volatility regime shifts in international public property ... · volatility regime shifts in...

TRANSCRIPT

IRES2014-009

IRES Working Paper Series

Volatility regime shifts in international public property markets

Qing Ye, Kim Hiang Liow

May 2014

1

Volatility regime shifts in international public property markets

This version: May 11th

, 2014

Miss Ye Qing1* and Professor Liow Kim Hiang

2*

Abstract

Prior research studies have indicated that stock market return series have very different properties

between low and high volatile market regimes. This paper examines this issue in ten developed

international public property market and assesses the state-dependent volatility characteristics

across these markets over the past two decades. The classification between low and high volatility

regimes provides an ideal platform to study the contagion effect during extreme market conditions.

We find that real estate securities returns can be better characterized and forecasted by a regime-

switching GARCH model compared to traditional models. Moreover, the volatility spillover is

significantly increased and market linkage is strengthened during market downturns across all

markets examined. Finally, portfolio analysis dependent on the market regimes shows superior

diversification profits than investing over constant correlation. Finally, we show that there is a

strong difference of real estate securities performance in terms of risk-return, volatility spillover

pattern and diversification benefit between financial tranquil and turmoil time.

1 Introduction

The fall of banking sector in the recent 2007 global financial crisis is mainly because

banks are largely exposed to real estate developers and mortgage lenders. The crisis has quickly

spread to all nations and pushed international real estate securities markets into great turmoil. This

upheaval in the global financial market has led researchers to reexamine the contagion effect of

real estate assets. Real estate securities market, as an important component of general equity

market, is experiencing high uncertainty. In some times it can have a great boom, but it can also

fall down all in a sudden. Prior literature shows that they display even higher volatility than

general stocks (Sagalyn, 1990; Kallberg, et al., 2002). However, they are much preferred by

investors as an additional diversification since real estate securities exhibit lower correlation

globally. While real estate securities provide investors exposure to broad areas of real estate, it is

* Department of Real Estate, School of Design and Environment, National University of Singapore

4 Architecture Drive, Singapore, 117566 1 Corresponding author: PhD Candidate, [email protected]

2 Professor, [email protected]

2

still less known whether they can offer constant benefits that hedge against the changing market

performance.

In this study, we explore, whether there is strong switching regime behavior over the past two

decades in ten developed international real estate securities markets. Given the frequently

occurred turbulence in the financial markets and its contagious nature, we expect that there is

significant regime change in the real estate securities market. We characterize the sample period

into two sub-periods: one with low market volatility (tranquil period) and the other with high

market volatility (turmoil period). From the results, we investigate whether international market

linkages have significant variation between the two periods.

We also study the varying degrees of interdependence and volatility spillovers among candidate

countries over time. The main goal is to compare the different pattern of volatility spillover

between low and high volatility market states. Following estimation of state-dependent

conditional volatility from regime switching model, we further apply the newly generalized

version of spillover index of Diebold and Yilmaz (2012) to the ten developed markets to study

the direction and magnitude of volatility spillover among international real estate securities

markets.

To understand how the introduction of switching regimes can help reduce the portfolio risk, we

compare the performance of a dynamic portfolio where the asset allocation is state-dependent with

the benchmark portfolio where the weightings are constant based on historical market

performance. Both portfolios are optimized in order to achieve the objective of minimum variance.

The switching regime strategy of portfolio construction tracts the state-varying nature of market

performance in terms of return, variance and correlation, which is expected to yield higher risk

reduction benefit than a constant strategy.

3

Though there has been extensive work that investigates time-varying relationship or contagion

effect among global real estate securitized markets, few of them condition it on market volatility

states, and more importantly, over an extensive period before and after the financial crisis period.

This study is the first to investigate international real estate securities market linkages under

switching regime market behavior. As suggested by Forbes and Rigobon (2002), correlation

coefficients are biased measurement of market dependence if markets become more volatile.

Therefore, this research is expected to improve the key understanding of market interdependence,

and especially contagion effect across markets during crisis period.

We apply a novel methodology to capture the occasional shifts in the volatility process of real

estate securities markets. Gray (1996) and Dueker (1997) developed a Markov regime-switching

GARCH (MRS-GARCH) model to allow the conditional volatility switching between two

GARCH processes governed by different normal distribution. This stream of Markov regime-

switching model has been popularly used in literature since they are able to well describe extreme

events that frequently hit the financial markets. To compare the performance of GARCH models

in terms of switching regime version and traditional one (single regime), we give the test of model

fit as well as forecasting outcomes in the context.

The empirical results, using ten developed real estate securities markets data, can be summarized

as follows: (a) The volatility in ten developed real estate securities markets is subject to regime

switching behavior and a regime switching GARCH model is superior to traditional GARCH

model in characterizing and forecasting the market volatility process. (b) Asian real estate

securities markets exhibit longer time visiting high volatility states than other counterparts, yet the

market returns are not significantly higher. (c) Cross-market correlation increases significantly

during high volatility states. (d) During the financial crisis period, the volatility spillover effect is

strengthened across markets, indicating strong interdependence, especially in the Asian markets.

4

(e) The portfolio risk is significantly reduced if the allocation strategy is dependent on the

switching regimes.

The paper is organized as follows: section 2 presents the literature devoted to examine properties

of real estate securities market volatility and dynamic linkages. Section 3 gives a detailed

description of MRS-GARCH methodologies. The data of real estate securities returns is discussed

in section 4, following by empirical results and discussions in section 5. Conclusions are

summarized in section 6.

2 Literature Review

2.1 Contagion effect in international financial market

Two main forces of financial market integration are broadly discussed in the literature. One is

globalization, which increases market integration gradually over time. The other is what I aim to

study: contagion, which occurs only in bad times. The phenomenon that the crisis originated in

one financial market can quickly spread to markets all over the world has drawn attention from

researchers. Forbes and Rigobon (2002) defines it as contagion when cross-market linkages

increase only after a shock to one country (or group of countries). Studying cross-market

contagion without accounting for changing market volatility is biased.

There are many empirical papers that study the contagion effect, to name a few, Bekaert, et al.

(2005) apply a two-factor model based on CAPM to stock markets globally and examine whether

there is sudden increase in correlations during periods of crises. They find significant increase of

correlation among Asian regions. However, in the end they point out that the result may fail to

capture asymmetric volatility and the potential effects it may exert on correlations during crisis.

They propose using a richer regime switching model to account for contagion effect. More

recently, Aloui, et al. (2011) employ a multivariate copula approach to examine extreme co-

5

movement of BRIC and the US markets. They find extreme co-movement in both the bearish and

bullish markets, but the degree is generally smaller in bearish markets among the BRIC pairs,

indicating lower probability of simultaneous crashes.

In the real estate finance literature, Wilson and Zurbruegg (2004) studied the period of Asian

financial crisis in 1997 and found that there is contagion effect from Thai securitized real estate

market to other Asian markets. But this result is sensitive to the sample period chosen and based

on a single event of Thai baht devaluation. Bond, et al. (2006) found that there was significant

increase of correlation among Asian real estate securitized markets during the crisis. But the

transmission of shocks is different between real estate stocks and general equity markets,

indicating significant cross-asset diversification opportunities. Liow, et al. (2009) also confirmed

the existence of contagion effect among Asian property markets during the Asian financial crisis,

though not significant. However, less attention has been paid to the contagion effect during the

more recent global financial crisis, of which the magnitude is expected to be larger and has a

wider scope of global markets. Therefore, this study is contributed to fill the literature gap in this

area.

2.2 Real Estate Securities Market Volatility and Co-movement

Ever since the work of Schwert (1989), both theoretical and empirical researches have come to

explain the time-varying stock return volatility. Many earlier studies have focused on the causes

of persistence of volatility of asset returns, pointing to the presence of both structural changes and

long memory, but have mostly conducted on developed markets (Giliberto, 1990; Asabere, et al.,

1991; Ross and Zisler, 1991; Devaney, 2001). Later work improves by exploring dynamic

properties of data at different frequency (Liow, et al., 2009; Hoesli and Reka, 2011), covering a

wider range of markets (Liow and Newell, 2012; Zhou and Gao, 2012) or conducting comparison

across different assets (Neil Myer and Webb, 1993; Glascock, et al., 2000).

6

Given the better performance of real estate securities than general stocks, they have attracted

much research attention. For example, Garvey, et al. (2001) studied inter-relationship between

real estate securities markets in Asia on a weekly basis. They found little evidence of market co-

movement in the short run, indicating diversification benefits within the Pacific-Rim region.

Kallberg, et al. (2002) studied regime shifts in Asian real estate securities and stock markets

during the 1997 Asian financial crisis. Generally they found evidence of switching regime

behavior in the summer of 1997 and spring of 1998, and there is evidence of common volatility

factors among the markets studied. Gerlach, et al. (2006) also studied the impact of Asian

financial crisis on Asian-pacific real estate markets. Their result suggests integration among these

markets, despite a common structural break around mid-1997.

This group of research does not yield uniform pattern of co-movement among the real estate

securities markets examined. One of the common problems is that the framework is not flexible

enough to allow for stationarity and persistence properties of real estate securities returns. To

distinguish between crisis and non-crisis period, the sample period is divided arbitrarily

(Chandrashekaran, 1999; Clayton and MacKinnon, 2003; Westerheide, 2006). Meanwhile, these

studies only focus on regional sectors of real estate markets but overlook the possible linkages

with international developed markets in the US and the UK, etc.

More recently, with the development of statistical tools, more researchers have adopted Markov

regime switching framework to study real estate securities returns. And the result generally shows

strong persistence and regime switching behavior in the real estate securities returns. Liow, et al.

