u.s. construction trends and outlook (q4 2014)

TRANSCRIPT

Leasing momentum boosting construction demand, but costs growing

United States Construction

Perspective

Q4 2014

Construction starts increased in 2014, driven by improved demand from the office and industrial sectors in energy producing markets, along with traditional office markets like New York City. Even as demand explodes, cost to build is higher than ever, thanks to the continued inflation of labor and materials costs.

Due to the recent decline in energy costs, construction will shrink in Texas, a reversal from 2014 trends. Interest rates are also projected to grow, creating a potential dip in construction activity. Still, this growth cycle should last another two to three years.

Did you know? U.S. construction metrics

3

2.0%

The construction industry remains 22 .0 percent below peak levels. According to

Gilbane, it may take seven to eight more years to retain previous levels.

Cost for material inputs in all construction in the last 12 months. Cost for materials

for non-residential construction increased 1.4 percent during that time. Prices are

projected to continued growth, though many inputs will decline in price after 2015.

22.0%

The construction industry has grown every month of 2014, gaining 48,000 jobs in

December to reach 290,000 total in 2014. However, overall construction

unemployment is still 1.5 million lower than the peak in 2007.

Spent in wages in Commercial Building in 2014, approximately 48.0 percent of

total revenue. Wages have continued to increase across the construction industry,

forcing up overall building costs. The industry average is approximately $42,000.

107.0M

$64.9B

Total nonresidential building completions exploded in Q2 2014, as 107.0 million

square feet of new space was completed, mostly in the industrial sector.

$982.0B Total construction spending in December 2014, up 2.2 percent

from December 2013.

Sources: JLL Research, Gilbane, Bureau of Labor Statistics, IBISWorld

National economic trends

Construction GDP is rebounding more quickly than overall GDP

5

Construction starts on backlogged projects across the United States spur sector growth

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Overall real GDP growth

Construction component growth

Construction GDP has

increased more quickly than

overall GDP since 2012.

Overall GDP growth in Q4 2014 2.6%

Source: JLL Research, Bureau of Labor Statistics

Construction employment is growing faster than overall

employment

6

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

Non-farm employment Construction employment

Construction jobs added

in 2014. 233k

Percent increase in

construction jobs back to

pre-recession levels.

However, overall productivity has declined,

despite the growth in construction

employment, as many new workers are

under-trained for construction jobs.

(percent chg. year-over-year)

Source: JLL Research, Bureau of Labor Statistics

Construction employment was disproportionately affected by

the recession

7

Thanks to a rebound in construction opportunities, construction unemployment should drop below

overall unemployment by 2017; this decline is partially due to a reduction in available construction

workers in the workforce.

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Construction

unemployment rate

December 2014

8.3%

Overall

unemployment rate

December 2014

5.6%

Source: JLL Research, Bureau of Labor Statistics

The Architectural Billings Index, a leading indicator, has started

to increase

8

This indicates an aggregate jump in construction activity

20

25

30

35

40

45

50

55

60

ABI has reached more

than the baseline, 50,

indicating a rebound in

billing. The ABI reports

on the change in billings

from the previous month.

Source: JLL Research, American Institute of Architects, McGraw-Hill Dodge

The Construction Backlog Index is growing

9

Due to the rebound of construction activity in communities previously stagnated by the financial

crisis; the South is behind in construction, but is positioned to expand

Source: JLL Research, Associated Builders and Contractors

9.42mos

8.98mos

CB

I

10.2mos CB

I

6.93mos CB

I

Arrows represent change from one year ago

CB

I

National average

construction backlog

8.88mos

Cost trends: Labor and materials

Overall construction spending increased each quarter in 2014,

driven by nonresidential spending.

11

This trend is expected to continue in 2015

Source: JLL Research, Gilbane

-25.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

2007 2008 2009 2010 2011 2012 2013 2014 2015

Nonresidential construction spending (Percent chg. year- over- year)

Education construction is approximated to have had the highest

overall spend in 2014.

12

Source: JLL Research, U.S. Census

Total spend Percent change year-over-year

Education $77.7 billion 3.9 percent

Healthcare $38.7 billion - 2.1 percent*

Commercial $60.1 billion 10.7 percent

Office $48.6 billion 17.6 percent

Manufacturing $60.9 billion 18.1 percent

* Decline due to decrease in public sector spending

Labor costs are leading the growth in construction cost.

