trends - how is the south florida real estate market performing?

DESCRIPTION

What is happening in South Florida real estate market? ONE | Sotheby's International Realty Trends examines the market in detail.TRANSCRIPT

2015R E A L E S T A T E M A R K E T R E P O R T

O N E S O T H E B Y S R E A L T Y . C O M

14 | 2015 TRENDS Market Report

Three Hundred Collins, South Beach | 300Collins.com

For assistance with your real estate needs, please contact:

Enrique J. TejeraGlobal Real Estate AdvisorONE Sotheby’s International [email protected]

SearchMiamiBeach.com

For more information, please visit:

ONE Sotheby’s International Realty | 3

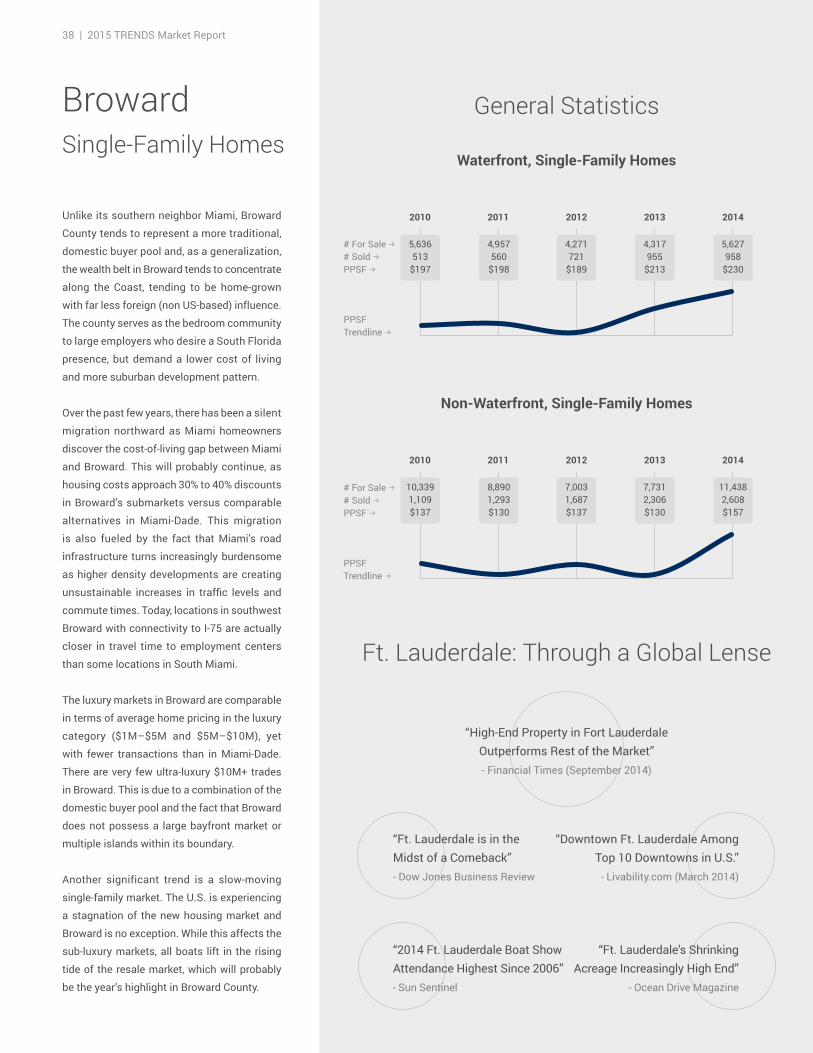

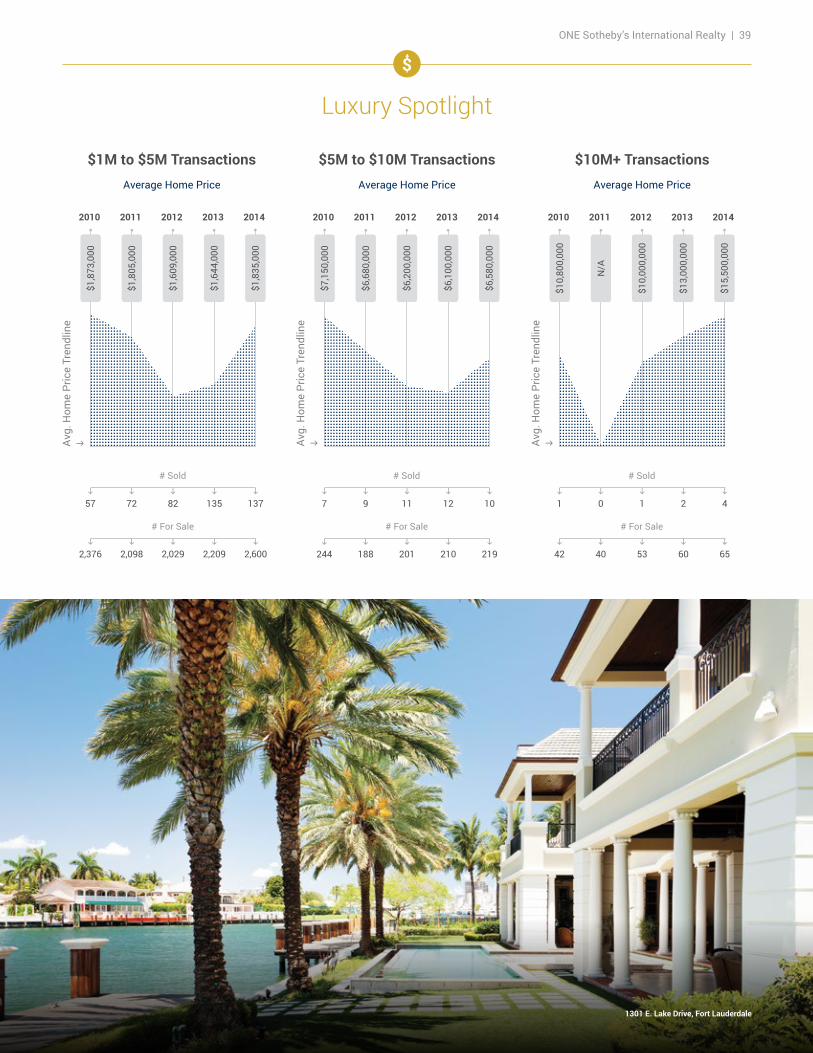

Looking back on ONE Sotheby’s International Realty’s seven years of operation, it’s telling to hear how the South Florida real estate market conversation now takes place with a drastically different tone. In the very first TRENDS market report published in 2010, it is stated that the general mood at the time was a sense of cautious optimism. Fast-forward to 2015, the year-to-year improvement of the market has led South Florida to become one of the most sought-after residential destinations in the world. Miami was ranked the happiest city to work in by Forbes Magazine and is now considered one of the top ten cities that matter to ultra-high-net-worth investors. By the same token, Fort Lauderdale, a prime destination for yacht owners and boating connoisseurs, is experiencing great demand due to its many canals and waterfront living options.

An ever-evolving real estate market must be analyzed in ever-evolving ways: this year’s report was prepared in conjunction with Integra Realty Resources (IRR) – Miami\Palm Beach, one of the nation’s leading real estate consulting firms. This joint publication is a new venture meant to provide insight into residential markets in Miami-Dade and Broward Counties.

Our two firms collaborated to provide this annual report to foster further dialogue regarding emerging market conditions at the submarket level. We endeavored to provide actionable insight into the direction of these various submarkets without the typical hyperbole or marketing fanfare.

IRR Miami was aided by interviews with ONE Sotheby’s International Realty associates and others in the marketplace, who provided important insight into the drivers in these various submarkets. To provide a consistent format for comparison, the team revised the methodology for quantifying the condominium value changes (see Methodology on page 5) and developed comparative statistics for the single-family, waterfront and non-waterfront markets.

The information contained herein is general to the market and should not be construed to represent advice on a specific property. We strongly encourage interaction with ONE Sotheby’s International Realty agents to provide relevant, property-specific advice. This report is meant to provide an overview of the major markets and submarkets for comparative purposes only and to frame some reasonable dimension of market activity and direction in the year to come.

We hope you find the report useful and even insightful, as you explore one of the most dynamic housing markets in the United States today. We stand ready to assist with further questions and comments and hope your feedback will improve future annual and quarterly reports.

Daniel de la Vega Anthony M. Graziano, MAI, CRE President & Managing Partner Senior Managing Director ONE Sotheby’s International Realty Integra Realty Resources

4 | 2015 TRENDS Market Report

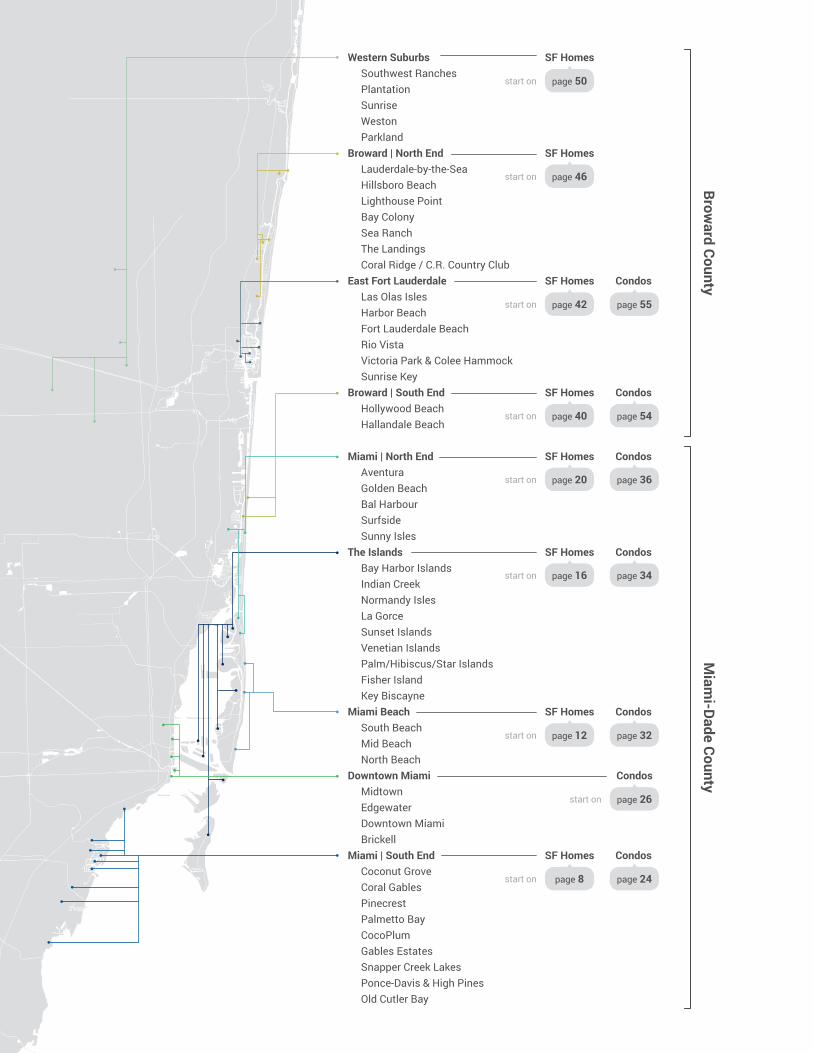

Western Suburbs Southwest Ranches Plantation Sunrise Weston ParklandBroward | North End Lauderdale-by-the-Sea Hillsboro Beach Lighthouse Point Bay Colony Sea Ranch The Landings Coral Ridge / C.R. Country Club East Fort Lauderdale Las Olas Isles Harbor Beach Fort Lauderdale Beach Rio Vista Victoria Park & Colee Hammock Sunrise KeyBroward | South End Hollywood Beach Hallandale Beach

Miami | North End Aventura Golden Beach Bal Harbour Surfside Sunny IslesThe Islands Bay Harbor Islands Indian Creek Normandy Isles La Gorce Sunset Islands Venetian Islands Palm/Hibiscus/Star Islands Fisher Island Key BiscayneMiami Beach South Beach Mid Beach North BeachDowntown Miami Midtown Edgewater Downtown Miami BrickellMiami | South End Coconut Grove Coral Gables Pinecrest Palmetto Bay CocoPlum Gables Estates Snapper Creek Lakes Ponce-Davis & High Pines Old Cutler Bay

SF Homes

SF Homes

SF Homes Condos

SF Homes Condos

SF Homes Condos

SF Homes Condos

SF Homes Condos

Condos

SF Homes Condos

Broward County

Miam

i-Dade County

page 50

page 46

page 42 page 55

page 40

page 20 page 36

page 16 page 34

page 12 page 32

page 26

page 8 page 24start on

start on

start on

start on

start on

start on

start on

start on

start on

page 54

ONE Sotheby’s International Realty | 5

Methodology

This report differs from prior ONE Sotheby’s International Realty market reports in the analytics models developed in conjunction with IRR Miami.

The report cannot be compared to prior annual or quarterly reports due to changes in the manner in which the metrics were developed for single-

family and condo developments.

Prior reports on single-family pricing relied on price averages which excluded certain classes of assets based on price thresholds. The current

model abandons the variable minimum price threshold view so that averages over time are not skewed by elimination of transactions beyond a

threshold and changes in market conditions do not skew the directionality of the market averages.

The most significant change in methodology is the development of the condominium index. The difficulty in comparing existing condominium

project average pricing is that the pricing averages have no control over penthouse units, waterview versus waterfront or age and market position

of the product. ONE Sotheby’s International Realty and IRR Miami developed an index of relevant condominium towers that comprise what we

consider to be a representative sample of the luxury projects within each submarket. The inclusion of each project was vetted by brokerage and

appraisal staff from the respective firms and the sampling reflects the center of the luxury market as it relates to the specific submarket.

Average pricing data was then calculated for each of the relevant years by submarket and unique units were excluded from the sample to avoid

skewing the average price indicators. The implementation of project samples also helped control the variability brought about by merely averaging

all condo projects within a specific submarket, which when comparing multiple years was less reflective of changing market conditions.

While this methodology only reflects a “sample” of the condo market, the number of projects and number of units in the sample are considered

representative of the market. The sample pool of projects does not include pre-construction projects. Therefore, the averages and indicators

reflect contemporary existing peers and are not meant to reflect pricing of the newest projects coming to market.

This methodology will also allow us future analytical capability to project floor premiums, view premiums and penthouse premiums since the data

will be isolated for direct and discrete comparison on these function points. We hope this will clarify directionality of the market and allow for

deeper analysis in future reports.

This report is not meant to replace property analysis by a qualified broker and should not be applied to specific properties without consultation

with a professional. The report is meant to inform on broader trends and to facilitate comparison and forecasting at the macro market level.

Louver House, South Beach | LouverHouse.com

6 | 2015 TRENDS Market Report

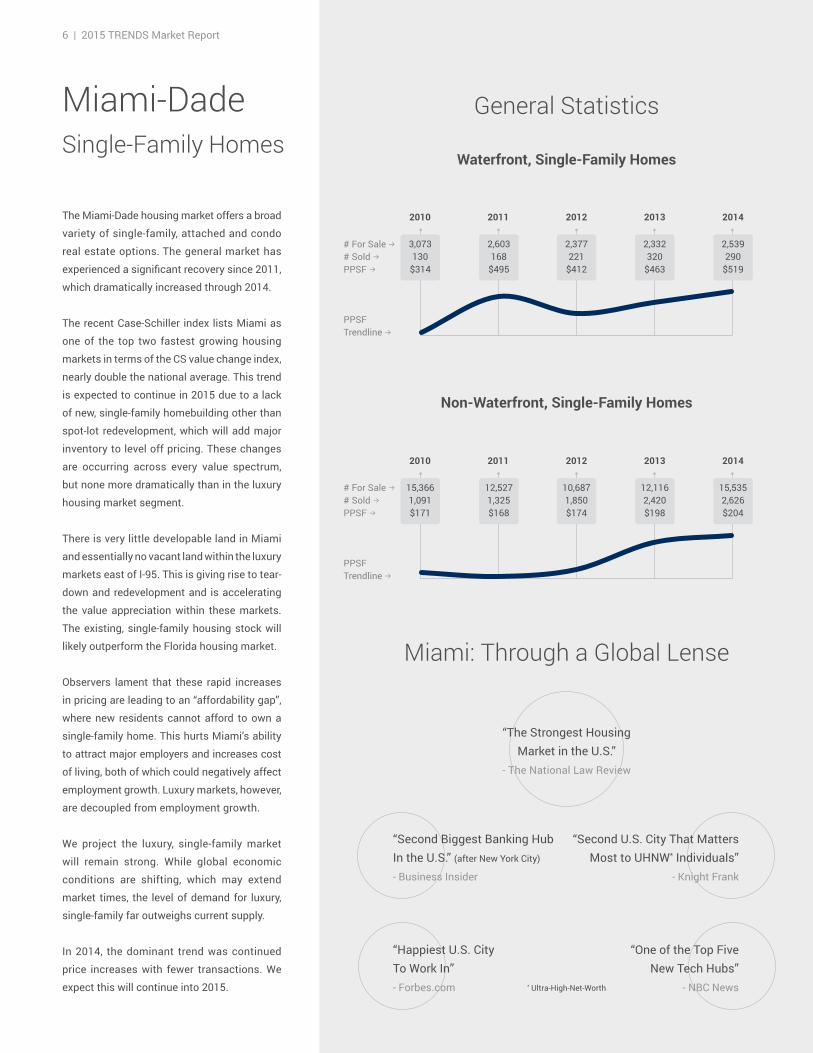

Luxury SpotlightMiami-DadeSingle-Family Homes

General Statistics

The Miami-Dade housing market offers a broad

variety of single-family, attached and condo

real estate options. The general market has

experienced a significant recovery since 2011,

which dramatically increased through 2014.

