webcast: results announcement - 3rd quarter 2007 (brazilian corporate law)

TRANSCRIPT

Almir BarbassaCFO and Investor Relations OfficerNovember 13th 2007

Conference Call / WebcastResults Announcement

3rd Quarter 2007(Brazilian Corporate Law)

The presentation may contain forecasts about future events. Such forecasts merely reflect the expectations of the Company's management. Such terms as "anticipate", "believe", "expect", "forecast", "intend", "plan", "project", "seek", "should", along with similar or analogous expressions, are used to identify such forecasts. These predictions evidently involve risks and uncertainties, whether foreseen or not by the Company. Therefore, the future results of operations may differ from current expectations, and readers must not base their expectations exclusively on the information presented herein. The Company is not obliged to update the presentation/such forecasts in light of new information or future developments.

The United States Securities and Exchange Commission permits oil and gas companies, in their filings with the SEC, to disclose only proved reserves that a company has demonstrated by actual production or conclusive formation tests to be economically and legally producible under existing economic and operating conditions. We use certain terms in this presentation, such as oil and gas resources, that the SEC’s guidelines strictly prohibit us from including in filings with the SEC.

Cautionary Statement for US investors

Disclaimer

3

Caxaréu and Pirambu

Tested Wells

Tupi AreaTupi Area

BMS-11 (Tupi)

BMS-9 and BMS-10

4

1,7971,789

2Q07 3Q07

Δ = 0.45%

Thou

s. b

pd

• Domestic Oil and NGL production slightly higher compared to the 2Q07;

• Expected growth lower than expected due primarily to scheduled stoppages and delays in the delivery of some production projects;

DOMESTIC OIL AND NGL PRODUCTION

5

Δ +33 thous. bpd

P - 34Jubarte

60,000 bpdDecember 06

Jan-Sept 2006 Jan-Sept 2007

1,7631,796

New Systems

Δ +203 thous. bpd

Existing Systems*

Δ -170 thous. bpd

FPSO – Cidade do Rio de JaneiroEspadarte

100,000 bpdJanuary 07

FPSO - CapixabaGolfinho

100,000 bpdMay 06

P - 50Albacora Leste

180,000 bpdApril 06

* Natural decline and production stoppages

203Total New Systems

2828-FPSO-Cidade do Rio de Janeiro (Espadarte)

4040-P-34 (Jubarte)

183820FPSO-Capixaba (Golfinho)

11714831P-50 (Albacora Leste)

Change9M07 (thous. bpd)9M06 (thous. bpd)Unity

DOMESTIC OIL AND NGL PRODUCTION: MAIN PROJECTS IN 2006 AND 2007

6

PRINCIPAIS PROJETOS DE ÓLEO PARA O 4T07MAIN OIL PROJECTS IN THE 4Q07

Golfinho Module 2

FPSO Cidade de Vitória

• Capacity: 100 thous. bpd

• Wells:• 4 Producers• 3 Injectors

• Moored platform

• Fist Oil: Nov. 2007

• 2 wells in 2007

• Production peak: 1H08

Roncador Module 1A Phase 2

P-52

• Capacity: 180 thous. bpd• Wells:

• 18 Producers• 11 Injectors

• 2 gas lift manifolds• 1 self-supported rigid riser• Moored platform• First oil: Nov. 2007• 2 wells in 2007• Production peak: 2H08

Roncador Module 2

P-54

• Capacity : 180 thous. bpd

• Wells :•11 Producers• 6 Injectors

• Platform is being moored at the Roncador Field

• Fist Oil: Dec. 2007

• 1 well in 2007

• Production peak: 2H08

7

MAIN OIL PROJECTS IN 2008

Marlim Sul Module 2

• Capcity: 180 thous. bpd

• Wells:• 10 Producers• 9 Injectors

• First Oil: Jun. 2008

P-51

Marlim Leste

• Capacity : 180 mil bpd

• Well:• 14 Producers• 7 Injectors

• First Oil: Dec. 2008P-53

Jabuti

• Capacity: 100 thous. bpd

• Wells :• 8 Producers

• First Oil: Dec. 2008

FPSO Cidade de Niterói

1,8002,000

2007E 2008E

11.1%

Thou

s. b

pd

• New projects will add 460 thousand barrels/day of capacity;• These projects, along with those that will come online in the end of 2007, will contribute to reach the 2

million target in 2008.

