transfer pricing - typical issues · tax advisory services tp assessments – typical issues...

TRANSCRIPT

1

All

right

s re

serv

ed

| 1

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issuesC h a l l e n g e U s

| 2

All

right

s re

serv

ed|

Tax advisory services TP assessments – Typical issues

TRANSFER PRICING ASSESSMENTS

TYPICAL ISSUES

Ajay RottiDirectorBMR & Associates

November 4, 2009

2

| 3

All

right

s re

serv

ed|

Tax advisory services TP assessments – Typical issues

CONTENTSASSESSMENT PROCEDURE

OverviewTYPICAL ISSUES

Methods and aggregationFilters and comparablesWorking capital and risk adjustmentsDispute resolution

RECENT DEVELOPMENTSRecent decisionsChallenges and way forward

| 4

All

right

s re

serv

ed|

Tax advisory services TP assessments – Typical issues

ASSESSMENT PROCEDURE

3

All

right

s re

serv

ed

| 5

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

Overview

Transfer pricing (‘TP’) refers to the pricing of cross-border transactions between two associated enterprises

Any income / allowance for any expense or interest / allocation of cost, arising from such international transactions shall be computed having regard to the ALP

A price between unrelated parties is known as the arm’s length price (‘ALP’)

All

right

s re

serv

ed

| 6

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

Indian Transfer Pricing requirements

International transactions with related entities to be at ALP – Section 92CArm’s length price

If required, representation before Indian Tax/Transfer Pricing authorities to justify arm’s length nature of international transactions – Section 92CA etc

Representation

DocumentationMaintenance of specified documentation to justify the arm’s length nature of international transactions – Section 92D

4

All

right

s re

serv

ed

| 7

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

Documentation requirements

Detailed documentation requirements have been laid down in the TP rulesThe documentation should demonstrate the basis of arriving at the ALPDocumentation required for self defense from TP auditsPenalties are leviable where documentation has not been maintainedFor transactions aggregating Rs 10 million in value in total during the previous year from April 1 to March 31 the documentation requirements condition is relaxed

Section 92D and Rule 10D

All

right

s re

serv

ed

| 8

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

Documentation – TP Report

Corporate BackgroundFunctional Analysis

Functions performedRisk undertakenAssets employed

Economic AnalysisChoice of Most Appropriate MethodIdentification of tested partySelection of the profit level indicatorSearch for comparables

Internal comparablesExternal comparables

5

All

right

s re

serv

ed

| 9

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

Documentation – TP Report

Financial analysis Identified comparable companiesTested party

Periodic review and appropriate adjustments for significant changes (if necessary) Conclusion

All

right

s re

serv

ed

| 10

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

Documentation – Accountant’s certificate

Whether required documentation (eg TP Report) has been preparedTypical particulars :

Names/addresses of Associated EnterprisesNature of transactionValue of transaction

As per books of accountArm’s Length Price as computed by the corporate

Certificate to be submitted for each tax year

Section 92E, Rule 10E and Form 3CEB

6

All

right

s re

serv

ed

| 11

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

TP assessment process – At macro level

TP assessment process

AO(Assessing officer) to refer to TPO (Transfer pricing officer)if value of International transaction> INR 150 million

TPO to send notice to the tax payer for the hearing

Documentation analysis & TP audit by the TPO

Copy of the order sent to the AO and the taxpayer

AO to incorporate the TPO’s order in the assessment order

All

right

s re

serv

ed

| 12

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

TP assessment process – At operational level

TPO will make further enquiries etc

TPO will review further documentation

Does the TPO agree with the arms length analysis

No

Tax payer given an opportunity to show cause to TPO’s stand

TPO would pass a

favorable order

without making any

TP adjustment

Yes

Has the taxpayer responded suitably to enable the TPO to reconsider

TPO revisits its earlier stand

Yes

Does the TPO agree with the taxpayer’s contentionYes

TP adjustment

No

No

7

All

right

s re

serv

ed

| 13

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

LEGISLATIVE FRAMEWORK

Assessing OfficerAssessing Officer TP OfficerTP OfficerReference to TP Officer

Transfer Pricing Order

AssesseeAssessee

Ord

er in

corp

orat

ing

the

TP O

rder

Rec

tific

atio

n ap

plic

atio

n

CIT (Appeals)CIT (Appeals)

Appeal against the order of the assessing officer

Copy o

f the T

P orde

r

Budget 2009 has made amendments to provide

an alternate dispute resolution mechanism for

eligible assessees to provide relief in high

demand cases and avoid long drawn litigation

All

right

s re

serv

ed

| 14

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

Revenue authorities - Approach

Understanding the business/operations of the assesseeUnderstanding the international transactions entered into by the assesseeRequiring detailed break up of the international transactions Revisiting all facts, figures and agreements concerning the international transactionsDemanding information on transactions by AEs with other AEs – even though these are not independent comparablesTP Officers are also using PROWESS/ Capitaline database as used by the majority of Transfer Pricing Consultants in the Industry

