vii role of the reserve bank in state finances

TRANSCRIPT

58

VIIRole of the Reserve Bank in

State Finances

1. Introduction

7.1 The Reserve Bank of India Act, 1934 providesthat the Reserve Bank, by agreement with any Stategovernment, shall be entrusted with all its money,remittance, exchange and banking transactions inIndia and the management of its public debt, and shallalso deposit all its cash balances with the ReserveBank, free of interest. Accordingly, the Reserve Bankis a banker to all the State governments, exceptSikkim. The Reserve Bank also manages the marketborrowings of all the States. The market borrowingprogramme of the State governments is finalised bythe Central government and the PlanningCommission, keeping in view the provisions of Article293(3) of the Constitution of India.

7.2 Apart from the statutorily mandatedobligations, the Reserve Bank constituted variousworking groups and committees to examine mattersrelating to State finances and to provide guidance toStates on institutional and policy reforms, such asconsolidated sinking fund, guarantee redemption

The Reserve Bank’s contribution towards shaping the State finances has progressively broadened beyond the statutory

ambit of being a banker and debt manager of the State governments. As a banker, the Reserve Bank has modulated the

system of Ways and Means Advances to and minimum balances from the States in consonance with their growing

requirements for short-term accommodation. Simultaneously, the overdraft regulations of States were made more

stringent to preserve short-term fiscal discipline and monetary stability. The Reserve Bank conducted market

borrowings through an administered system of pre-determined notified amounts of borrowings and coupons thereon

until 1998. Since then, the Reserve Bank has allowed States to access market borrowings through the auction route in

a graduated manner before eventually migrating to a full-fledged system of auction of State government securities

from 2006-07. Progressively, since the late 1990s, the Reserve Bank has been playing an advisory role whereby it

formulated model fiscal responsibility legislation for the States, thereby facilitating the introduction of the rule-based

medium-term fiscal consolidation in the States. The Reserve Bank has also been sensitising the States on policy issues

relating to fiscal sustainability. The Reserve Bank has been organising Conferences of State Finance Secretaries since

1997. These have provided a regular platform for interaction with officials of the Central government, the Reserve

Bank and other agencies on issues relating to State finances that emerge from time to time. The dissemination of

information and analysis of State finances by the Reserve Bank every year have become an important reference for not

only undertaking policy decisions but also facilitating research in this area.

fund, model fiscal responsibility bills, fiscaltransparency guidelines, and information disclosuresrelating to outstanding liabilities and guarantees.

7.3 Accordingly, this chapter presents theevolution of the Reserve Bank’s role as a banker, debtmanager and adviser on financial matters to the Stategovernments and its response to the challenges inthis area in terms of policy initiatives undertaken fromtime to time. Section 2 provides the legal frameworkunderpinning the Reserve Bank’s role as a bankerand debt manager of the States. Section 3 focuseson the challenges faced by the Reserve Bank duringthe evolution of its role as a banker and debt managerof the States from 1935-1990. Section 4 covers theperiod since 1990 when the Reserve Bank started toplay an important role in its advisory capacity onmatters relating to the fiscal position of the Stateswhile it became more active as a banker and debtmanager to State governments. Section 5 undertakesan overall assessment of the Reserve Bank’s role inState finances. Concluding observations are providedin Section 6.

59

Role of the Reserve Bank in State Finances

2. The Reserve Bank and State Finances: Legaland Institutional Underpinnings

7.4 The genesis of the Reserve Bank’s role inState finances dates to its inception in 1935. Theinterface between the Reserve Bank and the Statesstarted when the individual States entered intoagreements with the Reserve Bank. By the early1950s, the Reserve Bank took over the function ofserving as a banker to all the States (Section 21A ofthe Reserve Bank of India Act, 1934), whereby itundertakes all money, remittance, exchange andbanking transactions of the States in India includingholding their deposits, free of interest. Furthermore,the Reserve Bank assumed responsibility forproviding secured and unsecured Ways and MeansAdvances (WMAs)/Overdrafts (ODs) to the Stategovernments to meet temporary mismatches in theircash flows (Section 17(5) of the Reserve Bank of IndiaAct, 1934). The limits and the interest rates applicableon such advances are, however, not specified in theReserve Bank of India Act but are regulated byvoluntary agreements with the State governments.The State governments, in turn, are obliged tomaintain interest-free minimum balances in theiraccounts with the Reserve Bank, depending upon therelative size of their budgets and the level of economicactivities in their States. Currently, the Reserve Bankacts as a banker to all the State governments in Indiaexcept Sikkim. A notable feature, particularly sincethe introduction of fiscal rules in 2004-05, has beenthe reduction in fiscal imbalances of the States. Assmall saving collections autonomously built up thecash balances of the States while their deficits camedown, managing the surplus cash balances of theCentre emerged as a challenge.

7.5 The Reserve Bank has also been managingmarket borrowings of the States (under Section 21Aof the RBI Act) since its inception. Stategovernments are permitted to undertake onlydomestic borrowings upon the security of theConsolidated Fund of the State and within limits,

and they cannot raise any loans without the consentof the Central government so long as they areindebted to the Centre (Article 293 of theConstitution). Furthermore, the public debtmanagement comes under the ambit of theGovernment Securities Act, 2006, effective fromDecember 1, 2007.16 Currently, the Reserve Bankmanages the market debt of al l the Stategovernments (28 States) and the Union Territory ofPuducherry. As part of this responsibility, theReserve Bank decides the timing and issuingprocess, and disseminates details about the auctionof State government loans to the public andinvestors.The method of issuance of market loanshas migrated from the administratively controlledsystem to an auction based system for all the Statessince 2006-07. This was facil i tated by themoderation in fiscal imbalances, following variousinstitutional and fiscal reforms and the enactmentof Fiscal Responsibility and Budget Management(FRBM) Acts by the State governments since 2004-05. The Reserve Bank conducts auctions of States’borrowings to enable price discovery.

7.6 As part of its advisory role, the Reserve Bankhas been setting up several committees/workinggroups to examine issues concerning the Statefinances from time to time. The Reserve Bank alsoprovided inputs facilitating the introduction of a rule-based fiscal consolidation by the States. Besides,the Reserve Bank has been regularly organisingConferences of State Finance Secretaries whichprovide a platform for their interaction with seniorofficials of the Central government, PlanningCommission, Comptroller and Auditor General ofIndia (CAG), Controller General of Accounts (CGA),and the Reserve Bank on issues of mutual interest.The Reserve Bank compiles and disseminatesconsolidated and State-wise disaggregated data inits report on State budgets, which constitutes aprimary source of information on State finances forpolicymakers and researchers.

16 The Government Securities Act,2006 replaced the Public Debt Act,1944 and the Indian Securities Act,1920.

60

State Finances : A Study of Budgets of 2011-12

7.7 International experience suggests thatcountries have been using a mix of approachesfor appropriate management of sub-nationaldebt (Box VII.1). While in most countries centralgovernments play a major role, in India, theReserve Bank, being a full service central bank,

has played a unique complementary role byassisting the Central government in the adoptionof an appropriate combination of approaches todebt management that remains consistent with ajudicious balance between growth and macroeconomicstability.

Box VII.1: Approaches to Sub-national Debt Management: Cross-country Experiences

A growing trend worldwide is towards decentralised delivery ofgovernment services. Consequently, the expenditure obligations ofsub-national tiers of governments have risen without commensurategrowth in their own and devolved sources of revenue from the centralgovernment, thereby necessitating recourse to debt. Various studieshave emphasised the need for transparency in the finances of sub-national governments (SNG) through establishment of appropriateinstitutions and processes akin to the Central government system,so as to ensure better accountability, efficiency, and governance ofdecentralised administrations. Considering the implications of sub-national debt for overall macroeconomic stability, the centralgovernments across countries play a critical role in monitoring sub-national debt management (Ahmad, et al, 2005). In India, the ReserveBank plays a unique role of assisting the Central government to fulfillthese responsibilities by acting as the banker and debt manager ofState governments as well as providing advice on issues and concernsrelating to their finances from time to time.

