tops 2014 bonds and equities v3

TRANSCRIPT

Targets of Opportunity System (“TOPS”)A Short-term, Long-only Approach to Trading Stocks and Bonds

Clark Collins 2014

0.75

1.25

1.75

2.25

2.75

3.25

133 65 97 12

916

119

322

525

728

932

135

338

541

744

948

151

354

557

760

964

167

370

573

776

980

183

386

589

792

996

199

310

2510

5710

8911

2111

5311

8512

1712

4912

8113

1313

4513

7714

0914

4114

7315

0515

3715

6916

0116

3316

6516

9717

2917

6117

93

50-.5

50-.6

50-.7

50-.8

50-.9

150-0.50

150-0.60

150-0.70

150-0.80

150-0.90

250-0.50

250-0.60

250-0.70

250-0.80

250-0.90

350-0.50

350-0.60

350-0.70

Contents

Page

2. Contents3. Introduction4. Daily Growth and Drawdowns5. Investment Highlights6. Portfolio Composition and Margin7. Frequency Histogram of Daily Returns8. Worst S&P 500 months vs. TOPS9. Monthly Comparison to S&P 500 and Correlation visualization10. Monthly Scattergram and Regression to the S&P 500 Index11. Stock and Bond Indices and Combinations12. Risk Management and Engineering and Testing Construct13. NO Fit Parameter Selection14. Chart of all reasonable parameter outcomes15. Trade illustrations Monthly16. Trade illustrations Detailed Weekly17. Conclusion18. Resume

2

Introduction

Introduction

At present, the global financial markets carry tremendous uncertainty. Potential risk of loss due to “systemic failure” is ashigh as it has ever been, and today’s monetary policies have displaced much of what most of us have learned about financeover decades of general fundamental consensus. Will massive injections of future tax payer debt continue to artificiallysupport equity prices amidst the stark contrasts to a sluggish economy? What do investors do to protect themselves againstthe inevitable systemic risks? This is the same $100,000 question chased by investment professionals for decades.

My interest in constructing this project is an expansion of my long held belief that price action itself is one of very few inputsneeded to make appropriate investment decisions in the capital marketplace. Secondly, regardless of the systemic riskspresent I wanted to show that it is possible to construct an investment vehicle that can perform positively in the short andlong-term and with non-correlation when these price shocks across all asset classes reveal themselves

Using intraday price data , I have compiled a long-only (net of all fees) composite simulation utilizing six well known domesticfutures markets. Three of these individual markets utilize the “Equity-Stock” sector and the other three use U.S. Treasuryinstruments of different durations in the “Fixed Income-Bond” sector. These sectors/markets are some of the most liquidand transparent markets in the world.

Splitting a $ based risk budget equally and utilizing these traditionally non-correlated sectors, my summary shows the “TOPS”signal generations inherent strength which is to strategically enter/invest on measured pullbacks in the “Equity” marketswhile locking in short-term profits in the “Fixed Income” markets which were also previously invested on prior retracementsin its own measured pullback.

The "TOPS" signal generator is NOT built around a mandate that equity positions and bond positions cannot co-exist as onemight ask. The cross blending and alternating between these specific markets and sectors take place quite often as it logicallymakes sense in the short-term to have a sideways market where neither equities or bonds exhibits more directional pricemovement.

