unit root time series econometrics 7777 - wordpress.com...augmented dickey-fuller (adf)unit root...

TRANSCRIPT

11/5/2013

1

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 1

Time Series EconometricsTime Series EconometricsTime Series EconometricsTime Series Econometrics

7777

VijayamohananVijayamohananVijayamohananVijayamohanan PillaiPillaiPillaiPillai NNNN

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 2

Unit Root Unit Root Unit Root Unit Root

TestsTestsTestsTests

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 3

Unit Root Unit Root Unit Root Unit Root

TestsTestsTestsTests

‘Jack and Jill went up the hill, to look at the stars.“Do you see any unit roots there?”

Jack asks Jill who was using a telescope.“The stars all seem to be cointegrated”, replies Jill.’

G.S. Maddala (1998) ‘Recent Developments in Dynamic

Econometric Modelling: A Personal Viewpoint’,

Political Analysis; 7: 59-875 November 2013Vijayamohan: CDS MPhil: Time Series 5 4

Non-stationarity due to

(1)Integrated process: random walk:

Yt = Yt-1 + εt

Difference stationary process

Stochastic trend

(2) Trend: Trend stationary process

Both stochastic and deterministic trend

Non-stationarity

5 November 2013Vijayamohan: CDS MPhil: Time Series 5 5

Consequences of Non-stationarity

(1) With stationary series, possible to model the process via a fixed-coefficients equationestimated from past data.

Not possible if the structural relationship changes over time (if non-stationary).

(2) For non-stationary series, Var and Covs are functions of time:

so the conventional asymptotic theory cannotbe applied to these series.

5 November 2013Vijayamohan: CDS MPhil: Time Series 5 6

Consequences of Non-stationarity

(2) For non-stationary series, Var and Covs are functions of time: so the conventional asymptotic theory cannot be applied to these series.

For example: In a regression of Yt on Xt:

If Xt is non-stationary, Var(Xt) ↑↑↑↑ infinitely, and dominates the Cov(Yt, Xt):

Then the OLS estimator does not have an asymptotic distribution.

====ββββ̂ )(),( ttt XVarXYCov

11/5/2013

2

5 November 2013Vijayamohan: CDS MPhil: Time Series 5 7

Consider two unrelated RW processes:

Yt = Yt–1 + Ut; Ut ∼∼∼∼ IIN(0, σσσσU2)

Xt = Xt–1 + Vt; Vt ∼∼∼∼ IIN(0, σσσσV2);

Cov(Ut ,Vt) = 0.

Consequence of unit root (non-stationarity):

5 November 2013Vijayamohan: CDS MPhil: Time Series 5 8

Consequence of unit root (non-stationarity):

0 50 100 150 200 250 300

-10

-5

0

5

10

15

20y x

0 50 100 150 200 250 300

-10

-5

0

5

10

15

20y x

Yt = Yt–1 + Ut; Ut ∼∼∼∼ IIN(0, σσσσU2)

Xt = Xt–1 + Vt; Vt ∼∼∼∼ IIN(0, σσσσV2);

Cov(Ut ,Vt) = 0.

5 November 2013Vijayamohan: CDS MPhil: Time Series 5 9

Consequence of unit root (non-stationarity):

0 50 100 150 200 250 300

-3

-2

-1

0

1

2

3 eps ep

0 50 100 150 200 250 300

-3

-2

-1

0

1

2

3 eps ep

Ut ∼∼∼∼ IIN(0, σσσσU2)

Vt ∼∼∼∼ IIN(0, σσσσV2)

5 November 2013Vijayamohan: CDS MPhil: Time Series 5 10

Consequence of unit root (non-stationarity):

0 5 10

-0.75

-0.50

-0.25

0.00

0.25

0.50

0.75

1.00CCF-eps x ep CCF-ep x eps

0 5 10

-0.75

-0.50

-0.25

0.00

0.25

0.50

0.75

1.00CCF-eps x ep CCF-ep x eps

Cov(Ut , Vt) = 0.

Cross Correlation function

5 November 2013Vijayamohan: CDS MPhil: Time Series 5 11

Consequence of unit root (non-stationarity):

Now consider the regression:

Yt =ββββ 0 + ββββ 1 Xt + εεεεt.

We expect R2 from this regression would tend

to zero; BUT….

5 November 2013Vijayamohan: CDS MPhil: Time Series 5 12

Consequence of unit root (non-stationarity):

11/5/2013

3

5 November 2013Vijayamohan: CDS MPhil: Time Series 5 13

Consequence of unit root (non-stationarity):

5 November 2013Vijayamohan: CDS MPhil: Time Series 5 14

Granger and Newbold (1974):

High R2 and highly significant t,

but a low DW statistic.

When the regression was run

in first differences……

?

Consequence of unit root (non-stationarity):

5 November 2013Vijayamohan: CDS MPhil: Time Series 5 15

Consequence of unit root (non-stationarity):

5 November 2013Vijayamohan: CDS MPhil: Time Series 5 16

When the regression was run

in first differences,

R2 close to zero; DW close to 2: ⇒⇒⇒⇒

No relationship between Yt and Xt ; and

the high R2 obtained was ‘spurious’.

R2 > DW ⇒⇒⇒⇒ ‘Spurious Regression’.

Consequence of unit root (non-stationarity):

5 November 2013Vijayamohan: CDS MPhil: Time Series 5 17

So, check for stationarity of time series:

Classical: Autocorrelation function (ACF):

Correlogram

Fast-decreasing ACF ⇒⇒⇒⇒ Stationarity

Modern: Unit root tests:

(Augmented) Dickey-Fuller test;

Phillips-Perron non-parametric test; etc.

