welcome to tma’s 94 th annual meeting & conference may 18, 2009 williamsburg, virginia

TRANSCRIPT

Welcome to TMA’s 94th Annual Meeting &

ConferenceMay 18, 2009

Williamsburg, Virginia

Farrell DelmanPresident

Tobacco Merchants Association

TMA’s 94th Annual Meeting & ConferenceMay 18, 2009

Williamsburg, Virginia

SCHIP

FCTC

FDA

RECESSION

Conference Overview

• Some Key Trends

• The WHO’s Framework Convention

• SCHIP

• FDA

Conference Overview

• Some Key Trends

• The WHO’s Framework Convention

• SCHIP

• FDA

World CigaretteProduction & Consumption

(Billions of Pieces)

6,0255,745

5,5855,3415,230

5,695

4,693

5,818

5,469 5,5905,296

5,1105,170

4,658

4,000

4,500

5,000

5,500

6,000

6,500

1984 1988 1992 1996 2000 2004 2008

Production Consumption

Source: USDA-FAS, TMA Estimates

World (excluding China)Cigarette Prod. vs. Cons.

(Billions of Pieces)

3,8193,8713,907

3,6973,685

3,994

3,630

3,6233,798

3,7313,636

3,4883,6133,595

3,000

3,500

4,000

4,500

1984 1988 1992 1996 2000 2004 2008

World Production World Consumption

Source: USDA-FAS, TMA Estimates

TAXES … SMOKING BANS … NO ADVERTISING

POINT-OF-SALE AD BANS … KIDS

IN CARS … OUTDOOR SMOKING

Sales Trends: Shorter Cigarettes

Marlboro 72’s(Philip Morris USA and PMI)

Sales Trends: Smokeless Products Around the

World

United States

Sweden

India

The E-Cigarette

Ruyun

Freedome-Cigarette-USA

Equazcion

The China National Tobacco Corp. (CNTC) is the largest cigarette producer in the world

and China is nearing 40% of the world’s consumption

2,206

1,677

1,874

1,684

2,022

1,722

2,196

1,6711,666

1,859

1,708

2,008

1,600

1,700

1,800

1,900

2,000

2,100

2,200

2,300

1998 2000 2002 2004 2006 2008

Production

Consumption

China’s Cigarette Market(Billions of Pieces)

Source: CNTC

2,218

3,545

2,219

3,497

2,221

3,449

2,223

3,401

2,224

3,353

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2009 2010 2011 2012 2013

China Cig. Consumption World minus China Cig. Consumption

China vs. World Cigarette Consumption

Forecasts(Billions of Pieces)

Source: TMA Estimates

CNTCSales

Imports

CNTCSales

Imports

A Chinese WallAgainst Cigarette Imports

(% of Total)

1998 2008

Source: TMA.org, CNTC

1988

CNTCSales

Imports2,195.74 bn(99.84%)

3.50 bn(0.16%)

1,655.3 bn(99.79%)

15.99 bn(1.02%)

3.42 bn(0.21%)

1,557.08 bn(98.98%)

Since Joining the WTO in 1997,China’s Market is as Closed as Ever

15.75016.186

17.01718.728

19.45121.404

22.067 23.203

2001 2002 2003 2004 2005 2006 2007 2008

Sales Trends: Cigars

(Billions of Pieces)

Source: TMA International Issues Monitor

68.2769.89 71.86

87.1892.93 94.36

$15.17$13.80$11.47$6.93$6.04$6.60

1998 2000 2002 2004 2006 2008

Volume (Th. of MT) Value (Bn of US$)

Sales Trends: Roll-Your-Own

(Billions of Pieces)

Source: TMA International Issues Monitor

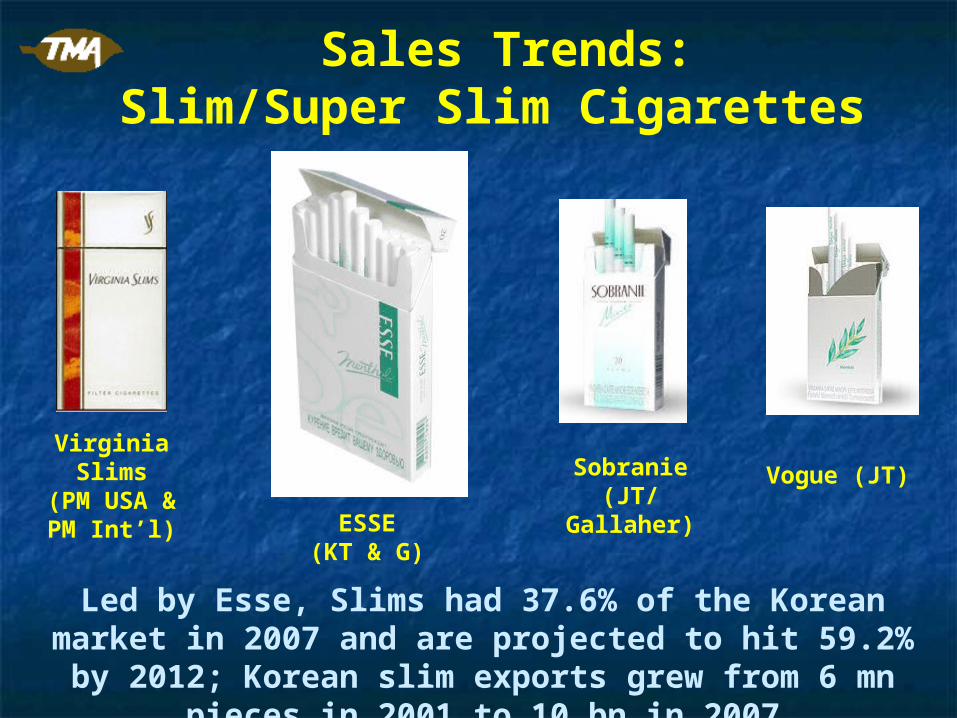

Sales Trends:Slim/Super Slim Cigarettes

Virginia Slims(PM USA &

PM Int’l)Vogue (JT)

ESSE(KT & G)

Sobranie(JT/Gallaher)

Led by Esse, Slims had 37.6% of the Korean market in 2007 and are projected to hit 59.2% by 2012; Korean slim exports grew

from 6 mn pieces in 2001 to 10 bn in 2007

Next Stops for Public Health?