3

-30%

-25%

-20%

-15%

-10%

-5%

0%

$0.9

$1.1

$1.3

$1.5

$1.7

$1.9

$2.1

$2.3

$2.5

$2.7

$2.9

2008

0408

2008

0508

2008

0608

2008

0708

2008

0807

2008

0907

2008

1007

2008

1106

2008

1207

2009

0106

2009

0205

2009

0308

2009

0407

2009

0507

2009

0607

2009

0707

2009

0806

2009

0906

2009

1006

2009

1105

2009

1206

2010

0105

2010

0204

2010

0307

2010

0406

2010

0506

2010

0606

2010

0706

2010

0805

2010

0905

2010

1005

2010

1104

2010

1205

2011

0104

2011

0203

2011

0306

2011

0405

2011

0505

2011

0605

2011

0705

2011

0804

2011

0904

2011

1004

2011

1103

2011

1204

2012

0103

2012

0202

2012

0304

2012

0403

2012

0503

2012

0603

2012

0703

2012

0802

2012

0902

2012

1002

2012

1101

2012

1202

2013

0101

2013

0131

2013

0303

2013

0402

2013

0502

2013

0611

2013

0711

2013

0811

2013

0910

2013

1010

2013

1110

2013

1210

Compounded Net Annualized 16.2%Annualized Standard Deviation 11.2 %Sharpe (2% r.f.) 1.26Annualized Downside Deviation 7.88 %Max Drawdown - 11.69 %Max Days to recovery 230 daysSortino Ratio (2% r.f.) 1.80Compound Annual / Max Draw 1.39

“TOPS” Simulated $1 NET Linear Daily Growth and Associated DrawdownsApril 2008 to January 2014

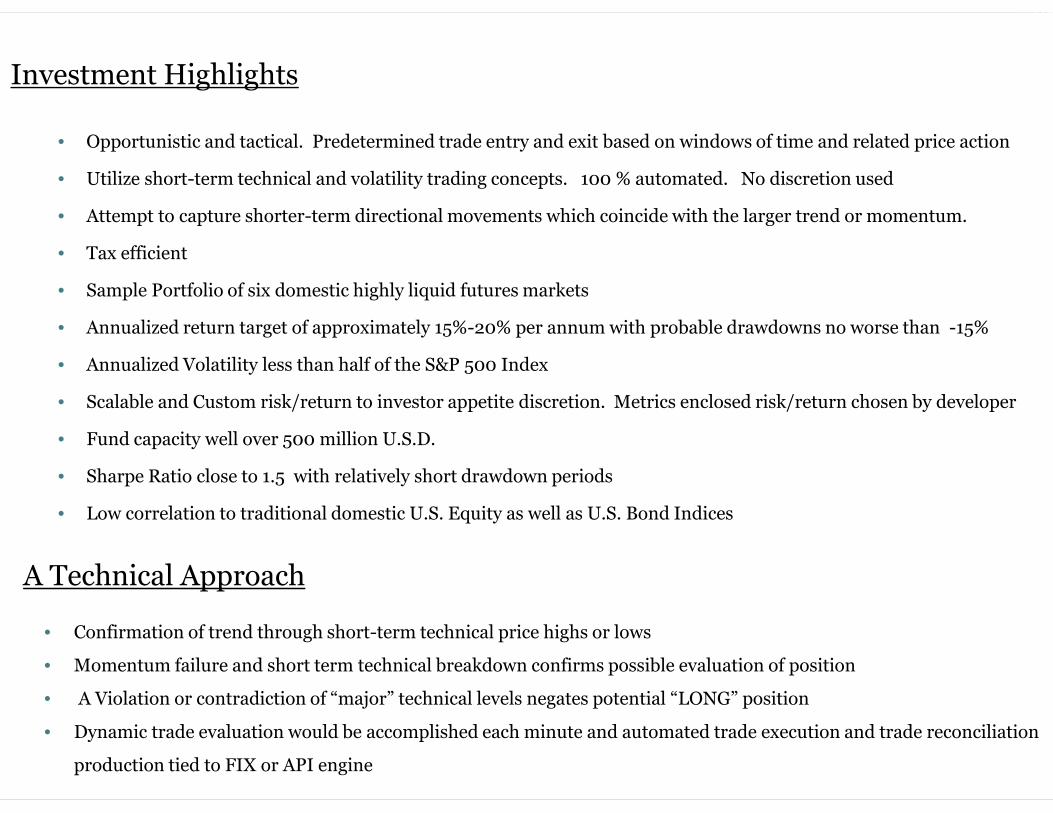

Investment Highlights

• Opportunistic and tactical. Predetermined trade entry and exit based on windows of time and related price action

• Utilize short-term technical and volatility trading concepts. 100 % automated. No discretion used

• Attempt to capture shorter-term directional movements which coincide with the larger trend or momentum.

