trade in intermediate inputs and trade facilitation in ... · siope v. ‘ofa and stephen karingi*...

TRANSCRIPT

1

Trade in Intermediate Inputs and Trade Facilitation in Africa’s Regional

Integration

Selected Paper for Presentation in the African Economic Conference, 28-30 October 2013,

Johannesburg, South Africa.

Siope V. ‘Ofa and Stephen Karingi*

28 October 2013

Abstract:

Despite concerted efforts, Africa’s regional integration process has encountered delays. Since the

third stage of the Abuja Treaty in 2008, piece meal progress has been observed. It therefore begs a

difficult but relevant question: why is the regional integration process stalling? The conventional

answer lies in challenges such as inadequate financial resources and infrastructure for trade among

others. However, this paper proposes an approach to regional integration refocused on resource-based

industrialisation. A recent UNECA survey found that several Member states believed that regional

integration does not contribute significantly to job creation and regional value chains. Resource-based

industrialisation could contribute to job creation and inclusive growth if properly managed. We

examine the industrialisation level in Africa using Balassa’s Revealed Comparative Advantage

Indexes based on the BACI dataset. Further, we evaluate Kenya’s trade in intermediate inputs vital for

industrialisation, using an input-output table analysis on production, based on GTAP 8 dataset.

Regional analyses of five African Regions triangulated the Kenya results. The analysis finds that

while the level of industrialisation is heterogeneous among African economies, the overall level is

low. Also, in the case of Kenya, the manufacturing sector spends significant amounts on imported

intermediate inputs from the manufacturing sector critical to all four major industry categories (57 per

cent for food, 79 per cent for agriculture, 15 per cent for energy and mining, 83 per cent for

manufacturing and 57 per cent for services), demonstrating the importance of trade facilitation

measures to ensure timely and cost-effective sourcing. Moreover, results from five African regions

triangulate this finding by suggesting that manufacture, energy and mining imported intermediate

inputs together make out 76 per cent of total imported intermediate inputs for production in Africa.

* Mr. Stephen Karingi is the Director, of the Regional Integration and Trade Division, UNECA. At the time this

paper was written, Mr. Siope V. ‘Ofa was Associate Economic Affairs Officer, African Trade Policy Centre,

Regional Integration and Trade Division, UNECA. Mr. Siope V. ‘Ofa is now working for UNESCAP. The

views expressed in this paper are the authors’ own and may not necessarily reflect the position of the United

Nations Economic Commission for Africa. Any mistakes or omissions are the sole responsibility of the authors.

Maja Reinholdsson and William Davis of the Regional Integration and Trade Division, UNECA is gratefully

acknowledged for the analyses on African Regions section and useful comments on an earlier draft.

2

1. Introduction

Against the backdrop of the global economic and financial crisis in many industrialised

countries and the failure to reach a comprehensive agreement in the WTO Doha round

negotiations, Africa’s regional trade integration has emerged as a crucial instrument for

sustaining economic growth in Africa. Increased intra-African trade and development of

African markets are necessary to serve as a launch pad for enhancing African

competitiveness and its integration with the world economy (ECA et al., 2012).

2. Africa’s Transformative Regional Integration: need for a paradigm shift?

A lot of concerted efforts have been made towards Africa’s regional integration by

African countries, Regional Economic Communities (RECs) and Development partners.

Deeper integration would allow the continent not only to achieve sustained and robust

economic growth but it will also ensure poverty alleviation, enhanced movement of goods

and services, infrastructure development and promotion of peace and security within and

between the regions (ECA et al., 2010)

Despite concerted efforts, Africa’s integration process has encountered delays. Since the

beginning of the third stage of the Abuja Treaty in 2008—creation of free trade areas and

custom unions in each REC with a deadline of 2017—piecemeal progress has been observed.

While the political commitment at the continental level is undeniable, implementation at the

country level is noticeably lacking. In January 2012, the AU Summit of Heads of

Governments and States endorsed both fast -tracking of the establishment of an African

Continental Free Trade Area by the indicative date of 2017 and boosting of intra-African

trade through the implementation of a comprehensive action plan1 towards encouraging

member states to fast-tracking and boosting intra-African trade. With the deadline for this

third stage looming in four years time, and extremely limited progress on the ground, one

needs to ask why Africa’s regional integration process is stalling.

The conventional answer lies in the challenges that member states and RECs encounter in

their efforts towards negotiating free trade areas (FTAs) and custom unions. ECA et al.,

(2010 and 2012) provide a comprehensive account of the specific challenges for each REC

that are hindering the regional integration process within their respective regions. The

1 Visit African Union ‘Action Plan for Boosting Intra-African Trade’ for further information,

http://www.au.int/en/sites/default/files/Action%20Plan%20for%20boosting%20intra-African%20trade%20F-

English.pdf

3

challenges range from inadequate financial resources, inadequate infrastructure for trade,

high non-tariff barriers, lack of harmonisation of rules of origin among member countries,

and conflict and political instability (see ECA et al., 2010 and 2012 for detail discussions of

these challenges). UNECA recently conducted a regional survey (UNECA, 2012) to gauge

the progress in mainstreaming regional integration programs, protocols, decisions and

activities into national development strategies of member states. Based on the 5 geographic

regions in Africa—North, West, Central, East and South—32 African economies were

selected of which 69 Government Ministries responsible for regional integration were

interviewed or given structured questionnaires. The general findings of the survey noted that

“one of the main challenges underpinning the acceleration of Africa’s continental integration

is the limited or lack of progress in mainstreaming regional integration agreements into

national development plans and strategies” (UNECA, 2012).

In particular, the survey noted that although the AU Assembly requested member states to

establish a focal point—Government Ministry—in charge of Regional Integration, only 8

member states have established such a dedicated Government body. The survey report also

highlighted three other gaps worth noting. First, dissemination of information on regional

integration decisions to national stakeholders was lacking and this contributed to the lack of

implementation and ownership. Second, a noticeable number (43 per cent) of respondents

indicated that the level of consultation between the coordinating ministry or entity and the

private sector and civil society was weak. Third, the financial costs in terms of multiple

memberships2 in the RECs increases in proportion to number of memberships. Further,

multiple memberships stretch financial and human resources in term of the need for

representation to different negotiation meetings, and thus coordination and dissemination of

information become real challenges.

However, one of the findings in the regional survey prompted us to look beyond the

conventional answers into the question of why Africa’s regional integration stalling. In

particular, respondents were asked about the significance of regional integration to different

sectors of the economy. The majority of respondents indicated that regional integration does

not significantly contribute to job creation and creation of regional value chains 58 per cent

and 54 per cent respectively (UNECA, 2012). Although anecdotal, these figures do provide

2 The report gave an example of the projected financial costs for Swaziland in 2012 which amounted to around

USD3.5 million on annual contribution, contribution to COMESA Court of Justice and COMESA Fund.

Swaziland was also expected to pay similar costs to SADC, as a member of that grouping (UNECA, 2012).

4

first-hand evidence of the perspectives of selected Government officials directly involved

with implementing regional integration in these member states. Specifically, although

renewed political commitments and concerted efforts at the continental level have been made

towards the regional integration process, doubts remains in several member states about the

impact of regional trade integration on job creation. Indeed, there are good grounds for their

reservations.

Even the literature on the link between trade and unemployment is undecided. Felbermayr

et al (2011) empirically tested the relationship between rate of unemployment and openness

over two groups of countries—20 OECD countries and 63 countries—over the period 1970 to

2000. They concluded that over time, higher trade openness decreases unemployment3 for

both groups. Also, Mashayekhi et al (2012) using the Global Trade Analysis Project (GTAP)

model analysed the effects of regional integration in the Southern African Development

Community (SADC) and employment. Their findings indicate that regional trade

liberalisation among developing countries can lead to increasing or decreasing demand for

labour intensive goods and hence the demand for labour can increase or decrease. Hence, a

flexible scenario— where surplus unskilled labour is available and there is no change in the

level of skilled labour4 would result in greater welfare gains since real wages are fixed and an

increase in demand for labour is assumed to be totally accommodated by changes in

employment rather than in real wages.

In contrast, Chinembiri (2010) found that the derived labour demand in the primary sector

(agriculture, fishery forestry and mining activities) and the secondary (manufacturing,

utilities and construction) industries have been impacted negatively by increased imports—

implying trade liberalisation. Another country-study by Rattso and Torvik (1998) of

Zimbabwe found that the drastic trade liberalization implemented in the early 1990s resulted

in a contraction in output and employment that was accompanied by a sharp increase in

imports and a rising trade deficit. Furthermore, study on Morocco by Currie and Harrison

(1997) found that the substantial trade liberalization implemented during 1984-1990 did not

have very strong employment effects.

