valueguide dec2015 ins - sharekhan · please refer the risk disclosure document issued by sebi and...

TRANSCRIPT

December 2015 Sharekhan ValueGuide2

REGULAR FEATURESReport Card 3Earnings Guide 33

Two thousandand fifteen beganon a high note.After winning themajority mandatein the generalelection of May2014, theNarendra Modi-led National Democratic Alliance bagged the key states ofHaryana and Maharashtra in the assembly elections in late2014 and also garnered enough seats in the Jammu & Kashmirelection to become part of the ruling alliance in the state. Nowonder, a lot was expected from the government on the policyfront, given its strong position and political capital gained in2014.

TECHNICALSNifty 21

Stock Updates 11

Sharekhan Special 18

Viewpoints 19

From Sharekhan’s Desk EQUITY

05

2015: Win some; lose some FUNDAMENTALS

DERIVATIVESView 22

TECHNICALS

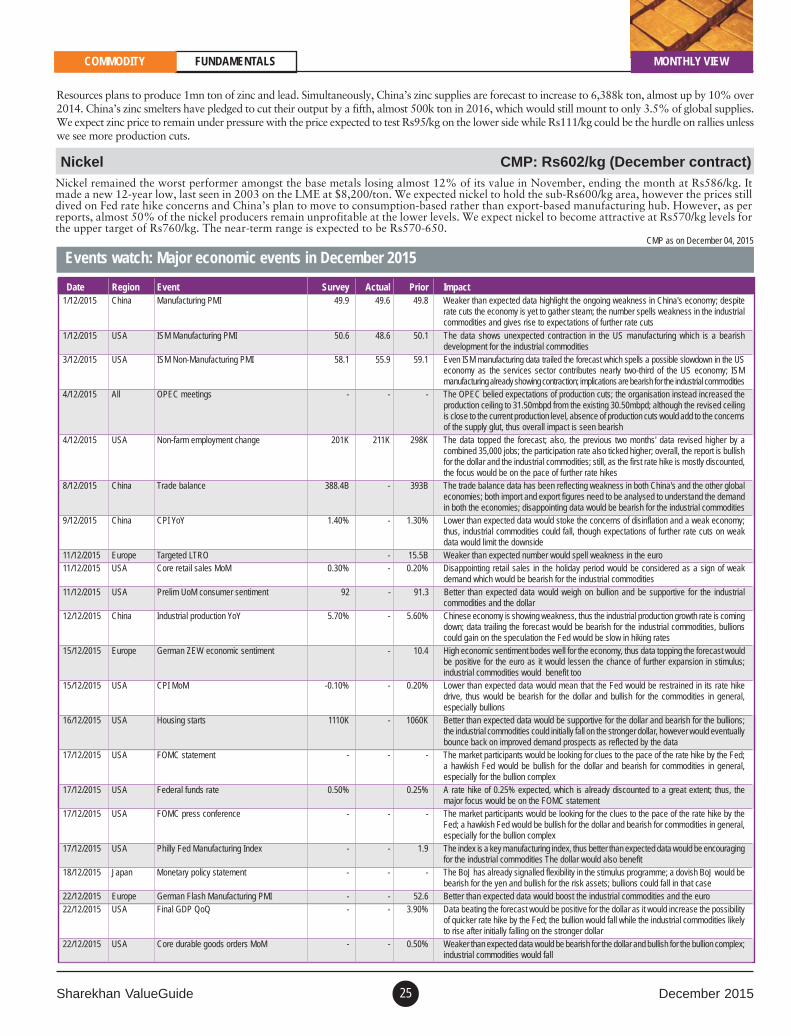

Crude Oil 23Gold 24Silver 24Copper 24Lead 24

FUNDAMENTALSZinc 24Nickel 25Castor seed 26Chana 26Soya bean 26

Gold 27Silver 27Crude Oil 27

Copper 28Jeera 28Soya bean 28

TECHNICALS

FUNDAMENTALS

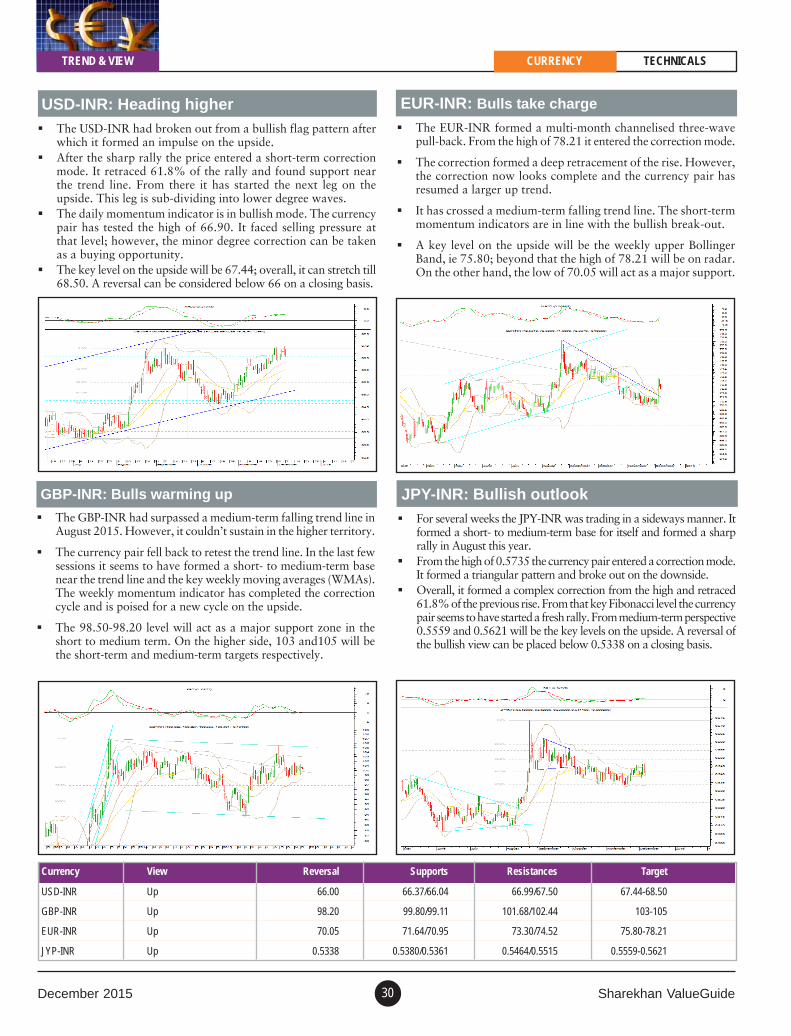

USD-INR 30EUR-INR 30

GBP-INR 30JPY-INR 30

disclaimerDISCLAIMER: “This document has been prepared by Sharekhan Ltd. (SHAREKHAN) and is intended for use only by the person or entity to which it is addressed to. This document may contain confidential and/or privileged material and is not forany type of circulation and any review, retransmission, or any other use is strictly prohibited. This document is subject to changes without prior notice. This document does not constitute an offer to sell or solicitation for the purchase or sale ofany financial instrument or as an official confirmation of any transaction. Though disseminated to all customers who are due to receive the same, not all customers may receive this report at the same time. SHAREKHAN will not treat recipientsas customers by virtue of their receiving this report. The information contained herein is obtained from publicly available data or other sources believed to be reliable and SHAREKHAN has not independently verified the accuracy andcompleteness of the said data and hence it should not be relied upon as such. While we would endeavour to update the information herein on a reasonable basis, SHAREKHAN, its subsidiaries and associated companies, their directors andemployees (“SHAREKHAN and affiliates”) are under no obligation to update or keep the information current. Also, there may be regulatory, compliance, or other reasons that may prevent SHAREKHAN and affiliates from doing so. This documentis prepared for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. Recipients of this report should also be aware that past performance is not necessarily a guide to future performanceand value of investments can go down as well. The user assumes the entire risk of any use made of this information. Each recipient of this document should make such investigations as he deems necessary to arrive at an independent evaluationof an investment in the securities of companies referred to in this document (including the merits and risks involved), and should consult his own advisors to determine the merits and risks of such an investment. The investment discussed orviews expressed may not be suitable for all investors. We do not undertake to advise you as to any change of our views. Affiliates of SHAREKHAN may have issued other reports that are inconsistent with and reach different conclusion from theinformation presented in this report. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution,publication, availability or use would be contrary to law, regulation or which would subject SHAREKHAN and affiliates to any registration or licencing requirement within such jurisdiction. The securities described herein may or may not be eligiblefor sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction. Either SHAREKHAN or its affiliates or its directors oremployees/representatives/clients or their relatives may have position(s), make market, act as principal or engage in transactions of purchase or sell of securities, from time to time or may be materially interested in any of the securities or relatedsecurities referred to in this report and they may have used the information set forth herein before publication. SHAREKHAN may from time to time solicit from, or perform investment banking, or other services for, any company mentioned herein.Without limiting any of the foregoing, in no event shall SHAREKHAN, any of its affiliates or any third party involved in, or related to, computing or compiling the information have any liability for any damages of any kind. The analyst certifies thatall of the views expressed in this document accurately reflect his or her personal views about the subject company or companies and its or their securities and do not necessarily reflect those of SHAREKHAN. Further, no part of the analyst’scompensation was, is or will be, directly or indirectly related to specific recommendations or views expressed in this document.”Please refer the Risk Disclosure Document issued by SEBI and go through the Rights and Obligations and Do’s and Dont’s issued by Stock Exchanges and Depositories before trading on the Stock Exchanges. Please refer disclaimer for Terms of Use.

Compliance Officer: Ms. Namita Amod Godbole; Tel: 022-6115000; e-mail: [email protected] • Contact: [email protected]