Fast FoodObesity

AlcoholBig Pharma

Conference Overview

• Some Key Trends

• The WHO’s Framework Convention

• SCHIP

• FDA

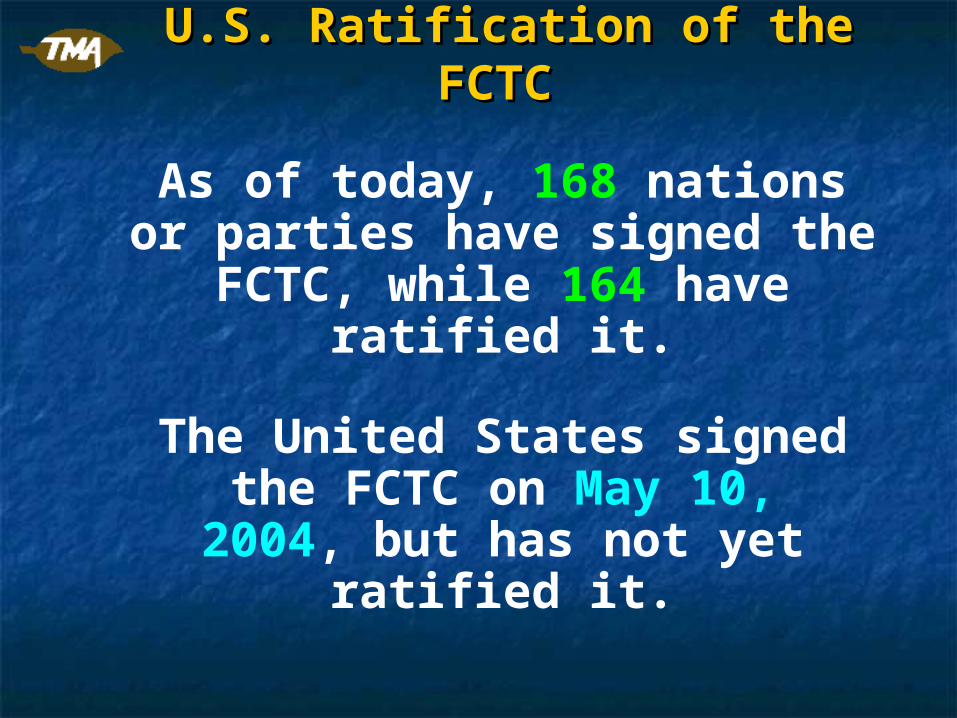

U.S. Ratification of the U.S. Ratification of the FCTCFCTC

As of today, 168 nations or parties have signed the FCTC, while 164 have

ratified it.

The United States signed the FCTC on May 10, 2004, but has not yet

ratified it.

May 1999: The 52nd World Health Assembly backs aresolution which calls for the development of aFramework Convention on Tobacco Control.

October 1999: 1st session of FCTC Technical Working GroupOctober 2000: Public hearings on FCTC held

1st session of Intergovernmental Negotiating Body heldMarch 2003: WHO members draft FCTC text May 2003: 192 nations adopt FCTC text at WHO’s 56th AssemblyOctober 2004: 1st TobReg MeetingApril 2005: 1st TobLabNet MeetingFeb. 2006: 1st Conference of the Parties [COP]Feb. 2008: 1st session of INB to negotiate protocol on illicit tradeMarch 2009: 4th TobLabNet meeting held in Rio, BrazilJune 2009: 3rd session of INB to be held in Geneva4Q10: 4th session of the COP to be held in Uruguay

FCTC - TimelineFCTC - Timeline

FCTC: Articles 9 and 10FCTC: Articles 9 and 10 Article 9: Tobacco Product Content

COP 3 recommended to submit a report at COP 4 which: Identifies best practices in reporting to regulators regarding

content, emissions and product characteristics Validate, within 5 years, the analytical chemical methods for

testing and measuring cigarette content and emissions

Article 10: Tobacco Product Disclosure COP 3 recommended to submit a report at COP 4 which: Collects and analyzes information on legal

cases related to tobacco product disclosures

FCTC: Article 11FCTC: Article 11 Tobacco Product Packaging and

Labeling

The COP 3 recommends: Well-designed health warnings and

messages Large picture warnings located on principal

display areas The use of color rather than just black &

white along with relevant qualitative statements to be displayed on each pack (or package) about the emissions of the tobacco

Nations should also consider adopting measures to restrict or prohibit the use of logos, colors, brand images or promotional information on packaging other than brand names and product names displayed in a standard color and font style (plain packaging).

FCTC: Article 15 - Illicit TradeFCTC: Article 15 - Illicit Trade INB -3 Protocol Now Being Developed

Defines “Illicit” as Smuggling Illicit Manufacturing Counterfeiting

Create Practical T&T System (s) Cases / Pallets vs. Cartons vs. Packs

“Sales only allowed in X Country/Province” To Determine Point of Diversion Monitoring & Reporting System (s) to Track the Product Movement

through Distribution Authorized Enforcement Access to commercial shipment data bases

Mandates Cooperation & Data Sharing Among National & International Agencies (AP) Monitor & Collect Data on Cross-border trade

(not national data alone) As well as all product “moving under suspension

of taxes or duties within its jurisdiction” Provide COP Reports

Requires destroying counterfeit & contraband product and machinery used to produce it and the confiscation of ill-gotten gains

Encourages Nations to Enact Penalties and Remedies, including licensing, to prevent illicit trade “including counterfeit and contraband” (AP)

FCTC: Article 15 - Illicit TradeFCTC: Article 15 - Illicit Trade

U.S. Ratification of the U.S. Ratification of the FCTCFCTC

FCTC Checklist:

(Article 5) General Obligations (Article 6) Price and Tax

Measures (Article 8) Protection from ETS (Article 9) Contents of Tobacco Products

[FDA] (Article 10)Tobacco Product Disclosure [FDA] (Article 11) Packaging & Labeling of Tobacco

Products [FDA](Article 12) Education, Communication, Training & Public Awareness

(Article 13)Tobacco Advertising, Promotion & Sponsorship [FDA]

(Article 15) Illicit Trade in Tobacco Products [FDA]

(Article 19) Liability

Conference Overview

• Some Key Trends

• The WHO’s Framework Convention

• SCHIP

• FDA

US Federal Excise Taxes on US Federal Excise Taxes on Tobacco ProductsTobacco ProductsFirst ImplementedFirst Implemented

1862: Large Cigars1865: Cigarettes1897: Little Cigars (Under 3 pounds per 1,000)1917: Pipe, Snuff and Chewing Tobacco1965: Pipe, Snuff and Chewing tax eliminated1989: Pipe, Snuff and Chewing Tobacco2000: Roll-Your-Own Tobacco

The US Federal Cigarette The US Federal Cigarette Excise Tax TimelineExcise Tax Timeline

(US$ per 1,000 pieces)(US$ per 1,000 pieces)1865: $1.20 - to pay costs from the Civil Warc.1880: $1.75c.1890: $0.501920: $3.00 - to pay costs from World War I1941: $3.25 - to pay costs from World War II1943: $3.50 - to pay costs from World War II1952: $4.00 - to pay costs from the Korean War1983: $8.00 - “Tax Equity & Fiscal Resp. Act of 1982”1991: $10.00 - “Omnibus Budget Recon. Act of 1990”1993: $12.00 - “Omnibus Budget Recon. Act of 1990”2000: $17.00 - for uninsured children’s health care2002: $19.50 - for uninsured children’s health care2009: $50.33 – State Children’s Health Insurance (SCHIP)

““SCHIP” Excise Tax Rate SCHIP” Excise Tax Rate HikesHikes

ProductProduct Old RateOld Rate Current Rate Current Rate % % IncreaseIncrease

CigarettesCigarettes 3939¢/pack¢/pack $1.0066/pack$1.0066/pack 158.1%158.1%

Little CigarsLittle Cigars 3.763.76¢/pack¢/pack $1.0066/pack$1.0066/pack 2,577.1%2,577.1%

Large Large CigarsCigars

20.719%20.719% 52.75%52.75% 154.6%154.6%

Large Cigar Large Cigar Tax CapTax Cap

4.8754.875¢/¢/piecepiece

40.2640.26¢/¢/piecepiece 725.8%725.8%

Chewing Chewing Tob.Tob.

