what are you waiting for? enroll now. - smcps.org · what are you waiting for? enroll now. start...

TRANSCRIPT

WHAT ARE YOU WAITING FOR?

ENROLL NOW.

START SAVING TODAY!

St. Mary's County Public Schools Retirement SavingsPlan

WHAT ARE YOU WAITING FOR?

Welcome to the St. Mary's County Public Schools Retirement SavingsPlan! Participation in the Plan provides you with a great way to eitherstart or continue saving for retirement. The sooner you can getstarted, the better. Enrolling in your employer-sponsored retirementsavings Plan is simple, and can put you on the path to a comfortableretirement today.

It's important to begin saving as soon as possible so your money has more time to benefit fromcompounding. When you invest money and it has the potential to grow, you have the ability to keep earningmore and more. Compounding takes time to generate substantial returns, so the longer your savings areinvested, the more they can potentially grow.

No matter how long you have until retirement, you don't want to miss out on valuable compounding. Tolearn more about all your Plan has to offer and to start taking advantage of it, keep reading.

WE

LCO

ME

WE

LCO

ME

1

SO LET'S GET STARTED! ENROLL IN THE ST. MARY'S COUNTY PUBLICSCHOOLS RETIREMENT SAVINGS PLAN TODAY.

� IT'S EASY. Your contributions are automatically deducted from your paycheck - no checks towrite or deposits to worry about. The traditional 403(b) contributions are deducted on a pre-taxbasis, ROTH is after tax. You don't have to pay taxes on your traditional 403(b) account until youtake money out of your plan, so your savings can potentially benefit from years of tax-freecompounding.*

� IT'S SMART. The money you put into your traditional 403(b) plan reduces your current taxableincome dollar for dollar. As a result, you'll pay less in taxes each pay period.

� IT'S FLEXIBLE. No matter what type of investor you are or where you are in your career, you canchoose from a wide variety of funding options to suit your needs. Once you've chosen them,remember to monitor your investments periodically to make sure they're earning enough to sustainyou throughout retirement.

BEGIN SAVING RIGHT AWAY!

All you need to do is contact your MetLife Resources Financial Services Representative!

YOUR METLIFE RESOURCES FINANCIAL SERVICES REPRESENTATIVE:Ellen [email protected]

6700 Alexander Bell Dr. Suite 115Columbia, MD 21046(ofc)800-446-1615

*Funding your retirement program with a fixed annuity offers no additional tax benefit. There should be rea-sons other than tax deferral for investing in a fixed annuity.

AC

HIE

VIN

G Y

OU

R G

OA

LS

2

SAVE FOR TOMORROW — TODAYTHE POWER OF TAX DEFERRALSince your contributions to the Plan are made with pre-tax dollars, they reduce your taxable income eachyear.

Your employer also offers a Roth option. You contribute to a Roth account with after-tax dollars. Earnings onthe contributions will not be subject to federal income tax if they remain in the Plan for at least five yearsafter your first contribution, and you do not take withdrawals before attaining age 59½, death or disability.Anyone who expects to be in a higher tax bracket in retirement may want to consider contributing to a Rothaccount.

Of course, no one can predict the future, so if you're unsure how your income may change throughout yourcareer, or after you retire, you don't have to choose one or the other. Consider splitting your contributionsbetween a Traditional and a Roth account. Your representative can help you determine the best choices foryour unique circumstances. You should speak with your tax advisor to decide what's best for your particularsituation.

Unlike other types of investments where earnings may be taxed each year, your Plan earningsgrow tax deferred. That means 100% of your earnings are reinvested, and you pay no taxesuntil you take a distribution.

The income tax rate used in this chart is a hypothetical tax rate as it might apply to one's marginal taxable income after taking

into consideration all taxable income in a given year. Your actual income taxes in a given year may be higher or lower and can

vary from year to year depending on your income level, sources and types of income, tax deductions, tax credits, state income

taxes, applicability of alternative minimum tax (AMT), and other factors that can affect your tax rate. Tax laws are subject to

change. Currently reduced income tax rates apply to long-term capital gains and qualified dividend income (maximum of 15%).

The illustration assumes a federal income tax bracket of 15% for currently taxable account withdrawals made annually to pay

taxes on any earnings. Please check with your tax advisor for details specific to your situation. Distributions from the program

will be subject to ordinary income tax in the year made and are not eligible for the lower maximum tax rate that applies to

long-term capital gains and eligible dividends. Additionally, a 10% federal penalty tax (subject to certain exceptions) will gener-

ally apply to withdrawals prior to age 59½. This example assumes an 8% growth rate. Figures are for illustrative purposes only

and do not indicate the future performance of any MetLife product or returns.

