wes lefroy raboresearch agricultural analyst september ... · q1 2016 q2 2016 6 q4 2016 q1 2017 q2...

TRANSCRIPT

Rabobank Land Price Outlook

Wes LefroyRaboResearch Agricultural Analyst

More Smoke, Less Fire

September 2019Monaro Farming Systems

RaboResearch Food and Agri

2

A global team of analysts – supporting insight based banking

Our Agenda for Today

3

Section 1 The key driver of land prices has shifted

Section 2 Macro forces look more challenging ahead

Section 3 Land price growth will slow

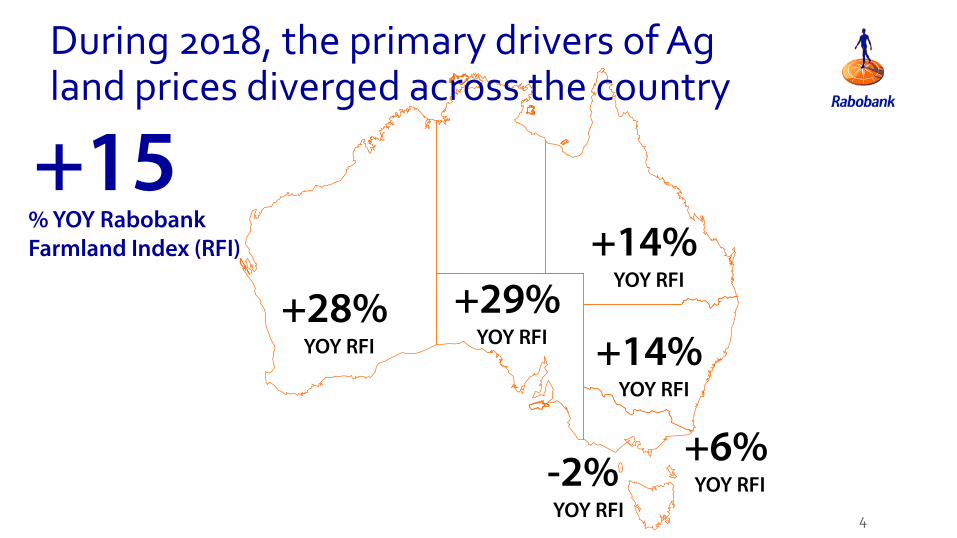

During 2018, the primary drivers of Ag land prices diverged across the country

4

+6%YOY RFI-2%

YOY RFI

+29%YOY RFI

+14%YOY RFI

+14%YOY RFI

+28%YOY RFI

+15% YOY Rabobank Farmland Index (RFI)