Here lies a conceptual proposition for a paradigm shift. While we continue to support

Africa’s regional integration agenda, we should ask ourselves the difficult but relevant

3 Reduction in aggregate unemployment is primarily due to reduction in high-skilled workers unemployment.

4 Real wages of unskilled labour is exogenous.

5

question of why the regional integration process (despite concerted efforts) is stalling in

several countries. We have discussed one key potential reason above which is the linkages

between regional integration (including trade liberalisation) and employment. However, we

propose a transformative approach to regional integration that would focus on the key role of

trade facilitation for trade in intermediate inputs that are crucial for industrialisation in Africa.

A transformative industrialisation will not only contribute to create jobs but it could also

contribute to inclusive growth if properly managed. Hence, perhaps Africa’s regional

integration agenda needs to be recalibrated to incorporate a transformative dimension thereby

ensuring that any activities planned incorporate inclusive growth and most importantly job

creation.

The argument for a paradigm shift towards prioritising industrial transformation in

Africa’s regional integration agenda will continue in the next section of this paper, which will

be a discussion on the links between the identification of key industry sectors

competitiveness (measured by revealed comparative advantage index) and regional

integration.

3. Transformative regional trade integration and industrialisation in Africa

Africa is increasingly focusing on regional integration as a strategy for achieving

sustainable economic growth as there is consensus that by merging its economies—to create

one big market—and pooling its capacities—thereby sharing costs on public infrastructures

crucial for development—the continent can overcome its daunting development challenges

(ECA et al., 2010)5. This agenda as mentioned earlier has intensified in the last couple of

years with several continental agreements on boosting intra-African trade made. The

importance of the regional integration agenda is more relevant today than ever, particularly in

the context of current global economic difficulties. Building resilience through regional

integration and trade provides a buffer for most small fragmented African economies.

To examine in which industry sectors African countries have comparative advantage, we

compute a normalised revealed comparative advantage index (NRCA)6 of each African

country to the world. Using trade statistics, this computation allows us to identify potential

industry sectors of comparative advantage when African economies trade with each other by

5 Please refer to ECA et al., (2010) for detailed discussions on the links between regional integration (and trade)

and sustainable economic growth in Africa. 6 Please refer to Balassa (1965) for details on calculating the RCA index, and also to Laursen (2000) for

developing a simple normalisation process of RCA.

6

comparing the ratio of a particular product (or sector) in a country’s exports, to its share in

total intra-African trade, as follows:

Where,

- country i’s exports of product or sector s,

- country i’s total exports,

- African total exports of product or sector s,

- African total exports,

(1)

(2)

We use the BACI dataset developed by CEPII, provides bilateral values and quantities of

exports at the HS6-digit product disaggregation, for more than 200 countries over 5,000

products based on input data from the United Nations Statistical Division (COMTRADE

database). Four African economies were included with Southern African Customs Union

(SACU)7 as one economy. Two years (2000 and 2011) were merged to allow for comparison

over time.

Intuitively, if the share of a particular commodity in a particular country’s exports is high

relative to the commodity’s share in total intra-African trade, then the country has a revealed

comparative advantage in the commodity in question. Hence, when interpreting an NRCA,

the index ranges from -1 to 1 with the value of 0 as the ideal index (NRCA). Indexes

between 0 and 1 are considered revealed comparative advantages and vice versa. Looking at

the overall picture of revealed comparative advantage (normalised) in Africa for 2000 and

2011, five important trends stands out. First, we find 27 African economies—the biggest

group by Broad Economic Categories (BEC) in 2011—have NRCA in BEC8 1 (agriculture

and food). BEC 1 is the only category that African economies showed an average positive

NRCA index to world with (0.014) in 2011. This implies that the agriculture and food

industry is quite competitive in most African countries.

7 Members include Namibia, Lesotho, Botswana, South Africa and Swaziland.

8 1 - Food and beverages (11 – Primary & 12 – Processed); BEC 2 - Industrial supplies not elsewhere specified

(21 – Primary & 22 – Processed); BEC 3 - Fuels and lubricants (31 – Primary & 32 – Processed); BEC 4 Capital

goods (except transport equipment), and parts and accessories thereof (41 - Capital goods (except transport

equipment) & 42 - Parts and accessories); BEC 5 - Transport equipment and parts and accessories thereof (51 -

Passenger motor cars, 52 – Other & 53 - Parts and accessories); BEC 6 - Consumer goods not elsewhere

specified (61 – Durable, 62 - Semi-durable & 63 - Non-durable); and BEC 7 - Goods not elsewhere specified

(includes, among other commodities, a range of military equipment, postal packages and special transactions

and commodities not classified according to kind).

7

Second, the NRCA index for 2011 indicates that a substantial number9 of African

economies—27 African economies in 2000— had a positive NRCA index, with indices for

the said countries ranging from (0.006) to (0.448), while in 2011 19 African economies had a

positive NRCA index for BEC 2 (industrial supplies not supplied elsewhere), with indices for

these countries ranging from (0.116) to (0.458). BEC 2 economies were the second highest

group with positive NRCA index among the 7 BEC categories. While it reflects

competitiveness in trading in industrial supplies among African countries, it also provides

further support towards African economies trading in more sophisticated goods compared to

trading with external partners. For example, it is estimated that intra-African exports in 2011

totalled around USD 69 million, 36 per cent of this amount—the highest of all product

categories—was export in industrial supplies (BEC 2) (see Table 1).

Table 1

Third, our estimation shows that Somalia held the ideal10

NRCA index for BEC 1

(0.030) and BEC 6 (0.049) in 2011 (see Figure 1). In the case of BEC 1, Somalia has shown a

significant improvement from an NRCA index of 0.649 in 2000 to 0.030 in 2011, and

similarly for BEC 6, an index of -0.510 in 2000 compared to 0.049 in 2011. For the other

BECs, in 2011 Senegal hold the ideal NRCA index for BEC 2 (0.116), Cote d’Ivoire for BEC

3 (0.072), Madagascar for BEC 4 (0.065) and Tunisia for BEC 5 (0.005).

9 27 African economies in 2000 had positive NRCA index (ranges from 0.006 to 0.448) while 19 African

economies had a positive NRCA index in 2011 with NRCA index ranging from 0.116 to 0.458. BEC 2

economies were the second highest group with positive NRCA index among the 7 BEC categories. 10

Closest index value to zero.

BEC USD (000) % Share

1 9,134,432.00 13.1

2 25,101,208.00 36.0

3 21,932,458.00 31.4

4 5,396,058.50 7.7

5 3,564,832.75 5.1

6 4,620,937.00 6.6

7 32,800.38 0.0

Total 69,782,726.63 100

Source: Author's estimation based on BACI Dataset (CEPII), 2013.

Intra-African Exports by BEC, 2011

8

Figure 1

Fourth, our estimation identifies the potential for African economies in each of the

broad economic categories to improve revealed comparative advantages. These are African

economies that showed revealed comparative disadvantages in each BEC, but approaching

the ideal NRCA index of zero. The top 5 potential African countries for each BEC are listed

in Table 2. Cetris paribus, these identified African economies are expected to progress next

to the revealed comparative advantages in the respective broad economic categories.

