topic 9 company_reconstruction_a141

TRANSCRIPT

COMPANY RECONSTRUCTION

TOPIC 9

BKAF3063 FAR III A141 1

2

Chapter Outline

Compromises and arrangement, S176 Company Act 1965. Debt restructuring Internal reorganization (S61,62,64 CA)

1. alteration of authorized capital.2. reduction of paid up capital.3. issue of bonus shares.4. redemption of preference shares.

External reorganization (S176 – 178 CA) 1. sales of assets & liabilities to another company.2. a scheme of arrangement with creditors.3. business combination.4. The devising of a scheme to avoid liquidation

BKAF3063 FAR III A141

3

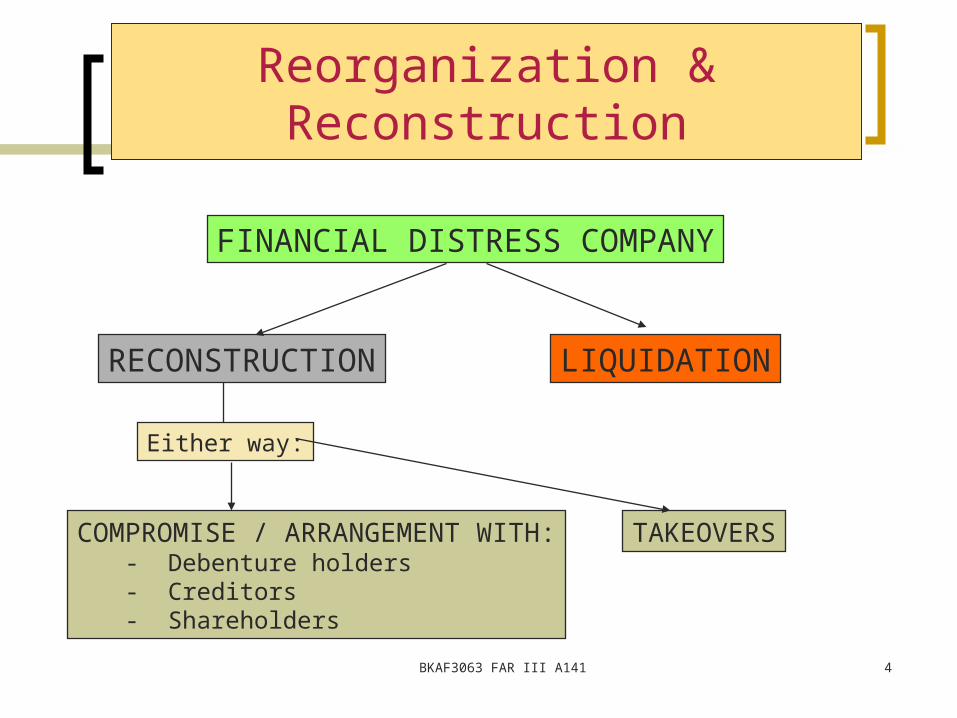

Reorganization & Reconstruction

When company incurring heavy losses and has been unable to pay dividends for few consecutive years. The company has two options:

- Winding up (liquidate)- Reorganization (turn around)

Reorganization - any alteration in the structure of the firm which enables to adapt to changes in its environment.

Reconstruction – reorganizing various aspects, from management, finance, productions etc.

Reorganization can only be undertaken if the company has evidence of making profits in the near future and able to pay dividends to its shareholders.

BKAF3063 FAR III A141

4

Reorganization & Reconstruction

FINANCIAL DISTRESS COMPANY

RECONSTRUCTION LIQUIDATION

Either way:

COMPROMISE / ARRANGEMENT WITH:- Debenture holders- Creditors- Shareholders

TAKEOVERS

BKAF3063 FAR III A141

5

Compromises and Arrangements

S. 176 of CA – power to compromise with creditors and members.

“Arrangement” been defined in S. 176(11) to include a reorganisation of the share capital of a company by the consolidation of shares of different classes or by the division of shares into shares of different classes or by both these methods.

A company can enter into a compromise or arrangement with its creditors or any class of them, or with its members or any class of them without going into liquidation.

BKAF3063 FAR III A141

6

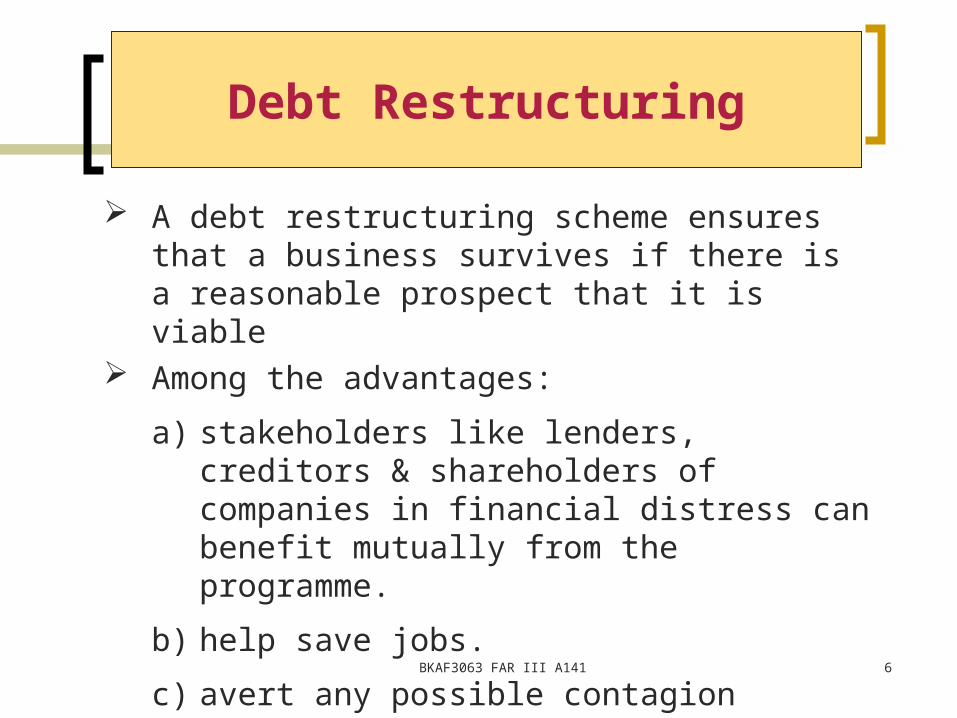

Debt Restructuring

A debt restructuring scheme ensures that a business survives if there is a reasonable prospect that it is viable

Among the advantages:

a) stakeholders like lenders, creditors & shareholders of companies in financial distress can benefit mutually from the programme.

b) help save jobs.

c) avert any possible contagion effects in the corporate sector (i.e. co. A fails & can’t pay co. B, B then can’t pay C & so on).

BKAF3063 FAR III A141

7

Debt Restructuring…

Basic steps in debt restructuring : a) assess process management.b) financial stock take.c) assess future cash flows.d) identify various alternatives available to increase its

financial situation.e) negotiate with shareholders, creditors, employees,

customers & suppliers.f) implement the plan which should lead to a win-win

outcome for both creditors & debtors. BKAF3063 FAR III A141

8

Debt Restructuring…

Most common form of debt restructuring:1. Modification of the debt term to alleviate the short-term

cash needs of the debtor. Example, creditors may:a) reduce the current interest rate .b) forgive some of the accrued interest or principal.c) modify some other term of the debt agreement .d) extend the maturity date of the original debt at a

lower rate of interest.2. Creditor’s acceptance of assets or equity with a FV less

than the amount of the debt.

BKAF3063 FAR III A141

9

Reorganization & Reconstruction

Two types of reorganization: Internal reorganization (S61,62,64 CA)

- redefinition of rights of shareholders:1. alteration of authorized capital.2. reduction of paid up capital.3. issue of bonus shares.4. redemption of preference shares.

External reorganization (S176 – 178 CA) – changes in legal relationships with outsiders and accounting activity

beyond the company itself:1. sales of assets & liabilities to another company.2. a scheme of arrangement with creditors.3. business combination.

4. The devising of a scheme to avoid liquidationBKAF3063 FAR III A141

10

External Reorganization

Involves with outsiders in few ways:

1. Disposal of all part of undertakings.

2. The rearrangement of the capital structure.

3. Expansion through business combination.

4. The devising of a scheme to avoid liquidation

BKAF3063 FAR III A141

11

1. Disposal of all part of undertakings

The sales of non current assets Need approval from the shareholders in the

general meeting Includes the discontinuing operations (MFRS 5) After the disposal, the remaining balance of

the sales proceeds might be distributed to shareholders.

BKAF3063 FAR III A141

12

2. The rearrangement of the capital structure

May involve changes in debt capital Power to rearrange company’s debt capital by

redeeming debentures & unsecured notes will depend on its articles & on the terms of the contracts.

