financial market outlook q4 2016 investment …bsbm.biz/database/docu/jb/20160921_q4_outlook.pdf ·...

TRANSCRIPT

Zurich, September 2016

FINANCIAL MARKET OUTLOOK Q4 2016 INVESTMENT OPPORTUNITIES

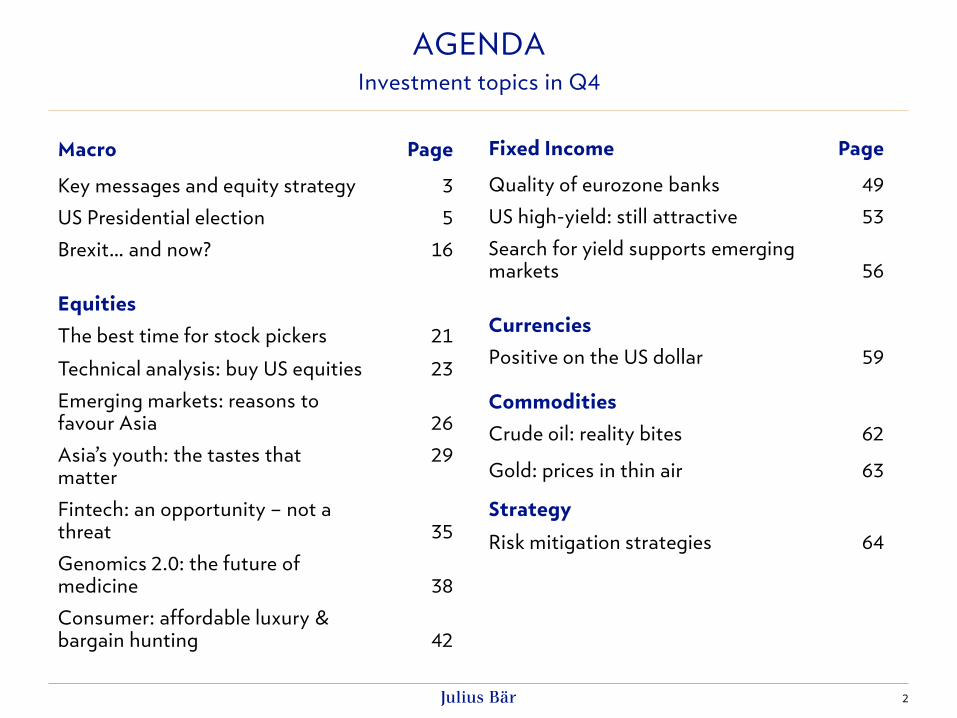

AGENDA

Investment topics in Q4

2

Macro Page

Key messages and equity strategy 3

US Presidential election 5

Brexit… and now? 16

Equities

The best time for stock pickers 21

Technical analysis: buy US equities 23

Emerging markets: reasons to favour Asia

26

Asia’s youth: the tastes that matter

29

Fintech: an opportunity – not a threat

35

Genomics 2.0: the future of medicine

38

Consumer: affordable luxury & bargain hunting

42

Fixed Income Page

Quality of eurozone banks 49

US high-yield: still attractive 53

Search for yield supports emerging markets

56

Currencies

Positive on the US dollar Commodities

59

Crude oil: reality bites 62

Gold: prices in thin air 63

Strategy

Risk mitigation strategies 64

3

Global cyclical backdrop improving at a modest pace

• Economic activity to accelerate in the US, robust momentum in most of Europe. Brexit now

negatively impacting the UK. Slowdown decelerating in China and Japan. Major emerging

markets are a mixed bag, with many economies looking rather fragile.

Brexit, other geopolitical risks and latent cyclical risks do not allow monetary restriction –

fiscal reflation re-emerging as an additional policy option

• The Bank of England has loosened monetary policy in response to the Brexit referen-dum.

Apart from the US Fed, no major central bank is considering policy tightening.

• With major central banks running out of options to stimulate growth, ruling authorities are

eroding fiscal austerity for deficit and even debt-financed spending: major examples are China

and Japan. Both US presidential candidates argue for additional fiscal stimulus. The new UK

government is expected to implement fiscal reflation to counter negative post-Brexit impacts.

Even in the eurozone, the pressure is on to undo the fiscal stability pact constraints.

Inflationary risks remain negligible until fiscal reflation materialises

• In the current environment of strong central bank stimuli, inflation risks appear low until fiscal

reflation becomes widespread, which is not very likely in the near to medium term.

ECONOMICS: KEY MESSAGES

4

OVERVIEW Equity Strategy Ratings

Global sector/industry group Rating Global sector/ind. group Rating Investment styles USA Europe Emerging markets Rating

Energy OW Info Tech OW Quality OW OW South Africa UW

Materials neutral Software OW Value UW UW Russia UW

Industrials neutral Hardware neutral Growth OW OW Turkey neutral

Capital Goods neutral Semiconductors OW Small caps neutral neutral Poland OW

Commercial & Professional Services neutral Telecom neutral Mid caps neutral neutral Brazil neutral

Transportation neutral Utilities UW Large caps neutral neutral Mexico neutral

Consumer Discretionary neutral High dividends neutral OW Chile OW

Automobiles neutral Developed markets Rating Dividend growers neutral neutral Colombia neutral

Consumer Durables UW USA neutral High Beta neutral neutral China * OW

Consumer Services neutral Canada neutral Low Beta neutral neutral South Korea * neutral

Media neutral Eurozone neutral Taiwan * OW

Retailing OW Germany neutral India * OW

Consumer Staples UW France neutral Malaysia * OW

Food & Staples Retailing neutral Netherlands OW Indonesia * OW

Food, Beverage & Tobacco UW Spain UW Thailand * neutral

Household & Personal Products UW Italy UW Philippines * neutral

Healthcare OW UK OW Vietnam (frontier market)

OW

Healthcare Equipment & Services neutral Switzerland neutral

Pharma, Biotech & Life Science OW Sweden neutral

Financials neutral Japan * neutral

Banks neutral Australia * neutral

Diversified Financials neutral Hong Kong * OW

Insurance neutral Singapore * UW

Real Estate neutral Emerging markets OW

OW = Overweight; UW = Underweight Columbia and Vietnam: Julius Baer makes no offering in local markets.

Source: Strategy Research, * Research Asia Taiwan: Julius Baer’s offering in the local market is restricted.

THE NEXT UNCERTAINTY: US PRESIDENTIAL ELECTION USD well-supported by various election outcomes. Clinton’s steady policy would

deliver cyclical support, Trump’s disruptive policy would give safe-haven support.

Source: Julius Baer; GDP = Gross domestic product

US presidential election 2016 and possible outcomes with estimated probabilities

5

GDP

Inflation

US presidential

election

Hillary R. Clinton

1.8% 1.3% 1.3% 2.1%

Donald Trump

Aggressive policy

2.4% 1.9% 1.5% 2.8%

‘Unguided missile’

0.5% 1.0% 1.8% 2.5%

85%

70%

30%

15%

2017 2018 2017 2018

70%

25%

5%

6

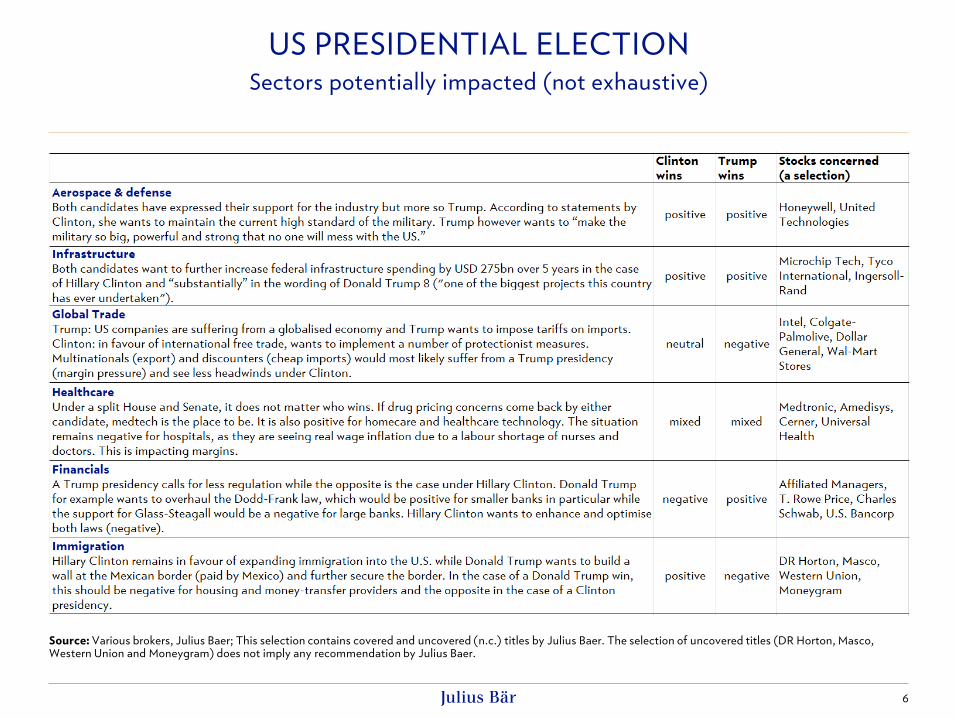

US PRESIDENTIAL ELECTION Sectors potentially impacted (not exhaustive)

Source: Various brokers, Julius Baer; This selection contains covered and uncovered (n.c.) titles by Julius Baer. The selection of uncovered titles (DR Horton, Masco, Western Union and Moneygram) does not imply any recommendation by Julius Baer.

7

Infrastructure to profit as both candidates intend to increase fiscal spending

• Both candidates for the US presidency have announced to further increase federal

infrastructure spending in case of being elected. While Clinton intends stemming an

additional USD 275bn package, Trump has communicated a ‘substantial’ ramp-up of

spending. Our take is that - in both cases - infrastructure stands to profit.

• Looking at the broader picture, too, infrastructure is set to receive a boost, in our view. As

monetary policy has by and large reached its limits across the globe, more expansionary fiscal

policy has become the only policy instrument left.

• Infrastructure is generally seen as a defensive investment. Applicable to large- and small-scale

organisational frameworks, infrastructure can include a variety of systems and structures as

long as there are physical components required.

• As infrastructure companies can be found across several sectors, it is challenging to make an

assessment in terms of valuation. Based on our recommended infrastructure equities,

however, valuations are fair.

• Infrastructure in the US has performed well since the beginning of the year, up by 18%

according to LPX group’s NMX Infrastructure America index.

• We advise buying exposure via diversified direct investments or actively managed funds.

US PRESIDENTIAL ELECTION - INFRASTRUCTURE

US infrastructure stands to profit from a renaissance of fiscal policies

Growing appetite to use fiscal policy

• Monetary policy has largely reached its

limits making expansionary fiscal policy the

only policy instrument left.

• Growing ‘intellectual’ consensus that

expansionary fiscal policy is able to foster

structural reforms, hence increasing the

economies’ growth potential in addition to

the short-lived demand push.

• Examples include investments in childcare

to raise women’s participation rate, tax cuts

to increase employment or infrastructure

investments to lower transport costs.

• Falling debt-servicing costs loosen the

constrains on deficit-financed fiscal policy

despite elevated debt levels.

US PRESIDENTIAL ELECTION - INFRASTRUCTURE Fiscal policy returns on the agenda as monetary policy has lowered interest rates to

zero and benefits of unconventional policies are becoming questionable.

Source: Datastream, Julius Baer; ECB = European Central Bank; BoJ = Bank of Japan; Fed = US Federal Reserve; BoE

Policy rates have converged at zero

8

05 06 07 08 09 10 11 12 13 14 15 16

0

1

2

3

4

5

6

% p.a

ECB BoJ Fed BoE

9

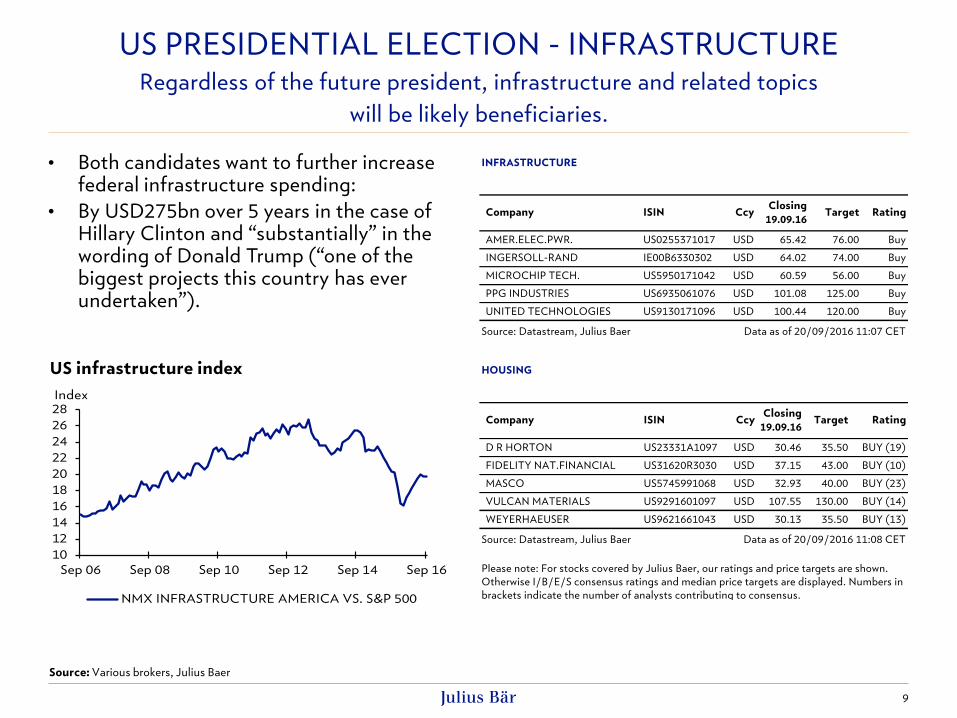

US PRESIDENTIAL ELECTION - INFRASTRUCTURE Regardless of the future president, infrastructure and related topics

will be likely beneficiaries.

Source: Various brokers, Julius Baer

• Both candidates want to further increase federal infrastructure spending:

• By USD275bn over 5 years in the case of Hillary Clinton and “substantially” in the wording of Donald Trump (“one of the biggest projects this country has ever undertaken”).

US infrastructure index

INFRASTRUCTURE

Closing

19.09.16

AMER.ELEC.PWR. US0255371017 USD 65.42 76.00 Buy

INGERSOLL-RAND IE00B6330302 USD 64.02 74.00 Buy

MICROCHIP TECH. US5950171042 USD 60.59 56.00 Buy

PPG INDUSTRIES US6935061076 USD 101.08 125.00 Buy

UNITED TECHNOLOGIES US9130171096 USD 100.44 120.00 Buy

Source: Datastream, Julius Baer Data as of 20/09/2016 11:07 CET

Company RatingTargetCcyISIN

HOUSING

Closing

19.09.16

D R HORTON US23331A1097 USD 30.46 35.50 BUY (19)

FIDELITY NAT.FINANCIAL US31620R3030 USD 37.15 43.00 BUY (10)

MASCO US5745991068 USD 32.93 40.00 BUY (23)

VULCAN MATERIALS US9291601097 USD 107.55 130.00 BUY (14)

WEYERHAEUSER US9621661043 USD 30.13 35.50 BUY (13)

Source: Datastream, Julius Baer Data as of 20/09/2016 11:08 CET

Please note: For stocks covered by Julius Baer, our ratings and price targets are shown.

