trends in the world traditional & renewable heating … in the world traditional & renewable...

TRANSCRIPT

Trends in the World Traditional &

Renewable Heating Markets

Krystyna Dawson

BSRIA WMI

June 2014

2 Excellence in Market Intelligence

• Turnover £3.7 million for 2013

40% multi-client

60% private client including

management consultancy

• Research across 94 countries

• 35 permanent multi-lingual analysts and

• 35 independent consultants

• Offices in China, US, Brazil, UK, France,

Spain, Germany, partners in other countries

• Japan office opening shortly

• Global network of associates eg. JARN

BSRIA Worldwide Market Intelligence

3 Excellence in Market Intelligence

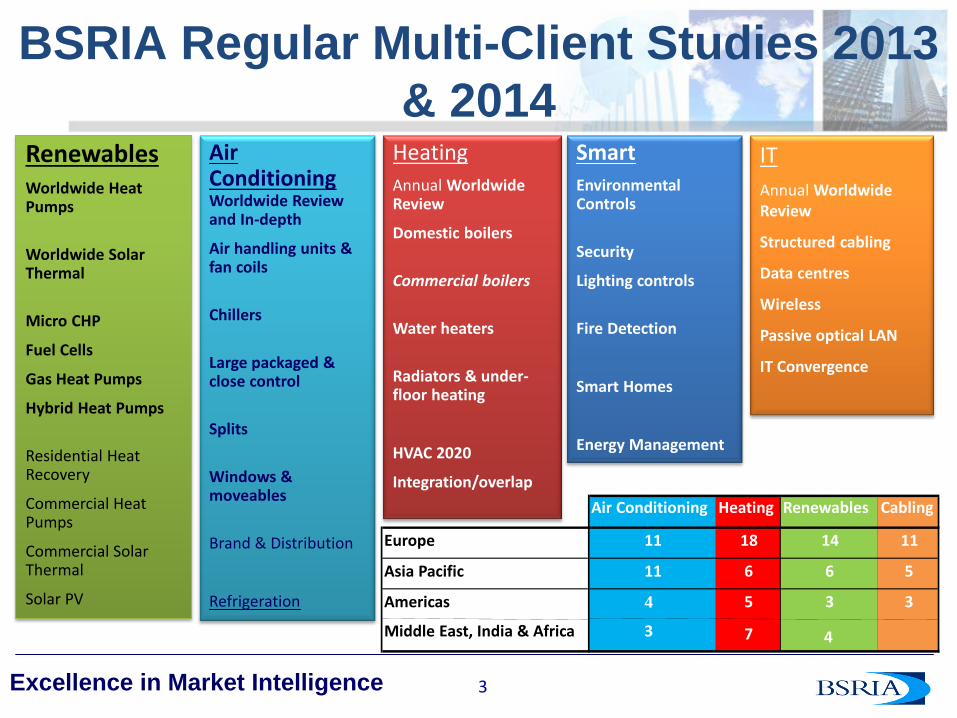

BSRIA Regular Multi-Client Studies 2013

& 2014 Smart

Environmental Controls

Security

Lighting controls

Fire Detection

Smart Homes

Energy Management

Air Conditioning Worldwide Review and In-depth

Air handling units & fan coils

Chillers

Large packaged & close control

Splits

Windows & moveables

Brand & Distribution

Refrigeration

Renewables Worldwide Heat Pumps

Worldwide Solar Thermal

Micro CHP

Fuel Cells

Gas Heat Pumps

Hybrid Heat Pumps

Residential Heat Recovery

Commercial Heat Pumps

Commercial Solar Thermal

Solar PV

Heating

Annual Worldwide Review

Domestic boilers

Commercial boilers

Water heaters

Radiators & under-floor heating

HVAC 2020

Integration/overlap

IT

Annual Worldwide Review

Structured cabling

Data centres

Wireless

Passive optical LAN

IT Convergence

Air Conditioning Heating Renewables Cabling

Europe 11 18 14 11

Asia Pacific 11 6 6 5

Americas 4 5 3 3

Middle East, India & Africa 3 7 4

4 Excellence in Market Intelligence 11/02/2010

Policy long term impact on dwellings –

Europe

Reduction of CO2 emissions

Efficiency of products & systems

Integration of products & systems