• Tax efficient

• Sample Portfolio of six domestic highly liquid futures markets

• Annualized return target of approximately 15%-20% per annum with probable drawdowns no worse than -15%

• Annualized Volatility less than half of the S&P 500 Index

• Scalable and Custom risk/return to investor appetite discretion. Metrics enclosed risk/return chosen by developer

• Fund capacity well over 500 million U.S.D.

• Sharpe Ratio close to 1.5 with relatively short drawdown periods

• Low correlation to traditional domestic U.S. Equity as well as U.S. Bond Indices

A Technical Approach

• Confirmation of trend through short-term technical price highs or lows

• Momentum failure and short term technical breakdown confirms possible evaluation of position

• A Violation or contradiction of “major” technical levels negates potential “LONG” position

• Dynamic trade evaluation would be accomplished each minute and automated trade execution and trade reconciliation

production tied to FIX or API engine

6Portfolio Composition

Monthly and Equally Rebalanced Risk Budget of 6 Futures Markets in Simulation

ES – Mini S&P 500 Index (CME- “Globex”) FV – US Five Year Note (CBOT- “Globex”)

NQ – Mini NASDAQ 100 Index (CME- “Globex) TY – US Ten Year Note (CBOT- “Globex”)

YM - Dow Jones Index (CBOT-”Globex”) US – US 30 Year Bond (CBOT – “Globex”)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

15%

20%

25%

30%

2008

1126

2008

1225

2009

0123

2009

0222

2009

0323

2009

0421

2009

0520

2009

0618

2009

0717

2009

0816

2009

0914

2009

1013

2009

1111

2009

1210

2010

0108

2010

0207

2010

0308

2010

0406

2010

0505

2010

0603

2010

0702

2010

0801

2010

0830

2010

0928

2010

1027

2010

1125

2010

1224

2011

0123

2011

0221

2011

0322

2011

0420

2011

0519

2011

0617

2011

0717

2011

0815

2011

0913

2011

1012

2011

1110

2011

1209

2012

0108

2012

0206

2012

0306

2012

0404

2012

0503

2012

0601

2012

0701

2012

0730

2012

0828

2012

0926

2012

1025

2012

1123

2012

1223

2013

0121

2013

0219

2013

0320

2013

0418

2013

0517

2013

0616

2013

0715

2013

0813

2013

0911

2013

1010

2013

1108

2013

1208

20 Day and 200 Day Moving Averages of Margin to Static $1,000,000 PortfolioAugust 2008 to January of 2014

Average Margin to Equity 20.1 %Max Margin to Equity 33.7 %Non-Trading Days of Total Days 16.2 %