(2005) examined shifts in returns and volatility Asian property markets and compared with the US

and the UK. Strong evidence of regime switching behavior is detected among international

securitized property markets. Liow and Zhu (2007) apply regime switching strategies in the asset

allocation model. A shortcoming of the two papers is that they only allow for regime switching

process in the mean equation of real estate securities return. More recently, Case, et al. (2012)

7

applied regime switching GARCH model to REITs, stock and bond return in the US over the

period 1972-2008. The result suggested existence of separate regimes in the conditional

expectation and variance process. The multivariate result indicated that REITs return was in synch

with stock but not with bonds. Though in their framework the cross-asset linkages were

considered, the synchronization among international real estate securities markets was overlooked.

With the trend of globalization and contagion effect across markets, the lead-lag relationship and

volatility synchronization remains important for both investors and practitioners.

3 Sample data

3.1 Sample market review

In this study, we focus on ten developed real estate securities markets across the world, including

Australia, Hong Kong, Japan, Singapore, France, Germany, Switzerland, United Kingdom,

Canada and United States. These markets account for a significantly large proportion of broader

equity markets in terms of market capitalization3 by rank. Given their relatively large size and

degree of openness, we expect that the sample markets are more influential toward other

international markets and reflect market trend of global real estate securities. The variation of

market linkages between tranquil and turmoil market state is also expected to be larger than within

emerging markets. An important reason we do not study emerging markets is that they are more

prone to be affected by frequent structural breaks due to equity market liberalization. And studies

of emerging markets are usually subject to poor data quality.

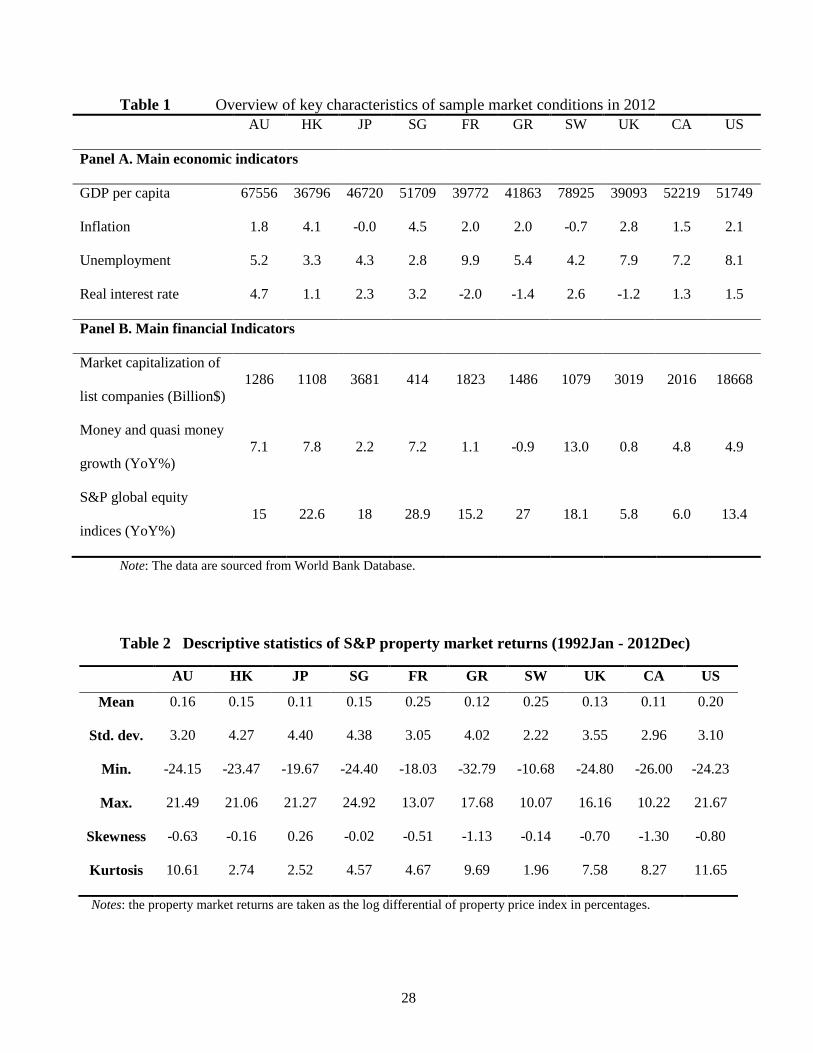

Table 1 offers a quick glimpse of the sample market conditions in the year 2012. As can be seen,

the macroeconomic conditions remain steady for most markets examined, with the exception of

European markets. And the positive return performance of the stock market also indicates the

3 Due to data availability, we exclude Brazil, Korea, Russia and India in the analysis.

8

market bounce after the financial crisis. The ten real estate securities markets studied in this

research fall into three geographical regions and different region-specific factors will play a role in

influencing their market performance.

The United States remains the top position among advanced nations in securitized property

markets. It is slowly recovering from financial turmoil due to strengthening job market and

income growth. The Canadian market, which has a close tie with the economic condition of the

US, also remained firm as the housing price is steadily showing an upward trend.

European securitized property markets are more mixed, especially after the subprime crisis. With

the support from government, the UK market is gaining traction to recover from market

downturns. And Switzerland securitized market return is seeing strong growth, benefiting from its

steady economy. Depressed labor market in Germany and France hinders these markets from

recovery, resulting in volatile performance of the securitized property markets.

While some European markets are showing weak signs, major Asian securitized property markets

are growing prosperously. It also leads to more market fluctuations in the region due to

speculation behavior. Singapore and Hong Kong’s securitized real estate markets are developing

quickly, though the Asian financial crisis in 1997 has triggered a number of large swings. With its

weak growth of the economy and the deflationary environment, Japan, the tycoon of Asian

property stock market, maintains a depressed growth compared to other Asian counterparts over

these years.

Overall, we expect the switching regime behavior to be strong in our sample markets studied.

With the occurrence of regional crisis in Asia and Europe, the volatility variation between tranquil

and turmoil period in those markets are reckoned to be larger.

[Insert Table 1 here]

9

3.2 Data description and preliminary analysis

The dataset of this study consists of weekly returns of major securitized real estate markets from

Standard and Poor (S&P) Global Database. The price indices from S&P are computed consistently

across different markets and are comparable directly. An advantage of this database is that it

covers a wide range of both emerging and developed markets for a long period at individual and

regional level. It also provides stock market index (Broader Market Index) based on the same

methodology and can be used for comparison with real estate securities index directly.

The weekly return series used in this study are computed from daily total return indices in US

dollar currency (Thursday to next Wednesday). Daily data suffer from non-synchronous trading

hours and weekend effect, while monthly data do not provide enough information. The sample

period starts from July of 1992 and ends in December of 2012, which is the longest available time

span of the database for all sample markets. There are 1069 observations in the sample.

A simple description of property return data is reported in Table 2. Over the sample period, the

Asian property market exhibits higher volatility and larger range of price variation than those of

European and North American property markets. The skewness and kurtosis statistics also

confirm the non-normality distribution of the data.

[Insert Table 2 here]

4 Methodology

In order to model the time-varying market volatility and incorporate the changes of market

performance at different market stages, we employ a switching regime GARCH model. In fact,

Hamilton and Susmel (1994) firstly introduce Markov switching model into the standard ARCH

process to overcome its poor out-of-sample forecasting ability. A Markov switching model

governs the change between different variance regimes so that in each regime, the volatility is

10

expressed by a unique ARCH process. While the variance of MS-ARCH model depends only on

the regimes of all ARCH lags, MS-GARCH model, though is more flexible and widely used, is

notoriously difficult for estimation (especially in large time-series data) since the lagged variance

term depends upon the entire history of regimes. Later, the MS-GARCH model developed by

Gray (1996) and Dueker (1997) overcome the problem by reducing the length of dependence and

approximately estimating the function. Of the two, Dueker’s filter requires only one lag of the

regime, therefore is simpler for estimation than Gray’s model. The following of this section will

start by explicitly explaining the setup of the MS-GARCH model, and describes the volatility

spillover methodology:

4.1 Switching regime GARCH model

The difference between MS-GARCH model and GARCH model is that, while GARCH model

assumes an ARMA process of volatility, the MS-GARCH model keeps same structure for

volatility, but allows the possibility of sudden jumps between two market states. It is recently

becoming popular in finance literature because it can well deal with volatility persistency and

determines the market states endogenously. A simple illustration of the model is as follows:

t t ty (1)

where ~student- t (mean=0, tn , th ) t , tn is the degree of freedom in the dependent variable ty .

The conditional mean t is allowed to switch according to a Markov process governed by a state

variable tS , indicating good time when 1tS and bad times when 0tS .

(1 )t l h tS (2)

( ) ( ) 2

1 1

1

ˆ( )( )

j j

t t t

t

h hg S j

(3)

11

where and are constant and ( 1)g S is the relative factor to scale down the ( ) 2

1( )j

t . The

initial probability of being in regime i is given by 1Pr( ) iS i p where 1S is the first regime in

the Markov chain. The transition probability between state 1 and 0 is given by:

11 12

21 22

(4)

where 1Pr( | )ij t tS j S i denotes the transition probability to state j at time t from state i

at time 1t .

4.2 Volatility Spillovers

To examine the spillover of volatility among ten real estate securitized markets, we apply the

newly proposed methodology by Diebold and Yilmaz (2012) and construct the volatility spillover

index4. One significant innovation of this methodology is that the spillover is measured in a

general VAR framework (Koop, et al. (1996) and Pesaran and Shin (1998)) so that the result is

not subject to the ordering of variables.

Assume a covariance stationary N -variable VAR( p ), 1

p

t i t i tix x , where (0, )

is a vector of independently and identically distributed disturbances and tx is a vector of

endogenous variables. The moving average representation is 0t i t ii

x A

, where the N N´

coefficient matrices iA obey the recursion 1 1 2 2 ...i i i p i pA A A A , with 0A the 4´

4 identity matrix and iA =0 for 0i .

