webinar slides: eye on washington - quarterly business tax update, 2014 q4

TRANSCRIPT

CBIZ & MHM Executive Education Series™

Eye on Washington: Quarterly Business Tax Update

January 21, 27 and 28, 2015

Presented by: Stephen C. Henley, CPA National Tax Practice Leader, CBIZ MHM, LLC William M. Smith, Esq. Managing Director, CBIZ MHM, LLC National Tax Office

2 #CBIZMHMwebinar #CBIZMHMwebinar

To view this webcast in full screen mode, click on view options in the upper right hand corner.

Click the Support tab for technical assistance.

If you have a question during the presentation, please use the Q&A feature at the bottom of your screen.

Before We Get Started…

3 #CBIZMHMwebinar #CBIZMHMwebinar

This webcast is eligible for CPE credit. To receive credit, you will need to answer periodic participation markers throughout the webcast.

External participants will receive their CPE certificate via email immediately following the webcast.

CPE Credit

4 #CBIZMHMwebinar

Today’s Presenters

Stephen C. Henley , CPA Senior Managing Director, CBIZ MHM 770.858.4443 | [email protected] Steve has 30 years experience in serving the tax needs of clients in a variety of industries including retail, distribution and manufacturing, services, technology and communications. In serving as lead tax engagement executive, Steve’s focus is identifying and executing value creating strategies to meet the needs of his clients in a variety of technical areas, such as revenue recognition, acceleration of deductions, research and experimentation credits, state and local tax minimization, M&A tax structures, international tax planning and tax implications of compensation programs.

William M. Smith, Esq. Managing Director, CBIZ National Tax Office 301.951.3636 | [email protected] Bill Smith is a managing director in the CBIZ National Tax Office. Bill monitors federal tax legislation and consults nationally on a broad range of foreign and domestic tax services for businesses and individuals, including mergers and acquisitions, domestic and international investments or divestitures, and the review, negotiation and drafting of tax aspects of business agreements.

5 #CBIZMHMwebinar

Agenda

Post Year-End Tax Planning Tangible Property Regulations Cost Segregation

Legislative Updates Changes to Tax Writing Committees Rhetoric State of the Union Comprehensive Tax Reform Happy New Year – What’s Been Done Already Extender Legislation ACA Updates

6 #CBIZMHMwebinar

Agenda

Administrative Updates Budget Woes Year-End Bonuses PLR 201445010: Software licensing income qualified

as domestic production gross receipts for DPAD Proposed regulations on treatment of partner’s interest

in partnership/LLC’s unrealized receivables and inventory items (“Hot Assets”)

Guidance on SE tax treatment of LLC income Reporting of Payments to LLCs IRS Reefer Madness

7 #CBIZMHMwebinar

Agenda

Cases King v. Comm’r Supreme Court to Hear ACA Appeal Mingo v. Comm’r (5th Cir. 2014) – installment method

for hot assets Long v. Comm’r (11th Cir. 2014) – sale of contract

rights Mylan, Inc. v. Comm’r (Tax Court petition) – sale or

license?

POST YEAR-END TAX PLANNING

9 #CBIZMHMwebinar

Tangible Property Regulations Process to ensure compliance Protective 3115 Filings Depreciation review

Cost Segregation

Fixed Asset Issues

LEGISLATIVE UPDATES

11 #CBIZMHMwebinar

Senate Finance Orrin Hatch (R – Utah) taking over Favors revenue neutrality, geographic tax system (tax

earnings where earned) 14 Republicans; 12 Democrats

House Ways and Means Camp (R- Mich) retired Paul Ryan (R – Wis) taking over Applauded Rep. Camp’s tax reform proposal Will use Camp proposal as a “Marker,” not necessarily as a

starting point 35 Republicans; 15 Democrats (Van Hollen, D-Md, bumped)

Tax Writing Committees

11

12 #CBIZMHMwebinar

Obama Wants a “serious attempt at tax reform” in 2015 – “The tax

area is one area where we can get things done.” Corporate reform must be offset by eliminating