BKAF3063 FAR III A141

BKAF3063 FAR III A141 13

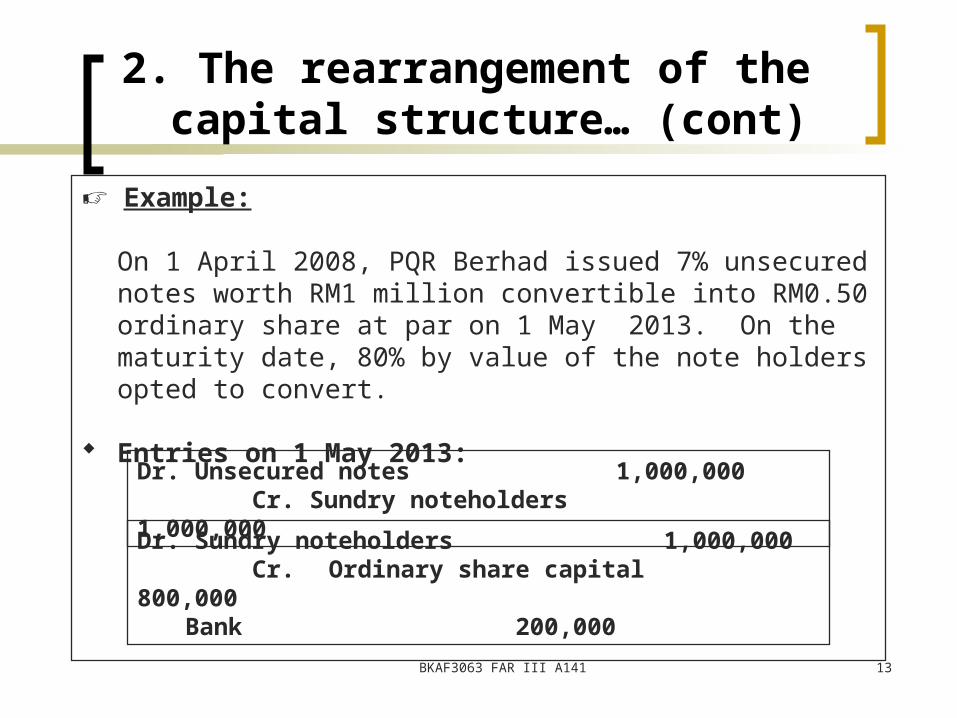

2. The rearrangement of the capital structure… (cont)

☞ Example:

On 1 April 2008, PQR Berhad issued 7% unsecured notes worth RM1 million convertible into RM0.50 ordinary share at par on 1 May 2013. On the maturity date, 80% by value of the note holders opted to convert.

Entries on 1 May 2013:

Dr. Unsecured notes 1,000,000 Cr. Sundry noteholders 1,000,000

Dr. Sundry noteholders 1,000,000 Cr. Ordinary share capital 800,000

Bank 200,000

14

3. Expansion through business combination

This type of reorganisation is motivated by a desire to expand within the industry or to diversify by acquiring businesses in other industries.

The possibilities of the combination are limitless (the terms reorganisation, absorption,amalgamation, consolidation, acquisition, merger & takeover are used interchangeably or sometimes used in a very specific situation in the business world).

MFRS 3 Business Combinations.

BKAF3063 FAR III A141

15

4. The devising of a scheme to avoid liquidation

The scheme is devised in conjunction with creditors & shareholders to avoid the last resort in financial difficulties i.e. liquidation.

BKAF3063 FAR III A141

16

Internal Reorganization

1. Alteration of authorized capital1. increase or reduce authorized capital.2. change in the par value of shares.3. conversion of shares into unit of stock or vice versa.

2. Reduction of paid up capital1. Extinguish or reduce share capital not paid up2. Cancellation of capital loss3. Return of excess capital to shareholders

3. Issue of bonus shares1. Recognition of the amount of capital required for operations.2. Relieving shareholders’ of liability.3. ‘tidying up’ the balance sheet.4. Recognition of increases in the value of assets

4. Redemption of preference shares.BKAF3063 FAR III A141

BKAF3063 FAR III A14117

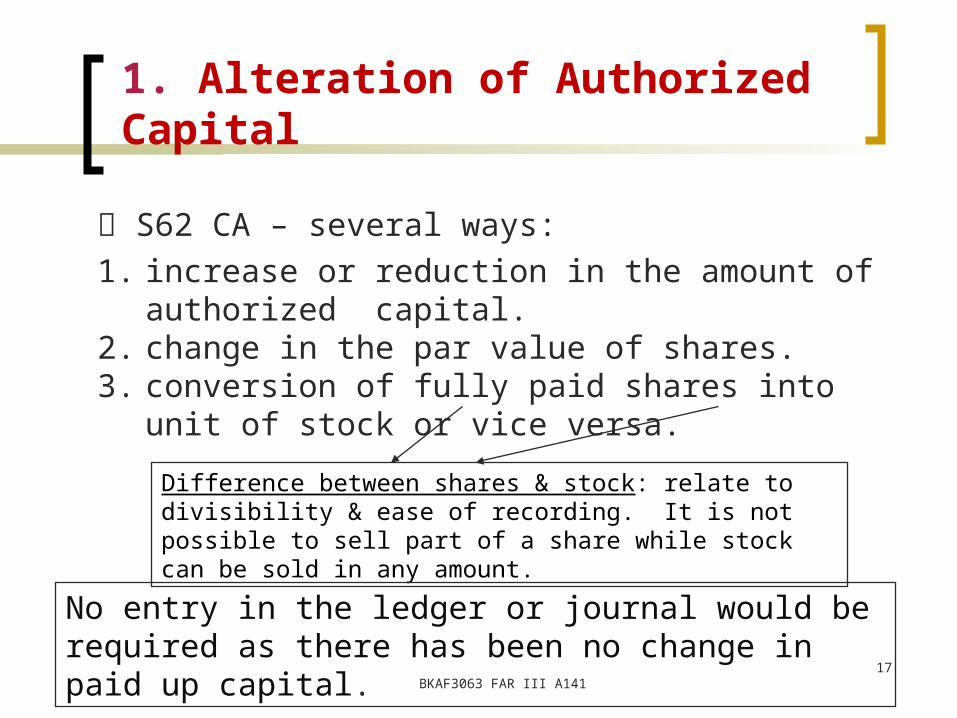

1. Alteration of Authorized Capital

S62 CA – several ways:1. increase or reduction in the amount of authorized

capital.2. change in the par value of shares.3. conversion of fully paid shares into unit of stock or vice

versa.

Difference between shares & stock: relate to divisibility & ease of recording. It is not possible to sell part of a share while stock can be sold in any amount.

No entry in the ledger or journal would be required as there has been no change in paid up capital.

18

☞ Illustration 1:Selamat Berhad had been incorporated on 1 January 1993 with authorized capital of 10,000,000 ordinary shares of RM1.00 par, had an issued and paid up capital of 1,000,000 ordinary shares of RM1.00 each fully paid.

At the AGM held on 7 May 2013, the shareholders resolved:1. To decrease authorized capital to RM7,000,000 by cancelling

3,000,000 unissued shares;2. To alter the par value of the remaining unissued shares from RM1.00

to RM0.50; and3. To convert the fully paid ordinary shares into stock units of RM20.00

each.

BKAF3063 FAR III A141

1. Alteration of Authorized Capital…

BKAF3063 FAR III A141

19

☞ Solution to Illustration 1Stmt of capital presented at the meeting:

Authorized capital:10,000,000 shares of RM1.00 each 10,000,000

Issued & paid up capital:1,000,000 ordinary shares of RM1.00 each 1,000,000

Stmt of capital presented immediately after the meeting:

Authorized capital:50,000 ordinary stock units of RM20.00 each 1,000,00012,000,000 shares of RM0.50 each 6,000,000

Issued & paid up capital:50,000 ordinary stock units at RM20.00 each 1,000,000

RMAuthorized 10mIssued 1mUnissued 9mLess 3mBal unissued 6m

RM6,000,000/0.50

1. Alteration of Authorized Capital…

20

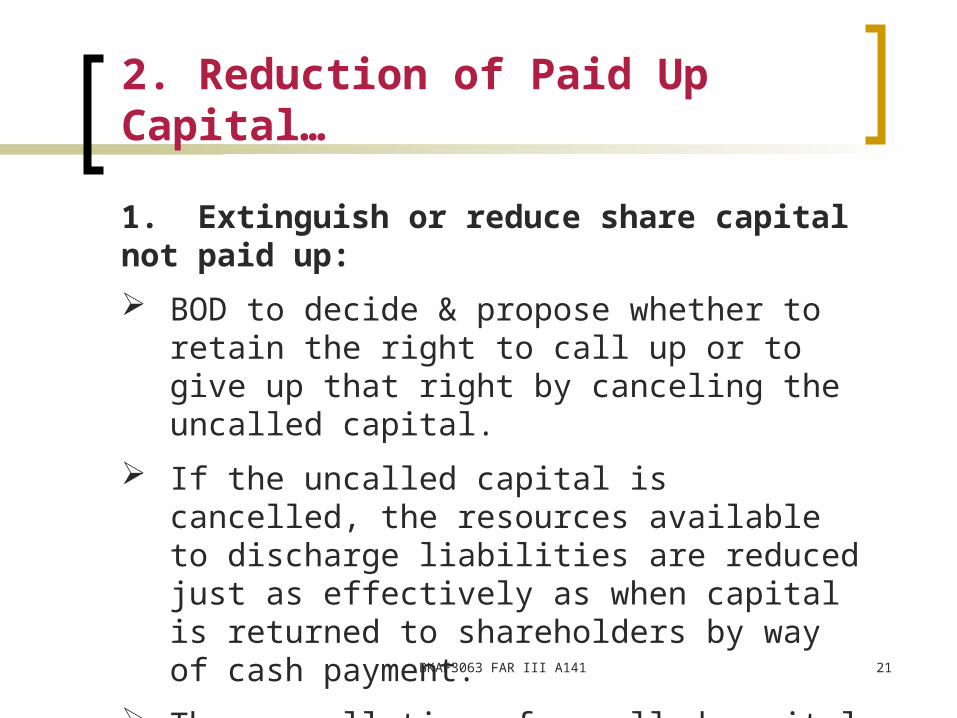

2. Reduction of Paid Up Capital

S64 CA - subject to confirmation by the Court & must be authorised by its articles by special resolution to reduce its share cap. 3 conditions: 1. Extinguish or reduce share capital not paid up2. Cancel any paid up capital which is loss or is

unrepresented by available assets.3. Return of excess capital to shareholders

• Pay off any paid up share capital which is an excess of the needs of the company, and may, so far as is necessary, alter its memorandum by reducing the amount of its share capital and of its shares accordingly.

BKAF3063 FAR III A141

21

2. Reduction of Paid Up Capital…

1. Extinguish or reduce share capital not paid up:

BOD to decide & propose whether to retain the right to call up or to give up that right by canceling the uncalled capital.

