ultramax sector analysis - times navigation sector_june... · ultramax vs old panamax relation the...

TRANSCRIPT

ULTRAMAX SECTOR ANALYSISTailor made for Messrs “Times Navigation”

A l l i e d S h i p b r o k i n g I n c .1

TABLE OF CONTENTS

INTRODUCTION 2

CHARACTERISTICS 4

PROFILE 7

MARKET 9

CARGOES 15

This presentation has been conducted by Allied Shipbroking Inc. to summarize the main features ofthe newly introduced Ultramax design.

After a brief reference to its distinctive traits that distinguish it from the old Panamax and theSupramax, the analysis concentrates on the Ultramaxes’ comparative advantages related to both themarket overall and the sector’s seaborne trade.

History

• The decade of 90’s was the period whenmainly Handymaxes of 45,000 dwt were beingbuilt.

• Thereafter during the “Gold” period of 2003-2008, shipyards started building bigger shipsin order to improve cargo capacity of thevessels. That was the time when Supramaxsize of 50,000 – 59,000 dwt started to prevail.

• Ultramax design 60,000 – 65,000 dwt is thebrand new direct development. Such design isan aftereffect of the need for bigger and moreefficient ships.

Handymax Supramax Ultramax

Introduction

A l l i e d S h i p b r o k i n g I n c .2

Ultramax VS Old Panamax relation

The design of Ultramax bulker resembles the one of the olderPanamax (64-69k Dwt), which was being built during 80’s-90’s. However, there are main differences between them,pointed out as follows:

• The Ultramaxes are geared in contrast to the majority ofthe gearless Old Panamaxes.

• The length overall (LOA) of the Ultramaxes is 199 mtrs,shorter than the 225mtrs of the Old Panamaxes.

• The Ultramax design is characterized by low fuel oilconsumption.

Introduction

A l l i e d S h i p b r o k i n g I n c .3

Dimensions• LOA: 199,99 mtrs

• Dwt: 63,500 ts

• Cargo Cap: 77,400 m3

Characteristics

A l l i e d S h i p b r o k i n g I n c .

• Breadth: 32,26 mtrs

• Draft: 13,3 mtrs

• Geared: 4 x 35t Cranes

• Service Speed: 14,3 knts

• Endurance: Abt 20,000 n.m.

• HO/HA: 5

4

Characteristics

A l l i e d S h i p b r o k i n g I n c .

Comparison table of Ultramax designs

Design Dwt Cargo Cap. M/E Speed Consumption Draft

Crown 63 63.500 77.400 MAN B&W 5S60ME-C8 14,25 kts 25,75 t/Day 13,3 mtrs

SDARI 64 64.000 78.000 MAN B&W 5S60ME-C8 14,5 kts 26,6 t/Day 13,3 mtrs

Daesun 62 62.000 75.600 MAN B&W 6S50ME-B9.2 14 kts 26,4 t/Day 13,3 mtrs

HHIC 64 63.700 77.500 MAN B&W 5S60ME-B8.2 14 kts 26,3 t/Day 13,3 mtrs

HMD 63 63.000 76.200 MAN B&W 5S60ME-B8.2 14,5 kts 29,9 t/Day 13,3 mtrsNe

w D

es

ign

sO

ld D

es

ign

s Design Dwt Cargo Cap. M/E Speed Consumption Draft

Crown 58 58.000 71.500 MAN B&W 6S50MC-C 14,3 kts 30,4 t/Day 12,95 mtrs

SDARI 57 57.000 71.500 MAN B&W 6S50MC-C 14,2 kts 30 t/Day 12,8 mtrs

STX 57 57.300 71.850 STX MAN B&W 6S50MC-C7 14,5 kts 35,4 t/Day 13 mtrs

SPP 59 59.000 75.000 MAN B&W 6S50MC-C 14,5 kts 37,2 t/Day 13 mtrs

5

Advantages• High fuel prices along with strict pollution regulations, enforced the building

of fuel efficient vessels, achieving the goal of 25,75t per day 14,25 knts. Newpropeller design, more efficient hull form and the Eco type main engine arethe main factors that contributed to such an achievement.