19.519.5¢/lb.¢/lb. 50.3350.33¢/lb.¢/lb. 158.1%158.1%

SnuffSnuff 58.558.5¢/lb.¢/lb. $1.51/lb.$1.51/lb. 158.1%158.1%

Pipe Pipe TobaccoTobacco

109.69109.69¢/lb.¢/lb. 283.11283.11¢/lb.¢/lb. 158.1%158.1%

RYO RYO TobaccoTobacco

109.69109.69¢/lb.¢/lb. $24.78/lb.$24.78/lb. 2,159.1%2,159.1%

State Tobacco Product State Tobacco Product Excise TaxesExcise Taxes

Cigarettes - All 50 States and D.C.- All 50 States and D.C.

Large Cigars - 47 States and D.C.- 47 States and D.C. (excl. (excl. FLFL, , NHNH, , PAPA))

Little Cigars - 49 States and D.C. (excl. - 49 States and D.C. (excl. PAPA))

Smoking Tob. - 49 States and D.C. (excl. - 49 States and D.C. (excl. PAPA))

Chewing Tob. - 49 States and D.C. (excl. - 49 States and D.C. (excl. PAPA))

Snuff - 49 States and D.C. (excl. - 49 States and D.C. (excl. PAPA))

NOTE: Florida Senate Bill 1840 would impose anOTP tax rate of $1 per ounce on cigars.

Local Tobacco Product Local Tobacco Product Excise TaxesExcise Taxes

Cigarette - 8 States (- 8 States (AKAK, , ALAL, , HIHI, , ILIL, , MOMO,, NYNY, , OHOH, , VAVA))

Major cities include among Major cities include among others:others:

Anchorage, AKAnchorage, AK Chicago, ILChicago, IL Honolulu, HI Honolulu, HI New York City, NYNew York City, NY Cleveland, OH Cleveland, OH

AlabamaAlabama (269 cities, 53 counties); (269 cities, 53 counties); MissouriMissouri - 129 - 129

Cigar - 4 States (- 4 States (AKAK, , ALAL, , HIHI, , MDMD))

OTP - 4 States (- 4 States (AKAK, , ALAL, , HIHI, , MDMD))Source: TMA’s Tobacco Tax Guide (May 2009)

State Cigarette Excise Tax IncreasesState Cigarette Excise Tax Increases (1999 (1999 – 2009)– 2009)

# of Bills # of States # of Approvals

1999 57 21 3 (MD, NH, NY)

2000 24 7 1 (LA)

2001 51 26 5 (ME (2), RI, WA, WI)

2002 116 34 21 (AZ, CT, DC, HI, IN, IL, KS,

LA, MA, MD, MI, NE, NJ, NY,

OH, OR, PA, RI, TN, UT, VT)

2003 175 37 15 (AR, CT, DE, DC, GA, ID, MT,

NJ, NM, NV, PA, RI, SD, WV, WY)

2004 139 33 8 (AL, AK, CO, MI, MT, NJ, RI, VA)

2005 114 30 9 (KY, ME, MN(2), NC, NH,NM, OH, RI, WA)

2006 57 25 6 (AZ, HI, NJ, SD, TX, VT)

2007 105 24 8 (CT, DE, IN, IA, MD, NH, TN, WI)

2008 57 20 4 (DC, MA, NH, NY)

2009 89 32 4 (AR, KY, MS, RI…HI)

The Shrinking U.S. The Shrinking U.S. Cigarette MarketCigarette Market

300

350

400

450

500

550

600

650

700

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

Cigarette Consumption

FET Doubled(1983)

Peak: 1981 – 641 bn. pieces

Marlboro Friday(April 1993)

MSA (November 1998)

Bottom: 2008 – 345.1 bn. pieces

Source: USDA-Economic Research Service

TMA’s Tobacco USA

Source: TTB

Cigarette DomesticCigarette DomesticTaxable RemovalsTaxable Removals

(First Quarter 2009)(First Quarter 2009)

25.469 25.368 25.967

0

5

10

15

20

25

30

January February March

Domestic Taxable Removals

(Bn. of Pcs.)

50

60

70

80

90

100

2002 2003 2004 2005 2006 2007 2008 2009

1Q 2Q 3Q 4Q

U.S. Cigarette Sales by Quarter

(Billions of Pieces)

Source: Maxwell Consumer Report

-10.45% vs. 1Q08

Taxable Removals by ProductTaxable Removals by Product(February 2009 vs. March 2009)(February 2009 vs. March 2009)

2.502.60

7.607.00

0.190.27

1.871.30

0

1

2

3

4

5

6

7

8

Chew.Tob.

Snuff Pipe Tob. RYOTob.

February March

(Mn. of Lbs.)

(Mn. of Pcs.)

455.0

548.5498.2

323.3

0

100

200

300

400

500

600

Large Cigars Little Cigars

February March

Source: TTB

2008 Est. price: 2008 consumption:$4.58 345.1 billion pieces

2009 Est. price: 2009e consumption:Elasticity:$5.50 327.8 billion pieces -0.250

$5.50 324.3 billion pieces -0.300

$5.50 320.8 billion pieces -0.350

$5.50 317.4 billion pieces -0.400

U.S. CigaretteU.S. CigarettePrice ElasticityPrice Elasticity

e = Δ Quantity/ Δ Price

388376

372364

345

324319

314

2004 2005 2006 2007 2008 2009e 2010e 2011e

Cigarettes (Bn. Pcs)

U.S. Cigarette Forecast(Billions of Pieces)

Source: TMA Estimate

2009 FET 2009 Consumption 2009 Fed. Tax. Rev.$0.39/pk 80.11 bn. pc. (Jan-Mar) $1,562.1 mn$1.0066/pk 244.19 bn. pc. (Apr-Dec) $12,290.1 mnTOTAL 324.30 bn. pc. $13,852.2 mn

Cigarette Tax Revenue Forecast(Millions of US$)

2008 FET 2008 Consumption 2008 Fed. Tax. Rev.$0.39/pk 345.15 bn. pc $6,730.4 mn

Source: TMA Estimate

The Federal government is expected to collect an additional $7.12 billion in

2009.