If the uncalled capital is cancelled, the resources available to discharge liabilities are reduced just as effectively as when capital is returned to shareholders by way of cash payment.

The cancellation of uncalled capital reduces the par value of the shares involved.

BKAF3063 FAR III A141

BKAF3063 FAR III A141

22

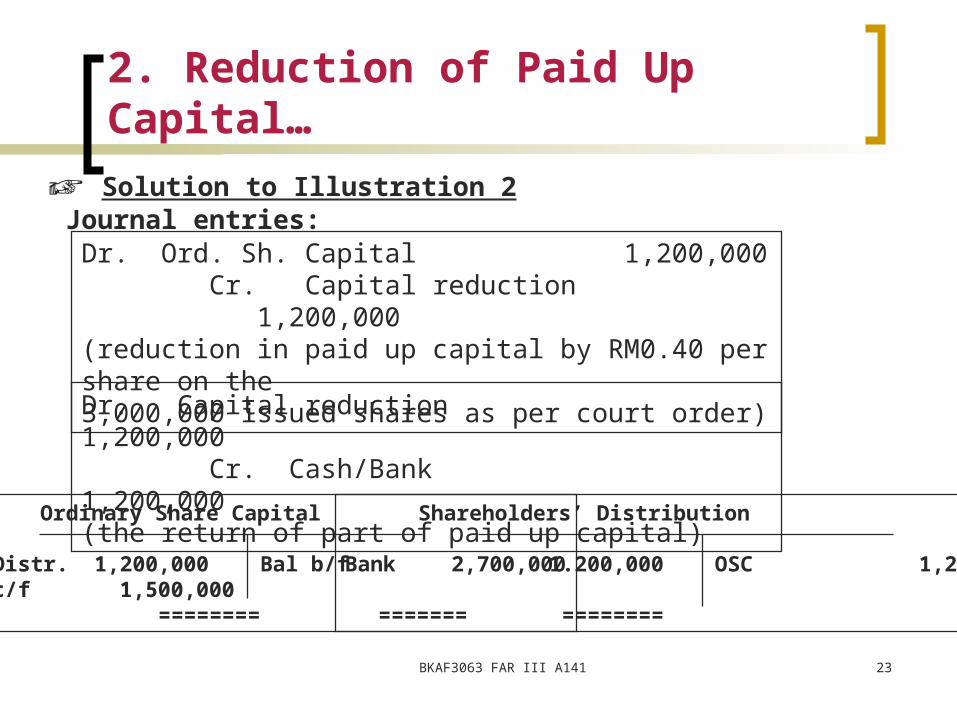

☞ Illustration 2:

Sejahtera Berhad has the following related to its capital as at 30 June 2013:

Authorized capital:5,000,000 ordinary shares of RM1.00 each 5,000,000

Issued & paid up capital:3,000,000 ordinary shares of RM1.00 each paid to RM0.90 2,700,000

As the company has more assets than can be used profitable at present, the directors proposed to reduce paid up capital and return the RM0.40 per share in cash to shareholders. Because they do not anticipate any growth in the company’s activities, the directors also proposed to cancel the RM0.10 per share uncalled capital. In addition, they proposed that both of these changes ought to affect authorized capital.

2. Reduction of Paid Up Capital…

23

☞ Solution to Illustration 2 Journal entries:

Dr. Ord. Sh. Capital 1,200,000 Cr. Capital reduction 1,200,000(reduction in paid up capital by RM0.40 per share on the3,000,000 issued shares as per court order)

Ordinary Share Capital

Sh. Distr. 1,200,000 Bal b/f 2,700,000Bal c/f 1,500,000 ======== =======

Shareholders’ Distribution

Bank 1.200,000 OSC 1,200,000

======== =======

Dr. Capital reduction 1,200,000 Cr. Cash/Bank 1,200,000(the return of part of paid up capital)

BKAF3063 FAR III A141

2. Reduction of Paid Up Capital…

BKAF3063 FAR III A141 24

Stmt of capital after the distribution of surplus:

Authorized capital:2,000,000 ordinary shares of RM1.00 each 2,000,0003,000,000 ordinary shares of RM0.50 each 1,500,000

3,500,000

Issued & paid up capital:3,000,000 ordinary shares of RM0.50 each 1,500,000

Par value RM1.00Return in cash RM0.40Cancel uncalled RM0.10New par value RM0.50

2. Reduction of Paid Up Capital…

25

2. Reduction of Paid Up Capital…

2. Cancellation of capital loss:

known as Turnaround Situation. Badly managed companies might suffer losses of some

of their paid-up cap due to a large scale embezzlement or a series of operating losses or a fire in uninsured building or by an economic, political or technological changes.

Hence, companies might have to write-off or writing down the accounts which contain the loss including adjusting their paid-up capital.

BKAF3063 FAR III A141

26

2. Reduction of Paid Up Capital…

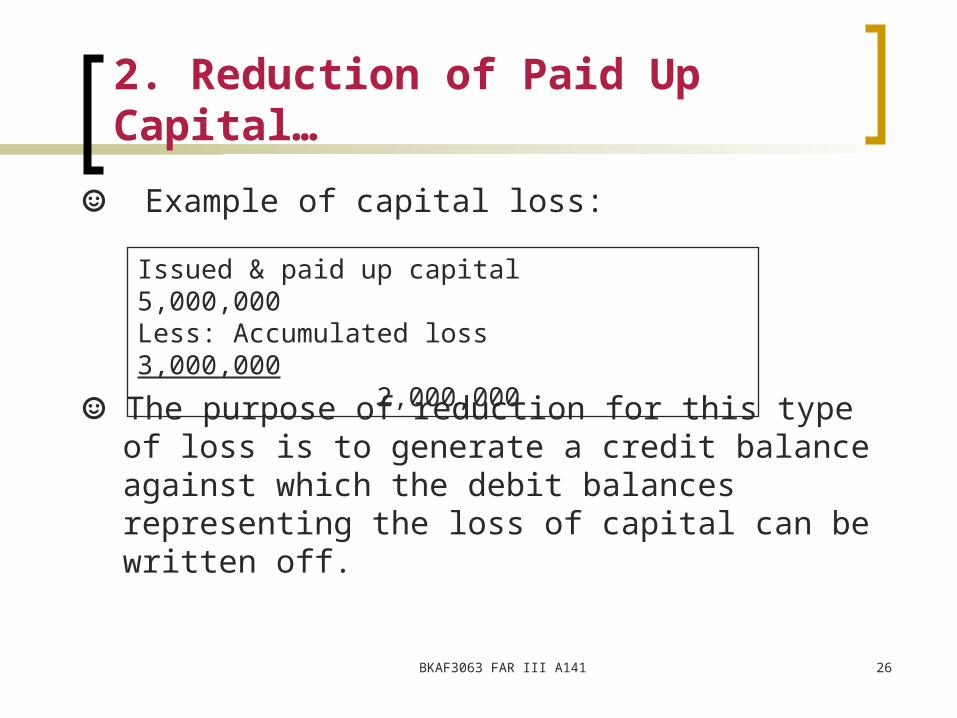

☺ Example of capital loss:

Issued & paid up capital 5,000,000Less: Accumulated loss 3,000,000

2,000,000

☺ The purpose of reduction for this type of loss is to generate a credit balance against which the debit balances representing the loss of capital can be written off.

BKAF3063 FAR III A141

BKAF3063 FAR III A141

27

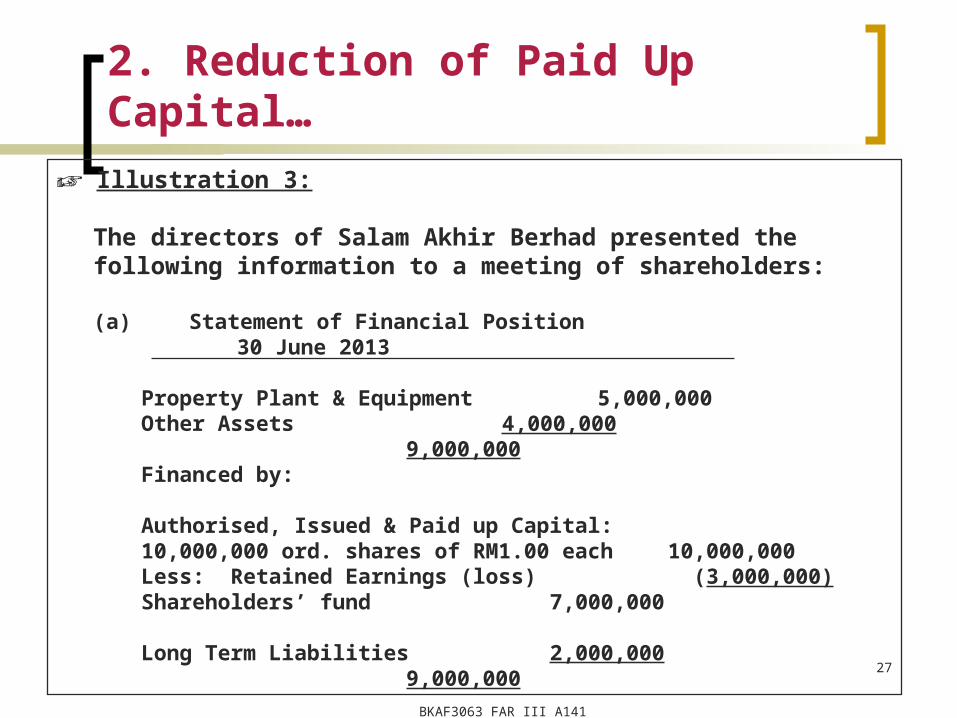

☞ Illustration 3:

The directors of Salam Akhir Berhad presented the following information to a meeting of shareholders:

(a) Statement of Financial Position30 June 2013

Property Plant & Equipment 5,000,000Other Assets 4,000,000

9,000,000Financed by:

Authorised, Issued & Paid up Capital:10,000,000 ord. shares of RM1.00 each 10,000,000Less: Retained Earnings (loss) (3,000,000)Shareholders’ fund 7,000,000

Long Term Liabilities 2,000,000 9,000,000

2. Reduction of Paid Up Capital…

28

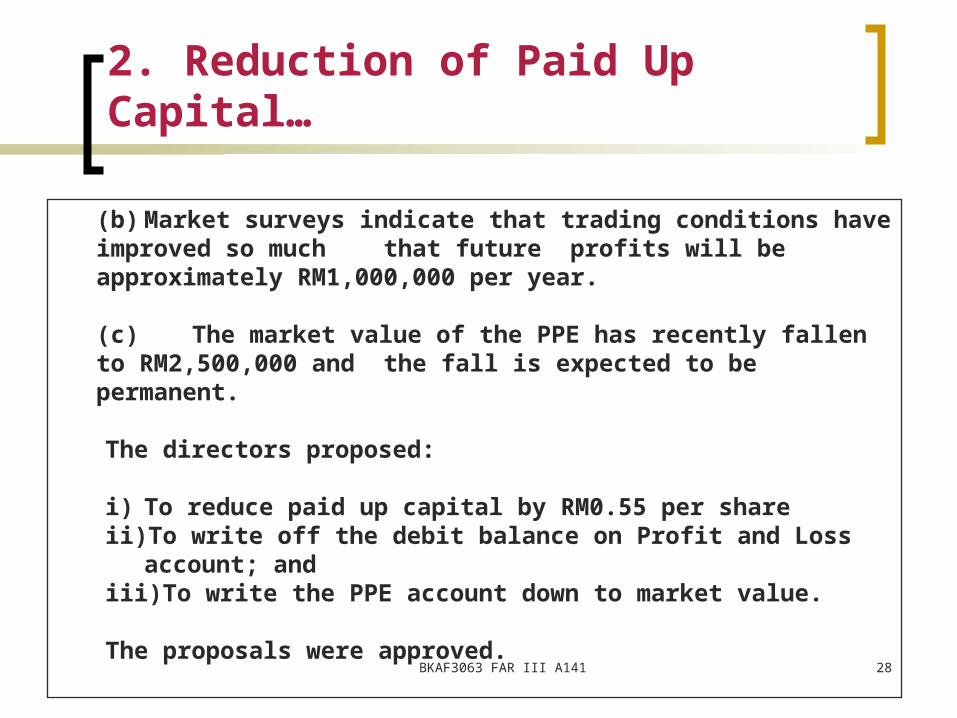

(b) Market surveys indicate that trading conditions have improved so much that future profits will be approximately RM1,000,000 per year.

(c) The market value of the PPE has recently fallen to RM2,500,000 and the fall is expected to be permanent.

The directors proposed:

i) To reduce paid up capital by RM0.55 per shareii) To write off the debit balance on Profit and Loss account; andiii) To write the PPE account down to market value.

The proposals were approved.

BKAF3063 FAR III A141

2. Reduction of Paid Up Capital…

29

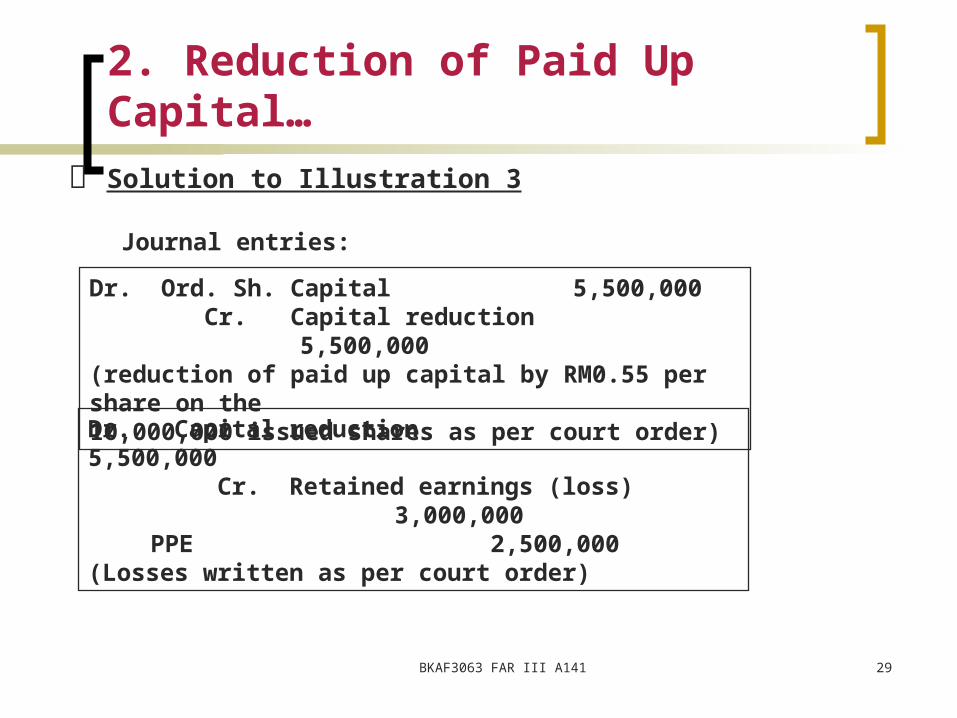

Solution to Illustration 3

Journal entries:

Dr. Ord. Sh. Capital 5,500,000 Cr. Capital reduction 5,500,000(reduction of paid up capital by RM0.55 per share on the10,000,000 issued shares as per court order)

Dr. Capital reduction 5,500,000 Cr. Retained earnings (loss) 3,000,000

PPE 2,500,000(Losses written as per court order)

BKAF3063 FAR III A141

2. Reduction of Paid Up Capital…

BKAF3063 FAR III A141 30

Ordinary Share Capital ‘000 ‘000Cap. reduction 5,500 Bal b/f 10,000Bal c/f 4,500 ====== ======

Retained Earnings ‘000 ‘000Bal b/f 3,000 Cap. Reduction 3,000 ====== =====

PPE ‘000 ‘000Bal b/f 5,000 Cap. Reduction 2,500

Bal c/f 2,500 ===== =====

Capital Reduction ‘000 ‘000Ret. earnings 3,000 OSC 5,500PPE 2,500 ===== =====

2. Reduction of Paid Up Capital…

BKAF3063 FAR III A141 31

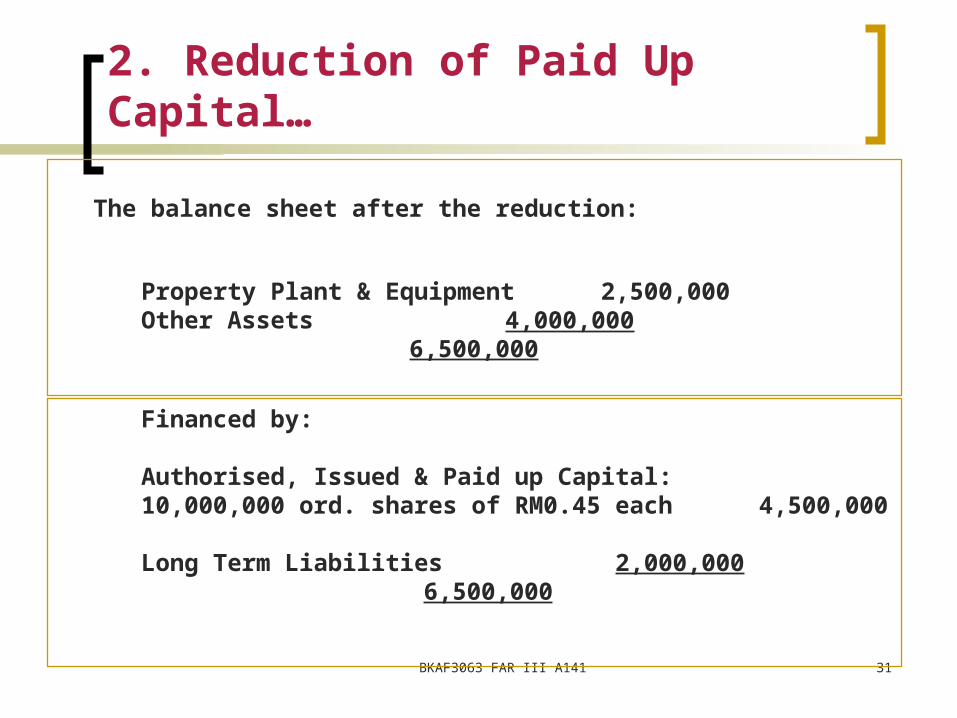

The balance sheet after the reduction:

Property Plant & Equipment 2,500,000Other Assets 4,000,000

6,500,000

Financed by:

Authorised, Issued & Paid up Capital:10,000,000 ord. shares of RM0.45 each 4,500,000

Long Term Liabilities 2,000,000 6,500,000

2. Reduction of Paid Up Capital…

32

2. Reduction of Paid Up Capital…

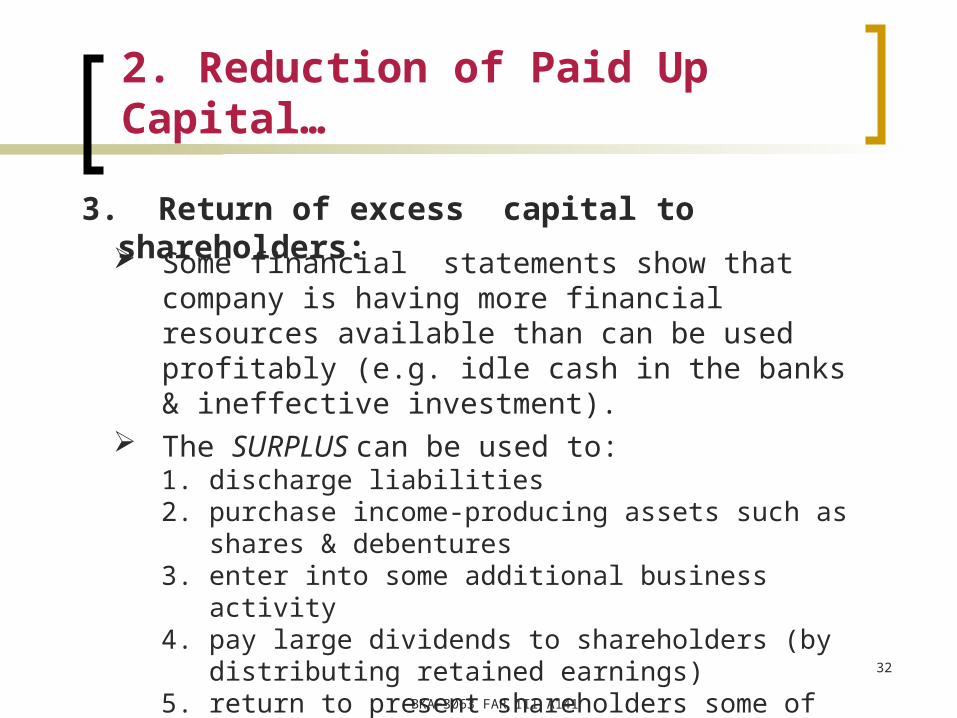

3. Return of excess capital to shareholders:

Some financial statements show that company is having more financial resources available than can be used profitably (e.g. idle cash in the banks & ineffective investment).

