welcome to the 2012 annual meeting - dbag-website · negative net income: €-16.6mn (prev.yr. net...

TRANSCRIPT

Frankfurt, 29 March 2012

Welcome to the 2012 Annual Meeting

Financial year 2010/2011 at a glance

Three new investments –Romaco –Spheros, Brötje-

Automation (2011/2012)

Two realisations –Heim & Haus, Preh

NAV per share declines to €17.47 –Return on NAV -6.2%

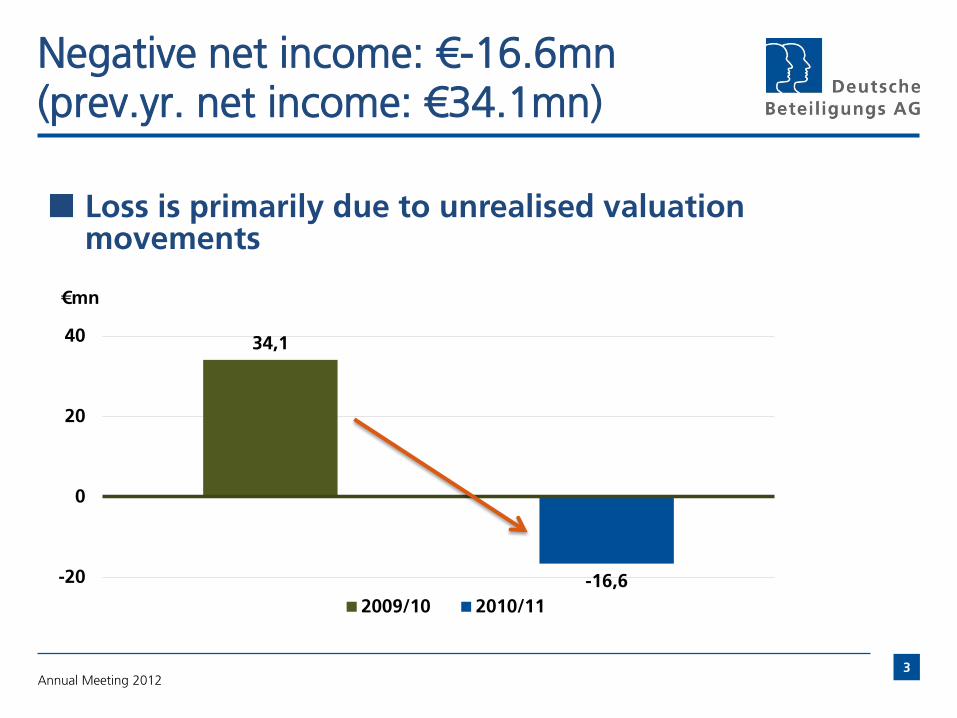

Negative net income of €-16.6mn in financial year 2010/2011 –Previous year: €34.1mn

Distribution: €0.40 dividend and €0.40 surplus dividend €0.80 total per share

Annual Meeting 2012

2

Negative net income: €-16.6mn (prev.yr. net income: €34.1mn)

Loss is primarily due to unrealised valuation movements

34,1

-16,6 -20

0

20

40

€mn

2009/10 2010/11

Annual Meeting 2012 3

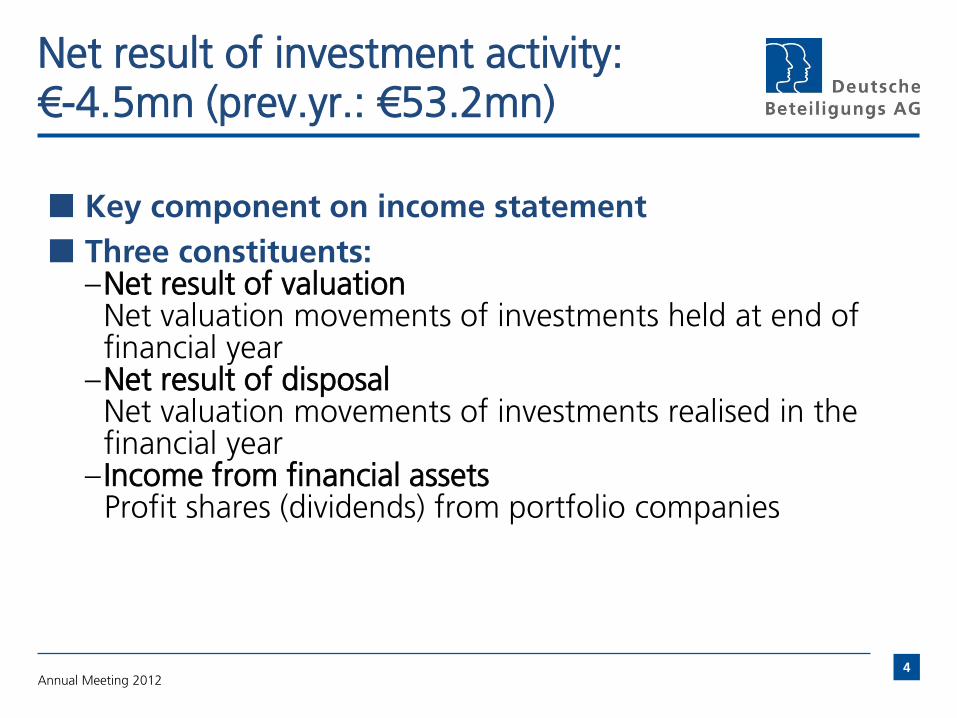

Net result of investment activity: €-4.5mn (prev.yr.: €53.2mn)

Key component on income statement

Three constituents: –Net result of valuation

Net valuation movements of investments held at end of financial year

–Net result of disposal Net valuation movements of investments realised in the financial year

– Income from financial assets Profit shares (dividends) from portfolio companies

