transport and logistics - singapore economic · pdf fileprofitability and the competition...

TRANSCRIPT

Asia Competition Barometer Transport and logisticsAn Economist Intelligence Unit report

Supported by

© The Economist Intelligence Unit Limited 2012 1

Asia Competition BarometerTransport and logistics

Contents

Preface 2

Executive summary 3

Asia’s growing importance for corporate performance and global competitiveness 5

Competition and profitability at Asian firms 8 Competition: Rising 8

Case study: APL Logistics 13

Profitability:Onthedeclineoverall,butpocketsofgrowthexist 10

World trade 12

Positioning for success in Asia 14 Resilientdemand:IndustrygrowthwillcomefromAsia 14

ProfitingfromAsia’sevolvingmanufacturingfootprints 15

Case study: DHL Express 16

Outlook 17

Barometer methodology 19

© The Economist Intelligence Unit Limited 20122

Asia Competition BarometerTransport and logistics

SupportedbySingapore’sEconomicDevelopmentBoard(EDB),theEconomistIntelligenceUnithasdevelopedtheAsiaCompetitionBarometerwiththeaimofunderstandingthechangingmarketdynamicsinkeysectorsandassessingtheintensityofcompetitioninthem.Drawinguponcompany-leveldataonprofitabilityandotherindicators,theBarometerquantifiesthechangingdynamicsofcompetitivenessinAsiaforselectindustriesbetween2004and2009.

ThisreportfocusesontheBarometerfindingsforthetransportandlogistics(T&L)sector.Assessingauniverseofover275T&Lcompaniesthatarepubliclylistedineightcountries—China,India,Indonesia,Malaysia,thePhilippines,Singapore,ThailandandVietnam—theBarometerexamineschangingprofitabilityandthecompetitionlandscapefortheT&Lsector.

Otherreportsinthisserieslookattheinformationtechnologyservices,precisionengineering,petrochemicalsandchemicals,andpharmaceuticalssectorsinAsia.

January2012

Preface

© The Economist Intelligence Unit Limited 2012 3

Asia Competition BarometerTransport and logistics

Executive summary

WhatdoestheemergenceofAsiaasamajorengineofglobaleconomicgrowthmeanforcompaniesoperatingintheregion?Asia’srobusteconomicoutlook—coupledwithdiminishedgrowth

prospectsinmanyotherpartsoftheworld—hasattractednewinvestmentintothemarketbothfromregionalplayersandWesternmultinationals.Asaresult,competitionintheregionisexpectedtointensify.Giventhedarkeningglobaleconomicoutlook,andtheexpectedimpactonsomeeconomiesandsectorsintheregion,growthandprofitabilitylookuncertaininthenearterm.Butoverthemediumtolongerterm,Asia’sstrongeconomicfundamentalswillensureconsistentgrowthacrossarangeofindustries.HowarecompaniespositioningthemselvestocapitaliseonAsia’sgrowthopportunitiesoverthenextfewyears?

TheAsiaCompetitionBarometerassessestheintensityofcompetitionandchangingmarketdynamicsinseveralkeysectors.Thisreportexaminesthetransportandlogistics(T&L)sector,whichincludesthefollowingsub-segments:landtransportandtransportviapipelines,watertransport,airtransport,warehousingandsupportactivitiesfortransportationandpostalandcourierservices.

Amongthekeyfindingsofthisreportarethefollowing:

• Asia’s T&L sector has been expanding rapidly, in line with the region’s stellar economic growth. Severalbroadmacroeconomictrends,includingAsia’swideningmanufacturingbase,deeperintra-Asiantradeintegration,risinghouseholdincomes,highurbanisationratesandwidespreadgovernmenteffortstoimproveinfrastructurehaveboosteddemandforT&LservicesinAsia.By2009,nineoutofthetenbiggestcontainerportsintheworldwereinAsia,upfromjustfivein2000.Thisgrowthlookssettocontinue,givenAsia’srelativelyrobusteconomicoutlook.

• The number of players in Asia’s T&L sector, homegrown and global, is rising.Thenumberandsizeofpublicly-listedfirmsintheT&LsectorinAsiahasincreaseddramatically,from199firmsin2004to275in2009.TotalcombinedrevenuesmorethandoubledfromUS$66.1bntoUS$140.8bnduringtheperiod.

© The Economist Intelligence Unit Limited 20124

Asia Competition BarometerTransport and logistics

Meanwhile,inrecognitionofAsia’sincreasingimportancetotheglobalT&Lsector,foreignMNCshavebeenbuildinguptheirpresenceintheregion.

• Competition in Asia’s T&L sector is intensifying, as firms get leaner.Theinfluxofnewplayersintotheregion’sT&Lsectorhasledtoamorecompetitiveoperatingenvironment.Theindustry’slargestpublicly-listedAsianplayerssawtheirmarketsharesdeclinebetween2004and2009,asnewplayers,includingmanylow-costcompetitors,enteredthebusiness.Currenttrendsintheindustrysuggestthatfiercepricecompetitionwillcontinue.Insuchanenvironment,sourcesofcompetitiveadvantagewillemergebothinbigfirmsthatcanreapcostefficienciesandsmallfirmsthatcanservenichesegments.

• Profitability in Asia’s T&L sector has been declining, but pockets of growth exist.Theaveragegrossmarginofpublicly-listedAsianfirmsdeclinedfrom49.8%in2004to39.8%in2009.Competitionisonlyonefactorpushingdownprofits.Anumberofothers—includingtheglobaleconomicdownturn,higherfuelcostsandrisingwages—haveputpressureonmargins.Tomaintainprofitability,manyfirmswillhavetofocusonspecificgrowthniches,suchaslow-costairtravelorexpressandfreightforwardingservices,particularlyinChinaandIndia.

• Rising domestic demand in Asia will change the nature of trade in the region, creating new growth opportunities.AstheglobalbalanceofeconomicpowershiftsfromtheWesttotheEast,andasprivateconsumptioninAsiapicksup,thenatureoftradeflowsintheregionwillchangedramatically.Thoughcomponenttradeisstillhuge,andgrowing,thistrendindicatesashifttowardsmorefinaldemand.Thiswillpushlogisticsproviderstoimprovetheirimportingandintra-regionalcapabilities.Thisalsosuggeststhatshorter-haulfreightcompaniesconcentratingontheregionwillgrowfasterthanthosefocussedonlong-haulroutes,forinstancebetweenAsiaandEurope.Inaddition,smallT&LfirmsabletoserveremotepartsofAsiawhereincomesarerising—suchascommodity-richpartsofIndonesia—standtoboostrevenues.

• Asia’s evolving manufacturing footprints will affect the region’s T&L industry by shifting demand to newer markets.SeveralbroadtrendsarecausingarethinkofAsianmanufacturing,includingrisingwagesinChina,whichareleadingtotheflightoflow-costmanufacturingawayfromthesouthandcoastalareasofthatcountrytoinlandprovincesandneighbouringcountriessuchasVietnam.T&Lfirmswillneedtoadapttothesechangingdynamicsinordertomaintainprofitability.

© The Economist Intelligence Unit Limited 2012 5

Asia Competition BarometerTransport and logistics

Asia’s growing importance for corporate performance and global competitiveness

Overthepastdecade,Asiahasrapidlygrowninimportancetotheglobaleconomy.ItsshareofglobalGDP,measuredinpurchasing-powerparityterms,increasedfrom26.8%in2001to33.8%in2010.1

By2016,theEconomistIntelligenceUnit(EIU)expectsthisproportiontoriseto38.9%.ThereareseveralbroadtrendsassociatedwithAsia’srapidgrowthanddevelopmentthathavebeen

drivingitstransportandlogistics(T&L)sector.2First,intra-Asiantradehasboomedasmanufacturingsupplychainshavespreadanddeepenedacrosstheregion.AccordingtotheWorldTradeOrganisation(WTO),theshareofintra-AsianexportsasaproportionoftotalAsianexportshasrisenfrom42.1%in1990to52.6%in2010.3Theseintricatesupplychainshavebecomefundamentaltoglobalmanufacturingoutput,asshownbythetradedisruptionsfollowingnaturaldisastersinJapanandThailandin2011.Increasinglyintegratednetworkshaveboosteddemandfor,amongotherthings,contractlogistics,expressandfreightforwardingservices,aswellasunifiedservicestosmoothencustomsclearance.