Otherwise I/B/E/S consensus ratings and median price targets are displayed. Numbers in

brackets indicate the number of analysts contributing to consensus.

Company RatingTargetCcyISIN

10

12

14

16

18

20

22

24

26

28

Sep 06 Sep 08 Sep 10 Sep 12 Sep 14 Sep 16

Index

NMX INFRASTRUCTURE AMERICA VS. S&P 500

US PRESIDENTIAL ELECTION - INFRASTRUCTURE

10

Partners Group Invest Infrastructure

Fund description

• The fund provides access a global portfolio of companies that make infrastructure investments and are listed on major stock exchanges.

• Targeted sectors include Transport (e.g. toll roads), transmission and distribution, pipelines, airports, ports, railways as well as satellites ramp towers.

• The fund has a global allocation to infrastructure with approx. 40% US, 30% Europe and a sizeable allocation of 30% to growth markets.

• Core infrastructure should act as a stabilizing factor within the equity allocation.

• Due to its exclusive focus on core infrastructure, the fund can be characterised by low volatility and limited draw down risk when compared to equity or other infrastructure funds.

• In a negative market environment, the fund is expected to outperform its peers due to its exclusive focus on core infrastructure and the lack of exposure to more cyclical stocks.

Fund performance 5-year performance, in percentage (net)

Additional information Provider: MultiConcept Fund Mgmt. SA.; paying agent: Credit Suisse, Paradeplatz 8, CH-8001 Zürich; representative: ACOLIN Fund Services AG, Affolternstrasse 56, CH-8050 Zürich Please find supporting documents (fund fact sheet, prospectus, annual report, etc.) on www.fundinfo.com, or contact your Julius Baer representative for further information

As of 20.09.2016; Source: Datastream, Julius Baer, Morningstar

Low Moderate Considerable High

Lower risk Higher risk

Julius Baer product risk classification

Benchmark MSCI World (NR)

Base Currency EUR

Other Currencies USD, CHF

ISIN (USD Share Class) LU0617149793

ISIN (EUR Share Class) LU0949730401

ISIN (CHF Share Class) LU0661297050

NAV as of 19.09. 2016 USD 140.50

Size as of 31.08.2016 EUR 536.18 mln

Domicile Luxembourg

Launch Date 28.06.2012

TER 2.19%

Sales Registrations CH, DE, UK, IT, SG, others

Supporting Documents http://www.fundinfo.com/PG Infrastructure

Product facts

US PRESIDENTIAL ELECTION - INFRASTRUCTURE

11

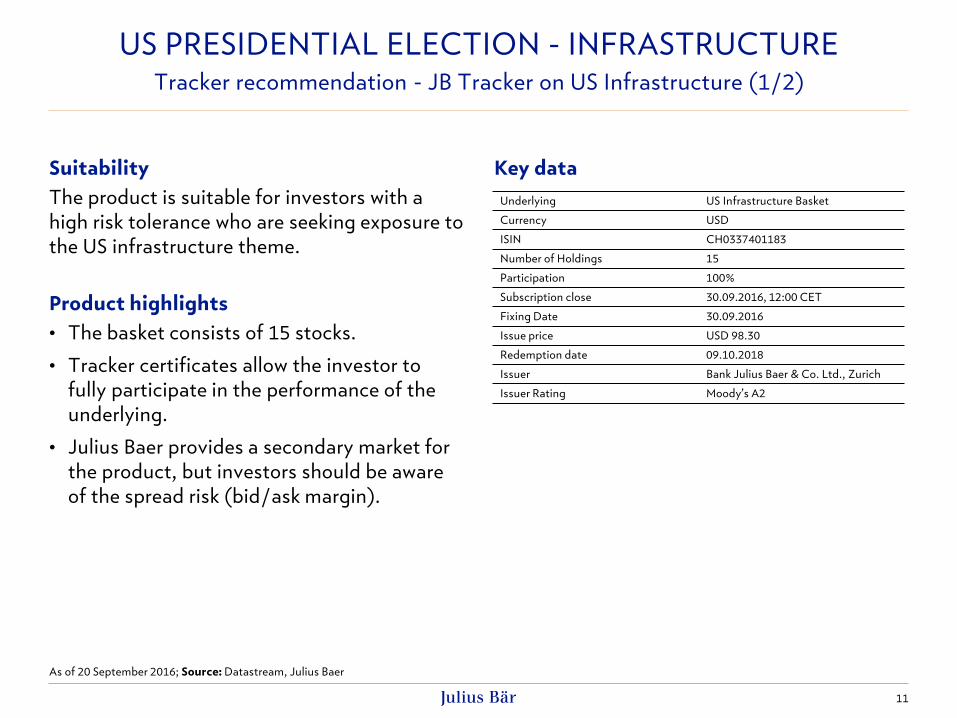

Tracker recommendation - JB Tracker on US Infrastructure (1/2)

Suitability

The product is suitable for investors with a

high risk tolerance who are seeking exposure to

the US infrastructure theme.

Product highlights

• The basket consists of 15 stocks.

• Tracker certificates allow the investor to

fully participate in the performance of the

underlying.

• Julius Baer provides a secondary market for

the product, but investors should be aware

of the spread risk (bid/ask margin).

Key data

As of 20 September 2016; Source: Datastream, Julius Baer

Underlying US Infrastructure Basket

Currency USD

ISIN CH0337401183

Number of Holdings 15

Participation 100%

Subscription close 30.09.2016, 12:00 CET

Fixing Date 30.09.2016

Issue price USD 98.30

Redemption date 09.10.2018

Issuer Bank Julius Baer & Co. Ltd., Zurich

Issuer Rating Moody’s A2

US PRESIDENTIAL ELECTION - INFRASTRUCTURE

12

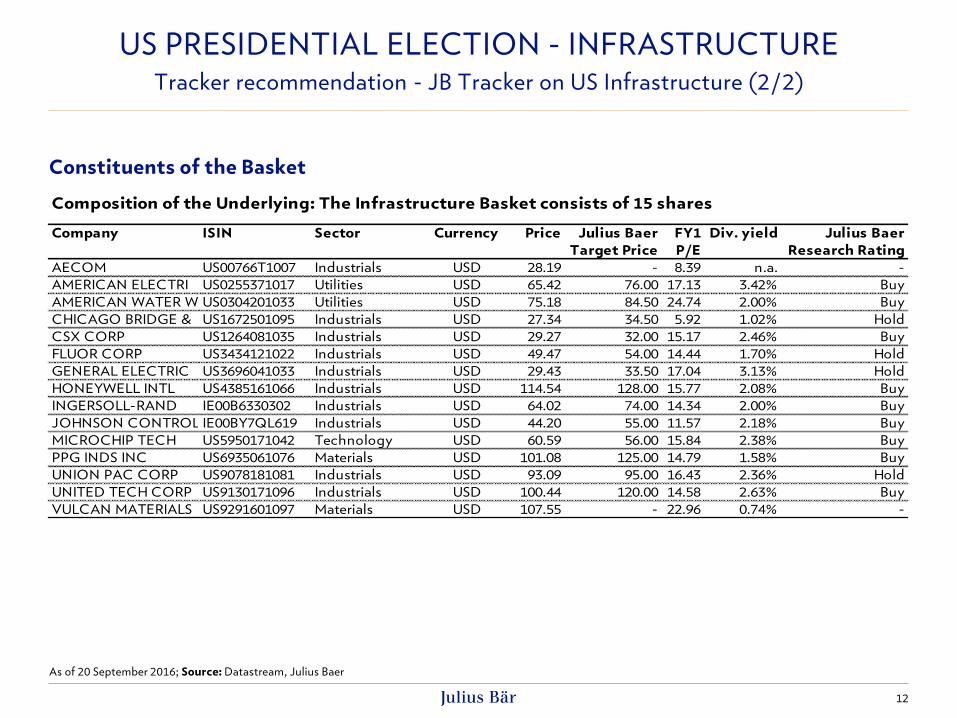

Tracker recommendation - JB Tracker on US Infrastructure (2/2)

Constituents of the Basket

Company ISIN Sector Currency Price Julius Baer

Target Price

FY1

P/E

Div. yield Julius Baer

Research Rating

AECOM US00766T1007 Industrials USD 28.19 - 8.39 n.a. -

AMERICAN ELECTRI US0255371017 Utilities USD 65.42 76.00 17.13 3.42% Buy

AMERICAN WATER W US0304201033 Utilities USD 75.18 84.50 24.74 2.00% Buy

CHICAGO BRIDGE & US1672501095 Industrials USD 27.34 34.50 5.92 1.02% Hold

CSX CORP US1264081035 Industrials USD 29.27 32.00 15.17 2.46% Buy

FLUOR CORP US3434121022 Industrials USD 49.47 54.00 14.44 1.70% Hold

GENERAL ELECTRIC US3696041033 Industrials USD 29.43 33.50 17.04 3.13% Hold

HONEYWELL INTL US4385161066 Industrials USD 114.54 128.00 15.77 2.08% Buy

INGERSOLL-RAND IE00B6330302 Industrials USD 64.02 74.00 14.34 2.00% Buy

JOHNSON CONTROLSIE00BY7QL619 Industrials USD 44.20 55.00 11.57 2.18% Buy

MICROCHIP TECH US5950171042 Technology USD 60.59 56.00 15.84 2.38% Buy

PPG INDS INC US6935061076 Materials USD 101.08 125.00 14.79 1.58% Buy

UNION PAC CORP US9078181081 Industrials USD 93.09 95.00 16.43 2.36% Hold

UNITED TECH CORP US9130171096 Industrials USD 100.44 120.00 14.58 2.63% Buy

VULCAN MATERIALS US9291601097 Materials USD 107.55 - 22.96 0.74% -

Composition of the Underlying: The Infrastructure Basket consists of 15 shares

As of 20 September 2016; Source: Datastream, Julius Baer

13

Medtech – ‘hiding place’ if drug pricing concerns return to the market

• Hillary Clinton becoming the next US president is generally perceived as a less positive

outcome for the healthcare sector as a whole. However, for the medtech segment, it does not

matter that much who wins the presidential election. If drug pricing concerns return, medtech

is the place to be.

• Healthcare is one of three sectors which we currently rate ‘overweight’ (the others are energy

and information technology). Medtech represents the most defensive segment of the

healthcare sector.

• Medtech encompasses a wide range of healthcare products and is generally used to diagnose,

monitor or treat diseases or medical conditions. The basic goal of medtech is to improve the

quality of healthcare delivered through earlier diagnosis, less invasive treatment options and

reductions in hospital stays and rehabilitation times.

• Like its peers of the other healthcare segments, medtech profits from positive socio-

demographics. In addition, it has a low exposure to US healthcare spend pressure, generally

provides stable growth with low exposure to R&D binary events and pays medium dividends.

• Despite its outperformance this year, medtech has by no means become expensive (based on

P/E ratios), relative to the rest of the sector. Our analysts believe that current uncertainties

with regard to drug pricing debates in the run up to the presidential elections will keep the

segment underpinned.

US PRESIDENTIAL ELECTION - MEDTECH

Medtech is relatively unaffected, no matter who will become US president

14

US PRESIDENTIAL ELECTION - MEDTECH Under a split House and Senate, it does not matter for medtech who wins the

presidential election. If drug pricing concerns return, medtech is the place to be.

Source: Datastream, Julius Baer

Medtech remaining outperformers US MEDTECH COMPANIES

Closing

19.09.16

BECTON DICKINSON US0758871091 USD 175.66 192.00 Buy

INTUITIVE SURGICAL US46120E6023 USD 693.55 765.00 Buy

MEDTRONIC IE00BTN1Y115 USD 85.99 94.00 Buy

ZIMMER BIOMET HDG. US98956P1021 USD 124.97 146.00 Buy

Source: Datastream, Julius Baer Data as of 20/09/2016 11:05 CET

Company RatingTargetCcyISIN

80

100

120

140

160

180

200

220

240

260

Sep 11 Sep 12 Sep 13 Sep 14 Sep 15 Sep 16

Index

MORGAN STANLEY MEDICAL TECH INDEX

S&P 500

US PRESIDENTIAL ELECTION - MEDTECH

15

Fund recommendation – Variopartner SICAV – MIV Global Medtech Fund

Fund description

• The fund invests primarily in a portfolio of global medical technology equity securities.

• The fund is expected to move in line with the underlying market and to outperform its benchmark over an investment cycle (Julius Baer fund label: Market Exposure).

• The research effort is focused on finding devices with the highest commercial potential regardless of the domicile of their producers. Inception-to-date performance has benefited from MIV's research analysts' track record of identifying M&A targets.

• Security selection favours companies with an above-average revenue growth potential.

Fund performance 5-year performance, in percentage (net)

Low Moderate Considerable High

Lower risk Higher risk

Julius Baer product risk classification

Additional information Provider: Vontobel Asset Management S.A.; paying agent: Bank Vontobel AG; representative: Vontobel Fonds Services AG. Please find supporting documents (fund fact sheet, prospectus, annual report, etc.) on www.fundinfo.com, or contact your Julius Baer representative for further information.

As of 20.09.2016; Source: Datastream, Julius Baer, Morningstar

Product facts Benchmark MSCI World / HC Equip & Supl NR USD

Base Currency CHF

Other Currencies (unhedged) USD, EUR

ISIN (USD Share Class) LU0969575561

ISIN (CHF Share Class) LU0329630999

ISIN (EUR Share Class) LU0329630130

NAV as of 16.09.2016 CHF 1’391.43

Size as of 31.08.2016 CHF 753.61 mln

Domicile Luxembourg

Launch Date 11.03.2008

TER 1.61%

Sales Registrations LI, LUX, CH, DE, AT

Supporting documents http://www.fundinfo.com/Variopartner

16

The weakening GBP turns into a tailwind for internationally exposed UK companies

• Despite some solid fundamental data releases since the UK vote on Brexit, our Research

expects the UK economy to weaken over the coming months.

• The Bank of England (BoE) has released a comprehensive set of further quantitative easing

measures to mitigate the potentially adverse impact of Brexit. A GBP-related inflation

overshoot will be tolerated by the BoE, implying negative consequences for the currency.

• Slowing foreign direct investments and trade disruptions will increase the current account

deficit.

• We expect the British pound to weaken further over the coming months – however, the

weakening currency will turn into a tailwind for those large and internationally exposed UK

companies having their cost base mostly in the UK.

• The impact of Brexit on the majority of stocks we cover and on their growth prospects should

be limited given that many UK companies have a globally well-diversified footprint and derive

only a low-to-mid-single digit percentage of their sales from the UK.

• By sector, we particularly see no major negative impact in general for UK consumer staples,

healthcare, business services and utility equities we cover.

