univaasa 2020 tuukkanen emilia - osuva

TRANSCRIPT

1

EmiliaTuukkanen

Order-to-cashbusinessprocessimprovementbyLeanSixSigmatoolsStudyofacasecompany

Vaasa2020

SchoolofTechnologyandInnovationsMaster’sthesisinIndustrialManagement

2

UNIVERSITYOFVAASASchoolofTechnologyandInnovationsAuthor: EmiliaTuukkanenTitleoftheThesis: Order-to-cashbusinessprocessimprovementbyLeanSixSigmatools:StudyofacasecompanyDegree: MasterofScienceinEconomicsandBusinessAdministrationProgramme: IndustrialManagementSupervisor: AhmShamsuzzohaYear: 2020 Pages:79

ABSTRACT:Worldwidecompetitiondrivesbusinessestofocusonsuperioroperationalexcellenceactivitiesalongwithcreatingvalueforthestakeholders.Thepurposeofthismaster’sthesiswastoanalyzethecasecompany’scurrentstateoftheorder-to-cash(O2C)processaswellasidentifyingtheareasofdevelopmentbythemeansofLeanSixSigmatools.Thestudywasconductedasamixofquantitativeandqualitativeanalysis.Basedonthedata,avaluestreammappingworkshopwasconductedtoanalyzethecurrentstateoftheO2Cprocessofthecasecompany.TheO2Cprocessisthemostvisibleprocesstothecustomerandthereforeitspunctualandfluentordermanagementisvital.ToensurethattheO2Cprocessisoperatingasdesired,suitableprocessperformancemetricsneedtobealignedandfollowed.Theresultsgatheredfromthedata,in-terviewsandworkshopallhighlightedthatthehighdegreeofmanualworkcausemistakes,de-laysandreworkintheprocess.ThemanualworkismainlycausedbytheAllegrosystemfunc-tionalitythatisunreliableandrequiresmanualcontrollingandchecking.Theresultsfoundthatexcessivemanualworkwashighlyconnectedtoinadequateorincorrectdatainpricingandin-voicingactivitieswhichresultedincancelledinvoices.Cancelledinvoicesarevisibletothecus-tomerandhaveanegativeimpactonthecustomerexperience.Additionally,asthecurrentpro-cess is split into different process phases which are interdependent of each other, the im-portanceofcommunicationiscrucialforawell-functioningprocess.ToanalyzeandimprovethecurrentO2Cprocess,someLeanSixSigmatoolscouldbeutilizedforfurtheractions.Thesetoolsareprocessmining,rootcauseanalysisanddailycontinuousimprovementactivities.Addition-ally,keyprocessperformancemetricssuchas,touchlessrate,creditinvoicerateandtheamountofmanualfieldchangescouldbecreatedintheprocessminingtoolsystem,Celonis,inordertounderstandthereal-timeO2Cprocessperformance.Ensuringstrongperformanceandenhanc-ingcontinuousimprovementleadstooperationalexcellenceandcommercialcompetitiveness.Byimprovingtheperformanceofactivitiesandcommunicationwithinternalandexternalstake-holders, thewhole O2C process can performmore effectively and provide better customervalue.KEYWORDS:Order-to-cash,businessprocessimprovement,LeanSixSigma,processperfor-mancemetrics,valuestreammapping,casestudy

3

VAASANYLIOPISTOTekniikanjainnovaatiojohtamisenyksikköTekijä:EmiliaTuukkanenTutkielmannimi:Tilaus-toimitusprosessinkehittäminenLeanSixSigma-työkaluillaTutkinto:KauppatieteidenmaisteriOppiaine:TuotantotalousTyönohjaaja:AhmShamsuzzohaValmistumisvuosi:2020Sivumäärä:79TIIVISTELMÄ:Globaalikilpailuedellyttääyrityksiltäammattitaitoistaoperatiivistatoimintaa,jokaluolisäar-voasidosryhmille.Tämänlopputyöntavoitteenaolianalysoidacase-yrityksentilaus-toimitus-prosessinnykytilaa,sekätunnistaasenkehitysalueetLeanSixSigma–työkalujenavulla.Tut-kimusperustuusekäkvantitatiiviseenettäkvalitatiiviseenanalyysiin.Analyyseistasaatuihintietoihinperustuenlaadittiinarvovirtakuvaus,jollakartoitettiintilaus-toimitusprosessintuot-tavuuscase–yrityksentoiminnoissa.Asiakkaalletilaus-toimitusprosessionyksinäkyvimmistä,jonkavuoksiontärkeää,ettäsetoimiitäsmällisestijasujuvasti.Tilaus-toimitusprosessilleonasetettavaoikeatsuorituskykymittarit,joitaseuraamallavoidaanvarmistaaprosessintoimi-vuusodotetullatavalla.Kvantitatiivisenjakvalitatiivisenanalyysintuloksistajalaaditustaar-vovirtakuvauksestasaaduttuloksetosoittavat,ettämanuaalisentyönosuusonhuomattavaaiheuttaenvirheitä,viivästyksiäjaylimääräistätyötä.Manuaalisentyöntarvejohtuuensisijai-sestiAllegrojärjestelmäntoiminnanepäluotettavuudesta.Saatujentulostenmukaisestipuut-teellisistataivirheellisistätiedoistajohtuenmanuaalistatyötäesiintyyenitenhinnoittelussajalaskutuksessajohtaenhyvityslaskujentarpeeseen.Hyvityslaskutovatnäkyvinosaprosessiaasiakkaalle ja ne vaikuttavat negatiivisesti asiakaskokemukseen. Case-yrityksellä käytössäolevanykyprosessionjaettuerivaiheisiin,jotkaovattoisistaanriippuvaisia.Viestinnänmer-kitysonkriittinentoimivanprosessinkannalta.ProsessiaonmahdollistaanalysoidajakehittääLeanSixSigma–työkalujenavulla.Keskeisiätyökalujaovatesimerkiksiprosessinlouhinta,juu-risyidenanalysointijajatkuvaparantaminen.Prosessilouhinnanjärjestelmä,Celonis,mahdol-listaa prosessin suorituskykymittareiden luomisen.Mittareita voivat olla esimerkiksi auto-maatioaste,hyvityslaskujenosuusjamanuaalistenmuutostenmäärä.Näidenavullaonmah-dollistatarkastellatilaus-toimitusprosessintehokkuutta.Hyväprosessintoimivuusjasenjat-kuvaparantaminenovatoperatiivisentoiminnanjataloudellisenkilpailukyvynmenestysteki-jöitä.Myöstoimivaviestintäsisäisillejaulkoisillesidosryhmillemahdollistaaprosessintoimi-vuudenjaparantaaasiakaskokemusta.AVAINSANAT:tilaus-toimitusprosessi,prosessinkehittäminen,LeanSixSigma,prosessinsuo-rituskykymittarit,arvovirtakuvaus,case-tutkimus

4

Contents

1 Introduction 8

1.1 Descriptionofthecasecompany 8

1.2 Background 9

1.3 Purpose 9

1.4 Method 10

1.5 Delimitations 10

1.6 Structureofthethesis 11

2 TheoreticalFramework 12

2.1 Order-to-Cash 14

2.1.1 WhyisO2Cimportant? 16

2.1.2 Deliveryincoterms 17

2.2 BusinessProcessManagement 18

2.2.1 BusinessProcessImprovement 18

2.2.2 Processowners 20

2.2.3 BusinessProcessLeadershipatthecasecompany 21

2.3 KeyPerformanceIndicatorsandmetrics 22

2.4 LeanSixSigma 25

2.4.1 SixSigma 26

2.4.2 LeanOperations 28

2.4.3 Leantoolsandapproaches 29

3 Methodology 34

3.1 Quantitativedata 34

3.2 Qualitativeinterviews 35

3.3 Workshop 36

4 Results 38

4.1 CurrentO2Cprocessmanagement 38

4.2 Quantitativeresults 44

4.3 Qualitativeresults 55

5

4.4 Workshop 59

4.5 Discussion 66

4.6 Recommendations 67

5 Conclusions 69

References 71

Appendices 75

Appendix1.Theinterviewquestions 75

Appendix2.TheSIPOCmodel 77

Appendix3.Theswimlanediagram 78

Appendix4.TheVSMmatrix 79

6

ImagesImage1.TheCIFIncoterm(Bansar,2020). 17

FiguresFigure1.Casecompany’sCommercialExcellenceManagementSystem(CaseCompany,

2020). 13

Figure2.ThePDCAcycleandtheDMAICimprovementmodel(Kanbanize,2020). 27

Figure3.TheANSIsymbols(Trent,2008). 30

Figure4.Fishbonechart(Andersen,2007). 32

Figure5.The5Whysanalysis(Andersen,2007). 33

Figure6.TheO2CprocessphasesandtheflowofactionsintheSAPsystem(Adapted

fromCaseCompany,2020). 40

Figure7.AnexampleoftheO2Cprocess(CaseCompany,2020). 43

Figure8.Activitycountofeachprocessphase(CaseCompany,2020). 45

Figure9.Activitycountinaccordancetosalesorderspermonth(CaseCompany,2020).

46

Figure10.Manualchangecountoccurrences(CaseCompany,2020). 47

Figure11.Amountofmanual field changes inaccordance to the salesorderamount

(CaseCompany,2020). 48

Figure12.Manualchangesmadepersalesorder(CaseCompany,2020). 49

Figure13.Billingblockrate(CaseCompany,2020). 50

Figure14.Averagebillingblockcount(CaseCompany,2020). 51

Figure15.Billingblockcountoccurrences(CaseCompany,2020). 51

Figure16.Reverseticketingtimes(CaseCompany,2020). 52

Figure17.Averagereverseticketingmonthly(CaseCompany,2020). 53

Figure18.Creditinvoicerateofthesalescases(CaseCompany,2020). 54

Figure19.ASIPOCmodeloftheO2Cprocess. 60

Figure20.AswimlanediagramoftheO2Cprocess. 61

Figure21.VSMworkshopoutput. 63

7

Figure22.VSMoftheO2Cprocess. 64

TablesTable1.Processperformancemeasurements(Trent,2008). 24

Table2.TheO2Cprocessperformersandtheirresponsibilities(Adaptedfrompersonal

communicationswithinterviewees,February,2020). 41

AbbreviationsBPM BusinessProcessManagement

CIF Cost,Insurance,Freight

ERP EnterpriseResourcePlanning

KPI KeyPerformanceIndicator

O2C Order-to-Cash

RCA Rootcauseanalysis

TQM Totalqualitymanagement

VSM Valuestreammap

8

1 Introduction

Thismaster’sthesisstudiestheimprovementoftheorder-to-cash(O2C)businesspro-

cessthroughtheimplementationofLeanSixSigmatools.O2Cmeanshandlingandpro-

cessingacustomerorderandthisisdescribedinmoredetailinsection2.1.Thestudy

wasconductedforaFinnishenergyandenvironmentcompany.Theaimwastofindso-

lutionstoimprovetheoverallprocessperformance, inadditiontoprovidingvaluefor

thestakeholders.Additionally,thisthesisstudiesthebottlenecksanddefectsofthecur-

rentO2Cprocess.ItprovidesacomprehensivestudyonhowtheO2Cprocessiscurrently

operatingandwhichpartsoftheprocesscouldbestreamlined.Theinformationusedin

thisthesishasbeenbasedondataandotherrelevantmaterialsregardingthesalesop-

erationsofthecasecompany.Thisstudywasconductedforthecasecompanytoprovide

additionalvaluefortheiroperationalexcellenceactivities.

