using r for hedge fund of funds risk managementfunds risk management

TRANSCRIPT

Using R for Hedge Fund of Funds Risk ManagementFunds Risk Management

R/Finance 2009: Applied Finance with RR/Finance 2009: Applied Finance with RUniversity of Illinois Chicago, April 25, 2009

Eric ZivotProfessor and Gary Waterman Distinguished Scholar,

Department of EconomicsAdjunct Professor, Departments of Finance and Statistics

University of Washington

OutlineOutline

• Hedge fund of funds environmentHedge fund of funds environment• Factor model risk measurement

i l i i i• R implementation in corporate environment• Dealing with unequal data histories• Some thoughts on S-PLUS and S+FinMetrics

vs. R in Finance

© Eric Zivot 2009

Hedge Fund of Funds Environment• HFoFs are hedge funds that invest in other hedge

funds– 20 to 30 portfolios of hedge funds– Typical portfolio size is 30 funds

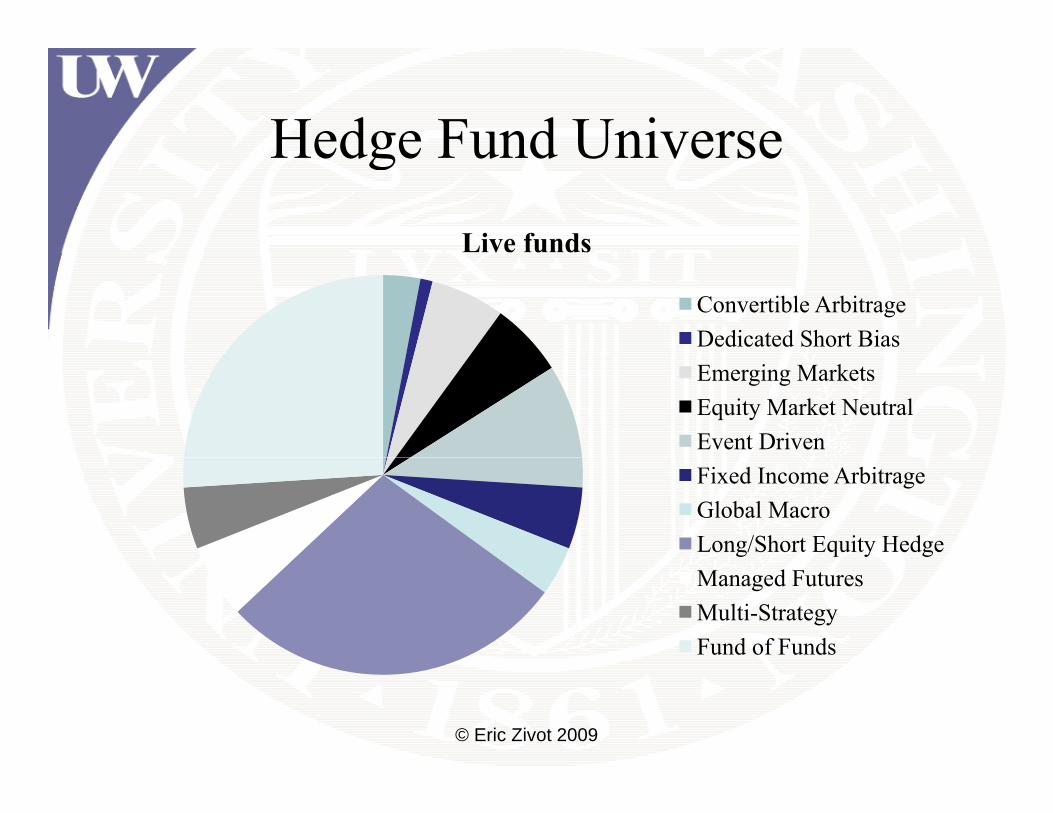

• Hedge fund universe is large: 5000 live funds– Segmented into 10-15 distinct strategy types

• Hedge funds voluntarily report monthly performance to commercial databases– Altvest, CISDM, HedgeFund.net, Lipper TASS,

CS/Tremont, HFR• HFoFs often have partial position level data on

invested funds © Eric Zivot 2009

Hedge Fund UniverseHedge Fund UniverseLive funds

Convertible ArbitrageDedicated Short BiasEmerging MarketsEquity Market NeutralEvent DrivenFixed Income ArbitrageGlobal MacroLong/Short Equity HedgeManaged FuturesMulti-StrategyFund of Funds

© Eric Zivot 2009

Characteristics of Monthly ReturnsCharacteristics of Monthly Returns

• Reporting biasesReporting biases– Survivorship, backfill

N l b h i• Non-normal behavior– Asymmetry (skewness) and fat tails (excess

k t i )kurtosis)• Serial correlation

– Performance smoothing, illiquid positions• Unequal histories

© Eric Zivot 2009

Characteristics of Hedge Fund DataCharacteristics of Hedge Fund Datafund1 fund2 fund3 fund4 fund5

Observations 122.0000 107.0000 135.0000 135.0000 135.0000NAs 13.0000 28.0000 0.0000 0.0000 0.0000Minimum -0.0842 -0.3649 -0.0519 -0.1556 -0.2900Quartile 1 -0.0016 -0.0051 0.0020 -0.0017 -0.0021Median 0.0058 0.0046 0.0060 0.0073 0.0049Arithmetic Mean 0.0038 -0.0017 0.0063 0.0059 0.0021Geometric Mean 0.0037 -0.0029 0.0062 0.0055 0.0014Quartile 3 0.0158 0.0129 0.0127 0.0157 0.0127Maximum 0.0311 0.0861 0.0502 0.0762 0.0877Variance 0.0003 0.0020 0.0002 0.0008 0.0013Stdev 0.0176 0.0443 0.0152 0.0275 0.0357Skewness -1.7753 -5.6202 -0.8810 -2.4839 -4.9948Kurtosis 5.2887 40.9681 3.7960 13.8201 35.8623Rho1 0.6060 0.3820 0.3590 0.4400 0.383

Sample: January 1998 – March 2009

© Eric Zivot 2009

p y

Factor Model Risk Measurement in HFoFs Portfolio

• Quantify factor risk exposuresQuantify factor risk exposures– Equity, rates, credit, volatility, currency,

commodity etccommodity, etc.• Quantify tail risk

V R ETL– VaR, ETL• Risk budgeting

– Component, incremental, marginal• Stress testing and scenario analysis

© Eric Zivot 2009

Commercial ProductsCommercial Products

www riskdata com www finanalytica comwww.riskdata.com www.finanalytica.com

Very expensive! R is not!