8

All

right

s re

serv

ed

| 15

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

APPELLATE PROCEEDINGS

Commissioner (Appeals)No specialized personnel for scrutiny at appellate levelFew appeal cases decided thus far – no trend discernableNo substantive relief at first appellate level

Appellate judiciaryRecent debate on setting up of a specialized appellate body for transfer pricing disputesNow position settled - jurisdictional Tribunal to adjudicate transfer pricing disputesSeveral cases pending for adjudication at Tribunal levelRecent judicial decisions provide guidance on complex issues –Morgan Stanley ruling (Supreme Court), Aztec Software Services (Tribunal)

| 16

All

right

s re

serv

ed|

Tax advisory services TP assessments – Typical issues

TYPICAL ISSUES

9

All

right

s re

serv

ed

| 17

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

Provision of servicesDistribution of finished

goods where RPM cannot be applied

Transactions involving integrated services by more than 1 enterprise

Provision of servicesDistribution of semi

finished goods

Distribution of products

Transfer of commodities/services

Loans/financing activities and intangibles

Applicability

Complex Method, sparingly used

Net Operating Profit margins are benchmarked

MediumPSM

Most commonly used method

Difficult to apply as high degree of comparability required

Difficult to apply as high degree of comparability required

Very difficult to apply as very high degree of comparability required

Remarks

Net Operating Profit margins are benchmarked

MediumTNMM

Gross Profit margins are benchmarked

HighCPLM

Gross Profit margins are benchmarked

HighRPM

Prices are benchmarked

Very HighCUP

ApproachComparability Requirements

Methods

Applicability of TP methods - Comparison

All

right

s re

serv

ed

| 18

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

SELECTION OF MOST APPROPRIATE METHOD

Factors considered for selection of the most appropriate method to be used for determining arm’s length price:

Nature and class of international transaction

Class of associated enterprise and functions performed

Availability, coverage and reliability of data

Degree of comparability between:

International transaction and uncontrolled transaction

Enterprises entering into such transactions

Extent to which reliable and accurate adjustments can be made

The nature, extent and reliability of assumptions for application of the method

10

All

right

s re

serv

ed

| 19

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

REFERENCE CRITERION

Reference based on transaction value - all international transactions exceeding INR 150 million referred to TPO for scrutinyLegal validity of administrative circular upheld (Sony and Aztec Ruling)Reference criterion very broadReference based on value resulting in high volume of cases -creating pressure on administrative resourcesSelect cases picked up for scrutiny based on qualitative factors

Probability of income-shiftingTransactions with low-tax jurisdictions / tax havensAbnormally low profitabilityInadequate documentation

Absence of risk based audit approachIndustry/OECD pushing for a change in reference criterion

All

right

s re

serv

ed

| 20

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

SPECIFIC AUDIT ISSUESHigh risk for low margin and loss making companiesAd-hoc aggregation / segregation of transactionsUse of secret comparables prevalentCherry picking of comparablesLoss making comparables generally not acceptedAd-hoc risk adjustments in some cases to account for varying risk profilesPublic information on benchmarking royalties not availablePreference for local comparablesDiscretionary use of OECD guidelinesDespite six years of compliance, no substantial change in lawConfounding views on the use of multiple year dataNo guidance on computation of arm’s length rangeHow many number of comparables are enough to benchmark?Whether TNMM is the most appropriate method?No guidance on the use of other Transfer Pricing methods

11

All

right

s re

serv

ed

| 21

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

AGGREGATION – STATUTORY PROVISION

Section 92(1) requires that ‘income arising from an international transaction’ should be computed having regard to arm’s length priceGeneral rule - arm’s length nature of each international transaction to be analyzed separately (transactional approach)On exceptional basis regulations permit use of aggregation approachPrinciple of aggregation enshrined in Rule 10A(d) - “a transaction includes a number of closely linked transactions.”No guidance on what constitutes ‘closely linked transactions’Transactions to be considered ‘closely linked’ having regard to commercial reality

Non availability of comparable data at transactional levelInter-linking of prices of different transactions

All

right

s re

serv

ed

| 22

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

AGGREGATION – REVENUE’S APPROACH

Generally arm’s length analysis at entity level not acceptableRevenue requires transactional analysisTransactional approach subject to availability of segmental informationAggregation \ segregation undertaken on ad-hoc basisIT industry

Sale of hardware and softwareSale of hardware and provision of servicesSale of traded and manufactured goods

Choice of comparable companies skewed towards determination of high benchmarksTarget driven approach

12

All

right

s re

serv

ed

| 23

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

RISK/WORKING CAPITAL ADJUSTMENT

A Co.(captive)