5 November 2013Vijayamohan: CDS MPhil: Time Series 5 18

If non-stationary series,

run regression in (first) differences as in

Classical (ARIMA) modelling

or check for Cointegration among the series

11/5/2013

4

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 19

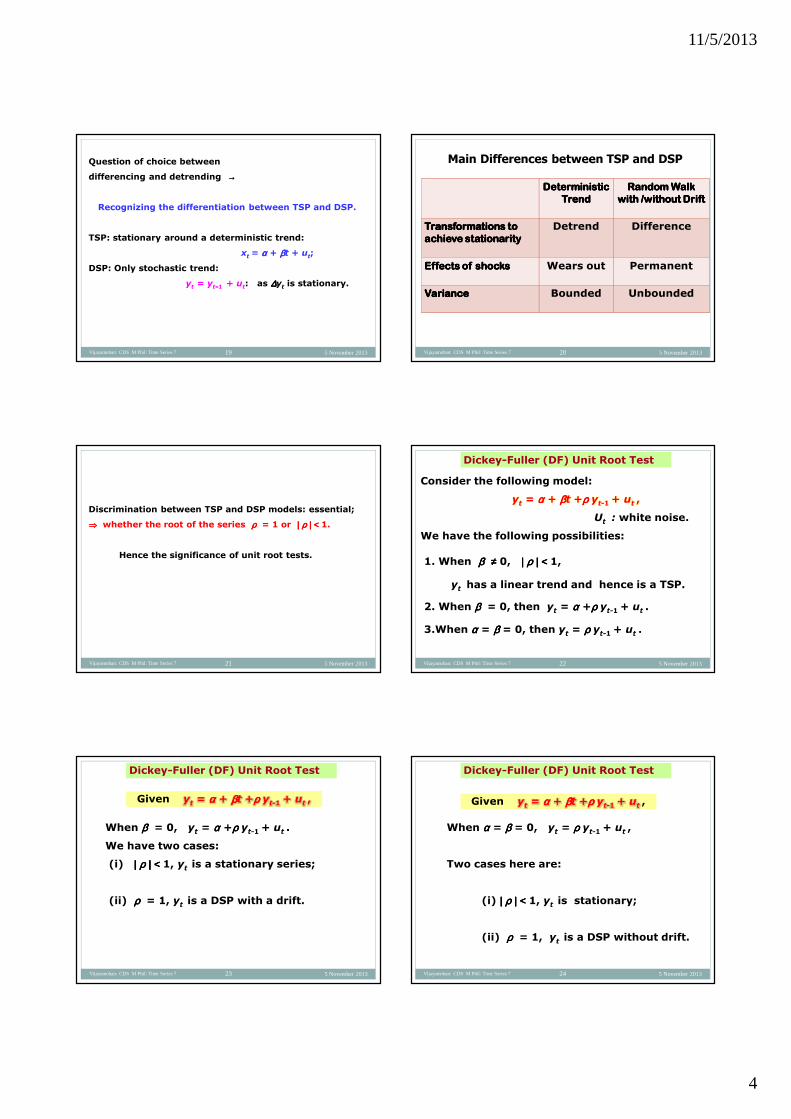

Question of choice between

differencing and detrending →→→→

Recognizing the differentiation between TSP and DSP.

TSP: stationary around a deterministic trend:

xt = αααα + ββββt + ut;

DSP: Only stochastic trend:

yt = yt−−−−1 + ut: as ∆∆∆∆yt is stationary.

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 20

Deterministic Deterministic Deterministic Deterministic

Trend Trend Trend Trend

Random Walk Random Walk Random Walk Random Walk

with /without Driftwith /without Driftwith /without Driftwith /without Drift

Transformations to Transformations to Transformations to Transformations to

achieve achieve achieve achieve stationaritystationaritystationaritystationarity

Detrend Difference

Effects of shocksEffects of shocksEffects of shocksEffects of shocks Wears out Permanent

VarianceVarianceVarianceVariance Bounded Unbounded

Main Differences between TSP and DSP

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 21

Discrimination between TSP and DSP models: essential;

⇒⇒⇒⇒ whether the root of the series ρρρρ = 1 or |||| ρρρρ |||| <<<< 1.

Hence the significance of unit root tests.

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 22

Consider the following model:

yt = αααα + ββββt +ρρρρ yt-1+ ut ,

Ut : white noise.

We have the following possibilities:

1. When ββββ ≠≠≠≠ 0, |||| ρρρρ |||| <<<< 1,

yt has a linear trend and hence is a TSP.

2. When ββββ = 0, then yt = αααα +ρρρρ yt-1+ ut .

3.When αααα = ββββ = 0, then yt = ρρρρ yt-1+ ut .

Dickey-Fuller (DF) Unit Root Test

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 23

When ββββ = 0, yt = αααα +ρρρρ yt-1+ ut .

We have two cases:

(i) |||| ρρρρ |||| <<<< 1, yt is a stationary series;

(ii) ρρρρ = 1, yt is a DSP with a drift.

Given yt = αααα + ββββt +ρρρρ yt-1+ ut ,

Dickey-Fuller (DF) Unit Root Test

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 24

When αααα = ββββ = 0, yt = ρρρρ yt-1+ ut ,

Two cases here are:

(i) |||| ρρρρ |||| <<<< 1, yt is stationary;

(ii) ρρρρ = 1, yt is a DSP without drift.

Given yt = αααα + ββββt +ρρρρ yt-1+ ut ,

Dickey-Fuller (DF) Unit Root Test

11/5/2013

5

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 25

Rewrite (1) yt = αααα + ββββt +ρρρρ yt-1+ ut as

∆∆∆∆ yt = αααα + ββββt +γγγγ yt-1+ ut ,

where γγγγ = (ρρρρ −−−−1).

Now, testing the null hypothesis

Ho: γγγγ = 0,

in the usual way is equivalent to testing

Ho: ρρρρ = 1.

Dickey-Fuller (DF) Unit Root Test

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 26

||ly rewrite (2) yt = αααα +ρρρρ yt-1+ ut

as ∆∆∆∆ yt = αααα +γγγγ yt-1+ ut .

and (3) yt = ρρρρ yt-1+ ut ,

as ∆∆∆∆ yt = γγγγ yt-1+ ut .

Then test for Ho: γγγγ = 0,

vs. the one-sided alternative |||| ρρρρ |||| <<<< 1 .

Dickey-Fuller (DF) Unit Root Test

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 27

Dickey-Fuller (DF) Unit Root Test: 3 DF Type Formulations

Note: In (1), ∆∆∆∆ yt = αααα + ββββt +γγγγ yt-1+ ut ,

where γγγγ = (ρρρρ −−−−1),

the model has both a constant and a trend;

Note: In (2), ∆∆∆∆ yt = αααα +γγγγ yt-1+ ut ,

the model has a constant; and

Note: In (3), ∆∆∆∆ yt = γγγγ yt-1+ ut ,

the model is without constant.

In a DF test all 3 formulations are considered.

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 28

Dickey-Fuller (DF) Unit Root Test

But we cannot use the usual t-test to test

Ho: ρρρρ = 1,

because under the null, yt is I(1),

and hence the t-statistic does not have an asymptotic normal distribution (Dickey and Fuller 1979).

Its asymptotic distribution,

based on Wiener processes, is called

Dickey-Fuller distribution, and the statistic, Dickey-Fuller ττττ (tau) statistic.

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 29

Norbert Wiener Norbert Wiener Norbert Wiener Norbert Wiener (1894 (1894 (1894 (1894 ––––1964,) 1964,) 1964,) 1964,)

American mathematician;American mathematician;American mathematician;American mathematician;

originator of cyberneticsoriginator of cyberneticsoriginator of cyberneticsoriginator of cybernetics: : : :

interdisciplinary study of the structure of interdisciplinary study of the structure of interdisciplinary study of the structure of interdisciplinary study of the structure of

regulatory systemsregulatory systemsregulatory systemsregulatory systems

Wiener process: a continuous-time stochastic processAlso called Brownian Motion

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 30

Robert Brown (1773 – 1858) Scottish botanist

Brownian motion: 1827

11/5/2013

6

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 31

Robert Brown (1773 – 1858) Scottish botanist

Graphs of Graphs of Graphs of Graphs of five five five five sampled sampled sampled sampled

Brownian motionsBrownian motionsBrownian motionsBrownian motions::::

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 32

Critical values tabulated by Dickey and Fuller(1979) and MacKinnon (1990) for a wider range of sample.