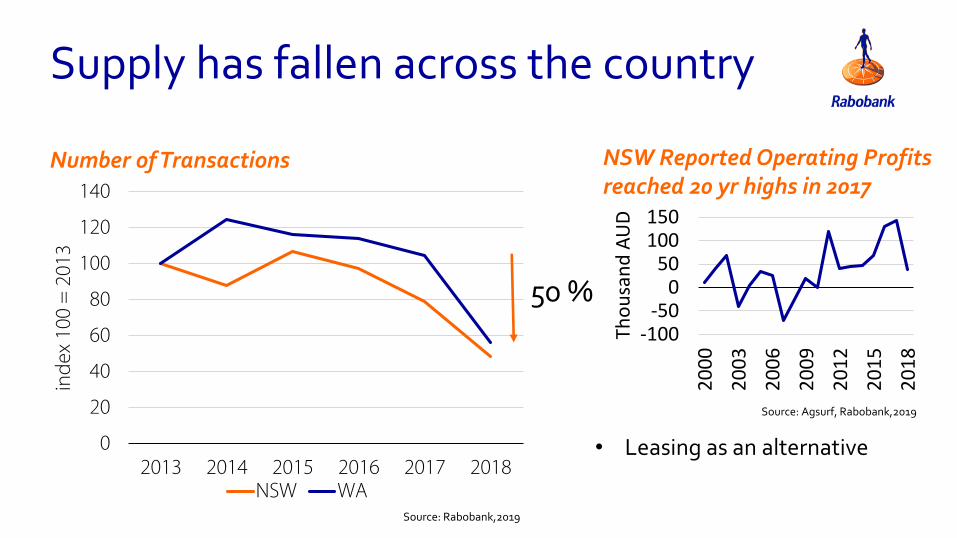

Supply has fallen across the country

Number of Transactions

0

20

40

60

80

100

120

140

2013 2014 2015 2016 2017 2018

ind

ex 1

00 =

201

3

NSW WA

50 %-100

-500

50100150

20

00

20

03

20

06

20

09

20

12

20

15

20

18

Tho

usa

nd

AU

D

NSW Reported Operating Profits reached 20 yr highs in 2017

• Leasing as an alternative

Source: Rabobank,2019

Source: Agsurf, Rabobank,2019

0%

5%

10%

15%

Q1

20

16

Q2

20

16

Q3

20

16

Q4

20

16

Q1

20

17

Q2

20

17

Q3

20

17

Q4

20

17

Q1

20

18

Q2

20

18

Q3

20

18

Q4

20

18

% o

f fa

rmer

s

NSW WA

Demand has diverged

% of farmers with 12 month purchasing intentions

Source: Rabobank,2019

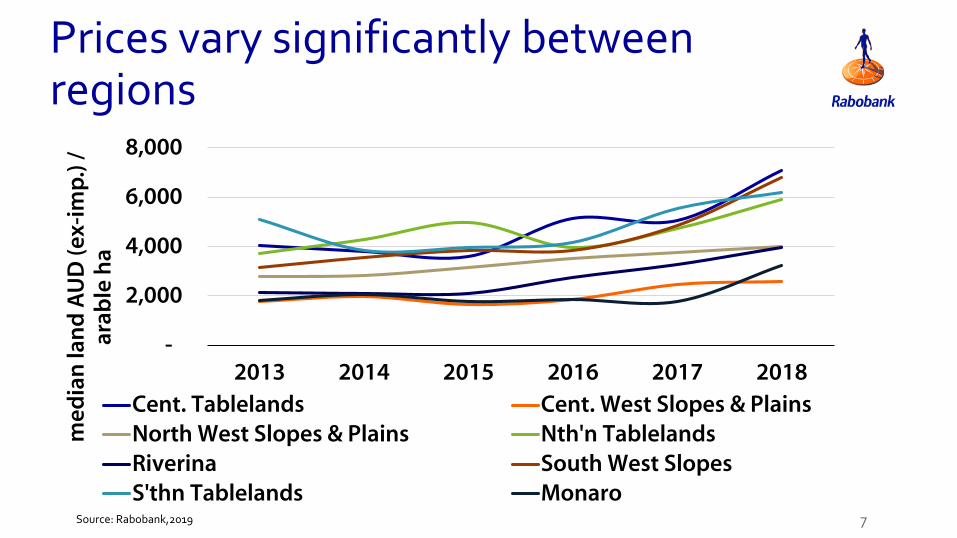

Prices vary significantly between regions

7

-

2,000

4,000

6,000

8,000

2013 2014 2015 2016 2017 2018

med

ian

lan

d A

UD

(ex-

imp

.) /

ar

able

ha

Cent. Tablelands Cent. West Slopes & PlainsNorth West Slopes & Plains Nth'n TablelandsRiverina South West SlopesS'thn Tablelands Monaro

Source: Rabobank,2019

Capital appreciation of ag land has performed well against other assets

8

Capital return of selected asset classes, 2013-2018

0

40

80

120

160

Jan-14 Jan-15 Jan-16 Jan-17 Jan-18

Ind

ex 1

00 =

1 J

an 2

014

AU govt. bond yield ASX all ordinariesS&P 500 Index S&P/ASX 200 A-ReitAU residential house prices AU ag land median prices