8

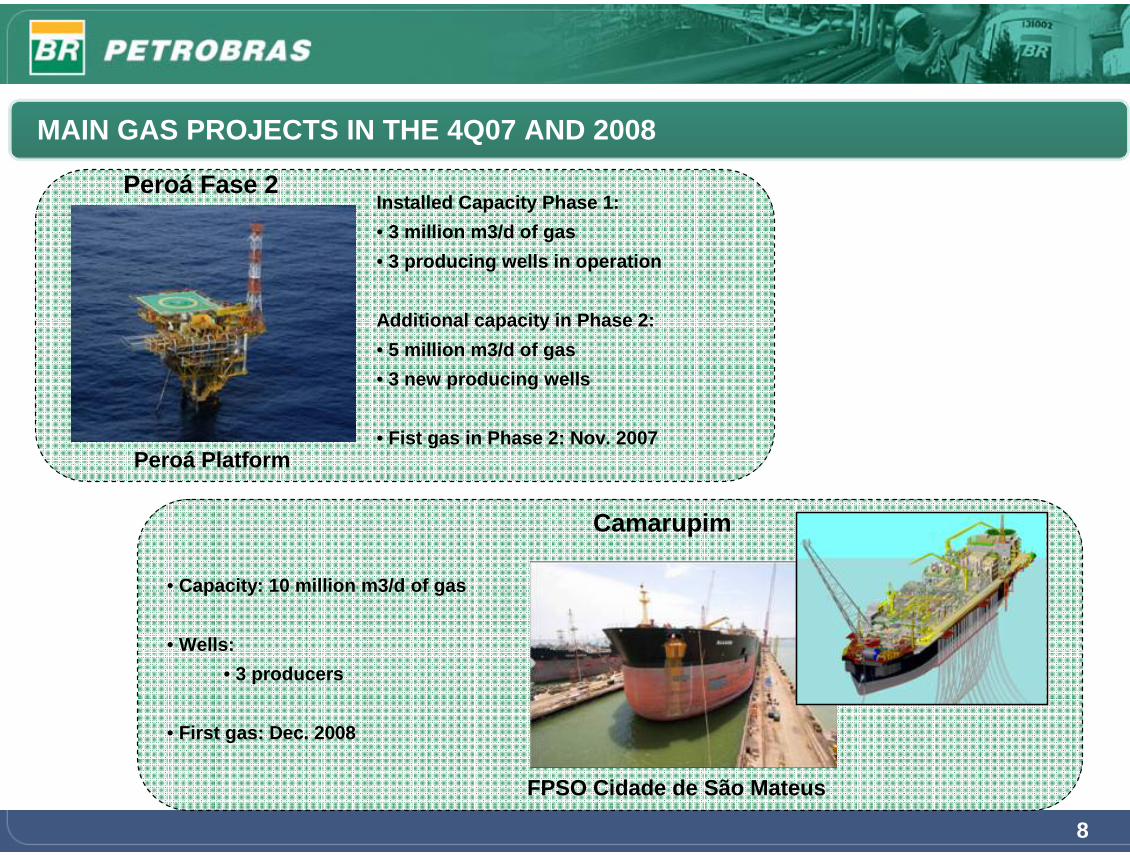

Peroá Fase 2Installed Capacity Phase 1: • 3 million m3/d of gas• 3 producing wells in operation