The recent Case-Schiller index lists Miami as

one of the top two fastest growing housing

markets in terms of the CS value change index,

nearly double the national average. This trend

is expected to continue in 2015 due to a lack

of new, single-family homebuilding other than

spot-lot redevelopment, which will add major

inventory to level off pricing. These changes

are occurring across every value spectrum,

but none more dramatically than in the luxury

housing market segment.

There is very little developable land in Miami

and essentially no vacant land within the luxury

markets east of I-95. This is giving rise to tear-

down and redevelopment and is accelerating

the value appreciation within these markets.

The existing, single-family housing stock will

likely outperform the Florida housing market.

Observers lament that these rapid increases

in pricing are leading to an “affordability gap”,

where new residents cannot afford to own a

single-family home. This hurts Miami’s ability

to attract major employers and increases cost

of living, both of which could negatively affect

employment growth. Luxury markets, however,

are decoupled from employment growth.

We project the luxury, single-family market

will remain strong. While global economic

conditions are shifting, which may extend

market times, the level of demand for luxury,

single-family far outweighs current supply.

In 2014, the dominant trend was continued

price increases with fewer transactions. We

expect this will continue into 2015.

Miami: Through a Global Lense

“Happiest U.S. City To Work In”- Forbes.com

“Second Biggest Banking Hub In the U.S.” (after New York City)

- Business Insider

“One of the Top Five New Tech Hubs”

- NBC News

“The Strongest HousingMarket in the U.S.”

- The National Law Review

Non-Waterfront, Single-Family Homes

2010 2011 2012 2013 2014

15,366 1,091$171

12,527 1,325$168

10,687 1,850$174

12,116 2,420$198

15,535 2,626$204

# For Sale b# Sold bPPSF b

PPSF Trendline b

Waterfront, Single-Family Homes

2010 2011 2012 2013 2014

3,073 130

$314

2,603168

$495

2,377 221

$412

2,332 320

$463

2,539 290

$519

# For Sale b# Sold bPPSF b

PPSF Trendline b

“Second U.S. City That Matters Most to UHNW* Individuals”

- Knight Frank

* Ultra-High-Net-Worth

ONE Sotheby’s International Realty | 7

Luxury Spotlight

$1M to $5M TransactionsAverage Home Price

$5M to $10M TransactionsAverage Home Price

$10M+ TransactionsAverage Home Price

2010 2011 2012 2013 2014

$1,8

56,0

00

$1,8

78,0

00

$1,8

49,0

00

$1,8

71,0

00

$1,8

83,0

00

h

112

h

4,036

h

123

h

3,228

# Sold

# For Sale

h

288

h

3,046

h

280

h

3,363

h

171

h

2,856

2010 2011 2012 2013 2014

$6,7

50,0

00

$6,4

35,0

00

$5,9

23,0

00

$6,6

28,0

00

$6,8

17,0

00h

1

h

407

h

13

h

385

# Sold

# For Sale

h

15

h

408

h

23

h

459

h

12

h

466

2010 2011 2012 2013 2014

N/A

$17,

120,

000

$14,

486,

000

$15,

184,

000

$18,

274,

000

h

0

h

222

h

6

h

227

# Sold

# For Sale

h

6

h

277

h

6

h

350

h

5

h

268

9405 Old Cutler Lane, Coral Gables

Avg.

Hom

e Pr

ice

Tren

dlin

eh Av

g. H

ome

Pric

e Tr

endl

ine

h Avg.

Hom

e Pr

ice

Tren

dlin

eh

8 | 2015 TRENDS Market Report

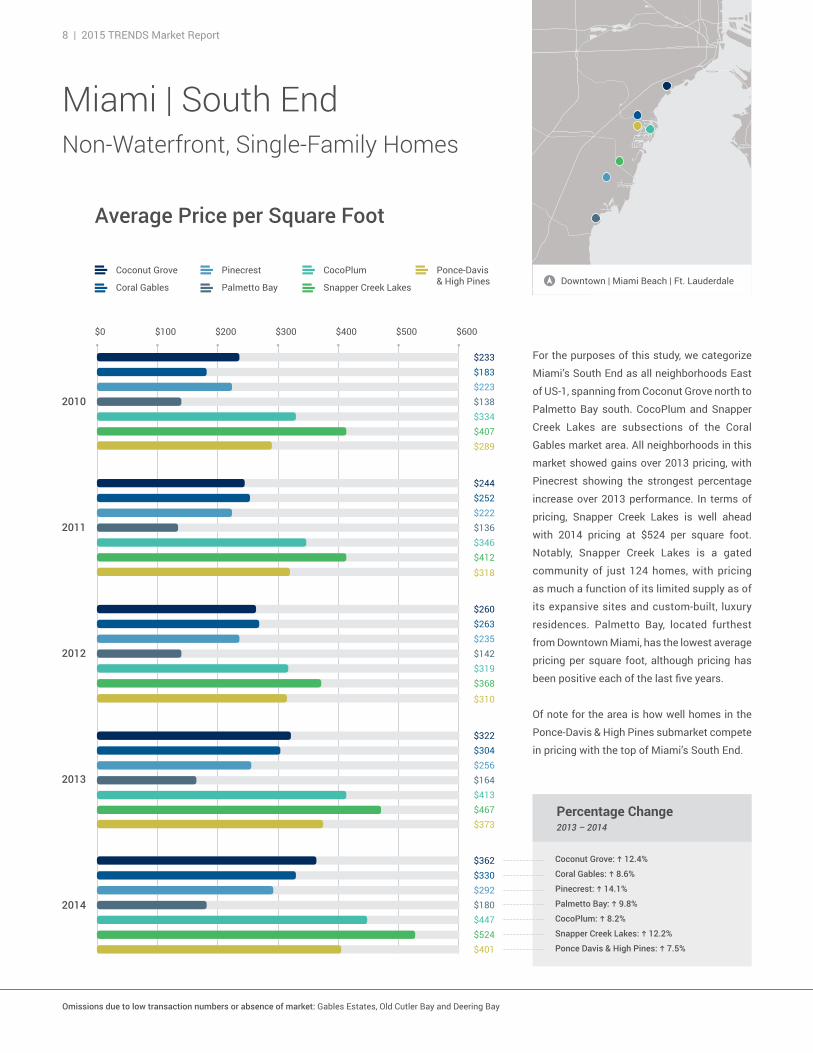

Miami | South EndNon-Waterfront, Single-Family Homes

Downtown | Miami Beach | Ft. LauderdaleCoconut Grove

Coral Gables

$600$500$400$300$200$100$0

Pinecrest

Palmetto Bay Snapper Creek Lakes

CocoPlum

$233$183$223$138$334$407$289

$244$252$222$136$346$412$318

$330$292$180$447$524$401

$260$263$235$142$319$368

$310

$322$304$256$164$413$467$373

Ponce-Davis& High Pines

Average Price per Square Foot

Coconut Grove: g 12.4%

Percentage Change2013 – 2014

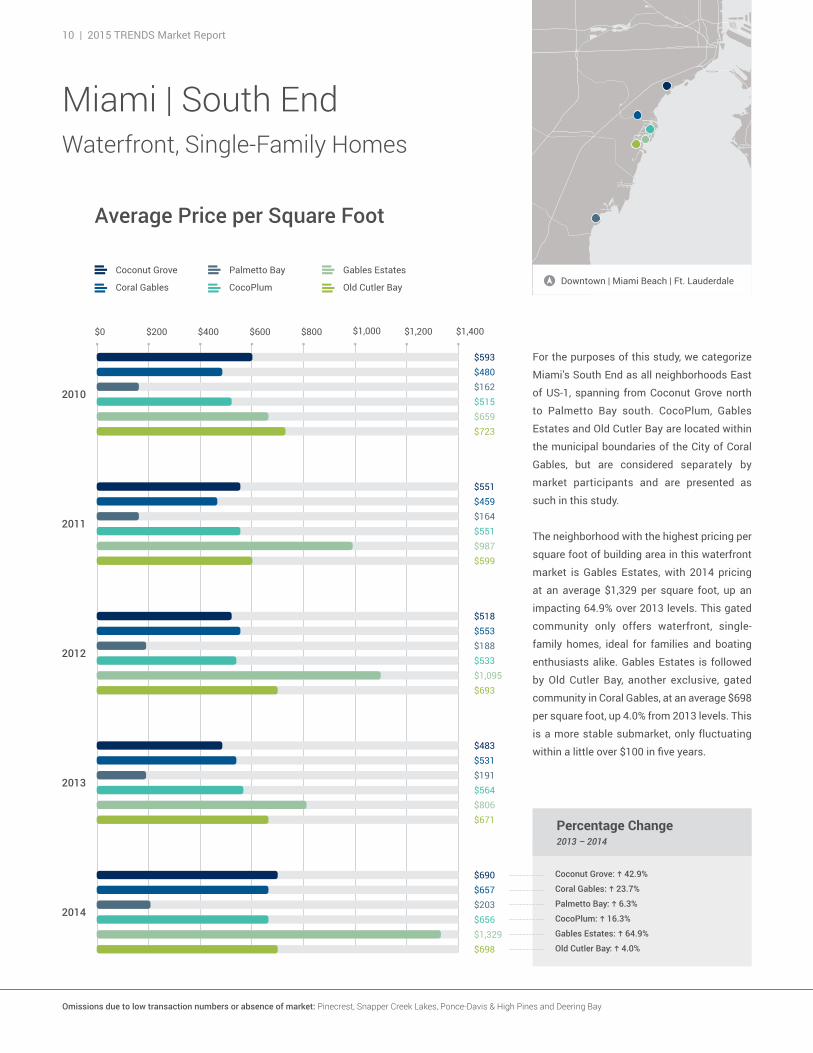

For the purposes of this study, we categorize

Miami’s South End as all neighborhoods East

of US-1, spanning from Coconut Grove north to

Palmetto Bay south. CocoPlum and Snapper

Creek Lakes are subsections of the Coral

Gables market area. All neighborhoods in this

market showed gains over 2013 pricing, with

Pinecrest showing the strongest percentage

increase over 2013 performance. In terms of

pricing, Snapper Creek Lakes is well ahead

with 2014 pricing at $524 per square foot.

Notably, Snapper Creek Lakes is a gated

community of just 124 homes, with pricing

as much a function of its limited supply as of

its expansive sites and custom-built, luxury

residences. Palmetto Bay, located furthest

from Downtown Miami, has the lowest average

pricing per square foot, although pricing has

been positive each of the last five years.

Of note for the area is how well homes in the

Ponce-Davis & High Pines submarket compete

in pricing with the top of Miami’s South End.

$362

Ponce Davis & High Pines: g 7.5%

Pinecrest: g 14.1%

Coral Gables: g 8.6%

Palmetto Bay: g 9.8%

Snapper Creek Lakes: g 12.2%

CocoPlum: g 8.2%

Omissions due to low transaction numbers or absence of market: Gables Estates, Old Cutler Bay and Deering Bay

ONE Sotheby’s International Realty | 9

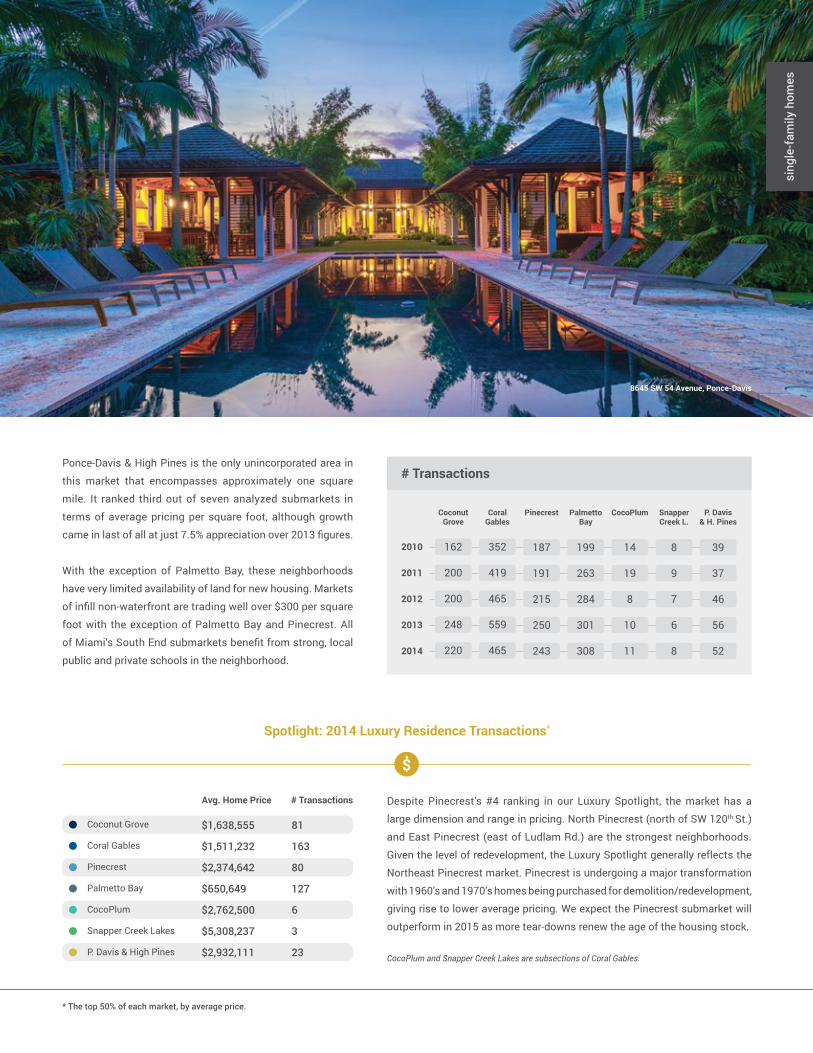

Despite Pinecrest’s #4 ranking in our Luxury Spotlight, the market has a

large dimension and range in pricing. North Pinecrest (north of SW 120th St.)

and East Pinecrest (east of Ludlam Rd.) are the strongest neighborhoods.

Given the level of redevelopment, the Luxury Spotlight generally reflects the

Northeast Pinecrest market. Pinecrest is undergoing a major transformation

with 1960’s and 1970’s homes being purchased for demolition/redevelopment,

giving rise to lower average pricing. We expect the Pinecrest submarket will

outperform in 2015 as more tear-downs renew the age of the housing stock.

sing

le-f

amily

hom

es

# Transactions

Coconut Grove

187 199 14 8 39

Coral Gables

191 263 19 9 37

Pinecrest

215 284 8 7 46

Palmetto Bay

250 301 10 6 56

CocoPlum

243 308 11 8 52

Snapper Creek L.

P. Davis & H. Pines

2010

2011

2012

2013

2014

162 352

200 419

200 465

248 559

220 465

Ponce-Davis & High Pines is the only unincorporated area in

this market that encompasses approximately one square

mile. It ranked third out of seven analyzed submarkets in

terms of average pricing per square foot, although growth

came in last of all at just 7.5% appreciation over 2013 figures.

With the exception of Palmetto Bay, these neighborhoods

have very limited availability of land for new housing. Markets

of infill non-waterfront are trading well over $300 per square

foot with the exception of Palmetto Bay and Pinecrest. All

of Miami’s South End submarkets benefit from strong, local

public and private schools in the neighborhood.

Coconut Grove

Coral Gables

Pinecrest

Palmetto Bay

CocoPlum

Snapper Creek Lakes

P. Davis & High Pines

Avg. Home Price # Transactions

$1,638,555 81

$1,511,232 163

$2,374,642 80

$650,649 127

$2,762,500 6

$5,308,237 3

$2,932,111 23

8645 SW 54 Avenue, Ponce-Davis

Spotlight: 2014 Luxury Residence Transactions*

* The top 50% of each market, by average price.

CocoPlum and Snapper Creek Lakes are subsections of Coral Gables.

10 | 2015 TRENDS Market Report

Miami | South EndWaterfront, Single-Family Homes

Omissions due to low transaction numbers or absence of market: Pinecrest, Snapper Creek Lakes, Ponce-Davis & High Pines and Deering Bay

Downtown | Miami Beach | Ft. Lauderdale

Percentage Change2013 – 2014

For the purposes of this study, we categorize

Miami’s South End as all neighborhoods East

of US-1, spanning from Coconut Grove north

to Palmetto Bay south. CocoPlum, Gables

Estates and Old Cutler Bay are located within

the municipal boundaries of the City of Coral

Gables, but are considered separately by

market participants and are presented as

such in this study.

The neighborhood with the highest pricing per

square foot of building area in this waterfront

market is Gables Estates, with 2014 pricing

at an average $1,329 per square foot, up an

impacting 64.9% over 2013 levels. This gated

community only offers waterfront, single-

family homes, ideal for families and boating

enthusiasts alike. Gables Estates is followed

by Old Cutler Bay, another exclusive, gated

community in Coral Gables, at an average $698

per square foot, up 4.0% from 2013 levels. This

is a more stable submarket, only fluctuating

within a little over $100 in five years.