Ter-Minassian (1996), in a cross-country survey, identified fourprincipal approaches to managing sub-national debt. At one extreme,there are countries (United States, Canada, Japan and Switzerland)with developed capital markets that have adopted a market disciplineapproach whereby the borrowing activities of SNGs are mainlymonitored and controlled by the market and/or regulated by local-level regulations. At the other extreme, there are countries (Lithuania,Columbia, Latvia, and Indonesia) which have imposed administrativeconstraints, whereby the Central government is empowered with directcontrol over sub-national borrowings through setting up debt limits,special treatment/prohibition of external borrowings, review andauthorisation of individual borrowing operations or centralisation ofall government borrowings with on-lending to SNGs. In India, whilethe States’ annual borrowing limits are decided by the Centre, theyhave been allowed to approach the market directly from 2006-07subject to their borrowings remaining within annual limits. However,for external borrowings, the States in India have to depend upon on-lending from the Centre, which passes on external assistance to theStates on a 'back-to-back' basis. Between the two extremes, thereare countries (Australia, Austria, Germany and Spain) that follow co-operative approach, whereby SNG borrowings are set as part of fiscaltargets and debt ceilings through a negotiation process betweenCentral and local governments. Finally, there are countries whichhave adopted rule-based controls on SNG borrowings imposed bythe Central/upper-tiers of government for the of purpose of borrowing(Germany, Italy, Mexico and South Africa) and numerical constraintsbased on parameters such as fiscal balance and expenditure(Germany, Italy, France and Brazil) and also debt (Spain, Peru,Lithuania and Poland). In India, the States were incentivised tolegislatively frame fiscal rules setting targets for revenue balanceand fiscal balance, which work towards controlling debt.

Cross-country practices show that countries have chosen acombination of these approaches for sub-national debt management.For instance, in principle, though market discipline can be an effectiveapproach, very few countries, particularly developing ones, can satisfythe stringent pre-conditions (free and open market, sufficient

information on borrower’s debt level and repayment capacity, absenceof bailout expectation in the event of default and strong marketsensitive institutional infrastructure). Even in Canada where provincesrely solely on market discipline and there are no constitutional/legallimits on their borrowings, there has been a mixed record. The marketdiscipline approach, which does not stipulate any limits on SNGborrowings, is also prone to risks of uninhibited accumulation ofprovincial debt as was the case in Brazil from the late 1960s to the1980s (IMF Survey, 1996). This necessitated a migration towards anadministrative approach by setting new legal rules and Central bankregulations that prohibit states from borrowing from their own banks.However, country experiences also support the need to accord primaryemphasis on the fiscal discipline of SNGs as, in its absence, Centralgovernment controls over SNG borrowings tend to be less effective.Therefore, Brazil also undertook various institutional reforms(enactment of fiscal rules, introduction of golden rule provisions, newaccounting norms and transparency requirements at all levels ofgovernment) that improved the effectiveness of its administrativeapproach for managing SNG debt. Other countries (Australia andScandinavian countries), where the culture of fiscal discipline isalready in place, have instituted co-operative arrangements involvingSNGs in formulating budgetary policies with due recognition ofassociated macroeconomic implications. The co-operative approachfacilitates exchange of information across the various tiers ofgovernment and improves communication. However, this approachmay be prone to protracted bargaining. Thus, some industrial countries(United States, Spain and Japan) have adopted rule-based controls.

Several lessons follow from the cross-country experiences on sub-national debt management. First, management of SNG debt cannotrely solely on a single institutional arrangement as none of theapproaches seem to be superior. Second, SNGs cannot be givenunconstrained borrowing authority. Typically, at low levels of verticalfiscal imbalances, the fiscal rules adopted by SNGs themselvesimprove fiscal outcomes. Widening of vertical imbalances requiresthe institution of Centrally imposed rules. Third, central governmentsneed to avoid bailing out SNGs wherever possible as they reducethe effectiveness of borrowing controls (Singh and Plekhanov, 2005).

References :

1. Ahmad, E, M. Albino-War and R. Singh (2005): ‘Subnational PublicFinancial Management : Institutions and MacroeconomicConsiderations’ IMF Working Paper, WP/05/108, InternationalMonetary Fund (IMF), June.

2. IMF (1996): ‘Deficit Reduction, Decentralisation Highlight Needto Manage Subnational Government Debt’, IMF Survey,November 25.

3. Singh, Raju and Alexander Plekhanov (2005): “How Should Sub-national Government Borrowing Be Regulated?’’ IMF WorkingPaper, WP/05/54, IMF, March.

4. Ter-Minnassian, Teresa (1996): ‘Borrowings by SubnationalGovernments: Issues and Selected International Experiences’,IMF Paper on Policy Analysis and Assessment PPAA/96/4, FiscalAffairs Department, IMF, April.

61

Role of the Reserve Bank in State Finances

3. Evolving Role of the Reserve Bank in the Pre-reform period (1935-1990)

7.8 The pre-reform period witnessed the ReserveBank taking over the responsibility for managing thepublic debt of the Central and State governments,besides playing the role of a banker in an environmentof underdeveloped financial system. With theincreasing participation of both the Central and Stategovernments in the process of planned economicdevelopment, their dependence on the Reserve Bankalso increased. At the start of the planning process,an abiding objective of the Reserve Bank as a banker,was to integrate the departmental treasury operationsof all the provinces/States into the banking system.The Reserve Bank also provided short-termaccommodation in the form of WMA to the States withthe limits usually set as a multiple of their minimumbalances held with the Reserve Bank. However, itrealised the need to keep a check on the tendency ofthe States to remain persistently in WMA/OD so asto guard against undue automatic monetisation ofdeficits as was the case for the Centre. As a debtmanager of the States, the Reserve Bank initially hadto underwrite States' borrowings. While the Stateswere keen to directly access the market to meet theirexpanding funding requirements, the Reserve Bankwas not only apprehensive about their capacity toraise funds directly from the market in view of thelimited clientele but also about its unintendedconsequences in terms of unco-ordinated andcompetitive borrowings by the States. The challengesfaced by the Reserve Bank in conducting itsresponsibilities on behalf of the State governmentsup to 1990 are set out below.

Deeper financial integration through Banker ofPart B States

7.9 Initially, the Reserve Bank served as a bankeronly to Part A States17. The imperative of expanding

the Reserve Bank’s role as a banker to all the Stateswas recognised by the V.T.KrishnamachariCommittee, 194918 for the following two reasons. First,handling the critical operations in respect of treasury,currency chest and remittance arrangements forStates in a country-wide manner provided scope indeepening the financial sector of the Indian economy.This, in turn, was required for fostering integration ofall the States across the Union. Second, the natureof currency and governmental banking facilities in theformer Part B States19 was found unsatisfactory, andhence, was identified to be addressed closely as aprelude to future reforms. Accordingly, the RuralBanking Enquiry Committee, 1950 (Chairman:Purshotamdas Thakurdas) recommended that theReserve Bank may be permitted to operate as solebanker to Part B States as well, whose bankingactivities were either performed departmentally or bythe Imperial Bank of India/local banking institutions.The Central government took the initiative foramending the Reserve Bank of India Act, 1934 toenable it to become the banker to Part B States afterexecuting agreements with them. Supporting thisview, the Reserve Bank argued that, according to theinternational practice, central banks function asbankers to the government. It was pointed out thatthis arrangement, apart from being economical andconvenient, was required for having an intimateconnection between public finances and monetaryaffairs. This also enabled the central bank to assessfinancial situation at any point of time in a wholesomemanner, so as to appropriately advise the government.

7.10 Some Part B States were, however, not keenon this arrangement; they felt that they would be losinga number of accommodation facilities being offeredby their prevailing bankers, including the interest theyearned on their cash balances maintained with theseinstitutions which they would cease to earn once theReserve Bank becomes their banker. While the

17 Part A States refer to nine States which were provinces of British India.18 As referred in Balachandran G. (1998), The Reserve Bank of India 1951-1967, pp:185, Oxford University Press, Delhi.19 Part B States refer to eight States which were former princely States.

62

State Finances : A Study of Budgets of 2011-12

Central government advised Part B States in 1951 toappoint the Reserve Bank as their banker by April ofthe following year, the target date was subsequentlyshifted to July. Eventually, it was decided that someof these States can make their prevailing bankersserve as agents of the Reserve Bank under ‘suitablesafeguards’. Thus, the process started, with thegovernments of Madhya Bharat, Travancore-Cochin,Mysore and Hyderabad appointing the Reserve Bankas their banker during the curse of 1952-53.

Conflict between financial integration andmonetary stability due to huge overdrafts by theStates

7.11 The Reserve Bank stipulated and revisedupwards the levels for the interest free minimumbalances of the States during the pre-reform period,based on certain indicators reflecting expansion inState finances relative to benchmark periods. At thesame time, it also had to grant Ways and MeansAdvances (WMAs) to the States within specified limitslinked to minimum balances to tide over temporaryliquidity mismatches in revenues and expenditures.Originally, in April 1937, both the limits of minimumbalances and WMAs of States were fixed at the levelequivalent to the ratio of their total revenue andexpenditure to the corresponding total of the Centrefor the period 1931-32 to 1933-34. Although theWMAs were repayable after three months, the lawdid not prevent renewals of WMAs after the stipulatedperiod. Nonetheless, the Reserve Bank preferred notto allow such renewals. After the smooth working ofthe WMA system until 1948, there were severalinstances when the States were unable to repay evenafter being called upon by the Reserve Bank. Someof them also started running large overdrafts (ODs)on their accounts with the Reserve Bank from 1950.As the States were virtually able to draw amounts fromthe Reserve Bank, the State Bank of India branchesand the treasuries, without any evident limit, it wasrecognised that such unregulated financing of budgetdeficits by States could pose concerns for monetarystability.