Limited risk profileERR lower than third party service providersAssured return in many casesAccess to global technology

Full-fledged risk takerHigh ERRReturn dependent on market conditionsMay own intangibles

Tested party Comparable

To use B Co as comparable, risk adjustment requiredRevenue ignoring risk differential and imposing adjustments on captives

B Co.(independent)

All

right

s re

serv

ed

| 24

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

Risk adjustment may be carried out as follows:Risk faced by non-captives to be quantified − Distinction between diversifiable and non diversifiable risk− Standard deviation, Beta etc. to be used to quantify risk

Risk free return for the industry to be determined− Return on long term government bonds may be used as a proxy

Return per unit of risk earned by non-captives to be quantified using financial ratiosRisk for tested party to be quantifiedAdditional return earned by non-captives due to excess risk assumed to be adjustedAdjusted returns to be used for benchmarking

Working capital adjustmentInventoryDebtorsCreditors

RISK/WORKING CAPITAL ADJUSTMENT

13

All

right

s re

serv

ed

| 25

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

CONTEMPORANEOUS DATA

‘Contemporaneous’ – reference in regulations [Rule 10D(4)]Term used with reference to prescribed documentationExpression not defined in regulationsRevenue assuming it to imply single year dataJustification for use of different expressions – ‘data relating to the financial year’ versus ‘contemporaneous’?OECD comparability draft notes (May 10, 2006) define it as: “While ‘contemporaneous’ means during the same period of time, it does not necessarily mean during the same tax year.”Whether events occurring after relevant financial year but around the same time could also be considered?

All

right

s re

serv

ed

| 26

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

MULTIPLE YEAR DATA

Regulations require use of single year dataReliance on prior year’s data permitted only exceptionallyNon availability of data for relevant financial year not accepted as justification for use of multiple year dataNo guidance on what would constitute sufficient justification for use of prior year’s dataTarget driven approach by Revenue in use of prior year’s data No clarification even post Aztec decision

14

All

right

s re

serv

ed

| 27

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

REIMBURSEMENT OF OPERATING EXPENSES

Particular relevance to Transactional Net Margin Method (TNMM)Expenditure for business operations considered part of operatingcost even if reimbursedReimbursements not considered part of ‘operating income’Cumulative impact - deflation of profit margin resulting in adjustmentAccounting concepts such as ‘matching principle’ considered irrelevant Revenue’s stand appears logical

TNMM focuses on income from business operations (concept of operating income)Similar expenditure incurred by comparables may not be reimbursed

All

right

s re

serv

ed

| 28

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

COORDINATION WITH CUSTOMS VALUATION

Recent move to dovetail customs and transfer pricing department Common requirement of arm’s length benchmarkingApply same methods to compute arm’s length pricePrescribe common documentation to avoid duplication

OECD Guidelines endorse coordination (between transfer pricing and customs valuation) but advise caution

Conflicting objectives – no undervaluation does not imply that imports are not overpricedTiming differences

Customs valuation – at the time of importTransfer pricing valuation – at the time of contractTiming differences may restrict utility of documentation under customs regulations for income-tax purposes or vice versa

15

All

right

s re

serv

ed

| 29

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

USE OF SECRET COMPARABLES

Revenue known to rely on secret comparables in certain casesNo statutory bar on use of secret comparablesIssue of violation of principles of natural justiceJudicial precedent does not prohibit reliance on secret comparables where substantive details are disclosed

No disclosure of company nameDisclosure of important particularsOpportunity of hearing to taxpayer

Implementation of best practices on usageLimited use – last resortDisclosure of material particulars

All

right

s re

serv

ed

| 30

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

RELIANCE ON LAST YEAR’S APPROACH

Reliance on last year’s approachOfficer of same rank reluctant to overrule predecessorTarget driven approachPossibility of relief at appellate level

Breaking traditionDeviation from last year on basic approach/principle generally not acceptedRevenue may still allow relief in comparability analysis

Exclusion of a high margin comparableInclusion of a loss making comparableInclusion/exclusion of comparables on other grounds (related party transactions, abnormal circumstances, non-availability of data etc)

Taxpayer should provision for adjustment (FIN 48)Though Revenue likely to follow last year’s approach, possible to bring down adjustment

16

All

right

s re

serv

ed

| 31

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

ACCEPTABLE COMPARABILITY FILTERS

Functional profileProduct characteristicsScale of operationsPersistently loss making companiesAbnormal trend in profitabilityNon – availability of data for relevant financial year Related party transactions Foreign exchange earnings to sales Employee cost to sales

All

right

s re

serv

ed

| 32

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

AUDIT TRENDS – PHARMACEUTICALS

Relying on customs databases, imported drugs taken as comparables for imported API (Active Pharmaceutical ingredient)Reliance on CUPs without regard to comparability factorsInnovative features of taxpayer’s drugs not considered Differences in market conditions, quality and pharmacopoeia standards ignored