Reduction of energy consumption

Source: BSRIA

5 Excellence in Market Intelligence 11/02/2010

France Germany

Policy & incentives impact on HP sales –

Europe

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

0

20,000

40,000

60,000

80,000

100,000

120,000

Growth

211%

Decline

40%

Growth

51%

Growth

99%

Growth

45%

Growth

52%

Decline

22%

2006

• Low interest loans

• Lower electricity tariffs from utilities

• Market driven by new dwellings that was going strong

2008

• HP included in market incentive program

2010

• HP financial support available for existing dwellings

only

Quick rise of electricity prices slows market growth

2006

• Existing tax credit have been raised to 50%

• Quick rise in fossil fuel prices but low electricity price

2010

• Reduction of tax credit to 25% for A/W HP

(15% in 2012)

• Announced increase in electricity price

• High tax credit and FiT for PV

• SHW HP receive 40% tax credit (reduced to 15% in

2014)

Source: BSRIA

Source: BSRIA

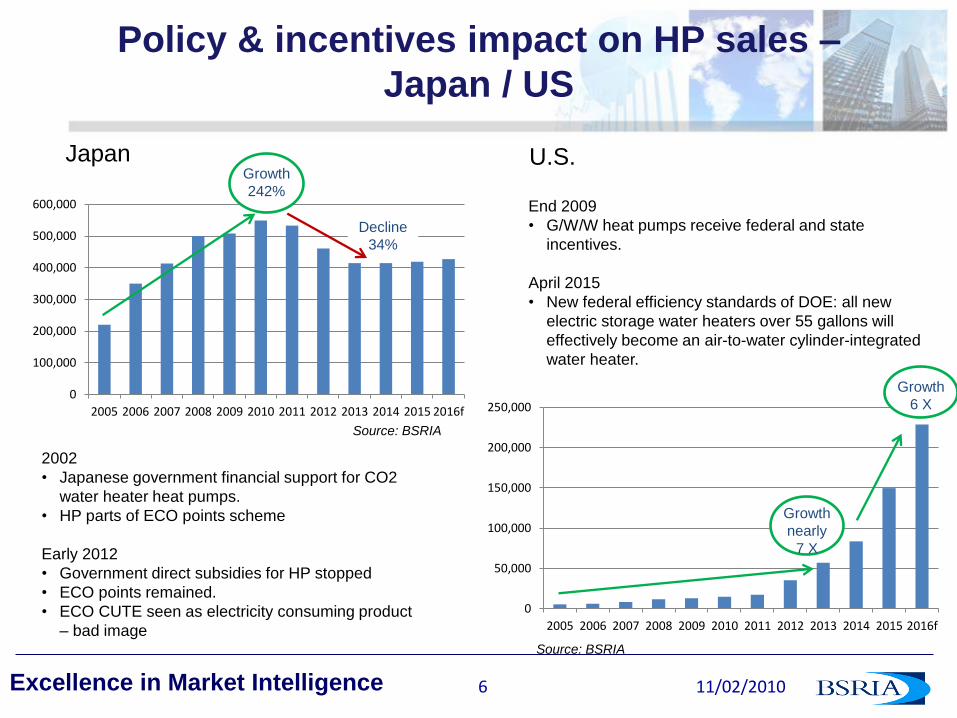

6 Excellence in Market Intelligence 11/02/2010

Japan U.S.

Policy & incentives impact on HP sales –

Japan / US

0

50,000

100,000

150,000

200,000

250,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016f

0

100,000

200,000

300,000

400,000

500,000

600,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016f

2002

• Japanese government financial support for CO2

water heater heat pumps.

• HP parts of ECO points scheme

Early 2012

• Government direct subsidies for HP stopped

• ECO points remained.

• ECO CUTE seen as electricity consuming product

– bad image

End 2009

• G/W/W heat pumps receive federal and state

incentives.

April 2015

• New federal efficiency standards of DOE: all new

electric storage water heaters over 55 gallons will

effectively become an air-to-water cylinder-integrated

water heater.