Cigarette Tax Revenue Forecast(Millions of US$)

2008 SET 2008 Consumption 2008 State. Tax. Rev.$1.08/pk 345.15 bn. pc $18,638.1 mn2009 SET 2009 Consumption2009 State. Tax. Rev.$1.12/pk 324.30 bn. pc $18,160.8 mn

State governments will collect $477.3 mn less in tax revenues even as some States raise their excise tax rates in

2009.Source: TMA Estimate

State MSA Revenue Forecast(Millions of US$)

2008 Consumption 2008 MSA Payment (in 2009) 345.15 bn. pc $6,769.1 mn

State governments will collect $138.3 mn less in MSA payments as the

cigarette market continues to decline.

Source: TMA Estimate

2009 Consumption 2009 Est. MSA Payment (in 2010) 324.30 bn. pc $6,630.8 mn

Cigarette Tax Incidence - 2007Cigarette Tax Incidence - 2007(tax share of retail price)(tax share of retail price)

Avg. Price Sales Tax State per pack FET SET Tax Inc.

South $3.658 $0.39 $0.07 $0.196 17.9%Carolina

US $4.678 $0.39 $1.0725 $0.239 36.4%(Average)

Rhode $6.590 $0.39 $2.46 $0.405 49.4%Island

NOTE: The price figures include sales taxes.Source: TMA, Orzechowski & Walker

Cigarette Tax Incidence - 2009Cigarette Tax Incidence - 2009(% of tax share of retail price)(% of tax share of retail price)

Avg. Price Sales Tax State per pack FET SET Tax Inc.

South $4.574 $1.01 $0.07 $0.259 29.3%Carolina +25%

US $5.743 $1.01 $1.12 $0.247 41.4%(Average)

Rhode $8.584 $1.01 $3.46 $0.562 58.6%Island +30.26%

NOTE: The price figures contain sales taxes.Source: TMA estimates

Retail Price and Tax Incidence Retail Price and Tax Incidence Figures f0r 2008Figures f0r 2008

Retail Price Tax Incidence

Norway $11.72 71.20%UK $9.16 76.49%Australia $8.46 65.65%Singapore $7.95 70.54%Canada $7.50 70.73%France $7.24 80.39%Germany $6.82 76.45%Italy $5.80 75.17%

All Prices are in US Dollars per pack of 20.

Retail PriceTax Incidence

United States $4.6836.97%

Spain $4.0977.35%

Portugal $3.8650.25%

Poland $3.1474.15%

Japan $3.2163.06%

China $2.2060.73%

South Korea $1.8862.61%

Indonesia $0.9049.09%

Estimated Price Structure of aPremium Pack of Cigarettes

(2009)(% of total price)

9.7

18.4

20.4

32.5

10.9

8.2

0

20

40

60

80

100Operating Expenses($1.79)

State Excise Tax ($1.12)

Federal Excise Tax($1.01)

MSA Payment ($0.45)

Trade (Wholesale andRetail ($0.53)

Profit ($0.60)

Assuming an average retail price of a pack of premium cigarettes in 2009 at $5.50 (not

including sales tax).Source: TMA EstimateSource: TMA Estimate

Estimated Price Structure of a4th Tier Pack of Cigarettes

(2009)(Percentage of total price)

9.7

30.6

33.9

10.9

4.5

10.3

0

20

40

60

80

100Operating Expenses($0.36)

State Excise Tax ($1.12)

Federal Excise Tax($1.01)

MSA Payment (SPM)/Escrow (NPM) ($0.34)

Trade (Wholesale andRetail ($0.32)

Profit ($0.15)

Assuming a 4th tier average national retail price in 2009 of $3.30.

Source: TMA EstimateSource: TMA Estimate

““SCHIP” Excise Tax Rate SCHIP” Excise Tax Rate HikesHikes

ProductProduct Old RateOld Rate Current Rate Current Rate % % IncreaseIncrease

CigarettesCigarettes 3939¢/pack¢/pack $1.0066/pack$1.0066/pack 158.1%158.1%

Little CigarsLittle Cigars 3.763.76¢/pack¢/pack $1.0066/pack$1.0066/pack 2,577.1%2,577.1%

Large Large CigarsCigars

20.719%20.719% 52.75%52.75% 154.6%154.6%

Large Cigar Large Cigar Tax CapTax Cap

4.8754.875¢/¢/piecepiece

40.2640.26¢/¢/piecepiece 725.8%725.8%

Chewing Chewing Tob.Tob.

19.519.5¢/lb.¢/lb. 50.3350.33¢/lb.¢/lb. 158.1%158.1%

SnuffSnuff 58.558.5¢/lb.¢/lb. $1.51/lb.$1.51/lb. 158.1%158.1%

Pipe Pipe TobaccoTobacco

109.69109.69¢/lb.¢/lb. 283.11283.11¢/lb.¢/lb. 158.1%158.1%

RYO RYO TobaccoTobacco

109.69109.69¢/lb.¢/lb. $24.78/lb.$24.78/lb. 2,159.1%2,159.1%

Source: US-TTB

1.642.20 2.24 2.17 2.25 2.30

2.703.77

4.164.77

5.45

0

1

2

3

4

5

6

7

1998 2000 2002 2004 2006 2008

Production Sales

U.S. Little Cigars(Billions of pieces)

1 cigarette = 0.0325 ounces of RYOSource: USDA-AMS

3.163.81

4.164.97

5.546.21

5.756.34 6.06 5.97

6.76

0

1

2

3

4

5

6

7

8

1998 2000 2002 2004 2006 2008

Production Sales

U.S. Roll-Your-Own Tobacco

(Billions of pieces [converted])

Projected Declines in Consumption

(Billions of Pieces)2008 Cons. Proj.

2009 Cons. DifferenceLittle Cigars 5.448 3.269 (-40%) -2.179(bn. pc.) RYO Tobacco 6.762 4.057 (-40%) -2.705(bn. pc.)

Source: TMA Estimate

Combined, the disproportionate excise tax increases for little cigars and RYO

tobacco could boost cigarette consumption by an additional 4.884

billion pieces.