Old Cutler Bay: g 4.0%

Coral Gables: g 23.7%

Coconut Grove: g 42.9%

Palmetto Bay: g 6.3%

Gables Estates: g 64.9%

CocoPlum: g 16.3%

Palmetto Bay

CocoPlum Old Cutler Bay

Gables EstatesCoconut Grove

Coral Gables

$1,200$1,000$800$600$400$200$0 $1,400

$593$480$162$515$659$723

$551$459$164$551$987$599

$518$553$188$533$1,095$693

$483$531$191$564$806$671

$690$657$203$656$1,329$698

Average Price per Square Foot

ONE Sotheby’s International Realty | 11

sing

le-f

amily

hom

es

# Transactions

Coconut Grove

18 9 3 4

Coral Gables

20 10 3 4

Palmetto Bay

23 13 12 5

CocoPlum

25 16 8 6

Gables Estates

25 12 8 9

Old Cutler

2010

2011

2012

2013

2014

10 56

8 57

8 86

4 77

10 76

Coconut Grove

Coral Gables

Palmetto Bay

CocoPlum

Gables Estates

Old Cutler Bay

Avg. Home Price # Transactions

$5,396,250 4

$6,452,708 25

$3,970,000 5

$5,216,667 3

$9,250,000 4

$4,125,000 4

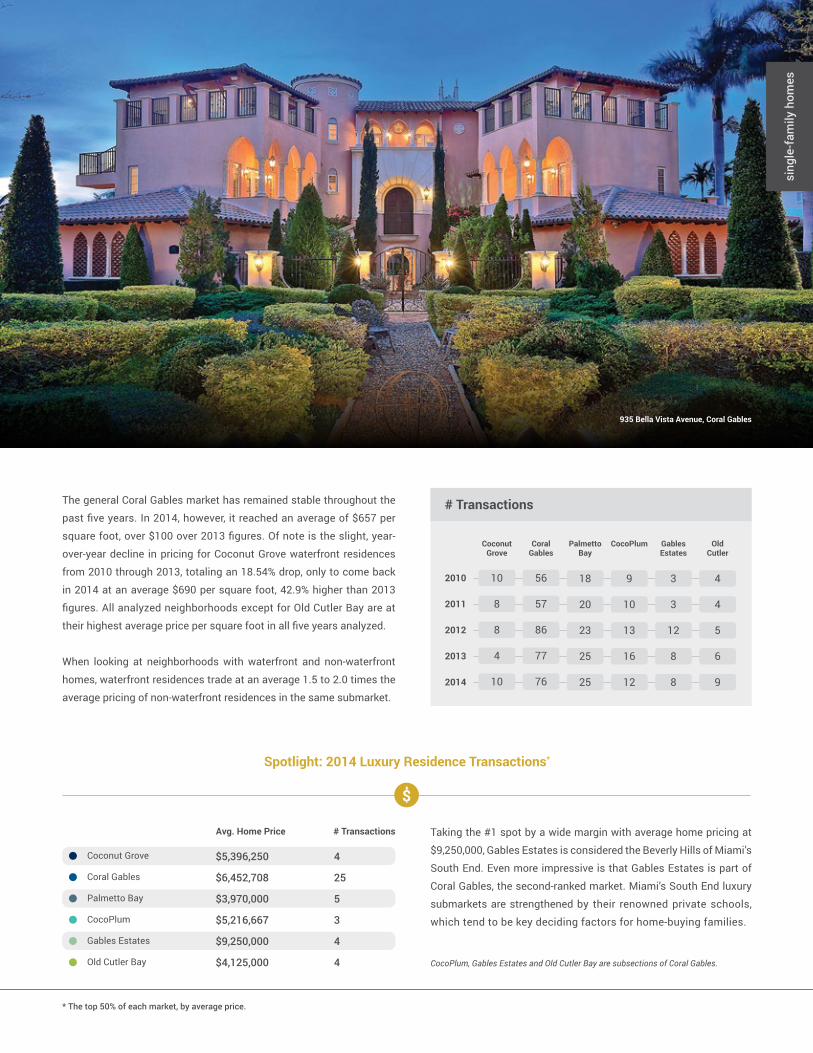

The general Coral Gables market has remained stable throughout the

past five years. In 2014, however, it reached an average of $657 per

square foot, over $100 over 2013 figures. Of note is the slight, year-

over-year decline in pricing for Coconut Grove waterfront residences

from 2010 through 2013, totaling an 18.54% drop, only to come back

in 2014 at an average $690 per square foot, 42.9% higher than 2013

figures. All analyzed neighborhoods except for Old Cutler Bay are at

their highest average price per square foot in all five years analyzed.

When looking at neighborhoods with waterfront and non-waterfront

homes, waterfront residences trade at an average 1.5 to 2.0 times the

average pricing of non-waterfront residences in the same submarket.

Taking the #1 spot by a wide margin with average home pricing at

$9,250,000, Gables Estates is considered the Beverly Hills of Miami’s

South End. Even more impressive is that Gables Estates is part of

Coral Gables, the second-ranked market. Miami’s South End luxury

submarkets are strengthened by their renowned private schools,

which tend to be key deciding factors for home-buying families.

* The top 50% of each market, by average price.

935 Bella Vista Avenue, Coral Gables

Spotlight: 2014 Luxury Residence Transactions*

CocoPlum, Gables Estates and Old Cutler Bay are subsections of Coral Gables.

12 | 2015 TRENDS Market Report

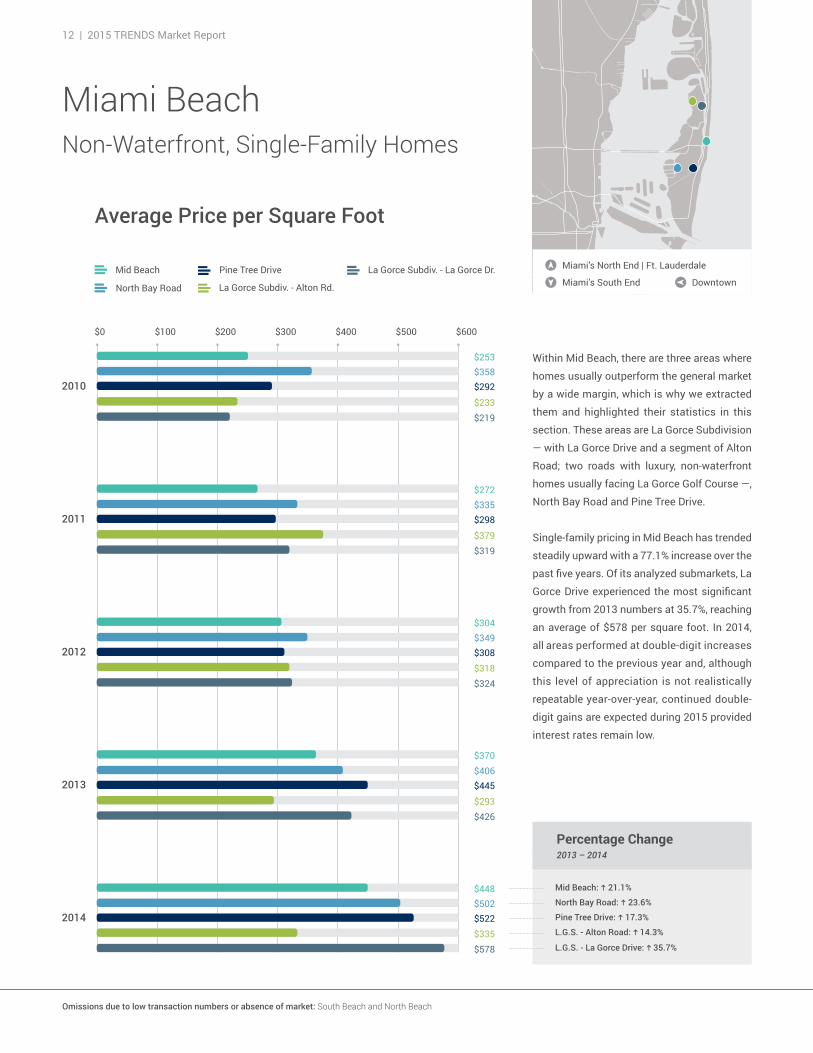

Within Mid Beach, there are three areas where

homes usually outperform the general market

by a wide margin, which is why we extracted

them and highlighted their statistics in this

section. These areas are La Gorce Subdivision

— with La Gorce Drive and a segment of Alton

Road; two roads with luxury, non-waterfront

homes usually facing La Gorce Golf Course —,

North Bay Road and Pine Tree Drive.

Single-family pricing in Mid Beach has trended

steadily upward with a 77.1% increase over the

past five years. Of its analyzed submarkets, La

Gorce Drive experienced the most significant

growth from 2013 numbers at 35.7%, reaching

an average of $578 per square foot. In 2014,

all areas performed at double-digit increases

compared to the previous year and, although

this level of appreciation is not realistically

repeatable year-over-year, continued double-

digit gains are expected during 2015 provided

interest rates remain low.

$400$300$200$100$0 $600

Miami BeachNon-Waterfront, Single-Family Homes

Average Price per Square Foot

Mid Beach

La Gorce Subdiv. - Alton Rd.North Bay Road

Pine Tree Drive

Percentage Change2013 – 2014

North Bay Road: g 23.6%

Mid Beach: g 21.1%

L.G.S. - Alton Road: g 14.3%

Pine Tree Drive: g 17.3%

$500

Omissions due to low transaction numbers or absence of market: South Beach and North Beach

La Gorce Subdiv. - La Gorce Dr.

$448

$335$522$502

$578

$370

$445$406

$293$426

$304

$308$349

$318$324

$272

$298$335

$379$319

$253

$292$358

$233$219

L.G.S. - La Gorce Drive: g 35.7%

Miami’s South End

Miami’s North End | Ft. Lauderdale

Downtown

ONE Sotheby’s International Realty | 13

Our Luxury Spotlight stars are North Bay Road, Pine Tree Drive and La Gorce

Drive, all three around the $2 million mark for non-waterfront homes. These

streets are the setting for many ultra-luxury, single-family homes, attracting high-

profile buyers from around the world. These properties also have a walkability

advantage over similarly priced homes in some of the islands, as they’re closer

to a plethora of entertainment options offered in Mid Beach and South Beach.

La Gorce Subdivision, North Bay Road and Pine Tree Drive are subsections of the Mid Beach market area.

sing

le-f

amily

hom

es

6222 Alton Road, Miami Beach

* The top 50% of each market, by average price.

Spotlight: 2014 Luxury Residence Transactions*

# Transactions

Mid Beach

2010

2011

2012

2013

2014

73

100

95

133

122

N. Bay Road

Pine Tree Drive

11 6

6 12

14 11

13 9

14 12

L.G.S.Alton Rd.

L.G.S.La Gorce Dr.

4 2

3 7

11 7

8 17

12 13

Avg. Home Price # Trans.

$1,960,099 41

$2,355,000 5

$2,632,143 7

Mid Beach

N. Bay Road

Pine Tree Drive

L.G.S. - Alton Road

L.G.S. - La Gorce Drive

$1,589,167

$2,395,180

6

5

“A member of La Gorce Country Club will certainly find a price premium worthy if

the residence sits on La Gorce Golf Course. The club has been known to extend

the privilege of providing golf cart access directly from homes to the golf course, a

feature that ultimately proves to be a weighing factor on potential buyers.”

– Dina Goldentayer, ONE Sotheby’s International Realty

Pine Tree Drive and North Bay Road are mostly known for their waterfront product,

but non-waterfront homes for both areas are in the $500-per-square-foot range,

outperforming the general Mid Beach market by 12% and 18% respectively. Alton

Road in La Gorce is the only analyzed submarket that didn’t reach Mid Beach’s

average pricing during 2014, most likely due to the price boost experienced by

the remaining submarkets and, ultimately, the general area.

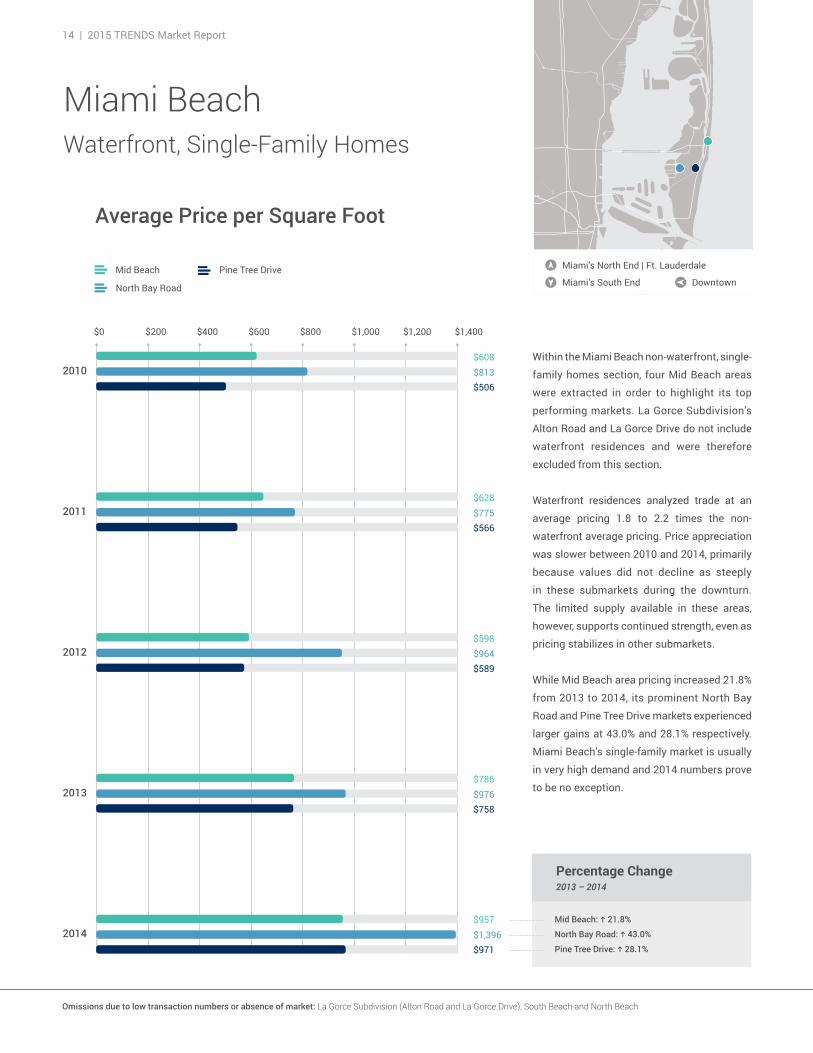

14 | 2015 TRENDS Market Report

Within the Miami Beach non-waterfront, single-

family homes section, four Mid Beach areas

were extracted in order to highlight its top

performing markets. La Gorce Subdivision’s

Alton Road and La Gorce Drive do not include

waterfront residences and were therefore

excluded from this section.

Waterfront residences analyzed trade at an

average pricing 1.8 to 2.2 times the non-

waterfront average pricing. Price appreciation

was slower between 2010 and 2014, primarily

because values did not decline as steeply

in these submarkets during the downturn.

The limited supply available in these areas,

however, supports continued strength, even as

pricing stabilizes in other submarkets.

While Mid Beach area pricing increased 21.8%

from 2013 to 2014, its prominent North Bay

Road and Pine Tree Drive markets experienced

larger gains at 43.0% and 28.1% respectively.

Miami Beach’s single-family market is usually

in very high demand and 2014 numbers prove

to be no exception.

Miami BeachWaterfront, Single-Family Homes

Miami’s South End

Miami’s North End | Ft. Lauderdale

Downtown

Average Price per Square Foot

Percentage Change2013 – 2014

North Bay Road: g 43.0%

Mid Beach: g 21.8%

Pine Tree Drive: g 28.1%

$608

$506$813

$628

$566$775

$598

$589$964

$786

$758$976

$957

$971$1,396

$600$400$200$0 $1,400$1,000$800 $1,200

Omissions due to low transaction numbers or absence of market: La Gorce Subdivision (Alton Road and La Gorce Drive), South Beach and North Beach

Mid Beach

North Bay Road

Pine Tree Drive

ONE Sotheby’s International Realty | 15

Avg. Home Price # Trans.

$10,485,958 12

$17,275,000 4

$6,400,000 3

Mid Beach

N. Bay Road

Pine Tree Dr.

# Transactions

Mid Beach

2010

2011

2012

2013

2014

19

21

31

26

32

N. Bay Road

Pine Tree Drive

8 7

10 5

6 6

5 9

10 4

North Bay Road is far and beyond the most high-end waterfront market in Miami Beach. Waterfront

homes in this area come with unbeatable views of Biscayne Bay and the Downtown Miami skyline.

North Bay Road homes also have an edge when it comes to buyers looking for the latest technology

and contemporary architecture.

Pine Tree Drive, running through eastern Mid Beach and providing canalfront residences, closed

2014 at $6,400,000 for its luxury segment. While much lower than Mid Beach in general, Pine Tree

Drive had the lowest transactional volume and is therefore subject to price volatility.North Bay Road and Pine Tree Drive are subsections of the Mid Beach market area.

sing

le-f

amily

hom

es

528 Lakeview Court, Miami Beach

* The top 50% of each market, by average price.

Spotlight: 2014 Luxury Residence Transactions*

Mid Beach contains some of South Florida’s most spectacular homes, many of them set on the

spotlight areas of North Bay Road and Pine Tree Drive. These streets have garnered a great deal

of attention due to the high profile of some of their residents, which undoubtedly increases the

demand for their exclusive properties.

Mid Beach is also the setting for many new developments such as The Residences at Ritz-Carlton,

a 111-residence luxury project featuring 15 exclusive villas directly on Surprise Lake. The Piero-

Lissoni-designed development is one of the most awaited new buildings because of the Ritz-

Carlton brand’s legendary service and quality standard. We expect the Mid Beach waterfront

market to continue drawing great demand, as new developments and an already strong, existing

housing market make the neighborhood one of the most exciting living options in the city.

