w1 lecture power point

TRANSCRIPT

8/8/2019 W1 Lecture Power Point

http://slidepdf.com/reader/full/w1-lecture-power-point 1/30

1

Accounting for Decision Making

Week 1 Lecture

(2010)

8/8/2019 W1 Lecture Power Point

http://slidepdf.com/reader/full/w1-lecture-power-point 2/30

2

Module number: U50029Module title: Accounting for Decision Making

Contents

Week Lecture

1 Seminar 2 - Budgeting (revision)

2 Seminar 3 - Appraising the Long-term Plan (revision)

3 Seminar 4 - Cost Allocation

4 Seminar 5 - Unit cost & Pricing

5 Seminar 6 – Controlling the Plan (Variance Analysis)

6 Consolidation

7 Seminar 7 - Identifying Contribution & Break Even Analysis

8 Seminar 8 - Relevant Costs and Revenues Analysis

9 Seminar 9 - Balanced Scorecard & Performance Indicators10 Revision

11 Sample Exam Paper

12 Optional

8/8/2019 W1 Lecture Power Point

http://slidepdf.com/reader/full/w1-lecture-power-point 3/30

3

Costing System of a Merchandiser

MerchandiseInventory

Revenues

=

Profit

Cost of

Goods Sold(an expense)

Gross Profit

Marketing,

selling andadministrative

expenses

_

_

MerchandisePurchases

whensalesoccur

BALANCE SHEET INCOME STATEMENT

Marketing,

selling andadministrativeexpenses

8/8/2019 W1 Lecture Power Point

