“what’s come to perfection perishes*”: adjusting capital ... · adjusting capital gains...

TRANSCRIPT

Adjusting Capital Gains Taxation in Italy

197

National Tax JournalVol. LVI, No. 1, Part 2March 2003

Abstract - Italy is the first country to have experimented withboth accruals and retrospective capital gains taxation along the linessuggested by Vickrey (1939) and Meade (1978). This paper describesthe Italian experience, highlighting its peculiar features and thelessons that can be learned by other countries wishing to pursuethese approaches. It illustrates the mechanics of the adjustments tothe realization based capital gains tax and how far they divergefrom the original proposals. The paper also draws attention to theadministrative and political difficulties encountered in implement-ing the reform. These factors ultimately resulted in a repeal ofretrospective taxation, and, in due course, may also entail the abo-lition of taxation on an accrual basis. The paper highlights the cru-cial role that financial intermediaries can play in lowering compli-ance costs under a proportional tax system and the effects on taxrevenues.

INTRODUCTION

Capital gains taxation on a realization basis is known togive rise to a number of distortions in behavior. “Lock–

in effects,” the absence of constructive realization at deathand arbitrage opportunities that exploit inconsistencies in taxcodes can result in a significant erosion of the tax base. Taxauthorities have responded to the potential loss of tax rev-enue by adopting an increasingly complex array of tax pro-visions aimed at limiting loss offsets and closing many po-tential loopholes, albeit in an “ad hoc” fashion.

Economists have proposed two types of solution to over-come these problems. The first is to move from a tax systembased on realization (cash basis) towards one based on ac-cruals (Shakow, 1986). The second is to introduce retrospec-tive taxation of capital gains along the lines suggested alter-natively by Vickrey (1939), Meade (1978), Auerbach (1991),Bradford (1995), and Auerbach and Bradford (2001).

To our knowledge, Italy is the first country to have experi-mented with both types of proposals. The purpose of thispaper is to describe the Italian experience, highlighting itspeculiar features and the lessons that can be learned by othercountries wishing to pursue these approaches. The recent Ital-ian experience illustrates various mechanisms for implement-

“What’s Come to Perfection Perishes*”:Adjusting Capital Gains Taxation in Italy

Julian AlworthEpta Group, Milano,Italy

and

EconPubblica,Università LuigiBocconi, Milano, Italy

Giampaolo ArachiDipartimento diScienze Economiche,Università di Lecce,Lecce, Italy

and

EconPubblica,Università LuigiBocconi, Milano, Italy

Rony HamauiIntesaBCI,Milano, Italy

and

Università Cattolica,Milano, Italy

*Robert Browning, Old Pictures in Florence. xvii

NATIONAL TAX JOURNAL

198

ing such systems as well as the adminis-trative and political difficulties encoun-tered by the “mark to market” (accruals)and the “retrospective” capital gains taxapproaches. It also highlights the crucialrole that financial intermediaries can playin lowering compliance costs under a pro-portional tax system and the effects on taxrevenues.

The next section of this paper summa-rizes briefly the well–known effects ofcapital gains taxation on a realizationbasis and the various adjustments thathave been proposed to mitigate the dis-tortions arising therefrom. The third sec-tion describes the framework of capitalincome taxation in Italy. It examinesthe major features of the Italian tax sys-tem prior to 1997–98, focusing on thenumerous deficiencies that led to its re-form. We then provide a critical assess-ment of the very innovative changesintroduced by the 1998 tax reform. In par-ticular, this reform introduced an accru-als based regime in a number of situations.Where this was not feasible, various typesof retrospective capital gains taxationwere introduced with the purpose of“equalizing” realizations based taxes withthose resulting from a system based onaccruals.

The fourth section examines some of theeffects of the new regimes. The revenueimpact is probably the most striking as-pect of the introduction of the new regime.Unfortunately it is difficult to assess othereffects owing to the large number of con-founding developments that occurred atthe time of the reform. However, it is pos-sible to calculate the potential impact ofthe Italian tax system on hypothetical ex–post returns and compare these returnswith those of the theoretical benchmarksto assess potential distortions to simpleportfolios. We also examine possible ef-fects of retrospective capital gains on re-alization behavior using an event studymethodology. The major conclusion of thissection is that the Italian system of retro-

spective capital gains taxation has createdsome distortions, but these do not appearto be very significant.

The regimes introduced by the 1997–98reform met with increasing oppositionfrom various quarters. Indeed, the newgovernment that was elected in mid–2001abolished retrospective capital gains taxa-tion and also appears intentioned to abol-ish the accruals regime. The fifth sectionexamines the criticisms of both the accru-als and retrospective capital gains tax re-gime that lie behind these changes andprovides an assessment of the extent towhich the Italian regime approximates atruly comprehensive income tax. The fi-nal section provides some concludingcomments.

THE THEORY OF CAPITAL GAINSTAXATION

It is well known that realization basedtaxation provides taxpayers with the op-portunity to reduce substantially their ef-fective tax burden by deferring the recog-nition of capital gains (“lock in effects”).The overall tax burden can be further re-duced (down to nil) if capital losses canbe fully offset against other types of in-come (Constantinides, 1983; Stiglitz, 1985).The traditional response to these problemshas been to limit loss offsets and imposerestrictions on “abuses.” All of these rem-edies have ultimately been unsatisfactoryand resulted in very complicated provi-sions in the tax code.

Two different strategies have been pro-posed to eliminate the incentives to real-ize gains and losses selectively. The firstis to move towards a system based on ac-cruals (Shakow, 1986). Economists havetypically shown great scepticism on theviability of this approach for a variety ofreasons: (a) it increases compliance costs;(b) “marking to market” is difficult fornon–traded assets; (c) unrealized gainsmay pose problems forcing liquidation atthe time of tax payment (Alworth, 1998).

Adjusting Capital Gains Taxation in Italy

199

For these reasons, attention has beenfocused on a second solution based onretrospective capital gains taxation.With full information regarding thepath of asset prices and holdings, it ispossible to adjust taxes paid on realiza-tion to those that would have accrued ifportfolios had been marked to market.The adjustment is determined by calcu-lating “ex post” accrued gains in eachtax year between purchase and realiza-tion, and capitalizing the implicit or “vir-tual” tax payment (or tax credit) for eachyear using the net–of–tax period–by–pe-riod internal rate of return. After payingthe adjusted tax at realization, terminalwealth from investing in a particular as-set would be equivalent to terminalwealth under accrual taxation. We willrefer to this procedure for calculating taxa-tion upon realization as the “full equiva-lence” method.

However, as first argued by Vickrey(1939), the incentive to defer gains andrealize losses can be eliminated even inthe absence of ex–post equivalence be-tween taxation upon accrual and realiza-tion. If “virtual” tax payments are capi-talized at the risk–free net–of–tax interestrate and charged at realization, investorswould be ex–ante indifferent between ac-crual and realization based taxes becausecertainty–equivalent after–tax returnswould be equated.

If the actual path of an asset’s value isunknown and taxes are levied upon real-ization it is not possible to replicate theex–post terminal wealth that would resultunder accrual taxation. In this case, theMeade report (Meade, 1978) proposed toapproximate accrual taxation by assum-ing that assets appreciate at the implicitrate of return over the holding period.Accrual taxation would be approximatedby capitalizing these annual “virtual” tax

payments by using the net–of–tax inter-est rate.

Unfortunately, the Meade method doesnot eliminate “lock–in effects.” Taxpayersmay find it profitable to anticipate or post-pone the recognition of gains and lossesdepending on the actual time path of as-set prices. In fact, as shown by Auerbach(1991), there exists only one tax systemthat does not affect the timing of realiza-tions and that can be implemented withno information regarding the path of as-set prices. As in the Meade proposal, as-sets are assumed to appreciate steadilythrough time at a given rate, and ”virtual”taxes are calculated for each tax periodand capitalized at the net–of–tax risk freeinterest rate. In contrast to the Meademethod, it is assumed that income accruesin each period at the risk free interest rate.Furthermore, the interest is calculatedstarting from a “virtual” initial asset valuecomputed by discounting the terminalvalue of the asset at the risk free interestrate.1

Despite the equivalence between ac-crual taxation and the Auerbach retrospec-tive tax formulation from an ex–ante per-spective, there is a widespread belief thatthe two are not equivalent from an ex–postbasis. Auerbach in his original contribu-tion acknowledged this difference andrecognized that from an ex–post perspec-tive his method works much like a wealthtax, as it charges a higher burden on be-low–normal returns and a lower burdenon above–normal returns. SubsequentlyKaplow (1994) challenged this view byshowing that a tax on riskless returns isequivalent to an ex–ante wealth tax whichin turn is equivalent to a tax on invest-ment returns. For any return that mightbe realized on the risky assets, the threetax regimes are equivalent if investors canachieve the same after–tax wealth by ad-

1 The equivalence with an accruals tax on an ex–ante basis is achieved by replacing “the requirement of assetvaluation (which may not be feasible) with the assumption of an efficient capital market in which investorsequate the certainty equivalent after–tax returns on different assets” Auerbach and Bradford (2001). The origi-nal Auerbach proposal has been generalized by Bradford (1995) and Auerbach and Bradford (2001).

NATIONAL TAX JOURNAL

200

justing their portfolios2 so as to sterilizethe impact of changes in tax systems onthe overall ex–post return.

THE ITALIAN TAX REFORM

Capital Income Taxation Prior to Reform

The current structure of taxation in Italydates back to reforms of 1973, which in-troduced a personal and progressive in-come tax as well as a corporation tax.These reforms also established new defi-nitions of the tax base and revised tax as-sessment procedures for different sourcesof income.3 As regards capital income, adistinction was made between “capitalincome,” (“redditi de capitale”), which com-prised a detailed specific list of proceedson financial investments (such as divi-dends and interest), and “other income”(“redditi diversi”), a catchall category in-clusive of capital gains on a limited set ofassets.