1.1 Descriptionofthecasecompany

Thecasecompanyoperatesinthefieldofenergyandenvironmentsectorandisalead-

ingcorporation insustainablebusiness (CaseCompany,2020).Thecompany’sopera-

tionsareglobalthus,theofficesandproductionsitesarelocatedworldwide.However,

itsstrongestpresenceisintheBalticSeaarea.Thecasecompany’sbusinessenvironment

ismainlyfocusedontheenergyproductionandcreatingsolutionsfortransportationby

road,sea,airandpipeline.

Thestrategyandvisionofthecasecompanyistooperateresponsiblyandtooffersus-

tainable solutions for consumer and corporate consumption (Case Company, 2020).

Theirsolutionsareconstantlydevelopingnewwaystocutdownoncarbonemissions

andtocirculateandreuseitsproducts.Thecasecompany’smissionistodobusiness

responsibly, innovativelyaswellaswithexcellenceandthesevaluesarerespected in

9

theiractions.Thus,thecompanyhasanoperationalexcellenceteamthatpromotesuni-

fiedwaysofworkinginaccordancewiththecompanystrategyinordertoensuregrowth

andcompetitiveness.Furthermore,thisthesissupportsitsactivitiesandfuturedevel-

opmentprojects.

1.2 Background

Thecasecompanyhasanongoingdevelopmentprojectofassessingthecurrentbusiness

processesandtheirmaturity,thusO2Cisoneoftheseprocessesthatneedstobedevel-

oped.Inordertodeveloptheprocess,acomprehensivestudyandassessmentofthe

currentprocessisrequiredandtheaimofthisstudyistosupportthecasecompanyto

achievethatgoal.Manualworkandlargenumberofchangesthroughouttheprocess

arerecognizedissuesbuttheireffectontheprocessperformanceisunknown.Currently,

therearelimitedperformancemetricsfortheO2Cprocessandthecompanyhasidenti-

fiedaneedtogainfurtherunderstandingwhethertheprocessisefficient.Itwouldbe

beneficial forthecompanytounderstandtheamountofwaste, itseffectonthecus-

tomerandthereal-timeprocessperformance.

1.3 Purpose

TheO2Cprocessisthemostvisibleprocessforthecustomer.Therefore,itisavitalbusi-

nessprocesstobemanaged.ByoptimizingtheO2Cprocessactivitiesthereismoretime

leftforadditionalsalesactivitiesandthusincomingrevenue.Thismaster’sthesisisfo-

cusingonthemethodstoimprovetheO2CbusinessprocessbythemeansofLeanSix

Sigmatools.Theresearchquestionsofthisstudyarethefollowing:

- WhatisLeanSixSigmaanditstools?

10

- Whatarethechallengesofthecurrentorder-to-cashprocessandwhatmethods

canbeusedtoimprovetheprocessperformance?

- Whatarethebestmetricstomeasuretheorder-to-cashprocessperformanceto

providevaluefortherelevantstakeholders?

ThisthesisstudiesthecurrentstateoftheO2Cprocessinordertogainunderstandingof

thechallengesandrootcausesofthearisingproblems.Thetheoreticalframeworksand

findingsfromdataprovidecomprehensiveknowledgeinordertodeterminerecommen-

dationsforthecasecompany.

1.4 Method

This studyhasbeen conducted as amixof quantitative andqualitative analysis. The

quantitativeanalysiswasbasedondataprovidedbythecompany’senterpriseresource

planning(ERP)system.Theanalysishasbeenconductedbyfindingthebottlenecksand

defectsoftheprocessfollowingwithacomparisontotheidealprocessflow.Additionally,

thequalitativeanalysiswasreflectedonthebottlenecksanddefectsinordertounder-

standthereasontheprocessiscurrentlyfunctioninginthisspecificway.Avaluestream

mapping(VSM)workshopwasalsoconductedasapartofthestudy.Intheworkshop,a

selectedteammappedthecurrentstateoftheO2Cprocessanddeterminedthemain

areasofdevelopment.

1.5 Delimitations

ThescopeofthethesisislimitedtotheBalticSeaareaoperationsandsurplussalesdone

asspotsales(unplannedsales).TheO2Cprocesswasanalyzedthroughvesseldeliveries

operatedbyFinland’sandEurope’ssalesoperations.Thisstudytakesintoconsideration

theCIFdelivery incoterms,only. Thevesseldeliverieswere chosenbecause theyare

11

businesscriticalasglobaloperationsenablealargermarket.Thesedeliverieshighlight

theimportanceofcooperationbetweendifferentstakeholdersasseveraldepartments

takepartintheprocess.

Themainaimofthisthesiswastostudyandanalyzethecurrentorder-to-cashprocess

andgiverecommendationsforthecasecompanytoacton.Theimplementationofthe

recommendationswillbedoneafterthepublicationofthisthesis.Thedatahasbeen

classifiedcompanyconfidentialaswellasothercompanyspecificinformationhasnot

beenreleased.

1.6 Structureofthethesis

Thisthesishasbeenconductedscientificallyandfollowsascientificstructure.Thefirst

chapterintroducesthethesistopic,backgroundandpurpose.Thesecondchaptercovers

thefollowingtheoreticalframeworks:

- Order-to-Cashprocess,

- BusinessProcessManagement,

- KeyPerformanceIndicatorsandMetricsand

- LeanSixSigma.

Thethirdchapter,reviewsthemethodology’sanddescribestheimplementationofthe

empiricalstudy.Thefourthchapterexplainsthedatagathered,analysesthedataand

theworkshopandfinallydiscussestheirresults.Thelastchaptersummarizestheresults

thatarereflectedtorecommendationsforthecasecompanyfollowedbythefinalcon-

clusions.

12

2 TheoreticalFramework

Worldwide competition is growing rapidly, and in order to receive competitive ad-

vantagebusinessesshoulddevelopasuitablestrategy.Thetraditionalcompetitivestrat-

egiesarebasedondifferentiationbycostsorproducts (Martin,2015).Consequently,

companiesthathavegainedrecognizedcompetitiveadvantageintheirindustrieshave

succeededbydeliveringexceptionalcustomervalue(Treacy&Wiersema,1993).Treacy

andWiersema (1993) state that in order to succeed one of the following disciplines

shouldbefollowed:operationalexcellence,customerintimacyorproductleadership.

Inthiscontext,operationalexcellencemeansprovidingreliablegoodswithcompetitive

pricingandwithnoinconveniencewhereas,customerintimacymeanstargetingthemar-

ketsandprovidingtailoredsolutionstomatchthecustomerneeds(Treacy&Wiersema,

1993).Companiesthatsucceedinmatchingcustomerneeds,havegoodmarketintelli-

gence and operational flexibility to rapidly respond to the market needs (Treacy &

Wiersema,1993).Leadinginproductleadershipmeanspossessingaproductwiththe

bestcharacteristicswhichinturnattractscustomerstousethatproductandanyother

productsthecompanyproduces(Treacy&Wiersema,1993).Consequently,suchorgan-

izationstendtohavesolidcustomerloyalty.AstheO2Cprocessisthemostvisibleto

customer,focusingonprovidingvalueforthecustomerisakeyactivitytokeepinmind

inordertomaintaincustomersatisfactionandloyalty.

Thecasecompany(2020)hascreatedaCommercialExcellenceManagementSystemin

ordertotrackandmanagecommongoalsandinterestsofallbusinessactions. Inthe

casecompany,commercialexcellence iscarriedoutby focusingoncustomersandby

optimizingtheoperations.AspresentedinFigure1,thecommercialexcellenceactivities

aredividedintothefollowingcategories:“CreateMarketsandManageCustomers”,“Op-

timizeSupplyChain”and“DeliverandFulfillCustomerPromise”.

13

Figure1.Casecompany’sCommercialExcellenceManagementSystem(CaseCompany,2020).

Thepurposeofthetoplevelphase“CreateMarketsandManageCustomers”istocreate

amarkettoprospectfollowingwithanimplementationofprospecttoorderactivities

(CaseCompany,2020).Creatingamarkettoprospectisbuildingacompetitivemarket-

placeallowingtofindthepotentialcustomers.Thus,prospecttoorderhandlesforecast-

ing demand, developing sales and supply plans,managing key accounts, negotiating

seller/buyercontractsandmanagingsuppliers.

Themeaningofthesecondlevel“OptimizeSupplyChain”includesthecommercialex-

cellenceactivitiesbuiltonplanningandoptimizingtheoperations(CaseCompany,2020).

Theseactivities includesustainabilityandcompliance,schedulingsupplychainopera-

tions,managingsupplychainperformance,managinginventoriesandpricerisks.

Onthethird level,“DeliverandFulfillCustomerPromise”, theteammembersensure

thatcustomerpromisesaredeliveredandfulfilled,onbothsupplytopayandorderto

cashprocesses(CaseCompany,2020).“SupplytoPay”operationsmakesurethatthe

orderisexecuted,logisticsisplannedandloading,transportationandunloadingofthe

MarkettoProspect Prospect toOrder

PlanandOptimize Operations

SupplytoPay OrdertoCash

CreateMarketsandManageCustomers

OptimizeSupplyChain

DeliverandFulfillCustomerPromise

14

productareexecuted.Consequently,theO2Cprocessmanagesandexecutessalesor-

dersanddeals,organizeslogisticsaswellasmakessurethatloading,transportationand

unloadingareexecuted.

2.1 Order-to-Cash

ManagingtheO2Cprocessisrelevantforanorganization’ssuccess(Shapiro,Rangan&

Sviokla2004).Byanalyzingtheordermanagementprocess,managersareabletounder-

stand the process performance and the customer perspective in order processing

(Shapiro,Rangan&Sviokla2004).Theorderprocessingisperformedbycriticalpeople

workingwithjointefforttofulfillthecustomerorder(Shapiro,Rangan&Sviokla2004).

TheO2Cprocessisthehandlingofacustomerorderanditincludestheactivitiesstarting

fromordertothestageoffinallyreceivingthemoneyfromthesale(Parravicini,2015).

Parravicini(2015)statesthattheO2Cprocess’skeyfeaturesaretocollectcustomeror-

ders,deliverthegoodstocustomer’sdesiredplaceontimeandfinallytoreceivethe

paymentfromthecustomer. Inadditiontodeliveringthegoods,thequalityofgoods

mustbeupasagreedandtherelevantdeliverydocumentationmustbeprovided.The

O2Cprocesshasastronglinktothecompany’sreputationandcustomerrelationshipas

errorsaffectcustomersatisfactionlevelsdirectly(Parravicini,2015).Themoreimproved

and the optimized theO2Cprocess is, themore time therewill be available for the

seller’sactivitiestoacquirenewsales.

TheO2Cprocesshasaclearcycleconsistingofseveralkeyactivities:

- preparation,

- customerorderanditsimplementation,

- deliveryofthegoods,

- invoicingthecustomerand

- gettingthepaymentoftheorder(Parravicini,2015).