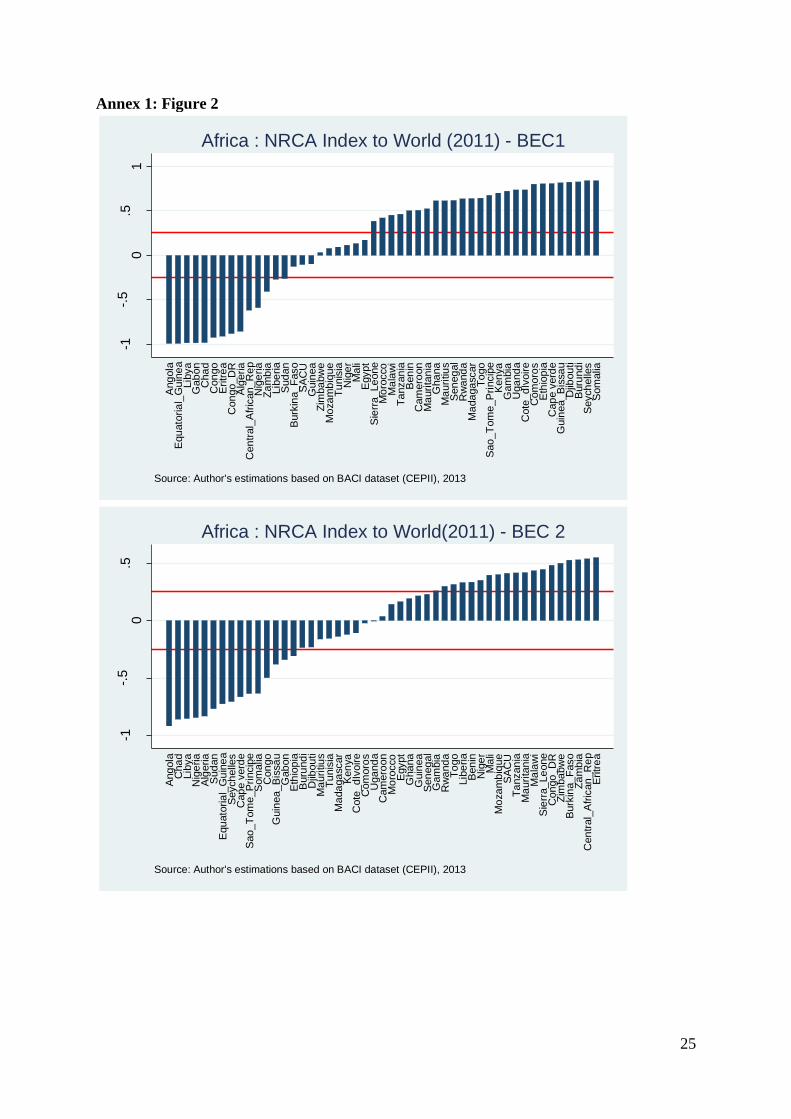

Fifth, when computing African countries’ NRCA indexes to the world, we find a

different set of countries holding the top spots (see Figure 2, Annex 1). For example, for BEC

1, we find Zimbabwe (0.033), Mozambique (0.077) and Tunisia (0.094) ranking closest to the

ideal NRCA index in 2011, with 32 African counties holding a positive NRCA index. In the

case of BEC2, we find that Cameroon (0.037), Morocco (0.141) and Egypt (0.164) ranked the

highest with 16 countries holding positive NRCA indexes, while Gabon (0.208), Republic of

Congo (0.245) and (0.255) ranked the highest among African countries in BEC 3 with only 9

countries holding a positive NRCA.

4

5

1

6

2

-1

-.5

0

.5

1

NR

CA

200

0

-1 -.5 0 .5 1NRCA 2011

Somalia : BEC1 & 6

34

5

21

6

-1

-.5

0

.5

1

NR

CA

200

0

-1 -.5 0 .5 1NRCA 2011

Senegal : BEC 2

54

2

31

6

-1

-.5

0

.5

1

NR

CA

200

0

-1 -.5 0 .5 1NRCA 2011

Cote d'Ivoire:BEC 3 & 7

23

4

5

1

6

-1

-.5

0

.5

1

NR

CA

200

0

-1 -.5 0 .5 1NRCA 2011

Madagascar : BEC 4

3

2546

1

-1

-.5

0

.5

1

NR

CA

200

0

-1 -.5 0 .5 1NRCA 2011

Tunisia : BEC 5

Source:Author's estimations based on BACI dataset (CEPII), 2013

Top 5 African Economies - NRCA Index by BEC (2011)

9

Table 2

For BEC 4, Djibouti (0.001), Mali (0.008) and Mauritius (0.028) ranked closest to the ideal

NRCA index, with 15 countries holding positive NRCA indexes while Sierra Leone (0.002),

Gabon (0.003) and Uganda (0.005) ranked closest to ideal NRCA index in BEC 5 (with only

11 countries holding positive NRCA index). For BEC 6, Rwanda (0.066), Tanzania (0.112)

and Uganda (0.143) ranked closest to the ideal NRCA index with 14 countries holding

positive NRCA indexes, while Guinea (0.297), Burundi (0.416), and Cote d’Ivoire (0.451) on

BEC 7 with only 8 countries with positive NRCA indexes. It is worthy to note that Africa

hold an average positive NRCA index (0.139) in BEC 1 to the world (agriculture and food)—

although slightly lower than its average NRCA index in BEC 1 for intra-African trade at

(0.014). The difference in the composition of countries with NRCA indexes when comparing

intra-African trade and trade with the world reflects the nature of trading in Africa with most

African countries trading more in natural resources with the world while another set of

countries focuses on trading in more sophisticated goods among African countries.

Overall, the use of a simple estimation of revealed comparative advantage index allowed

us not only gauge industry sectors’ competitiveness in African economies, but also to identify

future African economies and potential industry sectors deemed useful for policymakers in

prioritising sectors for industrial development. Through this process, we have provided and

-0.028 Zambia -0.115 Eritrea -0.048 SACU

-0.034 SACU -0.124 Uganda -0.441 Seychelles

-0.037 Burkina Faso -0.148 Chad -0.539 Tanzania

-0.080 Togo -0.165 Tanzania -0.559 Kenya

-0.116 Tanzania -0.169 Mali -0.696 Zambia

-0.009 Tunisia -0.036 Kenya

-0.015 SACU -0.051 Morocco

-0.020 Kenya -0.073 Equatorial Guinea

-0.030 Uganda -0.081 Malawi

-0.043 Cameroon -0.094 Congo

-0.234 Libya -0.054 Eritrea

-0.434 Madagascar -0.256 Gambia

-0.451 Niger -0.373 Benin

-0.476 Senegal -0.378 Zimbabwe

-0.488 Kenya -0.380 Malawi

Top 5 African Countries with Potential Industry Development (by BEC), 2011

Source: Author's estimations based on BACI Dataset (CEPII), 2013.

Note: * - Normalised Revealed Comparative Disadvantage in 2011.

NRCD* Index-BEC 1 NRCD* Index-BEC 4 NRCD* Index-BEC 7

NRCD* Index-BEC 2

NRCD* Index-BEC 3

NRCD* Index-BEC 5

NRCD* Index-BEC 6

10

additional justification for a shift in paradigm towards a ‘transformative’ regional integration

agenda for Africa. Industrialisation for transforming each African economy should be at the

heart of a transformative regional integration with a particular focus on the potential for each

industrial cluster identified earlier.

4. Industrialisation, Intermediate Inputs and Trade Facilitation in Africa’s

Transformative Regional Integration

Industrialisation and Intermediate Inputs

Africa’s industrialization has been weak and inconsistent as shown by the share of

manufacturing value added to GDP (1980-2009) which increased marginally in North Africa

(12.6 per cent to 13.6 per cent) but fell from 16.6 per cent to 12.7 per cent in the rest of

Africa (ECA et al., 2013). Africa’s low export diversification and intra-industry trade in

recent years also highlight this weakness. In 2009, Africa lagged behind other major

regions—Europe, the Americas, Asia and the Pacific—in terms of export diversification with

a weighted average of 0.4 in 2009 compared to 0.2 in 199811

, while intra-industry trade was

found to be low at around 10 per cent (average) for Africa, with 32 African economies in a

sample of 49 were below the average with another 8 African economies below 2 per cent

(‘Ofa et al., 2012).

Africa’s dependence on primary commodities provides opportunities and risks for

industrialisation. On the one hand, Africa should capitalise on the abundant resource

endowments and the current commodity price boom to fund its industrialisation efforts;

however, focusing on primary commodities carries the risk of further deindustrialisation (see

ECA et al., 2013 for detailed discussion on this point). A recent report released by ECA et al.,

(2013) advocates that a resource-based industrialisation will yield employment, income and

dynamic benefits provided that the resource processing industries—which should move up

the value chain and develop backward and forward linkages to the commodity sector—are

internationally competitive and well integrated into global value chains. Resource-based

industrialisation via linkage development creates an opportunity to maximise positive

externalities derived from clusters due to agglomeration effects12

of supplier (and therefore

11

Export Diversification using a normalised Hirschman-Herfindahl Index gives values between 1 (export

concentration) and 0 (export diversification). Most industrialised economies have indexes very close to zero. 12

Through knowledge and information flows allowing for firms to adopt new technology. It facilitates

specialisation and clustering lowers entry barriers for small and medium enterprises (ECA et al., 2013).

11

extraction) location and resource-processing industries’ geographical closeness to each other

(ECA et al., 2013).