“unspecified” loopholes Aware that some companies are paying “full freight” 35% Met with Congressional leaders January 13 No discussions in advance of proposals in the State

of the Union address January 20 Democrats pushed tax breaks for middle class Republicans silent on whether they will address

corporate tax rate reduction without individual/pass-through rates addressed

Tax Reform Rhetoric

12

13 #CBIZMHMwebinar

Increase capital gains and dividend rates from 23.8% (with NIIT) to 28% (rate was 15% when Obama took office)

Impose capital gains tax on asset transfers at death (closing “largest single loophole” – the “stepped-up basis”) No tax until death of second spouse First $200,000 exempt for couples with automatic portability, and

$100,000 for individuals Home exempt up to $500,000 for couples with automatic portability

($250,000 individuals) All personal property, except art and collectibles, exempt Delay tax on family owned businesses until sold Current estate tax exemption up to $10.86 million per couple

80% of taxes will be paid by top 0.1% of households, 90% by top 1%

State of the Union

13

14 #CBIZMHMwebinar

Up to $500 credit for double earners, with phase out at family income between $120,000 and $210,000 (5% of first $10,000 of lower earner) 80% of two earner couples would benefit

Limit ability to contribute to retirement accounts worth $3.4 million or more ($210,000 annual income)

Increase maximum child care tax credit to $3,000 for families with children under 5 Make credit available for all families with income up to $120,000

Consolidate education breaks into one $2,500 annual credit for five years for students working towards degree

Tax on liabilities of largest financial institutions (7 basis points) to discourage excessive borrowing Would apply to roughly 100 firms with assets over $50 billion Similar to Camp proposal

State of the Union

14

15 #CBIZMHMwebinar

House Ways and Means – Paul Ryan (R – Wis) To lower rates, have to broaden base, meaning the

closure of loopholes Committee to hold retreat during week of January 19 Democrats on committee not invited Asking for timeline for passing comprehensive tax reform,

says it will be “pretty aggressive” Congress limited in undertaking “full throttle tax reform”

due to Obama’s opposition to lowering individual rates Both Committees plan to hold hearings on tax reform

in 2015

Tax Reform Rhetoric

15

16 #CBIZMHMwebinar

At the end of February 2014, Chairman of House Ways and Means Committee Dave Camp (R-Mich.) released discussion draft of a comprehensive tax reform bill

President Obama released his annual list of budget proposals a week after Camp’s proposal (March 2014) Over 80% of the tax proposals are the same as in last year’s

budget proposal

Obama and Camp on Tax Reform

16

17 #CBIZMHMwebinar

Camp Comprehensive Tax Reform

Top corporate tax rate of 25% (down from 35%)

Effective Actual Corporate Tax Rates By Selected Industry 2007-2008*

Industry Tax Rate

Agriculture, forestry, Fishing and Hunting 22% Mining 18% Utilities 14% Construction 31% Manufacturing 26% Wholesale and Retail Trade 31% Transportation and Warehousing 19% Information 25% Insurance 25% Finance & Holding Companies 28% Real Estate 23% Leasing 18% All Services 29% Average Effective Actual Tax Rate 26%

*Source: U.S. Treasury, Office of Tax Analysis

17

18 #CBIZMHMwebinar

Camp Comprehensive Tax Reform: Other

Corporate NOL limited to 90% of taxable income Software development / R&D amortized over 5 years Most businesses with gross receipts > $10 million

required to use accrual basis Income required to be recognized no later than when

recognized for financial statement purposes

18

19 #CBIZMHMwebinar

Camp Comprehensive Tax Reform: Other

Repealed provisions would include (not all inclusive): Accelerated depreciation DPAD (phased out over several years) Corporate AMT Exception to $1 million compensation deduction limit for stock

options, commissions, etc.

