unlocking the potential of the telecommunications sector to support networked readiness harvard...

Post on 21-Dec-2015

216 views

TRANSCRIPT

Unlocking the Potential of the Telecommunications Sector to Support Networked Readiness

Unlocking the Potential of the Telecommunications Sector to Support Networked Readiness

Harvard University – March 14, 2002

This report is solely for the use of client personnel. No part of it may be circulated, quoted, or reproduced for distribution outside the client organisation without prior written approval

from McKinsey & Company. This material was used by McKinsey & Company during an oral presentation; it is not a complete record of the discussion.

2

• Impact of telecommunications sector reform• Impact of telecommunications sector reform

AgendaAgenda

• Importance of reform going forward• Importance of reform going forward

• Priorities for reform• Priorities for reform

3

Lower high income countries

4747 3333 202010 - 20 15

Emerging countries

4343 2525 32323 - 10 28

Developingcountries

3333 262641413 85

Spread of sector reform Spread of sector reform No reform

Privatization only

Liberalization

Share of countries having undergone sector reform, %

Real GDP per capita$000

No. of countries

Upper high income countries

100100

100%

20 21

Fixed voice telephony, status end of year 2000Fixed voice telephony, status end of year 2000

4

Value impactIncumbent market capitalization, $ billions

Value impactIncumbent market capitalization, $ billions

933

60

January 18, 2002

993

-24%

+105%744

85

Flotation +3 years

829 CAGR 3%

CAGR 18%

456

78

At flotation

Emerging and developing countries

High-income countries

534

5

+21+13

+3

Teledensity growth Change in teledensity between 1996 and 2000

Teledensity growth Change in teledensity between 1996 and 2000 No reform

Privatization only

Liberalization

+48

+20

+5

Lower high income Emerging countries Developing countries

+53

+26

+5

+54

Upper high

income

6

+11

+4+1

+25

+1

+8

+31

Internet penetration % change in Internet users per 100 inhabitants from 1996-2000

Internet penetration % change in Internet users per 100 inhabitants from 1996-2000

+15

+6

+1

Lower high income Emerging countries Developing countries Upper high

income

No reform

Privatization only

Liberalization

7

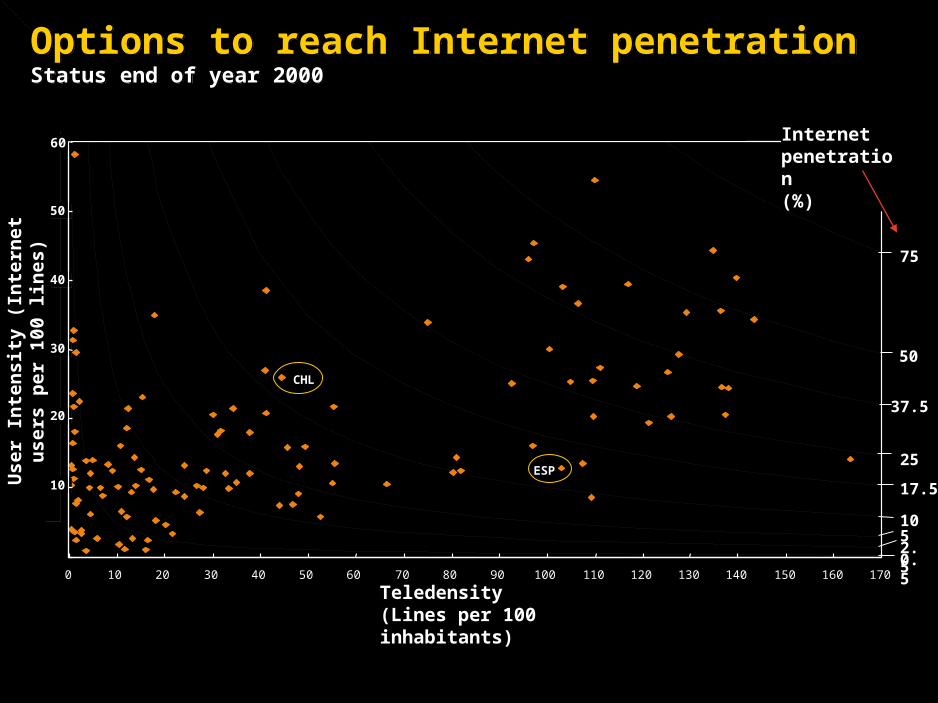

Options to reach Internet penetrationStatus end of year 2000

Options to reach Internet penetrationStatus end of year 2000

1

2

3

4

5

6

0 10 20 30 40 50 60 70 80 90 100 110 120 130 140 150 160 170

Teledensity (Lines per 100 inhabitants)

75

50

37.5

17.5

25

1052.50.5

Internet penetration(%)

6060

5050

4040

3030

2020

1010

Use

r In

ten

sit

y (

Inte

rnet

use

rs

per

10

0 li

ne

s)