Annual Meeting 2012 4

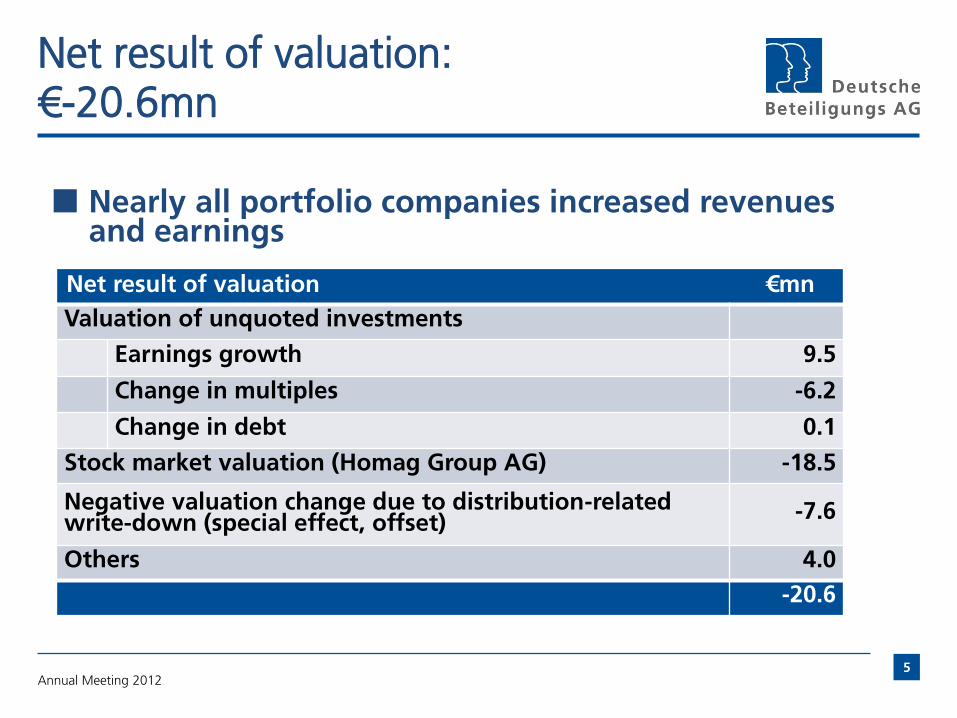

Net result of valuation: €-20.6mn

Net result of valuation €mn

Valuation of unquoted investments

Earnings growth 9.5

Change in multiples -6.2

Change in debt 0.1

Stock market valuation (Homag Group AG) -18.5

Negative valuation change due to distribution-related write-down (special effect, offset)

-7.6

Others 4.0

-20.6

Nearly all portfolio companies increased revenues and earnings

Annual Meeting 2012 5

Price trend of Homag shares caused greatest valuation effect

IPO in 2007: DBAG sold 40% of its holding in Homag –Proceeds (incl. dividends

since 2008) 140% of historical cost of entire investment

Price trend 2010/11: €15.48 €8.48, -45%

Price trend 2009/10: €8.46 €15.48, +83%

0,00

5,00

10,00

15,00

20,00

31/10/09 31/10/10 31/10/11

Annual Meeting 2012 6

€

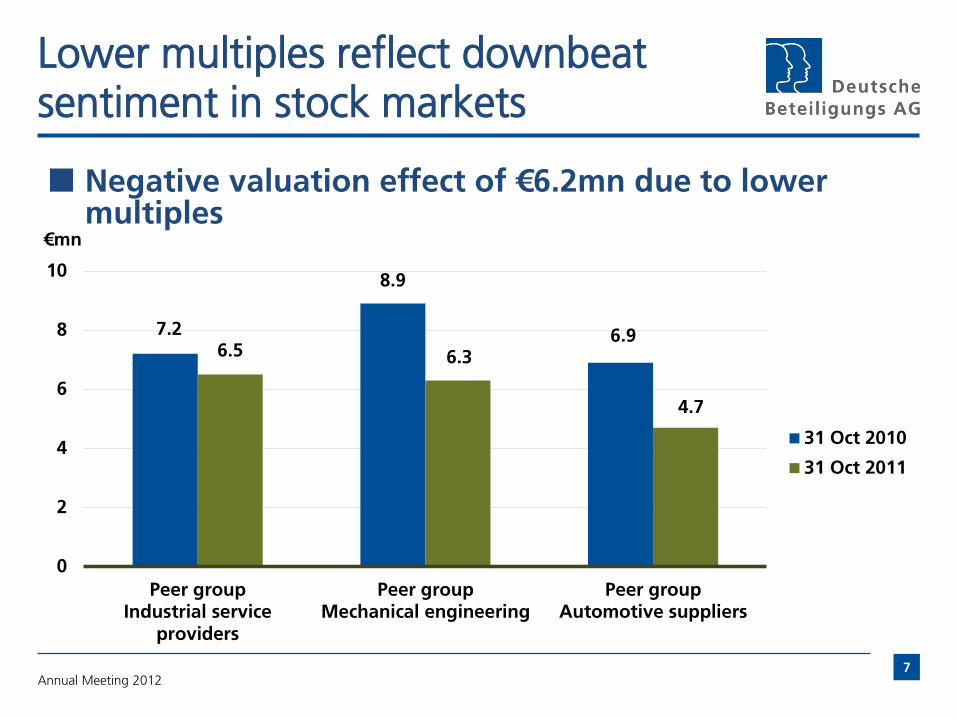

Lower multiples reflect downbeat sentiment in stock markets

Negative valuation effect of €6.2mn due to lower multiples

7.2

8.9

6.9 6.5 6.3

4.7

0

2

4

6

8

10

Peer groupIndustrial service

providers

Peer groupMechanical engineering

Peer groupAutomotive suppliers

31 Oct 2010

31 Oct 2011

Annual Meeting 2012 7

€mn

Net result of valuation: €-20.6mn (prev.yr.: €42.5mn)

Nearly all portfolio companies increased revenues and earnings

Annual Meeting 2012 8

Net result of valuation €mn

Valuation of unquoted investments

Earnings growth 9.5

Change in multiples -6.2

Change in debt 0.1

Stock market valuation (Homag Group AG) -18.5

Negative valuation change due to distribution-related write-down (special effect, offset)

-7.6

Others 4.0

-20.6

Net result of disposal: €6.7mn (prev.yr.: €1.1mn)

Net result of disposal: difference between sales proceeds and opening valuation at start of financial year not conclusive of long-term performance

Two realisations –Preh – (partial) realisation in April 2011

• Put option for remaining shares (25.1% of original investment) exercisable beginning of 2013

