vce accounting unit 3 chapter 1 -...

TRANSCRIPT

1

VCE Accounting Unit 3 1. Pre double-entry

VCE Accounting Unit 3

Chapter 1 Pre double-entry

Excluding GST

Concepts and skills:

Balance Sheet

Assets and equities Stakeholders

Stock cards

Transactions evidenced by documents

Cash journals

Unclassified Cash Flow Statement

Income Statement

Reporting period

Revenue and expenses Net profit

Gross profit

Drawings

Liability

Accounting equation

Review of the elements

Agreed value

Stock for advertising purposes

Instructional videos:

Basic concepts (1 & 2): assets,

Balance Sheet, equities, owners equity, capital, liabilities, accounting equation.

Documents (simple) Stock card (simple)

Revenue (1 & 2)

Expenses (1, 2 &3)

Simple Cash Flow Statement

Income Statement (simple)

Reporting period (simple)

Drawings

Stock for advertising use

Agreed value (simple)

Podcasts:

Assets

Equities

Liabilities

Revenue

Expenses

2

VCE Accounting Unit 3 1. Pre double-entry

Clean Cut Mowers. Balance Sheet at 30/6/18

Assets $ Equities $

Bank 40000 Owners equity

Stock control 20000 Capital, Bob 175000

Office assets 25000

Premises 90000

Total assets 175000 Total equities 175000

The accounting reports, like the Balance Sheet, are prepared for stakeholders. Stakeholders are individuals or businesses that are interested in the performance of the business. Examples of stakeholders include the owner, manager, potential owner, people/businesses who are owed money by the business, employees, Australian Taxation Office (ATO) etc.

Clean Cut Mowers buy and sell ride-on mowers. Clean Cut Mowers is a trading business which buys and sells mowers on a cash basis. Selling the mowers is the business‟s revenue activity. The business is owned by one person, Bob, thus

Clean Cut Mowers is a sole-trader or sole-proprietorship. On 30/6/18. Clean Cut Mowers had the following Balance Sheet.

STOCK CARD: Ride on mower

2018 IN OUT BALANCE

Date Details QTY. COST VALUE QTY. COST VALUE QTY. COST VALUE

30/6 Balance 10 2000 20000

7/7 CHQ 56 3 2000 6000 13 2000 26000

8/7 REC 43 2 2000 4000 11 2000 22000

28/7 REC 44 3 2000 6000 8 2000 16000

Stock card

Equities refers to who has an interest or ownership in the assets. At 30/6/18, Bob, the owner, has 100% interest or ownership in the assets. Bob‟s ownership is called owners equity or capital.

Assets and equities „balance‟ in a Balance Sheet.

„Ride on mowers‟ is the stock that is traded by Clean Cut Mowers. Detailed information about stock is recorded in the stock card: see below. Note that the stock balance at 30/6/18 is $20000 as per the Balance

Sheet of the same date: see above.

On 30/6/18 the business has 10 ride-

on mowers with a unit cost of $2000. The IN column of the stock card records all movements of stock into the business. The most common example of an IN transaction would be the purchase of stock.

The OUT column of the stock card records all movements of stock out of the business. The most common example of an OUT transaction would be the sale of stock.

The BALANCE column changes after each stock transaction and represents the value of stock on hand at any point in time.

Balance Sheet

Assets are resources under the control of the business, as a result of past events, which will provide future economic benefits.

3

VCE Accounting Unit 3 1. Pre double-entry

Clean Cut Mowers. Unclassified Cash Flow Statement for July 2018.

Cash Receipts $ $

Sales 20000

Cash Payments

Stock purchases 6000

Office expenses 900 6900

Change in cash 13100

+ Cash at start 40000

= Cash at end 53100

Cash Receipts Journal (CRJ) CFS X √ √ √ √

IS √ exp. √ rev. X X

BS calc. X X calc. calc.

Date Details Doc. Bank Cost of Sales

Sales Sundry Loan Capital

8/7 SALES 43 8000 4000 8000

28/7 SALES 44 12000 6000 12000

31/7 Totals 20000 10000 20000

Cash Payments Journal (CPJ) CFS √ √ √ √ √ √ √ √

IS √ exp. X X √ exp. X √ exp. √ exp. ?

BS calc. X √ calc. X calc. X X ?

Date Details Doc. Bank Internet

Exps. Drawings Loan Interest Stock Cleaning

Office Exps.

Sundry

7/7 STOCK 56 6000 6000

17/7 OFFICE EXPS. 57 900 900

31/7 Totals 6900 6000 900

July transactions The following transactions, evidenced by documents, occurred during July 2018.

Bank of Melton

Date: 7/7/18

To: Just Mowers

For: 3 Mowers at $2000

each.

This cheque $6000

Cheque number 56

Clean Cut Mowers

Clean Cut Mowers

Receipt # 43

Date: 8/7/18

From: Cash Customers

For: Sale of 2 mowers

at $4000 each.

$: $8000.00

Thank you

Bank of Melton

Date: 17/7/18

To: OfficeWorks

For: Office expenses.

(Stationery etc.)

This cheque $900

Cheque number 57

Clean Cut Mowers

Clean Cut Mowers

Receipt # 44

Date: 28/7/18

From: Cash Customers

For: Sale of 3 mowers

at $4000 each.

$: $12000.00

Thank you

Cheque #56 is for the cash purchase of more trading stock.

Receipt #43 is for the cash sale of trading stock. Cost of sales = $4000.

Cheque #57 is for the cash payment of office expenses.

Receipt #44 is for the cash sale of trading stock. Cost of sales = $6000.

Cash Journals

Reports Clean Cut Mowers.

Income Statement for July 2018.

Revenue $

Sales 20000

Less Cost of Goods Sold

Cost of sales 10000

Gross profit 10000

Less other expenses

Office expenses 900

Net profit 9100

Clean Cut Mowers. Balance Sheet at 31/7/18

Assets $ Equities $

Bank 53100 Owners equity

Stock control 16000 Capital, Bob 175000

Office assets 25000 Add net profit 9100

Premises 90000

Total assets 184100 Total equities 184100

Profit is revenue earned less expenses incurred over the reporting period (July) and this data is reported in the Income Statement. The revenue activity for this

business is sales. Expenses are incurred to earn revenue. In July, the expenses are cost of sales and office expenses. Revenue and expense data is sourced from the cash journals and/or the Cash Flow Statement.

The Cash Flow Statement reports cash receipts and cash payments over the reporting period and shows the cash balance at the end of the reporting period. The cash flow data is sourced from the cash journals.

Net profit belongs to the owner so it is added to Capital in the new Balance at the end of the reporting period.

The data for the Balance Sheet at the end of the reporting period comes from the original Balance but takes into account any changes to assets, (such as Bank and Stock) and equities.

Total the cash journals at the

end of July.

Receipts are recorded in the Cash Receipts Journal and cheques in the Cash

Payments Journal.

From Balance Sheet.

From stock cards

4

VCE Accounting Unit 3 1. Pre double-entry

Clean Cut Mowers. Balance Sheet at 1/8/18

Assets $ Equities $

Bank 53100 Owners equity

Stock control 16000 Capital, Bob 184100

Office assets 25000

Premises 90000

Total assets 184100 Total equities 184100

Balance Sheet

STOCK CARD: Ride on mower

2018 IN OUT BALANCE

Date Details QTY. COST VALUE QTY. COST VALUE QTY. COST VALUE

1/8 Balance 8 2000 16000

5/8 CHQ 58 4 2000 8000 12 2000 24000

11/8 REC 45 3 2000 6000 9 2000 18000

28/8 REC 46 5 2000 10000 4 2000 8000

Stock card

August transactions The following transactions, evidenced by

documents, occurred during August 2018.

Bank of Melton

Date: 5/8/18

To: Just Mowers

For: 4 Mowers at $2000

each.