http://slidepdf.com/reader/full/w1-lecture-power-point 4/30

4

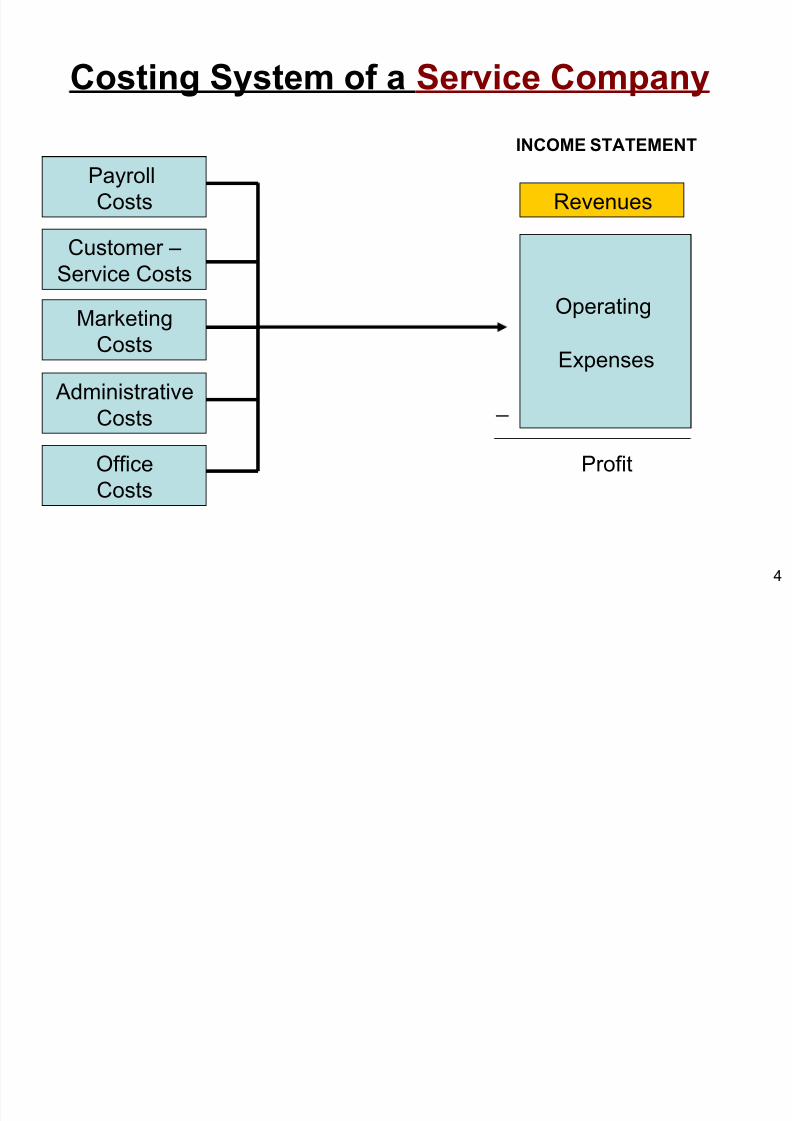

Costing System of a Service Company

Customer –

Service Costs

PayrollCosts

MarketingCosts

Administrative

Costs

OfficeCosts

Revenues

Operating

Expenses

Profit

_

INCOME STATEMENT

8/8/2019 W1 Lecture Power Point

http://slidepdf.com/reader/full/w1-lecture-power-point 5/30

5

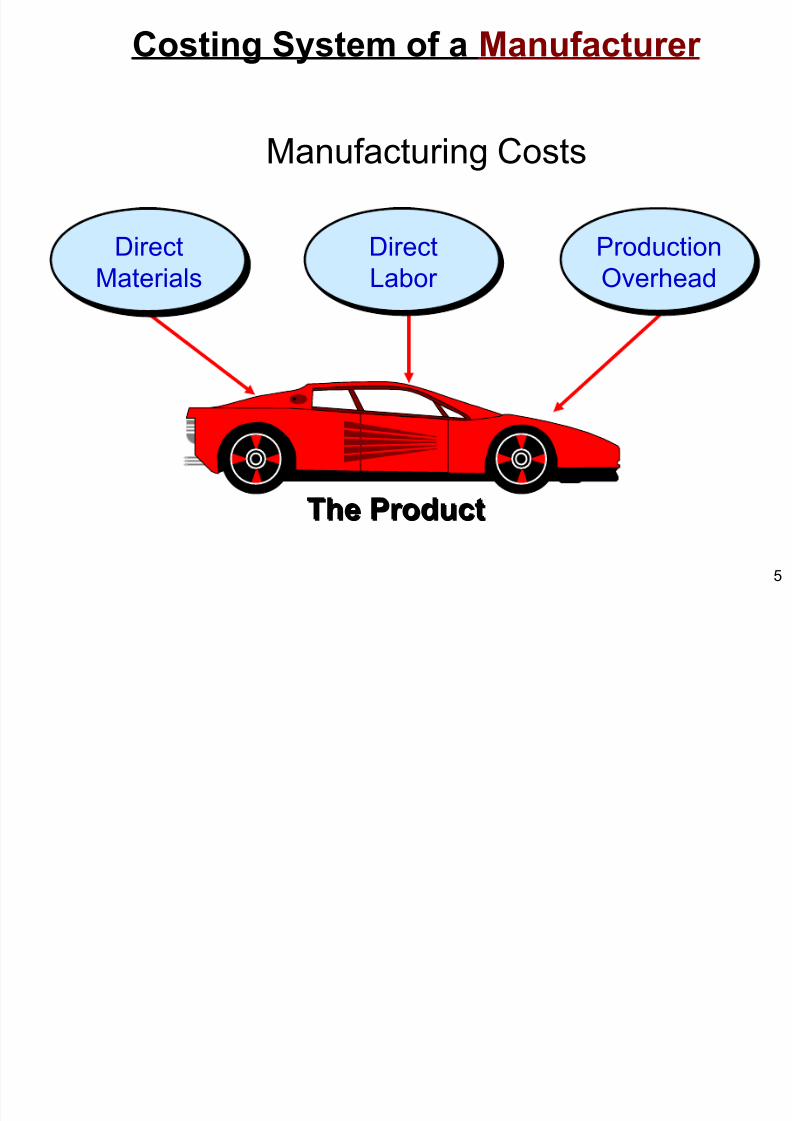

The ProductThe Product

Direct

Materials

Direct

Materials

Direct

Labor

Direct

Labor

Production

Overhead

Production

Overhead

Manufacturing Costs

Costing System of a Manufacturer

8/8/2019 W1 Lecture Power Point

http://slidepdf.com/reader/full/w1-lecture-power-point 6/30

6

Sale of FinishedGoods(Cost of

Goods Sold)

Conversioninto Finished

GoodsInventory

Conversioninto Work-in-

ProcessInventory

Materials,Labor, andProductionOverhead

Costing System of a Manufacturer

8/8/2019 W1 Lecture Power Point

http://slidepdf.com/reader/full/w1-lecture-power-point 7/30

8/8/2019 W1 Lecture Power Point

http://slidepdf.com/reader/full/w1-lecture-power-point 8/30

8

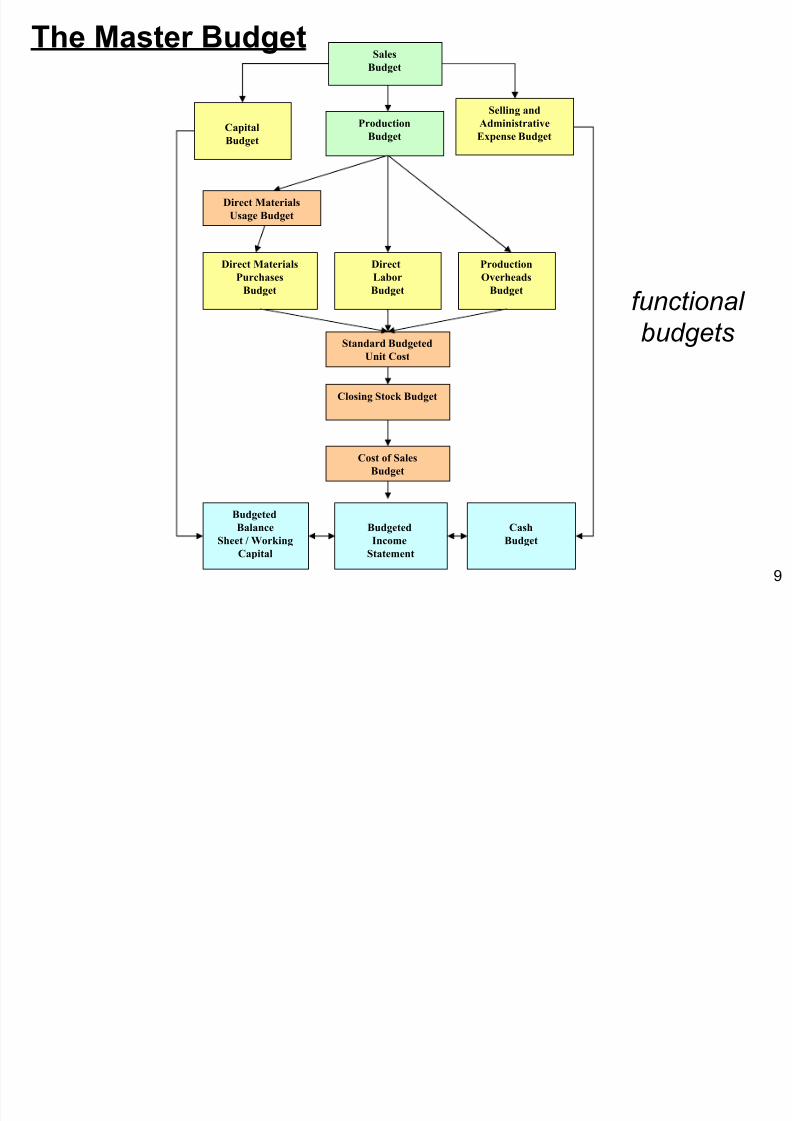

Budgeting

The Chartered Institute of ManagementAccountants defines a budget as ‘a financial