7.12 With the increasing cost of managing thegovernment accounts, following the rising turnover inthese accounts, a need for an upward revision in theminimum cash balances, which had remained fixedat 1937 levels. Furthermore, it was noticed that withinterest rate downturn, the Reserve Bank’s annualearnings from investment of these balances fell farshort of commissions it paid to agency banks of theStates. Although the Reserve Bank proposed toquadruple the aggregate minimum balances of theStates, the Central government only permitteddoubling of the existing limit of aggregate minimumbalances to avoid pressure on the States’ resources.On the other hand, WMA limit was quadrupled,thereby raising the ratio of WMA limit to minimum cashbalance from 1:1 to 2:1 in 1953. Moreover, in additionto ‘normal’ WMA which was unsecured, each Statewas allowed to draw a ‘special’ WMA up to ̀ 20 millionagainst Central government securities.

7.13 The problem of States’ overdrafts re-emerged and escalated by the mid-1960s on theback of deterioration in States’ fiscal conditions dueto dwindling revenues, on the one hand, and asharp increase in drought relief expenditures, onthe other. Some States even began using overdraftsas ‘Plan resources’. The fiscal position of the Centrewas also adversely impacted, as the States’overdrawn accounts began to be settled throughCentral assistance to them. With the Centreenjoying the facility of automatic monetisation ofCentral government deficit through issue of ad hoctreasury bills to the Reserve Bank, the practice ofsettling States’ ODs by the Centre through specialassistance was tantamount to de facto unbridledmonetisation of even the States’ deficits,notwithstanding the fact that State governmentborrowings from the Reserve Bank were subject tostipulated limits.

Overdraft Regulation aimed at stricter financialdiscipline

7.14 State governments recorded large budgetarydeficits as their outlays surged since the beginning ofthe Third Five-Year Plan. These deficits were financed

63

Role of the Reserve Bank in State Finances

seven working days. The WMA limits to States weredoubled to provide them with sufficient room tomanage their financial commitments within theavailable resources. However, the ODs continued,which led the Centre to clear the States’ outstandingamount of ODs again at end-March, 1982 by grantingterm loans, advance release of the States’ share inCentral assistance and taxes, while deciding to rigidlyenforce the OD regulation scheme thereafter. TheWMA limit was doubled from July 1, 1982, recognisingthe increased budgetary expenditure of the States.

Enhancement in WMA, OD in the wake of drought

7.17 The fiscal conditions of the States worsenedduring the 1980s, with drought conditions impactingrevenue collections while their expenditures grew.Consequently, the States continued to overdraw theiraccounts with the Reserve Bank, which had to becleared by the Centre through medium-term loans.The WMA limits were enhanced during 1986-87.Consequent to another drought during 1987-88, whichaffected the liquidity position of several States, theReserve Bank further enhanced the limits for normalWMA in March 1988. Nonetheless, as fiscal stress inthe States continued in the 1990s, the time limit forclearing ODs was raised (from seven to tenconsecutive working days) in November 1993, andlimits under normal and special WMA were furtherdoubled in August 1996.

Gradual upward revisions in minimum balancesand sharper hikes in WMA in consonance withgrowing stress in State Finances

7.18 As already mentioned, the minimum balanceswere periodically revised by the Reserve Bank duringthe pre-reform period, in the light of expansion in theState finances relative to benchmark periods.Beginning with a stipulated minimum balance levelof `19.5 million for Part A States in April 1937, theReserve Bank enhanced the level to `39.4 million forall States in April 1953 when its role as a banker wasextended to Part B States as well. The stipulatedminimum level was increased gradually to ̀ 133 millionin 1996. Up to August 1996, minimum balances were

to a large extent by recourse to ODs from the ReserveBank. To avoid persistence of this situation, theReserve Bank, with the approval of the Centralgovernment, evolved a new procedure to deal withsuch ODs beyond approved limits with effect fromMarch 1, 1967. With ODs becoming a serious problemby the end of the Third Plan, this issue was examinedby the Fifth Finance Commission. The Commissionnoted that the recourse to ODs by the States reflectedan uneven pattern of their receipts and expenditures,and attributed it to chronic imbalances betweensources of funds and functions of the States whiledevolution of resources to them remained inadequateand no suitable mechanism was present to deal withunforeseen difficulties. At the same time, theCommission recommended continuous monitoring bythe Reserve Bank so that the stipulated three-monthperiod of WMA was not exceeded, the notice periodwas not violated in case of an OD, and paymentswere stopped if States failed to comply with the notice.

7.15 With the OD position becoming a concern dueto its effects on the financial stability of the economy,a new policy on ODs came into force from May 1,1972, whereby no State government could resort tounauthorised borrowing from the Reserve Bank.However, to meet the genuine needs of the Statesarising out of their increased budgetary operations,the limits of clean or unsecured WMAs from theReserve Bank were raised to four-times their earlierlimits. The outstanding ODs on the Reserve Bank’saccounts on that date were cleared by the Centregranting special ways and means assistance andreleasing the States’ share in income tax and planassistance. These measures were expected to impartconsiderable financial discipline by containing bothPlan and non-Plan expenditures of the States withinthe constraints of the available resources.

7.16 As a measure to tightly regulate ODs, a systemwas put in place from October 1, 1978, whereby theReserve Bank would caution the State after itexhausted 75 per cent of the authorised WMA limitand automatically suspend the payments if, despitesuch action, the account was overdrawn for more than

64

State Finances : A Study of Budgets of 2011-12

revised upwards on 11 occasions, taking into accountexpansion in State finances and formation of newStates from time to time. The pace of upward revisionof stipulated minimum balances to be maintained bythe States, however, lagged behind the upwardrevisions in their WMA limits. Thus, the ratio betweenminimum balance and the normal WMA limit workedout to 1:168 in August 1996 as compared with 1:1 in1938. The Special WMAs began to be linked tominimum balances from March 1967. The ratiobetween minimum balances to Special WMA worked

out to 1:64 in August 1996 as compared with 1:6 inMarch 1967 (Table VII.1).

Interest Rates on WMA and ODs made moreprogressive to restrain use of temporary advancefrom the Reserve Bank as a normal budgetaryresource

7.19 The interest rates on normal and specialWMAs, and ODs did not exceed the Bank Rate beforeMay 1976. In particular, interest rates on normal WMAand ODs were kept at one per cent below the Bank

Table VII.1: Minimum Balances and Limits of WMAs(Amount in ` million)

Date Minimum Balance Ways and Means Limits (Expressed asTotal for States a Multiple of the Minimum Balance)

Normal / Clean Special / Secured

1 2 3 4

1. April 1, 1937 (effective 19.5 1 #April 1, 1938) Provincial (19.5)Governments/Part A States)

2. April 1, 1953 (Part A andPart B States) a) 39.4 on Friday 2 20.0 for each State

b) 33.8 on days other than Friday (78.8)c) 45.0 before repayment of

Ways and Means Advances3. March 1, 1967 62.5 3 6

(187.5) (375.0)4. May 1, 1972 65.0 + 12 6

(780.0) (426.6)5. May 1, 1976 130.0 10 10

(1300.0) (1300.0)6. October 1, 1978 130.0 20 10

(2600.0) (1300.0)7. July 1, 1982 130.0 40 20

(5200.0) (2600.0)8. October 1, 1986 52 20

a) April-September 130.0 (6760.0) (2600.0)b) October-March 130.0 48 20

(6240.0) (2600.0)9. March 1, 1988 133.0 56 20

(7448.0) (2660.0)10. November 1, 1993 133.0 84 32

(11172.0) (4256.0)11. August 1, 1996 133.0 168 64

(22344.0) (8522.0)12. March 1, 1999 ## ## (36850.0) ++

Figures in parentheses in Columns 3 and 4 are the total monetary limits for all States.# : Secured ways and means advances were occasionally granted on an ad hoc basis.+ : The increase of `2.5 million over the figure for 1967 was due to the fixation of minimum balances for four States, viz., Himachal

Pradesh, Manipur, Meghalaya and Tripura. There was no revision for other States.## : The minimum balance was revised upwards, linking it to the same base as for WMA. The base for the revised WMA limits will be the

three-year average of revenue receipts plus capital expenditure.++ : The limit for special WMA was liberalised; no upper limit on Special WMA. Special WMA was to be provided against actual holdings of

Government securities.Source: Informal Advisory Committee on Ways and Means Advances to State Governments, Reserve Bank of India, 1999.