Second,risingincomesintheregionasaresultofbroadereconomicgrowthhaveledtogreaterprivateconsumption,sparkinggrowthinimports.Forinstance,thecompositionofChina’simportsisshiftingfromrawmaterialsandintermediatecomponentsforexport-orientedmanufacturingtoanincreasingamountofconsumergoods.4Asia’slogisticsmarketwillsurpassNorthAmerica’sby2013,saysProcurementIntelligenceUnit,abusinessintelligenceprovider.5ItexpectsAsia’stransportandwarehousingsector’sshareoftheglobalmarkettorisefrom18%in2010to21%by2013.

Today,some70%ofglobalcontainerthroughputishandledbyportsinAsia.6By2009,nineoutofthetenbiggestcontainerportsintheworldwereinAsia,upfromjustfivein2000.Indeed,AsiaisincreasinglyimportantforcorporateperformanceintheT&Lsectorglobally.“Asiawithoutanydoubtisthemostactiveregionintheworld.Itisflowering.TheworldtendstofocusonChina,buttherealityisthatthereareseveraleconomiesherethataregrowingveryfast,”NilsAndersen,CEOofMaersk,aDanishconglomeratewithbigtransportationandenergybusinesses,wasquotedassayinginMay2011.7“Soifwelookattrade,weseeourintra-Asiabusinessbeingthemostdynamic.WeseetradebetweenAsiaandLatinAmericagrowingfast,thesamewithAfrica.”

From2004to2008,theproportionofMaersk’stotalallocatedassetsinAsiarosefrom6.1%to16.5%.8 Meanwhile,Maersk’sAsiarevenuesalmostdoubledfrom2005to2010,withAsia’sshareofglobalrevenuesrisingfrom11%to13%overthatsameperiod.

1AsiahereincludesBangladesh,China,HongKong,Indonesia,India,Japan,SouthKorea,Malaysia,Myanmar,Philippines,Pakistan,Singapore,SriLanka,Thailand,Taiwan,andVietnam.

2 The transport and logistics (T&L)sectorincludesthefollowingsub-segments:landtransportandtransportviapipelines,watertransport,airtransport,warehousingandsupportactivitiesfortransportation and postal and courierservices.

3 International Trade Statistics.WorldTradeOrganisation.2001and2011.

4“Intra-Asiatrafficgrowsascarriersaddservices”,Cargonews Asia,Sep12th2011

5“Asianlogisticsectortobecomedriverforglobalgrowth”,ProcurementIntelligenceUnit,Sep2nd2011

6“Containershipping:Successfulturnaround”,DeutscheBankResearch,Mar28th 2011

7“TheViewFromTheBridge”,Forbes Asia Magazine,Jun6th 2011

8ThisfiguredoesnotincludeMaersk’sassetsthatarenotallocatedtoaspecificregion.

© The Economist Intelligence Unit Limited 20126

Asia Competition BarometerTransport and logistics

Risingincomeshavealsocausedastrongsurgeindomestictravel.TheInternationalAirTransportAssociation(IATA)forecaststhattheairindustrywillhavetohandle800mmorepassengersand12.5mextratonnesofinternationalcargoby2014.9MuchofthatgrowthwillcomefromAsia.“Asiaisthemostprofitableregionintheworld,”GiovanniBisignani,IATA’sdirectorgeneral,saidinearly2011.10“Ofthe800mnewpassengerswhowillflyby2014,360mwillbeinAsia-Pacificand214mofthoseinChina.”

Inadditiontoboostingrevenuesattraditional,premiumtravelserviceproviders,thisgrowthindisposableincomeshassparkedthedevelopmentofahugelow-costcarrier(LCC)market.TheLCC’sshareoftheintra-Asiantravelmarket,intermsofpassengerseats,increasedfrom1.1%in2001to17.7%in2010.11Inthepassengerairlinessector,forexample,Jetstar,anewerLCC,hasgrowntoaccountformorethan25%oftheoperatingprofitatQantas,itsparentcompany,inunderadecade.ThesenewentrantstotheT&Lsectorcandisrupttraditionalbusinessmodels,puttingpressureonmarginsattheestablishedfirms.Thesuccessoflow-costcarriers,forinstance,hasforcedincumbentlegacycarrierstoofferbetterandmorecompetitiveproducts.Tomaintainprofitability,theymayhavetotrimtheircostbase,asPhilippineAirlinesdidin2010byretrenching3,000ofitsemployees.

ThethirdtrenddrivingAsia’sT&Lsectoristhehighurbanisationrateintheregion,whichhascreatednumerousopportunitiesforT&Lfirms.TheAsianDevelopmentBankbelievesthatAsia’surbanpopulationisgrowingbyabout44mpeopleayear—or120,000peopleaday.Thisisboostingdemandforinter-regionaltransitservices—asmigrantstravelbackandforthfromtheirruralprovinces—aswellasintra-citycommuterservices.Thesenewurbanresidentswillalsokeeppushingupdemandforarangeofgoodsandservices,whichwillinturnensureconsistentgrowthforthewarehousing,supplychainmanagement,andlogisticssectors.

Fourth,manygovernmentsintheregion,fromIndiatoIndonesia,aremakingconcertedeffortstopluginfrastructuredeficitsintheircountries.Asia’sgenerallypoorinfrastructurenetworkshavelongbeenadragongrowthintheT&Lsector.Aspublicandprivatesectorinvestmentshelpconstructnewairports,renovateoldseaports,andbuildbetterhighways,theywillboostproductivityintheT&Lsector.

ForeignT&LMNCshavebeenoperatinginAsiaforseveraldecades.Recently,inrecognitionofAsia’sgrowingimportance,theyhavebeeninvestingheavilyintheregion.BetweenJanuary2003andAugust2011,fDiMarkets,aresearchhouse,recordedatotalof670T&LinvestmentprojectsinAsiafrom217companies.12ManyofthoseinvestmentsoriginatedfromtheUS(18%oftheinvestmentprojects),Germany(18%)andJapan(9%).Meanwhile,thetopthreeinvestmentdestinationmarketswereChina(35%oftheinvestmentprojects),India(19%)andVietnam(8%).

Whiletherearenumerousopportunities,T&LfirmsinAsiawillalsocontinuetofaceseveralchallenges.InChina,forinstance,firmshavetocontendwithnon-uniformtaxratesatvariouslinksofthesupplychain,andrepeatedtaxation.Inaddition,highroadandbridgetollsaccountforasmuchasone-thirdofthecostsoflogisticsenterprisesinChina.

Meanwhile,eventhoughgovernmentsareprioritisinginfrastructureinvestments,theywillfindithardjusttokeeppacewiththeregion’storriddemandgrowth.McKinsey,aconsultancy,believesthatIndia’snetworkofroads,rail,andwaterwayswillactasapossiblebrakeonthecountry’sgrowth,asitwillbeunabletoaccommodatetheexpectedthreefoldincreaseinfreightmovementoverthecomingdecade.

RecentfreetradeagreementssuchasthosesignedbetweentheAssociationofSoutheastAsianNations

9TheInternationalAirTransportAssociation,Feb14th2011

10“Chinaairpassengergrowthtoleadglobalmarket”,China Daily,Feb16th2011

11CAPACentreforAviation

12ThisincludesGreenfieldinvestmentsaswellasadditionstoexistingprojects.