Source: USDA-ERS, US-TTB

3.66 3.85 3.854.11 4.21 4.53

4.944.88

5.30 5.555.76

0

1

2

3

4

5

6

1998 2000 2002 2004 2006 2008

Production Sales

U.S. Large Cigars(Billions of pieces)

Source: USDA-AMS

59.9 61.664.8

66.368.6 71.0

74.7 76.7

81.586.2

91.3

50556065707580859095

1998 2000 2002 2004 2006 2008

Production Sales

U.S. Moist SnuffU.S. Moist Snuff(Millions of pounds)(Millions of pounds)

U.S. Dark Fire-Cured and Dark Air-Cured Production

(Metric Tons)

34.5

11.8

37.1

11.5

37.6

13.2

39.4

13.5

41.7

24.4

0

10

20

30

40

50

2004 2005 2006 2007 2008

Dark Fire-Cured

Dark Air-Cured(One Sucker +Green River)

Source: USDA-NASS

U.S. Tobacco Consumptionby Leaf Equivalents – 2007

(Millions of Pounds)34.4

88.3

634.9

16.3

105.5

Source: US-TTB, USDA-AMS, TMA

Cigarettes (360 bn pc) Cigars (1 cigar = 10g) Smoking Tobacco Chewing TobaccoSnuff

U.S. Tobacco Productionby Leaf Equivalents – 1880

(Millions of Pounds)

32.9

35.3

1.1

4.0

107.2

Source: US Department of Agriculture – ERS, TMA

Cigarettes Cigars (1 cigar = 10g) Smoking Tobacco Chewing TobaccoSnuff

Conference Overview

• Some Key Trends

• The WHO’s Framework Convention

• SCHIP

• FDA

Tobacco RegulatoryTobacco RegulatoryBill ComparisonBill Comparison

IssueIssue Waxman/Waxman/KennedyKennedy

Buyer Buyer Burr/HaganBurr/Hagan

Bill No.Bill No. H.1256/H.1256/S.982S.982

H.1261H.1261 S.579S.579

AgencyAgency ““Center for Center for Tobacco Tobacco

Products” Products” within FDAwithin FDA

““Tobacco Tobacco Harm Harm

Regulation Regulation Center” Center”

within HHSwithin HHS

““Tobacco Tobacco Regulatory Regulatory Agency” Agency”

within HHSwithin HHS

IngredienIngredient t

DisclosurDisclosuree

‘‘Tar’ Tar’ LimitsLimits

Flavor Flavor BanBan

Fire-SafeFire-Safe

IssueIssue Waxman/Waxman/KennedyKennedy

Buyer Buyer Burr/Burr/HaganHagan

AdvertisinAdvertisingg

BanBan

(restrictions(restrictions

))

Graphic Graphic WarningsWarnings

Waxman: May Waxman: May Kennedy: ShallKennedy: Shall

Retail Retail LicensingLicensing

DescriptorDescriptorss

Illicit Illicit tradetrade

Tobacco RegulatoryTobacco RegulatoryBill ComparisonBill Comparison

Manufacturers

TobaccoProduct

ComplianceCenter(TPCC)

StateTax

AdministratorsWholesalers/Distributors

Retailers

LocalTax

Administrators

One important condition:One important condition: Data integrity and Data integrity and audit trail documenting company usageaudit trail documenting company usage

Creating a Centralized License Data Base Creating a Centralized License Data Base of Publicly Available Informationof Publicly Available Information

to Facilitate Public-Private Communicationto Facilitate Public-Private Communication

One-Stop Updating One-Stop Updating with License Suspension Reports Providedwith License Suspension Reports Provided

IssueIssue Waxman/Waxman/KennedyKennedy

Buyer Buyer Burr/HaganBurr/Hagan

Sales Sales RestrictioRestrictio

nsns

SamplingSampling Smokeless in adult

Any TP in adult

SeizureSeizure Small Small Man. Man.

ExemptioExemptionn

User FeesUser Fees From $85mn From $85mn in FY09 to in FY09 to $712mn in $712mn in FY19 and FY19 and

thereafter.thereafter.

Civil money Civil money penalties & penalties & license fees.license fees.

$100mn/yr $100mn/yr starting in starting in FY10 with FY10 with

inflationary inflationary factor factor

thereafter.thereafter.

Tobacco RegulatoryTobacco RegulatoryBill ComparisonBill Comparison

Modified RiskModified Risk

Waxman/Waxman/KennedyKennedy

Sets Sets a very high bara very high bar to making reduced risk claims. to making reduced risk claims. Requires pre-market approval whereby manufacturer Requires pre-market approval whereby manufacturer files an application detailing elements including files an application detailing elements including product description, formulation, and research. Multi-product description, formulation, and research. Multi-year research likely.year research likely.

BuyerBuyer Creates Creates a “reasonably likely” testa “reasonably likely” test for reduced risk for reduced risk claims based on measurable and substantial reductions claims based on measurable and substantial reductions in morbidity and mortality among users; Smokeless in morbidity and mortality among users; Smokeless tobacco product can not be sold as a MR product; tobacco product can not be sold as a MR product; Requires MR product to be labeled such that the Requires MR product to be labeled such that the consumer can easily comprehend the risk.consumer can easily comprehend the risk.

Burr/Burr/HaganHagan

Creates Creates a “totality of scientific knowledge” testa “totality of scientific knowledge” test based based on a number of joint conditions for reduced risk claims on a number of joint conditions for reduced risk claims based on available scientific evidence demonstrating based on available scientific evidence demonstrating that a given product "yields a reduced amount of 1 or that a given product "yields a reduced amount of 1 or more toxicants when compared to an appropriate more toxicants when compared to an appropriate reference tobacco product or products“. reference tobacco product or products“.

Tobacco RegulatoryTobacco RegulatoryBill ComparisonBill Comparison

Uses of the Tobacco Plant(Nicotina Tabacum/Rustica)

Proteins Nicotine

Food EnzymeGeneratio

n

Medicines

Vaccines

HIV, Malaria, Hepatitis B,

Insulin, Auto-Immune Deficiencies

Depression, Cancer, Parkinson’s,Alzheimer’s

Cereal

Traditional

Non-Traditiona

l

Other

Human Growth

Hormone

Nicotine Delivery

Traditional

Non-Traditional

E-Cigarette PatchesSmokin

gTobacco

Smokeless

TobaccoGum/

Lozenges

Snuff

Dry

Moist

Loose Leaf

Cigars

Plug

Twist/Roll

Cigarettes

Firm

MoistMachin

eMade

Hand Made (RYO)

Chewing

Tobacco

Little

Large

PipeTobacc

o

Nasal Spray

Water

Snus

Orbs/Strips/Sticks

U.S. CigaretteNicotine Consumption

(Metric Tons)