15

Thepreparationactivitiesensurethatcustomerdatasetsarecorrectlyenteredintothe

systems,thegoodsareavailableandthepricingiscorrect(Parravicini,2015).Onceall

thenecessaryinformationhasbeensetinthedatabaseandERPsystems,thesellerre-

ceivesthecustomerorder.Priortoconfirmingthecustomerorder,theavailabilityofthe

goodsandcustomercreditmustbechecked.Finally,wheneverythinghasbeenputin

placethesalesteamconfirmstheordertothecustomerandsetsuptheoutboundde-

liverytotheERPsysteminordertobookatransportmodeandtime.IntheERPsystem

thesalesteam,logisticsandthesupplychainplannersplanthecargomovements.

Oncetheupcomingdeliveryhasbeenfinalized,theorderfulfillmentactivitiesincludes

theorder picking, loading, transporting anddischarging to the customer (Parravicini,

2015).Throughoutthewholeorderfulfillmentprocesstheactivitiesoftransportation

shallbedocumented(e.g.BillofLading,loadinganddischargereports,inspectoranalysis

onqualityofgood).Theactofdeliveringthegoodsinitiatestheactualtransportationof

thegoodsmakingsurethattheproductisinthecorrectquantityandqualityandinad-

dition,attimeagreed.Iferrorsoccurduringthetransportation,theyneedtobenoted

anddocumented.Afterthedelivery,theinvoicewillbesenttothecustomeraccording

totheagreedbillingtypeandterms.Basedonthebillingtype,theinvoicewillbecreated

andsenttothecustomer.Afterhandlingthepossibledeliveryreturnsthepaymentfrom

thecustomerfinalizestheactivity.Ifthepaymentisreceivedontime,theO2Cprocess

iscomplete. If forsomereasonthepayment isoutstandingorapartialpayment, the

customerwillbesentareminder.Incasethecustomerrefusestopay,themostextreme

formistoblockdeliveriesandtakelegalactions.

IftheO2Cprocessisefficientandtheactivitiesoftheprocesshavebeenaccomplished

correctly,providinggoodcustomerservicewillbeacompetitiveadvantageforthecom-

pany(Parravicini,2015).ToensurethattheO2Cprocessisperforminginthebestway

possible,itiscrucialtomakesurethatinthepreparationstageoftheprocesseverything

isavailableinthedatabaseandtheERPsystemcorrectlyinordertoavoidmistakes.In

additiontohavingastrongperformanceoftheseactions,Parravicini(2015)highlights

16

thathavingaclearcustomercommunicationisimportant.Moreover,anyerrorsinthe

processshouldleadtocorrectiveactions.Astrongrelationshipwithcustomerswhoreg-

ularlyprovidefeedbackoftheorganization’sactionscanalsoleadtoO2Cimprovements.

InordertoimprovetheO2Cprocess,allteammembersmustbecommittedtopartici-

pateintheprocess(salesteam,customercare,pricing,masterdata,logistics,etc.)(Par-

ravicini,2015).Theremightbemanyactionsindifferentteamsthatcouldbeimproved

tomakethewholeprocessperformbetter.

2.1.1 WhyisO2Cimportant?

Shapiro,RanganandSviokla(2004)statethattheO2Cprocessisthemostvisibleprocess

tothecustomerandthereforetheordermanagement isvital.Everyordercanbere-

ferredtoasacustomer,andtheirmanagementisthewaythecustomeristreated(e.g.

anuncaredorderisanuncaredcustomer).TheO2Cprocessconsistsofmultiplephases

andorderprocessorswhicharethecriticalpeoplemanagingtheorder(Shapiroetal.,

2004). By tracking anorderphasebyphase, theO2Cprocesswill revealwhat effect

changes have on the customer. Consequently, by analyzing and improving the order

managementprocess,organizationscancreateacompetitiveadvantage.

AsanO2Cprocessrequirescooperationacrossdifferentteamstheretendstobeinter-

activeandpossiblyevenoverlappingactivities(Shapiroetal.,2004).Thus,itiscriticalto

makesurethatthecustomerishandledthroughouttheprocesswithhighqualityand

customerservice. Itcannot justbeeachprocessperformerfocusingontheirownre-

sponsibility.Thecoreofawell-functioningO2Cprocessistofillorderseffectivelyandto

matchcustomerexpectations(Shapiroetal.,2004).Inaddition,awell-functioningpro-

cessminimizesinternalconflictsandoverlappingwork,aswellasincreasesthefinancial

performancebyincreasingsalesandreducingwaste.Toensurethattheprocessiswell-

functioning,suitableprocessperformancemetricsneedtobealignedasthesemetrics

willrevealiftheprocessisoperatingasdesired(Shapiroetal.,2004).

17

2.1.2 Deliveryincoterms

InternationalChamberofCommerce’sIncotermsaregloballyagreedtermsforthesale

ofgoods(ICC,2020a).Thedelivery incotermrulesareincludedinsalescontractsand

followedbyimporters,exporters,transportersandinsurers.TheCIFincotermrepresents

Cost,InsuranceandFreight(ICC,2020a).TheCIFincotermisappliedforseaandinland

transportation.InImage1,ithasbeenshowntowhatdegreetheCIFincotermworksin

practiceasthecargodeliverymovesfromthesellertothebuyer.

Image1.TheCIFIncoterm(Bansar,2020).

UnderCIFincoterms,thesellerhastopayforthecarriageandarrangethetransportation

(ICC,2020b).However,thesellerisnotresponsiblefortheriskoflossordamageofgoods

oranyadditionalcostduetoeventsoccurringaftertheshipment(ICC,2020b).Inaddi-

tion,thesellerisobligedtohaveinsurancewhichhasminimumcoverage(ICC,2020b).

TheCIFincotermisonescopeofthisstudyasitwasthemostcommondeliveryincoterm

ofthedataset.

18

2.2 BusinessProcessManagement

Businessprocessmanagement(BPM)enablesprocessestobeexecutedandchangedon

thespotinordertomatchtheneedsofthemarket(Ould,2005).Oneofthekeyactivities

ofBPMistomanageprocessesinawayinwhichtheycanbemonitoredandcontrolled

whilerunninganddistributingthroughouttheorganization(Ould,2005).Thecoreidea

ofBPMistooptimizethebusinessprocessthroughoutitslifespaninordertoincrease

profitability(Khan,2004).Toachievethiscommongoal,businessprocessmanagement

requiresthecontributionofallparticipantsandanunderstandingofthebusinessand

organizationofthecompany(Ould,2005).Abusinessprocesscanbe,forinstance,an

orderoranysystematicprocessperformedbythejointeffortofdifferentteams(Khan,

2004).

Khan(2014)statesthatabusinessprocessshouldfunctionwelltobeprofitableanda

welloperatingbusinessprocessisusuallymeasuredbythespeedofresponseandthe

clarityofdecisionmaking.Toensuretheflowofgoodsandinformation,abusinesspro-

cessshouldbeamonitoredsequenceofactivities,alongwithamutualunderstanding

ofrolesandresponsibilitiesofpeopleandsystems(Khan,2004).Glykas(2013)states

thatbusinessprocessmodelingisonekeyactivityofBPM.Businessprocessmodeling

takesintoaccountvariousperspectivessuchasthebehavioral,organizational,functional,

goal-oriented and object-oriented factors (Khan, 2004). The different perspectives of

businessprocessmodelingidentifyandanalyzethecurrentstateoftheprocessesand

indicatesthewaytheyshouldbeoperated.Zabjek,KovacicandStemberger(2009)argue

thatBPMshouldbeavitalelementwhilemanagingbusinesschange.

2.2.1 BusinessProcessImprovement

Hammer(2007)arguesthatacommonbusinessprocessimprovementapproachisrede-

signing.Byredesigningorganizationshaveachievedimprovedperformance,increased

customervalueandincreasedprofitsforshareholders.Theseimprovementsofquality,

19

cost,agilityandprofitabilitywereachievedbyanalyzingandmeasuringinternalandex-

ternalcustomerprocesses.Inadditiontoredesigningandarrangingwork,businesspro-

cessimprovementrequiresredefiningrolesandresponsibilities,trainingpersonnel,en-

hancing organizational culture and improving information flow to enable cross-func-

tionalprocessesbetweendifferentdepartments(Hammer,2007).

Awell-functioningbusinessprocessespossesstwocharacteristics:processenablersand

organizationwidecapabilities(Hammer,2007).Theprocessenablersdefinethedegree

ofeffectivenessoftheprocessfunctions.Theenablersaredistinguishedbythescopeof

theredesigning,competencesofpersonneloperatingtheprocessandthemetricsby

whichtheprocessperformanceismeasured.Tobeabletoputtheseprocessenablersin

place,organizationsneedimportantcapabilities.Thesearemanagerialsupportandem-

ployee’swhovaluecustomersandcooperation.Theemployeesalsohavecompetences

ofredesigningprocessesandproblemsolving.Betterprocessperformanceisachieved

bygoodprocessenablersandorganizationalcapabilities(Hammer,2007).

DavenportandSpanyi(2019)claimthattherearetwomainchallengeswhenimproving

abusinessprocess.Firstly,acrucialactivityistoanalyzethecurrentstateoftheprocess

andunderstandwhereperformanceproblemsarise.Thedegreeofvariationisanim-

portantparametertounderstandwhytheprocessisnotperforminginacertainway.In

addition,asignificantchallengeisthattheERPsystemsandbusinessprocessesrequire

integratedconnectionsbetweeneachother.Forexample(1),theSAPsystemisprocess-

orientedthatsupportstheO2Cprocessbutdoesnotrevealthewayinformationflow

runsintheprocess.Inordertounderstandthesystemprocess,differenttechnologies

(e.g.Microsoft’sVisioorSoftwareAG’sAris)areusedtosupporttheunderstandingof

theprocessdesign(Davenport&Spanyi,2019).

Inordertobettercomprehendtheprocessperformanceaprocessminingsoftware,such

asCelonis,canbeputintoservice(Davenport&Spanyi,2019).Celonisprovidesdetailed

information from SAP transactions to reveal the process performance (Davenport &

20

Spanyi,2019).Itgenerateseventactionsforeachphaseoftheprocessidentifyingthe

personperformingtheactivity,thedurationoftheactivityandthevariationoftheac-

tivities.Celonisalsoenablesthedefiningofkeyperformanceindicators.Processmining

providesadata-basedviewofprocessperformancewhichenablesmanagementtorec-

ognizeperformanceproblemsandtomakedecisionsbasedonthedata(Davenport&

Spanyi,2019).

2.2.2 Processowners

Theredesigningprocessandprocessmanagementhascreatedanewaspectforprocess

enterprises,whereoperationalexcellenceiscrucial(Hammer&Stanton,1999).Inapro-

cessenterprise,thecontrolisseparatedfromthemanagementleveltothepeopleper-

formingthework.Inaprocessenterprise,aprocessownerishiredforacertainprocess

toensurethattheprocessimprovementisimplementedacrossallfunctions.Aprocess

ownerisresponsibleandauthorizedtodesignandtodevelopthecurrentprocess,to

measure itsperformanceand toensure thatall the individuals involvedhave the re-

quiredtraining(Hammer&Stanton,1999).Inaddition,processownersshouldunder-

standthewaythecustomervaluesthecompanyandtheirservices.Thus,theymustbe

certainthatthekeyprocessesarecontinuouslycreatingcompetitiveadvantageforthe

company(Power,2011a).Power(2011a)arguesthatbymakingsuretherelevantmetrics

measuretheprocessperformance,themorevalueitprovidesforthetopmanagement

onhowthebusinessisperforming.

