welcome to hondros college of business updated.pdf/33/… · welcome to hondros college of business...

TRANSCRIPT

6/10/2016

1

Welcome to

Hondros College of Business

Property & Casualty

Your instructor today is:

@hondros.com

1

The purpose of this class is to:

• Help you learn the test material well enough to

pass the exam

• Help you become comfortable with the format of

the test questions

• Build your confidence to master the test material

• Furnish you with the benefit of a “real live

person” to coach you through the experience.

2

What this class is not:

• An in-depth examination of the intricacies

of the insurance business.

• A substitute for you:

– Reading the book and learning the material

– Studying outside of class

– Using Comp-u-cram

3

6/10/2016

2

Taking the Exam

• Test scheduling procedures are in the candidate

information handbook & textbook

• You do NOT have to wait to complete the class

to schedule your exam. Call or login---TODAY.

• The faster you do it, the better chance you have

of getting the date and time that’s best for you.

• The quicker you test after the class is over, the

more information you retain.

4

Exam success stats

• Test taken within 2 weeks of course completion -

--- 72% success rate

• Test taken within 30 days - 65%

• Test taken within 60 days - 53%

• Test taken 60 days or later - 45%

• Once the date is set, you create a structured

time table of study and we are here to help

• The sooner you test, the sooner you pass!!

5

Overview of the Exam

Unlimited attempts for 6 months

Test is all multiple choice

A comprehensive exam for Property and

Casualty Insurance consisting of:

General knowledge questions, and,

State specific questions with about

1 minute to answer each question

6

6/10/2016

3

Overview of the Exam

155 questions; 5 do not count either way

150 questions are scorable

70% overall score - not per chapter

105 correct answers and you pass

45 wrong answers and you still pass!!

D- just as good as an A

Score does not appear on license

60% knowledge of the material

40% on how to take a test

7

How to pass the exam:

Know the laws: Chapter 1 = 22

questions

Learn the terms & concepts: Chapters 2

& 3 = 38 questions

Typical questions: – Positive: Which of the following are covered…

– Negative: All of the following are covered EXCEPT…..

– Situational: Joe is in an auto accident and injuries 3 people, how

will his policy pay out

8

General Insurance 14

questions • Insurance = Social device to spread losses

• Insured gives up small certain loss (premium) in

exchange for large uncertain loss (claim)

• Policy = Contract between insurer & insured

• Loss = Reduction in the value of an asset

• Risk = The possibility/uncertainty of loss

– Pure Risk: possibility of loss only - insurable

– Speculative Risk: loss or gain – not insurable

• Exposure = The amount of risk presented

9

6/10/2016

4

General Insurance

• Risk Management – Acronym C-A-R-T-S

– Control (reduce)

– Avoid

– Retain

– Transfer

– Share

• Law of Large Numbers

– The larger the group of similar risks; the more

predictable the losses of the group will be

10

General Insurance

• Peril – Anything that can cause a loss

• Hazard – Anything that increases the

likelihood or the severity of a loss

– Physical - material or structural part of risk

– Moral – dishonest client/ intentional damage

– Morale – careless client/ no pride of

ownership

11

General Insurance

• Insurable Risks

– Large group of Homogeneous Units

– Loss must be ascertainable or measurable

– Loss must be uncertain

– Loss must cause an economic hardship

• Catastrophic Perils

– Can’t calculate loss – not insurable

• Adverse Selection – not insurable

• Indemnity - Make whole again, back in the position prior

to the loss; Not better, Not worse.

12

6/10/2016

5

Insurers

Stock – owned by the stockholders

Mutual – owned by the policyholders

Reciprocal – managed by an attorney-in-fact

Surplus Lines – will insure anything for a price – need a special

license

Reinsurance – Insurance for Insurers

Government Insurers – Social insurance: Flood, Medicare,

Crop, Terrorism

Fraternal – belong to the club

Lloyd’s Association - Individuals that assume risks

Risk Retention Groups: Insurance for themselves often called

“Captives”

13

General Insurance

• Classification of Insurers

Domestic – located in Ohio

Foreign – located in another state

Alien – located out of the U.S.

Admitted/Authorized – licensed to do

business in the state

Non admitted/Unauthorized – not licensed

to do business in the state (Surplus Lines)

14

General Insurance

• Financial Rating Services

Company credit score

AM Best; Moodys; Standard & Poors

• Marketing Systems

Independent agent

Captive Agent

Direct writer

Direct response

15

6/10/2016

6

General Insurance

• Agent – Represents the Insurer (principal)

Binder – Temporary insurance contract. Oral or

written. P&C agent has binding authority.

Expressed – authority the agent has that is written in

the contract

Implied – authority the agent believes they have to do

business on behalf of the company

Apparent – authority the public believes the agent

has based on actions and advice.

Fiduciary duty – Acts of the agent are acts of the

principal.

16

General Insurance

• Contracts – Insurance is a Contract -- Acronym

C-O-A-L

– Consideration: Something of value in the eyes

of the law

– Offer: Application and premium

– Acceptance: Policy issued

– Legal Purpose – Legal Capacity (18, Sane

and Sober) 16 for car insurance

17

General Insurance - Contracts

Adhesion – Insured is “stuck” with it, buy it as its written

Representations – truth to the best of your

knowledge

Utmost Good Faith – Rely on honesty of each other

Waiver and Estoppel

• Giving up a known right voluntarily

• Waived right is “stopped” from ever coming back.

Misrepresentations - untruths

• Concealment – deliberate omission of material fact

• Fraud – deliberate attempt to deceive to get value

18

6/10/2016

7

General Insurance - Contracts

Unilateral – “One Sided”: Insurer only one held

legally to honor promise

Conditional – Based on rules both parties must

follow

Aleatory – Unequal consideration: based on chance

of loss

Personal – Policy does not pass to new owner

Warranty – 100% absolute truth – Breach of

Warranty voids the contract

Reasonable Expectations – Certain things should

be covered

19

P&C Basics – 24 questions

• Insurable Interest – financial stake in

preservation of property; must be present at the

time of loss

• Underwriting – Compare risk and exposure with

premium

– Loss Ratio – Premiums compared to claims

– Credit Scoring – basis for rate determination;

can’t be accept or reject; subject to Fair Credit

Reporting Act

20

P&C Basics

• Rates

– Loss Costs; developed by ISO based on

expected losses

– Levels take into account: claims, expenses,

less interest earned on premiums

– Can’t be too high; too low; or unfairly

discriminatory

21

6/10/2016

8

P&C Basics

• Liability

– Legal obligation to pay due to Negligence

– Bodily injury: bodily harm, sickness or

disease, death that results

– Property Damage: physical destruction of or

loss of use of tangible property

– Personal injury: Liable, slander, defamation

22

P&C BASICS

• Negligence Elements – Failure to do what a

reasonable person would have done under

normal circumstances

Duty - Standard of Care

Breach of Duty – Failure to do something

Proximate Cause – Unbroken chain of

events

Damages – Economic and non economic loss

23

P&C Basics

• Negligence Defenses

Intervening Cause – break in the chain of events

Assumption of Risk – If you assume risk, you can’t

blame others

Contributory Negligence – If you contribute, you get

NOTHING

Comparative Negligence – Partly at fault, damages

are reduced

Statute of Limitations – Time limit to file claim; 2

years in Ohio

24

6/10/2016

9

P&C BASICS

• Damages – Compensatory

Special – Actual monetary economic loss

General – Pain & suffering; disfigurement;

loss of services i.e. non economic losses

Punitive- Punishment

• Awarded over and above the special and general

to punish the wrong doer and make an example

• Not covered by insurance in Ohio

25

P&C BASICS

• Absolute Liability – Inherently

dangerous

• Strict Liability – Product liability

• Vicarious Liability – Others

• Liability Limits – Pay per event – Occurrence: over a period of time

– Accident: sudden and unforeseen

26

P&C Basics

• Cost of Defense – In addition to the policy

limit; whatever the amount

– Attorney fees, court costs, investigative

expenses

– Insurer bears this cost regardless of

outcome

– Insurer settles the suit in its best interest

– Insured’s consent – not required

27

6/10/2016

10

P&C Basics

• Liability Limits – Single Limit: One amount for both BI & PD – restored

for each event

– Split Limit: BI-PD listed separately, per person,per

occurrence – restored for each event

– Aggregate: Maximum payout for all claims per policy

period, each claim reduces what is left for future

losses for the rest of the policy period.