65

Role of the Reserve Bank in State Finances

Rate and at the Bank Rate, respectively. The interestrate on special WMAs, after having a graduatedstructure based on the size of the advance, was madeuniform and equal to the interest rate of normal WMA,i.e., one per cent below the Bank Rate, betweenMarch 1967 and April 1976. However, from May 1976to August 1996, a graduated scale of interest rateswas charged based on the duration of the advanceto discourage states from using the WMA as a normalbudgetary resource. While interest rates on specialand normal WMAs continued to remain equal, theybecame progressively based on the duration of useof the WMA facility. While the interest rate of normaland special WMA up to 90 days was kept unchangedat one per cent below the Bank Rate, higher interestrates (up to two per cent above the Bank Rate) wereapplied when these advances were availed of beyondthe 90-day period. In respect of ODs, while the interestrate up to seven days was kept unchanged at theBank Rate, it was raised to three per cent above theBank Rate for ODs of 8-10 days, reflecting sharperprogressivity and the need to address the problem ofthe States' ODs during this period.

Ensuring success of States borrowingprogramme primarily through Reserve Bank’sunderwriting system in the initial period

7.20 The Reserve Bank continued to undertakeresponsibility for the management and issue of debtof the provinces even after their legislatures weregranted autonomy to do the same in 1937. Theprovinces delayed enacting the laws that wouldenable them to issue and manage debt on their own,pending lack of clarity about whether their legislaturescould bypass the power granted to the Reserve Bankin this regard. Furthermore, under the British laws,the prevailing system of the Reserve Bankundertaking debt management of the provinces hadto continue till their legislatures were found‘competent’ to take over this responsibility. The systemremained in force even after the Republic’sinauguration in 1950. Initially, the Reserve Bankfollowed the practice of underwriting provincial loans.

Some States, however, felt that this system preventedthem from coming directly to the market through‘straight public issues’ and advocated that they shouldbe allowed to access the market directly to mobilise‘realistic amounts’ at ‘reasonable rates’. Althoughsome views favoured discontinuing the system ofunderwriting State loans and arrangements were alsomade for the State governments to float ‘straight loansin the market’, the Reserve Bank had to ensure thesuccess of the market borrowing programme of theStates, in case public subscriptions fell short of theissued amounts in the early 1950s.

Balancing the States’ aggressive approach formarket loans with imperatives of sound monetarymanagement and absorptive capacity of investors

7.21 Amidst the easing of monetary conditionsduring the latter half of the 1950s and the dearth ofState loans, the market response to State borrowingsimproved, which drove down the coupon rates. Thesuccess of State loans prompted the Reserve Bankto consider lengthening the tenor and narrowing thespreads between State and Central loans. TheReserve Bank, however, cautioned against the Statesagainst pressurising involuntary subscriptions.Another concern, notwithstanding a positive marketresponse, emerged in the wake of reports thatcommercial banks were financing their subscriptionsto State loans through borrowings from the ReserveBank and the State Bank of India. During the ThirdFive-Year Plan, States adopted aggressive practicesto mobilise funds from the market by paying highercoupon rates and accepting deposits from potentialsubscribers/investors even before the loan issuancedate. However, as the policy stance becamedisinflationary by the mid-1960s, the Reserve Bankcould not extend any support to State loans in keepingwith its overall responsibility of sound monetarymanagement. With the State loans being under-subscribed against the backdrop of lack of supportfrom the Reserve Bank and weak investor appetite,the States were persuaded to set modest targets atmore attractive terms to investors.

66

State Finances : A Study of Budgets of 2011-12

Deterioration in State finances and growingrecourse to captive institutional investor base

7.22 The fiscal conditions of the States improvedfrom the mid-1970s to the mid-1980s as they recordedsurpluses in their revenue account in the wake ofimproved buoyancy in both own tax and non-taxrevenues, while revenue expenditures increasedmoderately. State government securities generallyhaving a maturity of 10 to 15 years were issued atcoupon rates slightly higher than the coupon rates ofcomparable maturities of Central governmentsecurities. A rising proportion of State governmentsecurities were held by commercial banks, followedby the Life Insurance Corporation of India andProvident Funds. The Reserve Bank did not subscribeto the State government securities during this period.

7.23 The fiscal conditions of the States, however,deteriorated significantly from 1987-88, with therevenue account turning into deficit on account ofdroughts/floods, which not only entailed additionalexpenditure on relief work but also affected States'revenue collections. There was also a sharpdeterioration in the financial performance of Statepublic enterprises with a bearing on the finances ofStates. The implementation of the revised paystructure across States also contributed todeterioration in the fiscal position of the States duringthe late 1980s. Reflecting the impact of the increasingrecourse to borrowed funds by the States, interestpayments shot up, pre-empting 11.0 per cent of theirrevenue receipts during the second half of the 1980sas compared with 8.1 per cent during 1980-85. A fewStates curtailed their plan outlays to contain fiscaldeficits. The co-existence of both revenue and grossfiscal deficits during the second half of the 1980simplied that a large portion of borrowing was used tomeet the revenue gap. As a result developmentprospects suffered and debt accumulated. It may benoted that the Central government’s revenue andfiscal deficits had also expanded significantly duringthe 1980s, leading to the enlargement of debtservicing obligations. To contain the bulging debtservicing obligations, the Central and State

governments tapped the financial surpluses of thehousehold sector through statutory pre-emptionsstipulated for financial intermediaries at lower thanmarket clearing rates. Mandatory investments ingovernment and other approved securities by banksunder the statutory liquidity ratio (SLR) requirementwas steadily raised from 26 per cent of their netdemand and time liabilities in 1970 to 38.5 per centin 1990.

4. Role of the Reserve Bank in the Post-ReformPeriod since 1990

7.24 The unsustainable level of fiscal deficits of theCentre and State governments during the 1980seventually triggered a balance of payments crisis bythe early 1990s, necessitating fiscal reforms as a pre-condition for restoring macroeconomic balances inthe Indian economy. As fiscal adjustments occurredinitially at the Central government level, the ReserveBank reduced the statutory pre-emption ratios of thebanks, introduced the auctioning system in the Centralgovernment securities market and phased outautomatic monetisation of the Centre’s fiscal deficitsby 1997-98. The deterioration in State finances,however, persisted up to the mid-1990s. The situationbecame acute during the second half of the decade,following the implementation of the Fifth PayCommission awards for State government employeesand significant losses incurred by State Public SectorUndertakings. The fiscal deterioration of States wasfurther exacerbated by the growing size of interestpayments, the inability to levy adequate user chargesand falling buoyancy in Central transfers to States.While the focus of fiscal reforms was initially on theCentral government finances, the continueddeterioration of State finances prompted the ReserveBank to play a more proactive role in institutingreforms at the State government level by the late1990s.

7.25 As part of its proactive approach to Statefinances during the post-reforms period, the ReserveBank assumed responsibilities beyond its traditionalrole of serving as a banker and debt manager to the

67

Role of the Reserve Bank in State Finances

States. Among its several initiatives, the ReserveBank examined the implications of States’ contingentliabilities/guarantees on their finances and set upfunds to build cushions for repayments of loans andguarantees. It also played an active role in designing‘Model Fiscal Responsibility Legislation’ for theStates, which paved the way for the introduction offiscal rules at the State government level under theirFRBM Acts. Several of these initiatives were theoutcome of intensive discussions at the interactiveplatform provided by the Reserve Bank in theform of Conference of State Finance Secretaries.Various facets of the Reserve Bank’s role in Statefinances during the post-reform period are discussedbelow.

Volume of Budgetary Transactions becomesdeterminant of stipulated level of minimumbalances and normal WMA Limits

7.26 The Reserve Bank revised the WMA Schemefor the State governments from time to time, takinginto account their fiscal situation, financial andinstitutional developments, and the objective of co-ordinating monetary and fiscal policies. Thepersistent recourse to WMAs/ODs by the Statesnecessitated re-examination of the practice of linkingnormal WMA limits to stipulated levels of minimumbalances, when the latter had remained unchangedsince 1976. Persistent WMAs reflected acombination of liquidity mismatches and underlyingstructural imbalances. The Informal AdvisoryCommittee on Ways and Means Advances,1999(Chairman: Shri B.P.R. Vithal) (Vithal Committee)noted that the size of WMA expressed as a multipleof minimum balances did not capture the differingneeds of the States as evident from the size of theirbudgetary transactions. Accordingly, the VithalCommittee recommended that the normal WMAlimits be linked to the sum of revenue receipts andcapital expenditure. It also recommended increasingthe level of minimum balances by linking it to thesame base as was applicable to normal WMA limits,albeit with a lower ratio. These recommendations

were accepted by the Reserve Bank. As the Statescontinued their demand for a higher quantum ofWMAs, normal WMA limits were further revisedupwards by a similar magnitude across non-specialand special category States based on therecommendations of the Informal Group of StateFinance Secretaries in 2001 and 2002. It may,however, be noted that while the minimum balancesof the States continued to remain at the absolutelevel stipulated by the Vithal Committee, the normalWMA limits were revised over the years.Subsequently, the Advisory Committee on WMA toState governments (Chairman: ShriC.Ramachandran, 2003) pointed out that theinclusion of capital expenditure in the base for linkingnormal WMA limits caused distortions. It, therefore,recommended linking of normal WMA limitsexclusively to revenue receipts, as this proxyindicator was considered relatively transparent,simpler to calculate and also a proper measure ofthe repayment capacity of the States. Accordingly,its recommendations were accepted (Table VII.2).