This cheque $8000

Cheque number 58

Clean Cut Mowers

Clean Cut Mowers

Receipt # 45

Date: 11/8/18

From: Cash Customers

For: Sale of 3 mowers

at $4000 each.

$: $12000.00

Thank you

Bank of Melton

Date: 18/8/18

To: Netspace

For: Internet expenses

This cheque $500

Cheque number 59

Clean Cut Mowers

Clean Cut Mowers

Receipt # 46

Date: 28/8/18

From: Cash Customers

For: Sale of 5 mowers

at $4000 each.

$: $20000.00

Thank you

Cheque #58 is for the cash purchase of more trading stock.

Receipt #45 is for the

cash sale of trading stock. Cost of sales = $6000.

Cheque #59 is for the cash payment of internet expenses.

Receipt #46 is for the cash sale of trading stock. Cost of sales = $10000.

Cash Receipts Journal (CRJ) CFS X √ √ √ √

IS √ exp. √ rev. X X

BS calc. X X calc. calc.

Date Details Doc. Bank Cost of Sales

Sales Sundry Loan Capital

11/8 SALES 45 12000 6000 12000

28/8 SALES 46 20000 10000 20000

31/8 Totals 32000 16000 32000

Cash Payments Journal (CPJ) CFS √ √ √ √ √ √ √ √

IS √ exp. X X √ exp. X √ exp. √ exp. ?

BS calc. X √ calc. X calc. X X ?

Date Details Doc. Bank Internet

Exps. Drawings Loan Interest Stock Cleaning

Office Exps.

Sundry

5/8 STOCK 58 8000 8000

18/8 INTERN.EXPS. 59 500 500

31/8 Totals 8500 500 8000

Journals for August

Total the cash journals at the end of August.

Stock cards only record

the cost price of stock.

Capital at the start of August is the capital at the end of July. This capital figure includes the impact of the profit from July. This data comes from the last Balance Sheet.

5

VCE Accounting Unit 3 1. Pre double-entry

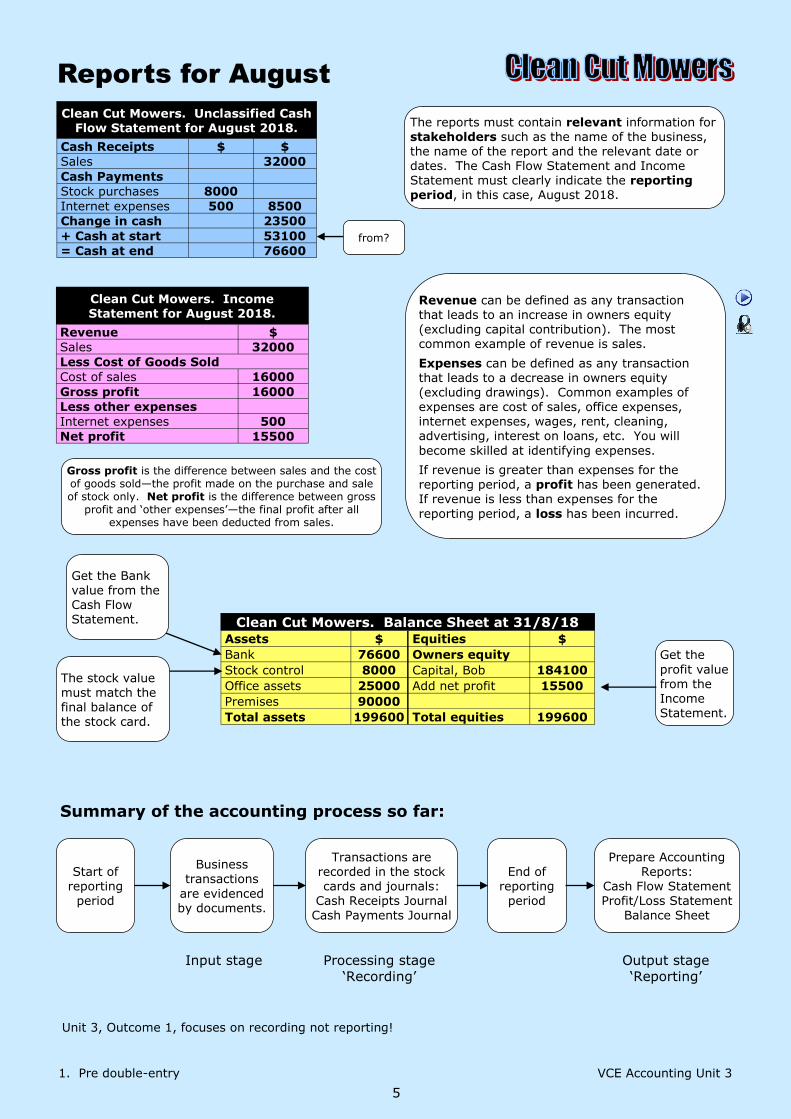

Summary of the accounting process so far:

Start of

reporting period

Business

transactions

are evidenced by documents.

Transactions are recorded in the stock

cards and journals: Cash Receipts Journal Cash Payments Journal

End of

reporting period

Prepare Accounting Reports:

Cash Flow Statement Profit/Loss Statement

Balance Sheet

Input stage Processing stage

„Recording‟

Output stage

„Reporting‟

Reports for August

Clean Cut Mowers. Unclassified Cash Flow Statement for August 2018.

Cash Receipts $ $

Sales 32000

Cash Payments

Stock purchases 8000

Internet expenses 500 8500

Change in cash 23500

+ Cash at start 53100

= Cash at end 76600

Clean Cut Mowers. Income Statement for August 2018.

Revenue $

Sales 32000

Less Cost of Goods Sold

Cost of sales 16000

Gross profit 16000

Less other expenses

Internet expenses 500

Net profit 15500

The reports must contain relevant information for stakeholders such as the name of the business, the name of the report and the relevant date or dates. The Cash Flow Statement and Income Statement must clearly indicate the reporting period, in this case, August 2018.

Revenue can be defined as any transaction that leads to an increase in owners equity (excluding capital contribution). The most common example of revenue is sales.

Expenses can be defined as any transaction that leads to a decrease in owners equity (excluding drawings). Common examples of expenses are cost of sales, office expenses, internet expenses, wages, rent, cleaning, advertising, interest on loans, etc. You will

become skilled at identifying expenses.

If revenue is greater than expenses for the

reporting period, a profit has been generated. If revenue is less than expenses for the

reporting period, a loss has been incurred.

Clean Cut Mowers. Balance Sheet at 31/8/18

Assets $ Equities $

Bank 76600 Owners equity

Stock control 8000 Capital, Bob 184100

Office assets 25000 Add net profit 15500

Premises 90000

Total assets 199600 Total equities 199600

The stock value

must match the final balance of the stock card.

Get the Bank value from the Cash Flow Statement.

Get the

profit value

from the Income Statement.

from?

Gross profit is the difference between sales and the cost of goods sold—the profit made on the purchase and sale of stock only. Net profit is the difference between gross

profit and „other expenses‟—the final profit after all expenses have been deducted from sales.

Unit 3, Outcome 1, focuses on recording not reporting!