and/or quantified statement, prepared and

approved prior to a period, of the policy to be pursued during that period’.

From the Businessman's point-of-view it is a

financial plan of where the business wants tobe in the future and how it is to get there.

8/8/2019 W1 Lecture Power Point

http://slidepdf.com/reader/full/w1-lecture-power-point 9/30

8/8/2019 W1 Lecture Power Point

http://slidepdf.com/reader/full/w1-lecture-power-point 10/30

10

Advantages of budgeting

• It is an aid to planning

• It identifies the existence of any limiting factor

which restricts the performance of a business

• It co-ordinates the activities of the business and encourages teamwork

• It communicates the plans formulated by the senior

management team to all employees

• It motivates managers to achieve goals• It facilitates the evaluation of actual performance by

establishing a ‘bench-mark’.

8/8/2019 W1 Lecture Power Point

http://slidepdf.com/reader/full/w1-lecture-power-point 11/30

11

+

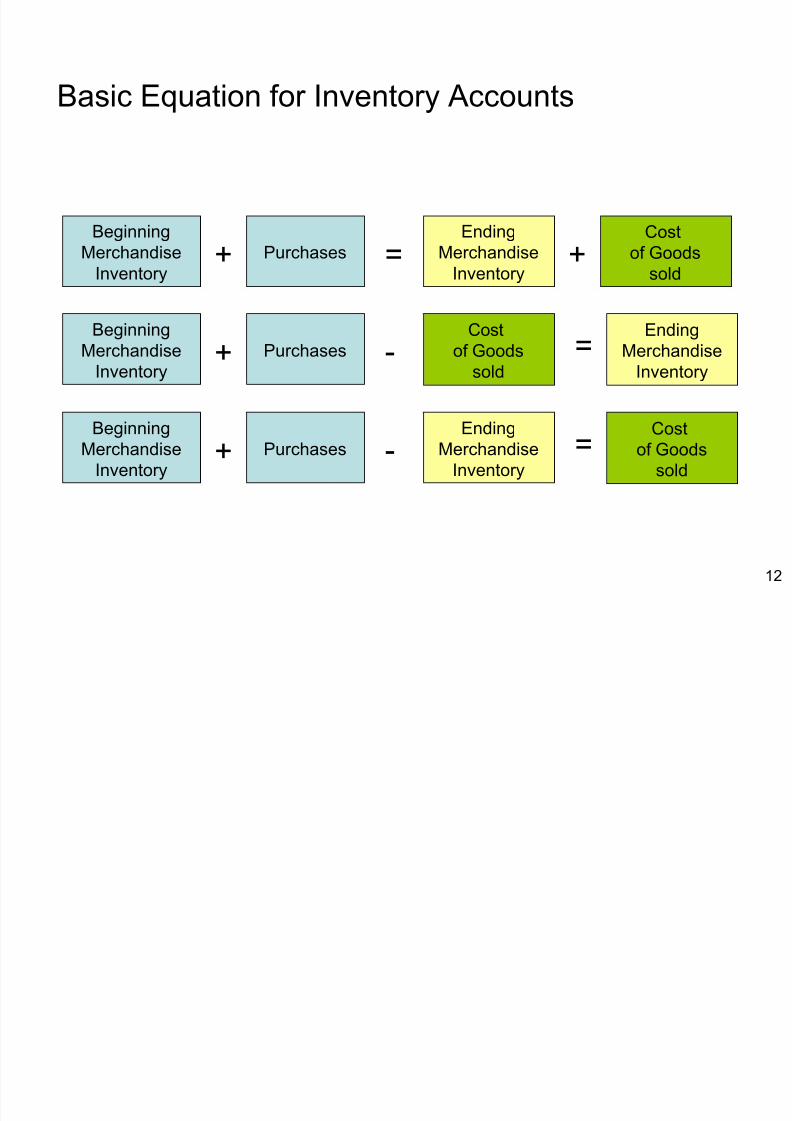

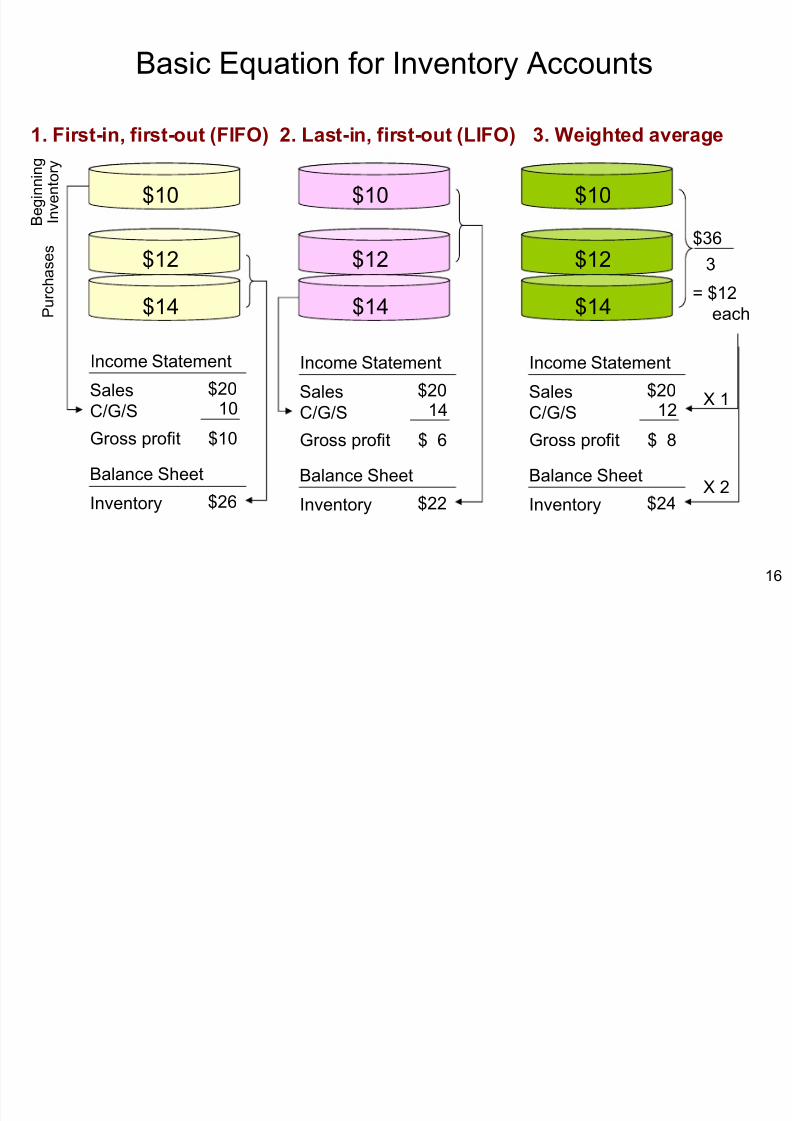

Basic Equation for Inventory Accounts

+

BeginningMerchandise

InventoryPurchases

Cost of Goodssold

EndingMerchandise

Inventory

Goods availablefor

Sale

8/8/2019 W1 Lecture Power Point

http://slidepdf.com/reader/full/w1-lecture-power-point 12/30

12

+

Basic Equation for Inventory Accounts

+Beginning

Merchandise

Inventory

PurchasesCost

of Goods

sold

EndingMerchandise

Inventory

=

+Beginning

MerchandiseInventory

PurchasesEnding

MerchandiseInventory

- =Cost

of Goodssold

+Beginning

MerchandiseInventory

PurchasesEnding

MerchandiseInventory

- =Cost

of Goodssold

8/8/2019 W1 Lecture Power Point

http://slidepdf.com/reader/full/w1-lecture-power-point 13/30

13

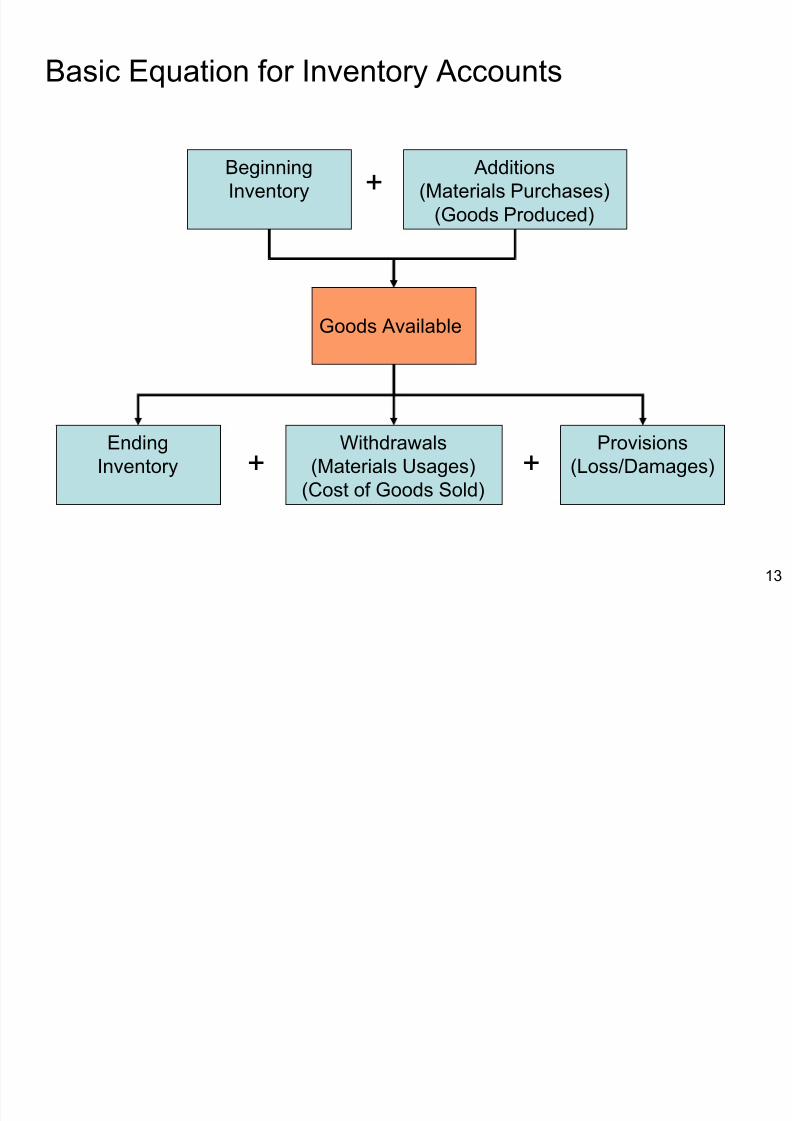

Basic Equation for Inventory Accounts

+

+

BeginningInventory

Additions(Materials Purchases)

