united states metals in the americas 26 september 2016

TRANSCRIPT

Deutsche Bank Markets Research

North America

United States

Periodical

Metals in the Americas

Date

26 September 2016

The Weekly Extract

________________________________________________________________________________________________________________

Deutsche Bank Securities Inc.

Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MCI (P) 057/04/2016.

Jorge Beristain, CFA

Research Analyst

(+1) 203 863-2381

Chris Terry

Research Analyst

(+1) 212 250-5434

Jeremy Kliewer

Research Associate

(+1) 904 527-6532

Top picks

Alcoa (AA.N), USD9.76 Buy Kaiser (KALU.OQ),USD85.42 Buy Newmont (NEM.N), USD39.56 Buy Steel Dynamics (STLD.OQ), USD24.84 Buy

DB coverage stock performance 9/23/2016 % 1W % 1M % YTD

Coeur 12.56 1 (3) 406 Teck 18.18 (0) 15 371

Hecla 6.00 9 9 217

Pan American

Silver

17.79 5 (0) 174

Barrick 18.11 4 (0) 145

US Steel 18.95 19 (5) 137

Kinross 4.30 5 2 136

Silver Standard 16.71 5 (1) 133

Silver Wheaton 27.82 5 6 124

AK Steel 4.96 21 8 121

Newmont 39.56 3 (1) 120

Vale 5.42 8 (4) 65

Franco-Nevada 71.87 2 (1) 57

Freeport-

McMoRan

10.63 7 (4) 57

Allegheny Tech. 17.55 11 6 56

Century Aluminum 6.59 11 (4) 49

Goldcorp 16.66 7 4 44

S&P 500 M&M 99 5 (2) 43

Steel Dynamics 24.84 6 1 39

Reliance 71.63 4 (1) 24

Nucor 48.81 7 (0) 21

Ryerson 11.17 8 (5) 8

S&P 500 2,165 1 (0) 6

Kaiser 85.42 3 2 2

Southern Copper 25.96 2 1 (1)

Alcoa 9.76 3 (3) (1)

Constellium 7.20 3 34 (6) Source: Thomson One and Deutsche Bank

DB coverage forward P/E (x)

23.0

39.8

12.2

21.1 17.9

14.4

30.3

13.9 16.2 16.4

0

10

20

30

40

50

Industrial

Metals

Precious

Metals

Steel &

Service

Centers

Aluminum

& Specialty

Metals

S&P 500

2016E 2017E

Source: Thomson One and Deutsche Bank

WEEKLY EXTRACT The S&P 500 rose 1% WoW to 2,165 and the S&P 500 M&M increased 5%

to 99. Nickel (+10% WoW to $4.82/lb) led the gains following concerns that Philippines may suspend more mines under environmental crackdown. Silver (+5% WoW to $19.82/oz) and gold (+2% to $1,340/oz) increased after US Federal Reserve kept interest rates unchanged. Similarly, aluminum price was up 4% to $0.74/lb on lower USD as Fed rates stay flat. Meanwhile, US Hot-Rolled Coil (HRC) price fell 5% to $529/st while the spread between HR and Cold-Rolled (CRC) sheet widened to $218/st (+$7/st WoW).

PRICE PERFORMANCE DB M&M equities posted positive performance last week with Steel &

Service Centers equities (+8% WoW) rising the most despite a decline in US HRC prices (-5%). Industrial Metals equities increased 6% WoW aided by higher prices for nickel (+10%), zinc (+3%) and copper (+1%). Precious Metals equities rose 5% on gains in silver (+5%) and gold (+2%). Lastly, Aluminum & Specialty Metals equities were up 4% in-line with the improvement in aluminum (+4%).

AK Steel (+21% WoW) and US Steel (+19%) led the gains within Steel & Service Centers equities after filing anti-circumvention request against Chinese CRC and galvanized sheet. Amongst Industrial Metals, Vale (+8%) traded higher after Brazil granted a 10-year license for a 63-mile rail line for its S11D mine. Hecla (+9%) and Goldcorp (+7%) were the leading performers within Precious Metals equities on higher underlying bullion prices. Within Aluminum & Specialty Metals equities, Century Aluminum and Allegheny Tech. (+11% each) increased the most on higher aluminum and nickel prices.

RECENT RESEARCH Americas Metals and Mining – Notes from the road - Denver Gold. A

glimmer of hope post-slump?

UPCOMING EVENTS East Coast marketing – Synagowitz/Beristain New York and Boston,

October 3-4

STOCK AND COMMODITY LEADERS & LAGGARDS (%) – 1 WEEK

1

5

0

1

2

2

3

9

11

11

19

21

-5 0 5 10 15 20 25

S&P 500

S&P 500 M&M

Teck

Coeur

Franco-Nevada

Southern Copper

Kaiser

Hecla

Allegheny Tech.

Century Aluminum

US Steel

AK Steel

1

5

-7

-6

-5

-1

0

3

3

4

5

10

-10 -5 0 5 10 15

S&P 500

S&P 500 M&M

Molybdenum ($/lb)

Scrap #1 ($/t)

HRC ($/t)

Lead ($/lb)

Coal - CAPP ($/t)

Natural gas …

Tin ($/lb)

Aluminum ($/lb)

Silver ($/oz)

Nickel ($/lb)

Note: based on DB coverage; Source: Thomson One and Deutsche Bank Source: Thomson One and Deutsche Bank

Distributed on: 26/09/2016 16:03:26 GMT

26 September 2016

Metals in the Americas

Page 2 Deutsche Bank Securities Inc.

PRICE PERFORMANCE

DB M&M equities posted positive performance last week with Steel & Service Centers equities (+8% WoW) rising the

most despite a decline in US HRC prices (-5%). Industrial Metals equities increased 6% WoW aided by higher prices for

nickel (+10%), zinc (+3%) and copper (+1%). Precious Metals equities rose 5% on gains in silver (+5%) and gold (+2%).

Lastly, Aluminum & Specialty Metals equities were up 4% in-line with the improvement in aluminum (+4%).

AK Steel (+21% WoW) and US Steel (+19%) led the gains within Steel & Service Centers equities after filing anti-

circumvention request against Chinese CRC and galvanized sheet. Amongst Industrial Metals, Vale (+8%) traded higher

after Brazil granted a 10-year license for a 63-mile rail line for its S11D mine. Hecla (+9%) and Goldcorp (+7%) were the

leading performers within Precious Metals equities on higher underlying bullion prices. Within Aluminum & Specialty

Metals equities, Century Aluminum and Allegheny Tech. (+11% each) increased the most on higher aluminum and

nickel prices.

Figure 1: Commodity performance summary Figure 2: Commodity prices relative to 52 wk range 23-Sep-16 Price % 1W % YTD

Aluminum (LME) ($/lb) 0.74 4 9

Cobalt (LME) ($/lb) 12.36 2 14

Copper (LME) ($/lb) 2.19 1 3

Lead (LME) ($/lb) 0.87 (1) 6

Molybdenum (LME) ($/lb) 6.66 (7) 26

Nickel (LME) ($/lb) 4.82 10 21

Tin (LME) ($/lb) 8.93 3 35

Zinc (LME) ($/lb) 1.03 3 42

Gold (COMEX) ($/oz) 1,340 2 26

Silver (COMEX) ($/oz) 19.82 5 (0)

HRC (US Midwest) ($/st) 529 (5) 39

MB Scrap Index ($/ton) 202 (6) 14

Iron ore (62% Fe) ($/ton) 57 0 31

Coal - API2 (ICE) ($/ton) 63 2 32

Coal - CAPP (NYMEX) ($/ton) 40 - (8)

Crude Oil - WTI ($/bbl) 44 3 19

Natural Gas (NYMEX) ($/mmBTU) 3.03 3 31

0%

20%

40%

60%

80%

100%

Alu

min

um

(LM

E)

Co

balt (

LM

E)

Co

pp

er

(LM

E)

Lead

(LM

E)

Mo

lyb

denum

(LM

E)

Nic

kel (L

ME

)

Tin

(LM

E)

Zin

c (

LM

E)

Go

ld (

CO

ME

X)

Silv

er

(CO

ME

X)

HR

C (

US

Mid

west)

MB

Scra

p I

nd

ex

Iro

n o

re (

62%

Fe)

Co

al -A

PI2

(IC

E)

Co

al -C

AP

P (

NYM

EX

)

Cru

de O

il -W

TI

Natu

ral G

as (

NYM

EX

)

S&

P 5

00

M&

M

S&

P 5

00

Source: Thomson One, Platts, CRU, Metal Bulletin and Deutsche Bank

Source: Thomson One, Platts, CRU, Metal Bulletin and Deutsche Bank

Figure 3: Commodity performance (%) (1W) Figure 4: Commodity performance (%) (YTD)

10

5 43 3 3 3 2 2 2 1

0 0

-1

-5 -6-7

5

1

-8-6-4-202468

1012

Nic

kel (L

ME

)

Silv

er

(CO

ME

X)

Alu

min

um

(LM

E)

Tin

(LM

E)

Natu

ral G

as (

NYM

EX

)

Zin

c (LM

E)

Cru

de O

il -

WTI

Co

al -

AP

I2 (

ICE

)

Go

ld (C

OM

EX

)

Co

balt (

LM

E)

Co

pp

er

(LM

E)

Iro

n o

re (

62%

Fe)

Co

al -

CA

PP

(N

YM

EX

)

Lead

(LM

E)

HR

C (U

S M

idw

est)

MB

Scra

p I

nd

ex

Mo

lyb

denum

(LM

E)

S&

P 5

00 M

&M

S&

P 5

00

Commodity prices Indices

4239

3532 31 31

26 2621 19

14 149 6

3

0

-8

43

6

-20

-10

0

10

20

30

40

50

Zin

c (LM

E)

HR

C (U

S M

idw

est)

Tin

(LM

E)

Co

al -

AP

I2 (

ICE

)

Natu

ral G

as (

NYM

EX

)

Iro

n o

re (

62%

Fe)

Mo

lyb

denum

(LM

E)

Go

ld (C

OM

EX

)

Nic

kel (L

ME

)

Cru

de O

il -

WTI

Co

balt (

LM

E)

MB

Scra

p I

nd

ex

Alu

min

um

(LM

E)

Lead

(LM

E)

Co

pp

er

(LM

E)

Silv

er

(CO

ME

X)