6

VCE Accounting Unit 3 1. Pre double-entry

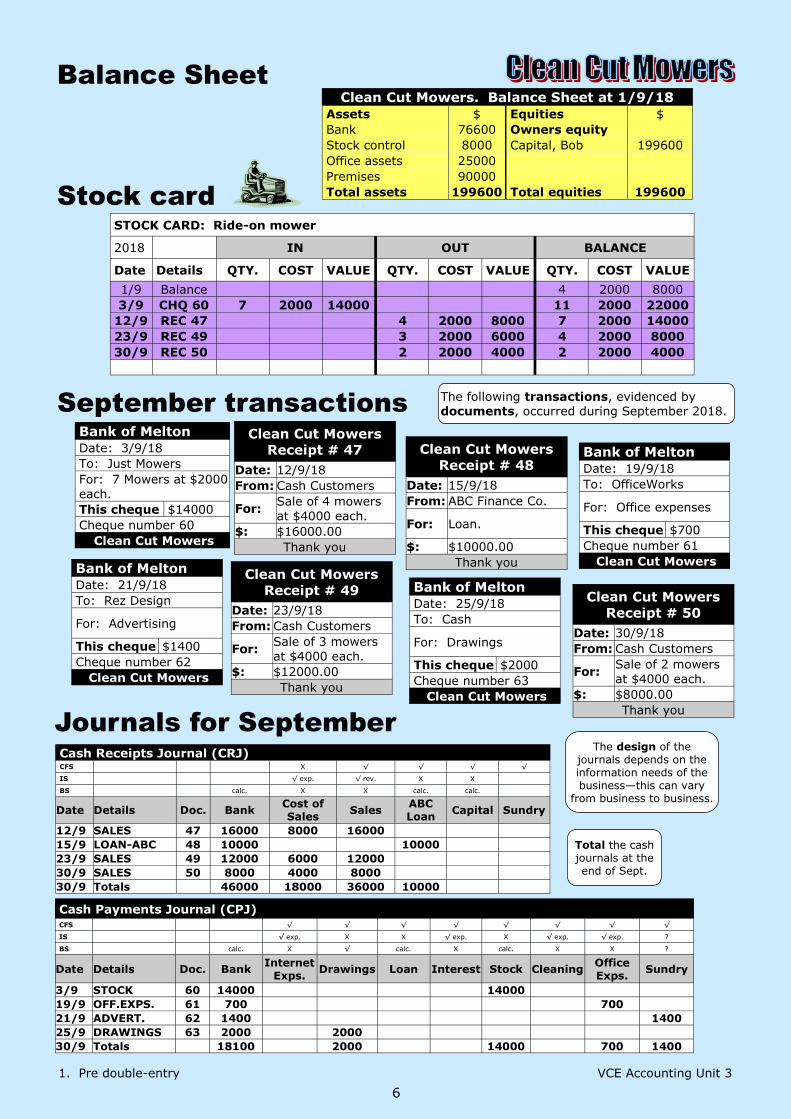

Clean Cut Mowers. Balance Sheet at 1/9/18

Assets $ Equities $

Bank 76600 Owners equity

Stock control 8000 Capital, Bob 199600

Office assets 25000

Premises 90000

Total assets 199600 Total equities 199600

Balance Sheet

STOCK CARD: Ride-on mower

2018 IN OUT BALANCE

Date Details QTY. COST VALUE QTY. COST VALUE QTY. COST VALUE

1/9 Balance 4 2000 8000

3/9 CHQ 60 7 2000 14000 11 2000 22000

12/9 REC 47 4 2000 8000 7 2000 14000

23/9 REC 49 3 2000 6000 4 2000 8000

30/9 REC 50 2 2000 4000 2 2000 4000

Stock card

September transactions The following transactions, evidenced by documents, occurred during September 2018.

Bank of Melton

Date: 3/9/18

To: Just Mowers

For: 7 Mowers at $2000

each.

This cheque $14000

Cheque number 60

Clean Cut Mowers

Clean Cut Mowers

Receipt # 47

Date: 12/9/18

From: Cash Customers

For: Sale of 4 mowers

at $4000 each.

$: $16000.00

Thank you

Bank of Melton

Date: 19/9/18

To: OfficeWorks

For: Office expenses

This cheque $700

Cheque number 61

Clean Cut Mowers Clean Cut Mowers

Receipt # 49

Date: 23/9/18

From: Cash Customers

For: Sale of 3 mowers

at $4000 each.

$: $12000.00

Thank you

Cash Receipts Journal (CRJ) CFS X √ √ √ √

IS √ exp. √ rev. X X

BS calc. X X calc. calc.

Date Details Doc. Bank Cost of Sales

Sales Sundry ABC Loan

Capital

12/9 SALES 47 16000 8000 16000

15/9 LOAN-ABC 48 10000 10000

23/9 SALES 49 12000 6000 12000

30/9 SALES 50 8000 4000 8000

30/9 Totals 46000 18000 36000 10000

Cash Payments Journal (CPJ) CFS √ √ √ √ √ √ √ √

IS √ exp. X X √ exp. X √ exp. √ exp. ?

BS calc. X √ calc. X calc. X X ?

Date Details Doc. Bank Internet

Exps. Drawings Loan Interest Stock Cleaning

Office Exps.

Sundry

3/9 STOCK 60 14000 14000

19/9 OFF.EXPS. 61 700 700

21/9 ADVERT. 62 1400 1400

25/9 DRAWINGS 63 2000 2000

30/9 Totals 18100 2000 14000 700 1400

Journals for September

Total the cash journals at the end of Sept.

Clean Cut Mowers

Receipt # 48

Date: 15/9/18

From: ABC Finance Co.

For: Loan.

$: $10000.00

Thank you Bank of Melton

Date: 21/9/18

To: Rez Design

For: Advertising

This cheque $1400

Cheque number 62

Clean Cut Mowers

Bank of Melton

Date: 25/9/18

To: Cash

For: Drawings

This cheque $2000

Cheque number 63

Clean Cut Mowers

Clean Cut Mowers

Receipt # 50

Date: 30/9/18

From: Cash Customers

For: Sale of 2 mowers

at $4000 each.

$: $8000.00

Thank you

The design of the journals depends on the information needs of the business—this can vary

from business to business.

7

VCE Accounting Unit 3 1. Pre double-entry

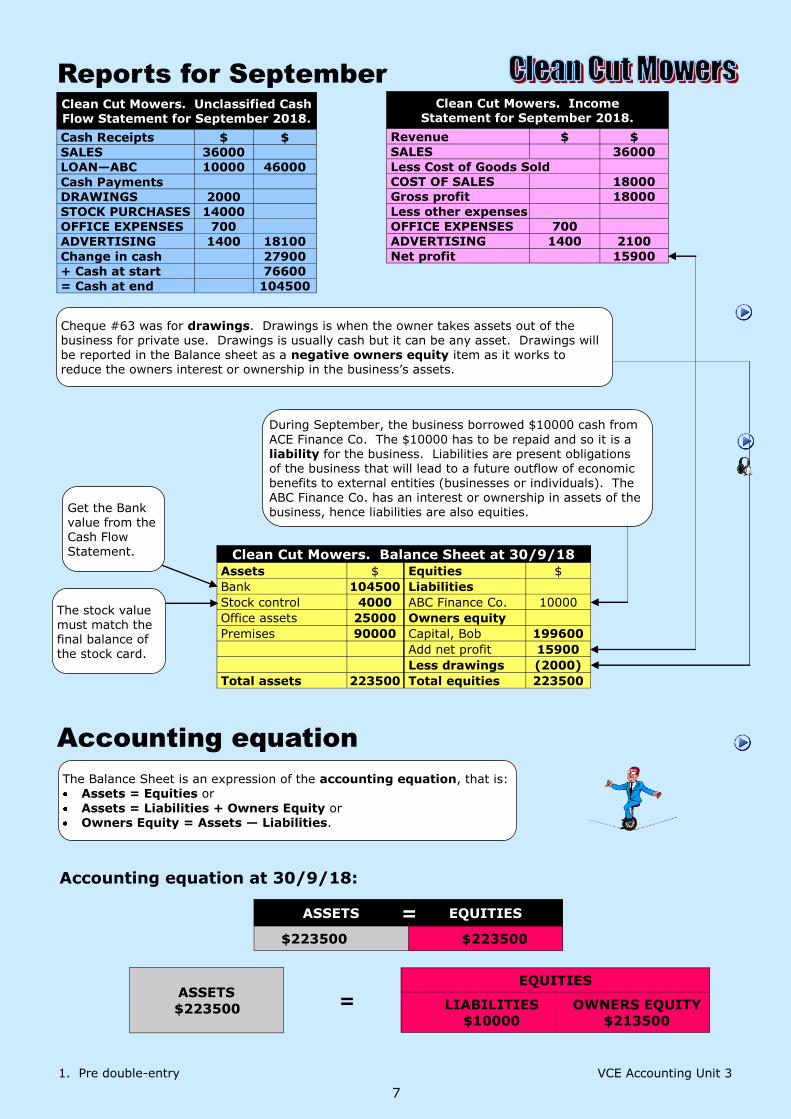

Accounting equation at 30/9/18:

ASSETS EQUITIES

$223500 $223500

=

ASSETS

$223500 = EQUITIES

LIABILITIES

$10000

OWNERS EQUITY

$213500

Reports for September

Clean Cut Mowers. Unclassified Cash Flow Statement for September 2018.