(Goods Produced)

Withdrawals(Materials Usages)

(Cost of Goods Sold)

EndingInventory

Goods Available

Provisions(Loss/Damages)+

8/8/2019 W1 Lecture Power Point

http://slidepdf.com/reader/full/w1-lecture-power-point 14/30

14

Basic Equation for Inventory Accounts

Financial Statement

Cost of goods sold:

Beg. merchandise

inventory 14,200$

+ Purchases 234,150 Goods available

for sale

248,350$

- Ending

merchandise

inventory (12,100)

= Cost of goods

sold 236,250$

8/8/2019 W1 Lecture Power Point

http://slidepdf.com/reader/full/w1-lecture-power-point 15/30

15

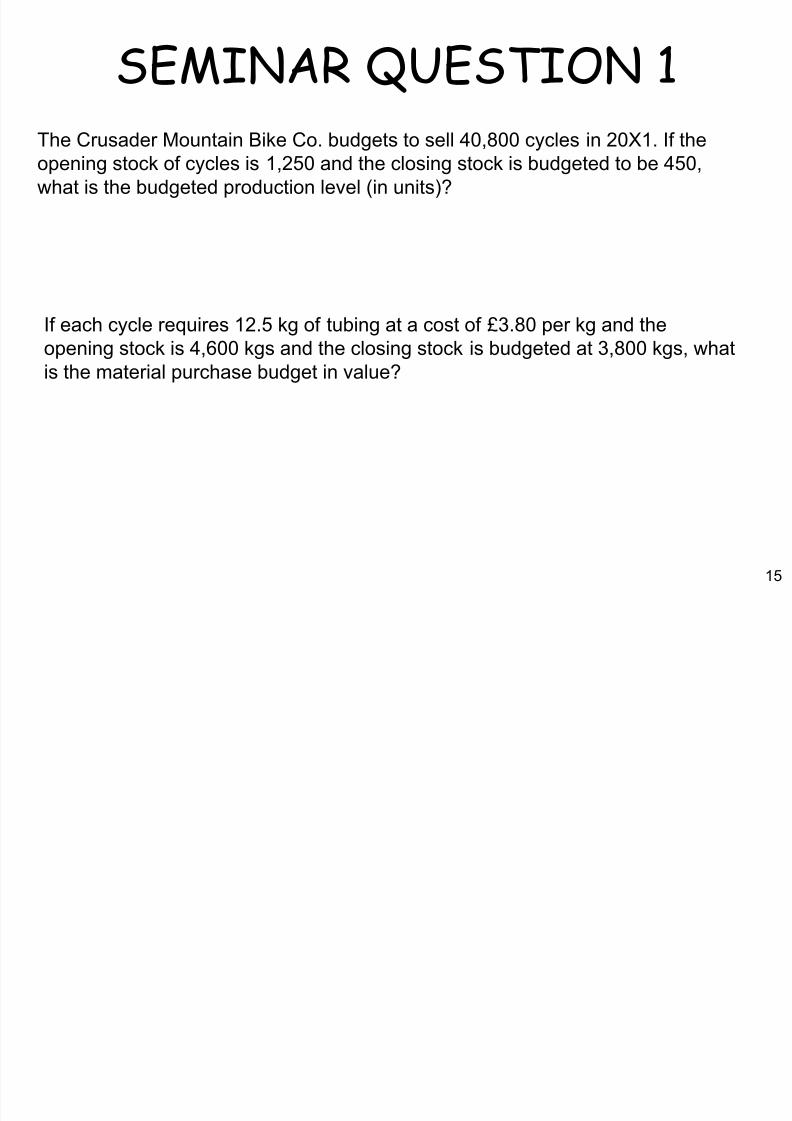

SEMINAR QUESTION 1

The Crusader Mountain Bike Co. budgets to sell 40,800 cycles in 20X1. If theopening stock of cycles is 1,250 and the closing stock is budgeted to be 450,what is the budgeted production level (in units)?

If each cycle requires 12.5 kg of tubing at a cost of £3.80 per kg and theopening stock is 4,600 kgs and the closing stock is budgeted at 3,800 kgs, whatis the material purchase budget in value?