COMMODITY

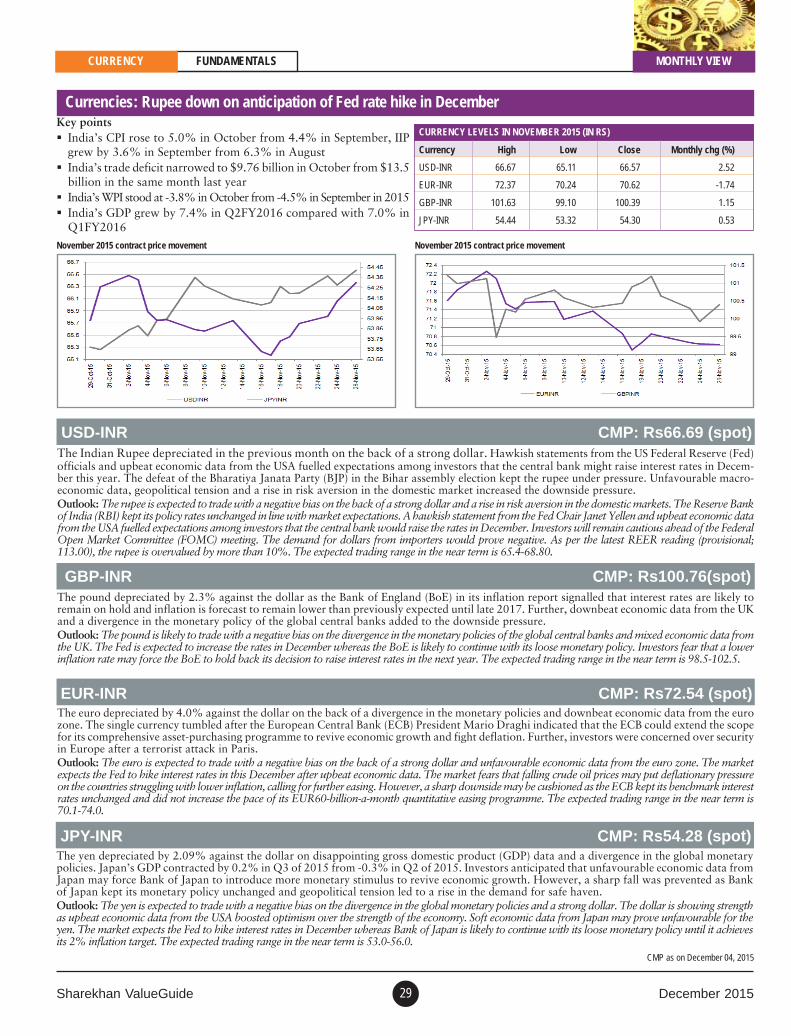

CURRENCY

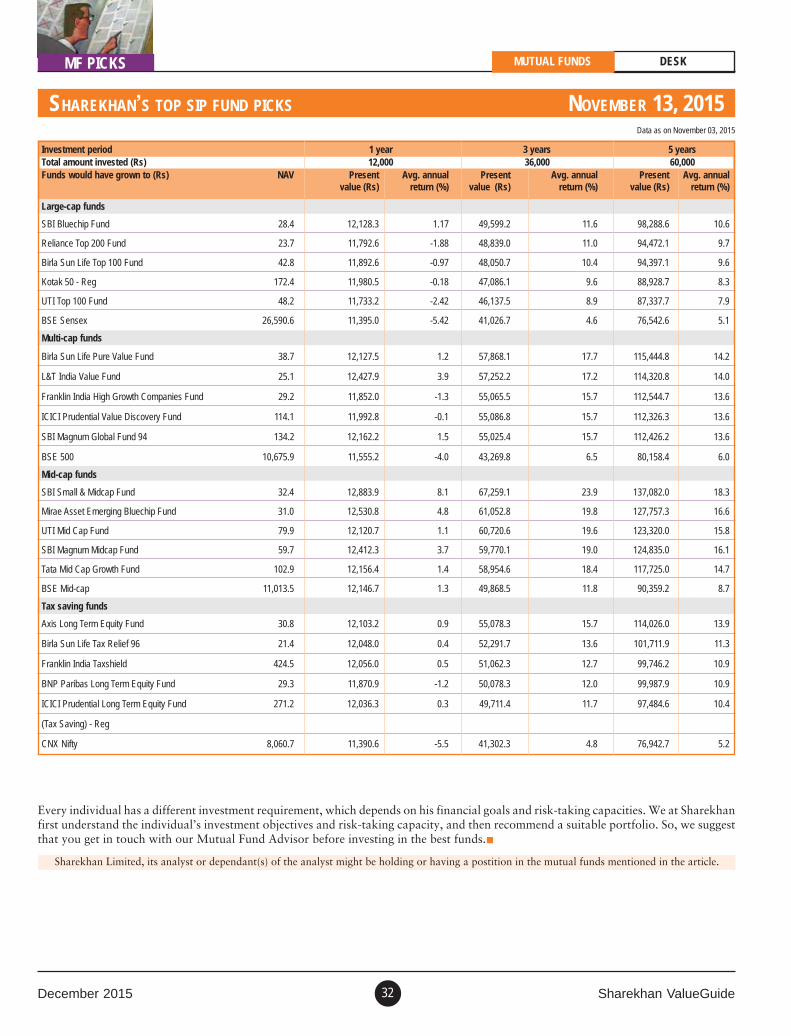

MUTUAL FUNDS DESK

Top MF Picks (equity) 31

Top SIP Fund Picks 32

RESEARCH BASED EQUITY PRODUCTS

Top Picks Basket 06Wealth Creator Portfolio 10

GBP-INR 29JPY-INR 29

USD-INR 29EUR-INR 29

REGISTRATION DETAILS Regd Add: Sharekhan Limited, 10th Floor, Beta Building, Lodha iThink Techno Campus, Off. JVLR, Opp. Kanjurmarg Railway Station,Kanjurmarg (East), Mumbai – 400042, Maharashtra. Tel: 022 - 61150000. Fax: 67481899; E-mail: [email protected]; Website: www.sharekhan.com;CIN: U99999MH1995PLC087498. Sharekhan Ltd.: SEBI Regn. Nos. BSE- INB/INF011073351 ; CD-INE011073351; NSE– INB/INF231073330; CD-INE231073330; MSEI-INB/INF261073333 ; CD-INE261073330; DP-NSDL-IN-DP-NSDL-233-2003 ; CDSL-IN-DP-CDSL-271-2004 ; PMS-INP000000662; Mutual Fund-ARN 20669 ; Commoditytrading through Sharekhan Commodities Pvt. Ltd.: MCX-10080 ; (MCX/TCM/CORP/0425) ; NCDEX-00132 ; (NCDEX/TCM/CORP/0142) ; NCDEX SPOT-NCDEXSPOT/116/CO/11/20626; For any complaints email at [email protected] ; Disclaimer: Client should read the Risk Disclosure Document issued by SEBI & relevantexchanges and Do’s & Don’ts by MCX & NCDEX and the T & C on www.sharekhan.com before investing.

CONTENTS

Sharekhan ValueGuide December 20153

REPORT CARD EQUITY FUNDAMENTALS

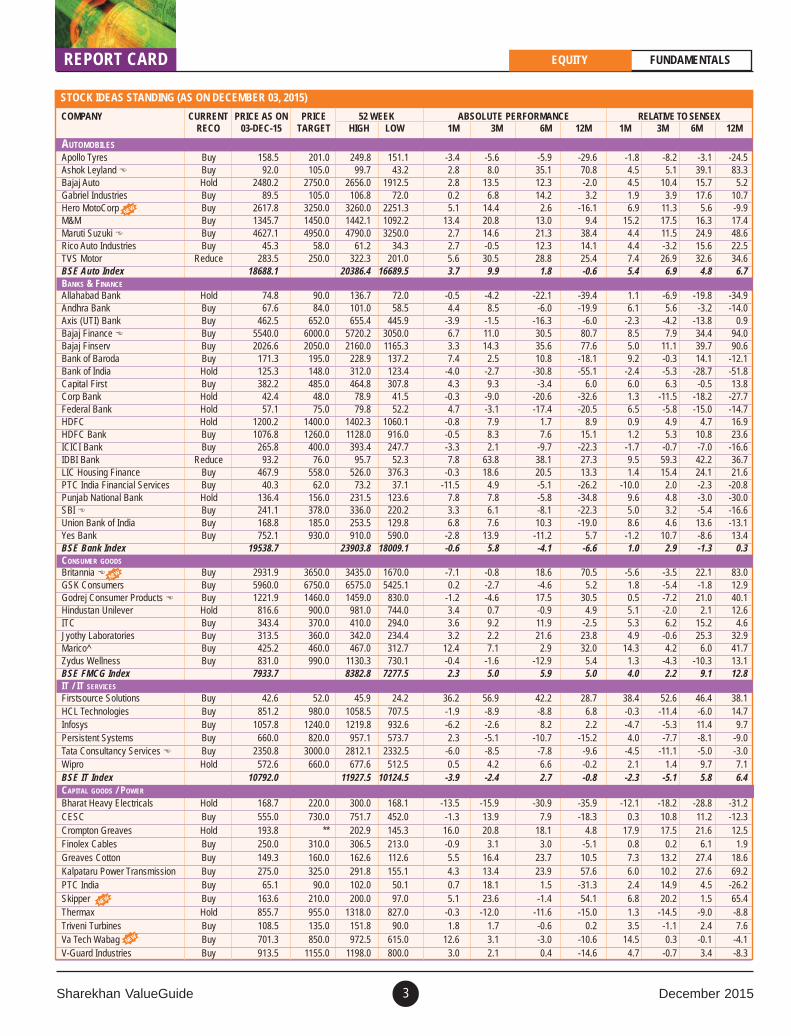

STOCK IDEAS STANDING (AS ON DECEMBER 03, 2015)

COMPANY CURRENT PRICE AS ON PRICE 52 WEEK ABSOLUTE PERFORMANCE RELATIVE TO SENSEXRECO 03-DEC-15 TARGET HIGH LOW 1M 3M 6M 12M 1M 3M 6M 12M

AUTOMOBILES

Apollo Tyres Buy 158.5 201.0 249.8 151.1 -3.4 -5.6 -5.9 -29.6 -1.8 -8.2 -3.1 -24.5Ashok Leyland Buy 92.0 105.0 99.7 43.2 2.8 8.0 35.1 70.8 4.5 5.1 39.1 83.3Bajaj Auto Hold 2480.2 2750.0 2656.0 1912.5 2.8 13.5 12.3 -2.0 4.5 10.4 15.7 5.2Gabriel Industries Buy 89.5 105.0 106.8 72.0 0.2 6.8 14.2 3.2 1.9 3.9 17.6 10.7Hero MotoCorp Buy 2617.8 3250.0 3260.0 2251.3 5.1 14.4 2.6 -16.1 6.9 11.3 5.6 -9.9M&M Buy 1345.7 1450.0 1442.1 1092.2 13.4 20.8 13.0 9.4 15.2 17.5 16.3 17.4Maruti Suzuki Buy 4627.1 4950.0 4790.0 3250.0 2.7 14.6 21.3 38.4 4.4 11.5 24.9 48.6Rico Auto Industries Buy 45.3 58.0 61.2 34.3 2.7 -0.5 12.3 14.1 4.4 -3.2 15.6 22.5TVS Motor Reduce 283.5 250.0 322.3 201.0 5.6 30.5 28.8 25.4 7.4 26.9 32.6 34.6BSE Auto Index 18688.1 20386.4 16689.5 3.7 9.9 1.8 -0.6 5.4 6.9 4.8 6.7BANKS & FINANCE

Allahabad Bank Hold 74.8 90.0 136.7 72.0 -0.5 -4.2 -22.1 -39.4 1.1 -6.9 -19.8 -34.9Andhra Bank Buy 67.6 84.0 101.0 58.5 4.4 8.5 -6.0 -19.9 6.1 5.6 -3.2 -14.0Axis (UTI) Bank Buy 462.5 652.0 655.4 445.9 -3.9 -1.5 -16.3 -6.0 -2.3 -4.2 -13.8 0.9Bajaj Finance Buy 5540.0 6000.0 5720.2 3050.0 6.7 11.0 30.5 80.7 8.5 7.9 34.4 94.0Bajaj Finserv Buy 2026.6 2050.0 2160.0 1165.3 3.3 14.3 35.6 77.6 5.0 11.1 39.7 90.6Bank of Baroda Buy 171.3 195.0 228.9 137.2 7.4 2.5 10.8 -18.1 9.2 -0.3 14.1 -12.1Bank of India Hold 125.3 148.0 312.0 123.4 -4.0 -2.7 -30.8 -55.1 -2.4 -5.3 -28.7 -51.8Capital First Buy 382.2 485.0 464.8 307.8 4.3 9.3 -3.4 6.0 6.0 6.3 -0.5 13.8Corp Bank Hold 42.4 48.0 78.9 41.5 -0.3 -9.0 -20.6 -32.6 1.3 -11.5 -18.2 -27.7Federal Bank Hold 57.1 75.0 79.8 52.2 4.7 -3.1 -17.4 -20.5 6.5 -5.8 -15.0 -14.7HDFC Hold 1200.2 1400.0 1402.3 1060.1 -0.8 7.9 1.7 8.9 0.9 4.9 4.7 16.9HDFC Bank Buy 1076.8 1260.0 1128.0 916.0 -0.5 8.3 7.6 15.1 1.2 5.3 10.8 23.6ICICI Bank Buy 265.8 400.0 393.4 247.7 -3.3 2.1 -9.7 -22.3 -1.7 -0.7 -7.0 -16.6IDBI Bank Reduce 93.2 76.0 95.7 52.3 7.8 63.8 38.1 27.3 9.5 59.3 42.2 36.7LIC Housing Finance Buy 467.9 558.0 526.0 376.3 -0.3 18.6 20.5 13.3 1.4 15.4 24.1 21.6PTC India Financial Services Buy 40.3 62.0 73.2 37.1 -11.5 4.9 -5.1 -26.2 -10.0 2.0 -2.3 -20.8Punjab National Bank Hold 136.4 156.0 231.5 123.6 7.8 7.8 -5.8 -34.8 9.6 4.8 -3.0 -30.0SBI Buy 241.1 378.0 336.0 220.2 3.3 6.1 -8.1 -22.3 5.0 3.2 -5.4 -16.6Union Bank of India Buy 168.8 185.0 253.5 129.8 6.8 7.6 10.3 -19.0 8.6 4.6 13.6 -13.1Yes Bank Buy 752.1 930.0 910.0 590.0 -2.8 13.9 -11.2 5.7 -1.2 10.7 -8.6 13.4BSE Bank Index 19538.7 23903.8 18009.1 -0.6 5.8 -4.1 -6.6 1.0 2.9 -1.3 0.3CONSUMER GOODS

Britannia Buy 2931.9 3650.0 3435.0 1670.0 -7.1 -0.8 18.6 70.5 -5.6 -3.5 22.1 83.0GSK Consumers Buy 5960.0 6750.0 6575.0 5425.1 0.2 -2.7 -4.6 5.2 1.8 -5.4 -1.8 12.9Godrej Consumer Products Buy 1221.9 1460.0 1459.0 830.0 -1.2 -4.6 17.5 30.5 0.5 -7.2 21.0 40.1Hindustan Unilever Hold 816.6 900.0 981.0 744.0 3.4 0.7 -0.9 4.9 5.1 -2.0 2.1 12.6ITC Buy 343.4 370.0 410.0 294.0 3.6 9.2 11.9 -2.5 5.3 6.2 15.2 4.6Jyothy Laboratories Buy 313.5 360.0 342.0 234.4 3.2 2.2 21.6 23.8 4.9 -0.6 25.3 32.9Marico^ Buy 425.2 460.0 467.0 312.7 12.4 7.1 2.9 32.0 14.3 4.2 6.0 41.7Zydus Wellness Buy 831.0 990.0 1130.3 730.1 -0.4 -1.6 -12.9 5.4 1.3 -4.3 -10.3 13.1BSE FMCG Index 7933.7 8382.8 7277.5 2.3 5.0 5.9 5.0 4.0 2.2 9.1 12.8IT / IT SERVICES