Co

al -

CA

PP

(N

YM

EX

)

S&

P 5

00 M

&M

S&

P 5

00

Commodity prices Indices

Source: Thomson One, Platts, CRU, Metal Bulletin and Deutsche Bank

Source: Thomson One, Platts, CRU, Metal Bulletin and Deutsche Bank

Figure 5: Equities rel. to 52wk range Figure 6: Performance (%) (1W) Figure 7: Performance (%) (YTD)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Ind

ustr

ial M

eta

ls

Pre

cio

us M

eta

ls

Ste

el &

Serv

ice

Cente

rs

Alu

min

um

&

Sp

ecia

lty M

eta

ls

S&

P 5

00 M

&M

S&

P 5

00

6

5

8

45

1

0

1

2

3

4

5

6

7

8

9

Ind

ustr

ial M

eta

ls

Pre

cio

us M

eta

ls

Ste

el &

Serv

ice

Cente

rs

Alu

min

um

&

Sp

ecia

lty M

eta

ls

S&

P 5

00 M

&M

S&

P 5

00

56

115

37

4

43

6

0

20

40

60

80

100

120

140

Ind

ustr

ial M

eta

ls

Pre

cio

us M

eta

ls

Ste

el &

Serv

ice

Cente

rs

Alu

min

um

&

Sp

ecia

lty M

eta

ls

S&

P 5

00 M

&M

S&

P 5

00

Source: Thomson One and Deutsche Bank Source: Thomson One and Deutsche Bank Source: Thomson One and Deutsche Bank

26 September 2016

Metals in the Americas

Deutsche Bank Securities Inc. Page 3

Figure 8: DB M&M performance (%) (1W) Figure 9: DB M&M performance (%) (YTD)

8 72

0

97

5 5 55 4 3 2 1

21 19

87

6 4

11 11

3 3 3

-10

0

10

20

30

Vale

Fre

ep

ort

-McM

oR

an

So

uth

ern

Co

pp

er

Teck

Hecla

Go

ldco

rp

Pan A

merican S

ilver

Kin

ross

Silv

er

Sta

nd

ard

Silv

er

Wheato

n

Barr

ick

New

mo

nt

Fra

nco

-Nevad

a

Co

eur

AK

Ste

el

US

Ste

el

Ryers

on

Nuco

r

Ste

el D

ynam

ics

Relia

nce

Centu

ry A

lum

inum

Alle

gheny T

ech.

Alc

oa

Co

nste

llium

Kais

er

Industrial Metals Precious Metals Steel & SC Al & SM

371

65 57

-1

406

217174

145136133124

12057 44

137121

3924 21 8

56 492

-1 -6-100

0

100

200

300

400

500

Teck

Vale

Fre

ep

ort

-McM

oR

an

So

uth

ern

Co

pp

er

Co

eur

Hecla

Pan A

merican S

ilver

Barr

ick

Kin

ross

Silv

er

Sta

nd

ard

Silv

er

Wheato

n

New

mo

nt

Fra

nco

-Nevad

a

Go

ldco

rp

US

Ste

el

AK

Ste

el

Ste

el D

ynam

ics

Relia

nce

Nuco

r

Ryers

on

Alle

gheny T

ech.

Centu

ry A

lum

inum

Kais

er

Alc

oa

Co

nste

llium

Industrial Metals Precious Metals Steel & SC Al & SM

Source: Thomson One and Deutsche Bank

Source: Thomson One and Deutsche Bank

Figure 10: DB M&M performance (%) (1Y) Figure 11: DB M&M performance (%) (1Y)

-

50

100

150

200

250

300

Sep

-15

Oct-

15

No

v-1

5

Dec-1

5

Jan

-16

Feb

-16

Mar-

16

Ap

r-16

May-1

6

Jun-1

6

Jul-16

Aug

-16

Sep

-16

Industrial Metals Precious Metals

Steel & Service Centers Aluminum & Specialty Metals

26

114

37

7

38

12

0

20

40

60

80

100

120

140

Ind

ustr

ial M

eta

ls

Pre

cio

us M

eta

ls

Ste

el &

Serv

ice

Cente

rs

Alu

min

um

&

Sp

ecia

lty M

eta

ls

S&

P 5

00 M

&M

S&

P 5

00

Source: Thomson One and Deutsche Bank

Source: Thomson One and Deutsche Bank

Figure 12: DB M&M 2017E P/E (x) Figure 13: DB M&M 2017E EV/EBITDA (x)

37

24

12

77

35 3430 28

21 21 21 21 1822

15 14 14 128

2519 16 14

9

-

10

20

30

40

50

60

70

80

90

Teck

So

uth

ern

Co

pp

er

Fre

ep

ort

Fra

nco

-Nevad

a

Hecla

Silv

er

Wheato

n

Pan A

merican

Silv

er

Sta

nd

ard

Go

ldco

rp

Co

eur

Min

ing

Kin

ross

Barr

ick

New

mo

nt

AK

Ste

el

US

Ste

el

Nuco

r

Relia

nce

Ste

el D

ynam

ics

Ryers

on

Centu

ry

Alle

gheny T

ech.

Alc

oa

Kais

er

Co

nste

llium

Industrial Metals Precious Metals Steel & SC Aluminum & SM

1211

96

26

19

10 9 97 7 6 6

4

87 6 6 6

4

8 7 6 6 5

-

5

10

15

20

25

30

So

uth

ern

Co

pp

er

Vale

Teck

Fre

ep

ort

Fra

nco-N

evad

a

Silv

er

Wheato

n

Hecla

Pan A

merican

Go

ldco

rp

Co

eur

Min

ing

New

mo

nt

Silv

er

Sta

nd

ard

Barr

ick

Kin

ross

Relia

nce

AK

Ste

el

Nuco

r

Ryers

on

Ste

el D

ynam

ics

US

Ste

el

Alle

gheny T

ech.

Kais

er

Alc

oa

Co

nste

llium

Centu

ry

Industrial Metals Precious Metals Steel & SC Aluminum &

SM

Source: Deutsche Bank estimates

Source: Deutsche Bank estimates

Figure 14: DB M&M forward P/E Figure 15: DB M&M forward EV/EBITDA

0x

10x

20x

30x

40x

50x

Sep

-09

Mar-

10

Sep

-10

Mar-

11

Sep

-11

Mar-

12

Sep

-12

Mar-

13

Sep

-13

Mar-

14

Sep

-14

Mar-

15

Sep

-15

Mar-

16

Sep

-16

Industrial Metals Precious Metals

Steel & Svc Centers Aluminum & Spec Metals

0x

5x

10x

15x

Sep

-09

Mar-

10

Sep

-10

Mar-

11

Sep

-11

Mar-

12

Sep

-12

Mar-

13

Sep

-13

Mar-

14

Sep

-14

Mar-

15

Sep

-15

Mar-

16

Sep

-16

Industrial Metals Precious Metals

Steel & Svc Centers Aluminum & Spec Metals

Note: Based on consensus estimates; Source: Thomson One and Deutsche Bank

Note: Based on consensus estimates; Source: Thomson One and Deutsche Bank

Meta

ls in th

e A

meric

as

26

Sep

tem

ber 2

01

6

Pag

e 4

D

eu

tsch

e B

an

k S

ecu

rities In

c.

Figure 16: DB Metals & Mining price performance

Price 52W 52W Price Upside/

Company Ticker 9/23/2016 High Low Target Downside 1W 3M 12M YTD 1W 3M 12M YTD

Freeport-McMoRan FCX.N 10.63 14.00 3.74 12 13 7 (10) 6 57 2 (14) (76) (31)

Southern Copper SCCO.N 25.96 30.21 22.29 25 (4) 2 (7) (2) (1) (3) (12) (84) (88)

Teck Resources TCK.N 18.18 18.44 2.66 11.5 (37) (0) 42 252 371 (6) 38 169 283

Vale VALE.N 5.42 6.07 2.15 6.5 20 8 9 18 65 3 5 (64) (23)

Industrial Metals 4 5 6 44 89 (0) 1 (38) 1

Barrick Gold Corporation ABX.N 18.11 23.16 6.19 22 21 4 (6) 205 145 (1) (11) 122 58

Franco-Nevada FNV.N 71.87 79.72 42.46 74 3 2 6 69 57 (3) 1 (13) (31)

Goldcorp GG.N 16.66 20.15 9.82 15 (10) 7 (5) 33 44 2 (10) (50) (44)

Kinross Gold Corporation KGC.N 4.30 5.74 1.38 4.5 5 5 (12) 169 136 0 (17) 86 48

Newmont Mining NEM.N 39.56 45.86 15.82 49 24 3 12 154 120 (2) 7 72 32

Gold 12 4 1 132 103 (1) (4) 50 16

Coeur Mining CDE.N 12.56 15.98 1.73 7.5 (40) 1 32 355 406 (4) 28 273 319

Hecla Mining HL.N 6.00 7.14 1.52 5.5 (8) 9 29 200 217 4 24 118 130

Pan American Silver PAAS.OQ 17.79 21.46 5.63 14.5 (18) 5 17 185 174 0 12 102 86

Silver Standard SSO.TO 16.71 20.02 5.49 14 (16) 5 14 103 133 (0) 10 20 46

Silver Wheaton SLW.N 27.82 30.88 10.50 37 33 5 34 140 124 (1) 29 58 36

Silver 11 5 29 171 169 (0) 25 89 82

Precious Metals 12 4 7 141 118 (1) 2 58 30

AK Steel AKS.N 4.96 6.70 1.83 4 (19) 21 2 110 121 16 (3) 28 34

Nucor NUE.N 48.81 56.90 34.86 60 23 7 (3) 27 21 2 (8) (56) (67)

Steel Dynamics STLD.OQ 24.84 27.98 15.86 32 29 6 (3) 46 39 1 (7) (37) (49)

US Steel X.N 18.95 27.49 6.67 23 21 19 5 69 137 14 1 (14) 50

Steel 22 9 (2) 40 43 3 (6) (43) (45)

Reliance RS.N 71.63 83.97 51.75 75 5 4 (9) 33 24 (1) (13) (50) (64)

Ryerson RYI.N 11.17 19.40 2.63 16 43 8 (33) 110 139 3 (38) 27 51

Service Centers 7 4 (10) 38 32 (1) (15) (44) (56)

Steel & Service Centers 20 8 (3) 39 41 3 (8) (43) (47)

Alcoa AA.N 9.76 11.31 6.74 12 23 3 (4) 6 (1) (2) (8) (76) (89)

Allegheny Technologies ATI.N 17.55 18.57 7.62 20 14 11 24 14 56 6 19 (69) (32)

Century CENX.OQ 6.59 9.21 2.80 7.5 14 11 (4) 31 49 6 (9) (51) (39)

Constellium CSTM.N 7.20 8.86 3.66 10 39 3 48 (8) (6) (2) 44 (90) (94)

Kaiser KALU.OQ 85.42 94.83 73.71 100 17 3 (7) 4 2 (3) (12) (79) (86)

Aluminum & Specialty Metals 22 4 1 7 6 (1) (4) (76) (81)

DB Metals & Mining 11 5 4 82 88 - - - -

S&P 500 Index SPSA 2,165 2,190 1,829 1 2 12 6

Relative PerformanceAbsolute Performance

Silver Standard price target stated in Canadian Dollars Source: Deutsche Bank, Bloomberg Finance LP

Meta

ls in th

e A

meric

as

26

Sep

tem

ber 2

01

6

Deu

tsch

e B

an

k S

ecu

rities In

c.