Growth

242%

Growth

nearly

7 X

Growth

6 X

Decline

34%

Source: BSRIA

Source: BSRIA

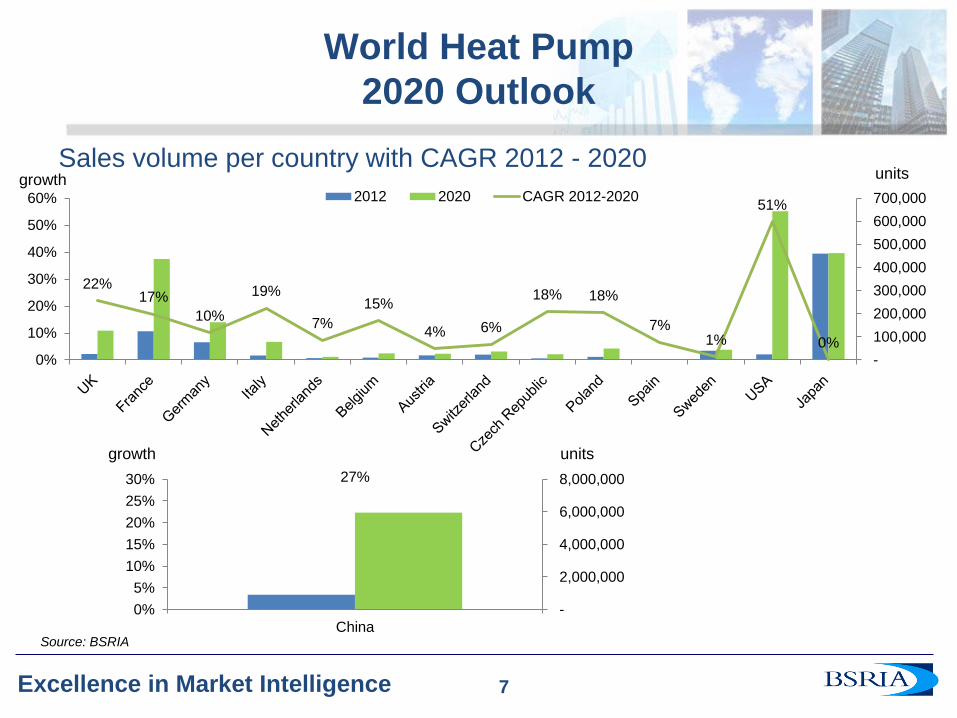

7 Excellence in Market Intelligence

World Heat Pump

2020 Outlook

7

22% 17%

10%

19%

7%

15%

4% 6%

18% 18%

7% 1%

51%

0% 0%

10%

20%

30%

40%

50%

60%

-

100,000

200,000

300,000

400,000

500,000

600,000

700,0002012 2020 CAGR 2012-2020

27%

0%

5%

10%

15%

20%

25%

30%

China

-

2,000,000

4,000,000

6,000,000

8,000,000

Sales volume per country with CAGR 2012 - 2020 growth units

growth units

Source: BSRIA

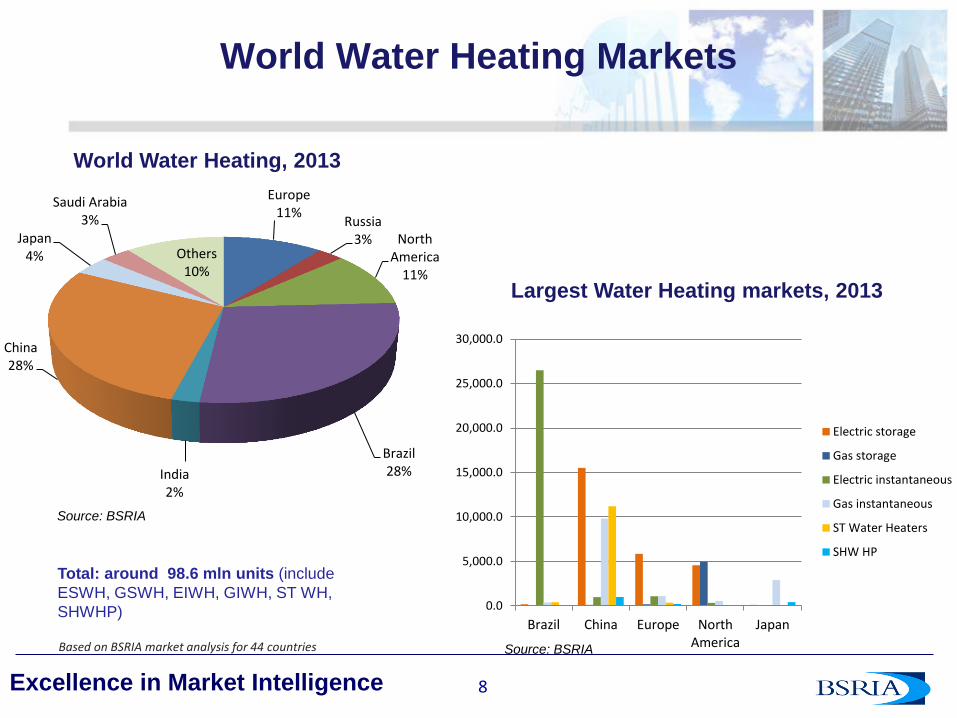

8 Excellence in Market Intelligence

World Water Heating Markets

8

World Water Heating, 2013

Largest Water Heating markets, 2013

Total: around 98.6 mln units (include