Although the original proposals envis-aged that all sources of personal incomewould be taxed comprehensively at pro-gressive rates, to all intents and purposes“capital income” became subject to a spe-cial “substitute” regime of withholdingtaxes. The withholding taxes operated asa final tax for individuals but could becredited against corporation tax. As re-gards “other income,” capital gains, mostnotably on shareholdings, were excludedfrom taxation. The system guaranteed taxanonymity for bearer instruments but notfor shares and most other registered se-curities.

Owing to the limited development ofdomestic financial markets (a relativelynarrow equity market, the absence of de-rivatives, etc.) and the presence of rigidcapital controls, there was arguably littleneed for a separate capital gains tax. More-

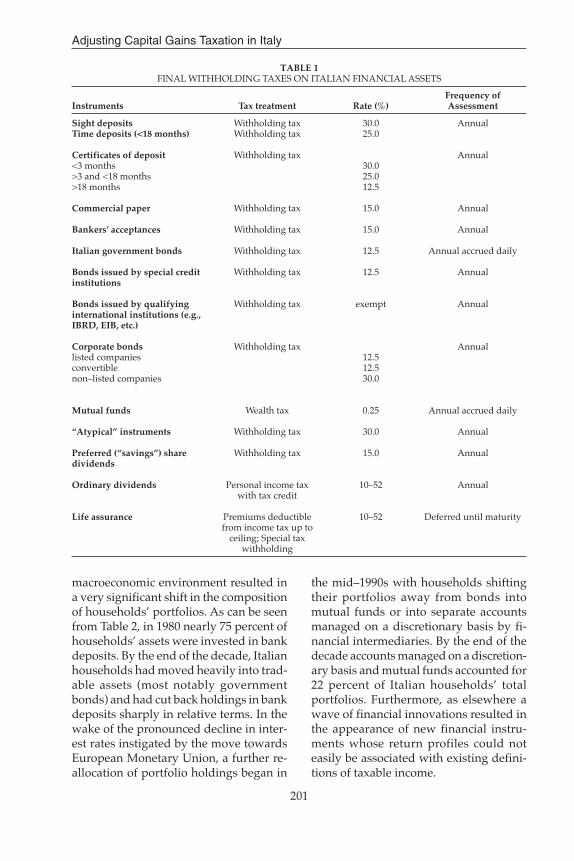

over, since there was a substitute with-holding tax regime, there were no signifi-cant deductions for interest payments.The only tax deduction against personalincome, for interest on mortgages, wasand remains very limited. As a result, incontrast to the Anglo Saxon and Nordiccountries, there was no incentive for in-dividuals to engage in zero cost arbitragesby borrowing and transferring high taxedincome into low taxed capital gains. Table1 shows the complex array of tax rates andvaluation procedures for individual in-struments and issuers under the “substi-tute” tax regimes.

The peculiar features of this “dualincome tax” regime can be attributedto numerous factors. From the standpointof this paper it is important to notetwo. First, there was a widespread percep-tion that tax anonymity—and hencewithholding of taxes at source—was im-portant to ensure compliance and thatcompliance costs for the taxpayer shouldbe minimal (a point to which we shall re-turn later). This was partly due to thebelief that the tax administration was in-capable of monitoring and enforcinga personal and progressive tax on capitalincome.

Second, withholding taxes had a strongappeal in the heavily regulated Italianeconomy. These taxes could be used tochannel credit to particular sectors, as ablunt tool of monetary policy and as a wayof distorting competition in financial mar-kets (particularly that coming from for-eign financial intermediaries and borrow-ers). It was also widely believed that keep-ing taxes on government debt at a lowlevel would help the government to fi-nance its burgeoning deficit.

During the 1980s and early 1990s ma-jor changes in the financial system and

2 The government obtains the same revenue under the three regimes for any return that might be realized onthe risky assets.

3 Six sources of income with different assessment criteria are set down in the tax law: (i) real estate and immov-able property; (ii) income from capital; (iii) employment income (iv) income from self employment; (v) enter-prise income and (vi) other income.

Adjusting Capital Gains Taxation in Italy

201

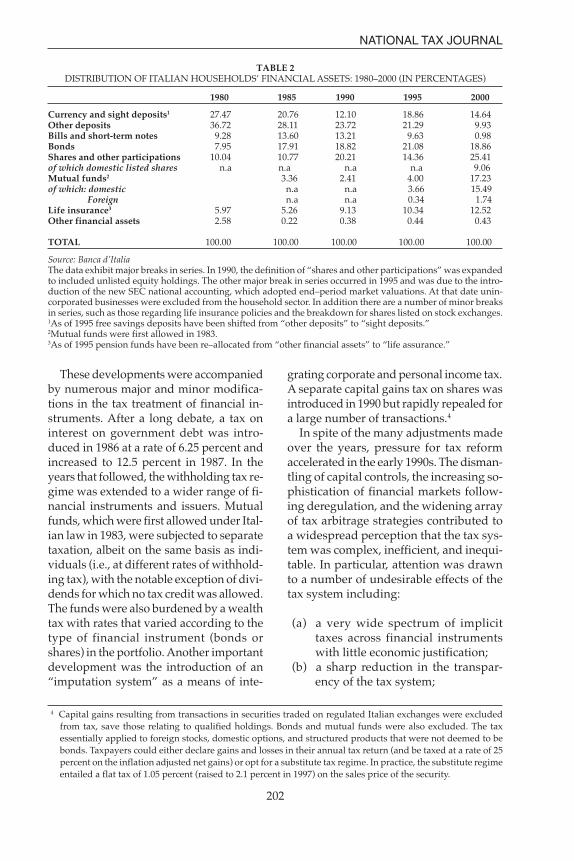

macroeconomic environment resulted ina very significant shift in the compositionof households’ portfolios. As can be seenfrom Table 2, in 1980 nearly 75 percent ofhouseholds’ assets were invested in bankdeposits. By the end of the decade, Italianhouseholds had moved heavily into trad-able assets (most notably governmentbonds) and had cut back holdings in bankdeposits sharply in relative terms. In thewake of the pronounced decline in inter-est rates instigated by the move towardsEuropean Monetary Union, a further re-allocation of portfolio holdings began in

the mid–1990s with households shiftingtheir portfolios away from bonds intomutual funds or into separate accountsmanaged on a discretionary basis by fi-nancial intermediaries. By the end of thedecade accounts managed on a discretion-ary basis and mutual funds accounted for22 percent of Italian households’ totalportfolios. Furthermore, as elsewhere awave of financial innovations resulted inthe appearance of new financial instru-ments whose return profiles could noteasily be associated with existing defini-tions of taxable income.

TABLE 1FINAL WITHHOLDING TAXES ON ITALIAN FINANCIAL ASSETS

Instruments

Sight depositsTime deposits (<18 months)

Certificates of deposit<3 months>3 and <18 months>18 months

Commercial paper

Bankers’ acceptances

Italian government bonds

Bonds issued by special creditinstitutions

Bonds issued by qualifyinginternational institutions (e.g.,IBRD, EIB, etc.)

Corporate bondslisted companiesconvertiblenon–listed companies

Mutual funds

“Atypical” instruments

Preferred (“savings”) sharedividends

Ordinary dividends

Life assurance

Tax treatment

Withholding taxWithholding tax

Withholding tax

Withholding tax

Withholding tax

Withholding tax

Withholding tax

Withholding tax

Withholding tax

Wealth tax

Withholding tax

Withholding tax

Personal income taxwith tax credit

Premiums deductiblefrom income tax up to

ceiling; Special taxwithholding

Rate (%)

30.025.0

30.025.012.5

15.0

15.0

12.5

12.5

exempt

12.512.530.0

0.25

30.0

15.0

10–52

10–52

Frequency ofAssessment

Annual

Annual

Annual

Annual

Annual accrued daily

Annual

Annual

Annual

Annual accrued daily

Annual

Annual

Annual

Deferred until maturity

NATIONAL TAX JOURNAL

202

These developments were accompaniedby numerous major and minor modifica-tions in the tax treatment of financial in-struments. After a long debate, a tax oninterest on government debt was intro-duced in 1986 at a rate of 6.25 percent andincreased to 12.5 percent in 1987. In theyears that followed, the withholding tax re-gime was extended to a wider range of fi-nancial instruments and issuers. Mutualfunds, which were first allowed under Ital-ian law in 1983, were subjected to separatetaxation, albeit on the same basis as indi-viduals (i.e., at different rates of withhold-ing tax), with the notable exception of divi-dends for which no tax credit was allowed.The funds were also burdened by a wealthtax with rates that varied according to thetype of financial instrument (bonds orshares) in the portfolio. Another importantdevelopment was the introduction of an“imputation system” as a means of inte-

grating corporate and personal income tax.A separate capital gains tax on shares wasintroduced in 1990 but rapidly repealed fora large number of transactions.4

In spite of the many adjustments madeover the years, pressure for tax reformaccelerated in the early 1990s. The disman-tling of capital controls, the increasing so-phistication of financial markets follow-ing deregulation, and the widening arrayof tax arbitrage strategies contributed toa widespread perception that the tax sys-tem was complex, inefficient, and inequi-table. In particular, attention was drawnto a number of undesirable effects of thetax system including:

(a) a very wide spectrum of implicittaxes across financial instrumentswith little economic justification;

(b) a sharp reduction in the transpar-ency of the tax system;

TABLE 2DISTRIBUTION OF ITALIAN HOUSEHOLDS’ FINANCIAL ASSETS: 1980–2000 (IN PERCENTAGES)

1980 1985 1990 1995 2000

Currency and sight deposits1 27.47 20.76 12.10 18.86 14.64Other deposits 36.72 28.11 23.72 21.29 9.93Bills and short-term notes 9.28 13.60 13.21 9.63 0.98Bonds 7.95 17.91 18.82 21.08 18.86Shares and other participations 10.04 10.77 20.21 14.36 25.41of which domestic listed shares n.a n.a n.a n.a 9.06Mutual funds2 3.36 2.41 4.00 17.23of which: domestic n.a n.a 3.66 15.49 Foreign n.a n.a 0.34 1.74Life insurance3 5.97 5.26 9.13 10.34 12.52Other financial assets 2.58 0.22 0.38 0.44 0.43

TOTAL 100.00 100.00 100.00 100.00 100.00

Source: Banca d’ItaliaThe data exhibit major breaks in series. In 1990, the definition of “shares and other participations” was expandedto included unlisted equity holdings. The other major break in series occurred in 1995 and was due to the intro-duction of the new SEC national accounting, which adopted end–period market valuations. At that date unin-corporated businesses were excluded from the household sector. In addition there are a number of minor breaksin series, such as those regarding life insurance policies and the breakdown for shares listed on stock exchanges.1As of 1995 free savings deposits have been shifted from “other deposits” to “sight deposits.”2Mutual funds were first allowed in 1983.3As of 1995 pension funds have been re–allocated from “other financial assets” to “life assurance.”