Most of the statistic outcomes are negative;

Note: Ho: γγγγ = (ρρρρ −−−−1) = 0.

If the estimated ττττ–value is more negative

(i.e., less) than the critical value

at the chosen significance level, reject Ho.

Dickey-Fuller (DF) Unit Root Test

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 33

Augmented Dickey-Fuller (ADF) Unit Root Test

In deriving the asymptotic distributions,Dickey and Fuller (1979, 1981) assumed:

ut ∼∼∼∼ iid(0,σσσσ2 ).

But, if the errors are non-orthogonal

(i.e., serially correlated),

the limiting distributions cease to beappropriate.

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 34

Dickey and Fuller (1979) and

Said and Dickey (1984)

modified the DF test

by means of AR correction:

Adding lags to ‘whiten’ the residuals

gives ADF test.

Augmented Dickey-Fuller test (ADF)

Augmented Dickey-Fuller (ADF) Unit Root Test

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 35

Augmented Dickey-Fuller test (ADF):

by estimating an autoregression of ∆∆∆∆yt on itsown lags and yt-1 using OLS:

When γγγγ = 0, ρρρρ = 1.

The (t -) test statistic follows the sameDF distribution (ττττ–statistic)

∑∑∑∑====

−−−−−−−− ++++∆∆∆∆++++====∆∆∆∆p

1ititi1tt .uyyy ββββγγγγ

Augmented Dickey-Fuller (ADF) Unit Root Test

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 36

Test for a unit root in Yt ;

If the unit root null is not rejected

(if Yt appears I(1)),

test for a second unit root (see if Yt is I(2)):

Testing: (1):

Estimate the regression of ∆∆∆∆2Yt on a constant,

∆∆∆∆Yt–1, and the lagged values of ∆∆∆∆2Yt, and

compare the ‘t-ratio’ of the coefficient of ∆∆∆∆Yt–1

with the DF critical values.

Double Unit Roots TestingDouble Unit Roots TestingDouble Unit Roots TestingDouble Unit Roots Testing

11/5/2013

7

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 37

Double Unit Roots TestingDouble Unit Roots TestingDouble Unit Roots TestingDouble Unit Roots Testing

Testing: (2):

Estimate the regression of ∆∆∆∆2Yt on Yt–1, ∆∆∆∆Yt–1,

and the lagged values of ∆∆∆∆2Yt, and

compute the usual F-statistic for testing the

joint significance of Yt–1 and ∆∆∆∆Yt–1,

using the critical values given as

ΦΦΦΦ1(2) by Hasza and Fuller (1979).

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 38

Consumption

∆∆∆∆Consumption

Testing for Unit Root:(Augmented) Dickey - Fuller test:

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 39

EQ( 1) Modelling ∆∆∆∆Ct by OLS (using Data.in7)The estimation sample is: 1953 (2) to 1992 (3)

Coefficient Std.Error t-value t-prob Constant 9.09221 11.46 0.793 0.429 Ct-1 -0.0106221 0.01308 -0.812 0.418

sigma 2.21251 RSS 763.648214R^2 0.00420671 F(1,156) = 0.659 [0.418]log-likelihood -348.658 DW 1.6no. of observations 158 no. of parameters 2

∆∆∆∆Ct = 9.092 – 0.0106 Ct – 1t = (0.793) (–0.812)

Critical values used in ADF test: 5%= -2.88, 1%= -3.473

Testing for Unit Root:(Augmented) Dickey - Fuller test:

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 40

EQ( 1) Modelling ∆∆∆∆2Ct by OLS (using Data.in7)The estimation sample is: 1953 (3) to 1992 (3)

Coefficient Std.Error t-value t-prob Constant -0.148864 0.1736 -0.857 0.393

∆∆∆∆Ct -1 -0.813544 0.07824 -10.4 0.000

sigma 2.16501 RSS 726.524426R^2 0.410943 F(1,155) = 108.1 [0.000]**log-likelihood -343.037 DW 2.04no. of observations 157 no. of parameters 2

∆∆∆∆2Ct = –0.149 – 0.814 ∆∆∆∆Ct – 1

t = (–0.857) (–10.399)

Critical values used in ADF test: 5%=-2.88, 1%=-3.473

Testing for Unit Root:(Augmented) Dickey - Fuller test:

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 41

Testing for Unit Root:(Augmented) Dickey - Fuller test:

Variable Ct in level

CONS: ADF tests (T=152, Constant; 5% = -2.88 1% = -3.47)

D-lag t-adf beta Y_1 sigma t-DY_lag t-prob AI C F-prob

5 -1.094 0.98551 2.123 -2.767 0.0064 1.551

4 -1.464 0.98038 2.171 1.253 0.2123 1.589 0.0064

3 -1.298 0.98274 2.176 1.448 0.1496 1.587 0.0110

2 -1.120 0.98516 2.184 1.687 0.0937 1.588 0.0112

1 -0.9317 0.98766 2.197 2.481 0.0142 1.594 0.0075

0 -0.6361 0.99149 2.234 1.621 0.0013

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 42

Testing for Unit Root:(Augmented) Dickey - Fuller test:Variable Ct in First Difference

DCONS: ADF tests (T=152, Constant; 5% = -2.88 1% = -3.47)

D-lag t-adf beta Y_1 sigma t-DY_lag t-prob AIC F-prob

5 -4.870** 0.28208 2.132 0.06925 0.9449 1.559

4 -5.305** 0.28618 2.125 2.948 0.0037 1.546 0.9449

3 -4.448** 0.42488 2.180 -1.053 0.2941 1.591 0.0151

2 -5.313** 0.37033 2.181 -1.293 0.1981 1.585 0.0232

1 -6.801** 0.29538 2.185 -1.570 0.1185 1.583 0.0246

0 -10.08** 0.19164 2.196 1.586 0.0182

11/5/2013

8

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 43

Unit Root Test for TSP vs. DSP:

Nelson and Plosser (1982)

The first ever attempt: Nelson and Plosser(1982), using the (augmented) Dickey-Fuller unit root tests:

H0: a time series belongs to DSP class against Ha: it belongs to TSP class.

Nelson and Plosser found that 13 out of 14 US macroeconomic time series that they analyzed belonged to the DSP class (the exception being the unemployment rate).