19

20 #CBIZMHMwebinar

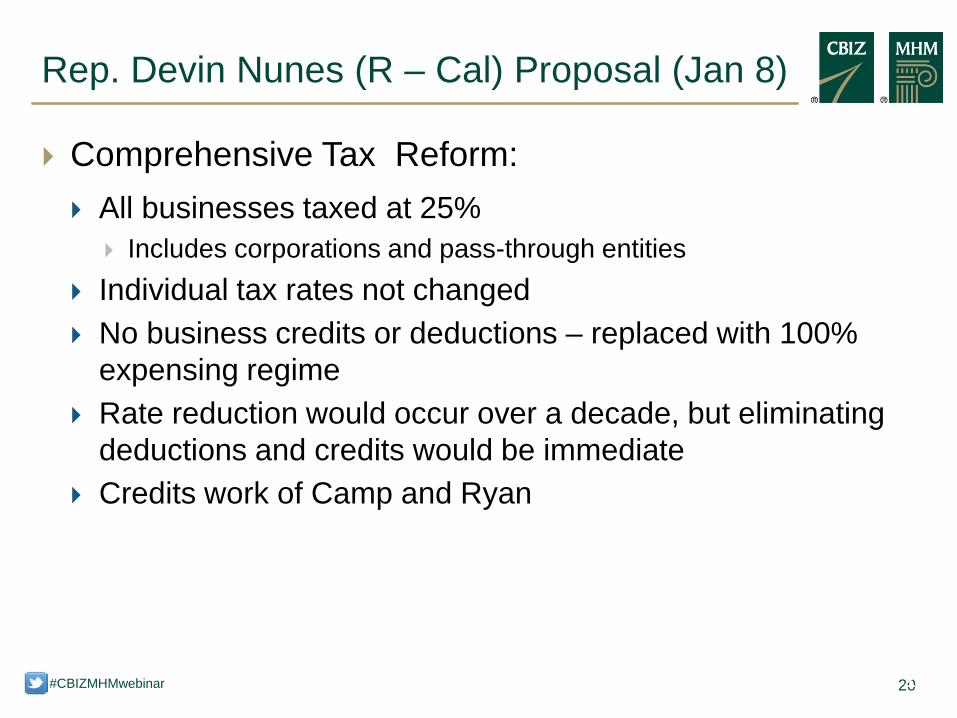

Rep. Devin Nunes (R – Cal) Proposal (Jan 8)

Comprehensive Tax Reform: All businesses taxed at 25%

Includes corporations and pass-through entities Individual tax rates not changed No business credits or deductions – replaced with 100%