8/8/2019 W1 Lecture Power Point

http://slidepdf.com/reader/full/w1-lecture-power-point 16/30

8/8/2019 W1 Lecture Power Point

http://slidepdf.com/reader/full/w1-lecture-power-point 17/30

17

Fixed vs Flexible Budget

Fixed Actual Flexed Variance

Activity

Variable costs (@$2)

Fixed costs

1,000

2,000

3,000

1,200

2,450

2,980

1,200

2,400

3,000

0

(50) U

20 F

Total 5,000 5,430 5,400 (30)U

U – Unfavorable F - Favorable

8/8/2019 W1 Lecture Power Point

http://slidepdf.com/reader/full/w1-lecture-power-point 18/30

18

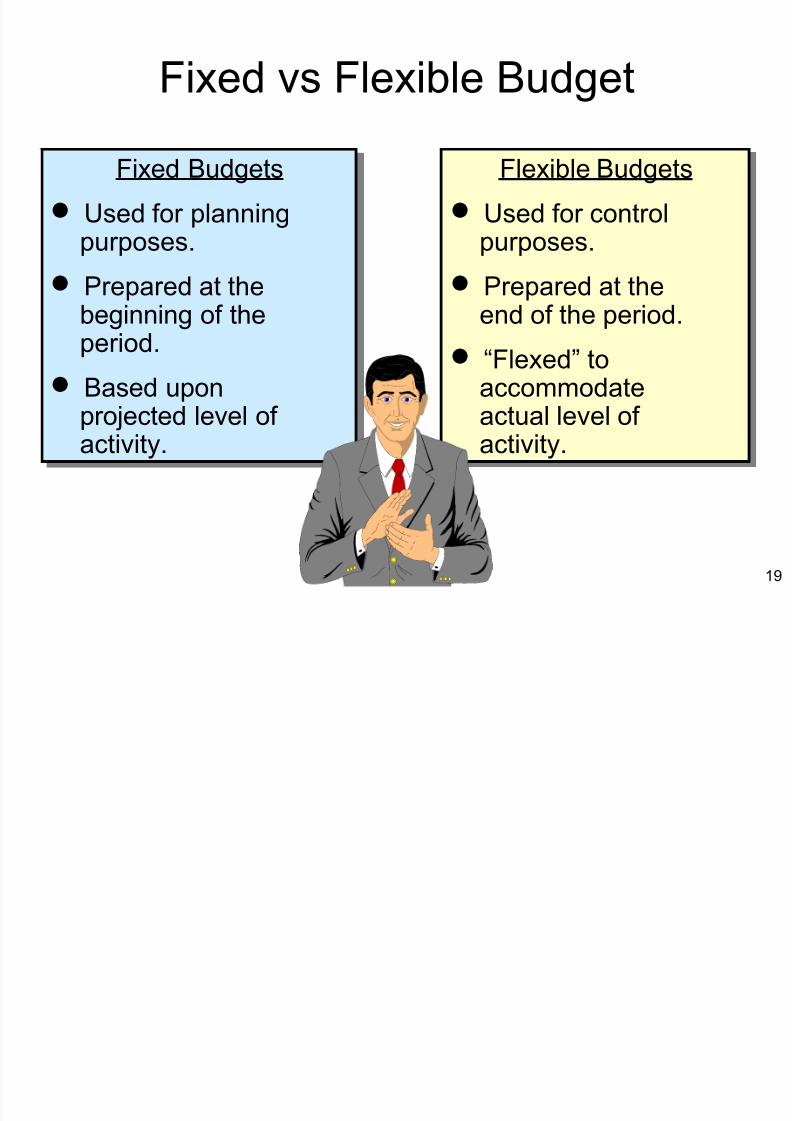

Fixed vs Flexible Budget

• A fixed budget is prepared at the beginning of the budgeting period and is valid for only theplanned level of activity.

• A flexible budget calculates budgets revenuesand budgeted costs based on the actual output

level in the budget period . It is prepared at theend of a period after the actual output level is

known.

8/8/2019 W1 Lecture Power Point

http://slidepdf.com/reader/full/w1-lecture-power-point 19/30

19

Fixed vs Flexible Budget

Fixed Budgets

Used for planningpurposes.

Prepared at thebeginning of theperiod.

Based upon

projected level of activity.

Fixed Budgets

Used for planningpurposes.

Prepared at thebeginning of theperiod.

Based upon

projected level of activity.

Flexible Budgets

Used for controlpurposes.

Prepared at theend of the period.

“Flexed” toaccommodate

actual level of activity.

Flexible Budgets

Used for controlpurposes.

Prepared at theend of the period.

“Flexed” toaccommodate

actual level of activity.

8/8/2019 W1 Lecture Power Point

http://slidepdf.com/reader/full/w1-lecture-power-point 20/30

20

Cash Budget

CASH RECEIPTS

Cash SalesFrom debtors ( Beginning Debtors + Credit Sales - Ending Debtors)

CASH PAYMENTS

To creditors (Beginning Creditors + Credit Purchases - EndingCreditors)