16 | 2015 TRENDS Market Report

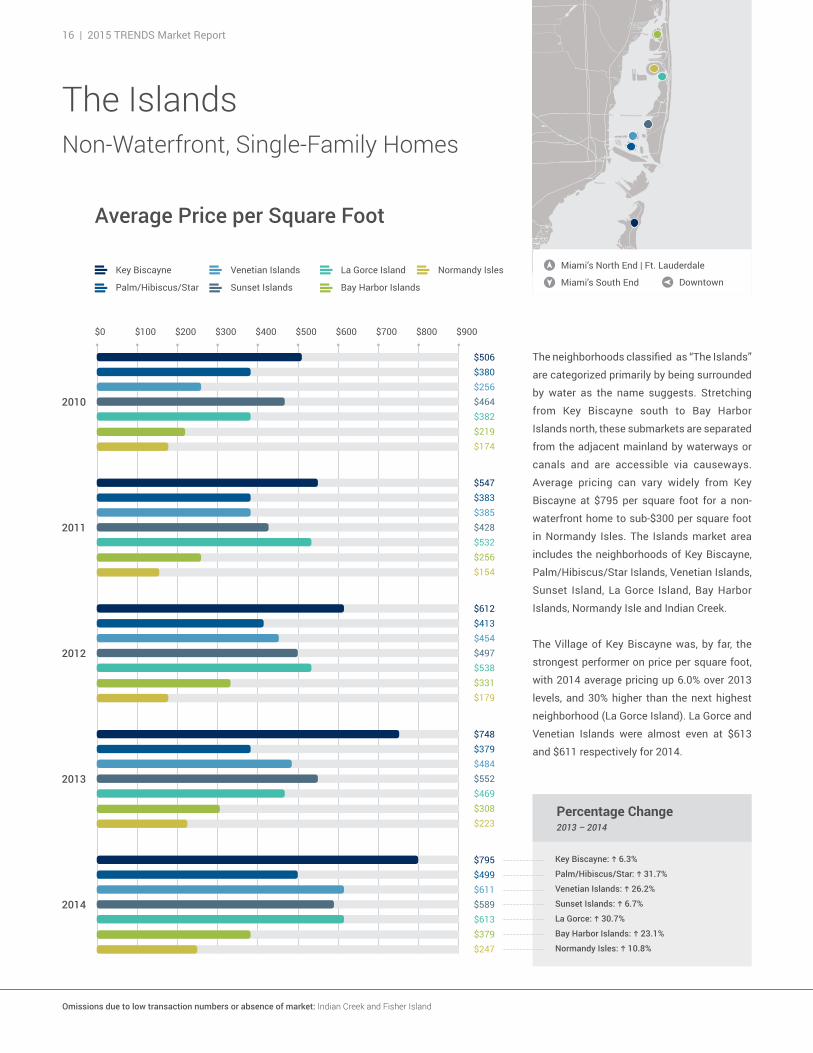

Key Biscayne: g 6.3%

Percentage Change2013 – 2014

The neighborhoods classified as “The Islands”

are categorized primarily by being surrounded

by water as the name suggests. Stretching

from Key Biscayne south to Bay Harbor

Islands north, these submarkets are separated

from the adjacent mainland by waterways or

canals and are accessible via causeways.

Average pricing can vary widely from Key

Biscayne at $795 per square foot for a non-

waterfront home to sub-$300 per square foot

in Normandy Isles. The Islands market area

includes the neighborhoods of Key Biscayne,

Palm/Hibiscus/Star Islands, Venetian Islands,

Sunset Island, La Gorce Island, Bay Harbor

Islands, Normandy Isle and Indian Creek.

The Village of Key Biscayne was, by far, the

strongest performer on price per square foot,

with 2014 average pricing up 6.0% over 2013

levels, and 30% higher than the next highest

neighborhood (La Gorce Island). La Gorce and

Venetian Islands were almost even at $613

and $611 respectively for 2014.

Normandy Isles: g 10.8%

Venetian Islands: g 26.2%

Palm/Hibiscus/Star: g 31.7%

Sunset Islands: g 6.7%

Bay Harbor Islands: g 23.1%

La Gorce: g 30.7%

$600$500$400$300$200$100$0 $900$800$700

Key Biscayne

Palm/Hibiscus/Star

The IslandsNon-Waterfront, Single-Family Homes

Venetian Islands

Sunset Islands

La Gorce Island Normandy Isles

Bay Harbor Islands

$506$380$256$464$382$219$174

$795$499$611$589$613$379$247

$547$383$385$428$532$256$154

$612$413$454$497$538$331$179

$748$379$484$552$469$308$223

Miami’s South End

Miami’s North End | Ft. Lauderdale

Downtown

Average Price per Square Foot

Omissions due to low transaction numbers or absence of market: Indian Creek and Fisher Island

sing

le-f

amily

hom

es

# Transactions

Key Biscayne

10 7 4 5 17

Palm/Hib./Star

14 4 5 8 17

VenetianIslands

19 6 2 7 36

Sunset Islands

23 8 2 9 30

La GorceIsland

19 7 4 19 26

Bay Harbor Islands

NormandyIsles

2010

2011

2012

2013

2014

59 4

63 5

63 6

59 5

63 2

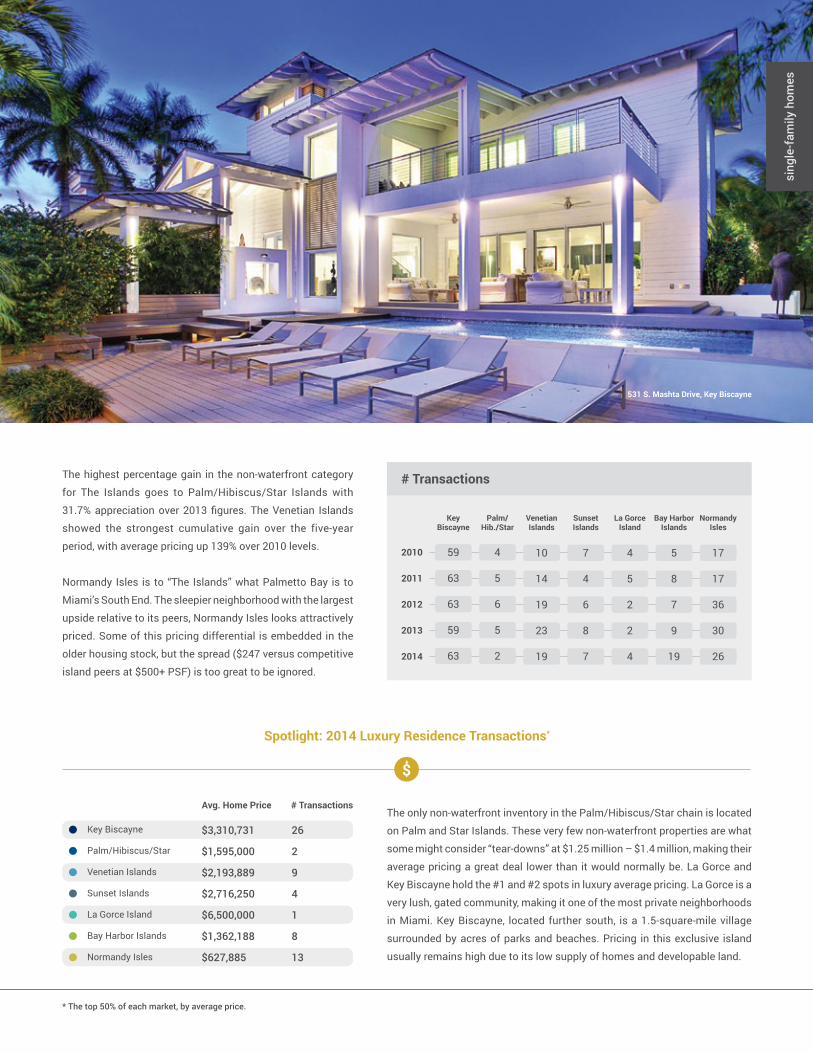

The highest percentage gain in the non-waterfront category

for The Islands goes to Palm/Hibiscus/Star Islands with

31.7% appreciation over 2013 figures. The Venetian Islands

showed the strongest cumulative gain over the five-year

period, with average pricing up 139% over 2010 levels.

Normandy Isles is to “The Islands” what Palmetto Bay is to

Miami’s South End. The sleepier neighborhood with the largest

upside relative to its peers, Normandy Isles looks attractively

priced. Some of this pricing differential is embedded in the

older housing stock, but the spread ($247 versus competitive

island peers at $500+ PSF) is too great to be ignored.

Key Biscayne

Palm/Hibiscus/Star

Venetian Islands

Sunset Islands

La Gorce Island

Bay Harbor Islands

Normandy Isles

Avg. Home Price # Transactions

$3,310,731 26

$1,595,000 2

$2,193,889 9

$2,716,250 4

$6,500,000 1

$1,362,188 8

$627,885 13

The only non-waterfront inventory in the Palm/Hibiscus/Star chain is located

on Palm and Star Islands. These very few non-waterfront properties are what

some might consider “tear-downs” at $1.25 million – $1.4 million, making their

average pricing a great deal lower than it would normally be. La Gorce and

Key Biscayne hold the #1 and #2 spots in luxury average pricing. La Gorce is a

very lush, gated community, making it one of the most private neighborhoods

in Miami. Key Biscayne, located further south, is a 1.5-square-mile village

surrounded by acres of parks and beaches. Pricing in this exclusive island

usually remains high due to its low supply of homes and developable land.

Spotlight: 2014 Luxury Residence Transactions*

* The top 50% of each market, by average price.

531 S. Mashta Drive, Key Biscayne

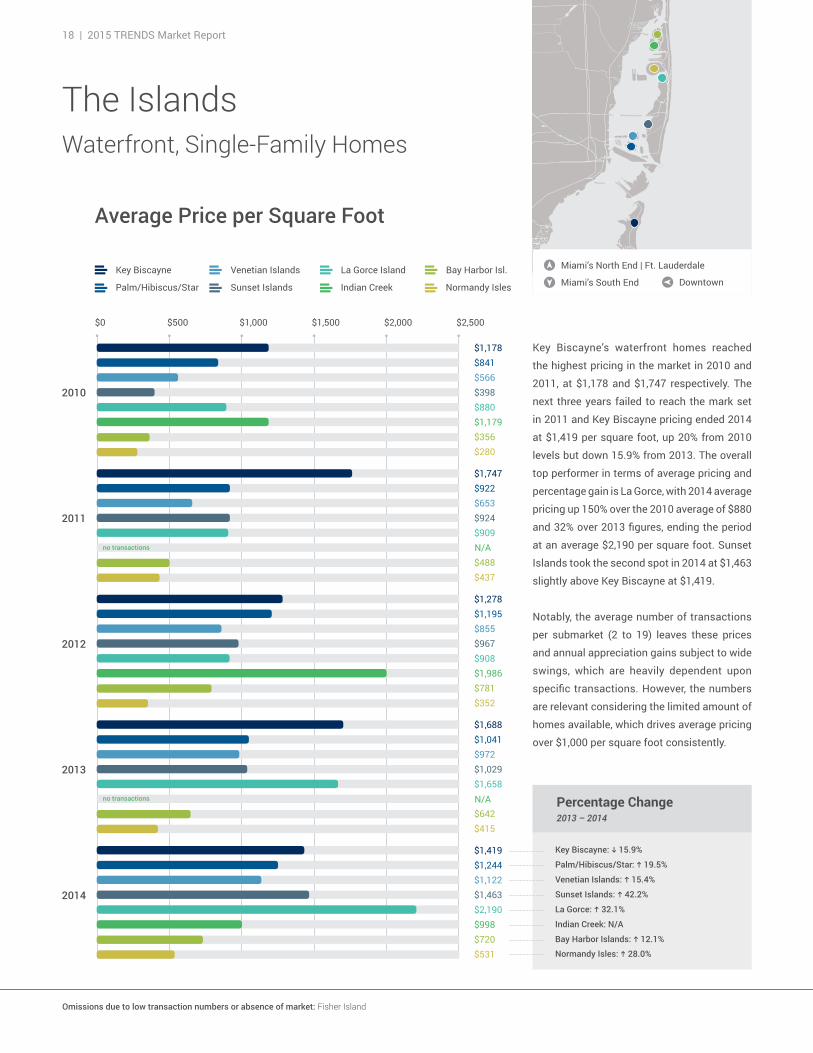

18 | 2015 TRENDS Market Report

The IslandsWaterfront, Single-Family Homes

$2,500$2,000$1,500$1,000$500$0

$1,178$841$566$398$880$1,179$356$280

$1,747$922$653$924$909

$488$437

$1,278$1,195$855$967$908$1,986$781$352

$1,688$1,041$972$1,029$1,658

$642$415

$1,419$1,244$1,122$1,463$2,190$998$720$531

Miami’s South End

Miami’s North End | Ft. Lauderdale

Downtown

Average Price per Square Foot

Key Biscayne: h 15.9%

Percentage Change2013 – 2014

Key Biscayne’s waterfront homes reached

the highest pricing in the market in 2010 and

2011, at $1,178 and $1,747 respectively. The

next three years failed to reach the mark set

in 2011 and Key Biscayne pricing ended 2014

at $1,419 per square foot, up 20% from 2010

levels but down 15.9% from 2013. The overall

top performer in terms of average pricing and

percentage gain is La Gorce, with 2014 average

pricing up 150% over the 2010 average of $880

and 32% over 2013 figures, ending the period

at an average $2,190 per square foot. Sunset

Islands took the second spot in 2014 at $1,463

slightly above Key Biscayne at $1,419.

Notably, the average number of transactions

per submarket (2 to 19) leaves these prices

and annual appreciation gains subject to wide

swings, which are heavily dependent upon

specific transactions. However, the numbers

are relevant considering the limited amount of

homes available, which drives average pricing

over $1,000 per square foot consistently.

Bay Harbor Islands: g 12.1%

Venetian Islands: g 15.4%

Palm/Hibiscus/Star: g 19.5%

Sunset Islands: g 42.2%

Indian Creek: N/A

La Gorce: g 32.1%

Normandy Isles: g 28.0%

Key Biscayne

Palm/Hibiscus/Star

Venetian Islands

Sunset Islands

La Gorce Island Bay Harbor Isl.

Indian Creek Normandy Isles

N/A

N/A

no transactions

no transactions

Omissions due to low transaction numbers or absence of market: Fisher Island

ONE Sotheby’s International Realty | 19

sing

le-f

amily

hom

es

# Transactions

Key Biscayne

13 2 4 1 1

Palm/Hib./Star

20 6 2 0 3

VenetianIslands

17 17 2 3 1

Sunset Islands

15 12 2 0 4

La GorceIsland

18 10 2 2 5

Bay Harbor Islands

NormandyIsles

2010

2011

2012

2013

2014

7 9

9 12

16 12

8 11

9 19

11

8

15

21

9

IndianCreek

Unlike most of the other markets studied in this

report, which showed price appreciation between

2013–2014 with a decline in the total number of

transactions, almost all of these submarkets had

more total transactions in 2014 than in 2013, with

the exception of Sunset Islands and Normandy

Isles. This could be a sign that appreciation rates

are expected to continue in the near future, since it

seems increased pricing is not slowing velocity. The

demand for The Islands will remain high, as their

luxurious lifestyle and amenities coupled with their

unparalleled privacy are highly desirable.

Key Biscayne

Palm/Hibiscus/Star

Venetian Islands

Sunset Islands

La Gorce Island

Indian Creek

Bay Harbor Islands

Normandy Isles

Avg. Home Price # Trans.

$9,417,500 4

$17,638,830 5

$7,015,000 5

$13,814,000 4

$14,250,000 2

$21,200,000 2

$4,333,333 3

$1,383,000 6

The waterfront Islands submarket represents the absolute top of the entire Miami-

Dade luxury market. Indian Creek and Palm/Hibiscus/Star hold the #1 and #2 spot in

the highest overall luxury pricing. Indian Creek’s main price driver is the fact that there

is little to no housing supply, as some years go by without seeing a single transaction.

To put these numbers in perspective, Indian Creek’s 86 residents’ net worth is estimated

at over $37 billion (most of which comes from a single uber-investor), which is greater

than the gross domestic product of half the world’s nations. In 2012, ONE Sotheby’s

International Realty represented the buyer in a $47 million transaction in Indian Creek,

breaking the county record at the time.

Spotlight: 2014 Luxury Residence Transactions*

* The top 50% of each market, by average price.

9 Harbor Point, Key Biscayne

20 | 2015 TRENDS Market Report

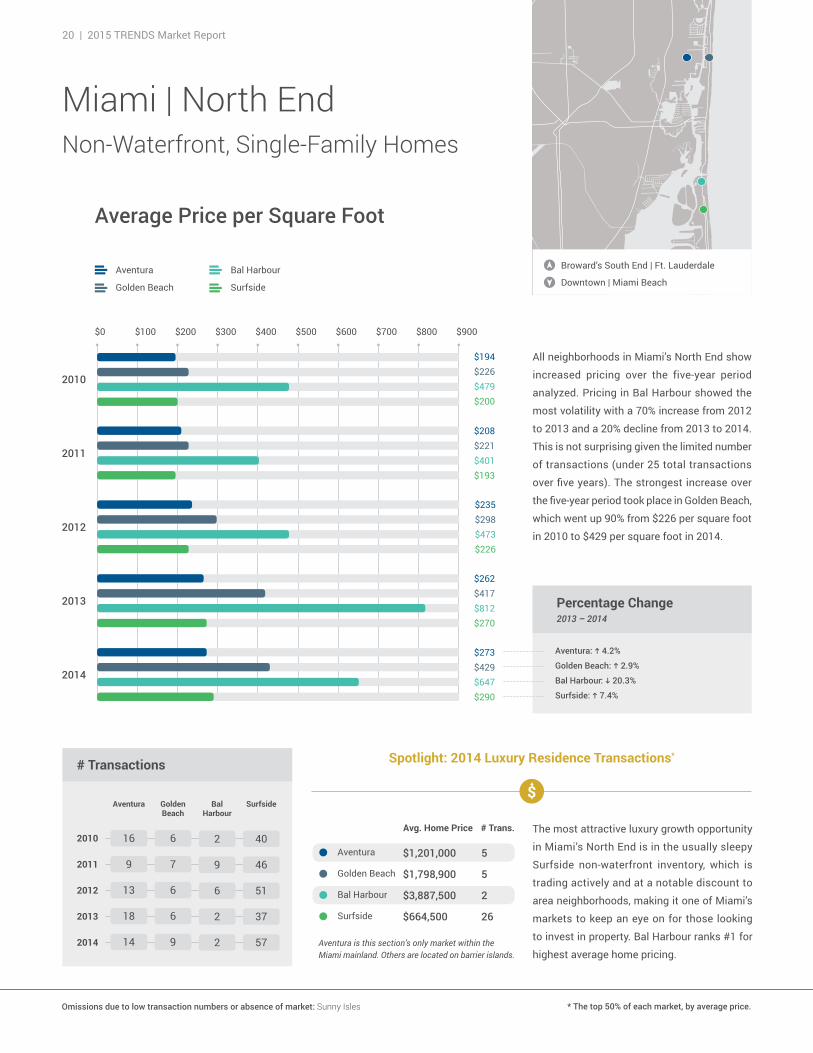

Percentage Change2013 – 2014

All neighborhoods in Miami’s North End show

increased pricing over the five-year period

analyzed. Pricing in Bal Harbour showed the

most volatility with a 70% increase from 2012

to 2013 and a 20% decline from 2013 to 2014.