© Eric Zivot 2009

Very expensive! R is not!

Factor Model: MethodologyFactor Model: Methodology1 1 , it i i t ik kt itR F Fα β β ε= + + + +

1i i it

i t t Tα ε′= + +tβ F

F

1, , ; , ,~ ( , )

i

t F

i n t t T= =

F μ Σ… …

F2,

( )

~ (0, )t F

it iεε σ

μ

cov( , ) 0 for all , and

cov( ) 0 forjt itf j i t

i j

ε

ε ε

=

= ≠© Eric Zivot 2009

cov( , ) 0 for it jt i jε ε = ≠

Practical ConsiderationsPractical Considerations

• Many potential risk factors ( > 50)Many potential risk factors ( > 50)• High collinearity among some factors

i k f di i li /• Risk factors vary across discipline/strategy• Nonlinear effects• Dynamic effects• Time varying coefficientsTime varying coefficients• Common histories for factors; unequal

histories for fund performancehistories for fund performance© Eric Zivot 2009

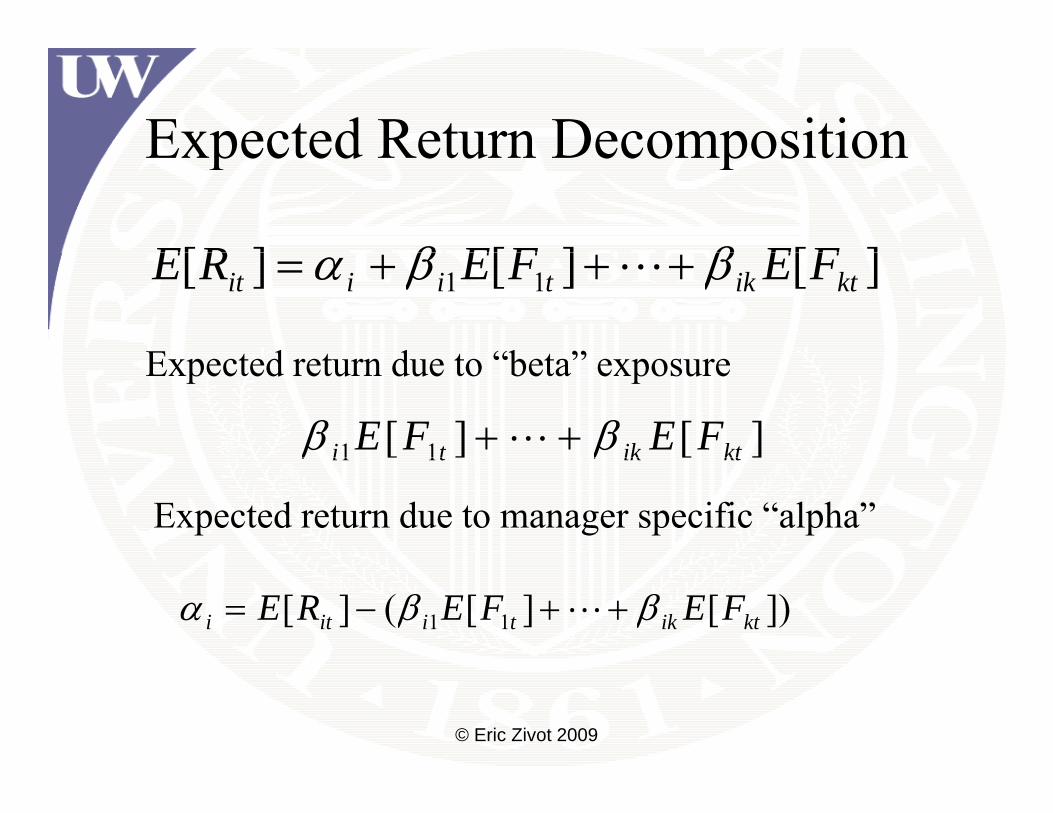

Expected Return DecompositionExpected Return Decomposition

][][][ FEFERE ββ ][][][ 11 ktiktiiit FEFERE ββα +++=

E t d t d t “b t ”

][][ 11 ktikti FEFE ββ ++

Expected return due to “beta” exposure

11 ktikti ββ

Expected return due to manager specific “alpha”

])[][(][ 11 ktiktiiti FEFERE ββα ++−=

© Eric Zivot 2009

Variance Decompositionp

2var( ) var( ) var( )R ε σ′ ′= + = +β F β β Σ β ,var( ) var( ) var( )it i t i it i i iR εε σ= + = +Fβ F β β Σ β

