total cost of ownership of corporate car fleet · total cost of ownership of corporate car fleet...

TRANSCRIPT

Sommario

Total Cost of Ownership

of corporate car fleet

Prof. Angelo Paletta

Department of Management

Alma Mater Studiorum - Unibo

Sommario

In many companies the budget of the corporate car fleet

represents a significant proportion of the total costs. In this

circumstance, the fleet manager is one of the managerial roles

that is mainly under pressure to reduce costs.

If the fleet manager is not able to propose cost management

strategies for the company’s fleet car park, he might be involved

in huge discussions about cost reduction policies.

In this sense, the course analyzes the Total Cost of Ownership

(TCO) as a fleet management philosophy that allows to get a

systemic vision of total costs and their reasons (drivers).

Summary

From cost analysis to cost management

• Basic assumptions:

– Globally, the last thirty years have been characterized by a

radical rethinking of the traditional methods of cost accounting

– Direct costing and full costing have revealed serious

shortcomings that are the reasons behind wrong managerial

decisions.

– Traditional methods have lost their importance and many

companies have developed new approaches.

– Why those same companies should not use more sophisticated

methods to manage a significant part of their fleet management

costs?

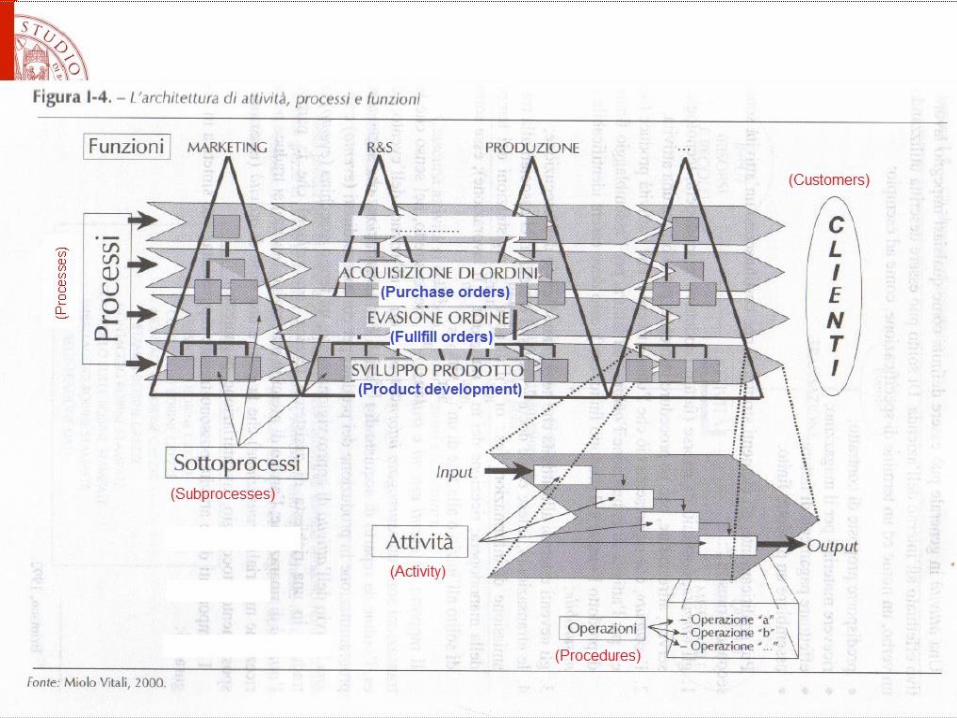

Principles of process management

Principles of process management

• Homogeneity in organizational tasks (from the technical point of view); people with common and specialized skills

• Processes are sets of activities aimed to obtain an “operational objective” for a business (purchase orders, fulfill orders, product development, supply management…)

• Processes cross the formal or legal boundaries of the productive entities

• Processes are assigned to a “cross-functional coordinator” (process owner)

Total cost of ownership

Total cost of ownership

• It’s a particular application of ABC/

ABM to the supply chain processes

• The TCO is a new approach to the

suppliers relationship management in the

procurement processes:

– From a “low price” system to a “low cost”

system

– Assessment dei fornitori in base al TCO e ad altri indicatori

“Low price” suppliers Vs.