4 Capital gains resulting from transactions in securities traded on regulated Italian exchanges were excludedfrom tax, save those relating to qualified holdings. Bonds and mutual funds were also excluded. The taxessentially applied to foreign stocks, domestic options, and structured products that were not deemed to bebonds. Taxpayers could either declare gains and losses in their annual tax return (and be taxed at a rate of 25percent on the inflation adjusted net gains) or opt for a substitute tax regime. In practice, the substitute regimeentailed a flat tax of 1.05 percent (raised to 2.1 percent in 1997) on the sales price of the security.

Adjusting Capital Gains Taxation in Italy

203

(c) an incentive for widespread taxavoidance and, in some instances,near fraudulent behavior;

(d) potentially serious competitive dis-tortions both among financial inter-mediaries and instruments, and be-tween domestic and foreign invest-ments and investors;

(e) excessive resources being dedicatedto tax planning; and

(f) horizontal and vertical inequitiesacross taxpayers generated by buoy-ant equity markets and sizeable capi-tal gains.

The Reform of Capital Income Taxation

The unsatisfactory state of affairs de-scribed above lay behind widespread de-mands for a more consistent tax system andto a number of different reform proposals.The Minister of Finance (Prof. Tremonti5)issued a White Paper in 1994 suggestingseveral changes to the tax treatment of capi-tal income. Following a change in govern-ment those proposals were scrapped. Whilein opposition, the Finance Minister of theincoming government (Prof. Visco6) hadprepared a number of proposals that, tosome extent, were similar to those of theWhite Paper, albeit much more wide–rang-ing and radical. The new finance ministerset up a number of separate committees toinvestigate the feasibility of his proposals,including the reform of corporation taxalong the lines of a regime reminiscent ofthe ACE (allowance for corporate equity)and a substantial overhaul of the personaltaxation of capital income.

As far as the taxation of capital incomeis concerned the Tax Reform of 1997–98was characterized by three main features:

(a) a greater uniformity of tax rates;(b) the redefinition of the concept of

taxable income; and(c) the introduction of capital gains taxa-

tion through three types of tax re-gimes allowing for the taxation ofcapital gains.

The reform was debated in several Par-liamentary Committees. Although theopposition parties voted against the intro-duction of taxation based on accruals,most organizations affected by the re-forms (such as financial intermediaries)appeared to support the gist of the pro-posals.7 The issues raised at the time wereof a technical nature and drew attentionto the complexities of specific provisions.8

The review of tax rates

While the overall spirit of the reformseemed to support a single tax rate on alltypes of capital income,9 pressures on gov-ernment finances limited tax reductionsand fears of capital flight placed pressureson raising rates. The final legislation re-sulted in a compromise with a drastic re-duction in the number of rates to only two:12.50 percent and 27 percent. All forms ofcapital income, which prior to 1 July 1998were subject to a tax rate equal to or lessthan 15 percent, were now taxed at the taxrate of 12.5 percent. All other capital in-come, which previously had been subjectto a tax rate higher than 15 percent (pri-

5 A professor of tax law and a very successful tax practitioner.6 A professor of public finance and a staunch supporter of the Haig–Simons definition of income.7 Sen. D’Ali,’ a member of the opposition on the Tax Committee of the House of Deputies, hinted that the

approval by the financial intermediaries of the new regime was due to the fact that they would benefit fromthe new regime. Individual investors under the “administered” and “tax return” regime (described below)would be penalized.

8 Furthermore, within the ministerial committees mentioned above (for which no minutes of meetings appearto be available), it appears that there was also some disagreement between economists and legal expertsregarding the definition of income.

9 In later debates, Prof. Visco suggested that ideally this rate should be 19 percent in order to achieve neutralitybetween the corporate and personal taxes.

NATIONAL TAX JOURNAL

204

gains and losses resulting from the sale forconsideration of “qualified” holdings, and(ii) all other gains (and losses) on capital.10

The tax law also introduced a new typeof income assessment termed “operatingincome” (“risultato di gestione”)11 for assetsmanaged on a discretionary basis by au-thorized intermediaries and for mutualfunds. Broadly speaking “operating in-come,” Y(t), can be viewed as either thechange in the “mark to market” value ofinvestors’ portfolios or the sum of “capi-tal income” and “other income.” In prac-tice it is defined as:

[1] Y(t) = W(t) – W(t – 1) – X(t) –S(t),

where W(t) is the “mark to market” valueof the net assets in portfolio (i.e., wealth)at time t, X(t) is the value of any proceedsreceived between t and t – 112 which havealready been subject to tax or are tax ex-empt and S(t) are additions to net assets(net savings flowing into the “operatingincome” account).

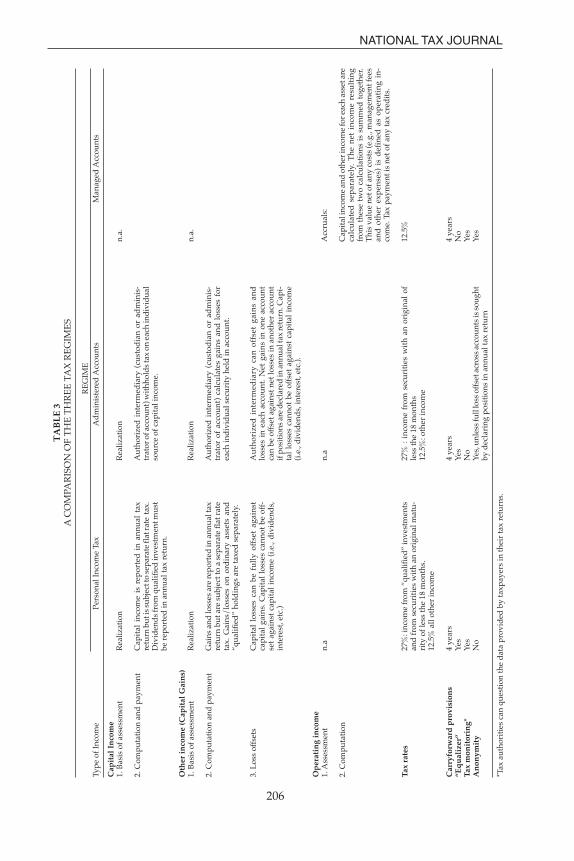

The taxation regimes

Capital gains (net of any capital losses)incurred from the sale of qualified hold-ings by individuals must be declared un-der the personal income tax schedule, al-though they are subject to a special sub-stitute tax rate 27 percent. All other formsof capital income or other income are sub-ject to three possible types of regime:

• the managed portfolio method, whichapplies to “operating income;”

• the tax return regime under whichtaxpayers opt to declare income in

marily bank deposits) were taxed at a rateof 27 percent. As already mentioned, therate of 27 percent also applied to gainsfrom the sale of qualified holdings.

For non–residents, the system and levelof taxation had already begun to changein 1996. In combination with the reformof capital income taxation of residents, inthe years following the rate levels for non–residents were revised significantly and,in a number of instances, reduced unilat-erally or by virtue of the provisions indouble tax treaties. In practice, residentsfrom countries that do not provide pref-erential tax regimes and with double taxa-tion treaties that allow an “exchange ofinformation” are presently no longertaxed at source on interest income. Forother sources of income, double tax trea-ties entail that the tax rates applicable tonon–residents may differ from 12.5 per-cent and 27 percent.

The redefinition of the types of income

The reform retained the broad distinc-tion between “capital income” and “otherincome,” although the original proposalsought to abolish this differentiation. Thecomponents of “capital income” (divi-dends, interest, etc.) remained unchangedbut the definition of “other income” waswidened to include capital gains. Thesegains included the proceeds from sales ofequity shares, bonds, currencies and pre-cious metals, as well as the proceeds fromderivative contracts (with or without un-derlying securities) and from other secu-rities and credits. Capital gains fromshareholdings and other forms of equityparticipation were classified as: (i) capital

10 The criteria for establishing “qualified” holdings were redefined to take as reference the percentage of thevoting rights that can be exercised at shareholders’ meetings. In the case of securities traded on regulatedmarkets, voting rights (other than savings shares), which can be exercised at the ordinary shareholders’ meet-ings in excess of 2 percent or participations in the capital of a company in excess of 5 percent constitutequalified holdings. In the case of securities not traded on regulated exchanges, such percentages increaserespectively to 20 percent and 25 percent.

11 This concept was not included as an additional type of income alongside “capital” and “other” income.12 This item includes income that has been subject to a withholding tax, such as interest on bank deposits, in-

come from closed and open–ended mutual funds, and “tax exempt securities (such as bonds issued by inter-national institutions prior to 1992).”