This is not surprising given the limited number

of transactions (under 25 total transactions

over five years). The strongest increase over

the five-year period took place in Golden Beach,

which went up 90% from $226 per square foot

in 2010 to $429 per square foot in 2014.

Surfside: g 7.4%

Aventura: g 4.2%

Bal Harbour: h 20.3%

Golden Beach: g 2.9%

$600$500$400$300$200$100$0 $900$800$700

Aventura

Golden Beach

Bal Harbour

Surfside

Average Price per Square Foot

Miami | North EndNon-Waterfront, Single-Family Homes

$194$226$479$200

$208$221$401$193

$262$417$812$270

$273$429$647$290

$235$298$473$226

Downtown | Miami Beach

Broward’s South End | Ft. Lauderdale

# Transactions

Aventura

2 40

Golden Beach

9 46

BalHarbour

6 51

Surfside

2 37

2 57

2010

2011

2012

2013

2014

16 6

9 7

13 6

18 6

14 9

Aventura

Golden Beach

Bal Harbour

Surfside

Avg. Home Price # Trans.

$1,201,000 5

$1,798,900 5

$3,887,500 2

$664,500 26

The most attractive luxury growth opportunity

in Miami’s North End is in the usually sleepy

Surfside non-waterfront inventory, which is

trading actively and at a notable discount to

area neighborhoods, making it one of Miami’s

markets to keep an eye on for those looking

to invest in property. Bal Harbour ranks #1 for

highest average home pricing.

Omissions due to low transaction numbers or absence of market: Sunny Isles * The top 50% of each market, by average price.

Spotlight: 2014 Luxury Residence Transactions*

Aventura is this section’s only market within the Miami mainland. Others are located on barrier islands.

ONE Sotheby’s International Realty | 21

sing

le-f

amily

hom

es

Miami | North EndWaterfront, Single-Family Homes

$1,200$1,000$800$600$400$200$0 $1,400

Downtown | Miami Beach

Broward’s South End | Ft. LauderdaleAventura

Golden Beach

Bal Harbour

Surfside

Average Price per Square Foot

Percentage Change2013 – 2014

Pricing volatility in the waterfront category for

this market area is again dominated by the Bal

Harbour neighborhood, with the top average

price of $1,287 per square foot in 2013, 48%

higher than the next highest neighborhood for

any time period analyzed. Bal Harbour sales

volume for waterfront homes has averaged

one annual sale, limiting the reliability of the

analysis for this area. But for those listing a

Bal Harbour waterfront home, the market price

point will probably start at $1,200 per SF.

Surfside: h 14.9%

Aventura: g 8.9%

Bal Harbour: N/A

Golden Beach: g 16.4%$356$867

$607

$256$552

$353

$327$745$1,287$713

$300$791$796$338

$273$629$885$285

# Transactions

Aventura

1 3

Golden Beach

0 4

BalHarbour

1 3

Surfside

3 2

0 7

2010

2011

2012

2013

2014

20 8

15 16

22 11

31 14

25 7

Aventura

Golden Beach

Bal Harbour

Surfside

Avg. Home Price # Trans.

$881,429 7

$9,400,000 2

N/A 0

$3,550,000 3

no transactions N/A

no transactions N/A

Located on a barrier island separating the

Intracoastal Waterway from the ocean, the

high-end Golden Beach community offers one

of the only “on the sand”, single-family home

markets in Miami-Dade County, taking the #1

spot in Miami’s North End Luxury Spotlight by

a wide margin at an average $9,400,000. Bal

Harbour had no transactions during 2014.

Omissions due to low transaction numbers or absence of market: Sunny Isles * The top 50% of each market, by average price.

Spotlight: 2014 Luxury Residence Transactions*

Aventura is this section’s only market within the Miami mainland. Others are located on barrier islands.

22 | 2015 TRENDS Market Report

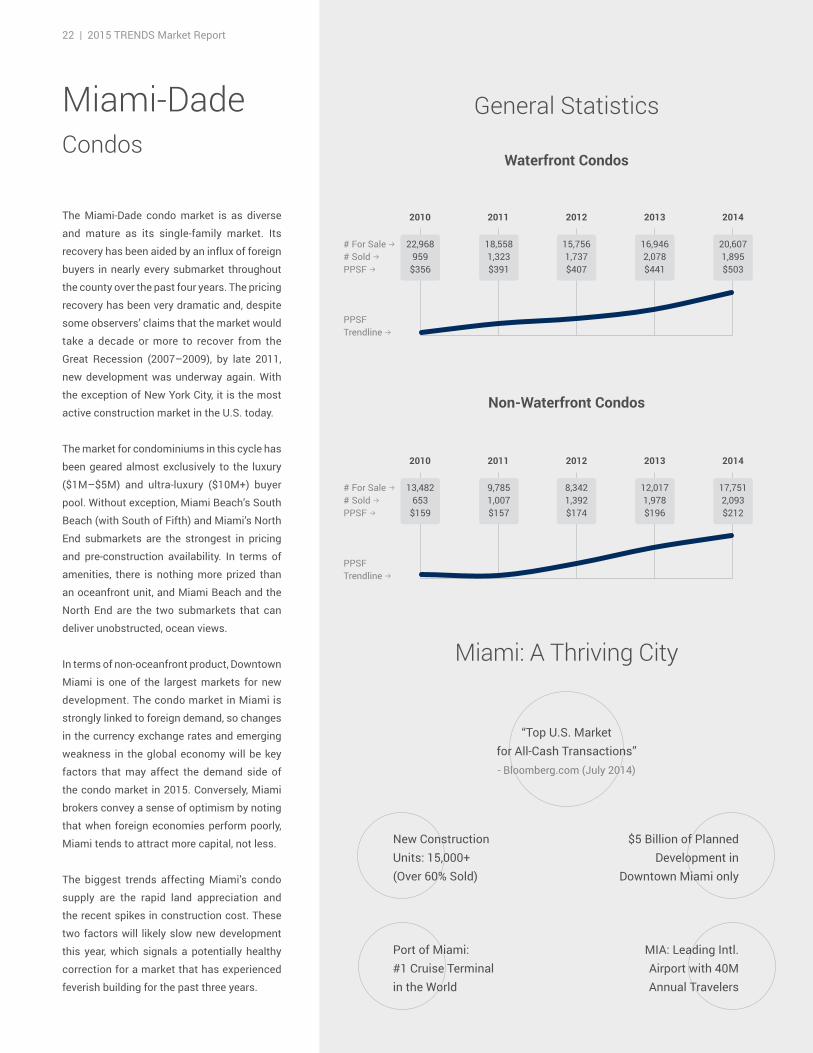

Luxury Spotlight

Non-Waterfront Condos

2010 2011 2012 2013 2014

13,482 653

$159

# For Sale b# Sold bPPSF b

9,785 1,007$157

8,342 1,392$174

12,017 1,978$196

17,7512,093$212

PPSF Trendline b

Waterfront Condos

2010 2011 2012 2013 2014

22,968 959

$356

# For Sale b# Sold bPPSF b

18,5581,323$391

15,756 1,737$407

16,946 2,078$441

20,607 1,895$503

PPSF Trendline b

Miami-DadeCondos

General Statistics

The Miami-Dade condo market is as diverse

and mature as its single-family market. Its

recovery has been aided by an influx of foreign

buyers in nearly every submarket throughout

the county over the past four years. The pricing

recovery has been very dramatic and, despite

some observers’ claims that the market would

take a decade or more to recover from the

Great Recession (2007–2009), by late 2011,

new development was underway again. With

the exception of New York City, it is the most

active construction market in the U.S. today.

The market for condominiums in this cycle has

been geared almost exclusively to the luxury

($1M–$5M) and ultra-luxury ($10M+) buyer

pool. Without exception, Miami Beach’s South

Beach (with South of Fifth) and Miami’s North

End submarkets are the strongest in pricing

and pre-construction availability. In terms of

amenities, there is nothing more prized than

an oceanfront unit, and Miami Beach and the

North End are the two submarkets that can

deliver unobstructed, ocean views.

In terms of non-oceanfront product, Downtown

Miami is one of the largest markets for new

development. The condo market in Miami is

strongly linked to foreign demand, so changes

in the currency exchange rates and emerging

weakness in the global economy will be key

factors that may affect the demand side of

the condo market in 2015. Conversely, Miami

brokers convey a sense of optimism by noting

that when foreign economies perform poorly,

Miami tends to attract more capital, not less.

The biggest trends affecting Miami’s condo

supply are the rapid land appreciation and

the recent spikes in construction cost. These

two factors will likely slow new development

this year, which signals a potentially healthy

correction for a market that has experienced

feverish building for the past three years.

Miami: A Thriving City

“Top U.S. Market for All-Cash Transactions” - Bloomberg.com (July 2014)

Port of Miami: #1 Cruise Terminal in the World

New Construction Units: 15,000+(Over 60% Sold)

MIA: Leading Intl. Airport with 40M Annual Travelers

$5 Billion of Planned Development in

Downtown Miami only

ONE Sotheby’s International Realty | 23

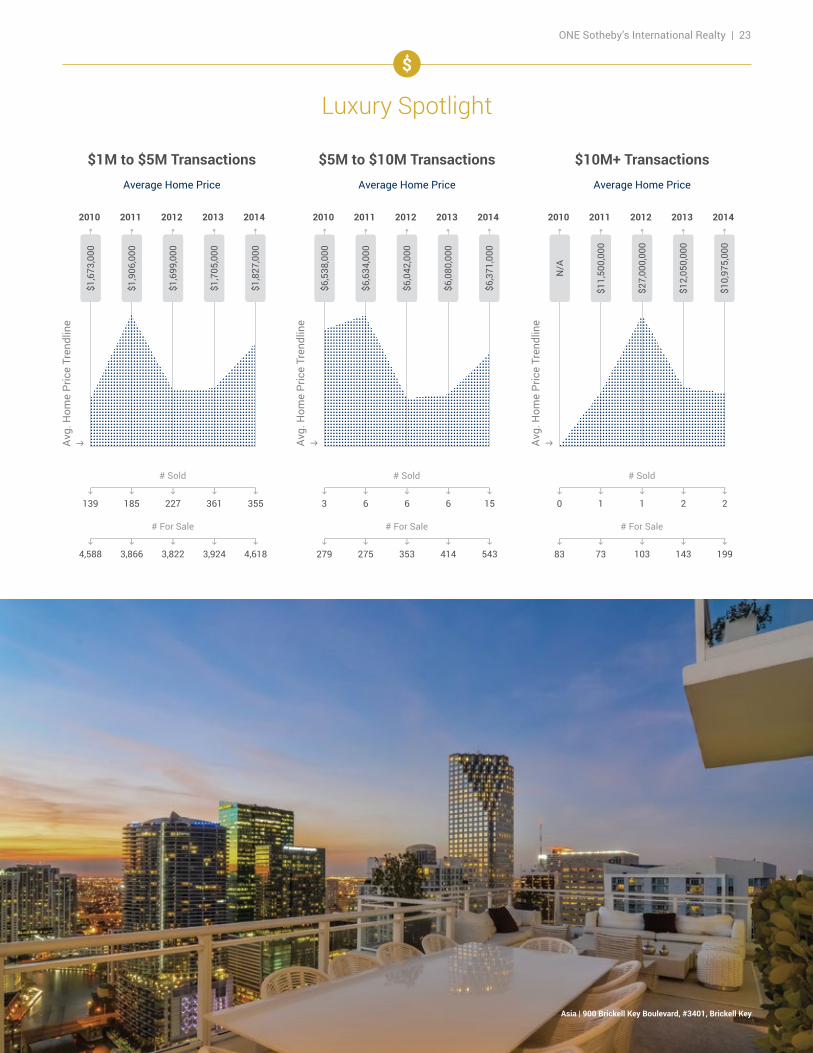

Luxury Spotlight

$1M to $5M TransactionsAverage Home Price

$5M to $10M TransactionsAverage Home Price

$10M+ TransactionsAverage Home Price

2010 2011 2012 2013 2014

$1,6

73,0

00

$1,9

06,0

00

$1,6

99,0

00

$1,7

05,0

00

$1,8

27,0

00

h

139

h

4,588

h

185

h

3,866

# Sold

# For Sale

h

361

h

3,924

h

355

h

4,618

h

227

h

3,822

2010 2011 2012 2013 2014

$6,5

38,0

00

$6,6

34,0

00

$6,0

42,0

00

$6,0

80,0

00

$6,3

71,0

00h

3

h

279

h

6

h

275

# Sold

# For Sale

h

6

h

414

h

15

h

543

h

6

h

353

2010 2011 2012 2013 2014

N/A

$11,

500,

000

$27,

000,

000

$12,

050,

000

$10,

975,

000

h

0

h

83

h

1

h

73

# Sold

# For Sale

h

2

h

143

h

2

h

199

h

1

h

103

Asia | 900 Brickell Key Boulevard, #3401, Brickell Key

Avg.

Hom

e Pr

ice

Tren

dlin

eh Av

g. H

ome

Pric

e Tr

endl

ine

h Avg.

Hom

e Pr

ice

Tren

dlin

eh

24 | 2015 TRENDS Market Report

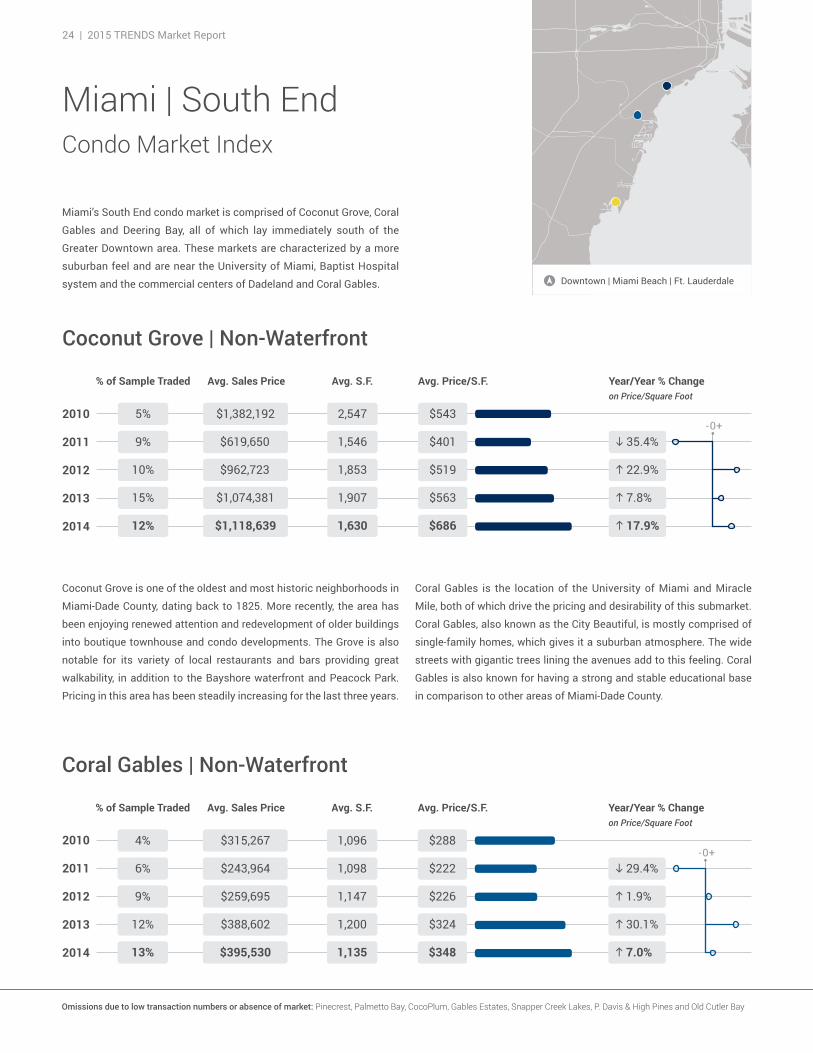

Miami | South EndCondo Market Index

Miami’s South End condo market is comprised of Coconut Grove, Coral

Gables and Deering Bay, all of which lay immediately south of the

Greater Downtown area. These markets are characterized by a more

suburban feel and are near the University of Miami, Baptist Hospital

system and the commercial centers of Dadeland and Coral Gables.

Coconut Grove is one of the oldest and most historic neighborhoods in

Miami-Dade County, dating back to 1825. More recently, the area has

been enjoying renewed attention and redevelopment of older buildings

into boutique townhouse and condo developments. The Grove is also

notable for its variety of local restaurants and bars providing great

walkability, in addition to the Bayshore waterfront and Peacock Park.

Pricing in this area has been steadily increasing for the last three years.

Downtown | Miami Beach | Ft. Lauderdale

-0+

Coral Gables | Non-Waterfront

% of Sample Traded

4%

6%

9%

12%

13%

Avg. Sales Price Avg. S.F. Avg. Price/S.F. Year/Year % Changeon Price/Square Foot

g 30.1%

g 1.9%

h 29.4%

g 7.0%

$324

$226

$222

$348

$288

1,200

1,147

1,098

1,135

1,096$315,267

$243,964

$259,695

$388,602

$395,530

2010

2011

2012

2013

2014

Coral Gables is the location of the University of Miami and Miracle

Mile, both of which drive the pricing and desirability of this submarket.