The variance decomposition of the moving average form can help understand dynamics of the

system. It allows us to fraction of the H -step –ahead error variance in forecasting ix that is due to

4 For a detailed description of this methodology please refer to their paper.

12

shocks to jx , j i" ¹ , for each i . An innovation of p this spillover index is that it employs the

generalized VAR framework of, which produces variance decomposition invariant to the ordering

of variables. Based on the framework, the H -step-ahead forecast error variance decomposition is

1 21

0

1

0

( )( )

( )

H

jj i h jg hij H

i h h ih

e A eH

e A A e

(5)

where is the variance matrix of the error vector , jj is the standard deviation of the error

term for the j th equation.

5 Empirical result

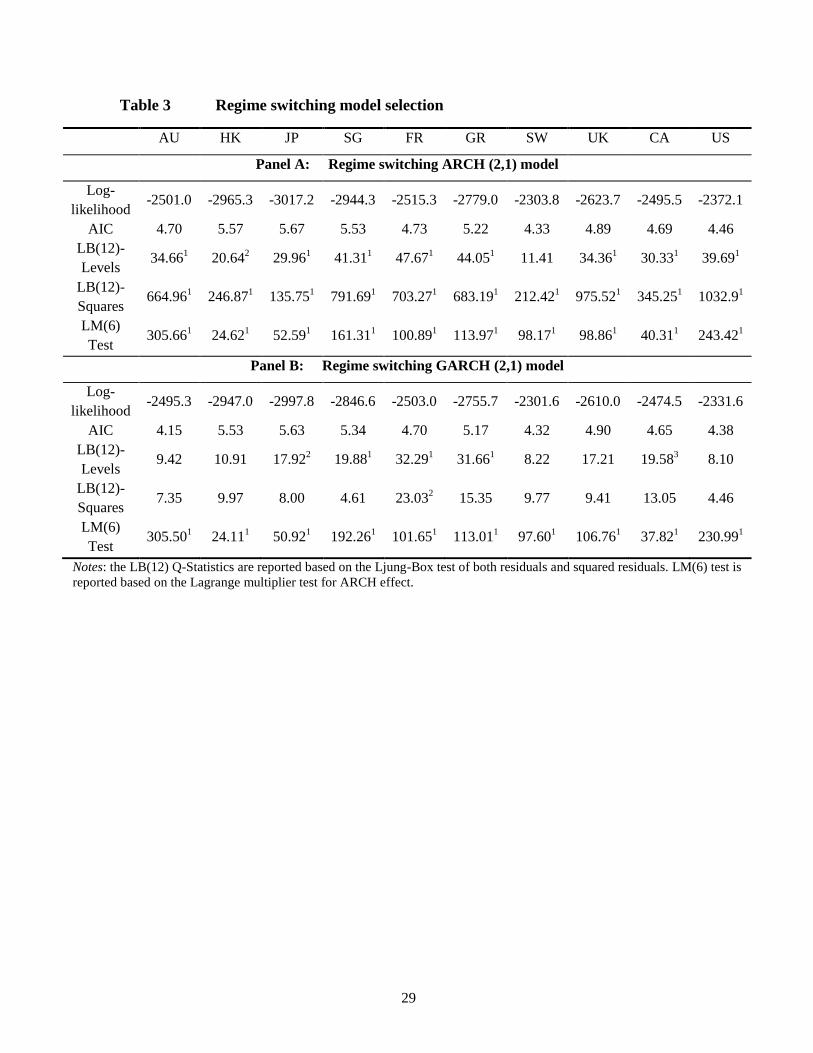

5.1 Regime switching model specification test

Before proceeding to the empirical analysis, we first test select which regime switching model

performs best in characterizing market returns. This is to compare the performance of regime

switching ARCH model and regime switching GARCH model based on log-likelihood value, AIC,

serial correlation test and ARCH effect test. Both models are specified with ARCH order at one

and two regimes5 with an asymmetric term. As previously mentioned, the order of GARCH term

is fixed at one to simplify computation in MS-GARCH models.

As shown in the first row of both panels in Table 3, the log-likelihood value supports MS-

GARCH model in advance of MS-ARCH model, indicating better fitness of the MS-GARCH

model. The AIC value is minimized in MS-GARCH models for all cases except the UK market.

Therefore we reckon that MS-GARCH outperform MS-ARCH models in terms of data fitness and

model complexity. To check whether the specification is enough or not, Ljung-Box test is applied

to the (standardized) residuals from ARCH or GARCH equations to check for serial correlation.

5 One ARCH order is determined so that there is no serial autocorrelation in the residuals. To reduce the

heavy computation of MS-GARCH model, I only consider regime switching models with two regimes.

13

For the MS-ARCH model in panel A of Table 3, the null-hypothesis is rejected for all markets

except for Switzerland at residual level, whereas for MS-GARCH model, the serial correlation is

reduced at residual levels and fully eliminated at residual squares, except for France. This is not

surprising as MS-GARCH accounts for conditional heteroskedasticity and the conditional

variance is flexible to vary across regimes. This is, however, not incorporated in the MS-ARCH

specification. Therefore, the standardized residuals are reduced to be white noise in MS-GARCH

models. The LM test in the last row of each panel also rejects the ARCH effect in the residuals.

Therefore, the result is in favor of MS-GARCH specification, where I continue the analysis

thereafter.

[Insert Table 3 here]

5.2 Switching regimes in international real estate securities markets

The two regimes are referred to as one low volatility regime with high return and one high

volatility regime with low return, respectively. The high volatility regime corresponds to the

financial crisis period which takes place only occasionally. The low volatility coincides with

normal tranquil period and accounts for most of the sample period. Panel A to C of Figure 1 plots

the estimated probabilities of being in state 1 (low volatility state) for all the property markets

studied. We can infer the smoothed probability of being in state 2 by subtracting the plotted

probability from unity. From the result, it is observed that within Asia, the low volatility

probability of Australia property market exhibits strong persistence, whereas that of Singapore

and Japan quickly decreases to low level, which result in frequent visit of high volatility state. The

results in Panel B and C show that the probability of being in the low volatility state is less

persistent and stable , especially in Europe where the estimated probabilities are lower than unity.

The three figures also yield evidence of strong regional patterns where all markets in that region

tend to visit the particular state at the same time. The 1997 Asian financial crisis, the 2007 global

financial crisis and the following European sovereign debt crisis all influence the global property

14

markets and add to the market volatility. Australia and Switzerland are characterized by strongest

persistence of low volatility, which only vanishes during the three crisis periods. The sovereign

debt crisis also adds to the uncertainty of the Switzerland property market, but to a lesser extent.

This is not surprising not only because of its steady economy and government, but also because of

its independent fiscal policy and economies of being no EU members. By counting the days of

being in the low volatility state when the smoothed probability of state 1 is larger than 0.5, it is

shown that United Kingdom (876 days), France (906 days) and Singapore (912 days) are among

the markets which are less likely to be in the low volatility state, whereas United States (1024

days), Canada (1003 days), Switzerland (999 days) shows lowest level of being in the high

volatility state.

[Insert Figure 1]

The Regime switching GARCH model is applied to each of property market returns and is

estimated independently across markets. The result is reported in Table 4. The first three rows

reports the parameters in the GARCH process. is largely significant and close to unity,

indicating high persistence of the conditional volatility as in (Lamoureux and Lastrapes, 1990).

( )tgv S is a normalization factor which is used to scale down the conditional volatility process in

the respective regime. ( , )P i j in the last two rows of Table 4 present the probability of changing

from j to i . As is shown, (1,1)P is highly significantly and rather close to unity for most

markets except for Japan United Kingdom and France, indicating persistence of low volatility

state. This is compatible with large body of literature documenting the persistence of financial

return volatility, but from a different perspective.

[Insert Table 4 here]

15

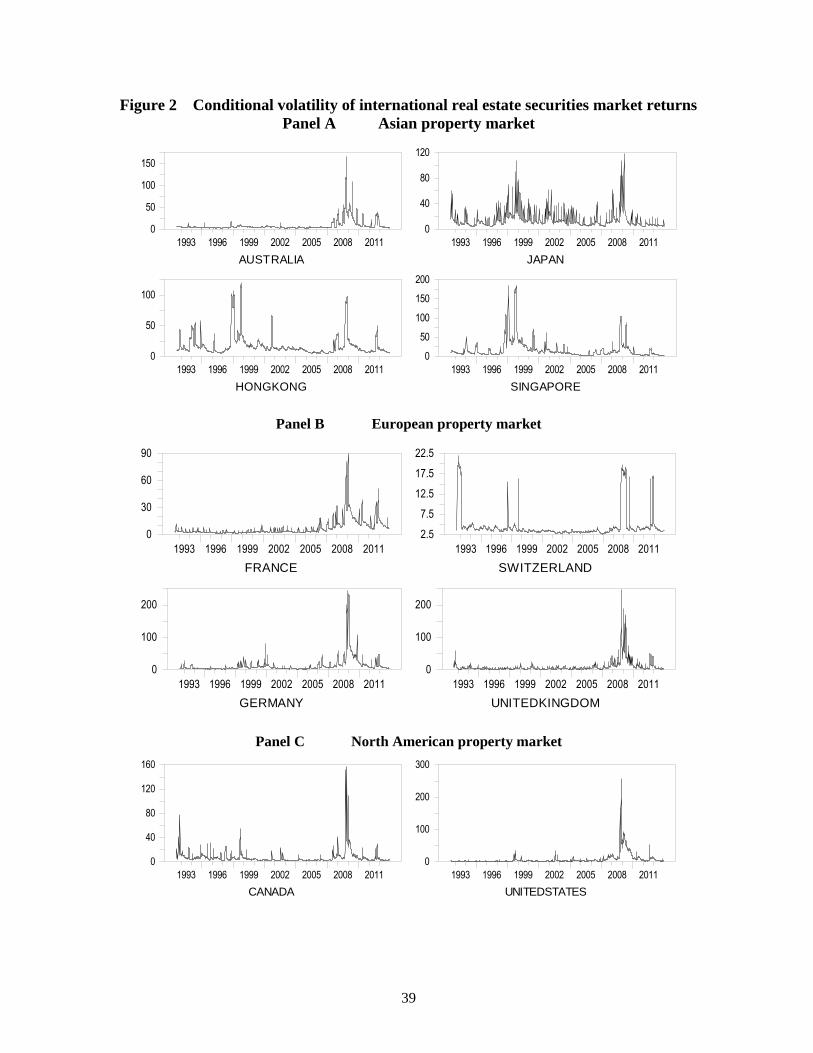

Panel A to C of Figure 2 present the time-varying conditional volatility of the sample property

market returns. Under the Markov modeling framework, the volatility process can be interpreted

as expected value since it is weighted by the normalization factor ( )tgv S in the respective state

distinguished by the smoothed probability. As is observed, the volatility persistence, which is

usually found in conventional GARCH framework, is significantly reduced. The volatility value

quickly reverts back to normal level after climbing up due to shocks. To look at the performance

of international real estate securities markets during the sample period, it is observed that the

expected variance is everywhere high during the subprime crisis around 2008, when the expected

volatility can be more than ten times higher than in normal tranquil period. For the Asian property

markets in Panel A of Figure 2, the estimated volatility reached even higher peak value during the