13

Source: JLL Research, ENR, Gilbane

A decline in available construction workers in the workforce, due to a lack of job training and general

frustration with the market, leads to an increase in costs.

2000

7000

12000

17000

22000

27000

0

2000

4000

6000

8000

10000

12000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Nat'l CCI

Materials Cost

Labor Cost

Com

mon labor index: U

nion wage plus fringe benefits

CC

I: 20

-city

ave

rage

of c

omm

on la

bor

rate

s pl

us m

ater

ial i

nput

s

New York City, Chicago, and Minneapolis lead the pack in terms

of high-cost construction.

14

Source: JLL Research, ENR

Cities with more land availability and lower labor costs maintain lower overall prices

Highest Cost

Lowest Cost

Dallas (Has not grown significantly)

Denver, CO

Atlanta (Increase for the first time

in 2014 since 2008)

Pittsburgh

New York City

Chicago

Minneapolis (Large spike in

cost in 2014)

Boston

Los Angeles

Philadelphia

San Francisco

Seattle

$0.0

$10.0

$20.0

$30.0

$40.0

$50.0

$60.0

$70.0

$80.0

$90.0

Atla

nta

Bal

timor

e

Bos

ton

Chi

cago

Cle

vela

nd

Dal

las

Den

ver

Det

roit

Los

Ang

eles

Min

neap

olis

New

Orle

ans

New

Yor

k

Phi

lade

lphi

a

Pitt

sbur

gh

San

Fra

ncis

co

Sea

ttle

Sai

nt L

ouis

Construction Costs- Major Cities

Union cities, such as New York, San Francisco, and Boston, have

higher labor cost than their “right to work” counterparts

15

Source: JLL Research, ENR

National

average:

51.67

Material price index shows high prices remain, though cost

growth slows

16

Source: JLL Research, ENR

2300

2400

2500

2600

2700

2800

2900

3000

3100

3200

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Closer inspection of the Materials Cost Index (ENR) shows a recent history of

growth. Economists project a slight decline in materials cost after 2015.

ENR Materials Price Index tracks weight price movement of

structural steel, portland cement, and 2x4 lumber.

Wei

ghte

d pr

ice

mov

emen

t of s

teel

, cem

ent,

and

lum

ber

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

% C

han

ge 2014

% C

han

ge 2015

% C

han

ge 2016

Steel

Rebar

Gypsum

Plywood

Softwood Lumber

Steel and rebar costs will decline after 2015

17

Source: JLL Research, ENR

Due to import pressures and decline in housing starts, lowering overall materials costs

Steel prices are forecast to decline

0.9 percent in 2014 and 1.8 percent

decline forecast through 2016.

Cities with high labor costs and land constraints have high

replacement costs versus rental price.

18

Source: JLL Research

Moving into 2015, this could hamper construction growth in some markets

$0.0

$200.0

$400.0

$600.0

$800.0

$1,000.0

$1,200.0

$ per s.f. Replacement Cost

Construction starts and put-in place

2014 saw a spike in demand for both new and remodeled space.

20

Source: JLL Research, CoStar, McGraw Hill

Nonresidential construction starts are growing as vacancy declines

178k 190k 208k 2012

166k

2013 2014 2015

Nonresidential construction starts are increasing as vacancy levels decrease. For industrial properties, vacancy has declined

from 8.9 percent in 2012 to 7.2 percent in Q4 2014. Office vacancy rates dropped from 14.1 percent to 10.9 percent in that

same time.

Nonresidential starts flattened slightly in Q4 2014, but will see an upturn again in 2015.

The value of U.S. private construction put-in-place has grown.

21

Source: JLL Research, Moody’s Analytics, Census Bureau

Due to an increase in new, trophy office development

$0.0

$50,000.0

$100,000.0

$150,000.0

$200,000.0

$250,000.0

$300,000.0

$350,000.0

$400,000.0

$450,000.0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

($M) Total Construction put-in-place in

November 2014. Approximately 1/3 of

this was nonresidential spending.

$975.0 billion Value of public construction

in November 2014

$277.0 billion

Demand for office and industrial space has increased, impacting

the construction starts in these sectors.