Pag

e 5

Figure 17: DB Metals & Mining valuation

Price Price Mkt cap P/BV Div yield ROE FCF Yld ND/Eq.

Company Ticker 9/23/2016 Rating Target (US$m) 2016E 2017E 2016E 2017E (x) (%) (%) (%) (%)

Freeport-McMoRan FCX.N 10.63 Hold 12 14,264 7.8 6.0 30.1 12.4 1.3 - (34.2) 2.9 115

Southern Copper SCCO.N 25.96 Hold 25 20,090 12.8 11.8 26.5 24.2 3.4 0.5 13.5 (0.4) 96

Teck Resources TCK.N 18.18 Sell 11.5 10,477 9.0 8.7 44.1 37.0 0.8 0.4 1.9 (0.5) 47

Vale VALE.N 5.42 Buy 6.5 27,931 7.3 10.6 8.9 nm 0.7 - 8.1 24.8 70

Industrial Metals 72,762 9.2 9.8 23.0 14.4 1.6 0.2 0.4 9.9 83

Barrick Gold Corporation ABX.N 18.11 Hold 22 21,098 7.2 6.5 28.5 20.6 2.1 0.4 5.2 7.1 61

Franco-Nevada FNV.N 71.87 Hold 74 12,656 26.6 25.8 86.3 77.1 3.0 1.1 4.1 2.8 (7)

Goldcorp GG.N 16.66 Sell 15 13,983 11.0 8.6 44.9 21.4 1.1 0.7 1.9 2.5 16

Kinross Gold Corporation KGC.N 4.30 Hold 4.5 5,342 5.0 3.9 33.1 20.7 1.2 - 2.2 7.1 20

Newmont Mining NEM.N 39.56 Buy 49 20,927 7.4 6.8 20.2 18.2 1.4 0.4 1.4 5.0 9

Gold 74,008 11.1 10.1 39.5 29.7 1.8 0.5 3.1 4.9 23.3

Coeur Mining CDE.N 12.56 Sell 7.5 1,993 10.3 7.2 nm 21.0 3.9 - 0.7 5.6 48

Hecla Mining HL.N 6.00 Hold 5.5 2,329 10.5 10.1 30.2 34.8 1.6 0.2 4.9 1.8 23

Pan American Silver PAAS.OQ 17.79 Hold 14.5 2,712 12.4 9.5 88.6 30.3 2.0 0.3 3.2 (2.2) (10)

Silver Standard SSO.TO 16.71 Hold 14 1,507 7.5 6.5 35.2 28.2 1.7 - 4.2 2.3 (7)

Silver Wheaton SLW.N 27.82 Buy 37 11,974 20.3 18.9 39.6 34.4 2.4 0.8 6.6 (1.4) 22

Silver 20,515 16.2 14.6 40.9 32.2 2.4 0.5 5.2 (0.2) 18

Precious Metals 94,523 12.2 11.1 39.8 30.3 1.9 0.5 3.6 3.8 22

AK Steel AKS.N 4.96 Sell 4 1,081 7.1 6.6 nm 22.4 nm - nm 32.9 nm

Nucor NUE.N 48.81 Buy 60 15,586 6.8 6.3 15.0 14.1 1.8 3.1 12.8 9.7 15

Steel Dynamics STLD.OQ 24.84 Buy 32 6,050 5.6 5.6 11.2 12.1 2.0 2.2 19.7 12.2 47

US Steel X.N 18.95 Hold 23 2,978 6.8 4.4 nm 14.5 1.1 1.1 (5.2) 18.7 60

Steel 25,695 6.5 5.9 11.7 14.0 1.7 2.5 11.8 12.3 27

Reliance RS.N 71.63 Hold 75 5,177 8.6 7.8 14.9 13.6 1.2 2.3 9.0 6.4 45

Ryerson RYI.N 11.17 Hold 16 385 5.5 5.7 7.5 8.3 nm - nm 40.5 nm

Service Centers 5,563 8.4 7.7 14.4 13.2 1 2.1 8.4 8.8 42

Steel & Service Centers 31,258 6.9 6.2 12.2 13.9 1.6 2.5 11.2 11.7 30

Alcoa AA.N 9.76 Buy 12 13,262 7.7 6.4 25.0 16.1 0.9 1.2 2.4 0.7 43

Allegheny Technologies ATI.N 17.55 Buy 20 1,883 29.0 7.5 nm 18.9 0.9 1.8 (38.5) 0.2 80

Century CENX.OQ 6.59 Hold 7.5 574 10.3 5.4 nm 25.2 0.6 - (3.7) 0.2 7

Constellium CSTM.N 7.20 Buy 10 760 7.0 5.8 29.1 8.9 nm - nm (2.7) nm

Kaiser KALU.OQ 85.42 Buy 100 1,554 7.8 6.6 17.2 13.9 1.9 2.1 13.3 2.8 13

Aluminum & Specialty Metals 18,032 10.0 6.5 21.1 16.2 0.9 1.2 (1.3) 0.6 42

DB Metals & Mining 216,576 10.2 9.5 28.6 21.4 1.7 0.8 3.2 6.7 45

EV/EBITDA (x) P/E (x)

Silver Standard price target stated in Canadian Dollars Source: Thomson One and Deutsche Bank

26 September 2016

Metals in the Americas

Page 6 Deutsche Bank Securities Inc.

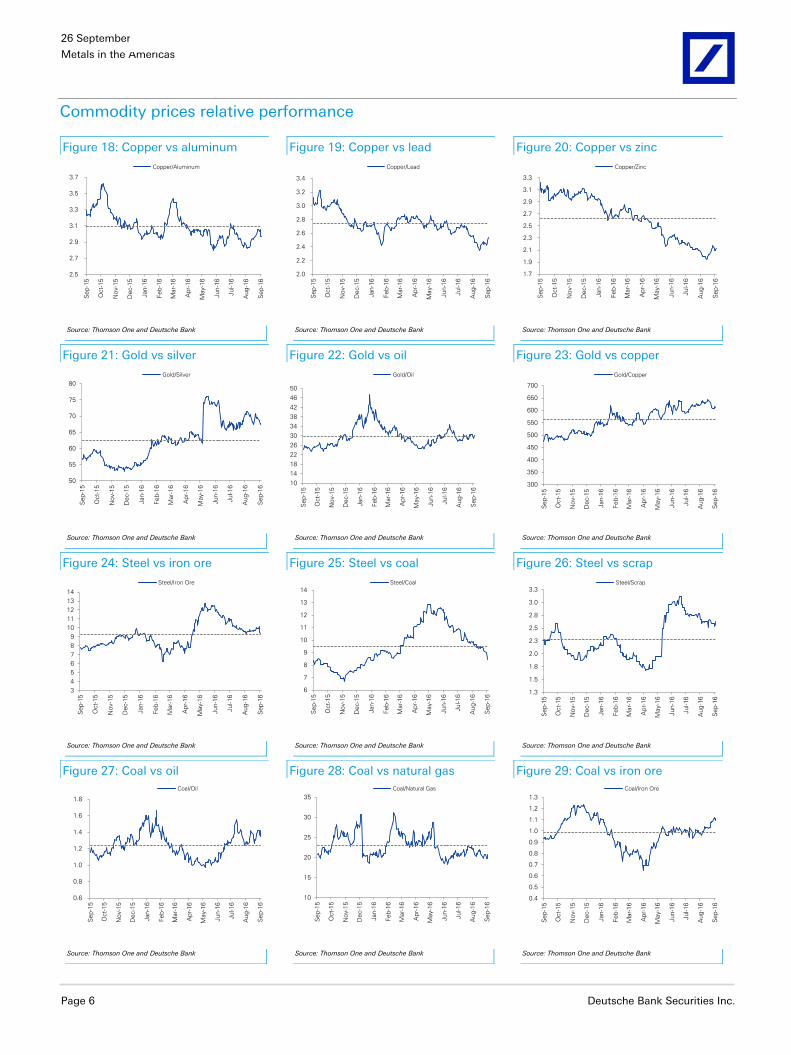

Commodity prices relative performance

Figure 18: Copper vs aluminum Figure 19: Copper vs lead Figure 20: Copper vs zinc

2.5

2.7

2.9

3.1

3.3

3.5

3.7

Sep

-15

Oct-

15

No

v-1

5

Dec-1

5

Jan

-16

Feb

-16

Mar-

16

Ap

r-16

May-1

6

Jun-1

6

Jul-16

Aug

-16

Sep

-16

Copper/Aluminum

2.0

2.2

2.4

2.6

2.8

3.0

3.2

3.4

Sep

-15

Oct-

15

No

v-1

5

Dec-1

5

Jan-1

6

Feb

-16

Mar-

16

Ap

r-16

May-1

6

Jun-1

6

Jul-16

Aug

-16

Sep

-16

Copper/Lead

1.7

1.9

2.1

2.3

2.5

2.7

2.9

3.1

3.3

Sep

-15

Oct-

15

No

v-1

5

Dec-1

5

Jan-1

6

Feb

-16

Mar-

16

Ap

r-16

May-1

6

Jun-1

6

Jul-16

Aug

-16

Sep

-16

Copper/Zinc

Source: Thomson One and Deutsche Bank Source: Thomson One and Deutsche Bank Source: Thomson One and Deutsche Bank