Aztec Ruling emphasized on robust comparability analysis for CUP

17

All

right

s re

serv

ed

| 33

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

IT / ITES

Revenue continues to impose high adjustments Risk differential between captive and independent units ignoredLopsided selection of comparables – rejection of loss making companies and inclusion of high profit companiesGuidance from Mentor Graphics and Egain Communication

Comparables with extraordinary results should be closely scrutinized while benchmarking captiveUndertake adjustments for differences in risk, working capital and intangibles

Arbitrary adjustments continue despite guidance from Tribunal Rulings

All

right

s re

serv

ed

| 34

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

Once a defaulter – always a defaulterRevenue refuses to lower its benchmarksCase of hidden IPs (reverse royalties) becoming stronger – FMCG’sStay of demand – a big challengeGetting appeal affect – a nightmareUse of secret comparablesFAR analysis – disregard taxpayers businessRevenue target driven approachAd-hoc economic adjustments – rule of thumb applied in most casesLopsided selection of comparables – rejection of loss making companies and inclusion of high profit companiesWide variation in the sales turnover of comparable companies – use of filtersUpdation of comparables with current year’s data during audit proceedings –contemporaneous principle

TRENDS IN AUDIT / ASSESSMENTS

18

All

right

s re

serv

ed

| 35

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

Flawed comparability analysis resulting in high adjustments for captive BPO / KPO unitUnrealistic benchmark for captive service providers:

IT enabled services – 30-35%Software development – 21-25%

Aggregation of transactionsArm’s length rangeEnhanced cost of compliance due to onerous documentationPenalties

Upward adjustmentsDocumentation related

TRENDS IN AUDIT (CONT)

All

right

s re

serv

ed

| 36

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

ALTERNATE DISPUTE RESOLUTION

MAP assuming greater importanceHigh value adjustmentsDelay in administrative appeal processNon binding nature of MAP Memoranda on MAP - Indian treaties with US and UK

Penalty proceedings, tax demand and interest to be held in abeyance until MAP outcome is knownRecent CBDT Circular allows even Indian taxpayer to apply for suspension of tax demandMAP - a strategic option for US / UK multinationals

Competent authority grappling with a backlog of casesNeed for an overhaul of administrative machinery to deal with MAP casesAdvance Pricing Agreement – still a far cry???