7.27 The year 2004-05 marked a turning point inState finances against the backdrop of theincentivised process of rule-based fiscalconsolidation at the State government level, guidedby the recommendations of the Twelfth FinanceCommission (TwFC) and the implementation of theDebt Swap Scheme (DSS). In the wake of improvedState finances, the Advisory Committee to reviewthe WMA Scheme (Chairman: Shri M. P. Bezbaruah,2005) recommended that total expenditure could beused as the base for fixing normal WMA limits forrevenue surplus States. Total expenditure was foundto be a suitable proxy to capture total budgetarytransactions, which would not be affected bycomputational differences in classifying capitalexpenditures across States. The total expenditurewas to exclude repayments, lottery expenditure andone-time ad hoc expenditure. For States that had arevenue deficit, the Committee recommended thatthe base should also exclude the revenue deficit.

68

State Finances : A Study of Budgets of 2011-12

Table VII.2: Salient Features of WMA Scheme of the State Governments

Item Just Prior to Vithal Group of Ramachandran BezbaruahVithal Committee Committee Finance Secretaries Committee Committee(1998) (1999) (2002) (2003) (2005)

Methodology forComputation of Limit

Aggregate NormalWMA Limits

i) Non-SpecialCategory States

ii) Special CategoryStates

Rate of Interest

Special WMA

Computation of limits(Margin)

Rate of Interest

Use of SpecialWMA

No. of consecutiveWorking Days aState can be underOD (excludingholidays)

Expressed 168 times theminimum balances of theStates

`22.34 billion

`20.33 billion

`2.01 billion

Bank Rate

Limits were placed at 64times the minimumbalances

Bank Rate

This is availed of afterNormal WMA

10

Average ofrevenue receiptsand capitalexpenditure of thelatest three yearsmultiplied by aratio of 2.25 fornon-specialcategory Statesand 2.75 forspecial categoryStates

`39.41 billion

`35.89 billion

`3.52 billion

Bank Rate

15 per cent*10 per cent**

Bank Rate

This is availed forafter Normal WMA

10

Average of revenuereceipts and capitalexpenditure of the latestthree years multiplied by aratio of 2.4 for non-specialcategory States and 2.9 forspecial category States

`60.35 billion

`53.85 billion

`6.50 billion

Bank Rate

15 per cent*10 per cent**

Bank Rate

This is availed of afterNormal WMA

12

Average of onlyrevenue receipts oflatest three yearsmultiplied by a ratio of3.19 for non-specialcategory States and3.84 for specialcategory States

`71.70 billion

`64.45 billion

`7.25 billion

Bank Rate for theperiod of 1-90 daysand 1 per cent abovethe Bank Rate for theperiod beyond 90days.

5 per cent uniformly

1 per cent below theBank Rate

To be availed ofbefore utilising NormalWMA limit

14

Multiplying ratios of3.1 per cent and4.1 per cent to theaverage of the total(revenuepluscapital expenditureexcludingrepayments andadjusted foronetimead hocexpenditures andlottery expenditure)expenditure forthe three years inrespect of Non-Special CategoryStates and SpecialCategory States,respectively aState has revenuedeficit, the baseshould excludethe revenuedeficit.

`98.75 billion @

`88.20 billion @

`10.55 billion @

Repo Rate for theperiod of 1-90 daysand 1 per centabove the RepoRate for the periodbeyond 90 days.

5 per cent uniformly(no change)

1 per cent below theRepo Rate

To be availed ofbefore NormalWMA

14 (No change)

Overdraft Regulation Scheme

69

Role of the Reserve Bank in State Finances

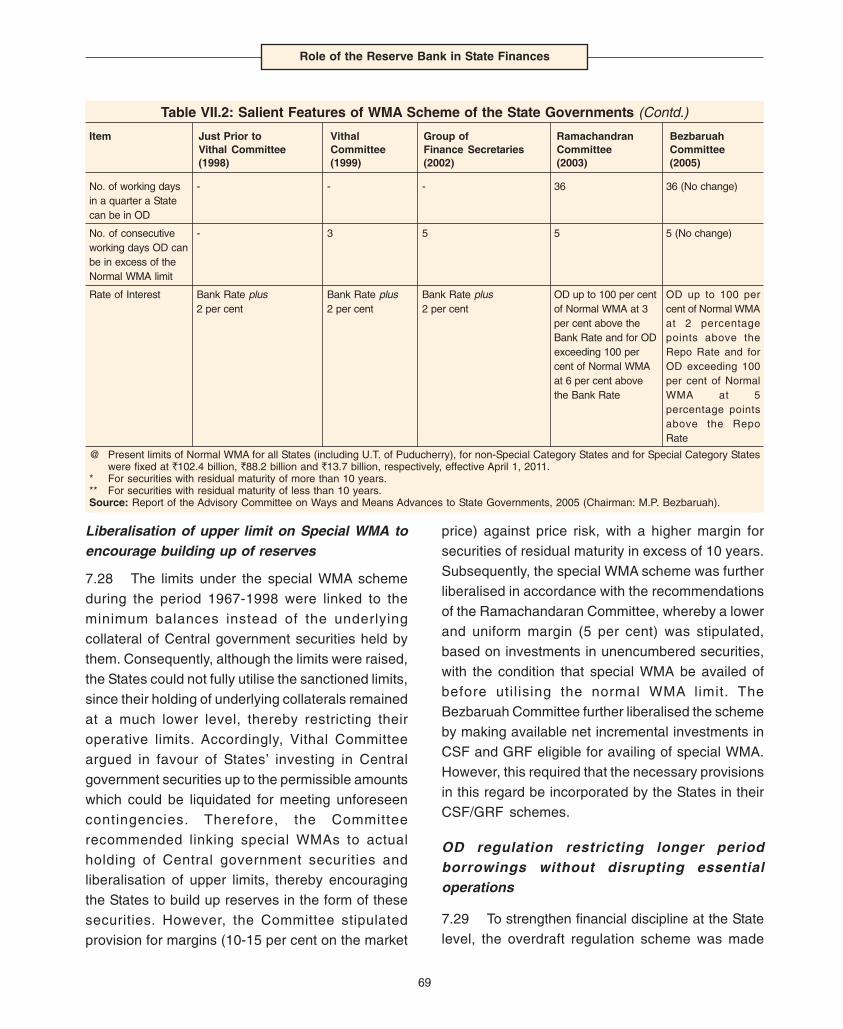

Liberalisation of upper limit on Special WMA toencourage building up of reserves

7.28 The limits under the special WMA schemeduring the period 1967-1998 were linked to theminimum balances instead of the underlyingcollateral of Central government securities held bythem. Consequently, although the limits were raised,the States could not fully utilise the sanctioned limits,since their holding of underlying collaterals remainedat a much lower level, thereby restricting theiroperative limits. Accordingly, Vithal Committeeargued in favour of States’ investing in Centralgovernment securities up to the permissible amountswhich could be liquidated for meeting unforeseencontingencies. Therefore, the Committeerecommended linking special WMAs to actualholding of Central government securities andliberalisation of upper limits, thereby encouragingthe States to build up reserves in the form of thesesecurities. However, the Committee stipulatedprovision for margins (10-15 per cent on the market

price) against price risk, with a higher margin forsecurities of residual maturity in excess of 10 years.Subsequently, the special WMA scheme was furtherliberalised in accordance with the recommendationsof the Ramachandaran Committee, whereby a lowerand uniform margin (5 per cent) was stipulated,based on investments in unencumbered securities,with the condition that special WMA be availed ofbefore util ising the normal WMA limit. TheBezbaruah Committee further liberalised the schemeby making available net incremental investments inCSF and GRF eligible for availing of special WMA.However, this required that the necessary provisionsin this regard be incorporated by the States in theirCSF/GRF schemes.

OD regulation restricting longer periodborrowings without disrupting essentialoperations

7.29 To strengthen financial discipline at the Statelevel, the overdraft regulation scheme was made

Table VII.2: Salient Features of WMA Scheme of the State Governments (Contd.)