28

P&C BASICS

• Cause of Loss Form – Perils

Named: Perils on the list are named and

covered

Open – All Risk: Everything covered unless

excluded

Accident - Sudden and unforeseen event

Occurrence – Repeated and continuous

exposure to the same event.

29

P&C Basics

• Direct Loss: Caused directly by a peril - fire,

lightning etc.

• Indirect Loss: Expense incurred because of

loss of use of the damaged property.

• Blanket vs. Specific:

– Many locations – Many Types

– One Location – One Type

• Types of Construction:

– Frame, Brick, Non Combustible, Fire Resistive

30

6/10/2016

11

P&C BASICS

• Loss Valuation

Actual Cash Value

Replacement cost minus depreciation

Replacement Cost

New for Old: No depreciation

Market Value

What someone is willing to pay or sell

something for

31

P&C Basics

• Loss Valuation

Functional Replacement Cost

Not look the same or be the same, but will

function

Agreed or Stated Amount

Appraisal, Bill of Sale, Photos. Insured for

specific amount

32

P&C BASICS

• Policy Structure – Acronym D-I-C-E

– Declarations / Definitions

– Insuring Agreement

– Conditions

– Exclusions / Endorsements

• Additional/Supplementary Coverage

– Debris removal – Emergency repairs

– Cost of bail bonds – Loss of earnings

33

6/10/2016

12

P&C BASICS

• Common Policy Provisions

– Insureds: Named, First Named, Additional

– Policy period: Start date and end date

– Policy Territory: US, Territories, Puerto Rico, Canada

– Cancellation: Ends mid term and a refund may be due

company cancels refund is pro rata; return unearned

insured cancels refund is short rate; keep portion of unearned

– Non Renewal: Finishes the term – no refund of premium

– Deductibles: Per occurrence, risk retention

34

P&C BASICS

• Other Insurance

– Two or more policies covering same property

– Concurrent or Non Concurrent (not the same

perils covered)

– Each policy pays pro rata; claim % equals

amount of coverage %

– Sometimes referred to as the Pro Rata

Liability clause

35

P&C Basics

• Primary and Excess

– Primary pays first till limits are exhausted

– Excess pays after

• Contribution by equal shares

– Each policy shares the claim equally until it’s limit is

exhausted then the remaining policies share balance

• Partial Loss: Damages do NOT exceed policy limit or

value of the car

• Total Loss: Damages exceed the policy limit or value of

the car

36

6/10/2016

13

P&C BASICS

• Co-insurance: Insure property correctly

– Minimum of 80% of cost to replace or rebuild

– Penalty if not insured correctly and a partial

loss occurs.

– DID (amount insured for) divided by

– SHOULD (amount required) times

– LOSS (amount of damage) equals payment

37

P&C BASICS

• Vacancy or Unoccupancy

– Vacancy – No people; No Stuff; No coverage

after 60 consecutive days

– Unoccupancy – No People; No problem

• Named Insured Provisions Duties after a loss

• Report losses immediately

• Allow insurer to examine damaged property

• Protect property from further damage

38

P&C Basics

• Named Insured Provisions

– Assignment

• Transfer rights or coverage to someone

else; only if the company agrees

– Abandonment

• Must co-operate with insurer

• Can not abandon property and demand

payment

– Proof of Loss

39

6/10/2016

14

P&C BASICS

• Insurer Policy Provisions

– Liberalization

• Change policy wording without notifying insured

• Must benefit insured and no extra premium charge

– Subrogation – means “to substitute”

• Insurer takes the place of insured

• Insured gives up right of recovery for amount paid

by insurer

• Insurer goes after the negligent party

40

P&C Basics

• Insurer Policy Provisions

– Salvage

• Damaged property now belongs to insurer

• Recovered property belongs to both insurer and

insured:

– Insured makes the initial decision

– If insured demands property back – must return

the claim money

– If insurer refuses property – insured keeps both

41

P&C BASICS

• Appraisal

– Dispute on a property claim

– Each party gets an appraisal and pays for it

– Appraisers don’t agree- hire 3rd party umpire

and the cost is shared equally

– Decision of the umpire is final

• Arbitration

– Same situation for Liability claim dispute

42

6/10/2016

15

P&C BASICS

• Third Party Provisions

– Mortgagee Clause/ Loss Payable Clause

• Bank is mortgagee; Insured is mortgagor

• Bank in an auto loan or personal property loan

• Has right to make premium payment & file claims

• Must be notified by insurer if policy is going to end

• Insured can’t jeopardize the bank/lender’s rights

– No Benefit to the Bailee – holding property of others

• No claim payment to Bailee; payment made to

insured

43

Test Taking Tip

• Edition dates mean NOTHING !!!

– ISO assigns edition dates to each policy

version

– Typical question:

• In the Homeowner 3 (‘11) which of the following

are covered?

• The (‘11) refers to the homeowner policy issued by

ISO in 2011. It means nothing, don’t let it fool you

• Edition dates could appear in parenthesis for each

policy form question on the exam

44

Dwelling Policy - 9 questions

• Who is eligible

– Owners (landlords); Owner/occupant; tenants

• Eligible dwellings

– 1,2,3 or 4 family structure

– Up to 4 families & 5 roomers/boarders per family

• Purchasing a Dwelling Policy

– Ala carte property policy; NO theft or liability

– Direct loss to buildings (real property)

– Direct loss to contents (personal property)

– Indirect loss – Rental value; Additional living expense

45

6/10/2016

16

Dwelling Policy

• Dwelling Forms

– DP-1 Basic

• Named perils on building and contents

– DP-2 Broad

• Named perils on building and contents

• All the DP-1 perils plus several more

– DP-3 Special

• All risk on buildings

• Broad named perils on contents

46

Dwelling Policy

• Coverage A – Dwelling

– Structure and anything permanently attached

– Materials used to service, repair or construct

• Coverage B – Other Structures – Separated from the dwelling by a clear space

– Private garage, no commercial or business use

– 10% of dwelling amount can be extended

• DP-1 > reduces dwelling limit

• DP-2 & 3 > additional coverage over dwelling limit

47

Dwelling Policy

• Coverage C – Contents/Personal Property

– Only covered if on dec and premium paid

– 10% of coverage “C” amount off the premises

• Exclusions

– Animals, birds and fish

– Cars, planes, boats (except rowboats/canoes)

– MONEY

48

6/10/2016

17

Dwelling Policy

• Indirect loss coverage

– Coverage D – Fair Rental Value

– Coverage E – Additional Living Expenses

– 20% of dwelling amount can be extended

• DP-1> reduces dwelling limit

• DP 2 & 3 > additional coverage over

dwelling limit

49

Dwelling Policy

• Standard Policy Exclusions

– Ordinance & law: bringing building up to code

– Earthquake

– Water damage: Flood, tidal waves, backup of

sewers; seepage through basement walls

– Off premises power failure

– Neglect, War, Nuclear, Intentional losses

• Deductible – $500 per occurrence

50

Dwelling Policy

• DP-1 Basic Form: Building and Contents – Riot/Civil Commotion

– Explosion

– Vehicles (not yours)Volcano; Vandalism* *(extra $$)

– Fire

– Lightning

– Smoke

– Hail

– Aircraft

– Wind

51

6/10/2016

18

Dwelling Policy

DP-2 Broad Form

• Riot/Civil Commotion

• Explosion

• Vehicles,Volcano,Vandals

• Fire

• Lightning

• Smoke

• Hail

• Aircraft

• Wind

Building and Contents

• The REV joins the WWF

• Weight of Ice & Snow

• Water accidental

discharge from plumbing

• Falling objects and

freezing of pipes

52

Dwelling Policy

• DP-3 Special Form: Building and Contents

– All Risk on buildings

– Everything is covered unless its excluded:

• Wear & Tear Deterioration & mold

• Rust, Dry Rot Industrial smoke & pollution

• Mechanical Breakdown, Settling, Shrinking,

Expansion of drives,patios,walkways,porches

• Vermin, rodents, insects and domestic animals

– Broad named perils: REV FL SHAW WWF on

contents

53

Dwelling Policy

• Loss Settlement Provisions

DP-1 ACV on building and contents

DP-2 Replacement Cost on buildings

----if co-insured correctly (80%)

ACV on Contents

DP-3 Replacement Cost on buildings

----if co-insured correctly (80%)

ACV on contents

54

6/10/2016

19

Dwelling Policy

• Additional Coverage Automatic

– Debris removal – up to policy limit

– Fire department service charge - $500

– Reasonable Repairs- to protect property from

further damage after a loss

– Removal to protect – All risk coverage

anywhere

• 5 days on DP-1; 30 days on DP-2 & DP-3

55

Dwelling Policy

• Extra additional coverage for DP-2 & DP-3 – Collapse of building & glass breakage

– Ordinance & law – 10% of dwelling limit

– Trees, Shrubs & Plants

• Fire, explosion, riot, aircraft, vandalism, vehicles

• NO WIND, WEIGHT OF ICE, DISEASE, THEFT

• 5% of dwelling limit – max payout for all damage

per occurrence

• $500 max payout per tree, shrub or plant

56

Dwelling Policy

• Endorsements

– Inflation guard – keep coverage adequate

– Broad Theft – contents on and off premises

• Limited Theft – contents on premises only

– Dwelling Under Construction

– Personal Liability – on and off premises

• Premises Liability – coverage on premises only

– Replacement cost on contents

• No depreciation

57

6/10/2016

20

Homeowners Policy

21 questions • Package Policy --- THEFT included!!