19

All

right

s re

serv

ed

| 37

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

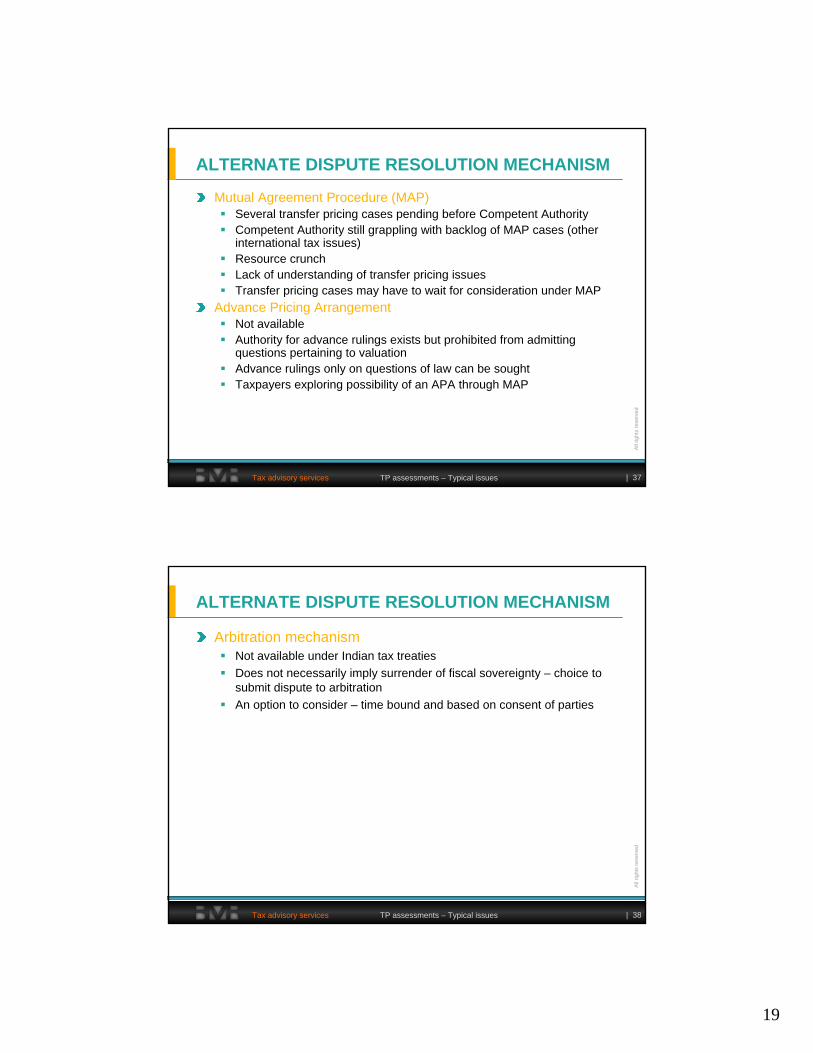

ALTERNATE DISPUTE RESOLUTION MECHANISM

Mutual Agreement Procedure (MAP)Several transfer pricing cases pending before Competent AuthorityCompetent Authority still grappling with backlog of MAP cases (other international tax issues)Resource crunch Lack of understanding of transfer pricing issuesTransfer pricing cases may have to wait for consideration under MAP

Advance Pricing Arrangement Not availableAuthority for advance rulings exists but prohibited from admitting questions pertaining to valuationAdvance rulings only on questions of law can be soughtTaxpayers exploring possibility of an APA through MAP

All

right

s re

serv

ed

| 38

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

ALTERNATE DISPUTE RESOLUTION MECHANISM

Arbitration mechanismNot available under Indian tax treatiesDoes not necessarily imply surrender of fiscal sovereignty – choice to submit dispute to arbitrationAn option to consider – time bound and based on consent of parties

20

| 39

All

right

s re

serv

ed|

Tax advisory services TP assessments – Typical issues

RECENTDEVELOPMENTS

All

right

s re

serv

ed

| 40

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

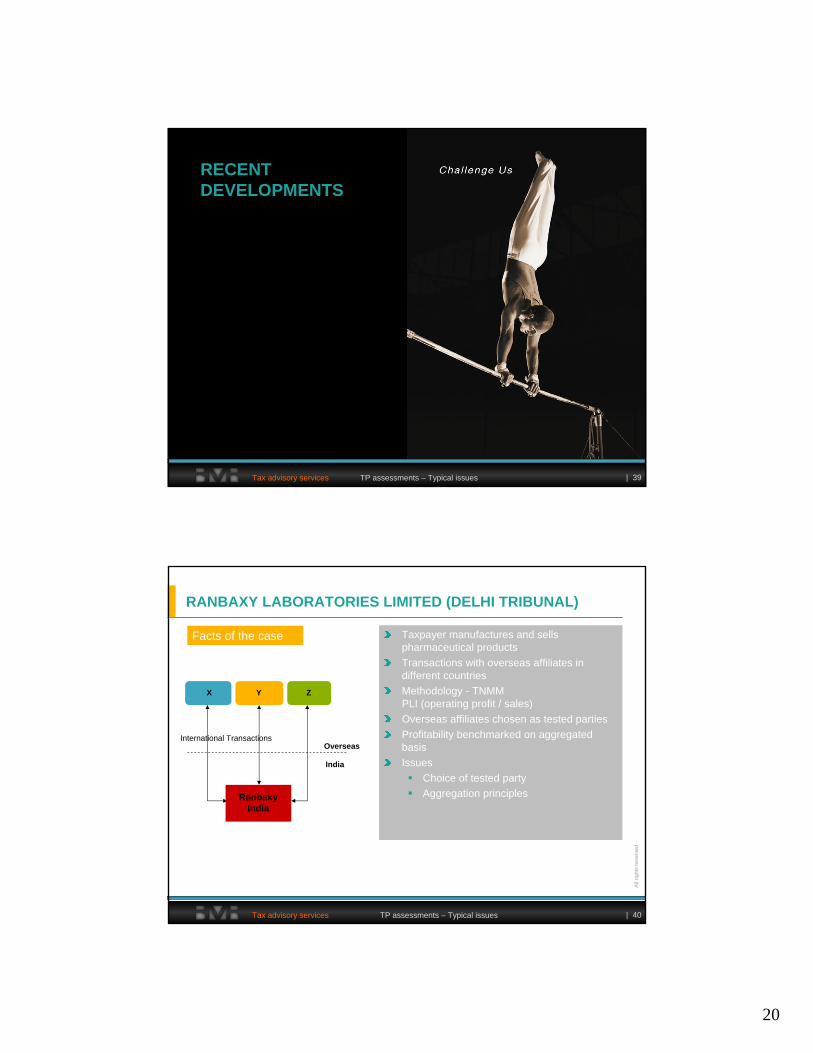

RANBAXY LABORATORIES LIMITED (DELHI TRIBUNAL)

Taxpayer manufactures and sells pharmaceutical products Transactions with overseas affiliates in different countriesMethodology - TNMM PLI (operating profit / sales)Overseas affiliates chosen as tested partiesProfitability benchmarked on aggregated basisIssues