Asian financial crisis period, such as Hong Kong and Singapore, where the strike from the crisis is

most severe. The European property markets generally stay in the low volatility state since the

start of the sample period, but quickly climb to peak value from year 2007. After returning to

medium level, the estimated volatility in European property markets picks up again at the end of

year 2011. Particularly, it is observed that Asian property markets are more volatile than those in

Europe and North America over the sample period, especially in Japan, Hong Kong and Singapore.

Given the growing prospects of Asian markets from global real estate securities fund, it implies

that despite the higher volatility estimated, investors are still willing to allocate assets in Asian

property markets to secure higher returns.

[Insert Figure 2 here]

Table 5 presents the average return and constant variance of each real estate securities market of

two volatility states. In the terms of magnitude of variance, Japan, the US and Germany are most

volatile during high volatility state, while Switzerland and France stays quieter during crisis time.

It is also observed that Asian real estate securities markets exhibit higher volatility and spend

16

longer time in the high volatility state than other international real estate markets, yet the return is

not significantly higher during this sample period.

[Insert Table 5 here]

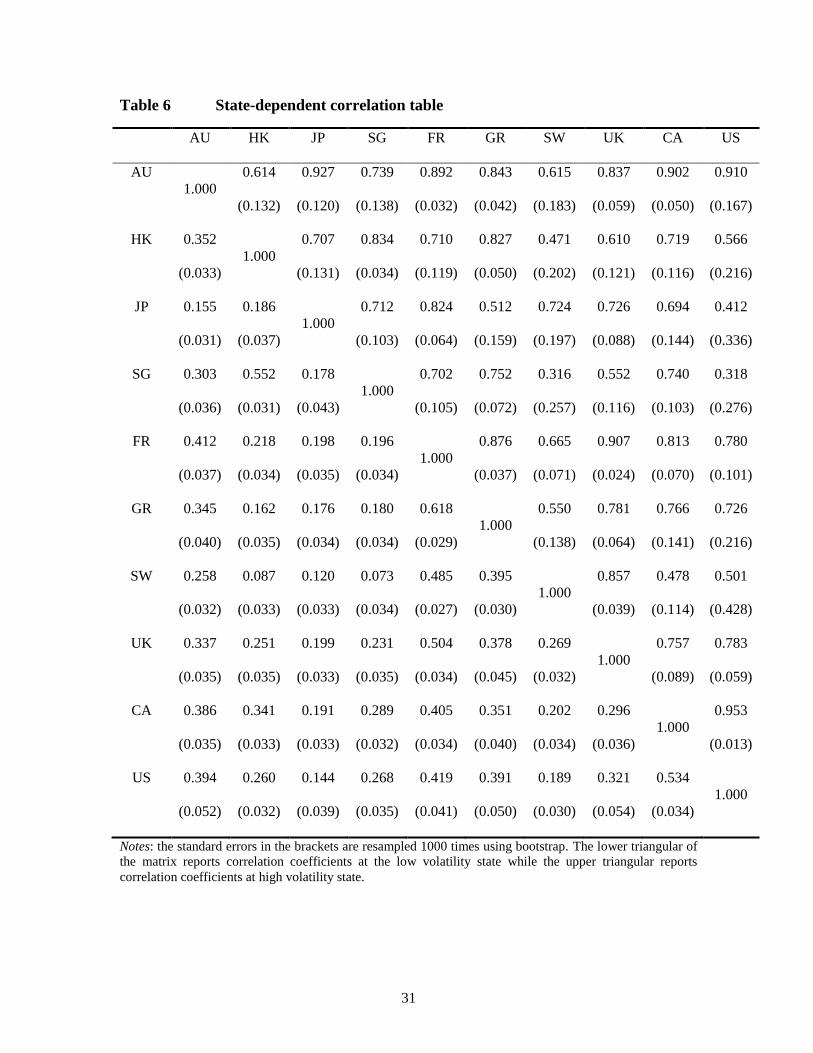

Finally, the state-dependent correlation coefficients are estimated when both markets are in the

same volatility state. Specifically, the observation belongs to low volatility state if the smoothed

probability of state one is larger than 0.5, and vice versa. The correlation coefficient in each

regime is calculated based on the series in the overlapping periods of both markets. The

correlation matrix is presented in Table 6 with the lower triangular reporting correlation

coefficients in low volatility regime and upper triangular reporting correlation coefficients in high

volatility regime. It is not surprising that the correlation coefficients are found to be much higher

for all market pairs during high volatility regime, providing evidence of contagion across markets

during crisis time.

[Insert Table 6]

From Table 5, three main regional patterns are also observed. Firstly, Singapore and Hong Kong

represent the most fast growing regions in real estate securities markets in Asia. They are also

mostly correlated during both low and high volatility regimes. Similarly, Canada and the US

exhibit highest correlation than the rest international markets in both volatility regimes. The

correlation coefficient even reaches 0.953 during high volatility period, indicating almost perfect

synchronization between the two real estate securities markets. Secondly, it appears that inter-

regional correlations increase to be the highest during high volatility period for all real estate

securities markets. This finding provides additional evidence to the work of Bekaert, et al. (2005)

that integration of regional real estate securities markets sharply increases during crisis period.

Thirdly, the increment of correlation during high volatility period in Asia is generally more than

the other counterparts, indicating that the contagious effect in bear market is higher in this region.

17

For investors, however, the findings are dangerous signals for asset allocation strategies merely at

regional levels, especially in the Asian region. Instead, based on our statistical evidence, broader

investment strategy at international levels is much recommended.

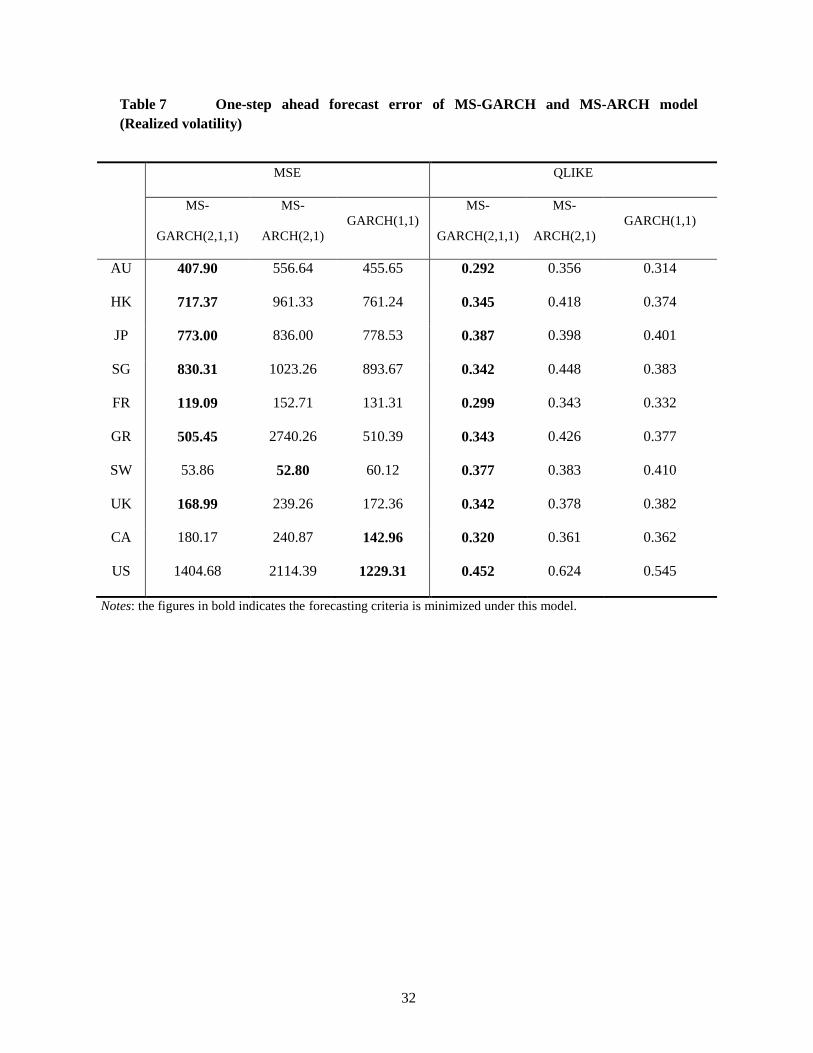

5.3 Prediction of real estate securities volatility: a comparison of MS-

GARCH and MS-ARCH models

Whilst evaluating past performance may help us understand the unique risk properties of real

estate securities, investors care more about how the introduction of regime shifts may help predict

the securities performance in the future. We next proceed to examine the one-step ahead

prediction of real estate securities conditional volatility. More importantly, we care about whether

MS-GARCH models offers better forecast ability than other regime switching models.

