value's x-ray market research for technology vision co

TRANSCRIPT

1

2

INDEX i) Introduction…………………………………………………………. 4

ii) Abbreviation Letters……………………………………………. 4

1. General Market Analysis

1.1. Economical Market Growth……………………………5

1.2 Industrial Market Growth ..…………………………….7

1.3. X.RAY apparatus Market Growth…………………..9

2.Customer Analysis

i) Market Share of XRF……..…………………………………………10

ii) Export Volume 2013 for all Sectors…………………………11

2.1Construction and Building industries

2.1.1 Cement………………………………………………14

2.1.2 Gypsum……………………………………………..16

2.1.3 Iron & Steel………………………………………..17

2.1.4 Ceramic & Sanitary Ware…………………..18

2.1.5 Glass…………………………………………………..20

3

2.2 Oil & Petrol industries

2.2.1 Petrol & Petrochemicals……………………21

2.2.2 Fertilizers…………………………………….......22

2.3 Metal Industries

2.3.1 Machining of Metals………………………...23

2.3.2 Metals……………………………………………….24

2.3.3 Cables………………………………………….......25

2.3.4 Intermediate Goods………………………....26

2.3.5 Equipments and Transportation……….27

2.3.6 Ships & Boats…………………………………...28

2.4 Research & Development…………………………….29

3.Competitor Analysis

3.1 No. Of Apparatus for each competitor……….30

3.2 Market Volume For Competitors' Origin…….31

4

i) Introduction :

In this XRF market study we aimed our focus on the following marketing and economical areas:- 1- Egyptian general economic atmosphere and equations. 2- The reality of the industrial sector growth in Egypt. 3- Overview of XRF market volume in Egypt in the last ten years. 4- Present and analyze the market share of every targeted sector using XRF. 5- Develop a relative estimation for the different sectors using XRF. 6- Analyze the sectors that use XRF and have the most export potential in the next few years. 7-.Aiming to Offer a thorough study of the market, customer and competitors. Tools and methodology of this study. 1. Quantitative methodology. 1.1 Gathering, processing, combining and analyzing the official quantitative data for the market, different sectors and competitors. 1.2 Collecting only authenticated data. 2. Qualitative methodology. 2.1 Using statistical data to reach the right conclusion. Support the reader of this market research with non exaggerated forecasting. We depend on organizing the quantitative data to help the reader reach conclusion, nothing is more real than numbers.

ii) Abbreviation Letters Here is some of letters that will be shown in this report and what they stand for :

Letters Stands For

M$ Million Dollars

EGP Egyptian Pounds

U.D Undefined

Q Yearly Quarter

SCAF Military Council of Egypt

GDP Gross domestic product

5

1.General Market Analysis

As the Egyptian Market is going through many ups and downs,

in this part of the Study we are showing and discussing the whole

Egyptian economic growth conditions, and mainly the industrial

sector's growth.

1.1. Economical Market Growth

As all economic experts know since Q1 2011 - the Egyptian revolution

- the Egyptian market has suffered a large and fast decreasing rates

due to many factors that will be repeated after every dramatic

political event. Some of these factors are:-

1. The suspensions of many governmental tenders and contracts.

2. Security problems and political conflicts.

3. Vague and unclear political atmosphere leading to downsizing

of foreign capitals.

4. Social bad mode covers all the economical chain from (business

people to consumers).

2010-2011 2011-2012 2012-2013

-6

-4

-2

0

2

4

6

8

Q3 2010

Q4 2010

Q1 2011

Q2 2011

Q3 2011

Q4 2011

Q1 2012

Q2 2012

Q3 2012

Q4 2012

Q1 2013

Q2 2013

Q3 2013

6.75.6

-4.2

0.4 0.7 0.4

5.2

3.32.6 2.2 2.2

1.51

M$

Economical Growth in Egypt ( Per ) Quarter ( Q=3 Months )

6

Overview :

What clearly appears is that any dramatic event affects the

economic growth in three stages, these stages are:-:

o Firstly, we have the critical dramatic point: uncertainty about

the (upcoming or current) regime results in enormous

decreasing in economical growth rate.

Example 1: Quarter 1 2011 “the falling of Mubarak’s Regime

and its substitution with SCAF regime".