Choice of tested partyAggregation principles

Facts of the case

X Y Z

India

OverseasInternational Transactions

Ranbaxy India

21

All

right

s re

serv

ed

| 41

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

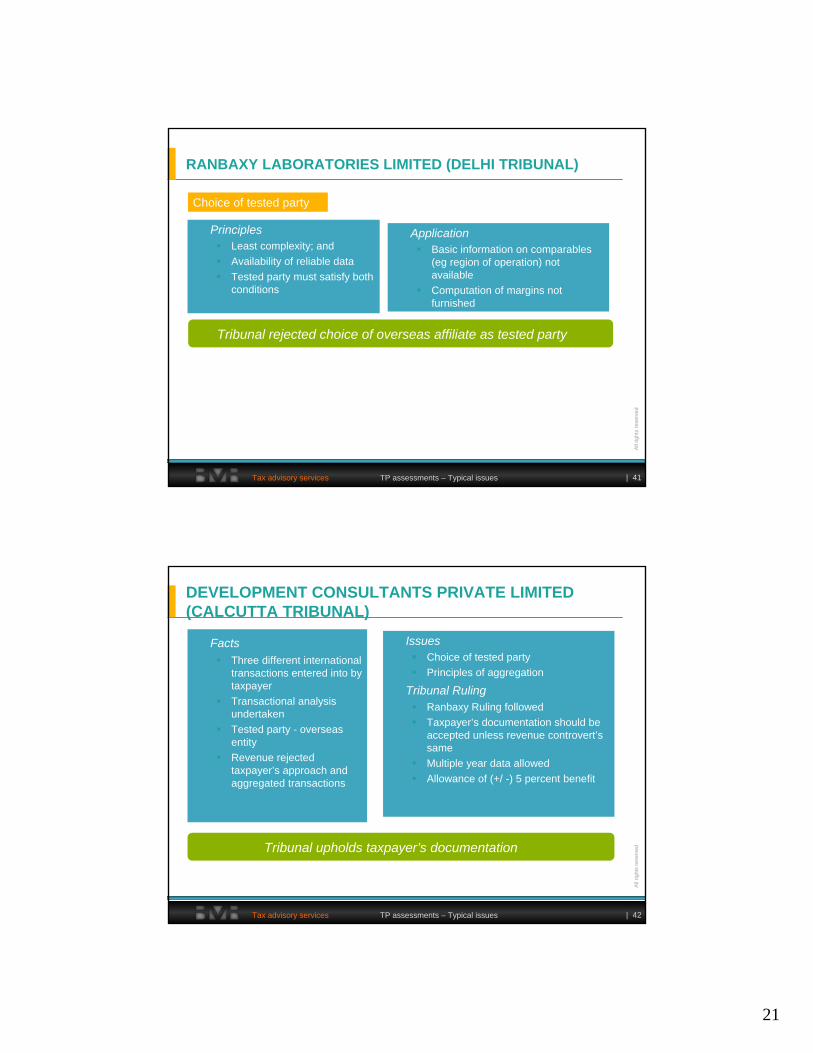

PrinciplesLeast complexity; andAvailability of reliable dataTested party must satisfy both conditions

Application Basic information on comparables (eg region of operation) not availableComputation of margins not furnished

Choice of tested party

RANBAXY LABORATORIES LIMITED (DELHI TRIBUNAL)

Tribunal rejected choice of overseas affiliate as tested party

All

right

s re

serv

ed

| 42

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

Facts Three different international transactions entered into by taxpayerTransactional analysis undertakenTested party - overseas entityRevenue rejected taxpayer’s approach and aggregated transactions

IssuesChoice of tested partyPrinciples of aggregation

Tribunal RulingRanbaxy Ruling followedTaxpayer’s documentation should be accepted unless revenue controvert’s sameMultiple year data allowedAllowance of (+/ -) 5 percent benefit

DEVELOPMENT CONSULTANTS PRIVATE LIMITED (CALCUTTA TRIBUNAL)

Tribunal upholds taxpayer’s documentation

22

All

right

s re

serv

ed

| 43

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

FactsTransfer Pricing Officer (TPO) issued notice calling for informationTaxpayer sought adjournment number of times before furnishing documentsRevenue ruled that taxpayer failed to comply with documentation requirements Sufficient ground for initiation of penalties

CARGILL INDIA PRIVATE LIMITED (DELHI TRIBUNAL)

Key PrinciplesRevenue must call only for prescribed informationRevenue should be specific in request for documentsNotice imposing penalty must specify default and provision invokedVague penalty notices are invalid

Held that documentation requirements were met and penalty notices were invalid

All

right

s re

serv

ed

| 44

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

Key PrinciplesImportance of adjustments following earlier Rulings (Aztec and Mentor Graphics) Companies with extraordinary results need to be closely scrutinized Comparables to be rejected where no segmental results availableConsistent accounting policies to be adopted across comparables and taxpayerTurnover screening criterion should be applied consistently