Additional capacity in Phase 2:• 5 million m3/d of gas• 3 new producing wells

• Fist gas in Phase 2: Nov. 2007Peroá Platform

MAIN GAS PROJECTS IN THE 4Q07 AND 2008

Camarupim

• Capacity: 10 million m3/d of gas

• Wells:• 3 producers

• First gas: Dec. 2008

FPSO Cidade de São Mateus

9

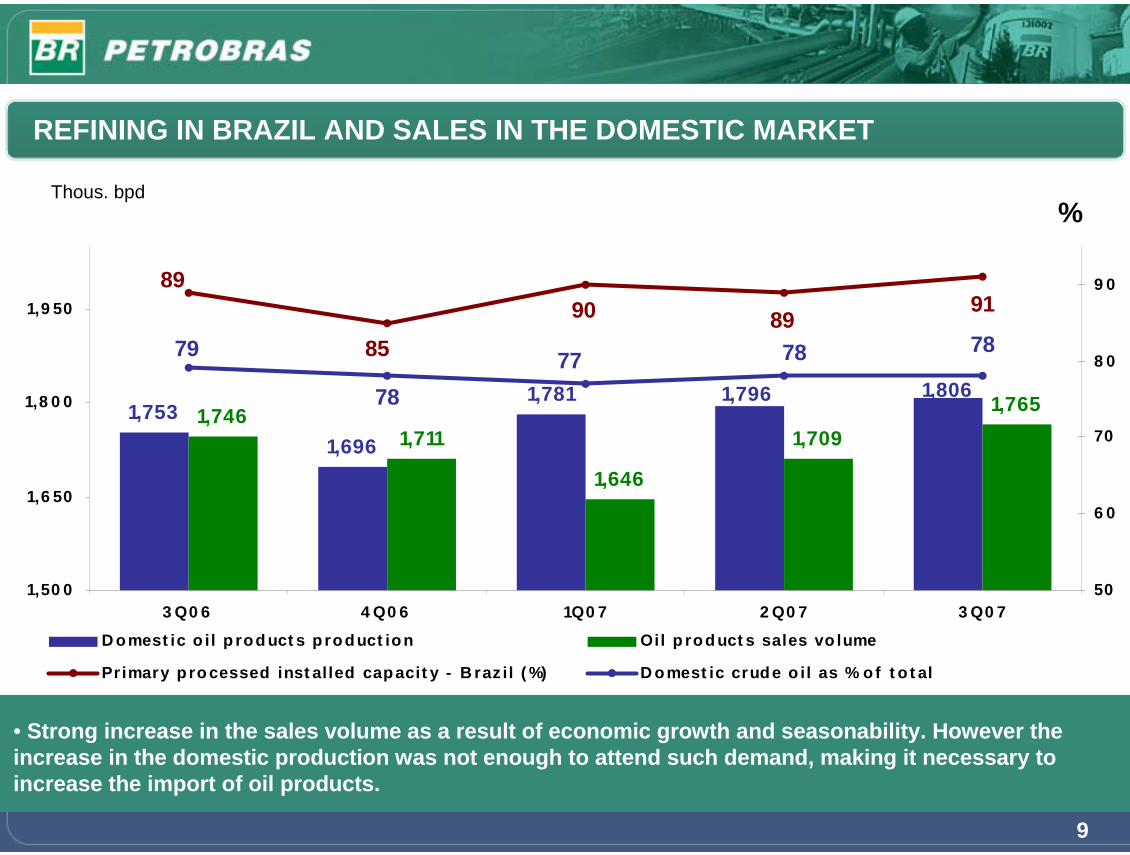

• Strong increase in the sales volume as a result of economic growth and seasonability. However the increase in the domestic production was not enough to attend such demand, making it necessary to increase the import of oil products.

%

1,7531,696

1,7811,746

1,711

1,646

1,7091,7651,796 1,806

899085

8991

787879 7778

1,50 0

1,6 50

1,8 0 0

1,9 50

3 Q0 6 4 Q0 6 1Q0 7 2 Q0 7 3 Q0 750

6 0

70

8 0

9 0

D omest ic o il p rod uct s p roduct ion Oil p rod uct s sales vo lume

Primary p ro cessed inst alled capacit y - B raz il ( %) D omest ic crude o il as % o f t o t al

Thous. bpd

REFINING IN BRAZIL AND SALES IN THE DOMESTIC MARKET

10

DOWNSTREAM- CONVERSION PROJECTS (COKING UNITS)

Objective:

• Increase production of light oil products instead of fuel oil.

• Allow the processing of heavy oil from Campos Basin with no additional production of fuel oil.

• Profitability increase.