5 November 2013 Vijayamohan: CDS M Phil: Time Series 7 44

Results of Nelson and Plosser (1982, Table 5, p. 151): Critical value at 5% level: −−−−3.45

Series Sample size (T)

Lag (k) ττττ-value

Real GDP 62 2 −−−−2.99Nominal GDP 62 2 −−−−2.32Real per capita GNP 62 2 −−−−3.04Industrial production 111 6 −−−−2.53Employment 81 3 −−−−2.66Unemployment rate 81 4 −−−−3.55*GNP deflator 82 2 −−−−2.52Consumer prices 111 4 −−−−1.97Wages 71 3 −−−−2.09Real wages 71 2 −−−−3.04Money stock 82 2 −−−−3.08Velocity 102 1 −−−−1.66Interest rate 71 3 0.686

Common stock prices 100 3 −−−−2.05

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 45

Other Unit Root Tests

Mushrooming of Unit root tests ever since N and P (1982) feat:

1. Sargan and Bhargava (1983): based on DW statistic;

2. Phillips and Perron (1988): non-parametric test;

3. Cochrane (1988): Variance ratio test;

4. Sims (1988): Bayesian approach to unit root testing;

5. Perron (1989): unit root test under structural break;

6. Pantula and Hall (1991): IV test in ARMA models;

7. Schmidt and Phillips (1992): LM test;

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 46

8. Choi (1992): Pseudo-IV estimator test;9. Yap and Reinsel (1995): Likelihood ratio test in

ARMA models;

10. Leybourne (1995): based on forward and reverse DF regressions;

11. Park and Fuller (1995): Weighted symmetric estimator test;

12. Elliott, Rothenberg and Stock (1996): Dickey-Fuller GLS test;

Other Unit Root Tests

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 47

Tests with stationarity as null:

1. Park (1990)’s J-test;

2. Kwiatkowski, Phillips, Schmidt and Shin (1992): (KPSS) test;

3. Bierens and Guo (1993): based on Cauchy distribution;

4. Leybourne and McCabe (1994): Modified KPSS test;

5. Choi (1994): based on testing for a MA unit root;

6. Arellano and Pantula (1995): based on testing for a MA unit root.

Other Unit Root Tests

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 48

Panel data unit root tests:

• Levin and Lin (1993);

• Breitung and Meyer (1994)

• Quah (1994);

• Pesaran and Shin (1996);

Other Unit Root Tests

11/5/2013

9

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 49

Empirical Studies by Model Unit Root

(withpossible

breaks)

Stationary

(withpossible

breaks)

Nelson and Plosser

(1982)

ADF test with no

break

13 1

Perron (1989)** Exogenous with

one break

3 11

Zivot and Andrews

(1992)*

Endogenous with

one break

10 3

Lumsdaine and

Papell (1997)*

Endogenous with

two breaks

8 5

Lee and Strazicich

(2003)**

Endogenous with

two breaks

10 4

* Assume no break(s) under the H0 of unit root.** Assume break(s) under both the null and the HA

Unit Root Tests with the Nelson and

Plosser’sData (1982) Set

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 50

Time series in STATA

Tsset : Declare data to be time-series dataCopy-paste data in data editorGenerate a time variable by typing the command:

For monthly data starting with 1995 July:

. generate time = m(1995m7) + _n -1

. format t %tm

You can now tsset your data set. tsset time

time variable: time, 1995m7 to 2004m6delta: 1 month

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 51

If the first observation is for the first quarter of 1990,

generate time = q(1990q1) + _n-1format time %tqtsset time

For yearly data starting at 1942 type:generate time = y(1942) + _n-1format time %tytsset time

For half yearly data starting at 1921h2 type:generate time = h(1921h2) + _n-1format time %thtsset time

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 52

For weekly data starting at 1994w1 type:

. generate time = w(1994w1) + _n-1

. format time %tw

. tsset time

For daily data starting at 1jan1999 type:

. generate time = d(1jan1999) + _n-1

. format time %td

. tsset time

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 53

. dfuller cons, lags(5)

Augmented Dickey-Fuller test for unit root Number of obs = 153

---------- Interpolated Dickey-Fuller ---------Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value------------------------------------------------------------------------------Z(t) -1.117 -3.492 -2.886 -2.576------------------------------------------------------------------------------MacKinnon approximate p-value for Z(t) = 0.7081

Unit Root Tests in STATA:Statistics →→→→

Time series →→→→Tests

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 54

. dfuller D.cons, lags(5)

Augmented Dickey-Fuller test for unit root Number of obs = 152

---------- Interpolated Dickey-Fuller ---------Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value------------------------------------------------------------------------------Z(t) -4.870 -3.493 -2.887 -2.577------------------------------------------------------------------------------MacKinnon approximate p-value for Z(t) = 0.0000

11/5/2013

10

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 55

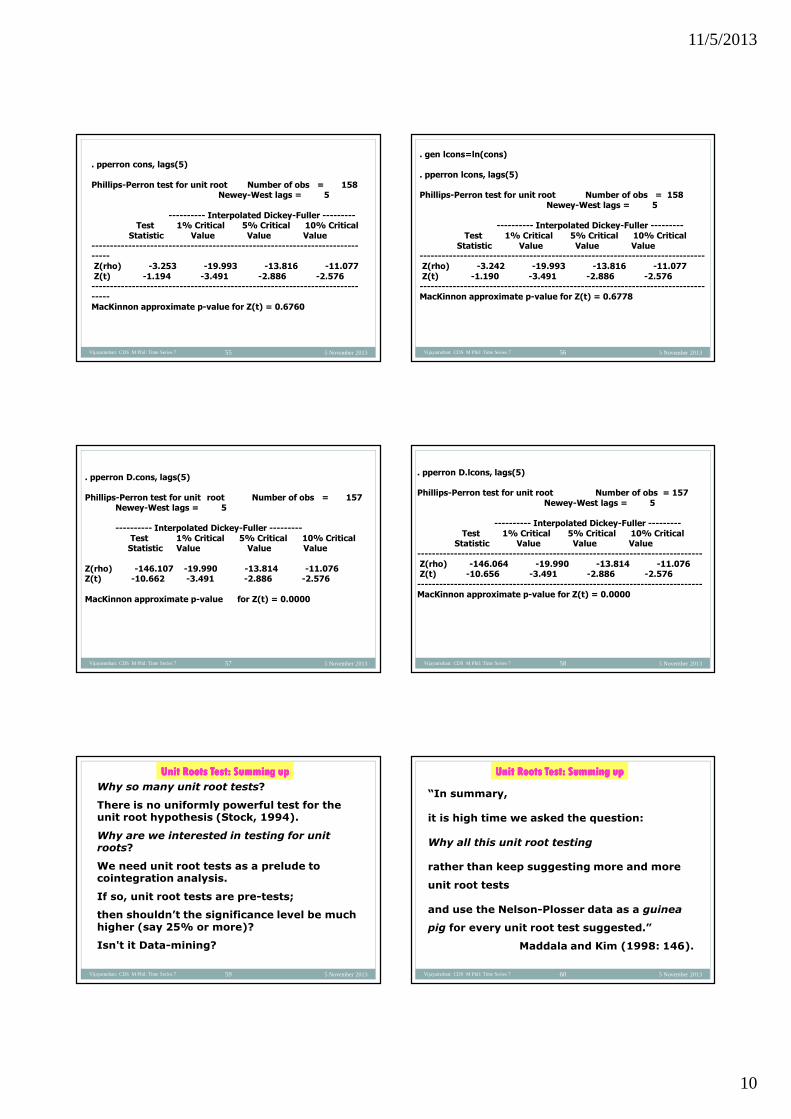

. pperron cons, lags(5)