AC

HIE

VIN

G Y

OU

R G

OA

LS

3

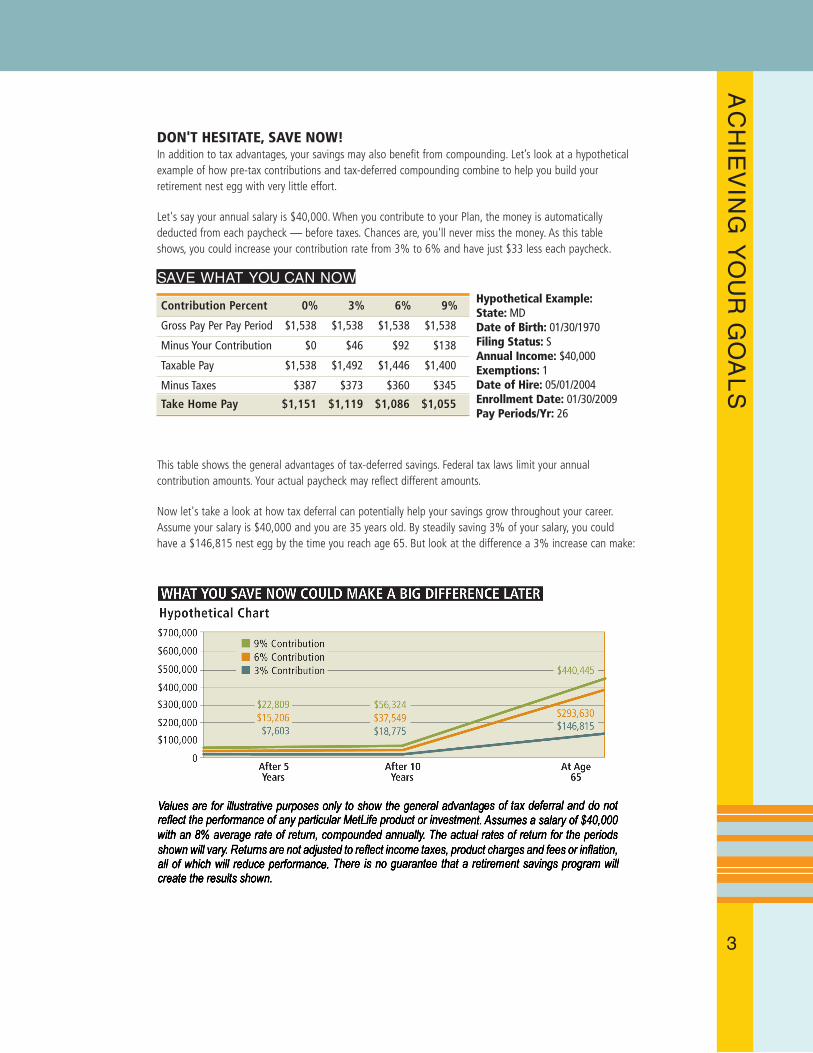

DON'T HESITATE, SAVE NOW!In addition to tax advantages, your savings may also benefit from compounding. Let’s look at a hypotheticalexample of how pre-tax contributions and tax-deferred compounding combine to help you build yourretirement nest egg with very little effort.

Let's say your annual salary is $40,000. When you contribute to your Plan, the money is automaticallydeducted from each paycheck — before taxes. Chances are, you'll never miss the money. As this tableshows, you could increase your contribution rate from 3% to 6% and have just $33 less each paycheck.

SAVE WHAT YOU CAN NOW

Contribution Percent 0% 3% 6% 9%

Gross Pay Per Pay Period $1,538 $1,538 $1,538 $1,538

Minus Your Contribution $0 $46 $92 $138

Taxable Pay $1,538 $1,492 $1,446 $1,400

Minus Taxes $387 $373 $360 $345

Take Home Pay $1,151 $1,119 $1,086 $1,055

Hypothetical Example:State: MD Date of Birth: 01/30/1970 Filing Status: S Annual Income: $40,000 Exemptions: 1 Date of Hire: 05/01/2004 Enrollment Date: 01/30/2009 Pay Periods/Yr: 26

This table shows the general advantages of tax-deferred savings. Federal tax laws limit your annualcontribution amounts. Your actual paycheck may reflect different amounts.

Now let's take a look at how tax deferral can potentially help your savings grow throughout your career.Assume your salary is $40,000 and you are 35 years old. By steadily saving 3% of your salary, you couldhave a $146,815 nest egg by the time you reach age 65. But look at the difference a 3% increase can make:

PL

AN

HIG

HL

IGH

TS

4

FEATURES OF YOUR PLANELIGIBILITYYou are eligible to participate in your Plan effective immediately.

YOUR CONTRIBUTIONSThe Internal Revenue Code limits the amount you can contribute in pre-tax dollars each calendar year. Thecurrent federal general limit is $16,500. If you participate in the Roth program, then the general limit andthe catch-up limits apply to all salary reduction contributions, whether allocated to pre-tax amounts or after-tax Roth amounts.

SPRINT FOR THE FINISHIf you've begun saving a little late, you can still boost your savings as you approach retirement. And if you'vebeen saving diligently, you may still want to take advantage of this opportunity to boost your savings evenmore.

If you are age 50 or older in 2010, you can contribute an additional "catch-up" contribution of $5,500.After 2010, the general and the catch-up contribution limits will be subject to cost of living increases.

Additional catch-up contributions may be available if you have participated in the Plan for at least 15 years.There is an overall limit on aggregate contributions (including employer and employee contributions) thatcan be made to your Plan.

If you have questions about these limits, please contact your employer.

ROLLOVERSIf you have an existing qualified retirement plan account with a prior employer or a rollover IRA, you mayroll over all or some of that account into this Plan once you enroll. You may want to consider this if your oldplan or IRA's costs, feature or investment options are not satisfactory to you. Your money can continue toaccumulate on a tax-deferred basis in one place, which may make your retirement savings easier to manage.

CHOOSING FUND OPTIONS You may choose from a range of funding options across a variety of asset classes. For a list of the mutualfunds available to you, please see the Funding Options section of this guide.

COST OF PARTICIPATIONExpressed on an annual basis, MetLife's fee is 45 basis points (or 0.45%) of Plan assets in the Funds andany other Funds with respect to which it provides Services under the Agreement plus a $12.00 annual planadministrative participant fee, payable in quarterly installments at a rate of 11.25 basis points of such Planassets plus $3.00 per plan administrative participant fee at each quarter's-close. Mutual fund companiesassess certain annual fees and expenses. For more information regarding fees and expenses, please readeach mutual fund prospectus carefully. MetLife and/or its affiliates receive fees from the fund families ortheir affiliates in connection with certain administrative, distribution and recordkeeping services.

ACCOUNT ACCESSEach quarter, you will receive a personal account statement with a detailed summary of all activity. Pleaserefer to the inside back cover of this guide for telephone and web access information.

PL

AN

HIG

HL

IGH

TS

5

LOANS Loans are permitted. The amount you may borrow is limited by rules under the Internal Revenue Code. Allloans will be based on your account balance. Please note, these loan limits apply on a combined basis to allretirement accounts with the same employer. If you have any questions, please contact your employer.

WITHDRAWALSSince your Plan is designed primarily to help you save for retirement, the IRS has placed restrictions on whenmoney may be withdrawn from your account before you retire. You may withdraw money from your accountunder the following circumstances:

Normal Retirement Age1 Termination of EmploymentDisability2 DeathHardship2

Always consult your tax advisor or investment professional about the income tax consequences of anywithdrawals. Ordinary federal income taxes generally apply. State income taxes may also apply. Federalincome tax rules generally prohibit withdrawals prior to age 59½. If permitted, such withdrawals may alsobe subject to an additional tax of 10% of the amount withdrawn.

1 As defined by your Plan2 Subject to IRS rules

ENROLL Your MetLife Resources Financial Services Representative is available on-site to help you with the enrollmentprocess.

See Explanations and Footnotes in the back of the book.