“Low cost”suppliers

• “Low price” suppliers – Spot market – Responsibility of purchase managers on the basis of standard cost variance

• Large quantity purchases: discounts • Purchases from “marginal” suppliers in terms of quality, innovation, service • Purchases from suppliers in countries with lower personnel costs • Purchases from suppliers with low cost structure because of their underinvestment in technology and operating systems • Purchases from suppliers with limited engineering capacity

• “Low cost” suppliers – Optimize the “cost of ownership” (Total cost of ownership) – Long term relationships with a few trusted suppliers - Supplier Assessment, based on Tco and other indexes

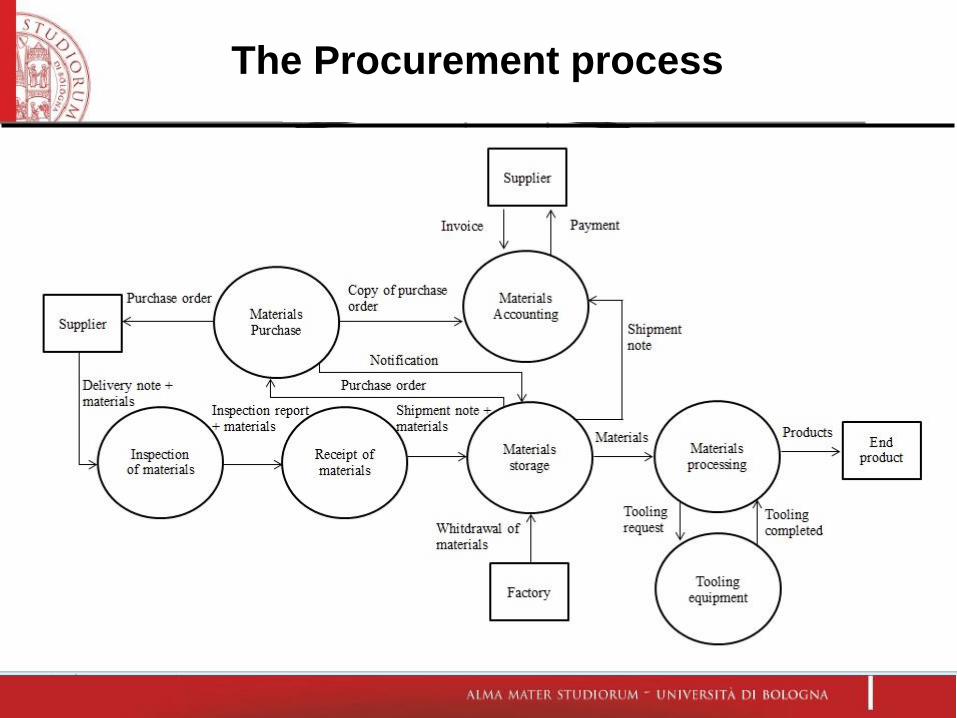

The Procurement process

ABC/ABM of the procurement activities of ACME

Activities Cost of

resources

Cost driver Cost driver

amount

Cost driver

rate

Purchase

requisition

processing

$200,000 Number of

requisition

6,000 $33,33

Vendor

selection

$510,000 Number of

vendors

200 $2,550

Vendor

evaluation

$510,000 Number of

vendors

200 $2,550

Vendor

coordination

$615,000 Number of

vendors

200 $3,075