Cash Receipts $ $

SALES 36000

LOAN—ABC 10000 46000

Cash Payments

DRAWINGS 2000

STOCK PURCHASES 14000

OFFICE EXPENSES 700

ADVERTISING 1400 18100

Change in cash 27900

+ Cash at start 76600

= Cash at end 104500

Clean Cut Mowers. Income Statement for September 2018.

Revenue $ $

SALES 36000

Less Cost of Goods Sold

COST OF SALES 18000

Gross profit 18000

Less other expenses

OFFICE EXPENSES 700

ADVERTISING 1400 2100

Net profit 15900

Clean Cut Mowers. Balance Sheet at 30/9/18

Assets $ Equities $

Bank 104500 Liabilities

Stock control 4000 ABC Finance Co. 10000

Office assets 25000 Owners equity

Premises 90000 Capital, Bob 199600

Add net profit 15900

Less drawings (2000)

Total assets 223500 Total equities 223500

The stock value must match the final balance of the stock card.

Get the Bank value from the Cash Flow Statement.

Cheque #63 was for drawings. Drawings is when the owner takes assets out of the business for private use. Drawings is usually cash but it can be any asset. Drawings will be reported in the Balance sheet as a negative owners equity item as it works to reduce the owners interest or ownership in the business‟s assets.

Accounting equation

The Balance Sheet is an expression of the accounting equation, that is: Assets = Equities or

Assets = Liabilities + Owners Equity or Owners Equity = Assets — Liabilities.

During September, the business borrowed $10000 cash from

ACE Finance Co. The $10000 has to be repaid and so it is a liability for the business. Liabilities are present obligations of the business that will lead to a future outflow of economic

benefits to external entities (businesses or individuals). The ABC Finance Co. has an interest or ownership in assets of the business, hence liabilities are also equities.

8

VCE Accounting Unit 3 1. Pre double-entry

ASSETS LIABILITIES OWNERS EQUITY

INCREASE STOCK $14000

DECREASE CASH $14000

= +

Identify how the following transactions will impact on the accounting equation. Treat each transaction separately. Non cumulative.

Bank of Melton

Date: 3/9/18

To: Just Mowers

For: 7 Mowers at $2000

each.

This cheque $14000

Cheque number 60

Clean Cut Mowers

Clean Cut Mowers

Receipt # 47

Date: 12/9/19

From: Cash Customers

For: Sale of 4 mowers

at $4000 each.

$: $16000.00

Thank you

Bank of Melton

Date: 19/9/18

To: OfficeWorks

For: Office expenses

This cheque $700

Cheque number 61

Clean Cut Mowers

Clean Cut Mowers

Receipt # 48

Date: 15/9/19

From: ABC Finance Co.

For: Loan.

$: $10000.00

Thank you

ASSETS LIABILITIES OWNERS EQUITY

INCREASE CASH $16000

DECREASE STOCK $8000

NET INCREASE $8000

INCREASE $16000 SALES

DECREASE $8000 COST OF SALES

NET INCREASE $8000

= +

Difficult transaction. Cash sale of stock. The total cost of sales = $8000 (4 x $2000).

ASSETS LIABILITIES OWNERS EQUITY

INCREASE CASH $10000

INCREASE ABC LOAN $10000

= +

ASSETS LIABILITIES OWNERS EQUITY

DECREASE CASH $700

DECREASE $700 DUE TO

OFFICE EXPENSES

= +

Cash purchase of stock.

Loan of $10000 cash.

Cash expenses of $700. Important

On the two exams, avoid all abbreviations such as arrows : the

examiners do not like them! Also, avoid abbreviations such as „C.O.S.‟

9

VCE Accounting Unit 3 1. Pre double-entry

Clean Cut Mowers

Receipt # 49

Date: 23/9/19

From: Cash Customers

For: Sale of 3 mowers

at $4000 each.

$: $12000.00

Thank you

Bank of Melton

Date: 21/9/18

To: Rez Design

For: Advertising

This cheque $1400

Cheque number 62

Clean Cut Mowers

Bank of Melton

Date: 25/9/18

To: Cash

For: Drawings

This cheque $2000

Cheque number 63

Clean Cut Mowers

Clean Cut Mowers

Receipt # 50

Date: 30/9/19

From: Cash Customers

For: Sale of 2 mowers

at $4000 each.

$: $8000.00

Thank you

ASSETS LIABILITIES OWNERS EQUITY

DECREASE CASH $1400

DECREASE $1400 DUE TO

ADVERTISING EXPENSES

= +

ASSETS LIABILITIES OWNERS EQUITY

INCREASE CASH $12000

DECREASE STOCK $6000

NET INCREASE $6000

INCREASE $12000 SALES

DECREASE $6000 COST OF SALES

NET INCREASE $6000

= +

ASSETS LIABILITIES OWNERS EQUITY

DECREASE CASH $2000

DECREASE $2000 DUE TO

DRAWINGS.

= +

ASSETS LIABILITIES OWNERS EQUITY

INCREASE CASH $8000

DECREASE STOCK $4000

NET INCREASE $4000

INCREASE $8000 SALES

DECREASE $4000 COST OF SALES

NET INCREASE $4000

= +

Cash expenses of $1400.

Difficult transaction. Cash sale of stock. The total cost of sales = $6000 (3 x $2000).

Cash drawings $2000.

Difficult transaction. Cash sale of stock. The total cost of sales = $4000 (2 x $2000).

Important You can use pencil in class and

on all assessment tasks including the two exams!

10

VCE Accounting Unit 3 1. Pre double-entry

General Journal (GJ)

Date Details $

29/10/18 CAPITAL CONTRIBUTION OF OFFICE ASSETS (COMPUTER), MEMO #1 1000

31/10 DRAWINGS OF STOCK X 1 UNIT, MEMO #2 2000

MEMO #1: 29/10/18 The owner, Bob, contributed his personal

computer to the business (office assets). $1000.

Clean Cut Mowers. Balance Sheet at 1/10/18

Assets $ Equities $

Bank 104500 Liabilities

Stock control 4000 ABC Finance Co. 10000

Office assets 25000 Owners equity

Premises 90000 Capital, Bob 213500

Total assets 223500 Total equities 223500

Balance Sheet

STOCK CARD: Ride-on mower

2018 IN OUT BALANCE

Date Details QTY. COST VALUE QTY. COST VALUE QTY. COST VALUE

1/10 Balance 2 2000 4000

4/10 CHQ 64 9 2000 18000 11 2000 22000

15/10 REC 51 5 2000 10000 6 2000 12000

31/10 MEM 2 1 2000 2000 5 2000 10000

Stock card

October transactions The following transactions, evidenced by documents, occurred during October 2018.

Bank of Melton

Date: 4/10/18

To: Just Mowers

For: 9 Mowers at $2000

each.

This cheque $18000

Cheque number 64

Clean Cut Mowers

Clean Cut Mowers

Receipt # 51

Date: 15/10/18

From: Cash Customers

For: Sale of 5 mowers

at $4000 each.

$: $20000.00

Thank you

Bank of Melton

Date: 25/10/18

To: OfficeWorks

For: Power expenses.