FU

ND

ING

OP

TIO

NS

6

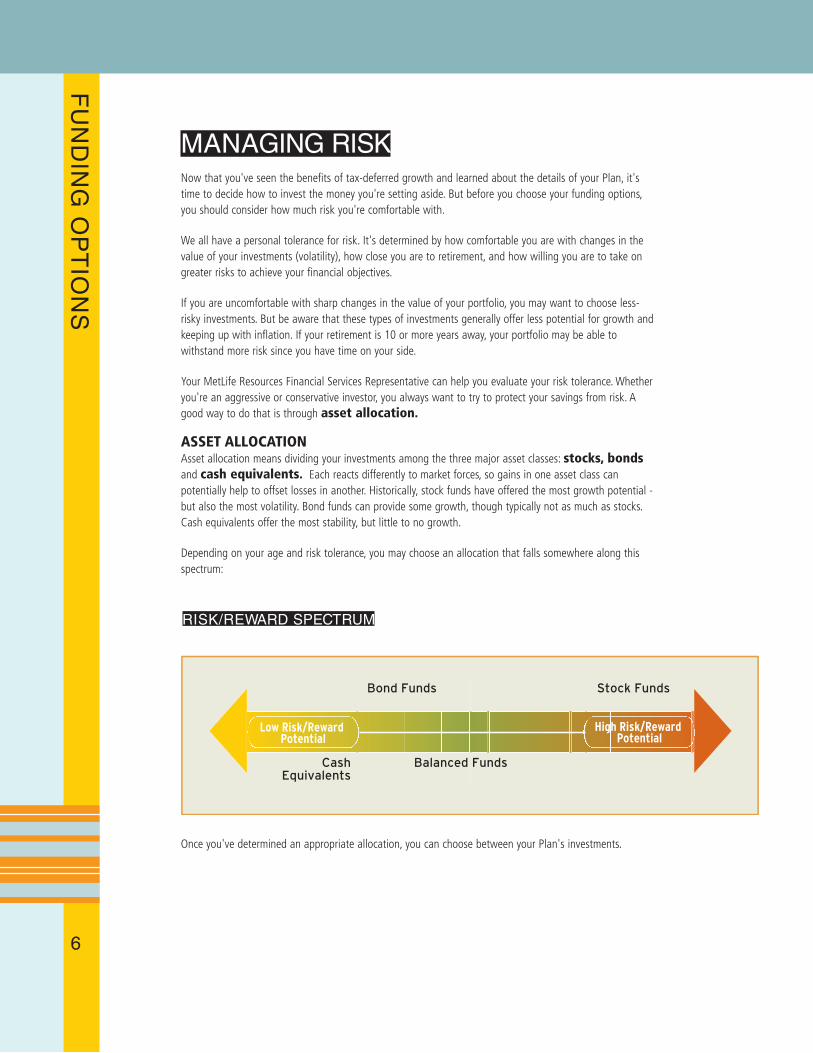

MANAGING RISKNow that you've seen the benefits of tax-deferred growth and learned about the details of your Plan, it'stime to decide how to invest the money you're setting aside. But before you choose your funding options,you should consider how much risk you're comfortable with.

We all have a personal tolerance for risk. It's determined by how comfortable you are with changes in thevalue of your investments (volatility), how close you are to retirement, and how willing you are to take ongreater risks to achieve your financial objectives.

If you are uncomfortable with sharp changes in the value of your portfolio, you may want to choose less-risky investments. But be aware that these types of investments generally offer less potential for growth andkeeping up with inflation. If your retirement is 10 or more years away, your portfolio may be able towithstand more risk since you have time on your side.

Your MetLife Resources Financial Services Representative can help you evaluate your risk tolerance. Whetheryou're an aggressive or conservative investor, you always want to try to protect your savings from risk. Agood way to do that is through asset allocation.

ASSET ALLOCATIONAsset allocation means dividing your investments among the three major asset classes: stocks, bondsand cash equivalents. Each reacts differently to market forces, so gains in one asset class canpotentially help to offset losses in another. Historically, stock funds have offered the most growth potential -but also the most volatility. Bond funds can provide some growth, though typically not as much as stocks.Cash equivalents offer the most stability, but little to no growth.

Depending on your age and risk tolerance, you may choose an allocation that falls somewhere along thisspectrum:

RISK/REWARD SPECTRUM

Once you've determined an appropriate allocation, you can choose between your Plan's investments.

FU

ND

ING

OP

TIO

NS

7

TWO WAYS TO INVEST� PICK A DATE — Designed for people who want a simple and effective option that leaves most

ongoing investment decisions to investment professionals.

� MIX AND MONITOR — Designed for people who want to take a more hands-on approach andselect their own mix of funds.

1. PICK A DATEIf you're uncomfortable choosing funds on your own or don't have the time to manage your account, youmay want to consider investing in a target date fund. A target date fund is managed so that its assetallocation is adjusted over time. Typically, the farther the "target date" is from the present, the moreweighted the fund is toward equities (stocks). If you like the simplicity of this approach, choose the targetdate fund that most closely matches your expected retirement date. Then sit back and let the fund'smanagers adjust the fund's asset allocation as your target retirement date approaches.

Your Plan offers the following target date funds. Each one is a diversified mutual fund managed by anexperienced portfolio management team.

American Funds Target Date 2010 (R3)American Funds Target Date 2015 (R3)American Funds Target Date 2020 (R3)American Funds Target Date 2025 (R3)American Funds Target Date 2030 (R3)American Funds Target Date 2035 (R3)American Funds Target Date 2040 (R3)American Funds Target Date 2045 (R3)American Funds Target Date 2050 (R3)

2. MIX AND MONITORYour retirement savings Plan offers a variety of funding options which are listed on the following pages. Youcan create your own investment mix by choosing any combination; you then need to monitor yourinvestments and make adjustments as your goals change over time.

FU

ND

ING

OP

TIO

NS

8

HOW TO INVESTFUNDING OPTIONS [TICKER SYMBOL] ASSET CLASS

FIXED ANNUITY (SVA) CASH/CASH EQUIVALENT (CASH/CASH EQUIVALENT)

The Fixed Annuity (SVA) is a deferred fixed annuity that provides security while earning current income at a rate

guaranteed by the financial strength and claims-paying ability of MetLife Insurance Company of Connecticut.

CALVERT SHORT DURATION INCOME A [CSDAX]1 SHORT-TERM BOND (BONDS)

The Fund seeks to provide competitive total return and maximum yield, to the extent consistent with prudent investment

management and preservation of capital, through investment primarily in short term bonds along with other income

producing securities.

JPMORGAN SHORT DURATION BOND SELECT [HLLVX]6 SHORT-TERM BOND (BONDS)

The Fund seeks current income consistent with preservation of capital through investment in high and medium grade fixed

income securities.