ESWH, GSWH, EIWH, GIWH, ST WH,

SHWHP)

Based on BSRIA market analysis for 44 countries

Europe 11%

Russia 3% North

America 11%

Brazil 28% India

2%

China 28%

Japan 4%

Saudi Arabia 3%

Others 10%

0.0

5,000.0

10,000.0

15,000.0

20,000.0

25,000.0

30,000.0

Brazil China Europe NorthAmerica

Japan

Electric storage

Gas storage

Electric instantaneous

Gas instantaneous

ST Water Heaters

SHW HP

Source: BSRIA

Source: BSRIA

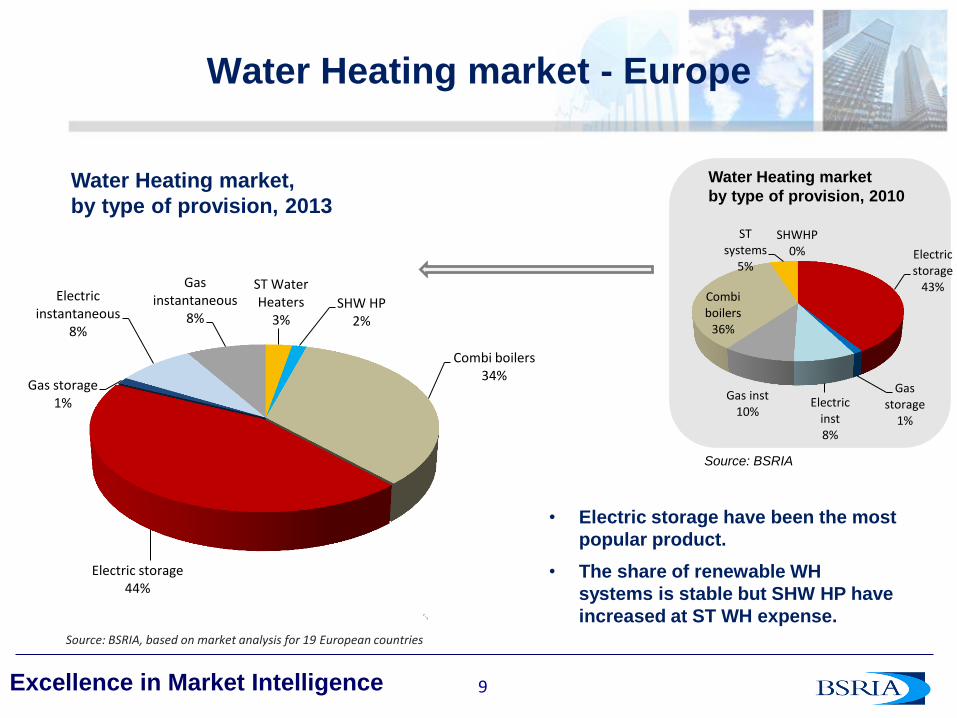

9 Excellence in Market Intelligence

Water Heating market - Europe

9

Water Heating market,

by type of provision, 2013

Water Heating market

by type of provision, 2010

• Electric storage have been the most

popular product.

• The share of renewable WH

systems is stable but SHW HP have

increased at ST WH expense.