22

Source: JLL Research, CoStar Group

Office construction Industrial construction

Retail construction

47.3 m.s.f. under

construction

77.8 m.s.f under

construction

111.5 m.s.f. under

construction

Q4 2013

Q4 2014

Q4 2013 Q4 2014 142.2

m.s.f . under

construction

48.2 m.s.f.

under

construction

49.4 m.s.f. under

construction

Q4 2013 Q4 2014

of businesses plan to increase space

density through 2016 72%

Leading organizations

pushing density to

According to a JLL/CoreNet survey:

150 s.f. per person or less

Office completions are on the rise, after bottoming out in 2012,

driven by demand from the energy sector.

23

Source: JLL Research

0

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Ann

ual c

ompl

etio

ns (

s.f.)

Prime office costs have grown across the board

24

Source: JLL Research, Rider Levett Bucknell

Demand increases for high-class, CBD buildings, and input costs spike

$0.0

$50.0

$100.0

$150.0

$200.0

$250.0

$300.0

$350.0

$400.0

Boston Chicago Los Angeles New York San Francisco Washington DC

($ p.s.f.)

San Francisco’s cost of

building increased the most

for both low and high cost

office space since 2014.

Range of office construction costs in major markets

5,369,595 s.f.

Boston

Office square feet under construction grew across the country

in 2014.

25

Source: JLL Research

Growth in the energy sector fueled construction

6,487,023 s.f.

Dallas

4,153,534 s.f

Seattle

438,935 s.f

Portland

5,847,556 s.f

San Francisco

1,039,772 s.f

San Diego

2,404,819 s.f.

Phoenix

1,860,932 s.f.

Denver

17,760,993 s.f.

Houston

4,189,935 s.f.

Chicago

379,587 s.f.

Charlotte

8,425,911 s.f.

New York City

5,928,933 s.f. DC

3,506,297 s.f.

Philadelphia

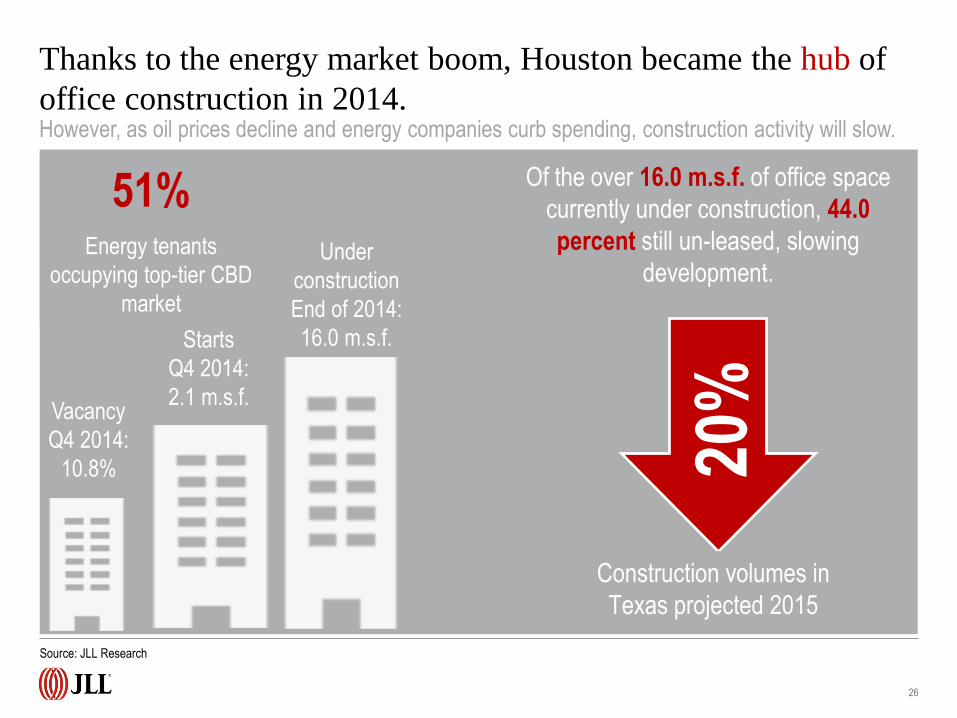

Thanks to the energy market boom, Houston became the hub of

office construction in 2014.

26

Source: JLL Research

However, as oil prices decline and energy companies curb spending, construction activity will slow.

Vacancy

Q4 2014:

10.8%

Under

construction

End of 2014:

16.0 m.s.f. Starts

Q4 2014:

2.1 m.s.f.

51% Energy tenants

occupying top-tier CBD

market

Of the over 16.0 m.s.f. of office space

currently under construction, 44.0

percent still un-leased, slowing

development.