Example 2: Quarter 2 2012 the beginning of the unclear view

of the political future of Egypt

o Secondly, a decaying period: about 2 to 3 Quarters the

economy suffers the chaotic behaviors and closing of many

business activities.

Example : Q2 and Q3 2012

o Finally , The economical Adaptation Period

Example : Q4 2012 a stable phase

Key Indications :

o The Egyptian economic in this political instability period in

every political critical point goes through three stages :

1. Critical dramatic point

2. Decaying period

3. Economical adaptation

7

1.General Market Analysis

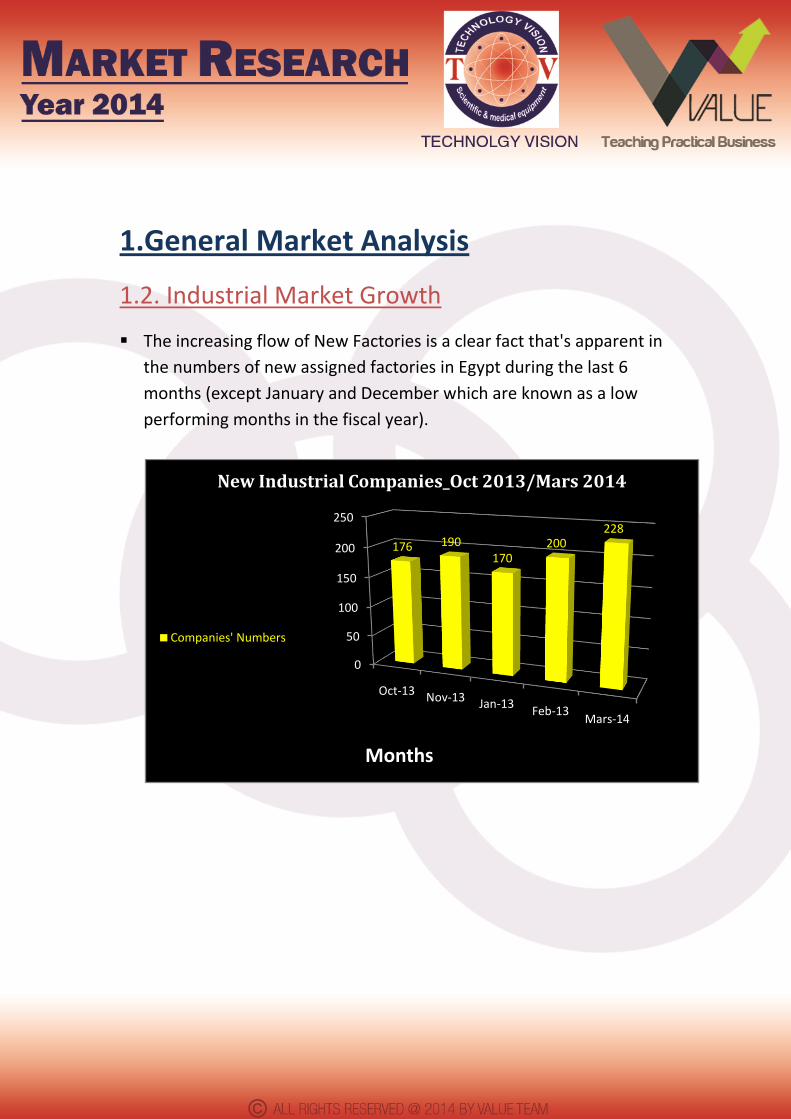

1.2. Industrial Market Growth

The increasing flow of New Factories is a clear fact that's apparent in

the numbers of new assigned factories in Egypt during the last 6

months (except January and December which are known as a low

performing months in the fiscal year).

0

50

100

150

200

250

Oct-13 Nov-13 Jan-13Feb-13

Mars-14

176 190170

200228

Months

New Industrial Companies_Oct 2013/Mars 2014

Companies' Numbers

8

Also The Capital flow increases from (275 M EGP) in Oct 2013 to (364

M EGP) in Mar 2014 including the low performing months (Dec and

Jan).

This uniform Market stretching despite of the political instability

results from two main reasons :

1. The gap caused by the closure of many industrial business that

couldn’t face the (decaying phase we have just mentioned) is

being filled.