0

20

40

60

80

100

120

-6.0

%-5

.9%

-5.7

%-5

.6%

-5.4

%-5

.3%

-5.1

%-5

.0%

-4.8

%-4

.7%

-4.5

%-4

.4%

-4.2

%-4

.1%

-3.9

%-3

.8%

-3.6

%-3

.5%

-3.3

%-3

.2%

-3.0

%-2

.9%

-2.7

%-2

.6%

-2.4

%-2

.3%

-2.1

%-2

.0%

-1.8

%-1

.7%

-1.5

%-1

.4%

-1.2

%-1

.1%

-0.9

%-0

.8%

-0.6

%-0

.5%

-0.3

%-0

.2%

0.0%

0.1%

0.3%

0.5%

0.6%

0.8%

0.9% 1.1%

1.2%

1.4%

1.5%

1.7%

1.8%

2.0%

2.1%

2.3%

2.4%

2.6%

2.7%

2.9%

3.0%

3.2%

3.3%

3.5%

3.6%

3.8%

3.9%

4.1%

4.2%

4.4%

4.5%

4.7%

4.8%

5.0% 5.1%

5.3%

5.4%

5.6%

5.7%

5.9%

6.0%

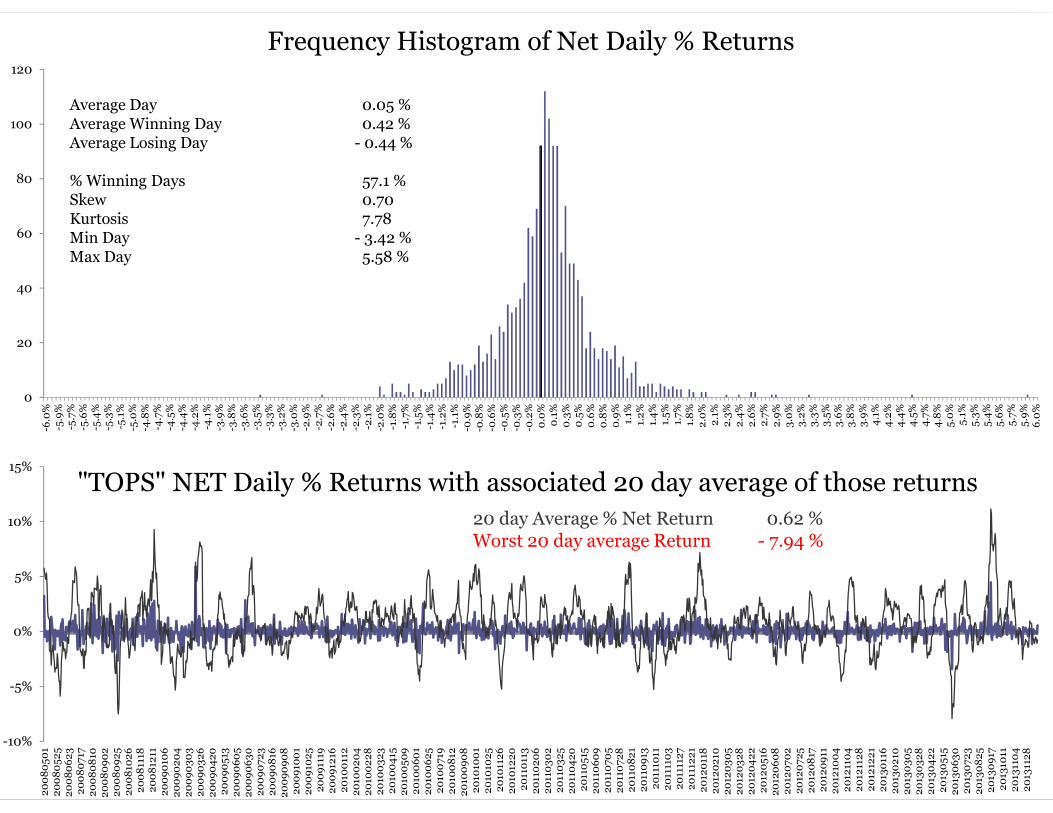

Average Day 0.05 %Average Winning Day 0.42 %Average Losing Day - 0.44 %

% Winning Days 57.1 %Skew 0.70Kurtosis 7.78Min Day - 3.42 %Max Day 5.58 %

Frequency Histogram of Net Daily % Returns

-10%

-5%

0%

5%

10%

15%

2008

0501

2008

0525

2008

0623

2008

0717

2008

0810

2008

0902

2008

0925

2008

1026

2008

1118

2008

1211

2009

0106

2009

0204

2009

0303

2009

0326

2009

0420

2009

0513

2009

0605

2009

0630

2009

0723

2009

0816

2009

0908

2009

1001

2009

1025

2009

1119

2009

1216

2010

0112

2010

0204

2010

0228

2010

0323

2010

0415

2010

0509

2010

0601

2010

0625

2010

0719

2010

0812