© The Economist Intelligence Unit Limited 2012 7

Asia Competition BarometerTransport and logistics

(ASEAN)andAustraliaandNewZealand,China,andIndia,arehasteningintegrationofAsiancountries.Between2000and2011,thenumberofbilateralFTAsrecordedbytheWTOthatinvolvedanAsiancountryincreasedfrom8to74.However,theregion’swebofcomplexnon-tariffbarrierswillcontinuetoposechallengestoT&Lfirms.Otheroperationalchallengesincludebureaucracy,cross-bordertariffs,corruptionandtalentshortages.ThesechallengescanvaryconsiderablyfromoneAsiancountrytothenext;hencefirmsfaceaheterogeneousoperatingenvironmentinAsia.Environmentalregulationsmayalsoeventuallyhaveanimpactontheindustry.

© The Economist Intelligence Unit Limited 20128

Asia Competition BarometerTransport and logistics

Competition and profitability at Asian firms

ReflectingtheboominggrowthinAsia’sT&Lsector,thenumberandsizeofpublicly-listedfirmsinAsiahasincreaseddramatically.Thetotalnumberoflistedcompaniesintheindustryincreasedby

40%,from199firmsin2004to275in2009,whiletheirtotalcombinedrevenuemorethandoubledfromUS$66.1bntoUS$140.8bn.Theinfluxofnewplayers,bothAsianandnon-Asian,intotheregion’sT&Lsectorhasledtoamorecompetitiveoperatingenvironment.

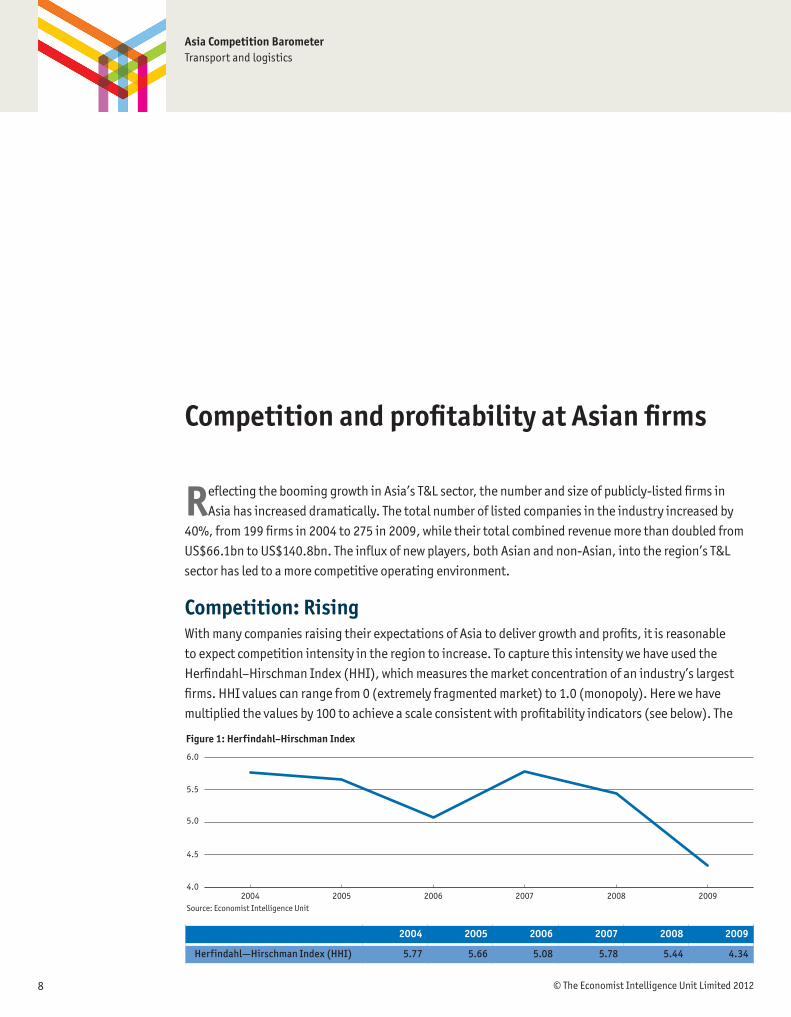

Competition: RisingWithmanycompaniesraisingtheirexpectationsofAsiatodelivergrowthandprofits,itisreasonabletoexpectcompetitionintensityintheregiontoincrease.TocapturethisintensitywehaveusedtheHerfindahl–HirschmanIndex(HHI),whichmeasuresthemarketconcentrationofanindustry’slargestfirms.HHIvaluescanrangefrom0(extremelyfragmentedmarket)to1.0(monopoly).Herewehavemultipliedthevaluesby100toachieveascaleconsistentwithprofitabilityindicators(seebelow).The

Figure 1: Herfindahl–Hirschman Index

4.0

4.5

5.0

5.5

6.0

200920082007200620052004Source: Economist Intelligence Unit

2004 2005 2006 2007 2008 2009

Herfindahl—Hirschman Index (HHI) 5.77 5.66 5.08 5.78 5.44 4.34

© The Economist Intelligence Unit Limited 2012 9

Asia Competition BarometerTransport and logistics

13Ameasureofthesizeofcompanies in relation to the industry,andanindicatoroftheamountofcompetitionamongthem,theHHIisdefinedasthesumofthesquaresofthemarketsharesofthe50largestfirmsfromtheuniverseof275listedcompaniesassessed.FormoreinformationontheBarometermethodology,pleaserefertothelastsectioninthisreport.

HHIforAsia’sT&Lindustrydecreasedfrom5.77in2004to4.34in2009(seeFigure1),signifyingthatthe50biggestfirmsintheBarometerdecreasedtheirmarketconcentrationoverthatperiod.13

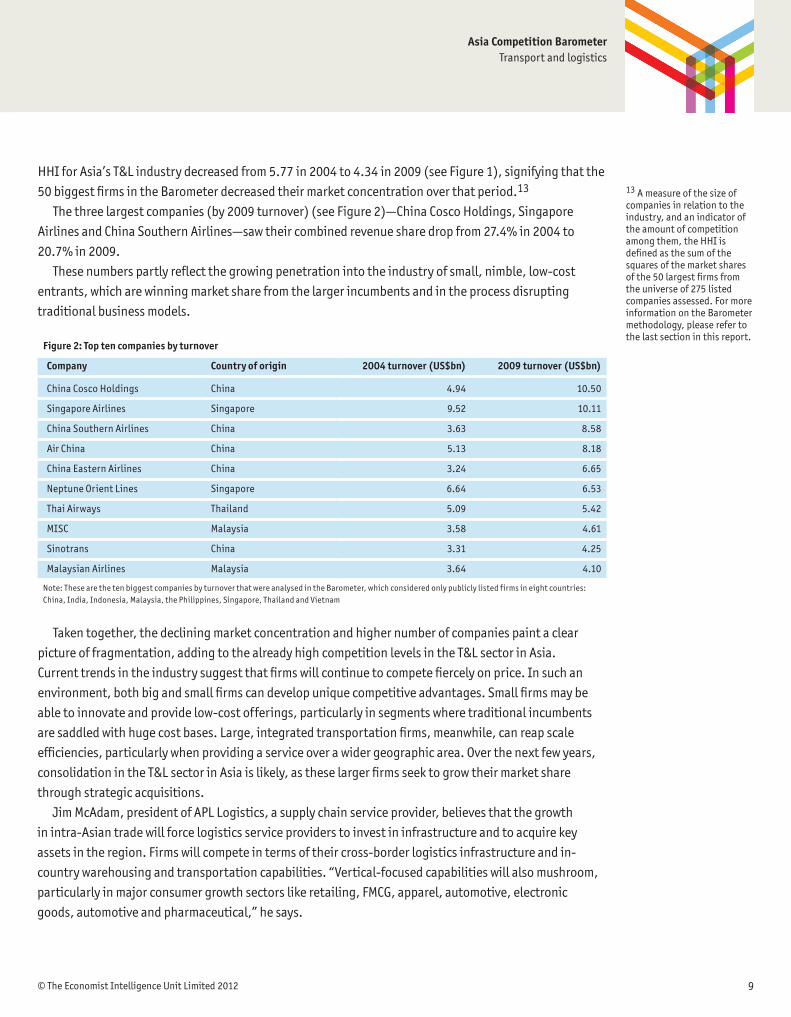

Thethreelargestcompanies(by2009turnover)(seeFigure2)—ChinaCoscoHoldings,SingaporeAirlinesandChinaSouthernAirlines—sawtheircombinedrevenuesharedropfrom27.4%in2004to20.7%in2009.