Cash expenses

NET INFLOW/OUTFLOW OF CASH = Cash receipts – cash payments

CLOSING BALANCE = Beginning Balance + Net Inflow/Outflow of Cash

8/8/2019 W1 Lecture Power Point

http://slidepdf.com/reader/full/w1-lecture-power-point 21/30

21

• Managers responsible for costs in their own cost

centres to achieve their budgeted goals

• Gives high level of motivation, provided

favourable and unfavourable variances are

equally considered

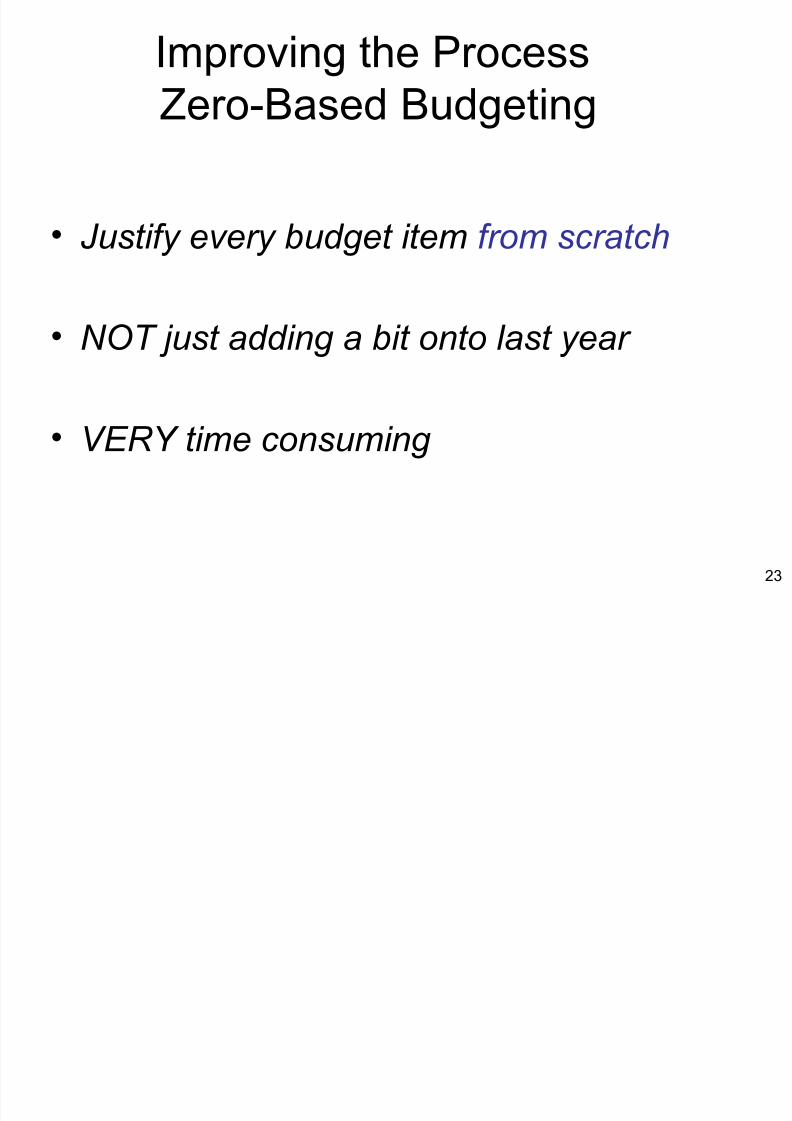

Improving the ProcessResponsibility Accounting

8/8/2019 W1 Lecture Power Point

http://slidepdf.com/reader/full/w1-lecture-power-point 22/30

22

• Recognises the impact on the budget as soon as

a commitment is made – when an order is

placed

• Rather than waiting until goods are actually paid

for

Improving the ProcessCommitment Accounting

8/8/2019 W1 Lecture Power Point

http://slidepdf.com/reader/full/w1-lecture-power-point 23/30

8/8/2019 W1 Lecture Power Point

http://slidepdf.com/reader/full/w1-lecture-power-point 24/30

24

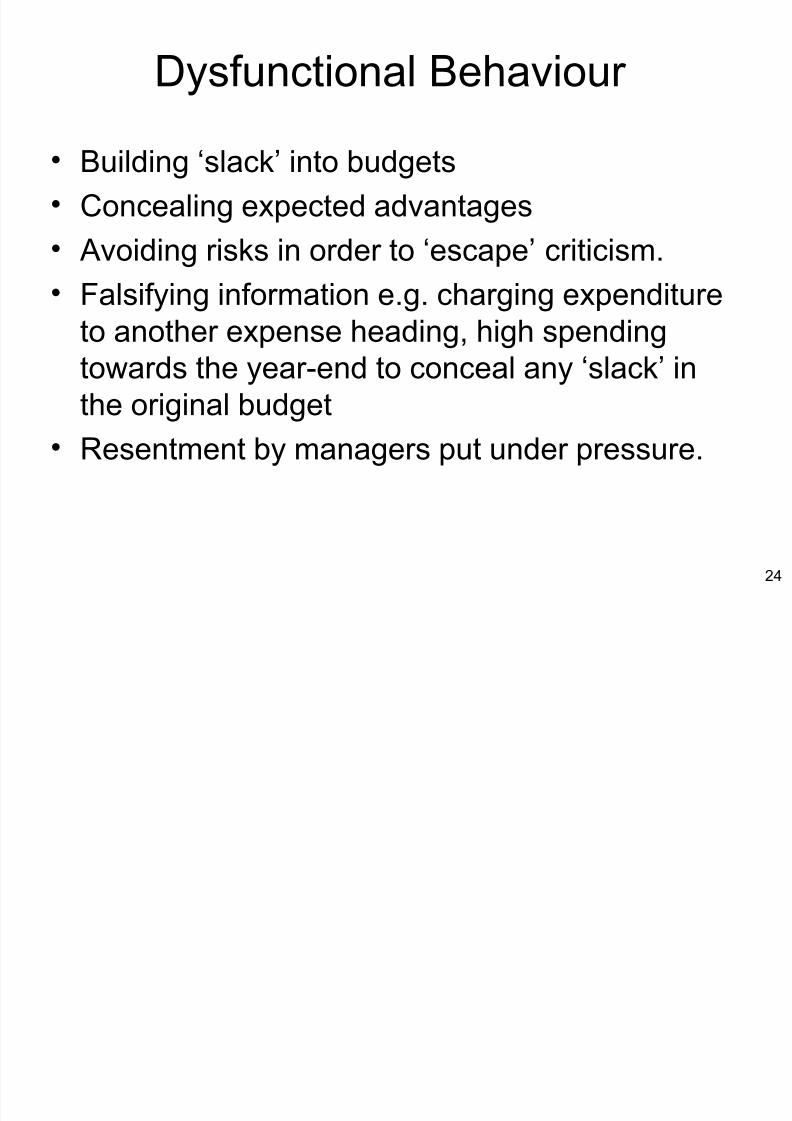

• Building ‘slack’ into budgets

• Concealing expected advantages

• Avoiding risks in order to ‘escape’ criticism.