CALVERT SOC INVESTMENT BOND (A) [CSIBX]1 INTERMEDIATE-TERM BOND (BONDS)

The Fund seeks income consistent with preservation of capital. The fund normally invests at least 80% of assets in fixed-

income securities of any quality, with at least 65% of assets in investment grade debt securities rated A or above.

PIMCO TOTAL RETURN (A) [PTTAX]1, 3 INTERMEDIATE-TERM BOND (BONDS)

The Fund seeks maximum total return, consistent with preservation of capital and prudent investment management. The

Fund seeks to achieve its investment objective by investing in a diversified portfolio of fixed income instruments. The

average portfolio duration normally varies within a three- to six-year time frame.

AMERICAN FUNDS TARGET DATE 2010 (R3) [RCATX] TARGET DATE 2000-2010 (STOCKS & BONDS)

The Fund seeks to provide for investors that plan to retire in 2010. Depending on its proximity to its target date, the Fund

will seek to achieve the following: growth, income and conservation of capital. Each Fund will attempt to achieve its

investment objectives by investing in a mix of American Funds.

AMERICAN FUNDS TARGET DATE 2015 (R3) [RCJTX] TARGET DATE 2011-2015 (STOCKS & BONDS)

The Fund seeks to provide for investors that plan to retire in 2015. Depending on its proximity to its target date, the Fund

will seek to achieve the following: growth, income and conservation of capital. Each Fund will attempt to achieve its

investment objectives by investing in a mix of American Funds.

AMERICAN FUNDS TARGET DATE 2020 (R3) [RCCTX] TARGET DATE 2016-2020 (STOCKS & BONDS)

The Fund seeks to provide for investors that plan to retire in 2020. Depending on its proximity to its target date, the Fund

will seek to achieve the following: growth, income and conservation of capital. Each Fund will attempt to achieve its

investment objectives by investing in a mix of American Funds.

AMERICAN FUNDS TARGET DATE 2025 (R3) [RCDTX] TARGET DATE 2021-2025 (STOCKS & BONDS)

The Fund seeks to provide for investors that plan to retire in 2025. Depending on its proximity to its target date, the Fund

will seek to achieve the following: growth, income and conservation of capital. Each Fund will attempt to achieve its

investment objectives by investing in a mix of American Funds.

AMERICAN FUNDS TARGET DATE 2030 (R3) [RCETX] TARGET DATE 2026-2030 (STOCKS & BONDS)

The Fund seeks to provide for investors that plan to retire in 2030. Depending on its proximity to its target date, the Fund

will seek to achieve the following: growth, income and conservation of capital. Each Fund will attempt to achieve its

FU

ND

ING

OP

TIO

NS

9

investment objectives by investing in a mix of American Funds.

AMERICAN FUNDS TARGET DATE 2035 (R3) [RCFTX] TARGET DATE 2031-2035 (STOCKS & BONDS)

The Fund seeks to provide for investors that plan to retire in 2035. Depending on its proximity to its target date, the Fund

will seek to achieve the following: growth, income and conservation of capital. Each Fund will attempt to achieve its

investment objectives by investing in a mix of American Funds.

NEUBERGER BERMAN SOCIALLY RESPONSIVE (TR) [NBSTX] LARGE BLEND (STOCKS)

The Fund seeks long-term growth of capital by investing primarily in securities of companies that meet the fund's financial

criteria and social policy.

OAKMARK EQUITY & INCOME FUND II [OARBX]1 LARGE BLEND (STOCKS)

The Fund seeks high current income, preservation and growth of capital by investing in a diversified portfolio of equity

and fixed-income securities.

VANGUARD 500 INDEX FUND (INV) [VFINX]4 LARGE BLEND (STOCKS)

The Fund seeks to track the performance of a benchmark index that measures the investment return of large-

capitalization stocks. The Fund employs a "passive management" approach designed to track the performance of the

Standard & Poor's 500 Index.

AMERICAN FUNDS TARGET DATE 2040 (R3) [RCKTX] TARGET DATE 2036-2040 (STOCKS & BONDS)

The Fund seeks to provide for investors that plan to retire in 2040. Depending on its proximity to its target date, the Fund

will seek to achieve the following: growth, income and conservation of capital. Each Fund will attempt to achieve its

investment objectives by investing in a mix of American Funds.

EATON VANCE LARGE CAP VALUE (A) [EHSTX] LARGE VALUE (STOCKS)

The Fund seeks total return. The Fund invests primarily in value stocks of large-cap companies. Value stocks are common

stocks that, in the opinion of the investment adviser, are inexpensive or undervalued relative to the overall stock market.

The Fund primarily invests in dividend-paying stocks.

AMERICAN FUNDS TARGET DATE 2045 (R3) [RCHTX] TARGET DATE 2041-2045 (STOCKS & BONDS)

The Fund seeks to provide for investors that plan to retire in 2045. Depending on its proximity to its target date, the Fund

will seek to achieve the following: growth, income and conservation of capital. Each Fund will attempt to achieve its

investment objectives by investing in a mix of American Funds.

AMERICAN FUNDS TARGET DATE 2050 (R3) [RCITX] TARGET DATE 2050+ (STOCKS & BONDS)

The Fund seeks to provide for investors that plan to retire in 2050. Depending on its proximity to its target date, the Fund

will seek to achieve the following: growth, income and conservation of capital. Each Fund will attempt to achieve its

investment objectives by investing in a mix of American Funds.

AMER. FUNDS GROWTH FUND OF AMER. (R3) [RGACX]1, 5 LARGE GROWTH (STOCKS)

The Fund seeks to invest primarily in common stocks of companies that appear to offer superior opportunities for growth

of capital.

AMER. FUNDS CAPITAL WORLD GROWTH & INCOME (R3) [RWICX]1 WORLD STOCK (STOCKS)

The Fund seeks current income by investing primarily in stocks of well-established companies located around the world.

COLUMBIA MID CAP VALUE A [CMUAX]3 MID-CAP VALUE (STOCKS)

The Fund seeks long-term growth of capital with income as a secondary consideration. The Fund normally invests at least

80% of its assets in equity securities of U.S. companies with market capitalizations between $1 billion and $10 billion

FU

ND

ING

OP

TIO

NS

10

that are believed to have the potential for long-term growth of capital.

AMER. FUNDS EUROPACIFIC GROWTH FUND (R3) [RERCX]1 FOREIGN LARGE BLEND (STOCKS)

The Fund seeks to provide long-term growth of capital by investing in companies based outside the United States. The

Fund Invests in companies based chiefly in Europe and the Pacific Basin, ranging from small firms to large corporations.