As the changingmarket and business environment requires the business process to

changetoo.Theroleoftheprocessownerisimportantinguidingthedevelopmentof

theprocess(Hammer&Stanton,1999).Consequently,aprocessowner’sroleshouldbe

permanentandintegratedtoperformancemanagement(Power,2011b).Astheprocess

ownerisresponsibleforthewholeprocessimprovementandchangemanagement,they

arealsoresponsiblefortakingactionwhentheprocessperformanceisnotdesired.By

21

involvingtheprocessownerinmanagementlevelmeetings(e.g.budgeting,monthlyre-

porting), itcanprovideorganizationalandbusinesswiseunderstandingoftheprocess

performance(Power,2011b).Finally,agoodprocessownerpossessesleadershipskills

andencouragescooperationacrossdifferentteams(Power,2011b).

2.2.3 BusinessProcessLeadershipatthecasecompany

Operationalexcellenceisakeydriverinthecasecompany’sactionsandprocesses(Case

Company,2020).Inordertoenableoperationalexcellenceactivities,thecasecompany

focusesonfourkeyactivities:“focus”,“speed”,“simplicity”and“discipline”.“Focus”re-

ferstoidentifyingandprioritizingactionsthathavethehighestbusinessimpactandsup-

portthestrategicpriorities.“Speed”referstothewaste-freeprocessesthatcreatecus-

tomervaluealongwith“simplicity”ofactions thatminimize impactsandcomplexity.

“Discipline”referstorelevantkeyperformancemetricsthatsupportthestrategicobjec-

tivesoftheorganization.Thesecoreactivitiespursueoperationalexcellenceintheor-

ganization.

Inpractice,operationalexcellencemeansunifiedwaysofworking,comprehensiveedu-

cationanddocumentationoffunctions(CaseCompany,2020).Thecoreprocesses,func-

tionsandsystemsaredescribedindetailtoguaranteethatthecorrectprocessphases

andprotocolarefollowed.Byunifiedwaysofworkingandcomprehensiveknowledgeof

operations,thepurposeofoperationalexcellenceistoensurehighqualityandefficient

activitiesinthedeliveriesofgoods.

For2020,thecasecompanyhasdefinedsomekeyactivitiesinordertohavecleartargets

forthedevelopmentprocesses(CaseCompany,2020).Sofar,hiringaprocessownerfor

theO2Cprocesshasbeendone.Themaintasksoftheprocessownerare(a)participat-

ingintheoverallaccountabilityofEnd-to-End(allstagesofaprocess)processesand(b)

leadingprocessrelatedactivities.Theresponsibilitiesofaprocessownerarecarrying

22

outmanagementreportingaswellascreatingandmonitoringprocessperformancemet-

rics.Thus,oneofthekeytargetsistoimplementareal-timeprocessperformancemetric

fortheO2Cprocessbytheendoftheyear.

2.3 KeyPerformanceIndicatorsandmetrics

Measuringperformanceisanimportantfactorinmotivatingandguidingteammembers’

actionsthatsupporttheorganizationalgoals(Trent,2008).Usually,thechosenperfor-

mancemetricsindicatethekeyactivitieswhichareseenimportantfortheorganization.

Consequently,thosemetricsaredefinedasthekeyperformanceindicators(KPI’s).AKPI

couldbe,forexample(2),accomplishingtaskswithouterrors(Trent,2008).Inaddition,

performancemetricsshowcaseprocessareas inwhich improvingactionsareneeded.

Performancemetricsallowsmanagerstoobjectivelymakedecisionsbasedonthedata

andtocreatetargetmetricsforcontinualimprovement(Trent,2008).

Performancemeasurementstendtoformaroundfourdifferentaspects(Trent,2008).

Thefirstaspectisdecidingontheparameterthemeasurementwillconcern,forexample

(3) leadtime,qualityorcustomersatisfaction.Thesecondaspect is theperformance

targetwhichmightberatherexternalthaninternal.Thethirdcomponentistheaware-

nessoftheactualperformancelevel.ThisinformationshouldflowfromtheERPsystems

database.Lastly,itisimportanttocreateanimprovementplanthatdefinesthewaythe

commontargetwillbereachedonbothanindividualandteamlevel.

MeasuringperformanceandcreatinggoodandtransparentmetricsandKPIsshouldbe

alignedwiththeleanobjectives(Trent,2008).Goodmetricshavetobeinaccordance

withthecorporatestrategyandmission.Additionally,asmanagersmakedecisionsbased

on theprocessperformance theybenefitof figurespresenting financialperformance

(Trent,2008).Thesefiguresshowtheincreaseinreturnonassets(ROA)orcashflow.

Goodperformancemetricsenhancethecross-functionalcooperationintheorganization

23

andprovidedatathatistransparentandvisibletoeveryone(Trent,2008).Asthemeas-

urements relate to the customer requirements and organizational goals, the targets

shouldbereassessedandadapted fromtimeto timetoensure thealignmentof the

actualandtargetedperformance.

Asalesstrategycanbereflectedinthecorporatestrategyandmission(Parravicini,2015).

Thesalesstrategyandperformanceneedstobemeasurabletobeabletomonitorde-

velopment(Parravicini,2015).Tomeasuresalesactivities,therightKPI’sshouldbese-

lectedtosettargetsfortheteam.ThechosenKPI’sshouldenhancetheprocess,mission

andcontinuousimprovementofthecompany.Forexample(4),thechosenKPI’scould

berelatedtofinancialperformance(e.g.turnover),goodcustomerservice(e.g.grading

theexperiencefrom1-10),perfectorderrateandgoodbusinessplanning(Parravicini,

2015).ThechallengeforsettinggoodKPI’s is to findrelevantmeasuresandawayto

measurethem(Parravicini,2015).

Trent(2008)suggeststhatsomepossibleperformancemeasurementscouldbeasfol-

lows:

- theperfectcustomerorderrate,

- orderfillrates,

- unplannedbackorders,

- order-to-cashcycletime,

- conformancetodeliverydates,

- traveldistancesanddistributionqualityand

- costindicators.

ThesemeasurementsaredefinedinTable1.

24

Table1.Processperformancemeasurements(Trent,2008).

MEASURES COMMENTS

Perfectcustomerorderrate The % of orders shipped to customerswithouterrors.

Orderfillrates Rateofunfilledordersduetolackofstock.Thesecreatewaste,costsandlossofsales.

Unplannedbackorders Orderswithnophysicalstockwhichaffectcostsandcustomerservice.

Order-to-cashcycletime Acommonmeasureusedtoestimatethecooperationofdifferentteams.

Conformancetocustomer-drivendeliverydates

Measurestheon-timedeliveryatthecus-tomer’slocation.

Averagedistancetravelledbetweeninter-nalmaterialmovements

Reveals a major source of supply chainwaste.

Totalmilestraveled Animportantmeasureforcustomerdeliv-erynetworks.

Distributionqualityindicators Provides information of wrong goods,wrong quantities, missed deliveries anddamage.

Total distribution cost%of total productcosts/sales

Acommoncost-relatedmeasureforman-agement.

FromthemeasurementspresentedinTable1,themostrelevantperformancemetrics

fortheO2Cprocessare(a)theperfectcustomerrate,(b)thecycletimeoftheprocess,

(c)theorderfillrate,(d)theconformancetodeliverydatesand(e)thequalityandcost

indicators.Theseperformancemeasurementsprovidethemostcrucial informationin

accordancewiththeprocessperformance.

AstheO2Cprocessisusuallymeasuredbyefficiency,acommonsupplychainmetricfor

theperformanceistheperfectorderindex(POI)(Parravicini,2015).Theperfectorder

indexhasthreeperspectivesOT-IF-NIEasfollowing:

- theordertobedeliveredontime(OT),

- inthefullform(IF)and

25

- withnoinvoiceerrors(NIE)(Parravicini,2015).

Thenoinvoiceerrors(NIE)aspectcanbemeasuredbythepercentageofinvoicesthat

needmanualcollections(Parravicini,2015).Inadditiontotheseaspects,onecanalso

measurewhetherthegoodwasdeliveredwithoutanydamageandwiththecorrectdoc-

umentation(Parravicini,2015).Theimplementationoftouchlessorderactivitieshasen-

abledcorporationstostreamlinetheiroperationsanddecreaseanymanualworkand

rework(Parravicini,2015).Touchlessorderactivitiesareprocessphasesthatflowauto-

maticallywithoutanymanualworkafterbeingenteredintothesystem.

HallandJohnson(2009)statethatbusinessprocessestendtobestandardizedandcut

downtoclearroutines.Yet,notallprocessesarescientificnorcantheybemeasured

statistically,suchascustomersatisfactionandfeedback(Hall&Johnson,2009).Work

thatvariesandhasdivergenceareartisticprocesses(e.g.customerservice).Theyshould

beperformed inaccordancewith thechangingenvironmentandcustomerdemands.

Thesekindsofartisticprocessesenable innovativegoods thatcannotbecopied.The

combinationofstandardizedandartisticprocessescreatesstrongbusinessprocessper-

formance(Hall&Johnson,2009).Bothperformancemeasuresshouldbedetermined

andevaluatedaccordinglytotheprocess(Hall&Johnson,2009).

2.4 LeanSixSigma

LeanthinkingandmanagementisamethodfirstintroducedbytheJapanesecarindustry,

especiallyToyota(Oakland,2014).Theprincipleofleanthinkingistofocusontheoper-

ationalandquality featuresofprocessesand improvethem(Oakland,2014).Thecar

industriesimplementedleanmanufacturingbyreducingwasteandreassuringqualityin

everyoperationinproduction.OnekeymethodofleanistheJust-In-Time(JIT)method,

inwhichtheproductionmaterialsareorderedandreceivedjustwhentheyareneeded

intheprocess(Oakland,2014).TheJITmethodreduceswasteofcostandinventories.

26

Theconceptofleanisagileandcanbeimplementedtootherindustriessuchasinthe

serviceenvironment.

Plenert(2012)arguesthatleanmanagementconcentratesoncuttingdownonallactiv-

itiesthatarenotnecessarywhendeliveringaproductorservice,whilstmaintainingthe

quality,punctualityindeliveryandlowcostoftheproduct,tothecustomer.Thecore

activityofleanbusinessprocessmanagementistoidentifythevalueforthecustomer

andtoidentifythewasteofresources,costandtimeintheprocess(Plenert,2012).By

identifyingwaste,thebottlenecksoftheprocesscanberesolvedbyimprovingthepro-

cess.Aleanprocessshouldreacttotheinitiativefromthecustomer(e.g.asalesforecast

oracustomerorder)(Plenert,2012).Inordertosustainleanbusinessprocessmanage-

ment,astrategicplanthatsupportsthegoalsofthecompanyandaimsforcontinuous

improvementshouldbecreated(Plenert,2012).Byupdatingthisplan,managementis

abletodetermine,influenceandoverseestrategicareasofimprovement.