– Section I Property - Deductible $500 per occurrence

• Coverage A Dwelling

• Coverage B Other Structures

• Coverage C Contents

• Coverage D Loss of Use

– Section II Liability - No Deductible

• Coverage E Personal Liability

• Coverage F Medical Payments to Others

58

Homeowners

59

Homeowners

• HO-1 – Basic (not used anymore)

• HO-2 – Broad (similar to DP-2)

• HO-3 – Special (similar to DP-3)

• HO-4 – Tenant (renter’s insurance)

• HO-5 – Comprehensive (Ho-3 on steroids)

• HO-6 – Condo (owns the residence unit)

• HO-8 – Modified (older homes)

60

6/10/2016

21

Homeowners

• Eligibility – Structure used exclusively as a residence

• Incidental business occupancy ok: private office, studio etc

– Owner occupied 1 to 4 family dwellings

– Tenants in a building used as a residence

– Condominium Unit owners

– Dwellings under construction, land contract or life

estate

– Seasonal dwellings if insuring the primary residence

– Mobile homes with the proper endorsement attached

61

Homeowners

• Definitions

– Insured

• Named Insured, Spouse, Resident Relatives

• Non relative under 21 in the care of the insured

• Child away at school full time and under age 24

– Residence Premises

• 1,2,3 or 4 family structure and other structures at

the address listed on the declarations page

• Up to 4 families and 2 roomers/boarders per family

• A new residence acquired within the policy period

62

Homeowners

• Definitions

– Insured Location

• Residence listed on the declarations page

• Any place an insured is temporarily residing

• Vacant Land (other than farmland)

• Cemetery Plots

– Business

• Full or part time activity grossing $2,000 or more

• Activities of minors or volunteers are not business

63

6/10/2016

22

Homeowners

• Section I - Property Coverage

– Insured chooses Dwelling limit – Coverage A

• Based on the cost to replace or rebuild

• Co-insurance rule applies – minimum 80%

• Premium is based on dwelling amount chosen

– Other coverages “stack” on top of Coverage A

– Coverage B additional 10%

– Coverage C additional 50%

– Coverage D additional 30%

64

Homeowners

• Section I - Property Coverage

– Limits are per occurrence

– No aggregate limit per policy period

– Deductible is per occurrence not

separate

65

Homeowners

• Coverage A – Dwelling

– Structure and anything permanently attached

– Materials used to service, repair or construct

• Coverage B – Other Structures – Separated from the dwelling by a clear space

– Private garage, no commercial or business use

unless used to store non combustible business stuff

– 10% of dwelling amount additional coverage for all

other structures. More coverage can be purchased

66

6/10/2016

23

Homeowners

• Coverage C – Contents/Personal Property

– 50% of dwelling amount – additional coverage

– Owned or used by an insured anywhere in the

world

– Property of guests or resident employees at

insured’s request

– 10% of coverage “C” amount or $1,000 for

contents off the premises:

• If regularly at another residence or in storage unit

67

Homeowners

• Special limits on certain types of Contents

– $200 money, securities, gold, silver, coins

– $2500 for business property on the premises

– $1500 for business property off the premises

– $1500 for watercraft and trailers

– $1500 for portable electronics in a car

– $1500 for THEFT of jewelry, watches, furs

– $2500 for THEFT of guns and related items

– $2500 for THEFT of silver, gold, pewter ware

68

Homeowners

• Exclusions on Contents

– Animals, birds and fish

– Motor vehicles unless servicing premises

– Planes unless hobby aircraft

– Property of roomers or boarders

– Articles described or insured elsewhere

– Property in a rental unit on or off premises

– Business “data” & Credit, Debit or ATM Cards

69

6/10/2016

24

Homeowners

• Coverage D – Loss of Use

– 30% of dwelling or contents amount for tenant

policy – additional coverage

– Additional living expenses

• Pays increase in living expenses due to loss

• Does NOT pay regular monthly bills

• Shortest time to repair dwelling or relocate

– Loss of rents

• Actual loss of rents until dwelling repaired

70

Section I – Perils Insured

PERILS including THEFT HO-2 HO-3 HO-4 HO-5 HO-6 HO-8

BLDGS CNTNS BLDGS CNTNS

Riot X Open X X Open Open X X

Explosion X X X X X

Vandalism/Vehicles/Volcano X X X X X

Fire X X X X X

Lightning X X X X X

Smoke X X X X X

Hail X X X X X

Aircraft X X X X X

Wind X X X X X

Weight of Ice & Snow X X X X

Water (accidental discharge) X X X X

Falling Objects X X X X

Freezing of Plumbing X X X X

71

Homeowners

• Standard Policy Exclusions

– Ordinance & law: bringing building up to code

– Earthquake

– Water damage: Flood, tidal waves, backup of

sewers; seepage through basement walls

– Off premises power failure

– Neglect,

– War, Nuclear, Intentional losses

72

6/10/2016

25

Homeowners

• All Risk Exclusions • Wear & Tear

• Deterioration, Dry or Wet Rot, Mold

• Industrial smoke

• Pollution

• Mechanical Breakdown,

• Settling, Shrinking, Expansion of driveways, patios,

walkways, porches

• Vermin, rodents, insects and domestic animals

73

Homeowners

• Additional coverage - Automatic

– Debris removal – up to policy limit

• Extra 5% of dwelling if policy limit is maxed out

• $500 per tree, $1,000 maximum for felled trees

– damages a covered structure or blocks a drive

– Reasonable Repairs

– Trees, Shrubs, Plants

• 5% of dwelling maximum; $500 max per tree

• Limited perils: NO wind, weight of ice, disease

74

Homeowners

• Additional Coverage - Automatic

– Fire Department Service Charge - $500

– Collapse – weight of people, rain, animals or

hidden and undetected insects

– Glass Breakage – NOT if vacant over 60 days

– Landlord’s furnishings - $2,500

– Ordinance & Law – 10% of dwelling limit

– Grave Markers - $5,000

– Credit, Debit, ATM Cards - $500

75

6/10/2016

26

Homeowners

• Conditions – Section I

• Vacancy – 60 consecutive days

– Lose coverage for Vandalism, Glass Breakage

• Volcanic Eruption – 72 hours, same event

• Pair & Set Clause

– Repair or replace the damaged part of the set

– Pay the difference between the value BEFORE the

loss and what’s left over AFTER the loss

76

Homeowners

• Section II – Liability Coverage

• Coverage E – Personal Liability

– Bodily Injury & Property Damage to others not insured

– On and Off Premises coverage due to Negligence

– $100,000 per occurrence; No deductible or aggregate

– Duty to Defend -- Defense Costs

• Additional coverage, not out of the policy limit

• UNLIMITED, No matter the outcome of the suit

• Duty to defend ends when policy limit is paid out

• Bankruptcy of the insured not an issue

77

Homeowners

• Section II – Liability Coverage

• Coverage F – Medical Payments to Others

– Immediate medical bills and funeral costs

– $1,000 per person, per occurrence

– Goodwill gesture, no liability required to be proven

– Claim must be made 3 years from date of injury

– OTHERS, not an insured or any regular resident

• Domestic employee while working if no work comp

– On the premises with permission or due to activities

of an insured off the premises

78

6/10/2016

27

Homeowners

• Section II – Liability EXCLUSIONS – Intentional Acts – self defense OK

– Business Pursuits incl: off premises rental property

– Professional Services

– Motor Vehicles – unless:

• Used to service premises or assist handicapped

• Unlicensed recreational vehicle on YOUR

premises

• Golf cart on the golf course or gated community

• Trailer not attached to a car

79

Homeowners

– Watercraft – owned or non owned – unless:

• Inboard motor up to 50 horsepower

• Outboard motor up to 25 horsepower

• Sailboat (no motor) under 26 feet in length

– Aircraft, War, Sale of Controlled Substance, Mold

– Transmission of Communicable Disease by insured

– Sexual Molestation, Corporal Punishment, Physical or

Mental Abuse

– Damage to Insured’s Property or Property of Others in

Insured’s care, custody and control

80

Homeowners

• Section II – Additional Coverages – Accrued Interest on judgments

– Claim expenses incl: $250 per day for lost earnings

– First aid expenses incurred for others

– Property of Others in your care -- $1,000 – unless:

• Intentional by insured 13 years of age or older

• Property of roomer or boarder

– Loss Assessments -- $1,000

• Home or condo association levies against insured

• Insured acting as director or officer without pay

81

6/10/2016

28

Homeowners

• Bankruptcy - Insurer must still defend

• Endorsements

– Limited fungi – mold

• $5,000 for property damage; $50,000 for liability

– Inflation guard – automatic increase-buildings

– Permitted Incidental Occupancies

• Liability coverage for in home office, studio

• High risk not eligible

82

Homeowners

– Scheduled Personal Property

• Endorsement to home or separate policy – PAF

• Jewelry, Fine Arts, Coins, Cameras, Collectibles,

• All Risk; Worldwide; No deductible; coverage floats

• Appraisals, Receipts, Photographs establish stated

or agreed value. Each item listed and described

• Newly acquired items automatic coverage 30 days

– If similar category already scheduled

– 25% of existing category limit or $10,000

whichever is less

83

Homeowners

– Personal Injury

• Libel, slander, defamation including defense costs

– Home Day Care – premises coverage only

• Premium based on number of children cared for

– Watercraft -over $1500 in value & larger motors

– Liability to Other Premises

– Earthquake

• Deductible is a percentage of policy limit

– Replacement Cost on Contents

84

6/10/2016

29

Homeowners

• Homeowner Forms -- Similarities

– Package Policy – property and liability

• $500 Deductible on property; $0 on liability

– Property coverage stack

– Theft peril included

– Contents are settled ACV

– Special Limits on certain types of Contents

– $100,000 liability and $1,000 Med pay

85

Homeowners

• HO-2– Broad**

– Broad Perils on buildings and contents

• HO-3– Special**

– All-Risk on buildings; Broad perils on contents

• HO-4– Tenant

– Broad perils on Contents; Loss of use 30% of

contents

• HO-5 – Comprehensive**

– All risk on building AND contents

**Building losses: R/C if insured correctly

86

Homeowners

• HO-6 – Condo

– Broad perils; Loss of Use 50% of contents

• HO-8 – Modified (older)

– Rebuild is much greater then market value

– Basic peril coverage; no glass or collapse

– Coverage A written at market value

– No Co-insurance rules or penalties

– Loss settled at ACV with functional materials

87

6/10/2016

30

Auto Insurance

21 questions • Financial Responsibility Laws

– To operate and/or plate a motor vehicle

– Surety Bond, Certificate of Deposit, Insurance

• Split Limit Liability – 25/50/25

– 25,000 per person per accident

– 50,000 all injuries per accident

– 25,000 property damage per accident

• Single Limit Liability – 75,000

88

Auto Liability Example Using

25/50/25 Policy Limits

Individual Claim Amt Paid Not Paid

Injury to Party A $50000 $25000 $25000

Injury to Party B $25000 $25000 $ -0-

Injury to Party C $20000 -0- $20000

Prop. Damage $29000 $25000 $ 4000

89

Auto Insurance

Structure of the Personal Auto Policy

Part A – Liability: Bodily Injury and Property Damage

Part B – Medical Payments

Part C – Uninsured/Underinsured Motorist

Part D – Damage to your Auto

Collision -- Other Than Collision

Part E – Duties after a loss

Part F – General Provisions

90

6/10/2016

31

Auto Insurance

• Types of Auto Policies

– Personal Auto Policy (PAP)

– Commercial Auto Insurance

• Business Auto Policy (BAP)

• Garage Policy

• Motor Carrier (Truckers) Policy

• Premium Factors

– Base Rates: age, gender, marital status, territory

– Underwriting: driving, claims & credit reports; usage

– Coverage: Limits, Physical damage, Endorsements

91

Auto Insurance

• Declarations Page

–Named Insured

–Covered Autos

–Policy Limits

–Policy Period

–Premium

92

Auto Insurance

• PAP – Definitions

– Eligible Vehicle

• 4 wheels,

• private passenger types, pickups,

vans, SUV’s

• Weighing under 10,000 pounds GVW

• Not used for business – farming &

ranching are ok

93

6/10/2016

32

Auto Insurance

Covered Vehicle

• Owned autos listed on the declarations page

• Newly Acquired auto – additional or replacement

– Broadest policy coverage for 14 days

– If no physical damage on policy: 4 days of

physical damage-$500 deductible

• Trailer (liability automatic when attached)

• Non-owned vehicle…if:

– Used as a temporary substitute and

– Covered vehicle not drivable due to servicing,

repair, breakdown or destruction

94

Auto Insurance

• PAP - Definitions

–Insured • Part A Liability

• Named insured & spouse if they live together

• Family Members – Anyone related by blood

marriage or adoption and residing in the household

• Ownership, Maintenance or Use of ANY auto

• Anyone using a covered auto

95

Auto Insurance

• Part A – Liability

– Owner policy primary/ Driver policy excess

– Coverage Limits per accident – no aggregate

– Defense Costs – Unlimited

• Duty to defend ends when policy limit is paid

• Supplementary Payments

– Accrued Interest on judgment until paid

– Bail Bonds - $250; Appeal bonds

– Loss of Earnings - $200 per day

96

6/10/2016

33

Auto Insurance

• Liability Exclusions no coverage = no defense

– Intentional Acts

– Damage to your property or property of others

in your care, custody and control

– Injury to employees

– Taxi or livery service

– Used in an auto related business

– Non-owned vehicle used regularly

– Racing or stealing a car

97

Auto Insurance

• Policy Territory

– United States

– Territories

– Puerto Rico

– Canada

• Out of State coverage

– Liability coverage expands to meet minimum

limits of state temporarily driving in

98

Medical Payments 3 year time limit to make claim

Insured and Passengers

No Fault Coverage

Per Person Limit; per Accident

Coverage while in an auto or as a pedestrian but not “under”

99

6/10/2016

34

Uninsured Motorists (UM)

1) No Liability policy in force

2) Ins, but less then the legal minimum

3) Hit-Skip Accident---Police report

4) Insured, but company denies claim

or is bankrupt

100

Underinsured Motorist

(UIM) • Automatic with UM

in Ohio

• Coverage available

from state

minimums up to

amount of bodily

injury coverage

Covers injuries

caused by driver

with insurance BUT

not enough

Your UIM coverage

must be greater

then at fault driver

101

Uninsured Motorists Property Damage

1) Optional – fixes the car

2) ACV coverage up to $7,500

3) NO Hit-Skips

4) Minimum $250 deductible

5) Maybe offered with Collision

coverage

102

6/10/2016

35

Part D- Physical Damage

• Based on value of the car

– Deductible on each coverage – customer choice

• Collision

– Collide with another object: moving or still

– Upset or overturn of the auto

• Other than Collision- Comp

– Missiles, falling objects, fire, theft, vandalism, hail,

water, flood, earthquake, glass breakage, wind, riot,

explosion, contact with an animal

103

Auto Insurance - Collision

104

Auto Insurance - Comp

105

6/10/2016

36

Auto Insurance

• Part D – Additional Coverage

– Transportation Expenses

• IF Collision and Comprehensive on vehicle

• $20 per day; $600 Maximum

• 24 hours after covered loss disables the vehicle

• 48 hours after total THEFT of the vehicle

• No deductible

• Paid directly to insured

• Not Rental Reimbursement

106

Auto Insurance

• Loss Settlement

– Repair, Replace with like kind & quality

– Actual Cash Value

• Exclusions

– Predictable

• Wear & Tear

• Mechanical or electrical breakdown

– Preventable

• Freezing, Neglect, Intentional, Racing

107

Auto Insurance

• PAP – Endorsements

– Miscellaneous Type Vehicle

• Motorcycles, Motor homes, Trailers, Dune Buggy

– Towing & Labor

• Car out of harm’s way; labor performed at scene

– Extended Non-Owned

• Regular use of a non-owned auto

– Substitute Transportation (Rental Reimbursement)