2. The starting of new adaptation period.

050

100150200250300350400450

275.2

395.1

201.6

419.9

364.2

Months

New Capital_Oct 2013/Mars 2014

Share Capital ( Million EGP )

9

1.General Market Analysis

1.3. X.RAY apparatus Market Growth

Please note that XRF is 35 % – 40 % of the total X-Ray market

0

10000000

20000000

30000000

40000000

50000000

60000000

70000000

80000000

90000000

2005 2006 2007 2008 2009 2010 2011 2012 2013

30,127,959

39,654,218

29,161,082

82,030,061

63,382,698

48,187,498

86,191,542

55,290,763

51,616,392

EGP

10

2.Customer Analysis

i) Market Share of XRF Customers 2013 calculated

through ( Production + Earnings )

Sector Market Share % Cement 4.75% Iron & Steel 8.23%

Petrol & Petrochemicals 67.36%

Glass 0.43% Machining of Metals 0.14%

Cables 0.44% Tools , Equipments and Transportation 2.33%

Ships & Boats 0.12% Metals 10.50%

Fertilizers 3.70%

Gypsum 0.10% Ceramic & Sanitary Ware 1.90%

Cement Iron & Steel

Petrol & Petrochemicals Glass

Machining of Metals Cables

Tools , Equipments and Transportation Ships & Boats

Metals Fertilizers

Gypsum Ceramic & Sanitary Ware

11

ii) Export Volume 2013 for all Sectors

Sector Export Volume % Cement 00.15%

Iron & Steel 01.85% Petrol & Petrochemicals 87.00%

Glass 01.40% Machining of Metals 00.04%

Cables 01.70%

Tools , Equipments and Transportation 00.69% Ships & Boats 00.01%

Metals 02.90% Fertilizers 02.24%

Gypsum 00.01%

Ceramic & Sanitary Ware 01.00%

Cement Iron & Steel

Petrol & Petrochemicals Glass

Machining of Metals Cables

Tools , Equipments and Transportation Ships & Boats

Metals Fertilizers

Gypsum Ceramic & Sanitary Ware

12

2.1Construction and Building

As shown below The black horse of Egypt’s Market Sectors is the

construction and building sector appears in its market growth

remaining in the most difficult years (+.3% for 2010/2011) also it

exceeded the general economical market growth itself (+5.9% 2013)

This data indicates how much this sector is expanding regardless the

political issues we can see it in the flow of capital in this sector

( exceeds 500 MEGP in Mar 2014)