• Ultramax vessel has been designed ideally for Asian trade, as China and Indiaconstitute the major importers affecting global market, where the gears andgrabs are required at most of the ports. Ultramax’s LOA is 199 mtrs, which is10 mtrs longer than the one of Supramax and 25 mtrs shorter than same ofPanamax. Hence, every port that can host a Panamax can easily host anUltramax. Similarly, an Ultramax vessel can load or discharge almost in everyport where a Supramax does. Same advantages fortify the Ultramax vesselsuitable for African ports as well. Bearing in mind that Africa is a majorimporter of bagged cement and rice, gears and grabs are mandatory for thedischarging operation of such cargoes.

• Moreover, an Ultramax can compete with a Panamax in the lots of 60-70k ±10%, considering that the chartering of an Ultramax saves the costs of afloating crane (region $1,50/mt), which is inevitable for the gearlessPanamaxes.

• The operation of an Ultramax vessel in the Spot market highlights thecomparative advantages over a Supramax, as low fuel consumption alongwith increased cargo capacity results in optimum cost efficiency.

Characteristics

A l l i e d S h i p b r o k i n g I n c .6

Profile

A l l i e d S h i p b r o k i n g I n c .

• Ultramax sector is a new breed in the shippingindustry. The first Ultramax came into waterduring 2010, while over this period 138vessels have been delivered, in contrast toalmost 1910 vessels that constitute theSupramax Fleet.

• Approximately 470 Ultramaxes are expectedto be delivered till 2017. Despite the size ofthe current orderbook, Ultramax fleetcontinues to be much smaller than that ofSupramax which is its direct competitor.

*Supramax design includes vessels with Dwt: 50,000-59,999

*Ultramax design includes vessels with Dwt: 60,000-66,000

7

139

463

1908

115

0

500

1000

1500

2000

2500

Delivered On Order Delivered On Order

Ultramax Supramax

Ultramax & Supramax fleet

Profile

A l l i e d S h i p b r o k i n g I n c .

45

94

Shipyards – Vessels delivered

China

Japan

354

103

6

Shipyards – Vessels on order

China

Japan

Vietnam

• Japanese shipyards had initialized the production of the Ultramax design and that’s the reason whymost vessels of the current fleet have been built in Japan. For the time being there are no availableberths, while priority has been given to major Japanese Owners and Trading Houses. Nevertheless, theanalogy will change in the short-term future, as the current orderbook contains a 77% share of Chineseorders.

• It is worthmentioning that “Sinopacific Group” along with “CSSC-Chengxi Shipyard” were the pioneersin the Chinese Shipbuilding segment, as they were the first Chinese shipyards that started buildingUltramaxes, based on the designs “Crown 63” and “SDARI 64” respectively.

8

0

10

20

30

40

50

60

70

0

5.000

10.000

15.000

20.000

25.000

30.000

35.000

40.000

45.000

50.000

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

USD

(M

ILLI

ON

S)