Thesenumberspartlyreflectthegrowingpenetrationintotheindustryofsmall,nimble,low-costentrants,whicharewinningmarketsharefromthelargerincumbentsandintheprocessdisruptingtraditionalbusinessmodels.

Figure 2: Top ten companies by turnover

Company Country of origin 2004 turnover (US$bn) 2009 turnover (US$bn)

ChinaCoscoHoldings China 4.94 10.50

SingaporeAirlines Singapore 9.52 10.11

ChinaSouthernAirlines China 3.63 8.58

AirChina China 5.13 8.18

ChinaEasternAirlines China 3.24 6.65

NeptuneOrientLines Singapore 6.64 6.53

ThaiAirways Thailand 5.09 5.42

MISC Malaysia 3.58 4.61

Sinotrans China 3.31 4.25

MalaysianAirlines Malaysia 3.64 4.10

Note:ThesearethetenbiggestcompaniesbyturnoverthatwereanalysedintheBarometer,whichconsideredonlypubliclylistedfirmsineightcountries:China,India,Indonesia,Malaysia,thePhilippines,Singapore,ThailandandVietnam

Takentogether,thedecliningmarketconcentrationandhighernumberofcompaniespaintaclearpictureoffragmentation,addingtothealreadyhighcompetitionlevelsintheT&LsectorinAsia.Currenttrendsintheindustrysuggestthatfirmswillcontinuetocompetefiercelyonprice.Insuchanenvironment,bothbigandsmallfirmscandevelopuniquecompetitiveadvantages.Smallfirmsmaybeabletoinnovateandprovidelow-costofferings,particularlyinsegmentswheretraditionalincumbentsaresaddledwithhugecostbases.Large,integratedtransportationfirms,meanwhile,canreapscaleefficiencies,particularlywhenprovidingaserviceoverawidergeographicarea.Overthenextfewyears,consolidationintheT&LsectorinAsiaislikely,astheselargerfirmsseektogrowtheirmarketsharethroughstrategicacquisitions.

JimMcAdam,presidentofAPLLogistics,asupplychainserviceprovider,believesthatthegrowthinintra-Asiantradewillforcelogisticsserviceproviderstoinvestininfrastructureandtoacquirekeyassetsintheregion.Firmswillcompeteintermsoftheircross-borderlogisticsinfrastructureandin-countrywarehousingandtransportationcapabilities.“Vertical-focusedcapabilitieswillalsomushroom,particularlyinmajorconsumergrowthsectorslikeretailing,FMCG,apparel,automotive,electronicgoods,automotiveandpharmaceutical,”hesays.

© The Economist Intelligence Unit Limited 201210

Asia Competition BarometerTransport and logistics

case study APL Logistics

APL Logistics: Investments in assets, technology and talentAPLLogistics,asupply-chainserviceprovider,hasenjoyeddouble-

digitannualrevenuegrowthinAsiaoverthepastfiveyears,exceptin2009whentheglobaleconomywasinrecession.In2010,itsAsiarevenuesgrew37%yearonyear,comparedwith26%growthinnon-Asiarevenues.

“Today,Asiaaccountsfor26%ofAPLLogistics’globalrevenue,upfrom17%in2005,”saysJimMcAdam,thefirm’spresident.

MrMcAdamidentifiesseveralfactorsthathavedrivenprofitabilityatAPL.Theseincludeeconomiesofscale,closecostcontrol(particularlyforoperationalandpersonnelcosts),smarterprocurementpractices,streamlinedprocesses(including,wherepossible,centralisingback-roomoperationsinaffordableregionalorglobalcenters),andflexibilitywithexternalinfrastructureandassets.Healsocitesselectiveinvestmentinproductivity-boostingtechnologyandbettercollaborationwiththird-partylogisticsservicescompanies.

MrMcAdamalsorecognisestheimportanceofserviceinnovationsthatcanboostbothtop-andbottom-linegrowth.HecitestheexampleofAPLLogistics’day-definiteoceanservicesthatallowcustomerstodelivertheirtime-sensitivecargoespredictably,withouthavingtopayexpensiveairfreightrates.

MrMcAdamcontendsthatinordertoensurefutureprofitability,playersintheT&Lindustrywill“needtolookatputtinginplacecost-efficiencystrategiesthatwillallowthemtoreapbenefitsoverthelongerterm,”ratherthanlookingatshort-term,isolatedcostsavings.“Amongotherthings,thiswillinvolveinvestingincriticalgroundinfrastructureandassets,includingtransportroutes.”

Since2007,APLhasbeenprovidingrailservicesinIndia,whileinIndonesiaandVietnamithasinvestedinwarehousing,equipmentandtechnology.

“Manyoftheseemergingcountriesdon’thaveadequateinfrastructureforstate-of-the-artdomesticsupplychains,”hetoldThe Journal of Commerce,atradepublication,inaseparateinterviewinSeptember2011.1“Asoperatorswecaneitherwaitforgovernmentsorprivateenterprisetomovefirst,orwecanputourownmoneyintohelpdevelopitfaster.Wearedoingthelatter.”

Inparticular,hebelievesthatT&LfirmsinAsiaaregoingtocompeteintermsoftechnologyandtalent.Advancedplanningandsupply-chainoptimisationtechnologieswillbecrucial,hesays.Meanwhile,asdemandgrowsforknowledge-basedconsultancyservices,hesaysthat“hiringtherightskillsetsattherightpricesisakeytoo.Inthesamevein,itisimportanttoinvestintrainingandpeopledevelopment.”