To conduct the out-of-sample forecast, we first estimate the one-step-ahead predictions of the

variance. In the regime switching model setting, the estimated conditional volatility is calculated

as the average of two conditional volatility processes in the low and high volatility regimes

weighted by the probabilities of the two regimes at time t given 1t . For comparison, we also

estimate and forecast regime switching ARCH(2,1)6 and GARCH (1,1) model, both with an

asymmetric term in the variance equation.

The proxy of ex-post volatility is difficult to obtain. The mean-adjusted squared return, though

unbiased, is known to be a noise measurement that leads to the bad forecasting performance of

many models (Andersen and Bollerslev, 1998). This paper follows this idea and employs the

measurement of realized volatility which can significantly reduce the noise. Since we use weekly

return and the highest frequency available is daily data, the observed volatility is calculated as the

sum of squared daily returns over a week’s horizon:

6 To be consistent, we estimate ARCH (2,1) with two volatility regimes and one lag of ARCH term.

18

52

1

t i

i

RV r

where tRV is the realized variance at week t , and ir is the daily return at trading day i .

The loss function is calculated as follows:

1 2

1 1|

1

( )n

t t t

t

MSE n RV h

1 1 1

1 1| 1|

( log 1)n

t t

t t t t t

RV RVQLIKE n

h h

For volatility forecast comparison, Table 7 summarizes the loss function of Mean Squared Error

(MSE) and QLIKE of the one-step-ahead estimation. In terms of MSE, MS-GARCH(2,1,1) is

minimized in most markets except Switzerland, Canada and the US. But the QLIKE value

supports MS-GARCH(2,1,1) in all markets, indicating the forecasting performance gains relative

to other alternative models. The overall result supports the better performance of regime switching

models in terms of volatility forecasting, as is observed from the comparison with MS-ARCH(2,1)

and GARCH(1,1) model. This is because regime switching GARCH model is generalized to

account for the volatility persistence, which is a critical important feature of asset returns.

[Insert Table 7 here]

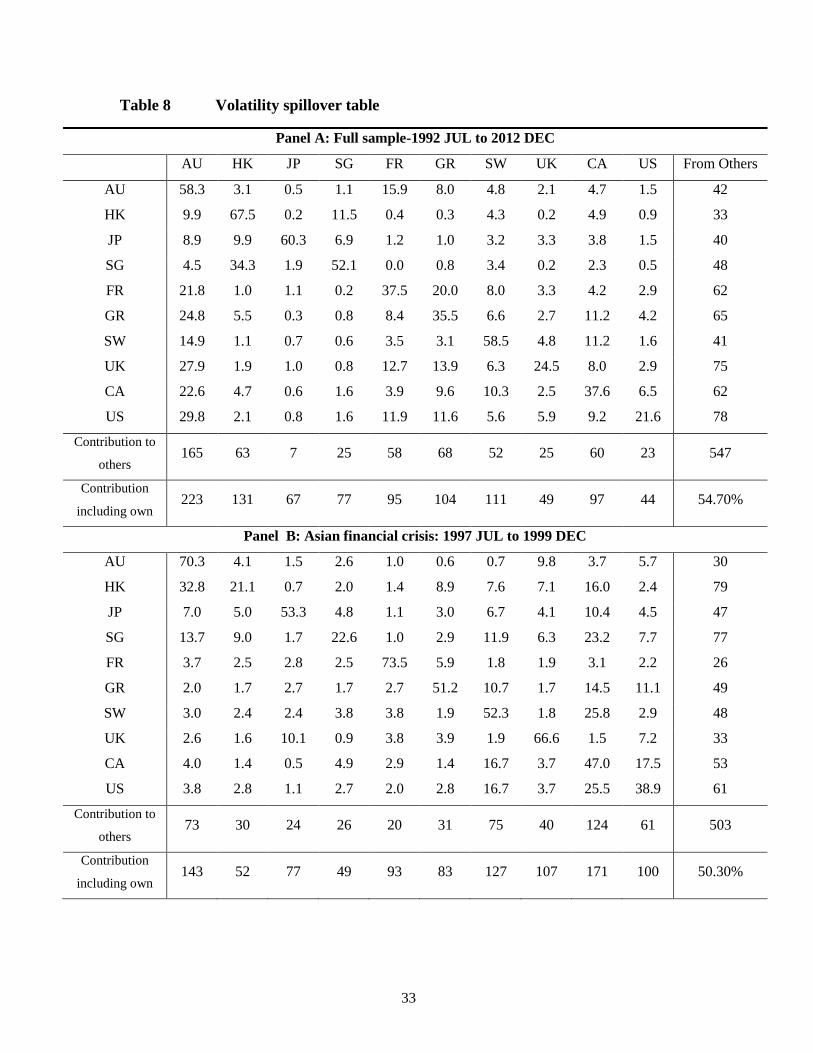

5.4 Volatility spillovers across markets

An important advantage of regime switching model is that it can well capture the contagion effect

during the financial crisis time. According to the definition of Forbes and Rigobon (2002),

contagion takes place only when cross-market linkages increase after a shock to one country (or

group of countries). This is usually accompanied by the increase of volatility in the financial

19

market. Regime switching model is capable to distinguish the different levels of market volatility,

which provides an unbiased measure of contagion effect (Ang and Chen, 2002).

Next I examine, in addition to contagion at return level, how volatility would spill over across real

estate securities markets during different states of market performance. Moreover, the recently-

developed method by Diebold and Yilmaz (2012) makes it possible to identify both direction and

magnitude of volatility spillover across markets.

The recent financial crisis has dramatically changed the pattern of interdependence among

international real estate securities markets and, consequently, question rises as which market

dominates the influence to other markets at regional and international level. Therefore, in this

section the aim is to explore transmission of shocks across markets and evaluate how and to what

extent the volatility of market is influenced by shocks of market within/outside the same region.

There are mainly two advantages of volatility spillover measurement employed in this paper. First,

this methodology does not require the identification or existence of crisis period, thus is less prone

to subjective problems. Secondly, the variance decomposition calculation in this method is

invariant to ordering of the variables since the underlying VAR does not depend on Cholesky

factor identification.

To implement the volatility spillover analysis, we employ the estimated conditional volatility

from MS-GARCH and measure the directional impact between any of the two markets. Before

discussion, it is necessary to explain the rows and the columns of results in Table 8. The ( , )i j

element of the numerical area in the table is the estimated contribution from innovations of

volatility j to the forecast error variance of volatility i . The diagonal elements measure own-

market volatility spillovers, while the off-diagonal elements capture cross-market volatility

spillovers between two markets. The column “From Others” and row “Contribution to others”

give the total “from” and “to” volatility spillovers of each market by summing up all non-diagonal

20

elements in each row and column, respectively. The net volatility spillover from market i to

market j is calculated as the difference between the “Contribution to others” and “From Others”

in the respective market. The total volatility spillover index, given in the lower right corner of the

table, estimates the sum of the second last row “Contribution to others” over the sum of the last

row “Contribution including own”.

There are several interesting observations from Table 8. Firstly, the volatility spillovers from the

own market explains most of forecast error volatility, as shown the higher value of diagonal

elements compared with off-diagonal ones. Secondly, from panel B and C of crisis periods, the

volatility spillover from other markets increases significantly. In particular, during AFC period,

Asian real estate securities markets are more vulnerable to volatilities from other markets,

especially for the case of Hong Kong and Singapore. But other European and North American

markets are not significantly influenced. Meanwhile, in the GFC time, all sample markets exert

higher influence to others and receive more shocks, indicating strong interdependence among

these markets. Hong Kong becomes the main source of “volatility exporter” to other markets.

Thirdly, the volatility spillover has been mainly concentrated at regional level, whereas in the

crisis period, volatility transmission across regions is strengthened.

[Insert Table 8]

5.5 Portfolio diversification analysis under switching regimes

To further analyze if portfolio investment strategies can be improved by incorporating the regime-

switching framework, we construct portfolio real estate securities assets whose performance are

benchmarked by market indices. To simplify the analysis, we stay in a bivariate formulation of the

US real estate securities index and the rest individual market index. Specifically, investors in the

respective property market are assumed to diversify their portfolio risk by allocating part of their

wealth in the US real estate securities market and the rest in their domestic market. This

21

hypothesis of keeping US real estate in the portfolio is plausible as many historical and forward-

looking analyses suggest that in an optimized global portfolio, at least one-third of real estate

allocations should be invested in the US real estate7.

To perform this investment strategy under regime-switching framework, we classify the

performance of the two market indices into four combined states based on the smoothed

probabilities of the two markets: (a) State 1 indicates both markets are jointly in the low volatility

states; (b) State 2 is when the individual market is in the low volatility state and the US market is

in the high volatility state; (c) State 3 corresponds to the period that the individual market is in the

high volatility state and the US market in the low volatility state; (d) State 4 is the nightmare

period when both markets are in the high volatility state. The classification of four combined

states enables us to estimate the state-dependent correlation in Table 9, where we start the

portfolio analysis afterwards.

[Insert Table 9]

To construct the portfolio, it is assumed that investors are allowed to choose the proportion of the

two assets in order to minimize the portfolio risk. The formula of the portfolio variance is given

by:

2 2 2 2

, , , , , , , , ,2i j i j i j us j us j i j us j i j us j jVar w w w w (6)

where i, jw and ,us jw indicates the weighting of the individual market i and the US market in state

j and , , 1i j us jw w . 2

,i j and2

,us j is the variance of the respective market returns and j is

the state-dependent correlation between the two markets.