E- GAIN COMMUNICATIONS (PUNE TRIBUNAL)

India

USA

Software services

Parent

Cost plus 5 percent

E-Gain

FactsTaxpayer is a captive software service provider Methodology – TNMM

Cost plus 5 percent upheld by Tribunal

23

All

right

s re

serv

ed

| 45

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

FactsTaxpayer engaged in three distinct businesses Separate transfer pricing analysis for each businessTPO insisted on combined analysis Assessing Officer (AO) disallowed license fee payments made to affiliates

IssuesAggregation of transactions

Tribunal RulingHighlights importance of adjustmentsFollowed Ranbaxy (Aggregation)Emphasis on robust analysis of functions, assets and risksIn view of RBI’s approval for license fee payments, AO should have closely examined transfer pricing analysis

STAR INDIA PRIVATE LIMITED (MUMBAI TRIBUNAL)

With above guidance, Tribunal remanded case to AO

All

right

s re

serv

ed

| 46

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

AZTEC SOFTWARE (BANGALORE TRIBUNAL)

Aztec India has a wholly owned US subsidiary (Aztec US)Aztec US provides marketing and onsite services for Aztec IndiaAztec US receives cost-plus remuneration for marketing and onsite services

Several procedural issues including validity of reference to TPOWhether arm’s length price for services was correctly computed?

CBDT circular (compulsory reference where transaction value exceedsINR 50 million ) valid and binding on departmentNo tax avoidance to be proved for referenceNeither reference nor determination of arm’s length price can be arbitrary (due consideration to principles of natural justice) Appellate body cannot reject price determined by taxpayer without itself determining arm’s length price

Facts

Issue

Decision

24

All

right

s re

serv

ed

| 47

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

AZTEC SOFTWARE (BANGALORE TRIBUNAL)

Industry average can not be used as CUPComparability requires that appropriate adjustments should be madeWhere cost plus model is used cost base too should be examined10 comparable companies held not to be enough (on the facts of Aztec’s case)Multiple year data not to be used unless influence of prior year’s data on current year’s data is demonstratedRevenue and taxpayer to equally share in burden of proof where transfer pricing methodology is changedOECD transfer pricing guidelines referred extensivelyUS regulations referred to in case of CUP and cited as ‘principles of universal application’Case remanded to jurisdictional officer with above guidance

Decision (CONT)

All

right

s re

serv

ed

| 48

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

Mentor Graphics India is a captive service provider providing software development support to its parent company in USA

Choice of comparable companies for determining arm’s length price

Emphasis on comprehensive FAR analysis while applying TNMM Use of current year data for computing arm’s length priceClose scrutiny of high profit and loss making companies while benchmarking captiveComputation of arm’s length range based on several arm’s length pricesTPO can undertake a fresh search only if apparent deficiencies exist in taxpayer’s documentationOECD guidelines and US Court Ruling relied uponBased on five comparable companies, MGI held to be within arm’s length range

Facts

Issues

Tribunal Ruling

MENTOR GRAPHICS (DELHI TRIBUNAL)