1“APLLogisticsChiefSaysAsset-BasedModelKey”,The Journal of Commerce,Sep9th2011

© The Economist Intelligence Unit Limited 2012 11

Asia Competition BarometerTransport and logistics

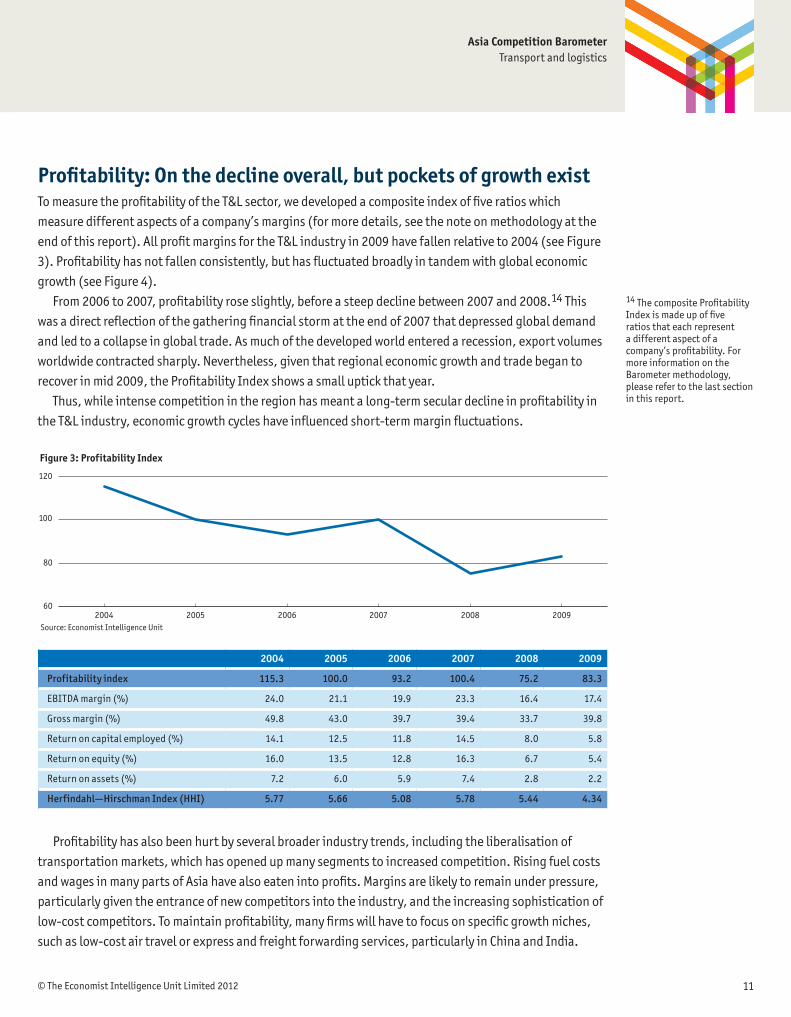

Profitability: On the decline overall, but pockets of growth existTomeasuretheprofitabilityoftheT&Lsector,wedevelopedacompositeindexoffiveratioswhichmeasuredifferentaspectsofacompany’smargins(formoredetails,seethenoteonmethodologyattheendofthisreport).AllprofitmarginsfortheT&Lindustryin2009havefallenrelativeto2004(seeFigure3).Profitabilityhasnotfallenconsistently,buthasfluctuatedbroadlyintandemwithglobaleconomicgrowth(seeFigure4).

From2006to2007,profitabilityroseslightly,beforeasteepdeclinebetween2007and2008.14 This wasadirectreflectionofthegatheringfinancialstormattheendof2007thatdepressedglobaldemandandledtoacollapseinglobaltrade.Asmuchofthedevelopedworldenteredarecession,exportvolumesworldwidecontractedsharply.Nevertheless,giventhatregionaleconomicgrowthandtradebegantorecoverinmid2009,theProfitabilityIndexshowsasmalluptickthatyear.

Thus,whileintensecompetitionintheregionhasmeantalong-termseculardeclineinprofitabilityintheT&Lindustry,economicgrowthcycleshaveinfluencedshort-termmarginfluctuations.

Figure 3: Profitability Index

60

80

100

120

200920082007200620052004Source: Economist Intelligence Unit

2004 2005 2006 2007 2008 2009

Profitability index 115.3 100.0 93.2 100.4 75.2 83.3

EBITDAmargin(%) 24.0 21.1 19.9 23.3 16.4 17.4

Grossmargin(%) 49.8 43.0 39.7 39.4 33.7 39.8

Returnoncapitalemployed(%) 14.1 12.5 11.8 14.5 8.0 5.8

Returnonequity(%) 16.0 13.5 12.8 16.3 6.7 5.4

Returnonassets(%) 7.2 6.0 5.9 7.4 2.8 2.2

Herfindahl—Hirschman Index (HHI) 5.77 5.66 5.08 5.78 5.44 4.34

14ThecompositeProfitabilityIndexismadeupoffiveratios that each represent adifferentaspectofacompany’sprofitability.FormoreinformationontheBarometermethodology,pleaserefertothelastsectioninthisreport.

Profitabilityhasalsobeenhurtbyseveralbroaderindustrytrends,includingtheliberalisationoftransportationmarkets,whichhasopenedupmanysegmentstoincreasedcompetition.RisingfuelcostsandwagesinmanypartsofAsiahavealsoeatenintoprofits.Marginsarelikelytoremainunderpressure,particularlygiventheentranceofnewcompetitorsintotheindustry,andtheincreasingsophisticationoflow-costcompetitors.Tomaintainprofitability,manyfirmswillhavetofocusonspecificgrowthniches,suchaslow-costairtravelorexpressandfreightforwardingservices,particularlyinChinaandIndia.

© The Economist Intelligence Unit Limited 201212

Asia Competition BarometerTransport and logistics

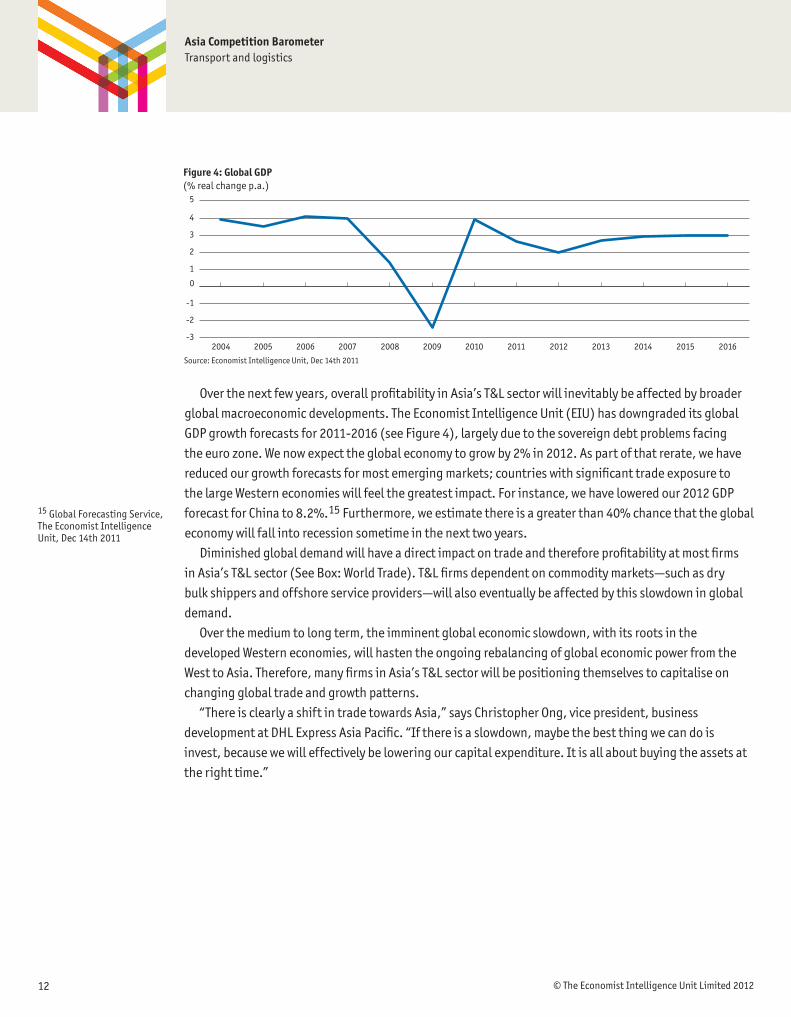

Overthenextfewyears,overallprofitabilityinAsia’sT&Lsectorwillinevitablybeaffectedbybroaderglobalmacroeconomicdevelopments.TheEconomistIntelligenceUnit(EIU)hasdowngradeditsglobalGDPgrowthforecastsfor2011-2016(seeFigure4),largelyduetothesovereigndebtproblemsfacingtheeurozone.Wenowexpecttheglobaleconomytogrowby2%in2012.Aspartofthatrerate,wehavereducedourgrowthforecastsformostemergingmarkets;countrieswithsignificanttradeexposuretothelargeWesterneconomieswillfeelthegreatestimpact.Forinstance,wehaveloweredour2012GDPforecastforChinato8.2%.15Furthermore,weestimatethereisagreaterthan40%chancethattheglobaleconomywillfallintorecessionsometimeinthenexttwoyears.