–Heim & Haus – realisation in May 2011

Annual Meeting 2012 9

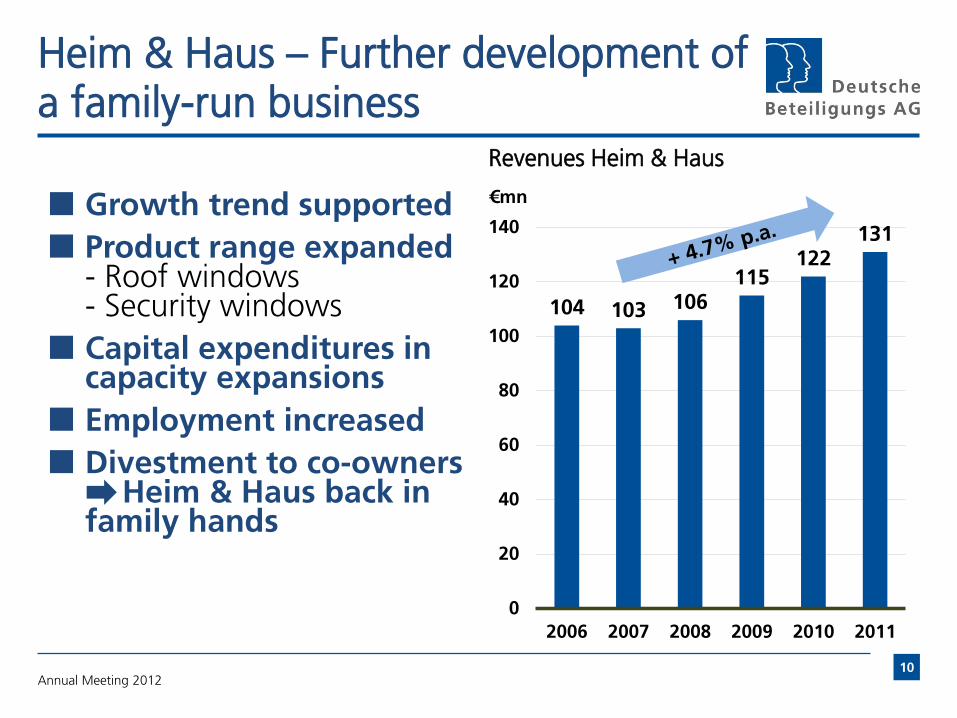

Heim & Haus – Further development of a family-run business

Growth trend supported

Product range expanded - Roof windows - Security windows

Capital expenditures in capacity expansions

Employment increased

Divestment to co-owners Heim & Haus back in family hands

104 103 106 115

122 131

0

20

40

60

80

100

120

140

2006 2007 2008 2009 2010 2011

Annual Meeting 2012 10

Revenues Heim & Haus

€mn

Preh – Successful implementation of investment strategy

Transformed into a purely automotive supplier - Two partial entities (2004 share of revenues: 18%) divested in 2008 and 2011

Attractive new product categories initiated - “Electronic control units”: battery management for electro-vehicles - “Driver control units”

Customer base expanded / internationalisation - Sept. 2005: Production site set up in Mexico - March 2009: Production site set up in Romania - Nov. 2010: Joint venture founded and production site set up in China Rapid market entry in China

Annual Meeting 2012 11

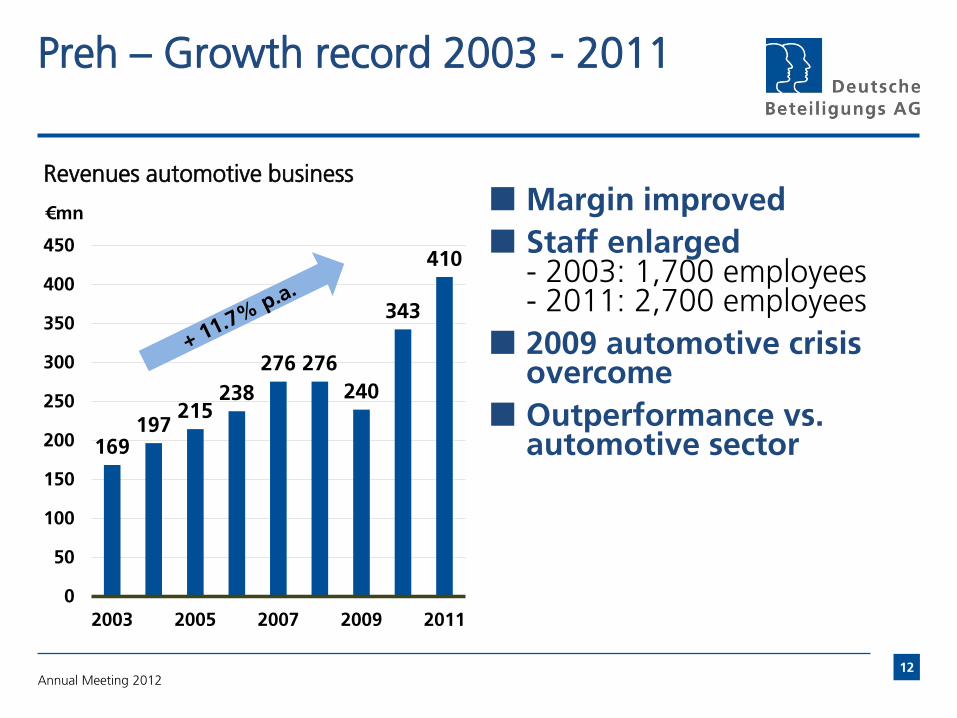

Preh – Growth record 2003 - 2011

Margin improved

Staff enlarged - 2003: 1,700 employees - 2011: 2,700 employees

2009 automotive crisis overcome

Outperformance vs. automotive sector 169

197 215

238

276 276

240

343

410

0

50

100

150

200

250

300

350

400

450

2003 2005 2007 2009 2011

€mn

Annual Meeting 2012 12

Revenues automotive business

Current income from financial assets: €9.4mn (prev.yr.: €6.6mn)

Increase due to special effects –Distribution of €7.6mn offset by distribution-related

writedown on an investment

Details in Management’s Report

Annual Meeting 2012 13

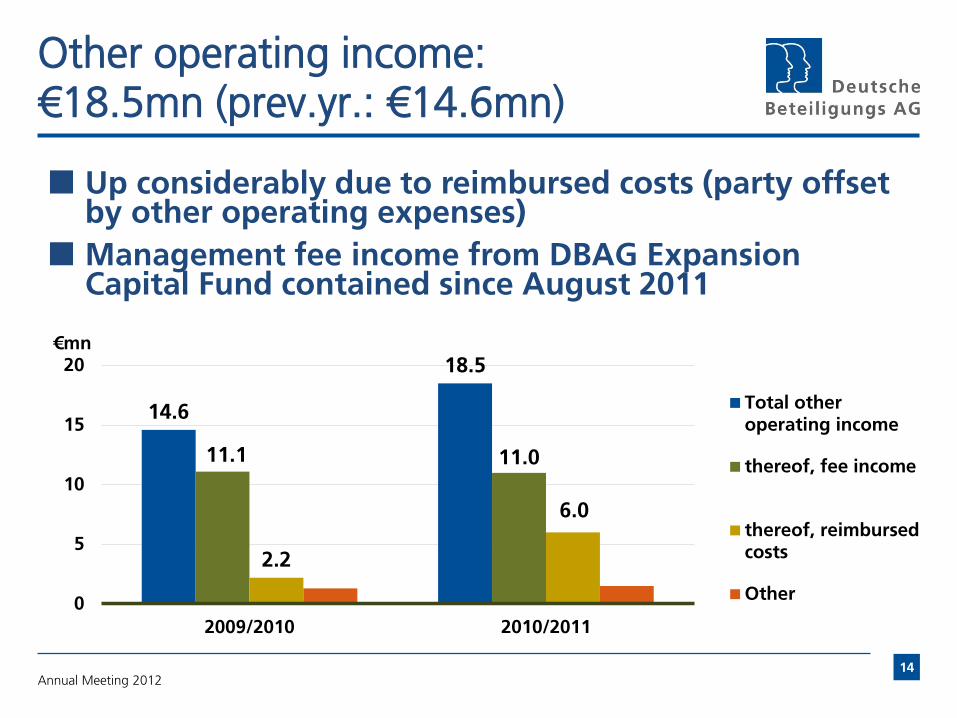

Other operating income: €18.5mn (prev.yr.: €14.6mn)