systematic specific

Variance contribution due to factor exposures

)var()var()var( 22

221

21 ktktt FFF βββ +++

)cov(2)cov(2 FFFF ++ ββββ

Variance contribution due to covariances between factors

© Eric Zivot 2009

),cov(2),cov(2 112121 kttkkktt FFFF −−++ ββββ

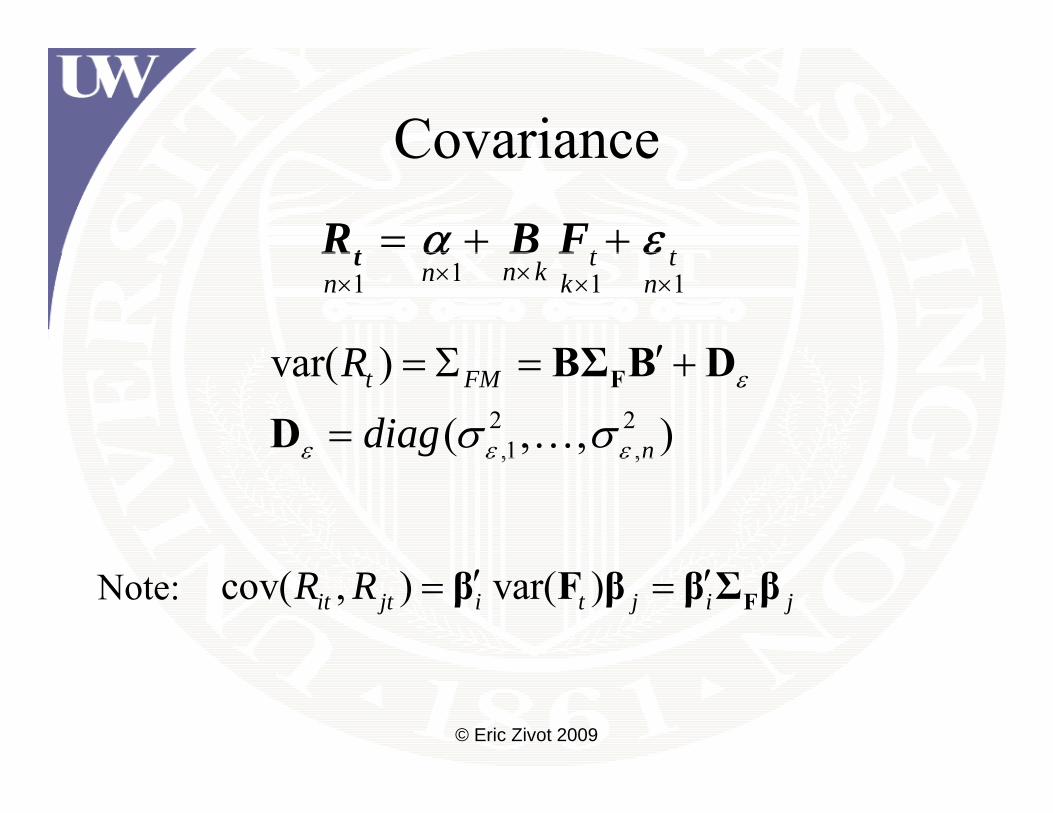

CovarianceCovariance

t t= + +tR B Fα ε

( )R ′Σ +BΣ B D

11 1 1t tn knn k n××× × ×

+ +tR B Fα ε

2 2,1 ,

var( )

( , , )t FM

n

R

diagε

ε ε εσ σ

′= Σ = +

=FBΣ B D

D …,1 ,nε ε ε

cov( , ) var( )it jt i t j i jR R ′ ′= = Fβ F β β Σ βNote:

© Eric Zivot 2009

Portfolio AnalysisPortfolio Analysis

1( , , ) portfolio weightsnw w ′= =w …

R ′+′+′=′= εwBFwαwRw

1( , , ) p gn

n

itit

n

ii

n

ii

n

iti

tttpt

wwwRw

R

εα +′+==

++==

∑∑∑∑ Fβ

εwBFwαwRw

pttpp

iitit

iii

iii

iiti wwwRw

εα

εα

+′+=

++ ∑∑∑∑====

Fβ

Fβ1111

pttpp

© Eric Zivot 2009

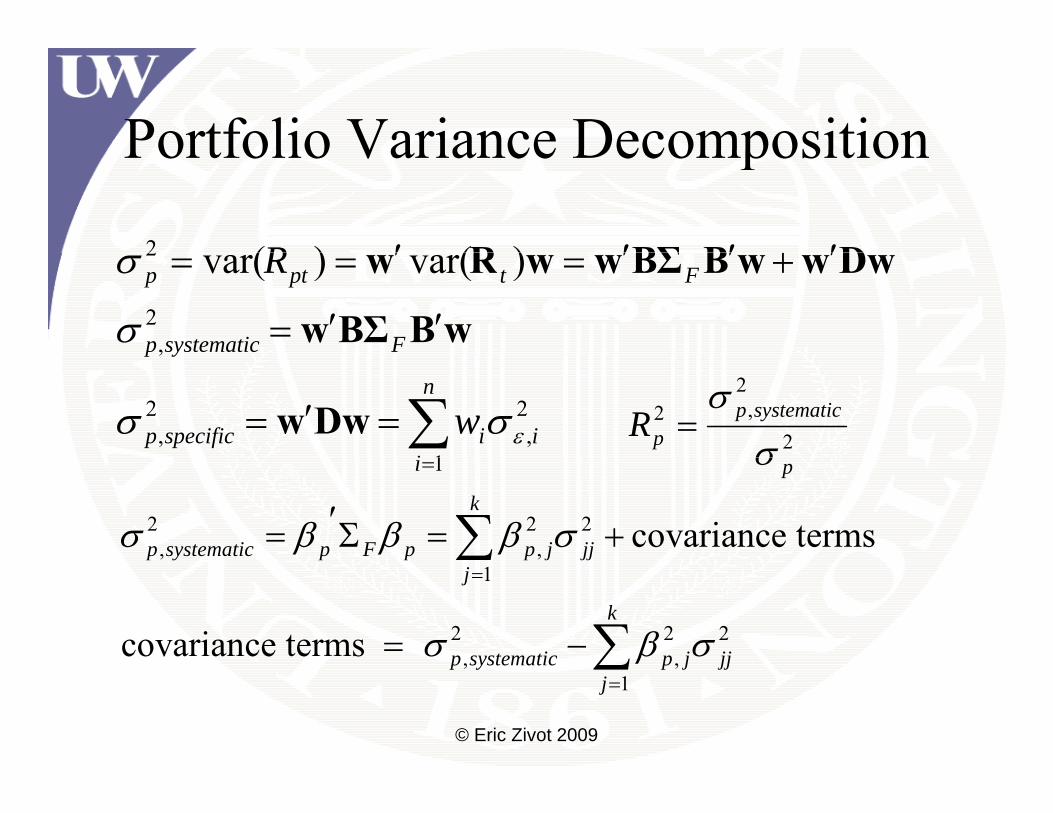

Portfolio Variance DecompositionPortfolio Variance Decomposition

′+′′′R2 )()( DBBΣR

′′=

′+′′=′==

Fsystematicp

Ftptp R2

,

2 )var()var(

σ

σ

wBBΣw

DwwwBBΣwwRw

∑=′=n

iiispecificp

yp

w1

2,

2,

,

εσσ Dww2

2,2 systematicp

pRσ

σ=

=i 1 pσ

2 2 2, , covariance terms

k

p systematic p F p p j jjσ β β β σ′= Σ = +∑1

2 2 2covariance terms

j

k

p systematic p j jjσ β σ

=

= −∑© Eric Zivot 2009

, ,1

p systematic p j jjjβ

=∑

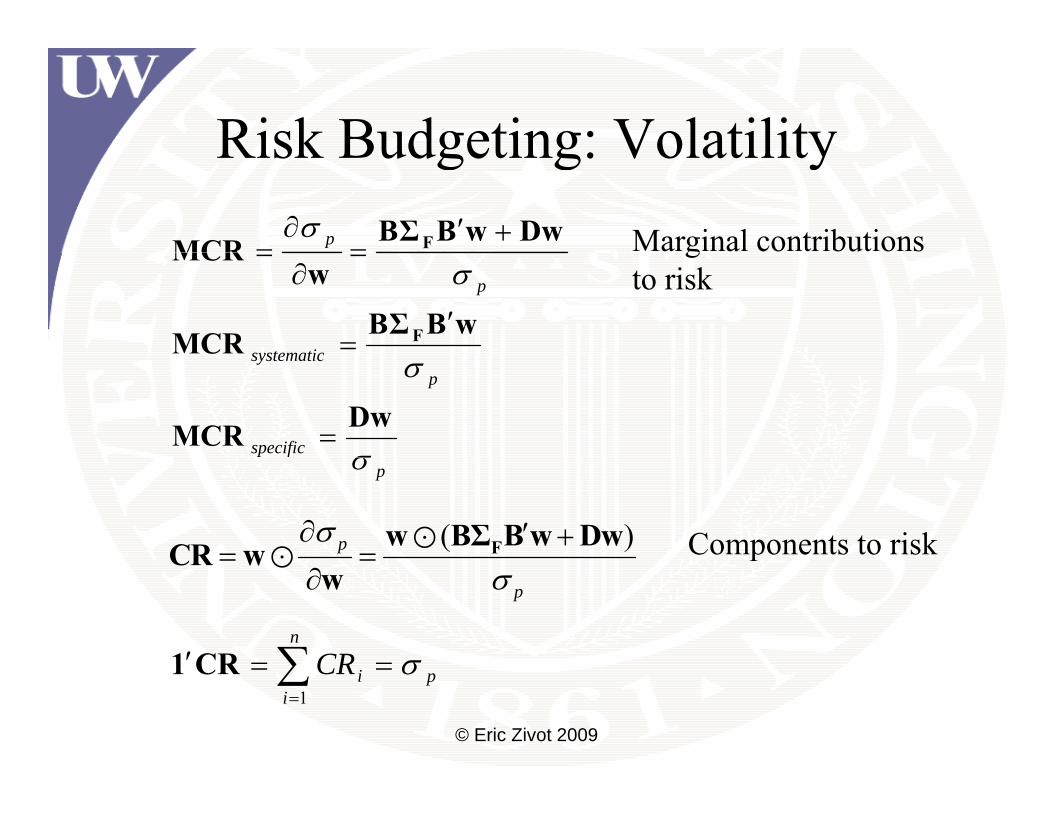

Risk Budgeting: VolatilityRisk Budgeting: Volatilitypσ DwwBBΣMCR F +′=

∂= Marginal contributions

systematic

pσ

wBBΣMCR

wMCR

F ′=

=∂

= gto risk

specific

psystematic

σ

σ

DwMCR =pσ

( )pσ∂ ′ += = Fw BΣ B w DwCR w Components to risk

pσ= =

∂CR w

w

∑ ==′n

CR σCR1

p

© Eric Zivot 2009

∑=

==i

piCR1

σCR1

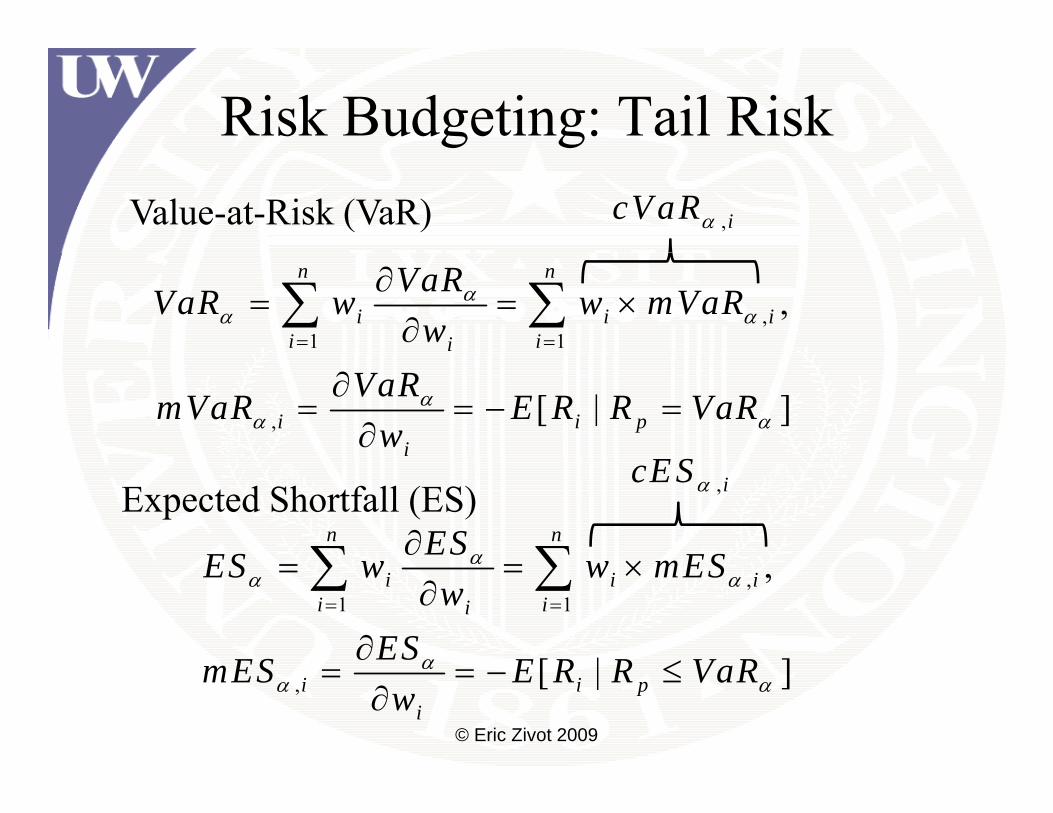

Tail Risk MeasuresTail Risk MeasuresValue-at-Risk (VaR)

1( )VaR q Fα α α−= − = −

of returns F CDF R=

Expected Shortfall (ES)

[ | ]ES E R R VaR≤[ | ]ES E R R VaRα α= − ≤

© Eric Zivot 2009

Tail Risk Measures: Normal DistributionTail Risk Measures: Normal Distribution

2 2~ ( , ), p p p p FMR N w wμ σ σ ′= Σ1, ( )

1

Np pVaR z zα α αμ σ α−= − − × = Φ

1 ( )Np pES zα αμ σ φ

α= −

See functions in PerformanceAnalytics

© Eric Zivot 2009

Tail Risk Measures: Non-Normal DistributionsTail Risk Measures: Non Normal Distributions

Use Cornish-Fisher expansion to account for asymmetry p y yand fat tails

CFi iVaR zα αμ σ= − − ×

( ) ( ) ( )2 3 3 21 1 11 3 2 56 24 36

i i

i i i iz skew z z ekurt z z skew

α α

α α α α α

μ

σ ⎡ ⎤+ − − − − + −⎢ ⎥⎣ ⎦