Firstsource Solutions Buy 42.6 52.0 45.9 24.2 36.2 56.9 42.2 28.7 38.4 52.6 46.4 38.1HCL Technologies Buy 851.2 980.0 1058.5 707.5 -1.9 -8.9 -8.8 6.8 -0.3 -11.4 -6.0 14.7Infosys Buy 1057.8 1240.0 1219.8 932.6 -6.2 -2.6 8.2 2.2 -4.7 -5.3 11.4 9.7Persistent Systems Buy 660.0 820.0 957.1 573.7 2.3 -5.1 -10.7 -15.2 4.0 -7.7 -8.1 -9.0Tata Consultancy Services Buy 2350.8 3000.0 2812.1 2332.5 -6.0 -8.5 -7.8 -9.6 -4.5 -11.1 -5.0 -3.0Wipro Hold 572.6 660.0 677.6 512.5 0.5 4.2 6.6 -0.2 2.1 1.4 9.7 7.1BSE IT Index 10792.0 11927.5 10124.5 -3.9 -2.4 2.7 -0.8 -2.3 -5.1 5.8 6.4CAPITAL GOODS / POWER

Bharat Heavy Electricals Hold 168.7 220.0 300.0 168.1 -13.5 -15.9 -30.9 -35.9 -12.1 -18.2 -28.8 -31.2CESC Buy 555.0 730.0 751.7 452.0 -1.3 13.9 7.9 -18.3 0.3 10.8 11.2 -12.3Crompton Greaves Hold 193.8 ** 202.9 145.3 16.0 20.8 18.1 4.8 17.9 17.5 21.6 12.5Finolex Cables Buy 250.0 310.0 306.5 213.0 -0.9 3.1 3.0 -5.1 0.8 0.2 6.1 1.9Greaves Cotton Buy 149.3 160.0 162.6 112.6 5.5 16.4 23.7 10.5 7.3 13.2 27.4 18.6Kalpataru Power Transmission Buy 275.0 325.0 291.8 155.1 4.3 13.4 23.9 57.6 6.0 10.2 27.6 69.2PTC India Buy 65.1 90.0 102.0 50.1 0.7 18.1 1.5 -31.3 2.4 14.9 4.5 -26.2Skipper Buy 163.6 210.0 200.0 97.0 5.1 23.6 -1.4 54.1 6.8 20.2 1.5 65.4Thermax Hold 855.7 955.0 1318.0 827.0 -0.3 -12.0 -11.6 -15.0 1.3 -14.5 -9.0 -8.8Triveni Turbines Buy 108.5 135.0 151.8 90.0 1.8 1.7 -0.6 0.2 3.5 -1.1 2.4 7.6Va Tech Wabag Buy 701.3 850.0 972.5 615.0 12.6 3.1 -3.0 -10.6 14.5 0.3 -0.1 -4.1V-Guard Industries Buy 913.5 1155.0 1198.0 800.0 3.0 2.1 0.4 -14.6 4.7 -0.7 3.4 -8.3

NEW

NEW

NEW

NEW

December 2015 Sharekhan ValueGuide4

REPORT CARDEQUITY FUNDAMENTALS

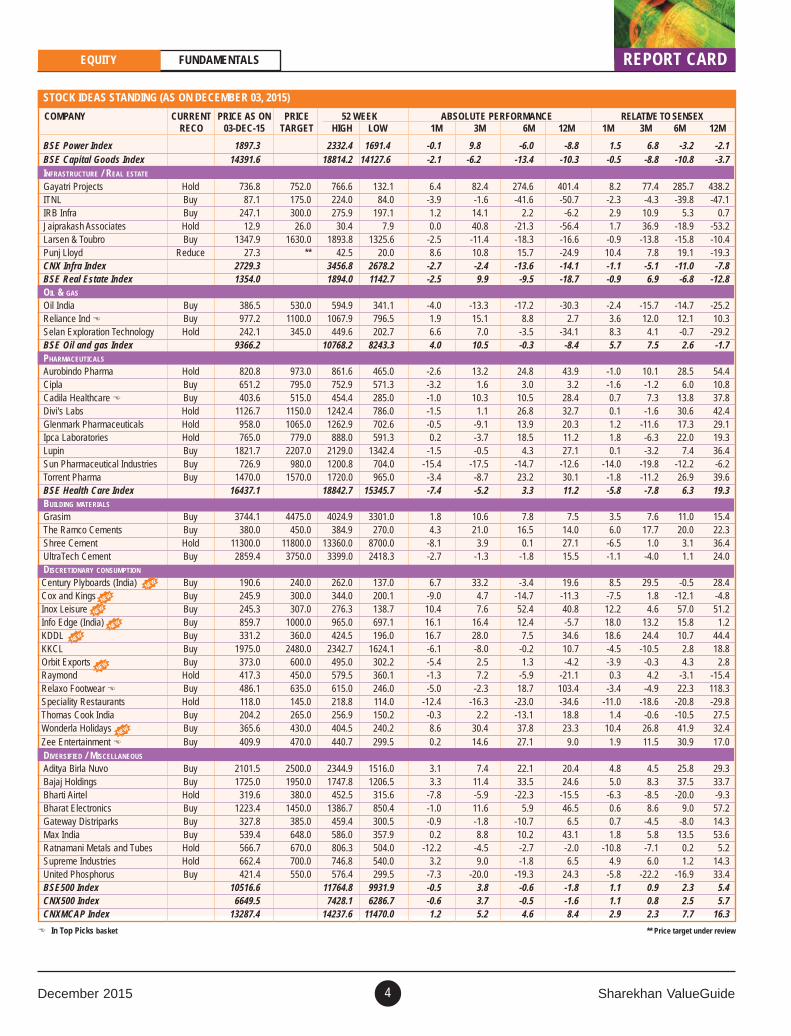

STOCK IDEAS STANDING (AS ON DECEMBER 03, 2015)

COMPANY CURRENT PRICE AS ON PRICE 52 WEEK ABSOLUTE PERFORMANCE RELATIVE TO SENSEXRECO 03-DEC-15 TARGET HIGH LOW 1M 3M 6M 12M 1M 3M 6M 12M

In Top Picks basket ** Price target under review

NEW

NEW

NEW

NEW

NEW

NEW

NEW

BSE Power Index 1897.3 2332.4 1691.4 -0.1 9.8 -6.0 -8.8 1.5 6.8 -3.2 -2.1BSE Capital Goods Index 14391.6 18814.2 14127.6 -2.1 -6.2 -13.4 -10.3 -0.5 -8.8 -10.8 -3.7INFRASTRUCTURE / REAL ESTATE

Gayatri Projects Hold 736.8 752.0 766.6 132.1 6.4 82.4 274.6 401.4 8.2 77.4 285.7 438.2ITNL Buy 87.1 175.0 224.0 84.0 -3.9 -1.6 -41.6 -50.7 -2.3 -4.3 -39.8 -47.1IRB Infra Buy 247.1 300.0 275.9 197.1 1.2 14.1 2.2 -6.2 2.9 10.9 5.3 0.7Jaiprakash Associates Hold 12.9 26.0 30.4 7.9 0.0 40.8 -21.3 -56.4 1.7 36.9 -18.9 -53.2Larsen & Toubro Buy 1347.9 1630.0 1893.8 1325.6 -2.5 -11.4 -18.3 -16.6 -0.9 -13.8 -15.8 -10.4Punj Lloyd Reduce 27.3 ** 42.5 20.0 8.6 10.8 15.7 -24.9 10.4 7.8 19.1 -19.3CNX Infra Index 2729.3 3456.8 2678.2 -2.7 -2.4 -13.6 -14.1 -1.1 -5.1 -11.0 -7.8BSE Real Estate Index 1354.0 1894.0 1142.7 -2.5 9.9 -9.5 -18.7 -0.9 6.9 -6.8 -12.8OIL & GAS

Oil India Buy 386.5 530.0 594.9 341.1 -4.0 -13.3 -17.2 -30.3 -2.4 -15.7 -14.7 -25.2Reliance Ind Buy 977.2 1100.0 1067.9 796.5 1.9 15.1 8.8 2.7 3.6 12.0 12.1 10.3Selan Exploration Technology Hold 242.1 345.0 449.6 202.7 6.6 7.0 -3.5 -34.1 8.3 4.1 -0.7 -29.2BSE Oil and gas Index 9366.2 10768.2 8243.3 4.0 10.5 -0.3 -8.4 5.7 7.5 2.6 -1.7PHARMACEUTICALS

Aurobindo Pharma Hold 820.8 973.0 861.6 465.0 -2.6 13.2 24.8 43.9 -1.0 10.1 28.5 54.4Cipla Buy 651.2 795.0 752.9 571.3 -3.2 1.6 3.0 3.2 -1.6 -1.2 6.0 10.8Cadila Healthcare Buy 403.6 515.0 454.4 285.0 -1.0 10.3 10.5 28.4 0.7 7.3 13.8 37.8Divi's Labs Hold 1126.7 1150.0 1242.4 786.0 -1.5 1.1 26.8 32.7 0.1 -1.6 30.6 42.4Glenmark Pharmaceuticals Hold 958.0 1065.0 1262.9 702.6 -0.5 -9.1 13.9 20.3 1.2 -11.6 17.3 29.1Ipca Laboratories Hold 765.0 779.0 888.0 591.3 0.2 -3.7 18.5 11.2 1.8 -6.3 22.0 19.3Lupin Buy 1821.7 2207.0 2129.0 1342.4 -1.5 -0.5 4.3 27.1 0.1 -3.2 7.4 36.4Sun Pharmaceutical Industries Buy 726.9 980.0 1200.8 704.0 -15.4 -17.5 -14.7 -12.6 -14.0 -19.8 -12.2 -6.2Torrent Pharma Buy 1470.0 1570.0 1720.0 965.0 -3.4 -8.7 23.2 30.1 -1.8 -11.2 26.9 39.6BSE Health Care Index 16437.1 18842.7 15345.7 -7.4 -5.2 3.3 11.2 -5.8 -7.8 6.3 19.3BUILDING MATERIALS

Grasim Buy 3744.1 4475.0 4024.9 3301.0 1.8 10.6 7.8 7.5 3.5 7.6 11.0 15.4The Ramco Cements Buy 380.0 450.0 384.9 270.0 4.3 21.0 16.5 14.0 6.0 17.7 20.0 22.3Shree Cement Hold 11300.0 11800.0 13360.0 8700.0 -8.1 3.9 0.1 27.1 -6.5 1.0 3.1 36.4UltraTech Cement Buy 2859.4 3750.0 3399.0 2418.3 -2.7 -1.3 -1.8 15.5 -1.1 -4.0 1.1 24.0DISCRETIONARY CONSUMPTION

Century Plyboards (India) Buy 190.6 240.0 262.0 137.0 6.7 33.2 -3.4 19.6 8.5 29.5 -0.5 28.4Cox and Kings Buy 245.9 300.0 344.0 200.1 -9.0 4.7 -14.7 -11.3 -7.5 1.8 -12.1 -4.8Inox Leisure Buy 245.3 307.0 276.3 138.7 10.4 7.6 52.4 40.8 12.2 4.6 57.0 51.2Info Edge (India) Buy 859.7 1000.0 965.0 697.1 16.1 16.4 12.4 -5.7 18.0 13.2 15.8 1.2KDDL Buy 331.2 360.0 424.5 196.0 16.7 28.0 7.5 34.6 18.6 24.4 10.7 44.4KKCL Buy 1975.0 2480.0 2342.7 1624.1 -6.1 -8.0 -0.2 10.7 -4.5 -10.5 2.8 18.8Orbit Exports Buy 373.0 600.0 495.0 302.2 -5.4 2.5 1.3 -4.2 -3.9 -0.3 4.3 2.8Raymond Hold 417.3 450.0 579.5 360.1 -1.3 7.2 -5.9 -21.1 0.3 4.2 -3.1 -15.4Relaxo Footwear Buy 486.1 635.0 615.0 246.0 -5.0 -2.3 18.7 103.4 -3.4 -4.9 22.3 118.3Speciality Restaurants Hold 118.0 145.0 218.8 114.0 -12.4 -16.3 -23.0 -34.6 -11.0 -18.6 -20.8 -29.8Thomas Cook India Buy 204.2 265.0 256.9 150.2 -0.3 2.2 -13.1 18.8 1.4 -0.6 -10.5 27.5Wonderla Holidays Buy 365.6 430.0 404.5 240.2 8.6 30.4 37.8 23.3 10.4 26.8 41.9 32.4Zee Entertainment Buy 409.9 470.0 440.7 299.5 0.2 14.6 27.1 9.0 1.9 11.5 30.9 17.0DIVERSIFIED / MISCELLANEOUS

Aditya Birla Nuvo Buy 2101.5 2500.0 2344.9 1516.0 3.1 7.4 22.1 20.4 4.8 4.5 25.8 29.3Bajaj Holdings Buy 1725.0 1950.0 1747.8 1206.5 3.3 11.4 33.5 24.6 5.0 8.3 37.5 33.7Bharti Airtel Hold 319.6 380.0 452.5 315.6 -7.8 -5.9 -22.3 -15.5 -6.3 -8.5 -20.0 -9.3Bharat Electronics Buy 1223.4 1450.0 1386.7 850.4 -1.0 11.6 5.9 46.5 0.6 8.6 9.0 57.2Gateway Distriparks Buy 327.8 385.0 459.4 300.5 -0.9 -1.8 -10.7 6.5 0.7 -4.5 -8.0 14.3Max India Buy 539.4 648.0 586.0 357.9 0.2 8.8 10.2 43.1 1.8 5.8 13.5 53.6Ratnamani Metals and Tubes Hold 566.7 670.0 806.3 504.0 -12.2 -4.5 -2.7 -2.0 -10.8 -7.1 0.2 5.2Supreme Industries Hold 662.4 700.0 746.8 540.0 3.2 9.0 -1.8 6.5 4.9 6.0 1.2 14.3United Phosphorus Buy 421.4 550.0 576.4 299.5 -7.3 -20.0 -19.3 24.3 -5.8 -22.2 -16.9 33.4BSE500 Index 10516.6 11764.8 9931.9 -0.5 3.8 -0.6 -1.8 1.1 0.9 2.3 5.4CNX500 Index 6649.5 7428.1 6286.7 -0.6 3.7 -0.5 -1.6 1.1 0.8 2.5 5.7CNXMCAP Index 13287.4 14237.6 11470.0 1.2 5.2 4.6 8.4 2.9 2.3 7.7 16.3

Sharekhan ValueGuide December 20155

2015: Win some; lose some

FROM SHAREKHAN’S DESK

from

sha

rekh

an’s

des

k Two thousand and fifteen began on a high note. After winning the majority mandate in thegeneral election of May 2014, the Narendra Modi-led National Democratic Alliance baggedthe key states of Haryana and Maharashtra in the assembly elections in late 2014 and alsogarnered enough seats in the Jammu & Kashmir election to become part of the ruling alliancein the state.