0

20

40

60

80

100

120

140

Oct-13 Nov-13 Jan-13Feb-13

Mars-14

73 81 81

118133

Months

New Construction & Building CompaniesOct 2013/Mars 2014

Companies' Numbers

13

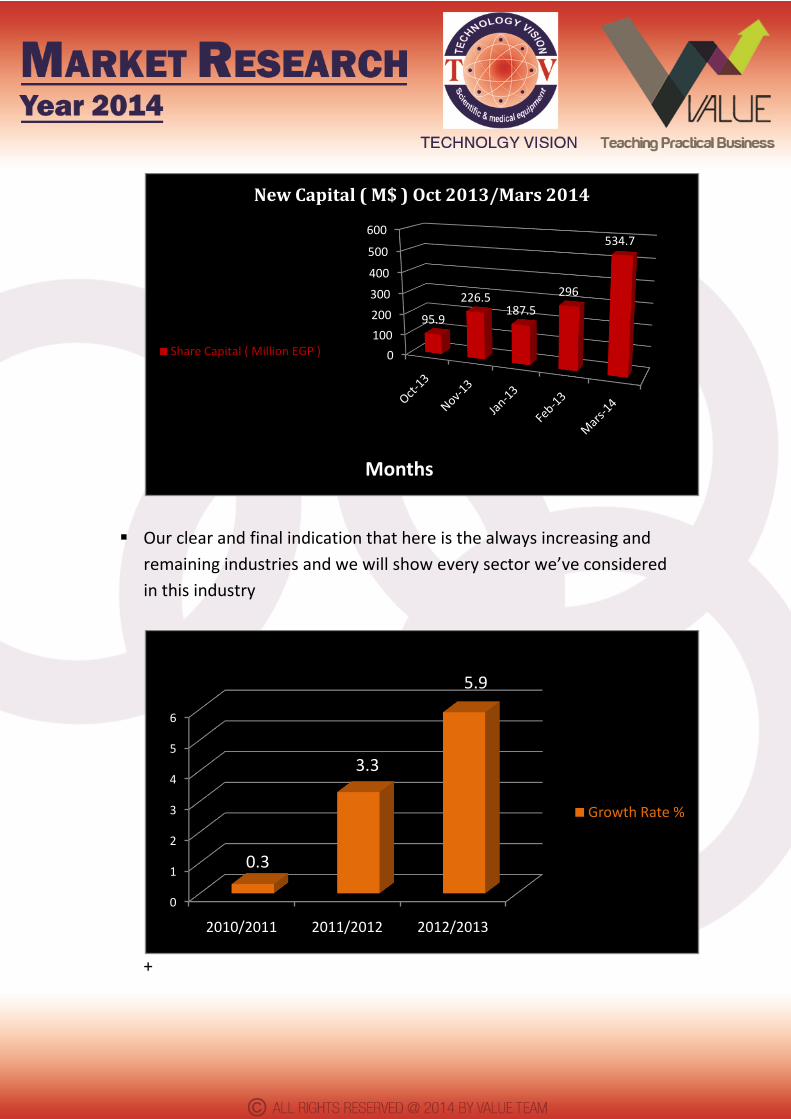

Our clear and final indication that here is the always increasing and

remaining industries and we will show every sector we’ve considered

in this industry

+

0

100

200

300

400

500

600

95.9

226.5187.5

296

534.7

Months

New Capital ( M$ ) Oct 2013/Mars 2014

Share Capital ( Million EGP )

0

1

2

3

4

5

6

2010/2011 2011/2012 2012/2013

0.3

3.3

5.9

Construction & Building Trade Volume/Year

Growth Rate %

14

2.1Construction and Building

2.1.1 Cement

No. of Factories 22 Market Share (Production + Earnings) (EGP) 24,000,000,000 Market Share (Production + Earnings) % 04.75%

Last Export 2013 (M$) 70 Last Export 2013 % 00.15 % X.R.F Market Share % 07.89 %

The Second Contributing Industrial Sector in the GDP after the

petroleum industries it’s one of the most promising industries now

and the next years

As appeared from 2012 a decay in cement exports (100 M$ for 2012

– 70 M$ for 2013) because of the enormous increasing in growth rate

of construction and building sector (5.9% for 2012) as the local

market demand covered the majority of production Capacity.

0

20

40

60

80

100

20102011

20122013

55

84

100

70

M$

Years

(Cement ) Export Volume_Annual (2010/2013)

15

Key Customers

Building Materials Industries Company (BMIC) Assiut Cement Company Arabian Cement Company ( ACC ) Amreyah Cement Company Qena Cement Company ( MCQE ) ALEXANDRIA PORTLAND CEMENT (TITAN) El-Nahda Cement Company Wadi El Nile Cement Company LAFARGE CEMENT EGYPT MEDCOM - Aswan Cement Sinai White Portland Cement Co. Sinai Cement Company (SCEM) National Cement Company - Helwan Helwan Cement Company (HCC Misr Beni Suef Cement Co (MBSC) SEWEDY CEMENT Company Suez Cement Company South Valley Cement (SVCE) Royal El Minya Cement Co. Tourah Portland Cement (TORA) El Arish Cement. Company

Promising opportunities

The government decided releasing 12 new cement factories license

very soon Covering the (demand – production) Gap

The Emirates Construction Company (Arabtech) announced the

Million unit Construction project putting a condition for Cement

factories that it will import Cement if there’s no new factories

support it.

16

2.1Construction and Building

2.1.2 Gypsum

Facts We import more than 80 % of its manufacturing components

Factories are facing some difficult times

The quality isn't good enough to help export it

The product doesn't meet the expectation of the Egyptian

market

No. of Factories 24

Market Share (Production + Earnings) (EGP) 750,000,000

Market Share (Production + Earnings) % 0.10 % Last Export 2013 (M$) 5.5

Last Export 2013 % 0.01 % X.R.F Market Share % U.D

Key Customers

Egyptian Gypsum Company

National Cement Company - Helwan

ALEXANDRIA PORTLAND CEMENT (TITAN)