To achieve the objective of minimum portfolio variance, ,i jVar is derived with respect to 1, jw :

7 Source: http://www.reit.com/investing/reit-basics/reit-faqs/global-real-estate-investment

22

,

,

0i j

i j

dVar

dw (7)

and the optimal weighting of the i -th individual market is given by:

2

, , ,

, 2 2

, , , ,2

us j i j us j j

i j

i j us j i j us j j

w

(8)

The weighting ,i jw of the individual market i is reported in Table 10. As shown in the table, in

different state combinations, the weighting is significantly different from each other. For example,

in state 2 when the US market is highly volatile and the individual market is in the boom period, it

is beneficial to transfer part of the investment from the US market to the individual market. As is

shown in Table 10, compared to the normal state 1 period, the weighting of the individual market

is largely increased to almost 100% in most of the markets in state 2. Likewise, in state 3 when the

US market is tranquil and the individual market is highly volatile, the allocation of the latter is

nearly zero with the exception of Switzerland where the financial market is stable and less risky.

[Insert Table 10]

Finally, the minimized variance and risk-reduction percentage is presented in Table 11. The first

column reports the variance of the portfolio without taking a regime switching strategy, while the

last two columns report the portfolio variance under regime switching and its risk reduction

percentage. As can be seen, the portfolio risk can be significantly reduced by around 20% in all

markets if the regime-dependent correlation is considered. It offers important implications for

investors to diversify part of their assets to a less-correlated or tranquil market when the domestic

market is highly risky. This state-dependent investment strategy will significantly reduce their

portfolio risk than a constant allocation strategy.

[Insert Table 11]

23

6 Conclusion

The dynamic correlation and volatility of international real estate securities markets have been

well studied. Motivated by the frequent occurrence of extreme financial events and persistence of

shocks, this study provides a different perspective by distinguishing between low and high

volatility period where the pattern of interdependence and contagion effect across markets could

be dramatically different. The fruitful result produced provides a number of valuable additions to

the existing literature: (a) There exists significant regime switching behavior between low and

high volatility period among the sample real estate securities markets. (b) The GARCH model

with switching regimes in the conditional volatility process can well deal with the volatility

persistence issues usually found in previous literature. (c) Asian real estate securities markets,

especially Hong Kong and Singapore, exhibit higher level and persistence of volatility than

European and North American counterparts. (d) The regime switching GARCH model performs

better in terms of forecasting ability than GARCH model or regime switching ARCH model for

the sample markets studied. (e) Correlation and volatility spillover among real estate securities

markets still remain at regional levels, whereas during the crisis time, the pattern of international

interdependence is much strengthened. (f) The portfolio analysis shows strong diversification

benefits if the allocation of assets is dependent on the switching regimes. Compared to the strategy

of making investment constantly over the whole period, the switching regime method can lower

the portfolio risk by around 20% for all sample markets.

Based on the regime switching model in this paper, the result is closely associated with literature

concerns the integration and contagion of international real estate securities markets and portfolio

risk management. Future research can explore the macroeconomic factors that drive the switching

regime behavior of real estate securities market returns and dynamic correlations. Expansions of

wider sample markets that include emerging markets may provide additional evidence on the

24

volatility and correlation dynamics of real estate securities markets and is a promising area for

future work.

25

Reference

Aloui, R., Aïssa, M.S.B., Nguyen, D.K., 2011. Global financial crisis, extreme interdependences,

and contagion effects: The role of economic structure? Journal of Banking & Finance 35, 130-141

Andersen, T.G., Bollerslev, T., 1998. Answering the skeptics: Yes, standard volatility models do

provide accurate forecasts. International economic review, 885-905

Ang, A., Chen, J., 2002. Asymmetric correlations of equity portfolios. Journal of Financial

Economics 63, 443-494

Asabere, P.K., Kleiman, R., McGowan, C., 1991. The Risk-Return Attributes of International

Real Estate Equities. Journal of Real Estate Research

Bekaert, G., Harvey, C.R., Ng, A., 2005. Market Integration and Contagion. The Journal of

Business 78, 39-69

Bond, S.A., Dungey, M., Fry, R., 2006. A web of shocks: crises across Asian real estate markets.

The Journal of Real Estate Finance and Economics 32, 253-274

Case, B., Guidolin, M., Yildrim, Y., 2012. Markov Switching Dynamics in REIT Returns:

Univariate and Multivariate Evidence. Real Estate Economics, Forthcoming

Chandrashekaran, V., 1999. Time-series properties and diversification benefits of REIT returns.

Journal of Real Estate Research 17, 91-112

Clayton, J., MacKinnon, G., 2003. The Relative Importance of Stock, Bond and Real Estate

Factors in Explaining REIT Returns. The Journal of Real Estate Finance and Economics 27, 39-60

Devaney, M., 2001. Time varying risk premia for real estate investment trusts: A GARCH-M

model. The Quarterly Review of Economics and Finance 41, 335-346

Diebold, F.X., Yilmaz, K., 2012. Better to give than to receive: Predictive directional

measurement of volatility spillovers. International Journal of Forecasting 28, 57-66

Dueker, M.J., 1997. Markov switching in GARCH processes and mean-reverting stock-market

volatility. Journal of Business & Economic Statistics 15, 26-34

26

Forbes, K.J., Rigobon, R., 2002. No contagion, only interdependence: measuring stock market

comovements. The Journal of Finance 57, 2223-2261

Garvey, R., Santry, G., Stevenson, S., 2001. The linkages between real estate securities in the

Asia-Pacific. Pacific Rim Property Research Journal 7, 240-258

Gerlach, R., Wilson, P., Zurbruegg, R., 2006. Structural breaks and diversification: the impact of

the 1997 Asian financial crisis on the integration of Asia-Pacific real estate markets. Journal of

International Money and Finance 25, 974-991

Giliberto, M.S., 1990. Equity real estate investment trusts and real estate returns. Journal of Real

Estate Research 5, 259-263

Glascock, J.L., Lu, C., So, R.W., 2000. Further evidence on the integration of REIT, bond, and

stock returns. The Journal of Real Estate Finance and Economics 20, 177-194

Gray, S.F., 1996. Modeling the conditional distribution of interest rates as a regime-switching

process. Journal of Financial Economics 42, 27-62

Hamilton, J.D., Susmel, R., 1994. Autoregressive conditional heteroskedasticity and changes in

regime. Journal of Econometrics 64, 307-333

Hoesli, M., Reka, K., 2011. Volatility spillovers, comovements and contagion in securitized real

estate markets. The Journal of Real Estate Finance and Economics, 1-35

Kallberg, J.G., Liu, C.H., Pasquariello, P., 2002. Regime shifts in Asian equity and real estate

markets. Real Estate Economics 30, 263-291

Koop, G., Pesaran, M.H., Potter, S.M., 1996. Impulse response analysis in nonlinear multivariate

models. Journal of Econometrics 74, 119-147

Lamoureux, C.G., Lastrapes, W.D., 1990. Persistence in variance, structural change, and the

GARCH model. Journal of Business & Economic Statistics, 225-234

Liow, K., Zhu, H., 2007. Regime switching and asset allocation: Evidence from international real

estate security markets. Journal of Property Investment & Finance 25, 274-288

27

Liow, K.H., Ho, K.H.D., Ibrahim, M.F., Chen, Z., 2009. Correlation and volatility dynamics in

international real estate securities markets. The Journal of Real Estate Finance and Economics 39,

202-223

Liow, K.H., Newell, G., 2012. Investment dynamics of the Greater China securitized real estate

markets. Journal of Real Estate Research 34, 399-428

Liow, K.H., Zhu, H., Ho, D.K., Addae-Dapaah, K., 2005. Regime changes in international

securitized property markets. Journal of Real Estate Portfolio Management 11, 147-165

Neil Myer, F., Webb, J.R., 1993. Return properties of equity REITs, common stocks, and

commercial real estate: a comparison. Journal of Real Estate Research 8, 87-106

Pesaran, H.H., Shin, Y., 1998. Generalized impulse response analysis in linear multivariate

models. Economics letters 58, 17-29

Ross, S.A., Zisler, R.C., 1991. Risk and return in real estate. The Journal of Real Estate Finance

and Economics 4, 175-190

Sagalyn, L.B., 1990. Real estate risk and the business cycle: evidence from security markets.

Journal of Real Estate Research 5, 203-219

Schwert, G.W., 1989. Why Does Stock Market Volatility Change over Time? Journal of Finance

44, 1115-53

Westerheide, P., 2006. Cointegration of real estate stocks and REITs with common stocks, bonds

and consumer price inflation-An international comparison. ZEW-Centre for European Economic

Research Discussion Paper

Wilson, P., Zurbruegg, R., 2004. Contagion or interdependence?: Evidence from comovements in

Asia-Pacific securitised real estate markets during the 1997 crisis. Journal of Property Investment

& Finance 22, 401-413

Zhou, J., Gao, Y., 2012. Tail dependence in international real estate securities markets. The

Journal of Real Estate Finance and Economics 45, 128-151

28

Table 1 Overview of key characteristics of sample market conditions in 2012

AU HK JP SG FR GR SW UK CA US

Panel A. Main economic indicators

GDP per capita 67556 36796 46720 51709 39772 41863 78925 39093 52219 51749

Inflation 1.8 4.1 -0.0 4.5 2.0 2.0 -0.7 2.8 1.5 2.1

Unemployment 5.2 3.3 4.3 2.8 9.9 5.4 4.2 7.9 7.2 8.1

Real interest rate 4.7 1.1 2.3 3.2 -2.0 -1.4 2.6 -1.2 1.3 1.5

Panel B. Main financial Indicators

Market capitalization of

list companies (Billion$)

1286 1108 3681 414 1823 1486 1079 3019 2016 18668

Money and quasi money

growth (YoY%)

7.1 7.8 2.2 7.2 1.1 -0.9 13.0 0.8 4.8 4.9

S&P global equity

indices (YoY%)

15 22.6 18 28.9 15.2 27 18.1 5.8 6.0 13.4

Note: The data are sourced from World Bank Database.