DiminishedglobaldemandwillhaveadirectimpactontradeandthereforeprofitabilityatmostfirmsinAsia’sT&Lsector(SeeBox:WorldTrade).T&Lfirmsdependentoncommoditymarkets—suchasdrybulkshippersandoffshoreserviceproviders—willalsoeventuallybeaffectedbythisslowdowninglobaldemand.

Overthemediumtolongterm,theimminentglobaleconomicslowdown,withitsrootsinthedevelopedWesterneconomies,willhastentheongoingrebalancingofglobaleconomicpowerfromtheWesttoAsia.Therefore,manyfirmsinAsia’sT&Lsectorwillbepositioningthemselvestocapitaliseonchangingglobaltradeandgrowthpatterns.

“ThereisclearlyashiftintradetowardsAsia,”saysChristopherOng,vicepresident,businessdevelopmentatDHLExpressAsiaPacific.“Ifthereisaslowdown,maybethebestthingwecandoisinvest,becausewewilleffectivelybeloweringourcapitalexpenditure.Itisallaboutbuyingtheassetsattherighttime.”

Figure 4: Global GDP(% real change p.a.)

-3

-2

-1

0

1

2

3

4

5

2016201520142013201220112010200920082007200620052004

Source: Economist Intelligence Unit, Dec 14th 2011

15GlobalForecastingService,The Economist Intelligence Unit,Dec14th2011

© The Economist Intelligence Unit Limited 2012 13

Asia Competition BarometerTransport and logistics

World trade

Followingareboundin2010,worldtradegrowthhasslowedin2011,withmomentumstallingparticularlysincethethirdquarter.InGermany,afterastrongfirsthalf-year,annualexportearningsgrowthslowedto10%inSeptember,whileinChinaexportsgrewatanannualrateof15.9%inOctober,downfrom17.1%amonthearlier.IntheUS,whereindicatorsofeconomichealtharenotyetpointinguniformlydownwards,exportearningsgrewby18.1%inSeptember,comparedwithanaveragerateof21%in2010.Japan’s

economyisstillrecoveringfromthetsunamiandnucleardisasterinMarch,withexportsinSeptembergrowingmoreslowlythanimportsonanannualisedbasis.Inthelightoftheslowdownevidentinrecentdata,notablyinEuropeandAsia,theEconomistIntelligenceUnithasreviseddownitsworldtradegrowthestimatefor2011to6.6%.Meanwhile,inresponsetothedowngradeofoureurozonegrowthforecastandthedeterioratingglobalmacroeconomicpicture,wehavecutourworldtradegrowthforecastfor2012to4.2%.Weexpectgrowthtorecovertocloseto6%in2013andtostrengthenoverfrom2014-2016.

Figure 5: World trade(% change; goods)

-12

-9

-6

-3

03

6

9

12

15

2016201520142013201220112010200920082007

Source: Economist Intelligence Unit, Dec 14th 2011

© The Economist Intelligence Unit Limited 201214

Asia Competition BarometerTransport and logistics

Positioning for success in Asia

Resilient demand: Industry growth will come from Asia

Giventhelong-termstructuralproblemsinmanyWesternmarketsandemergingAsia’slargelybullisheconomicfundamentals,theshiftintradeandinvestmentfromtheWesttoAsiawillcontinue.The

EIUestimatesthatby2016theeightAsiancountriesinthisstudyalonewillaccountfor28.9%ofglobalGDP(measuredinpurchasing-powerparityterms),upfrom23.2%in2010.

ThestronggrowthofAsia’semergingeconomieswillboosttheintra-regionalmovementofgoodsandpeople.ManyindustryanalyststhereforebelieveAsiaoffersbetterprospectsforT&Lfirms.TransportIntelligence,anindustryresearchfirm,projectsdouble-digitincreasesthrough2014incontractlogisticsandexpressandfreightforwardingservicesintheregion,ledbyChinaandIndia.16Meanwhile,ChinareplacedtheUSthisyearasthelargestaircargomarketforSingapore,anexampleofhowChina’sgrowthisdrivingtheAsianlogisticsindustry.

ManyotherAsiancountriesarealsokeentoboostprivateconsumption,partlyinabidtoreducetheirrelianceonexportsandinvestment.“Wehavehugecontractswithalotofbrandowners,includingApple,”saysMrOngatDHLExpress.“ThereisalotofgrowthindemandinAsiafortheseendproducts.”Thoughcomponenttradeisstillhuge,andgrowing,thistrendsuggeststhatthenatureoftradeflowsintheregionisshiftingtowardsmorefinaldemand.Thisisforcinglogisticsproviderstoimprovetheirimportingandintra-regionalcapabilities.

Thissuggeststhatshorter-haulfreightcompaniesconcentratingontheregionwillgrowfasterthanthosefocussedonlong-haulroutes,forinstancebetweenAsiaandEurope.Inaddition,smallT&LfirmsabletoserveremotepartsofAsiawhereincomesarerising—suchascommodity-richpartsofIndonesia—standtoboostrevenues.

Inlinewiththis,companiesareaggressivelygrowingtheirpresenceandoperationsinAsia.Forexample,Singapore-basedREITGlobalLogisticProperties,Asia’slargestproviderofmodernlogisticsfacilities,willdevelop14msquarefeetofnewspaceinChinain2011,and16-17msquarefeetin2012.A

16“AsiaPacificTransportandLogistics2011”,TransportIntelligence,Sep2011

© The Economist Intelligence Unit Limited 2012 15

Asia Competition BarometerTransport and logistics

numberofestablishedcompanies,suchaslogisticsservicescompanyFedEx,expressservicesfirmTNT,marineterminaloperatoranddeveloperDPWorld,andlogisticsandtransportationsolutionsproviderTollGroup,areusingacquisitionsofIndiancompaniestogainapresenceinIndia.

ThedevelopmentofChinaandIndiawillalsodrivethecommoditiestradewithinAsia.Frost&Sullivan,aresearchhouse,believesthatIndonesia’srobustoilandgassectoranditsstatusasthelargestcoalexporterintheworldwillcontributetoan8.3%expansioninthecountry’slogisticssectorin2011.17

Thoughintra-Asiantradewillcontinuetodrivegrowthincontainershipping,theindustry’sprofitabilityoutlookisslightlymorecautiousduetohighoilprices,over-capacityanddepressedfreightrates.Inthisenvironment,shippingfirmswillwanttoadoptmorefuel-savinginitiatives,minimiseidlingcapacityandredraftroutestostrengthentheirbottomlines.

Profiting from Asia’s evolving manufacturing footprintsJustthreeyearsago,supplychainsinAsiawerestillfollowingapredictablepattern,withmanycomponentsfromaroundtheregionbeingshippedtoChinaforfinalassembly,beforebeingsenttoothermarketsforsale.Today,severalbroadtrendsarecausingarethinkofAsianmanufacturing.FirstandforemostisrisingwagesinChina,whichareleadingtotheflightoflow-costmanufacturingawayfromthesouthandcoastalareastoinlandprovincesandneighbouringcountriessuchasVietnam.

AnotheristhecontinuedrapidgrowthofAsianeconomies,coupledwithsluggishrecoveriesintheWest,whichhaspromptedmorefirmstofocusonservingAsia’sconsumers.Finally,therecentnaturaldisastersinJapanandThailand,andtheirimpactontheproductionofcertaincomponents,havehighlightedtheimportanceofhavingalternativesuppliers.

WithinChina,economicdevelopmenthasbeenshiftingwestwards.“InsteadofShenzhenandGuangdong,weareseeingalotofgrowthinChengdu,”saysMrOng.China’sT&Lindustry,therefore,willexpandstronglyintothecentralandwesternregions,andboostdevelopmentofrurallogisticsservices.China’sbroadgeographicalspreadandthepresenceofproductionbasesacrossthecountryofferopportunitiesforsmallandlargelogisticsservicesproviders.