No wonder, a lot was expected from the government on the policy front, given its strongposition and political capital gained in 2014. Backed by policy activism and improving macroconditions, the economy was expected to revive sooner than later and start reflecting on corporateearnings from FY2016 itself.

However, the hopes were belied in 2015. Key policy bills are stuck in the upper house of theParliament where the new government lacks a brute majority and has been unable to form apolitical consensus to push through the reforms. Perhaps the government also underestimatedthe extent of the economic damage and the complexity of repairing the economy. On the otherhand, market participants are guilty of building unrealistic hopes of a quick recovery in theeconomy.

But all is not lost yet. The government on its part has taken several executive decisions that arereviving and revitalising certain pockets of the economy, like the road, power transmission anddistribution, and mining sectors, and addressing the ills of the power sector (including therestructuring of the state electricity boards). Additionally, the government has made efforts tostreamline the delivery of subsidies and other rural schemes (thereby reducing the leakage) andmoderated the hike in the support prices for the procurement of agricultural produce to controlstructurally high inflationary trends. This has not only resulted in a better fiscal health but alsoprovided enough room to the Reserve Bank of India to reduce the policy rates by 125 basispoints in the last one year.

Consequently, the macro conditions have distinctly improved in 2015 and built the right basefor the economy. At the same time, the expectations have mellowed significantly now. It isclearly visible in the 12-14% cut in the consensus estimate of the Sensex earnings over FY2016and FY2017. On the policy front, the government has turned more flexible and receptive to thedemand of the opposition parties in a bid to make progress on the key reforms including theGoods and Services Tax (GST) Bill. The rationalisation of the indirect tax regime under theGST could potentially add 1.0-1.5% to India’s gross domestic product (GDP) growth in thecoming years.

Globally, the dynamics are set to change after a status quo for the past seven years. Within thedeveloped economies, the USA would begin tightening its monetary policy with a rate hike inthe forthcoming policy meet. On the other hand, Europe, China and Japan are likely to pursuea very accommodative policy stance in the foreseeable future. The move could cause gyrationsin the financial markets especially the foreign exchange and emerging equity markets.

However, past experience (including the recent event of the withdrawal of quantitative easingto the tune of $85 billion per month by the USA) shows that the markets quickly adjust tochanges and volatility is seen more during the run-up to an event rather than after it. Moreover,India is much better placed now to face any global upheaval. As compared to being part of the“Fragile Five” group of stressed economies India is seen as one of the few bright spots globallytoday, thanks to the good work done by the new government and a very capable economist atthe helm of the RBI.

Importantly for investors, the macro situation is better than the last year’s. The government isreaching out to the opposition parties to build a political consensus to push through reforms.Corporate earnings would look up on a low base effect and a gradual reflection of the improvedmacros in the business momentum. Plus, valuations are comfortable. An ideal set-up for stockpickers and long-term investors!

December 2015 Sharekhan ValueGuide6

EQUITY FUNDAMENTALSSHAREKHAN TOP PICKS

Sharekhan Top PicksSHAREKHAN TOP PICKS

Benchmark indices continued to move in a narrow range with anegative bias in November of 2015. The unfavourable results of Biharstate elections and lacklustre Q2FY2016 performance of corporateswere the key concerning factors locally. The rising probability of arate hike in the USA and the surge in volatility in the Chinese marketadded to the weakness in market sentiment.

The benchmark indices, Nifty and Sensex, ended the month with aloss of 1.6% and 1.9% respectively since our last revision of the TopPicks basket on October 31, 2015. The Top Picks basket performedin line with the benchmark indices with a decline of 1.9% in thesame period. However, it should be noted that this was despite adent of close to 15% taken in Dr Reddy’s Laboratories (DRL) afterthe unexpected warning letter for three of its manufacturing plants

*CMP as on November 30, 2015 # Price target for next 6-12 months ** Under review

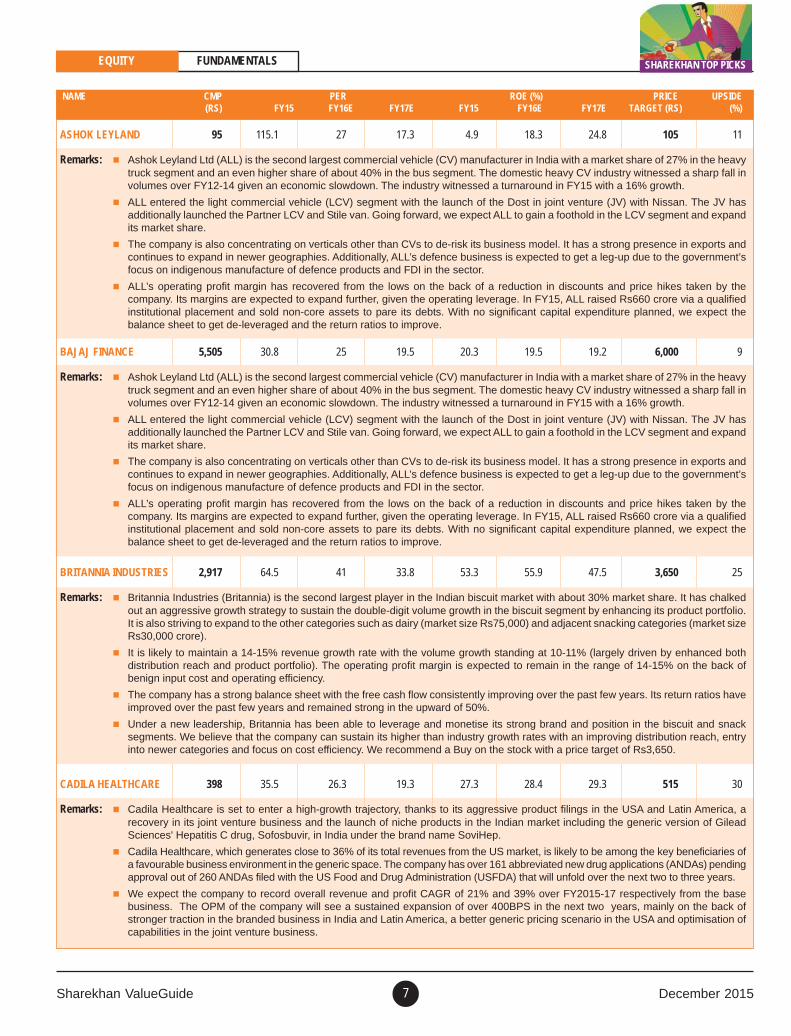

NAME CMP* PER ROE (%) PRICE UPSIDE(RS) FY15 FY16E FY17E FY15 FY16E FY17E TARGET (RS)# (%)

Ashok Leyland 95 115.1 27 17.3 4.9 18.3 24.8 105 11

Bajaj Finance 5,505 30.8 25 19.5 20.3 19.5 19.2 6,000 9

Britannia Industries 2,917 64.5 41 33.8 53.3 55.9 47.5 3,650 25

Cadila Healthcare 398 35.5 26.3 19.3 27.3 28.4 29.3 515 30

GCPL 1,245 45.9 37.2 30.2 24.6 25.7 25.8 1,460 17

IndusInd Bank 932 27.6 22.2 17.5 19.2 20.5 21.5 1,108 19

Maruti Suzuki 4,559 37.1 25.5 20.1 16.6 20.8 22.2 4,950 9

Relaxo Footwear 510 59.3 45.9 34.0 22.1 22.3 24.9 635 25

Reliance Industries 969 12.1 12.4 10.4 10.8 9.7 10.5 1,100 14

SBI 249 14.2 10.4 7.8 10.6 13.2 15.7 378 52

TCS 2,371 87.5 70.8 57.5 33.7 32.7 29.7 3,000 27

Zee Entertainment 410 4.1 3.3 3.0 19.0 18.8 20.6 470 15

ABSOLUTE RETURNS (TOP PICKS VS BENCHMARK INDICES) % CONSTANTLY BEATING NIFTY AND SENSEX (CUMULATIVE RETURNS) SINCEAPRIL 2009Sharekhan Sensex Nifty CNX

(Top Picks) MIDCAP

YTD CY2015 13.8 -5.0 -4.2 5.3

CY2014 63.6 29.9 30.9 55.1

CY2013 12.4 8.5 6.4 -5.6

CY2012 35.1 26.2 29.0 36.0

CY2011 -20.5 -21.2 -21.7 -25.0

CY2010 16.8 11.5 12.9 11.5

CY2009 116.1 76.1 72.0 114.0

Since inception 422.7 160.5 160.3 265.7(Jan 2009)

CONSISTENT OUTPERFORMANCE (ABSOLUTE RETURNS; NOT ANNUALISED) (%)1 month 3 months 6 months 1 year 3 years 5 years

Top Picks -1.9 2.4 0.7 16.3 114.9 120.0

Sensex -1.9 -0.5 -6.1 -8.6 35.5 31.0

Nifty -1.6 -0.4 -6.0 -7.2 35.2 32.6

CNX Mid-cap 0.1 1.4 0.5 7.2 62.9 48.2

Please note the returns are based on the assumption that at the beginning of each month an equal amount was invested in each stock of the Top Picks basket

earlier in the month. Consequently, we had replaced DRL with GodrejConsumer Products on an intra-month basis. Excluding the impactof DRL the Top Picks basket declined by 0.7% during the last month.

We are not making any change in the Top Picks basket for the eventfulmonth of December. In the next month, central bankers would be infocus with the scheduled review meeting of the Reserve Bank of Indiain India and that of the US Federal Reserve and European CentralBank in the two developed regions of the world. Expectations arealso building up from the ongoing winter session of the Parliamentsince the government has reached out to the opposition parties forthe passage of the Goods and Services Tax Bill and other criticalpending reforms.

Sharekhan ValueGuide December 20157

NAME CMP PER ROE (%) PRICE UPSIDE(RS) FY15 FY16E FY17E FY15 FY16E FY17E TARGET (RS) (%)

ASHOK LEYLAND 95 115.1 27 17.3 4.9 18.3 24.8 105 11

Remarks: Ashok Leyland Ltd (ALL) is the second largest commercial vehicle (CV) manufacturer in India with a market share of 27% in the heavytruck segment and an even higher share of about 40% in the bus segment. The domestic heavy CV industry witnessed a sharp fall involumes over FY12-14 given an economic slowdown. The industry witnessed a turnaround in FY15 with a 16% growth.

ALL entered the light commercial vehicle (LCV) segment with the launch of the Dost in joint venture (JV) with Nissan. The JV hasadditionally launched the Partner LCV and Stile van. Going forward, we expect ALL to gain a foothold in the LCV segment and expandits market share.

The company is also concentrating on verticals other than CVs to de-risk its business model. It has a strong presence in exports andcontinues to expand in newer geographies. Additionally, ALL’s defence business is expected to get a leg-up due to the government’sfocus on indigenous manufacture of defence products and FDI in the sector.

ALL’s operating profit margin has recovered from the lows on the back of a reduction in discounts and price hikes taken by thecompany. Its margins are expected to expand further, given the operating leverage. In FY15, ALL raised Rs660 crore via a qualifiedinstitutional placement and sold non-core assets to pare its debts. With no significant capital expenditure planned, we expect thebalance sheet to get de-leveraged and the return ratios to improve.