Adjusting Capital Gains Taxation in Italy

205

their tax returns according to crite-ria similar to those provided for“qualified“ capital gains;

• the administered portfolio method,whereby an authorized financial in-termediary withholds tax at sourceon an instrument by instrument andtransaction by transaction basis.

Under the managed portfolio methodtaxation is based on accruals. Individualscan opt for this regime only if they entrustthe management of their wealth to finan-cial intermediaries on a discretionary ba-sis. A substitute tax rate of 12.5 percent isapplied to “operating income” as definedabove.13 Any net losses can be carried for-ward for four years.

The managed portfolio method is alsoapplied to Italian mutual funds andSICAVS (variable capital companies), inways that are not very different from thoseindicated above. For example, in terms ofthe definition of operating income pro-vided in [1], S(t) can be interpreted as sub-scriptions less redemptions. Moreover, theshift to the concept of “operating income”as of 1st July 1998 means that funds are nolonger subject to withholding tax and do-mestic revenues are accrued on a “gross”basis. The major difference between thetaxation of mutual funds and that of other“managed accounts” is that for the formera tax accrual (or tax credit) is set aside ona daily basis within a fund. In other wordspurchases and sales of funds are net of anytaxes that have accrued over the period.Individual accounts managed on a discre-

tionary basis are taxed once a year (as wellas at the time of the closing of an account).It should also be noted that authorized in-termediaries, including asset manage-ment companies, can offset tax credits anddebits across accounts and funds.

Under the tax return regime and theadministered portfolio method, taxes areapplied on a realization basis (mostlythrough withholding taxes at source) sub-ject to a “tax equalization” factor de-scribed below. Capital gains are computednet of any losses by the taxpayer (underthe “tax return” method) or by the autho-rized intermediary (under the “adminis-tered portfolio method”). However, capi-tal income and “other income” are treatedseparately in the sense that losses arisingfrom “other income” (i.e., capital losses)cannot be used to offset capital income(dividends, interest, etc.). Net losses from“other income” arising in different ac-counts can be offset against one anotherif the net gains and losses are declared bytaxpayers in their annual tax returns. Re-alized losses in an individual account canbe carried forward for four years. Finallyit should be noted that the administeredportfolio method and managed portfoliomethod guarantee full tax anonymity.

The “Equalizer”

In order to place taxation on realizationson par with accruals, the reform providedfor an adjustment to the realization taxbasis under the tax return and the admin-istered portfolio regimes. This adjustment

13 For non–residents the administered portfolio method is the norm, if there is a custody, management or de-posit relationship with an Italian intermediary. However, non–residents may opt out of the administeredportfolio method (and thus fall within the tax return regime) by giving notice to the Italian intermediary. Theaforesaid waiver is granted also to non–resident intermediaries relative to custody, administration, and de-posit relationships registered in their name, and within which third party financial assets are held (so–called“omnibus” accounts). In this case non–resident intermediaries must appoint a tax representative in Italy thatwill notify the tax authorities of the data relative to the individual transactions carried out by its clients in theprevious year. The managed portfolio method appears to prejudice non–residents. In fact no tax treaty con-templates the “operating income” as a taxable event, and therefore provides for exemption from or reducedtaxation. Unilateral relief also does not appear to be applicable. Thus, a non–resident should be obliged to paythe substitute tax of 12.5 percent provided for fund management. In order to avoid this problem a unilateraltax credit is provided for the underlying taxes paid by the fund. The complexities of the regime, however,have discouraged non–residents from investing in Italian funds.

NATIONAL TAX JOURNAL

206

TA

BL

E 3

A C

OM

PAR

ISO

N O

F T

HE

TH

RE

E T

AX

RE

GIM

ES

RE

GIM

ETy

pe o

f Inc

ome

Pers

onal

Inco

me

Tax

Ad

min

iste

red

Acc

ount

sM

anag

ed A

ccou

nts

Cap

ital

In

com

e1.

Bas

is o

f ass

essm

ent

2. C

ompu

tati

on a

nd p

aym

ent

Oth

er in

com

e (C

apit

al G

ain

s)1.

Bas

is o

f ass

essm

ent

2. C

ompu

tati

on a

nd p

aym

ent

3. L

oss

offs

ets

Op

erat

ing

inco

me

1. A

sses

smen

t

2. C

ompu

tati

on

Tax

rate

s

Car

ryfo

rwar

d p

rovi

sion

s“E

qu

aliz

er”

Tax

mon

itor

ing*

An

onym

ity

*Tax

aut

hori

ties

can

que

stio

n th

e d

ata

prov

ided

by

taxp

ayer

s in

thei

r ta

x re

turn

s.

Rea

lizat

ion

Cap

ital

inc

ome

is r

epor

ted

in

annu

al t

axre

turn

but

is su

bjec

t to

sepa

rate

flat

rate

tax

.D

ivid

end

s fr

om q

ualif

ied

inve

stm

ent m

ust

be r

epor

ted

in a

nnua

l tax

ret

urn.

Rea

lizat

ion

Gai

ns a

nd lo

sses

are

repo

rted

in a

nnua

l tax

retu

rn b

ut a

re s

ubje

ct to

a s

epar

ate

flat

rat

eta

x. G

ains

/lo

sses

on

ord

inar

y as

sets

and

“qua

lifie

d”

hold

ings

are

taxe

d s

epar

atel

y.

Cap

ital

los

ses

can

be f

ully

off

set

agai

nst

capi

tal g

ains

. Cap

ital

loss

es c

anno

t be

off

-se

t ag

ains

t ca

pita

l inc

ome

(i.e

., d

ivid

end

s,in

tere

st, e

tc.)

n.a

27%

: inc

ome

from

“qu

alif

ied

” in

vest

men

tsan

d fr

om s

ecur

itie

s w

ith

an o

rigi

nal m

atu-

rity

of l

ess

the

18 m

onth

s.12

.5%

all

othe

r in

com

e

4 ye

ars

Yes

Yes

No

Rea

lizat

ion

Aut

hori

zed

int

erm

edia

ry (

cust

odia

n or

ad

min

is-

trat

or o

f acc

ount

) wit

hhol

ds t

ax o

n ea

ch in

div

idua

lso

urce

of c

apit

al in

com

e.

Rea

lizat

ion

Aut

hori

zed

int

erm

edia

ry (

cust

odia

n or

ad

min

is-

trat

or o

f ac

coun

t) c

alcu

late

s ga

ins

and

los

ses

for

each

ind

ivid

ual s

ecur

ity

held

in a

ccou

nt.

Au

thor

ized

in

term

edia

ry c

an o

ffse

t ga

ins

and

loss

es i

n ea

ch a

ccou

nt. N

et g

ains

in

one

acco

unt

can

be o

ffse

t aga

inst

net

loss

es in

ano

ther

acc

ount

if p

osit

ions

are

dec

lare

d in

ann

ual t

ax re

turn

. Cap

i-ta

l lo

sses

can

not

be o

ffse

t ag

ains

t ca

pita

l in

com

e(i

.e.,

div

iden

ds,

inte

rest

, etc

.).

n.a

27%

: in

com

e fr

om s

ecur

itie

s w

ith

an o

rigi

nal

ofle

ss th

e 18

mon

ths

12.5

%: o

ther

inco

me

4 ye

ars

Yes

No

Yes,

unl

ess

full

loss

off

set a

cros

s ac

coun

ts is

sou

ght

by d

ecla

ring

pos

itio

ns in

ann

ual t

ax r

etur

n

n.a.

n.a.

Acc

rual

s:

Cap

ital

inco

me

and

oth

er in

com

e fo

r eac

h as

set a

reca

lcu

late

d s

epar

atel

y. T

he n

et i

ncom

e re

sult

ing

from

the

se t

wo

calc

ulat

ions

is

sum

med

tog

ethe

r.T

his

valu

e ne

t of a

ny c

osts

(e.g

., m

anag

emen

t fee

san

d o

ther

exp

ense

s) i

s d

efin

ed a

s op

erat

ing

in-

com

e. T

ax p

aym

ent i

s ne

t of a

ny ta

x cr

edit

s.

12.5

%

4 ye

ars

No

Yes

Yes

Adjusting Capital Gains Taxation in Italy

207

was called the “equalizer.” It took differentforms but was similar to the proposals putforth by Vickrey (1939) and Meade (1978).

Because of its complexity the “equal-izer” was the subject of much debate be-fore its introduction and its implementa-tion required creating a sophisticated da-tabase to permit the precise computationof accrued capital gains at the end of eachtax year. As a result, its introduction wasdelayed until January 2001. However, ittook effect retroactively on gains accruingfrom July 1, 1998.14

Three separate types of regime wereultimately put in place covering (a) secu-rities traded on regulated exchanges; (b)securities not traded on regulated ex-changes; and (c) foreign mutual fundsregulated under the European Directive.15

Securities traded on regulated exchanges

Where the prices of traded securities areknown (full information), it is possible todetermine the value of the tax that wouldhave matured in each year in which thesecurity was held. The realization–basedadjustment under these circumstances(known as the “analytical method”) isreminiscent of the system proposed byVickrey (1939). This system envisages cal-culating “ex post” accrued gains in eachtax year between purchase and realiza-tion, and capitalizing the “virtual” taxpayment (or tax credit) for each year. The“virtual” tax payment on a single secu-rity j at time t is then given by:

[2] τ(t – 1)[pj(t) – pj(t – 1)]nj,

where τ (t – 1) is the tax rate on gains be-tween the end of year t and the end ofperiod t – 1, pj(t) is the price of security iat time t,16 nj is the number of securities

held at time t – 1. Henceforth for simplic-ity it will be assumed that τ (t – 1) = τ andnj = 1.