Table 2 Descriptive statistics of S&P property market returns (1992Jan - 2012Dec)

AU HK JP SG FR GR SW UK CA US

Mean 0.16 0.15 0.11 0.15 0.25 0.12 0.25 0.13 0.11 0.20

Std. dev. 3.20 4.27 4.40 4.38 3.05 4.02 2.22 3.55 2.96 3.10

Min. -24.15 -23.47 -19.67 -24.40 -18.03 -32.79 -10.68 -24.80 -26.00 -24.23

Max. 21.49 21.06 21.27 24.92 13.07 17.68 10.07 16.16 10.22 21.67

Skewness -0.63 -0.16 0.26 -0.02 -0.51 -1.13 -0.14 -0.70 -1.30 -0.80

Kurtosis 10.61 2.74 2.52 4.57 4.67 9.69 1.96 7.58 8.27 11.65

Notes: the property market returns are taken as the log differential of property price index in percentages.

29

Table 3 Regime switching model selection

AU HK JP SG FR GR SW UK CA US

Panel A: Regime switching ARCH (2,1) model

Log-

likelihood -2501.0 -2965.3 -3017.2 -2944.3 -2515.3 -2779.0 -2303.8 -2623.7 -2495.5 -2372.1

AIC 4.70 5.57 5.67 5.53 4.73 5.22 4.33 4.89 4.69 4.46

LB(12)-

Levels 34.66

1 20.64

2 29.96

1 41.31

1 47.67

1 44.05

1 11.41

34.36

1 30.33

1 39.69

1

LB(12)-

Squares 664.96

1 246.87

1 135.75

1 791.69

1 703.27

1 683.19

1 212.42

1 975.52

1 345.25

1 1032.9

1

LM(6)

Test 305.66

1 24.62

1 52.59

1 161.31

1 100.89

1 113.97

1 98.17

1 98.86

1 40.31

1 243.42

1

Panel B: Regime switching GARCH (2,1) model

Log-

likelihood -2495.3 -2947.0 -2997.8 -2846.6 -2503.0 -2755.7 -2301.6 -2610.0 -2474.5 -2331.6

AIC 4.15 5.53 5.63 5.34 4.70 5.17 4.32 4.90 4.65 4.38

LB(12)-

Levels 9.42 10.91 17.92

2 19.88

1 32.29

1 31.66

1 8.22 17.21 19.58

3 8.10

LB(12)-

Squares 7.35 9.97 8.00

4.61

23.03

2 15.35 9.77 9.41 13.05 4.46

LM(6)

Test 305.50

1 24.11

1 50.92

1 192.26

1 101.65

1 113.01

1 97.60

1 106.76

1 37.82

1 230.99

1

Notes: the LB(12) Q-Statistics are reported based on the Ljung-Box test of both residuals and squared residuals. LM(6) test is

reported based on the Lagrange multiplier test for ARCH effect.

30

Table 4 Regime switching GARCH model result

AU HK JP SG FR GR SW UK CA US

-0.013

(0.023)

0.034

(0.021)

0.0221

(0.001)

0.0641

(0.020)

0.0422

(0.017)

0.0781

(0.025)

0.0323

(0.018)

0.0662

(0.031)

0.029

(0.029)

0.0962

(0.040)

0.9362

(0.022)

0.9211

(0.020)

0.8881

(0.006)

0.8961

(0.020)

0.9411

(0.017)

0.9021

(0.028)

0.9241

(0.010)

0.8251

(0.040)

0.8691

(0.043)

0.8561

(0.046)

0.1132

(0.024)

0.0582

(0.029)

0.1181

(0.003)

0.0552

(0.024)

0.027

(0.017)

0.023

(0.025)

-0.003

(0.016)

0.1251

(0.040)

0.1271

(0.036)

0.0822

(0.041)

0.1011

(0.031)

0.1922

(0.080)

0.3331

(0.025)

0.0912

(0.040)

0.0232

(0.010)

0.073

(0.050)

0.1641

(0.003)

0.2122

(0.089)

0.1582

(0.072)

0.047

(0.029)

0.4721

(0.166)

0.7572

(0.349)

1.1001

(0.069)

0.3672

(0.163)

0.0632

(0.028)

0.296

(0.186)

0.7351

(0.186)

0.6992

(0.272)

0.7842

(0.371)

0.287

(0.177)

P(1,1) 0.9771

(0.014)

0.9781

(0.012)

0.6481

(0.072)

0.9531

(0.025)

0.8301

(0.168)

0.9191

(0.052)

0.9911

(0.007)

0.7571

(0.093)

0.9391

(0.035)

0.9381

(0.029)

P(1,2) 0.1683

(0.096)

0.134

(0.087)

0.7831

(0.191)

0.1702

(0.079)

0.3432

(0.147)

0.2842

(0.122)

0.0912

(0.044)

0.4352

(0.034)

0.3882

(0.181)

0.5271

(0.185)

Notes: results are reported based on the equation: 1

2 2

, 1 , 1

, , 1 { 0}1( ) ( )

t t

t t t

s t s t

s t s t uR

t t

u uh h

gv s gv s

.

Table 5 Return and variance in two volatility states: 1992 Jul to 2012 Dec

AU HK JP SG FR GR SW UK CA US

Panel A: Low volatility state

Mean 0.31 0.28 0.15 0.28 0.37 0.20 0.30 0.26 0.32 0.32

Variance 5.69 12.21 9.52 11.00 4.70 8.03 3.66 4.27 5.19 6.61

# of Obs 982 952 945 912 906 931 999 876 1003 1024

Panel B: High volatility state

Mean. -0.13 -0.10 -0.02 -0.10 -0.08 -0.06 -0.02 -0.09 -0.20 -0.11

Variance 61.33 67.83 96.48 67.35 35.06 72.91 23.65 50.73 55.14 76.34

# of Obs 84 114 121 154 160 135 67 190 63 42

31

Table 6 State-dependent correlation table

AU HK JP SG FR GR SW UK CA US

AU

1.000

0.614

(0.132)

0.927

(0.120)

0.739

(0.138)

0.892

(0.032)

0.843

(0.042)

0.615

(0.183)

0.837

(0.059)

0.902

(0.050)

0.910

(0.167)

HK 0.352

(0.033)

1.000

0.707

(0.131)

0.834

(0.034)

0.710

(0.119)

0.827

(0.050)

0.471

(0.202)

0.610

(0.121)

0.719

(0.116)

0.566

(0.216)

JP 0.155

(0.031)

0.186

(0.037)

1.000

0.712

(0.103)

0.824

(0.064)

0.512

(0.159)

0.724

(0.197)

0.726

(0.088)

0.694

(0.144)

0.412

(0.336)

SG 0.303

(0.036)

0.552

(0.031)

0.178

(0.043)

1.000

0.702

(0.105)

0.752

(0.072)

0.316

(0.257)

0.552

(0.116)

0.740

(0.103)

0.318

(0.276)

FR 0.412

(0.037)

0.218

(0.034)

0.198

(0.035)

0.196

(0.034)

1.000

0.876

(0.037)

0.665

(0.071)

0.907

(0.024)

0.813

(0.070)

0.780

(0.101)

GR 0.345

(0.040)

0.162

(0.035)

0.176

(0.034)

0.180

(0.034)

0.618

(0.029)

1.000

0.550

(0.138)

0.781

(0.064)

0.766

(0.141)

0.726

(0.216)

SW 0.258

(0.032)

0.087

(0.033)

0.120

(0.033)

0.073

(0.034)

0.485

(0.027)

0.395

(0.030)

1.000

0.857

(0.039)

0.478

(0.114)

0.501

(0.428)

UK 0.337

(0.035)

0.251

(0.035)

0.199

(0.033)

0.231

(0.035)

0.504

(0.034)

0.378

(0.045)

0.269

(0.032)

1.000

0.757

(0.089)

0.783

(0.059)

CA 0.386

(0.035)

0.341

(0.033)

0.191

(0.033)

0.289

(0.032)

0.405

(0.034)

0.351

(0.040)

0.202

(0.034)

0.296

(0.036)

1.000

0.953

(0.013)

US 0.394

(0.052)

0.260

(0.032)

0.144

(0.039)

0.268

(0.035)

0.419

(0.041)

0.391

(0.050)

0.189

(0.030)

0.321

(0.054)

0.534

(0.034)

1.000

Notes: the standard errors in the brackets are resampled 1000 times using bootstrap. The lower triangular of

the matrix reports correlation coefficients at the low volatility state while the upper triangular reports

correlation coefficients at high volatility state.

32

Table 7 One-step ahead forecast error of MS-GARCH and MS-ARCH model

(Realized volatility)

Notes: the figures in bold indicates the forecasting criteria is minimized under this model.