Up considerably due to reimbursed costs (party offset by other operating expenses)

Management fee income from DBAG Expansion Capital Fund contained since August 2011

14.6

18.5

11.1 11.0

2.2

6.0

0

5

10

15

20

2009/2010 2010/2011

€mn

Total otheroperating income

thereof, fee income

thereof, reimbursedcosts

Other

Annual Meeting 2012 14

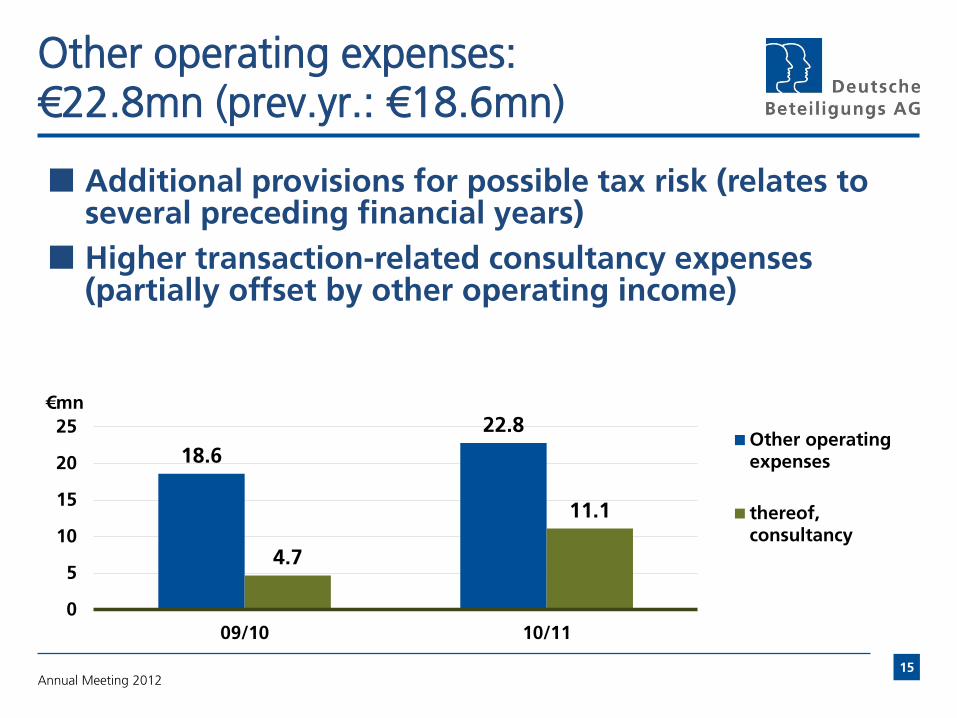

Other operating expenses: €22.8mn (prev.yr.: €18.6mn)

18.6

22.8

4.7

11.1

0

5

10

15

20

25

09/10 10/11

€mn

Other operatingexpenses

thereof,consultancy

Additional provisions for possible tax risk (relates to several preceding financial years)

Higher transaction-related consultancy expenses (partially offset by other operating income)

Annual Meeting 2012 15

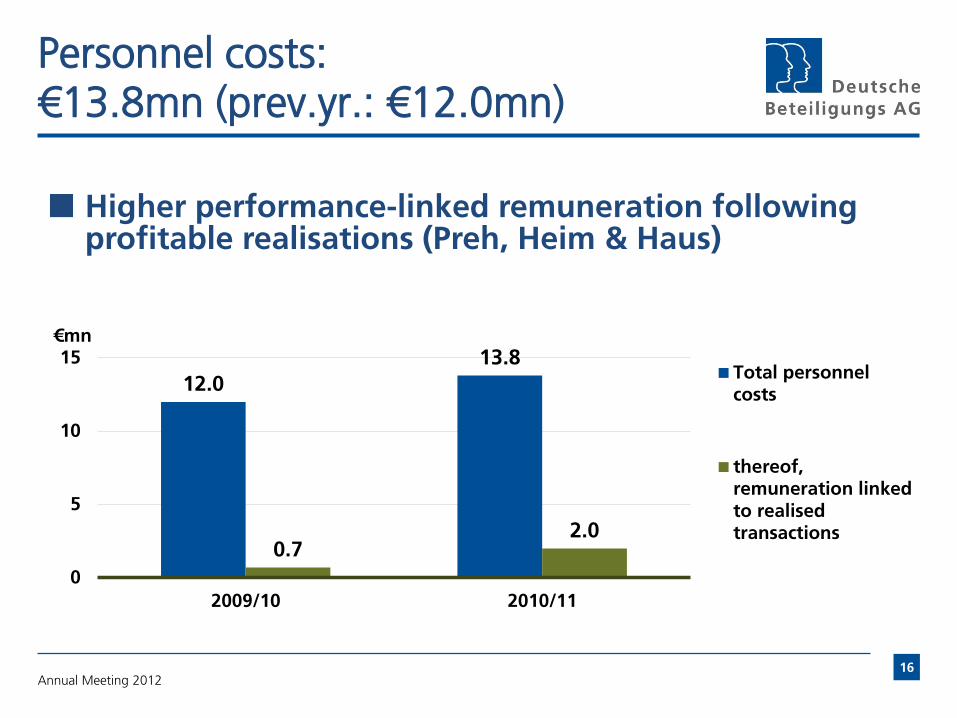

Personnel costs: €13.8mn (prev.yr.: €12.0mn)

12.0

13.8

0.7 2.0

0

5

10

15

2009/10 2010/11

€mn

Total personnelcosts

thereof,remuneration linkedto realisedtransactions

Higher performance-linked remuneration following profitable realisations (Preh, Heim & Haus)

Annual Meeting 2012 16

Net interest: €3.1mn (prev.yr.: €0.8mn) Net taxes: €1.8mn (prev.yr.: €1.3mn)