If the value in [2] is positive, it is capi-talized at an official interest rate i(t) fortime t (based on the return to governmentbonds at time t). If the security is held untiltime T, the capitalization factor for thegain accruing between t and t – 1 is theproduct of the capitalization factors be-tween t and T, K(t,T), defined as:

K(t,T) = Π(1 + i(s)).

If [2] is negative it is carried forwardwithout being capitalized and the accumu-lated value of such losses Lj (t) is givenby:

Lj(t) = Max[Lj(t – 1) – τ(pj(t) – pj(t – 1)), 0].

Accordingly “virtual” taxes at time t aregiven by:

TAXjA(t) = Max[τ(pj(t) – pj(t – 1)) – Lj(t – 1), 0],

and upon realization the total taxes pay-able on security i are given by:

TAXjA (T) = Σ [K(t, T)TAXj

A(t)] – Li(T).

The overall tax liability for securities taxedunder the analytical method is given by:

TAXA (T) = Σ TAXjA (T).

The actual tax law includes some addi-tional complications. In particular, theprecise formulae take into account the tim-ing differences between the payment ofthe “equalizer” and the realization of the

14 Unpublished documents, that have been made available to the authors, highlight that the precise formulasadopted were the object of long discussions between financial intermediaries and the Ministry of Finance.

15 Two important exclusions from the “equalizer” regime where gains from “qualified” shareholdings and frominvestments in foreign non–harmonized mutual funds (i.e., not covered by the European Directive on collec-tive investments—UCITs).

16 The price is net of any dividends paid during the period that have already been taxed.

T

s=t

J

j=1

T

t=1

NATIONAL TAX JOURNAL

208

capital gain or loss.17 Prices for the tradedsecurities that serve as a basis for the cal-culation of the “equalizer” are providedfrom a database established by the UIC(Ufficio Italiano Cambi, the former For-eign Exchange Office).

Securities not traded on regulated exchanges

When full information regarding thepath of the prices of securities over timedoes not exist the Vickrey or “analytical”method cannot be applied. One proposalto deal with this circumstance was sug-gested by Meade (1978); the Italian au-thorities implemented a variant.18 This so–called “simplified” method consists ofdetermining the average annual price in-crease over the holding period, and in thecase of a capital gain capitalizing thisamount at the reference interest rate sothat:

T [pj(T) – pj(0)]TAXj

S(T) = ΣτK(t, T) —————— .1 T

If there is a capital loss, no capitaliza-tion factor is applied and the tax credit isgiven by:

TAXjS(T) = τ[pj(T) – pj (0)].

Accordingly the overall liability for secu-rities taxed under the “simplified”method is equal to:

TAXS(T) = Σ TAXjs(T).

Foreign mutual funds regulated under theEuropean Directive (UCITS)

In the case of foreign mutual funds thesystem is similar to that adopted for the“analytical” method. Accordingly the lossand tax liability in each period are given by:

Lj(t) = Max[Lj(t – 1) – τ(pj(t) – pj(t – 1)), 0]

TAXjM(t) = Max[τ(pj(t) – pj(t – 1)) – Lj(t – 1), 0].

However there are two important dis-tinctions. First, gains are not capitalizedat the reference (“riskless”) interest rate.In order to approximate the effects of themark–to–market regime for domestic mu-tual funds, accrued gains are capitalizedat the internal rate of return of the funditself in each period between the accrualof the “virtual” tax and the time of real-ization. As a result the tax on foreign mu-tual fund j is given by:

T pj(T) – pj(t – 1)TAXj

M(T) = Σ [(1 + ———————)T–t

t=1 pj(t – 1)

TAXjM(t)] – Lj(T).

Second, it is not possible to offset fundsfor which there are positive tax paymentsagainst funds in a credit position (exceptwithin an “umbrella” fund structure). Thisis because net positive gains over the hold-ing period for an individual fund are con-sidered “capital income,” whereas a fundfor which an aggregate loss has been real-ized is treated as “other income.” No off-set is possible between “capital income”and “other income” outside of a “man-aged account.”

ECONOMIC EFFECTS OF ACCRUALTAXATION AND THE “EQUALIZER”

In this section we attempt to assess theimpact of the new capital gains tax regimeon tax revenues and economic behavior.Any empirical investigation of the effectsof the reform on prices and portfolio com-

J

j = 1

17 The precise calculation methods were described in a technical appendix to the tax law.18 As in the case of the “analytical method” losses are carried forward without being capitalized. Another differ-

ence between the Meade and the Italian simplified method is that under the former method the growth ofasset prices is assumed to occur exponentially.

Adjusting Capital Gains Taxation in Italy

209

position is a complicated task. The evi-dence is limited because the equalizer wasabolished soon after its introduction andthe evaluation of its impact may be af-fected by several confounding factors. Forexample, during the electoral campaignthe winning coalition repeatedly advo-cated removing the equalizer. With theselimitations in mind, we focus our atten-tion on two questions concerning the be-havioral effects of the reform:

(a) whether the various regimes mayhave significantly distorted portfo-lio decisions relative to a no tax or aperfect accruals regime; and

(b) whether the retroactive applicationof the “equalizer” resulted in abnor-mal trading before its introduction.

Tax Revenues

The new capital gains regime had animpressive performance in terms ofrevenue in the first three years of imple-mentation due to the exceptional upsurgeof equity markets in 1998 through early2000. Table 4 provides tax revenue datafrom withholding taxes on capital income,capital gains taxes under the tax returnand administered portfolio regimes, andtaxes on the “operating income” of mu-tual funds and individual managedaccounts.

The yield of the capital gains tax leviedunder the tax return and the administeredportfolio regimes almost doubled between1999 and 2000, reaching, 3,000 million.Revenue from the tax on the “operatingincome” of mutual funds and individualmanaged accounts displayed an evenmore exceptional expansion, from 1,525million in 1999 to 7,868 million in 2000.The bulk of the tax was paid by mutualfunds. The low tax yield on individualmanaged accounts is mainly due to thestructure of holdings. More than half ofthe accounts’ total assets are invested inmutual funds; in order to avoid doubletaxation, no additional tax is due on thisportion of managed accounts.

The rise in revenue from capital gainsand operating income taxation was offsetby the sharp reduction in withholdingtaxes on capital income from 9,806 mil-lion in 1999 to 6,241 million in 2000. Thisshortfall is attributable to two develop-ments. First, interest rates on deposits andTreasury bonds steadily fell during theperiod. Second, an increasing share ofbonds and stocks were held in managedaccounts or by mutual funds, which arenot subject to the withholding tax (inter-est and dividends are taxed as part of the“operating income”).

It is interesting to note that the flipsideof the massive revenues in 1999 and 2000has been the equally sizeable volume of

TABLE 4REVENUE FROM CAPITAL INCOME AND CAPITAL GAINS TAXES IN ITALY

(in millions of Euro)

1998 1999 2000

Witholding taxes on capital income 9,806 7,780 6,241of which withholding tax on interest 5,743 3,459 3,696

Capital gains tax under the tax return and administered portfolio regimes 543 1,715 3,153of which capital gains realised before July 98 338 335 42

capital gains realised after July 98 205 1,380 3,111

Tax on operating income 212 1,525 7,868of which mutual funds 208 1,026 6,895

individual managed accounts 5 499 973

Total 10,562 11,020 17,262

Source: Ministry of the Economy and Finance

NATIONAL TAX JOURNAL

210

tax credits, which have resulted from thesharp turnaround in equity markets.While no official data are available on thistopic, Assogestioni (the Italian Associationof Fund Managers) has estimated thatmutual funds alone had accumulated over

6 billion in tax credits at end–May2002.19 A further 3.4 billion tax creditswere estimated for other “managed ac-counts” and “administered accounts.”

The Distortions Introduced by theEqualizer

As previously mentioned, the adjust-ments made under the three different re-gimes (securities traded on regulated ex-changes, securities not traded on regu-lated exchanges and foreign mutualfunds) are variants of the Vickrey, Meade,and full equivalence methods, respec-tively. There are three main differencesbetween the “equalizers” and their theo-retical counterparts.

First, the adjustment of the income fromforeign mutual funds uses a gross–of–taxreturn to capitalize virtual tax paymentsinstead of the net–of–tax rate employedin the theoretical model of full equiva-lence. This increases the effective tax bur-den above the level that would arise un-der accrual taxation and provides an in-centive to anticipate realizations.

Second, for securities not traded onregulated exchanges, the adjustment fol-lows the Meade method but the virtualannual price increase over the holdingperiod is set equal to the arithmetic meaninstead of the geometric mean used in theoriginal Meade proposal.

Finally, capital losses are not capitalizedunder any of the regimes. As a result ofthis asymmetric treatment of gains andlosses, the Vickrey and full equivalence

methods no longer neutralize the lock–ineffect. In addition assets with higher vola-tility will be subject to higher expected taxpayments. Given the asymmetry of the taxschedule it is not possible to derive ananalytical solution for the effective taxburden on risky investments under thethree alternative regimes. The expectedvalue of the tax will depend not only onthe expected appreciation of the asset butalso on the volatility and path of prices.We can overcome this hurdle by simulat-ing expected final wealth and taxes.20

The simulations assume that the asset(or portfolio) returns in each tax year arenormally distributed with mean δ andstandard deviation σ., i.e.:

p(t) – p(t – 1)—————— = δ + εt,p(t – 1)

where p(t) is the price of the individualsecurity and εt is a white noise processwith εt ~ N(0, σ).

For each series of draws from the Nor-mal distribution, one for each tax year, wecalculated final wealth and taxes to bepaid under the different types of “equal-izer.” The average values over two thou-sand simulations were used to calculateexpected gross, u, and net–of–tax returns,v. The expected effective tax rate (EETR)was computed as:

u – νEETR = ——— .u

The results of the simulations are re-ported in Table 5. Part A contains the simu-lated EETR for a five year holding periodunder the assumption that the mean re-turn is equal to the risk free interest rate.