458.0451.8

420.4

395.0378.1

354.8340.2

315.5

200

250

300

350

400

450

500

1994 1996 1998 2000 2002 2004 2006 2008

Source: TMA Estimates

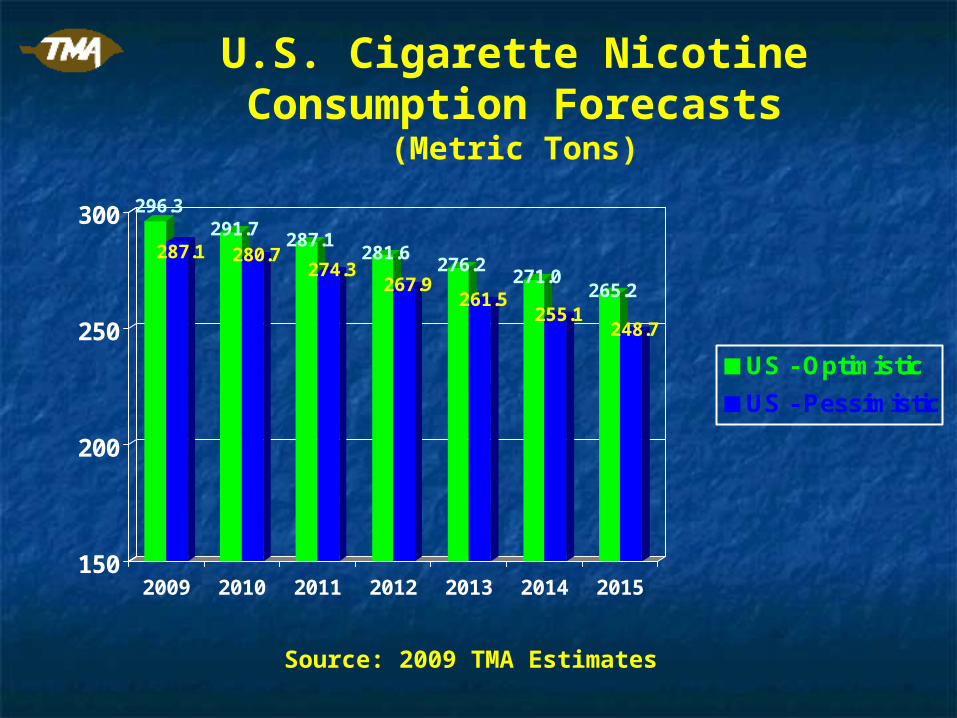

U.S. Cigarette Nicotine Consumption Forecasts

(Metric Tons)

296.3

287.1291.7

280.7287.1

274.3281.6

267.9276.2

261.5271.0

255.1265.2

248.7

150

200

250

300

2009 2010 2011 2012 2013 2014 2015

US - Optimistic

US - Pessimistic

Source: 2009 TMA Estimates

India: Multi-Ethnic,Multi-Lingual, Multi-

Tobacco

THANK YOU!THANK YOU!

And now to the World Leaf And now to the World Leaf Situation & Outlook withSituation & Outlook with

Jim StarkeyJim Starkey

(TMA Chairman and former SVP (TMA Chairman and former SVP Universal Leaf Tobacco)Universal Leaf Tobacco)

TMA Annual Meeting and Conference

Global Leaf Trends Changing Dynamics / Future Trends

Presentation By:

Jim Starkey

Williamsburg, VirginiaMay18, 2009

• Some Significant Changes• Market Implications• Current Supply and Demand Situation• Future Trends / Potential Beneficiaries• Final Observations

2008 Estimated World Leaf Production

Significant Changes

• Sources of leaf have shifted dramatically

Flue-Cured Tobacco Production

1960 2008

Burley Tobacco Production

1960 2008

A Dynamic Industry

• Sources of leaf have shifted dramatically• Consolidation has reduced the number of

industry players– Leaf dealers– Manufacturers

Leaf Industry Consolidation

Past

Universal LeafSocotab (49%)Thorpe & RicksGKCasalee

DibrellIntabexA.G. MonkAustin

TranscontinentalAdamsMeridional

Present

Universal Leaf

Alliance OneMonk Austin

DIMON

Standard Commercial

Manufacturer Consolidation

JT RJI/Gallaher

Imperial Altadis / Commonwealth

BAT ETI / RJ(42%) / Tekel / Scantoco

PM USA John Middleton / UST

PMI Lakson / Sampoerna / Rothmans, Canada

RJ Conwood

The Current SituationA Dynamic Industry

• Cigarette manufacturers expand portfolio– New products/smoking devices– New categories

• Cigars• Smokeless• Snus• Other

Market Implications

• New origins entail greater production risk– Less irrigation– Shift from large commercial farms to small scale– Shift from auction to contracting

• Result is greater downside production risk

Market Implications

• Increased production risk• Buyer/user consolidation

– Smaller numbers– No unplanned inventory– Shorter durations

• Higher market volatility

Market Implications

• Increased production risk• Market volatility• Higher production costs

– Fertilizers– Pesticides and herbicides– Fuel– Labor

• Plus alternative crops– Tobacco growers have alternatives– Crop prices have risen dramatically

Market Implications

• Cost of buyer-mandated programs– Improve leaf quality– Eliminate foreign matter– GAP– Social responsibility

Market Implications

Attractive Alternatives

Buyer Mandates

Higher Leaf

Prices

Increased: Production Risk Market Volatility Production Costs

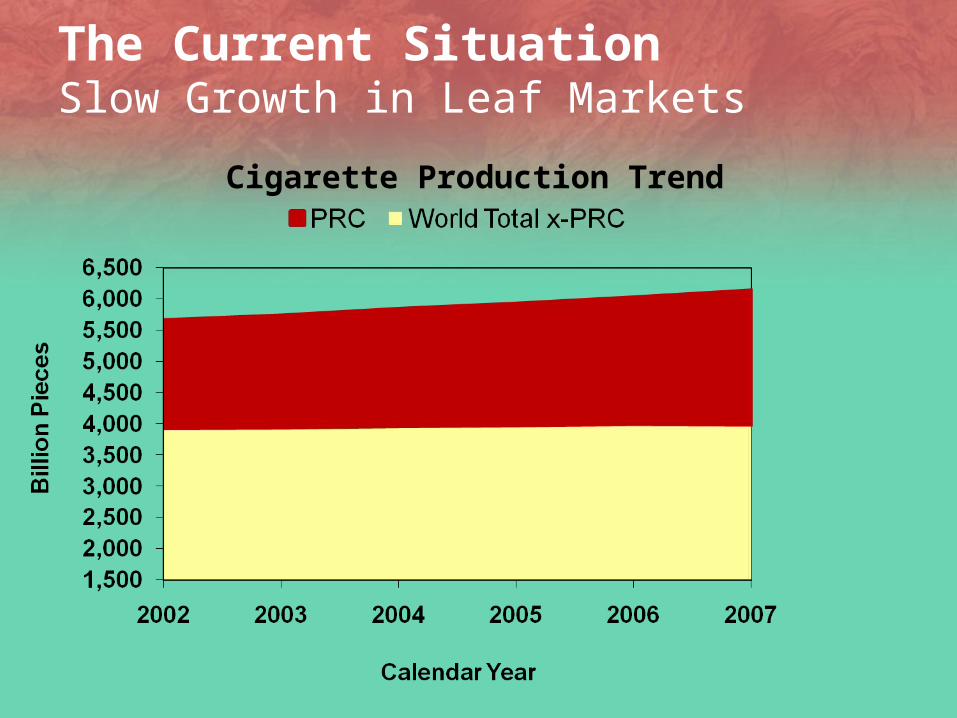

The Current SituationSlow Growth in Leaf Markets

Cigarette Production Trend

The Current SituationSlow Growth in Leaf Markets

• Growth mainly in:– Asia– Eastern Europe– Middle East

• Declines in developed countries– Characterized by:

• Increasing taxation• Increasing regulation• Production shifts

Population growth

Rising income levels

The Current SituationSlow Growth in Leaf Markets

• Less clear how much leaf utilization has increased, if at all outside PRC– New manufacturing technology uses less leaf/stick– Impact of industry consolidation

• Supply chain efficiency• Waste reduction/increased utilization

– American blend growth has stalled – affects burley demand

The Current Situation

FC Leaf Production 2003-2008 (Million Green Kgs)

3,3153,513

3,792 3,702 3,6563,969

PRC Other Exporters

The Current SituationFlue-Cured Leaf Production

• Two very different stories– PRC

• Dramatic growth• 500 mKgs or 28%• Only slightly greater than cigarette production growth (24%)

The Current SituationFlue-Cured Leaf Production

• Exporters down 2%

World Flue-Cured Exporters’ Leaf Production (x-PRC)

The Current SituationFlue-Cured Leaf Production

• 2008 declines in Brazil, Zimbabwe, other Africa and Canada

• More than offset increases in US, EU and India

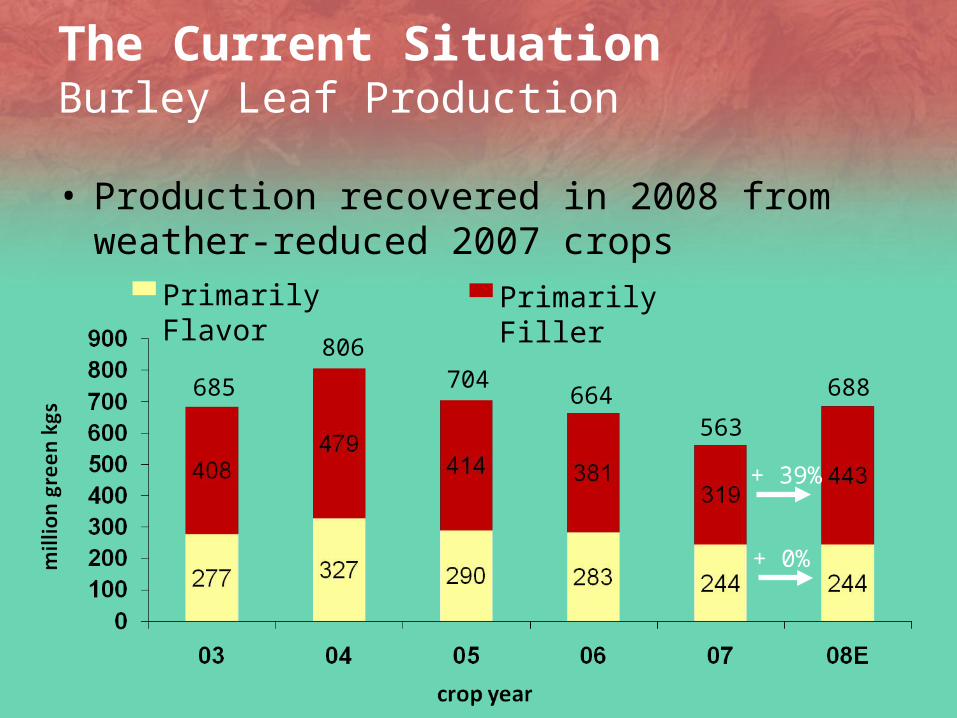

The Current SituationBurley Leaf Production

• Production recovered in 2008 from weather-reduced 2007 crops

685

806704

664563

Primarily Flavor Primarily Filler

+ 39%

+ 0%

688

The Current SituationBurley Leaf Production

• However– Filler primary beneficiary– Flavor styles flat– Burley supplies, particularly flavor remain tight

The Current SituationBurley Production - Flavor

Selected Countries

2000Million

Green Kgs

2007Million

Green Kgs

2008Million

Green Kgs

2007-08%

2000-08%

US 143 102 102 - -29

Brazil 95 105 100 -5 +5

Argentina 39 37 42 +14 +8

The Current SituationBurley Production - Filler

*EU exporters include Poland for all years

Selected Countries

2000Million

Green Kgs

2007Million

Green Kgs

2008Million

Green Kgs

2007-08%

2000-08%

Malawi 142 87 170 +95 +20

Mozambique 6 28 44 +57 +633

Zambia 3 5 12 +140 +300

India 9 15 23 +53 +185

Thailand 28 43 36 -16 +29

EU Exporters*

87 53 56 -3 -36

PRC 62 25 38 +52 -39

Philippines 27 8 9 +13 -67

Mexico 23 10 10 - -57

S. Korea 22 9 9 - -59

The Current SituationUnsold Stocks

• Last piece of market puzzle– Flue-cured unsold stocks

• At lowest level since 1991• Reflects lower 2008 production x-PRC

The Current SituationUnsold Stocks

85

128

151

187

98

72

U.S. Pool Others

World Uncommitted Flue-Cured Stocks as of June 30

The Current SituationUnsold Stocks

• Flue-cured markets balanced heading into 2009

The Current SituationUnsold Stocks

• Burley unsold stocks– Essentially gone

49

86 8572

29

U.S. Pool Others

9

World Uncommitted Burley Stocks as of June 30

The Current SituationUnsold Stocks

• Burley markets remain– Extremely tight for flavor– Still tight for filler

Future Trends/Potential Beneficiaries

• Cigarette Production– China will be main growth engine– Growth outside China will be slow (0-0.3%)

• Growth in Asia, Middle East, and Eastern Europe• Offset by continued declines in developed countries• Leaf markets will be at best flat

Future Trends/Potential Beneficiaries

• Leaf production – short term– 2009 Flue-cured

• Total production forecast to increase due to mainly PRC• Production by exporters x-PRC projected to rise