Item Just Prior to Vithal Group of Ramachandran BezbaruahVithal Committee Committee Finance Secretaries Committee Committee(1998) (1999) (2002) (2003) (2005)

No. of working daysin a quarter a Statecan be in OD

No. of consecutiveworking days OD canbe in excess of theNormal WMA limit

Rate of Interest

-

-

Bank Rate plus2 per cent

-

3

Bank Rate plus2 per cent

-

5

Bank Rate plus2 per cent

36

5

OD up to 100 per centof Normal WMA at 3per cent above theBank Rate and for ODexceeding 100 percent of Normal WMAat 6 per cent abovethe Bank Rate

36 (No change)

5 (No change)

OD up to 100 percent of Normal WMAat 2 percentagepoints above theRepo Rate and forOD exceeding 100per cent of NormalWMA at 5percentage pointsabove the RepoRate

@ Present limits of Normal WMA for all States (including U.T. of Puducherry), for non-Special Category States and for Special Category Stateswere fixed at `102.4 billion, `88.2 billion and `13.7 billion, respectively, effective April 1, 2011.

* For securities with residual maturity of more than 10 years.** For securities with residual maturity of less than 10 years.Source: Report of the Advisory Committee on Ways and Means Advances to State Governments, 2005 (Chairman: M.P. Bezbaruah).

70

State Finances : A Study of Budgets of 2011-12

stringent over the years through restrictions such asstopping payments in case the State remains in ODbeyond the stipulated number of working days.However, in the 1990s, considering therepresentations from certain State governments,the Reserve Bank had enhanced the periodfor which a State government could run ODso that the essential operations of the Statesdo not get unduly disrupted. Nonetheless, theAdvisory Committees on WMAs/ODs continuedto work towards stipulating new restrictions tocheck the extent and frequency of States’recourse to ODs so that the use of OD by theStates remains under control. Accordingly, theadditional stipulation relating to the number ofconsecutive working days that States can remain inOD in excess of normal WMA limits as well as thepermissable number of days for ODs during a quarterwere introduced.

Move towards Interest Rates more reflective ofshort-term market conditions and policy rates

7.30 The interest rates on WMA (both special andnormal) and OD were protected from changes in theBank Rate by varying their spreads over the Bankrates during the late 1990s. Subsequently, in orderto use interest rate as a deterrent for persistentWMA, the interest rates on normal WMA wereapplied on a graduated scale and were chargedbased on the duration of the advance, with normalWMA beyond 90 days attracting a rate higher thanthe Bank Rate. The interest rates in respect of ODswere charged based on the magnitude of theseadvances and their spreads over the Bank Rate weremade more progressive. On the other hand, theinterest rate on special WMA was lowered below theinterest rate on normal WMA to encourage the Statesto build up reserves in the form of investment inCentral government securities. With the repo ratebecoming an indicator of short term policy rate andmore reflective of market conditions, the interestrates on WMA (normal and special)/ODs were linkedto the repo rate.

Transition in liquidity positions of States fromdeficit to surplus cash balances pose newchallenges to monetary management

7.31 The commencement of a rule-based fiscalconsolidation from 2004-05 onwards engendered ashift in the short-term liquidity position of the Stategovernments. The improvement in State governmentfinances was due to several factors. First, theincentivised fiscal roadmap recommended by theTwFC made the States eligible for availing the DebtConsolidation and Relief Facility (DCRF) scheme asand when they enacted their FRBM Acts. Second,the Debt Swap Scheme (DSS), operative between2002-03 and 2004-05, helped the States to swap theirhigh cost debt owed to the Central government withlow cost market borrowings/NSSF so as to benefitfrom the interest rate downturn. Third, pensionexpenditures of the States also moderated reflecting,inter alia, the implementation of the new pensionscheme by most of the States. Fourth, tax buoyancyof the States – both own taxes and tax devolutionfrom the Centre – improved, supported by theacceleration in economic growth. The improvementin States’ own tax buoyancy was further aided by theimplementation of VAT in lieu of sales tax. Thesefactors enabled a turnaround in the revenue accountfrom a deficit to a surplus position by 2006-07, bothat the consolidated level as well as at the individualstate level for most States. This improvement inrevenue account of the States coincided with largeautonomous inflows from NSSF collections, resultingin an accumulation of cash balances by the States asopposed to their earlier practice of taking frequentrecourse to WMAs/ODs to meet their expenditurerequirements. The cash balances of the Statescontinued to build up since 2004-05, despite a shortfallin NSSF inflows in 2007-08 and 2008-09, reflectingthe tendency of States to avoid recourse to WMAs/ODs. The surplus cash balances of the States stoodat `852 billion as at March 11, 2012. These cashbalances get automatically invested in the Centralgovernment’s 14-day intermediate treasury bills aswell as in auction treasury bills (ATBs) where States

71

Role of the Reserve Bank in State Finances

are non-competitive bidders, without any ceilings/limits. Consequently, there is a spillover of the surplusposition of the States to the liquidity position of theCentre. The build-up (and volatility) of the Centralgovernment’s cash surplus, in turn, reflects theunintended absorption of liquidity from the bankingsystem which poses a challenge to the ReserveBank’s monetary management. The ThFC, therefore,advised the State governments to first utilise their cashbalances before taking recourse to fresh borrowings,to finance their deficits so as to reduce the interestburden. Nonetheless, as advised by the ReserveBank from time to time, there is no substitute foradopting an effective forecasting and monitoringmechanism of cash flows by the States to addressthe issue of negative carry20 on their surplus cashbalances.

Focus on greater market access for resources:Sequential Evolution of Market borrowings

7.32 The Reserve Bank’s conduct of marketborrowings of State governments has evolvedsequentially from a completely administered system(traditional tranche method) prevailing till 1998,whereby the market borrowings of all the States weregenerally completed during the year in two or moretranches through issuances of bonds with pre-determined coupon and pre-notified amounts for eachState. During 1998-99, the States were permitted toaccess the market individually through the auctionmethod (with a predetermined notified amount butwithout predetermined coupons) to raise between 5-35 per cent of allocated market borrowings, or thetap method (with predetermined coupons but withouta predetermined notified amount), thereby providingscope for better managed States to raise resourcesat market rates. Nonetheless, some States continuedto prefer the traditional tranche method. To addressthe risk of under-subscription faced by some States,‘umbrella tranche’ method was introduced during2001-02, whereby the total targeted amount at pre-determined coupons was indicated without notifying

the amounts for individual States. The limit for utilisingthe auction option was raised to 50 per cent in 2002-03, before the States were eventually allowed to raisetheir entire market borrowings through auctioning ofState Development Loans (SDLs) from 2006-07. Afterhaving a system of fixed coupon spreads (raised from25 basis points to 50 basis points in 2001), thecomplete switchover to the auction system enabledthe market determination of spreads.

Operation of Debt Swap Scheme enabledsubstitution of existing high cost loans with freshlow cost market borrowings and small savings

7.33 In view of the mounting interest burden andalso to supplement the efforts of States towards fiscalmanagement, the Central government formulated theDSS allowing States to prepay the high cost loansfrom the Central government, contracted at interestrates of 13 per cent and above, through the low costborrowings such as small savings and market loans.Accordingly, these loans were swapped throughadditional market borrowings (allocated under theDSS in addition to the normal borrowing allocationsof the States) and net small savings proceeds at theprevailing administered interest rates, over a periodof three years ending in 2004-05. The total debtswapped during 2002-03 to 2004-05 amounted to`1,020.34 billion, of which `535.66 billion (52.5 percent) was swapped through additional marketborrowings at interest rates below 6.5 per cent, i.e.,at less than half the earlier cost.

Introduction of innovative practices aimed atwider base of investors and reduction in cost ofborrowings

7.34 During recent years, for the States' debtmanagement the Reserve Bank has enabled the useof various innovative practices aimed at minimisinginterest burden and widening the investor base forState government securities. Towards effective cashmanagement, the Reserve Bank introduced the buy-back scheme for State government loans. Under the

20 The rate of discount on ITBs is one per cent less than Bank Rate, which is lower than the interest paid out on market borrowings and smallsavings.

72

State Finances : A Study of Budgets of 2011-12

Scheme, States were allowed to prepay theiroutstanding SDLs through buy-back auctions toreduce their future coupon payment liabilities. Thebuy-back auctions were conducted for two StateGovernments during 2006-07. Second, to widen thescope of participation of retail investors in SDLs, thenon-competitive bidding facility was introduced inAugust 2009. Third, embedded derivative options inthe issuance of SDLs, which is an innovative way ofprice discovery and reducing the States’ cost ofborrowings, was introduced in September 2009.Finally, based on the recommendation of the WorkingGroup on Liquidity of State Government Securities(Chairman: Shri V.K. Sharma), SDLs have been madeeligible for repo transaction under the liquidityadjustment facility.