Isoblock Swiss

17

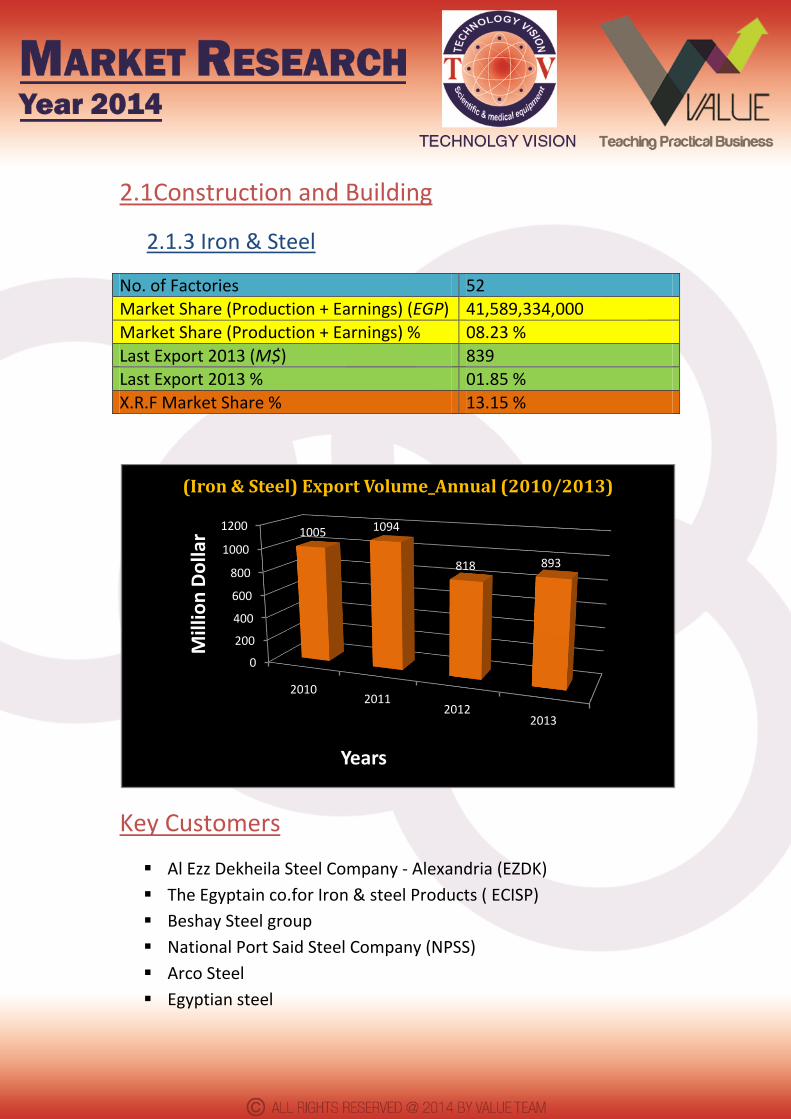

2.1Construction and Building

2.1.3 Iron & Steel

No. of Factories 52 Market Share (Production + Earnings) (EGP) 41,589,334,000 Market Share (Production + Earnings) % 08.23 %

Last Export 2013 (M$) 839 Last Export 2013 % 01.85 % X.R.F Market Share % 13.15 %

Key Customers

Al Ezz Dekheila Steel Company - Alexandria (EZDK)

The Egyptain co.for Iron & steel Products ( ECISP)

Beshay Steel group

National Port Said Steel Company (NPSS)

Arco Steel

Egyptian steel

0

200

400

600

800

1000

1200

20102011

20122013

1005 1094

818 893

Mill

ion

Do

llar

Years

(Iron & Steel) Export Volume_Annual (2010/2013)

18

2.1Construction and Building

2.1.4 Ceramic & Sanitary Ware

No. of Factories 37 Market Share (Production + Earnings) (EGP) 10,000,000,000

Market Share (Production + Earnings) % 01.90 % Last Export 2013 (M$) 466 Last Export 2013 % 01.00 % X.R.F Market Share % U.D

0

100

200

300

400

20102011

20122013

260

208

398

361

Mill

ion

Do

llar

Years

(Ceramic) Export Volume_Annual (2010/2013)

19

Key Customers

Royal Ceramica

Cleopatra Ceramics

EL GAWHARA FOR CERAMIC AND PORCELAIN

ALFA Ceramic

Rock Ceramic

Ideal Standard Sanitary Ware

Roka Sanitary Ware

Duravit Sanitary Ware

0

20

40

60

80

100

120

20102011

20122013

86

72

95 105

Mill

ion

Do

llar

Years

(Sanitary Ware) Export Volume_Annual (2010/2013)