USD

/ D

AY

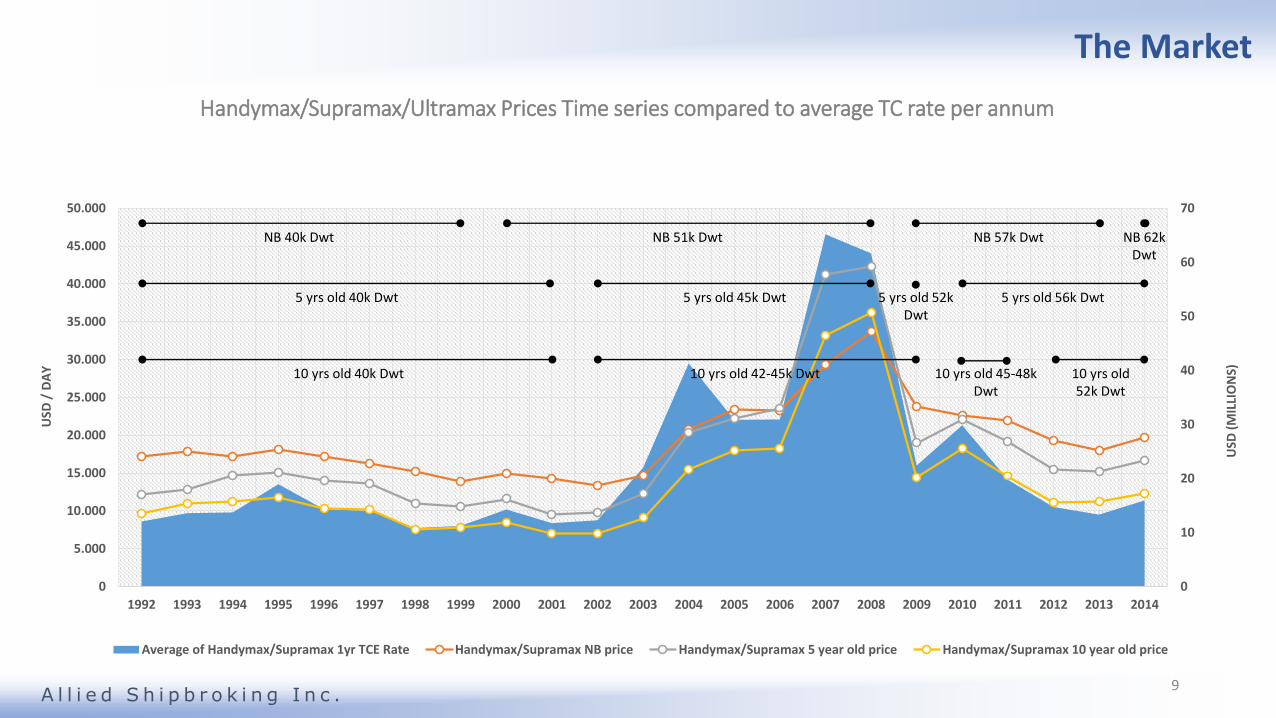

Handymax/Supramax/Ultramax Prices Time series compared to average TC rate per annum

Average of Handymax/Supramax 1yr TCE Rate Handymax/Supramax NB price Handymax/Supramax 5 year old price Handymax/Supramax 10 year old price

NB 62k Dwt

5 yrs old 56k Dwt

10 yrs old 45-48k Dwt

10 yrs old 52k Dwt

Handymax/Supramax/Ultramax sector

A l l i e d S h i p b r o k i n g I n c .

NB 40k Dwt

5 yrs old 40k Dwt

10 yrs old 40k Dwt

NB 51k Dwt

5 yrs old 45k Dwt

10 yrs old 42-45k Dwt

NB 57k Dwt

5 yrs old 52k Dwt

The Market

9

0

5

10

15

20

25

30

35

40

45

0

5.000

10.000

15.000

20.000

25.000

30.000

35.000

40.000

45.000

50.000

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

USD

(M

ILLI

ON

S)

USD

/ D

AY

Deflated Handymax/Supramax/Ultramax Prices Time series compared to average TC rate per annum, based on 1992

Average of Handymax/Supramax 1yr TCE Rate Deflated Hmax/Smax NB prices based on 1992

Deflated Hmax/Smax 5 year old prices based on 1992 Deflated Hmax/Smax 10 year old prices based on 1992

5 yrs old 40k Dwt

10 yrs old 40k Dwt

5 yrs old 45k Dwt 5 yrs old 52k Dwt

5 yrs old 56k Dwt

10 yrs old 42-45k Dwt 10 yrs old 45-48k Dwt

10 yrs old 52k Dwt

Handymax/Supramax/Ultramax sector

A l l i e d S h i p b r o k i n g I n c .

NB 40k Dwt NB 51k Dwt NB 57k Dwt NB 62k Dwt

The FleetMarketThe Market

10

0

10

20

30

40

50

60

70

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

USD

(M

ILLI

ON

S)

BD

I

Handymax/Supramax/Ultramax prices time series compared to average BDI per annum

Average BDI Handymax/Supramax NB price Handymax/Supramax 5 year old price Handymax/Supramax 10 year old price

5 yrs old 56k Dwt

10 yrs old 40k Dwt 10 yrs old 42-45 k Dwt 10 yrs old 42-45k Dwt

10 yrs old 52k Dwt

Handymax/Supramax/Ultramax sector

A l l i e d S h i p b r o k i n g I n c .