Phillips-Perron test for unit root Number of obs = 158Newey-West lags = 5

---------- Interpolated Dickey-Fuller ---------Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value------------------------------------------------------------------------------Z(rho) -3.253 -19.993 -13.816 -11.077Z(t) -1.194 -3.491 -2.886 -2.576------------------------------------------------------------------------------MacKinnon approximate p-value for Z(t) = 0.6760

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 56

. gen lcons=ln(cons)

. pperron lcons, lags(5)

Phillips-Perron test for unit root Number of obs = 158Newey-West lags = 5

---------- Interpolated Dickey-Fuller ---------Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value------------------------------------------------------------------------------Z(rho) -3.242 -19.993 -13.816 -11.077Z(t) -1.190 -3.491 -2.886 -2.576------------------------------------------------------------------------------MacKinnon approximate p-value for Z(t) = 0.6778

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 57

. pperron D.cons, lags(5)

Phillips-Perron test for unit root Number of obs = 157Newey-West lags = 5

---------- Interpolated Dickey-Fuller ---------Test 1% Critical 5% Critical 10% CriticalStatistic Value Value Value

Z(rho) -146.107 -19.990 -13.814 -11.076Z(t) -10.662 -3.491 -2.886 -2.576

MacKinnon approximate p-value for Z(t) = 0.0000

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 58

. pperron D.lcons, lags(5)

Phillips-Perron test for unit root Number of obs = 157Newey-West lags = 5

---------- Interpolated Dickey-Fuller ---------Test 1% Critical 5% Critical 10% Critical

Statistic Value Value Value------------------------------------------------------------------------------Z(rho) -146.064 -19.990 -13.814 -11.076Z(t) -10.656 -3.491 -2.886 -2.576------------------------------------------------------------------------------MacKinnon approximate p-value for Z(t) = 0.0000

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 59

Unit Roots Test: Summing upUnit Roots Test: Summing upUnit Roots Test: Summing upUnit Roots Test: Summing up

Why so many unit root tests?

There is no uniformly powerful test for the unit root hypothesis (Stock, 1994).

Why are we interested in testing for unit roots?

We need unit root tests as a prelude to cointegration analysis.

If so, unit root tests are pre-tests;

then shouldn’t the significance level be much higher (say 25% or more)?

Isn't it Data-mining?

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 60

Unit Roots Test: Summing upUnit Roots Test: Summing upUnit Roots Test: Summing upUnit Roots Test: Summing up

“In summary,

it is high time we asked the question:

Why all this unit root testing

rather than keep suggesting more and more

unit root tests

and use the Nelson-Plosser data as a guinea

pig for every unit root test suggested.”

Maddala and Kim (1998: 146).

11/5/2013

11

05 November 2013Vijayamohan: CDS MPhil: Time Series 8 61 05 November 2013Vijayamohan: CDS MPhil: Time Series 8 62

Regression of Integrated Variables

Yt

Deterministic Stochastic

Xt

Deterministic Regression valid

Spurious regression

Stochastic Spurious regression

Spurious regression

unless Xt and Yt are

cointegrated

05 November 2013Vijayamohan: CDS MPhil: Time Series 8 63

Spurious (Nonsense) regression with

integrated variables

→ using differenced variables in regression.

BUT…..

Solving non-stationarity problem via

differencing =

“Throwing the baby out with the bath water”

∵∵∵∵ differencing →→→→

“valuable long-run information being lost’’.

Cointegration

05 November 2013Vijayamohan: CDS MPhil: Time Series 8 64

∵∵∵∵ differencing →→→→ ‘valuable long-run information

being lost’’.

Regression in differences (∆∆∆∆Yt on ∆∆∆∆Xt):

short run only;

In the long run (in equilibrium): ∆∆∆∆Yt = 0 and ∆∆∆∆Xt = 0.

Most economic relationships are stated in

theory as long run relationships between

variables in their levels, not in their

differences.

Cointegration

5 November 2013Vijayamohan CDS Time Series: Introduction 65

Two seemingly irreconcilable objectives :

1. Avoid spurious regression of I(d) variables

and

2. Conserve the long-term relationship.

Hence Cointegration

(Granger 1981; Engle and Granger 1987).

05 November 2013Vijayamohan: CDS MPhil: Time Series 8 66

If two series yt and xt are both I(1),

then in general, any linear combination

of them will also be I(1);

e.g. Yt – Ct = St: All show upward trend.