Construction volumes in

Texas projected 2015

20%

Industrial completions are continuing to grow at a high rate,

eclipsing 2013 totals.

27

Source: JLL Research, CoStar

Ann

ual c

ompl

etio

ns (

s.f)

0

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

300,000,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

The development of e-commerce and large scale development are

driving industrial demand growth.

28

Source: JLL Research, Urban Land Institute

• e-commerce has been the fastest-growing segment of the retail market, creating a need for

new types of industrial development

• These buildings need more office space and parking, as they need to house more onsite

employees than traditional industrial buildings

• The “guts” of these buildings need more automation- there will be increased demand for

build outs of existing space to fit these parameters

• Companies are working to enhance economies of scale post-recession, are developing larger

industrial spaces that can serve multiple markets

• Consolidation of services into one large warehouse key to industrial development

• More large-scale construction projects to come due to this trend

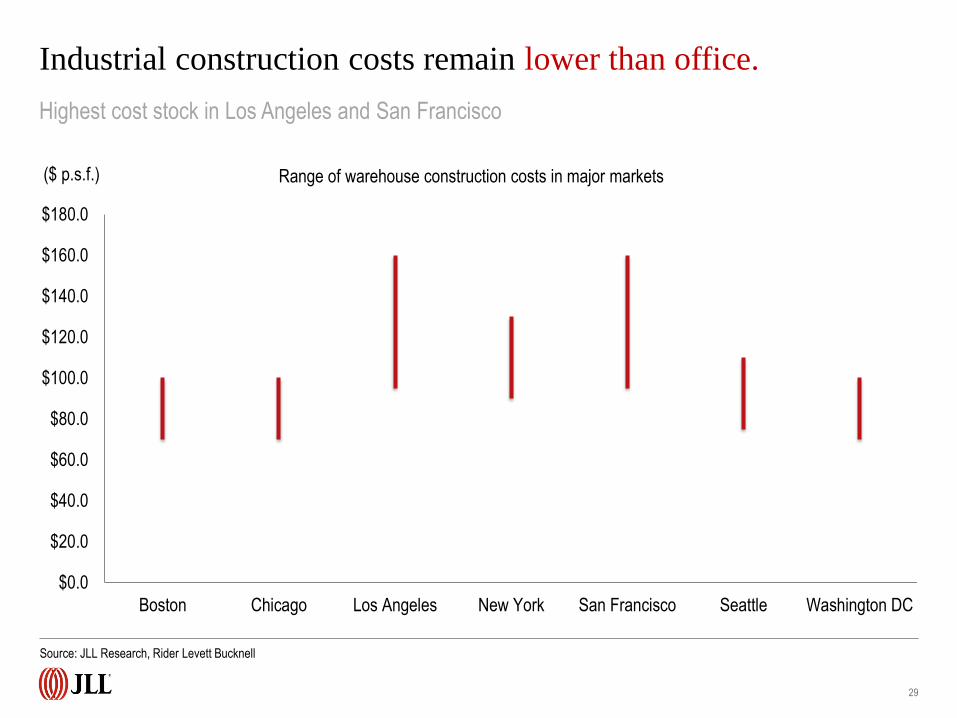

Industrial construction costs remain lower than office.

29

Source: JLL Research, Rider Levett Bucknell

Highest cost stock in Los Angeles and San Francisco

$0.0

$20.0

$40.0

$60.0

$80.0

$100.0

$120.0

$140.0

$160.0

$180.0

Boston Chicago Los Angeles New York San Francisco Seattle Washington DC

($ p.s.f.) Range of warehouse construction costs in major markets

13,090,582 s.f.

Inland Empire

220,000 s.f.

Boston 65,000

s.f. Long Island

Industrial centers like Inland Empire saw an increase in square

footage under construction in 2014

30

Source: JLL Research

17,517,455 s.f.

Dallas

2,932,970 s.f.

Seattle

2,866,426 s.f. Los

Angeles

895,646 s.f.

Northern NJ

7,273,541 s.f

Indianapolis

4,794,068 s.f.

Houston

13,393,047 s.f.

Chicago

1,745,130 s.f.

Baltimore

12,395,607 s.f.

Atlanta

2,234,134 s.f.

Charlotte

12,639,496 s.f.

Philadelphia

Demand for large retail space declines due to an increase in

digital retail.