This cheque $500

Cheque number 65

Clean Cut Mowers

Cash Receipts Journal (CRJ) CFS X √ √ √ √

IS √ exp. √ rev. X X

BS calc. X X calc. calc.

Date Details Doc. Bank Cost of Sales

Sales Loan Capital Sundry

15/10 SALES 51 20000 10000 20000

31/10 Totals 20000 10000 20000

Cash Payments Journal (CPJ) CFS √ √ √ √ √ √ √ √

IS √ exp. X X √ exp. X √ exp. √ exp. ?

BS calc. X √ calc. X calc. X X ?

Date Details Doc. Bank Internet

Exps. Drawings

ABC Loan

Interest on loan

Stock Cleaning Office Exps.

Sundry

9/10 STOCK 64 18000 18000

25/10 POWER EXPS. 65 500 500

27/10 LOAN-ABC 66 770 700 70

31/10 Totals 19270 700 70 18000 500

Journals for October

Total the cash journals at the

end of Oct.

MEMO #2: 31/10/18

The owner, Bob, took 1 unit of stock home for his private use. $2000. Drawings of stock.

Bank of Melton

Date: 27/10/18

To: ABC Finance Co.

For: Repayment of

loan including $70 interest.

This cheque $770

Cheque number 66

Clean Cut Mowers

Of course most businesses use electronic systems not these ol‟ fashioned manual

systems!

11

VCE Accounting Unit 3 1. Pre double-entry

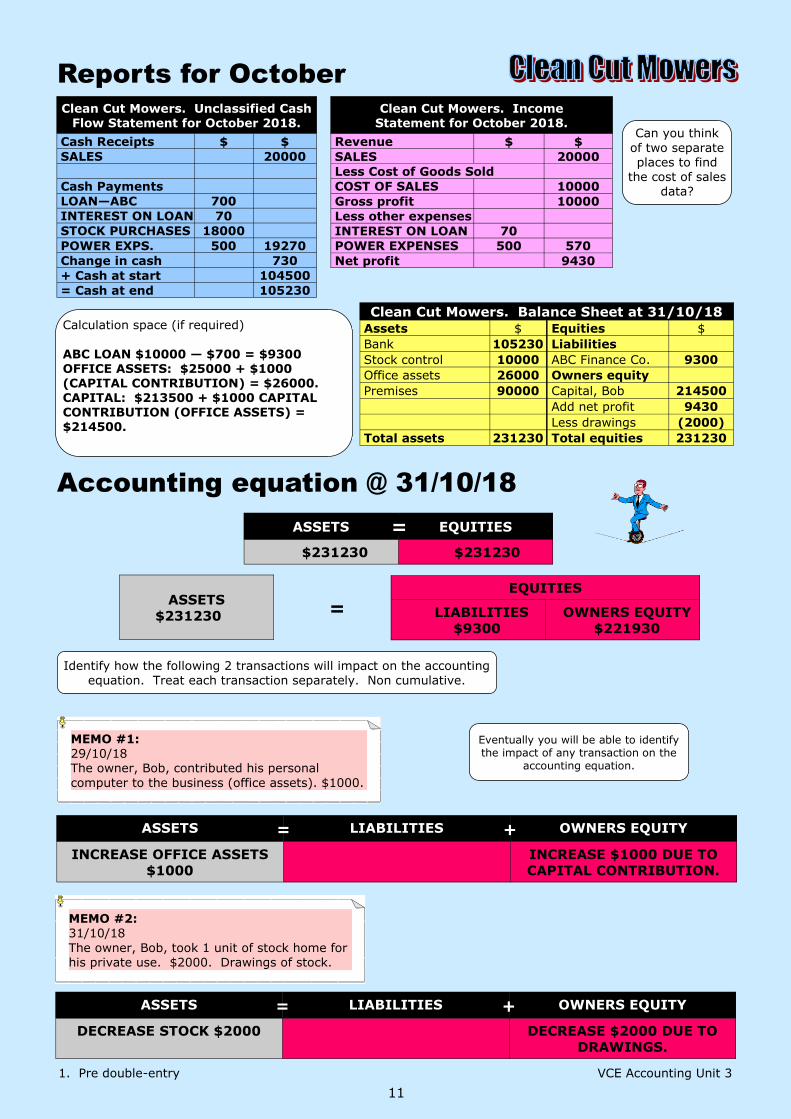

ASSETS EQUITIES

$231230 $231230

=

ASSETS

$231230 = EQUITIES

LIABILITIES

$9300

OWNERS EQUITY

$221930

Reports for October

Clean Cut Mowers. Unclassified Cash Flow Statement for October 2018.

Cash Receipts $ $

SALES 20000

Cash Payments

LOAN—ABC 700

INTEREST ON LOAN 70

STOCK PURCHASES 18000

POWER EXPS. 500 19270

Change in cash 730

+ Cash at start 104500

= Cash at end 105230

Clean Cut Mowers. Income Statement for October 2018.

Revenue $ $

SALES 20000

Less Cost of Goods Sold

COST OF SALES 10000

Gross profit 10000

Less other expenses

INTEREST ON LOAN 70

POWER EXPENSES 500 570

Net profit 9430

Clean Cut Mowers. Balance Sheet at 31/10/18

Assets $ Equities $

Bank 105230 Liabilities

Stock control 10000 ABC Finance Co. 9300

Office assets 26000 Owners equity

Premises 90000 Capital, Bob 214500

Add net profit 9430

Less drawings (2000)

Total assets 231230 Total equities 231230

Calculation space (if required)

ABC LOAN $10000 — $700 = $9300 OFFICE ASSETS: $25000 + $1000 (CAPITAL CONTRIBUTION) = $26000. CAPITAL: $213500 + $1000 CAPITAL CONTRIBUTION (OFFICE ASSETS) = $214500.

Accounting equation @ 31/10/18

Identify how the following 2 transactions will impact on the accounting

equation. Treat each transaction separately. Non cumulative.

ASSETS LIABILITIES OWNERS EQUITY

INCREASE OFFICE ASSETS

$1000

INCREASE $1000 DUE TO

CAPITAL CONTRIBUTION.

= +

MEMO #1: 29/10/18 The owner, Bob, contributed his personal

computer to the business (office assets). $1000.

MEMO #2: 31/10/18

The owner, Bob, took 1 unit of stock home for his private use. $2000. Drawings of stock.

ASSETS LIABILITIES OWNERS EQUITY

DECREASE STOCK $2000

DECREASE $2000 DUE TO

DRAWINGS.

= +

Can you think

of two separate places to find

the cost of sales data?

Eventually you will be able to identify the impact of any transaction on the

accounting equation.

12

VCE Accounting Unit 3 1. Pre double-entry

A L OE R E Quick Review

9. Transactions are evidenced by … A. Cash Flow Statement. B. Income Statement. C. Documents. D. Journals.

10. An item will usually get its own column in the journals if … A. It has a high dollar value. B. It is a frequent transaction. C. It is an infrequent transaction. D. There is enough room. 11. The report that provides stakeholders with detailed information about the businesses cash resources …

A. Balance sheet B. Cash receipts journal. C. Cash flow statement. D. Income statement. 12. Owners equity can change due to … A. Revenue. B. Expenses. C. Drawings. D. All of the above.

13. If drawings exceeds profit for a reporting period, owners equity will … A. Increase. B. Decrease. C. No impact. D. Impact cannot be determined from this data. 14. The owners equity section of the Balance Sheet can report …

A. Capital plus revenue less drawings. B. Assets plus profit less drawings. C. Capital plus profit less drawings. D. Assets less loss less drawings. 15. The most likely sequence for a simple accounting process is … A. Documents, journals & stock-cards, reports. B. Journals & stock-cards, documents, reports. C. Reports, documents, journals & stock-cards. D. Documents, reports, journals & stock-cards.