Coral Gables, also known as the City Beautiful, is mostly comprised of

single-family homes, which gives it a suburban atmosphere. The wide

streets with gigantic trees lining the avenues add to this feeling. Coral

Gables is also known for having a strong and stable educational base

in comparison to other areas of Miami-Dade County.

Coconut Grove | Non-Waterfront

% of Sample Traded

5%

9%

10%

15%

12%

Avg. Sales Price Avg. S.F. Avg. Price/S.F. Year/Year % Changeon Price/Square Foot

g 7.8%

g 22.9%

h 35.4%

g 17.9%

$563

$519

$401

$686

$543

1,907

1,853

1,546

1,630

2,547$1,382,192

$619,650

$962,723

$1,074,381

$1,118,639

2010

2011

2012

2013

2014

-0+

Omissions due to low transaction numbers or absence of market: Pinecrest, Palmetto Bay, CocoPlum, Gables Estates, Snapper Creek Lakes, P. Davis & High Pines and Old Cutler Bay

ONE Sotheby’s International Realty | 25

-0+2010

2011

2012

2013

2014

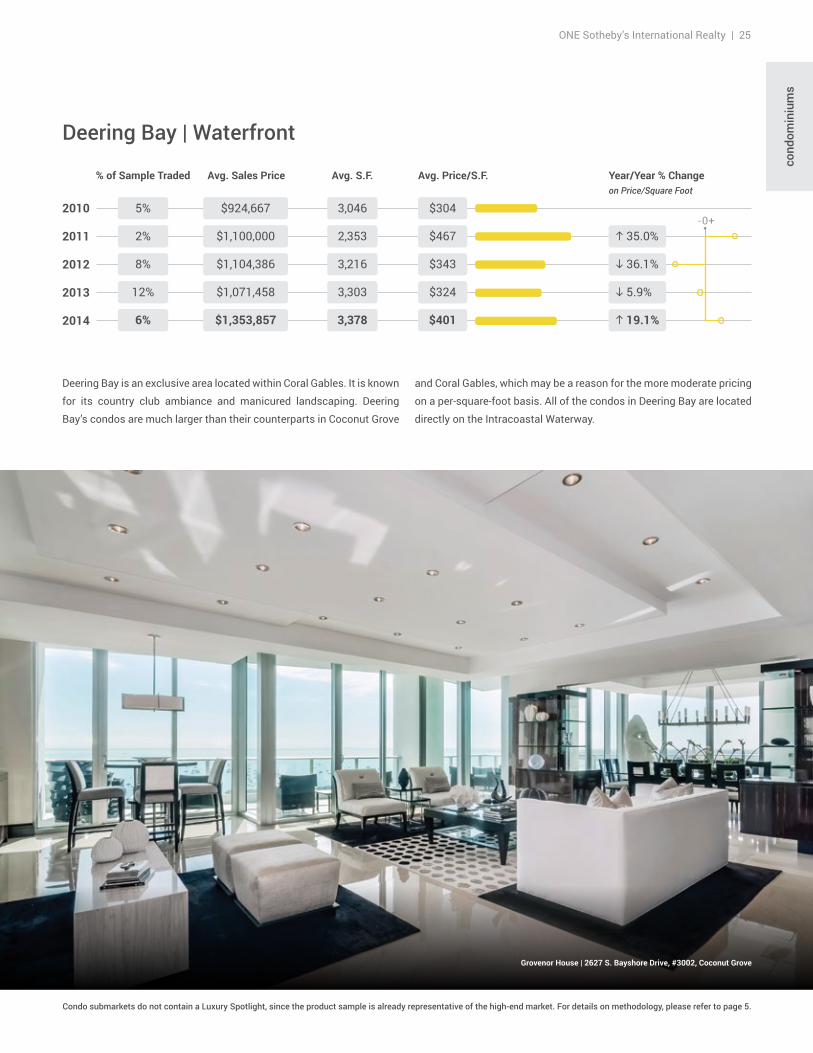

Deering Bay | Waterfront

% of Sample Traded

5%

2%

8%

12%

6%

Avg. Sales Price Avg. S.F. Avg. Price/S.F. Year/Year % Changeon Price/Square Foot

h 5.9%

h 36.1%

g 35.0%

g 19.1%

$324

$343

$467

$401

$304

3,303

3,216

2,353

3,378

3,046$924,667

$1,100,000

$1,104,386

$1,071,458

$1,353,857

cond

omin

ium

s

Deering Bay is an exclusive area located within Coral Gables. It is known

for its country club ambiance and manicured landscaping. Deering

Bay’s condos are much larger than their counterparts in Coconut Grove

and Coral Gables, which may be a reason for the more moderate pricing

on a per-square-foot basis. All of the condos in Deering Bay are located

directly on the Intracoastal Waterway.

Grovenor House | 2627 S. Bayshore Drive, #3002, Coconut Grove

Condo submarkets do not contain a Luxury Spotlight, since the product sample is already representative of the high-end market. For details on methodology, please refer to page 5.

26 | 2015 TRENDS Market Report

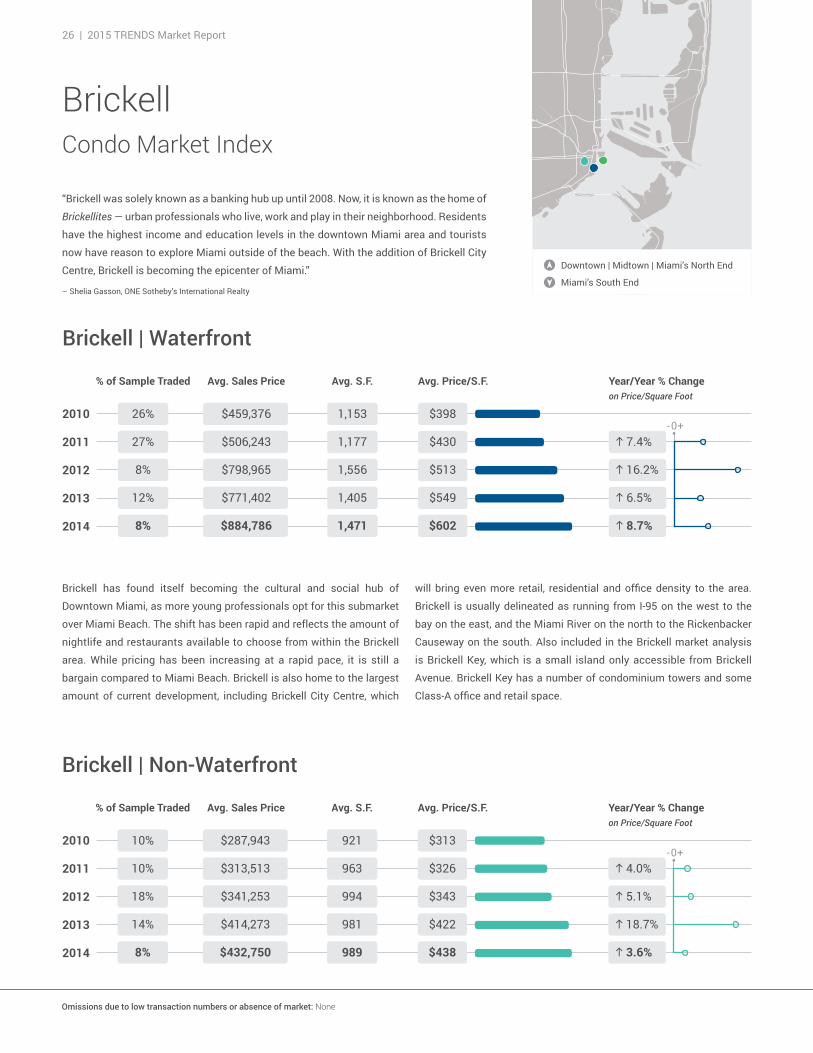

BrickellCondo Market Index

Miami’s South End

Downtown | Midtown | Miami’s North End

-0+2010

2011

2012

2013

2014

Brickell | Waterfront

% of Sample Traded

26%

27%

8%

12%

8%

Avg. Sales Price Avg. S.F. Avg. Price/S.F. Year/Year % Changeon Price/Square Foot

g 6.5%

g 16.2%

g 7.4%

g 8.7%

$549

$513

$430

$602

$398

1,405

1,556

1,177

1,471

1,153$459,376

$506,243

$798,965

$771,402

$884,786

-0+2010

2011

2012

2013

2014

Brickell | Non-Waterfront

% of Sample Traded

10%

10%

18%

14%

8%

Avg. Sales Price Avg. S.F. Avg. Price/S.F. Year/Year % Changeon Price/Square Foot

g 18.7%

g 5.1%

g 4.0%

g 3.6%

$422

$343

$326

$438

$313

981

994

963

989

921$287,943

$313,513

$341,253

$414,273

$432,750

“Brickell was solely known as a banking hub up until 2008. Now, it is known as the home of

Brickellites — urban professionals who live, work and play in their neighborhood. Residents

have the highest income and education levels in the downtown Miami area and tourists

now have reason to explore Miami outside of the beach. With the addition of Brickell City

Centre, Brickell is becoming the epicenter of Miami.”

– Shelia Gasson, ONE Sotheby’s International Realty

Brickell has found itself becoming the cultural and social hub of

Downtown Miami, as more young professionals opt for this submarket

over Miami Beach. The shift has been rapid and reflects the amount of

nightlife and restaurants available to choose from within the Brickell

area. While pricing has been increasing at a rapid pace, it is still a

bargain compared to Miami Beach. Brickell is also home to the largest

amount of current development, including Brickell City Centre, which

will bring even more retail, residential and office density to the area.

Brickell is usually delineated as running from I-95 on the west to the

bay on the east, and the Miami River on the north to the Rickenbacker

Causeway on the south. Also included in the Brickell market analysis

is Brickell Key, which is a small island only accessible from Brickell

Avenue. Brickell Key has a number of condominium towers and some

Class-A office and retail space.

Omissions due to low transaction numbers or absence of market: None

ONE Sotheby’s International Realty | 27

-0+2010

2011

2012

2013

2014

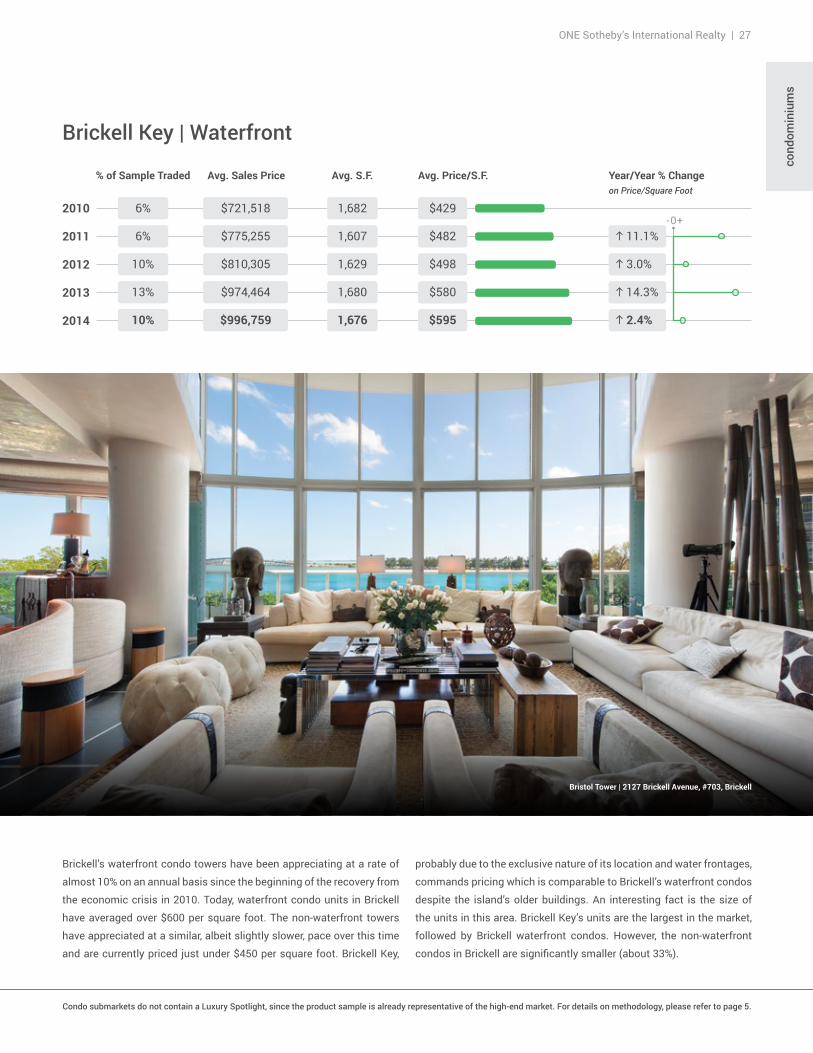

Brickell Key | Waterfront

% of Sample Traded

6%

6%

10%

13%

10%

Avg. Sales Price Avg. S.F. Avg. Price/S.F. Year/Year % Changeon Price/Square Foot

g 14.3%

g 3.0%

g 11.1%

g 2.4%

$580

$498

$482

$595

$429

1,680

1,629

1,607

1,676

1,682$721,518

$775,255

$810,305

$974,464

$996,759

cond

omin

ium

s

Brickell’s waterfront condo towers have been appreciating at a rate of

almost 10% on an annual basis since the beginning of the recovery from

the economic crisis in 2010. Today, waterfront condo units in Brickell

have averaged over $600 per square foot. The non-waterfront towers

have appreciated at a similar, albeit slightly slower, pace over this time

and are currently priced just under $450 per square foot. Brickell Key,

probably due to the exclusive nature of its location and water frontages,

commands pricing which is comparable to Brickell’s waterfront condos

despite the island’s older buildings. An interesting fact is the size of

the units in this area. Brickell Key’s units are the largest in the market,

followed by Brickell waterfront condos. However, the non-waterfront

condos in Brickell are significantly smaller (about 33%).

Bristol Tower | 2127 Brickell Avenue, #703, Brickell

Condo submarkets do not contain a Luxury Spotlight, since the product sample is already representative of the high-end market. For details on methodology, please refer to page 5.

28 | 2015 TRENDS Market Report

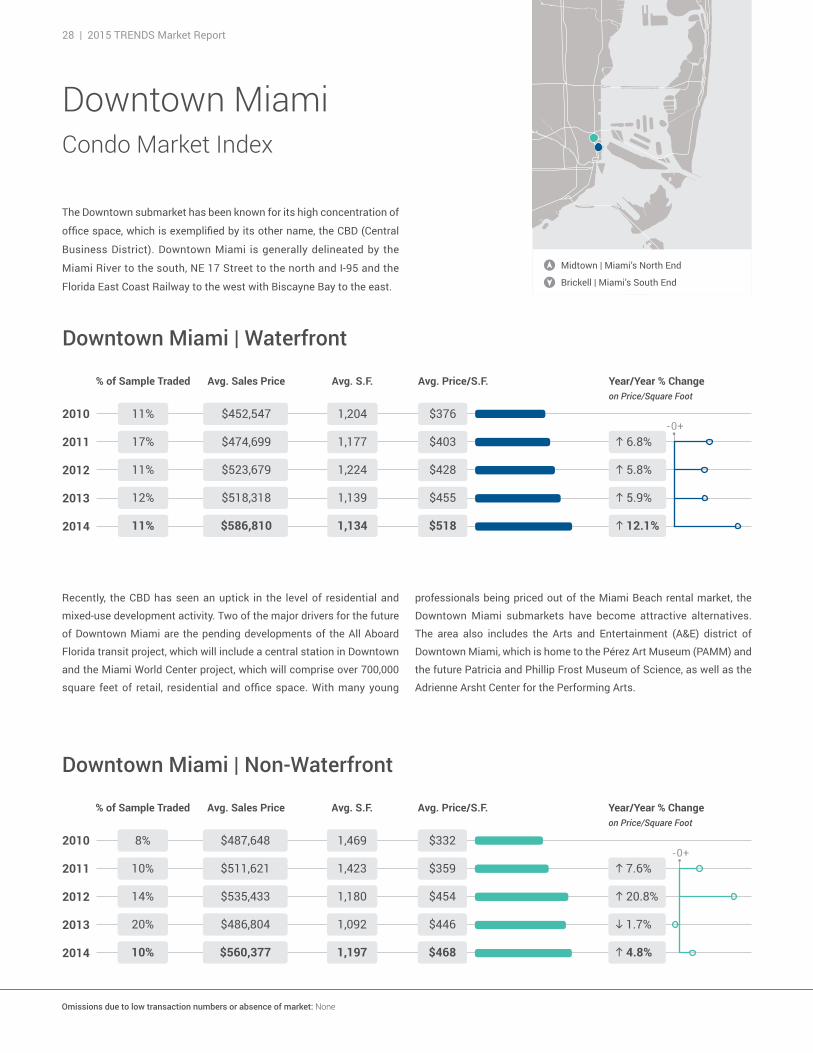

Downtown MiamiCondo Market Index

Brickell | Miami’s South End

Midtown | Miami’s North End

-0+2010

2011

2012

2013

2014

Downtown Miami | Waterfront

% of Sample Traded

11%

17%

11%

12%

11%

Avg. Sales Price Avg. S.F. Avg. Price/S.F. Year/Year % Changeon Price/Square Foot

g 5.9%

g 5.8%

g 6.8%

g 12.1%

$455

$428

$403

$518

$376

1,139

1,224

1,177

1,134

1,204$452,547

$474,699

$523,679

$518,318

$586,810

-0+2010

2011

2012

2013

2014

Downtown Miami | Non-Waterfront

% of Sample Traded

8%

10%

14%

20%

10%

Avg. Sales Price Avg. S.F. Avg. Price/S.F. Year/Year % Changeon Price/Square Foot

h 1.7%

g 20.8%

g 7.6%

g 4.8%

$446

$454

$359

$468

$332

1,092

1,180

1,423

1,197

1,469$487,648

$511,621

$535,433

$486,804

$560,377

The Downtown submarket has been known for its high concentration of

office space, which is exemplified by its other name, the CBD (Central

Business District). Downtown Miami is generally delineated by the

Miami River to the south, NE 17 Street to the north and I-95 and the

Florida East Coast Railway to the west with Biscayne Bay to the east.