The resource-based industrialisation path is critical but not sufficient for structural

adjustment from the extraction of primary commodities to a manufacturing-based economy in

Africa. Production activities require two types of inputs. One is primary factor inputs (land13

,

labour and capital) and the second key input is intermediate inputs (different components to

make one product) (Burfisher, 2011). The primary factor-based industrialisation relies more

on Africa’s natural resources for industrialisation and economic transformation. While we are

content with this industrialisation path, we propose that the role of intermediate inputs in the

resource-based industrialisation process should be given equal attention. While some

intermediate inputs may be sourced from within the continent, some may need to be sourced

from outside Africa.

Africa’s trade in the intermediate goods that are required for higher value production has

been limited and this reflects the continent’s lack of industrial transformation and growth

over time. In fact, Africa’s imports of intermediate goods from within Africa have remained

low when comparing 2000 (at 11 per cent share of total imports of intermediate goods from

Africa) and 2011 (12 per cent) (see Table 3). A majority (more than 80 per cent for both

periods) of the intermediate inputs for Africa are imported from outside Africa. These figures

reflect the reality that some of the intermediate inputs crucial for Africa’s industrialization

may not necessarily be available from within the continent, and must therefore be sourced

from outside Africa.

Table 3

To examine the need for intermediate inputs (imported) at the country level, we take the case

of Kenya. In the earlier section, using revealed comparative advantage index, we identified

that Kenya has the potential to further industrialise in BEC 2, 3, 5 and 7. Hence, using an

Specialisation and clustering however is expected at the middle to higher end of the value chain to avoid

specialisation in primary commodities (implying no progress towards industrialisation). 13

Natural resources included.

Africa % Share Africa % Share

Africa 2,083,328.97 11 12,060,903.96 12

Rest of the World 16,118,412.63 89 87,106,994.39 88

World 18,201,741.60 100.0 99,167,898.35 100.0

20112000

Source: Author's estimation based on WITS Database, 2013.

Africa's Intermediate Goods Import (2000 and 2011), USD (000).

12

input output table on production for Kenya based on GTAP 8 dataset, we to analyse the use

of imported intermediate inputs for industries’ production processes14

(see Table 4).

Table 4

Kenya Production Inputs, 2007, (USD millions).

Activities (incl.CGDS)

Sam entry Agri Food NRGM Manuf Services

Commodities total 4742.1 7955.7 2240.5 5179.9 14822.5

Agri Imports 106.7 111.1 0 6.1 1.3

Food Imports 39.3 308.1 4.2 38.1 225.8

NRGM Imports 100.7 59.4 1175.7 182.2 588.4

Manuf Imports 1016.1 710.3 210 1625.1 1756.1

Services Imports 16.8 52.3 24 102 478

1279.6 1241.2 1413.9 1953.5 3049.6

Agri Domestic 886.7 456.4 0 0 0

Food Domestic 614.5 4763 77.3 587.4 3772.8

NRGM Domestic 274.9 110.8 422.1 422.8 691.6

Manuf Domestic 831.3 317.7 95.5 1330.7 1186

Services Domestic 855.1 1066.6 231.7 885.5 6122.5

3462.5 6714.5 826.6 3226.4 11772.9

Factors -total 5702.6 7250.1 638.3 2304.2 11526.66

1 Land 684.2 0 0 0 0

2 UnskLab 4073 1718.9 224.3 1008.5 3406.06

3 SkLab 32.9 331.9 70.3 133.2 2357.3

4 Capital 912.5 5199.3 337.3 1030.4 5763.3

5 NatlRes 0 0 6.4 132.1 0

Factors use taxes- total 91.2 45.6 58.9 89.3 73.2

1 Land 22.8 0 0 0 1

2 UnskLab 22.8 15.2 17.1 28.5 24.7

3 SkLab 22.8 15.2 17.1 28.5 22.8

4 Capital 22.8 15.2 17.1 28.5 24.7

5 NatlRes 0 0 7.6 3.8 0

Sales Tax 0 0 168.3 10.9 -12.1

Total 10535.9 15251.4 2937.7 7573.4 26422.36

(Gross Value of output)

Source: GTAP 8 Note: Sales Tax: Is the sum of private domestic consumption tax and firms domestic purchase

tax

14

The industry activity column accounts of the SAM describe the inputs used in industries’ production

processes while the activity rows accounts show the use of inputs.

13

Each column in the table shows the expenditure by a particular industry—in this case,

agriculture, food, energy and mining (NRGM), manufacturing and services—on intermediate

inputs, factors inputs and taxes. The Kenyan economy (in 2007) utilised the highest inputs for

production on services industries (42 per cent of total intermediate input expenditure)

followed by food (23 per cent) and manufacturing (15 per cent). Service providers spend

around USD 14,823 million on intermediate inputs, followed by food producers with around

USD 7,956 million and manufacturers at USD 5,180 million.

In terms of industries’ spending on imported and domestic intermediate inputs, we find

that the food sector spends 84 per cent on domestic and 16 per cent on imported intermediate

inputs, the agricultural sector spends 73 per cent on domestic intermediate inputs, energy and

mining spends 63 per cent on imported and 37 per cent on domestic, manufacturing spends

38 per cent on imported and 62 per cent on domestic, and services industries spend 21 per

cent on imported and 79 per cent on domestic. From these percentage shares, we find that

imported intermediate inputs are critical in the energy and mining and the manufacturing

sectors. In addition, we find that expenditure on imported intermediate inputs from the

manufacturing sector is critical to all five major industry categories (57 per cent for food, 79

per cent for agriculture, 15 per cent for energy and mining, 83 per cent for manufacturing and

57 per cent for services).

The services industry spends USD14,823 million on production inputs which comprise

USD6,601 worth of service inputs (USD478 million imported and USD 6,122 million

produced domestically), USD 2942 million of manufacturing inputs (USD 1756 million

imported and USD 1186 million domestically produced), and USD 3999 million on food

(USD 225 million imported and USD 3773 million domestic) and USD 1.3 million of

agricultural inputs (USD1.3 million imported). It is worth noting that the services industry

used more imported manufactured inputs (12 per cent of total inputs to the services industry

by value) than domestically produced manufactured inputs (8 per cent)15

. It is also interesting

to note that Kenyan service providers used USD11,527 million of factor inputs (USD3,406

for unskilled labour, USD2,357 for skilled labour and USD5,763 for capital), while paying a

total of USD73 million in taxes on use of factors. However, service providers received

USD12.1 million in subsidies (negative sales tax) to purchase additional intermediate inputs.

15

This ratio of higher imported intermediate inputs in manufacturing compared to domestic is also reflected in

the other major categories of food, agriculture, energy and mining and manufacturing.

14

Moving one step further, we compute an input-output coefficient table (based on Table 4)

for Kenya to evaluate the ratio16

of the respective quantities of intermediate inputs and factor

inputs per unit of output. In other words, the input-output coefficient table allows us to

explain the intermediate input intensity of a production activity. A sector is considered

intensive (using more input—intermediate or factor—than output) when the coefficient is the

highest (see Table 5).

Table 5

Hence, the Kenyan agricultural sector is intensive in imported manufacturing inputs (0.096).

The food sector is intensive in domestic intermediate inputs (0.312), while the energy sector

is intensive in imported intermediate inputs (0.400). The manufacturing sector is intensive in

imported manufacturing inputs (0.215) relative to domestic inputs (0.176), while the services

sector is intensive in domestic services inputs (0.232) compared to imported services inputs

(0.018).

Overall, the discussion so far has shown that Africa imports more than 80 per cent of

its intermediate goods crucial for value creation in the manufacturing sector from outside

Africa. Furthermore, using the input-output table to analyse the use of imported (and

domestic) production inputs in Kenya (identified to be a country with potential revealed

comparative advantage (world) in BEC 2, 3, 5 and 7), we find that imported intermediate

16

Calculated by dividing each spending value by total input.

Agri Food NRGM Manuf Services

Intermediate Inputs

Agric. Imports 0.010 0.007 - 0.001 0.000

Food Imports 0.004 0.020 0.001 0.005 0.009

NRGM Imports 0.010 0.004 0.400 0.024 0.022

Manuf Imports 0.096 0.047 0.071 0.215 0.066

Services Imports 0.002 0.003 0.008 0.013 0.018

Agric. Domestic 0.084 0.030 - - -

Food Domestic 0.058 0.312 0.026 0.078 0.143

NRGM Domestic 0.026 0.007 0.144 0.056 0.026

Manuf Domestic 0.079 0.021 0.033 0.176 0.045

Services Domestic 0.081 0.070 0.079 0.117 0.232

Factors Inputs

Land 0.065 - - - -

Unskilled Labour 0.387 0.113 0.076 0.133 0.129

Skilled Labour 0.003 0.022 0.024 0.018 0.089

Capital 0.087 0.341 0.115 0.136 0.218

Natural Resources 0 0 0.00218 0.01744 0

Source: Author's estimation based on GTAP v.8.0, 2013.