16. Information in the accounting reports is said to be more reliable if … A. The Income Statement reports a profit. B. The reports are supported by documentary

evidence. C. The reports are prepared frequently. D. The Balance Sheet balances. 17. The accounting equation shows …

A. Liabilities equals assets plus owners equity. B. Assets equal liabilities plus owners equity. C. Owners equity less liabilities equals assets. D. Assets plus liabilities equals owners equity.

1. Which one of the following is the best description of an asset? A. Present obligations of the business that will lead to a

future outflow of economic benefits. B. Resources under the control of the business

which will provide future economic benefits. C. Causes an increase in owners equity. D. Causes a decrease in owners equity. 2. Which one of the following is the best description of a liability? A. Present obligations of the business that will

lead to a future outflow of economic benefits. B. Resources under the control of the business which

will provide future economic benefits. C. Causes an increase in owners equity.

D. Causes a decrease in owners equity. 3. Which one of the following is the best description of owners equity? A. Future obligations of the business. B. Resources under the control of the business which

will provide future economic benefits. C. Liabilities less assets. D. Assets less liabilities. 4. Revenue could be defined as ..

A. Future obligations of the business. B. Resources under the control of the business which

will provide future economic benefits. C. Transactions that cause an increase in owners

equity excluding capital contributions. D. Transactions that cause a decrease in owners equity

excluding drawings. 5. Expenses could be defined as …

A. Future obligations of the business. B. Resources under the control of the business which

will provide future economic benefits. C. Transactions that cause an increase in owners equity

excluding capital contributions. D. Transactions that cause a decrease in owners

equity excluding drawings. 6. The reporting period is best described as … A. Period of time over which assets are determined. B. Period of time over which profit is determined.

C. Period of time over which liabilities are determined. D. 1/7/XX to 30/6/XX 7. Equities are best described as … A. Assets and liabilities. B. Assets less liabilities. C. Liabilities and owners equity. D. Assets less owners equity. 8. In a Balance Sheet, the following „balance‟ …

A. Assets and liabilities. B. Assets and equities. C. Assets and revenues. D. Equities and liabilities.

PS: the current VCE exams do

not include multiple-choice

questions.

17 17

13

VCE Accounting Unit 3 1. Pre double-entry

The accounting equation is Assets (A)= Liabilities (L) + Owners Equity (OE) which represents the relationships in the Balance Sheet. Alternative ways to express the accounting equation are: OE = A — L and A — L = OE.

Example 1: Excludes revenue, expenses and GST.

ASSETS LIABILITIES OWNERS EQUITY = +

Transaction 1: owner contributed $100000 cash to start business.

$100000 $100000 = +

2: owner contributed personal stock to business worth $6000.

$6000 $6000 = +

3: owner contributed personal vehicle to business worth $20000.

$20000 $20000 = +

4: bought computer for $4000 cash.

$4000

$4000 = +

5: bought office desk for $2000 cash.

$2000

$2000 = +

6: borrowed $8000 from ANZ Bank.

$8000 $8000 = +

7: paid ANZ Bank $500 to reduce loan.

$500 $500 = +

8: paid $5000 cash for stock.

$5000 $5000

= +

9: owner took $1000 cash for private use (Drawings).

$1000 $1000 = +

10: borrowed additional $3000 from ANZ.

$3000 $3000 = +

Accounting Equation … again

Treat each transaction separately.

14

VCE Accounting Unit 3 1. Pre double-entry

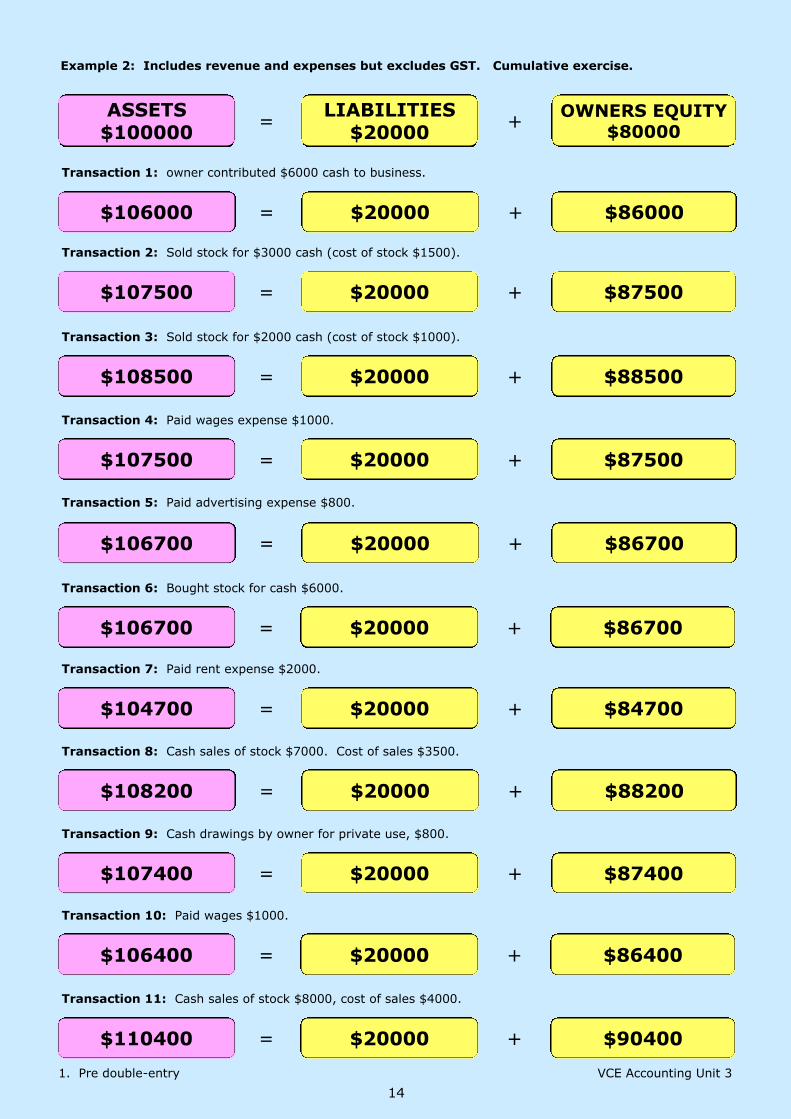

Example 2: Includes revenue and expenses but excludes GST. Cumulative exercise.

ASSETS $100000

LIABILITIES $20000

OWNERS EQUITY $80000

= +

Transaction 1: owner contributed $6000 cash to business.

$106000 $20000 $86000 = +

Transaction 2: Sold stock for $3000 cash (cost of stock $1500).

$107500 $20000 $87500 = +

Transaction 3: Sold stock for $2000 cash (cost of stock $1000).

$108500 $20000 $88500 = +

Transaction 4: Paid wages expense $1000.

$107500 $20000 $87500 = +

Transaction 5: Paid advertising expense $800.

$106700 $20000 $86700 = +

Transaction 6: Bought stock for cash $6000.

$106700 $20000 $86700 = +

Transaction 7: Paid rent expense $2000.

$104700 $20000 $84700 = +

Transaction 8: Cash sales of stock $7000. Cost of sales $3500.

$108200 $20000 $88200 = +

Transaction 9: Cash drawings by owner for private use, $800.

$107400 $20000 $87400 = +

Transaction 10: Paid wages $1000.

$106400 $20000 $86400 = +

Transaction 11: Cash sales of stock $8000, cost of sales $4000.

$110400 $20000 $90400 = +

15

VCE Accounting Unit 3 1. Pre double-entry

The elements are: assets (A), liabilities (L), owners equity (OE), revenue (R) and expenses (E). You need to understand these terms — eventually! You could use this sheet to assist you! Why not do this in pairs? Resources?

Find the AASB Glossary to help you complete this page.