2010

0908

2010

1001

2010

1025

2010

1126

2010

1220

2011

0113

2011

0206

2011

0302

2011

0325

2011

0420

2011

0515

2011

0609

2011

0705

2011

0728

2011

0821

2011

0913

2011

1011

2011

1103

2011

1127

2011

1221

2012

0118

2012

0210

2012

0305

2012

0328

2012

0422

2012

0516

2012

0608

2012

0702

2012

0725

2012

0817

2012

0911

2012

1004

2012

1104

2012

1128

2012

1221

2013

0116

2013

0210

2013

0305

2013

0328

2013

0422

2013

0515

2013

0630

2013

0723

2013

0825

2013

0917

2013

1011

2013

1104

2013

1128

"TOPS" NET Daily % Returns with associated 20 day average of those returns20 day Average % Net Return 0.62 %Worst 20 day average Return - 7.94 %

-15.95% -15.64%

-11.72% -11.56%

-9.85% -9.54% -9.15%-8.15%

-6.46% -6.31%

4.12%

0.47%

-2.10%

-4.56%

-0.58%

1.63%2.10%

-0.01%

-3.01%

4.55%

-20%

-15%

-10%

-5%

0%

5%

10%

200811 200810 200902 200901 200809 201005 201205 200806 201109 201108

S&P 500 TOPS

S&P 500 Index worst 10 Months with corresponding "TOPS" SYSTEM Net PerformanceOver the past six years, the average performance of all negative months for S&P 500 Index was -5.83% while "TOPS"

performance average of all negative months over same time period was a mere -1.99 %