Increase in net interest primarily due to interest on tax refund

Tax refunds in 2009/2010 and 2010/2011 from preceding years

0.8

3.1

1.3

1.8

0

2

4

2009/2010 2010/2011

€mn

Net interest

Income taxes

Annual Meeting 2012 17

Balance sheet: NAV per share fell to €17.47

Net asset value per share lost 6.2%

20.03 €

18.63 €

17.47 €

1.40 €

16,00

16,50

17,00

17,50

18,00

18,50

19,00

19,50

20,00

20,50

31 Oct 10 31 Oct 11

2011 dividend

NAV per share

-1.16 € /

-6.2%

Annual Meeting 2012 18

€

Balance sheet: Liquidity of €155.6mn at reporting date

Financial assets and loans: “portfolio”, shelf companies and companies the majority of which is attributable to third parties

“Liquidity”: cash, short-term securities and long-term securities

Liquidity outflows for investments (Spheros GmbH, Brötje-Automation GmbH) and dividend of ~ €32mn

Assets

(€mn)

31 Oct.

2011

31 Oct.

2010

Liabilities

(€mn)

31 Oct.

2011

31 Oct.

2010

Financial assets

and loans 97.1 134.6 Equity 238.9 273.9

Other (e.g. receivables)

27.2 40.8 Non-current liabilities

10.9 15.8

Liquidity 155.6 140.7 Current liabilities

30.1 26.4

279.9 316.1 279.9 316.1

Annual Meeting 2012 19

Ten-year average return on NAV per share: 11.2 percent

Annual Meeting 2012

-15.8

3.1

18.2

41.3

82.7

136.5

-51.1

19.6

34.1

-16.6 -9.7%

2.1%

10.8%

20.0%

36.4%

56.2%

-17.5%

7.3% 12.7%

-6.2%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

-60

-40

-20

0

20

40

60

80

100

120

140

01/02 02/03 03/04 04/05 05/06 06/07 07/08 08/09 09/10 10/11

Net income in €mn Return on NAV per share as a %

20

2001/02 to 2003/04 based on HGB accounting, thereafter on IFRS.

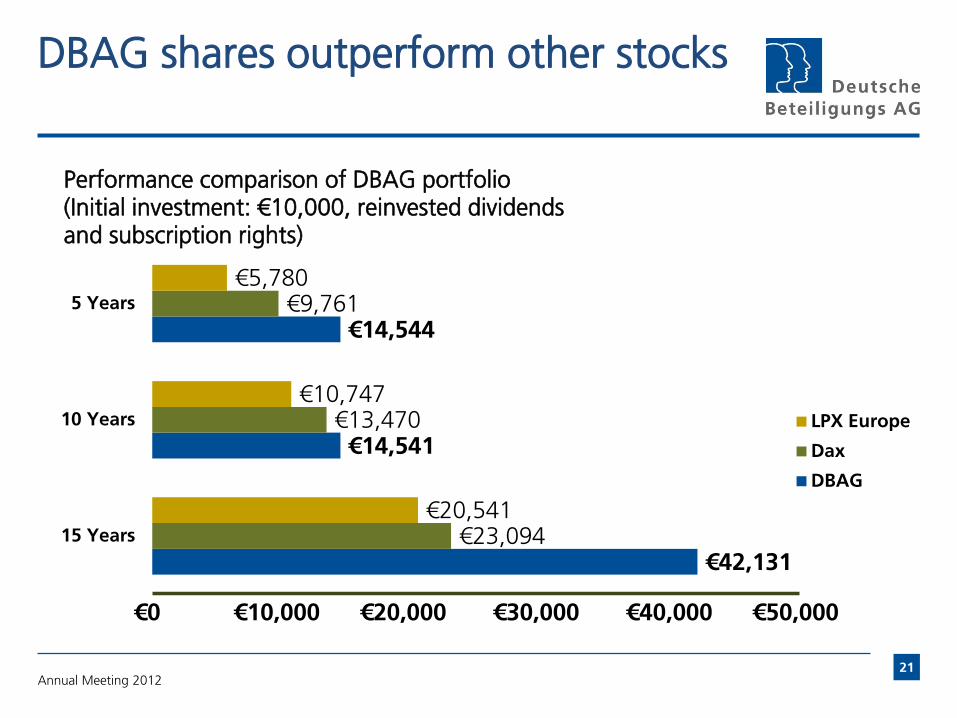

DBAG shares outperform other stocks

Annual Meeting 2012 21

€42,131

€14,541

€14,544

€23,094

€13,470

€9,761

€20,541

€10,747

€5,780

0 € 10.000 € 20.000 € 30.000 € 40.000 € 50.000 €

15 Years

10 Years

5 Years

Performance comparison of DBAG portfolio (Initial investment: €10,000, reinvested dividends and subscription rights)

LPX Europe

Dax

DBAG

€0 €10,000 €20,000 €30,000 €40,000 €50,000

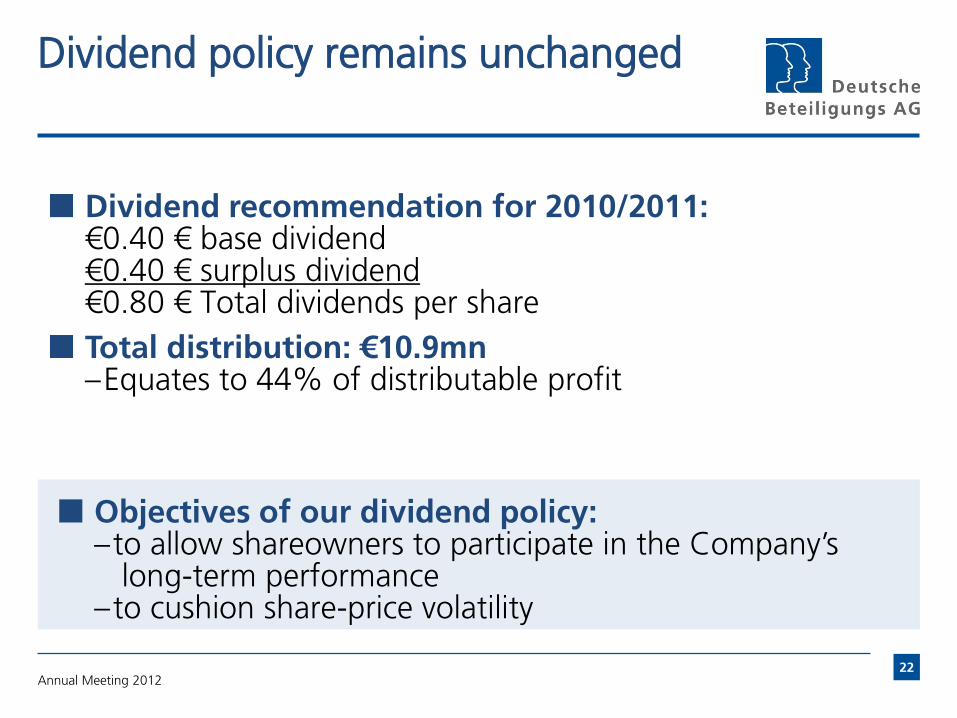

Dividend policy remains unchanged

Dividend recommendation for 2010/2011: €0.40 € base dividend €0.40 € surplus dividend €0.80 € Total dividends per share