Just Computers. Balance Sheet at 31/7/21

ASSETS $ EQUITIES $

Bank 24700 LIABILIITIES

Fixtures & Fittings 2000 Loan, ANZ 10000

Stock of Computer Systems 9600 OWNERS EQUITY

Office Equipment 3700 Capital, Jennifer 30000

Total Assets 40000 Total Equities 40000

Assets Liabilities Owners Equity

A resource:

(a) controlled by an entity as a

result of past events; and

(b) from which future economic

benefits are expected to flow to the

entity.

A present obligation of the entity

arising from past events, the

settlement of which is expected to

result in an outflow from the entity

of resources embodying economic

benefits.

The residual interest in the assets of

the entity after deducting all its

liabilities.

Find the AASB definitions of the following:

The Elements … again

Just Computers, Income Statement for August 2022

Revenue $ $

Sales 29000

Less Cost of Goods Sold

Cost of sales 8700

Gross Profit 20300

Less other Expenses

Advertising 3700

Wages 12400 16100

Net Profit 4200

Revenue Expenses

The gross inflow of economic benefits during the period

arising in the course of the ordinary activities of an entity

when those inflows result in increases in equity, other than

increases relating to contributions from equity

participants (yuk!)

Decreases in economic benefits during the accounting

period in the form of outflows or depletions of assets or

incurrences of liabilities that result in decreases in equity,

other than those relating to distributions to equity

participants (yuk!)

Find the AASB definitions of the following:

A L OE R E

www.aasb.gov.au

A L OE R E

16

VCE Accounting Unit 3 1. Pre double-entry

Agreed value

Which value should the business use to value the vehicle? $40000 or $30000? The original cost of $40000 is not relevant to the business since it was paid by the owner as a private individual: the business entity did not pay $40000. Even though the $30000 is an estimate, and thus lacks

reliability, it is a more relevant valuation for the stakeholders. (Note that the use of „experts‟ does, however, help to improve the reliability of the estimate).

MEMO #66: 3/6/22 Owner contributed a personal vehicle to

the business which had originally cost her $40000 on 1/6/19. After consulting some valuation experts, the agreed value is $30000.

Ace Traders. Balance Sheet extract at 3/6/22

ASSETS $ EQUITIES $

Vehicle 30000

General Journal (GJ)

Date Details $

3/6/22 Contribution of vehicle at agreed value, memo #66 30000

Explain how memo #66 impacts on the accounting equation of Ace Traders. Assets: increase $30000

Liabilities: no impact

Owners equity: increase $30000 due to capital contribution

Stock for advertising purposes

Sometimes a business will take some of its stock to use for

promotional or advertising purposes. It might be that the business is attending a Trade Expo or other function and wants to display its stock. Perhaps the business has a travelling sales

person who takes stock to show to potential customers.

MEMO #22: 1/11/32 Took 5 iPads for advertising purposes.

STOCK CARD: iPads

2032 IN OUT BALANCE

Date Details QTY. COST VALUE QTY. COST VALUE QTY. COST VALUE

1/11 Balance 20 300 6000

Memo 22 5 300 1500 15 300 4500

General Journal (GJ)

Date Details $

1/11/32 Stock for advertising purposes, 5 iPads, memo #22 1500

Hi Tech Traders. Income Statement extract for November 2032.

$ $

Less other expenses

Advertising 1500

Net profit

The stock used for advertising will be reported as an expense in the Income Statement. This is an example of a non cash expense. Another example of an non cash expense is cost of sales.

17

VCE Accounting Unit 3 1. Pre double-entry

18

VCE Accounting Unit 3 1. Pre double-entry

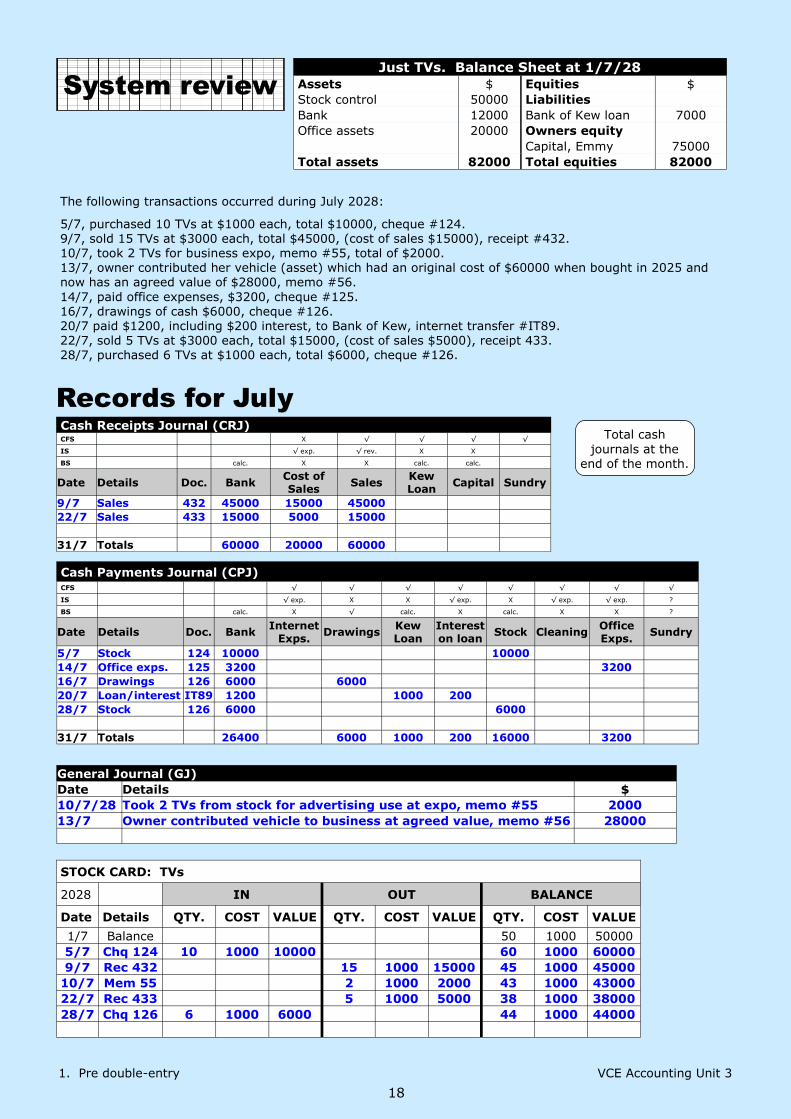

Just TVs. Balance Sheet at 1/7/28

Assets $ Equities $

Stock control 50000 Liabilities

Bank 12000 Bank of Kew loan 7000

Office assets 20000 Owners equity

Capital, Emmy 75000

Total assets 82000 Total equities 82000

The following transactions occurred during July 2028:

5/7, purchased 10 TVs at $1000 each, total $10000, cheque #124. 9/7, sold 15 TVs at $3000 each, total $45000, (cost of sales $15000), receipt #432. 10/7, took 2 TVs for business expo, memo #55, total of $2000. 13/7, owner contributed her vehicle (asset) which had an original cost of $60000 when bought in 2025 and now has an agreed value of $28000, memo #56.

14/7, paid office expenses, $3200, cheque #125. 16/7, drawings of cash $6000, cheque #126. 20/7 paid $1200, including $200 interest, to Bank of Kew, internet transfer #IT89. 22/7, sold 5 TVs at $3000 each, total $15000, (cost of sales $5000), receipt 433. 28/7, purchased 6 TVs at $1000 each, total $6000, cheque #126.

General Journal (GJ)

Date Details $

10/7/28 Took 2 TVs from stock for advertising use at expo, memo #55 2000

13/7 Owner contributed vehicle to business at agreed value, memo #56 28000

Cash Receipts Journal (CRJ) CFS X √ √ √ √

IS √ exp. √ rev. X X

BS calc. X X calc. calc.