COLUMBIA ACORN FUND (A) [LACAX]2, 3 MID-CAP GROWTH (STOCKS)

The Fund seeks to provide long-term growth of capital by investing primarily in the stocks of small- and medium-sized

companies with capitalizations of less than $2 billion.

VANGUARD MID CAP INDEX (INV) [VIMSX]3, 4 MID-CAP BLEND (STOCKS)

The Fund seeks to track the performance of a benchmark index that measures the investment return of mid-capitalization

stocks. The Fund employs a "passive management" approach designed to track the performance of the MSCI U.S. Mid

Cap 450 Index, a broadly diversified index of stocks of medium-size U.S. companies.

ALLIANZ NFJ SMALL CAP VALUE FUND (A) [PCVAX] SMALL VALUE (STOCKS)

The Fund seeks long-term growth of capital and income by investing primarily in common stocks from companies with

market capitalizations between $50 and $500 million that are characterized by having below-average P/E ratios relative

to their industry groups.

KEELEY SMALL CAP VALUE FUND [KSCVX]2 SMALL VALUE (STOCKS)

The Fund seeks capital appreciation by investing in companies with relatively small market capitalization, emphasizing

companies undergoing substantial changes such as: emerging from bankruptcy, spin-offs and recapitalizations.

OPPENHEIMER SMALL & MID CAP VALUE (A) [QVSCX]1, 2, 3 SMALL BLEND (STOCKS)

The Fund seeks capital appreciation. Under normal market conditions the Fund will invest at least 80% of its net assets,

plus the amount of any borrowings for investment purposes, in equity securities of small-cap and mid-cap issuers.

ROYCE VALUE PLUS FUND (SVC) [RYVPX]2 SMALL BLEND (STOCKS)

The Fund seeks long-term growth of capital by investing at least 80% of its assets in common stocks and convertible

securities of mid-, small- and micro-cap companies.

VANGUARD SMALL CAP INDEX (INV) [NAESX]2, 4 SMALL BLEND (STOCKS)

The Fund seeks to track the performance of a benchmark index that measures the investment return of small-

capitalization stocks. The Fund employs a "passive management" approach designed to track the performance of the

MSCI U.S. Small Cap 1750 Index, a broadly diversified index of stocks of smaller U.S. companies.

Morningstar Associates, LLC believes that the list shows the approximate risk relationships among the assetclasses for the funding options from the most conservative to the most aggressive. Within each asset classfunding options are listed in alphabetical order. The ranking of asset classes is based on an analysis byMorningstar Associates, LLC. In determining the ranking, Morningstar Associates, LLC utilized certainquantitative risk measures in conjunction with its fundamental investing experience and portfolioconstruction philosophy. The asset classes are supplied by Morningstar Associates, LLC and are used bypermission. Other methodologies for ranking asset classes may produce different results. Since pastperformance of investments is no guarantee of future performance, no assurance can be given that theranking of asset classes shown here will correspond to rankings in the future. Purchasers should understandthat each funding option incurs its own risks, which will be dependent upon the investment decisions madeby the respective portfolio manager. Please consult the appropriate prospectus for more completeinformation including costs, expenses, and risks for each investment choice.

Certain Mutual Fund information above is provided by Lipper. Copyright 2008 ®Reuters. All rights reserved.

FU

ND

ING

OP

TIO

NS

11

For additional information, please see the explanations and footnotes in the next section.