Source: BSRIA, based on market analysis for 19 European countries

Electric storage

43%

Gas storage

1%

Electric inst 8%

Gas inst 10%

Combi boilers

36%

ST systems

5%

SHWHP 0%

ST Water Heaters

3% SHW HP

2%

Combi boilers 34%

Electric storage 44%

Gas storage 1%

Electric instantaneous

8%

Gas instantaneous

8%

Source: BSRIA

10 Excellence in Market Intelligence

World Solar Thermal

2020 Outlook

10

0

20

40

60

80

100

120

China

Th

ou

sa

nd

s m

2

CAGR

2012-2020=

7.1%

12.3%

5.4% 6.2%

3.8%

8.2%

15.7%

-2.4%

0.3%

7.1%

13.9%

0.7%

2.0%

10.4%

2.5%

7.1%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0

500

1000

1500

2000

2500

3000

3500

4000

2012 2020 CAGR 2012-2020 growth Thousands m2

Source: BSRIA,

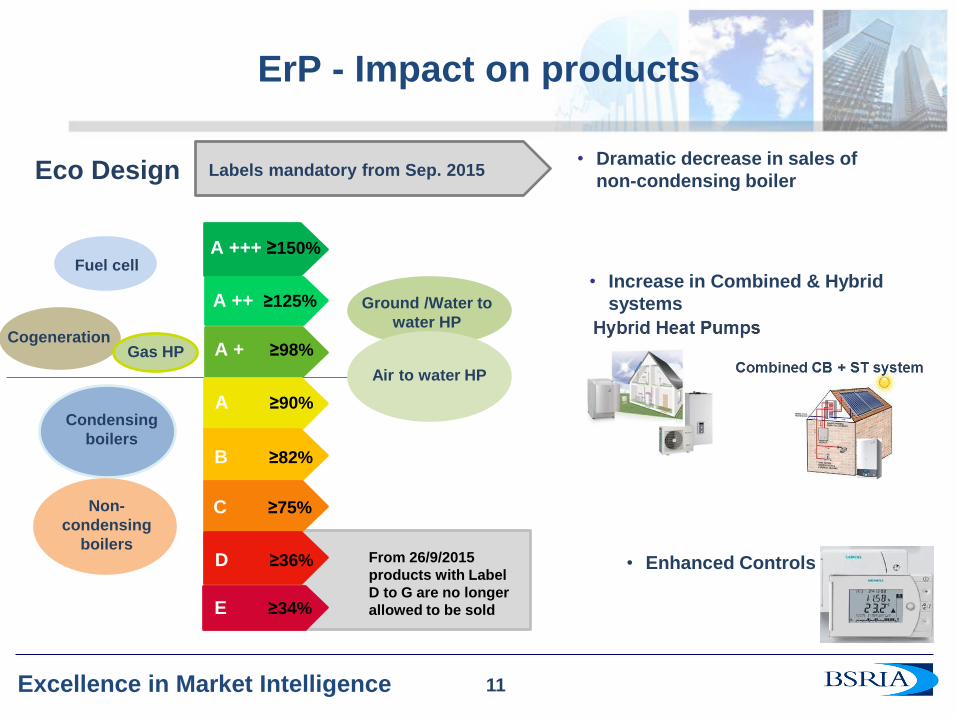

11 Excellence in Market Intelligence

ErP - Impact on products

• Increase in Combined & Hybrid