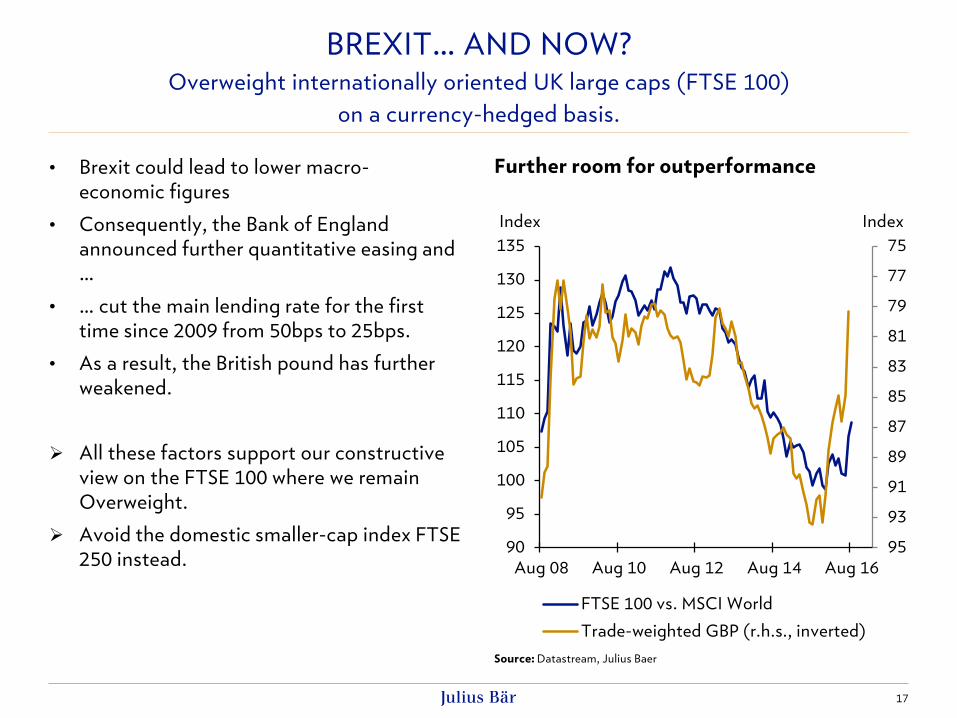

BREXIT… AND NOW?

Large internationally exposed UK companies to profit

• Brexit could lead to lower macro-

economic figures

• Consequently, the Bank of England

announced further quantitative easing and

…

• … cut the main lending rate for the first

time since 2009 from 50bps to 25bps.

• As a result, the British pound has further

weakened.

All these factors support our constructive

view on the FTSE 100 where we remain

Overweight.

Avoid the domestic smaller-cap index FTSE

250 instead.

17

BREXIT… AND NOW? Overweight internationally oriented UK large caps (FTSE 100)

on a currency-hedged basis.

Source: Datastream, Julius Baer

Further room for outperformance

75

77

79

81

83

85

87

89

91

93

9590

95

100

105

110

115

120

125

130

135

Aug 08 Aug 10 Aug 12 Aug 14 Aug 16

IndexIndex

FTSE 100 vs. MSCI World

Trade-weighted GBP (r.h.s., inverted)

2017

2016

2018

2014

2015

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

-1 0 1 2 3 4

Julius Baer forecast

Bloomberg consensus

Bank of England forecast

CPI inflation*

Real GDP growth*

Inflationary bust ("stagflation")

Inflationary boom

Deflationary bust

Deflationary boom

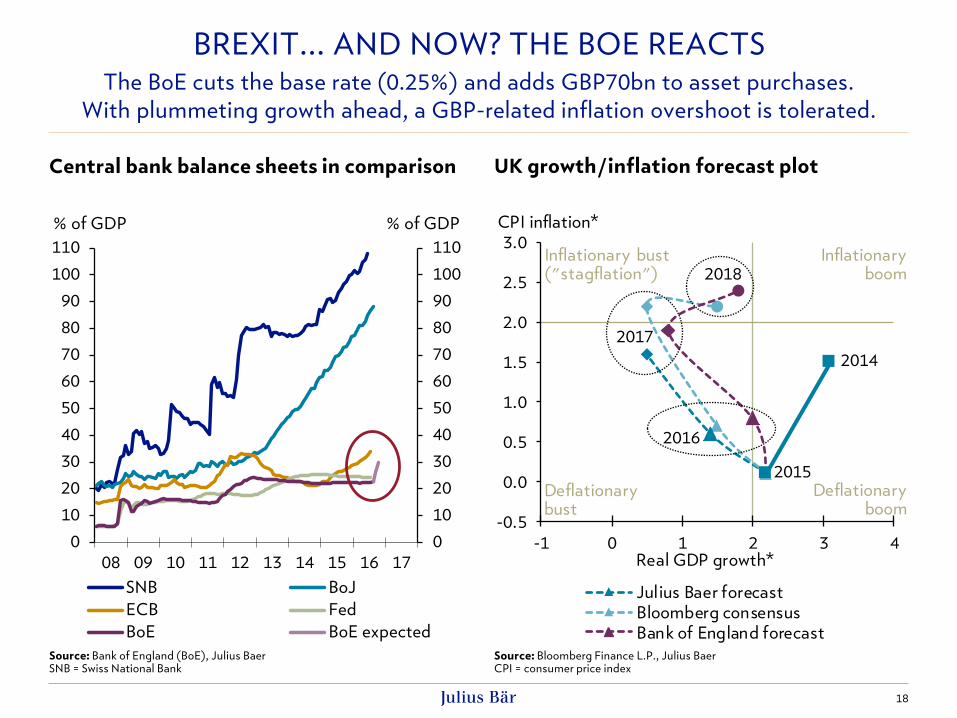

BREXIT... AND NOW? THE BOE REACTS The BoE cuts the base rate (0.25%) and adds GBP70bn to asset purchases.

With plummeting growth ahead, a GBP-related inflation overshoot is tolerated.

Source: Bank of England (BoE), Julius Baer SNB = Swiss National Bank

Source: Bloomberg Finance L.P., Julius Baer CPI = consumer price index

Central bank balance sheets in comparison UK growth/inflation forecast plot

18

0

10

20

30

40

50

60

70

80

90

100

110

0

10

20

30

40

50

60

70

80

90

100

110

08 09 10 11 12 13 14 15 16 17

SNB BoJ

ECB Fed

BoE BoE expected

% of GDP % of GDP

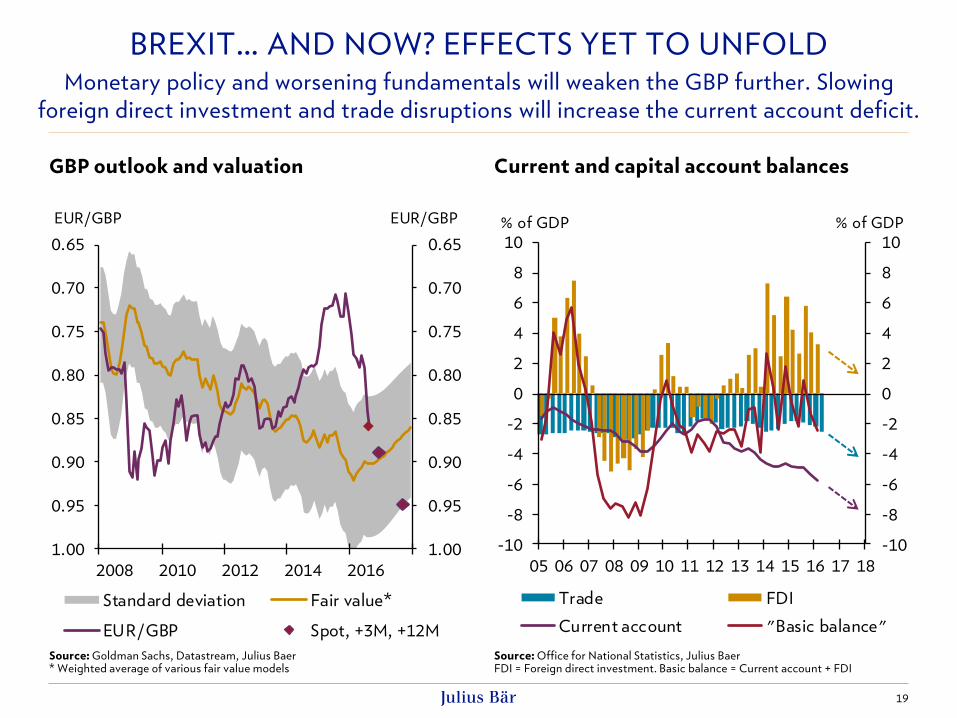

BREXIT… AND NOW? EFFECTS YET TO UNFOLD Monetary policy and worsening fundamentals will weaken the GBP further. Slowing

foreign direct investment and trade disruptions will increase the current account deficit.

Source: Goldman Sachs, Datastream, Julius Baer * Weighted average of various fair value models

Source: Office for National Statistics, Julius Baer FDI = Foreign direct investment. Basic balance = Current account + FDI

GBP outlook and valuation Current and capital account balances

19

0.65

0.70

0.75

0.80

0.85

0.90

0.95

1.00

2008 2010 2012 2014 2016

0.65

0.70

0.75

0.80

0.85

0.90

0.95

1.00

EUR/GBPEUR/GBP

Standard deviation Fair value*

EUR/GBP Spot, +3M, +12M

-10

-8

-6

-4

-2

0

2

4

6

8

10

05 06 07 08 09 10 11 12 13 14 15 16 17 18

-10

-8

-6

-4

-2

0

2

4

6

8

10

% of GDP% of GDP

Trade FDI

Current account "Basic balance"

BREXIT… AND NOW?

20

Fund recommendation - MFS Meridian UK Equity Fund

Fund description • The fund offers exposure to UK equities through a reasonably

diversified portfolio of large and mid-cap stocks.

• The fund is expected to move in line with the underlying

market and to outperform its benchmark over an investment

cycle (Julius Baer fund label: Market Exposure).

• The managers believe that the market is too short-term and

they seek out less volatile high-quality franchises that have

above average growth prospects that the market

underappreciates. They are valuation conscious and will avoid

overpaying for quality or growth prospects.

• We advise buyers of this fund to hedge the currency risk.

Fund performance 5-year performance, in percentage (net)

Low Moderate Considerable High

Lower risk Higher risk

Julius Baer product risk classification

Additional information Provider: MFS Meridian Funds; paying agent: Banque Cantonale de Genève; representative: Carnegie Fund Services S.A.. Please find supporting documents (fund fact sheet, prospectus, annual report, etc.) on www.fundinfo.com, or contact your Julius Baer representative for further information.

As of 20.09.2016; Source: Datastream, Julius Baer, Morningstar

Product facts

Benchmark FTSE All-Share Index

Base Currency GBP

Other Currencies (unhedged) USD

ISIN (GBP Share Class) LU0219431854

ISIN (USD Share Class) LU0219441655

NAV as of 16.09.2016 GBP 8.70

Size as of 31.08.2016 GBP 94.42 mln

Domicile Luxembourg

Launch Date 27.02.2006

TER 2.01%

Sales Registrations CH, DE, AT, IT, SG, HK, others

Supporting documents http://www.fundinfo.com/MFS UK

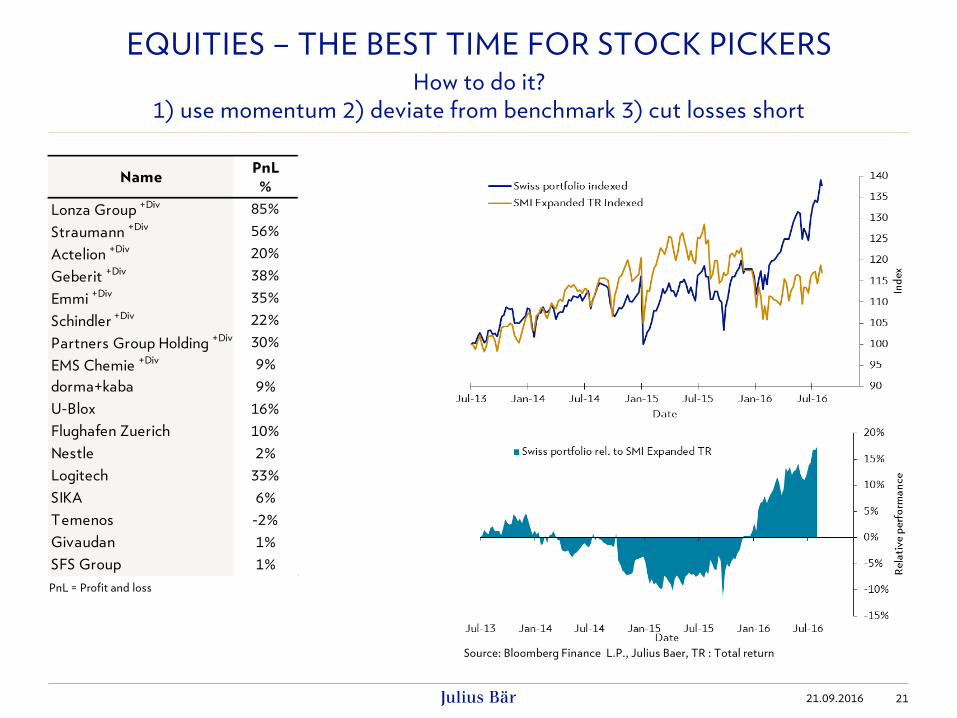

EQUITIES – THE BEST TIME FOR STOCK PICKERS

21.09.2016 21

How to do it?

1) use momentum 2) deviate from benchmark 3) cut losses short

NamePnL

%

Lonza Group +Div 85%

Straumann +Div 56%

Actelion +Div 20%

Geberit +Div 38%

Emmi +Div 35%

Schindler +Div 22%

Partners Group Holding +Div 30%

EMS Chemie +Div 9%

dorma+kaba 9%

U-Blox 16%

Flughafen Zuerich 10%

Nestle 2%

Logitech 33%

SIKA 6%

Temenos -2%

Givaudan 1%

SFS Group 1%

Source: Bloomberg Finance L.P., Julius Baer, TR : Total return

PnL = Profit and loss

EQUITIES – THE BEST TIME FOR STOCK PICKERS

22

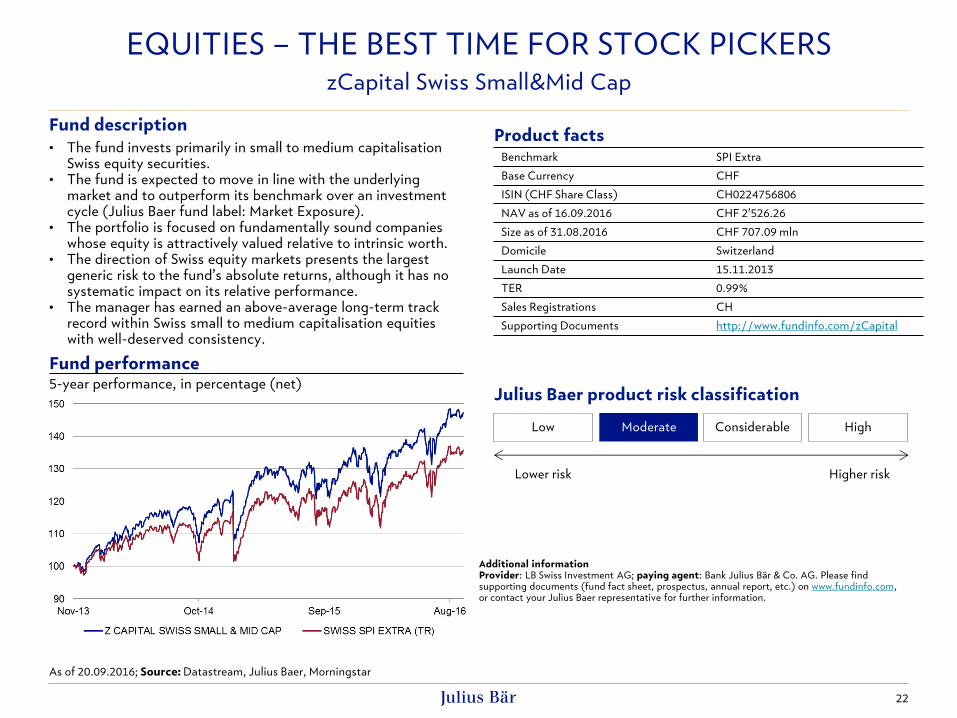

zCapital Swiss Small&Mid Cap

Fund description

• The fund invests primarily in small to medium capitalisation Swiss equity securities.