Kenya Input-Output Coefficients, 2007, (USD millions).

Activities

15

inputs comprise a substantial share of the inputs used in the energy and mining sector (63 per

cent imported) and manufacturing (38 per cent imported).

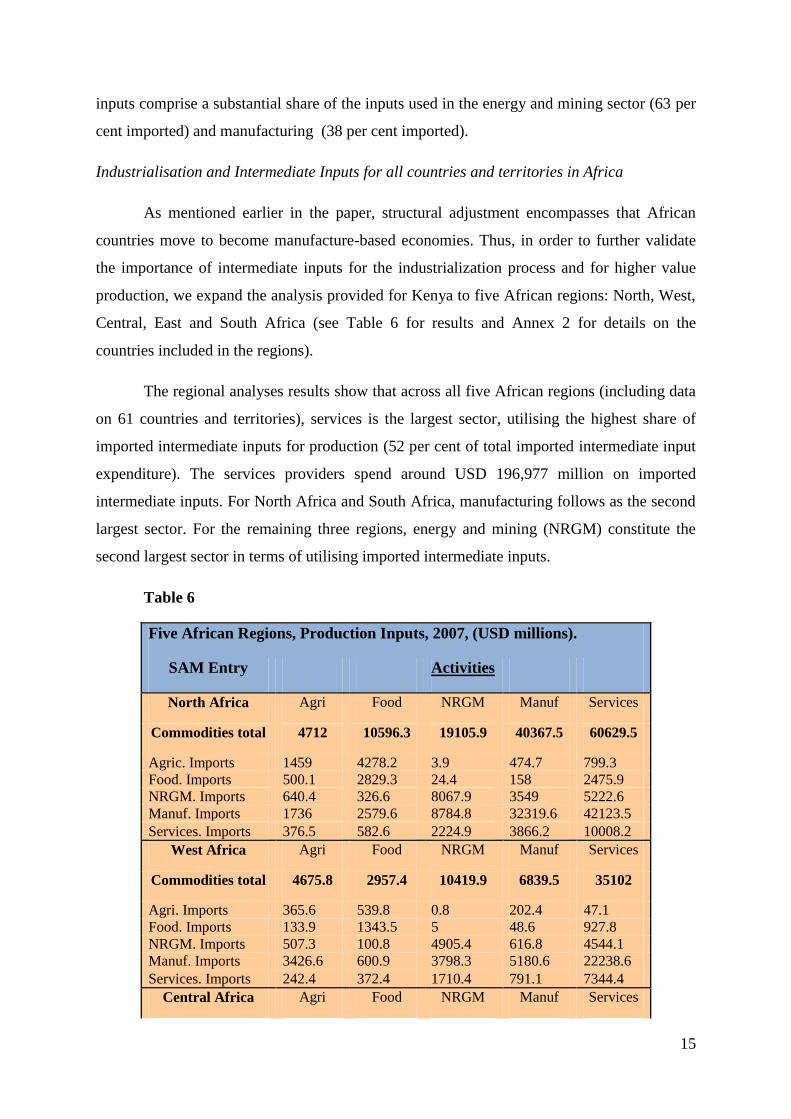

Industrialisation and Intermediate Inputs for all countries and territories in Africa

As mentioned earlier in the paper, structural adjustment encompasses that African

countries move to become manufacture-based economies. Thus, in order to further validate

the importance of intermediate inputs for the industrialization process and for higher value

production, we expand the analysis provided for Kenya to five African regions: North, West,

Central, East and South Africa (see Table 6 for results and Annex 2 for details on the

countries included in the regions).

The regional analyses results show that across all five African regions (including data

on 61 countries and territories), services is the largest sector, utilising the highest share of

imported intermediate inputs for production (52 per cent of total imported intermediate input

expenditure). The services providers spend around USD 196,977 million on imported

intermediate inputs. For North Africa and South Africa, manufacturing follows as the second

largest sector. For the remaining three regions, energy and mining (NRGM) constitute the

second largest sector in terms of utilising imported intermediate inputs.

Table 6

Five African Regions, Production Inputs, 2007, (USD millions).

SAM Entry Activities

North Africa Agri Food NRGM Manuf Services

Commodities total 4712 10596.3 19105.9 40367.5 60629.5

Agric. Imports 1459 4278.2 3.9 474.7 799.3

Food. Imports 500.1 2829.3 24.4 158 2475.9

NRGM. Imports 640.4 326.6 8067.9 3549 5222.6

Manuf. Imports 1736 2579.6 8784.8 32319.6 42123.5

Services. Imports 376.5 582.6 2224.9 3866.2 10008.2

West Africa Agri Food NRGM Manuf Services

Commodities total 4675.8 2957.4 10419.9 6839.5 35102

Agri. Imports 365.6 539.8 0.8 202.4 47.1

Food. Imports 133.9 1343.5 5 48.6 927.8

NRGM. Imports 507.3 100.8 4905.4 616.8 4544.1

Manuf. Imports 3426.6 600.9 3798.3 5180.6 22238.6

Services. Imports 242.4 372.4 1710.4 791.1 7344.4

Central Africa Agri Food NRGM Manuf Services

16

Commodities total 451.91 998.6 6488.16 2684.65 24064.82

Agri. Imports 14.43 67.07 1.74 17.7 31.22

Food. Imports 50 242.17 20.07 151.59 645.49

NRGM. Imports 6.72 26.77 292.14 166.26 1532.93

Manuf. Imports 314.24 319.34 3192.22 1593.09 10773.57

Services. Imports 66.52 343.25 2981.99 756.01 11081.61

East Africa Agri Food NRGM Manuf Services

Commodities total 2967.46 3462.34 10099.72 7415.12 39596.6

Agri. Imports 227.02 491.17 2.85 133.69 69.55

Food. Imports 146.64 889.42 32.35 138.64 1013.75

NRGM. Imports 233.89 125.07 3075.21 803.16 5107.22

Manuf. Imports 2092.66 1445.39 4350.1 5216.78 21357.02

Services. Imports 267.25 511.29 2639.21 1122.85 12049.06

South Africa Agri Food NRGM Manuf Services

Commodities total 1248.2 3119.72 16809.77 25255.31 37584.42

Agri. Imports 58.06 966.32 0.84 54.1 63.34

Food. Imports 72.64 828.51 6.59 171.23 268.26

NRGM. Imports 179.87 88.09 14149.96 3402.04 4244.91

Manuf. Imports 755.05 838.86 2000.74 20046.69 29103.22

Services. Imports 182.58 397.94 651.64 1581.25 3904.69

Total 14055.37 21134.36 62923.45 82562.08 196977.3

Source: GTAP 8 and 8.1 (2013)

Furthermore, across all regions, manufacturing imported intermediate inputs constitutes the

largest share (60 per cent) of total imported intermediate inputs, USD 226,187 million. For

the three regions—North, South and West Africa—energy and mining follows as the second

largest commodity group. In Central and East Africa services make out the second largest

group of imported intermediate inputs.

The results from the regional data suggest that imported intermediate inputs are

critical in the manufacturing and energy and mining sectors. Moreover, manufacture and

energy and mining imported intermediate inputs together make out 76 per cent of total

imported intermediate inputs.

Trade Facilitation

In light of the preliminary findings that imported intermediate inputs are crucial for

manufacturing production, the timely and cost-effective sourcing of intermediate inputs

17

between African countries (and also African countries with the rest of the world) are of

utmost importance. Trade facilitation is therefore important and relevant in this context.

Trade facilitation is understood as the simplification of the trade relationship between

partners.17

In the WTO, it has a more elaborate scope which focuses ‘“on the simplification

and harmonisation of international trade procedures” 18

(ECA et al., 2010). Table 7 illustrates

the key components.

Table 7

Trade Facilitation (with Financing) Trade Facilitation Doha Negotiating Text

(without Financing)

Broad Scope of Coverage Compliance to government rules by traders;

authorities’ enforcement of these rules (including

taxes); exchange of information; financing; insurance;

ICT and legal services; transport; handling;

measurement and storage.