:CFESαFormula given in Boudt, Peterson and Croux (2008) "Estimation and Decomposition of Downside Risk for Portfolios with Non-Normal Returns," Journal of Risk and implementation in PerformanceAnalytics

© Eric Zivot 2009

Risk Budgeting: Tail RiskValue-at-Risk (VaR) ,icV aRα

,1 1

,n n

i i ii ii

VaRVaR w w mVaRw

αα α

= =

∂= = ×

∂∑ ∑

, [ | ]i i pi

VaRmVaR E R R VaRw

αα α

∂= = − =

∂

Expected Shortfall (ES)n nESES ESα∂∑ ∑

,icE Sα

,1 1

,

[ | ]

i i ii ii

ES w w mESw

ESES E R R V R

αα α

α

= =

= = ×∂

∂≤

∑ ∑

© Eric Zivot 2009

, [ | ]i i pi

mES E R R VaRw

αα α= = − ≤

∂

Risk Budgeting: Explicit FormulasRisk Budgeting: Explicit Formulas

• Normal distributionNormal distribution– See Jorian (2007) or Dowd (2002)

N l di t ib ti i C i h Fi h• Non-normal distribution using Cornish-Fisher expansion

S B d P d C (2008) "E i i– See Boudt, Peterson and Croux (2008) "Estimation and Decomposition of Downside Risk for Portfolios with Non Normal Returns " Journal ofPortfolios with Non-Normal Returns, Journal of Risk and implementation in PerformanceAnalytics

© Eric 9ivot 2008

Risk Budgeting: SimulationRisk Budgeting: Simulation1{ } simulated returnsM

it tR M= =

Method 1: Brute Force

, , , i ii i

VaR ESmVaR mESw w

α αα α

Δ Δ≈ =

Δ Δi i

Method 2: Average Rit around values for which Rpt = VaRVaRα

, ,: :

, i it i itt R VaR t R VaR

mVaR R mES Rα αε= ± ≤

≈ − ≈ −∑ ∑

© Eric Zivot 2009

: :pt ptt R VaR t R VaRα αε= ± ≤

R Functions for Factor Model Risk Analysis

Function FunctionfactorModelCovariance normalESfactorModelRiskDecomposition normalPortfolioESnormalVaR normalMarginalESnormalVaR normalMarginalESnormalPortfolioVaR normalComponentESnormalMarginalVaR modifiedESnormalComponentVaR modifiedPortfolioESnormalVaRreport modifiedESreportmodifiedVaR simulatedMarginalVaRmodifiedPortfolioVaR simulatedComponentVaRmodifiedMarginalVaR simulatedMarginalESmodifiedComponentVaR simulatedComponentESmodifiedComponentVaR simulatedComponentES