Cointegration

Income

Consumption

Saving

11/5/2013

12

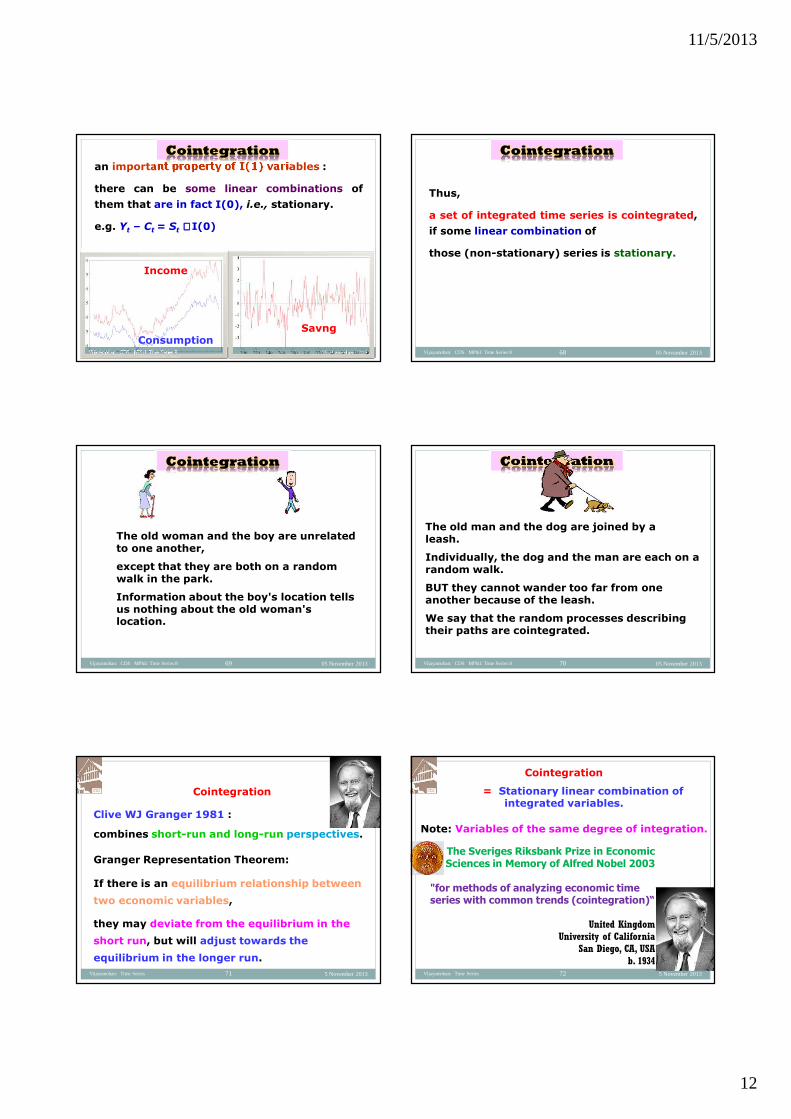

05 November 2013Vijayamohan: CDS MPhil: Time Series 8 67

an important property of I(1) variables :

there can be some linear combinations of

them that are in fact I(0), i.e., stationary.

e.g. Yt – Ct = St ∼∼∼∼ I(0)

Cointegration

Consumption

Income

Savng

05 November 2013Vijayamohan: CDS MPhil: Time Series 8 68

Thus,

a set of integrated time series is cointegrated,

if some linear combination of

those (non-stationary) series is stationary.

Cointegration

05 November 2013Vijayamohan: CDS MPhil: Time Series 8 69

The old woman and the boy are unrelated to one another,

except that they are both on a random walk in the park.

Information about the boy's location tells us nothing about the old woman's location.

Cointegration

05 November 2013Vijayamohan: CDS MPhil: Time Series 8 70

The old man and the dog are joined by a leash.

Individually, the dog and the man are each on a random walk.

BUT they cannot wander too far from one another because of the leash.

We say that the random processes describing their paths are cointegrated.

Cointegration

5 November 2013Vijayamohan: Time Series 71

Cointegration

Clive WJ Granger 1981 :

combines short-run and long-run perspectives.

Granger Representation Theorem:

If there is an equilibrium relationship between

two economic variables,

they may deviate from the equilibrium in the

short run, but will adjust towards the

equilibrium in the longer run.

5 November 2013Vijayamohan: Time Series 72

Cointegration

= Stationary linear combination of integrated variables.

Note: Variables of the same degree of integration.

The Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel 2003

"for methods of analyzing economic time series with common trends (cointegration)“

United KingdomUniversity of California San Diego, CA, USA

b. 1934

11/5/2013

13

05 November 2013Vijayamohan: CDS MPhil: Time Series 8 73

If there exists a relationship between two non

stationary I(1) series, Yt and Xt , such that the

residuals of the regression:

Yt = βXt + ut , that is, ut = Yt – βXt

are stationary, i.e., I(0), then the variables,

Yt and Xt , are said to be cointegrated.

The system is in long-run equilibrium when

E(Yt – βXt) = 0.

∴∴∴∴ ut = equilibrium error (deviation from long-

run equilibrium).

Cointegration

05 November 2013Vijayamohan: CDS MPhil: Time Series 8 74

The system is in long-run equilibrium when

E(Yt – βXt) = 0.

∴∴∴∴ ut = equilibrium error (deviation from long-

run equilibrium).

For the equilibrium to be meaningful,

equilibrium error process must be stationary.

β is called the constant of cointegration, and

the equation is called cointegrating regression

or Cointegrating vector (CV).

Cointegration

05 November 2013Vijayamohan: CDS MPhil: Time Series 8 75

Equilibrium Errors: (i.e. ut = Yt - βXt)

ut

0 timeError rarely drifts from zero

No tendency to return to zero

05 November 2013Vijayamohan: CDS MPhil: Time Series 8 76

Two series Yt and Xt are said to be cointegrated if:

1. Both are I(d), d ≠≠≠≠ 0 and the same for both series (having the same ‘wave length’); and

2. There is a linear combination of them that is I(0),

i.e., there exists ut = Yt – βXt that is I(0).

In this light, the regression of these two

variables, yt = ββββ xt + ut makes sense

(is not spurious).

Cointegration

05 November 2013Vijayamohan: CDS MPhil: Time Series 8 77

How can we distinguish between a genuine long-run relationship and a spurious regression? We need a test.

Two categories:

1. Single equation method: Residual-based test:

using (A)DF -statistic:Engle and Granger (1987): (A)EG test;

1. System (Multiple equation) method: Johansen and Juselius (1990): JJ test.

Cointegration

05 November 2013Vijayamohan: CDS MPhil: Time Series 8 78

Testing for Cointegration: Residual based tests

(1) After estimating the model, save residuals fro m static regression. Consider whether residuals are stationary.

0 90

10 20 30 40 50 60 70 80 100

-0.5

0.0

0.5

1.0

0 1 2 3 4 5 6 7 8 9 10 11 12

-0.5

0.0

0.5

1.0

residuals

ACF

11/5/2013

14

05 November 2013Vijayamohan: CDS MPhil: Time Series 8 79

We proceed in three steps :Step 1: Test that both variables have the same order

of integration , say, that they are both I(1). This can be

performed with the unit-root tests described before .

Step 2: Estimate a `long-run relationship by OLS:

yt =αααα + ββββ xt + ut

Step 3: Extract the residuals of this regression (ut )

and test for a unit-root in this series, using (A)DF test

statistic: ut has a unit root ⇒⇒⇒⇒ NO cointegration .

Testing for Cointegration: Residual based tests

(2): Cointegrating Regression (A)DF test: (Augmented) Engle-Granger test

05 November 2013Vijayamohan: CDS MPhil: Time Series 8 80

(A)EG test is a test of no-cointegration :

H0: No Cointegration (= unit root in ut)

Acceptance of a unit root in the residuals suggests that the residual term is non-stationary , which implies NO cointegration:

= Not rejecting H 0. That is,

If the estimated (A)DF ττττ–value is more negative(i.e., less) than the critical value at the chosen

significance level, reject Ho

= There IS cointegration.