Meanwhile,TransportIntelligenceseeslong-termgrowthpotentialinVietnam,aslow-costmanufacturingworkshiftstherefromChina.18Vietnam’srapidlygrowingairandseaportindustrieshavefacilitatedahighervolumeoftrade,anditsvastnetworkofinlandwaterwaysservesasanefficientmodeofgoodstransportation.Vietnam’sT&Lsectorisstillinitsinfancy,withafragmentedindustrymakeup.Earlyentrantshaveanopportunitytoestablishafirst-moveradvantage.Forinstance,MaerskhasconstructedtheCaiMepInternationalTerminalinVietnam,whichbeganoperationsinmid-2011,throughajointventure.SourcesofcompetitiveadvantagewillincludebeingabletoleveragetransportationnetworkefficiencieswithChinaandnavigatingthegovernmentbureaucracyinVietnam.

ManufacturingfootprintselsewhereinAsiaarealsochanging.Indonesia’smanufacturingsectorhasbeengrowingrapidly,focussedbothonexportsaswellasitshuge,burgeoningdomesticmarket.MalaysiaandThailandwillcontinuetopushupthemanufacturingvaluechain,producing,forinstance,automotiveproductsandsolarpanels.India,meanwhile,iseagertoincreaseitsexport-orientedmanufacturing,partlytoservemarketsintheMiddleEastandAfrica.

Thisshiftwillleadtothegrowthofmanynewtradelinkswithintheregion,saysMrOng.Hebelieves

17“Indonesia’sLogisticsIndustrySettoGrow8.3%in2011”,Knight Ridder/Tribune Business News,Jan27th2011.

18“VietnamLogistics2009”,TransportIntelligence,Jan2009.

© The Economist Intelligence Unit Limited 201216

Asia Competition BarometerTransport and logistics

thiswillbenefitlargefirmssuchasDHL,because“foramultinationalthatwantstoworkwithasinglesource,wearethere.”ButthesedevelopmentswillalsocreateopportunitiesfornewregionalT&Lplayers,whocangrowanddevelopastradeblossomsintheirimmediateneighbourhood.

case study DHL Express

DHL Express: Growth in AsiaAsiaisthemostimportantcontributortogrowthformajorexpress

deliveryfirms,accordingtoChristopherOng,vicepresident,businessdevelopmentatDHLExpressAsiaPacific.“Eventhoughthe2008-09recessionhurtprofitabilityforsomecompanies,lastyear(2010)wasaverygoodyearformanyglobalexpressservicesfirms,andAsiawasdrivingmuchofthatgrowth,”hesays.

Nevertheless,MrOngagreesthatcompetitionhasintensifieddramaticallyoverthepastfewyears,andnotjustfromthelarge,integratedfirms.“IntheJapan-Korea-Chinagrowthtriangle,forinstance,wearestartingtoseealotofcompetitionfromregionalplayers,”hesays.“ThereareChineseplayerswhoareofferingextremelylowfreightratesintoKoreaandJapan.”

TheseemergingT&LSMEsand“nationalchampions”competeonpriceinlocalisedgeographies,saysMrOng,targetingsmallcompanieswhotradeonlyalongafewroutes.Inthatsegment,theypresenttoughcompetitiontobiggerfirmssuchasDHL.InJuly2011DHLexitedthedomesticdeliverybusinessinChina,whenitsloss-makingjointventurewithSinotrans,aChinesefirm,wassoldtoUni-top,anotherChineseplayer.Sinotranscited“overlyfiercecompetitioninthedomesticcourierservicessector”foritspoorperformance.

GiventhemultitudeofsmalllocalplayersinAsia,MrOngexpectstheretobesomeconsolidationintheregionoverthenextfewyears,particularlyinChina,withafewnationalchampionsgrowingbigger.“Someofthesemarketsaresofragmented,it’simpossibletoreapanyeconomiesofscale,”hesays.MrOngisconfidentthatconsolidationwillimproveservicestandardsinthesemarkets,asfirmsmoveawayfrompurepricecompetition.Thesefirmswillalsobroadentheirfootprint.MrOngcitesShunfeng,oneofChina’slargestdomesticexpressservices,which“hasstartedtomoveouttoSingapore,HongKongandTaiwan.”

Facedwiththeseemergingchallengers,DHL’scompetitivepositioningisbasedonitsglobalreachaswellasitsreputationforqualityandsecurity.

Overthepastfewyears,theindustryhashadtocontendwithrisingwagesaswellasfuelcosts.Tocurboperationalcosts,DHLhasbeenrelentlesslystrivingtoimprovetheefficiencyofitsprocesses,saysMrOng,whousedtorunthefirm’sSixSigmaprogramme.Thisefficiencydrivehasalsohelpedthefirmreduceitsenergyusage,improvingitsenvironmentalperformance.Meanwhile,ithasbeenabletopassonmostofitsfuelcostrisestoitscustomers.ThoughMrOngexpectsbothwagesandfuelcoststocontinuetoriseoverthenextfewyears,hedoesnotexpectthemtosignificantlycrimpprofitability.

Overthenearterm,T&LfirmsinAsiawillneedtocloselymonitormanufacturers’productionplanswithrespecttojust-in-timeproductionanddelivery(JIT),asthiswillimpactthenatureoftransportationandlogisticsservicesrequired.

Giventheglobaleconomy’srapidgrowthfrom2004to2007,manymanufacturingfirmsswitchedfromairtooceanfreightduringthattime,MrOngsays,inordertocutcosts.Butwhenthe2008-09recessionhit,theysuddenlyfoundthemselveswithahugeinventorybuild-up.

ThispromptedmanymanufacturingfirmstoincreasetheiruseofJIT.“Ithinktheyfiguredit’sbettertopayalittlemorefortransportthantohaveobsoleteinventory,”hesays.Therewasthenashiftbacktoairfreight.ThiscouldpartlyexplainthesupplydisruptionsmanyfirmsfacedfollowingthenaturaldisastersinJapanandThailandin2011,astheyhadrelativelysmallerinventoriesonhand.

Thus,ontheonehand,manymanufacturersareagainquestioningthewisdomofJITfollowingthosetwodisasters.Ontheotherhand,thedarkeningglobaleconomicoutlookisagainthreateningtodampendemandforgoods,suggestingthathugeinventoriesmayturnouttobealiability.Tostayaheadofthecompetition,T&LfirmsinAsiawillneedtobeabletohandleanyshiftsintraffic,asmanufacturersreacttochangingmarketconditions.

© The Economist Intelligence Unit Limited 2012 17

Asia Competition BarometerTransport and logistics

Outlook

AlthoughtheT&LmarketinAsiahasbeengrowingrapidly,profitabilityhasbeenonadownwardtrendoverthepastfiveyears,largelyduetoincreasedcompetitioninthesector.Thoughprofitabilityhas

risensincethe2008-09recession,thedarkeningeconomicoutlookportendsfurtherdeclinesinthenearterm.

CompaniesinAsiawillthereforehavetomanagenear-termuncertaintywhileanticipatingandpreparingforthelonger-termsecularshiftintradeandgrowth,aseconomicmomentumshiftsfromsluggishWesterncountriestodynamicemergingmarkets.

TheT&Lsectorwillcontinuetoadapttochangesintheglobalenvironmentbycompetingonprice.Cost-cuttingwillthereforebeakeytheme.AdditionalchallengestoT&Lcompanieswillcomeintheformofenergycosts,climatechange,andterrorism.Companieswillneedstrongriskmanagementprogrammesinordertomitigatethesethreats.