• Falsifying information e.g. charging expenditureto another expense heading, high spendingtowards the year-end to conceal any ‘slack’ in

the original budget• Resentment by managers put under pressure.

Dysfunctional Behaviour

8/8/2019 W1 Lecture Power Point

http://slidepdf.com/reader/full/w1-lecture-power-point 25/30

25

Source Short-term

(< 2 years)

long-term

(> 2 years)

Internal •Efficient working

capital management

•Retained profits

External •Bank overdrafts •Share capital•Long-term loans•Leasing of assets

Sources of Finance

8/8/2019 W1 Lecture Power Point

http://slidepdf.com/reader/full/w1-lecture-power-point 26/30

26

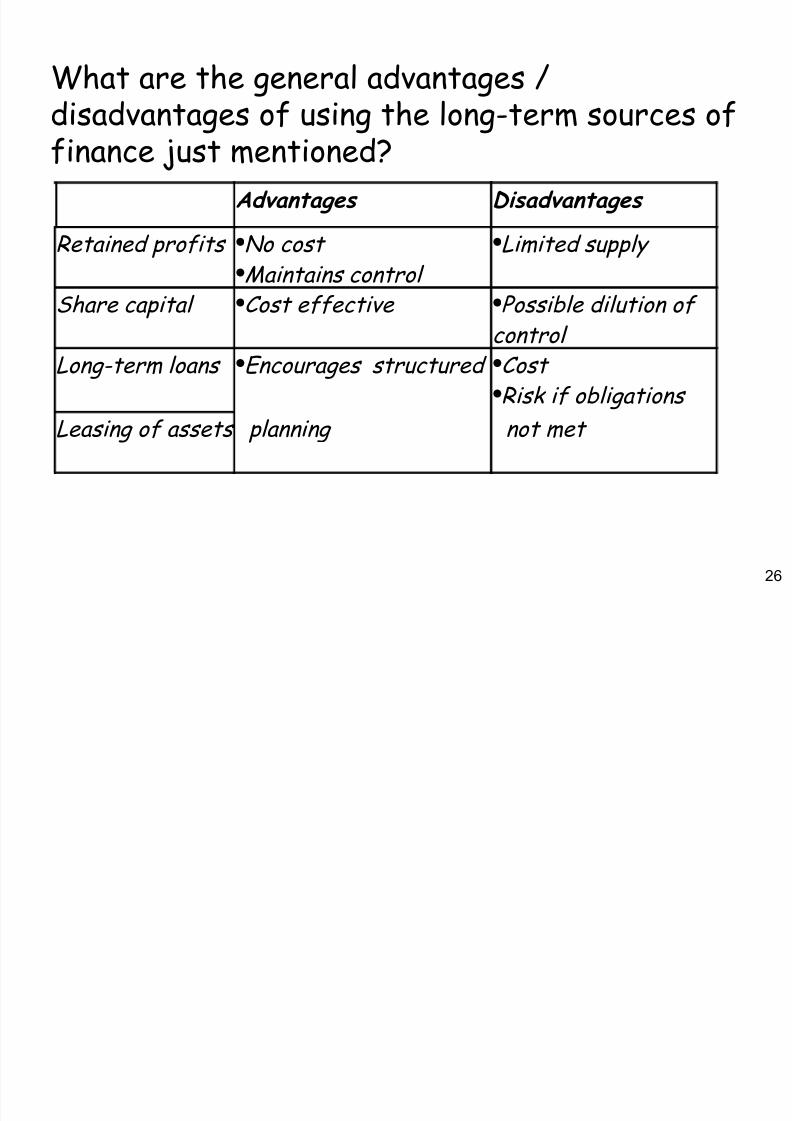

What are the general advantages /disadvantages of using the long-term sources offinance just mentioned?

Advantages Disadvantages

Retained profits •No cost •

Maintains control

•Limited supply

Share capital •Cost effective •Possible dilution of

control

Long-term loans •Encourages structured •Cost •Risk if obligations

Leasing of assets planning not met

8/8/2019 W1 Lecture Power Point

http://slidepdf.com/reader/full/w1-lecture-power-point 27/30

27

• Unstructured expansion

• Capital base too small for its expanded

levels of activity

• Profitable but insufficient funds to finance

working capital/fixed assets

Overtrading

8/8/2019 W1 Lecture Power Point

http://slidepdf.com/reader/full/w1-lecture-power-point 28/30

28

• Serious liquidity problems – cannot pay suppliers

• Diversion of management into dealing with

liquidity and not other business areas• Increased interest charges

• Inability to buy in bulk

• Cannot replace old fixed assets

Consequences of Overtrading

8/8/2019 W1 Lecture Power Point

http://slidepdf.com/reader/full/w1-lecture-power-point 29/30

29

Seminar 2: Questions 1 – 5

Students are required to hand in

solutions to the assigned exercises at

the beginning of the tutorial sessions.

Tutorial Exercise

8/8/2019 W1 Lecture Power Point

http://slidepdf.com/reader/full/w1-lecture-power-point 30/30

End ofWeek 1

Lecture