Recently, the CBD has seen an uptick in the level of residential and

mixed-use development activity. Two of the major drivers for the future

of Downtown Miami are the pending developments of the All Aboard

Florida transit project, which will include a central station in Downtown

and the Miami World Center project, which will comprise over 700,000

square feet of retail, residential and office space. With many young

professionals being priced out of the Miami Beach rental market, the

Downtown Miami submarkets have become attractive alternatives.

The area also includes the Arts and Entertainment (A&E) district of

Downtown Miami, which is home to the Pérez Art Museum (PAMM) and

the future Patricia and Phillip Frost Museum of Science, as well as the

Adrienne Arsht Center for the Performing Arts.

Omissions due to low transaction numbers or absence of market: None

ONE Sotheby’s International Realty | 29

cond

omin

ium

s

As for pricing, Downtown Miami has largely

mirrored the appreciation rates experienced

in the Brickell submarket, with waterfront

properties achieving almost $520 per square

foot and the non-waterfront properties not

far behind at $468 per square foot. Pricing is

comparable to Brickell but includes a greater

variety of product types, from more affordable

to ultra-luxury. As was previously mentioned,

the Downtown Miami submarket includes

the Arts and Entertainment District, home to

several luxury projects. With the increasing

profile of the neighboring Edgewater/Midtown

submarket and the new development success

in Brickell, the CBD and A&E submarkets are

likely to experience a beneficial spill-over of

successful infill projects.

Two key factors inhibiting future inventory

entering the pipeline are quickly-escalating

land prices and spiking construction costs.

These factors are expected to slow the new

construction in the coming year and may stall

some of the secondary CBD projects in 2015.

New Cultural Development

Microsoft Innovation CenterFirst MIC to be set in the U.S.

Condo submarkets do not contain a Luxury Spotlight, since the product sample is already representative of the high-end market. For details on methodology, please refer to page 5.

Miami World Center$2 Billion, Ten-Block Mega-Project

Frost Museum of ScienceDesigned by Grimshaw Architects

Pérez Art Museum MiamiDesigned by Herzog & de Meuron

Downtown Miami

30 | 2015 TRENDS Market Report

Edgewater & MidtownCondo Market Index

Downtown | Brickell | Miami’s South End

Miami’s North End | Ft. Lauderdale

-0+2010

2011

2012

2013

2014

Edgewater | Waterfront

% of Sample Traded

1%

1%

2%

3%

1%

Avg. Sales Price Avg. S.F. Avg. Price/S.F. Year/Year % Changeon Price/Square Foot

h 5.9%

h 36.1%

g 68.3%

g 19.1%

$324

$343

$467

$401

$148

3,303

3,216

2,353

3,378

1,128$167,000

$1,100,000

$1,104,386

$1,071,458

$1,353,857

-0+2010

2011

2012

2013

2014

Edgewater | Non-Waterfront

% of Sample Traded

8%

9%

10%

17%

11%

Avg. Sales Price Avg. S.F. Avg. Price/S.F. Year/Year % Changeon Price/Square Foot

g 18.3%

h 21.8%

g 27.0%

g 3.2%

$333

$272

$331

$344

$242

1,156

1,142

1,100

1,106

1,152$278,485

$364,299

$310,387

$384,652

$379,903

The Edgewater/Midtown submarket is comprised of East Edgewater

and the Midtown district just west of Biscayne Boulevard and West

Edgewater. Edgewater is located on the eastern strip of coastal land

immediately north of Downtown Miami (aka the CBD), with Midtown

found on the west side of the Florida East Coast Railway.

Edgewater had been overlooked for over a decade leading up to 2012,

when Jorge Pérez of the Related Group announced that he would be

developing a four-tower residential/resort project within the Edgewater

submarket known as the Paraiso Bay master development. Related’s

plan called for about 1,400 residential units, luxury amenities and an

elaborate, bayfront walkway within the two-acre development site.

Paraiso Bay was just the first of various residential and mixed-use

developments to be announced in the neighborhood later on. There

are now over 1,500 condo units currently under construction with more

than 2,000 more units in the planning pipeline. Much of the charm and

appeal of the Biscayne Corridor area is the easy accessibility to the

Miami CBD, the interstate highways and Miami Beach. Additionally, the

area is significantly less congested than the Central Business District

and condo residences are typically much larger and more affordable

than they are in comparable developments elsewhere in the Greater

Downtown Miami market.

Omissions due to low transaction numbers or absence of market: None

ONE Sotheby’s International Realty | 31

-0+2010

2011

2012

2013

2014

Midtown | Non-Waterfront

% of Sample Traded

3%

4%

17%

23%

23%

Avg. Sales Price Avg. S.F. Avg. Price/S.F. Year/Year % Changeon Price/Square Foot

g 17.1%

h 3.0%

g 37.5%

h 0.5%

$385

$319

$329

$383

$206

1,089

1,072

1,172

1,125

1,014$208,328

$385,160

$342,413

$419,365

$430,701

cond

omin

ium

s

Paramount Bay | 2020 N. Bayshore Drive, #2710, Edgewater

Condo submarkets do not contain a Luxury Spotlight, since the product sample is already representative of the high-end market. For details on methodology, please refer to page 5.

Midtown has seen a resurgence of development interest following the

creation of the Shops at Midtown and the Midtown condo projects,

developed during the last cycle (2003–2007). The area is seen as

an alternative to the density of Brickell and CBD for entertainment

and living, and offers lifestyle proximity to the edgy and very trendy

Wynwood Art District and up-and-coming neighbor, Design District.

Edgewater and Midtown are trading at a significant discount versus

other Downtown Miami area submarkets. Waterfront properties can

be purchased for about $400 per square foot and non-waterfront for

just $344 per square foot, with Midtown priced somewhere in between.

A project creating key linkage between the Design District, Midtown and

Edgewater at a pedestrian level would be ideal for this growing market.

32 | 2015 TRENDS Market Report

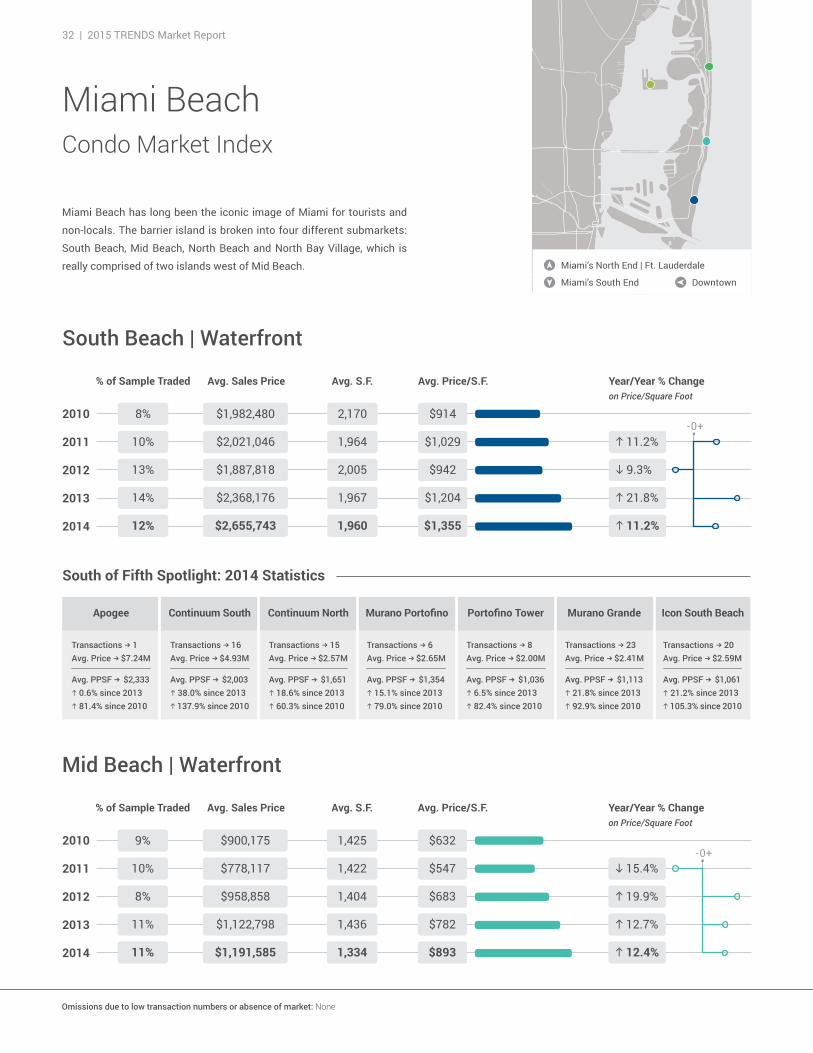

Miami BeachCondo Market Index

Miami’s South End

Miami’s North End | Ft. Lauderdale

-0+2010

2011

2012

2013

2014

South Beach | Waterfront

% of Sample Traded

8%

10%

13%

14%

12%

Avg. Sales Price Avg. S.F. Avg. Price/S.F. Year/Year % Changeon Price/Square Foot

g 21.8%

h 9.3%

g 11.2%

g 11.2%

$1,204

$942

$1,029

$1,355

$914

1,967

2,005

1,964

1,960

2,170$1,982,480

$2,021,046

$1,887,818

$2,368,176

$2,655,743

-0+2010

2011

2012

2013

2014

Mid Beach | Waterfront

% of Sample Traded

9%

10%

8%

11%

11%

Avg. Sales Price Avg. S.F. Avg. Price/S.F. Year/Year % Changeon Price/Square Foot

g 12.7%

g 19.9%

h 15.4%

g 12.4%

$782

$683

$547

$893

$632

1,436

1,404

1,422

1,334

1,425$900,175

$778,117

$958,858

$1,122,798

$1,191,585

Miami Beach has long been the iconic image of Miami for tourists and

non-locals. The barrier island is broken into four different submarkets:

South Beach, Mid Beach, North Beach and North Bay Village, which is

really comprised of two islands west of Mid Beach. Downtown

South of Fifth Spotlight: 2014 Statistics

Omissions due to low transaction numbers or absence of market: None

Apogee Continuum South Continuum North Murano Portofino Murano Grande Icon South BeachPortofino Tower

Transactions b 1 Avg. Price b $7.24M

Avg. PPSF b $2,333g 0.6% since 2013g 81.4% since 2010

Transactions b 16 Avg. Price b $4.93M

Avg. PPSF b $2,003g 38.0% since 2013g 137.9% since 2010

Transactions b 15 Avg. Price b $2.57M

Avg. PPSF b $1,651g 18.6% since 2013g 60.3% since 2010

Transactions b 6 Avg. Price b $2.65M

Avg. PPSF b $1,354g 15.1% since 2013g 79.0% since 2010

Transactions b 8 Avg. Price b $2.00M

Avg. PPSF b $1,036g 6.5% since 2013g 82.4% since 2010

Transactions b 23 Avg. Price b $2.41M

Avg. PPSF b $1,113g 21.8% since 2013g 92.9% since 2010

Transactions b 20 Avg. Price b $2.59M

Avg. PPSF b $1,061g 21.2% since 2013g 105.3% since 2010

ONE Sotheby’s International Realty | 33

-0+2010

2011

2012

2013

2014

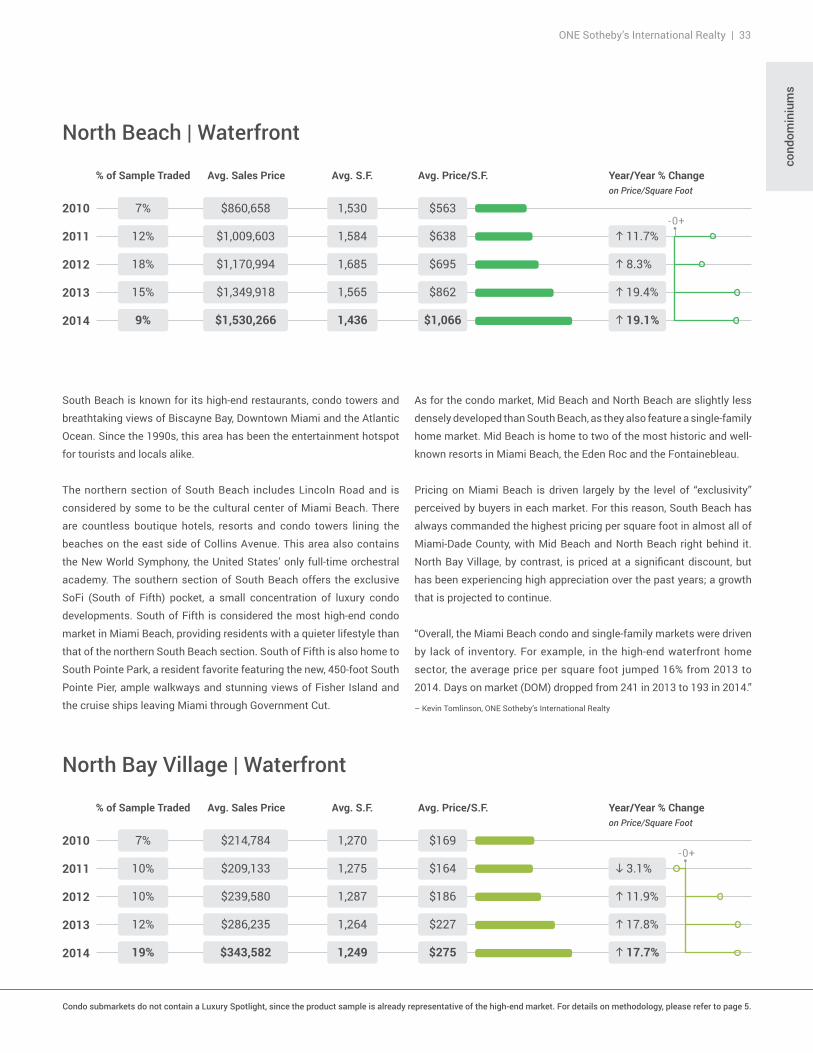

North Beach | Waterfront

% of Sample Traded

7%

12%

18%

15%

9%

Avg. Sales Price Avg. S.F. Avg. Price/S.F. Year/Year % Changeon Price/Square Foot

g 19.4%

g 8.3%

g 11.7%

g 19.1%

$862

$695

$638

$1,066

$563

1,565

1,685

1,584

1,436

1,530$860,658

$1,009,603

$1,170,994

$1,349,918

$1,530,266

-0+2010

2011

2012

2013

2014

North Bay Village | Waterfront

% of Sample Traded

7%

10%

10%

12%

19%

Avg. Sales Price Avg. S.F. Avg. Price/S.F. Year/Year % Changeon Price/Square Foot

g 17.8%

g 11.9%

h 3.1%

g 17.7%

$227

$186

$164

$275

$169

1,264

1,287

1,275

1,249

1,270$214,784

$209,133

$239,580

$286,235

$343,582

As for the condo market, Mid Beach and North Beach are slightly less

densely developed than South Beach, as they also feature a single-family

home market. Mid Beach is home to two of the most historic and well-

known resorts in Miami Beach, the Eden Roc and the Fontainebleau.

Pricing on Miami Beach is driven largely by the level of “exclusivity”

perceived by buyers in each market. For this reason, South Beach has

always commanded the highest pricing per square foot in almost all of

Miami-Dade County, with Mid Beach and North Beach right behind it.

North Bay Village, by contrast, is priced at a significant discount, but

has been experiencing high appreciation over the past years; a growth

that is projected to continue.

“Overall, the Miami Beach condo and single-family markets were driven

by lack of inventory. For example, in the high-end waterfront home

sector, the average price per square foot jumped 16% from 2013 to

2014. Days on market (DOM) dropped from 241 in 2013 to 193 in 2014.”

– Kevin Tomlinson, ONE Sotheby’s International Realty

cond

omin

ium

s

Condo submarkets do not contain a Luxury Spotlight, since the product sample is already representative of the high-end market. For details on methodology, please refer to page 5.

South Beach is known for its high-end restaurants, condo towers and

breathtaking views of Biscayne Bay, Downtown Miami and the Atlantic

Ocean. Since the 1990s, this area has been the entertainment hotspot

for tourists and locals alike.

The northern section of South Beach includes Lincoln Road and is

considered by some to be the cultural center of Miami Beach. There

are countless boutique hotels, resorts and condo towers lining the

beaches on the east side of Collins Avenue. This area also contains

the New World Symphony, the United States’ only full-time orchestral

academy. The southern section of South Beach offers the exclusive

SoFi (South of Fifth) pocket, a small concentration of luxury condo

developments. South of Fifth is considered the most high-end condo

market in Miami Beach, providing residents with a quieter lifestyle than

that of the northern South Beach section. South of Fifth is also home to

South Pointe Park, a resident favorite featuring the new, 450-foot South

Pointe Pier, ample walkways and stunning views of Fisher Island and

the cruise ships leaving Miami through Government Cut.