Figure 21: Gold vs silver Figure 22: Gold vs oil Figure 23: Gold vs copper

50

55

60

65

70

75

80

Sep

-15

Oct-

15

No

v-1

5

Dec-1

5

Jan-1

6

Feb

-16

Mar-

16

Ap

r-16

May-1

6

Jun-1

6

Jul-16

Aug

-16

Sep

-16

Gold/Silver

10

14

18

22

26

30

34

38

42

46

50

Sep

-15

Oct-

15

No

v-1

5

Dec-1

5

Jan

-16

Feb

-16

Mar-

16

Ap

r-16

May-1

6

Jun-1

6

Jul-16

Aug

-16

Sep

-16

Gold/Oil

300

350

400

450

500

550

600

650

700

Sep

-15

Oct-

15

No

v-1

5

Dec-1

5

Jan-1

6

Feb

-16

Mar-

16

Ap

r-16

May-1

6

Jun-1

6

Jul-16

Aug

-16

Sep

-16

Gold/Copper

Source: Thomson One and Deutsche Bank Source: Thomson One and Deutsche Bank Source: Thomson One and Deutsche Bank

Figure 24: Steel vs iron ore Figure 25: Steel vs coal Figure 26: Steel vs scrap

3

4

5

6

7

8

9

10

11

12

13

14

Sep

-15

Oct-

15

No

v-1

5

Dec-1

5

Jan

-16

Feb

-16

Mar-

16

Ap

r-16

May-1

6

Jun-1

6

Jul-16

Aug

-16

Sep

-16

Steel/Iron Ore

6

7

8

9

10

11

12

13

14

Sep

-15

Oct-

15

No

v-1

5

Dec-1

5

Jan-1

6

Feb

-16

Mar-

16

Ap

r-16

May-1

6

Jun-1

6

Jul-16

Aug

-16

Sep

-16

Steel/Coal

1.3

1.5

1.8

2.0

2.3

2.5

2.8

3.0

3.3

Sep

-15

Oct-

15

No

v-1

5

Dec-1

5

Jan-1

6

Feb

-16

Mar-

16

Ap

r-16

May-1

6

Jun-1

6

Jul-16

Aug

-16

Sep

-16

Steel/Scrap

Source: Thomson One and Deutsche Bank Source: Thomson One and Deutsche Bank Source: Thomson One and Deutsche Bank

Figure 27: Coal vs oil Figure 28: Coal vs natural gas Figure 29: Coal vs iron ore

0.6

0.8

1.0

1.2

1.4

1.6

1.8

Sep

-15

Oct-

15

No

v-1

5

Dec-1

5

Jan-1

6

Feb

-16

Mar-

16

Ap

r-16

May-1

6

Jun-1

6

Jul-16

Aug

-16

Sep

-16

Coal/Oil

10

15

20

25

30

35

Sep

-15

Oct-

15

No

v-1

5

Dec-1

5

Jan-1

6

Feb

-16

Mar-

16

Ap

r-16

May-1

6

Jun-1

6

Jul-16

Aug

-16

Sep

-16

Coal/Natural Gas

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

Sep

-15

Oct-

15

No

v-1

5

Dec-1

5

Jan-1

6

Feb

-16

Mar-

16

Ap

r-16

May-1

6

Jun-1

6

Jul-16

Aug

-16

Sep

-16

Coal/Iron Ore

Source: Thomson One and Deutsche Bank Source: Thomson One and Deutsche Bank Source: Thomson One and Deutsche Bank

26 September 2016

Metals in the Americas

Deutsche Bank Securities Inc. Page 7

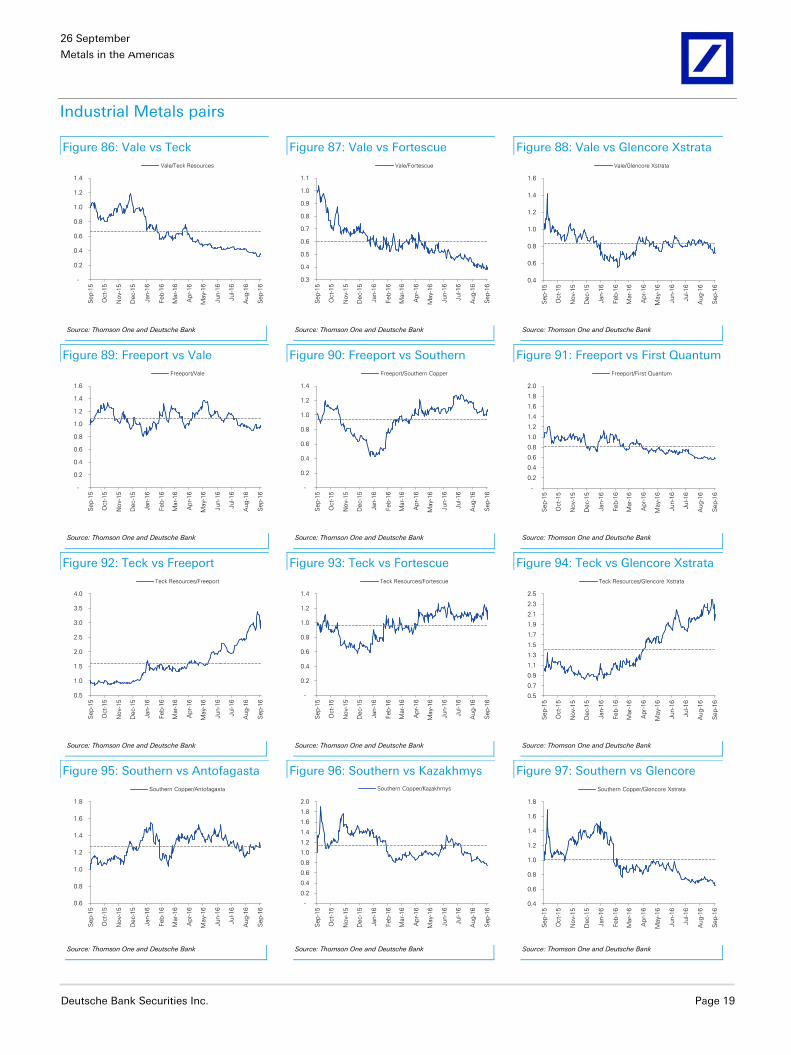

DB Metals & Mining equities relative performance by underlying commodity

Figure 30: Diversified vs steel Figure 31: Diversified vs aluminum Figure 32: Diversified vs gold

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

Sep

-15

Oct-

15

No

v-1

5

Dec-1

5

Jan

-16

Feb

-16

Mar-

16

Ap

r-16

May-1

6

Jun-1

6

Jul-16

Aug

-16

Sep

-16

DB Am Diversified/DB NA Steel

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

Sep

-15

Oct-

15

No

v-1

5

Dec-1

5

Jan

-16

Feb

-16

Mar-

16

Ap

r-16

May-1

6

Jun-1

6

Jul-16

Aug

-16

Sep

-16

DB Am Diversified/DB NA Aluminum and SM

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

Sep

-15

Oct-

15

No

v-1

5

Dec-1

5

Jan-1

6

Feb

-16

Mar-

16

Ap

r-16

May-1

6

Jun-1

6

Jul-16

Aug

-16

Sep

-16

DB Am Diversified/DB NA Gold

Source: Thomson One and Deutsche Bank Source: Thomson One and Deutsche Bank Source: Thomson One and Deutsche Bank

Figure 33: Copper vs diversified Figure 34: Copper vs aluminum Figure 35: Copper vs gold

0.6

0.8

1.0

1.2

1.4

1.6

1.8

Sep

-15

Oct-

15

No

v-1

5

Dec-1

5

Jan-1

6

Feb

-16

Mar-

16

Ap

r-16

May-1

6

Jun-1

6

Jul-16

Aug

-16

Sep

-16

DB Am Copper/DB Am Diversified

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

Sep

-15

Oct-

15

No

v-1

5

Dec-1

5

Jan

-16

Feb

-16

Mar-

16

Ap

r-16

May-1

6

Jun-1

6

Jul-16

Aug

-16

Sep

-16

DB Am Copper/DB NA Aluminum

-

0.2

0.4

0.6

0.8

1.0

1.2

Sep

-15

Oct-

15

No

v-1

5

Dec-1

5

Jan-1

6

Feb

-16

Mar-

16

Ap

r-16

May-1

6

Jun-1

6

Jul-16

Aug

-16

Sep

-16

DB NA Copper/DB NA Gold

Source: Thomson One and Deutsche Bank Source: Thomson One and Deutsche Bank Source: Thomson One and Deutsche Bank

Figure 36: Aluminum vs diversified Figure 37: Aluminum vs steel Figure 38: Aluminum vs gold

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

Sep

-15

Oct-

15

No

v-1

5

Dec-1

5

Jan-1

6

Feb

-16

Mar-

16

Ap

r-16

May-1

6

Jun-1

6

Jul-16

Aug

-16

Sep

-16

DB NA Aluminum/DB Am Diversified

0.6

0.7

0.8

0.9

1.0

1.1

1.2

Sep

-15

Oct-

15

No

v-1

5

Dec-1

5

Jan-1

6

Feb

-16

Mar-

16

Ap

r-16

May-1

6

Jun-1

6

Jul-16

Aug

-16

Sep

-16

DB NA Aluminum/DB NA Steel

-

0.2

0.4

0.6

0.8

1.0

1.2

Sep

-15

Oct-

15

No

v-1

5

Dec-1

5

Jan-1

6

Feb

-16

Mar-

16

Ap

r-16

May-1

6

Jun-1

6

Jul-16

Aug

-16

Sep

-16

DB NA Aluminum/DB NA Gold

Source: Thomson One and Deutsche Bank Source: Thomson One and Deutsche Bank Source: Thomson One and Deutsche Bank

Figure 39: Steel vs aluminum Figure 40: Steel vs gold Figure 41: Gold vs silver

0.4

0.6

0.8

1.0

1.2

1.4

1.6

Sep

-15

Oct-

15

No

v-1

5

Dec-1

5

Jan-1

6

Feb

-16

Mar-

16

Ap

r-16

May-1

6

Jun-1

6

Jul-16

Aug

-16

Sep

-16

DB NA Steel/DB NA Aluminum and SM

-

0.2

0.4

0.6

0.8

1.0

1.2

Sep

-15

Oct-

15

No

v-1

5

Dec-1

5

Jan-1

6

Feb

-16

Mar-

16

Ap

r-16

May-1

6

Jun-1

6

Jul-16

Aug

-16

Sep

-16

DB NA NA Steel/DB NA Gold

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

Sep

-15

Oct-

15

No

v-1

5

Dec-1

5

Jan-1

6

Feb

-16

Mar-

16

Ap

r-16

May-1

6

Jun-1

6

Jul-16

Aug

-16

Sep

-16

DB NA Gold/DB NA Silver

Source: Thomson One and Deutsche Bank Source: Thomson One and Deutsche Bank Source: Thomson One and Deutsche Bank

26 September 2016

Metals in the Americas

Page 8 Deutsche Bank Securities Inc.