Source: Bloomberg, Rabobank,2019

Investment five-year CAGR

S&P/ASX 200 A-Reit 7.3%

AU ag land median prices

7.0%

S&P 500 Index 6.3%

Australian residential house prices

4.2%

ASX all ordinaries 1.3%

AU govt. bond yield -11.5%

Our Agenda for Today

9

Section 1 The key driver of land prices has shifted

Section 2 Macro forces look more challenging ahead

Section 3 Land price growth will slow

Land prices have local and global drivers

10

• Growth strategies of local farmers

• Corporate Interest

• Operating Profits

• Prices

• Production

• Alternative production possibilities

• Access to infrastructure

• Access to regional centres

• Regional confidence

State Influences

• Proximity to international markets

• Climate (current and future)

• State regulation

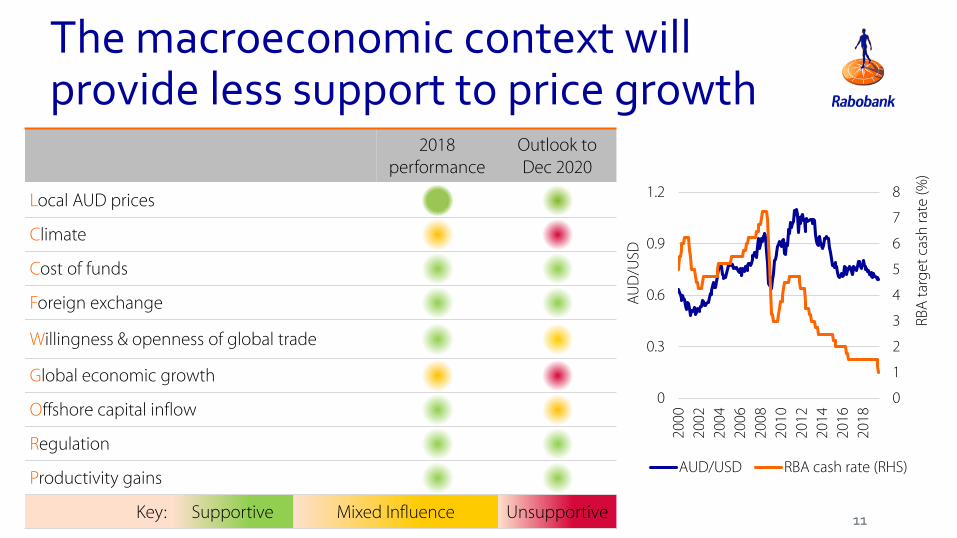

The macroeconomic context will provide less support to price growth

11

2018 performance

Outlook to Dec 2020

Local AUD prices

Climate

Cost of funds

Foreign exchange

Willingness & openness of global trade

Global economic growth

Offshore capital inflow

Regulation

Productivity gains

Key: Supportive Mixed Influence Unsupportive

0

1

2

3

4

5

6

7

8

0

0.3

0.6

0.9

1.2

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

RBA

tar

get

cas

h ra

te (%

)

AU

D/U

SD

AUD/USD RBA cash rate (RHS)

Our Agenda for Today

12

Section 1 The key driver of land prices has shifted

Section 2 Macro forces look more challenging ahead

Section 3 Land price growth will slow

More smoke, less fire ahead

13

West and SouthDrought affected regions

Number of properties on the

market

Demand

18 month price Direction

Number of properties on the

market

Demand

18 month price Direction

Market variation will continue to create purchasing opportunities

14

Within regions…. And between regions..