S&P 500 average over worst 10 months -10.43 %"TOPS" same period 0.26 %

0

0.5

1

1.5

2

2.5

3

TOPS S&P 500

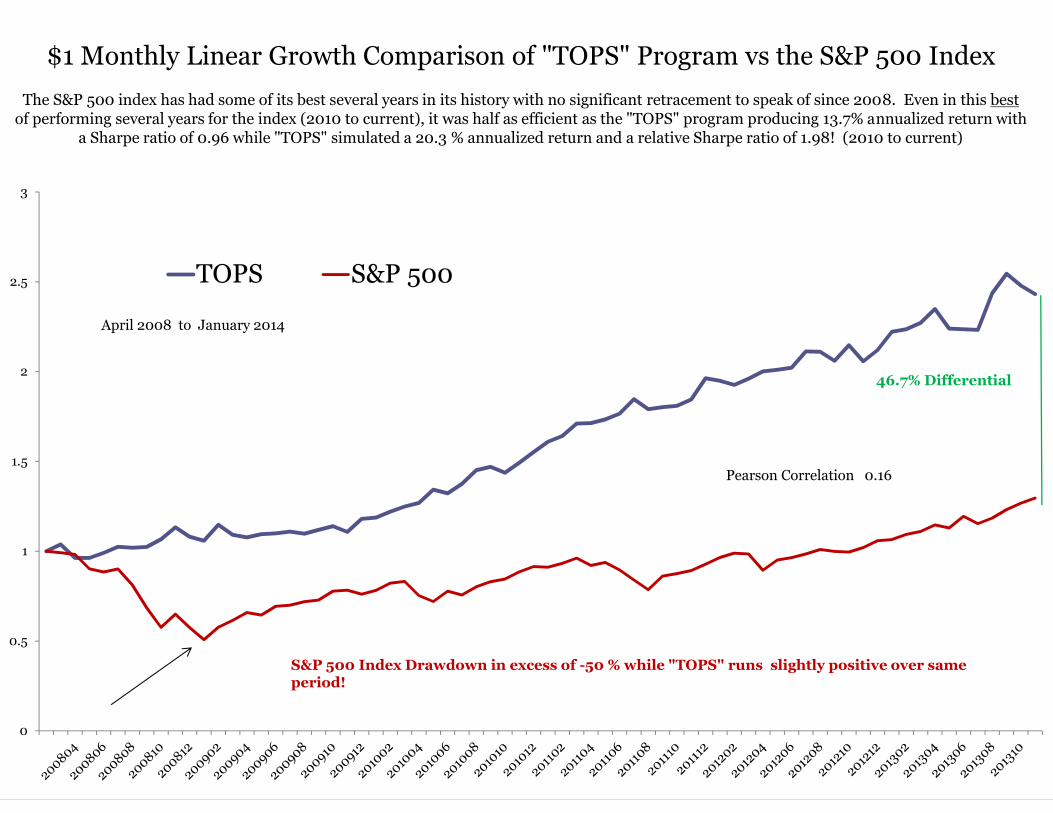

46.7% Differential

Pearson Correlation 0.16

$1 Monthly Linear Growth Comparison of "TOPS" Program vs the S&P 500 IndexThe S&P 500 index has had some of its best several years in its history with no significant retracement to speak of since 2008. Even in this best

of performing several years for the index (2010 to current), it was half as efficient as the "TOPS" program producing 13.7% annualized return witha Sharpe ratio of 0.96 while "TOPS" simulated a 20.3 % annualized return and a relative Sharpe ratio of 1.98! (2010 to current)

S&P 500 Index Drawdown in excess of -50 % while "TOPS" runs slightly positive over sameperiod!

April 2008 to January 2014

10

y = 0.3101xR² = 0.0255

-20%

-10%

0%

10%

20%

-20% -10% 0% 10% 20%

Scattergram Plot of "TOPS" Program Net Monthly Returns vs. S&P 500April 2008 to January 2014

"TOPS" PROGRAM X AXIS

S&P 500 Index Y AXIS

-

0.5

1.0

1.5

2.0

2.5

2008

0409

2008

0512

2008

0613

2008

0716

2008

0818

2008

0919

2008

1022

2008

1124

2008

1228

2009

0130

2009

0304

2009

0406

2009

0510

2009

0611

2009

0714

2009

0816

2009

0917

2009

1020

2009

1122

2009

1224

2010

0128

2010

0302

2010

0404

2010

0506

2010

0608

2010

0711

2010

0812

2010

0914

2010

1017

2010

1118

2010

1221

2011

0124

2011

0225

2011

0330

2011

0503

2011

0605

2011

0707

2011

0809

2011

0911

2011

1013

2011

1115

2011

1218

2012

0124

2012

0226

2012

0329

2012

0501

2012

0603

2012

0705

2012

0807

2012

0909

2012

1011

2012

1113

2012

1216

2013

0120

2013

0221

2013

0326

2013

0429

2013

0531

2013

0703

2013

0805

2013

0906

2013

1009

2013

1111

2013

1213

S&P 500 0.15

US 30 Yr Bond 0.07

Composite Stocks and Bonds 60/40 0.23

TOPS 1.22

Stock/Bond/TOPS Combination 50/30/20 0.46

Growth Profile of Stock and Bond Asset Classes, related Combinationsand risk adjusted by Sharpe Ratio

2008 to 2014

Risk Management and Assumptions

• General information such as net asset value, portfolio composition and risk budgeting are a startingpoint of measuring risk. End of day equal reset of NAV also used on a per million basis per market.This was done to not permit one market to gain or lose too much versus another market which couldsignificantly outperform or underperform.

• Used a $10 per round turn charge per contract as well as $10 per round turn charge for any chargesincurred on spreads from one contract month to the next.

• 1.0 % management fee charged at 1%/12 months. 20% incentive fees charged per month on newportfolio equity highs only. No portfolio risk adjustments were made although this could beaccommodated for managed accounts hoping to produce higher or lower risks.