• The fund is expected to move in line with the underlying market and to outperform its benchmark over an investment cycle (Julius Baer fund label: Market Exposure).

• The portfolio is focused on fundamentally sound companies whose equity is attractively valued relative to intrinsic worth.

• The direction of Swiss equity markets presents the largest generic risk to the fund’s absolute returns, although it has no systematic impact on its relative performance.

• The manager has earned an above-average long-term track record within Swiss small to medium capitalisation equities with well-deserved consistency.

Fund performance 5-year performance, in percentage (net)

Additional information Provider: LB Swiss Investment AG; paying agent: Bank Julius Bär & Co. AG. Please find supporting documents (fund fact sheet, prospectus, annual report, etc.) on www.fundinfo.com, or contact your Julius Baer representative for further information.

Low Moderate Considerable High

Lower risk Higher risk

Julius Baer product risk classification

Benchmark SPI Extra

Base Currency CHF

ISIN (CHF Share Class) CH0224756806

NAV as of 16.09.2016 CHF 2’526.26

Size as of 31.08.2016 CHF 707.09 mln

Domicile Switzerland

Launch Date 15.11.2013

TER 0.99%

Sales Registrations CH

Supporting Documents http://www.fundinfo.com/zCapital

Product facts

As of 20.09.2016; Source: Datastream, Julius Baer, Morningstar

1980 1990 2000 2010 2020

-40

-30

-20

-10

0

10

20

30

40

500

1000

1500

2000

2500

TECHNICAL ANALYSIS – BUY US EQUITIES Long-term buy signal for S&P 500 – secular bull resuming

Source: Bloomberg Finance L.P., Julius Baer

9/21/2016

Comments

Towards the end of May, the

long-term momentum indicator

gave a new buy signal.

Historically, the S&P 500 gained

on average 21% after 12 months.

S&P 500 12-month forward return

Date Return

31.07.1942 38.4%

29.08.1947 4.2%

30.09.1949 24.8%

29.01.1954 40.5%

30.04.1958 32.6%

30.12.1960 23.1%

31.01.1967 6.5%

31.08.1970 21.5%

31.01.1975 31.0%

28.04.1978 5.1%

31.08.1982 37.6%

31.12.1984 26.3%

30.09.1988 28.4%

28.02.1991 12.4%

31.01.1995 35.2%

31.12.2001 -23.4%

29.05.2009 18.5%

Average 21.3%

S&P 500

Momentum

23

TECHNICAL ANALYSIS – BUY US EQUITIES

24

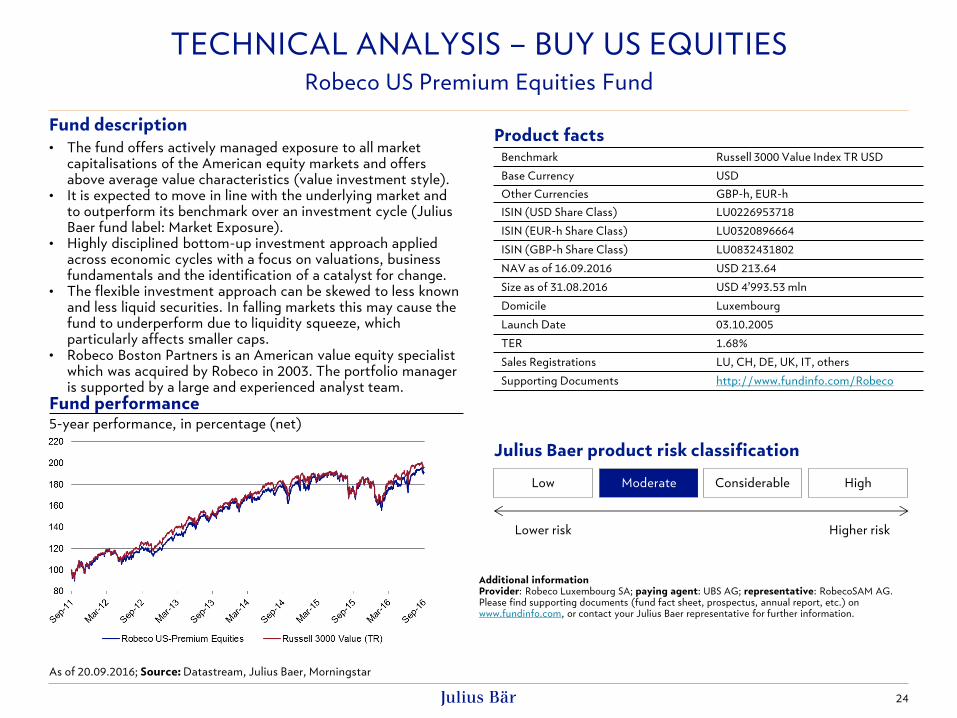

Robeco US Premium Equities Fund

Fund description

• The fund offers actively managed exposure to all market capitalisations of the American equity markets and offers above average value characteristics (value investment style).

• It is expected to move in line with the underlying market and to outperform its benchmark over an investment cycle (Julius Baer fund label: Market Exposure).

• Highly disciplined bottom-up investment approach applied across economic cycles with a focus on valuations, business fundamentals and the identification of a catalyst for change.

• The flexible investment approach can be skewed to less known and less liquid securities. In falling markets this may cause the fund to underperform due to liquidity squeeze, which particularly affects smaller caps.

• Robeco Boston Partners is an American value equity specialist which was acquired by Robeco in 2003. The portfolio manager is supported by a large and experienced analyst team.

Fund performance 5-year performance, in percentage (net)

Additional information Provider: Robeco Luxembourg SA; paying agent: UBS AG; representative: RobecoSAM AG. Please find supporting documents (fund fact sheet, prospectus, annual report, etc.) on www.fundinfo.com, or contact your Julius Baer representative for further information.

Low Moderate Considerable High

Lower risk Higher risk

Julius Baer product risk classification

Benchmark Russell 3000 Value Index TR USD

Base Currency USD

Other Currencies GBP-h, EUR-h

ISIN (USD Share Class) LU0226953718

ISIN (EUR-h Share Class) LU0320896664

ISIN (GBP-h Share Class) LU0832431802

NAV as of 16.09.2016 USD 213.64

Size as of 31.08.2016 USD 4’993.53 mln

Domicile Luxembourg

Launch Date 03.10.2005

TER 1.68%

Sales Registrations LU, CH, DE, UK, IT, others

Supporting Documents http://www.fundinfo.com/Robeco

Product facts

As of 20.09.2016; Source: Datastream, Julius Baer, Morningstar

TECHNICAL ANALYSIS – BUY US EQUITIES

25

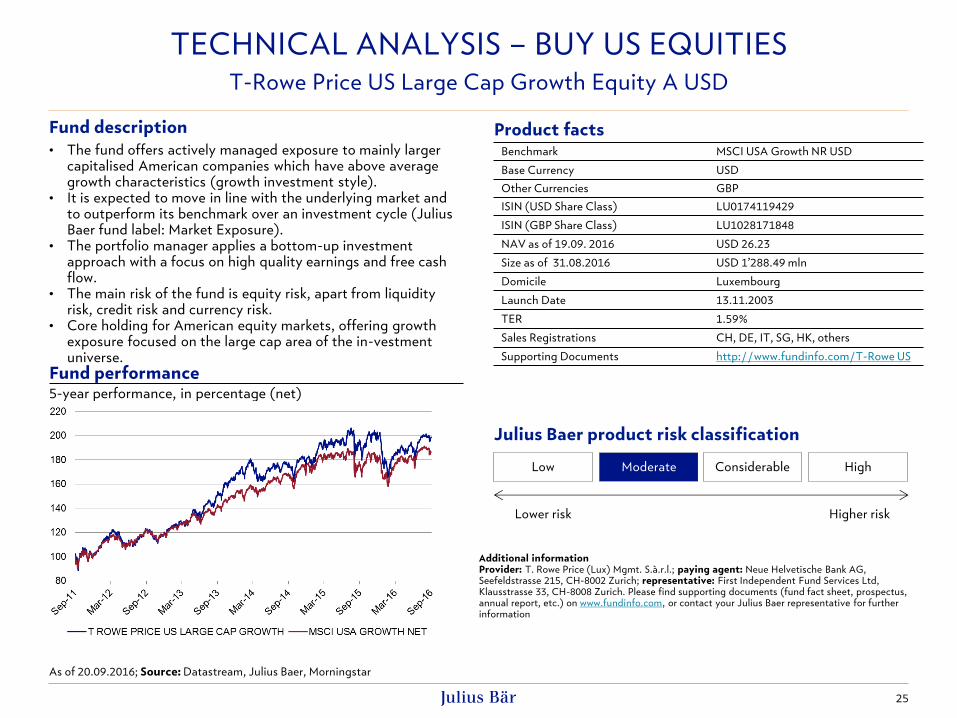

T-Rowe Price US Large Cap Growth Equity A USD

Fund description

• The fund offers actively managed exposure to mainly larger capitalised American companies which have above average growth characteristics (growth investment style).

• It is expected to move in line with the underlying market and to outperform its benchmark over an investment cycle (Julius Baer fund label: Market Exposure).

• The portfolio manager applies a bottom-up investment approach with a focus on high quality earnings and free cash flow.

• The main risk of the fund is equity risk, apart from liquidity risk, credit risk and currency risk.

• Core holding for American equity markets, offering growth exposure focused on the large cap area of the in-vestment universe.

Fund performance 5-year performance, in percentage (net)

Additional information Provider: T. Rowe Price (Lux) Mgmt. S.à.r.l.; paying agent: Neue Helvetische Bank AG, Seefeldstrasse 215, CH-8002 Zurich; representative: First Independent Fund Services Ltd, Klausstrasse 33, CH-8008 Zurich. Please find supporting documents (fund fact sheet, prospectus, annual report, etc.) on www.fundinfo.com, or contact your Julius Baer representative for further information

Low Moderate Considerable High

Lower risk Higher risk

Julius Baer product risk classification

Benchmark MSCI USA Growth NR USD

Base Currency USD

Other Currencies GBP

ISIN (USD Share Class) LU0174119429

ISIN (GBP Share Class) LU1028171848

NAV as of 19.09. 2016 USD 26.23

Size as of 31.08.2016 USD 1’288.49 mln

Domicile Luxembourg

Launch Date 13.11.2003

TER 1.59%

Sales Registrations CH, DE, IT, SG, HK, others

Supporting Documents http://www.fundinfo.com/T-Rowe US

Product facts

As of 20.09.2016; Source: Datastream, Julius Baer, Morningstar

26

Emerging market equities – favour Asia over Latam and EMEA

• Our Strategy Research has turned tactically more optimistic and has recently upgraded

emerging market equities from neutral to overweight.

• Our top-down investment rationale is that first, the US central bank will not raise rates in H2

2016, second, more funds will flow from Europe to emerging markets (due to political

uncertainty) and third, the earnings recovery will continue while valuations are attractive.

• Within Emerging Markets, Asia remains our favourite region for several reasons:

Asian governments have still room for fiscal and monetary stimulus measures.

Asia would be relatively less affected if the Fed raised rates over the coming months.

Political and structural reforms are under way.

Many of the emerging Asia countries are beneficiaries of lower commodity prices.

Valuation and earnings dynamics have turned positive over the last quarters.

Relative to the rally in other emerging markets, the region is lagging and valuations are

cheaper.

• We see most positive risk/return in China, Taiwan, India, Indonesia, Malaysia and Vietnam.

• We recommend investors buy into a broad-based emerging Asia investment vehicle to profit

from the current investment opportunity which we consider a short-term call (3-6 months).

EMERGING MARKETS (EM) – REASONS TO FAVOUR ASIA

Emerging Asian markets remain our favourite region

Investment rationale

Emerging Asian markets remain our

favourite region

1) Asian governments have room for fiscal

and monetary stimulus measures

2) Reforms are under way

3) Beneficiaries of lower commodity prices

4) Valuations and earnings dynamics

5) The region is lagging and valuations

have room to expand

Positive risk/return

• China, Taiwan, India, Indonesia,

Malaysia, Vietnam

27

EMERGING MARKETS (EM) – REASONS TO FAVOUR ASIA Focus on countries with a sound macroeconomic backdrop, less vulnerable to US

interest-rate increases, with attractive valuations and positive earnings dynamics.

Source: Bloomberg Finance L.P., Julius Baer; Ccy = Currency

Since 2012, the JP Morgan EM ccy index is -27%, the JPM Asia Dollar -7% and oil -60%

20

30

40

50

60

70

80

90

100

110

120

Dec 11 Oct 12 Aug 13 Jun 14 Apr 15 Feb 16

Index

Generic ICE brent futures -60.8%JPMorgan EM ccy index -26.6%JPMorgan Asia Dollar index -6.6%

Vietnam: Julius Baer makes no offering in local markets.

Taiwan: Julius Baer’s offering in the local market is restricted.

EMERGING MARKETS (EM) ASIA – RECOMMENDED FUND

28

Hermes Asia ex Japan Equity Fund

Fund description

• This is a flexible and purely bottom-up driven Asian equity fund, which invests in the entire market capitalisation spectrum of the Asian stock markets.

• The fund is targeting to be fully invested at all times with the aim to outperform its benchmark over an investment cycle.

• The manager‘s investment philosophy focuses on under-researched and out of fashion stocks, that offer value over a medium to long term horizon.

• Hermes is a UK investment boutique. The fund is managed by an experienced portfolio manager with support of a decent in-house analyst team.

Fund performance 5-year performance, in percentage (net)

Low Moderate Considerable High

Lower risk Higher risk

Julius Baer product risk classification

Product facts

Benchmark MSCI Asia ex Japan NR (USD)

Base Currency USD (risk in Asian local currencies)

Other Currencies EUR-h, CHF-h

ISIN (USD Share Class) IE00BBL4VW61

ISIN (EUR-h Share Class) IE00BBL4VX78

ISIN (CHF-h Share Class) IE00BBL4VZ92

NAV as of 19.09. 2016 USD 2.49

Size as of 31.08.2016 USD 2’097.46 mln

Domicile Ireland

Launch Date 01.10.2013

TER 1.60%

Sales Registrations LU, CH, DE, UK, FR, others

Supporting Documents http://www.fundinfo.com/Hermes

Additional information Provider: Hermes Investment Management Ltd.; paying agent: NPB New Private Bank Ltd.; representative: Acolin Fund Services AG. Please find supporting documents (fund fact sheet, prospectus, annual report, etc.) on www.fundinfo.com, or contact your Julius Baer representative for further information. * Fund performance before launch calculated on the base of an institutional tranche following exactly the same investment approach.