0

0.5

1

1.5

2

2.5

3

3.5

4

0 2000 4000 6000 8000 10000

Tota

l Lan

d A

UD

(mill

ion

s)

Total carrying capacity (DSE)

0

1

2

3

4

5

6

7

8

0 4000 8000 12000

Tota

l Lan

d A

UD

(mill

ion

s)Total carrying capacity (DSE)

Monaro Southern TablelandsSource: Rabobank,2019

Source: Rabobank,2019

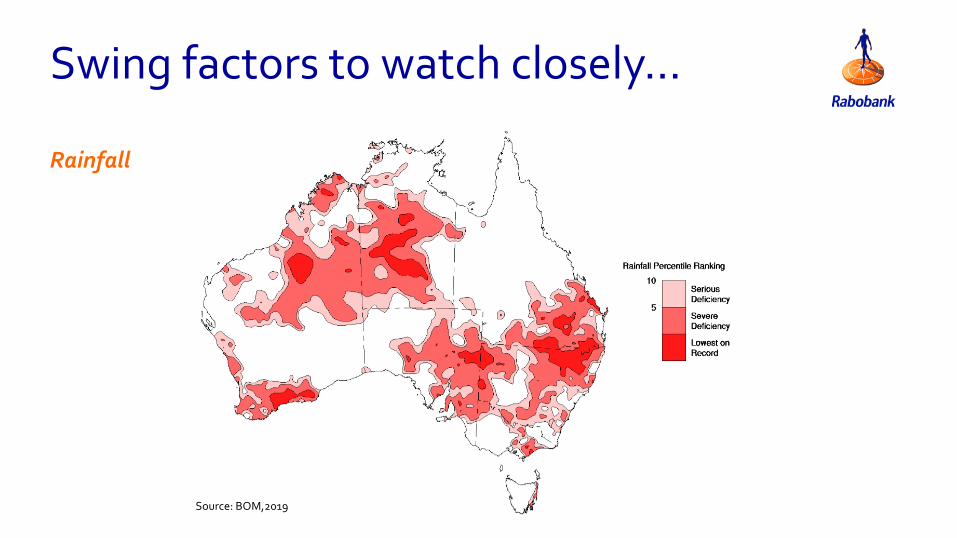

Swing factors to watch closely…

15

Geopolitics

Swing factors to watch closely…

Rainfall

Source: BOM,2019

The bottom line…

17

• Ag land prices have been on fire over the last five years, with growth accelerating during 2017 and 2018.

• During 2018, the primary drivers of Ag land prices diverged across the country

• We expect the macro forces to provide less support to land price growth

• Regardless of a wet or dry scenario, we expect land price growth will plateau in drought affected regions in the 18 months ahead.

1818

This document is meant exclusively for you and does not carry any right of publication or disclosure other than to Coöperatieve Rabobank U.A. (“Rabobank”), registered in Amsterdam. Neither this document nor any of its contents may be distributed, reproduced, or used for any other purpose without the prior written consent of Rabobank. The information in this document reflects prevailing market conditions and our judgement as of this date, all of which may be subject to change. This document is based on public information. The information and opinions contained in this document have been compiled or derived from sources believed to be reliable; however, Rabobank does not guarantee the correctness or completeness of this document, and does not accept any liability in this respect. The information and opinions contained in this document are indicative and for discussion purposes only. No rights may be derived from any potential offers, transactions, commercial ideas, et cetera contained in this document. This document does not constitute an offer, invitation, or recommendation. This document shall not form the basis of, or cannot be relied upon in connection with, any contract or commitment whatsoever. The information in this document is not intended, and may not be understood, as an advice (including, without limitation, an advice within the meaning of article 1:1 and article 4:23 of the Dutch Financial Supervision Act). This document is governed by Dutch law. The competent court in Amsterdam, the Netherlands has exclusive jurisdiction to settle any dispute which may arise out of, or in connection with, this document and/or any discussions or negotiations based on it. This report has been published in line with Rabobank’s long-term commitment to international food and agribusiness. It is one of a series of publications undertaken by the global department of RaboResearch Food & Agribusiness. ©2017 - All Rights Reserved.

18

For further insight

Wes LefroyAgricultural AnalystRaboResearch Food & AgriAustralia and New [email protected]

See our websitewww.research.rabobank.com/far

Subscribe to our podcast channel(search RaboResearch on Apple podcast app)