Currency movement summary

Figure 42: Currency movement - appreciation (depreciation) of currencies vs USD

Price 52W 52W Absolute Performance

Currency (FX/USD) Ticker 9/23/2016 High Low 1W 1M 3M 6M 12M Y TD

Argentine Peso ARS 15.15 15.94 9.37 (0) (2) (6) (5) (38) (15)

Brazilian Real BRL 3.23 4.21 3.13 2 (1) 4 14 28 23

Canadian Dollar CAD 1.31 1.46 1.25 1 (2) (3) 1 1 6

Chilean Peso CLP 661 732 645 2 1 1 3 6 7

Mexican Peso MXN 19.71 19.85 16.38 (0) (7) (7) (11) (14) (12)

Peruvian Sol PEN 3.36 3.54 3.19 1 (0) (2) 1 (4) 2

Americas 1 (2) (2) 0 (3) 2

Australian Dollar AUD 1.31 1.46 1.28 2 (0) 1 1 9 5

Indonesian Rupiah IDR 13,077 14,698 13,060 1 1 1 1 12 5

Russian Ruble RUB 63.75 84.24 61.29 2 1 1 7 3 15

South African Rand ZAR 13.68 16.94 13.08 4 (2) 6 12 1 13

Other producer currencies 2 0 2 5 6 10

Chinese Yuan CNY 6.67 6.70 6.32 0 (0) (1) (3) (4) (3)

Euro EUR 0.89 0.95 0.87 1 (1) (1) 0 1 3

Japanese Yen JPY 101 124 100 1 (1) 5 12 19 19

Rest of World (RoW) 1 (1) 1 3 5 7

Average 1 (1) (0) 3 2 5

Bloomberg Dollar Spot Index* BBDXY 1,186 1,253 1,156 1 (1) (2) 1 3 4 *Consists of trade-weighted basket of ten currencies (i.e. EUR, JPY, CAD, MXN, GBP, AUD, CHF, KRW, CNY and BRL) vs. USD; December 31, 2004 = 1,000 Source: Thomson One, Bloomberg Finance LP and Deutsche Bank

Figure 43: Currency performance vs USD (%) (1W) Figure 44: Currency performance vs USD (%) (YTD)

2 2

1

1

0 0

4

22

11

10

1

1

-1

0

1

2

3

4

5

CLP

BR

L

PE

N

CA

D

MX

N

AR

S

ZA

R

RU

B

AU

D

IDR

JP

Y

EU

R

CN

Y

Avera

ge

BB

DX

Y

Americas Other producing currencies RoW Overall

23

7 6

2

-12-15

15 13

5 5

19

3

-3

5 4

-20

-15

-10

-5

0

5

10

15

20

25

BR

L

CLP

CA

D

PE

N

MX

N

AR

S

RU

B

ZA

R

IDR

AU

D

JP

Y

EU

R

CN

Y

Avera

ge

BB

DX

Y

Americas Other producing currencies RoW Overall

Source: Thomson One, Bloomberg Finance LP and Deutsche Bank

Source: Thomson One, Bloomberg Finance LP and Deutsche Bank

Figure 45: 1Y currency movements - Americas Figure 46: 1Y currency movements - Others

50

60

70

80

90

100

110

120

130

140

Sep

-15

Oct-

15

No

v-1

5

Dec-1

5

Jan-1

6

Feb

-16

Mar-

16

Ap

r-16

May-1

6

Jun-1

6

Jul-16

Aug

-16

Sep

-16

ARS BRL CAD CLP MXN PEN

50

60

70

80

90

100

110

120

130

Sep

-15

Oct-

15

No

v-1

5

Dec-1

5

Jan

-16

Feb

-16

Mar-

16

Ap

r-16

May-1

6

Jun-1

6

Jul-16

Aug

-16

Sep

-16

AUD IDR RUB ZAR CNY EUR JPY

Source: Thomson One and Deutsche Bank

Source: Thomson One and Deutsche Bank

26 September 2016

Metals in the Americas

Deutsche Bank Securities Inc. Page 9

Industrial Metals

Figure 47: Industrial Metals price movement

Spot price WK %CH QTD %CH YTD% 12M %CH 2012A 2013A 2014A 2015A 2016E 2017E 2018E

Industrial Metals

Copper (Usc/lb) 219 1% -1% 3% -5% 361 334 311 250 208 203 228

Iron ore-IODEX 62% Fe ($/t) 57 0% 3% 31% -1% 124 130 97 56 49 42 45

Energy

Crude Oil-WTI ($/bbl) 44 3% -10% 19% -1% 94 98 93 49 44 53 65

Hard Coking Coal-Australia ($/t) 213 0% 129% 176% 165% 210 159 126 102 87 89 95

Natural Gas ($/mmBtu) 3.0 3% 5% 31% 18% 2.9 3.8 4.3 2.7 2.4 3.1 3.0

Thermal Coal-API2 ($/t) 63 2% 11% 32% 16% 119 100 85 71 63 59 58 Source: Deutsche Bank estimates, Platts and Thomson One

Figure 48: Copper stock vs prices Figure 49: Copper net position Figure 50: Copper forward curve

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

0

100

200

300

400

500

600

700

800

Sep-12 Mar-13 Sep-13 Mar-14 Sep-14 Mar-15 Sep-15 Mar-16 Sep-16

LME Copper stocks (LHS) LME Copper price (RHS)

US$/tKt

50

125

200

275

350

425

500

-50

-40

-30

-20

-10

0

10

20

30

40

50

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Non-commercial net positions (lhs) Copper price (rhs)

K ContractsNet Long

USc/lb

Net Short

K Contracts

1.80

2.05

2.30

2.55

2.80

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35

$/l

b

Tenor (Month)

23-Sep-16 1 Month Ago 2 Months Ago DB Copper

Source: Bloomberg Finance LP and Deutsche Bank Source: Bloomberg Finance LP and Deutsche Bank Source: Bloomberg Finance LP and Deutsche Bank

Figure 51: Chinese iron ore imports Figure 52: Chinese iron inventories Figure 53: Oil & natural gas price

20%

30%

40%

50%

60%

70%

80%

90%

0

20

40

60

80

100

120

140

Aug-01 Feb-04 Aug-06 Feb-09 Aug-11 Feb-14 Aug-16

Iron Ore Imports Fe adjusted production Imports of total needs

(m tons)

20

30

40

50

60

40

50

60

70

80

90

100

110

Aug-10 May-11 Feb-12 Nov-12 Aug-13 May-14 Feb-15 Nov-15 Aug-16

China iron ore inventory (LHS) No. of days of imports (RHS)

Days(m tons)

-

20

40

60

80

100

120

140

160

0

2

4

6

8

10

12

14

16S

ep-0

9

Mar-

10

Sep-1

0

Mar-

11

Sep-1

1

Mar-

12

Sep-1

2

Mar-

13

Sep-1

3

Mar-

14

Sep-1

4

Mar-

15

Sep-1

5

Mar-

16

Sep-1

6

Natural Gas (LHS)

Oil (RHS)($/mmBtu)

($/bbl)

Source: Bloomberg Finance LP and Deutsche Bank Source: Bloomberg Finance LP and Deutsche Bank Source: Bloomberg Finance LP and Deutsche Bank

Figure 54: Intl. coal price ($/t) Figure 55: US coal production Figure 56: US coal inventories

-

50

100

150

200

250

300

350

400

450

Sep

-09

Mar-

10

Sep

-10

Mar-

11

Sep

-11

Mar-

12

Sep

-12

Mar-

13

Sep

-13

Mar-

14

Sep

-14

Mar-

15

Sep

-15

Mar-

16

Sep

-16

Steam coal Met coal

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

5

10

15

20

25

Sep

-10

May-1

1

Jan-1

2

Sep

-12

May-1

3

Jan-1

4

Sep

-14

May-1

5

Jan-1

6

Sep

-16

US coal weekly output

YoY%(m tons)

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

0

50

100

150

200

250

Au

g-1

2

De

c-1

2

Apr-

13

Au

g-1

3

De

c-1

3

Apr-

14

Au

g-1

4

De

c-1

4

Apr-

15

Au

g-1

5

Dec-1

5

Apr-

16

Au

g-1

6Coal stocks (m tons)

YoY%

Source: Platts and Bloomberg Finance LP Source: Deutsche Bank and EIA Source: Deutsche Bank and EIA

26 September 2016

Metals in the Americas

Page 10 Deutsche Bank Securities Inc.