© Eric Zivot 2009

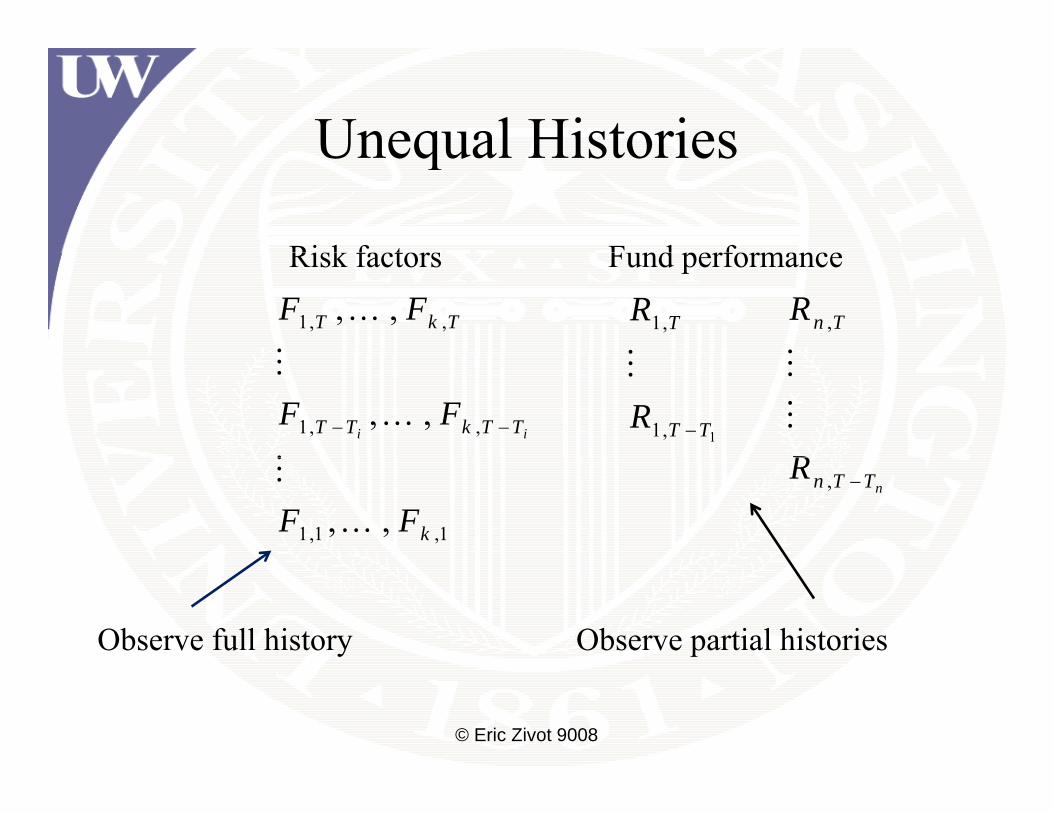

Unequal HistoriesUnequal Histories

Risk factors Fund performance

1, ,, ,T k TF F… 1,TRRisk factors Fund performance

,n TR

1, ,, ,i iT T k T TF F− −…

11,T TR −

R

1,1 ,1, , kF F…, nn T TR −

Observe full history Observe partial histories

© Eric Zivot 9008

Example Portfolio: Unequal Histories of Individual FundsX1

6593

9

0.04

0.00

X104

314

-0.0

50.

000.

05

-0.0

8-0

0.0

0.1 -0.1

5-0

.10

00

X295

54

0.3

-0.2

-0.1

0

X153

684

08-0

.04

0.00

-00

0.02

0.04

69

-0.0

0.02

45

-0.0

40.

00

X113

16

-0.0

6-0

.02

X156

14

© Eric Zivot 2009

1998 2000 2002 2004 2006 2008 1998 2000 2002 2004 2006 2008

Implication of Unequal HistoriesImplication of Unequal Histories

• Can’t fit factor models to some fundsCan t fit factor models to some funds– Need to create proxy factor model

St ti ti hi t i (t t d d t )• Statistics on common histories (truncated data) may be unreliable

• Difficult to compute non-normal tail risk measures

© Eric Zivot 2009

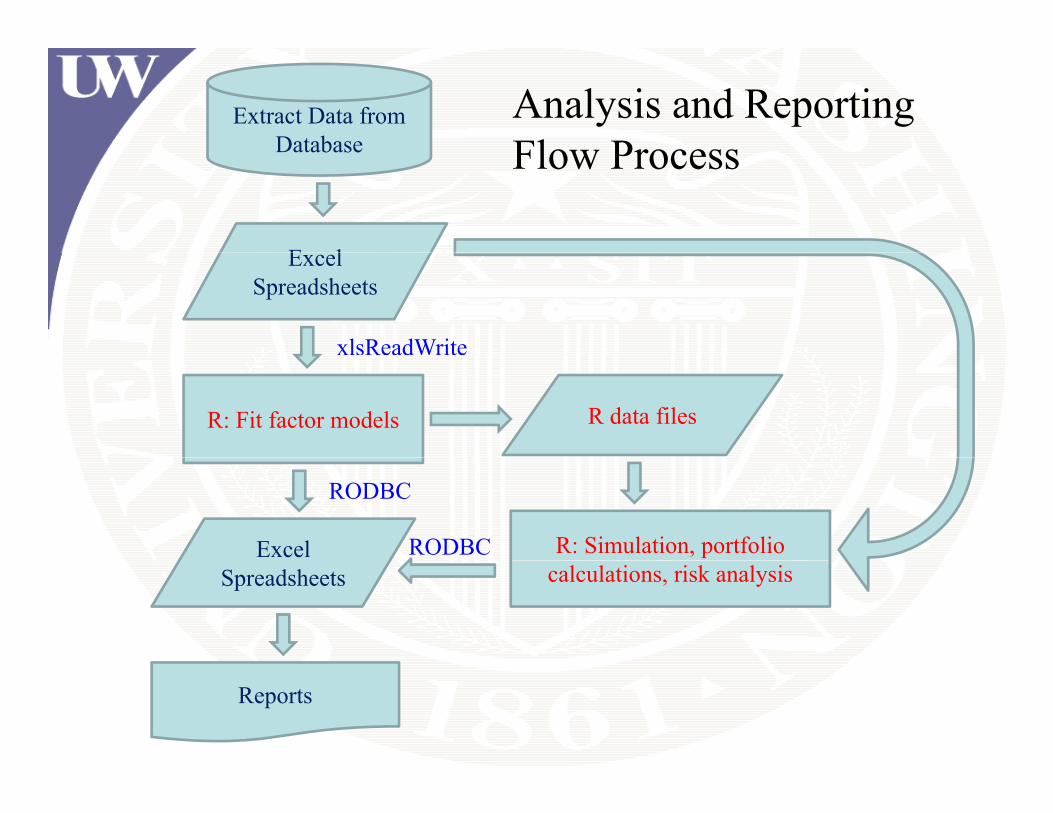

Extract Data from Database

Analysis and Reporting Flow ProcessDatabase

E l

Flow Process

Excel Spreadsheets

xlsReadWrite

R: Fit factor models R data files

Excel R: Simulation, portfolio

RODBC

RODBCSpreadsheets calculations, risk analysis

Reports

S ffi i

Factor Model ConstructionSufficient history? No

Yes

Fit factor model :Variable selection: leaps, MASSCollinearity diagnostics: card i i d l

Create proxy factor model from models with sufficient history

dynamic regression: dynlm

R data file

© Eric Zivot 2009

Evaluation of Fitted Factor ModelsEvaluation of Fitted Factor Models

• Graphical diagnosticsGraphical diagnostics– Created plot method appropriate for time series

regressionregression. • Stability analysis

CUSUM t t h– CUSUM etc: strucchange– Rolling analysis: rollapply (zoo)

Ti i dl– Time varying parameters: dlm• Dynamic effects

– dynlm, lmtest© Eric Zivot 2009

Diagnostic Plots: Example Fund0.