12

* Parameter selection

One of the biggest challenges in financial engineering; when utilizing simulation constructs to measure future outcomes;is how to avoid fitting the data. The importance of this critical error must be avoided at all cost. Transparency of thecode is one way to reassure some, but even in those situations does the institution validate the concept properly, and notjust its risk attributes?

While constructing "TOPS", much thought was given to these important issues. Based on my own experience in thisindustry, I am keenly aware of the reluctance of financial firms to even consider models presented to them that are basedon simulation, regardless of their merit. Although I don't necessarily disagree with this philosophy, in today's world ofalgorithmic trading; a non-fitted quantitative strategy; that utilizes simple risk/reward rules; that is developed, presentedand understood properly; found to be blindly robust across multiple asset classes should bear some merit. Determininga robustness of signal generation is a science all to itself. It can be very time consuming and to be frank, it is still anassumption that the future will be similar to the past. Trading system evaluation expertise and the related processes usedtoday are scarce and most concentrate on the risk attributes of a particular strategy more than the efficacy of the strategyitself.

(continued)

Engineering & Testing Procedure

13

Parameter Selection Continued:

In the attempt to address any fitting of data and a possible misrepresentation of results, I decided to use a cross sample ofall possible parameters in a population universe defined only by time. (1 to 7 days) I have already described what thegeneral premise that the signal generator looks for…….so the simplicity of the two parameter efficacy of the "TOPS" signalgenerator can also be measured.

The "TOPS" signal generation method looks for targets of opportunities utilizing two parameters. The first parameter isTime/Price(t). Utilizing short-term price action, I began to look at moving TIME/PRICE windows (t’) beginning with aone-day view out to one-week, stepping every 5 hours. That is the complete population of possible selections. As this is ashorter term trading model, to go out further would begin to correlate us to the longer-term market trend so I avoidedgoing out any further than one-week.

The second parameter is Time/Volatility(v) which I call vertical significance or y-axis relevance. Evaluated by (t’) themoving windows of prices, relevant targets of entry and targets of exit are determined by the scalable parameter ofvolatility. So beginning with half or (0.50 * (v’) ) in an associated moving window of time/price and extrapolating out to(1.0 * (v’) ) on the moving time/price window, I documented and averaged all the outcomes.

The multi-parametric results of stepping wide and utilizing *ALL parameter sets as viable trading options are on the nextpage of this brief document. As you can see, there were fluctuations in profitability by shift but overall the trading rulesshow positive results. *ALL of the statistical metrics exhibited in this document are the average of the entireuniverse of tested parameters. Some parameter pairs performed better than others and some worse as is expected.

There are certainly ways to determine which parameter sets overlapped others and muted the overall upside performancebut for the sake of producing a pure signal generation process undeterred by data fitting, *I have used them all.Bootstrapping techniques and Monte-Carlo simulations would also exhibit similar Risk/Return attributes.

* Certainly ALL is relative. Using all selections in the possible universe would produce many thousands of parameter sets and would theoretically produce very similar results towhat is presented here.

$0.8

$1.3

$1.8

$2.3

$2.8

$3.3

2008

0408

2008

0509

2008

0610

2008

0711

2008

0812

2008

0912

2008

1014

2008

1114

2008

1216

2009

0116

2009

0217

2009

0320

2009

0421

2009

0522

2009

0623

2009

0724

2009

0825

2009

0925

2009

1027

2009

1127

2009

1229

2010

0129

2010

0302

2010

0402

2010

0504

2010

0604

2010

0706

2010

0806

2010

0907

2010

1008

2010

1109

2010

1210

2011

0111

2011

0211

2011

0315

2011

0415

2011

0517

2011

0617

2011

0719

2011

0819

2011

0920

2011

1021

2011

1122

2011

1223

2012

0124

2012

0224

2012

0327

2012

0427

2012

0529

2012

0629

2012

0731

2012

0831

2012

1002

2012

1102

2012

1204

2013

0104

2013

0205

2013

0308

2013

0409

2013

0510

2013

0620

2013

0722

2013

0822

2013

0923

2013

1024

2013

1125

2013

1226

30-.5 30-.6 30-.7 30-.8 30-.9 45-0.50 45-0.60

45-0.70 45-0.80 45-0.90 60-0.50 60-0.60 60-0.70 60-0.80

60-0.90 90-0.50 90-0.60 90-0.70 90-0.80 90-0.90 COMPOSITE

Multi-Parameter Growth Simulations – One day to One week time frameApril 2008 to January 2014