Global Industrial Metals equities performance

Figure 57: Global Industrial Metals market cap ($bn) Figure 58: Industrial Metals relative to 52wk range

83

61

39

27

17 12 11

20 14

7 6 3 1

0

10

20

30

40

50

60

70

80

90

BH

P B

illito

n

Rio

Tin

to

Gle

nco

re X

str

ata

Vale

Ang

lo A

merican

Fo

rtescue

Teck R

eso

urc

es

So

uth

ern

Co

pp

er

Fre

ep

ort

Anto

fag

asta

First

Quantu

m

Lund

in

Kaza

khm

ys

Diversified Copper

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Ang

lo A

merican

BH

P B

illito

n

Fo

rtescue

Gle

nco

re X

str

ata

Rio

Tin

to

Teck R

eso

urc

es

Vale

Iro

n o

re (

62%

Fe)

Anto

fag

asta

Fre

ep

ort

Lund

in

Kaza

khm

ys

So

uth

ern

Co

pp

er

First

Quantu

m

Co

pp

er

(LM

E)

Diversified Copper

Source: Thomson One and Deutsche Bank

Source: Thomson One and Deutsche Bank

Figure 59: Industrial Metals performance (%) (1W) Figure 60: Industrial Metals performance (%) (YTD)

1613

10 9 8 6

0

0

107 7

4 4 2 15

1

-30

-25

-20

-15

-10

-5

0

5

10

15

20

Ang

lo A

meri

can

Gle

nco

re X

str

ata

BH

P B

illit

on

Rio

Tin

to

Vale

Fo

rtescue

Teck R

eso

urc

es

Iro

n o

re (

62%

Fe)

Kaza

khm

ys

Lund

in

Fre

ep

ort

Anto

fag

asta

Fir

st

Quantu

m

So

uth

ern

Co

pp

er

Co

pp

er

(LM

E)

S&

P 5

00 M

&M

S&

P 5

00

Diversified IndicesCopper

371

179 178

10665

27 1231

12386

57 47

-1 -3

343

6

-50

0

50

100

150

200

250

300

350

400

Teck R

eso

urc

es

Ang

lo A

meri

can

Fo

rtescue

Gle

nco

re X

str

ata

Vale

BH

P B

illito

n

Rio

Tin

to

Iro

n o

re (

62%

Fe)

First

Quantu

m

Kaza

khm

ys

Fre

ep

ort

Lund

in

So

uth

ern

Co

pp

er

Anto

fag

asta

Co

pp

er

(LM

E)

S&

P 5

00 M

&M

S&

P 5

00

Diversified IndicesCopper

Source: Thomson One and Deutsche Bank

Source: Thomson One and Deutsche Bank

Industrial Metals news flow

Met coal prices set for first drop in two months Met coal prices set for the first drop in two months on declining demand from steel mills in Asia (ex-China). On 9/22, two met coal cargo sales were priced for $190-195/t FOB Australia vs. $206/t spot. Separately, Teck receives environmental approval for ~C$600m Baldy Ridge coal expansion project, Canada. The project will extend the life of Teck’s Elkview open-cut coal mine by 23 years (until 2045) and will mine ~153Mt of coal. In 2015, Elkview produced 6.5Mt of hard coking coal. (Source: Reuters, AME)

Chinese copper output rises to six-month high Chinese copper production rises to six-month high of 743kt in August (+3% MoM; +12% YoY) as smelters expanded capacity amid favorable profit margins (spot treatment charges at $105/t, highest since 2015). YTD production at 5.5m t (+9% YoY). Separately, zinc output was 517kt in August (+2%, -2%) and 4.1m t YTD (-1%) amid tightness in global ore supplies. (Source: Bloomberg Finance LP)

Chilean mining investment to decline to $49.2bn for 2016-25 Chilean mining investment to decline to $49.2bn for 2016-25 vs. prior forecast of $77.3bn for 2015-24 as miners cut capex on weaker commodity prices, as per Cochilco. Majority of investment is for copper projects with remainder for iron and gold. Chile produced 5.76m tons of copper in 2015. (Source: Reuters)

US natural gas hits a 20-month high US natural gas price hits a 20-month high of $3.05/mmBtu (+4% DoD; +30% YTD) on continued warm weather forecasts for the next two weeks, which may lead to higher operating costs at steel mini-mills and aluminum smelters. (Source: Reuters, DB)

26 September 2016

Metals in the Americas

Deutsche Bank Securities Inc. Page 11

Vale prioritizes margins over volumes during S11D ramp-up Vale prioritizes margins over volumes during ramp-up of $14.3bn S11D iron ore project. Company to ramp up its ~90Mtpa S11D project over four years and expects first output in late 2016 and first shipments in Jan-17. Separately, Brazil grants Vale a 10-year license for a 63-mile rail line connecting S11D mine in the Amazon jungle to the Carajas Railway (CR). CR will allow Vale to haul S11D's output to the Port of Ponta da Madeira in Sao Luis. (Source: AME, Reuters)

Fortescue expects strong Chinese demand to revive discussions with Vale on JV Fortescue believes strong Chinese demand could revive discussions with Vale for an iron ore JV. China’s iron ore imports rose 9% YoY to 670m tons YTD through August. In March, Vale-Fortescue announced they were working on a proposal to blend up to 100m tons of iron ore in China, however Vale now seems to be less interested in executing the deal in the near-term. (Source: Reuters)

26 September 2016

Metals in the Americas

Page 12 Deutsche Bank Securities Inc.

Precious Metals

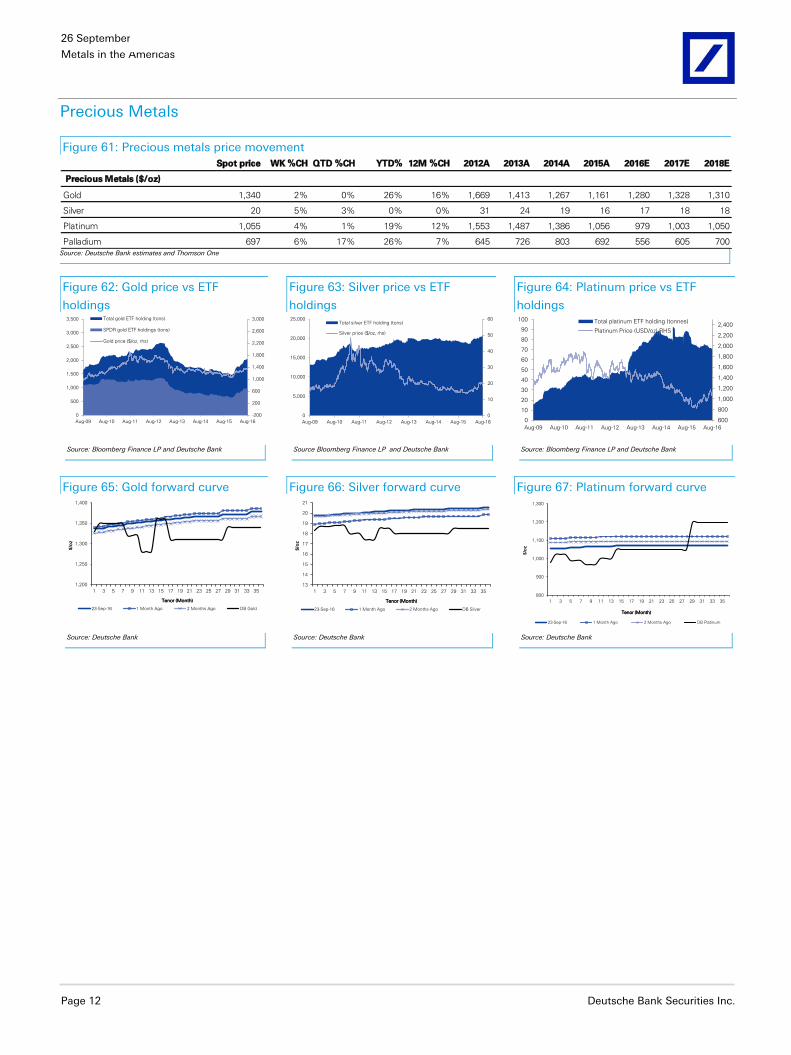

Figure 61: Precious metals price movement

Spot price WK %CH QTD %CH YTD% 12M %CH 2012A 2013A 2014A 2015A 2016E 2017E 2018E

Precious Metals ($/oz)

Gold 1,340 2% 0% 26% 16% 1,669 1,413 1,267 1,161 1,280 1,328 1,310

Silver 20 5% 3% 0% 0% 31 24 19 16 17 18 18

Platinum 1,055 4% 1% 19% 12% 1,553 1,487 1,386 1,056 979 1,003 1,050

Palladium 697 6% 17% 26% 7% 645 726 803 692 556 605 700 Source: Deutsche Bank estimates and Thomson One

Figure 62: Gold price vs ETF

holdings

Figure 63: Silver price vs ETF

holdings

Figure 64: Platinum price vs ETF

holdings

-200

200

600

1,000

1,400

1,800

2,200

2,600

3,000

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Aug-09 Aug-10 Aug-11 Aug-12 Aug-13 Aug-14 Aug-15 Aug-16

Total gold ETF holding (tons)

SPDR gold ETF holdings (tons)

Gold price ($/oz, rhs)

0

10

20

30

40

50

60

0

5,000

10,000

15,000

20,000

25,000

Aug-09 Aug-10 Aug-11 Aug-12 Aug-13 Aug-14 Aug-15 Aug-16

Total silver ETF holding (tons)

Silver price ($/oz, rhs)

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

0

10

20

30

40

50

60

70

80

90

100

Aug-09 Aug-10 Aug-11 Aug-12 Aug-13 Aug-14 Aug-15 Aug-16

Total platinum ETF holding (tonnes)

Platinum Price (USD/oz) RHS

Source: Bloomberg Finance LP and Deutsche Bank Source Bloomberg Finance LP and Deutsche Bank Source: Bloomberg Finance LP and Deutsche Bank

Figure 65: Gold forward curve Figure 66: Silver forward curve Figure 67: Platinum forward curve

1,200

1,250

1,300

1,350

1,400

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35

$/o

z

Tenor (Month)

23-Sep-16 1 Month Ago 2 Months Ago DB Gold

13

14

15

16

17

18

19

20

21

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35

$/o

z

Tenor (Month)

23-Sep-16 1 Month Ago 2 Months Ago DB Silver

800

900

1,000

1,100

1,200

1,300

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35

$/o

z

Tenor (Month)

23-Sep-16 1 Month Ago 2 Months Ago DB Platinum

Source: Deutsche Bank Source: Deutsche Bank Source: Deutsche Bank

26 September 2016

Metals in the Americas

Deutsche Bank Securities Inc. Page 13

Global Precious Metals equities performance

Figure 68: Precious Metals market cap ($bn) Figure 69: Precious Metals relative to 52wk range