systems

Eco Design

A +++ ≥150%

A ++ ≥125%

A + ≥98%

A ≥90%

B ≥82%

C ≥75%

D ≥36%

E ≥34%

Cogeneration Gas HP

Condensing

boilers

Non-

condensing

boilers

Ground /Water to

water HP

Air to water HP

From 26/9/2015

products with Label

D to G are no longer

allowed to be sold

• Enhanced Controls

Fuel cell

Labels mandatory from Sep. 2015

11

• Dramatic decrease in sales of

non-condensing boiler

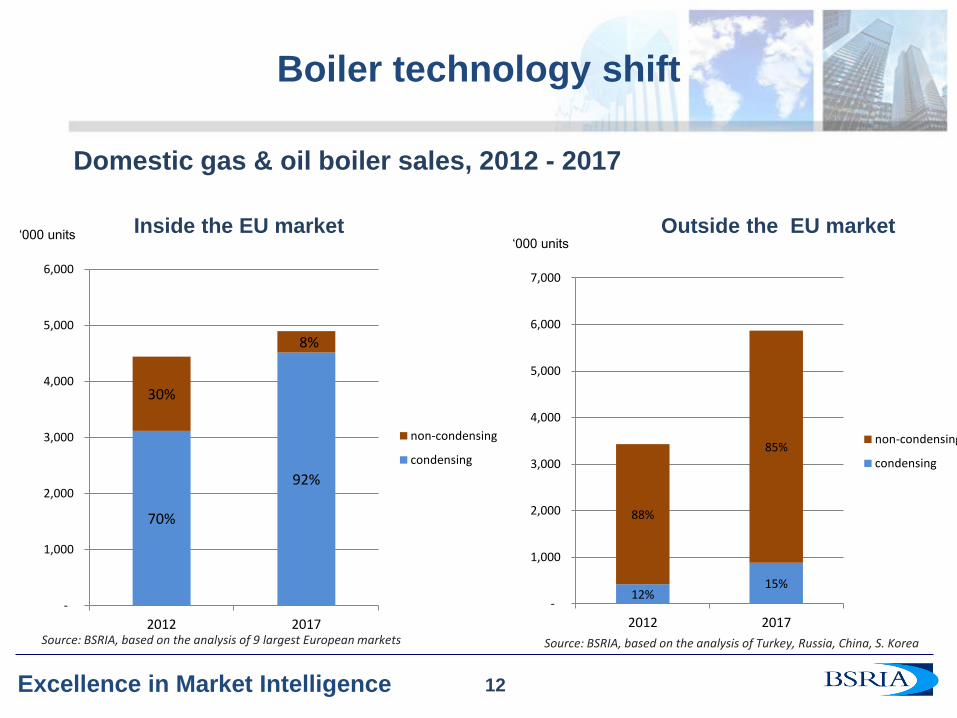

12 Excellence in Market Intelligence

Boiler technology shift

Domestic gas & oil boiler sales, 2012 - 2017

Outside the EU market Inside the EU market ‘000 units

‘000 units

12

70%

92%

30%

8%

-

1,000

2,000

3,000

4,000

5,000

6,000

2012 2017

non-condensing

condensing

Source: BSRIA, based on the analysis of 9 largest European markets Source: BSRIA, based on the analysis of Turkey, Russia, China, S. Korea