NOTES

FU

ND

ING

OP

TIO

NS

13

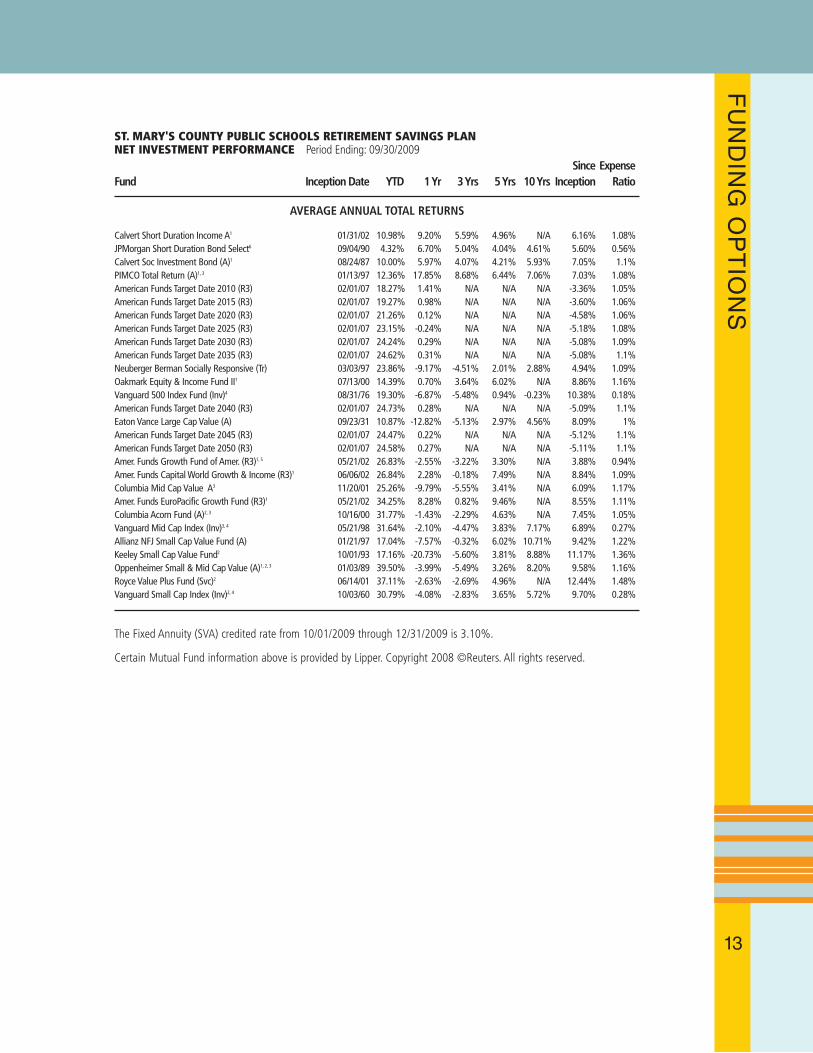

ST. MARY'S COUNTY PUBLIC SCHOOLS RETIREMENT SAVINGS PLANNET INVESTMENT PERFORMANCE Period Ending: 09/30/2009

Since ExpenseFund Inception Date YTD 1 Yr 3 Yrs 5 Yrs 10 Yrs Inception Ratio

AVERAGE ANNUAL TOTAL RETURNS

Calvert Short Duration Income A1 01/31/02 10.98% 9.20% 5.59% 4.96% N/A 6.16% 1.08%JPMorgan Short Duration Bond Select6 09/04/90 4.32% 6.70% 5.04% 4.04% 4.61% 5.60% 0.56%Calvert Soc Investment Bond (A)1 08/24/87 10.00% 5.97% 4.07% 4.21% 5.93% 7.05% 1.1%PIMCO Total Return (A)1, 3 01/13/97 12.36% 17.85% 8.68% 6.44% 7.06% 7.03% 1.08%American Funds Target Date 2010 (R3) 02/01/07 18.27% 1.41% N/A N/A N/A -3.36% 1.05%American Funds Target Date 2015 (R3) 02/01/07 19.27% 0.98% N/A N/A N/A -3.60% 1.06%American Funds Target Date 2020 (R3) 02/01/07 21.26% 0.12% N/A N/A N/A -4.58% 1.06%American Funds Target Date 2025 (R3) 02/01/07 23.15% -0.24% N/A N/A N/A -5.18% 1.08%American Funds Target Date 2030 (R3) 02/01/07 24.24% 0.29% N/A N/A N/A -5.08% 1.09%American Funds Target Date 2035 (R3) 02/01/07 24.62% 0.31% N/A N/A N/A -5.08% 1.1%Neuberger Berman Socially Responsive (Tr) 03/03/97 23.86% -9.17% -4.51% 2.01% 2.88% 4.94% 1.09%Oakmark Equity & Income Fund II1 07/13/00 14.39% 0.70% 3.64% 6.02% N/A 8.86% 1.16%Vanguard 500 Index Fund (Inv)4 08/31/76 19.30% -6.87% -5.48% 0.94% -0.23% 10.38% 0.18%American Funds Target Date 2040 (R3) 02/01/07 24.73% 0.28% N/A N/A N/A -5.09% 1.1%Eaton Vance Large Cap Value (A) 09/23/31 10.87% -12.82% -5.13% 2.97% 4.56% 8.09% 1%American Funds Target Date 2045 (R3) 02/01/07 24.47% 0.22% N/A N/A N/A -5.12% 1.1%American Funds Target Date 2050 (R3) 02/01/07 24.58% 0.27% N/A N/A N/A -5.11% 1.1%Amer. Funds Growth Fund of Amer. (R3)1, 5 05/21/02 26.83% -2.55% -3.22% 3.30% N/A 3.88% 0.94%Amer. Funds Capital World Growth & Income (R3)1 06/06/02 26.84% 2.28% -0.18% 7.49% N/A 8.84% 1.09%Columbia Mid Cap Value A3 11/20/01 25.26% -9.79% -5.55% 3.41% N/A 6.09% 1.17%Amer. Funds EuroPacific Growth Fund (R3)1 05/21/02 34.25% 8.28% 0.82% 9.46% N/A 8.55% 1.11%Columbia Acorn Fund (A)2, 3 10/16/00 31.77% -1.43% -2.29% 4.63% N/A 7.45% 1.05%Vanguard Mid Cap Index (Inv)3, 4 05/21/98 31.64% -2.10% -4.47% 3.83% 7.17% 6.89% 0.27%Allianz NFJ Small Cap Value Fund (A) 01/21/97 17.04% -7.57% -0.32% 6.02% 10.71% 9.42% 1.22%Keeley Small Cap Value Fund2 10/01/93 17.16% -20.73% -5.60% 3.81% 8.88% 11.17% 1.36%Oppenheimer Small & Mid Cap Value (A)1, 2, 3 01/03/89 39.50% -3.99% -5.49% 3.26% 8.20% 9.58% 1.16%Royce Value Plus Fund (Svc)2 06/14/01 37.11% -2.63% -2.69% 4.96% N/A 12.44% 1.48%Vanguard Small Cap Index (Inv)2, 4 10/03/60 30.79% -4.08% -2.83% 3.65% 5.72% 9.70% 0.28%

The Fixed Annuity (SVA) credited rate from 10/01/2009 through 12/31/2009 is 3.10%.

Certain Mutual Fund information above is provided by Lipper. Copyright 2008 ©Reuters. All rights reserved.

EX

PL

AN

AT

ION

S A

ND

FO

OT

NO

TE

S

14

IMPORTANT INFORMATIONPLAN HIGHLIGHTSThis is not intended to be a summary of your Plan's provisions; it only includes highlights of certain Planprovisions. The Plan document governs the terms of the Plan and is available from your employer. In general,if any conflicts occur between this material and the Plan documents provided by your employer, the Plandocuments provided by your employer will govern.

Pursuant to IRS Circular 230, MetLife is providing you with the following notification: Theinformation contained in this document is not intended to (and cannot) be used by anyone toavoid IRS penalties. This document supports the promotion and marketing of mutual fundsand annuities. You should seek advice based on your particular circumstances from anindependent tax advisor.

MetLife, its agents, and representatives may not give legal or tax advice. Any discussion of taxes herein orrelated to this document is for general information purposes only and does not purport to be complete orcover every situation. Tax law is subject to interpretation and legislative change. Tax results and theappropriateness of any product for any specific taxpayer may vary depending on the facts and circumstances.You should consult with and rely on your own independent legal and tax advisors regarding your particularset of facts and circumstances.

PERFORMANCECurrent performance may be lower or higher than the performance quoted in the previous pages. Eachmutual fund share class is indicated in parentheses next to the mutual fund name, if applicable. All mutualfunds offered in the Plan will be purchased at net asset value.

The Average Annual Total Returns assume a steady compounded rate of return. It is not the mutual fund'syear-by-year results, which actually varied over the periods shown. All distributions are assumed to bereinvested. The one, five and ten-year or since inception Average Annual Total Return figures shown aboveare required by the SEC to advertise performance for mutual funds. The three-year figure is calculated in thesame manner and is shown as additional information. These returns reflect performance of shares at netasset value, with no sales charges. Other fees and expenses do apply to a continued investment and aredescribed in the current prospectus. The Year to Date Return is calculated in the same manner as theAverage Annual Total Return and represents the return from the first of the year to the date of thisperformance sheet.

