to an event occurring after the

impairment loss was recognized in profit or loss.

In the case of an unquoted equity instrument or of a derivative asset linked to and must

be settled by delivery of an unquoted equity instrument, for which its fair value cannot be

reliably measured, the amount of impairment loss is measured as the difference between

the asset‟s carrying amount and the present value of estimated future cash flows from the

asset discounted using the historical effective rate of return on the asset.

Classification of Financial Instruments between Debt and Equity

From the perspective of the issuer, a financial instrument is classified as debt instrument

if it provides for a contractual obligation to:

deliver cash or another financial asset to another entity;

exchange financial assets or financial liabilities with another entity under conditions

that are potentially unfavorable to the Group; or

satisfy the obligation other than by the exchange of a fixed amount of cash or another

financial asset for a fixed number of own equity shares.

If the Group does not have an unconditional right to avoid delivering cash or another

financial asset to settle its contractual obligation, the obligation meets the definition of a

financial liability.

Debt Issue Costs

Debt issue costs are considered as an adjustment to the effective yield of the related debt

and are deferred and amortized using the effective interest rate method. When a loan is

paid, the related unamortized debt issue costs at the date of repayment are recognized in

profit or loss.

Offsetting Financial Instruments

Financial assets and financial liabilities are offset and the net amount is reported in the

statements of financial position if, and only if, there is a currently enforceable legal right

to offset the recognized amounts and there is an intention to settle on a net basis, or to

realize the asset and settle the liability simultaneously. This is not generally the case with

master netting agreements, and the related assets and liabilities are presented gross in the

statements of financial position.

- 15 -

Business Combination

Business combinations are accounted for using the acquisition method as at the

acquisition date, which is the date on which control is transferred to the Group. The

Group controls an entity when it is exposed to, or has rights to, variable returns from its

involvement with the entity and has the ability to affect those returns through its power

over the entity.

If the business combination is achieved in stages, the acquisition date fair value of the

acquirer‟s previously held equity interest in the acquiree is remeasured to fair value at the

acquisition date through profit or loss.

The Group measures goodwill at the acquisition date as: a) the fair value of the

consideration transferred; plus b) the recognized amount of any non-controlling interests

in the acquiree; plus c) if the business combination is achieved in stages, the fair value of

the existing equity interest in the acquiree; less d) the net recognized amount (generally

fair value) of the identifiable assets acquired and liabilities assumed. When the excess is

negative, a bargain purchase gain is recognized immediately in profit or loss.

Subsequently, goodwill is measured at cost less any accumulated impairment in value.

Goodwill is reviewed for impairment, annually or more frequently, if events or changes

in circumstances indicate that the carrying amount may be impaired.

The consideration transferred does not include amounts related to the settlement of pre-

existing relationships. Such amounts are generally recognized in profit or loss. Costs

related to the acquisition, other than those associated with the issue of debt or equity

securities that the Group incurs in connection with a business combination, are expensed

as incurred. Any contingent consideration payable is measured at fair value at the

acquisition date. If the contingent consideration is classified as equity, then it is not

remeasured and settlement is accounted for within equity. Otherwise, subsequent

changes to the fair value of the contingent consideration are recognized in profit or loss.

Goodwill in a Business Combination

Goodwill acquired in a business combination is, from the acquisition date, allocated

to each of the cash-generating units, or groups of cash-generating units that are

expected to benefit from the synergies of the combination, irrespective of whether

other assets or liabilities are assigned to those units or groups of units. Each unit or

group of units to which the goodwill is so allocated:

o represents the lowest level within the Group at which the goodwill is monitored

for internal management purposes; and

o is not larger than an operating segment determined in accordance with PFRS 8,

Operating Segments.

Impairment is determined by assessing the recoverable amount of the cash-

generating unit or group of cash-generating units, to which the goodwill relates.

Where the recoverable amount of the cash-generating unit or group of cash-

generating units is less than the carrying amount, an impairment loss is recognized.

Where goodwill forms part of a cash-generating unit or group of cash-generating

units and part of the operation within that unit is disposed of, the goodwill associated

with the operation disposed of is included in the carrying amount of the operation

when determining the gain or loss on disposal of the operation. Goodwill disposed

of in this circumstance is measured based on the relative values of the operation

disposed of and the portion of the cash-generating unit retained. An impairment loss

with respect to goodwill is not reversed.

- 16 -

Intangible Assets Acquired in a Business Combination

The cost of an intangible asset acquired in a business combination is the fair value as

at the date of acquisition, determined using discounted cash flows as a result of the

asset being owned.

Following initial recognition, intangible assets are carried at cost less any

accumulated amortization and impairment losses, if any. The useful life of an

intangible asset is assessed to be either finite or indefinite.

An intangible asset with finite life is amortized over the useful economic life and

assessed for impairment whenever there is an indication that the intangible asset may

be impaired. The amortization period and the amortization method for an intangible

asset with a finite useful life are reviewed at least at each reporting date. A change in

the expected useful life or the expected pattern of consumption of future economic

benefits embodied in the asset is accounted for as a change in accounting estimates.

The amortization expense on intangible asset with finite life is recognized in profit or

loss.