– Joint Ownership – 2 owners

• Related-unmarried or unrelated-living together

108

6/10/2016

37

Commercial Auto

• Business Auto Policy (BAP)

– Eligible Auto

• Any vehicle designed for the public roads and/or

requiring motor vehicle registration

– Covered Auto

• Defined by numerical symbol for each coverage

• Larger the symbol, more restrictive the definition

• #1 any auto; #7 specific listed autos; #8 hired

autos; #9 non-owned vehicles

• Symbols can be mixed to tailor coverage

109

Commercial Auto

Structure of the Business Auto Policy

Part A – Liability: #1

including pollution cleanup after an accident

Part B – Medical Payments #7

Part C – Uninsured/Underinsured Motorist #7,8,9

Part D – Damage to your Auto #7

Part E – Duties after a loss

Part F – General Provisions

110

Commercial Auto

• Business Auto Policy

– Insured

• Owner, Employees, Anyone using a covered auto

with the permission of the Named Insured

– Physical Damage

• Collision – collide with an object or upset

• Comprehensive– everything except a collision

• Specified Perils- alternative to comprehensive

• Transportation Expenses- $20 per day; $600 max

– 48 hours after THEFT of private passenger auto only

111

6/10/2016

38

Commercial Auto

• Exclusions– Physical Damage – Same as PAP

• Supplementary Payments – Accrued Interest, $2,000 bail bond, Appeal bonds

– $250 per day loss of earnings

• Loss Settlement – Repair or Replace with like kind & quality

– ACV

112

Commercial Auto

• Garage Policy– Combination of:

– Business Auto Policy

• Customers test driving dealer cars

• Insured driving customers’ cars

– Commercial General Liability Policy

• Premises liability – customer slips & falls

• Operations liability – customer hurt while work is

performed

• Product liability – parts are faulty

• Completed operations liability – workmanship is

faulty

113

Commercial Auto

• Eligibility – New and Used Auto dealers

– Auto Repair facilities

– Parking Lots, Car Washes, Valet Services

• Policy Structure – Garage – Liability

• Autos on the road; Premises/Operations; Products/Comp Op

– Med Pay; UM/UIM (optional)

– Physical Damage – Owned cars and/or lot cars

• EXCLUDED: Damage to Property in Care, Custody & Control

114

6/10/2016

39

Commercial Auto

• Garage Keepers Legal Liability

• Direct Primary - No fault required

• Legal Liability – Negligence of insured required

• Damage to customers’ vehicles

• Bailee type coverage – Autos left in insured’s care

• Collision and Comprehensive Coverage

• Premium based on exposure

– How many autos in possession at one time

– Average value of autos

• Deductible applies per auto; aggregate per loss

115

Commercial Auto

• Motor Carrier (Trucker’s) Form – Hauling goods or passengers for a fee

– Usually across state lines- Interstate Trucking

• Motor Carrier Act of 1980

– Federal Law requiring minimum liability limits

• General Goods & Cargo - $750,000

• Oil and Passengers - $1,000,000

• Hazardous substances - $5,000,000

– MCS-90 form filed with highway commission

116

Commercial Auto

• Trailer Interchange – Non owned trailer – Liability automatic if attached to truck

– Physical damage to non owned trailer

– No coverage for contents IN the trailer

• Commercial Auto Endorsements – Drive other Car

• Named persons driving other cars for personal use

– Additional Insured: Lessor, Employees, Individuals

• Specific people or entities with insurable interest

117

6/10/2016

40

Commercial Auto

• Commercial Auto Endorsements

– Mobile Equipment

• Not designed or licensed for public road use

• Tractors, Farm equipment, Cranes, Cherry Pickers

– Broad Form Products

• Will replace faulty product when installed properly

by garage

118

Commercial Package Policy

18 questions

CPP

119

7 Coverage Parts

• Commercial Property

• General Liability

• Commercial Auto

• Crime

• Inland Marine

• Equipment Breakdown

• Farm

120

6/10/2016

41

Components of the CPP

• Common Declarations page

• Common Conditions-Premium

Audit

• Two or more coverage parts-

must have property and liability

• Interline Endorsements

121

COMMERCIAL GENERAL

LIABILITY

CGL

122

OCCURRENCE FORM

• A: 1-1-11 to 1-1-12

• B: 1-1-12 to 1-1-13

• C: 1-1-13 to 1-1-14

• Claim happens on April-10-2012 and is reported to the carrier on July-6-2013.

• TRIGGER: Did the “event” happen during the policy period? What company is on the hook?

123

6/10/2016

42

COMPANY “B”

• Policy period was 1-1-12 to 1-1-13

• Claim happened during this time

• Date it was reported is NOT relevant

• In essence Company “B” is responsible for ANY claims that may OCCUR during its policy period. It doesn’t matter when they are reported.

124

CLAIMS MADE FORM

• TRIGGER: Was the event reported

during the policy period.

125

CLAIMS MADE FORM

• A: 1-1-11 to 1-1-12

• B: 1-1-12 to 1-1-13

• C: 1-1-13 to 1-1-14

• Claim happens on April-10-2012 and is reported to the carrier on July-6-2013.

• TRIGGER: When was the “event” reported? What company is on the hook?

126

6/10/2016

43

COMPANY “C”

• Policy period was 1-1-13 to 1-1-14

• Claim was reported during this policy

period

• In essence if no claims are reported during

the policy period, the company is off the

hook!

127

The RETRO Date

• The RETRO DATE goes back to a point in time and sets the 2nd “trigger” for the claims made form.

• This RETRO DATE is negotiated at each renewal. The farther back you want coverage to go, the more the premium will be.

• Customer wants any event reported to the insurer to be covered no matter when it happened.

• Company very concerned about events that happened in the past being reported to them.

128

CLAIMS MADE FORM

• TRIGGER 1: Did the “event” HAPPEN

after the RETRO DATE

• TRIGGER 2: Was the “event”

REPORTED during the policy period

129

6/10/2016

44

EXTENDED REPORTING

PERIOD

“Put a Tail on it”

• 60 days ERP automatic

on the policy giving you

an additional 60 days

from the end of the policy

to report claims

• Doesn’t extend coverage,

just the time to report the

claim.

• Known as the MINI TAIL

• $SUPPLEMENTAL TAIL

• MIDI TAIL extends reporting period 1 to 5 years.

• MAXI TAIL extends reporting period forever.

• Insd has 60 days from the end of the policy to purchase.

130

General Liability “Hazards”

• Premises / Operations

• Products /Completed Operations

• Personal / Advertising Injury

• Contractual

• Fire Legal Liability

• Medical Payments to Others

131

“Insured” Contracts

• Lease

• Easement

• Agreement to Indemnify

• Sidetrack

• Elevator/Escalator

132

6/10/2016

45

Limits of Liability

• Occurrence

• Most paid out for

any one “event”

• All claim amounts

must be eligible

here first.

• Aggregate

• Most paid out for

all claims during

the policy period.

• Products/ComOps

has separate

aggregate limit

133

134

Commercial

Property

135

6/10/2016

46

Property Coverage

• BUILDING: Structure and any permanently attached equipment; any property used to service the premises

• CONTENTS: Stock, equipment, materials furniture & fixtures in the building or within 100 feet of the premises.