Materials

processing

$195,000 Number of PO

line items

7,500 $26

Warehouse $84,000 Number of PO

line items

7,500 $11,20

Invoice

processing

$50,000 Number of

invoice

5,000 $10

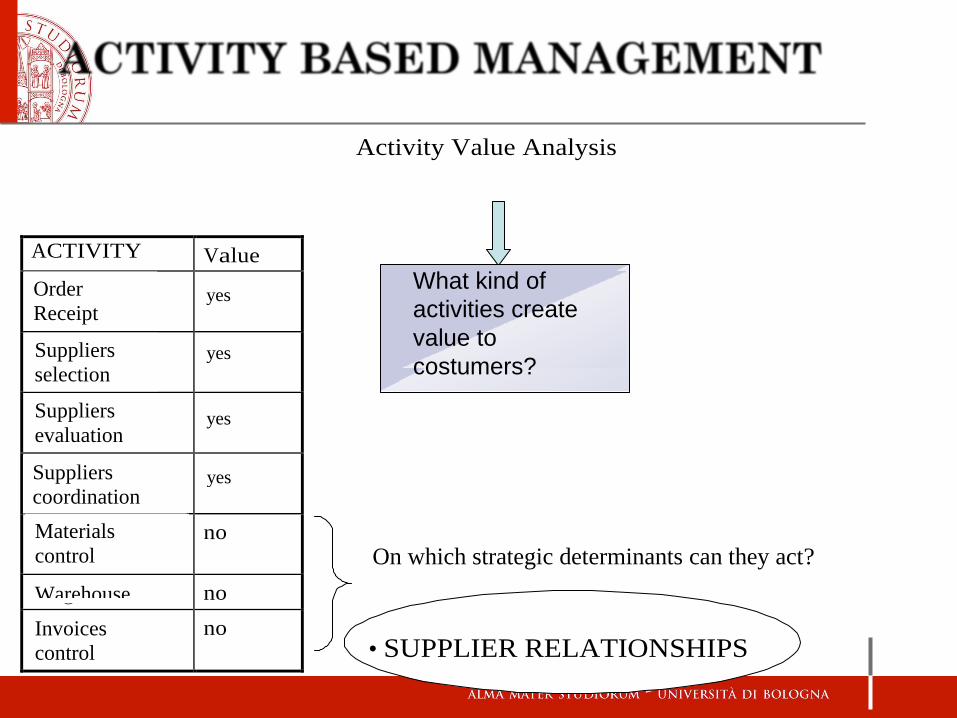

ACTIVITY Value

Ricevimento

ordine

si

Selezione

fornitori

si

Valutazione

fornitori

si

Coordinamento

fornitorI

si

Controllo

materiali

no

Magazzino no

Controllo

fatture

no

Activity Value Analysis

What kind of

activities create

value to

costumers?

On which strategic determinants can they act?

• SUPPLIER RELATIONSHIPS

yes

yes

yes

yes

Order

Receipt

Suppliers

selection

Suppliers

evaluation

Suppliers

coordination

Materials

control

Warehouse

Invoices

control

New relationships with suppliers affect the cost

driver and the business costs

• Number of suppliers

• Number of control over the

goods

• Number of orders

• Number of invoices

• Number of inspections on invoices

Consolidation of

relationships with a few

suppliers to increase

confidence;

Development of a supplier quality certification program to remove post-receipt controls

Do cumulative orders, and

not fragmented;