EQUITY FUNDAMENTALS SHAREKHAN TOP PICKS

BAJAJ FINANCE 5,505 30.8 25 19.5 20.3 19.5 19.2 6,000 9

Remarks: Ashok Leyland Ltd (ALL) is the second largest commercial vehicle (CV) manufacturer in India with a market share of 27% in the heavytruck segment and an even higher share of about 40% in the bus segment. The domestic heavy CV industry witnessed a sharp fall involumes over FY12-14 given an economic slowdown. The industry witnessed a turnaround in FY15 with a 16% growth.

ALL entered the light commercial vehicle (LCV) segment with the launch of the Dost in joint venture (JV) with Nissan. The JV hasadditionally launched the Partner LCV and Stile van. Going forward, we expect ALL to gain a foothold in the LCV segment and expandits market share.

The company is also concentrating on verticals other than CVs to de-risk its business model. It has a strong presence in exports andcontinues to expand in newer geographies. Additionally, ALL’s defence business is expected to get a leg-up due to the government’sfocus on indigenous manufacture of defence products and FDI in the sector.

ALL’s operating profit margin has recovered from the lows on the back of a reduction in discounts and price hikes taken by thecompany. Its margins are expected to expand further, given the operating leverage. In FY15, ALL raised Rs660 crore via a qualifiedinstitutional placement and sold non-core assets to pare its debts. With no significant capital expenditure planned, we expect thebalance sheet to get de-leveraged and the return ratios to improve.

BRITANNIA INDUSTRIES 2,917 64.5 41 33.8 53.3 55.9 47.5 3,650 25

Remarks: Britannia Industries (Britannia) is the second largest player in the Indian biscuit market with about 30% market share. It has chalkedout an aggressive growth strategy to sustain the double-digit volume growth in the biscuit segment by enhancing its product portfolio.It is also striving to expand to the other categories such as dairy (market size Rs75,000) and adjacent snacking categories (market sizeRs30,000 crore).

It is likely to maintain a 14-15% revenue growth rate with the volume growth standing at 10-11% (largely driven by enhanced bothdistribution reach and product portfolio). The operating profit margin is expected to remain in the range of 14-15% on the back ofbenign input cost and operating efficiency.

The company has a strong balance sheet with the free cash flow consistently improving over the past few years. Its return ratios haveimproved over the past few years and remained strong in the upward of 50%.

Under a new leadership, Britannia has been able to leverage and monetise its strong brand and position in the biscuit and snacksegments. We believe that the company can sustain its higher than industry growth rates with an improving distribution reach, entryinto newer categories and focus on cost efficiency. We recommend a Buy on the stock with a price target of Rs3,650.

CADILA HEALTHCARE 398 35.5 26.3 19.3 27.3 28.4 29.3 515 30

Remarks: Cadila Healthcare is set to enter a high-growth trajectory, thanks to its aggressive product filings in the USA and Latin America, arecovery in its joint venture business and the launch of niche products in the Indian market including the generic version of GileadSciences' Hepatitis C drug, Sofosbuvir, in India under the brand name SoviHep.

Cadila Healthcare, which generates close to 36% of its total revenues from the US market, is likely to be among the key beneficiaries ofa favourable business environment in the generic space. The company has over 161 abbreviated new drug applications (ANDAs) pendingapproval out of 260 ANDAs filed with the US Food and Drug Administration (USFDA) that will unfold over the next two to three years.

We expect the company to record overall revenue and profit CAGR of 21% and 39% over FY2015-17 respectively from the basebusiness. The OPM of the company will see a sustained expansion of over 400BPS in the next two years, mainly on the back ofstronger traction in the branded business in India and Latin America, a better generic pricing scenario in the USA and optimisation ofcapabilities in the joint venture business.

December 2015 Sharekhan ValueGuide8

NAME CMP PER ROE (%) PRICE UPSIDE(RS) FY15 FY16E FY17E FY15 FY16E FY17E TARGET (RS) (%)

GODREJ CONSUMERS 1,245 45.9 37.2 30.2 24.6 25.7 25.8 1,460 17

Remarks: Godrej Consumer Products Ltd (GCPL) is one of the largest FMCG companies in India with a strong portfolio of brands catering to thematured and fast growing categories in the domestic market. With a slew of acquisitions in markets such as Africa, Latin America andIndonesia, it has expanded its base globally (about 40% of its revenues come from the international market.

GCPL's domestic business is performing well in a weak demand environment (grew by 9% in Q2FY2016). The key reason for a betterperformance is a presence in the under-penetrated categories such as hair color and mosquito repellent, sustained innovation in theportfolio and expansion in distribution reach. On the other hand, the business in Africa is in a consolidation phase while the Indonesianbusiness is standing tall in a favourable demand environment.

Benign input prices would continue to boost its profitability and help GCPL to take adequate promotional actions and do higher brandinvestment in a weak demand environment.

GCPL's long-term growth prospects remain intact and we expect its earnings to grow at a CAGR of above 20% over the next two tothree years. Thus, better growth prospects and strong earning visibility make it one of the better picks in the mid-cap FMCG space. Wemaintain our Buy recommendation on the stock.

INDUSIND BANK 932 27.6 22.2 17.5 19.2 20.5 21.5 1,108 19

Remarks: IndusInd Bank is among the fastest growing banks (a 27% CAGR growth over FY10-15) having a loan book of Rs68,700 crore and 811branches across the country. About 25% of the bank’s book pertains to vehicle finance, which is a high-yielding category and isshowing signs of recovery.

Given the aggressive measures taken by the management, the deposit profile has improved considerably (a CASA ratio of 34%).Going ahead, the bank would follow a differentiated branch expansion strategy (a 5% branch market share in identified centers) thatwould help ensure healthy savings accounts and retail deposit growth.

Despite a weak economic growth and a higher proportion of vehicle finance book the bank has maintained its asset quality. With totalstressed loans (restructured loans + gross NPAs) forming just 1.4% of the book, the bank’s asset quality is among the best in the system.

A likely revival in the economy will further fuel growth in the consumer finance division and strong capital ratios will support the growthplans. The stock is trading at 3.3x its FY17E book value (not factoring in the QIP issue). Given the strong loan growth, high RoAs andhealthy asset quality, the stock should continue to trade at premium valuation. We have a positive outlook on the stock.

MARUTI SUZUKI 4,559 37.1 25.5 20.1 16.6 20.8 22.2 4,950 9

Remarks: Maruti Suzuki India Ltd (MSIL) is the market leader in the domestic passenger vehicle (PV) industry. In FY2015, as against an industrygrowth of a modest 3.9% MSIL has grown its volumes by 11.1% and in the process expanded its market share by 441BPS to 45%.

The company further strengthened its sales and service network, and added 309 outlets in FY15. Additionally, the drive undertaken byits management to tap the potential in rural areas paid rich dividends in difficult times for the industry and in the face of rising competitiveintensity; this reaffirms the resilience of MSIL’s positioning and business model.

MSIL’s new sedan, Ciaz, has received a positive response from the market and helped MSIL establish a presence in the segment.Also, with the new premium cross-over, ie S-Cross (to be retailed at exclusive Nexa outlets) the company is looking to move up theladder. Further, the recent launch of the new premium hatchback, ie Baleno, which has been priced aggressively as compared withpeers, is expected to help further gain market share. MSIL has a pipeline of new launches over the next few years, with the mostimportant being the entry into the compact utility vehicle and light commercial vehicle segments.

We expect customer sentiment to improve on the back of a strong government at the centre. Additionally the PV segment is expectedto benefit from the pent-up demand over the past two years; this will benefit MSIL the most due to its high market share in the entrylevel segment.

RELAXO FOOTWEAR 510 59.3 45.9 34.0 22.1 22.3 24.9 635 25

Remarks: Relaxo Footwear is present in the fast-growing footwear category, wherein it caters to customers with its four top-of-the-mind-recallbrands, viz, Hawaii, Sparx, Flite and Schoolmate. In the last quarter it also added another brand, Bahamas, to its product portfolio.

Relaxo has a proactive approach towards both brand building and creating capacities. To build its brand and create pull, like FMCGplayers it continues to rope Bollywood celebrities and this creates an aspirational quotient for its brands. On the one hand, thecompany is creating strong consumer centric aspiration for the consumers; on the other hand, it is keeping its eye on quality and thusdoes not believe in outsourcing. It is in the process of building capacity for future. Despite the current capacity (180 million pieces perannuam) that would take care of growth in the next three years, the company has bought a 15-acre land at Bhiwadi to built additionalcapacity to serve the future requirements.

Relaxo’s strong presence in the lucrative mid priced footwear segment (through its top-of-the-mind-recall brands like Hawaii, Flite andSparx) along with its integrated manufacturing set-up, lean working capital requirement and vigilant management puts it in a sweetspot to cash in on the strong growth opportunity unfolding in the footwear category due to a shift from unbranded to branded products.We thus maintain our Buy rating on the stock. We also roll over our multiple from FY2017 estimate to FY2018 estimate (valuing thestock at 33x FY2018E) with a price target of Rs635.

EQUITY FUNDAMENTALSSHAREKHAN TOP PICKS

Sharekhan ValueGuide December 20159

NAME CMP PER ROE (%) PRICE UPSIDE(RS) FY15 FY16E FY17E FY15 FY16E FY17E TARGET (RS) (%)

RELIANCE INDUSTRIES 969 12.1 12.4 10.4 10.8 9.7 10.5 1,100 14

Remarks: Reliance Industries Ltd (RIL) has a strong presence in the refining, petrochemical and upstream exploration businesses. The refiningdivision of the company is the highest contributor to its earnings and is operating efficiently with a better gross refining margin (GRM)compared with its peers in the domestic market due to the ability of its plant to refine more of heavier crude. The exploration businessremains weak due to low production in the Krishna-Godavari-D6 (KG-D6) field and weak pricing of global fuel prices. However, capitalemployed and profit contribution from the exploration business is low.

Moreover, the upcoming incremental capacities in the petrochemical and refinery businesses are going to drive the future earnings growthsubstantially as the downstream businesses are on the driving seat and contributing the lion’s share of the profitability and cash flow.

After a strong GRM in H1FY2016, we expect the GRM to remain healthy for the whole year. The stock is available at an attractivevaluation considering the size, strong balance sheet and cash flow generating ability of the company.

SBI 249 14.2 10.4 7.8 10.6 13.2 15.7 378 52

Remarks: SBI is India's largest bank in terms of most comparable parameters such as assets size, branch network (18,000 branches) andcustomer base. The bank has a market share of ~18% and along with its associate banks it commands a market share of over 25% inthe banking system. Therefore, with a revival in the investment cycle and pick-up in consumption the bank is likely to benefit significantlyin terms of loan growth and profitability.

SBI’s asset quality is relatively better compared with the other public sector banks (PSBs; its stressed loans stand at ~8.5% vs ~13.5%of the other PSBs) and has been showing improving trends in the past few quarters. While the pressure on the asset quality maycontinue in the near term, a higher tier-1 CAR (9.6%) and an improving operating performance remain comforting factors.

Going ahead, SBI will look to merge its associate banks which will give an unmatched hold in the domestic banking sector and boosteconomies of scale. In addition, the likely monetisation of the insurance and other subsidiaries will strengthen the capital position ofthe bank. The bank may also benefit from the government’s plans to infuse capital into the PSBs. SBI is a better pick among thegovernment-owned banks and is reasonably valued at the current levels.

TCS 2,371 87.5 70.8 57.5 33.7 32.7 29.7 3,000 27

Remarks: TCS pioneered the IT services outsourcing business from India and is the largest IT service firm in the country. It is a leader in mostservice offerings and has further consolidated its position as a full-service provider by delivering a robust financial and operationalperformance consistently over the years.

The consistency and predictability of its earnings performance has put the company at the top of its league. TCS’s managementremains positive on the digital technologies space, which grew by 10.7% QoQ, forms 13.3% of the revenues as compared with 12.5%in Q1FY2016. The management remains confident about the growth trajectory of the digital space for the coming years. Given theusual seasonal weakness in H2, it expects a soft revenue growth in the next two quarters. Further, it expects weakness in Diligenta(insurance) and Japan (integration issues related to the Mitsubishi acquisition) to continue for few more quarters.

We remain positive on TCS, given its strong positioning, scale advantage and head start in the digital technologies space (the highestamong the top Indian IT companies), which justify the valuation premium for TCS over the others.

ZEE ENTERTAINMENT 410 4.1 3.3 3.0 19.0 18.8 20.6 470 15

Remarks: Among the key stakeholders of the domestic TV industry, we expect the broadcasters to be the prime beneficiary of the mandatorydigitisation process initiated by the government. The broadcasters would benefit from higher subscription revenues at the least incrementalcapex as the subscriber declaration improves in the cable industry.

The management maintains that the advertisement spending will continue to grow in double digits going ahead and ZEEL will be ableto outperform the same. The growth in the advertisement spending will be driven by an improvement in the macro-economic factorsand the fact the ZEEL is well placed to capture the emerging opportunities being a leader in terms of market share.

ZEEL continues to outperform the broadcasting advertising market. We expect the momentum to continue with an improvement in themacro economy. The management indicated the strong momentum in the advertisement revenue growth would continue led by marketshare gains and improvement in spending from segments like FMCG, e-commerce, consumer durables and telecom companies.Subscription revenues are also expected to benefit from the run-up phases III and IV of the digitisation process (to be more visible inFY2017 and FY2018). We continue to see ZEEL as the prime beneficiary of the macro revival and digitisation.