NB 40k Dwt NB 51k Dwt NB 57k Dwt NB 62k Dwt

5 yrs old 40k Dwt 5 yrs old 45k Dwt 5 yrs old 52k Dwt

The FleetMarketThe Market

11

0

5

10

15

20

25

30

35

40

45

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

USD

(M

ILLI

ON

S)

BD

I

Deflated Handymax/Supramax/Ultramax prices time series compared to average BDI per annum, based on 1992

Average BDI Deflated Handymax/Supramax NB price based on 1992Deflated Handymax/Supramax 5 year old price based on 1992 Deflated Handymax/Supramax 10 year old price based on 1992

NB 40k Dwt

5 yrs old 40k Dwt

10 yrs old 40k Dwt

NB 51k Dwt NB 57k Dwt

5 yrs old 45k Dwt 5 yrs old 56k Dwt5 yrs old 52k Dwt

10 yrs old 42-45k Dwt 10 yrs old 45-48k Dwt

10 yrs old 52k Dwt

Handymax/Supramax/Ultramax sector

A l l i e d S h i p b r o k i n g I n c .

NB 62k Dwt

The FleetMarketThe Market

12

Handymax/Supramax/Ultramax sectorThe FleetMarketThe Market

Since 1992, as per our point of view, Shipping industry has gone through 2 completed economic cycles,with the last one beginning in the early 00’s. It is clear from deflated graphs, that 2001-2002 was thetrough phase, whenafter the 5-year recovery led to the peak of 2007-2008 and presently back again torecession phase.

The duration of the recession period cannot be predicted neither guaranteed - due to the variability ofmajor factors such as demolition, New Building activity, global economic growth, weather, oil prices, wars -but it seems that we may have passed already the second cruel trough phase.

According to graph “Deflated Handymax/Supramax/Ultramax prices compared to average BDI per annum,based on 1992”, we can ascertain that during 2013 NB Supramax / Ultramax prices were similar to thoseduring 2003, which represents a 10-year-old business cycle basis deflated asset values of ships. Havingsaid that, we understand that most probably we have already reached the bottom-line having “seen” thelowest prices during the last decade.