12% 15%

88%

85%

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2012 2017

non-condensing

condensing

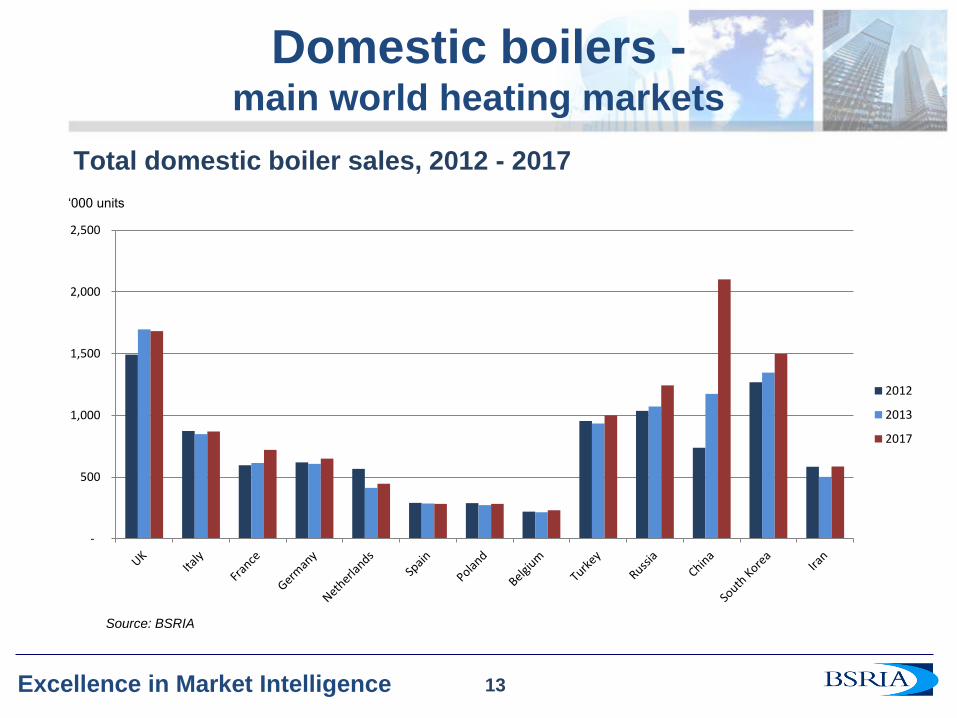

13 Excellence in Market Intelligence

Domestic boilers - main world heating markets

Total domestic boiler sales, 2012 - 2017

‘000 units

13

-

500

1,000

1,500

2,000

2,500

2012

2013

2017

Source: BSRIA

14 Excellence in Market Intelligence

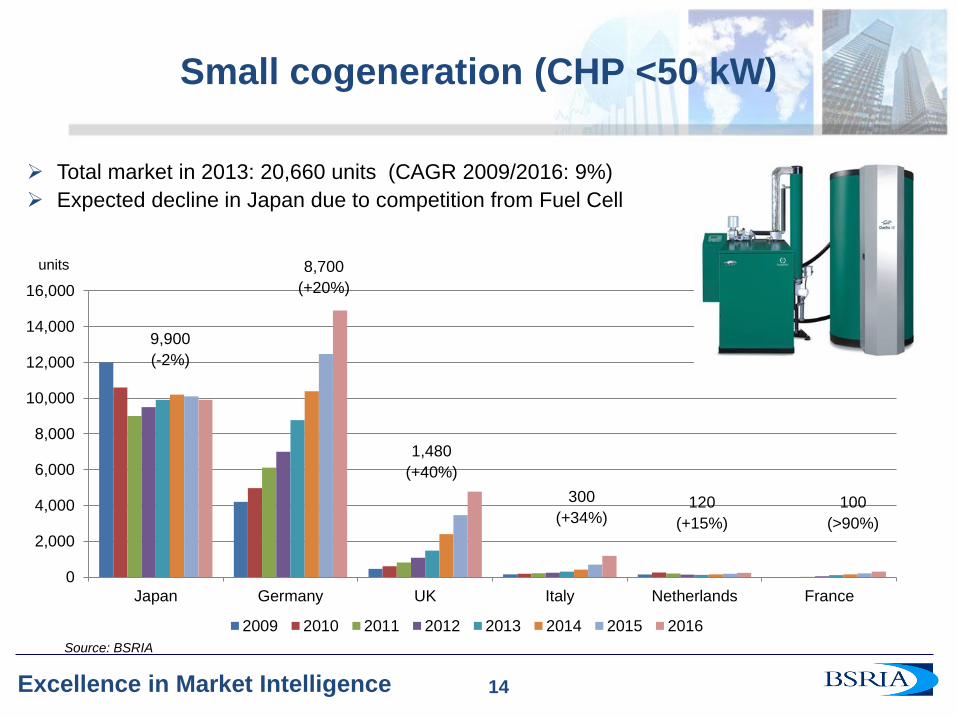

Small cogeneration (CHP <50 kW)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

Japan Germany UK Italy Netherlands France

2009 2010 2011 2012 2013 2014 2015 2016

300

(+34%)

Total market in 2013: 20,660 units (CAGR 2009/2016: 9%)

Expected decline in Japan due to competition from Fuel Cell

9,900

(-2%)

8,700

(+20%)

1,480

(+40%)

120

(+15%)

100

(>90%)