2.4.1 SixSigma

TheSixSigmamethodologywasformedaroundthequalityaspectofoperationsandthe

valueprovidedtothecustomer(Oakland,2014).Ascompetitivenessrises,businesses

needtofocusoncorrectactivitiesalongwithhighqualitymanagement(Oakland,2014).

ThemanufacturingindustrywasthefirsttointroduceSixSigmaasmaintainingahigh

standardofqualitywasacrucialelementforsurvival intheindustry(Oakland,2014).

Thiswasthestartingpointoftotalqualitymanagement(TQM).TosucceedinSixSigma,

qualitymanagementsystemshavetobeimplementedtoallsystems.Theadoptionof

qualitytoolsandmethodsalongwiththeimprovementandinvolvementoftheteam,

willresultinimprovedbusinessprocessperformanceandbetterbusinessplanning(Oak-

land,2014).LeanmethodologysystematicallyeliminateswasteandSixSigmadecreases

variationinactivities(Oakland,2014).Bycombiningthesetwo,LeanSixSigmaprovides

acontinuousimprovementapproachtoenhanceperformance.

27

TheSixSigmamodelconsistsoffivestepswhenitisusedasatooltoimproveperfor-

mance:Define,Measure,Analyze,ImproveandControl(DMAIC)(Oakland,2014).This

model can be implemented to Deming’s original continuous improvement Plan, Do,

CheckandActmodel(PDCA).ThePDCAmodelpresentsaframeworkforimprovingteam

members’ actionsandprocessperformance. ThePDCAcyclehelps teams to test im-

provement ideas and their solutions in a controlled scale before implementing it

throughouttheprocesses(Oakland,2014).Figure2.showsthePDCAcycleandDMAIC

improvementmodel(Kanbanize,2020).

Figure2.ThePDCAcycleandtheDMAICimprovementmodel(Kanbanize,2020).

The“Plan”phaseofthePDCAcyclecarriesoutacomprehensiveplanofactionsthat

needtobedoneinthescopeoftheproject(Kanbanize,2020).Thisstageanswers

questionsregardingtheresourcesneededandpossessedandthemainissuesneedto

besolved.Whentheplanisready,theplannedactionsareimplemented(the“Do”

phase).Aserrorsorunexpectedsituationsmayarise,itisimportanttoimplementthe

projectinacontrolledscaleandenvironment.Afterimplementingtheplan,theresults

arecheckedandanalyzed(the“Check”phase).Thisisthemostimportantstageinor-

dertoavoidmistakesinthefuturebycorrectingthembeforeimplementingthenew

processtothewholebusinessmodel.Onceeverythingistestedandcheckedandthe

Do

CheckAct

PlanDefine

Measure

Analyze

Improve

Control

28

outcomeisasdesired,theplancanbeputintopractice(the“Act”phase).ThePDCAcy-

cleisagreattoolforsolvingproblemsandtestingpossibleoutcomesasmanytimesas

needed(Kanbanize,2020).

Oakland(2014)arguesthatthePDCAcycleprovidesagreatframeworkfortheSixSigma

DMAICimprovementmodel.TheDMAICstep“Define”isthe“Plan”phase,“Measure”is

the“Do”phase,“Analyze”and“Improve”arethe“Check”phaseand“Control” isthe

“Act”phase.Inthe“Define”phaseoftheDMAICcycle,theresources,scopeandgoals

oftheprojectaredefined.Inthe“Measure”phase,theprocessperformanceisanalyzed

alongwithitsshort-andlong-termcapability.The“Analyze”phasefocusesonchecking

foranypossiblemistakesandtracingtherootcausesofanyarisingproblems.Further-

more,“Improve”phasefocusesonfindingsolutionstotheseproblemsinordertobe

abletoreachthedesiredoutcome.Finally,the“Control”phaseisaboutimplementing

theimprovedprocessintotheorganization.Inadditiontothisprocessimplementation,

it isstandardizedaccordingly tomeetthe ISO9000qualitystandardsofperformance

(Oakland,2014).Withallthesephasesimprovementmodelscanbeplannedtoanylevel

oforganization(Oakland,2014).

2.4.2 LeanOperations

Althoughleanmanagementisstronglydetectedinthemanufacturingindustryitcanbe

appliedtoallindustriesandservicemodels(Trent,2008).Aneffectivesupplychainhas

acontinuousflowofactionswhereeachsteprunssmoothlytoanotherwithoutanydis-

ruptions(Trent,2008).Ifdisruptionsorerrorsarise,theyaffectthecapacityandthrough-

puttimeofthewholecycle.Thismodelcanalsobeutilizedinaprocesscycle.Theactiv-

itiesofaprocessshouldbeorganizedasaclearstep-by-stepflowratethatmatchesthe

demandfromthecustomer(Trent,2008).Asupplychainthatreactstothecustomer’s

pulldemandoperatesbettersincenoproductionhappensunlessthecustomerforecasts

salesorrequestsanoffer(Trent,2008).

29

AsTrent(2008)suggests,akeyactivitytoleanoperationsistoidentifythethroughput

andleadtimesofoperationsandtofindsolutionstoreducetime.Inaddition,thepro-

cess layoutand informationflowshouldbetaken intoconsideration. It iscrucial that

informationflowsfromtheERPandsupportsystemseasilyfortheusersandthatthe

informationisaccurateandreliable(Trent,2008).

2.4.3 Leantoolsandapproaches

Toenhanceprocess improvementacrossorganizationand individuals, theemployees

should have knowledge and access to improvement supporting lean tools and ap-

proaches(Trent,2008).Themostcommonleantooliskaizen,whichtranslatestocon-

tinuous improvement (Trent, 2008). The main action of kaizen is to focus on small

changesintheprocess.Bydoinglittleimprovementsfromtimetotime,theimprove-

mentactionsarereviewedandaccessedcontinuouslyinordertoperformbetter.The

kaizenprocesshasthreesteps,thefirstofwhichistoanalyzeandpreparematerialfor

theactionsthatneedtobeimproved(Trent,2008).Afterpreparation,thekaizenevent

isperformedandtheactionplansaredecidedonwithin the team.To followup, the

improvementmodelistestedandcheckedtoseeifthechangesmadeworkedandcan

beimplementedpermanently.

Toolsrelatedtoprocessdesignarevaluestreammapping(VSM),processmappingand

theuseofaRACImatrix(Trent,2008).Valuestreammapping(VSM)wasfirstdeveloped

forToyotabyTaiichiOhno(Trent,2008).TheideaofVSMistohelpunderstandtheflow

ofmaterialorinformationbyvisualizingit(Rother&Shook,2009).VSMhelpstoidentify

wasteandthesourcescausingwaste(Rother&Shook,2009).VSMprovidesacoherent

frameworkandidentifiesareasofdevelopment(Trent,2008).SimilartoVSMisprocess

mapping and modeling which presents the process as a flowchart (Trent, 2008).

Flowchartsdefineactivitiesandtheirsequenceintheprocesswiththeuseofdifferent

symbolsandlineswhicharestandardizedtorepresentacertainaction.Thestandardized

30

symbolsfollowtheAmericanNationalStandardsInstitute(ANSI)symbolswhicharethe

mostrecognized.ThesesymbolsareshowninFigure3.

Figure3.TheANSIsymbols(Trent,2008).

Trent(2008)arguesthatitiscrucialfororganizationstobeabletomodelprocesses,to

identifywhatprocessestheydependonandwhatprocesseshavethemostpotentialfor

improvement.Processmappingoffersagoodframeworktoidentifythebusinessprocess

showingthepartsofitthatshouldbeimproved(Trent,2008).Processmappingcanalso

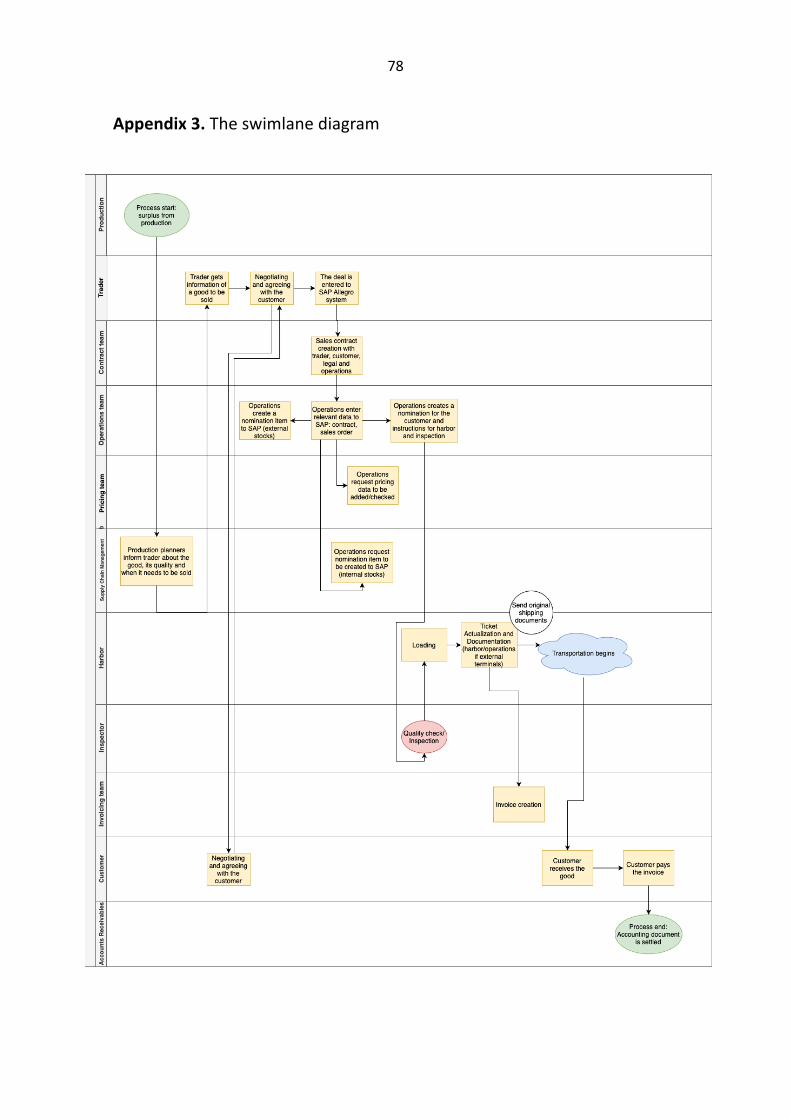

bedonewithaswimlanediagram.AswimlanediagrampresentsthesameVSMactivities

byinsertingtheprocessphasesinthecorrectdepartmentlanedefiningthepersonper-

formingtheprocess(Wedgwood,2016).ToclarifythescopeofprocessmappingaSIPOC

modelisagenerallyusedtooltoidentifythesuppliers,inputs,process,outputsandcus-

tomersoftheprocessonahigh-level(Taghizadegan,2013).ASIPOCmodelhelpsinclar-

ifying the key process actions andmeasures that provide value for the stakeholders

(Taghizadegan,2013).