34 | 2015 TRENDS Market Report

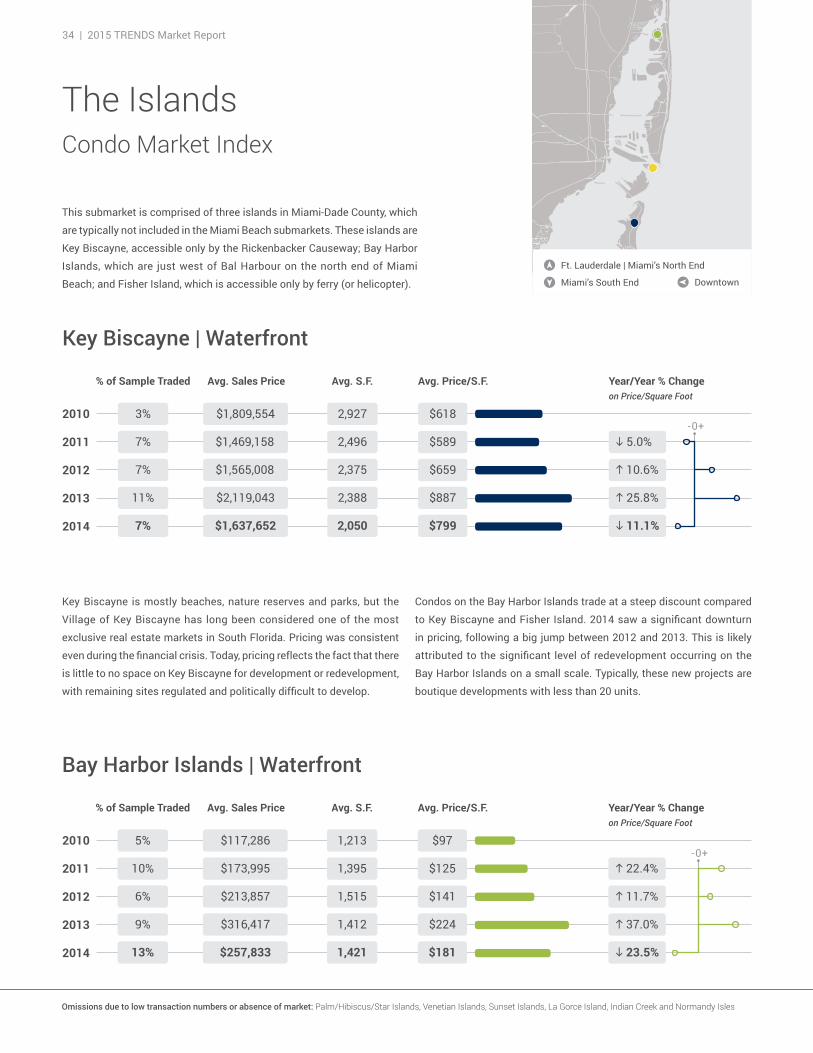

The IslandsCondo Market Index

-0+2010

2011

2012

2013

2014

Key Biscayne | Waterfront

% of Sample Traded

3%

7%

7%

11%

7%

Avg. Sales Price Avg. S.F. Avg. Price/S.F. Year/Year % Changeon Price/Square Foot

g 25.8%

g 10.6%

h 5.0%

h 11.1%

$887

$659

$589

$799

$618

2,388

2,375

2,496

2,050

2,927$1,809,554

$1,469,158

$1,565,008

$2,119,043

$1,637,652

-0+2010

2011

2012

2013

2014

Bay Harbor Islands | Waterfront

% of Sample Traded

5%

10%

6%

9%

13%

Avg. Sales Price Avg. S.F. Avg. Price/S.F. Year/Year % Changeon Price/Square Foot

g 37.0%

g 11.7%

g 22.4%

h 23.5%

$224

$141

$125

$181

$97

1,412

1,515

1,395

1,421

1,213$117,286

$173,995

$213,857

$316,417

$257,833

This submarket is comprised of three islands in Miami-Dade County, which

are typically not included in the Miami Beach submarkets. These islands are

Key Biscayne, accessible only by the Rickenbacker Causeway; Bay Harbor

Islands, which are just west of Bal Harbour on the north end of Miami

Beach; and Fisher Island, which is accessible only by ferry (or helicopter). Miami’s South End

Ft. Lauderdale | Miami’s North End

Downtown

Key Biscayne is mostly beaches, nature reserves and parks, but the

Village of Key Biscayne has long been considered one of the most

exclusive real estate markets in South Florida. Pricing was consistent

even during the financial crisis. Today, pricing reflects the fact that there

is little to no space on Key Biscayne for development or redevelopment,

with remaining sites regulated and politically difficult to develop.

Condos on the Bay Harbor Islands trade at a steep discount compared

to Key Biscayne and Fisher Island. 2014 saw a significant downturn

in pricing, following a big jump between 2012 and 2013. This is likely

attributed to the significant level of redevelopment occurring on the

Bay Harbor Islands on a small scale. Typically, these new projects are

boutique developments with less than 20 units.

Omissions due to low transaction numbers or absence of market: Palm/Hibiscus/Star Islands, Venetian Islands, Sunset Islands, La Gorce Island, Indian Creek and Normandy Isles

ONE Sotheby’s International Realty | 35

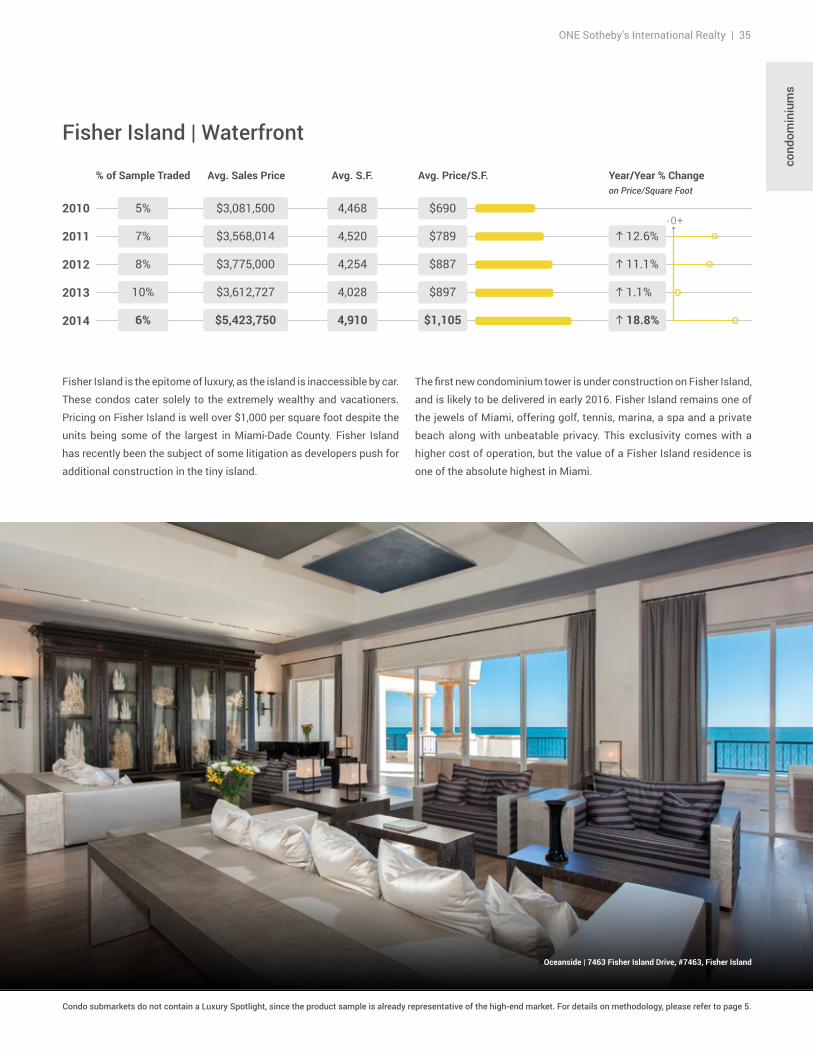

Fisher Island is the epitome of luxury, as the island is inaccessible by car.

These condos cater solely to the extremely wealthy and vacationers.

Pricing on Fisher Island is well over $1,000 per square foot despite the

units being some of the largest in Miami-Dade County. Fisher Island

has recently been the subject of some litigation as developers push for

additional construction in the tiny island.

-0+2010

2011

2012

2013

2014

Fisher Island | Waterfront

% of Sample Traded

5%

7%

8%

10%

6%

Avg. Sales Price Avg. S.F. Avg. Price/S.F. Year/Year % Changeon Price/Square Foot

g 1.1%

g 11.1%

g 12.6%

g 18.8%

$897

$887

$789

$1,105

$690

4,028

4,254

4,520

4,910

4,468$3,081,500

$3,568,014

$3,775,000

$3,612,727

$5,423,750

cond

omin

ium

s

The first new condominium tower is under construction on Fisher Island,

and is likely to be delivered in early 2016. Fisher Island remains one of

the jewels of Miami, offering golf, tennis, marina, a spa and a private

beach along with unbeatable privacy. This exclusivity comes with a

higher cost of operation, but the value of a Fisher Island residence is

one of the absolute highest in Miami.

Condo submarkets do not contain a Luxury Spotlight, since the product sample is already representative of the high-end market. For details on methodology, please refer to page 5.

Oceanside | 7463 Fisher Island Drive, #7463, Fisher Island

36 | 2015 TRENDS Market Report

Miami | North EndCondo Market Index

Downtown | Miami Beach

Broward’s South End | Ft. Lauderdale

-0+2010

2011

2012

2013

2014

Aventura | Waterfront

% of Sample Traded

7%

13%

12%

11%

10%

Avg. Sales Price Avg. S.F. Avg. Price/S.F. Year/Year % Changeon Price/Square Foot

g 20.2%

g 6.1%

g 9.9%

g 2.2%

$397

$316

$297

$405

$267

2,788

2,741

2,513

2,522

2,764$739,169

$746,419

$867,531

$1,105,983

$1,022,262

-0+2010

2011

2012

2013

2014

Bal Harbour | Waterfront

% of Sample Traded

3%

6%

18%

13%

25%

Avg. Sales Price Avg. S.F. Avg. Price/S.F. Year/Year % Changeon Price/Square Foot

g 1.3%

g 31.2%

g 27.4%

g 43.7%

$1,362

$1,344

$925

$2,419

$672

2,433

2,586

2,701

1,402

2,718$1,825,675

$2,499,032

$3,475,337

$3,312,535

$3,391,048

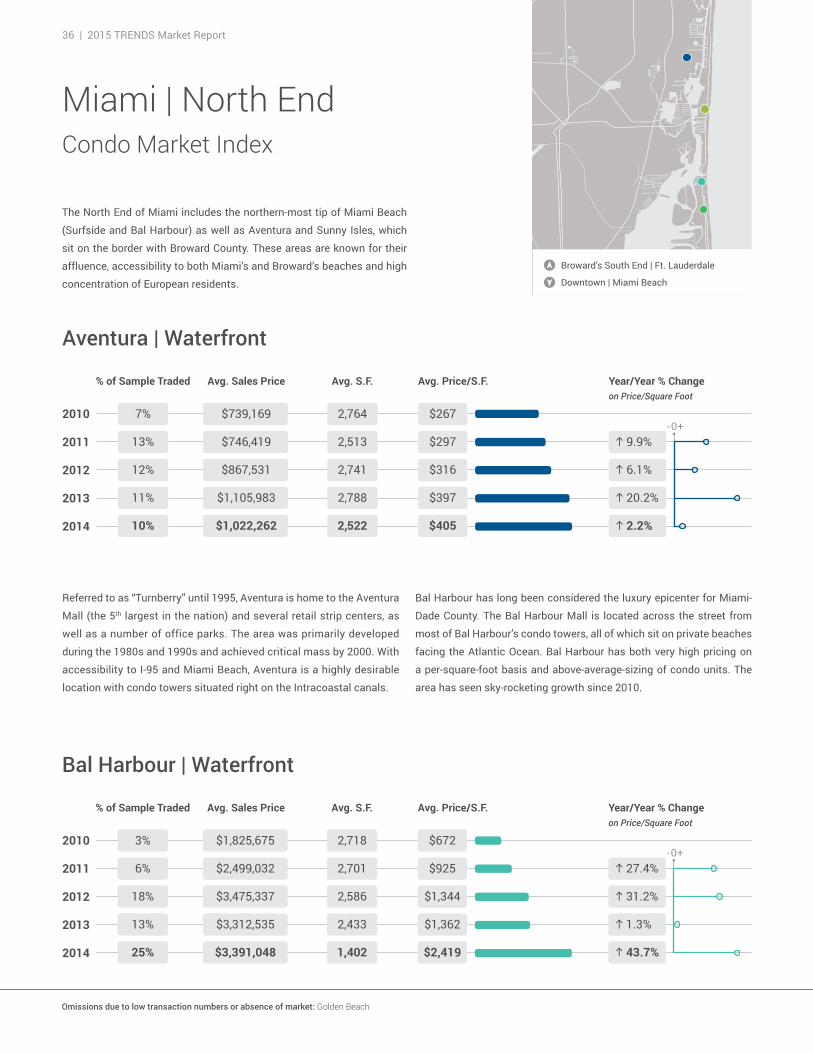

The North End of Miami includes the northern-most tip of Miami Beach

(Surfside and Bal Harbour) as well as Aventura and Sunny Isles, which

sit on the border with Broward County. These areas are known for their

affluence, accessibility to both Miami’s and Broward’s beaches and high

concentration of European residents.

Referred to as “Turnberry” until 1995, Aventura is home to the Aventura

Mall (the 5th largest in the nation) and several retail strip centers, as

well as a number of office parks. The area was primarily developed

during the 1980s and 1990s and achieved critical mass by 2000. With

accessibility to I-95 and Miami Beach, Aventura is a highly desirable

location with condo towers situated right on the Intracoastal canals.

Bal Harbour has long been considered the luxury epicenter for Miami-

Dade County. The Bal Harbour Mall is located across the street from

most of Bal Harbour’s condo towers, all of which sit on private beaches

facing the Atlantic Ocean. Bal Harbour has both very high pricing on

a per-square-foot basis and above-average-sizing of condo units. The

area has seen sky-rocketing growth since 2010.

Omissions due to low transaction numbers or absence of market: Golden Beach

ONE Sotheby’s International Realty | 37

cond

omin

ium

s

-0+2010

2011

2012

2013

2014

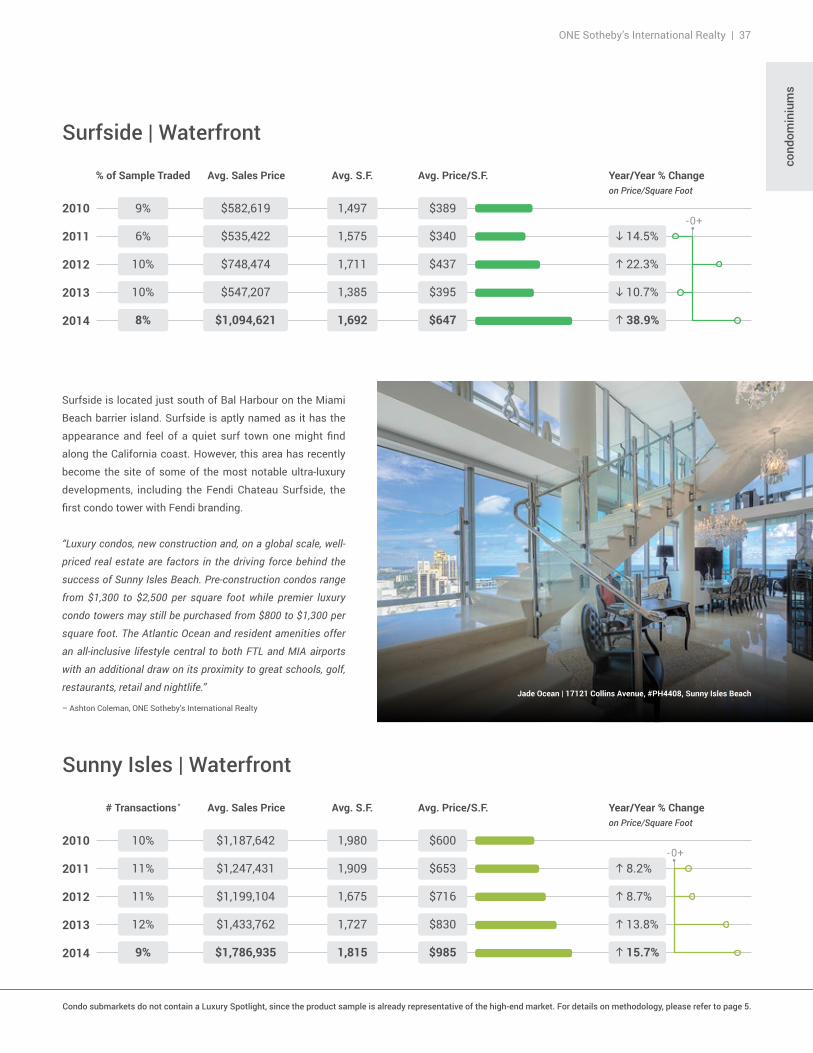

Surfside | Waterfront

% of Sample Traded

9%

6%

10%

10%

8%

Avg. Sales Price Avg. S.F. Avg. Price/S.F. Year/Year % Changeon Price/Square Foot

h 10.7%

g 22.3%

h 14.5%

g 38.9%

$395

$437

$340

$647

$389

1,385

1,711

1,575

1,692

1,497$582,619

$535,422

$748,474

$547,207

$1,094,621

-0+2010

2011

2012

2013

2014

Sunny Isles | Waterfront

# Transactions *

10%

11%

11%

12%

9%

Avg. Sales Price Avg. S.F. Avg. Price/S.F. Year/Year % Changeon Price/Square Foot

g 13.8%

g 8.7%

g 8.2%

g 15.7%

$830

$716

$653

$985

$600

1,727

1,675

1,909

1,815

1,980$1,187,642

$1,247,431

$1,199,104

$1,433,762

$1,786,935

Surfside is located just south of Bal Harbour on the Miami

Beach barrier island. Surfside is aptly named as it has the