Testing for Cointegration: Residual based tests:(Augmented) Engle-Granger test

05 November 2013Vijayamohan: CDS MPhil: Time Series 8 81

Testing for Cointegration: Residual based tests:(Augmented) Engle-Granger test

Step 1: Test for the order of integration of Xt and Yt:

Unit-root tests (using Data1)The sample is 4 - 300

X: ADF tests (T=297, Constant; 5% = -2.87; 1% = -3.45)D-lag t-adf beta Y_1 sigma t-DY_lag t-prob AIC F-prob2 1.941 1.0006 0.9939 -0.1358 0.8920 0.0010961 1.942 1.0006 0.9922 0.5127 0.6085 -0.005575 0.89200 2.028 1.0007 0.9910 -0.01142 0.8692

Y: ADF tests (T=297, Constant; 5%=-2.87 1%=-3.45)D-lag t-adf beta Y_1 sigma t-DY_lag t-prob AIC F-prob2 -0.9251 0.99935 0.9635 1.163 0.2459 -0.060911 -0.9554 0.99932 0.9641 -0.9526 0.3416 -0.06304 0.24590 -0.9305 0.99934 0.9640 -0.06669 0.3244

05 November 2013Vijayamohan: CDS MPhil: Time Series 8 82

Step 1: Test for the order of integration of Xt and Yt:

Testing for Cointegration: Residual based tests:(Augmented) Engle-Granger test

Unit-root tests (using Data1)The sample is 5 - 300

DX: ADF tests (T=296, Constant; 5% = -2.87; 1% = -3.45)D-lag t-adf beta Y_1 sigma t-DY_lag t-prob AIC F-prob2 -9.604** 0.057433 1.002 -0.1413 0.8878 0.017131 -11.77** 0.049579 1.000 -0.08180 0.9349 0.01045 0.88780 -16.39** 0.045016 0.9985 0.003713 0.9868

DY: ADF tests (T=296, Constant; 5% = -2.87; 1% = -3.45)D-lag t-adf beta Y_1 sigma t-DY_lag t-prob AIC F-prob2 -8.860** 0.099869 0.9527 -1.232 0.2191 -0.083491 -11.60** 0.028890 0.9535 -1.094 0.2749 -0.08507 0.21910 -18.02** -0.037637 0.9539 -0.08775 0.2589

05 November 2013Vijayamohan: CDS MPhil: Time Series 8 83

EQ( 1) Modelling Y by OLS (using Data1)The estimation sample is: 1 to 300

Coefficient Std.Error t-value t-prob Part.R^2Constant 4.85755 0.1375 35.3 0.000 0.9279X 1.00792 0.005081 198. 0.000 0.9975

sigma 0.564679 RSS 30.9296673R^2 0.997541 F(1,97) = 3.935e+004 [0.000]**log-likelihood -82.8864 DW 2.28no. of observations 99 no. of parameters 2

And save residuals.

Testing for Cointegration: Residual based tests:(Augmented) Engle-Granger test

Step 2: Estimate cointegrating regression

Yt = β0 + β1Xt + ut

05 November 2013Vijayamohan: CDS MPhil: Time Series 8 84

EQ( 6) Modelling Dresiduals by OLS (using Data1.in7)

The estimation sample is: 4 to 300

Coefficient Std.Error t-value t-prob Part.R^2residuals_1 -1.16140 0.1024 -11.3 0.000 0.5805

sigma 0.545133 RSS 27.6367834log-likelihood -75.8453 DW 1.95

Which means ∆ut = -1.161 ut-1 + et(-11.3)

CRDF test statistic = -11.3 << -3.39 = 1% Critical Value from MacKinnon.

Hence we reject null of no cointegration between X and Y.

Testing for Cointegration: Residual based tests:(Augmented) Engle-Granger test

Step 3: Check for unit root in the residuals:

11/5/2013

15

05 November 2013Vijayamohan: CDS MPhil: Time Series 8 85

Unit-root tests (using Data1)

The sample is 4 - 300

Residuals: ADF tests (T=297, Constant; 5% = -2.87; 1% = -3.39)

D-lag t-adf beta Y_1 sigma t-DY_lag t-prob AIC F-prob

2 -9.867** 0.016854 0.9869 0.4090 0.6828 -0.01308

1 -10.72** 0.040004 0.9855 -0.2931 0.7696 -0.01924 0.6828

0 -11.33** 1.16140 0.5451 -0.02568 0.8812

Testing for Cointegration: Residual based tests:(Augmented) Engle-Granger test

Step 3: Check for unit root in the residuals:

05 November 2013Vijayamohan: CDS MPhil: Time Series 8 86

Testing for Cointegration: Residual based tests:(Augmented) Engle-Granger test

Step 3: Check for stationarity (unit root) of the residuals:

0 50 100 150 200 250 300

-2.5

0.0

2.5

0 5 10

0

1

0 5 10

0

1

Residuals

ACF

PACF

05 November 2013Vijayamohan: CDS MPhil: Time Series 8 87

Testing for Cointegration: System method:Johansen – Juselius test

Most popular system method: JJ -test (Johansen1988; Johansen and Juselius 1990),

Provides two likelihood ratio (LR) tests.

(1)The trace test: tests the hypothesis that thereare at most r cointegrating vectors, and

(2) The maximum eigenvalue test: tests the nullhypothesis that there are r cointegratingvectors against the hypothesis that there arer+1 cointegrating vectors.

Johansen and Juselius (1990) recommend thesecond test as better.

05 November 2013Vijayamohan: CDS MPhil: Time Series 8 88

Testing for Cointegration: System method:Johansen – Juselius test

JJ-test is in the framework of VAR (Sims 1980)

In a VAR, all the variables are endogenous:

With two variables in a model, X and Y: two endogenous variables in VAR;

That is, two equations:

(1): Yt = a + b Xt; and (2): Xt = c + d Yt;

Thus two possible cointegrating vectors(CVs):

We need to identify the CVs.

05 November 2013Vijayamohan: CDS MPhil: Time Series 8 89

Trace test:

This tests the null hypothesis that there are at

most r (i.e., 0 ≤≤≤≤ r ≤≤≤≤ n) cointegrating vectors

(CVs)

Ho: r CVs against H1: >>>> r CVs.

Thus the first row tests Ho: r = 0 against

H1: r >>>> 0; if this is significant, Ho is rejected and

the next row is considered.

Thus the rank (r = number of CVs) is chosen as

the last significant statistic, or as zero if the first

is not significant.

Testing for Cointegration: System method:Johansen – Juselius test

05 November 2013Vijayamohan: CDS MPhil: Time Series 8 90

Testing for Cointegration: System method:Johansen – Juselius test

Maximum eigenvalue test:

This tests Ho: r CVs against H1: r + 1 CVs. Thus

the first row tests Ho: r = 0 against H1: r = 1; if

this is significant, Ho is rejected and the next

row is considered.