Article 1: Publication And Availability Of

Information, Article 2: Prior Publication And

Consultation , Article 3: Advance Rulings, Article 4:

Appeal Procedures, Article 5: Other Measures To

Enhance Impartiality, Non-Discrimination And

Transparency, Article 6: Fees And Charges

Connected With Importation And Exportation, Article

7: Release And Clearance Of Goods, Article 8:

Consularization, Article 9: Border Agency

Cooperation, Article 10: Formalities Connected With

Importation And Exportation , Article 11: Freedom Of

Transit, Article 12: Transitional Provisions For

Developing Country Members And Least Developed

Country Members, Article 13: [Customs] Cooperation

[Mechanism For [Trade Facilitation And]

[[Customs][Trade]] Compliance], Article

14: Institutional Arrangements, Article 15: National

Committee On Trade Facilitation, Article 16:

Preamble/Cross-Cutting Matters.

Responsibility REC’s based/Continental based. Individual Member

Funding of Trade Facilitation Measures Mostly REC’s based/Continental based/Donor

based

Mostly individual Members

Source: Extracted from ECA et al., (2010) and World Trade Organization (2009)

While the main objectives of both trade facilitation pathways are to simplify trading between

partners, the means to achieving the specific activities differs. In particular, there is no

specific reference in the Trade Facilitation negotiating text of the WTO to financial assistance

towards members taking up these new additional commitments. This is probably one reason

17

This includes compliance to government rules by traders, authorities’ enforcement of these rules (including

taxes), the exchanges of information, financing, insurance, ICT and legal services, transport, handling,

measurement and storage (ECA et al., 2010). 18

This includes activities, practices and formalities involved in collecting, presenting, communicating and

processing data required for the movement of goods in international trade.

18

why some developing countries (including African WTO members) are less supportive of the

current negotiating text since any new trade facilitation commitments will imply

disproportional financial costs to most African economies.

Recognising the importance of trade facilitation towards Africa’s access to intermediate

inputs for production in higher value commodities, it is worthy to note that trade facilitation

measures are costly. Hence, domestic (and international) resource mobilization is therefore

important towards funding trade facilitation measures in Africa. One of the untapped

domestic resources that Africa is yet to harness is international financial loss due to illicit

financial flows (IFF). Mevel et al., (2013) estimated that Africa lost a cumulated total of

USD409 billion through illicit financial flows from trade mispricing in the period 2001 to

2010. About 92.5 per cent of this cumulative total IFF was due to export under-invoicing

while 7.5 per cent was import- over-invoicing. The study showed that while IFF has

increased over the decade studied, the last five years witnessed a significant increase in IFF—

totalling USD280 billion between 2006 to 2010—compared to USD129 billion between 2001

and 2005, attributable to the recent global increase in the values of primary commodities of

which Africa exports the most and in which Africa has revealed comparative advantage19

.

To put this amount of loss due to IFF (USD409 billion) into perspective, we compare this

amount against the amounts on Official Development Aid (ODA) and Foreign Direct

Investment (FDI) to Africa during this period (see Figure 3). Comparing years with available

data (2002-2010) on IFF, ODA and FDI flows, two key issues stands out. First, the estimated

value for combined IFF, ODA and FDI flows in Africa is around USD1,151.8 billion

between 2002-2010. Although the value of ODA commitment over the period dominated

with 38 per cent of total, IFF followed second with 32 per cent and FDI flows at 30 per cent.

Second, in the later years (2007, 2008 and 2009), the share of IFF is higher compared to

ODA and FDI flows respectively.

Therefore, two policy implications emerge from these trends. First, Africa needs to put in

place practical policy measures to curb IFF, in order to tap into this substantial domestic

financial resource loss. Second, the amount of IFF loss is so substantial, that if it was curbed,

it could potentially replace ODA or FDI respectively, which is required for the

transformational growth of Africa.

19

Please refer to Mevel, ‘Ofa & Karingi (2013) for details on methodology on estimating IFF and sectoral

results.

19

Figure 3

To sum up this section, based on the continental trade in intermediate goods and the case

of Kenya and other countries and territories in Africa, we find that imported intermediate

inputs are crucial for manufacturing production. Therefore, the access of African countries to

imported intermediate inputs is crucial and the trade facilitation measures have an important

role to play to ensure timely and cost-effective access. However, trade facilitation measures

are costly in the context of Africa and therefore requires concerted efforts (domestic and

international) to ensure ample financial resources is available. One potential source of

funding—if appropriate policy measures are implemented to curb it—is financial resource

losses from Africa due to illicit financial flows, which is estimated to a cumulative total of

USD409 billion between 2001 and 2010.

5. The role of Regional Economic Communities (RECs) in fostering a transformative

regional integration and trade in Africa

The RECs20

play a crucial role in Africa’s regional integration effort, despite challenges.

The challenges to Africa’s regional integration are well documented (see ECA et al., 2010 &

2012). These challenges range from energy access to security, and from infrastructure to

multiple memberships in RECs. These challenges are best tackled by strengthening

coordination among the RECs—individual countries cannot overcome these challenges alone

20

Refers to the eight RECs recognised by the Africa Union; CEN-SAD, COMESA, EAC, ECCAS, ECOWAS,

IGAD, SADC and UMA. Please refer to ECA et al., (2012) for composition of membership.

38

44

18

30

48

22

32

47

21

28

44

28

22

47

29

41

29

30

41

29

30

30

38

32

37

36

27

0

20

40

60

80

100

Perc

enta

ge S

hare

2002 2003 2004 2005 2006 2007 2008 2009 2010

(Author's estimation based on OECD, UNCTADstat, UN COMTRADE & CEPII-BACI, 2013)

Africa: IFF, ODA and FDI Flows, 2002-2010

IFF ODA Commitment

FDI Inflows

20

(ECA et al., 2012). While the African Union is coordinating progress among the RECs, the

actual implementation remains the responsibility of each REC. The regional integration

process is anchored on initiatives (Minimum Integration Programme—MIP) that the RECs

have selected21

. The key sectors that RECs have accepted as priority sectors include free

movement of persons, goods, services and capital; peace and security; infrastructure and

energy; agriculture; trade; industry; investment; and statistics. Nevertheless, a key challenge

in relation to the implementation of the MIP is one of access to finance and funding of these

initiatives by each individual REC and its respective members.

In the area of investment and capital, there are specific regional agreements on investment

including the COMESA Common Investment agreement (CCIA) and the SADC Investment

and Finance Protocol (SIFP), while ECOWAS has no explicit agreement except for

investment in energy. At the country level, several governments (18 African countries in

2009), introduced national investment-specific policy measures to attract foreign investment

in air transport or banking. The progress has been hampered by countries’ lack of compliance

with their commitments due to duplication of agreements (from multiple members).

Weakness in compliance also stems partly from RECs’ failure to fully integrate investment

provisions, treating them as add-ons (ECA et al., 2012).

In the area of free movement of people, significant progress has been made by several

RECs, in particular the adoption of protocols on the free movement of people, labour,

services, right to establishment and right to residence. Yet the process of transition to full

mobility of workers among African countries remains one of the most contentious issues

among African countries for reasons including security and unemployment (ECA et al.,

2012). For example, the freedom of movement in ECOWAS region is more advanced than in

any other sub-region22

. Many other African countries still demand visas from neighbours. For

example, members of COMESA and SADC impose visa requirements. One of the key

challenges for free movement of labour is the fact that unemployment rates in Africa are

generally high ranging from 12 to 45 per cent and in some cases as high as 70 per cent (ECA

et al., 2012). Therefore, some African countries are reluctant to allow in temporary unskilled

labour, particularly if their own nationals are uncompetitive against temporary unskilled

labourers from another country.

21

See ECA et al., (2012) for detail of the initiatives for the MIP first phase (2009-2012). 22

But only the first of three phases of the relevant protocol (visa free entry for up to 90 days) have been

completely implemented in all ECOWAS countries (ECA et al., 2012).

21

In terms of trade in goods and services, infrastructure is the main challenge towards

facilitating intra-African trade. The AUC Heads of States and Government in Kampala

launched the Programme for Infrastructure Development in Africa (PIDA) in July 2010,

which focuses on infrastructure projects in the areas of energy, transport, and ICT. The PIDA

strategic framework was adopted by the Heads of States and Governments in Addis Ababa in

January 2012 outlining a priority action plan.23

All RECs have infrastructure policy

frameworks and in some cases these are implemented jointly with other RECs. For example,

the COMESA, EAC and SADC are jointly implementing the ‘North-South Corridor’, which

is a transport infrastructure and trade-facilitation initiative with the objective of harmonising

regulations and transport service among the three RECs members. The major challenge for

infrastructure projects of this nature is that it cuts across several countries with different rules

and requirements. Also, multiple memberships create duplication in projects delaying

implementation. In addition, some of these infrastructure projects require huge financial

funding that most African countries and communities do not have.