1200

1220

1240

1260

1280

1300

1320

2008

0811

2008

0811

2008

0812

2008

0812

2008

0812

2008

0813

2008

0813

2008

0813

2008

0814

2008

0814

2008

0815

2008

0815

2008

0817

2008

0818

2008

0818

2008

0819

2008

0819

2008

0819

2008

0820

2008

0820

2008

0820

2008

0821

2008

0821

2008

0822

2008

0822

2008

0824

2008

0825

2008

0825

2008

0825

2008

0826

2008

0826

2008

0827

2008

0827

2008

0827

2008

0828

2008

0828

2008

0828

2008

0829

2008

0829

2008

0901

2008

0901

2008

0902

2008

0902

2008

0902

2008

0903

2008

0903

2008

0904

2008

0904

2008

0904

2008

0905

2008

0905

2008

0907

2008

0908

2008

0908

2008

0909

2008

0909

2008

0909

2008

0910

2008

0910

"ES" - Mini S&P 500 Monthly Scale Trade Examples60 min chart

Kick out of all possible long positionsmust wait for significant rally from new lows tore-evaluate future entry

1820

1825

1830

1835

1840

1845

1850

1855

1860

1865

1870

2013

1023

2013

1023

2013

1023

2013

1023

2013

1023

2013

1024

2013

1024

2013

1024

2013

1024

2013

1024

2013

1024

2013

1024

2013

1024

2013

1025

2013

1025

2013

1025

2013

1025

2013

1025

2013

1025

2013

1027

2013

1027

2013

1028

2013

1028

2013

1028

2013

1028

2013

1028

2013

1028

2013

1028

2013

1028

2013

1029

2013

1029

2013

1029

2013

1029

2013

1029

2013

1029

2013

1029

2013

1029

2013

1030

2013

1030

2013

1030

2013

1030

2013

1030

2013

1030

2013

1030

2013

1030

2013

1031

2013

1031

2013

1031

2013

1031

2013

1031

2013

1031

2013

1031

2013

1031

"ES" - Mini S&P 500 Detailed Week Trade Examples60 min chart

+ are buys for example chosen parameter- are exits for example chosen parameter

trades are not numbered to match up whichbuy and exit is affiliated

Conclusion

To summarize, the “TOPS” signal generator is a valid and reasonably simple process where neither parameter fitting norany type of learning, walk-forward process is needed to reveal very good results.

This signal generator and basic portfolio was also run over the same six year period on multiple financial instrumentsincluding currencies, metals, commodities, energy and individual stocks with positive and interesting results. Theseadditional tests on other asset classes is always important in my opinion to re-affirm I have NOT fitted a strategy to aspecial circumstance related to just one market.

Trading logic that can exhibit robust positive results across many asset classes is a good indicator that the trading rulesmay have real merit. I also ran these exact trading rules inversely to short markets instead of only buying and exiting.The results were for the most part neutral, but tremendous for those markets which have experienced sustained downcycles in price.

Over the many years of building, reverse engineering and tearing apart trading strategies such as Trend Following,Momentum, Pattern Recognition, Mean Reversion and High Frequency, I can say with confidence that this “TOPS”trading approach is very solid, would be relatively easy to implement and understand and will hopefully be of interest tosomeone looking for a non-correlated strategy with reasonable capacity.

* Further research can be produced as needed for further evaluation.