• PROPERTY OF OTHERS: Stuff in the care custody and control of the insured within 100 feet of the premises

136

Property Coverage

• Deductible - $500 standard

• Loss Settlement – ACV;Co-insurance 80%

• Theft of Jewelry & Furs limited to $2500

• Standard Exclusions

– Money & Securities, Autos, Boats, Airplanes

– Land and anything growing out of it

• Except for vegetative roofs – part of the building

– Animals, Birds,& Fish unless stock for sale

137

Optional coverage

Offered for a price • Inflation Guard

• Builders Risk

• Business Interruption (indirect loss) Business Income sold to those who will shut down Extra Expense sold to those who must continue

• Glass Form

• Earthquake – 168 hours = same event

• Peak Season/ Value reporting form

• Ordinance & Law & Spoilage

138

6/10/2016

47

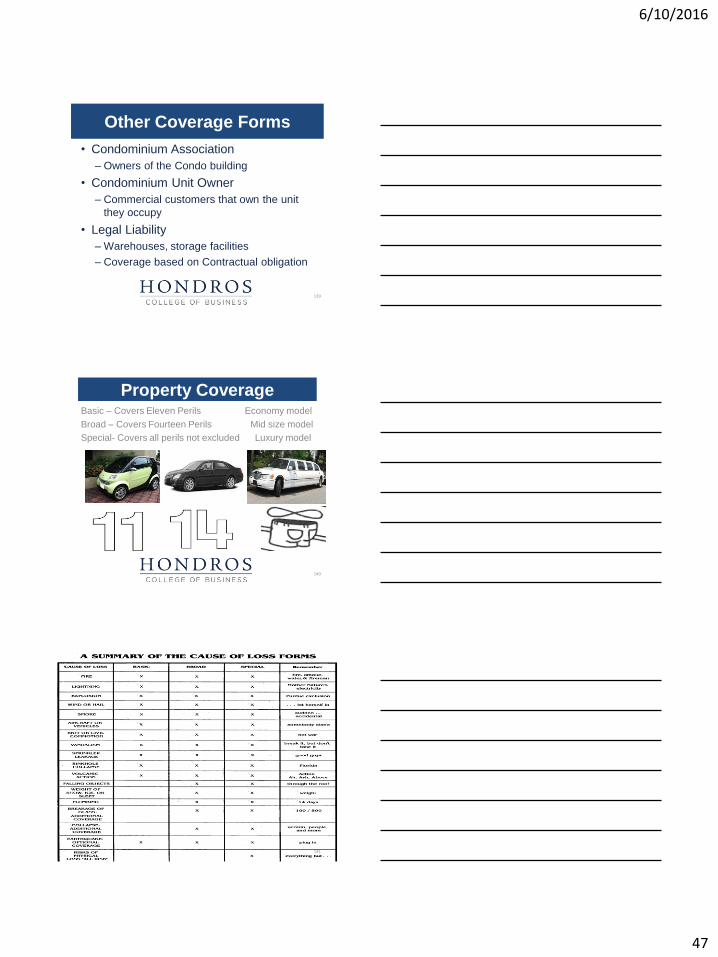

Other Coverage Forms

• Condominium Association

– Owners of the Condo building

• Condominium Unit Owner

– Commercial customers that own the unit

they occupy

• Legal Liability

– Warehouses, storage facilities

– Coverage based on Contractual obligation

139

Property Coverage Basic – Covers Eleven Perils Economy model

Broad – Covers Fourteen Perils Mid size model

Special- Covers all perils not excluded Luxury model

140

141

6/10/2016

48

Commercial Crime

• BURGLARY: taking of property by visible signs of a forced entry or exit

• ROBBERY: Taking of property by threat of bodily harm

• EXTORTION: Holding hostage = Kidnapping

• MYSTERIOUS DISAPPEARANCE: Losing something

• THEFT any act of stealing

• FORGERY & ALTERATION: Falsifying outgoing checks

142

People & Places

• Custodian: Named insured, Partners, Employees with custody of insured property ON the premises

• Messenger: Named insured, Partners, Employees with custody of insured property OFF the premises

• Premises: DUH!

• Watchperson: Custody of property ON the premises and no other duties

143

144

6/10/2016

49

145

Types of Property

• Money: Currency, coins, travelers checks, registered checks and money orders

• Securities: Negotiable & non-negotiable instruments or contracts representing money: tickets, stamps, evidence of debt, credit & debit charge slips

• Property other than Money & Securities: DUH!

146

Crime Forms

• Employee Theft

• Forgery & Alteration

• Inside the premises, theft of money &

securities

• Inside the premises, Robbery and Safe

Burglary

• Computer, Funds Transfer Fraud

• Outside the Premises

147

6/10/2016

50

Crime Forms

• Extortion- Commercial Entities

• Lessees of Safe Deposit Boxes

• Securities Deposited with Others

• Guests Property

• Safe Depository

• Outside the Premises

148

Inland Marine

Imports

Exports

Domestic Shipments

Instrumentalities of transportation or

communication

Personal Property Floaters

Commercial Property Floaters

149

Marine Forms

• Accounts Receivable

• Equipment Dealer Floater

• Jewelers Block

• Installation Floater

• Signs

• Valuable Papers and Records

• Bailee’s Customer Goods

• Contractors Equipment Floater

• Electronic Data Processing

150

6/10/2016

51

Transportation Coverages

• Motor Truck Cargo carrier responsible for

customers goods in shipment

• Owner’s/Shipper’s Form: For customer who

ships his stuff in his trucks or for the customer

who has a trucking company haul her goods

• Annual Transit for trips done during the year

• Trip Transit for a single shipment

• Free on Board (FOB): Shippers responsibility

for damaged goods ends when delivered

151

Equipment Breakdown

Coverage • Boilers

• Pumps

• Motors

• Refrigeration

• Air Conditioning

• PROTECT & PREVENT

• Objects scheduled

• Peril of Mechanical Breakdown

• Replacement cost settlement

• 25,000 extra expense coverage to expedite the repair or replacement

• Business Interruption (optional)

• RED TAGGED

152

FARM

• Homeowners

• Commercial Property

• Commercial Liability

• Building

• Other Structures

• Contents

• Loss of Use

• Scheduled Farm Prop

• Unscheduled Farm

Property

• Other Farm Buildings

153

6/10/2016

52

Farm owners Coverages

• Basic Broad and Special for Property

• Broad & Special Forms Cover Animals – Electrocution, drowning, suffocation, attacks

– Loading and unloading

• Mobile Agricultural Machinery

– Covered on Farm Property but can be stand alone

– $50,000 extension for newly acquired machinery for 30 days

• Livestock

– Newly acquired animals covered for 30 days

– No Freezing or Poultry

154

Businessowners Policy

13 questions • Package Policy

– Property and Liability

– Small to medium size businesses

155

Businessowners Policy

• Eligible Risks – Acronym O-F C-A-R-S – Office buildings

• 100,000 square feet

– Fast food & casual dining restaurants

• Limited cooking, seating up to 150, alcohol less then 50% of

receipts

– Convenience Stores

• With or Without gas pumps

– Apartment Buildings

• 6 Stories or 60 Units

– Retail & Service

• Up to 35,000 square feet and $6 million in sales

156

6/10/2016

53

Businessowners Policy

• Ineligible Risks – Taverns

– Auto Dealers

– Repair Shops

– Banks

– Contractors

– Manufacturing

157

Businessowners Policy

• Common policy conditions – Inflation Guard: 8% on building and 25% on contents for peak

season

– Claims Settlement: Replacement Cost

– Deductible: $500 standard

– Vacancy: 60 days

• Tenant = Not enough property to conduct normal business

operations

• Owner/Landlord = 69% or more of total square footage is not

being utilized

• Lose: Theft, Vandalism, Glass breakage, Sprinkler leakage,

and Water damage

158

BOP

• Standard – Basic coverage: building & contents

• Special - All Risk coverage: building and

contents

– Jewelry, Watches, Furs $2500 for THEFT

• Exclusions

– Normal peril exclusions on Basic and All Risk

– Money, Autos, Boats, Airplanes

– Animals, Birds and Fish (unless they are

stock)