The figures shown reflect past performance, which is not a guarantee of future results. The investmentreturn and principal value of an investment will fluctuate and shares, when redeemed, may be worth moreor less than their original cost. There is no assurance a mutual fund will attain its investment objective.Amounts in the mutual funds are subject to risk of loss, and you will have a gain or loss when shares areredeemed.

MUTUAL FUNDSMutual fund companies assess certain annual fees and expenses. For more information regarding fees,please read each mutual fund prospectus carefully. MetLife and/or its affiliates receive fees from the mutualfund families or an affiliate for providing certain administrative, distribution and recordkeeping services. Aprospectus for each mutual fund must precede or accompany this performance report.

1 Foreign securities pose additional risks that are not associated with U.S. domestic issues, suchas changes in currency exchange rates and different governmental regulations, economicconditions, and accounting standards.

2 Investments in small capitalization and emerging growth companies involve greater thanaverage risk. Such securities may have limited marketability and the issuers may have limited

EX

PL

AN

AT

ION

S A

ND

FO

OT

NO

TE

S

15

product lines, markets and financial resources. The value of such investments may fluctuate morewidely than investments in larger, more established companies.

3 The common stocks of medium-sized companies may be more volatile than those of larger,more established companies.

4 Market indices referenced are unmanaged and representative of large and small domestic andinternational stocks and bonds, each with unique risks. Information about them is provided toillustrate market trends and does not represent the performance of any specific investment. Youcannot invest directly in an index.

5 Lower-rated high-yield, high-risk securities generally involve more credit risk. These securitiesmay also be subject to greater market price fluctuations than lower yielding higher rated debtsecurities.

6 Bond and other fixed-income securities involve both credit risk and market risk, which includesinterest rate risk. Credit risk is the risk that the security's issuer will not pay the interest,dividends or principal that it has promised to pay. Market risk is the risk that the value of thesecurity will fall because of changes in market rates of interest or other factors. Interest rate riskreflects the fact that the values of fixed-income securities tend to fall as interest rates rise. Wheninterest rates go down, interest earned on fixed-income securities will tend to decline.

ANNUITIESThe Fixed Annuity (SVA) is a fixed deferred annuity issued by MetLife Insurance Company of Connecticut(MLICC), 1300 Hall Boulevard, Bloomfield, CT 06002-2910 under policy L-22419.MetLife InvestorsDistribution Company (MLIDC) (member FINRA), 5 Park Plaza, Suite 1900, Irvine, CA 92614 is thedistributor of the annuity. MLICC and MLIC are MetLife companies.

Like most insurance policies and annuity contracts, MetLife's policies and contracts contain exclusions,holding periods, termination provisions, limitations, reduction of benefits, surrender charges and terms forkeeping them in force. Please see your representative for complete costs and details.

PR

IVA

CY

NO

TIC

E

16

Our Privacy Notice We know that you buy our products and services because you trust us. This notice explains how we protect your privacy and treat your personal information. It applies to current and former customers. “Personal information” here means anything we know about you personally.

Protecting Your Information

We take important steps to protect your personal information. We treat it as confidential. We tell our employees to take care in handling it. We limit access to those who need it to perform their jobs. Our outside service providers must also protect it, and use it only to meet our business needs. We also take steps to protect our systems from unauthorized access. We comply with all laws that apply to us.

Collecting Your Information

We typically collect your name, address, age, and other relevant information. For example, we may ask about your:

● finances ● creditworthiness ● employment ● health

● We may also collect information about any business you have with us, our affiliates, or other companies. Our affiliates include life, car, and home insurers. They also include a bank, a legal plans company, and securities broker-dealers. In the future, we may also have affiliates in other businesses.

How We Get Your Information

We get your personal information mostly from you. We may also use outside sources to help ensure our records are correct and complete. These sources may include consumer reporting agencies, employers, other financial institutions, adult relatives, and others. These sources may give us reports or share what they know with others. We don’t control the accuracy of information outside sources give us. If you want to make any changes to information we receive from others about you, you must contact those sources.

Using Your Information

We collect your personal information to help us decide if you’re eligible for our products or services. We may also need it to verify identities to help deter fraud, money laundering, or other crimes. How we use this information depends on what products and services you have or want from us. It also depends on what laws apply to those products and services. For example, we may also use your information to:

● administer your products and services ● process claims and other transactions ● perform business research ● confirm or correct your information ● market new products to you ● help us run our business ● comply with applicable laws

PR

IVA

CY

NO

TIC

E

17

We may share your personal information with others with your consent, by agreement, or as permitted or required by law. For example, we may share your information with businesses hired to carry out services for us. We may also share it with our affiliated or unaffiliated business partners through joint marketing agreements. In those situations, we may share your information to jointly offer you products and services or have others offer you products and services we endorse or sponsor. Before sharing your information with any affiliate or joint marketing partner for their own marketing purposes, however, we will first notify you and give you an opportunity to opt out.

Other reasons we may share your information include:

● doing what a court, law enforcement, or government agency requires us to do (for example, complying with search warrants or subpoenas)

● telling another company what we know about you if we are selling or merging any part of our business

● giving information to a governmental agency so it can decide if you are eligible for public benefits

● giving your information to someone with a legal interest in your assets (for example, creditor with a lien on your account)

● giving your information to your health care provider ● those listed in our “Using Your Information” section above

HIPAA

We will not share your health information with any other company – even one of our affiliates – for their own marketing purposes. If you have dental, long term care, or medical insurance from us, the Health Insurance Portability and Accountability Act (“HIPAA”) may further limit how we may use and share your information.

Accessing and Correcting Your Information

You may ask us for a copy of the personal information we have about you. Generally, we will provide it as long as it is reasonably retrievable and within our control. You must make your request in writing listing the account or policy numbers with the information you want to access. For legal reasons, we may not show you anything we learned as part of a claim or lawsuit, unless required by law.

If you tell us that what we know about you is incorrect, we will review it. If we agree, we will update our records. Otherwise, you may dispute our findings in writing, and we will include your statement whenever we give your disputed information to anyone outside MetLife.

Questions

We want you to understand how we protect your privacy. If you have any questions about this notice, please contact us. When you write, include your name, address, and policy or account number.