Discontinuance of Centre as intermediary forState market borrowings necessitated measuresfor better planning and transparency in issuanceof SDLs

7.35 The TwFC marked a turning point in theborrowing arrangements of the States bydiscontinuing the system of the Centre acting asan intermediary in raising loans for the States.However, this transition called for an additionalresponsibility for the Reserve Bank to develop amarket for State government borrowings so as toenable them to raise funds from the market directlyin a smooth manner. Accordingly, as recommendedby the Technical Group (Chairperson: Smt.Shyamala Gopinath), the Standing TechnicalCommittee on State government borrowings wasconstituted in December 2006 to make annualprojections of the borrowing requirements of theState governments, taking cognisance of evolvingmacroeconomic and financial conditions, thesustainability of debt, and the provisions of fiscalresponsibility legislations. It may, however, be notedthat the tradit ional role of the Centre inintermediating the external assistance bymultilateral agencies for the States has beencontinued, although it is being passed to the Stateson a back-to-back basis since April 2005, whereby

States bear the foreign exchange risk. In this regard,the Reserve Bank also organised a workshop inMay 2007 to sensit ise the States on themanagement of foreign exchange risk. The ReserveBank has also been working towards issuance ofindicative calendars for State governments toimprove transparency and for better planning oftheir market borrowings. So far, indicative calendarswere announced in September 2007 and June 2008detailing net allocation, maturities, amount raisedand the amount that could be raised during theremaining period of the year.

Reserve Bank’s initiatives in developing deep,wide and secured government securities marketfacilitated the States’ smooth switch over todirect open market borrowings

7.36 In line with other countries, the ReserveBank has been taking a series of initiatives todevelop the government securities market since theearly 1990s when it had deregulated the system ofadministered price and quantity controls. Thelandmarks in fiscal-monetary coordination, such asphasing out the automatic monetisation of Centralgovernment’s fiscal deficits from April 1997 andprohibition of the Reserve Bank’s participation inprimary government securities market from April2006, acted as key catalysts in developing thissegment of the financial market. Over the years,the measures have led to deepening of governmentsecurit ies market, leading to a signif icanttransformation in various dimensions, viz., market-based price discovery, widening of the investorbase, introduction of new instruments,establishment of primary dealers (PDs), and settingup of electronic trading and sett lementinfrastructure. With the various market developmentmeasures, the market has witnessed entry ofsmaller entities, such as co-operative banks, andsmall Pension and other Funds. To increaseawareness about the government securities marketamongst small investors, the Reserve Bank hasarranged workshops on the basic concepts relating

73

Role of the Reserve Bank in State Finances

to fixed income securities/bonds, existing tradingand investment practices, and the related regulatoryaspects and guidelines. The non-competitivebidding facility, which was introduced for auctionsof Central government securities in 2002, wasextended to auctions of State government securitiesin 2009 to facilitate the participation of retailinvestors, thereby widening the investor base. Theinvestment limit on government securities forForeign Institutional Investors (FIIs) has beenenhanced to accommodate greater foreignparticipation.

7.37 A fast, transparent and efficient clearingsystem constitutes the basic foundation of a well-developed secondary market in governmentsecurities. Towards this goal, during the initial phase,the Reserve Bank introduced dematerialisation ofgovernment securities in the form of SubsidiaryGeneral Ledger (SGL) to enable holding of securitiesin an electronic book entry form and operationalisedthe Delivery versus Payments (DvP) system (in1995) to synchronise the transfer of securities withcash payments, thereby eliminating settlement riskin securities transactions. Under the present system,banks, financial institutions, insurance companiesand PDs are allowed to hold twin accounts, viz.,security accounts (SGL) and current accounts forcash. For these participants, the settlement is donethrough the DvP system. Other participants, who arenot allowed to hold direct SGL accounts with theReserve Bank, can operate via the constituents’ SGLaccount maintained by SGL account holders. Alandmark initiative in developing marketinfrastructure to ensure guaranteed settlement wastaken when Clearing Corporation of India Limited(CCIL) was established on February 15, 2002 to actas the clearing house and as a central counterpartythrough novation for transactions in governmentsecurities, thereby seeking to impart considerablestability to the government securities market.Through the multilateral netting arrangement, thismechanism has reduced funding requirements fromgross to net basis, thereby reducing liquidity risk and

greatly mitigating counterparty credit risk. Alltransactions in government securities concluded orreported on Negotiated Dealing System (NDS) aswell as transactions on the NDS-OM have to benecessarily settled through the CCIL. As a steptowards introducing the National Settlement System(NSS) to centrally settle the clearing positions ofvarious clearing houses, the integration of theintegrated accounting system (IAS) with the real timegross settlement system (RTGS) was initiated inAugust 2006. This facilitated the settlement ofvarious CCIL-operated clearing through multilateralnet settlement batch (MNSB) mode in the RTGS inMumbai.

Reserve Bank’s Advisory Role on guarantees andpension liabilities helps to contain their adverseimpact on State finances

7.38 The Reserve Bank in its advisory capacity hasbeen sensitising the States to various issues ofcontemporary concerns that have a bearing on theirfinances. The genesis of concern with respect toguarantees dates back to 1999 when their magnituderose substantially in the wake of the poor fiscalposition of the States which hampered the provisionof direct financial support to the State PSUs.Accordingly, the Reserve Bank constituted a TechnicalCommittee on State Government Guarantees toexamine all aspects of the issue of State governmentguarantees. The Committee stipulated a ceiling onthe guarantees and recommended setting up of aGuarantee Redemption Fund (GRF) to provide acushion to service contingent liability arising frominvocation of guarantees. As per the schemeintroduced in 2001, the States had to contribute anamount equal to 1/5th of the outstanding invokedguarantees and likely invocation as a result ofincremental guarantees issued during the year. In linewith the recommendations of the TwFC andBezbaruah Committee, the scheme was revised from2006-07 to make the net incremental annualinvestment in GRF eligible for availing of the specialWMA. Accordingly, several State governments

74

State Finances : A Study of Budgets of 2011-12

stipulated a ceiling on their guarantees and set upGRFs. This resulted in a reduction in outstandingguarantees for States from 8.0 per cent of GDP in2000-01 to 2.8 per cent in 2009-10. By February 2012,10 State Governments, including five continuing withthe old scheme, had notified the GRF scheme. Theoutstanding investment under the GRF scheme stoodat around `40 billion in February 2012.

7.39 Following the recommendations of the TenthFinance Commission (1995) and subsequentdiscussions with the State governments, the ReserveBank also enabled the creation of a ConsolidatedSinking Fund (CSF) in 1999 to provide the States witha cushion for repayment of open market loans,whereby the States were to contribute 1-3 per cent oftheir outstanding open market loans as at the end ofthe previous year. Subsequently, based on therecommendations of the Bezbaruah Committee, theambit of the CSF was expanded in 2006-07 to includeamortisation of all the liabilities with the stipulatedcontribution of minimum 0.5 per cent of theoutstanding liabilities of the State as at the end of thepreceding financial year. By February 2012, 20 Stategovernments, including U.T. of Puducherry (includingfour continuing with the old scheme) had notified theCSF scheme. The revised CSF scheme alsostipulates a 5-year lock-in period. The aggregateoutstanding investments in CSF were placed at `415billion in February 2012. Both the CSF and the GRFare being administered by the Central AccountsSection of the Reserve Bank at Nagpur.

7.40 The implementation of the Fifth PayCommission at the State level resulted in aconsiderable fiscal stress on the States, not onlythrough an increase in expenditure on wages andsalaries but also through significantly higherexpenditure on pensions. The consolidated pensionexpenditure for all States doubled to 1.2 per cent ofGDP between 1990-91 and 1999-2000, therebyincreasing the pre-emption of revenue receipts formeeting pension liabilities to 11.2 per cent from 5.4per cent in 1990-91.

7.41 Recognising the unfunded and non-contributory nature of the prevailing pension schemeand its implications for State government finances,a Group to Study Pension Liabilities of the StateGovernments (Chairman: Shri B.K. Bhattacharya)was constituted in 2003. The group recommendeda contributory pension scheme for new employeesbased on a mix of defined contribution and benefitschemes as also funding of pension obligations.Subsequently, 20 States introduced the New PensionScheme (NPS) for their employees. Consequently,the pension liabilities, relative to GDP, haveremained under control, notwithstanding theimplementation of the Sixth Pay Commission awardunlike the situation experienced during the Fifth PayCommission award.