The SURPLUS can be used to:1. discharge liabilities2. purchase income-producing assets such as shares &

debentures3. enter into some additional business activity4. pay large dividends to shareholders (by distributing retained

earnings)5. return to present shareholders some of the capital which had

been contributed in the pastBKAF3063 FAR III A141

33

2. Reduction of Paid Up Capital…

In choosing among the alternatives, the directors may consider:

- the costs of the various types of finance available,- the rates of return on other investments,- the long-term effects (including the incidence of

taxation) on the co. & its shareholders,- the requirements of the law relating to company [e.g.

For alternative (5), need to satisfy S. 64 of CA, need to get approvals etc.].

Could combine all the factors or combine several factors for an arrangement scheme.

BKAF3063 FAR III A141

BKAF3063 FAR III A141 34

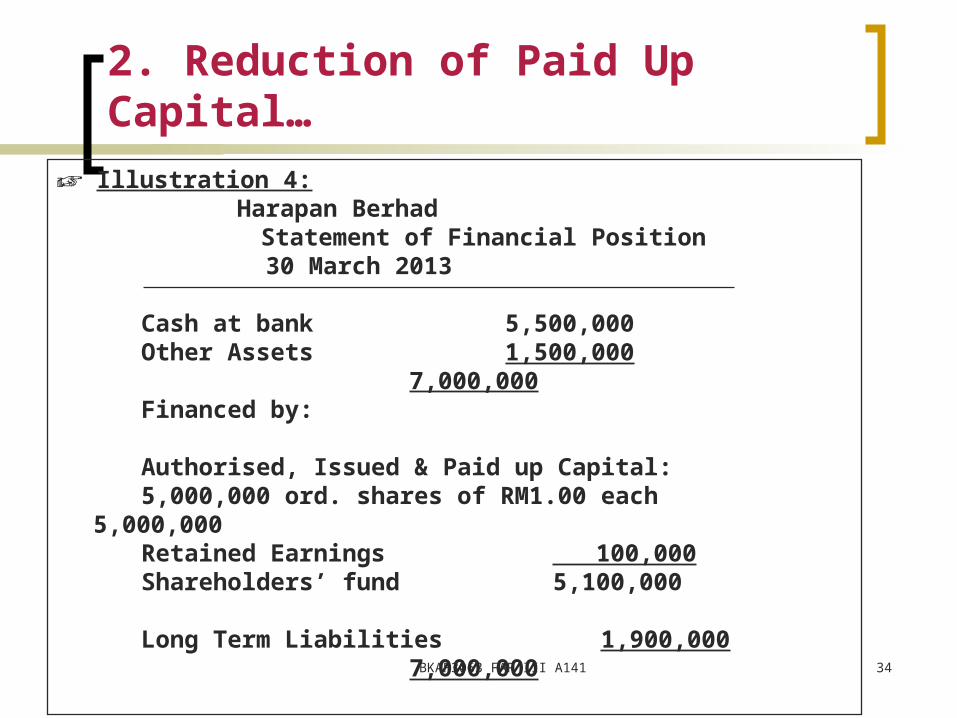

☞ Illustration 4:Harapan Berhad

Statement of Financial Position 30 March 2013

Cash at bank 5,500,000Other Assets 1,500,000

7,000,000Financed by:

Authorised, Issued & Paid up Capital:5,000,000 ord. shares of RM1.00 each 5,000,000Retained Earnings 100,000Shareholders’ fund 5,100,000

Long Term Liabilities 1,900,000 7,000,000

2. Reduction of Paid Up Capital…

35

The company is operating in a declining industry and the directors have considered how to use the surplus assets. They have discovered that no profitable investment opportunity exists in the industry and that it would be unprofitable to reduce liabilities by more than RM900,000. In addition, they agreed that it would be unwise for the existing management to attempt to move into other activities.

Therefore, after having obtained the appropriate approvals from creditors, shareholders and the Court for reduction of capital, the directors put the following reorganization into effect on 1 April 2013:

i) Pay off RM900,000 of the liabilities.ii) Pay a dividend of RM0.02 per share; andiii) Reduce the par value of all shares to RM0.45 and return RM0.55 per

share to shareholders.BKAF3063 FAR III A141

2. Reduction of Paid Up Capital…

BKAF3063 FAR III A141 36

Solution to Illustration 4Journal entries:

Dr. Ord. Sh. Capital 2,750,000 Cr. Capital reduction 2,750,000(reduction in paid up capital by RM0.55 per share on the5,000,000 issued shares as per court order)

Dr. Dividends payable 100,000 Capital reduction 2,750,000 Cr. Bank 2,850,000

Dr. Liabilities 900,000 Cr. Bank 900,000

Dr. Retained Earnings 100,000 Cr. Dividend payable 100,000(payment of dividend 5,000,000 x RM0.02)

2. Reduction of Paid Up Capital…

37

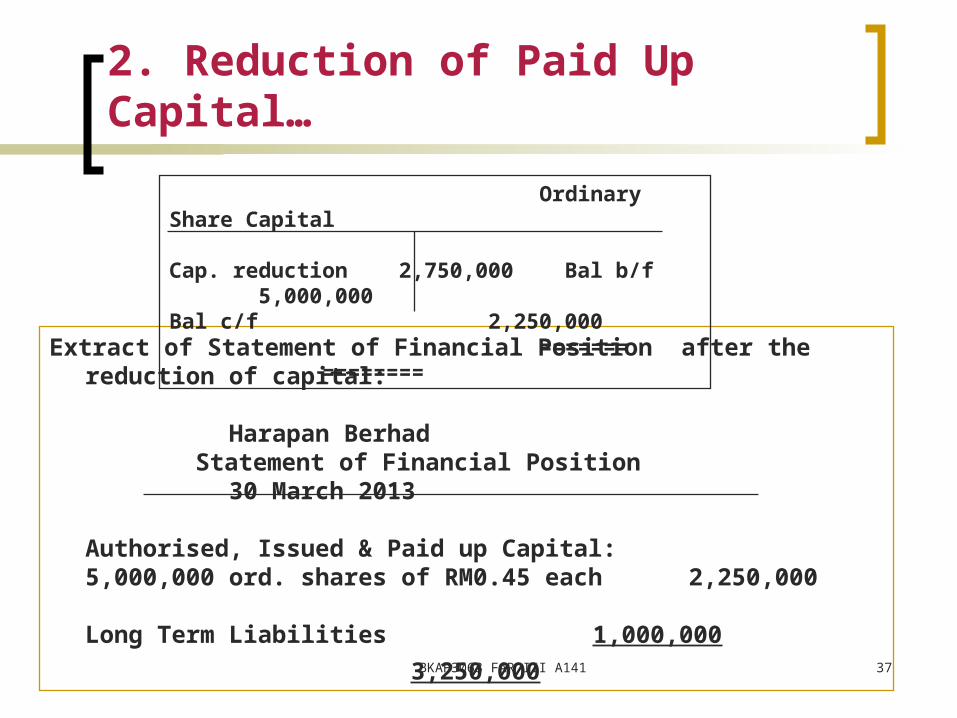

Extract of Statement of Financial Position after the reduction of capital:

Harapan Berhad Statement of Financial Position 30 March 2013

Authorised, Issued & Paid up Capital:5,000,000 ord. shares of RM0.45 each 2,250,000

Long Term Liabilities 1,000,000

3,250,000

Ordinary Share Capital

Cap. reduction 2,750,000 Bal b/f 5,000,000Bal c/f 2,250,000 ======= ========

BKAF3063 FAR III A141

2. Reduction of Paid Up Capital…

38

2. Reduction of Paid Up Capital…

In certain cases, reduction of capital may involve more than one class of shareholders.

As each class of capital issued by a company must be recorded in separate, appropriately described, accounts, a return of capital which affects more than one class of shares involves more accounting entries.