If gains and losses were treatedsymmetrically, the equaliser applied to

19 It is interesting to note that the accumulation of tax credits could lead to the insolvency of a mutual fund ifredemptions were excessive. Presumably tax credits could not be used to pay out investors requesting theredemption of their units in the fund.

20 Mintz and Smart (2002) have recently applied a similar approach to evaluate the effect of non refundability oflosses on taxable equities.

Adjusting Capital Gains Taxation in Italy

211

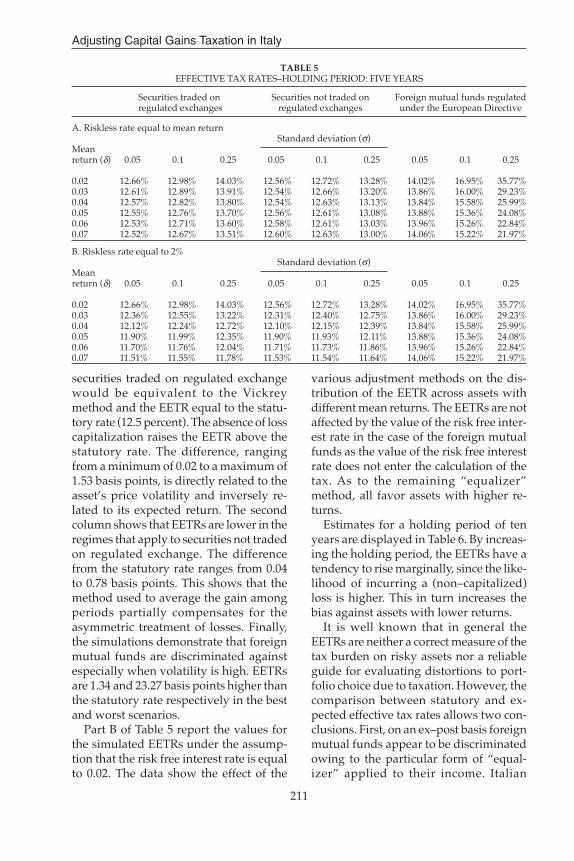

securities traded on regulated exchangewould be equivalent to the Vickreymethod and the EETR equal to the statu-tory rate (12.5 percent). The absence of losscapitalization raises the EETR above thestatutory rate. The difference, rangingfrom a minimum of 0.02 to a maximum of1.53 basis points, is directly related to theasset’s price volatility and inversely re-lated to its expected return. The secondcolumn shows that EETRs are lower in theregimes that apply to securities not tradedon regulated exchange. The differencefrom the statutory rate ranges from 0.04to 0.78 basis points. This shows that themethod used to average the gain amongperiods partially compensates for theasymmetric treatment of losses. Finally,the simulations demonstrate that foreignmutual funds are discriminated againstespecially when volatility is high. EETRsare 1.34 and 23.27 basis points higher thanthe statutory rate respectively in the bestand worst scenarios.

Part B of Table 5 report the values forthe simulated EETRs under the assump-tion that the risk free interest rate is equalto 0.02. The data show the effect of the

various adjustment methods on the dis-tribution of the EETR across assets withdifferent mean returns. The EETRs are notaffected by the value of the risk free inter-est rate in the case of the foreign mutualfunds as the value of the risk free interestrate does not enter the calculation of thetax. As to the remaining “equalizer”method, all favor assets with higher re-turns.

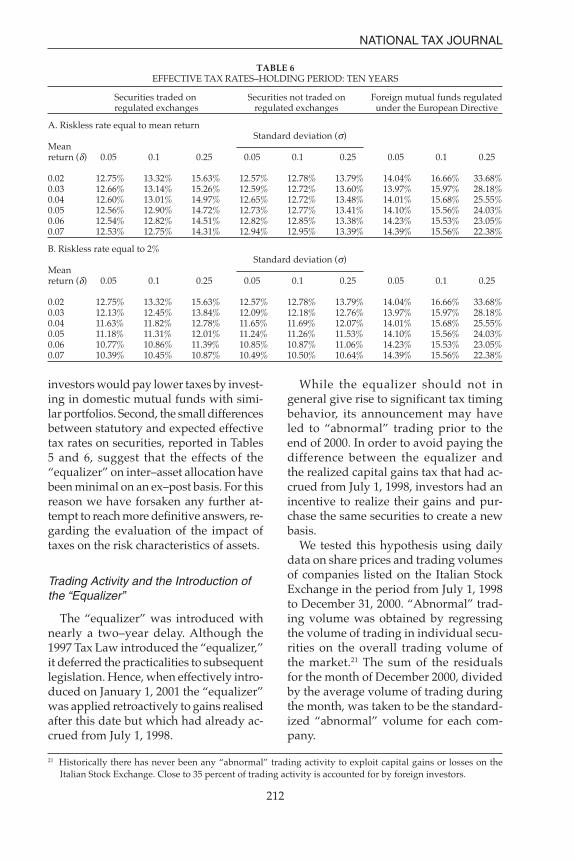

Estimates for a holding period of tenyears are displayed in Table 6. By increas-ing the holding period, the EETRs have atendency to rise marginally, since the like-lihood of incurring a (non–capitalized)loss is higher. This in turn increases thebias against assets with lower returns.

It is well known that in general theEETRs are neither a correct measure of thetax burden on risky assets nor a reliableguide for evaluating distortions to port-folio choice due to taxation. However, thecomparison between statutory and ex-pected effective tax rates allows two con-clusions. First, on an ex–post basis foreignmutual funds appear to be discriminatedowing to the particular form of “equal-izer” applied to their income. Italian

TABLE 5EFFECTIVE TAX RATES–HOLDING PERIOD: FIVE YEARS

Securities traded on Securities not traded on Foreign mutual funds regulatedregulated exchanges regulated exchanges under the European Directive

A. Riskless rate equal to mean returnStandard deviation (σ)

Meanreturn (δ) 0.05 0.1 0.25 0.05 0.1 0.25 0.05 0.1 0.25

0.02 12.66% 12.98% 14.03% 12.56% 12.72% 13.28% 14.02% 16.95% 35.77%0.03 12.61% 12.89% 13.91% 12.54% 12.66% 13.20% 13.86% 16.00% 29.23%0.04 12.57% 12.82% 13.80% 12.54% 12.63% 13.13% 13.84% 15.58% 25.99%0.05 12.55% 12.76% 13.70% 12.56% 12.61% 13.08% 13.88% 15.36% 24.08%0.06 12.53% 12.71% 13.60% 12.58% 12.61% 13.03% 13.96% 15.26% 22.84%0.07 12.52% 12.67% 13.51% 12.60% 12.63% 13.00% 14.06% 15.22% 21.97%

B. Riskless rate equal to 2%Standard deviation (σ)

Meanreturn (δ) 0.05 0.1 0.25 0.05 0.1 0.25 0.05 0.1 0.25

0.02 12.66% 12.98% 14.03% 12.56% 12.72% 13.28% 14.02% 16.95% 35.77%0.03 12.36% 12.55% 13.22% 12.31% 12.40% 12.75% 13.86% 16.00% 29.23%0.04 12.12% 12.24% 12.72% 12.10% 12.15% 12.39% 13.84% 15.58% 25.99%0.05 11.90% 11.99% 12.35% 11.90% 11.93% 12.11% 13.88% 15.36% 24.08%0.06 11.70% 11.76% 12.04% 11.71% 11.73% 11.86% 13.96% 15.26% 22.84%0.07 11.51% 11.55% 11.78% 11.53% 11.54% 11.64% 14.06% 15.22% 21.97%

NATIONAL TAX JOURNAL

212

investors would pay lower taxes by invest-ing in domestic mutual funds with simi-lar portfolios. Second, the small differencesbetween statutory and expected effectivetax rates on securities, reported in Tables5 and 6, suggest that the effects of the“equalizer” on inter–asset allocation havebeen minimal on an ex–post basis. For thisreason we have forsaken any further at-tempt to reach more definitive answers, re-garding the evaluation of the impact oftaxes on the risk characteristics of assets.

Trading Activity and the Introduction ofthe “Equalizer”

The “equalizer” was introduced withnearly a two–year delay. Although the1997 Tax Law introduced the “equalizer,”it deferred the practicalities to subsequentlegislation. Hence, when effectively intro-duced on January 1, 2001 the “equalizer”was applied retroactively to gains realisedafter this date but which had already ac-crued from July 1, 1998.

While the equalizer should not ingeneral give rise to significant tax timingbehavior, its announcement may haveled to “abnormal” trading prior to theend of 2000. In order to avoid paying thedifference between the equalizer andthe realized capital gains tax that had ac-crued from July 1, 1998, investors had anincentive to realize their gains and pur-chase the same securities to create a newbasis.

We tested this hypothesis using dailydata on share prices and trading volumesof companies listed on the Italian StockExchange in the period from July 1, 1998to December 31, 2000. “Abnormal” trad-ing volume was obtained by regressingthe volume of trading in individual secu-rities on the overall trading volume ofthe market.21 The sum of the residualsfor the month of December 2000, dividedby the average volume of trading duringthe month, was taken to be the standard-ized “abnormal” volume for each com-pany.