EQUITY FUNDAMENTALS SHAREKHAN TOP PICKS

December 2015 Sharekhan ValueGuide10

WEALTH CREATOR PORTFOLIO EQUITY FUNDAMENTALS

Wealth Creator portfolioWEALTH CREATOR PORTFOLIO NOVEMBER 30, 2015

COMPARATIVE RETURNSParticulars Returns (as on on November 30, 2015)

Since inception (August 21, 2014)

Wealth Creator folio (weighted average returns) 9.0

- Large-cap (64%) 9.3

- Mid-cap (36%) 8.3

Sensex -0.8

Nifty 2.1

CNX Mid-cap 18.5

UPDATE ON WEALTH CREATOR PORTFOLIOSr No Scrip Weights Reco price (Rs) Price target (Rs) Potential upside 30-Oct-2015 March-18

Large-caps (64% weightage; 8% each))

1 Axis Bank 8% 469 1210 158.1%

2 Larsen & Toubro 8% 1374 3800 176.6%

3 Maruti Suzuki 8% 4577 8750 91.2%

4 Cummins 8% 990 1708 72.6%

5 State Bank of India 8% 250 580 131.6%

6 Sun Pharmaceutical 8% 731 1650 125.8%

7 Tata Consultancy Services 8% 2365 5100 115.6%

8 Tata Motors DVR 8% 297 675 127.0%

Mid-caps (36% weightage; 4% each)

9 PTC India Financials 4% 41 112 175.9%

10 V-Guard 4% 925 2100 127.1%

11 Gateway Distripark 4% 342 810 137.1%

12 IRB Infra 4% 255 650 155.2%

13 Network 18 Media 4% 52 135 161.9%

14 Gabriel India 4% 89 200 124.0%

15 Century Plyboard 4% 192 440 129.1%

16 Triveni Turbines 4% 109 265 142.2%

17 Dhanuka Agritech 4% 491 1150 134.4%

Objective: To build a balanced and actively managed portfolio ofquality companies that will help create meaningful wealth forinvestors in the multi-year rally expected in the Indian equity market.

In addition to some bottom-up picks, the portfolio contains stocksidentified based on three key themes:

Policy push: Stocks from sectors benefiting from improvementin the policy environment

Early gainers: Beneficiaries of an economic recovery (stocks fromauto, banking & financial services, logistic sectors)

Evergreen: Steady performers that provide stable and consistentreturns including urban consumption plays

Portfolio performance review Wealth Creator folio has appreciated by 9% (weighted average

returns) since its inception comprehensively beating the returnsfrom the benchmark indices.

No changes/revisions suggested in the folio in the Month ofNovember 2015. Price as on on November 30, 2015.

* Please note we see scope for upward revision in target price (3-year) of some of the stocks depending on the extent of economic recovery and will keep updating on the same

Sharekhan ValueGuide December 201511

STOCK UPDATE EQUITY FUNDAMENTALS

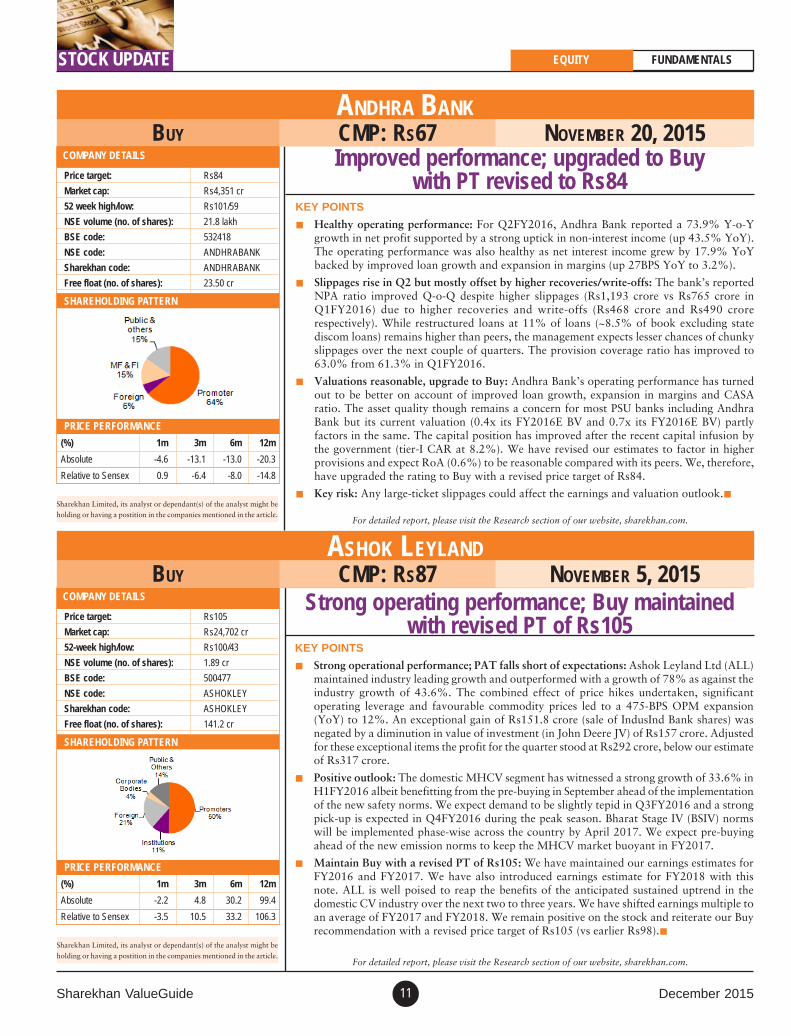

Improved performance; upgraded to Buywith PT revised to Rs84

COMPANY DETAILS

Price target: Rs84

Market cap: Rs4,351 cr

52 week high/low: Rs101/59

NSE volume (no. of shares): 21.8 lakh

BSE code: 532418

NSE code: ANDHRABANK

Sharekhan code: ANDHRABANK

Free float (no. of shares): 23.50 cr

(%) 1m 3m 6m 12m

Absolute -4.6 -13.1 -13.0 -20.3

Relative to Sensex 0.9 -6.4 -8.0 -14.8

PRICE PERFORMANCE

BUY CMP: RS67 NOVEMBER 20, 2015ANDHRA BANK

KEY POINTS

Healthy operating performance: For Q2FY2016, Andhra Bank reported a 73.9% Y-o-Ygrowth in net profit supported by a strong uptick in non-interest income (up 43.5% YoY).The operating performance was also healthy as net interest income grew by 17.9% YoYbacked by improved loan growth and expansion in margins (up 27BPS YoY to 3.2%).

Slippages rise in Q2 but mostly offset by higher recoveries/write-offs: The bank’s reportedNPA ratio improved Q-o-Q despite higher slippages (Rs1,193 crore vs Rs765 crore inQ1FY2016) due to higher recoveries and write-offs (Rs468 crore and Rs490 crorerespectively). While restructured loans at 11% of loans (~8.5% of book excluding statediscom loans) remains higher than peers, the management expects lesser chances of chunkyslippages over the next couple of quarters. The provision coverage ratio has improved to63.0% from 61.3% in Q1FY2016.

Valuations reasonable, upgrade to Buy: Andhra Bank’s operating performance has turnedout to be better on account of improved loan growth, expansion in margins and CASAratio. The asset quality though remains a concern for most PSU banks including AndhraBank but its current valuation (0.4x its FY2016E BV and 0.7x its FY2016E BV) partlyfactors in the same. The capital position has improved after the recent capital infusion bythe government (tier-I CAR at 8.2%). We have revised our estimates to factor in higherprovisions and expect RoA (0.6%) to be reasonable compared with its peers. We, therefore,have upgraded the rating to Buy with a revised price target of Rs84.

Key risk: Any large-ticket slippages could affect the earnings and valuation outlook.

SHAREHOLDING PATTERN

Sharekhan Limited, its analyst or dependant(s) of the analyst might beholding or having a postition in the companies mentioned in the article.

For detailed report, please visit the Research section of our website, sharekhan.com.

Strong operating performance; Buy maintainedwith revised PT of Rs105

COMPANY DETAILS

Price target: Rs105

Market cap: Rs24,702 cr

52-week high/low: Rs100/43

NSE volume (no. of shares): 1.89 cr

BSE code: 500477

NSE code: ASHOKLEY

Sharekhan code: ASHOKLEY

Free float (no. of shares): 141.2 cr

(%) 1m 3m 6m 12m

Absolute -2.2 4.8 30.2 99.4

Relative to Sensex -3.5 10.5 33.2 106.3

PRICE PERFORMANCE

BUY CMP: RS87 NOVEMBER 5, 2015ASHOK LEYLAND

KEY POINTS

Strong operational performance; PAT falls short of expectations: Ashok Leyland Ltd (ALL)maintained industry leading growth and outperformed with a growth of 78% as against theindustry growth of 43.6%. The combined effect of price hikes undertaken, significantoperating leverage and favourable commodity prices led to a 475-BPS OPM expansion(YoY) to 12%. An exceptional gain of Rs151.8 crore (sale of IndusInd Bank shares) wasnegated by a diminution in value of investment (in John Deere JV) of Rs157 crore. Adjustedfor these exceptional items the profit for the quarter stood at Rs292 crore, below our estimateof Rs317 crore.

Positive outlook: The domestic MHCV segment has witnessed a strong growth of 33.6% inH1FY2016 albeit benefitting from the pre-buying in September ahead of the implementationof the new safety norms. We expect demand to be slightly tepid in Q3FY2016 and a strongpick-up is expected in Q4FY2016 during the peak season. Bharat Stage IV (BSIV) normswill be implemented phase-wise across the country by April 2017. We expect pre-buyingahead of the new emission norms to keep the MHCV market buoyant in FY2017.

Maintain Buy with a revised PT of Rs105: We have maintained our earnings estimates forFY2016 and FY2017. We have also introduced earnings estimate for FY2018 with thisnote. ALL is well poised to reap the benefits of the anticipated sustained uptrend in thedomestic CV industry over the next two to three years. We have shifted earnings multiple toan average of FY2017 and FY2018. We remain positive on the stock and reiterate our Buyrecommendation with a revised price target of Rs105 (vs earlier Rs98).

SHAREHOLDING PATTERN

Sharekhan Limited, its analyst or dependant(s) of the analyst might beholding or having a postition in the companies mentioned in the article.

For detailed report, please visit the Research section of our website, sharekhan.com.

December 2015 Sharekhan ValueGuide12

Strong performance continued; Buy maintainedCOMPANY DETAILS

Price target: Rs3,650

Market cap: Rs36,536 cr

52-week high/low: Rs3,435/1,507

NSE volume (no. of shares): 2.1 lakh

BSE code: 500825

NSE code: BRITANNIA

Sharekhan code: BRITANNIA

Free float (no. of shares): 5.91 cr

(%) 1m 3m 6m 12m

Absolute -3.8 0.3 40.0 102.7

Relative to Sensex -1.5 7.1 40.8 112.4

PRICE PERFORMANCE

BUY CMP: RS3,045 NOVEMBER 9, 2015BRITANNIA INDUSTRIES

KEY POINTS

Britannia’s consolidated total revenue grew by 12% to Rs2,208.7 crore driven by a double-digit volume growth. Adjusting for the excise duty issue, the total revenue growth stood at13% on a Y-o-Y basis, which, we believe, is better in a difficult environment.

The gross profit margin improved by 297BPS YoY to 42.6% driven by a benign input cost.On the other hand, the operating profit margin improved by 357BPS to 14.7% on the backof better operating efficiencies. Hence, the operating profit grew by 47.6% YoY to Rs325.0crore and the adjusted PAT grew by 53.7% YoY to Rs218.6 crore in Q2FY2016.

Britannia has made reasonable in-roads into some of the low-presence states in the northernIndia and has strengthened its position in such regions. Also, the company has offered morevalue to consumers along with re-stage of its key brands, “Good Day” and “Milk Bikis”,which should help it maintain the strong growth momentum. The company started thecommercialisation of new factory at Tamil Nadu during the quarter. The initiatives in regardsto enhancing supply chain efficiencies, reducing wastage and accelerating cost efficiencyprogrammes will continue to aid in achieving good profitability in near future.

We have broadly maintained our earnings estimates for FY2016, FY2017 and FY2018.Britannia is well poised to achieve a double-digit revenue and earnings growth of 15% and33% respectively over FY2015-18. In view of better earnings visibility over the long run, wehave maintained our Buy recommendation on the stock with an unchanged price target ofRs3,650.

SHAREHOLDING PATTERN

Sharekhan Limited, its analyst or dependant(s) of the analyst might beholding or having a postition in the companies mentioned in the article.

For detailed report, please visit the Research section of our website, sharekhan.com.