Inaddition toVSMandprocessmapping,aRACImatrixalso reveals theprocessand

identifies the roles and responsibilities of individuals and teams (Trent, 2008). RACI

Operation

Transport Storage

Decision

Inspection/Approval Delay

31

standsforResponsible,Accountable,ConsultandInform.Responsibledefinestheper-

sonperformingtheactionandAccountabledescribesthepersonresponsibleforgetting

theworkdoneontime(CIToolkit,2020).TheConsultedpersonisamentorguidingthe

workwhilsttheInformedreferstothepersonwhoneedstheinformationonthedecision

sincetherestoftheworkdependsontheinformer’sactions(CIToolkit,2020).

Rootcauseanalysis(RCA)identifiesthecorereasoncausingproblemsandtriestofind

solutionsandapproachestosolvingit(Tableau,2020).Byanalyzingrootcausesandfind-

ing the right solutions,RCA tries to systematicallyprevent futureproblems. TheRCA

principlesfocusonthereasonsproblemsariseandithasseveraltechniques,fromwhich

themostcommonarecause-and-effectchartandthe5Whys(Tableau,2020).

Andersen(2007)statesthatthecause-and-effectchartisaclassictoolofTQMthatiden-

tifiesthepossiblecausestoaneffect.Thecause-and-effectchartcanbedisplayedasa

fishbonechartoraprocesschart(Andersen,2007).Thefishbonechartpresentsthemain

categoriesofpossiblecausessuchaspeople,processes,workenvironment,machines

andmethods.Themainissuesareidentifiedunderthemaincategoriesandattheend

ofthe‘fishbone’,istheproblemthatneedstobesolved.Thefishbonechartispresented

inFigure4.

32

Figure4.Fishbonechart(Andersen,2007).

Afishbonechartissimilartoaprocesschartexceptthattheprocesschartaimstoim-

provethebusinessprocessratherthanlookingforcauseandeffects(Andersen,2007).

Processchartsidentifyproblemsandlowperformancelevelsbyhighlightingthem(An-

dersen,2007).Aprocesschartcanbesimilartoafishbonechartbutitpresentsproblems

insteadofcauses.

The5Whysapproachfocusesonfindingdetailedandconciseresponsestoquestions

(Andersen,2007).Toconducta5Whysanalysis,aproblemthatneedssolvingmustfirst

bedetected(Andersen,2007).AnsweringthefirstWhy,identifiesacausefortheprob-

lem.TheanswerofthefirstWhycreatesanewquestionaslongasnonewanswersare

provided.Figure5presents5Whysanalysis.

Maincategory Maincategory

Maincategory Maincategory

Problemtobesolved(effect)

Cause Cause

Cause Cause

Cause Cause

Cause Cause

Cause Cause

Cause Cause

33

Figure5.The5Whysanalysis(Andersen,2007).

The5Whysapproachcanbecombinedwithcause-and-effectanalysistodiagnoseeach

factorandtodeterminetherootcauseforthatissue(Andersen,2007).Tofindthereal

root cause, it usually requires at least fivewhys (Andersen,2007).A SIPOCmodel, a

swimlanediagramandaVSMmatrixwillbeimplementedintheresultschaptertoana-

lyzethecurrentstateoftheprocessandtodefinethemostimportantareasofimprove-

ment.

Problem:Lowlevelofworkinprogress

Why?Maintainnostockoffinishedgoods.

Why?Shortmanufacturingtime.

Why?Runsmallbatches.

Why?Frequentdeliveriesfromsuppliers.

Why?Goodrelationshipswithcustomers.

34

3 Methodology

Thescopeofthisresearchwerespotsales(unplannedsurplusfromproduction),which

weredeliveredbyvesselandoperatedfromtheFinlandandEuropeofficewiththeuse

oftheCIFincotermswithinthetimeframeofMay2018toSeptember2019.Thisscope

waschosenbecausethemajorityofthedeliveriesaretransportedoverseasbyvessels

whichcancarrylargequantitiesatonce.Additionally,theCIFincotermswaschosensince

fromthesurplussalestheCIFsalesrepresented76%ofallspotvesseldeliveries.

Theresearchwasconductedasamixofquantitativeandqualitativemethodsinorder

togainamorecomprehensiveoverview.Basedonthedatacollectedthroughthedataset

and interviews, thereasons forcertainbottlenecksorerrorsoccurring in theprocess

couldbediscovered.Thequantitativeanalysiswasbasedondatareceivedfromthecase

company’sERPsystemduringthetimelineoftheresearch.Consequently,whateverthe

quantitativedatahighlightedasabottleneck,wasthenexaminedwithmethodsofqual-

itativeanalysis.Astheprocesswassplitintotrader’sactions,operator’saction,pricing

specialist,accountingspecialist’sactionsandharborspecialist’sactions,theinterviews

wereconductedseparatelywitheachdepartmentinvolvedintheprocess.Inadditionto

thequantitativeandqualitativedata,aVSMworkshopwasconducted,inwhichthecur-

rent state of the process was assessed and improvement areas were identified.

3.1 Quantitativedata

The quantitative dataset consisted of all data entered to the company’s ERP system

withinthetimeframeoftheproject.ThecasecompanyusesSAP,Allegroandaprocess

miningtoolcalledCelonis,whichvisualizestheirbusinessprocessesandperformance.

BylimitingthedatasettoallspotsalesdeliveredbyvesselwiththeCIFincoterms,the

datasetconsistedof249cases.Thetimerangeofthedatawasfromthe1stofApril2018

tothe30thofSeptember2019.

35

Theaimofthequantitativeresearchwastoanalyzethecurrentprocessflowandwhat

defectsarisefromthedata.Thedefectsandbottleneckswereanalyzedbyassessinglong

leadtimesandrepeatingactivitiesthatleadtoreworkoradditionalwork.Themainchal-

lengesfoundfromthedatawereassessed incloserdetailandbroughtupduringthe

interviews.

3.2 Qualitativeinterviews

Thequalitativepartofthestudywasconductedbyinterviewswiththespecialistsoper-

atingindifferentteamsandphasesoftheO2Cprocess.Theinterviewswereconducted

bydividingtheprocessintosixphasesandresponsibilities:traderresponsibilities,oper-

ationsspecialistresponsibilities,pricingspecialistresponsibilities,logisticsspecialistre-

sponsibilities,harborspecialistresponsibilitiesandinvoicingspecialistresponsibilities.

Fromeachprocessphase,betweenoneortwospecialistswereinterviewed.Theinter-

viewswereconductedinFinnishasitwasthenativelanguageofallinterviewees.The

interviewswereone-to-oneandtwo-to-oneaswellasconductedeitherfacetofaceor

byameetingcall.

Thereasonwhytheprocesswasdividedtosixdifferentphaseswasthataccordingtothe

quantitativedatathemajorbottlenecksareintheareaofpricingbillingblocks,logistics

ticketingandinvoicesthatneedcancelling.Theaimoftheinterviewswastofocuson

theseactivitiesandcomprehensivelyinvestigatetheeffectivenessoftheprocessindif-

ferentteams.

Theinterviewquestionsfocusedonidentifyingthebottlenecksoftheprocess.Further-

more,theyinvestigatedthecausesforthedefectsorreworkintheO2Cprocessinorder

tounderstandtheirimpactontheprocess.Theaimoftheinterviewquestionswasto

findexplanationsthatclarifythebottlenecksidentifiedinthedata.Thequestionnaire

wasthefollowingandtheyarealsoattachedtoAppendix1.:

36

- Whatarethechallenges(bottlenecksanddefects)ofthecurrentprocess?What

causesthese?

- Howarethedefectshandledandresolved?

- Arethereanyextrafeaturesorreworkthatincreaseoraffectyourworkload?

- Arethereanyactivitiesinyourjobthatrequireguidance/information/permis-

sion fromacolleaguebeforeyoucanget started? If yes,who/whomarecon-

tactedforfurtherinformation?

- Whatwouldyouchange/developinthecurrentprocess?

Theinterviewswereexecutedinanirregularordertogainasmuchinformationaspos-

sible.Theinterviewresultswereusedalongwiththequantitativedatatounderstand

thechallengesofthecurrentO2Cprocess.Moreover,theknowledgegatheredfromthe

quantitativeandqualitativestudyprovidedaviewpointfortheissuestobediscussedin

theVSMworkshop.

3.3 Workshop

Theworkshopconsistedofthecurrentprocessassessmentandanalysis.TheO2Cpro-

cesswasgonethroughfromstarttofinishbyvaluestreammappingalloftheactionsin

accordance to thescopeof the thesis.Thepeopleparticipating in theworkshophad

knowledgeoftheO2Cprocessasawholeandsomeparticipantswereexpertsinacer-

tainprocessarea(e.g.operationsspecialist).Theaimoftheworkshopwastomapall

activitiesoftheprocessfromtheviewpointofleadtimeandrework.Consequently,the

aimwastolocateissuesaffectinglongleadtimesandreworkaswellasdiscoveringareas

ofimprovementintheprocess.

37

Priortotheworkshop,thequalitativedatawasanalyzedalongwiththeinterviewresults

whichprovidedadditionalinformationfortheworkshop.Inordertomeasuretheactiv-

itiesandimprovementareasintheworkshopsomemetricswereneeded.Thechosen

metricsweretheleadtimeofactivitiesandinformationflow(doingthingsrightthefirst

timeandavoidingrework).

Sincetherewerevariousimprovementareas,onlythemostimportantoneswerehigh-

lightedandprioritized.Asthisworkshopfocusedonlyonthecurrentstateoftheprocess,

theimprovementareaswerechosenforafutureimplementationplanthatcanbeiniti-

atedoncethisthesishasbeenpublished.

38

4 Results

ThissectionreviewsthecurrentO2Cprocessmanagementinthecasecompanyandthe

resultsof thestudyconducted.Moreover, thequantitative,qualitativeandworkshop

resultsareassessedanddiscussed.Thequantitativeandqualitativedatafocusedonan-

alyzingthebottlenecksanddefectsoftheO2Cprocess.Consequently,theVSMwork-

shopwasconductedbasedonthetheoreticalframeworkandtheaimofthemethodwas

tomapthecurrentstateoftheprocessandtoshowcasetherootcausesoftheproblems.

Basedonthediscussionsomerecommendationsareprovidedforthecasecompany.

4.1 CurrentO2Cprocessmanagement

TheO2Cprocessmanagement inthecasecompanyfollowsthestepsaspresentedin

figure6(CaseCompany,2020):

1. Thetradernegotiatesasalewithacustomerandasalescontractisagreedon.

2. Thecontractteamformstheaforementionedsalescontractaccordingtothesale

agreed.Thetrader,thelegaldepartment,theoperationspecialistandthecus-

tomercommentonthecontractuntilitisacceptedbyallparties.

3. Oncethesaleisagreedon,thetraderinsertsthesaletotheAllegrosystemand

thecomplianceteamchecksthesales.

4. Whenthecompliancecheckisdone,theoperatorstartsworkingwiththesale

andaddsinformationtotheSAPsystem.Theoperatorcreatesacontractanda

salesorderforthedealandasksthelogisticsspecialisttocreateanominationfor

thedeal.

5. Oncethenominationiscreated,theoperatorchecksitandaddsadditionalinfor-

mationsuchasdemurragesandinspectorinformation.

6. Theoperationsspecialistinformsthepricingteamaboutthedealandthepricing.

Thentheyensurethatthepricingisinaccordancetothecontract.