TABLE 6EFFECTIVE TAX RATES–HOLDING PERIOD: TEN YEARS

Securities traded on Securities not traded on Foreign mutual funds regulatedregulated exchanges regulated exchanges under the European Directive

A. Riskless rate equal to mean returnStandard deviation (σ)

Meanreturn (δ) 0.05 0.1 0.25 0.05 0.1 0.25 0.05 0.1 0.25

0.02 12.75% 13.32% 15.63% 12.57% 12.78% 13.79% 14.04% 16.66% 33.68%0.03 12.66% 13.14% 15.26% 12.59% 12.72% 13.60% 13.97% 15.97% 28.18%0.04 12.60% 13.01% 14.97% 12.65% 12.72% 13.48% 14.01% 15.68% 25.55%0.05 12.56% 12.90% 14.72% 12.73% 12.77% 13.41% 14.10% 15.56% 24.03%0.06 12.54% 12.82% 14.51% 12.82% 12.85% 13.38% 14.23% 15.53% 23.05%0.07 12.53% 12.75% 14.31% 12.94% 12.95% 13.39% 14.39% 15.56% 22.38%

B. Riskless rate equal to 2%Standard deviation (σ)

Meanreturn (δ) 0.05 0.1 0.25 0.05 0.1 0.25 0.05 0.1 0.25

0.02 12.75% 13.32% 15.63% 12.57% 12.78% 13.79% 14.04% 16.66% 33.68%0.03 12.13% 12.45% 13.84% 12.09% 12.18% 12.76% 13.97% 15.97% 28.18%0.04 11.63% 11.82% 12.78% 11.65% 11.69% 12.07% 14.01% 15.68% 25.55%0.05 11.18% 11.31% 12.01% 11.24% 11.26% 11.53% 14.10% 15.56% 24.03%0.06 10.77% 10.86% 11.39% 10.85% 10.87% 11.06% 14.23% 15.53% 23.05%0.07 10.39% 10.45% 10.87% 10.49% 10.50% 10.64% 14.39% 15.56% 22.38%

21 Historically there has never been any “abnormal” trading activity to exploit capital gains or losses on theItalian Stock Exchange. Close to 35 percent of trading activity is accounted for by foreign investors.

Adjusting Capital Gains Taxation in Italy

213

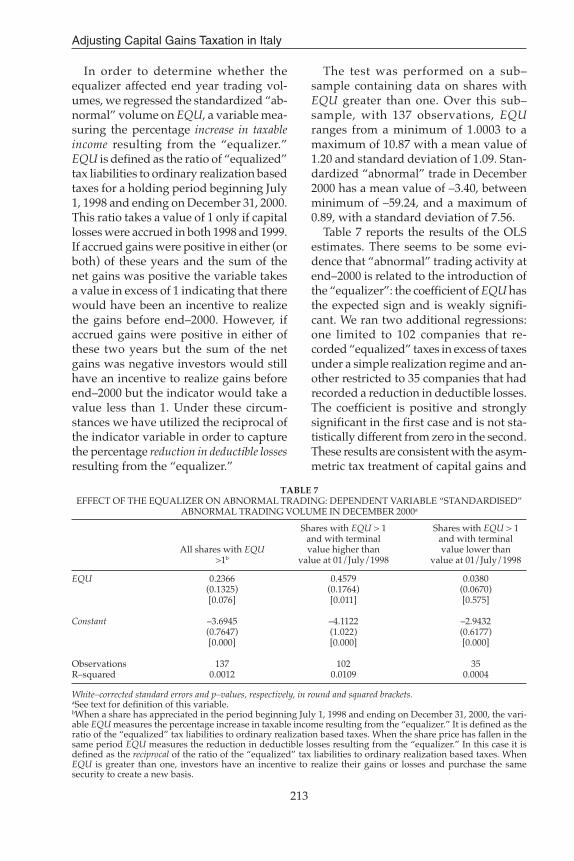

In order to determine whether theequalizer affected end year trading vol-umes, we regressed the standardized “ab-normal” volume on EQU, a variable mea-suring the percentage increase in taxableincome resulting from the “equalizer.”EQU is defined as the ratio of “equalized”tax liabilities to ordinary realization basedtaxes for a holding period beginning July1, 1998 and ending on December 31, 2000.This ratio takes a value of 1 only if capitallosses were accrued in both 1998 and 1999.If accrued gains were positive in either (orboth) of these years and the sum of thenet gains was positive the variable takesa value in excess of 1 indicating that therewould have been an incentive to realizethe gains before end–2000. However, ifaccrued gains were positive in either ofthese two years but the sum of the netgains was negative investors would stillhave an incentive to realize gains beforeend–2000 but the indicator would take avalue less than 1. Under these circum-stances we have utilized the reciprocal ofthe indicator variable in order to capturethe percentage reduction in deductible lossesresulting from the “equalizer.”

The test was performed on a sub–sample containing data on shares withEQU greater than one. Over this sub–sample, with 137 observations, EQUranges from a minimum of 1.0003 to amaximum of 10.87 with a mean value of1.20 and standard deviation of 1.09. Stan-dardized “abnormal” trade in December2000 has a mean value of –3.40, betweenminimum of –59.24, and a maximum of0.89, with a standard deviation of 7.56.

Table 7 reports the results of the OLSestimates. There seems to be some evi-dence that “abnormal” trading activity atend–2000 is related to the introduction ofthe “equalizer”: the coefficient of EQU hasthe expected sign and is weakly signifi-cant. We ran two additional regressions:one limited to 102 companies that re-corded “equalized” taxes in excess of taxesunder a simple realization regime and an-other restricted to 35 companies that hadrecorded a reduction in deductible losses.The coefficient is positive and stronglysignificant in the first case and is not sta-tistically different from zero in the second.These results are consistent with the asym-metric tax treatment of capital gains and

TABLE 7EFFECT OF THE EQUALIZER ON ABNORMAL TRADING: DEPENDENT VARIABLE “STANDARDISED”

ABNORMAL TRADING VOLUME IN DECEMBER 2000a

White–corrected standard errors and p–values, respectively, in round and squared brackets.aSee text for definition of this variable.bWhen a share has appreciated in the period beginning July 1, 1998 and ending on December 31, 2000, the vari-able EQU measures the percentage increase in taxable income resulting from the “equalizer.” It is defined as theratio of the “equalized” tax liabilities to ordinary realization based taxes. When the share price has fallen in thesame period EQU measures the reduction in deductible losses resulting from the “equalizer.” In this case it isdefined as the reciprocal of the ratio of the “equalized” tax liabilities to ordinary realization based taxes. WhenEQU is greater than one, investors have an incentive to realize their gains or losses and purchase the samesecurity to create a new basis.

EQU

Constant

ObservationsR–squared

All shares with EQU>1b

0.2366(0.1325)[0.076]

–3.6945(0.7647)[0.000]

1370.0012

Shares with EQU > 1and with terminalvalue higher than

value at 01/July/1998

0.4579(0.1764)[0.011]

–4.1122(1.022)[0.000]

1020.0109

Shares with EQU > 1and with terminalvalue lower than

value at 01/July/1998

0.0380(0.0670)[0.575]

–2.9432(0.6177)[0.000]

350.0004

NATIONAL TAX JOURNAL

214

losses. When the security had appreciatedthe wash sale reduced the investor tax li-abilities with certainty. In contrast, if theinvestor realizes a capital loss to preventa decrease in deductible losses, theinvestor’s tax liabilities decreased only iflosses could be compensated with realisedgains on other assets.

In order to test whether these resultswere spurious we tested whether the in-dicator variable explained abnormal trad-ing volumes in December 1999. The re-sults were mixed. When the regressionwas run over the entire sample of compa-nies, the coefficient of EQU was positiveand strongly significant. This result sup-ports the conclusion of a spurious corre-lation between “abnormal” trade at endDecember 2000 and the indicator variable.However, by splitting the sample betweenappreciated and depreciated shares, itturns out that the coefficient is weakly sig-nificant (at 5.6 percent probability level)in the first case and strongly significantin the second. These results suggest thatour findings may be in part fortuitous.

THE ITALIAN COMPREHENSIVEINCOME TAX IN PRACTICE

Compliance Costs of Implementing theTax Reform

As we have already mentioned, banksand other financial intermediaries have al-ways played a pivotal role in administer-ing the system of withholding taxes. How-ever, the last five years have witnessed a

broadening of their obligations. Financialintermediaries, in their capacity as pay-ing agents, became responsible for levy-ing withholding taxes on government and(most) corporate bonds, which until thenhad been collected directly from issuers.The reform itself necessitated that finan-cial intermediaries take direct responsibil-ity for running accruals taxation and cal-culating tax liabilities under the “admin-istered account” system.

The trend towards transferring compli-ance costs onto intermediaries is not un-common. It is associated with the central-ization of custody arrangements and the in-creasing role of banks as paying agents insecurities transactions. However, the actualadministrative burden borne by Italian fi-nancial intermediaries and their legal liabil-ity is probably higher than elsewhere andconsidered a positive feature of the tax sys-tem.22 Indeed, lowering compliance costsfor individual taxpayers was viewed as anobjective of the reform and, at the sametime, was aimed at gaining widespread ac-ceptance for the changeover (Ciocca, 1998).

The withholding of taxes by banks andother financial intermediaries in Italy ishighly automated and exhibits consider-able economies of scale. Alworth and Violi(1998) estimate the overall compliancecosts—including the filing costs for cor-porate tax—amounted annually to about210 million or only 1 percent of banks’

operating costs prior to the reform.23 Thebulk of these costs (over 75 percent) arerelated to its agency role on behalf of thetax authorities.24

22 Typically in other countries the role of financial intermediaries is to collect data for foreign tax authorities aswithholding agents. Recent changes in the U.S. practices regarding withholding taxes on non–residents (FormW–8 and applications to become a qualified intermediary) provide a good example of these procedures. TheEU proposal on withholding taxes on interest income and exchange of information would also expand therole of financial intermediaries in the administration of taxes on capital income.

23 This is a relatively small number if compared to the compliance costs for filing personal income taxes oncapital income in most countries (Blumenthal and Slemrod, 1992).

24 Banks indicated that operating as a withholding agent was the most burdensome compliance cost since it wasnot explicitly remunerated. Taxpayers (individuals and corporate entities) can use bank branches to pay alltaxes (checks are not accepted by the tax authorities). While there is an explicit charge for this service, bankscan offset part of this burden by benefiting from the lag between the time of withholding and the actualpayment of tax. ABI (the Italian Bankers Association) has argued that the role of banks as withholding agentsfor the tax authorities should be remunerated and subject to an explicit contract since these implicit revenuesvary according to the interest rate cycle and are extremely different across banks.