A potential problem with the size of these test statistics in small samples: that is, the JJprocedure tends to over-reject the null when it is true (Reimers 1992). Hence a small-sample correction is applied to these statistics, replacing T by T−−−− np, where T is the number of observations, n is the number of variables and pis the lag length of the VAR.

11/5/2013

16

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 91

Testing for Cointegration: System method:Johansen – Juselius test

Level variables

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 92

Testing for Cointegration: System method:Johansen – Juselius test

First-Differenced variables

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 93

Unit-root tests (using Data.in7)The sample is 1954 (1) - 1992 (3)

CONS: ADF tests (T=155; 5%=-1.94 1%=-2.58)D-lag t-adf beta Y_1 sigma t-DY_lag t-prob AIC F-prob

3 -0.6661 0.99987 2.161 1.241 0.2167 1.5672 -0.7434 0.99985 2.165 1.604 0.1109 1.564 0.21671 -0.8371 0.99983 2.176 2.392 0.0180 1.568 0.13110 -1.033 0.99979 2.209 1.592 0.0219

INC: ADF tests (T=155; 5%=-1.94 1%=-2.58)D-lag t-adf beta Y_1 sigma t-DY_lag t-prob AIC F-prob

3 -0.5555 0.99983 3.348 0.6839 0.4951 2.4422 -0.5895 0.99982 3.342 -0.1570 0.8754 2.432 0.49511 -0.5864 0.99982 3.332 -1.052 0.2945 2.420 0.78210 -0.5397 0.99984 3.333 2.414 0.6628

PRICE INDEX: ADF tests (T=155; 5%=-1.94 1%=-2.58)D-lag t-adf beta Y_1 sigma t-DY_lag t-prob AIC F-prob

3 -0.4096 0.99990 3.511 -0.4221 0.6736 2.5372 -0.3979 0.99991 3.501 -0.5968 0.5516 2.525 0.67361 -0.3806 0.99991 3.494 2.468 0.0147 2.515 0.76670 -0.4436 0.99989 3.551 2.541 0.0918

Unit R

oot Tests on th

e

Level Variables

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 94

Unit-root tests (using Data.in7)The sample is 1954 (2) - 1992 (3)

DCONS: ADF tests (T=154; 5%=-1.94 1%=-2.58)D-lag t-adf beta Y_1 sigma t-DY_lag t-prob AIC F-prob

3 -4.453** 0.43565 2.161 -1.124 0.2628 1.5662 -5.316** 0.37979 2.163 -1.337 0.1831 1.562 0.26281 -6.812** 0.30387 2.168 -1.648 0.1014 1.561 0.22040 -10.13** 0.19674 2.180 1.565 0.1272

DINC: ADF tests (T=154; 5%=-1.94 1%=-2.58)D-lag t-adf beta Y_1 sigma t-DY_lag t-prob AIC F-prob

3 -5.886** -0.0099325 3.355 -0.4643 0.6431 2.4462 -6.953** -0.047705 3.346 -0.5646 0.5732 2.435 0.64311 -9.144** -0.098829 3.338 0.1576 0.8750 2.424 0.76650 -13.49** -0.084793 3.328 2.411 0.9059

DPRICE INDEX: ADF tests (T=154; 5%=-1.94 1%=-2.58)D-lag t-adf beta Y_1 sigma t-DY_lag t-prob AIC F-prob

3 -6.972** 0.010731 3.488 1.764 0.0798 2.5242 -6.971** 0.13464 3.512 0.3980 0.6912 2.532 0.07981 -8.126** 0.16195 3.502 0.5392 0.5905 2.520 0.19820 -10.11** 0.19731 3.494 2.509 0.3162

Unit R

oot Tests on th

e

First-D

ifferenced Variables

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 95

Testing for Cointegration: System method:Johansen – Juselius test in PcGive 10

Testing for cointegration among 3 variables: 3 possible CVs:

I(1) cointegration analysis, 1953 (2) to 1992 (3)eigenvalue loglik for rank

-1113.071 00.27034 -1088.172 10.23740 -1066.761 2

0.0049281 -1066.371 3

rank Trace test [ Prob] Max test [ Prob] Trace test (T-nm) Max test (T-nm)

0 93.40 [0.000]** 49.80 [0.000]** 91.6 3 [0.000]** 48.85 [0.000]**1 43.60 [0.000]** 42.82 [0.000]** 42.7 7 [0.000]** 42.01 [0.000]**2 0.78 [0.377] 0.78 [0.377] 0. 77 [0.382] 0.77 [0.382]

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 96

Testing for Cointegration: System method:Johansen – Juselius test in Stata

. vecrank cons inc Priceindex, trend(none)

Johansen tests for cointegrationTrend: none Number of obs = 157Sample: 1953q3 - 1992q3 Lags = 2------------------------------------------------------------------------------

5%maximum trace criticalrank parms LL eigenvalue statistic value0 9 -1083.6944 . 41.2984 24.311 14 -1066.35 0.19824 6.6095* 12.532 17 -1063.3777 0.03716 0.6649 3.843 18 -1063.0452 0.00423

-------------------------------------------------------------------------------

11/5/2013

17

5 November 2013Vijayamohan: CDS M Phil: Time Series 7 97

Testing for Cointegration: System method:Johansen – Juselius test in Stata

(input all the variables in the column for dependent variables)

In Stata

Statistics →→→→ Multivariate Time Series →→→→ Cointegrating rank of a VECM

05 November 2013Vijayamohan: CDS MPhil: Time Series 8 98

Summing Up: ‘Much Ado about Nothing’?

If ut = Yt – βXt is I(0),

yt and xt are cointegrated

(Both I(d), d ≠≠≠≠ 0 )

and the regression yt = ββββ xt + ut

is not spurious.

05 November 2013Vijayamohan: CDS MPhil: Time Series 8 99

Summing Up: ‘Full of Sound and Fury; Signifying Nothing’?

ut ~~~~ I(0) ⇒⇒⇒⇒ ut is white noise

⇒⇒⇒⇒ OLS assumptions satisfied!

So just see if OLS assumptions are satisfied!

No need for the pre-tests

(of unit root and cointegration)!

(See my book ‘Econometrics of Electricity Demand:

Questioning the Tradition’ 2010, Lambert Academic

Publishing, Germany)

5 November 2013Vijayamohan CDS Time Series: Introduction 100

Most macroeconomic variables : non stationary.

Non-stationarity problem:Consequence: Spurious Regression

Approaches: Classical Modern

Diagnosis: ACF tests Unit root tests

Solution: Differencing Differencing/Cointegration

Estimation: ARIMA (Box-Jenkins)/ VAR (Sims 1980)/MARIMA (V)ECM (Sargan 1964;(Harvey 1997) Davidson et al. 1978)/

GETS (Hendry 1987)

5 November 2013 Vijayamohan: CDS M Phil: Time Series 7

101