159

6/10/2016

54

Additional Coverage – Debris Removal: 25% of loss up to $25,000

– Pollution Cleanup: $10,000

– Ordinance and Law: $10,000

– Fire Department Service Charge: $2,500

– Removal to Protect: 30 days--All Risk

– Mold damage: $15,000

– Electronic Data: $10,000

– Counterfeit Money: $1,000; Forgery: $2,500

– Business Income and Extra Expense

• Actual loss sustained up to 12 consecutive months

• 72 hour waiting period

160

BOP

• Extensions of Coverage – Coinsurance 80%

– Newly Acquired Property: $250,000 on

buildings/$100,000 contents

– Property off premises & in storage units: $10,000

– Outdoor Property: $2,500 w/$1000 max per tree,

shrub or plant

– Valuable Papers and Records: $10,000

– Accounts Receivable: $10,000

– Signs attached: $1,000

– Non-owned trailers $5,000

161

BOP

• Liability

– Bodily Injury, Property Damage,

Personal & Advertising, Premises

Rented to You

– Same exposures as CGL

– $300,000 Minimum occurrence limit

– $5,000 Medical payments to others

– Aggregates twice the occurrence limit

162

6/10/2016

55

BOP

• Exclusions

– Liquor Liability

– Workers Compensation

– Pollution Liability

– Professional Services

– Autos, Boats, Airplanes

– Property of others in care, custody and control

– Damage to insured’s own product or work

– Product recall

– Employment related practices

163

BOP

• Endorsements – Burglary and Robbery} Standard BOP

– Money and Securities} Special BOP

– Outdoor Signs and Glass

– Equipment Breakdown

– Employee Theft

– Hired and Non Owned auto

– Protective Safeguards

– Utility Services – Direct Loss

– Utility Services – Indirect Loss

164

Workers’ Compensation

6 questions • Workers Compensation Laws - Ohio

– Occupational: Work related accident or

illness

– No fault: worker gives up right to sue in return

for prompt and fair payment of claim

– Compulsory: required with 1 or more

employees; elective for self-employed,

partners

165

6/10/2016

56

Workers’ Compensation

• Monopolistic

– Buy from the BWC or Self Insure

• 500 employees minimum

• 2 years in business or more

• Financially stable with assets in Ohio

• Third Party Administrator

• Post a Surety Bond

• People who live and work in Ohio

166

Workers’ Compensation

• Federal Work Comp

– U.S. Longshoreman & Harbor Workers Act

• People who load, unload, build and repair ships

– Jones Act

• People who work on the ocean going vessels

– Federal Employers Liability Act (FELA)

• Interstate railroad workers

167

Workers’ Compensation

• Workers Compensation Policy

– Part One – Workers Compensation

• Medical Bills: Unlimited amount and time

– In & out of hospital including: Physical rehab,

Doctor bills, Rx drugs

• Disability: Income Replacement

– Partial or Total; Permanent or Temporary

– 2 week elimination period before benefits paid

– 66 2/3% of gross income = max benefit for total

disability

168

6/10/2016

57

Workers’ Compensation

• Survivor Benefits – Spouse and minor

children

–$5500 burial benefit; 66 2/3% of wages

at time of death

–Spouse collects until they remarry

–Children till age 18 or 25 if full time

student

• Vocational Rehabilitation - $ to re-train you

169

Workers’ Compensation

• Part One - Exclusions

– Non work related accidents and injuries

– Self Inflicted injury or intentional injury to

others

– Injuries sustained while under influence of

drugs or alcohol

– Injuries sustained while participating in

company sponsored athletic events

– Benefits payable under any other insurance

170

Workers’ Compensation

• Part Two – Employer’s Liability

– Defends employer if worker or related 3rd party sues

– Damages paid if employer negligent

• 100,000 per person per accident

• 500,000 aggregate for all disease claims

• 100,000 per person per disease

• Part Three – Other States Coverage

– Workers from Ohio temporarily in another

state

171

6/10/2016

58

Workers’ Compensation

• Part Four – Your Duties after a Loss

– Employee reports incident to employer immediately

– Employer notifies BWC about claim in timely manner

• Part Five – Premium determination

– Job Classification determines base rate

– Rate is multiplied by each $100 of payroll for each job

class

– Experienced rated: base rate is surcharged or

discounted based on past claims

– Premiums are auditable up to three years after

coverage expires

172

Workers’ Compensation

• Second Injury Fund

– State sponsored fund which pays benefits for

previously injured worker having a second or

subsequent injury

– Not charged against employer’s experience

modifications

– Prevents discrimination in hiring the handicapped

• Part Six – Conditions

– BWC can inspect the workplace at any time

173

Workers’ Compensation

• Voluntary Compensation Endorsement

– Benefits for volunteer workers

– Job class is stated on the endorsement

• Foreign Coverage Endorsement

– Ohio employees working temporarily out of the U.S

for max of 90 days

174

6/10/2016

59

Other Coverages & Options

11 questions • Umbrella/Excess

– Personal & Commercial: Worldwide –

could broaden coverage

– Pays AFTER the primary policies are

exhausted

– Self Insured Retention Limit - if no or

insufficient primary coverage

175

Other Coverages & Options

• Specialty Liability

– Professional > Malpractice: Bodily Injury

– Errors & Omissions > Malpractice: Financial Injury

– Directors & Officers > Lawsuits by the stockholders

– Fiduciary Liability > $$$$$

– Liquor Liability> Manufacturing, selling, distributing or

serving alcohol

– Employment Practices Liability

– Employee Benefit Plan Liability

– Identity Fraud / Cyber Liability

176

Other Coverages & Options

• Surplus Lines

– Unauthorized carriers

– Surplus lines broker license required

• $25000 Bond; License fee $100; Renews Jan 31st

– Affidavit signed by agent, customer, broker;

policy must be countersigned by licensed

agent

– No protection under Ohio Guaranty

Association for insolvency

177

6/10/2016

60

Other Coverages & Options

• Surety Bonds

– Bonds are not insurance

• Insurance based on uncertainty of loss

• Bonds guarantee that something will or won’t

happen

– Three party contract

• Principal = party that purchases & performs

• Surety/Guarantor = party assuring that principal

performs

• Obligee = party owed the money if principal fails

178

Other Coverages & Options

– Full right of recourse

• If principal fails, surety pays obligee, and

collects back from principal

– Types of Bonds

• Fidelity > probate, fiduciary, banking,

employee theft, public official

• Surety > bid, performance, license, permit

contractor, judicial

179

Other Coverages & Options

• Ocean Marine – Oldest form of insurance: virtually unregulated -

Surplus Lines

– Coverage

• Hull - ship itself Freight - shipping charges

• Cargo – contents P&I – Marine Liability

– Warranties

• Seaworthy Legal trip

• Specific route Cargo Packed Properly

180

6/10/2016

61

Other Coverages & Options

– Perils

• Perils of the Sea: War, Piracy, Barratry

(embezzlement of the cargo by the crew)

• Jettison (voluntarily throwing cargo overboard to

save the ship from sinking)

– Claims called “Average”

• Particular Average – paid by the specific insurer

covering the specific damaged cargo

• General Average – loss shared by all the insurers

involved in the trip.

181

Other Coverages & Options

• Aviation – Written by risk retention groups or “pools”

– Warranties and coverages same as Ocean Marine

• In the air, on the ground, take off and landing

– Usages stated on the declarations page

• Who’s flying it; What’s it hauling

• Where does it fly to and from; where is it parked

– Drone Coverage

• Intended use; Personal Injury exposure

182

Other Coverages & Options

• Flood Insurance – Government Insurance

– Definition of flood

• Temporary or complete inundation of 2 or more

acres by overflow of surface waters or mudflows

on normally dry land areas – no mudslides or

sewer backup

– 30 day waiting period – No binding authority

– Designated flood zone

• FEMA informs community or community applies to FEMA

• Inspection and recommendations made to prevent flooding

• Recommendations adopted – community is designated area

183

6/10/2016

62

Other Coverages & Options

• “Write your Own” Program

– Insurer can write policy

– FEMA determines coverage & premium

– Insurer pays claims from premiums collected

– Claims exceed premiums > FEMA takes over

– Premiums exceed claims > Excess sent to US

Treasury

– 100% government insurance

184

Other Coverage & Options

• Direct loss by flood - No indirect loss coverage

• Exclusions

– Money, securities, fine arts, collectibles

– Autos, airplanes

– Property in the open

– Underground contents or equipment

– Lawns, trees & shrubs

– Fences, retaining walls, piers, docks, wharves,

bridges

– Storage structures

185

Other Coverages & Options

• Flood Coverage

– Emergency Program Regular Program

• Bldg: 35000 PL * 100000 CL * 250000 PL 500000 CL

• Cnts: 10000 PL 100000 CL 100000 PL 500000 CL

• Deductible: 1500 pre firm post firm

1500 – 1000<100,000

2000 – 1250>100,000

– Applies separately to each building and each

contents loss per occurrence *PL (personal lines) CL (commercial lines)

186

6/10/2016

63

Other Coverages & Options

• Other Policies

– Boatowners – Premium based on value & usage

• Hull (boat itself); Liability & Personal effects

• Under 26 feet in length & personal watercraft such

as jet skis

– Recreational vehicles

• ATV’s, mopeds, scooters, segways, dune buggy,

golf carts, & trikes

• Not eligible for the personal auto policy

– Difference in Conditions – picks up gaps

187

Insurance Regulations

22 questions

• Who must be licensed:

– Anyone who sells, solicits or negotiates

insurance must be licensed.

• Non-Resident Agent • Must be in good standing in his previous home state.