BKAF3063 FAR III A141

BKAF3063 FAR III A141 39

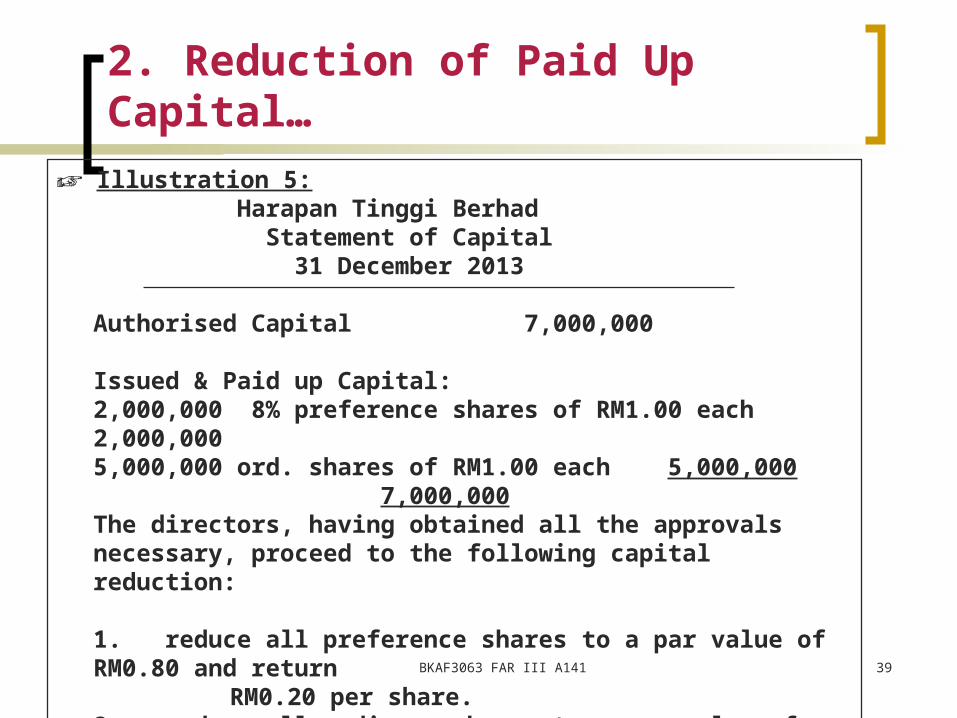

☞ Illustration 5:Harapan Tinggi Berhad Statement of Capital 31 December 2013

Authorised Capital 7,000,000

Issued & Paid up Capital:2,000,000 8% preference shares of RM1.00 each 2,000,0005,000,000 ord. shares of RM1.00 each 5,000,000

7,000,000The directors, having obtained all the approvals necessary, proceed to the following capital reduction:

1. reduce all preference shares to a par value of RM0.80 and return RM0.20 per share.

2. reduce all ordinary shares to a par value of RM0.60 and return RM0.40 per share.

2. Reduction of Paid Up Capital…

40

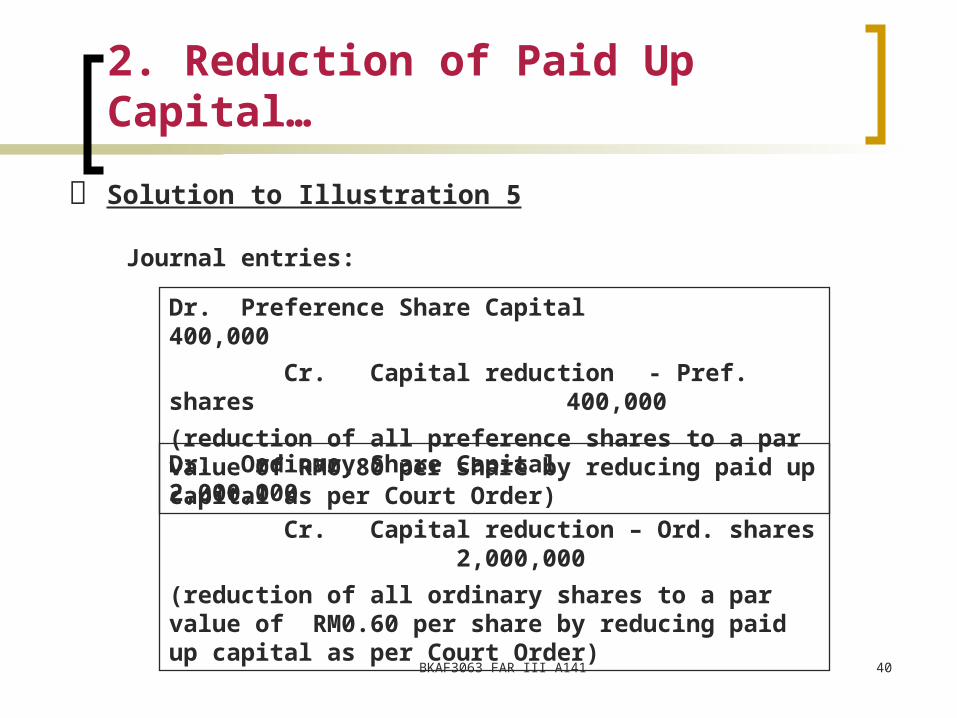

Solution to Illustration 5

Journal entries:

Dr. Ordinary Share Capital 2,000,000

Cr. Capital reduction – Ord. shares 2,000,000

(reduction of all ordinary shares to a par value of RM0.60 per share by reducing paid up capital as per Court Order)

Dr. Preference Share Capital 400,000

Cr. Capital reduction - Pref. shares 400,000

(reduction of all preference shares to a par value 0f RM0.80 per share by reducing paid up capital as per Court Order)

BKAF3063 FAR III A141

2. Reduction of Paid Up Capital…

41

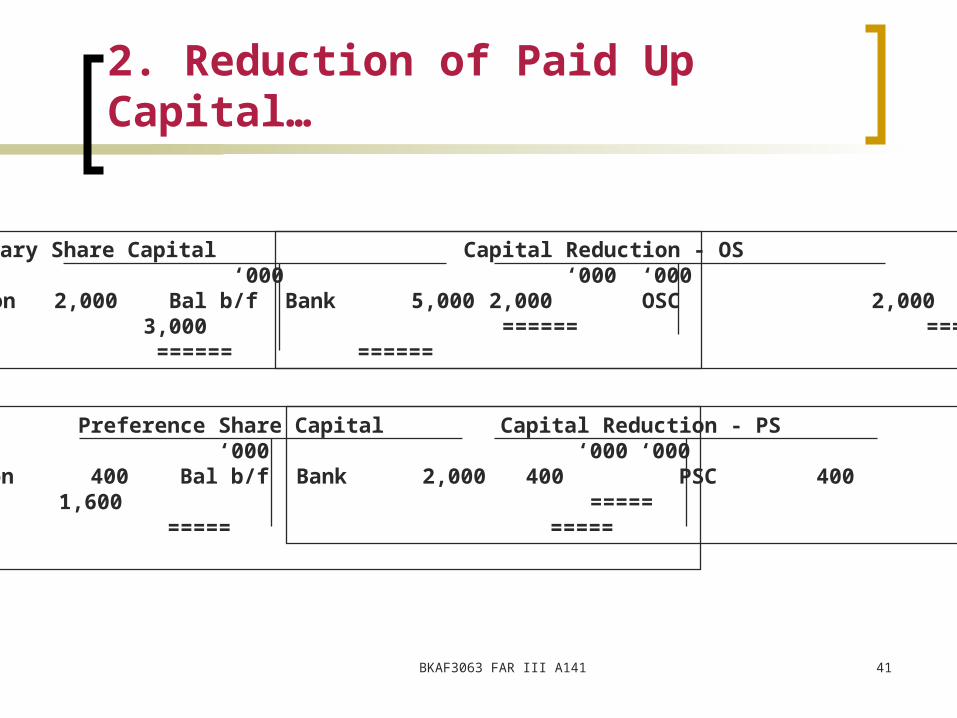

Ordinary Share Capital ‘000 ‘000Cap. reduction 2,000 Bal b/f 5,000Bal c/f 3,000 ====== ======

Capital Reduction - OS ‘000 ‘000Bank 2,000 OSC 2,000 ====== =====

Preference Share Capital ‘000 ‘000Cap. reduction 400 Bal b/f 2,000Bal c/f 1,600 ===== =====

Capital Reduction - PS ‘000 ‘ 000Bank 400 PSC 400 ===== =====

BKAF3063 FAR III A141

2. Reduction of Paid Up Capital…

BKAF3063 FAR III A141 42

Harapan Tinggi Berhad Statement of Capital 31 December 2013

Authorised Capital 7,000,000

Issued & Paid up Capital:2,000,000 8% preference shares of RM0.80 each fully paid 1,600,0005,000,000 ord. shares of RM0.60 each fully paid 3,000,000

4,600,000

2. Reduction of Paid Up Capital…

43

3. Issue of Bonus Shares

The issue of bonus shares does not add to the wealth of a company, or vary the rights of the shareholders.

It is merely a means of reclassifying the elements of shareholders funds by capitalising some of them (by converting some part of distributable profits into paid up capital).

The wealth of the shareholders may increase through increase in the market value of shareholders’ investment, even the share price may fall. It is assumed that the company will maintain its traditional rate of cash dividends.

BKAF3063 FAR III A141

44

3. Issue of Bonus Shares…

Bonus issue often used as a defence against take-over bid by way of:o persuade the shareholders to retain the shares for the

dividends.o the increase in number of shares to be acquired by

bidders.

Some internal reasons for the issue of bonus shares:

1. Recognition of the amount of capital required for operations.

2. Relieving shareholders’ of liability.3. ‘tidying up’ the balance sheet.4. Recognition of increases in the value of assets.

BKAF3063 FAR III A141

45

3. Issue of Bonus Shares…

(1) Recognition of the amount of capital required for operations: Most companies “retain” some of each year’s profit in way of

retained earnings, unappropriated profits & profit and loss appropriation (dividends paid not equal to reported profit).

These are regarded as permanent capital.

Argument: the balance sheet does not accurately describe the situation and that all or most of the undistributed profit ought to be converted into paid up capital through the issue of bonus shares.

BKAF3063 FAR III A141

46

3. Issue of Bonus Shares…

☞ Illustration 6: SerbaTinggi Berhad Statement of Capital 30 March 2013

Authorised Capital 10,000,000

Issued & Paid up Capital:2,000,000 ordinary shares of RM1.00 each 2,000,000

Retained earnings 5,500,000Shareholders’ fund 7,500,000

The directors estimated that to maintain its present level of operations, the company requires share capital and reserves of RM7 million. The directors recommend a bonus issue of five shares for every two held.