AmongstmoredevelopedT&Lmarkets,andinthemoresophisticatedlinksofthesupplychain,thereisagreatercallforincreasedcostefficiencythroughtheadoptionofnewtechnology.Forinstance,technologiessuchasradiofrequencyidentification(RFID)helptonarrowmarginsoferrorandtherebyreducethecostsofcorrectingerrors.Environmentallyfriendlyproductsandserviceswillalsobecomeincreasinglyimportant,acceleratingtheshiftto“GreenLogistics”.

Asia is likely to produce many global T&L leaders TwobroaderindustrytrendssuggestthatmanyoftheglobalT&LleadersofthefuturewillcomefromAsia.Firstisthelong-termshiftintradeandinvestmentfromtheWesttotheEast,whichwillprovideevermoreopportunitiesforgrowthintheregionacrossallsegments.Therewillbefurtherconsolidationinthesector,asfirmsgrowtoreapscaleefficienciesandimprovetheircross-bordercapabilities.

SecondisAsia’searlyadvantageinlow-costcompetitionand“frugalengineering”(aproductdesignapproachthatemphasisesusingthebareminimumofresourcestocreatebasic,no-frillsproducts).

© The Economist Intelligence Unit Limited 201218

Asia Competition BarometerTransport and logistics

ThisindicatesthatAsianT&Lfirmswillinnovatetoproducelow-costservicesthatwillappealnotonlytoemerging-marketconsumers,buttoincreasinglycost-consciousconsumersinWesterndevelopedmarkets.AnexampleofthisisLCCAirAsia’sincreasingpenetrationinglobalairtravelmarkets,asitexpandsgeographically,whilealsopushinguptoservehigher-valuesegmentsoncertainroutes(forinstance,onsomeroutesitofferspremiumseats,suchasflat-beds,atmuchlowerpricesthanregularairlines).

Similarly,otherT&LfirmsthatcancompeteandwinmarketshareinAsiawillbewellpositionedforglobalexpansion.AsAsiaprogressivelyaccountsforabiggershareofglobaltradeandtransportation,itislikelythattheregionwillproducemanyoftheworld’smostcompetitiveandinnovativeT&Lfirmsofthefuture.

© The Economist Intelligence Unit Limited 2012 19

Asia Competition BarometerTransport and logistics

Barometer methodology

Toassesstheintensityofcompetitionandunderstandthechangingmarketdynamicsinkeysectors,theEconomistIntelligenceUnit(EIU)hasdevelopedtheAsiaCompetitionBarometer.Drawing

uponcompany-leveldataonprofitabilityandotherindicators,theBarometerquantifiesthechangingdynamicsofcompetitivenessinAsiaforselectindustriesbetween2004and2009.

Assessingauniverseofover275publiclylistedtransportandlogistics(T&L)companiesacrosseightcountries—China,India,Indonesia,Malaysia,thePhilippines,Singapore,ThailandandVietnam—theBarometerexamineschangingprofitabilityandthecompetitionlandscapefortheT&Lsector.

How do we define the transport and logistics sector? GiventheincreasinglyintegratednatureofglobalandregionallogisticssupplychainstheT&Lsectorencompassesbothpassengerandfreightservices.Inaddition,activityforbothtypesofservicesisdrivenbysimilarmacroeconomicfactors,particularlyrelatedtoglobaltrade.

TheT&Lsectorincludesthefollowingsub-segments:landtransportandtransportviapipelines,watertransport,airtransport,warehousingandsupport

activitiesfortransportationandpostalandcourierservices.

Methodology TheBarometerhastwodimensions:profitabilityandmarketconcentration.

Profitability IndexToassesstheaggregateprofitabilityoftheT&LsectorinAsia,theEIUdevelopedacompositeindexoffiveratiosthateachrepresentadifferentaspectofacompany’sprofitability:

• EBITDA margin (%):Ameasureofacompany’soperatingprofitability.Itisequaltoearningsbeforeinterest,tax,depreciationandamortisation(EBITDA)dividedbytotalrevenue.BecauseEBITDA

© The Economist Intelligence Unit Limited 201220

Asia Competition BarometerTransport and logistics

excludesdepreciationandamortisation,EBITDAmarginprovidesaclearerviewofacompany’scoreprofitability.Anincreaseincompetitionmayputpressureonanindustry’sprofitmargins.

• Gross margin (%):Whenusedasamarketmeasureofcompetition,grossmarginmeasurestheprofitabilityconsideringonlythecostsofgoodssold.Thehigherthepercentage,themorethecompanyretainsoneachdollarofsalestoserviceitsothercostsandobligations.Anincreaseincompetitiontendstoreducefirms’abilitytoincreasepricesandtherebyincreaseitsgrossmargin.

• Return on capital employed (%):Ameasureoftheefficiencyandprofitabilityofacompany’scapitalinvestments.Returnoncapitalemployedalsoindicateswhetherthecompanyisearningsufficientrevenuesandprofitsinordertomakethebestuseofitscapitalassets.Anincreaseincompetitionmayrequirefirmstoemployadditionalcapitaltomaintainprofitability.

• Return on equity (%):Ameasureoftherateofreturnontheshareholders’equity.Itmeasuresafirm’sefficiencyatgeneratingprofitsfromeveryunitofshareholders’equity.Returnonequityshowshowwellacompanyusesshareholderfundstogenerateearningsgrowth.Ariseincompetitiontendstoputpressureonreturnsonshareholderfunds.

• Return on assets (%):Ameasureofhowprofitableacompany’sassetsareingeneratingrevenue,orhowprofitableacompanyisrelativetoitsassets.Returnonassetsdeterminesacompany’sabilitytoutiliseitsassetsefficientlyandeffectively.Highercompetitiontendstoputpressureonfirms’abilitytomaintainreturnonassets.

Weaggregatedcompany-leveldatafor275publicly-quotedT&Lcompaniesandexaminedtheirprofitabilityratios.Toenableobservationoftrendsovertime,acompositeProfitabilityIndexwasdeveloped(whereyear2005=100).EBITDAandgrossmarginaregivenahigherweightingintheindexastheyspeakdirectlytobottomlineprofitability,whilethereturnoncapitalemployed,returnonequityandreturnonassetsratiosspeaktohowacompanymakeuseofitsvariousresourcestodrivereturn(i.eefficiency/productivity).

Profitability indicator Weight in Profitability Index

EBITDAmargin(%) 35%

Grossmargin(%) 35%

Returnoncapitalemployed(%) 10%

Returnonequity(%) 10%

Returnonassets(%) 10%

19Orsummedforallthefirmsin the case that there are fewerthan50.

Market concentration Toassessmarketconcentration,theEIUcalculatedtheHerfindahl-HirschmannIndex(HHI)fortheT&LsectorinAsiafrom2004to2009.Ameasureofthesizeofcompaniesinrelationtotheindustry,andanindicatoroftheamountofcompetitionamongthem,theHHIisdefinedasthesumofthesquaresofthemarketsharesofthe50largestfirms19fromtheuniverseofover275listedcompaniesassessed.HHIvaluescanrangefrom0to1.0,movingfromanextremelyfragmentedmarket(0)toamonopoly(1).HHI

© The Economist Intelligence Unit Limited 2012 21

Asia Competition BarometerTransport and logistics

valueshavebeenmultipliedby100toachieveascaleconsistentwithprofitabilityindicators.ArisingHHIindexgenerallyindicatesfallingmarketcompetition,whileafallintheHHIsuggeststhatcompetitionisincreasing.

Whilsteveryefforthasbeentakentoverifytheaccuracyofthisinformation,neitherTheEconomistIntelligenceUnitLtd.northesponsorofthisreportcanacceptanyresponsibilityorliabilityforreliancebyanypersononthisreportoranyoftheinformation,opinionsorconclusionssetoutherein.

Coverimage-WaiLam