Send privacy questions to:

MetLife Privacy Office [email protected] P. O. Box 489 Warwick, RI 02887-9954

We may revise this privacy notice. If we make any material changes, we will notify you as required by law. We provide this privacy notice to you on behalf of these MetLife companies:

Metropolitan Life Insurance Company MetLife Securities, Inc. MetLife Investors Insurance Company MetLife Insurance Company of Connecticut MetLife Investors USA Insurance Company MetLife Associates, LLC

Sharing Your Information With Others

MO

RE

FR

OM

ME

TL

IFE

18

MORE THAN JUST RETIREMENT SAVINGSMetLife is renowned for products like life insurance that can help to protect your family. We're also one of the nation'sleading providers of employee benefits. But you may not be aware we also offer a wide array of other products andservices that can help you and your family achieve your financial goals. They include:

• Life Insurance• Disability Income Insurance• Auto & Home Insurance*• Annuities• Mutual Funds• IRAs• College Funding Strategies• Banking Products & Services**• Estate Conservation/Analysis• Financial Planning***

Contact your MetLife Resources Financial Services Representative for more information about any of these topics.

*Offered by Metropolitan Property and Casualty Insurance Company (MPCIC) and its Affiliates, Warwick, RI.

**Banking products and services, including deposit accounts, available ONLY from MetLife Bank®, NA, Member FDIC, aMetLife affiliated company. Up to $100,000 FDIC insurance per depositor. Insurance and other investment productsoffered are: NOT FDIC INSURED - NOT BANK PRODUCTS - MAY LOSE VALUE.

***Fee-based Financial Planning services offered only by qualified Financial Planners of MetLife Securities, Inc., (MSI) aBroker/Dealer (member FINRA, SIPC), and a Registered Investment Adviser, 200 Park Avenue, New York, NY 10166.

Insurance and Annuities issued by Metropolitan Life Insurance Company (MLIC), New York, NY 10166 anddistributed by MetLife Investors Distribution Company (MIDC) (member FINRA), Irvine, CA 92614. Securities,including variable products, offered through MetLife Securities, Inc., (MSI), (member FINRA, SIPC), 200 ParkAvenue, New York, NY 10166. MLIC, MPCIC, MetLife Bank, MIDC and MSI are MetLife companies.

KEEPING IN TOUCH WITHYOUR RETIREMENT ACCOUNTTo help monitor and manage your account, you can obtain information and make transactions virtually 24hours a day, 7 days a week. You may access your account in two ways:

� Log onto www.mlr.metlife.com

� Call 1-800-543-2520

Through either the Web site or the toll-free telephone number,you can obtain:

• Account balance• Contribution amount (deferral amount)• Contribution history• Current allocations• Transfer history• Monthly mutual fund performance reports• Fund fact sheets

You can also:

• Use the financial calculators• Change contribution amount (deferral amount)• Redirect future contributions• Rebalance investments• Change Personal Identification Number (PIN)

In addition, you can speak to a Client Service Representative, Monday through Friday from 9:00 a.m. to 8:00p.m. (Eastern Time).

ACCOUNT ACCESS VIRTUALLY 24/ 7 www.mlr.metlife.com 1-800-543-2520

WHAT ARE YOU WAITING FOR?With proper planning and action, you can get on

t rack for a comfortable ret i rement - today. The

sooner you enroll in your company's ret i rement

savings Plan, the sooner you can begin taking

advantage of everything it has to offer! Contact

your Met Life Resources Financial Services

Represent at ive t oday t o st ar t saving for your

fut ure.

Met

Life

Res

ourc

es St.M

ary'

s Co

unty

Pub

lic S

choo

lsEn

rollm

ent M

ater

ials

Mut

ual

Fund

s ar

e so

ld b

y pr

ospe

ctus

onl

y,w

hich

is

avai

labl

e fr

om y

our

regi

ster

edre

pres

enta

tive

.Ple

ase

care

fully

con

side

r in

vest

men

t ob

ject

ives

,ris

ks,c

harg

es,a

ndex

pens

es b

efor

e in

vest

ing.

For

this

and

oth

er i

nfor

mat

ion

abou

t an

y m

utua

l fu

ndin

vest

men

t pl

ease

obt

ain

a pr

ospe

ctus

and

rea

d it

car

eful

ly b

efor

e yo

u in

vest

.In

vest

men

t re

turn

and

pri

ncip

al v

alue

will

flu

ctua

te w

ith

chan

ges

in m

arke

tco

ndit

ions

suc

h th

at s

hare

s m

ay b

e w

orth

mor

e or

les

s th

an o

rigi

nal

cost

whe

nre

deem

ed.D

iver

sifi

cati

on c

anno

t el

imin

ate

the

risk

of

inve

stm

ent

loss

es,a

nd p

ast

mut

ual

fund

per

form

ance

is

not

a gu

aran

tee

of f

utur

e re

sult

s.

The

Fixe

d A

nnui

ty (

SVA

) is

off

ered

by

pros

pect

us o

nly,

whi

ch i

s av

aila

ble

from

you

rre

gist

ered

rep

rese

ntat

ive.

You

shou

ld c

aref

ully

con

side

r th

e pr

oduc

t's

feat

ures

,ris

ks,

char

ges

and

expe

nses

.Thi

s an

d ot

her

info

rmat

ion

is a

vaila

ble

in t

he p

rosp

ectu

s,w

hich

you

sho

uld

read

car

eful

ly b

efor

e in

vest

ing.

Prod

uct

avai

labi

lity

and

feat

ures

may

var

y by

sta

te.A

ll pr

oduc

t gu

aran

tees

are

bas

ed o

n th

e fi

nanc

ial

stre

ngth

and

clai

ms-

payi

ng a

bilit

y of

Met

Life

Ins

uran

ce C

ompa

ny o

f Co

nnec

ticu

t.W

ithd

raw

als

are

subj

ect

to w

ithd

raw

al c

harg

es a

nd a

mar

ket

valu

e ad

just

men

t.Th

e m

arke

t va

lue

adju

stm

ent

may

be

low

er o

r hi

gher

tha

n yo

ur c

ontr

act

valu

e.

Met

ropo

litan

Life

Insu

ranc

e Co

mpa

ny (

MLI

C),2

00 P

ark

Aven

ue,N

ew Y

ork,

NY 1

0166

.Sec

uriti

es,

inclu

ding

var

iabl

e pr

oduc

ts,of

fere

d th

roug

h M

etLif

e Se

curit

ies,

Inc.

(MSI

) (m

embe

r FI

NRA/

SIPC

),20

0 Pa

rkAv

enue

,New

Yor

k,NY

101

66.M

LIC

and

MSI

are

Met

Life

com

pani

es.

Met

Life

Reso

urce

s is

a di

visio

n of

Met

ropo

litan

Life

Insu

ranc

e Co

mpa

ny.

L110

9074

983[

exp0

210]

[All

Stat

es][D

C]