7.42 In view of the substantial differences in thedefinition and coverage of liabilities in the publicationspresenting States liabilities and the need for reliableand credible statistics on public debt comparableacross States, the Working Group on Compilation ofState Government Liabilities was constituted in theReserve Bank in 2006. Based on therecommendations of this Group, the coverage ofliabilities of the State governments has become morecomprehensive, as data were culled out from varioussources while ensuring that the compilation of States’liabilities was consistent with gross fiscal deficit.

Reserve Bank facilitated introduction of FiscalResponsibility and Budget Management Acts bythe States

7.43 The Reserve Bank also catalysed theintroduction of rule-based fiscal consolidation at theState government level by providing technicalguidance under the aegis of the Group on ModelFiscal Responsibility Legislation (FRL) at the StateLevel constituted in October 2003. The Groupprovided guidance for enacting the FRLs of the Statesby designing a model FRL bill based on internationalbest practices. The Group’s FRL Bill was quitecomprehensive in setting out the objectives andprinciples of sound fiscal management. It

75

Role of the Reserve Bank in State Finances

recommended the elimination of revenue deficit andcontainment of fiscal deficit to sustainable levels. Itsuggested that the bill should reflect the policies beingpursued by the State for raising non-tax revenues andprioritising capital expenditure to provide impetus foreconomic growth. It placed emphasis on key fiscalmanagement principles pertaining to transparency,stability and predictability, responsibility and integrity,fairness and efficiency. It suggested that the FRL billshould also include fiscal policy statements on themacroeconomic framework, medium-term fiscalpolicy and fiscal policy strategy. The Grouprecommended disclosure statements on key fiscalindicators. The model bill took into account thedisclosure requirements which were recommendedby the Core Group on Voluntary Disclosure Normsfor State governments. The model bill facilitated theState governments in formulating their FRBM Acts.All the State governments have enacted their FRBMActs.

Reserve Bank’s Conference of State FinanceSecretaries provides regular platform ofinteraction on issues of State finances

7.44 The Reserve Bank has been organisingConferences of State Finance Secretaries in astructured manner since 1997, where a consensualapproach among the Central Government, Stategovernments and the Reserve Bank has evolved onissues relating to State finances. Over the years, theConference has provided a very useful forum forinteractions among State Finance Secretaries, seniorofficials of the Government of India, the CGA, thePlanning Commission, the Finance Commission, theComptroller and Auditor General and the ReserveBank.

Reserve Bank’s dissemination of information onState Finances has progressively become morecomprehensive

7.45 The Reserve Bank disseminated data onState finances as an article in the RBI MonthlyBulletin from 1950-51 to 1998-99. However, from

1999-2000, this has been replaced by an annualpublication ‘State Finances: A Study of Budgets’,which provides as analytical presentation of Statefinances at the consolidated as well as at theindividual State level. The analysis, orientation,coverage and format of the report have beenrestructured periodically to make it morecontemporary. The overall purpose has been topresent a detailed and critical assessment of variousdevelopments and other issues that have asignificant bearing on the finances of Stategovernments. Since 2005-06, the analytical contentof the report has been further improved byincorporating a theme-based chapter that coversspecific aspects of State finances from a medium-term perspective. Such special theme-basedchapters covered in the past five years include‘Outstanding Liabilities of State Governments’,‘Social Sector Expenditure’, ‘Fiscal Transfers to Stategovernments’, ‘Revenue Receipts of StateGovernments: Trend and Composition’, ‘Expenditureof State Governments: Trend and Composition’ and‘Finance Commissions in India: An Assessment’. Tofacilitate research in the area of State finances, theReserve Bank provided access to all the articlespublished from 1950-51 to 2010-11 by releasing‘Compendium of Articles on State Finances (1950-51 to 2010-11),’ in the form of a CD.

7.46 To provide t ime series data on Stategovernment finances, the Reserve Bank broughtout a publication titled ‘Handbook of Statistics onState Government Finances’ in 2004, which wasrevised/expanded in 2010. This publication, whichprovides time series disaggregated data onconsolidated as well as State-wise transactions inthe revenue and capital accounts of 28 Stategovernments and two Union Territories, is a majorinit iat ive by Reserve Bank to improve datadissemination on the f inances of Stategovernments. The Handbook has been releasedin CD and web versions as well as in print form forwider dissemination.

76

State Finances : A Study of Budgets of 2011-12

5. Impact of Reserve Bank's role on StateFinances: Overall Assessment

Improvement in short term fiscal management ofStates

7.47 Systematic reforms in the conduct of financialarrangements of States initiated by the Reserve Bank,based on the recommendations of advisorycommittees as also the introduction of the rule-basedfiscal consolidation, have led to a structuralimprovement in the short-term fiscal management ofthe States. The occasions of temporary liquiditymismatches have progressively reduced particularly,from 2005-06 onwards. On the contrary, animprovement in the fiscal position of States asreflected in their surplus cash balances, posed achallenge for managing these cash balances whichwere invested in 14-day intermediate treasury billsand auction treasury bills (Chart VII.1a & b).

Reducing fiscal imbalances and rising proportionof market borrowings

7.48 The evolution of State government financessince the 1990s can broadly be divided into fourphases, viz., (i) 1990-91 to 1997-98, (ii) 1998-99 to2003-04, (iii) 2004-05 to 2006-07 and (iv) 2007-08 to

2011-12(BE). During the first phase (1990-91 to1997-98), fiscal imbalances persisted, although theconsolidated fiscal deficit-GDP ratio remainedcontained marginally below 3 per cent. The fiscaldeficits of States were essentially financed throughloans from the Centre and small savings collectionsearmarked for the States were also intermediatedthrough these loans. Market borrowings played asubordinate role and its share in the fiscal deficit ofthe States remained quite low. Consequently, theReserve Bank completed the market borrowings ofall the States in a combined fashion, generally in twoor more tranches through issuance of StateDevelopment Loans at pre-determined coupon andnotified amounts for each State.

7.49 During the second phase (1998-99 to 2003-04), the fiscal deficit-GDP ratio of the Statesreached a historical peak, crossing 4 per cent, onaccount of higher expenditures related to theimplementation of the Fifth Pay Commission awardand deceleration in State government revenues dueto economic slowdown. The National Small SavingsFund (NSSF) was established in 1999 to mobilisesmall savings and direct them to the Central andthe State governments through investments in their

a: Outstanding WMAs from RBI

0

10

20

30

40

50

60

70

80

90

100

2001-0

2

2002-0

3

2003-0

4

2004-0

5

2005-0

6

2006-0

7

2007-0

8

2008-0

9

2009-1

0

2010-1

1

`bill

ion

0

200

400

600

800

1000

1200

2001-0

2

2002-0

3

2003-0

4

2004-0

5

2005-0

6

2006-0

7

2007-0

8

2008-0

9

2009-1

0

2010-1

1

`bill

ion

Chart VII.1: Outstanding WMAs and Investment in Treasury Bills (as at end-March)

b: Outstanding Investment of Surplus CashBalances in Treasury Bills

Note: Investment from 2006-07 onwards includes Auction Treasury Bills.

77

Role of the Reserve Bank in State Finances

special securities. Consequently, small savings

collections, instead of being intermediated by the

Centre, were channelised through NSSF’s

investments in special securities issued by the

States for financing their fiscal deficits21. During

this phase, the NSSF’s investments became the

dominant source of financing fiscal deficit. The

States were allowed to use the auction mode, albeit

to a limited extent, for accessing market borrowings.

Market borrowings, as a source of financing fiscal

deficit for the States, increased in importance by

2003-04.

7.50 The third phase (2004-05 to 2006-07) sawoperationalisation of fiscal rules by most of the Stateswhich led to a decline in their fiscal deficit-GSDPratios. There was an increase in small savingcollections during this phase and the States had toabsorb the predominant share22 of small savingscollections earmarked to them, regardless of the costof borrowings. As a result, the States’ recourse tomarket borrowings for financing fiscal deficits declinedduring this phase (Chart VII.2). By 2006-07, the Stateswere allowed to raise market borrowings completelythrough the auction route so as to allow marketdetermination of yields on their SDLs.

7.51 With market access for States switchingcompletely to the auction-mode, market borrowingssteadily grew in importance for financing fiscal deficitsduring the fourth phase [2008-09 to 2011-12(BE)].Consequently, the States were able to meet theenhanced requirements during 2008-09 to 2009-10for implementing the Sixth Pay Commission awardand fiscal stimulus measures, particularly in the wakeof shortfall in small savings collections. Even afterthe States reverted to fiscal correction from 2010-11the importance of market borrowings continued, assmall saving collections remained low. During this

phase, market borrowings have emerged as adominant source of financing and, on an average,accounted for around 65 per cent of GFD (Chart VII.2).

Comparative cost advantage of marketborrowings relative to administered cost of NSSFloans