Loss of Control

Upon the loss of control, the Group derecognizes the assets and liabilities of the

subsidiary, any non-controlling interests and the other components of equity related

to the subsidiary. Any surplus or deficit arising on the loss of control is recognized

in profit or loss. If the Group retains any interest in the previous subsidiary, then

such interest is measured at fair value at the date that control is lost. Subsequently, it

is accounted for as an equity-accounted investee or as an AFS financial asset

depending on the level of influence retained.

Transactions Under Common Control

Transactions under common control entered into in contemplation of each other and

business combination under common control designed to achieve an overall commercial

effect are treated as a single transaction.

Transfers of assets between commonly controlled entities are accounted for using book

value accounting.

Non-controlling Interests

The acquisitions of non-controlling interests are accounted for as transactions with

owners in their capacity as owners and therefore no goodwill is recognized as a result of

such transactions. Any difference between the purchase price and the net assets of the

acquired entity is recognized in equity. The adjustments to non-controlling interests are

based on a proportionate amount of the net assets of the subsidiary.

Property, Plant and Equipment

Property, plant and equipment, except land, are stated at cost, less accumulated

depreciation and amortization and any accumulated impairment in value. Such cost

includes the cost of replacing part of the property, plant and equipment at the time that

cost is incurred, if the recognition criteria are met, and excludes the costs of day-to-day

servicing. Land is stated at cost less any impairment in value.

- 17 -

The initial cost of property, plant and equipment comprises of its construction cost or

purchase price, including import duties, taxes and any directly attributable costs in

bringing the asset to its working condition and location for its intended use. Cost also

includes any interest incurred during the construction period on funds borrowed to

finance the construction of the projects. Expenditures incurred after the asset has been

put into operation, such as repairs, maintenance and overhaul costs, are normally

recognized as expense in the period the costs are incurred. Major repairs are capitalized

as property, plant and equipment only when it is probable that future economic benefits

associated with the items will flow to the Group and the cost of the items can be

measured reliably.

Construction in progress (CIP) represents assets under construction and is stated at cost.

This includes the cost of construction and other direct costs. Borrowing costs that are

directly attributable to the construction of property and equipment are capitalized during

the construction period. CIP is not depreciated until such time that the relevant assets are

ready for use.

Depreciation and amortization, which commences when the assets are available for their

intended use, are computed using the straight-line method over the following estimated

useful lives of the assets:

Number of Years

Mill, refinery, buildings and mining equipment 5 - 30

Furniture fixtures and other office equipment 2 - 5

Leasehold improvements 10

The remaining useful lives, residual values, and depreciation and amortization methods

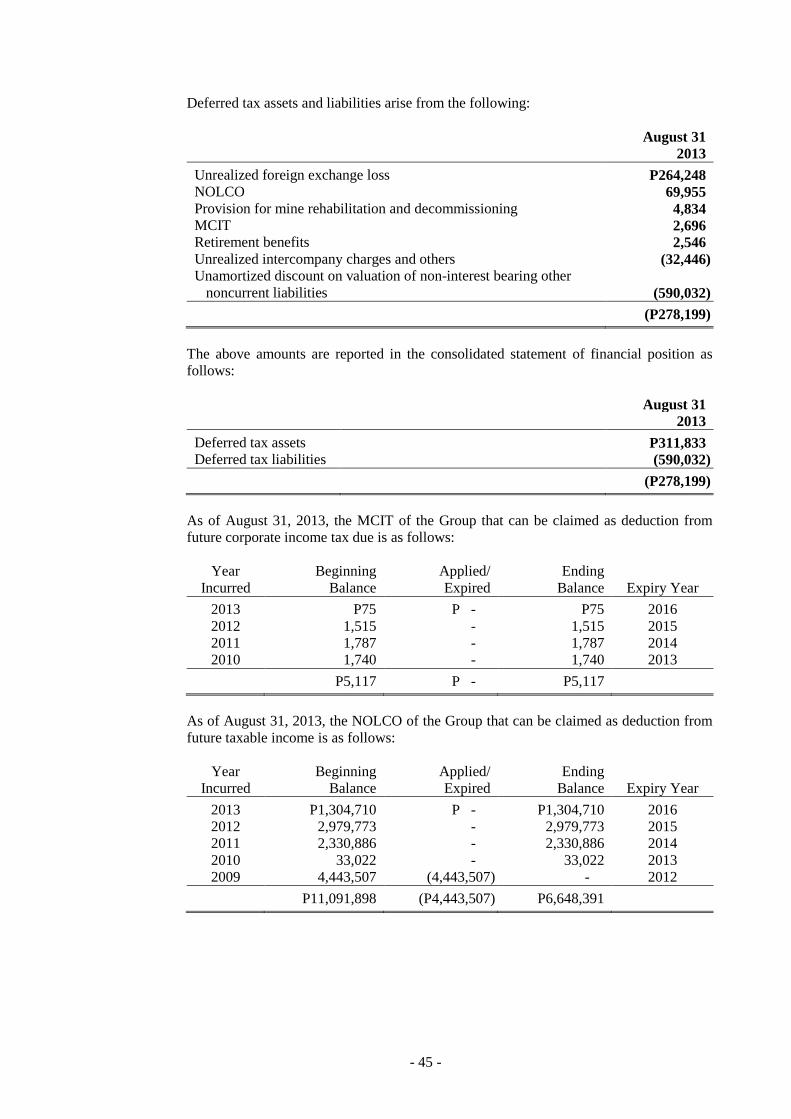

are reviewed and adjusted periodically, if appropriate, to ensure that such periods and