20

2.1Construction and Building

2.1.5 Glass

No. of Factories 41 Market Share (Production + Earnings) (EGP) 2,204,258,000 Market Share (Production + Earnings) % 00.43 %

Last Export 2013 (M$) 502 Last Export 2013 % 01.10 % X.R.F Market Share % 02.60 %

Key Customers

Dr.Greiche ( Glass Products )

El Asfour Crystal International

Obour For Glass Technology

Pearl Glass Group

0

100

200

300

400

500

600

700

20102011

20122013

663 657 654

502

Mill

ion

Do

llar

Years

(Glass) Export Volume_Annual (2010/2013)

21

2.2 Oil & Petrol Products

2.2.1 Petrol & Petrochemicals

No. of Factories 63 Market Share (Production + Earnings) (EGP) 340,136,160,000

Market Share (Production + Earnings) % 67.31 %

Last Export 2013 (M$) 39, 480 Last Export 2013 % 87.00 %

X.R.F Market Share % 15.70 %

Key Customers

The Egyptian Petrochemicals Holding Company (ECHEM)

Sidpec - Sidi Kerir Petrochemicals

ASORC - Assiut Oil Refining Co

Ganoub El-Wadi Petroleum Holding Company (GANOPE)

Cairo Oil Refining Company CORC

Engineering for the petroleum and process industries. (Enppi)

22

2.2 Petrol & Petrochemicals

2.2.2 Fertilizers

No. of Factories 86 Market Share (Production + Earnings) (EGP) 18,778,160,000

Market Share (Production + Earnings) % 03.07 %

Last Export 2013 (M$) 973 Last Export 2013 % 02.14 %

X.R.F Market Share % U.D

Key Customers

Misr Fertilizers Production Company (MOPCO)

The National Company for Fertilizers & Chemicals (AGROCHEM

Suez Company For Fertilizer Production

Abu Zaabal Fertilizer and Chemical Factory

Abu Qir Fertilizers and Chemicals Company (AFC)

0

200

400

600

800

1000

1200

1400

20102011

20122013

10051209 1207

973

Mill

ion

Do

llar

Years

(Fertlizers) Export Volume_Annual (2010/2013)

23

2.3 Metal Industries

2.3.1 Machining of Metals

No. of Factories 14 Market Share (Production + Earnings) (EGP) 728,236,000

Market Share (Production + Earnings) % 00.14 %

Last Export 2013 (M$) 20 Last Export 2013 % 00.04 %

X.R.F Market Share % 10.50 %

0

20

40

60

80

20102011

20122013

35

52

79

20

Mill

ion

Do

llar

Years

(Machining of Metals) Export Volume_Annual (2010/2013)

24

2.3 Metal Industries

2.3.2 Metals

No. of Factories 852 Market Share (Production + Earnings) (EGP) 53,126,422,000

Market Share (Production + Earnings) % 10.50 %

Last Export 2013 (M$) 1,375 Last Export 2013 % 2.90 %

X.R.F Market Share % U.D

0

500

1000

1500

2000

20102011

20122013

1574 17161694

1357

Mill

ion

Do

llar

Years

(Metals) Export Volume_Annual (2010/2013)

25

2.3 Metal Industries

2.3.3 Cables

No. of Factories 19 Market Share (Production + Earnings) (EGP) 2,256,400,000

Market Share (Production + Earnings) % 00.44 %

Last Export 2013 (M$) 782 Last Export 2013 % 1.70 %

X.R.F Market Share % 5.20 %

Key Customers

El Sewedy Cables

Schneider Electric

Abb Power Systems & Automation Technology

0

200

400

600

800

1000

1200

20102011

20122013

9911114

937

782

Mill

ion

Do

llar

Years

(Cables) Export Volume_Annual (2010/2013)

26

2.3 Metal Industries

2.3.4 Intermediate Goods

No. of Factories 308 Market Share (Production + Earnings) (EGP) U.D

Market Share (Production + Earnings) % U.D

Last Export 2013 (M$) 492 Last Export 2013 % 1.00 %

X.R.F Market Share % 5.20 %

Key Customers

Hamenz German Technological Industries

Egyptian Automotive & Trading Co.