21 21

14 13 13 13

10 10

7 5 5

4 4 4 3 3

17

12

3 2 2 2 2

0

5

10

15

20

25

Barr

ick

New

mo

nt

Go

ldco

rp

Po

lyus

New

cre

st

Fra

nco

-Nevad

a

Ag

nic

o-E

ag

le

Rand

go

ld

Ang

loG

old

Ashanti

Po

lym

eta

l

Kin

ross

Yam

ana

Go

ld F

ield

s

Buenaventu

ra

Sib

anye G

old

Eld

ora

do

Go

ld

Fre

snill

o

Silv

er

Whe

ato

n

Pan A

merican

Hecla

Co

eur

Min

ing

Ho

chschild

Silv

er

Sta

nd

ard

Gold Silver

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Ag

nic

o-E

ag

le

Ang

loG

old

Ashanti

Barr

ick

Buenaventu

ra

Eld

ora

do

Go

ld

Go

ldco

rp

Go

ld F

ield

s

Kin

ross

New

cre

st

New

mo

nt

Po

lym

eta

l

Po

lyus

Rand

go

ld

Sib

anye G

old

Yam

ana

Fra

nco

-Nevad

a

Go

ld (

CO

ME

X)

Co

eur

Min

ing

Fre

snill

o

Hecla

Ho

chschild

Pan A

merican

Silv

er

Sta

nd

ard

Silv

er

Wheato

n

Silv

er

(CO

ME

X)

Gold Silver

Source: Thomson One and Deutsche Bank

Source: Thomson One and Deutsche Bank

Figure 70: Precious Metals performance (%) (1W) Figure 71: Precious Metals performance (%) (YTD)

108

7 7 6 6 6 54

4 32 2

1

0

-4

2

12

9 9

5 5 5

1

5 5 5

1

-6

-4

-2

0

2

4

6

8

10

12

14

Ang

loG

old

Ashanti

New

cre

st

Go

ldco

rp

Go

ld F

ield

s

Rand

go

ld

Sib

anye G

old

Ag

nic

o-E

ag

le

Kin

ross

Barr

ick

Eld

ora

do

Go

ld

New

mo

nt

Fra

nco

-Nevad

a

Yam

ana

Buenaventu

ra

Po

lyus

Po

lym

eta

l

Go

ld (

CO

ME

X)

Ho

chschild

Fre

snill

o

Hecla

Silv

er

Sta

nd

ard

Pan A

merican

Silv

er

Wheato

n

Co

eur

Min

ing

Silv

er

(CO

ME

X)

PH

LX

Go

ld S

ilver

S&

P 5

00 M

&M

S&

P 5

00

Gold Silver Indices

231

147145142141136120107

85 81 79 68 57 48 44 39 26

423406

217

174147

124122

43

111

43

6

0

50

100

150

200

250

300

350

400

450

Buenaventu

ra

Sib

anye G

old

Barr

ick

Ang

loG

old

Ashanti

Yam

ana

Kin

ross

New

mo

nt

Ag

nic

o-E

ag

le

Go

ld F

ield

s

New

cre

st

Po

lyus

Rand

go

ld

Fra

nco

-Nevad

a

Po

lym

eta

l

Go

ldco

rp

Eld

ora

do

Go

ld

Go

ld (

CO

ME

X)

Ho

chschild

Co

eur

Min

ing

Hecla

Pan A

merican

Silv

er

Sta

nd

ard

Silv

er

Wheato

n

Fre

snill

o

Silv

er

(CO

ME

X)

PH

LX

Go

ld S

ilver

S&

P 5

00 M

&M

S&

P 5

00

Gold Silver Indices

Source: Thomson One and Deutsche Bank

Source: Thomson One and Deutsche Bank

Precious Metals news flow

Precious metals rally as Fed leaves rates unchanged Precious metals rally as Fed leaves rates unchanged but sends a strong signal for a rate hike before the end of 2016. Gold prices are up 1.4% DoD at $1,334/oz and silver 3.1% to settle at $19.84/oz. (Source: Reuters)

Japan adopts a zero interest rate target for 10-year bonds Bank of Japan adopts a zero interest rate target for 10-year government bonds to overcome deflation and achieve inflation target of >2%. New framework involves yield curve control vs. asset purchase and monetary expansion used previously. Gold prices are up ~0.5% intraday. (Source: Wall Street Journal)

India plans to double tax on precious metals Indian government plans to double tax on gold and other precious metals to 2-6% (from current 1-2%) under the Goods and Services Tax (GST) regime. The committee on GST cites that higher tax would protect revenues of the States even if standard rate of GST is set below 20%. India accounted for 25% (or 849 tons) of total consumer demand for gold in 2015. (Source: The Hindu, WGC)

Sberbank PJSC to register on the Shanghai Gold Exchange Sberbank PJSC to register on the Shanghai Gold Exchange and sell up to 100 tons/year. Also, VTB Capital is targeting sales of 20 tons in FY17 and 100 tons in FY18. If Sberbank and VTB Capital reach their target of 100 tons each, this would account for 5% of total global supply. Russian banks are targeting China as it’s the largest high paying customer. (Source: Bloomberg Finance LP)

26 September 2016

Metals in the Americas

Page 14 Deutsche Bank Securities Inc.

Barrick to resume Veladero operations in two weeks Barrick expects to resume operations at Veladero gold mine in two weeks after a second cyanide spill within a year halted operations. Company maintains Veladero’s 2016 gold production forecasts at 580-640koz (DBe 583koz). Separately, Barrick is on track to meet its 2016 debt reduction target of $2bn with or without asset sale. YTD (through 2Q16), company reduced debt by $968m and plans to repay $273m in 3Q16. (Source: Mining Weekly, Reuters)

Newmont may close Batu Hijau stake sale in 4Q16 Newmont may close Batu Hijau (Indonesia) stake sale in 4Q16, previously estimated in 3Q16, due to complex approvals process. Separately, company is interested to acquire remaining 50% of Kalgoorlie gold mine in Australia from Barrick. Kalgoorlie contributes 7% (or ~360k oz) of 2016E attributable production for each company. (Source: Reuters, DB)

Silver Wheaton keen to add 3-4 early stage financing deals Silver Wheaton keen to add three to four early stage financing deals to its portfolio with small mining exploration companies owning base metal deposits with precious metal byproducts. Company sees $2bn worth streaming deals in the market, down 60% YoY, due to availability of other forms of financing like share issuance. (Source: Reuters)

26 September 2016

Metals in the Americas

Deutsche Bank Securities Inc. Page 15

Steel & Service Centers, Aluminum & Specialty Metals

Figure 72: Steel & Service Centers, Aluminum & Specialty Metals price movement

Spot price WK %CH QTD %CH YTD% 12M %CH 2012A 2013A 2014A 2015A 2016E 2017E 2018E

Steel & Scrap

Hot rolled coil - US ($/st) 529 -5% -16% 39% 22% 664 628 627 456 520 500 550

No.1 bushelling scrap, Chicago ($/lt) 235 0% -15% 47% -2% 427 428 429 430 431 432 433

Aluminum & SM (USc/lb)

Aluminum 74 4% -2% 9% 4% 93 86 86 76 70 70 71

Lead 87 -1% 3% 6% 13% 94 98 96 81 79 79 75

Molybdenum (US$/lb) 7 -7% -11% 26% 24% 13 10 12 7 6 7 7

Nickel 482 10% 7% 21% 7% 798 685 769 538 411 454 499

Zinc 103 3% 5% 42% 36% 89 88 98 88 88 93 95 Source: Deutsche Bank estimates, mysteel.net, AMM and Bloomberg Finance LP

Figure 73: Price movements

($/tonne)

Figure 74: Input costs ($/tonne)

Figure 75: China inventories

(m tonnes)

0

200

400

600

800

1,000

1,200

0

200

400

600

800

1,000

1,200

1,400

Sep

-09

Mar-

10

Sep

-10

Mar-

11

Sep

-11

Mar-

12

Sep

-12

Mar-

13

Sep

-13

Mar-

14

Sep

-14

Mar-

15

Sep

-15

Mar-

16

Sep

-16

US HRC (left)

China HRC (left)

China Rebar (right)

0

50

100

150

200

250

300

350

400

450

0

100

200

300

400

500

600

700

800

900

1,000

Se

p-0

9

Mar-

10

Se

p-1

0

Mar-

11

Se

p-1

1

Mar-

12

Se

p-1

2

Mar-

13

Se

p-1

3

Mar-

14

Se

p-1

4

Mar-

15

Se

p-1

5

Mar-

16

Se

p-1

6

No.1 bushelling scrap (left)

Shredded auto scrap (left)

Iron ore (right)

Met coal (right)

40

60

80

100

120

140

160

0

5

10

15

20

25

Sep

-10

Jan

-11

May-1

1

Sep

-11

Jan

-12

May-1

2

Sep

-12

Jan

-13

May-1

3

Sep

-13

Jan

-14

May-1

4

Sep

-14

Jan-1

5

May-1

5

Sep

-15

Jan

-16

May-1

6

Sep

-16

China Steel Invs

China Iron ore invs (RHS)

Source: CRU and Deutsche Bank Source CRU, Platts and Deutsche Bank Source: Mysteel.net and Deutsche Bank

Figure 76: US steel imports vs

permits

Figure 77: US weekly steel output

Figure 78: Baltic freight rate

0

1

2

3

4

5

Sep

-10

Mar-

11

Sep

-11

Mar-

12

Sep

-12

Mar-

13

Sep

-13

Mar-

14

Sep

-14

Mar-

15

Sep

-15

Mar-

16

Sep

-16

Actual Imports (m stons)

Import Licenses (m stons)

20

30

40

50

60

70

80

90

700

950

1,200

1,450

1,700

1,950

2,200

Sep

-09

Jan-1

0

May-1

0

Sep

-10

Jan-1

1

May-1

1

Sep

-11

Jan-1

2

May-1

2

Sep

-12

Jan-1

3

May-1

3

Sep

-13

Jan-1

4

May-1

4

Sep

-14

Jan-1

5

May-1

5

Sep

-15

Jan-1

6

May-1

6

Sep

-16

Net output (000s tons) Capability utilization

0

1,000

2,000

3,000

4,000

5,000

6,000

Sep

-09

Mar-

10

Sep

-10

Mar-

11

Sep

-11

Mar-

12

Sep

-12

Mar-

13

Sep

-13

Mar-

14

Sep

-14

Mar-

15

Sep

-15

Mar-

16

Sep

-16

Baltic Freight Index

Source: Deutsche Bank and US Census Bureau (CB) Source: Deutsche Bank and AISI Source: Bloomberg Finance LP and Deutsche Bank

Figure 79: Aluminum stock vs prices Figure 80: Aluminum forward curve Figure 81: Nickel forward curve

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2,600

2,800

3,000

0

1000

2000

3000

4000

5000

6000

Sep-12 Mar-13 Sep-13 Mar-14 Sep-14 Mar-15 Sep-15 Mar-16 Sep-16

LME Aluminum stocks (LHS) LME Aluminum price (RHS)

US$/tKt

0.60

0.65

0.70

0.75

0.80

0.85

0.90

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35

$/l

b

Tenor (Month)

23-Sep-16 1 Month Ago 2 Months Ago DB Aluminum

3.00

4.00

5.00

6.00

1 3 5 7 9 11 13 15 17 19 21 23 25 27

$/l

b

Tenor (Month)

23-Sep-16 1 Month Ago 2 Months Ago DB Nickel

Source: Bloomberg Finance LP and Deutsche Bank Source: Bloomberg Finance LP and Deutsche Bank Source: Bloomberg Finance LP and Deutsche Bank

26 September 2016

Metals in the Americas

Page 16 Deutsche Bank Securities Inc.