As of 20.09.2016; Source: Datastream, Julius Baer, Morningstar

• By 2030, more than a quarter (26%) of global

consumption growth will be generated by the

working-age population of emerging Asia

(15–59 years old).

• Chinese and Indian millennials will represent most

of this essential consumer cohort. They are young,

digital natives, technologically savvy, disloyal to

brands and endlessly adaptable.

• We believe understanding this generation – which

will be at its peak consumption and household

formation point in 15 years – will be crucial for

investors in order to reap the fruits of the next two

decades’ worth of global consumption growth.

• We highlight six key trends on which they will

focus their consumption expenditure: premium

consumer goods, digital commerce, media &

entertainment, travel & tourism, banking &

insurance, fitness & sportswear.

• Companies, which are able to cater and adapt to

Chinese and Indian millennials’ consumption

preferences, will be the leaders of tomorrow.

29

ASIA’S YOUTH – THE TASTES THAT MATTER Scale, weight, changing tastes: Understanding the essential consumer of the future

Source: United Nations, US Census Bureau, Bank of America Merrill Lynch, Goldman Sachs, Julius Baer; bn=billion, EMs=emerging markets, DMs=developed markets; Note: Generation Z, 2000–present, Millennials, 1980–2000; Generation X, 1965–79; Baby Boomers, 1945–64; Greatest Generation, 1931–44.

86% of millennials in EMs, 34% in China and India: world population by generation (2015)

0.8

1.1

0.4

2.0

1.4

1.2

0.3

0%

20%

40%

60%

80%

100%

Population (bn)

GreatestGeneration

Baby Boomers

Gen-X

Gen-Z

Millennials(DMs)

Millennials(other EMs)

Millennials(China & India)

2.3bn millennials

Share (%)

ASIA’S YOUTH – THE TASTES THAT MATTER

30

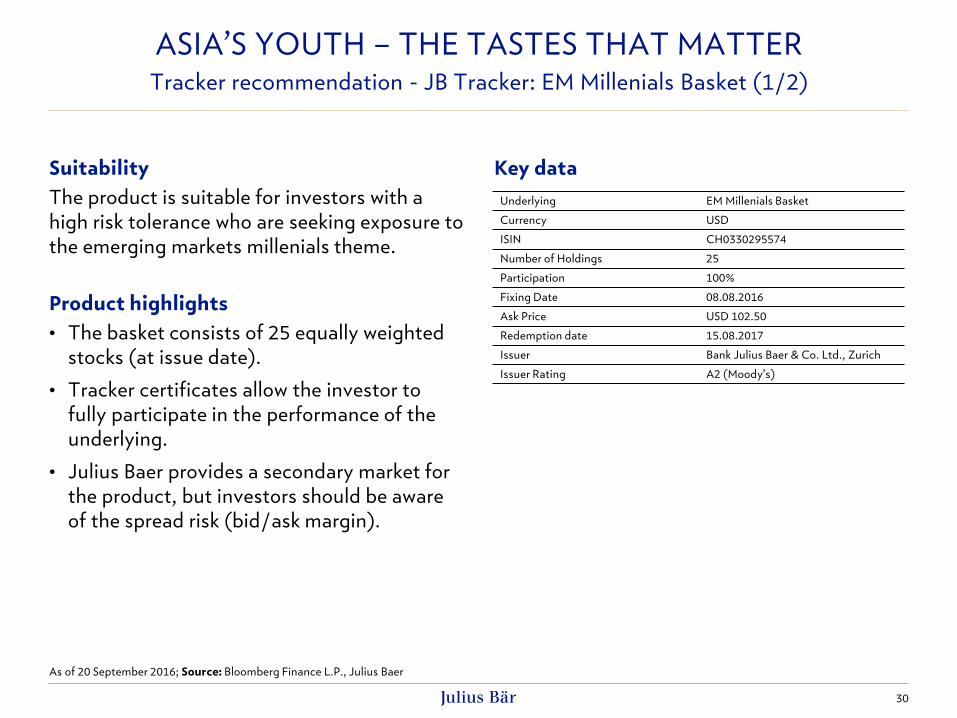

Tracker recommendation - JB Tracker: EM Millenials Basket (1/2)

Suitability

The product is suitable for investors with a

high risk tolerance who are seeking exposure to

the emerging markets millenials theme.

Product highlights

• The basket consists of 25 equally weighted

stocks (at issue date).

• Tracker certificates allow the investor to

fully participate in the performance of the

underlying.

• Julius Baer provides a secondary market for

the product, but investors should be aware

of the spread risk (bid/ask margin).

Key data

As of 20 September 2016; Source: Bloomberg Finance L.P., Julius Baer

Underlying EM Millenials Basket

Currency USD

ISIN CH0330295574

Number of Holdings 25

Participation 100%

Fixing Date 08.08.2016

Ask Price USD 102.50

Redemption date 15.08.2017

Issuer Bank Julius Baer & Co. Ltd., Zurich

Issuer Rating A2 (Moody’s)

ASIA’S YOUTH – THE TASTES THAT MATTER

31

Tracker recommendation - JB Tracker: EM Millennials Basket (2/2)

Constituents of the Basket

As of 20 September 2016; Source: Bloomberg Finance L.P., Julius Baer

Company ISIN Sector Currency Price Julius Baer

Target Price

FY1

P/E

Div. yield Julius Baer

Research Rating

Alibaba Grp-Adr US01609W1027 Information Technology USD 103.03 108.00 31.5 - Buy

Baidu Inc-Sp Adr US0567521085 Information Technology USD 184.74 190.00 39.7 - Buy

Naspers Ltd-N ZAE000015889 Consumer Discretionary ZAr 239,931 - 44.7 0.29% not rated

Tencent KYG875721634 Information Technology HKD 209.00 210.00 38.2 0.30% Buy

Yandex Nv-A NL0009805522 Information Technology USD 20.77 - 32.0 - not rated

Amorepacific Gro KR7002790004 Consumer Staples KRW 158,000 - 32.9 - not rated

Cp All Pcl-Nvdr TH0737010R15 Consumer Staples THB 60.00 - 33.1 - not rated

Imax China Holdi KYG476341030 Consumer Discretionary HKD 39.00 - 35.2 0.42% Hold

Lg Household & H KR7051900009 Consumer Staples KRW 973,000 - 25.8 0.62% not rated

Matahari Dept ID1000113301 Consumer Discretionary IDR 18,900 - 25.1 2.50% not rated

Universal Robina PHY9297P1004 Consumer Staples PHP 184.80 210.00 28.2 1.85% Hold

Ambev Sa BRABEVACNOR1 Consumer Staples BRL 19.45 - 21.9 4.06% not rated

Coca-Cola Icecek TRECOLA00011 Consumer Staples TRY 37.66 - 24.9 0.92% not rated

Fomento Econ-Ubd MXP320321310 Consumer Staples MXN 168.77 - 27.5 1.52% not rated

Anta Sports Prod KYG040111059 Consumer Discretionary HKD 20.40 - 18.6 3.73% not rated

Eclat Textile Co TW0001476000 Consumer Discretionary TWD 363.50 - 24.3 2.76% not rated

Hdfc Bank-Adr US40415F1012 Financials USD 71.58 - 34.3 0.79% not rated

Ping An-H CNE1000003X6 Financials HKD 42.40 49.00 11.2 1.46% Buy

Qualicorp Sa BRQUALACNOR6 Health Care BRL 19.88 - 14.6 3.05% not rated

Kroton BRKROTACNOR9 Consumer Discretionary BRL 15.10 - 13.3 2.52% not rated

New Oriental-Adr US6475811070 Consumer Discretionary USD 46.56 - 26.1 0.39% not rated

Airports of Thailand TH0765010R16 Industrials THB 395.00 400.0 30.8 - Hold

TAV Havalimanlari Holding AS TRETAVH00018 Industrials TRY 11.23 - 7.7 6.69% not rated

Minor Inter-Nvdr TH0128010R17 Consumer Discretionary THB 39.00 - 29.8 - not rated

Ctrip.Com-Adr US22943F1003 Consumer Discretionary USD 43.77 50.00 146.2 - Buy

ASIA’S YOUTH – THE TASTES THAT MATTER

32

Mirae Asset Asia Great Consumer Equity

Fund description

• This is a flexible and unconstrained managed Asian equity fund, which invests in Asian consumer related stocks across the market capitalisation spectrum.

• The fund is expected to move in line with the underlying market and to outperform its benchmark over an investment cycle (Julius Baer fund label: Market Exposure).

• The manager‘s investment philosophy focuses on bottom up stock selection to identify areas in Asia, which profit form the fast growing domestic consumption and deliver above average returns.

• Since the manager intends to be fully invested in Asian stocks at all times, the fund is exposed to market risk.

• The high conviction portfolio of around 30 to 40 names is mainly composed by a bottom up investment approach with a sector / macro overlay.

Fund performance 5-year performance, in percentage (net)

Low Moderate Considerable High

Lower risk Higher risk

Julius Baer product risk classification

Additional information Provider: Mirae Asset Global Investments Co Ltd; paying agent: Notenstein Privatbank AG; representative: 1741 Asset Management AG. Please find supporting documents (fund fact sheet, prospectus, annual report, etc.) on www.fundinfo.com, or contact your Julius Baer representative for further information.

Benchmark MSCI Asia ex Japan NR USD

Base Currency USD

Other Currencies EUR-h, EUR, GBP

ISIN (USD Share Class) LU0593848301

ISIN (EUR-h Share Class) LU0593848723

ISIN (GBP-h Share Class) LU0853239118

NAV as 19.09.2016 USD 12.91

Size as of 31.07.2016 USD 737.95 mln

Domicile Luxembourg

Launch Date 07.06.2011

TER 1.73%

Sales Registration CH, DE, UK, IT, SG, HK, others

Supporting Documents https://www.fundinfo.com/Mirae

Product facts

As of 20.09.2016; Source: Datastream, Julius Baer, Morningstar

33

GLOBAL EMERGING MARKETS WMP EM Established Leaders Fund

Fund performance 5-year performance, in percentage (net)

Product facts

Additional information Provider: WMPartners Vermögensverwaltungs AG; paying agent: Bank Julius Baer & Co. AG; representative: Swiss & Global Asset Mgmt. AG. Please find supporting documents (fund fact sheet, prospectus, annual report, etc.) on www.fundinfo.com, or contact your Julius Baer representative for further information.

Fund highlights

• The fund’s focus is mainly on subsidiaries of high-quality

multinational concerns (MNCs) or companies with strong ties

or joint ventures with MNCs based in emerging markets.

• The approach combines the growth opportunities in emerging

markets with the quality of multinationals.

• By applying this approach the fund managed to substantially

reduce the downside participation while achieving decent

upside since inception.

• The fund is always fully invested and therefore volatile stock

markets can lead to declines in the fund.

Benchmark MSCI EM PR USD

Base Currency CHF (local EM currencies)

Other Currencies USD, EUR

ISIN (USD Share Class) LU1328691545

ISIN (EUR Share Class) LU1144941785

ISIN (CHF Share Class) LU0469452717

NAV as of 16.09.2016 CHF 124.70

Size as of 31.08.2016 CHF 86.94 mln

Domicile Luxembourg

Launch Date 31.05.2010

TER 1.83%

Sales Registrations LU, CH, DE, AT

Supporting Documents http://www.fundinfo.com/WMP EM

Julius Baer product risk classification

Low Moderate Considerable High

Lower risk Higher risk

As of 20.09.2016; Source: Datastream, Julius Baer, Morningstar

GLOBAL EMERGING MARKETS

34

Fund recommendations - Polar Emerging Markets Income Fund

Fund description

• The fund offers actively managed exposure to global emerging market equities managed with a focus on high dividend payments.

• Combination of a bottom-up based investment approach with a macroeconomic overlay aims for a portfolio dividend yield in excess of 3.5%.

• The investment approach tends to be skewed to less known and less liquid securities. In falling markets, this may cause the fund to underperform due to the liquidity squeeze, which particularly affects companies in emerging markets or with smaller market capitalisation.

• The basis of the portfolio (60%) consists of growth companies with an established dividend culture. Up to 25% of the portfolio will be allocated to pure high dividend stocks and up to 15% will be allocated to the most undervalued stocks.

Low Moderate Considerable High

Lower risk Higher risk

Julius Baer product risk classification

Fund performance 5-year performance, in percentage (net)

Additional information Provider: Polar Capital LLP; paying agent: BNP Paribas Securities Services, Paris, succursale de Zurich; representative: BNP Paribas Securities Services, Paris, succursale de Zurich. Please find supporting documents (fund fact sheet, prospectus, annual report, etc.) on www.fundinfo.com, or contact your Julius Baer representative for further information.

Product facts

Benchmark MSCI EM TR USD

Base Currency USD (local EM currencies)

Other Currencies GBP, EUR

ISIN (USD Share Class) IE00B4VVWP88

ISIN (EUR Share Class) IE00B4WZTL41

ISIN (GBP Share Class) IE00B4YDSX18

NAV as of 16.09.2016 USD 9.88

Size as of 31.08.2016 USD 309.44 mln

Domicile Ireland

Launch Date 21.11.2011

TER 1.71%

Sales Registrations CH, UK, DE, IT, SG, others

Supporting Documents http://www.fundinfo.com/Polar EM

As of 20.09.2016; Source: Datastream, Julius Baer, Morningstar

• The continued evolution of finance and

technology is providing an opportunity-filled

investment landscape in payments, lending,

capital markets and asset and wealth

management.

• FinTech (financial technology) companies are a

growing threat to slow-moving financials, but

incumbents are fighting back with increasing in-

house development and external investments.

• From a risk/return perspective, we favour:

Payment networks, which are central to

expanding electronic payments penetration.

Payment processors, which help merchants

to drive better returns by expanding their

payments solutions.

Solutions providers (software &

information) to financial companies, since

financials need to leverage technology and

information services to remain competitive.

• Avoid marketplace lending at this juncture,

given risk/return profile.

35

FINTECH – AN OPPORTUNITY, NOT A THREAT The global financial industry is embarking on a new cycle of innovation. We favour

payments networks & processors, and solutions providers to financial institutions.

Source: CB Insights, KPMG, Credit Suisse, Citigroup, Julius Baer;

P2P=peer-to-peer, SME=Small and medium-sized enterprises

Ballooning investments into FinTech

Fintech

Payments

E.g. mobile payments, P2P money transfer

Lending

E.g. P2P lending, SME

financing

Asset & Wealth

Management

e.g. Robo-advisory

Capital Markets

e.g. Crowdfunding

Software and information providers

1.8 2.4 2.83.9

12.2

19.1

0

200

400

600

800

1'000

1'200

1'400

0

5

10

15

20

25

2010 2011 2012 2013 2014 2015

DealsUSD bn

Overall global FinTech investments (l.h.s.)

Overall FinTech deals (r.h.s.)