To sum up this section, concerted efforts have been implemented by the RECs towards a

transformative regional integration and trade in Africa. However, there are challenges that

hamper RECs ability to effectively play their important role in regional integration. These

challenges include lack of access to finance for infrastructure projects, high costs of

implementing new agreements due to multiple membership, different levels of labour skills

and qualifications across the continent, thereby discouraging free movement of labourers.

These challenges therefore need to be addressed thereby allowing the RECs to be effective.

6. Conclusions

In this paper, we have argued that Africa’s regional integration agenda needs to be

‘transformative’ in order to gain buy-in and support for fast-tracking implementation at all

levels. In particular, transformative regional integration should address the concerns

regarding employment creation and also, promote and support resource-based

industrialisation for African countries with the potential comparative advantage in each

industry sector.

Further, we argued that resource-based industrialisation requires both primary inputs—

with which Africa is naturally endowed—and also intermediate inputs. However, Africa

23

Refer to ECA et al., (2012) for list of priority infrastructure projects 2010-2015.

22

imports more than 80 per cent of its intermediate goods crucial for value creation in the

manufacturing sector from outside Africa. Furthermore, using the input-output table to trace

the use of imported (and domestic) production inputs in Kenya (identified to be a country

with potential revealed comparative advantage (world) in BEC 2,3,5 and 7), we find that

imported intermediate inputs comprise a substantial share of energy and mining (63 per cent

imported) and manufacturing production (38 per cent imported). In addition, manufacturing

inputs are found to be the biggest intermediate input for the services industry—which was

Kenya’s largest sector in 2007. In addition, across all African countries and territories,

manufactured imported intermediate inputs constitute the largest share (60 per cent) of total

imported intermediate inputs. Therefore, the results from the regional analyses suggest that

imported intermediate inputs are critical in the manufacturing and energy and mining sectors.

Moreover, manufacture and energy and mining imported intermediate inputs together make

out 76 per cent of total imported intermediate inputs.

As a result, the access of African countries to imported intermediate inputs is crucial and

therefore trade facilitation measures have an important role to play to ensure timely and cost-

effective access. However, trade facilitation measures are costly in the context of Africa and

therefore require concerted efforts—both from domestic and international sources—to ensure

ample financial resources are available. One potential source of funding—if appropriate

policy measures are implemented to curb it—is financial resource losses from Africa due to

illicit financial flows, which is estimated to a cumulative total of USD409 billion between

2001 and 2010.

Further, RECs do have an important role to play towards a transformative regional

integration and trade in Africa. However, there are challenges that hamper RECs’ ability to

effectively play their important role in regional integration. These challenges include a lack

of access to finance on infrastructure projects, high costs of implementing new agreements

due to multiple membership, different levels of labour skills and qualifications across the

continent, thereby discouraging free movement of labourers. These challenges therefore need

to be addressed thereby allowing the RECs to be effective.

23

References:

African Union, 2012, ‘Action Plan for Boosting Intra-African Trade’, accessed for further information,

http://www.au.int/en/sites/default/files/Action%20Plan%20for%20boosting%20intra-African%20trade%20F-

English.pdf

Balassa B, 1965, ‘Trade liberalisation and ‘revealed’ comparative advantage’, The Manchester School’, Vol. 33,

pp. 99-123.

Burfisher ME, 2011, ‘Introduction to General Equilibrium Models’, Cambridge University Press, New York.

CEPII, 2013, ‘BACI Database’, accessed 1 May 2013,

http://www.cepii.fr/CEPII/en/welcome.asp

Chinembiri E, 2010, ‘An Empirical Assessment of the Impact of Trade Liberalization on Employment in South

Africa’, Trade & Industrial Policy Strategies, accessed 7 May 2013,

http://www.tips.org.za/files/Evans_Assessment_of_the_Impact_of_Trade_Liberalization_on_EmploymentFINA

L.pdf

Currie, J & A. Harrison, 1997, ‘Sharing the costs: The impact of trade reform on capital and labour in Morocco’,

Journal of Labour Economics, Vol. 15 (3ii), July: S44-S72

ECA, AU & AfDB, 2010, ‘Assessing Regional Integration in Africa IV’, United Nations Economic

Commission for Africa UNECA, Addis Ababa.

ECA, AU & AfDB, 2012, ‘Assessing Regional Integration in Africa V’, United Nations Economic Commission

for Africa UNECA, Addis Ababa.

ECA & AU, 2013, ‘Economic Report on Africa 2013’, UNECA, Addis Ababa.

GTAP, 2013, ‘GTAP Database 8’, accessed 30 May 2013,

https://www.gtap.agecon.purdue.edu/#4

Laursen K, 2000, ‘Trade Specialisation, Technology and Economic Growth: Theory and Evidence from

Advanced Countries’, Cheltenham, Edward Elgar.

Mashayekhi M, Peters R and Vanizetti D, 2012, ‘Regional Integration and Employment Effects in SADC’,

Policy Priorities for International Trade and Jobs, OECD.

Mevel S, SV ‘Ofa & S Karingi, 2013, ‘Quantifying illicit financial flows from Africa through trade mis-pricing

and assessing their incidence on African economies’, Selected paper for Presentation at the 16th GTAP

Conference, Shanghai.

OECD, 2013, ‘Aid Statistics’, accessed 30 May 2013,

http://www.oecd.org/dac/stats/

‘Ofa SV, M Spence, S Mevel & S Karingi, 2012, ‘Export Diversification and Intra-Industry Trade in Africa’,

Selected Paper for Presentation in the African Economic Conference 2012, Kigali, Rwanda, 30 October – 2

November 2012, accessed 15 May 2013,

http://www.africaneconomicconference.org/2012/Documents/Papers/AEC2012-379.pdf

Rattso, J., and R. Torvik, 1998, ‘Zimbabwean trade liberalization: Ex post evaluation’, Cambridge Journal of

Economics, Vol. 22: 325-346.

UNCTADstat, 2013, accessed 30 May 2013,

http://unctadstat.unctad.org/ReportFolders/reportFolders.aspx

UN COMTRADE, 2013, accessed 30 May 2013,

http://comtrade.un.org/

24

UNECA, 2012, ‘Study Report on Mainstreaming Regional Integration into National Development Strategies

and Plans’, UNECA, Addis Ababa.

WITS Online Database, 2013, accessed 30 May 2013,

http://wits.worldbank.org/wits/

World Trade Organization, 2009, ‘Draft Consolidated Negotiating Text’, Negotiating Group on Trade

Facilitation, TN/TF/W/165, WTO, Geneva.

25

Annex 1: Figure 2

-1-.

50

.51

No

rmaliz

ed

Reve

ale

d C

om

pa

rative

Ad

van

tag

e

Ang

ola

Equ

ato

ria

l_G

uin

ea

Lib

ya

Gab

on

Cha

dC

on

go

Eritr

ea

Con

go

_D

RA

lgeria

Cen

tral_

Afr

ican

_R

ep

Nig

eria

Za

mb

iaLib

eria

Sud

an

Burk

ina_

Faso

SA

CU

Guin

ea

Zim

ba

bw

eM

oza

mb

ique

Tu

nis

iaN

ige

rM

ali

Egypt

Sie

rra_

Le

one

Mo

rocco

Ma

law

iT

anzan

iaB

en

inC

am

ero

on

Ma

uri

tan

iaG

ha

na

Ma

uri

tiu

sS

en

eg

al

Rw

and

aM

ada

ga

scar

To

go

Sao

_T

om

e_P

rincip

eK

en

ya

Gam

bia

Uga

nd

aC

ote

_d

Ivoire

Com

oro

sE

thio

pia

Cap

e v

erd

eG

uin

ea

_B

issa

uD

jibou

tiB

uru

nd

iS

eych

elle

sS

om

alia

Source: Author's estimations based on BACI dataset (CEPII), 2013

Africa : NRCA Index to World (2011) - BEC1-1

-.5

0.5

No

rmaliz

ed

Reve

ale

d C

om

pa

rative

Ad

van

tag

e

Ang

ola

Cha

dLib

ya

Nig

eria

Alg

eria

Sud

an

Equ

ato

ria

l_G

uin

ea

Seych

elle

sC

ap

e v

erd

eS

ao

_T

om

e_P

rincip

eS

om

alia

Con

go

Guin

ea

_B

issa

uG

ab

on

Eth

iop

iaB

uru

nd

iD

jibou

tiM

auri

tiu

sT

unis

iaM

ada

ga

scar

Ken

ya

Cote

_d

Ivoire

Com

oro

sU

ga

nd

aC

am

ero

on

Mo

rocco

Egypt

Gha

na

Guin

ea

Sen

eg

al

Gam

bia

Rw

and

aT

ogo

Lib

eria

Ben

inN

ige

rM

ali

Mo

za

mb

ique

SA

CU

Ta

nzan

iaM

auri

tan

iaM

ala

wi

Sie

rra_

Le

one

Con

go

_D

RZ

imba

bw

eB

urk

ina_

Faso

Za

mb

iaC

en

tral_

Afr

ican

_R

ep

Eritr

ea

Source: Author's estimations based on BACI dataset (CEPII), 2013

Africa : NRCA Index to World(2011) - BEC 2

26

-1-.