25

All

right

s re

serv

ed

| 49

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

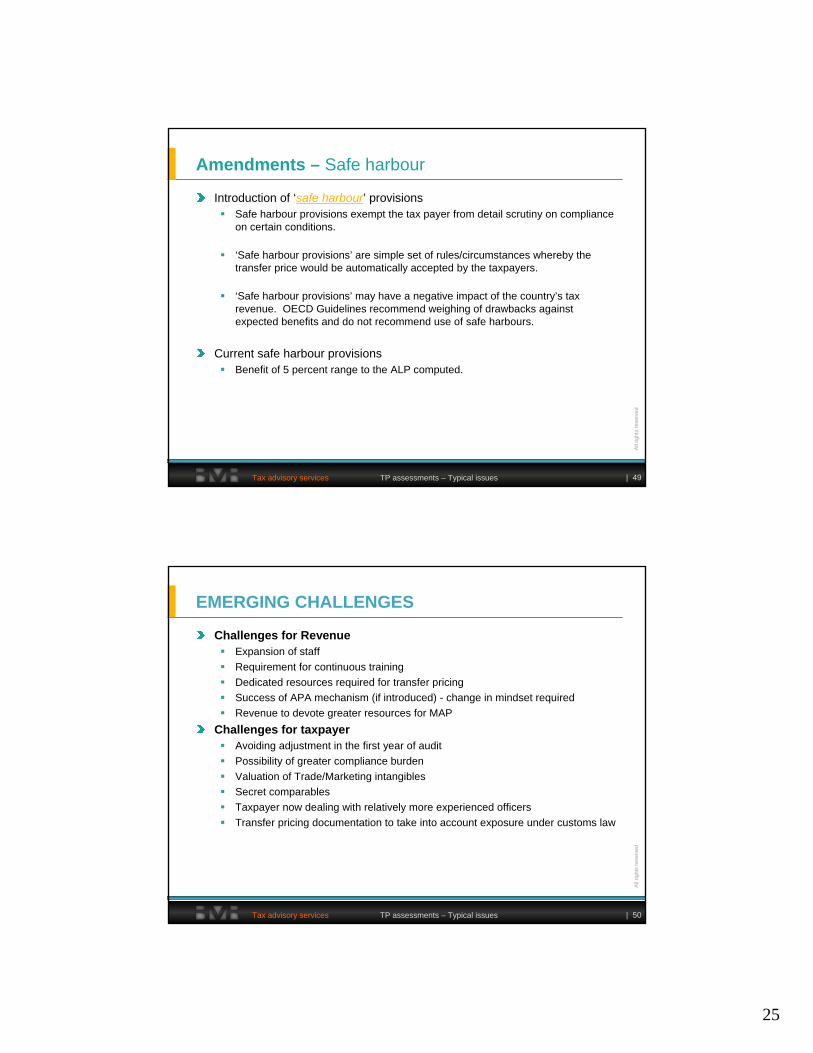

Amendments – Safe harbour

Introduction of ‘safe harbour’ provisionsSafe harbour provisions exempt the tax payer from detail scrutiny on compliance on certain conditions.

‘Safe harbour provisions’ are simple set of rules/circumstances whereby the transfer price would be automatically accepted by the taxpayers.

‘Safe harbour provisions’ may have a negative impact of the country’s tax revenue. OECD Guidelines recommend weighing of drawbacks against expected benefits and do not recommend use of safe harbours.

Current safe harbour provisionsBenefit of 5 percent range to the ALP computed.

All

right

s re

serv

ed

| 50

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

EMERGING CHALLENGES

Challenges for RevenueExpansion of staffRequirement for continuous trainingDedicated resources required for transfer pricingSuccess of APA mechanism (if introduced) - change in mindset requiredRevenue to devote greater resources for MAP

Challenges for taxpayerAvoiding adjustment in the first year of auditPossibility of greater compliance burden Valuation of Trade/Marketing intangiblesSecret comparablesTaxpayer now dealing with relatively more experienced officers Transfer pricing documentation to take into account exposure under customs law

26

All

right

s re

serv

ed

| 51

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

KEY LEARNINGS

Adequate planning required

Emphasis on comprehensive FAR analysis

Suitable comparability adjustments should be made

Justification for the use of Multiple year dataReasons for the rejection/ selection of comparables to be adequately documentedDisclosure of the characteristics of international transactions including quantitative information is necessaryReliance on OECD guidelines Learning from past year assessment experienceMAP can be explored as alternative dispute resolution avenue

All

right

s re

serv

ed

| 52

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

RISK MANAGEMEMT STRATEGIES - AUDITS

Every business is unique - don’t allow the Revenue treat you alike your peersMove away from comp selection to FAR analysisGo beyond single vs multiple year data – trend analysis/ business models / customer profile are areas still untappedBuild a business caseConsistency of submissions to TPO – alignment with documentationBenefit of Tribunal decisions; though some established principles could see legislative amendments and / or court reviewCIT(A) - a window for submitting additional analysis / documentationReliance on global experiences – APAs / audits in other jurisdictions / global benchmarking documentationDo you update FIN 48 analysisPenalty exposure

27

All

right

s re

serv

ed

| 53

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

Taxpayers to prepare robust documentation to support their transfer pricing policies. This entails the following:

Greater reliance on market, industry and competitor analysis Emphasis on economic condition surrounding the inter-company transactionSeeking alternative approach to corroborate transfer pricing analysis (alternative transfer pricing method)Document ‘business response' to challenges faced in the current economic slowdownState clear rationale for accept / reject decisions for comparable companies

Loss making comparables to be considered – sufficient rationale to be providedBroad-basing comparable set by including regional companies Financial data for multiple years may be used to demonstrate changes in business cycleRe-look at pricing strategies ensuring flexibility to changing economic environment

TAXPAYERS’ BAIL OUT…

All

right

s re

serv

ed

| 54

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issues

CONCLUSION

Special Bench in Aztec settled procedural law on transfer pricing – Tribunal gradually laying down substantive lawAlignment with international principles – greater reliance on OECD Guidelines and US regulationsRecent Tribunal decisions have been practical and stress on application of fundamental transfer pricing principles (Robust FAR analysis andComparability adjustments)Guidance available on

Aggregation of transactionsChoice of tested partySelection of comparables

Tribunal making up for lack of administrative guidanceFor taxpayer comprehensive documentation key to minimize transfer pricing risk

28

All

right

s re

serv

ed

| 55

All

right

s re

serv

ed

Tax advisory services TP assessments – Typical issuesC h a l l e n g e U s