FINTECH – AN OPPORTUNITY, NOT A THREAT

36

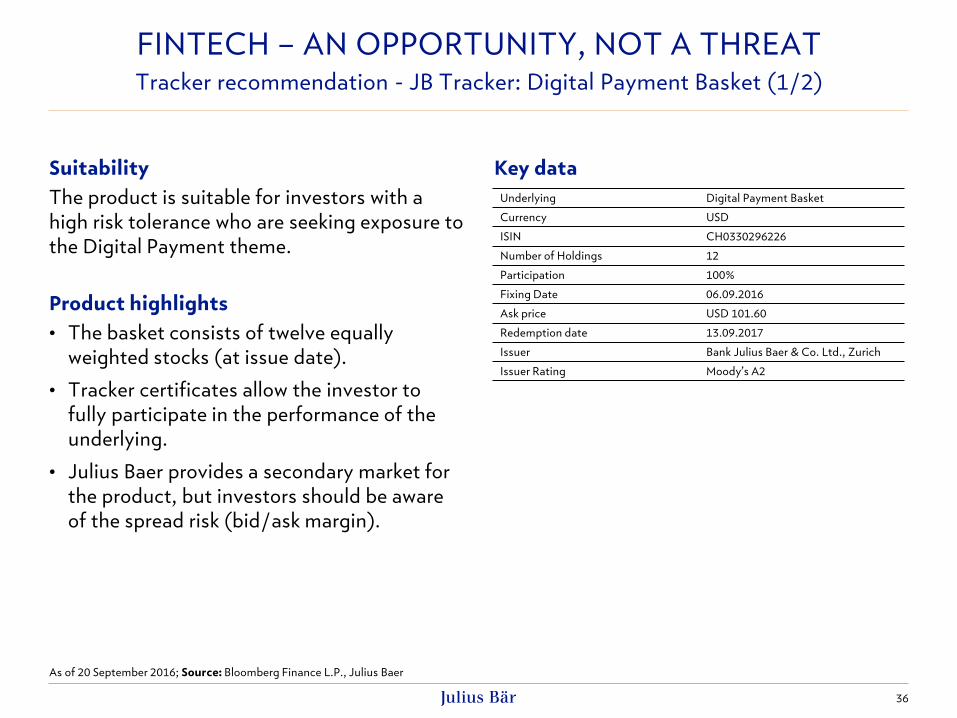

Tracker recommendation - JB Tracker: Digital Payment Basket (1/2)

Suitability

The product is suitable for investors with a

high risk tolerance who are seeking exposure to

the Digital Payment theme.

Product highlights

• The basket consists of twelve equally

weighted stocks (at issue date).

• Tracker certificates allow the investor to

fully participate in the performance of the

underlying.

• Julius Baer provides a secondary market for

the product, but investors should be aware

of the spread risk (bid/ask margin).

Key data

As of 20 September 2016; Source: Bloomberg Finance L.P., Julius Baer

Underlying Digital Payment Basket

Currency USD

ISIN CH0330296226

Number of Holdings 12

Participation 100%

Fixing Date 06.09.2016

Ask price USD 101.60

Redemption date 13.09.2017

Issuer Bank Julius Baer & Co. Ltd., Zurich

Issuer Rating Moody’s A2

FINTECH – AN OPPORTUNITY, NOT A THREAT

37

Tracker recommendation - JB Tracker: Digital Payment Basket (2/2)

Constituents of the Basket

As of 20 September 2016; Source: Bloomberg Finance L.P., Julius Baer

Company ISIN Country Currency Price Julius Baer

Target Price

FY1

P/E

Div. yield Julius Baer

Research Rating

Alibaba US01609W1027 China USD 101.64 108.00 31.1 - Buy

Alphabet Inc. US02079K3059 United States USD 799.78 910.00 23.4 - Buy

Apple US0378331005 United States USD 113.76 95.00 13.8 1.92% Hold

Global Payments US37940X1028 United States USD 74.33 - 21.4 0.05% -

Ingenico FR0000125346 France EUR 80.19 106.00 19.1 1.71% Hold

Mastercard US57636Q1040 United States USD 100.24 110.00 27.7 0.76% Buy

NXP Semiconductors NL0009538784 Netherlands USD 82.67 98.00 14.5 - Buy

PayPal Holdings US70450Y1038 United States USD 40.00 39.00 26.8 - Hold

Vantiv US92210H1059 United States USD 54.08 57.00 20.3 - Hold

Visa US92826C8394 United States USD 82.54 90.00 29.6 0.68% Buy

Worldline FR0011981968 France EUR 28.09 28.80 28.1 0.73% Hold

Worldpay Group GB00BYYK2V80 United Kingdom GBp 303.50 310.00 25.9 0.69% Buy

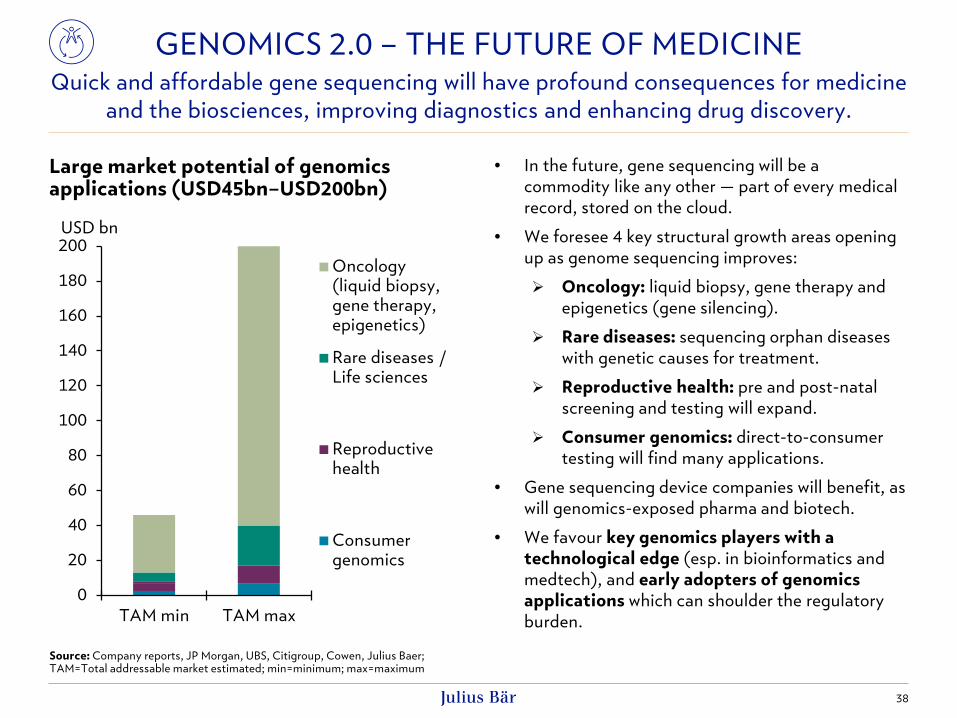

• In the future, gene sequencing will be a

commodity like any other — part of every medical

record, stored on the cloud.

• We foresee 4 key structural growth areas opening

up as genome sequencing improves:

Oncology: liquid biopsy, gene therapy and

epigenetics (gene silencing).

Rare diseases: sequencing orphan diseases

with genetic causes for treatment.

Reproductive health: pre and post-natal

screening and testing will expand.

Consumer genomics: direct-to-consumer

testing will find many applications.

• Gene sequencing device companies will benefit, as

will genomics-exposed pharma and biotech.

• We favour key genomics players with a

technological edge (esp. in bioinformatics and

medtech), and early adopters of genomics

applications which can shoulder the regulatory

burden.

38

GENOMICS 2.0 – THE FUTURE OF MEDICINE Quick and affordable gene sequencing will have profound consequences for medicine

and the biosciences, improving diagnostics and enhancing drug discovery.

Source: Company reports, JP Morgan, UBS, Citigroup, Cowen, Julius Baer; TAM=Total addressable market estimated; min=minimum; max=maximum

Large market potential of genomics applications (USD45bn–USD200bn)

0

20

40

60

80

100

120

140

160

180

200

TAM min TAM max

USD bn

Oncology(liquid biopsy,gene therapy,epigenetics)

Rare diseases /Life sciences

Reproductivehealth

Consumergenomics

GENOMICS 2.0 – THE FUTURE OF MEDICINE

39

Tracker recommendation - JB Tracker: Genomics Basket (1/2)

Suitability

The product is suitable for investors with a

high risk tolerance who are seeking exposure to

the Genomics theme.

Product highlights

• The basket consists of fifteen equally

weighted stocks (at issue date).

• Tracker certificates allow the investor to

fully participate in the performance of the

underlying.

• Julius Baer provides a secondary market for

the product, but investors should be aware

of the spread risk (bid/ask margin).

Key data

As of 20 September 2016; Source: Bloomberg Finance L.P., Julius Baer

Underlying Genomics Basket

Currency USD

ISIN CH0330296028

Number of Holdings 15

Participation 100%

Fixing Date 25.08.2016

Ask price USD 108.20

Redemption date 01.09.2017

Issuer Bank Julius Baer & Co. Ltd., Zurich

Issuer Rating A2 (Moody’s)

GENOMICS 2.0 – THE FUTURE OF MEDICINE

40

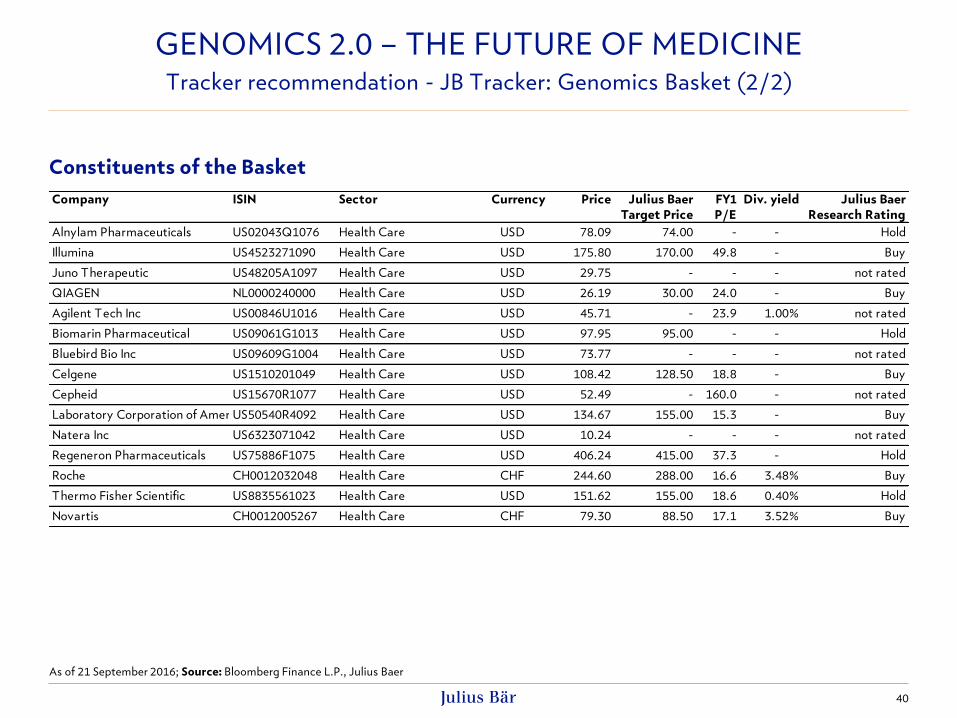

Tracker recommendation - JB Tracker: Genomics Basket (2/2)

Constituents of the Basket

As of 21 September 2016; Source: Bloomberg Finance L.P., Julius Baer

Company ISIN Sector Currency Price Julius Baer

Target Price

FY1

P/E

Div. yield Julius Baer

Research Rating

Alnylam Pharmaceuticals US02043Q1076 Health Care USD 78.09 74.00 - - Hold

Illumina US4523271090 Health Care USD 175.80 170.00 49.8 - Buy

Juno Therapeutic US48205A1097 Health Care USD 29.75 - - - not rated

QIAGEN NL0000240000 Health Care USD 26.19 30.00 24.0 - Buy

Agilent Tech Inc US00846U1016 Health Care USD 45.71 - 23.9 1.00% not rated

Biomarin Pharmaceutical US09061G1013 Health Care USD 97.95 95.00 - - Hold

Bluebird Bio Inc US09609G1004 Health Care USD 73.77 - - - not rated

Celgene US1510201049 Health Care USD 108.42 128.50 18.8 - Buy

Cepheid US15670R1077 Health Care USD 52.49 - 160.0 - not rated

Laboratory Corporation of AmericaUS50540R4092 Health Care USD 134.67 155.00 15.3 - Buy

Natera Inc US6323071042 Health Care USD 10.24 - - - not rated

Regeneron Pharmaceuticals US75886F1075 Health Care USD 406.24 415.00 37.3 - Hold

Roche CH0012032048 Health Care CHF 244.60 288.00 16.6 3.48% Buy

Thermo Fisher Scientific US8835561023 Health Care USD 151.62 155.00 18.6 0.40% Hold

Novartis CH0012005267 Health Care CHF 79.30 88.50 17.1 3.52% Buy

41

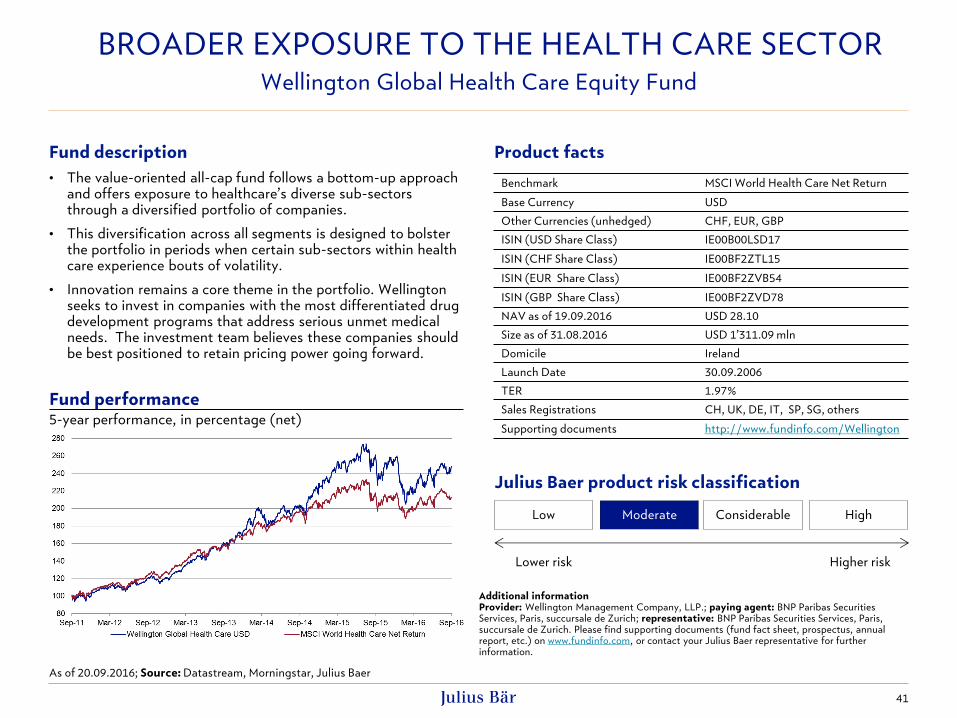

Fund description

• The value-oriented all-cap fund follows a bottom-up approach and offers exposure to healthcare’s diverse sub-sectors through a diversified portfolio of companies.

• This diversification across all segments is designed to bolster the portfolio in periods when certain sub-sectors within health care experience bouts of volatility.

• Innovation remains a core theme in the portfolio. Wellington seeks to invest in companies with the most differentiated drug development programs that address serious unmet medical needs. The investment team believes these companies should be best positioned to retain pricing power going forward.