BKAF3063 FAR III A141

BKAF3063 FAR III A141 47

3. Issue of Bonus Shares…

Solution to Illustration 6:

If articles permit the direct capitalization:

Journal entries:

If articles does not permit the direct capitalization:

Dr. Retained Earnings 5,000,000 Cr. Ordinary Share Capital 5,000,000(bonus issue of five fully paid ordinary shares for every two shares held out of retained earnings)

Dr. Retained Earnings 5,000,000 Cr. Dividend Payable 5,000,000

Dr. Dividend Payable 5,000,000 Cr. Ordinary Share Capital 5,000,000

48

3. Issue of Bonus Shares…

The statement of capital after the bonus issue:

Authorised Capital 10,000,000

Issued & Paid up Capital:7,000,000 ordinary shares of RM1.00 each 7,000,000

Retained earnings 500,000Shareholders’ fund 7,500,000

BKAF3063 FAR III A141

49

3. Issue of Bonus Shares…

(2) Relieving shareholders’ of liability:

It happens when company decides to capitalise undistributed profits by ‘paying up’ uncalled cap rather than by making a bonus issue of fully paid shares.

This has the effect of relieving shareholders of the liability to pay the uncalled capital.

BKAF3063 FAR III A141

50

3. Issue of Bonus Shares…

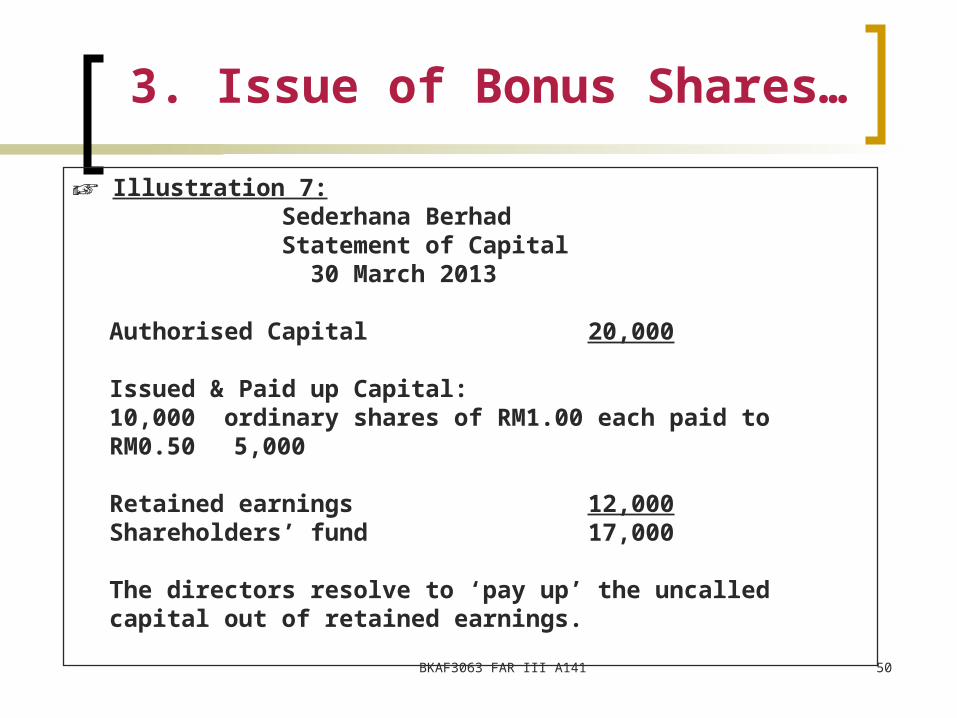

☞ Illustration 7: Sederhana Berhad Statement of Capital 30 March 2013

Authorised Capital 20,000

Issued & Paid up Capital:10,000 ordinary shares of RM1.00 each paid to RM0.50 5,000

Retained earnings 12,000Shareholders’ fund 17,000

The directors resolve to ‘pay up’ the uncalled capital out of retained earnings.

BKAF3063 FAR III A141

BKAF3063 FAR III A141 51

3. Issue of Bonus Shares…

Solution to Illustration 7:Journal entries:

Dr. Retained Earnings 5,000 Cr. Ordinary Share Capital 5,000(capitalization of retained earnings by eliminating uncalled capital)

The statement of capital after the bonus issue:

Authorised Capital 20,000

Issued & Paid up Capital:10,000 ordinary shares of RM1.00 each fully paid 10,000

Retained earnings 7,000Shareholders’ fund 17,000

52

3. Issue of Bonus Shares…

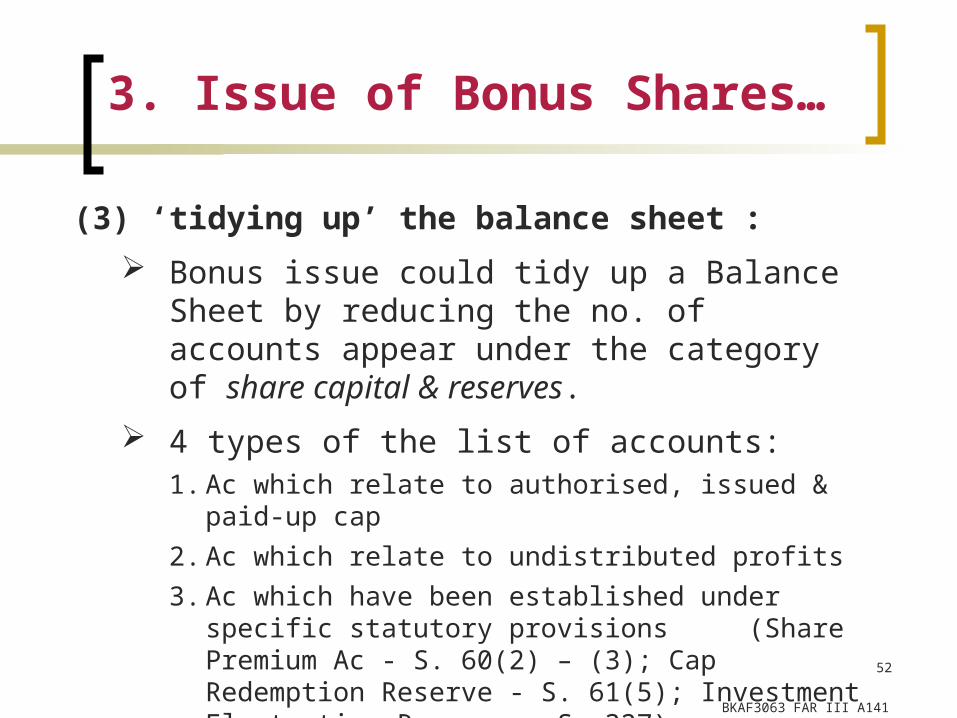

(3) ‘tidying up’ the balance sheet :

Bonus issue could tidy up a Balance Sheet by reducing the no. of accounts appear under the category of share capital & reserves.

4 types of the list of accounts:1. Ac which relate to authorised, issued & paid-up cap

2. Ac which relate to undistributed profits

3. Ac which have been established under specific statutory provisions (Share Premium Ac - S. 60(2) – (3); Cap Redemption Reserve - S. 61(5); Investment Fluctuation Reserve - S. 327).

4. Ac which have been established under specific provisions in the company’s Articles.

BKAF3063 FAR III A141

53

3. Issue of Bonus Shares…

Hence the issuance of bonus shares will reduce those many accounts into less number of accounts.

The presented statements will be easier to digest & will look simpler.

BKAF3063 FAR III A141

54

3. Issue of Bonus Shares…

(4) Recognition of increases in the value of assets :

Revaluation of assets:o Increase – upward revaluation (credit to revaluation

reserve)o Decrease – downward revaluation (impairment, debit to

profit and loss)

Revaluation gains (realised or unrealised) can be used to issue bonus shares or to ‘pay up’ uncalled capital.

BKAF3063 FAR III A141

55

4. Redemption of Preference Shares

Basically, a company is prohibited from returning back or distributing capital to its shareholders, except under the resolutions in S. 64 discussed earlier.

However, company can create a class of share which carries:o the right to a return of capital in future, or o the right to redeem this class of shares at company’s

option.

S. 61 - if authorised by its articles, company can issue redeemable preference shares & the redemption shall be effected only by the manner provided by the articles.

BKAF3063 FAR III A141

56

4. Redemption of Preference Shares…

WARNINGS in S. 61:o The redemption shall not be taken as reducing the amount of

authorised share capital.o The shares could only be redeemed:

- out of profits which would otherwise be available for dividend; OR

- out of the proceeds of a fresh issue of shares made for the purposes of the redemption; AND

- if they are fully paid-up.

Even though paid-up cap is not reduced, the value of assets & shareholders’ equity will decrease because the articles often require the redemption at premium (to compensate shareholders for the loss of income in the future). Thus, premium on redemption must be provided for redemption out of profits or out of Share Premium Account.