Steel & Service Centers, Aluminum & Specialty Metals equities performance

Figure 82: Steel & SC, Aluminum & SM market cap ($bn) Figure 83: Steel & SC, Al. & SM relative to 52wk range

15

6 5

3 2

1 0

12

8 8

5

3

2 2 2 1

0

2

4

6

8

10

12

14

16

Nuco

r

Ste

el D

ynam

ics

Relia

nce

US

Ste

el

Co

mm

erc

ial

Meta

ls

AK

Ste

el

Ryers

on

Alc

oa

No

rsk H

yd

ro

Chalc

o

Rusal

Co

nste

llium

Alle

gheny T

ech.

Carp

ente

r Tech.

Kais

er

Alu

min

um

Centu

ry A

lum

inum

Steel & Service Centers Aluminum & Specialty Metals

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

AK

Ste

el

Ryers

on

Nuco

r

Ste

el D

ynam

ics

US

Ste

el

Relia

nce

Co

mm

erc

ial M

eta

ls

HR

C (U

S M

idw

est)

MB

Scra

p I

nd

ex

Alc

oa

Alle

ghen

y T

ech.

Carp

en

ter

Tech.

Centu

ry A

lum

inum

Chalc

o

Co

nste

llium

Kais

er

Alu

min

um

No

rsk H

yd

ro

Rusal

Alu

min

um

(LM

E)

Nic

kel (L

ME

)

Steel & Service Centers Aluminum & Specialty Metals

Source: Thomson One and Deutsche Bank

Source: Thomson One and Deutsche Bank

Figure 84: Steel & SC, Al. & SM performance (%) (1W) Figure 85: Steel & SC, Al. & SM performance (%) (YTD)

2119

8 8 7 64

-5 -6

11 11 10 10

3 3 3 3

-11

4

10

5

1

-15

-10

-5

0

5

10

15

20

25

AK

Ste

el

US

Ste

el

Ryers

on

Co

mm

erc

ial M

eta

ls

Nuco

r

Ste

el D

ynam

ics

Relia

nce

HR

C (U

S M

idw

est)

MB

Scra

p I

nd

ex

Centu

ry A

lum

inum

Alle

gheny T

ech.

Carp

ente

r Tech.

No

rsk H

yd

ro

Alc

oa

Chalc

o

Co

nste

llium

Kais

er

Alu

min

um

Rusal

Alu

min

um

(LM

E)

Nic

kel (L

ME

)

S&

P 5

00 M

&M

S&

P 5

00

Steel & Sercvice Centers Aluminum & Specialty Metals Indices

139 137

121

39

24 21 18

39

14

5649

3116 11 8 2

-1

921

43

6

-20

0

20

40

60

80

100

120

140

160

Ryers

on

US

Ste

el

AK

Ste

el

Ste

el D

ynam

ics

Relia

nce

Nuco

r

Co

mm

erc

ial M

eta

ls

HR

C (U

S M

idw

est)

MB

Scra

p I

nd

ex

Alle

gheny T

ech.

Centu

ry A

lum

inum

Carp

ente

r Tech.

No

rsk H

yd

ro

Chalc

o

Rusal

Kais

er

Alu

min

um

Alc

oa

Alu

min

um

(LM

E)

Nic

kel (L

ME

)

S&

P 5

00 M

&M

S&

P 5

00

Steel & Service Centers Aluminum & Specialty Metals Indices

Source: Thomson One and Deutsche Bank

Source: Thomson One and Deutsche Bank

Steel & Service Centers, Aluminum & Specialty Metals news flow

World crude steel production rose 2% YoY in August

World crude steel production increased 1.9% YoY to 134m tons in August (flat MoM), with utilization at 68.5%

(+50bps YoY, +10bps MoM). China’s output increased 3.0% YoY to 69m tons (+2.6% MoM) while US production

decreased 3.4% to 6.7m tons (flat). YTD global output was 1.1bn tons (-0.7% YoY). (Source: WSA)

Global aluminum production up 1% MoM in August

Global aluminum production increased 1% MoM to 4.9Mt in August as China ramped production up 2% to 2.7Mt.

Through August global production was 38.1Mt (-1% YoY). (Source: International Aluminum Institute)

Chinese semi-finished aluminum net exports rose 6% MoM in August

Chinese semi-finished aluminum net exports increased to 335k tons (+5.7% MoM, +28.9% YoY) in August mainly on

higher Plates, Sheets & Strip products (+9kt or +7.7% MoM) and Foil (+7kt or +7.5%). (Source: Reuters)

Chinese aluminum producers push to supply auto and aerospace industries

Chinese aluminum producers push to supply automotive and aerospace industries, dominated by European and US

producers. China’s Hongqiao to expand smelting capacity by 16% YoY to 6m tons by YE16. (Source: Financial Times)

NA Service Center steel inventories rose 1% MoM in August

NA Service Center steel inventories rose 51kt (+1% MoM) to 9.0m st in August (-15% YoY), vs. 10-year avg. increase

of 15kt. This was mainly driven by higher flat-rolled products (+65kt, +1% MoM) partly offset by lower plates (-20kt, -

2%). Shipments increased to 3.7m st (+1% MoM and -8% YoY on days-adj. basis). Thus, inventories fell to 2.4 months

of supply (-0.4 MoM). YTD shipments total 29m st (-7% YoY). (Source: MSCI)

26 September 2016

Metals in the Americas

Deutsche Bank Securities Inc. Page 17

US sets antidumping duties of 42-94% on cut-to-length steel plate imports

US Department of Commerce sets high preliminary antidumping duties (AD) of 42-94% on cut-to-length (CTL) steel

plate imports from Brazil, South Africa and Turkey, as respondents did not cooperate with the probe. YTD (th ru July),

imports of CTL plates from these three countries declined 26% YoY to 33k st (4% of total). Next, preliminary ADs for

remaining 9 of 12 targeted countries are due Nov 7, where petitioners have alleged margins of 8-249%. (Source: SBB,

DB)

US maintains antidumping order on Russian HRC

US International Trade Commission maintains antidumping order on Russian hot-rolled coil (HRC) in its third sunset

review. HRC imports from Russia have largely stopped, after US Department of Commerce terminated the duty

suspension agreement in December 2014. Separately, Nucor may be planning a $230m cold mill expansion at its

Hickman mill in Blytheville, Arkansas. (Source: SBB)

US files complaint China to circumvent antidumping/countervailing duties on CRC

US mills file complaint with US Commerce Department alleging that China is circumventing

antidumping/countervailing duties on cold-rolled coil (CRC) and corrosion-resistant sheet by processing hot-rolled coil

in Vietnam. US imports of CRC/galvanized sheet from China dwindled from 335kt/577kt in 1H15 to 0.1kt/10kt in 1H16.

However, imports from Vietnam increased from 9kt/2kt in 1H15 to 173kt/131kt in 1H16, respectively. (Source: SBB)

US HRC price decreased $27/st WoW

US Hot-Rolled Coil (HRC) price decreased $27/st WoW to $529/st on 9/21. Spread between HR and Cold-Rolled sheet

widened to $218/st (+$7/st WoW). Separately, NYMEX 12-month forward HRC price was down $15/st WoW to

$493/st. Lastly, China spot HRC price declined $5/t WoW to $420/t (-$67/t vs. recent peak on 4/27). (Source: CRU,

CME)

US steel import permits for September through 9/20 total 2.1m st

US steel import permits for September through 9/20 total 2.1m st. If adjusted to a full month, imports would be 3.2m

st (+12% YoY), vs. August permits of 3.1m st and July imports of 3.3m st. Carbon semis (+133kt, +20% MoM) appear

to increase the most, followed by coated sheets (+50kt, +14%) and hot-rolled sheets (+46kt, +20%), whereas, cut-

length plate (-42kt, -34%) imports are decreasing. (Source: US Import Administration)

US files trade case against rebar imports from Japan, Taiwan and Turkey

US steel mills file trade case against rebar imports from Japan, Taiwan and Turkey, seeking antidumping duties of 86 -

206%. Also, counter-vailable penalties sought against Turkish rebars. From 2013-15, imports from these 3 countries

rose ~160% to 1.9m st, and held ~22% of market share. (Source: AMM)

Nucor to acquire Independence Tube Corp. for $435m

Nucor to acquire Independence Tube Corporation (ITC) for $435m or ~6x avg. EBITDA over 2013-15. ITC operates four

facilities in Illinois and Alabama (600kt combined capacity), that purchase hot-rolled coil and produce hollow

structural section steel tubing (#2 market share). Acquisition should boost internal consumption and strengthen value -

added product portfolio. (Source: Company)

Nucor plans to build a specialty cold mill at Arkansas division

Nucor plans to build a specialty cold mill at Arkansas division to expand its capability to produce advanced high-

strength, high-strength low-alloy and motor lamination steel products. The mill will cost ~$230m and is expected to

be operational in two years. (Source: Company)

Steel Dynamics provides 3Q16 EPS guide of $0.63-0.67

Steel Dynamics provides 3Q16 EPS guide of $0.63-0.67 (DBe $0.72, Thomson One consensus $0.71). Profitability of

Steel Operations to rise QoQ on higher pricing partly offset by lower shipments. Results of Fabrication and Metals

Recycling segments to decline on metal spread expansion. (Source: Company, DB, Thomson One)