REDUCStatus: Work in progress

Startup: 2008

Capacity: 31.5 thous. bpd

REVAPStatus: Work in progress

Startup : 2009

Capacity : 31.5 thous. bpd

REPARStatus : Work in progress

Startup : 2010

Capacity: 31.5 thous. bpd

• New delayed coking projects will allow the additional production of 47 thousand barrels/day of diesel, while decreasing the fuel oil production by

61 thousand barrels/day.

8,000 bbl/dREVAP – Coke

14,000 bbl/dREPAR - Coke

9,000 bbl/dREDUC – Coke

IncreaseProject

Increase in National Oil Processing due to coker projects(2008-2020 average)

11

RESULTS DRIVERS – MARGINS

Aver. 3Q06

$8.5/bbl

0,00

5,00

10,00

15,00

20,00

25,00

30,00

Mar-06 Jun-06 Set-06 Dez-07 Mar-07 Jun-07

WTI Cracking USGC

Set-07

Aver.3Q07

$8.8/bbl

Aver. 2Q07

$14.9/bbl

74.9

68.8

57.859.7

48.7

47.8

57.0

64.4

4T06 1T07 2T07 3T07

Brent (average) Average Sales Price

-41%$11.8

$10.5

US$

/bar

rel

• Compared to the 2Q07, international refining margins declined substantially;

• During 3Q07 there was a substantive increase in oil prices, improving E&P results. This increase, however, together with stability in oil product prices (in Reais), was responsible for the sharp decrease in refining margins.

Source: Petrobras

12

AVERAGE REALIZATION PRICE - ARP

20

40

60

80

100

Dec-05 Mar-06 Jun-06 Sep-06 Dec-06 Mar-07 Jun-07 Sep-07

A R P B rasil ( U S$/ bb l)A verag e B rent Price ( U S$/ bb l)A R P U SA ( U S$/ b b l w/ sales vo l. in B rasil)

82.4

68.7

78.2

2Q07Aver.

3Q06Aver.

72.3

69.5

81.1 85.6

74.9

81.1

3Q07Aver.

• Petrobras continuously monitors international price trends in order to maintain its pricing aligned in the medium / long term.

13

6,800

11,535

14,190

24,489

41,798

5,528

10,272

13,061

27,264

44,469

Net Income

Operational Profit

EBITDA

GOGS

Net Revenues

2Q07 3Q07

INCOME STATEMENT 3Q07 VS 2Q07

• Net Revenues increased compared to the previous quarter mainly due to higher sales volumes of oil products;

• Costs negatively affected by higher expenditure with oil and oil products imports; • Operational and net results were impacted not only by the decrease of refining margins, but also by

higher expenses (next slide).

-18.7%

6.4%

-10.9%

-8.0%

11.3%

R$

mill

ion

14

1,239

452

391

1,498

1,443

1,404

1,147

453

1,555

1,635

Others

Pension and HealthPlan

Exploratory Costs

General andAdministrative

Sales Expenses

2Q07 3Q07

OPERATIONAL EXPENSES ANALYSIS 3Q07 VS 2Q07

R$

mill

ion

• Operational Expenses were particularly affected by the increase of expenditures with the Pension Plan (Petros). Such expenses (R$ 695 million) were due to commitments related to the Petros Agreement and are not recurrent;

• The increase in sales expenses was a result of substantially higher sales volumes.

13.3%

15.9%

3.8%

13.3%

153.8%

15

LIFTING COSTS INCLUDING GOVERNMENT PARTICIPATION

15.46 15.20 14.45 14.66

22.2918.92 20.58

23.26

0

10

20

30

40

4Q06 1Q07 2Q07 3Q07

Lifting Cost (R$) Gov. Take (R$)

7.24 7.20 7.33 7.65

10.35 9.0410.62

12.48

74.968.8

57.859.7

0

10

20

30

4Q06 1Q07 2Q07 3Q070

20

40

60

80

Lifting Cost (US$) Gov. Take (US$) Brent

US$

/bar

rel

R$/

barr

el

20.1317.95

16.2517.59

37.9235.0334.12

37.75

• Government take and lifting costs highly correlated to Brent prices

16

CHANGE IN QUARTER REVENUES (3Q07 VS 2Q07)Exploration & Production – Operating Profit Change– R$ million

• Better E&P result is due to higher oil prices and slightly higher production.