Implementation of corporate

credit card for small orders

REDISIGN PROCESS

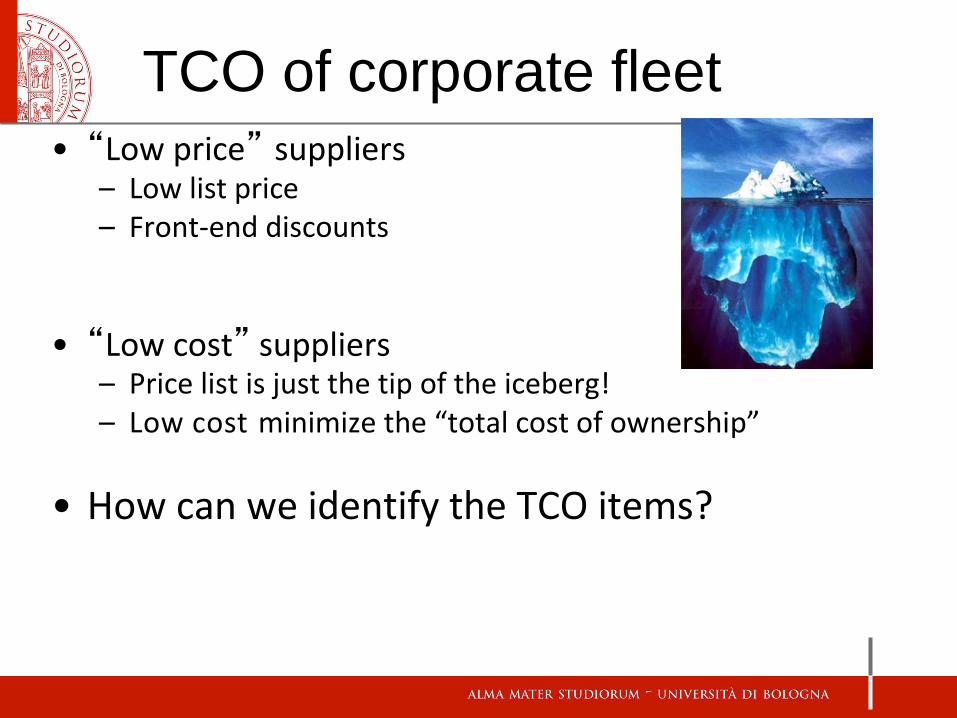

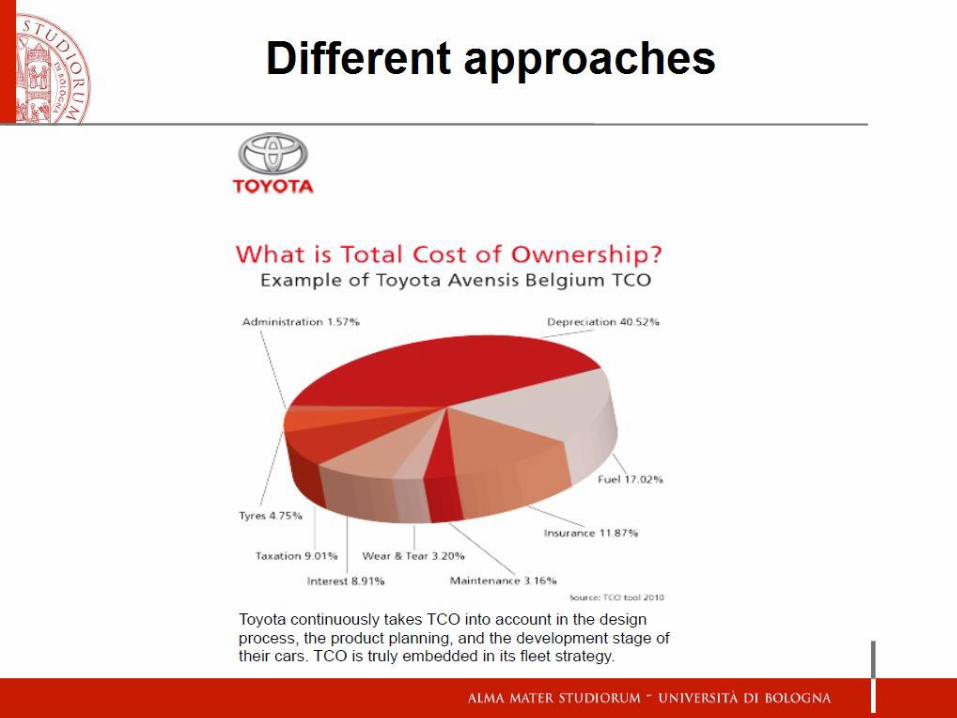

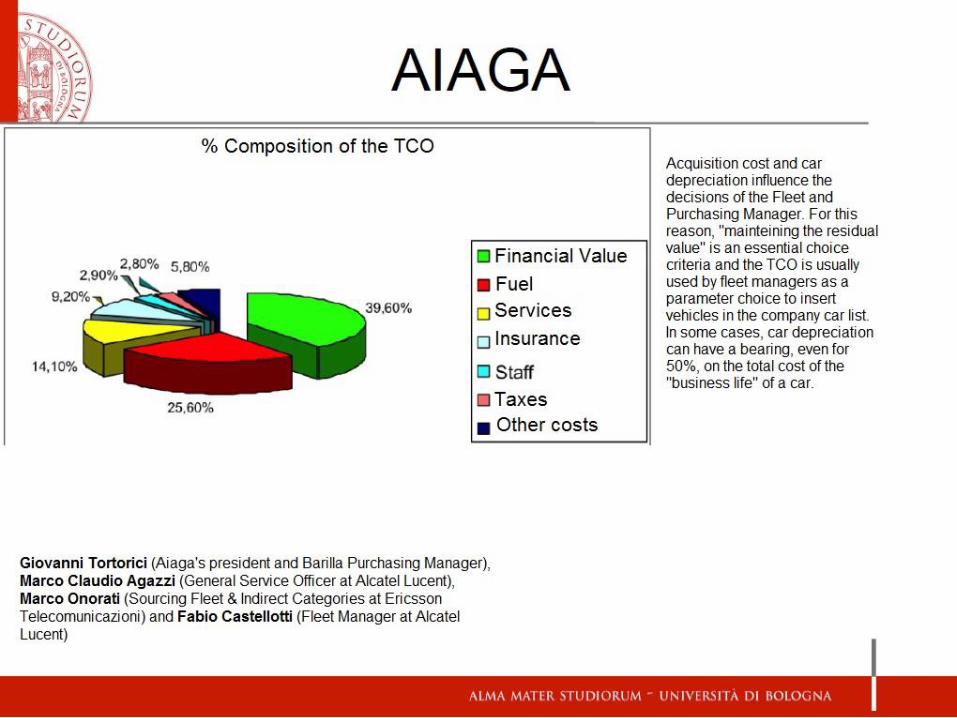

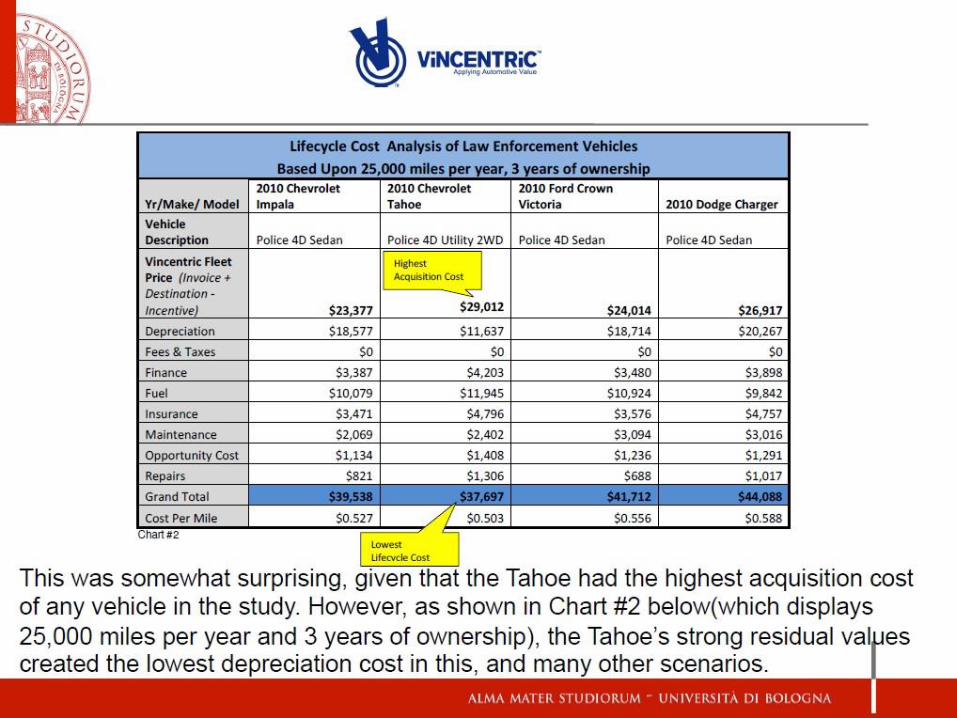

TCO of corporate fleet

• “Low price” suppliers – Low list price – Front-end discounts

• “Low cost” suppliers – Price list is just the tip of the iceberg! – Low cost minimize the “total cost of ownership”

• How can we identify the TCO items?

TCO of corporate fleet

• Fleet’s life cycle

– Procurement requests process – Suppliers selection and delivery management – Financing capital investment – Operating activities – Maintenance and repair service

– Replacement and Remarketing The TCO can be calculated through an Activity based Costing approach.