units

14

Source: BSRIA

15 Excellence in Market Intelligence

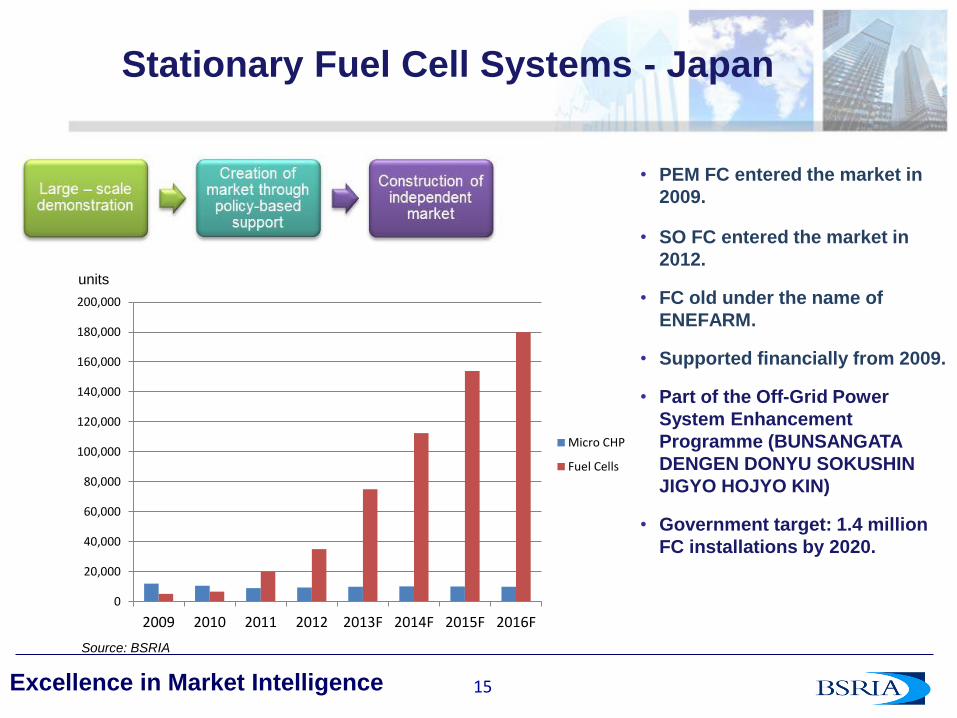

Stationary Fuel Cell Systems - Japan

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

2009 2010 2011 2012 2013F 2014F 2015F 2016F

Micro CHP

Fuel Cells

• PEM FC entered the market in

2009.

• SO FC entered the market in

2012.

• FC old under the name of

ENEFARM.

• Supported financially from 2009.

• Part of the Off-Grid Power

System Enhancement

Programme (BUNSANGATA

DENGEN DONYU SOKUSHIN

JIGYO HOJYO KIN)

• Government target: 1.4 million

FC installations by 2020.

units

Source: BSRIA

16 Excellence in Market Intelligence

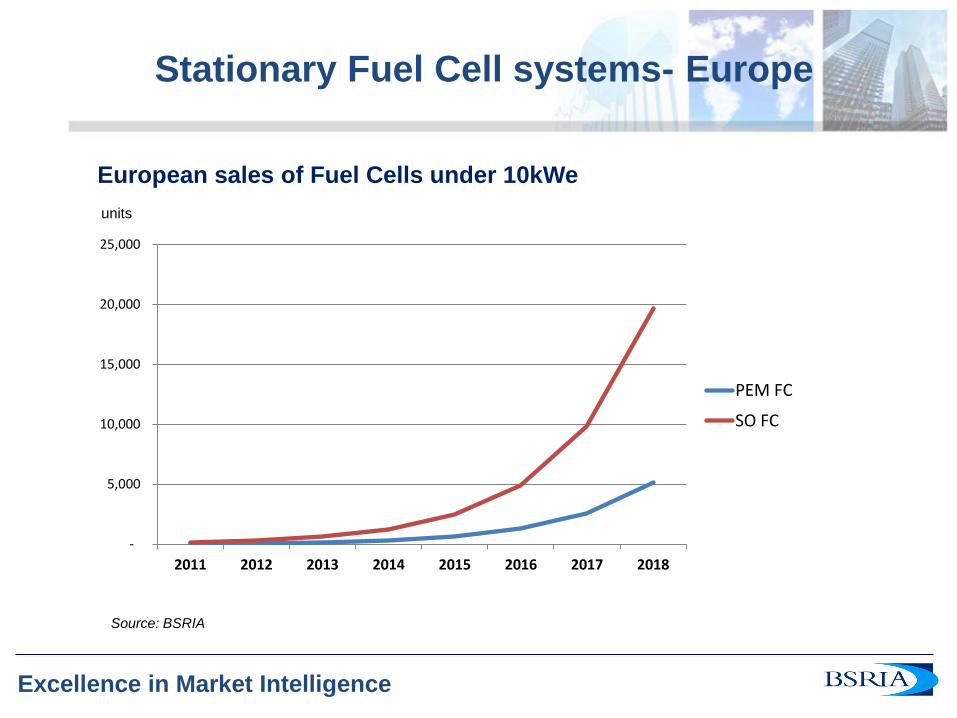

Stationary Fuel Cell systems- Europe

European sales of Fuel Cells under 10kWe

Source: BSRIA

units

-

5,000

10,000

15,000

20,000

25,000

2011 2012 2013 2014 2015 2016 2017 2018

PEM FC

SO FC

17 Excellence in Market Intelligence

Thank you

Contact:

Krystyna Dawson

Senior Manager – Heating & Renewables

BSRIA Worldwide Market Intelligence

Direct: +44 (0)1344 465 638; Mob: +44 (0)7990 595836

Email: [email protected]