ESP

CHL

8

Multiple tradeoffsMultiple tradeoffsIndustry Industry growthgrowth

Industry Industry growthgrowth

SocietySociety

• Government• Employees,

unions

• Government• Employees,

unions

Equipment providersEquipment providers

• Domestic• Foreign• Domestic• Foreign

CustomersCustomers

• Business• Residential• Business• Residential

OperatorsOperators

• Incumbent(s)• New entrant(s)• Incumbent(s)• New entrant(s)

Investors Investors

9

Priorities among multiple objectivesPriorities among multiple objectives

Promoted tele-density and additional investments

Promoted tele-density and additional investments

Compromised between efficiency, privatization proceeds and teledensity

Compromised between efficiency, privatization proceeds and teledensity

Broadly favored market efficiency and competition

Broadly favored market efficiency and competition

Similar emphasis

Networkedreadiness

Efficient industry

Attract investments

New Zealand

De

ve

lop

ing

c

ou

ntr

ies

D

ev

elo

pin

g

co

un

trie

s

Argentina (2)

Czech Republic

De

ve

lop

ed

co

un

trie

s

De

ve

lop

ed

co

un

trie

s

Malaysia

Em

erg

ing

co

un

trie

sE

me

rgin

g c

ou

ntr

ies

India Indonesia Philippines

China

Germany France U.K. (1)U.K. (2)Sweden U.S. Australia

Japan South Korea

Argentina (1)

Mexico (1)Mexico (2)

Russia Poland

South Africa

Brazil

Chile (2) Chile (1)

Hungary

Country Proceeds for government

Universal service

Benefits to customers

EXAMPLES

10

Measurable dimensionsMeasurable dimensions

*Footnote

Source: Source

• Teledensity Universal access• Teledensity Universal access

• Incumbent performance Proceeds to government• Incumbent performance Proceeds to government

• Price levels Benefits to consumers• Price levels Benefits to consumers

11

Universal ServiceCumulative growth of fixed-line Teledensity 3 years post-reform

Universal ServiceCumulative growth of fixed-line Teledensity 3 years post-reform

Source:ITU; Espicom; McKinsey

Developing countries

China India Indonesia Philippines Senegal

All with priority on Universal Service

739097

62

31111

15021111

Emerging countries Increase in lines per 100

Change Percent

Priority on Universal Service

No priority on Universal Service

Czech Republic

Hungary

Poland Brazil

Malaysia Chile (2)

Chile (1)South Africa

6971

534339

3529

6112

3012

6

Mexico (2)

Mexico (1)Argentina (1)Argentina (2)

9888343

32211

Teledensity at time of reform

121015198

119

510

61020

12

-28

-21

-21

-20

-16

0

11

Indonesia

Countries that did not emphasize benefits to customers

Mexico (2)

U.K. (1)

Argentina (2)

Japan

Poland

Brazil

Chile (2) Sweden

New ZealandAustralia (2)

Australia (1)

U.S.U.K. (2)

Countries that emphasized benefits to customers

South Korea

France

-65

-60

-45

-43

-34

-32

-20

-17

-13

0

Germany

Benefits to customersLong distance cumulative price change Incumbent tariffs 3 years post-reform, %

Benefits to customersLong distance cumulative price change Incumbent tariffs 3 years post-reform, %

13

Proceeds to GovernmentChange in performance and relative value of incumbent% median values

Proceeds to GovernmentChange in performance and relative value of incumbent% median values

At flotationFlotation + 3 years

4146

5343

Countries with priority on proceeds to Government

Countries with no priority on proceeds to Government

EBITDA

2130

2617

EBIT

32

51

28 27

P/E premium over main stock market index

14

Overview of regulatory levers

Pricing

Interconnection

IndustryStructure

CustomerAccess

UniversalService

PerformanceLevels

RegulatoryLevers

15

Detail of fixed and mobile regulatory leversDetail of fixed and mobile regulatory levers

Regulatory Levers

Industry Structure

Pricing

Inter-connection

Customer Access

Universal Service

Example of fixed and mobile regulatory levers

• Number of competitors• Ownership and control rules, including restrictions on foreign investment• Networks and services open to competition• Licensing procedures and conditions

• Price caps / tariff rebalancing • Access deficit compensation• Pricing constraints on local calls• Constraints on roaming charges

• Rights and obligations to interconnect• Structure and level of charges• Collocation and infrastructure sharing• Conditions for unbundling network elements• Interconnection for ISPs• Obligations and rights for virtual network mobile operators (MVNO’s)

• Numbering plan• Number portability • Length and ease of carrier pre-fixes• Subscription mechanism for carrier pre-selection

• Universal access and service obligation definitions• Universal service funding mechanism• Penetration targets• Network rollout and coverage targets

• Service quality targetsPerformance Levels

Source: McKinsey

16

Continued importance of reformContinued importance of reform

Source: McKinsey

AccessAccess

• Teledensity low in most developing world (>800 million households stilll without a phone line)

• Teledensity low in most developing world (>800 million households stilll without a phone line)