A l l i e d S h i p b r o k i n g I n c .13

NB orders & prices bottom out

The Market

A l l i e d S h i p b r o k i n g I n c .14

Sup

ply

exceed

s d

eman

d

High Charter market

Vessels’ prices

increase

NB orders & prices

peak

Low Charter market

Vessels’ prices soften

NB orders & prices increaseD

eman

d

exce

ed

s su

pp

lyDemolition

activity decreases

Demolition activity

increases

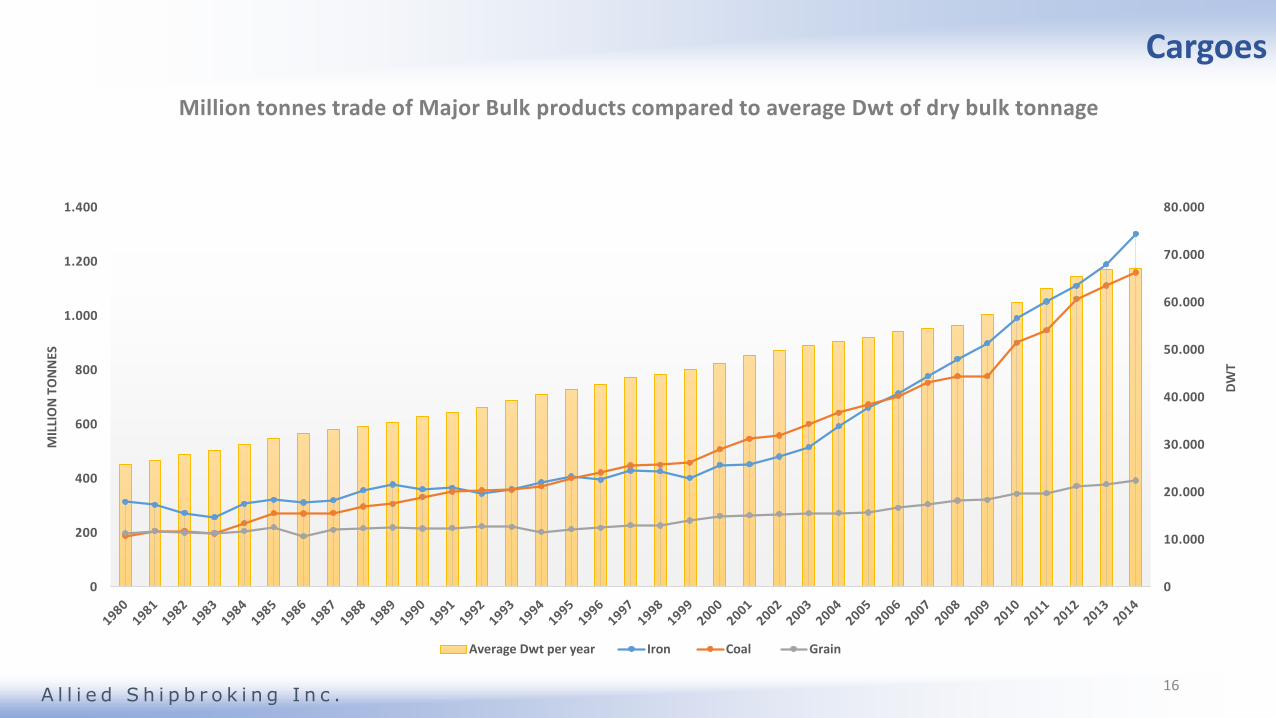

Ultramax CargoesBasic cargoes of Ultramaxes are:

• Coal

• Iron Ore

• Grain

Currently most South East Asian exporters seemto prefer 50 – 55k mt 10% cargo size, followingthe introduction of the Supramaxes, while 45k mt10% cargo size used to be chosen during previousyears due to the existence of the Handymaxesonly.

Same fact seems to take place nowadays, as thefrequency of bigger stems’ appearance isinfluenced by the appearance of the biggerUltramax design.

Cargoes

A l l i e d S h i p b r o k i n g I n c .15

Handymax/Supramax/Ultramax sector

A l l i e d S h i p b r o k i n g I n c .

The FleetMarketCargoes

0

10.000

20.000

30.000

40.000

50.000

60.000

70.000

80.000

0

200

400

600

800

1.000

1.200

1.400

DW

T

MIL

LIO

N T

ON

NES

Million tonnes trade of Major Bulk products compared to average Dwt of dry bulk tonnage

Average Dwt per year Iron Coal Grain

16

Cargoes

Handymax/Supramax/Ultramax sector

A l l i e d S h i p b r o k i n g I n c .

The FleetMarketThe Market

0

10.000

20.000

30.000

40.000

50.000

60.000

70.000

80.000

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

DW

T

BIL

LIO

N T

ON

NE-

MIL

ES

Billion tonne-miles of Major Bulk products compared to average Dwt of dry bulk tonnage

Average Dwt per year Iron Coal Grain

17

Cargoes

Iron ore seaborne trade

The Market

A l l i e d S h i p b r o k i n g I n c .

• Constitutes approximately 40% ofglobal major bulk trade*

• Main exporters: South America, ,India Australia, South Africa

• Main importers: Far East, Continent,North America

*Major bulk trade includes Iron ore,Grains, Coal, Bauxite and Phos. Rock.

18

Cargoes

Main exporters

Coal seaborne trade

The Market

A l l i e d S h i p b r o k i n g I n c .

• Constitutes approximately 40% ofglobal major bulk trade*

• Main exporters: North America,South Africa, Australia, SouthAmerica

• Main importers: Far East, Continent,South America *Major bulk trade includes Iron ore,

Grains, Coal, Bauxite and Phos. Rock.