Fund performance 5-year performance, in percentage (net)

Benchmark MSCI World Health Care Net Return

Base Currency USD

Other Currencies (unhedged) CHF, EUR, GBP

ISIN (USD Share Class) IE00B00LSD17

ISIN (CHF Share Class) IE00BF2ZTL15

ISIN (EUR Share Class) IE00BF2ZVB54

ISIN (GBP Share Class) IE00BF2ZVD78

NAV as of 19.09.2016 USD 28.10

Size as of 31.08.2016 USD 1’311.09 mln

Domicile Ireland

Launch Date 30.09.2006

TER 1.97%

Sales Registrations CH, UK, DE, IT, SP, SG, others

Supporting documents http://www.fundinfo.com/Wellington

BROADER EXPOSURE TO THE HEALTH CARE SECTOR Wellington Global Health Care Equity Fund

Additional information Provider: Wellington Management Company, LLP.; paying agent: BNP Paribas Securities Services, Paris, succursale de Zurich; representative: BNP Paribas Securities Services, Paris, succursale de Zurich. Please find supporting documents (fund fact sheet, prospectus, annual report, etc.) on www.fundinfo.com, or contact your Julius Baer representative for further information.

Product facts

As of 20.09.2016; Source: Datastream, Morningstar, Julius Baer

Low Moderate Considerable High

Lower risk Higher risk

Julius Baer product risk classification

• People’s old dream was to own a home and

two cars, while their new dream is to

preserve wealth and have a safe job – this is

the new economic climate amongst the

middle-income group.

• Developed markets’ middle class vs.

emerging markets’ middle class.

• Companies which can offer discounts that

are unmatchable by their ‘non-budget’

competitors, while maintaining the

perception of value for money should

benefit.

• Prime examples: Primark (Associated

British Foods), Ryanair, TJX.

42

CONSUMER: AFFORDABLE LUXURY & BARGAIN HUNTING Moving down on the income ladder

Source: Datastream, Julius Baer; AC = All Country

Bargain hunting proving value

0

50

100

150

200

250

300

2011 2012 2013 2014 2015 2016

Index, USD

Bargain hunting index (Total Return)

MSCI AC World index (Total Return)

• The exponentially growing middle class,

fuelled by lower oil prices, coupled with

globalisation and technological changes,

boosts the consumption of premium goods

and services.

• Both established and new companies with

an appealing image should profit from

these developments through even greater

brand awareness and sales.

• Prime examples: L’Oreal, Heineken or Lindt

& Sprüngli

43

CONSUMER: AFFORDABLE LUXURY & BARGAIN HUNTING Moving up on the income ladder

Source: Datastream, Julius Baer

Affordable luxury on the loose

0

50

100

150

200

250

300

2011 2012 2013 2014 2015 2016

Index, USD

Affordable luxury index (Total Return)

MSCI AC World index (Total Return)

Affordable luxury (Total Return)

CONSUMER: AFFORDABLE LUXURY & BARGAIN HUNTING

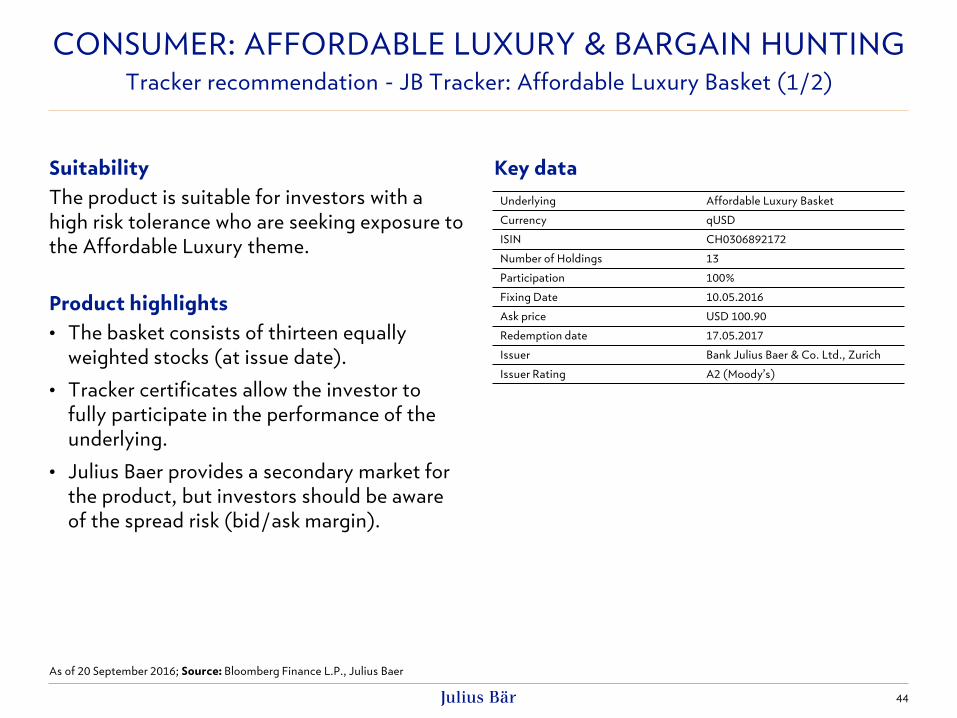

44

Tracker recommendation - JB Tracker: Affordable Luxury Basket (1/2)

Suitability

The product is suitable for investors with a

high risk tolerance who are seeking exposure to

the Affordable Luxury theme.

Product highlights

• The basket consists of thirteen equally

weighted stocks (at issue date).

• Tracker certificates allow the investor to

fully participate in the performance of the

underlying.

• Julius Baer provides a secondary market for

the product, but investors should be aware

of the spread risk (bid/ask margin).

Key data

As of 20 September 2016; Source: Bloomberg Finance L.P., Julius Baer

Underlying Affordable Luxury Basket

Currency qUSD

ISIN CH0306892172

Number of Holdings 13

Participation 100%

Fixing Date 10.05.2016

Ask price USD 100.90

Redemption date 17.05.2017

Issuer Bank Julius Baer & Co. Ltd., Zurich

Issuer Rating A2 (Moody’s)

CONSUMER: AFFORDABLE LUXURY & BARGAIN HUNTING

45

Tracker recommendation - JB Tracker: Affordable Luxury Basket (2/2)

Constituents of the Basket

As of 20 September 2016; Source: Bloomberg Finance L.P., Julius Baer

Company ISIN Country Currency Price Julius Baer

Target Price

FY1

P/E

Div. yield Julius Baer

Research Rating

Adidas DE000A1EWWW0 Germany EUR 151.70 150.00 31.3 1.32% Hold

British American Tobacco GB0002875804 United Kingdom GBp 4,814 5,300 19.7 3.44% Buy

Comcast US20030N1019 United States USD 65.85 75.00 18.8 1.68% Buy

Constellation Brands US21036P1084 United States USD 162.68 180.00 25.9 0.97% Buy

Estée Lauder US5184391044 United States USD 87.38 100.00 25.2 1.51% Buy

H&M SE0000106270 Sweden SEK 247.10 310.00 21.4 3.93% Buy

Heineken NL0000009165 Netherlands EUR 78.82 91.00 21.5 1.71% Buy

Lindt & Sprüngli CH0010570767 Switzerland CHF 5650.00 6500.00 32.1 1.57% Buy

L'Oreal FR0000120321 France EUR 167.25 195.00 26.0 1.98% Buy

Pernod Ricard FR0000120693 France EUR 104.30 110.00 19.1 1.88% Hold

Reckitt Benckiser GB00B24CGK77 United Kingdom GBp 7,252 7,500 24.7 2.07% Hold

Starbucks US8552441094 United States USD 53.01 60.00 28.0 1.54% Hold

Under Armour US9043111072 United States USD 38.74 48.00 65.5 - Buy

CONSUMER: AFFORDABLE LUXURY & BARGAIN HUNTING

46

Tracker recommendation - JB Tracker: Bargain Hunting Basket (1/2)

Suitability

The product is suitable for investors with a

high risk tolerance who are seeking exposure to

the Bargain Hunting theme.

Product highlights

• The basket consists of ten equally weighted

stocks (at issue date).

• Tracker certificates allow the investor to

fully participate in the performance of the

underlying.

• Julius Baer provides a secondary market for

the product, but investors should be aware

of the spread risk (bid/ask margin).

Key data

As of 20 September 2016; Source: Bloomberg Finance L.P., Julius Baer

Underlying Bargain Hunting Basket

Currency Composite USD

ISIN CH0330296143

Number of Holdings 10

Participation 100%

Fixing Date 02.09.2016

Ask price USD 96.25

Redemption date 10.09.2018

Issuer Bank Julius Baer & Co. Ltd., Zurich

Issuer Rating A2 (Moody’s)

CONSUMER: AFFORDABLE LUXURY & BARGAIN HUNTING

47

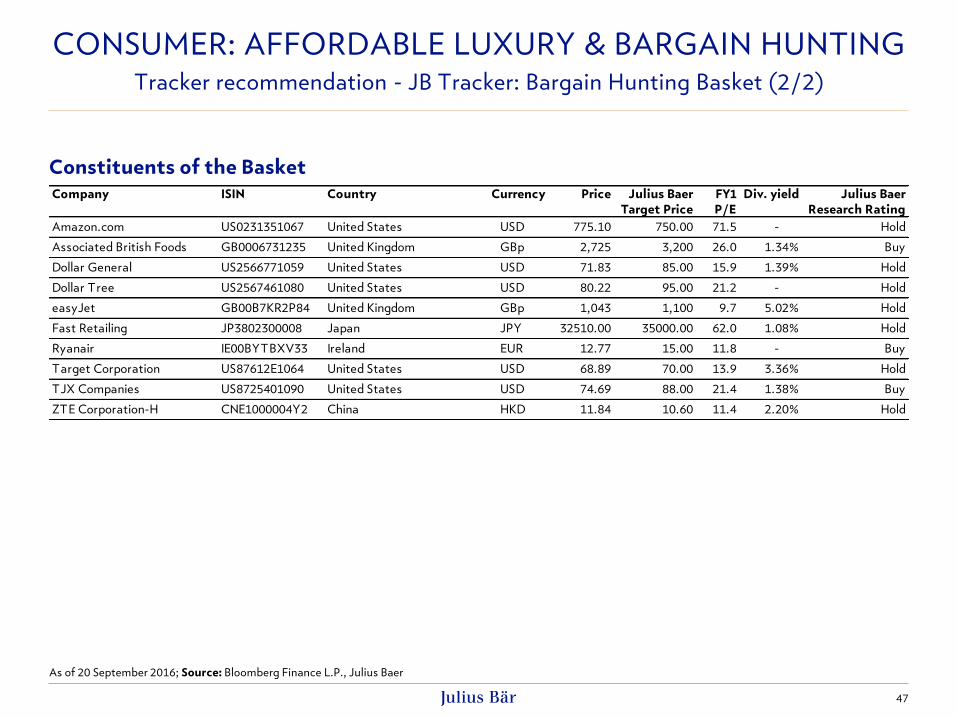

Tracker recommendation - JB Tracker: Bargain Hunting Basket (2/2)

Constituents of the Basket

As of 20 September 2016; Source: Bloomberg Finance L.P., Julius Baer

Company ISIN Country Currency Price Julius Baer

Target Price

FY1

P/E

Div. yield Julius Baer

Research Rating

Amazon.com US0231351067 United States USD 775.10 750.00 71.5 - Hold

Associated British Foods GB0006731235 United Kingdom GBp 2,725 3,200 26.0 1.34% Buy

Dollar General US2566771059 United States USD 71.83 85.00 15.9 1.39% Hold

Dollar Tree US2567461080 United States USD 80.22 95.00 21.2 - Hold

easyJet GB00B7KR2P84 United Kingdom GBp 1,043 1,100 9.7 5.02% Hold

Fast Retailing JP3802300008 Japan JPY 32510.00 35000.00 62.0 1.08% Hold

Ryanair IE00BYTBXV33 Ireland EUR 12.77 15.00 11.8 - Buy

Target Corporation US87612E1064 United States USD 68.89 70.00 13.9 3.36% Hold

TJX Companies US8725401090 United States USD 74.69 88.00 21.4 1.38% Buy

ZTE Corporation-H CNE1000004Y2 China HKD 11.84 10.60 11.4 2.20% Hold

CONSUMER: AFFORDABLE LUXURY & BARGAIN HUNTING

48

Robeco Global Consumer Trends

Fund description

• The fund invests primarily in a portfolio of global consumer equity securities.

• While it may invest in companies of any size, the fund generally focuses on those with large market capitalisation.

• The fund is expected to move in line with the underlying market and to outperform its investment universe over an investment cycle (Julius Baer fund label: Market Exposure). Note that no off-the-shelf market index is a close proxy for the investment universe.

• The fund's thematic investment approach is focused on developed market companies benefiting from structural changes to consumer behaviour across the globe.

• The fund's managers favour limited direct emerging market exposure. • In common with most thematic products the fund risks excessive

emphasis on thematic fit in stock selection at the expense of the fundamental soundness of investment theses.

Fund performance 5-year performance, in percentage (net)

Low Moderate Considerable High

Lower risk Higher risk

Julius Baer product risk classification

Additional information Provider: Robeco Luxembourg S.A.; paying agent: UBS AG; representative: RobecoSAM AG. Please find supporting documents (fund fact sheet, prospectus, annual report, etc.) on www.fundinfo.com, or contact your Julius Baer representative for further information.

Benchmark MSCI All Countries World (Net Return) (EUR)

Base Currency EUR

Other Currencies USD, USD-h

ISIN (USD Share Class) LU0554840073

ISIN (EUR Share Class) LU0187079347

ISIN (USD-h Share Class) LU1208677507

NAV as of 16.09.2016 EUR 152.99

Size as of 31.08.2016 EUR 1’347.67 mln

Domicile Luxembourg

Launch Date 03.06.1998

TER 1.68%

Sales Registration CH, DE, AT, FR, IT, UK, SG; HK, others

Supporting Documents https://www.fundinfo.com/Robeco

Product facts

As of 20.09.2016; Source: Datastream, Julius Baer, Morningstar

49

Contingent convertible (CoCo) bonds – our preferred investment in bank debt

• Contingent convertible (CoCo) bonds have become one of the fastest-growing segments in

the fixed income asset class over the last few years as Basel III and its accompanying directives

force banks to improve their balance sheets materially.

• This in turn will make them less vulnerable to adverse financial shocks and a safer place to

invest for fixed-income investors.

• With the implementation of the European Bank Recovery and Resolution Directive (BRRD) in

2016, even senior creditors will be bailed-in in case of financial distress of the debt-issuing

bank.

• Despite the banks’ uncomfortable situation in terms of profitability, it therefore makes sense

to invest in CoCo-bonds of fundamentally sound banks, which are systemically important and

have to build up additional capital under the coming TLAC (total loss-absorbing capacity)

regime until 2019. The TLAC regime will make the banks safer, from a fixed-income investor’s

point of view.

• Please note that CoCo’s are highly sophisticated and complicated financial products and

include multiple variables which need to be taken into consideration before investing

(potential loss of capital in case certain conditions are met).

• We have put together a selection of CoCo’s of our analysts’ favourite issuers (see page 52).