Total distribution: €10.9mn –Equates to 44% of distributable profit

Objectives of our dividend policy: –to allow shareowners to participate in the Company’s

long-term performance –to cushion share-price volatility

Annual Meeting 2012 22

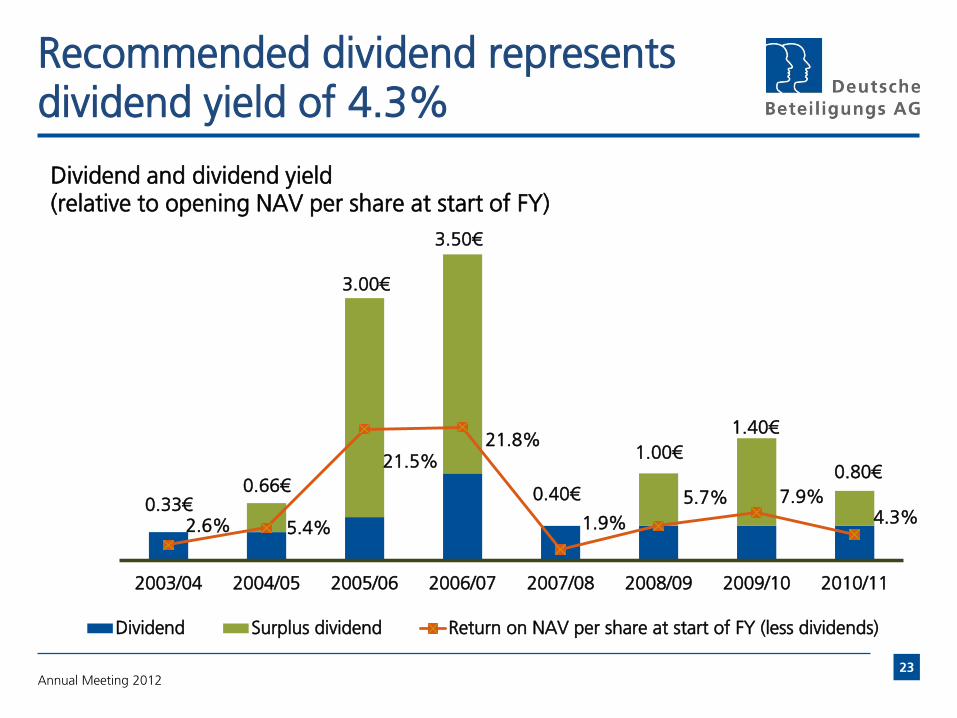

Recommended dividend represents dividend yield of 4.3%

0.33€ 0.66€

3.00€

3.50€

0.40€

1.00€

1.40€

0.80€

2.6% 5.4%

21.5% 21.8%

1.9%

5.7% 7.9% 4.3%

2003/04 2004/05 2005/06 2006/07 2007/08 2008/09 2009/10 2010/11

Dividend and dividend yield (relative to opening NAV per share at start of FY)

Dividend Surplus dividend Return on NAV per share at start of FY (less dividends)

Annual Meeting 2012 23

Changes to portfolio: New investments also very international

Annual Meeting 2012 24

Geographical revenue split

78%

21%

29%

53%

48%

20%

24%

17%

5%

8%

42%

51%

18%

31%

8%

12%

3%

6%

8%

44%

Brötje-Automation

Clyde-Bergemann

Coperion

Homag

Romaco

Spheros Europe

NorthAmerica

Asia/Pacific

Other

71%

Romaco Group – Invested in April 2011

Annual Meeting 2012

Leading manufacturer of machines and lines for packaging and processing applications for the pharma, cosmetics and food industries

Revenues of €93mn

450 employees

Investment: €7.7mn for a 18.7% share (another 77.3% held by DBAG Fund V)

25

Romaco at a glance

Two business segments: Packaging machines (share of revenues: 66%) - Technologically advanced, flexible machines - Clients: largely contract packers and generics manufacturers (market growing strongly) Process technology (33%) - Technologically mature products, partially with service-intensive components - Clients: Focus on food applications - Market sustainable and stable

Standard machines with low technology risks and order sizes

Strong service business and large installed base (24,000 machines worldwide)

Annual Meeting 2012 26

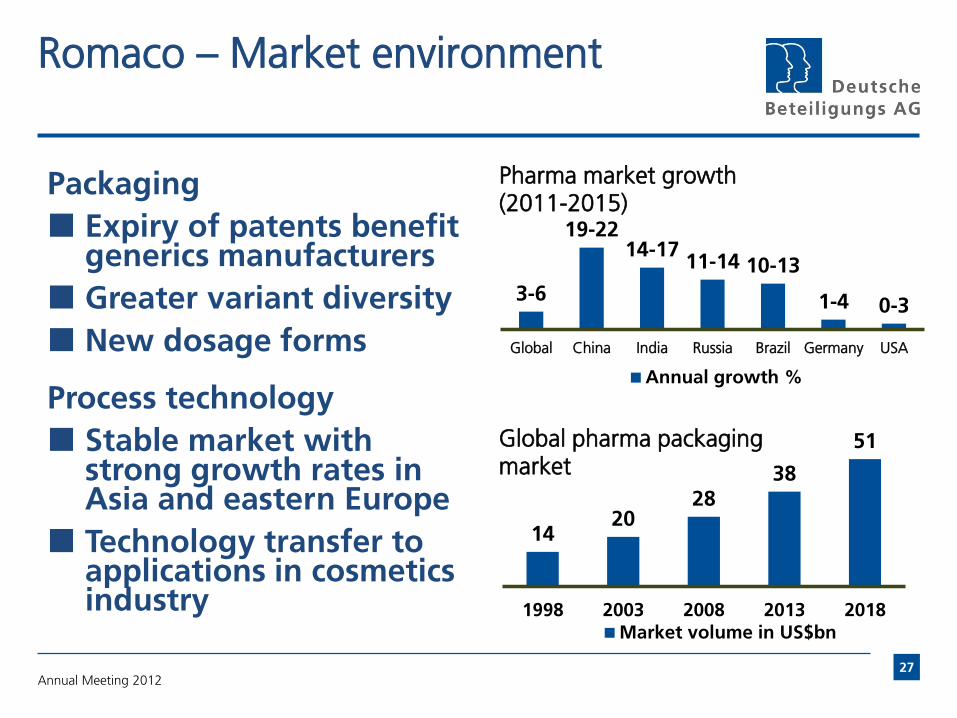

Romaco – Market environment

Packaging

Expiry of patents benefit generics manufacturers

Greater variant diversity

New dosage forms

Process technology

Stable market with strong growth rates in Asia and eastern Europe

Technology transfer to applications in cosmetics industry

14 20

28 38

51

1998 2003 2008 2013 2018

Global pharma packaging market

Market volume in US$bn

3-6

19-22 14-17

11-14 10-13

1-4 0-3

Global China India Russia Brazil Germany USA

Pharma market growth (2011-2015)