MSE QLIKE

MS-

GARCH(2,1,1)

MS-

ARCH(2,1)

GARCH(1,1)

MS-

GARCH(2,1,1)

MS-

ARCH(2,1)

GARCH(1,1)

AU 407.90 556.64 455.65 0.292 0.356 0.314

HK 717.37 961.33 761.24 0.345 0.418 0.374

JP 773.00 836.00 778.53 0.387 0.398 0.401

SG 830.31 1023.26 893.67 0.342 0.448 0.383

FR 119.09 152.71 131.31 0.299 0.343 0.332

GR 505.45 2740.26 510.39 0.343 0.426 0.377

SW 53.86 52.80 60.12 0.377 0.383 0.410

UK 168.99 239.26 172.36 0.342 0.378 0.382

CA 180.17 240.87 142.96 0.320 0.361 0.362

US 1404.68 2114.39 1229.31 0.452 0.624 0.545

33

Table 8 Volatility spillover table

Panel A: Full sample-1992 JUL to 2012 DEC

AU HK JP SG FR GR SW UK CA US From Others

AU 58.3 3.1 0.5 1.1 15.9 8.0 4.8 2.1 4.7 1.5 42

HK 9.9 67.5 0.2 11.5 0.4 0.3 4.3 0.2 4.9 0.9 33

JP 8.9 9.9 60.3 6.9 1.2 1.0 3.2 3.3 3.8 1.5 40

SG 4.5 34.3 1.9 52.1 0.0 0.8 3.4 0.2 2.3 0.5 48

FR 21.8 1.0 1.1 0.2 37.5 20.0 8.0 3.3 4.2 2.9 62

GR 24.8 5.5 0.3 0.8 8.4 35.5 6.6 2.7 11.2 4.2 65

SW 14.9 1.1 0.7 0.6 3.5 3.1 58.5 4.8 11.2 1.6 41

UK 27.9 1.9 1.0 0.8 12.7 13.9 6.3 24.5 8.0 2.9 75

CA 22.6 4.7 0.6 1.6 3.9 9.6 10.3 2.5 37.6 6.5 62

US 29.8 2.1 0.8 1.6 11.9 11.6 5.6 5.9 9.2 21.6 78

Contribution to

others 165 63 7 25 58 68 52 25 60 23 547

Contribution

including own 223 131 67 77 95 104 111 49 97 44 54.70%

Panel B: Asian financial crisis: 1997 JUL to 1999 DEC

AU 70.3 4.1 1.5 2.6 1.0 0.6 0.7 9.8 3.7 5.7 30

HK 32.8 21.1 0.7 2.0 1.4 8.9 7.6 7.1 16.0 2.4 79

JP 7.0 5.0 53.3 4.8 1.1 3.0 6.7 4.1 10.4 4.5 47

SG 13.7 9.0 1.7 22.6 1.0 2.9 11.9 6.3 23.2 7.7 77

FR 3.7 2.5 2.8 2.5 73.5 5.9 1.8 1.9 3.1 2.2 26

GR 2.0 1.7 2.7 1.7 2.7 51.2 10.7 1.7 14.5 11.1 49

SW 3.0 2.4 2.4 3.8 3.8 1.9 52.3 1.8 25.8 2.9 48

UK 2.6 1.6 10.1 0.9 3.8 3.9 1.9 66.6 1.5 7.2 33

CA 4.0 1.4 0.5 4.9 2.9 1.4 16.7 3.7 47.0 17.5 53

US 3.8 2.8 1.1 2.7 2.0 2.8 16.7 3.7 25.5 38.9 61

Contribution to

others 73 30 24 26 20 31 75 40 124 61 503

Contribution

including own 143 52 77 49 93 83 127 107 171 100 50.30%

34

Panel C Global financial crisis: 2007 JUL to 2009 DEC

AU 23.2 25.2 3.5 10.1 7.8 6.4 13.1 3.0 2.6 5.0 77

HK 12.7 41.3 3.5 7.3 7.6 4.6 11.4 2.9 2.5 6.1 59

JP 11.9 18.3 16.0 11.7 6.7 5.0 14.1 4.6 6.2 5.4 84

SG 17.9 26.3 3.5 12.5 5.9 3.3 22.2 2.3 2.1 4.0 88

FR 9.2 30.4 2.4 7.0 16.7 9.1 10.3 6.4 3.0 5.4 83

GR 8.6 42.4 1.9 4.4 9.8 6.9 14.1 2.3 2.2 7.3 93

SW 17.7 42.6 3.9 8.3 6.8 2.1 10.2 1.9 0.8 5.8 90

UK 12.0 25.0 2.3 9.4 13.2 8.9 9.8 9.4 5.0 5.1 91

CA 15.3 27.6 3.0 10.5 6.7 5.1 15.2 3.5 6.4 6.8 94

US 15.4 30.5 3.0 10.9 7.0 6.5 9.8 3.9 3.6 9.4 91

Contribution to

others 121 268 27 80 72 51 120 31 28 51 848

Contribution

including own 144 310 43 92 88 58 130 40 34 60 84.80%

Notes: results are reported based on variance decomposition for estimated VAR(3) models of the conditional volatility obtained from the

MS-GARCH model. Lag length of 3 is selected by SIC. Variance decompositions are based on 20-week-ahead forecasts.

35

Table 9 Cross-market correlation coefficient with the US

Market Whole Period State 1 State 2 State 3 State 4

S&P US real estate securities index

AU 0.455 0.394 0.367 0.492 0.910

JP 0.320 0.260 0.558 0.374 0.566

HK 0.234 0.144 0.326 0.426 0.412

SG 0.294 0.268 0.292 0.356 0.318

FR 0.486 0.419 0.228 0.575 0.780

GR 0.457 0.391 0.293 0.509 0.726

SW 0.230 0.189 -0.091 0.301 0.501

UK 0.501 0.321 0.095 0.666 0.783

CA 0.614 0.534 0.652 0.514 0.953

Notes: Four combined states between two markets are classified: State 1 (both individual market and the US

market in low volatility state), State2 (individual market in low volatility state and the US market in high

volatility state), State3 (individual market in high volatility state and the US market in low volatility state)

and State4 (both individual and the US market in high volatility state). The correlation coefficient is

calculated based on subsamples in each state. The correlation coefficients under “Whole Period” column are

estimated over the whole sample period.

Table 10 Portfolio weighting under constant and regime-dependent correlation

Market Whole Period State 1 State 2 State 3 State 4

S&P US real estate securities index

AU 47.09% 50.06% 100.00% 5.87% 76.66%

JP 27.88% 28.17% 72.72% 2.10% 99.85%

HK 28.57% 38.43% 95.62% 0.00% 46.38%

SG 27.09% 33.07% 85.13% 0.00% 64.37%

FR 51.65% 59.64% 99.94% 0.00% 100.00%

GR 27.18% 37.66% 98.95% 0.00% 4.29%

SW 70.71% 60.13% 89.60% 59.63% 100.00%

UK 36.88% 55.96% 96.14% 0.00% 94.87%

CA 56.16% 61.48% 100.00% 0.00% 100%

Notes: The table reports the weighting of individual market in the portfolio, which is estimated as:

2

, , ,

, 2 2

, , , ,2

us j i j us j j

i j

i j us j i j us j j

w

. The variance of individual market

2

,i j and the US market2

,us j and

correlation coefficient are dependent on state j in a regime-dependent framework. The weightings under

“Whole Period” column are estimated under constant correlation framework.

36

Table 11 Minimum portfolio variance under constant and regime-dependent

correlation

Market Variance under

Constant correlation

Variance under

Regime-dependent correlation Risk reduction percentage

Portfolio variance

AU 7.2344 5.7202 20.93%

JP 8.1372 6.3546 21.91%

HK 7.8009 5.7046 26.87%

SG 8.1167 6.1088 24.74%

FR 7.0425 5.3418 24.15%

GR 8.5793 7.0325 18.03%

SW 3.9475 3.2860 16.76%

UK 8.1238 6.0144 25.97%

CA 7.4020 6.1976 16.27%

Notes: The portfolio variance is estimated by the following formula: 2 2 2 2

, , , , , , , , ,2i j i j i j us j us j i j us j i j us j jVar w w w w , where ,i jw and

,us jw is the weighting of the individual

market and the US market, respectively. ,i j and

,us j is the variance of the respective market and j gives

the correlation.

The last column presents the percentage of risk reduction by using a regime-dependent framework and is

calculated as:tan

(%)regime dependent cons t

regime dependent

Var Varrisk reduction

Var

, where tancons tVar and regime dependentVar are

given in the first two numerical columns.

37

Figure 1 Smoothed Probabilities of Being in the Low Volatility State

Panel A Asian Property markets

Panel B European Property markets

AUSTRALIA

1993 1996 1999 2002 2005 2008 2011

0.0

0.4

0.8

HONGKONG

1993 1996 1999 2002 2005 2008 2011

0.0

0.4

0.8

JAPAN

1993 1996 1999 2002 2005 2008 2011

0.00

0.25

0.50

0.75

1.00

SINGAPORE

1993 1996 1999 2002 2005 2008 2011

0.0

0.4

0.8

FRANCE

1993 1996 1999 2002 2005 2008 2011

0.0

0.2

0.4

0.6

0.8

GERMANY

1993 1996 1999 2002 2005 2008 2011

0.0

0.4

0.8

SWITZERLAND

1993 1996 1999 2002 2005 2008 2011

0.0

0.4

0.8

UNITEDKINGDOM

1993 1996 1999 2002 2005 2008 2011

0.0

0.2

0.4

0.6

0.8

38

Panel C North American Property markets

CANADA

1993 1996 1999 2002 2005 2008 2011

0.0

0.2

0.4

0.6

0.8

1.0

UNITEDSTATES

1993 1996 1999 2002 2005 2008 2011

0.0

0.2

0.4

0.6

0.8

1.0

39

Figure 2 Conditional volatility of international real estate securities market returns

Panel A Asian property market

Panel B European property market

Panel C North American property market

AUSTRALIA

1993 1996 1999 2002 2005 2008 2011

0

50

100

150

HONGKONG

1993 1996 1999 2002 2005 2008 2011

0

50

100

JAPAN

1993 1996 1999 2002 2005 2008 2011

0

40

80

120

SINGAPORE

1993 1996 1999 2002 2005 2008 2011

0

50

100

150

200

FRANCE

1993 1996 1999 2002 2005 2008 2011

0

30

60

90

GERMANY

1993 1996 1999 2002 2005 2008 2011

0

100

200

SWITZERLAND

1993 1996 1999 2002 2005 2008 2011

2.5

7.5

12.5

17.5

22.5

UNITEDKINGDOM

1993 1996 1999 2002 2005 2008 2011

0

100

200

CANADA

1993 1996 1999 2002 2005 2008 2011

0

40

80

120

160

UNITEDSTATES

1993 1996 1999 2002 2005 2008 2011

0

100

200

300