STOCK UPDATEEQUITY FUNDAMENTALS

Decent result in challenging times;PT revised to Rs240

COMPANY DETAILS

Price target: Rs240

Market cap: Rs3,892 cr

52 week high/low: Rs262/135

NSE volume (no. of shares): 6.7 lakh

BSE code: 532548

NSE code: CENTURYPLY

Sharekhan code: CENTURYPLY

Free float (no. of shares): 5.9 cr

(%) 1m 3m 6m 12m

Absolute 8.6 -17.4 -14.1 19.0

Relative to Sensex 10.4 -11.6 -11.4 24.5

PRICE PERFORMANCE

BUY CMP: RS175 NOVEMBER 6, 2015CENTURY PLYBOARDS (INDIA)

KEY POINTS

Q2FY2016 result synopsis: Century Plyboards (Century)’s top line grew at 8.6% on a Y-o-Y basis, led by a 12.3% growth in the laminate business and a 6.8% Y-o-Y growth in theplyboard and allied business. Across the board, the home improvement business was muted.Aided by soft raw material prices and lower logistic cost, the gross profit margin improvedby 377BPS YoY, which resulted in a 102-BPS margin expansion at the operating level. As aresult, the operating profit grew by 15.7%. Due to a decent operating performance coupledwith lower depreciation and tax rate, the earnings grew by 29.4% on a Y-o-Y basis.

Management comments: The management continued to acknowledge the soft demandenvironment prevalent in the home improvement segment that continues to post challengesfor volume growth in the plyboard business.

Incorporated Q2, estimates reduced; maintain Buy with a revised price target of Rs240:Incorporating the H1FY2016 results and the reduced guidance by the management on thetop line growth, we have marginally tweaked our estimates. Our revised EPS estimates forFY2016 and FY2017 are Rs8.1 and Rs10.1 respectively. Despite revising earningsestimatesdownwards, we believe that Century is well positioned to ride the economic revival-driven recovery in demand and increase its market dominance in the plywood and laminatesegments. The implementation of GST would provide a fillip to the revenue and earningsperformance. In view of these positives, we maintain our Buy rating on the stock with arevised price target of Rs240 (valued at 24x its FY2017E EPS of Rs10.1).

SHAREHOLDING PATTERN

Sharekhan Limited, its analyst or dependant(s) of the analyst might beholding or having a postition in the companies mentioned in the article.

For detailed report, please visit the Research section of our website, sharekhan.com.

Sharekhan ValueGuide December 201513

STOCK UPDATE EQUITY FUNDAMENTALS

Q2 earnings much ahead of estimates; retain BuyCOMPANY DETAILS

Price target: Rs730

Market cap: Rs7,420 cr

52 week high/low: Rs765/452

NSE volume (no. of shares): 3.8 lakh

BSE code: 500084

NSE code: CESC

Sharekhan code: CESC

Free float (no. of shares): 6.7 cr

(%) 1m 3m 6m 12m

Absolute -9.0 -10.4 -1.6 -21.9

Relative to Sensex -4.9 -3.7 3.5 -17.0

PRICE PERFORMANCE

BUY CMP: RS558 NOVEMBER 13, 2015CESC

KEY POINTS

Earnings ahead of estimate: For Q2FY2016, CESC reported substantially better earningsthan estimated. The revenue was in line with our estimate but the operating profit as well asnet earnings were better than our estimates. The operating profit registered a 5% growthbut on account of a higher interest cost, the PAT was flat (up 2% YoY) at Rs195 crore.

A mixed bag--result of power assets under subsidiaries and slow recovery of Spencer’s: The600-MW power plant in Haldia is fully operational and supplying to Kolkata distribution.The Chandrapur-based 600MW power plant is not operational (lack of fuel and powerpurchase arrangement [PPA]), but the management plans to start the plant to supply 110MWto Tamil Nadu SEB, which would be helpful to cover some part of the losses currently it isincurring. FSL reported a strong quarter while on the retail business front, same-store salesgrowth momentum remained positive in Q2FY2016 though the recovery is slower thanexpected.

View and valuation–reiterate Buy with unchanged PT of Rs730: We believe the negativesrelated to the loss in the Chandrapur plant and potential under recovery as a result ofaggressive bidding for coal mines have been already priced in the stock. Nevertheless, thecompany continues to put efforts to cover the under recovery from exporting some power inexchange and get PPA linkage for the new plant. The drag related to retail subsidiaries isreceding though slower than expected. Overall, the financials of FSL should improve. Wehave retained our positive stance on CESC with a Buy rating and an unchanged price targetof Rs730.

SHAREHOLDING PATTERN

Sharekhan Limited, its analyst or dependant(s) of the analyst might beholding or having a postition in the companies mentioned in the article.

For detailed report, please visit the Research section of our website, sharekhan.com.

Multiple red flags emerge; exitCOMPANY DETAILS

Market cap: Rs2,224 cr

52 week high/low: Rs644/238

NSE volume (no. of shares): 3.5 lakh

BSE code: 533261

NSE code: EROSMEDIA

Sharekhan code: EROSMEDIA

Free float (no. of shares): 2.46 cr

(%) 1m 3m 6m 12m

Absolute -44.9 -51.9 -35.1 -7.0

Relative to Sensex -42.4 -48.4 -31.8 -1.1

PRICE PERFORMANCE

BOOK PROFIT CMP: RS238 NOVEMBER 13, 2015EROS INTERNATIONAL MEDIA

KEY POINTS

Probable class action suits against Eros Plc, concerning possible violations of Federal securitieslaws: Wolf Haldenstein Adler Freeman and Herz LLP announced that it has commenced aninvestigation on Eros International Plc (Eros Plc), pertaining to possible violation of Federalsecurities laws by the company and its officers/directors and has asked exiting investors inEros Plc to come forward to file a class action suit against the company.

Multiple red flags raised by international media and analysts, dented investors’ confidencein Eros: On October 30 2015, a report was published on Eros Plc asserting, among otherthings, that: (1) Eros Plc’s reported earnings are significantly overstating the economic realityof its business model; (2) the financials of Eros Plc’s subsidiary revealed a lack of free cashflow and raised many questions about the company’s accounting; and (3) Eros Plc hasenriched its controlling family at the expense of shareholders through a series of related-party transactions.

Stock to remain under pressure, till the overhang clears, advise to exit: Owing to the recentnegative news flow in the international media which have raised red flags on the company’sparent (Eros Plc)’s accounting policy and the overall corporate governance, Eros InternationalMedia Ltd (EIML) has corrected sharply. Given the concern of free cash flow generationand corporate disclosure, we had also earlier downgraded our rating on EIML from Buy toHold from Q1FY2015. Given the aggravation of corporate governance issue in internationalmedia and probable class action suits against its parent, it is very unlikely for the stock ofEMIL to recover lost ground soon or till the time the issues are clear. We advise to exit fromthe stock at the current level.

SHAREHOLDING PATTERN

Sharekhan Limited, its analyst or dependant(s) of the analyst might beholding or having a postition in the companies mentioned in the article.

For detailed report, please visit the Research section of our website, sharekhan.com.

December 2015 Sharekhan ValueGuide14

Maintain Buy with a revised price target of Rs105COMPANY DETAILS

Price target: Rs105

Market cap: Rs1,237 cr

52 week high/low: Rs107/72

NSE volume (no. of shares): 8.5 lakh

BSE code: 505714

NSE code: GABRIEL

Sharekhan code: GABRIEL

Free float (no. of shares): 65.16 cr

(%) 1m 3m 6m 12m

Absolute 3.9 -2.5 7.7 5.4

Relative to Sensex 2.3 3.1 8.1 8.9

PRICE PERFORMANCE

BUY CMP: RS86 NOVEMBER 4, 2015GABRIEL INDIA

KEY POINTS

Revenue decline continues in Q2FY2016: Gabriel India (Gabriel) had another disappointingquarter as its revenue declined by 2.4% YoY to Rs375 crore, in line with our expectation.However, the company benefitted from the softer commodity prices and favourable productmix which led to a 73-BPS Y-o-Y operating profit margin (OPM) expansion to 8.8% vis-à-vis our estimate of 8.5%. Gabriel posted a net profit of Rs19.4 crore (higher by 10.6%YoY) as against our expectation of Rs18.1 crore.

Revenue growth revival expected in FY2017: The two-wheeler industry (60% of the overallsales) is going through difficult times. Although the scooter segment has been growing, themotorcycle demand remains muted due to the slowdown in rural India and thus is affectingrevenues for Gabriel. The company’s revenues in the PV segment are expected to pick upwith the start of production on two models with Maruti Suzuki India Ltd (MSIL) and aplatform with Mahindra & Mahindra (M&M). We expect revenue growth in FY2016 to bemuted in low single digits and the company to return to double-digit growth in FY2017 asthe motorcycle segment recovers and production for new models with key customerscommences.

Maintain Buy with a revised price target of Rs105: We have cut our earnings estimates forFY2016 and FY2017 by about 10% each to factor in a lower revenue growth. While thedemand scenario is expected to remain muted in FY2016, we expect a robust growth inFY2017 on the back of a ramp-up in supplies to Honda Motorcycle and Scooter’s new plantin Gujarat and to the new models of both MSIL and M&M. We have shifted the targetmultiple to an average of FY2017 and FY2018 and reiterated our Buy rating on the stockwith a revised price target of Rs105 (earlier Rs100).

SHAREHOLDING PATTERN

Sharekhan Limited, its analyst or dependant(s) of the analyst might be

For detailed report, please visit the Research section of our website, sharekhan.com.

STOCK UPDATE EQUITY FUNDAMENTALS

Volume growth to pick up gradually; Buymaintained with revised PT of Rs6,750

COMPANY DETAILS

Price target: Rs6,750

Market cap: Rs24,384 cr

52 week high/low: Rs6,564/5,425

NSE volume (no. of shares): 10,419

BSE code: 500676

NSE code: GSKCONS

Sharekhan code: GSKCONS

Free float (no. of shares): 1.2 cr

(%) 1m 3m 6m 12m

Absolute -1.1 -5.1 -4.9 5.7

Relative to Sensex 3.5 1.8 0.0 13.6

PRICE PERFORMANCE

BUY CMP: RS5,816 NOVEMBER 16, 2015GLAXOSMITHKLINE CONSUMER HEALTHCARE

KEY POINTS

In Q2FY2016, GSK Consumer’s revenue stood flat at Rs1,074.7 crore with a volume declineof 1.5%. Adjusting for the impact of the excise benefit of 520BPS, the like-to-like revenuegrowth for the quarter stood at 5%. As anticipated, the lower raw material prices led to a371-BPS improvement in the gross profit margin to 65.3% and the operating profit marginimproved by 278BPS YoY to 22.1%. This coupled with a 31% increase in business auxiliaryincome led to a 25% growth in the adjusted PAT.

The company has maintained its distribution enhancement and new product/variants as itskey growth drivers going ahead. It has further enhanced its distribution reach by 77,000outlets to reach 3.2 million outlets in H1FY2016 (target is to reach close to 4.0 millionoutlets by the end of FY2016). Also, the company has maintained its thrust on adequatebrand building and promotional activities. It is banking on the new variants launched underthe “Horlicks” brand to improve the sales volume in long run.

We have revised downwards our earnings estimates for FY2016 and FY2017 by 5% and3% respectively to factor in a slow pick-up in the demand for HFD sales. GSK Consumercontinued to gain market share in the domestic HFD segment, which indicates a slowdownin the category. We expect the volume growth in the HFD segment to gradually improvewith substantial improvement in the urban demand environment. The company continuesto have strong cash flows and expect better dividend payout to continue in the comingquarters. Hence, we have maintained our Buy recommendation on the stock with a revisedprice target of Rs6,750.

SHAREHOLDING PATTERN

Sharekhan Limited, its analyst or dependant(s) of the analyst might beholding or having a postition in the companies mentioned in the article.

For detailed report, please visit the Research section of our website, sharekhan.com.

Sharekhan ValueGuide December 201515

STOCK UPDATEEQUITY FUNDAMENTALS

In-line operating performance; maintain Buy withrevised PT of Rs1,000

COMPANY DETAILS

Price target: Rs1,000

Market cap: Rs8,540 cr

52 week high/low: Rs1,014/700

NSE volume (no. of shares): 1.0 lakh

BSE code: 532777

NSE code: NAUKRI

Sharekhan code: NAUKRI

Free float (no. of shares): 6.8 cr

(%) 1m 3m 6m 12m

Absolute -7.9 -15.1 -5.0 -16.0

Relative to Sensex -6.3 -9.1 -2.0 -12.2

PRICE PERFORMANCE

BUY CMP: RS708 NOVEMBER 6, 2015INFO EDGE (INDIA)

KEY POINTS

In-line operating performance: For Q2FY2016, Info Edge has delivered an in-line operatingperformance, with a revenue growth of 18% YoY to Rs174.1 crore. The performance wasled by a 19.6% Y-o-Y growth in recruitment solutions (Naukri) to Rs128.2 crore while therevenue from 99acres was up by 13.5% YoY to Rs27.8 crore. The net income for thequarter was up by 2% YoY and 18% QoQ to Rs33.9 crore.