expensing regime Rate reduction would occur over a decade, but eliminating

deductions and credits would be immediate Credits work of Camp and Ryan

20

21 #CBIZMHMwebinar

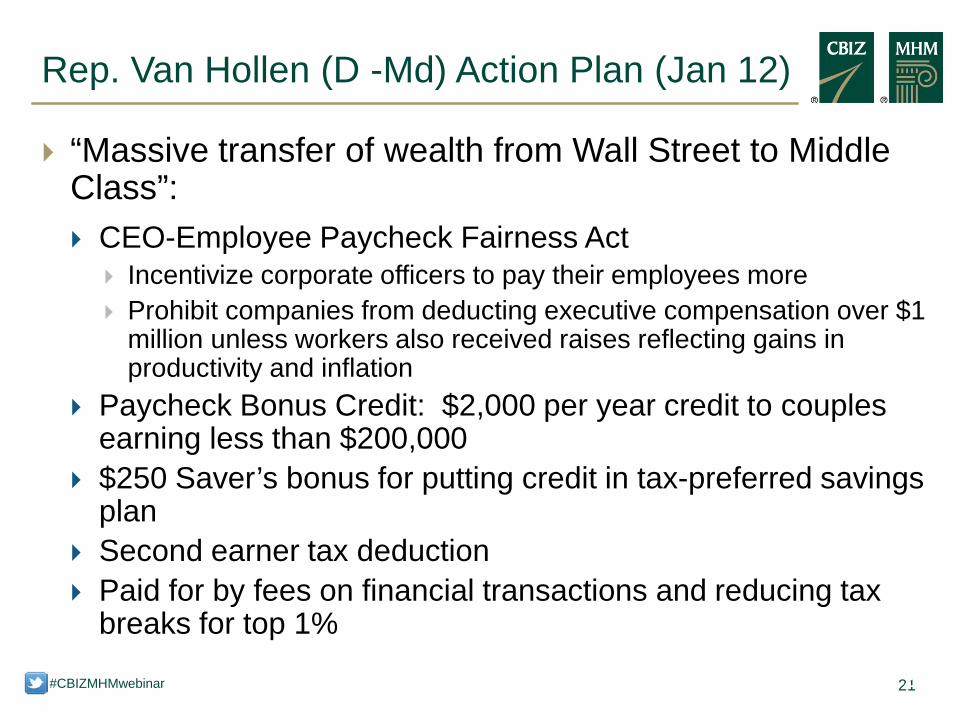

Rep. Van Hollen (D -Md) Action Plan (Jan 12)

“Massive transfer of wealth from Wall Street to Middle Class”: CEO-Employee Paycheck Fairness Act

Incentivize corporate officers to pay their employees more Prohibit companies from deducting executive compensation over $1

million unless workers also received raises reflecting gains in productivity and inflation

Paycheck Bonus Credit: $2,000 per year credit to couples earning less than $200,000

$250 Saver’s bonus for putting credit in tax-preferred savings plan

Second earner tax deduction Paid for by fees on financial transactions and reducing tax

breaks for top 1%

21

22 #CBIZMHMwebinar

Other Activity in Opening Days of the 114th

House adopts dynamic scoring of tax legislative proposals Intended to take into account the projected

macroeconomic effects the legislation will have on the economy

CBO and JCT will be required to estimate changes to Employment Available capital “Other economic variables”

Applies only to “large” bills – must affect ¼ of a percentage point of GDP

Senate has not signaled whether it will follow suit Potentially two sets of rules for same legislation

22

23 #CBIZMHMwebinar

Other Activity in Opening Days of the 114th

ACA Changes House passes bill to define “Full time” under ACA as 40

hours per week instead of 30 12 Democrats joined all House Republicans

Repeal of “medical device excise tax” legislation introduced in Senate on January 13 A Med Tech Ass’n claimed tax cost 33,000 jobs in first year Letter of support signed by 1,000 corporations

Obama says he will veto changes Neither House nor Senate had enough Republican

votes to override veto

2

24 #CBIZMHMwebinar

House and Senate passed one year Extender Package,

signed by Obama Dec. 16 All provisions expired again on Dec. 31 Will cost approx. $41.6B through 2024

House Bill H.R. 5771: One Year Extender

24

25 #CBIZMHMwebinar

Business tax provisions that expired at end of 2013 and were extended through 2014 include: Research and experimentation credit; Work opportunity tax credit; Increase in expensing to $500,000/$2,000,000 and expanded

definition of §179 property; Bonus depreciation; Exceptions under Subpart F for active financing income; Look-through treatment of payments between controlled foreign

corporations (“CFC ”); Special rules for qualified small business stock; Reduction in S corporation recognition period for built-in gains

tax; 15-year straight line cost recovery for qualified leasehold,

restaurant, and retail improvements

“Tax Extenders” - Expired Tax Provisions

25

26 #CBIZMHMwebinar

Affordable Care Act Update

Employer shared responsibility payment: Nondeductible excise tax on large employees who do not

provide affordable & adequate health coverage to full-time employees

Modifications: Delayed until 2016 for certain employers Percentage of employees who must be offered minimum essential

coverage decreased from 95% to 70% in 2015

Full-time Employees 2014 2015 2016 Less than 50 N/A N/A N/A 50 – 99 N/A N/A 95% 100 or more N/A 70% 95%

26

27 #CBIZMHMwebinar

ACA Update

Section 6055 requires reporting starting in 2016 for 2015 tax year.

Forms 1094-B and 1095-B already available No Penalties under Sections 6721 (information returns)

and 6722 (payee statements) will be imposed for 2015 returns on reporting entities that can show a good faith effort to comply.

House passed law that would allow employees who offered non-ACA compliant in 2013 to continue to offer those plans through 2018. Obama threatens veto.