Date Details Doc. Bank Cost of Sales

Sales Kew Loan

Capital Sundry

9/7 Sales 432 45000 15000 45000

22/7 Sales 433 15000 5000 15000

31/7 Totals 60000 20000 60000

Cash Payments Journal (CPJ) CFS √ √ √ √ √ √ √ √

IS √ exp. X X √ exp. X √ exp. √ exp. ?

BS calc. X √ calc. X calc. X X ?

Date Details Doc. Bank Internet

Exps. Drawings

Kew Loan

Interest on loan

Stock Cleaning Office Exps.

Sundry

5/7 Stock 124 10000 10000

14/7 Office exps. 125 3200 3200

16/7 Drawings 126 6000 6000

20/7 Loan/interest IT89 1200 1000 200

28/7 Stock 126 6000 6000

31/7 Totals 26400 6000 1000 200 16000 3200

Records for July

STOCK CARD: TVs

2028 IN OUT BALANCE

Date Details QTY. COST VALUE QTY. COST VALUE QTY. COST VALUE

1/7 Balance 50 1000 50000

5/7 Chq 124 10 1000 10000 60 1000 60000

9/7 Rec 432 15 1000 15000 45 1000 45000

10/7 Mem 55 2 1000 2000 43 1000 43000

22/7 Rec 433 5 1000 5000 38 1000 38000

28/7 Chq 126 6 1000 6000 44 1000 44000

Total cash

journals at the end of the month.

System review

19

VCE Accounting Unit 3 1. Pre double-entry

Reports for July

Just TVs. Unclassified Cash Flow Statement for July 2028.

Cash Receipts $ $

Sales 60000

Cash Payments

Drawings 6000

Kew loan 1000

Interest on loan 200

Stock purchases 16000

Office expenses 3200 26400

Change in cash 33600

+ Cash at start 12000

= Cash at end 45600

Just TVs. Income Statement for July 2028.

Revenue $ $

Sales 60000

Less Cost of Goods Sold

Cost of sales 20000

Gross profit 40000

Less other expenses

Interest on loan 200

Office expenses 3200

Advertising 2000 5400

Net profit 34600

Just TVs. Balance Sheet at 31/7/28

Assets $ Equities $

Stock 44000 Liabilities

Bank 45600 Kew loan 6000

Office assets 20000 Owners equity

Vehicle 28000 Capital 103000

Add net profit 34600

Less drawings (6000)

Total assets 137600 Total equities 137600

ASSETS LIABILITIES OWNERS EQUITY

Decrease stock $2000

Decrease $2000 due to

advertising expense

= +

Show the impact of memo #55 on the accounting equation:

ASSETS LIABILITIES OWNERS EQUITY

Increase $28000

Increase $28000 due to

capital contribution

= +

Show the impact of memo #56 on the accounting equation:

Assume that it is now discovered that wages of $2000 was not recorded in July 2028. Explain how this error would impact on:

1. The Cash Flow Statement for July: Cash payments would be understated $2000 thus the cash balance at the end would be overstated $2000.

2. The Income Statement for July: Expenses would be understated $2000 thus profit would be overstated $2000.

3. The Balance Sheet at 31/7/28: Assets: Bank would be overstated $2000. Liabilities: no impact. Owners equity: overstated $2000 due to profit impact.

20

VCE Accounting Unit 3 1. Pre double-entry

VCE Accounting Unit 3: Nano Exam 1. Marks = 34. Time = 34 minutes.

Stephanie owns and manages BusinessWorks trading in business equipment on a cash basis only. On 3/7/27 the business took 2 printers from stock so that the salesperson could demonstrate them for potential customers. Total value of stock = $1200.

1.1 What documentation would be used to record this transaction?

1 mark Memo or journal note. 1.2 List two accounting records that would be used to record this transaction.

2 marks

Record 1: General Journal Record 2: Stock Cards (OUT and BAL)

1.3 Show the impact of this transaction on the accounting equation by completing this following table:

2 marks

Cash Receipts Journal (CRJ) Date 2027

Details Doc. Bank Cost of Sales

Sales Loan Capital Sundry

30/11 Totals — 21000 4500 15000 1000 5000

Asset Liability Owners equity

Increase $________ Decrease $1200

No change

Increase $________ Decrease $_______

No change

Increase $________ Decrease $1200

No change

1.4 Which document (Doc. #99) was probably used on 3/9? Give evidence to support your answer. 1 mark

Cheque. Stock has come into the business and this business only trades on a cash basis. Doc #99 is most likely to be a cash purchase. (could be a capital contribution though unlikely).

1.5 Identify which journal would be used to record Doc. #99.

1 mark Cash payment journal. 1.6 List 3 separate types of transactions that may be recorded in the OUT column of the stock card.

3 marks

Transaction 1: Cash sales Transaction 2: Drawings of stock Transaction 3: Stock taken for advertising purposes 1.7 Stock is an asset. Provide a definition of an asset.

3 marks

A resource, under the control of the business, as a result of past events, that will provide economic benefits in the future. Examples include stock, computers and vehicle.

STOCK CARD: Leather Chairs

2027 IN OUT BALANCE

Date Details QTY. COST VALUE QTY. COST VALUE QTY. COST VALUE

1/9 Balance 11 1000 11000

3/9 Doc. #99 17 1000 17000

1.8 Calculate and record the total Bank value for November 2027 in the above journal. 1 mark

1.9 Indicate the impact of “Loan $1000” on the following accounting equation: 2 marks

Assets Liabilities Owners Equity

Increase cash $1000 Increase loan $1000

21

VCE Accounting Unit 3 1. Pre double-entry

1.10 How could you check or verify the accuracy of the cost of sales value of $4500? 2 marks

Check the stock cards: total of OUT columns excluding any non sale transactions. Refer back to original documentation, eg, sales receipts.

1.11 The cost of sales $4500 is an expense: explain why.

3 marks An expense leads to a decrease in owners equity, excluding drawings. Cost of sales leads to a decrease in owners equity and is not drawings so it fits the definition of an expense. (Could include reference to decrease in an asset, stock, that leads to a decrease in owners equity).

A B C

Reports Journals and stock cards

Transactions

Journals and stock cards Reports

Transactions

Transactions Journals and stock cards

Reports

1.12 Which of the above, A or B or C, best represents the order in a simple accounting system? 1 mark

C

1.13 Give 3 examples of „Reports‟. 3 marks

Report 1: Cash Flow Statement Report 2: Income Statement Report 3: Balance Sheet

The following transactions occurred during December 2028: Cash sales $3000 (cost of sales $900), paid wages $500, cash sales $4000 (cost of sales $1200), drawings of $1000, received ANZ loan $5000, paid advertising $900, purchased new computer $2500. 1.14 Calculate the net profit or loss for December. Show workings.

3 marks

Revenue: sales $3000 + $4000 = $7000. Expenses: cost of sales $900 + wages $500 + cost of sales $1200 + advertising $900 = $3500. Profit = revenue less expenses so profit = $3500.

STOCK CARD: Leather Brief Case

2028 IN OUT BALANCE

Date Details QTY. COST VALUE QTY. COST VALUE QTY. COST VALUE

1/6 Balance 40 200 8000

5/6 Rec. #75 7 200 1400 33 200 6600

10/6 Memo #13 1 200 200 32 200 6400

18/6 Rec. #76 10 200 2000 22 200 4400

28/6 Chq. #90 20 200 4000 42 200 8400

1.15 Work out the cost of sales for June 2028. 2 marks

OUT column (only sales transactions): $1400 + $2000 = $3400.

Date Journal?

5/6 Cash receipts

10/6 General

18/6 Cash receipts

28/6 Cash payments

1.16 Complete the following table to identify the relevant journal for each transaction.

2 marks

1.17 The last value in the stock card is $8400. Indicate how the manager would use this value at the end of June.

2 marks

To work out total value of stock on hand and then report that total in the Balance Sheet as an asset. (Note that leather brief case is only one type of stock traded).