interbus company

EL-Wahab Group

0

100

200

300

400

500

600

20102011

20122013

392472

577

492

Mill

ion

Do

llar

Years

(Intermediate Goods) Export Volume_Annual (2010/2013)

27

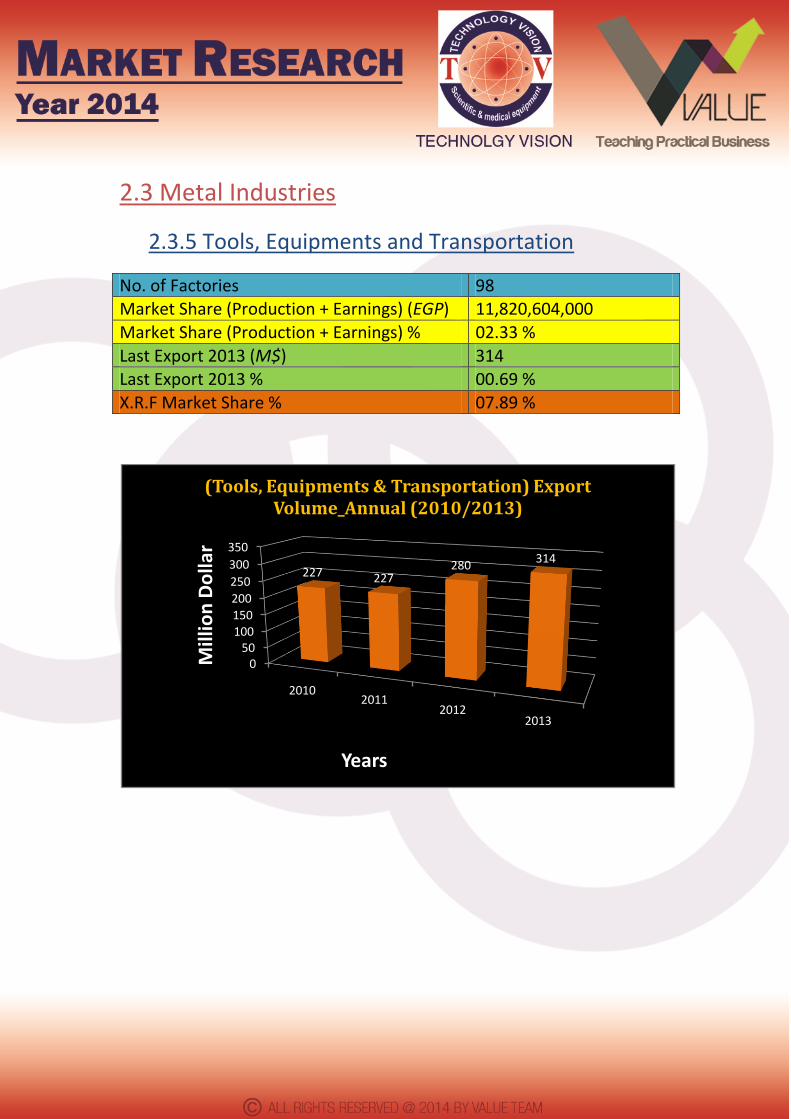

2.3 Metal Industries

2.3.5 Tools, Equipments and Transportation

No. of Factories 98 Market Share (Production + Earnings) (EGP) 11,820,604,000

Market Share (Production + Earnings) % 02.33 %

Last Export 2013 (M$) 314 Last Export 2013 % 00.69 %

X.R.F Market Share % 07.89 %

050

100150

200

250

300

350

20102011

20122013

227 227280

314

Mill

ion

Do

llar

Years

(Tools, Equipments & Transportation) Export Volume_Annual (2010/2013)