27

ADMINISTRATIVE UPDATES

29 #CBIZMHMwebinar

The 2014 year-end spending deal passed by Congress dealt $346 million in budget cuts to the IRS. In its 2013 Report to Congress, the IRS’s Taxpayer Advocate

Service raised concerns about its funding limitations: “Since FY 2010, the IRS’s workload has grown, and its budget has been reduced by 8%. The combination of more work and less funding has predictably impaired the IRS’s performance.”

Hiring freeze has been initiated Approximately 15,000 fewer employees by end of 2015 vs.

2010 Predicted $2 billion less in collections Only 50% of taxpayer calls will be answered during filing

season Possible refund delays – especially paper filed

IRS Budget

29

30 #CBIZMHMwebinar

Taxpayer Advocate Report January 14 IRS Taxpayer Services is unlikely to answer even half the

100 million telephone calls it receives, and levels of service may average as low as 43%.

The IRS budget is experiencing a cut at a time when the IRS is receiving 11% more returns from individuals, 18% more returns from business entities, and 70% more telephone calls (through FY 2013) than a decade ago.

This year taxpayers are likely to receive the worst levels of taxpayer service since 2001

Fewer audits Inability to implement taxpayer ID theft protections

IRS Budget

30

31 #CBIZMHMwebinar

Employers have been lured into a false sense of security, believing that any compensation paid within 2 ½ months of year end for services provided in the prior year were deductible in the year the services were provided

IRS attacks on bonus accrual; examples: Forfeited Bonuses Revert Back to Taxpayer Forfeited Bonuses Allocated to Other Employees Bonuses Forfeited After a Certain Date Revert Back to

Taxpayer

IRS Attacks Year-End Bonuses

31

32 #CBIZMHMwebinar

Code Sec. 199: deduction of 9% of the taxpayer's qualified production activities income (QPAI) for the tax year

QPAI: Excess of Domestic Production Gross Receipts (DPGR) from

specified activities over the sum of the cost of goods sold allocable to DPGR and other properly allocable expenses, losses, or deductions.

TP licensed software to Contracting Parties and End Users.

End Users submitted service requests to Contracting Party, who generated the final product for End Users using the licensed software.

IRS held that TP’s income was QPAI because it did not provide services to End Users.

PLR 201445010: Software Licensing and DPAD

32

33 #CBIZMHMwebinar

Section 751(b) attempts to avoid the conversion of ordinary income (if partnership sells inventory or collects receivables) to capital gains (if partner sells partnership interest)

The proposed Regs adopt a hypothetical sale approach to measure a partner’s interest in section 751 property and to determine whether a distribution reduces that interest.

The proposed Regs allow partnerships to use a reasonable approach consistent with the purpose of Code Sec. 751(b) for treating distributions, and provide examples of a reasonable approach.

Proposed Regs on “Hot Assets”

33

34 #CBIZMHMwebinar

CCA 201436049 and Renkemeyer case All of the income allocated to the members of an LLC (taxed

as a partnership) are subject to self-employment taxes when the income is primarily attributable to personal services In the PLR, the LLC was investment manager for a managed fund

Confirmed that LLC members should not have been issued Forms W-2 for “wages”

In Renkemeyer the LLC was a law firm IRS will issue guidance on how specifics of when and how

LLC income is subject to SE tax May apply to other entities, as well

LLC Income Subject To Self-Employment Tax

34

35 #CBIZMHMwebinar

CCA 201447025 IRS holds that payments of more than $600 to LLCs are not

exempt from 1009 reporting An LLC is an eligible entity under Reg. §301.7701-3(a) that can elect

its classification as a corporation, partnership or disregarded entity (DE) by filing Form 8832, Entity Classification Election, with the IRS. Multimember LLCs can elect either association or partnership status.

A single-member LLC can elect to be an association or a DE that is not separate from its owner. Under the default classification rules, an LLC that does not make an election will be either a partnership (if it has multiple members) or a disregarded entity (single member).

No record that any of the LLCs had filed Form 8832. Therefore, each LLC was either a partnership or DE, and was not exempt from reporting.