7. WhenalldataiscorrectinSAP,theoperatorinformstheinternalandexternal

stakeholdersaboutthedeal.

39

8. Theoperationsspecialistcreatesanominationforthecustomerwhichconfirms

whatproduct(s)willbedelivered,inwhatquantity,whereandwhen.

9. Additionally,aninspectorisappointedtomakesurethequantityandqualityof

thegoodisasagreed.

10. Theoperation specialist creates instructions for loading relatedactivities. The

harboroperators’andthevesseloperators’areinformedabouttheproductto

bedelivered,howmuch,where,whenandtheinspectorsactions.Theseinstruc-

tionshavetobesentprior to loading inorder toassurethateveryoneknows

whattodo.

11. Oncethenominationsandinstructionsarecompleted,sentandconfirmed,the

salesorderisreadyforloading.

12. Loadingishandledbytheharborspecialistsandtheytakecareofthepaperwork,

practicalarrangementsandsupervisetheloadings.

13. Oncetheloadingisdone,theharborspecialistactualizesaticketintoSAPinform-

ingthatloadingiscomplete.

14. OncetheticketactualizationisenteredintoSAP,thesystemautomaticallycre-

atesactionssuchas“Createdeliveryitem”and“Postgoodsissue”toinformthat

theownershipof thegoodshasbeen transferredand thegoodsare released

fromtheinventory.

15. Theharborspecialistsendstheoriginalcargodocumentstotheoperationsspe-

cialist.

16. Dependingonthesale,theordermighthaveabillingblockinordertoavoidin-

correctinvoicessenttothecustomer.Dependingonthebillingblocktype,the

operationsspecialistandpricingspecialistcheckthatthepricing,quantities,and

dataarecorrectbeforereleasingthebillingblock.

17. Oncethebillingblockhasbeenreleasedtheorderisreadytobeinvoiced.The

invoiceiscreatedautomaticallyandsenttothecustomer.

18. Oncethecustomerpaystheinvoice,theaccountingdocumentismatchedand

clearedandtheO2Ccycleiscomplete.

40

O2Cprocessphases

Supplychain planners andshipping inform thetrader that acertain product needs tobe sold

inacertain window

Negotiating with the potential customer

Agreeingonthesales

NewcustomerinformationisenteredtotheMasterData

Compliancecheck

Salescontractcreationandcommentingbeforethefinalcontract

TraderinsertsthedealtoSAP

OperatorentersacontractandasalesordertoSAP

OperatoraskspricingtobeenteredtoSAPandnominationtobecreated

Operatorchecksthenomination

Operatorcreatesanominationforthecustomerandinstructstheharbor,vessel

operatorsandinspectionclerks

Loadinginharborsupervisedbytheharborspecialist

TheharborspecialistcreatesatickettoSAP,whichindicatestheloadedquantity,datean

time.

Theownershipoftheproducttransferstothebuyer,aninvoiceiscreatedautomaticallyand

senttocustomer

Theinvoiceissettledandtheaccountingdocumentiscleared.

Figure6.TheO2CprocessphasesandtheflowofactionsintheSAPsystem(AdaptedfromCaseCompany,2020).

Figure6presentstheO2CprocessphasesandtheflowofactionsintheSAPsystem.In

additiontothesystemsteps,otherpartsoftheprocessare;salenegotiationsbetween

thetraderandcustomer,additionofpossiblenewcustomerinformationintotheMaster

Datasystem,compliancechecks,contractcreationandinstructingtheloadingactivities

O2Cprocess intheSAPsystem

Create trade position

Create contract item

Releasecontract

Create sales order item

Create nomination item

Confirm nomination item

Actual loading

Actualize ticket

Create delivery item

Postgoods issue

Releasebilling block

Create invoice item

Clear accounting document

41

arepartof theprocess.Table2presents theO2Cprocessperformersandtheirmain

responsibilitiesinmoredetail.

Table2.TheO2Cprocessperformersandtheirresponsibilities(Adaptedfrompersonalcom-municationswithinterviewees,February,2020).

Team/Individualperformingtheprocess Mainresponsibilities

Trader Receives information about product surplusand when it could be delivered. Cooperateswith the supply chain planners and shippingdepartment. Based on that information, thetradernegotiatesthesalewiththecustomer.

Compliance Monitorsoperationalandfinancialrisk,makessurethelegalregulationsarefollowed.

Contractteam Createsacontractandsendsitforcommentsfromthetrader,legaldepartment,operationsspecialistandcustomer.

Operationsspecialist An operations specialist is a connection be-tween theexternaland internal stakeholdersand ensures that the sale is carried out asplanned. The operations specialist should beawareofalltheactivitiesthroughoutthepro-cess.TheoperationsspecialistentersdataintoSAPandinstructsthestakeholdersonhowtooperatewiththesales.

Pricingteam Enter the pricing data into SAP, monitor thepricesonsalesandmakesuretheyarefulfilled.

Logistics/SupplyChainManagement Creates the nomination item into SAP andplansthecargomovements.

Harbor Takescareof thepracticalarrangementsandpaperwork in the harbor. Daily planning andmonitoring of the loadings. Creates a ticketintoSAP,which includes the loadedquantity,dateandtime,aftertheloadingisdone.

Invoicing Managesdailyinvoicingactivities,conductserrorinvestigations,handlescancellationsandre-invoicing,takescareofcheckingin-voicedetailsandmanagesaccuratefiling.

AccountsReceivables Checksthat the invoice ispaid,matches it totheinvoiceitemandclearsthedocument.

42

TheO2Cprocesshasaclearstep-by-stepdesignthatallcasesshouldfollow.However,

thedesignisnotalwaysclearandreworkorerrorsoccurintheprocess.Forexample

(5),commonerrorsthatthecasecompanyfacesareerrorsindata.Errorsindatacan

causemisunderstandingsintheharborandtheloadingmightnotgoasplannedorin-

correctinvoicesaresentthatneedtobecancelled.Figure7presentsanexampleofa

casewhereavarietyofO2Cprocessproblemscanbeseen.

43

Figure7.AnexampleoftheO2Cprocess(CaseCompany,2020).

Thisexampleshowcasesseveralareasinwhichreworkoccurs.Oncetheloadingactivity

iscomplete,theactualizedtickethasinadequatedataanditneedstobereversedand

Createtradeposition

Createcontractitem

Releasecontract

Createsalesorderitem

Createnominationitem

Confirmnominationitem

Actualloading

Actualizeticket

Reverse ticket

Actualizeticket

Createdeliveryitem

Postgoodsissue

Releasebillingblock

Createpreliminaryinvoiceitem

Createaccountingdocument

Createdifferentialinvoiceitem

Updatebillingblock

Cancelinvoiceitem

Releasebillingblock

Createdifferentiallinvoiceitem

Clearaccountingdocument

44

actualizedagain.Afterthepreliminaryinvoiceisgeneratedandcleared,thedifferential

invoiceisgeneratedandthebillingblockisupdated.However,thereisstillinadequate

dataasthedifferentialinvoiceiscancelled.Laterthebillingblockisreleasedandanew

differentialinvoiceisgeneratedandfinallycleared.Inthiscase,reworkwaspresented

inticketactualization,billingblockupdating,cancelinginvoicesandre-invoicingactivi-

ties.

4.2 Quantitativeresults

Thedatasetconsistsof249salescases.Thesecasesinclude30differentcustomersand

38differentproductstransportedto71differentlocations.Fromthe30customers,the

majorityof thedeliveries,withall coveringover10%of thedeliveries,wasbetween

threecustomersby22%,11%and10%.Fromalloftheproductstherewerethreemain

producttypeswhichconstitutedthemajorityofdeliverieswith19%,12%and8%ofthe

totalrespectively.Fromallofthelocationsthemajorityofdeliverieshavebeendelivered

totheARAregion(Amsterdam-Rotterdam-Antwerpen)andtheBalticSeaarea.These

locationswerethebusiestduringthetimeperiod.

Thedatasetrevealsthatareasofreworkandextraactivitieswerethefollowing:

1. manualfieldchangestosalesorders,

2. cancelledinvoicesdebitedbycreditinvoices,

3. releasingandupdatingthebillingblockand

4. reverseticketing.

Thefollowingfigureswillshowtheseactionsinmoredetail.

Activitycount

Figure8showstheactivitycountofeachprocessphasewithinthe249cases.Figure8

showsthedifferentactivitiesonthex-axisandtheamountoftheactivitiesmadeonthe

y-axis. The letters in the brackets refer to possible preliminary or differential invoice

items.

45

Figure8.Activitycountofeachprocessphase(CaseCompany,2020).

Thefigurerevealsthatthebillingblockwasreleased412times,meaningthatthereare

lotsofcaseswherethebillingblockwasreleasedmorethanonce.Itcanbeconcluded

thatreleasingbillingblock,clearingaccountingdocumentandactualizingticketwerethe

mostfrequentactivities.Figure9statestheamountofactivitiesdoneinaccordanceto

salesordersmadethatmonth.

46

Figure9.Activitycountinaccordancetosalesorderspermonth(CaseCompany,2020).

InSeptember2019,therewere20salesordersdoneand442activitieswereexecuted

forthem.Theactivitiescountedincludedallthedifferentcategories(e.g.createsales

order,createnominationitem)andthenumberoftimesitwasperformed.Asthenormal

systemprocessflowhas13activities(Figure6),20salesorder itemswouldhave260

activities(20salesordersx13activities=260activitiesalltogether).Itcanbeseenthat

comparingthe260activitiesto442activities,thereare182additionalactivities.

Changesmadetothesalesorderitems

Thedatasetrevealsthatinmostcasesthedataisnotinitiallycorrectorreliablewhenit

is inserted into the systems. Figures 10 and 11 show statistics on the manual field

changesmadetothesalesorders.Achangewascountedwheneveramodificationwas

madeandsavedtothesalesorder.Intotal,3000changesweremadeinthe249cases

analyzed.Anaveragemanualchangeforonesalesorderwas12changes.Figure10de-

scribestheamountofchangesinsalesorderswithinthelimitsprovided.

47

Figure10.Manualchangecountoccurrences(CaseCompany,2020).

Forthemajorityofthecases,salesorderswerechangedbetween1-16times.Only23

salesordershad1-4changesmade,and60salesorderswerechanged7-10times.How-

ever,somechangesarenecessaryandneedtobemade.Forexample(6),thepriceneeds

tobeupdatedinthesystemoncetheoperationsspecialisthascreatedthecontractand

salesorder.Thus,thatcountsasamanualfieldchange.Figure11statesmonthlythe

amountofmanualchangesdonetothesalesorders.

48

Figure11.Amountofmanualfieldchangesinaccordancetothesalesorderamount(CaseCompany,2020).

Figure11showcasesthecountofsalesordersontheleftaxisandthecountofmanual

fieldchangesontherightaxis.Asthemanualfieldchangecurveshows,allsalesorders

arechanged.DuringNovember2018,December2018andSeptember2019thechange

countwasthehighest.Figure12showsthetrendofmanualfieldchangespersalesor-

ders.

49

Figure12.Manualchangesmadepersalesorder(CaseCompany,2020).