28

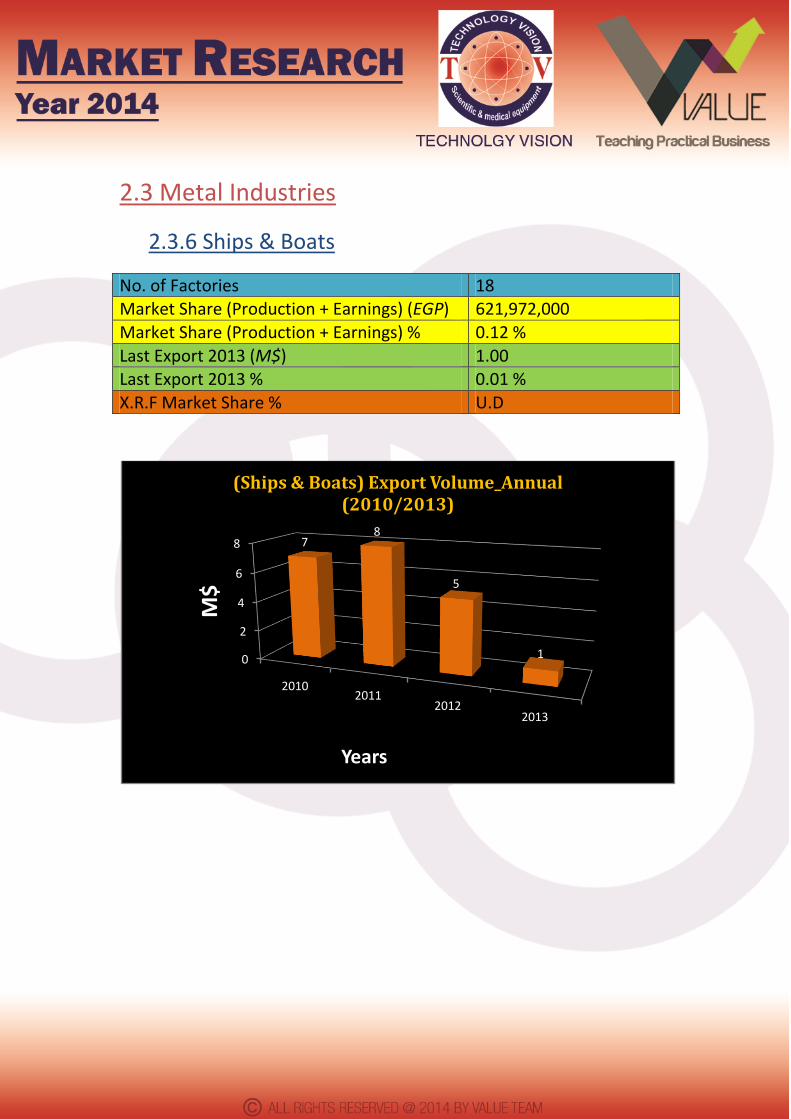

2.3 Metal Industries

2.3.6 Ships & Boats

No. of Factories 18 Market Share (Production + Earnings) (EGP) 621,972,000

Market Share (Production + Earnings) % 0.12 %

Last Export 2013 (M$) 1.00 Last Export 2013 % 0.01 %

X.R.F Market Share % U.D

0

2

4

6

8

20102011

20122013

78

5

1

M$

Years

(Ships & Boats) Export Volume_Annual (2010/2013)

29

2.4 Research & Development

Total No. of Facilities 132

Sector No. X.R.F Market Share % Research Sectors and Institutes 53 41.40% Engineering 37 28.90% Science 18 14.00% Agriculture 20 15.60%

41.40%

28.90%

14.00%

15.60%

Research Sectors and Institutes

Engineering

Science

Agriculture

30

3.Competitor Analysis

3.1 No. Of Apparatus for each competitor in 2013

Country Company Name No. Of Apparatus

USA Thermo Arl 3 to 6

Germany Bruker 3 to 5

Netherlands Panalytical 2 to 3

Japan Japanese Brands Maximum 2

China China Brandes Maximum 2

3.2 Market Volume For Competitors' Origin ( X-ray

in general )

Country Market Volume 2013

( Categorized By Origin) EGP

USA 29.94 %

Germany 27.44 %

Netherlands 09.90 %

Japan 04.00 %

China 02.70 %

31

3.3 Market Volume For Competitors' Origin ( X-ray

in general )

Total Import Volume ( EGP )

America Germany Netherlands Japan China

2010 9197121.97 3621501.84 10908475 3027752 503872

2011 8416829.8 10081604.35 9362032 5950500 858365

2012 9256803.95 18606945.47 8046224 1785046 3550485

2013 15457573 14165013.16 5157967.75 2094708 1444841

0

5000000

10000000

15000000

20000000

25000000

30000000

35000000

40000000

45000000

2010 2011 2012 2013

EGP

China

Japan

Netherlands

Germany

America

32