Key management commentary: (1) Naukri’s growth momentum to continue led by IT marketin Bengaluru, up by 20-25% YoY, while revival in non-IT segment will drive the incrementalgrowth with a 15-20% Y-o-Y growth. Expect growth to sustain at 18-20% and margins toimprove further; (2) 99acres (real estate market) is witnessing a slowdown in the Delhi NCRregion (the largest market for the company) and other markets like Mumbai; overall transactionsvolume has fallen across the markets with inventory piled up to an all-time high

Maintain Buy with a revised price target of Rs1,000: Given the slowness in demand in thereal estate market, we have lowered our estimates and target multiple for 99acres and alsolowered our overall SOTP-based valuation for Info Edge to Rs1,000 (from Rs1,103 earlier).Nevertheless, we continue to see Info Edge as a strong play on India’s internet and mobilepenetration theme. Info Edge, with a strong online presence through various ventures,recruitment (Naukri), real estate (99acres), restaurant listing (Zomato) and coupons industry(mydala.com), is a preferred play on both e-commerce/online shift and macro recovery. Wehave maintained our Buy rating on the stock with a revised price target of Rs1,000.

SHAREHOLDING PATTERN

Sharekhan Limited, its analyst or dependant(s) of the analyst might beFor detailed report, please visit the Research section of our website, sharekhan.com.

Outlook remains uncertain due to currencyheadwinds; Book profit

COMPANY DETAILS

Market cap: Rs2,397 cr

52 week high/low: Rs318/180

NSE volume(no. of shares): 1.9 lakh

BSE code: 506943

NSE code: JBCHEPHARM

Sharekhan code: JBCHEPHARM

Free float (no. of shares): 3.8 cr

(%) 1m 3m 6m 12m

Absolute -7.9 13.2 20.6 42.9

Relative to Sensex -1.9 12.7 29.3 55.7

PRICE PERFORMANCE

BOOK PROFIT CMP: RS282 NOVEMBER 26, 2015JB CHEMICALS & PHARMACEUTICALS

KEY POINTS

Sluggish performance continued in Q2: In Q2FY2016, JB Chemicals and PharmaceuticalsLtd (JBCPL) reported a subdued performance with a revenue growth of just 2%, whileoperating profit margin declined by 350BPS to 17%. This quarter was the fourth consecutivequarter of dismal operating performance by the company.

Volatility in currency affects exports in key emerging markets: JBCPL reported a moderate3% growth in exports of formulation to Rs133 crore during Q2FY2016. The exports to theRest of the World (RoW) markets (10% decline during the quarter) were affected due tolower demand and depreciation of market currencies against dollar.

Outlook remains bleak; Book profit: The volatility in currencies in key emerging markets islikely to have an effect on H2FY2016 performance too. Also, for FY2017, demand willcontinue to be weak as dollar is likely to strengthen further. Hence, the operating profitmargin and profitability are likely to remain under pressure over the next few quarters.Hence, in view of bleak future, we advise our investors to Book profit from the stock.

SHAREHOLDING PATTERN

Sharekhan Limited, its analyst or dependant(s) of the analyst might beholding or having a postition in the companies mentioned in the article.

For detailed report, please visit the Research section of our website, sharekhan.com.

December 2015 Sharekhan ValueGuide16

STOCK UPDATEEQUITY FUNDAMENTALS

Maintain Buy with revised PT of Rs360COMPANY DETAILS

Price target: Rs360

Market cap: Rs272 cr

52-week high/low: Rs425/153

NSE volume (No of shares): 0.15 lakh

BSE code: 532054

Sharekhan code: KAMLADLS

Free float (No of shares): 0.5 cr

(%) 1m 3m 6m 12m

Absolute -7.4 -17.2 -22.1 70.8

Relative to Sensex -5.8 -11.4 -19.7 78.8

PRICE PERFORMANCE

BUY CMP: RS270 NOVEMBER 6, 2015KDDL

KEY POINTS

Consolidated performance snapshot: For Q2FY2016, KDDL’s consolidated top line grewby 12.6% on a Y-o-Y basis, aided by a robust 25.4% Y-o-Y growth in Ethos, while themanufacturing business posted a 7% decline in the revenue.

Ethos performance good: For Ethos, festive and marriage season drives demand for itsproduct, thus in the light of Diwali falling in Q3 this year as against Q2 in the last year, arevenue growth of 25.4% YoY is robust. Further, the other key indicators like increasingsales from the online segment (for Q2FY2016, 28% sales came from online) and growth intraffic (for H1FY2016 36% Y-o-Y growth in the traffic was witnessed) are in line with thestrategy of attaining growth through omni-channel presence.

Maintain Buy; revised price target to Rs360: Incorporating weak Q2 manufacturing resultsinto our model, we have marginally revised our earnings estimates downwards for themanufacturing business. Thus, our consolidated EPS estimates for FY2016 and FY2017 areRs11.5 and Rs14.1 respectively. Further, the growth momentum and the margin expansiontrend in the Ethos business are panning in line with our expectation. Thus, we continue tolike Ethos' unique high-end watch retailing business, which is expected to grow manifold bycashing in on the growth in the luxury watch segment and the increasing trend towardsonline e-tailing. Hence, we have maintained our Buy rating on the stock with a revised pricetarget of Rs360 (valued at 6x its FY2017E earnings for the stand-alone business + 1.2x itsFY2017E sales of Ethos).

SHAREHOLDING PATTERN

Sharekhan Limited, its analyst or dependant(s) of the analyst might beholding or having a postition in the companies mentioned in the article.

For detailed report, please visit the Research section of our website, sharekhan.com.

Maintain Buy with an unchanged PT of Rs1,450COMPANY DETAILS

Price target: Rs1,450

Market cap: Rs77,239 cr

52 week high/low: Rs1,441/1,095

NSE volume (no. of shares): 11.1 lakh

BSE code: 500520

NSE code: M&M

Sharekhan code: M&M

Free float (no. of shares): 45.7 cr

(%) 1m 3m 6m 12m

Absolute -0.9 -9.2 7.8 1.2

Relative to Sensex 0.8 -2.8 11.2 5.9

PRICE PERFORMANCE

BUY CMP: RS1,258 NOVEMBER 6, 2015MAHINDRA & MAHINDRA

KEY POINTS

OPM at 13.2% below estimate; PAT beats estimates on higher revenues and lower tax rate:Mahindra & Mahindra (M&M)’s poor run in terms of volumes continued in Q2FY2016with auto and tractor divisions reporting a 2.2% and 26% fall respectively. The net sales forthe quarter at Rs8,794 crore (down 2.8% YoY) beat estimates due to a sharp jump inrevenues from the genset business. The OPM contracted by 110BPS sequentially to 13.2%(vs expectation of 13.5%) due to the lower operating leverage. A higher revenue and alower tax rate enabled M&M to post a net profit of Rs978 crore, slightly higher than ourestimate of Rs951 crore.

Weak monsoon casts a shadow on tractor segment recovery; new launches to boost autovolumes: The sub-par monsoon rainfall during the season has hampered the recovery in thetractor segment. The management has cut its guidance for FY2016 tractor industry from agrowth of 4-5% earlier to a decline of 5%. The outlook for the auto division is positive. Thecompany has received a positive response for the recently launched TUV3OO and themanagement expects the model to stabilise at monthly volumes of 5,000 units. The companywill be following with the launch of another model (code name S101) in January whichwould further boost volumes.

Maintain Buy with an unchanged PT of Rs1,450: Given the current weakness in the tractorsegment and a delay in the recovery, we have cut our earnings estimate for FY2016 by 3%.We remain positive on the stock, given its leadership position in the domestic tractor andUV segments as well as the value derived from its subsidiaries across business segments. Wemaintain our Buy recommendation on the stock with an SOTP-based price target, unchangedat Rs1,450.

SHAREHOLDING PATTERN

Sharekhan Limited, its analyst or dependant(s) of the analyst might be

For detailed report, please visit the Research section of our website, sharekhan.com.

Sharekhan ValueGuide December 201517

STOCK UPDATEEQUITY FUNDAMENTALS

Maintain Buy with a price target of Rs950COMPANY DETAILS

Price target: Rs950

Market cap: Rs182,134 cr

52-week high/low: Rs1,200/748

NSE volume (no. of shares): 36.8 lakh

BSE code: 524715

NSE code: SUNPHARMA

Sharekhan code: SUNPHARMA

Free float (no. of shares): 109 cr

(%) 1m 3m 6m 12m

Absolute -11.4 -4.6 -14.0 -7.5

Relative to Sensex -9.3 2.5 -13.5 -3.1

PRICE PERFORMANCE

BUY CMP: RS757 NOVEMBER 9, 2015SUN PHARMACEUTICAL INDUSTRIES

KEY POINTS

High tax rate dents earnings: Revenue for the quarter declined by 15% to Rs6, 838 crore onaccount of decline in sales in the US and RoW markets, and supply constraints at its Halolplant. Also, revenue in Q2FY2015 included sales from Valsartan, in its 180-day exclusivity.The operating profit margin declined by 986BPS to 28.3% in Q2FY2016.

Synergy with Ranbaxy and Halol plant, the key developments to watch ahead: Themanagement is confident about the synergy with Ranbaxy through improving productivityof the overall Ranbaxy business and getting synergy benefits on certain products fromFY2018. As part of strategy, the company will focus on high-margin products which arestrategically fit and will continue to remain focused on the OTC business. The launch ofGlivec in Q4FY2016 will remain a key trigger for the company.

Near-term outlook remains cautious: Earlier, the company had issued caution statementregarding sales and profits for FY2016 due to the integration of Ranbaxy and supplyconstraints from Halol. Remediation efforts at Halol are on track but will take some time.After the settlement of Glivec with Novartis, Sun Pharma has delisted the drug from Haloland filed from an alternate site. We believe Sun Pharma will take two to three quarters moreto complete its restructuring and remediation efforts at Halol.

Maintain Buy with price target of Rs950: Remediation efforts at Halol are on track but willtake some time. Complete benefits of the remediation processes will be visible in FY2018.The filing of Glivec from an alternate site is a silver lining to the cloud. We have maintainedour Buy rating on the stock with a price target of Rs950.

SHAREHOLDING PATTERN

Sharekhan Limited, its analyst or dependant(s) of the analyst might beholding or having a postition in the companies mentioned in the article.

For detailed report, please visit the Research section of our website, sharekhan.com.

Strong Q2 but joint venture order intake weak;PT revised to Rs135

COMPANY DETAILS

Price target: Rs135

Market cap: Rs3,629 cr

52 week high/low: Rs152/90

NSE volume (no. of shares): 62,205

BSE code: 533655

NSE code: TRITURBINE

Sharekhan code: TRITURBINE

Free float (no. of shares): 9.9 cr

(%) 1m 3m 6m 12m

Absolute -3.3 -6.6 -5.0 -3.8

Relative to Sensex 1.7 0.4 -0.7 3.3

PRICE PERFORMANCE

BUY CMP: RS110 NOVEMBER 18, 2015TRIVENI TURBINES

KEY POINTS

Pick-up in order execution drives Q2 growth: For Q2FY2016, Triveni Turbines Ltd (TTL)reported a 14% Y-o-Y growth in revenue led by a strong 21% growth in product sales. Theaftermarket segment has reported a marginal fall in revenue mainly due to unfavourablebase effect. Lower raw material cost led to a 110-BPS improvement in operating profitmargin to 23.5%, the highest in the past ten quarters. Overall, the net profit rose by 16% toRs27.7 crore.

Order booking robust in stand-alone business, sluggish intake in GE joint venture: InQ2FY2016, it reported an order intake of Rs200 crore (up 40% YoY) taking the stand-alone order book to Rs680 crore (up 13% YoY and 10% QoQ). The consolidated orderbook stood almost flattish at Rs790 crore as its joint venture (JV) with GE did not have anyorder finalisation during H1FY2016. Since the major overseas orders would be executed byFY2016 itself, the JV would need to pick up its order booking pace to achieve the requiredgrowth rate in FY2017.

Estimates downgraded, price target revised to Rs135: We have downgraded our earningsestimates for FY2016 and FY2017 by 7% and 11% respectively mainly in view of sloworder booking in its JV with GE. We have also introduced our FY2018 estimates in thisnote. We expect net profit to double (CAGR of 26%) in three years, FY2015-18. We likethe stock for its strong competitive positioning, international marketing efforts, marginprofile and healthy balance sheet (it is a debt-free company with superior return ratios). Anymajor order win in the GE JV in the near term would be a positive trigger for the stock. Wehave maintained our Buy rating on the stock with a revised price target of Rs135.

SHAREHOLDING PATTERN

Sharekhan Limited, its analyst or dependant(s) of the analyst might be

For detailed report, please visit the Research section of our website, sharekhan.com.

December 2015 Sharekhan ValueGuide18

Goods and Services Tax BillSHAREKHAN SPECIAL NOVEMBER 27, 2015

Key points

GST–simplified indirect tax regime: The Goods and ServicesTax (GST) Bill aims to simplify the current indirect tax regimeby bringing all central and state levies (like excise duty, salestax, octroi, VAT and other countervailing duties) under onesingle head having uniform tax rate across goods and services(with some exclusions like electricity, alcohol and petroleumproducts).