31

Source: JLL Research, Rider Levett Bucknell

0

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

300,000,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Though overall retail construction has

declined, outlet mall demand has

skyrocketed. As a result, between

2013 and 2016, 21 million square feet

outlet space will have been delivered.

Ann

ual c

ompl

etio

ns (

s.f)

Overall retail construction slows, but demand for outlet

space flourishes.

32

Source: JLL Research

• Between 2013 and 2016, it is estimated that 21 million square feet of outlet center space will

have been delivered

• Consumers are motivated by discounts on name brand products

• Outlet development will continue to penetrate new markets as various submarkets begin

to emerge from the recession

• As a percentage of all space, malls and specialty centers are the most active in current

construction activity

• Retail is a rising market in many U.S. markets, with Miami and Dallas leading the pack-

indicating more development in these markets is to come

• Due to lifestyle changes, as more people move to urban core settings, mixed use retail is

becoming a more integral part of retail development

Retail construction costs remain low in Denver, and have reached

new post-recession heights in Los Angeles and San Francisco.

33

Source: JLL Research

$0.0

$50.0

$100.0

$150.0

$200.0

$250.0

$300.0

Boston Chicago Denver Los Angeles New York San Francisco Seattle WashingtonDC

($ p.s.f.) Range of retail construction costs in major markets

Major markets like New York City saw moderate retail square

footage under construction in 2014

34

Source: JLL Research

3,652,781 s.f.

Dallas

453,432 s.f.

Seattle

352,250 s.f.

Hawaii

83,635 s.f. San

Francisco

1,690,835 s.f. Los

Angeles 991,111

s.f. Orange County

385,058 s.f.

Atlanta

2,355,126 s.f.

Houston

1,534,800 s.f.

Chicago

427,148 s.f.

Tampa

895,404 s.f.

New York City

1,894,008 s.f. DC

762,131 s.f.

Philadelphia

2,801,056 s.f.

Boston

35

Source: JLL Research

Beverly Hills Hotel

Beverly Hills, CA

75,000 s.f.

AMC Theaters

Nationwide

4.8 m.s. f.

Lyft

San Francisco, CA

65,493 s.f.

JLL construction and renovation projects are following

the market demands for hospitality, education, technology,

and entertainment.

Roosevelt University

Chicago, IL

414,000 s.f.

Overview and outlook

37

Source: JLL Research

New York City and Northern New Jersey continue to develop. Part of this is due to post-Sandy redevelopment,

along with a general increase in demand for real estate space. Industrial stock may continue to grow as a result of

increased traffic due to the Panama Canal expansion.

The Southeast is catching up to overall trends. This region holds the largest concentration of commercial building

establishments and had an approximately 16.0 percent increase in construction starts.

Replacement costs are low in places like Chicago, West LA, and Seattle indicate future building growth potential

in those markets.

Previously slower moving markets, such as Minneapolis, have seen an increase in construction starts. Costs

for building jumped in 2014 in Minneapolis, as the city works on a massive downtown refurbishment. Midsized markets

are seeing a jump in construction activity, leading to cost growth.

Houston led in office development, but this may stagnate in 2015. It delivered 5.4 million square feet of new

space by the end of 2014; however prices are increasing, and the decline in oil prices imply a future decline in

construction in Houston.

1.

2.

3.

4.

5.

Key construction markets in 2014

38

Source: JLL Research, IBISWorld

Construction costs are growing, though growth in materials cost will drop during 2015.

Construction unemployment rates remain high, indicating a large potential employment pool for new

construction. Unemployment will drop quickly as building continues to grow; it is projected 1.1 million jobs will

be added in construction by 2020.

Construction put-in-place has continued to grow since bottoming-out in 2009/2010. Office construction in the

energy sector may see a decline in 2015, as oil prices have dropped substantially.

In some markets, replacement costs are lower than purchase prices, meaning constructing new space is

more cost-effective than renting existing space.

Construction Backlog Index is high in all but the Southeast Region, indicating 2015 will be a big year

for construction.

Construction is in the mature phase of the industry life cycle, meaning markets are volatile and

advancements in techniques and materials have little impact on demand.

1.

2.

3.

4.

5.

What’s next for construction?

© Copyright 2015 Jones Lang LaSalle

Thank you

Dana Westgren

Research Analyst- Industry, Project and Development Services

tel +1 312-228-2867