Annual growth %

Annual Meeting 2012 27

Spheros GmbH – Invested since February 2012

Global leader in development and production of air conditioning/heating systems for buses

Revenues of €185mn

680 employees

Investment: up to €15mn for up to 19% interest (plus up to 76% for DBAG Fund V)

Annual Meeting 2012 28

Spheros at a glance

Annual Meeting 2012

Global market presence -Production sites in Germany, Finland, Turkey, Brazil, India and China - International R&D sites

Innovative, technologically differentiated product portfolio

Leadership position in growing niche market

Clients: bus manufacturers worldwide and bus fleet operators (public and private)

Growth potential through... ...further internationalisation …know-how transfer to other applications

29

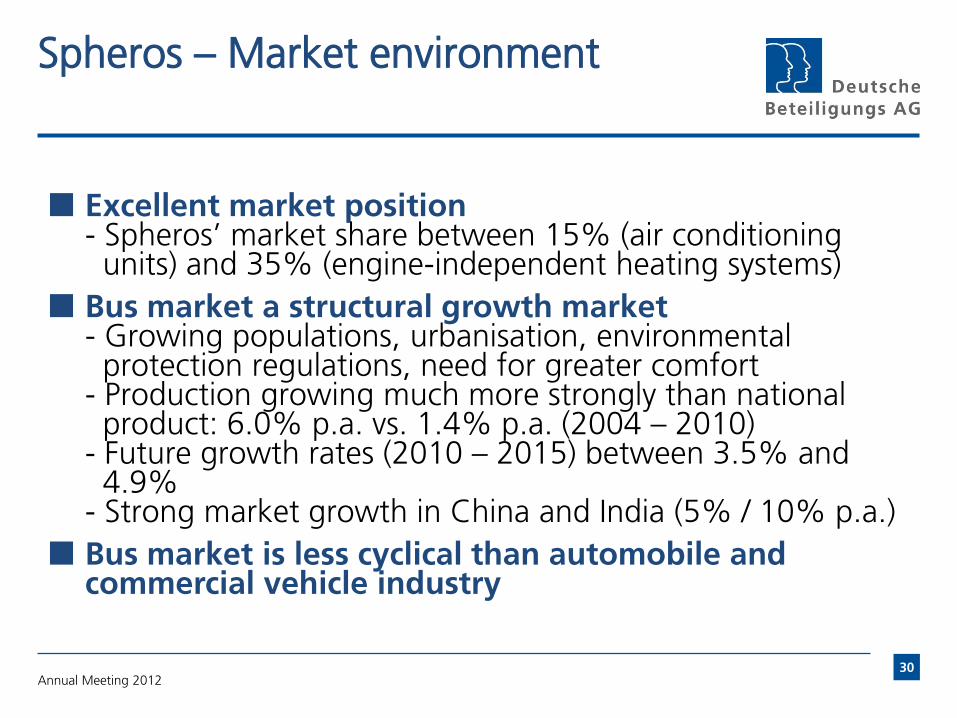

Spheros – Market environment

Excellent market position - Spheros’ market share between 15% (air conditioning units) and 35% (engine-independent heating systems)

Bus market a structural growth market - Growing populations, urbanisation, environmental protection regulations, need for greater comfort - Production growing much more strongly than national product: 6.0% p.a. vs. 1.4% p.a. (2004 – 2010) - Future growth rates (2010 – 2015) between 3.5% and 4.9% - Strong market growth in China and India (5% / 10% p.a.)

Bus market is less cyclical than automobile and commercial vehicle industry

Annual Meeting 2012 30

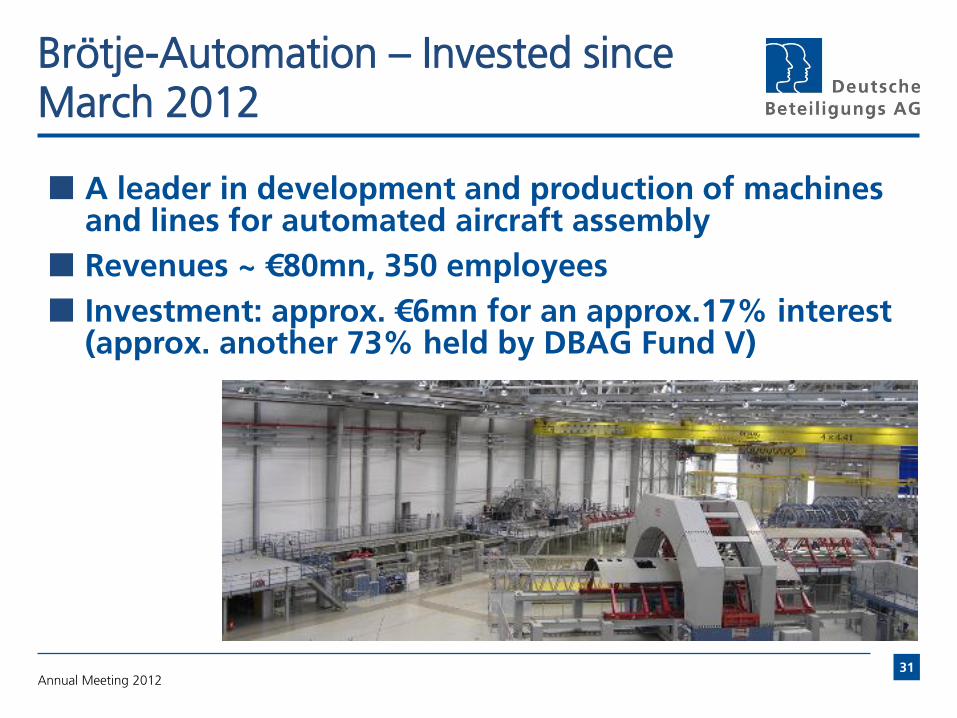

Brötje-Automation – Invested since March 2012

A leader in development and production of machines and lines for automated aircraft assembly

Revenues ~ €80mn, 350 employees

Investment: approx. €6mn for an approx.17% interest (approx. another 73% held by DBAG Fund V)

Annual Meeting 2012 31

Brötje-Automation at a glance

Annual Meeting 2012

Leading market player in its role as a strategic supplier to all major aircraft manufacturers

Products: –Joining technology, especially riveting machines

• Automated production of fuselage and individual sections • Riveting of metal or carbon fibre • Challenge: extremely high precision for positioning of rivets