BKAF3063 FAR III A141

BKAF3063 FAR III A14157

4.Redemption of Preference Shares…

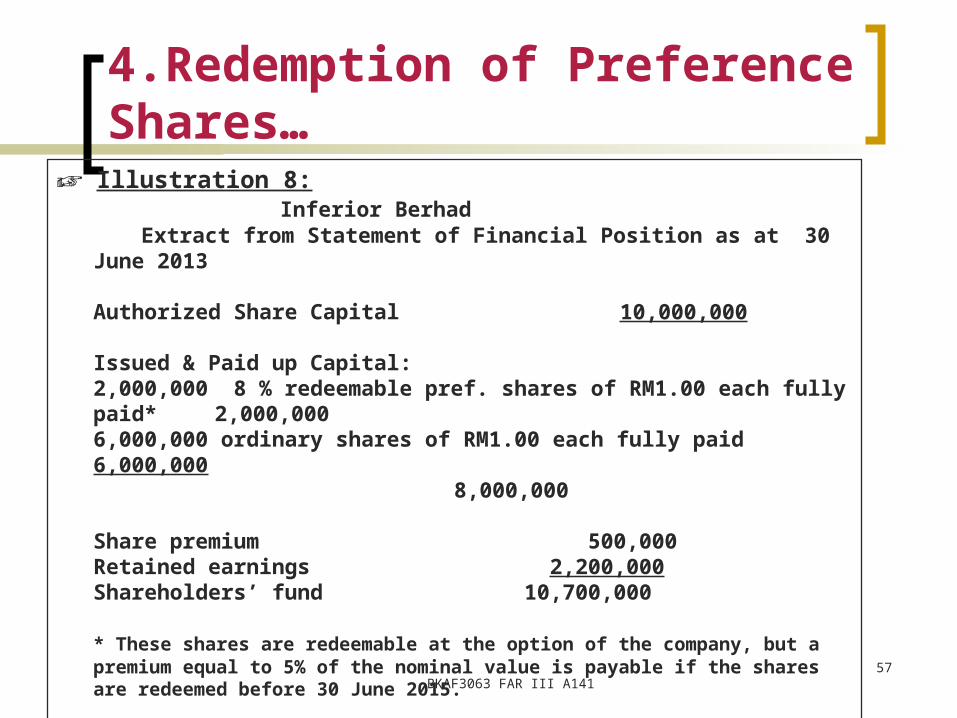

☞ Illustration 8: Inferior Berhad

Extract from Statement of Financial Position as at 30 June 2013

Authorized Share Capital10,000,000

Issued & Paid up Capital:2,000,000 8 % redeemable pref. shares of RM1.00 each fully paid* 2,000,0006,000,000 ordinary shares of RM1.00 each fully paid 6,000,000

8,000,000

Share premium 500,000Retained earnings 2,200,000Shareholders’ fund 10,700,000

* These shares are redeemable at the option of the company, but a premium equal to 5% of the nominal value is payable if the shares are redeemed before 30 June 2015.

On 1 August 2013, the directors resolve to exercise the company’s option to redeem all the preference shares.

BKAF3063 FAR III A141 58

4. Redemption of Preference Shares…

Solution to Illustration 8:

I. Redeem out of retained earnings:

Journal entries:

Dr. Share premium 100,000 Cr. Red. pref shareholders distribution 100,000

Dr. Retained earnings 2,000,000 Cr. Capital redemption reserve 2,000,000

Dr. Redeemable preference share capital 2,000,000

Cr. Red. pref shareholders distribution 2,000,000

Dr. Red. pref shareholders distribution 2,100,000 Cr. Bank 2,100,000

BKAF3063 FAR III A141 59

Redeemable Preference Share Capital ‘000 ‘000R.P.S.Distr. 2,000 Bal b/f 2,000 ====== ======

Share Premium ‘000 ‘000R.P.S.Distr. 100 Bal b/f 500Bal c/f 400 ====== =====

Retained Earnings ‘000 ‘000C.Red. Res. 2,000 Bal b/f 2,200Bal c/f 200 ===== =====

Red. Pref. Shareholders Distribution ‘000 ‘ 000Bank 2,100 Share prem. 100

Red. PSC 2,000 ===== =====

Capital Redemption Reserve ‘000 ‘000Bal. c/f 2,000 R. Earnings 2,000 ==== ====

4. Redemption of Preference Shares…

60

4. Redemption of Preference Shares…

The statement of capital after the redemption:RM‘000

Authorised Capital 10,000

Issued & Paid up Capital:6,000,000 ordinary shares of RM1.00 each fully paid 6,000Capital redemption reserve 2,000Share premium 400Retained earnings 200Shareholders’ fund 8,600

BKAF3063 FAR III A141

BKAF3063 FAR III A141 61

4. Redemption of Preference Shares…

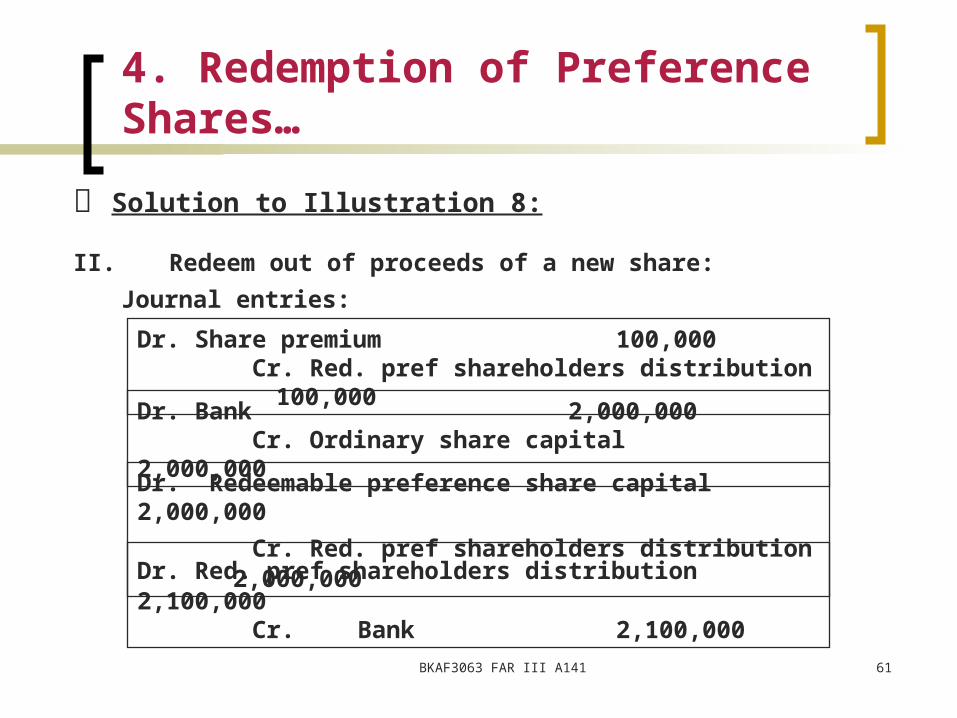

Solution to Illustration 8:

II. Redeem out of proceeds of a new share:

Journal entries:

Dr. Share premium 100,000 Cr. Red. pref shareholders distribution 100,000

Dr. Bank 2,000,000 Cr. Ordinary share capital 2,000,000

Dr. Redeemable preference share capital 2,000,000

Cr. Red. pref shareholders distribution 2,000,000

Dr. Red. pref shareholders distribution 2,100,000 Cr. Bank 2,100,000

BKAF3063 FAR III A141 62

Redeemable Preference Share Capital ‘000 ‘000R.P.S.Distr. 2,000 Bal b/f 2,000 ====== ======

Share Premium ‘000 ‘000R.P.S.Distr. 100 Bal b/f 500Bal c/f 400 ====== =====

Ordinary Share Capital ‘000 ‘000

Bal b/f 6,000Bal c/f 8,000 Bank 2,000 ===== =====

Red. Pref. Shareholders Distribution ‘000 ‘ 000Bank 2,100 Share prem. 100

Red. PSC 2,000 ===== =====

4. Redemption of Preference Shares…

63

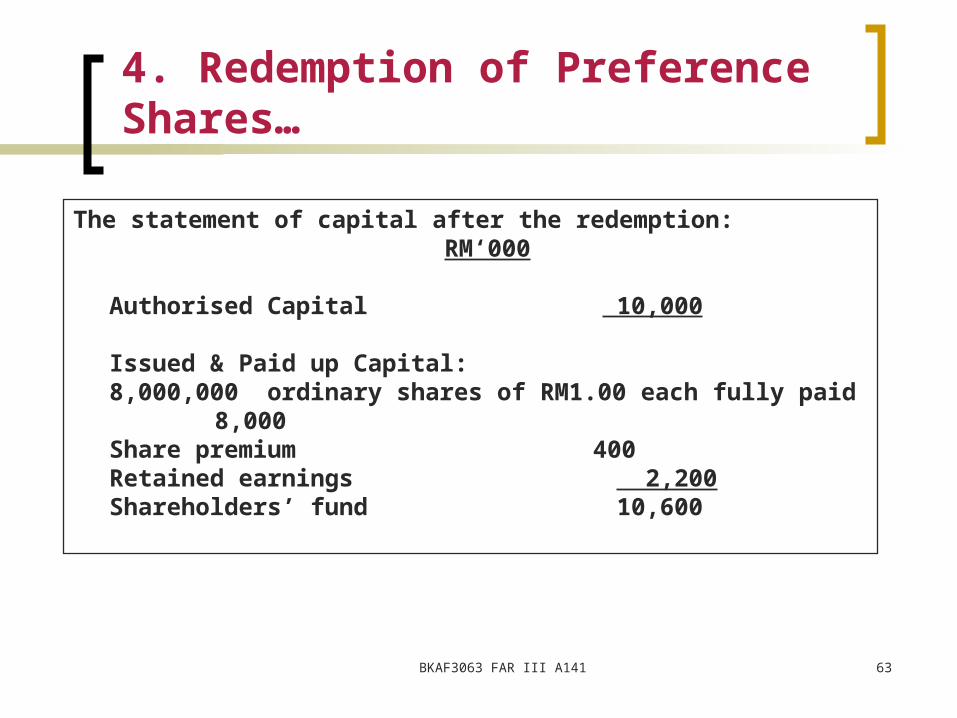

4. Redemption of Preference Shares…

The statement of capital after the redemption:RM‘000

Authorised Capital 10,000

Issued & Paid up Capital:8,000,000 ordinary shares of RM1.00 each fully paid 8,000Share premium 400Retained earnings 2,200Shareholders’ fund 10,600

BKAF3063 FAR III A141

Reference

Jane Lazar & Tan Lay Leng (2003), Company Account & Reporting, 5th Edition.

BKAF3063 FAR III A141 64