50

.5

No

rmaliz

ed

Reve

ale

d C

om

pa

rative

Ad

van

tag

e

Buru

nd

iB

urk

ina_

Faso

Com

oro

sS

ierr

a_

Le

one

Djib

ou

tiS

eych

elle

sE

thio

pia

Ma

law

iZ

am

bia

Cen

tral_

Afr

ican

_R

ep

Gam

bia

Ma

uri

tiu

sT

ogo

Ta

nzan

iaZ

imba

bw

eM

oro

cco

Rw

and

aK

en

ya

Uga

nd

aM

ada

ga

scar

Ma

uri

tan

iaS

om

alia

SA

CU

Tu

nis

iaG

uin

ea

_B

issa

uS

en

eg

al

Ma

liC

on

go

_D

RLib

eria

Ben

inM

oza

mb

ique

Cote

_d

Ivoire

Gha

na

Nig

er

Guin

ea

Egypt

Cam

ero

on

Gab

on

Con

go

Sud

an

Nig

eria

Equ

ato

ria

l_G

uin

ea

Alg

eria

Lib

ya

Cha

dA

ng

ola

Source: Author's estimations based on BACI dataset (CEPII), 2013

Africa : NRCA Index to World (2011) - BEC3-1

-.5

0.5

1

No

rmaliz

ed

Reve

ale

d C

om

pa

rative

Ad

van

tag

e

Cha

dS

om

alia

Sud

an

Eritr

ea

Equ

ato

ria

l_G

uin

ea

Ang

ola

Alg

eria

Gab

on

Con

go

_D

RLib

ya

Ma

uri

tan

iaC

on

go

Ben

inG

uin

ea

_B

issa

uB

urk

ina_

Faso

Gam

bia

Zim

ba

bw

eE

thio

pia

Gha

na

Nig

eria

Buru

nd

iM

ala

wi

Rw

and

aM

oza

mb

ique

Cote

_d

Ivoire

Lib

eria

To

go

Egypt

Cen

tral_

Afr

ican

_R

ep

Sen

eg

al

Za

mb

iaT

anzan

iaC

om

oro

sK

en

ya

Djib

ou

tiM

ali

Ma

uri

tiu

sN

ige

rS

ierr

a_

Le

one

Ma

da

ga

scar

Cam

ero

on

Cap

e v

erd

eS

eych

elle

sS

AC

UM

oro

cco

Uga

nd

aS

ao

_T

om

e_P

rincip

eT

unis

iaG

uin

ea

Source: Author's estimations based on BACI dataset (CEPII), 2013

Africa : NRCA Index to World (2011) - BEC4

27

-1-.

50

.51

No

rmaliz

ed

Reve

ale

d C

om

pa

rative

Ad

van

tag

e

Som

alia

Ma

uri

tan

iaA

ng

ola

Guin

ea

_B

issa

uLib

ya

Sud

an

Con

go

Equ

ato

ria

l_G

uin

ea

Ben

inC

ha

dE

ritr

ea

Alg

eria

Gha

na

Nig

eria

Con

go

_D

RC

am

ero

on

Burk

ina_

Faso

Za

mb

iaZ

imba

bw

eG

am

bia

Buru

nd

iD

jibou

tiS

eych

elle

sM

auri

tiu

sC

ote

_d

Ivoire

Cen

tral_

Afr

ican

_R

ep

Ta

nzan

iaC

om

oro

sE

gypt

Nig

er

Sen

eg

al

Eth

iop

iaC

ap

e v

erd

eM

oza

mb

ique

Ma

law

iS

ao

_T

om

e_P

rincip

eT

ogo

Ken

ya

Sie

rra_

Le

one

Gab

on

Uga

nd

aR

wa

nd

aG

uin

ea

Ma

da

ga

scar

Ma

liS

AC

UM

oro

cco

Tu

nis

iaLib

eria

Source: Author's estimations based on BACI dataset (CEPII), 2013

Africa : NRCA Index to World (2011) - BEC5-1

-.5

0.5

1

No

rmaliz

ed

Reve

ale

d C

om

pa

rative

Ad

van

tag

e

Equ

ato

ria

l_G

uin

ea

Ang

ola

Alg

eria

Lib

ya

Sud

an

Con

go

Cha

dS

om

alia

Gab

on

Ma

uri

tan

iaC

on

go

_D

RG

uin

ea

_B

issa

uN

ige

ria

Com

oro

sC

en

tral_

Afr

ican

_R

ep

Burk

ina_

Faso

Mo

za

mb

ique

Za

mb

iaB

en

inD

jibou

tiE

ritr

ea

Nig

er

Buru

nd

iS

eych

elle

sM

ali

Cam

ero

on

Lib

eria

Guin

ea

Gam

bia

SA

CU

Sie

rra_

Le

one

Zim

ba

bw

eC

ote

_d

Ivoire

Ma

law

iG

ha

na

Rw

and

aT

anzan

iaU

ga

nd

aT

ogo

Sen

eg

al

Eth

iop

iaE

gypt

Cap

e v

erd

eM

oro

cco

Ken

ya

Ma

da

ga

scar

Tu

nis

iaM

auri

tiu

sS

ao

_T

om

e_P

rincip

e

Author's estimation based on BACI Dataset (CEPII) 2013

Africa : NRCA Index to World (2011) - BEC6

28

-1-.

50

.51

No

rmaliz

ed

Reve

ale

d C

om

pa

rative

Ad

van

tag

e

Alg

eria

Con

go

Equ

ato

ria

l_G

uin

ea

Mo

rocco

Gha

na

Burk

ina_

Faso

Nig

eria

Eritr

ea

Seych

elle

sZ

imba

bw

eZ

am

bia

Som

alia

Gam

bia

Sie

rra_

Le

one

To

go

Tu

nis

iaT

anzan

iaM

auri

tan

iaN

ige

rC

ap

e v

erd

eS

en

eg

al

Ken

ya

Ma

da

ga

scar

Ma

uri

tiu

sC

am

ero

on

Egypt

Ma

liU

ga

nd

aG

uin

ea

Buru

nd

iC

ote

_d

Ivoire

SA

CU

Lib

eria

Rw

and

aM

oza

mb

ique

Ma

law

i

Author's estimation based on BACI Dataset (CEPII) 2013

Africa : NRCA Index to World (2011) - BEC7

29

Annex 2

Regions (all territories and countries)

North Africa

Egypt

Morocco

Tunisia

Algeria

Libyan Arab Jamahiriya

Western Sahara

West Africa

Benin

Burkina Faso

Cameroon

Cote d'Ivoire

Ghana

Guinea

Nigeria

Senegal

Togo

Cap Verde

Gambia

Guinea Bissau

Liberia

Mali

Mauritania

Niger

Saint Helena, Ascension and Tristan de Cunha

Sierra Leone

Central Africa

Central African Republic

Chad

Congo

Equatorial Guinea

Gabon

Sao Tome and Principe

Angola

Democratic Republic of Congo

East Africa

Ethiopia

Kenya

Madagascar

Malawi

Mauritius

Mozambique

Rwanda

Tanzania

Uganda

Zambia

Zimbabwe

Burundi

Comoros

Djibouti

Eritrea

Mayotte

Seychelles

Somalia

Sudan

South Africa

Botswana

Namibia

South Africa

Lesotho

Swaziland