–Assembly line construction • Factory planning and turnkey services

–Service: high number of installed systems

Transfer of skills to other industries –e.g. machines for use in wind-energy sector (rotor blade

production)

32

Brötje-Automation – Market environment

Brötje-Automation is a leader in a growth market - Aircraft production: expected to grow by 3.3% from

2010 to 2020 Expansion of existing production capacities

New clients: aircraft manufacturers in China and Russia

Quality, reliability, service and ability to construct complete lines are important purchasing criteria for clients - Long-standing customer relationships since early 1990s

USP through benchmark technologies

Annual Meeting 2012 33

Three new management buyouts a basis for future performance

Annual Meeting 2012

Portfolio companies operating in markets that exhibit superior growth

Portfolio companies profiting from current global trends –Romaco: greater prosperity in emerging countries –Spheros: increasing mobility –Brötje-Automation: increasing mobility, rising global cargo

traffic

DBAG Fund V more than 75 percent invested –Eight management buyouts, thereof

• three family-run businesses • one investment (MCE) realised completely, another (Homag

Group AG) partially

34

Focus remains on new investment – Good prerequisites

Experienced investment team, systematically enlarged and strengthened in key competencies –Research – Industrial experts –More team members

Good reputation among all market participants –Citations, i.a. “DACH House of the Year”

Ample liquid funds –Liquidity of ~ €120mn on balance sheet of DBAG –Commitments of ~ €250mn to co-investment funds

Annual Meeting 2012 35

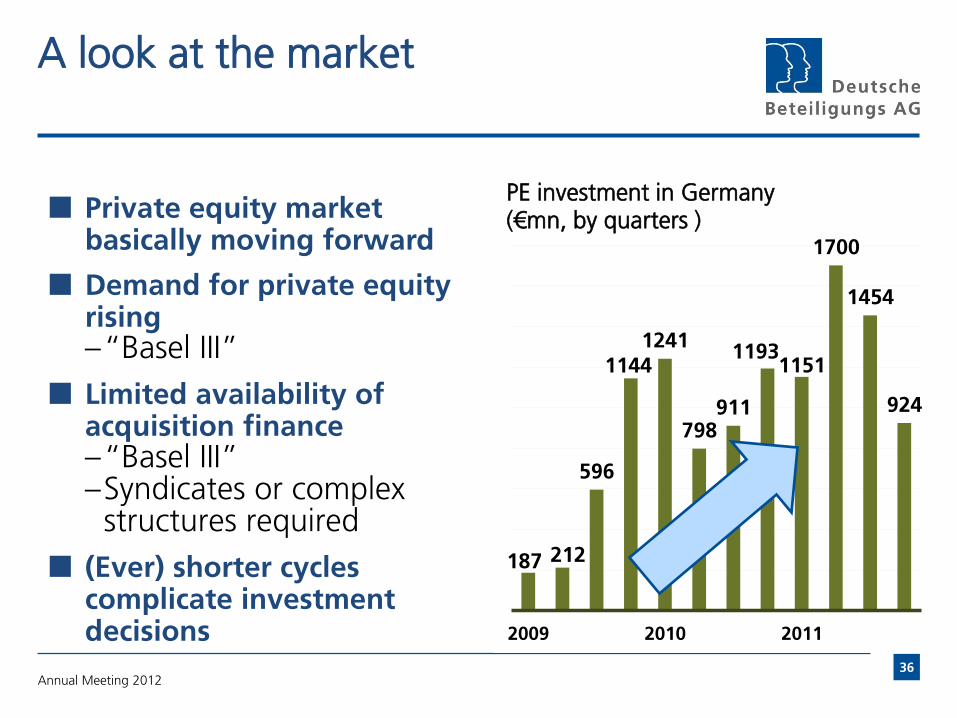

A look at the market

Private equity market basically moving forward

Demand for private equity rising –“Basel III”

Limited availability of acquisition finance –“Basel III” –Syndicates or complex

structures required

(Ever) shorter cycles complicate investment decisions

Annual Meeting 2012

187 212

596

1144 1241

798 911

1193 1151

1700

1454

924

2009 2010 2011

PE investment in Germany (€mn, by quarters )

36

Good start to new financial year: First-quarter net income of €6.9mn

Net income of €6.9mn in first quarter

Net asset value per share is €17.96 –An increase of 2.9% in the first three months of 2011/12*

Gain primarily derives from net result of valuation –Good current trading performance by portfolio companies:

2012 budgets > 2011 actual –Homag (share price up 15% in Q1) –Higher multiples in all sectors

Portfolio companies continue to make good progress

But: earnings forecasts remain difficult to make in view of prevailing uncertainty

Annual Meeting 2012

* Based on NAV per share at 31 October 2011, less proposed dividend

37

Commitment to social matters

“Friends and Sponsors of the Schirn”–

Sponsorship continued this year

Annual Meeting 2012 38

Agenda Item 1

Presentation of the adopted annual Financial Statements and Management’s Report of Deutsche Beteiligungs AG at 31 October 2011, together with an explanatory report by the Board of Management on disclosures pursuant to § 289 (4) HGB (German Commercial Code); presentation of the approved Consolidated Financial Statements and Management’s Report for the Group at 31 October 2011, together with an explanatory report by the Board of Management on disclosures pursuant to § 315 (4) HGB and the Report of the Supervisory Board

Annual Meeting 2012 39

Agenda Item 2

Resolution on the appropriation of retained profit

Annual Meeting 2012 40

Agenda Item 3

Resolution on the ratification of the actions of the members of the Board of Management for financial year 2010/2011

Annual Meeting 2012 41

Agenda Item 4

Resolution on the ratification of the actions of the members of the Supervisory Board for financial year 2010/2011

Annual Meeting 2012 42

Agenda Item 5

Appointment of auditors for financial year 2011/2012

Annual Meeting 2012 43

Thank you!

Auf Wiedersehen in March 2013

For the latest news visit www.deutsche-beteiligung.de

Annual Meeting 2012 44

This presentation contains forward-looking statements. Forward-looking statements are

statements that are not historical facts, including statements about our beliefs and expectations.

Any statement in this presentation that states our intentions, beliefs, expectations or predictions

(and the assumptions underlying them) is a forward-looking statement. These statements are

based on plans, estimates and projections as they are currently available to the management of

Deutsche Beteiligungs AG. Forward-looking statements therefore speak only as of the date they

are made, and we undertake no obligation to update publicly any of them in light of new

information or future events.

Forward-looking statements involve inherent risks and uncertainties. A number of important

factors could therefore cause actual results to differ materially from those contained in any

forward-looking statement. Such factors include the conditions in the financial markets in

Germany, in Europe, in the United States and elsewhere from which we derive a substantial

portion of our business.

Disclaimer

Annual Meeting 2012 45