19

Cargoes

Main exporters

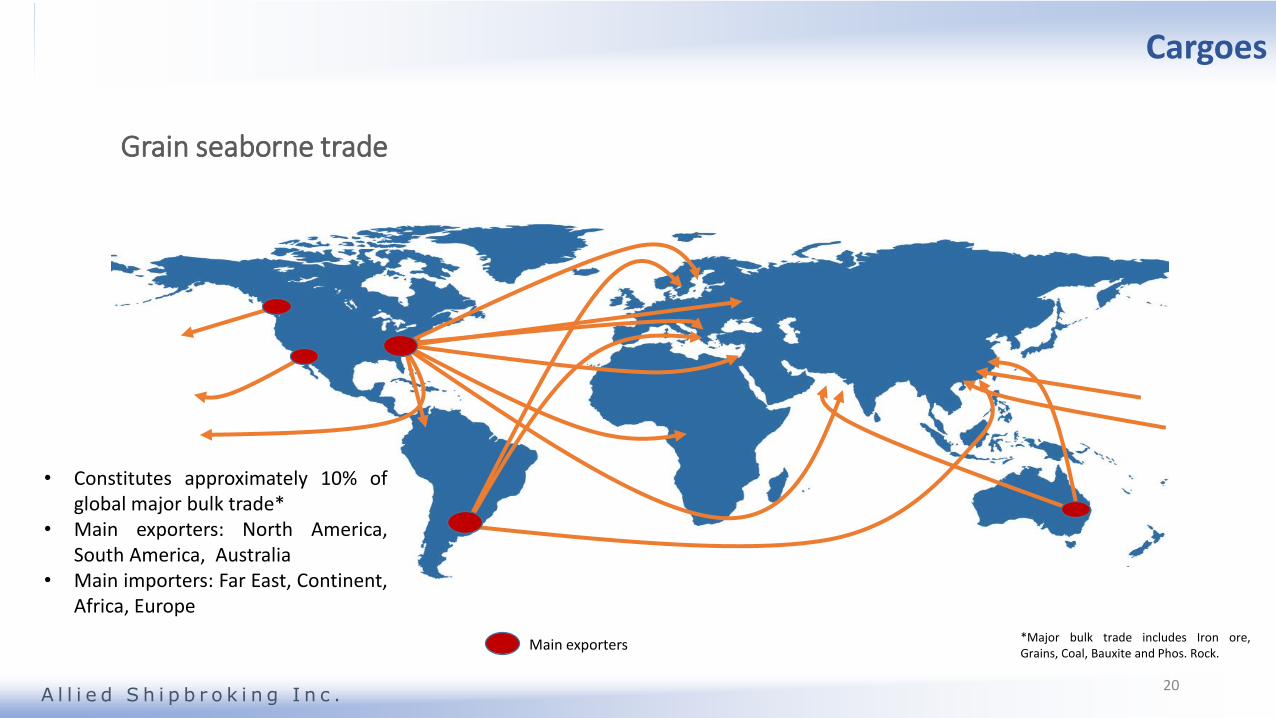

Grain seaborne trade

The Market

A l l i e d S h i p b r o k i n g I n c .

• Constitutes approximately 10% ofglobal major bulk trade*

• Main exporters: North America,South America, Australia

• Main importers: Far East, Continent,Africa, Europe

*Major bulk trade includes Iron ore,Grains, Coal, Bauxite and Phos. Rock.

20

Cargoes

Main exporters

Cargoes

LEGAL DISCLAIMER

-----------------------------------------

This report has been produced on information collected from various sources and whilst every care has been taken in

its preparation, it is presented for the sole and exclusive information of its recipients, in good faith and without any

guarantee from our part. None of the information contained in this report has been independently verified by any

member of “ALLIED SHIPBROKING INC”. Consequently no representation or warranty, express or implied, is

made in respect of the accuracy of the information contained herein. Neither our company nor its directors or

employees shall be in any way liable for any loss nor damage occurred to any party by the use of the information

and/or the comments contained in this report. Furthermore, no responsibility is accepted in respect of any errors or

inaccuracies which may be contained in this report. Whilst every care has been taken in the preparation of this report,

no liability can be accepted for any loss incurred in any way whatsoever by any person relying on the information

contained herein.

Dry bulk fleet profile

A l l i e d S h i p b r o k i n g I n c .