• Need not pass the licensing exam if he applies within 90

days of moving to Ohio

188

Insurance Regulations

• Exceptions to licensing Employees, officers or directors of an

insurance company who: do not receive any commission on policies

written or sold, or

are involved in underwriting, settling of claims, administration, or handling enrollments for group life, group health or employee benefit plans.

189

6/10/2016

64

Insurance Regulations

• Pre-Licensing 40 hours of classroom training, or

Self study/Online

- Self study students must pass a proctored exam with a score of 70% or better to get an authorization to take state exam.

- Certificate of course completion is issued when class is completed or when proctored exam is passed.

- You have unlimited attempts to pass the test within a 180 day period which begins when you receive your course completion certificate. Fee charged for exam

190

Insurance Regulations

• Obtaining a License • Be at least 18 years of age & resident of Ohio

• Be honest, trustworthy and of good character and reputation

• Consent to a criminal background check

• You do not need to be a U.S. citizen but you must have proof of legal authority to work in the U.S.

• Have not committed any acts that are grounds for denial, suspension, or revocation of a license.

• Complete a required insurance education course and pass an exam for each line of authority.

• Apply for a license within 180 days of passing the exam.

191

Insurance Regulations

• Change of Address

– 30 days to notify the Superintendent/Director

of Insurance.

• Renewal of License -An individual seeking to renew a resident insurance

agent license shall apply biennially on or before the

last day of the licensee’s birth month. $25 fee

-The Superintendent shall send a renewal notice to all

licensees at least one month prior to the renewal

date.

192

6/10/2016

65

Insurance Regulations

• Renewal of License • To be eligible for renewal, all continuing education

requirements must be met prior to the renewal date. If

the CE requirements have been met, the renewal fee

will be waived.

• An individual who is unable to comply with the license

renewal procedures due to military service, a long

term medical disability, or some other extenuating

circumstance may request an extension of the renewal

date upon written request along with all supporting

documentation to the Superintendent.

193

Insurance Regulations

• Late Renewal > If the renewal application and fee is not

submitted by the required date, the individual may submit a late renewal application along with the applicable renewal fee [$25] and a late renewal fee of $50 prior to the first day of the second month following the license renewal date.

> If the renewal or late renewal requirements are not met, the license will be suspended for non-renewal.

194

Insurance Regulations

• License Reinstatement > A license suspended for non-renewal may be

eligible for reinstatement if an application is made within 12 months of the original date the license should have been renewed and the renewal fee and a $100 reinstatement fee have been submitted.

> If the reinstatement requirements are not met, the license will automatically be cancelled.

• Temporary License >Superintendent decides who – good for 180 days

195

6/10/2016

66

Insurance Regulations

• Administrative Action

– Agent must notify DOI within 30 days of the

final disposition of the matter

• Criminal Prosecution

– Agent must notify the DOI within 30 days of

the initiation of charges/proceedings

• Assumed Names

– Agent must notify the DOI before using the

assumed name.

196

Continuing Education

Requirements

Each compliance period:

Consists of 24 months and is based on your birth month.

Requires completion of 24 hours of approved classes, including:

3 hours of Ethics

3 hours of Flood initially to sell it

197

Continuing Education

Requirements Exams are not required unless you take classes

online or by self study

Entire course must be attended or completed to

get credit.

Can’t repeat same course within your compliance

period.

12 excess hours can be carried over into next

compliance period – all general credits

Agents responsibility to report hours to the DOI

Superintendent can grant an extension of time

198

6/10/2016

67

Failure to meet CE requirements

• The license of any agent who fails to meet the

CE requirements and who has not obtained an

extension of time will be suspended. The

suspension continues until the person

demonstrates compliance with CE requirements.

• If the person has not obtained an extension and

has not demonstrated compliance within one

year from the end of the renewal period, the

license will be automatically cancelled.

199

Education Violations

• Refuse to issue or renew - $500 fine

– Filing false documentation

– Obtaining false course completion certs

– Cheating on an examination

– Aiding or abetting anyone else to violate laws

– Disruptive actions during course or exam

– Unauthorized use of cells phones or devices

200

Insurance Regulations

• Inactive License

– Not in the business that in any way requires a

license – up to $25,000 fine if still working

– In good standing & CE compliant

– Out for a minimum of two years

– No requirement to do CE while inactive

– $50 reactivation fee and current CE done

– If reactivating during first 2 years - RETEST

201

6/10/2016

68

Insurance Regulations

• License Suspended, Revoked, Denied

– Review list of reasons in textbook

– Failure to pay taxes or work comp premiums

– Failure to appear for an interview with DOI

– Failure to respond to inquiry within 21 days

– Up to $25,000 civil penalty per violation

– Ask Attorney General to prosecute

• Courts can also fine up to $25,000

202

Insurance Regulations

• Fines

– Transacting without a license

• $25 to $500 fine; 6 months in jail

– Selling for unauthorized company

• $25 to $500 fine; 6 months in jail

– Surplus Lines broker violation regulations

• $25 to $500 fine; 1 year in jail

– Failing to file fees, or advertising violations

• $100 to $500 fine

203

Insurance Regulations

• Cease and Desist Orders

– Sent by certified mail from the DOI

– Stop activity listed in the order immediately

– $10,000 civil penalty for violating order

– Hearing within 15 days of issuance to decide

if the activity may resume or still stopped

– Agent can appeal final ruling in writing

204

6/10/2016

69

Insurance Regulations

• Hearings

– Agent has right to a hearing if license in

jeopardy

– DOI has the power to subpoena documents

and witnesses

– Mergers/acquisitions of a domestic carrier

• Superintendent can approve or deny merger

• Public hearing within 7 days of notifying parties

205

Insurance Regulations

• Consent Agreements

– Formal Rehab contract in lieu of losing license

– Conduct unbecoming voids agreement

– Agreement is a public record

– Former, current and potential employers can

receive a copy of the agreement

– Agent must notify DOI within 14 days of any

additional convictions or treatment programs

206

Insurance Regulations

• Acts constituting Insurance Transactions

– Negotiate: confer or offer advice

– Sell: exchange insurance for money

– Solicit: attempt to sell or urge to buy

• Responsibilities of the Superintendent

– Set licensing procedures

– Set appointment procedures

– See that laws are executed and enforced

207

6/10/2016

70

Superintendent’s General

Duties & Powers

• May suspend, revoke or refuse to issue or renew any license

• Take written testimony under oath for violations

• Ask attorney general to request a declaratory judgment by the court if no administrative procedure in place

• Has authority to adopt, amend or rescind any rules

• Can impose any other sanction deemed appropriate for

– Lying, cheating or stealing while acting as an licensed insurance agent in Ohio

Mary Taylor

208

Insurance Regulations

• Company Regulations

– Certificate of Authority

• Required to do business in the state

• Renews annually

– Insolvency

• Inability to pay claims within 30 days when due

• Liabilities EXCEED assets

– Policy Forms/Rates/Exceptions

• Must be approved by the DOI

209

Insurance Regulations

• Financial Requirements

– $1,000,000 in paid in capital

– $1,000,000 in surplus to pay claims

– $2,500,000 in aggregate paid in capital and

surplus

– $50,000 bond or $100,000 in securities

posted with the state

• Funds – Company money is money held

in trust; no comingling with personal funds

210

6/10/2016

71

Insurance Regulations

• Unfair Claims Settlement Practices

– Misrepresenting policy provisions

– Failing to act promptly regarding:

• Communications

• Investigations

• Settlement

– Compelling insured to file lawsuits in order to

get obvious policy benefits

211

Insurance Regulations

• Unfair Claims Settlement Practices

– “days” refer to calendar days

– Make contact within 15 days of notice of loss

– Reply to DOI inquiries within 21 days

– Notify claimant of more time needed to investigate and settle every 90 days; 45 days on auto losses

– Affirm or deny coverage within 21 days of receipt of all required documentation

– Pay claim within 5 days of agreed settlement

212

Agent Regulations

Commissions and Compensation • Paid in the legal name of the agent

• Only paid if appointed by issuing company

• Can share with another agent licensed for that line of

authority

• Can assign commissions to collateralize a loan

• Can pay a flat fee to an unlicensed person or organization for

administrative services rendered

Policy/Application Signature • Forging any insurance document or transaction

• License can be suspended or revoked and fined

213

6/10/2016

72

Insurance Regulations

• Agent Appointment – Insurer must request agent be appointed to represent

them - $15 fee required