Adjusting Capital Gains Taxation in Italy

215

Unfortunately, no independent studyhas been carried out after the Reform butit is clear that the introduction of accrualstaxation and the “equalizer” has involveda considerable upgrading of systems andgreater maintenance of databases particu-larly in respect of less liquid and non–listed securities (including foreign mutualfunds). A small informal survey carriedout by the authors across some large bankssuggests that the burden of implement-ing this new system (information systemsupgrading, etc.) can be estimated atroughly 200 million, a not insignificantamount considering that parts of the taxhave now been repealed.

The Demise of the “Equalizer” and theFuture of “Accruals Taxation

Shortly after the elections, on Septem-ber 21, 2001 the new Italian Governmentapproved a decree that inter alia abolishedthe “equalizer.” The “equalizer” had ac-tually already been suspended on August4, 2001 (seven months after its introduc-tion) following a judgement by a regionalAdministrative Tribunal (TAR of Lazio)awaiting appeal that had ruled in a caseof constitutionality brought to the courtby the national consumer association.

The considerable hostility encounteredby the “equalizer” prior to its introduc-tion resulted in a two–year delay in imple-mentation. The delayed introduction ofthe new tax, a number of misperceptionsregarding the functioning of the tax andthe rapid build–up of strong “anti–equal-izer” lobbies helped to erode any politi-cal support for a tax that was increasinglyperceived to be inequitable, expensive,and inefficient.

Without discussing the merits of eachargument presented—which often re-flected the positions of rather narrow in-

terest groups—it is useful to provide abrief summary of the various viewpointsagainst the “equalizer.” Many have ar-gued that the formulae for the “equalizer”were not very transparent for taxpayers(De Nicola, 2001) or in practice unneces-sary—“why aim for perfection?” (Piazza,2001). In hindsight, the existence of threedifferent types of calculation may havebeen an important factor triggering thesecriticisms. Opposition to the possibilitythat taxes might be payable even if real-izations resulted in a loss was also voiced(Panzeri, 2002). Furthermore, a ministerof the current government (Prof.Marzano) and a number of tax lawyersargued that the “equalizer” was in breachof Article 53 of the Italian Constitution,which states that taxes should be basedon “effective” or “real” ability to pay.

Criticisms of the reform have not beenlimited to the “equalizer.” The currentgovernment appears to have been con-cerned with the “originality” of accrualstaxation and the “equalizer.”25 The intro-ductory document to the new proposedtax law argues that the equalizer and ac-cruals taxation present a competitive dis-advantage because Italy is the only coun-try to have such a regime in the EU. Forexample, although foreign investors inItalian mutual funds would be rebatedany taxes that have been accrued on thefund, income would not be capitalizedgross of tax and moreover the rebatingarrangement is quite cumbersome for fi-nancial intermediaries. Accruals taxationis also faulted with having been an ex-tremely volatile source of revenues. As wehave already seen, in rising markets ac-cruals taxation has generated very sizablerevenues, but the recent prolonged periodof market decline has given rise to a recordvolume of tax credits. The most immedi-ate effect of these credits has been to post-

25 The current government has also supported many of the changes introduced by the Visco Reforms of 1997–98.In particular, it has indicated that it wishes to maintain the role of financial intermediaries as withholdingagents. The Minister of the Economy is also on record as wishing to abolish the distinction between capitaland other income and as seeking to introduce a single uniform rate of tax for capital income.

NATIONAL TAX JOURNAL

216

pone the changeover to a generalized re-gime of taxing capital gains on a realiza-tion basis that the current Minister of theEconomy is on record as favoring. Theaccumulation of tax credits has also beena major concern for a number of mutualfunds since in some instances such cred-its have exceeded 50 percent of assets. Inthese circumstances, if investors raise theirredemptions beyond a certain level themutual funds could become insolvent(Panzeri, 2002).

Abolition of the accrual regime on man-aged accounts has not encountered thesame level of support as the ending of the“equalizer.” Assogestioni (the Italian Mu-tual Fund Association) appears to back thegovernment on the grounds that domes-tic Italian funds are discriminated,whereas ABI has argued that “accruals”taxation should be retained because it has“encountered wide acceptance amongstthe public” and “banks have incurred sub-stantial costs to implement the system.”At the same time ABI has argued that “ac-cruals” should not be considered the “tax”benchmark.

A “Comprehensive” Income Tax?

The Italian reform of 1998 is in manyrespects the most serious attempt to ap-proximate a comprehensive income tax,albeit within a “dual income” framework.However, an overall assessment of its ap-plicability elsewhere must take into ac-count some specific Italian institutionalfeatures.

First and foremost, the regime wasbased on rates that are independent of thetax status of individual taxpayers. Withthe operating income concept and theretrospective capital gains tax, financialintermediaries tax each specific account

without any reference to other sources ofincome. This means that an individualtaxpayer may not always be able to offsetfully gains on one account against losseson another. More significantly, progressiverates are not applicable to capital incomeand the concept of income is not fullycomprehensive in the sense that labor in-come and capital income are not addedtogether. Furthermore, potential issues ofequity that might arise in respect of thetiming of gains are non–existent with pro-portional tax rates. It should also be notedthat valuation problems are sidesteppedby concentrating on traded financial in-struments for which purchase and salesprices can be easily determined.

Second, Italian tax rates on capital in-come are very low by international stan-dards. It is not clear whether an accrualregime would have been acceptable iftaxes had been significantly higher. In-deed, the opposition to the “equalizer” onthe grounds that taxes may be levied evenif gains have not been realized suggests ahigh sensitivity to the level of tax rates.

Third, the concept of “operating in-come” is not truly comprehensive: deduc-tions for interest payments are limited,income from owner occupied housing issubject to a special regime and gains andlosses on real estate are not consideredunder the income tax and no adjustmentis allowed for inflation.26

Finally, implementing the Italian systemwas most likely possible because compli-ance costs are borne almost fully by finan-cial intermediaries and are relatively lowbecause of the economies of scale associ-ated with bulk processing. It is not clearwhether intermediaries in other jurisdic-tions would be willing to shoulder thisburden.27 Reliance on financial intermedi-aries has also come at the cost of a “one

26 Given the short existence of the present regime, it is not clear whether these separate regimes may haveresulted in resource allocation distortions. One may surmise that the current low rates of tax are not likely tohave led to major distortions.

27 The Italian Banking Association is now arguing that the cost of upgrading banks’ information systems to copewith further changes in the taxation of financial instruments should be borne by the government.

Adjusting Capital Gains Taxation in Italy

217

size fits all” approach. Transactions out-side of broadly defined categories are inmany instances tax discriminated. In par-ticular, this applies to assets held in for-eign bank accounts, collective investmentvehicles not covered by EU directives, orfinancial instruments whose returns donot fit neatly into the scheme foreseen bythe law (such as venture capital funds).Tax discrimination in this instance oftentends to take the form of encouragingdomestic over financial intermediation.Qualified or dominant shareholdings areanother significant form of investmentincome that is tax discriminated for rea-sons that have no bearing with the “com-prehensive income tax” concept.28

The Italian experience also providessome interesting lessons for the taxationof cross–border capital flows. The appli-cation of tax on accruals at source withinindividual accounts—particularly mutualfunds—is not currently compatible withexisting double tax treaty practices, whichtend to distinguish between dividendsand interest on the one hand and capitalgains on the other. In other words, the 12.5percent tax on accruals is not consideredby the tax authorities of the country ofresidence of foreign investors in Italianmutual funds as a withholding tax on asource of income that can give rise todouble taxation relief.29

CONCLUSIONS AND PROPOSALS

The Italian tax reforms have been veryshort–lived and it is difficult to drawmany conclusions regarding the workingof capital markets and the behavior of in-vestors. The introduction of accrualsbased taxes was accompanied by a num-ber of developments that contributed tovery significant adjustments in portfolios.

Unfortunately even event studies do notappear to provide much information be-cause the “equalizer” never actually cameinto effect. The conclusions one can drawfrom this experience must consequentlybe of a different type.

The Italian Tax Reform of 1998 isillustrative of the difficulties that any at-tempt to implement a close variant of theHaig–Simons concept of “comprehen-sive” income taxation has to face. Thesolution found by the Italian authoritiescombined several peculiar features of thetax system:

(a) a “dual income tax” regime whereincome from capital and capitalgains are taxed at proportional rates;

(b) very low tax rates on income fromcapital and capital gains;

(c) taxation upon accrual for managedaccounts and retrospective capitalgains taxation on individual ac-counts;

(d) compliance costs borne largely byfinancial intermediaries.

At first sight, all these elements seemessential for the coherence of the overallconstruction and may limit the appeal ofthe “Italian model” of taxing capital in-come for other countries. Most of thedrawbacks commonly imputed to accrualbased taxation (such as liquidity problemsthat could force taxpayers to dispose theassets in order to pay tax) appear to havebeen of second order importance in theItalian context due to the low level of taxrates. These issues will arise more force-fully in a tax system where capital incomeis taxed at high and progressive tax rates.Furthermore, in such a framework itwould be quite hard to defend limitationson the deductibility of capital losses from

28 Some may argue that the “ability to pay” concept should be interpreted in an extensive fashion as “power”over resources. “Accumulations of wealth confer valuable economic and social benefits to their owners evenif the wealth is not consumed” (Aaron and Galper, 1985).

29 Relief is typically available for withholding taxes on dividends and interests. This has led the Italian authori-ties to introduce a complex system of refunding tax for foreign investors.

NATIONAL TAX JOURNAL

218

other sources of income. This in turnwould raise concerns on the effective yieldof the tax.