Estimated Flue-Cured Production in Million Green Kgs

2007 2008E 2009P Change over 08

Brazil 643 608 595 -13

India 260 270 280 10

US 220 231 227 -4

All x-PRC 1,706 1,669 1,750 81

PRC 1,950 2,150 2,200 50

Others 216 217 210 -7

World Total 3,873 4,028 4,160 132

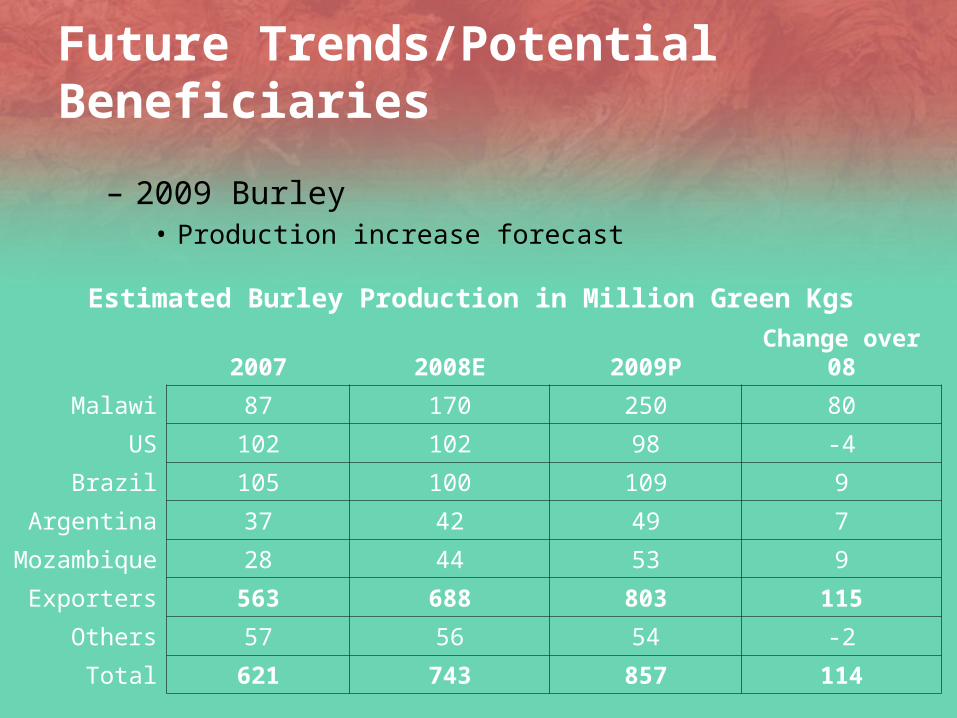

Future Trends/Potential Beneficiaries

– 2009 Burley• Production increase forecast

Estimated Burley Production in Million Green Kgs

2007 2008E 2009P Change over 08

Malawi 87 170 250 80

US 102 102 98 -4

Brazil 105 100 109 9

Argentina 37 42 49 7

Mozambique 28 44 53 9

Exporters 563 688 803 115

Others 57 56 54 -2

Total 621 743 857 114

Future Trends/Potential Beneficiaries

• Will not materially change tight supply situation, particularly flavor

• Significant downside risk

Future Trends/Potential BeneficiariesSlow Growth – What Could Change Trend?

• Higher production and leaf use– Development and consumer acceptance of reduced

risk products that look and act like traditional products– Increased consumption of OTP and snus could create

increased demand for dark air-cured leaf at expense of flue-cured and burley

Future Trends/Potential BeneficiariesSlow Growth – What Could Change Trend?

• Lower production and leaf use– Serious government effort to reduce PRC cigarette

consumption– Development and consumer acceptance of reduced

risk products using heating rather than burning technology

– These products require less leaf

Future Trends/Potential Beneficiaries

• Not much change from current situation• Flue-cured – Flavor

– Brazil• Will continue to dominate • Not immune to weather risk• Strong real raises dollar costs and prices

– U.S.• Termination of program improved leaf competitiveness• Quality remains best• Highest priced but dollar weakness reduces gap

Future Trends

• Flue-Cured - Flavor– U.S.

• Termination of program improved leaf competitiveness• Quality remains best• Highest priced but dollar weakness reduces gap• Probably will remain mainly domestic supplier

– Zimbabwe• Future depends on political/economic change• Would be strong demand, particularly from Europe and as

alternative to Brazil• Production will not recover quickly• Unlikely to reach past levels

Future Trends

• Flue-Cured – Filler

Future Trends

• Flue-Cured – Filler– PRC

• Will grow to meet domestic demand• Exports face increasing competition from India• Reliable supplier concerns make PRC alternate choice

• Questions:– Will PRC continue domestic focus or seek to expand

exports– Can PRC produce significant quantities of an

“acceptable” flavor style

Future TrendsWinners and Losers

• Flue-Cured – Filler– Other Africa

• Zambia, Malawi, Tanzania and Uganda have potential• Excellent conditions including land, labor and climate• Lack of infrastructure/high cost of expansion• Affects competitiveness in market• Absence of land tenure systems is a major problem in some

African countries

– India, Pakistan, Bangladesh• Very competitive in price/quality• Production increasing• Could benefit from European decline• However all have growing domestic markets

Future TrendsWinners and Losers

• Flue-Cured – Filler– Europe

• Full decoupling in 2011 could result in significant decline in production

• Some member states have talked about national subsidies to maintain industry/employment

– Canada• Is essentially a domestic crop now

Future TrendsWinners and Losers

• Burley situation is very tight and demand remains strong

• Uncommitted stocks likely continuing at very low levels

• Burley flavor– Brazil

• Only Brazil has potential for significant increases in short term

• Costs/prices will go up– Strength of real– Prices of other crops – maize, soybeans

Future TrendsWinners and Losers

• Burley flavor– U.S.

• Little interest in producing more even at higher prices in traditional areas

• Further U.S. increases will depend on developing non-traditional areas

Future TrendsWinners and Losers

• Burley – Filler– Malawi

• May be reaching practical limits• Weather risk, particularly drought may be increasing• Prices likely to increase

– Mozambique• Could double production with existing infrastructure• Additional increases possible with additional infrastructure

investment• Dollar prices will have to double to offset impact of strong

currency on local costs and grower incomes

Some Final ObservationsManufacturers Will Determine Where Leaf is Produced

• Price/quality• Risk diversification

– Weather– Political/economic– Reliability of supply

• Scale is important• Other factors

– Social responsibility– Sustainable production practices– Environmental stewardship

Some Final ObservationsProduction Will Likely Remain in Traditional Origins

• New origins are expensive to develop• Dealers can’t afford w/o manufacturer support• More than enough capacity in traditional areas

Some Final Observations

• Production volatility will increase– Shift to non-irrigated production– Little irrigation in new origins– Long term (20-50 year) forecast is:

• Drier weather patterns in Southern Hemisphere• Periods of much wetter and much drier weather

• Shift from auction to direct contracting shifts risk from growers to dealers

Some Final ObservationsContinued

• Leaf prices will rise– Offset dollar decline on local currency costs and

incomes outside U.S.– Rising prices of alternative crops– Cover costs of programs promoted by manufacturers

to:• Improve quality• GAP• Social responsibility

Some Final ObservationsContinued

• Reduced risk products could revolutionize and revitalize industry– Impact level of cigarette and other product

manufacture– Leaf requirements– Future origins

TMA Annual Meeting and Conference

Global Leaf Trends Changing Dynamics / Future Trends

Presentation By:

Jim Starkey

Williamsburg, VirginiaMay18, 2009