Internet and usage intensityInternet and usage intensity

• Increase usage of existing infrastructure already enabled for Internet

• 5.7 billion inhabitants are not using the Internet

• Increase usage of existing infrastructure already enabled for Internet

• 5.7 billion inhabitants are not using the Internet

QualityQuality

• Steps to ensure broadband reaches 187 million connections by 2005

• $150-200 billion to support rollout of 3G mobile technology

• Steps to ensure broadband reaches 187 million connections by 2005

• $150-200 billion to support rollout of 3G mobile technology

$150–200 billion in

value

$150–200 billion in

value

Value has been

unlocked

Value has been

unlocked

17

438

4,534

Developingcountries

220

614

Emergingcountries

TeledensityMillion access lines/population

TeledensityMillion access lines/population

Source: McKinsey

1,064

948

High-incomecountries

Access lines

Population

18

Lower incomedeveloped

31+

Developed

Highest in group

Median

Lowest in group

41+

Potential to increase usage intensityPotential to increase usage intensity

Internet user intensity

Emerging 38+

Developing 63+

Access availability

Price

Competition

Enabled line

Choice of service

Interconnection

19

2001 fixed lines

2001 fixed lines

Broadband penetration Broadband penetration

% of global access lines% of global access lines

Infrastructure challenge

Infrastructure challenge

20012001 20052005

20012001

20052005

Broadband access lines, millionBroadband access lines, million

20

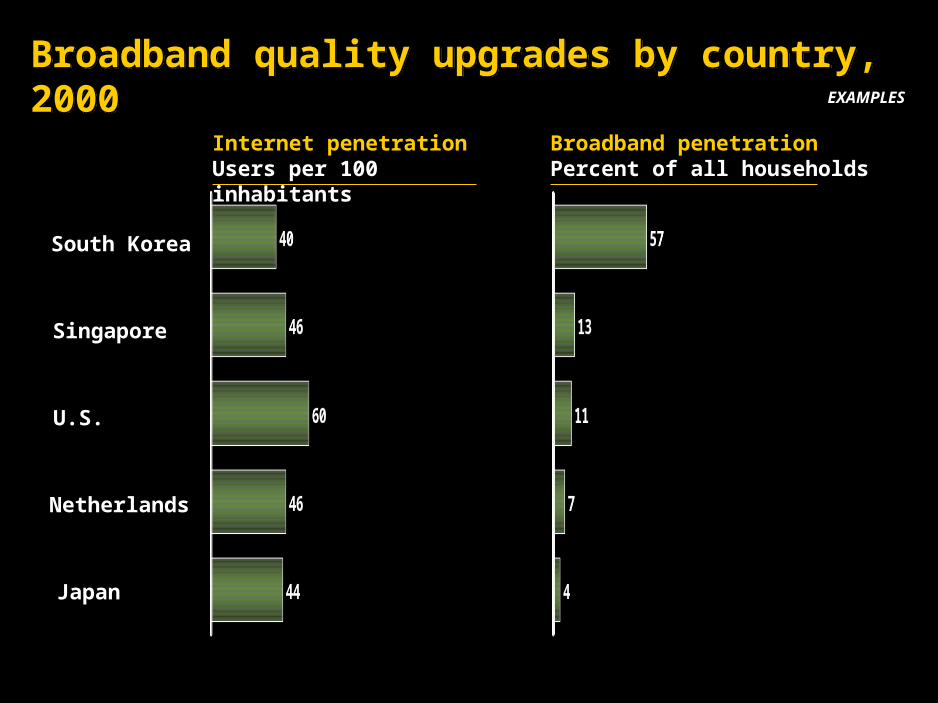

Broadband quality upgrades by country, 2000Broadband quality upgrades by country, 2000EXAMPLES

U.S.

Japan

Netherlands

Singapore

South Korea

Internet penetrationUsers per 100 inhabitants

Broadband penetrationPercent of all households

21

3G challenges3G challenges

• No deployment, available only in Japan

• US$130 bn paid in license auctions in Europe alone

• Unclear initial consumer value

• Additional US$150–200bn to deploy networks in Europe alone

22

What can be done?What can be done?

Source: McKinsey

Promote accessPromote access

• Developing countries

• Encourage and attract investment

• Explore mobile options

• Recognize mobile options

• Slow gradual process

• Developing countries

• Encourage and attract investment

• Explore mobile options

• Recognize mobile options

• Slow gradual process

Encourage Internet and usage intensityEncourage Internet and usage intensity

• All countries

• Stimulate demand

• Encourage competition and choice

• Fine tune and revise

• Iterating process

• All countries

• Stimulate demand

• Encourage competition and choice

• Fine tune and revise

• Iterating process

Fund quality improvementsFund quality improvements

• Mostly developed, but significant variation by country

• Require significant upgrades

• Explore funding options

• Experiment multiple approaches

• New approaches needed

• Mostly developed, but significant variation by country

• Require significant upgrades

• Explore funding options

• Experiment multiple approaches

• New approaches needed

Unlocking the Potential of the Telecommunications Sector to Support Networked Readiness

Unlocking the Potential of the Telecommunications Sector to Support Networked Readiness

Harvard University – March 14, 2002

This report is solely for the use of client personnel. No part of it may be circulated, quoted, or reproduced for distribution outside the client organisation without prior written approval

from McKinsey & Company. This material was used by McKinsey & Company during an oral presentation; it is not a complete record of the discussion.