02p ,

0.00

ce

4-0

.02

nthl

y pe

rform

anc

-0.0

6-0

.04

Mon

-0.0

8-

2005 2006 2007 2008 2009

ActualFitted

© Eric Zivot 2008

Index

2005 2006 2007 2008 2009

0.6

0.8

1.0

60

Time Series Regression Residual diagnosticsAC

F

-0.2

0.0

0.2

0.4

01.

0 Den

sity

3040

50

PAC

F

-0.2

0.0

0.2

0.4

0.6

0.8

010

20

Lag

5 10 15

Returns

-0.04 -0.02 0.00 0.02

OLS-based CUSUM test

1.5

.02

uatio

n pr

oces

s

00.

51.

0

al Q

uant

iles 0.

000.

Em

piric

al fl

uctu

-1.0

-0.5

0.0

Em

piric

a

-0.0

4-0

.02

© Eric Zivot 2009 Time

0.0 0.2 0.4 0.6 0.8 1.0norm Quantiles

-2 -1 0 1 2

24-month rolling estimates(In

terc

ept)

0.00

00.

004

X144

887

0.05

0.15

(

-0.0

040.

25

-0.0

50

0.3

X144

874

0.05

0.15

0.1

0.2

0

X144

911

-0.0

5-0

.10.

0

75

0.0

2007 2008 2009

Index

-0.4

-0.3

-0.2

X144

87

© Eric Zivot 2009

2007 2008 2009

Index

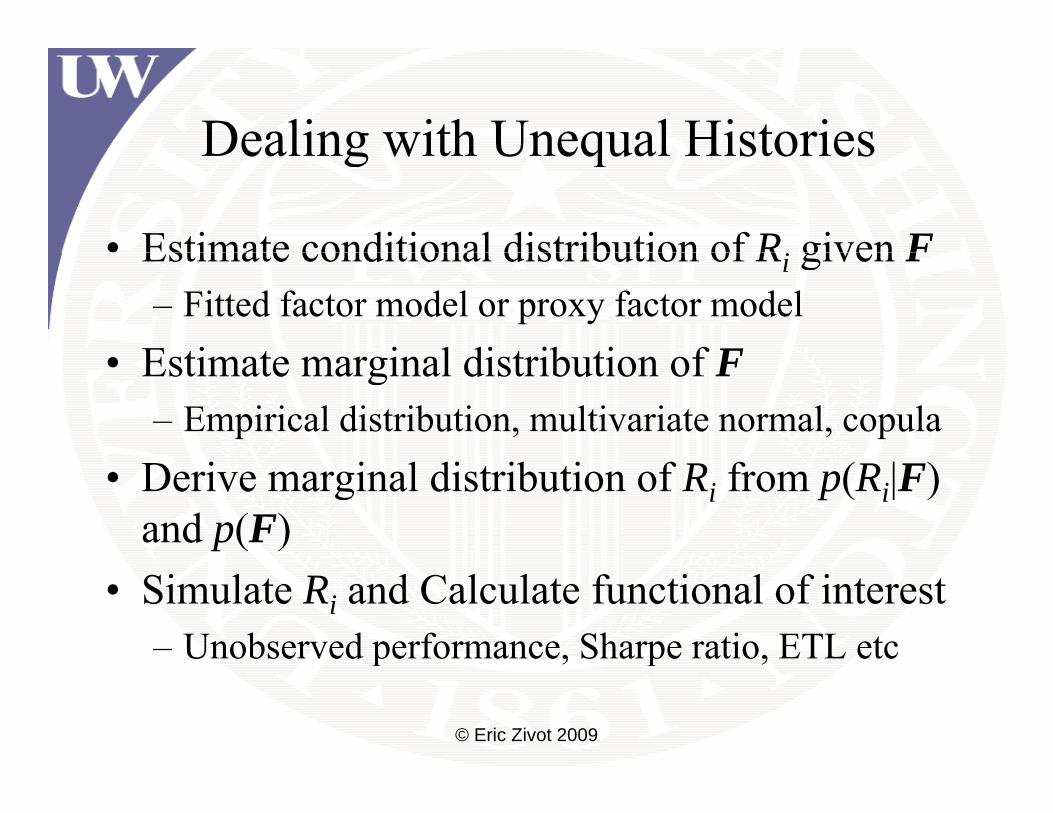

Dealing with Unequal HistoriesDealing with Unequal Histories

• Estimate conditional distribution of R given FEstimate conditional distribution of Ri given F– Fitted factor model or proxy factor model

E ti t i l di t ib ti f F• Estimate marginal distribution of F– Empirical distribution, multivariate normal, copula

• Derive marginal distribution of Ri from p(Ri|F) and p(F)

• Simulate Ri and Calculate functional of interest– Unobserved performance, Sharpe ratio, ETL etcp , p ,

© Eric Zivot 2009

Simulation AlgorithmSimulation Algorithm

• Draw by resampling from the{ }1 MF FDraw by resampling from the empirical distribution of F.

• For each (u = 1 M) draw a value

{ }1, , M…F F

F R• For each (u = 1, …, M), draw a value from the estimated conditional distribution of R given F= (e g from fitted factor model

uF ,i uR

FRi given F= (e.g., from fitted factor model assuming normal errors)

i h d i d l f R

uF

{ }MR• is the desired sample for Ri

• M ≈ 5000{ },

1i u

uR

=

© Eric Zivot 2009

What to do with ?{ },M

i uRWhat to do with ?