AccordingtoFigure12,inSeptember2019,onaverage15.45manualchangesweredone

peronesalescase.ThemanualfieldchangecurvesinFigure11andFigure12clearly

showthat in thosetimeperiodswhentherehavebeena lotofmanualchanges, the

businessmodelhaschangedbyexpandedoperations.Accordingtothecasecompany

(2020),inOctober2018theoperationswereunifiedwithEurope’sofficeoperationsby

creatingamutualprocessaltogether,exceptthatoperationsspecialistsarestillseparate

inbothlocations:inFinlandandinEurope.StartingfromOctober2019,anewproduct

categoryoperationwasalsounifiedandtherisingamountofchangesreflectsthechange

whichoccurredinthebusinessmodel.

Billingblockrates

Accordingtothedata,thebillingblockrateinallofthecaseswas97%meaningthat

only3%ofthecasesdidnothaveabillingblock.Thefollowingfigurespresentbilling

blockratesandcounts.ThebillingblockrateofallthecasesisshowninFigure13,the

ratewasunder100%forafewmonths,only.

50

Figure13.Billingblockrate(CaseCompany,2020).

AsFigure13shows,thebillingblockratewasunder100%inSeptember2018,October

2018,November2018,January2019,March2019andSeptember2019.Thenextfigure

showsthenumberofthebillingblockactivitiesdoneonaverageeachmonth.For in-

stance, inApril2018therewasonesalesorderanditsbillingblockwasupdatedfour

times.Onaveragetherewere2.8billingblockupdatesmadeperonesalesorder.

51

Figure14.Averagebillingblockcount(CaseCompany,2020).

Figure15presentsthebillingblockoccurrencesofthesalesorders.Itshowcasesthat

themajorityofcaseswereonlyonceheldinbillingblockbutalsoupdatingthebilling

blockthreetimeswascommonforonecase.Onlyeightsalesorderswerenotheldat

billingblockatall.

Figure15.Billingblockcountoccurrences(CaseCompany,2020).

52

Thebillingblockfiguresstatethatthisiscertainlyonebottleneckoftheprocess.Almost

allcasesareheldinthebillingblockhavinganeedtobemanuallyreleasedbeforethe

invoicingcanbeexecutedautomatically.Billingblockswereoneoftheaspects inthe

interviewswithpricingspecialists.Theaimwastofindoutthereasonforsalesorders

neededtobeheldinblocksmanuallywhichevidentlyslowsdowntheirworkprocesses.

Reverseticketcount

Areverse ticketingactivity isdone if theactualized tickethas inadequatedatawhich

needstobecorrected.Reverseticketingmeansthattheticketisrevokedandanewone

iscreated.Accordingtothedata,inmostcasesnoreverseticketwasneeded(202cases),

butinsomecasestheticketwasreversedonce(38cases)ortwice(9cases).Thisisshown

inFigure16.

Figure16.Reverseticketingtimes(CaseCompany,2020).

Figure17showsthenumberofreverseticketactivitiesmademonthly.Thecountofre-

verseticketsisanaverage.InApril2018,therewasonesalescaseinwhichtherewas

oneprocessofreverseticketing.

53

Figure17.Averagereverseticketingmonthly(CaseCompany,2020).

Itcanbeseenthatfromallofthecases,reverseticketingactivitiesweredonefor23%

ofcasesandmostlyonce.Thesereasonswillbediscussedinthesection4.3.astheother

informationcollectedfromtheinterviewsareaddressed.

Creditinvoicerate

Creditinvoiceisanincorrectinvoicewhichneedstobecancelled.Fromallofthe249

casestherewere600invoiceitemscreatedandallinall,thecreditinvoicerateofthe

caseswas46%.Figure18showstheamountofsalesorderspermonthandthenum-

berofthosesalesorderinvoicescredited.

54

Figure18.Creditinvoicerateofthesalescases(CaseCompany,2020).

InSeptember2019,therewere20salescasesfromwhich70%werecancelledwitha

credit invoice (14credit invoicedcases).Thisdataalsoshowswell thetimeframethe

operatingbusinesshasbeenchangedbytheintroductionofanewsalesofficeoranew

productcategory.Oneexplanationforthehighamountofcreditedinvoicescouldbethe

newoperationswhicharebeingexecuted first time leading toerrorsoccurringmore

oftenthanusual.Theissueoftheamountofcreditinvoiceswasaddressedintheinter-

views.

55

4.3 Qualitativeresults

Theinterviewswereconductedface-to-faceorbyameetingcallwithspecialistsoperat-

ingindifferentresponsibilitiesintheO2Cprocess.Asasummary,ninespecialistswere

interviewedandtheywereheldeitherasone-to-oneortwo-to-onepersonalcommuni-

cations.Theinterviewswerecarriedoutafterstudyingthequalitativedatainorderto

understandwhatweretheareasofreworkandchallenges.Theaimofthequestionnaire

wastofindexplanationsdescribingthebottlenecksidentifiedinthedata.Furthermore,

theinterviewquestionsstudiedthecurrentchallengesoftheprocessgivingguidancein

thewayaheadforthedevelopmentoftheprocess.

TheTrader

Tradercooperateswiththesupplychainplannersandshippingdepartmenttoreceive

informationaboutthesurplusproduct.Oncethetraderhasenoughinformationabout

theproduct,thesalesisnegotiatedwiththecustomer.Thetraderstatedthatoneofthe

biggestchallengesisthatasthesespotsalesarerapidandneedtobesoldquickly,one

mightnotevenknowtheexactqualityoftheproduct.Thiscanleadtolostrevenue,since

thevalueoftheproductincreasesdependingonthequality.AnotherissueistheAllegro

systemprocess.TheAllegrosystemgathersthedataofthedealandintegratesittoSAP.

ThetraderentersthedealtoAllegroandalltheinformationshouldflowtoSAP:tothe

contract, sales order and nomination. For unexplained system reasonsAllegro is not

workingproperlyandtheinformationisnotflowing.(Trader,personalcommunication,

February13,2020)

Thetraderhighlightedthatasanareaofdevelopment,theoperationsspecialistscould

takepartincommercialactivitiesbydoingsomekindofamarketresearchofthepoten-

tialcustomers.Itwasalsomentionedthatthephysicalcapacityoftheharborislimited

asonlyafewvesselscancarrycertainproductstocertainareas.Furthermore,thetanks

intheharborareaarealsolimitedandproductscannotbestoredforprolongedperiods

oftime.Byhavingmoreoperatingvesselsandtanksthesaleswouldnothavetobedone

rapidly. Lastly, the trader also underlined that the information flow throughout the

56

wholeprocessshouldalsobeimproved.(Trader,personalcommunication,February13,

2020)

TheOperationsspecialists

Theoperationsspecialistscooperatecross-functionallywithinternalandexternalstake-

holdersaswellasensurethatthesaleiscarriedoutasplanned.Theoperationsspecial-

istsarguedthatthecomplianceteamhasacrucialrole intheprocess.Spotsalesare

rapidandtheloadingscanevenoccuronthesameday,thefastercomplianceapproves

thedeal,thefastertheoperationsspecialistsgeteverythingundercontrol.Eventually,

theticketingcancausechallengesiftheharborcannotentertheloadingdetailstothe

systemandtheoperatorneedstoresolvetheissueanddotheticketing.Consequently,

thiscausesdelaysintheprocess.Additionally,ifthereisincorrectdatainSAP,thein-

voicingwillnotbeaccuratemeaningthattheoperationsspecialisthastohavethesales

onthebillingblockinordertocheckthedatabeforetheinvoiceiscreated.However,

sometimesthe invoicestillneeds tobecancelledandre-invoicedandtheoperations

specialistisinchargeofmanagingtheseactionswiththepricingandinvoicingteam.(The

Operationsspecialists,personalcommunication,February11,2020)

Theoperationsspecialistshighlightedthattheywouldliketoseedevelopmentinareas

ofrolesandresponsibilities,fasterdecisionmakingincomplianceandflexibilityinac-

tions.Duetothefactthatcurrentlyeverythingneedstohappenattheprecisemoment

thecasedropstotheoperationsspecialist’sdesk.Additionally,theoperationsspecialists

feltthattheycouldbenefitfromincreasedvisibilityininvoicingactionsastheyneedto

beawareifaninvoiceiscancelledandgetinformationofthepriceoftheinvoice.(The

operationsspecialists,personalcommunication,February11,2020)

ThePricingspecialists

Thepricingspecialistsensureandmonitorthatthepricingdataiscorrectinthesystems.

ThepricingspecialistshighlightedthatAllegrosystemcausesthemextraworksinceitis

notfunctioningproperly.Therefore,theyneedtomanuallyaddthepricingdata,monitor

57

andcheckonadailybasisthatthepricesaresetaccordingly.Stillsomeinvoicesneedto

becancelledandthepricesfixedforthere-invoicing.TheyarguedthatiftheAllegrosys-

temwouldworkasintended,theirmajorchallengeswouldberesolved.(ThePricingspe-

cialists,personalcommunication,February12,2020)

TheLogisticsspecialist

Thelogisticsspecialistcreatesthenominationkeyandparticipatesintheoverallplan-

ningofthecargomovementsandprioritizationofthecargoes.Thedailyoperationsare

mainlyfocusedonmanagingoperationalplanningandthecreationofnominations.If

changesarise,thenominationisupdatedaccordingly.However,thelogisticsspecialist

underlinesthatthephysicalcapacityoftheharboriscrucialwhichaffectsarisingbottle-

necksintheprocess.Thepiersandtanksarelimited,thushavinganeffectonrapidspot

on sales when the timeframe of action is so limited (1-2 days) to sell and load the

cargo.(TheLogisticsspecialist,personalcommunication,February19,2020)

Thelogisticsspecialisthighlightedthatonekeydevelopmentareaisthephysicalcapacity

oftheharbor.Additionally,itwasstatedthatimprovingthesystemandgivingvisibility

tootheractivitiesinthesystemwouldalsoimprovethecurrentwayofworking.(The

Logisticsspecialist,personalcommunication,February19,2020)

TheHarborspecialist

Theharborspecialisttakescareofallthepracticalarrangementsandpaperworkinthe

harbor.Theharborspecialistindicatedthatthemainchallengewithinthedailyopera-

tionsisthattheinformationdiffersbetweenthesystem,instructionsandinspector’sac-

tions.Tobesurewhattodo,theharborspecialistneedstocontacttheoperationsspe-

cialist.Inaddition,alsothecapacityandequipmentofthevesselscreatechallengesas

thereareonlyafewdifferentsizedpiersandtheharborisverybusyatcertaintimes.

Thelimitedphysicalcapacitymightcausedelaysinthewholeprocess.(TheHarborspe-

cialist,personalcommunication,February14,2020)

58

Theharborspecialisthighlightedthefactthatreworkhappensmainlyduetoinadequate

andinaccurateinformation.AlsoduetoSAPsystemerrors,theprocessofactualizingthe

ticketmightnotgothroughandinthatcase,theoperationspecialistresolvestheissue

anddoes the ticketingwhichalsocausesdelays.Theharborspecialist suggested that

somedevelopmentareascouldbeimprovingthephysicalcapacityoftheharbor(num-

berofpiers,vesselsandtanks)andimprovingtheinformationflowoftheprocess.(The