Payments to LLCs

35

36 #CBIZMHMwebinar

IRS Office of Professional Responsibility (OPR) to provide guidance in Q1;

Issues: Marijuana sales still illegal under federal law; Tax compliance headaches because have to operate in cash due to

federal anti-money laundering rules Can’t use Electronic Federal Tax Payment System Tax preparers concerned about potential Cir 230 violations

Sec 280E: prevents deductions or credits for expenses if business involved in trafficking controlled substances

Currently, marijuana retailers only able to deduct COGS

Advisory panel would like clarification as to preparers’ responsibilities

Guidance for Preparers of Marijuana Entrepreneurs

36

CASES

38 #CBIZMHMwebinar

Halbig v. Burwell, 114 AFTR 2d, 2014-5068 (DC Cir. July 22); King v. Burwell, 114 AFTR 2d, 2014-5071 (4th Cir. July 22)

DC Circuit –Federal [health insurance] exchange is not an “Exchange established by the State.” As a result, the premium tax credits under Code §36B are unavailable if the individuals purchase their insurance through a federal exchange.

Fourth Circuit – Concluded the plain language and context of the relevant statutory sections, along with the ACA’s legislative history made it unclear if Congress intended to limit the premium tax credits to state exchanges. Giving deference to the IRS’s determination in the regulations (and applying the Chevron Doctrine of statutory interpretation) the Court concluded the statute permitted the IRS to decide whether the tax credits would be available on federal exchanges.

U.S. Supreme Court: Set oral arguments for King v. Burwell for March 4, 2015

Supreme Court to Rule on Premium Tax Credits Under ACA

39 #CBIZMHMwebinar

Former PwC partner could not use installment method to report the gain on sale of her partnership interest to IBM to the extent that the sales price was attributable to unrealized receivables of the partnership

Mingo v. Comm’r, 2014-2 U.S.T.C. ¶50,538 (5th Cir. 2014)

40 #CBIZMHMwebinar

Long v. Comm’r, 2014-2 U.S.T.C. ¶50,510 (11th Cir. 2014)

An individual’s sale of his contractual right to purchase real property resulted in capital gain, not ordinary income.

The Tax Court erred when it determined that the property the individual sold was the land versus a distinct contractual right that was a capital asset.

Moreover, there was no evidence that the individual entered into the agreement to purchase the land with the intent of assigning his contractual rights in the ordinary course of business. The record was clear that the individual intended to develop the property himself.

Decision prevents IRS from expanding “substitute for ordinary income” doctrine to include investments with only the possibility of future income.

41 #CBIZMHMwebinar

Mylan said IRS improperly characterized the 2008 sale of its rights in the drug nebivolol to Forest Laboratories Holdings Ltd. as a license.

IRS said transfer generated ordinary income, not capital gains, and resulted in a total deficiency of $104 million for tax years 2007-10.

In 2006 Mylan agreed with Forest to market the drug in the U.S. and Canada for royalty and milestone payments. In 2008, Mylan sold all of its rights in nebivolol to Forest for a $370 million plus a royalty payment of $50 million to be made over three years.

Mylan never held owned patents to nebivolol. In 2001, it licensed the rights from Janssen Pharmaceutica N.V.

The IRS position: That the 2006 and 2008 agreements didn't “effectuate a transfer of Mylan's

obligations to Janssen under the 2001 License because those obligations were personal to Mylan and could not be shifted to a third party.”

Mylan retained a “significant power, right, or continuing interest”

Mylan, Inc. v. Comm’r, Tax Court Petition (11/14/2014)

42 #CBIZMHMwebinar #CBIZMHMwebinar

Questions?

43 #CBIZMHMwebinar #CBIZMHMwebinar

Join us for this course:

Eye on Washington: Quarterly Business Tax Update 1st Quarter – Offered on April 30th, May 5th, May 6th

More information to come….

If You Enjoyed This Webcast…

44 #CBIZMHMwebinar #CBIZMHMwebinar

Connect with Us

linkedin.com/company/ mayer-hoffman-mccann-p.c.

@mhm_pc

youtube.com/ mayerhoffmanmccann

slideshare.net/mhmpc

linkedin.com/company/ cbiz-mhm-llc

@cbizmhm

youtube.com/user/BizTipsVideos

slideshare.net/CBIZInc

MHM CBIZ