The TCO considers both the cost items directly depending by activities (fuel, insurance, taxes, staff, etc.) and also the sale proceeds from the used market (cost reduction)

The value chain of the fleet

How to change the Fleet Manager in a strategic partner

1. Creating a vision

2. Communicating the vision

3. Using new methods of performance management

4. Planning and creating continuous performance improvements

5. Consolidating improvements

6.

Institutionalizing new approaches

TCO and residual values

• From the economic point of view, it’s necessary to distinguish

between purchase price, residual value and operating costs.

• The purchase price is a multi-year cost that goes to the balance sheet.

• The residual value is the difference between the original capitalised

cost and amortization fund at a certain date.

• The operating costs are costs that pass through the profit and

loss account:

– According to nature: depreciation of goods of property, financial

expense/rental-leasing fees; fuels, maintenance and repair, etc.

– According to assignment procedures: direct costs vs indirect costs

– According to costs behavior: variable costs, fixed costs, semi-fixed costs and semi-variable costs

– Ordinary and extraordinary components (gains and losses)

TCO and residual values

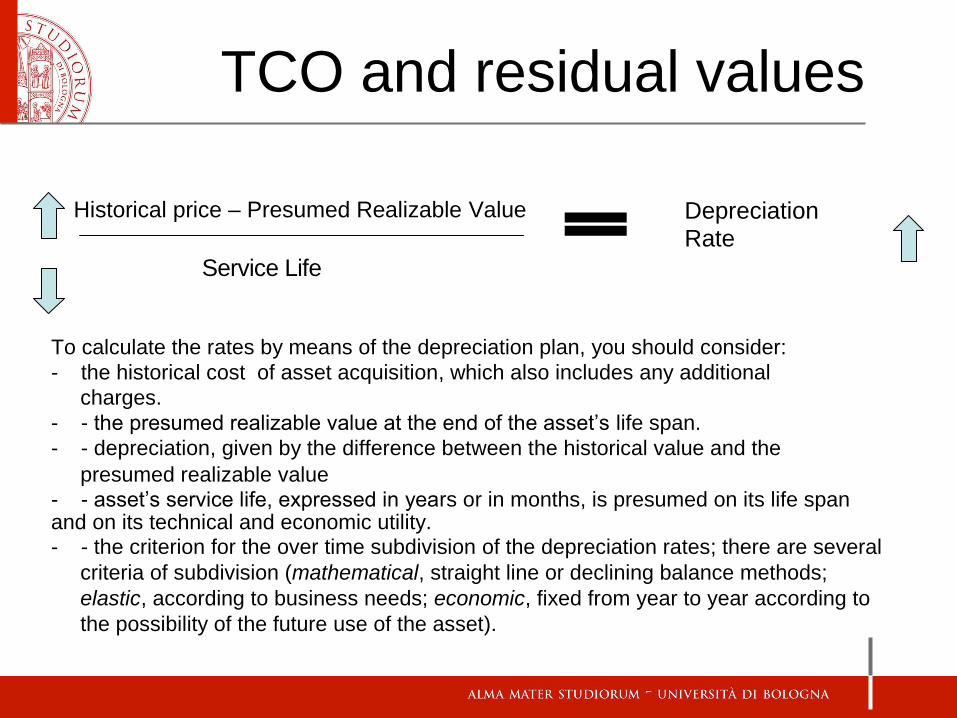

Historical price – Presumed Realizable Value

Service Life

Depreciation Rate

To calculate the rates by means of the depreciation plan, you should consider:

- the historical cost of asset acquisition, which also includes any additional

charges.

- - the presumed realizable value at the end of the asset’s life span.

- - depreciation, given by the difference between the historical value and the

presumed realizable value

- - asset’s service life, expressed in years or in months, is presumed on its life span and on its technical and economic utility. - - the criterion for the over time subdivision of the depreciation rates; there are several

criteria of subdivision (mathematical, straight line or declining balance methods;

elastic, according to business needs; economic, fixed from year to year according to

the possibility of the future use of the asset).

TCO management

• The TCO is determined by the costs of the

activities during the product life span:

Acquisition orders – suppliers selection –

contracts administration – operating

activities – maintenance and repair

services – realization of the residual

values.

To manage the TCO costs, it’s necessary

to manage the drivers of the activities

(ABC/ABM)

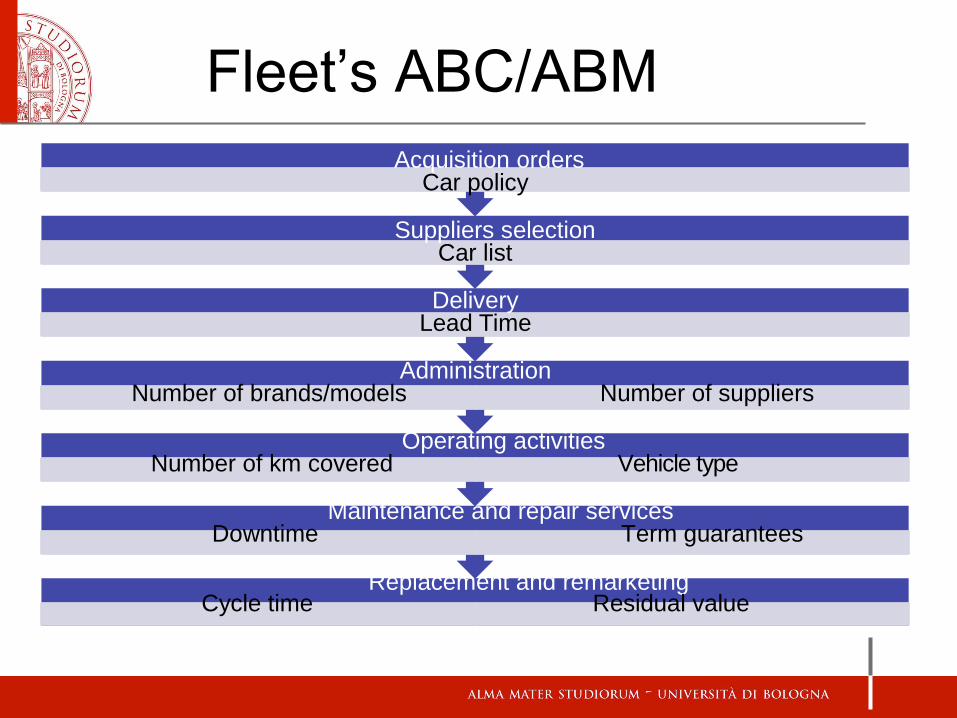

Fleet’s ABC/ABM

Acquisition orders Car policy

Suppliers selection Car list

Delivery Lead Time

Administration Number of brands/models Number of suppliers

Operating activities Number of km covered Vehicle type

Maintenance and repair services Downtime Term guarantees

Replacement and remarketing Cycle time Residual value