10.024

1.527637

44 11.436420

986

2Q07 Oper. Profit Price Effect onNet Revenue

Volume Effect onNet Revenue

Avrg Cost Effecton COGS

Volume Effect onCOGS

Oper. Exp. 3Q07 Oper. Profit

1,7971,789 Domestic Production of Oil, NGL and Condensate (thous. bpd)

17

CHANGE IN QUARTER REVENUES (3Q07 VS 2Q07)

• Despite the increase in sales volume, the Downstream result was directly affected by lower refining margins. There was a strong increase in acquisition prices for oil and oil products and imported volumes, with stable ARP in Reais.

3.358338

1.936

7 1.893

776

916

2Q07 Oper.Profit

Price Effect onNet Revenue

Volume Effecton Net

Revenue

Avrg CostEffect on

COGS

Volume Effecton COGS

Oper. Exp. 3Q07 Oper.Profit

Downstream – Change in Operating Profit – R$ million

18

NET INCOME CHANGE – R$ million (3Q07 VS 2Q07)

• Despite the elevated operating revenues in the quarter, which increased due to economic growth and seasonality, the high costs of the downstream segment led to lower refining margins, which, together with the increase of expenditures with the pension plan Petros, resulted in a net income below the previous quarter.

1,7971,789 Domestic Oil, NGL and Condensate – thousand bpd

6,800

2,671 2,775

1,159

184 389 214 5,528

2Q07 NetIncome

Revenues COGS Oper. Exp. Fin. Exp andNon Oper.

Taxes Minority Inter.and Particip. inEquity Income

3Q07 NetIncome

19

INVESTMENTS

• By 09.30.2007, total capital spending reached R$ 30,606 million, representing an increase of 35% over the year to date amount for the similar period in 2006.

2007 % 2006 % %• Direct Investments 26,060 87 20,264 90 29 Exploration and Production 14,295 48 11,404 51 25 Downstream 4,607 15 2,800 13 65 Gas and Energy 1,057 4 1,203 5 (12) International 4,867 16 3,923 17 24 Distribution 702 2 477 2 47 Corporate 532 2 457 2 16 • Special Purpose Companies (SPC) 4,205 14 2,072 9 103 • Ventures under Negotiation 341 1 300 1 14 • Structured Projects - - 1 - - Exploration and Production - - 1 - (100) Total Investments 30,606 100 22,637 100 35

R$ millionJan-Sep

20

19%17%

18%17%

18%

24%

20%

16%

Dec-05 Mar-06 Jun-06 Sep-06 Dec-06 Mar-07 Jun-07 Sep-07

Net Debt/Net Capitalization

LEVERAGE

(1) Inclui endividamento contraído através de contratos de Leasing (R$ 1.631 milhões em 30.09.2007 e R$ 1.980 milhões em 30.06.2007).(2) Endividamento Total – Disponibilidades

• 12% increase in net debt during the quarter as a consequence of the reduction of cash/cash equivalents in long term bonds (R$2,909 million), to counterbalance the liabilities with Petros.

Petrobras’ Leverage Ratio

R$ million 09/30/2007 06/30/2007Short Term debt (1) 10,519 10,720Long Term Debt (1) 28,230 29,100

Total Debt 38,749 39,820

Cash and Cash Equivalents 14,216 17,854

Net Debt (2) 24,533 21,966

21

Total Shareholder's Return

15.8%

7.5%

6.0%

6.0%

5.8%

95.7%

36.1%

85.7%

44.5%

79.2%

30.2% 31.5%39.5%

22.8%28.0%

85.2%91.5%

50.5%43.6%

111.5%

0%

20%

40%

60%

80%

100%

120%

2003 2004 2005 2006 9M 07

Shares Increase Dividends Amex Oil Index (*)

Source: Bloomberg (PBR) * includes dividends for comparison

SHAREHOLDER’S RETURN

22

QUESTION AND ANSWER SESSIONVisit our website: www.petrobras.com.br/ri

For more information contact:Petróleo Brasileiro S.A – PETROBRAS

Investor Relations Department

E-mail: [email protected]. República do Chile, 65 – 22o floor

20031-912 – Rio de Janeiro, RJ(55-21) 3224-1510 / 3224-9947