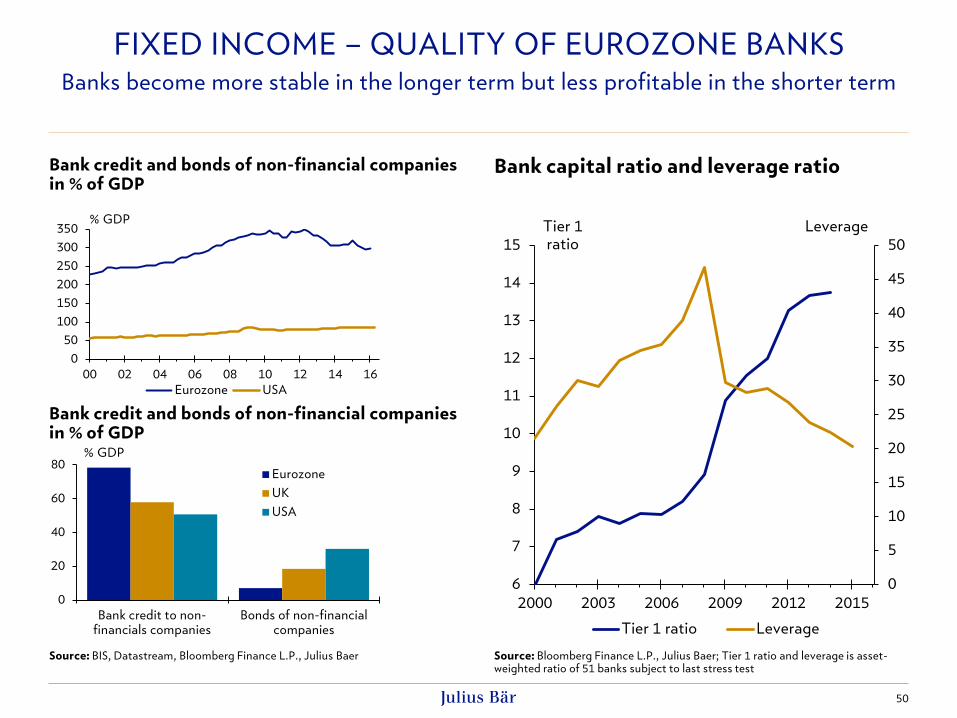

FIXED INCOME – QUALITY OF EUROZONE BANKS

Deeply subordinated bonds of solid banks offer value to the risk friendly

50

FIXED INCOME – QUALITY OF EUROZONE BANKS Banks become more stable in the longer term but less profitable in the shorter term

Source: BIS, Datastream, Bloomberg Finance L.P., Julius Baer

Source: Bloomberg Finance L.P., Julius Baer; Tier 1 ratio and leverage is asset-weighted ratio of 51 banks subject to last stress test

Bank credit and bonds of non-financial companies in % of GDP

Bank capital ratio and leverage ratio

0

5

10

15

20

25

30

35

40

45

50

6

7

8

9

10

11

12

13

14

15

2000 2003 2006 2009 2012 2015

Leverage Tier 1 ratio

Tier 1 ratio Leverage

0

20

40

60

80

Bank credit to non-financials companies

Bonds of non-financialcompanies

% GDP

Eurozone

UK

USA

Bank credit and bonds of non-financial companies in % of GDP

0

50

100

150

200

250

300

350

00 02 04 06 08 10 12 14 16

% GDP

Eurozone USA

Volume to increase

New issue activity slumped in period of

financial stress in February.

Market is recovering from temporary weakness

and capital intake will resume.

Decent yield

In case of financial stress, regulators can also

induce losses on holders of senior unsecured

bonds which have a very low yield.

It is more attractive to focus on deeply

subordinated bonds of solid banks than on

senior debt of second-tier issuers.

51

FIXED INCOME – QUALITY OF EUROZONE BANKS Deeply subordinated bonds of solid banks offer a better return

than traditional high-yield bonds.

Source: Bank of America Merrill Lynch, Julius Baer; Contingent Convertible (CoCo) bond index inception date 31 Dec 2013

Volume and performance of deeply subordinated bank debt

Yield of financial bonds

40

60

80

100

120

140

160

180

95

100

105

110

115

120

2014 2015 2016

USD bn Total return

CoCo total return index, right

CoCo index volume

0

2

4

6

8

10

2011 2012 2013 2014 2015 2016

%

CoCo index EUR non-investment grade

EUR senior banks

*According to the Product Intervention (Contingent Convertible Instruments and Mutual Society Shares) Instrument 2015, enacted by the U.K. Financial Conduct Authority (“FCA”), this/these product(s) must not be distributed to retail investors domiciled in the European Economic Area (“EEA” – EU, Liechtenstein, Norway and Iceland). Investors who intend to buy this/these product(s) must have an annual income of at least GBP 100,000 (or equivalent) or net assets (excluding property, insurance and other benefits) of at least GBP 250,000 (or equivalent) at their disposal.

52

FIXED INCOME – QUALITY OF EUROZONE BANKS

Deeply subordinated bonds of solid banks offer value to the risk friendly

Source: Bloomberg Finance L.P., Julius Baer, prices as of 20 September .2016

ISIN Issuer Cpn Maturity

First Call

Date Crncy Loss Absorption

Trigger

Level Price YtC

Cpn Reset

Date

Reset

Spread

Rep.

CET1

JB Research

Issuer Rating Min. Inv.

Tier2 Bonds

CH0236733827 UBS AG 4.75 12.02.2026 12.02.2021 EUR Permanent Write Down 5 107.25 2.87 12.02.2021 340 14.5 Buy/Quality 100,000

CH0244100266 UBS AG 5.125 15.05.2024 USD Permanent Write Down 5 103.75 14.5 Buy/Quality 200,000

Additional T1 Bonds

EUR

XS1033661866 BANCO BILBAO VIZCAYA ARG 7 PERPETUAL 19.02.2019 EUR Equity Conversion 5.125 95.61 8.85 19.02.2019 616 10.3 Buy/Opportunistic 200,000

XS1043535092 BANCO SANTANDER SA 6.25 PERPETUAL 12.03.2019 EUR Equity Conversion 5.125 90.82 10.33 12.03.2019 541 10.05 Buy/Quality 100,000

XS1190663952 BANCO BILBAO VIZCAYA ARG 6.75 PERPETUAL 18.02.2020 EUR Equity Conversion 5.125 94.29 8.56 18.02.2020 660 10.3 Buy/Opportunistic 200,000

XS0867620725 SOCIETE GENERALE 6.75 PERPETUAL 07.04.2021 EUR Temporary Write Down 5.125 99.28 6.84 07.04.2021 554 10.9 Buy/Opportunistic 100,000

XS1394911496 BANCO BILBAO VIZCAYA ARG 8.875 PERPETUAL 14.04.2021 EUR Equity Conversion 5.125 105.95 7.23 14.04.2021 918 10.3 Buy/Opportunistic 200,000

XS1055037177 CREDIT AGRICOLE SA 6.5 PERPETUAL 23.06.2021 EUR Temporary Write Down 5.125 100.29 6.34 23.06.2021 512 10.7 Buy/Opportunistic 100,000

XS1107291541 BANCO SANTANDER SA 6.25 PERPETUAL 11.09.2021 EUR Equity Conversion 5.125 90.88 8.41 11.09.2021 564 10.05 Buy/Quality 100,000

CH0271428309 UBS GROUP AG 5.75 PERPETUAL 19.02.2022 EUR Permanent Write Down 5.125 103.72 4.86 19.02.2022 529 14.5 Buy/Quality 200,000

XS1247508903 BNP PARIBAS 6.125 PERPETUAL 17.06.2022 EUR Temporary Write Down 5.125 102.27 5.59 17.06.2022 523 10.9 Buy/Quality 200,000

XS1111123987 HSBC HOLDINGS PLC 5.25 PERPETUAL 16.09.2022 EUR Equity Conversion 7 98.34 5.50 16.09.2022 438 11.9 Buy/Opportunistic 200,000

XS1298431104 HSBC HOLDINGS PLC 6 PERPETUAL 29.09.2023 EUR Equity Conversion 7 104.43 5.17 29.09.2023 534 11.9 Buy/Opportunistic 200,000

GBP

XS1055037920 CREDIT AGRICOLE SA 7.5 PERPETUAL 23.06.2026 GBP Temporary Write Down 5.125 99.64 7.47 23.06.2026 454 10.7 Buy/Opportunistic 100,000

USD

XS0926832907 BANCO BILBAO VIZCAYA ARG 9 PERPETUAL 09.05.2018 USD Equity Conversion 5.125 103.50 6.24 09.05.2018 826 10.3 Buy/Opportunistic 200,000

XS0867614595 SOCIETE GENERALE 8.25 PERPETUAL 29.11.2018 USD Temporary Write Down 5.125 102.00 6.99 29.11.2018 639 10.9 Buy/Opportunistic 200,000

XS1066553329 BANCO SANTANDER SA 6.375 PERPETUAL 19.05.2019 USD Equity Conversion 5.125 90.50 10.17 19.05.2019 479 10.05 Buy/Quality 200,000

USF22797YK86 CREDIT AGRICOLE SA 6.625 PERPETUAL 23.09.2019 USD Temporary Write Down 5.125 96.00 7.85 23.09.2019 470 10.7 Buy/Opportunistic 200,000

US404280AR04 HSBC HOLDINGS PLC 5.625 PERPETUAL 17.01.2020 USD Equity Conversion 7 99.13 5.75 17.01.2020 363 11.9 Buy/Opportunistic 200,000

USF8586CXG25 SOCIETE GENERALE 6 PERPETUAL 27.01.2020 USD Temporary Write Down 5.125 90.50 9.09 27.01.2020 407 10.9 Buy/Opportunistic 200,000

CH0271428317 UBS GROUP AG 7.125 PERPETUAL 19.02.2020 USD Permanent Write Down 7 101.88 6.31 19.02.2020 546 14.5 Buy/Quality 200,000

US456837AE31 ING GROEP NV 6 PERPETUAL 16.04.2020 USD Equity Conversion 7 97.75 6.48 16.04.2020 445 12.7 Buy/Opportunistic 200,000

USF1R15XK441 BNP PARIBAS 7.625 PERPETUAL 30.03.2021 USD Temporary Write Down 5.125 103.00 6.65 30.03.2021 631 10.9 Buy/Quality 200,000

US404280BC26 HSBC HOLDINGS PLC 6.875 PERPETUAL 01.06.2021 USD Equity Conversion 7 104.50 5.67 01.06.2021 551 11.9 Buy/Opportunistic 200,000

CH0331455318 UBS GROUP AG 7.125 PERPETUAL 10.08.2021 USD Permanent Write Down 7 102.00 6.54 10.08.2021 588 14.5 Buy/Quality 200,000

USF8586CRW49 SOCIETE GENERALE 7.875 PERPETUAL 18.12.2023 USD Temporary Write Down 5.125 97.75 8.15 18.12.2023 498 10.9 Buy/Opportunistic 200,000

USF22797RT78 CREDIT AGRICOLE SA 7.875 PERPETUAL 23.01.2024 USD Temporary Write Down 5.125 101.50 7.46 23.12.2023 490 10.7 Buy/Opportunistic 200,000

US404280AS86 HSBC HOLDINGS PLC 6.375 PERPETUAL 17.09.2024 USD Equity Conversion 7 98.25 6.58 17.09.2024 371 11.9 Buy/Opportunistic 200,000

US404280AT69 HSBC HOLDINGS PLC 6.375 PERPETUAL 30.03.2025 USD Equity Conversion 7 99.00 6.45 30.03.2025 437 11.9 Buy/Opportunistic 200,000

US456837AF06 ING GROEP NV 6.5 PERPETUAL 16.04.2025 USD Equity Conversion 7 97.25 6.85 16.04.2025 445 12.7 Buy/Opportunistic 200,000

CH0286864027 UBS GROUP AG 6.875 PERPETUAL 07.08.2025 USD Permanent Write Down 7 98.00 7.07 07.08.2025 459 14.5 Buy/Quality 200,000

USF1R15XK367 BNP PARIBAS 7.375 PERPETUAL 19.08.2025 USD Temporary Write Down 5.125 100.25 7.26 19.08.2025 515 10.9 Buy/Quality 200,000

USF43628B413 SOCIETE GENERALE 8 PERPETUAL 29.09.2025 USD Temporary Write Down 5.125 100.25 7.84 29.09.2025 587 10.9 Buy/Opportunistic 200,000

CH0271428333 UBS GROUP AG 7 PERPETUAL 19.02.2025 USD Permanent Write Down 5.125 106.13 5.97 19.02.2025 487 14.5 Buy/Quality 200,000

USF2R125CD54 CREDIT AGRICOLE SA 8.125 PERPETUAL 23.12.2025 USD Temporary Write Down 5.125 106.38 7.11 23.12.2025 619 10.7 Buy/Opportunistic 200,000

53

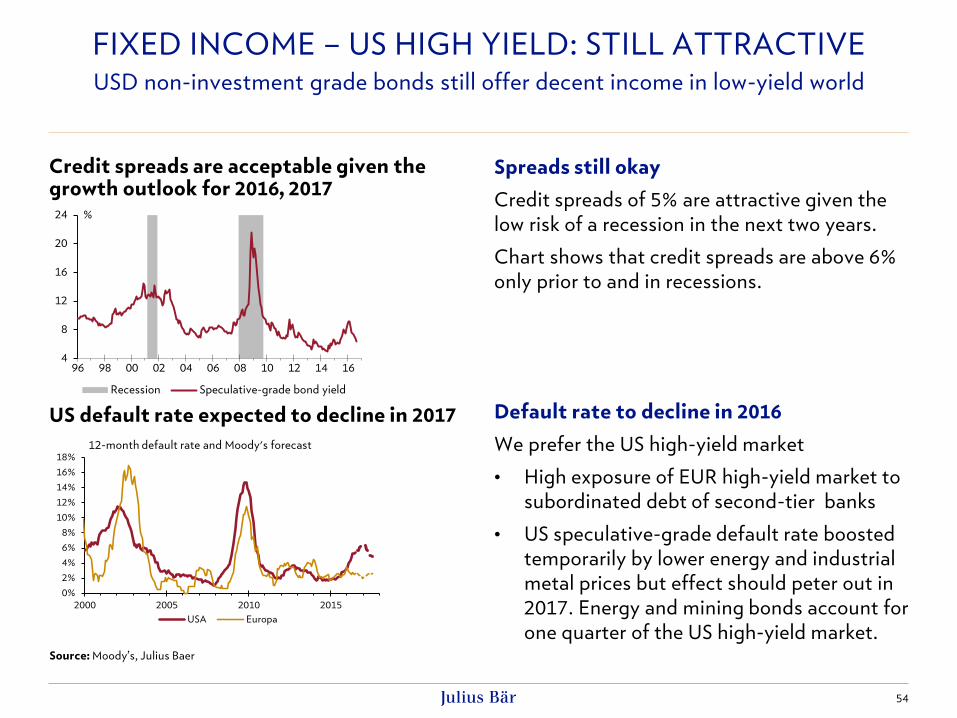

US high yield bonds – investors are compensated well for the risk

• The US high yield segment has been one of the best performing assets in 2016, returning c.

14.50% in USD year-to-date according to the Bank of America Merrill Lynch US High Yield

Index.

• Recovering commodity prices and reassuring data in regard to the overall economic

environment in the US have helped the segment to perform well over the past months.

• The segment has been quite resilient and the result of the Brexit referendum has led only to

limited spread widening, keeping investors well compensated for a potential surge of defaults.