• Backfill missing fund performance

{ },1

i uu=

Backfill missing fund performance• Compute fund and portfolio performance

measuresmeasures• Estimate non-parametric fund and portfolio tail

i krisk measures• Compute non-parametric risk budgeting

measures• Standard errors can be computed using a p g

bootstrap procedure© Eric Zivot 2009

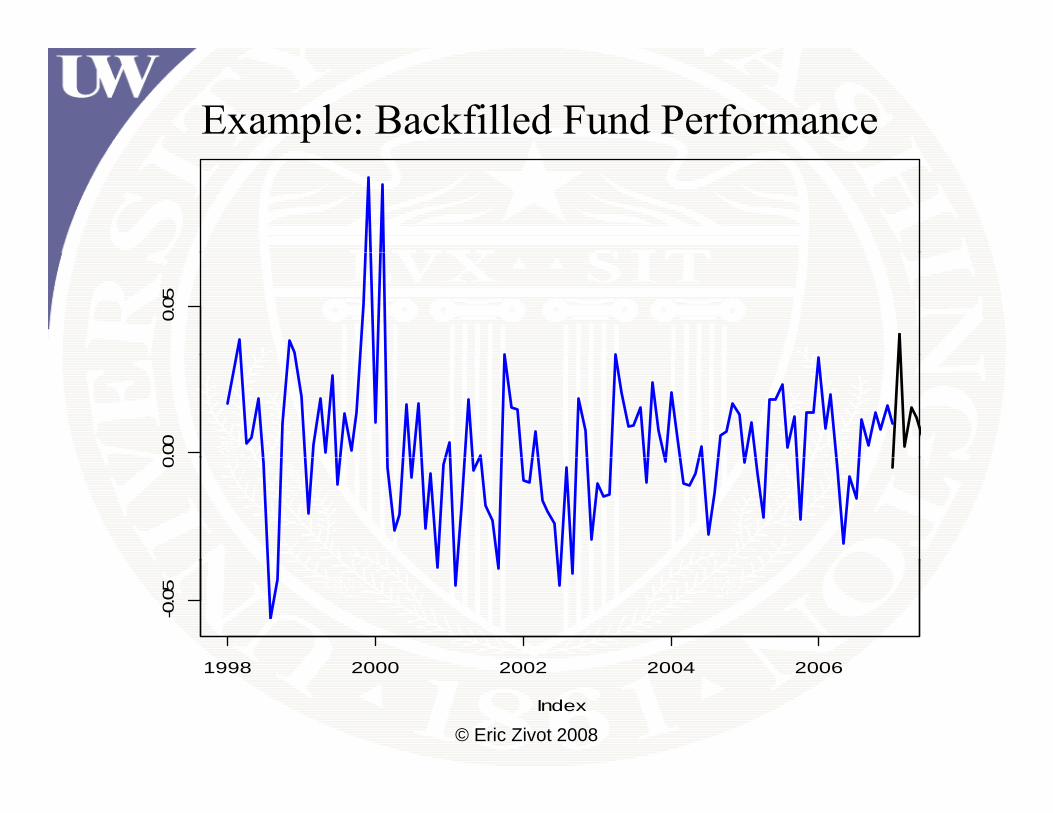

Example: Backfilled Fund Performance0.

050.

000

-0.0

5

1998 2000 2002 2004 2006

© Eric Zivot 2008Index

1998 2000 2002 2004 2006

Example: Simulated portfolio distribution60

% M

odVaR

99%

VaR

4050

99 %

Den

sity

3040

1020

01

© Eric Zivot 2009Returns

-0.08 -0.06 -0.04 -0.02 0.00 0.02 0.04

S-PLUS and S+FinMetrics vs RS PLUS and S+FinMetrics vs R

• Dealing with time series objects in R can beDealing with time series objects in R can be difficult and confusing

timeSeries zoo xts– timeSeries, zoo, xts• Time series regression in R is incompletely

i l t dimplemented– Diagnostic plots, prediction

• R packages give about 80% functional coverage to S+FinMetrics

© Eric Zivot 2009

Some Thoughts About Using R in a C iCorporate Environment

• IT doesn’t want to support itIT doesn t want to support it• Firewalls block R downloads

h ld f l d h• The world runs from an Excel spreadsheet• Analysts with some programming experience

learn R quickly• Not good for the casual userg

© Eric Zivot 2009

ReferencesReferences• Boudt, K., B. Peterson and C. Croux (2008) "Estimation and , , ( )

Decomposition of Downside Risk for Portfolios with Non-Normal Returns," Journal of RiskD d K (2002) M i M k Ri k J h Wil d• Dowd, K. (2002), Measuring Market Risk, John Wiley and Sons

• Goodworth, T. and C. Jones (2007). “Factor-based, Non-Goodwo t , . a d C. Jo es ( 007). acto based, Noparametric Risk Measurement Framework for Hedge Funds and Fund-of-Funds,” The European Journal of Finance.H ll b k J (2003) “D i P f li V l Ri k• Hallerback, J. (2003). “Decomposing Portfolio Value-at-Risk: A General Analysis”, The Journal of Risk 5/2.

• Jorian, P. (2007), Value at Risk, Third Edition, McGraw HillJorian, P. (2007), Value at Risk, Third Edition, McGraw Hill

© Eric Zivot 2009

ReferencesReferences• Jiang, Y. (2009). Overcoming Data Challenges in Fund-of-g, ( ) g g f

Funds Portfolio Management, PhD Thesis, Department of Statistics, University of Washington.L A (2007) H d F d A A l i P i• Lo, A. (2007). Hedge Funds: An Analytic Perspective, Princeton.

• Yamai, Y. and T. Yoshiba (2002). “Comparative Analyses of a a , . a d . os ba ( 00 ). Co pa at ve a yses oExpected Shortfall and Value-at-Risk: Their Estimation Error, Decomposition, and Optimization, Institute for Monetary and Economic Studies Bank of JapanEconomic Studies, Bank of Japan.

© Eric Zivot 2009