whitepaper: from resistance to partnership: operators shift into monetising ott

TRANSCRIPT

From Resistance to PartnershipOperators shift into monetising OTT

A whitepaper by Sponsored by

November 2014

INTRODUCTION 1 EXECUTIVE SUMMARY 2

PART 1: THE NOW• The exponential growth of OTT communications 6 • Haven’t we heard this all before? 7• Operator revenue 8• OTT subscribers becoming more plentiful 9 PART 2: THE NEXT BILLION • The next billion OTT communication users 11• All eyes on WhatsApp 12• Can Messenger beat WhatsApp to 1 billion users? 13• Mobile operator OTT epiphany 14• Mobile operators embracing OTT 15• Joyn remains mobile operator enigma 16• Mobile operator growth point: A2P traffic 17• Partnering 17• Privacy issues 18• The changing face of communications 19• A level playing field 19

PART 3: THE MOBILE OPERATOR OPPORTUNITY• Analysis 21• Business models 22• OTT communication forecasts 23 CONCLUSION 24APPENDIX 25METHODOLOGY 26ABOUT tyntec & mobilesquared

Table of Contents

INTRODUCTION

INTRODUCTION | PAGE 1

This is the third White Paper focusing on the impact of OTT communications, such as WhatsApp, LINE, WeChat and Skype, on the mobile operator business model. The first White Paper, OTT Services: How Operators can overcome the Fragmentation of Communication, was released in 2012, followed by OTT Blows Up the Mobile Universe. Operators Must Act Now!, in 2013.

Much has happened since the release of the last White Paper 12 months ago. Viber was purchased by Rakuten for $900 million in February 2014, only to have the deal overshadowed days later by Facebook’s $19 billion acquisition of WhatsApp.

The rest of 2014 has been played out by OTT communications providers jostling to become the “next WhatsApp”, striving to unlock a viable business model from an exponentially-increasing global community. WhatsApp remains the only OTT communications app to offer a subscription model. But the likes of LINE, WeChat, and Kakao have expanded beyond OTT communications to become social media platforms generating revenues from commerce and advertising. But as O2 inadvertently proved when trying to introduce NTT DoCoMo’s content delivery platform i-mode into Europe almost a decade ago, business models from Asia do not always export successfully.

While the majority of OTT communications providers concentrate on growing their community and exploring business models, this provides an opportunity for mobile operators to play an integral role and re-emerge as a force in the monetisation process of OTT communications.

Mobilesquared forecasts OTT communications users to more than double over the next 4 years. The OTT communications land-grab is not even at the halfway stage. But to capitalise on this opportunity, mobile operators must become smart faster and become an integral component of the OTT model beyond simply providing the bandwidth, while the OTT communications providers must become smart and incorporate the mobile operators into their monetisation model if they are to fulfil their commercial realisation.

This White Paper explores and outlines the OTT communications opportunity for mobile operators, and why it’s not too late to get in on the market dominated by start-ups and upstarts.

The OTT communications community is moving towards a revenue generation model as opposed to capturing high-market capitalisation, and could be conceived as being representative of a maturing of the marketplace. This means in the near term, greater pressure will be exerted on OTT communications providers to drive revenues, and not just increasing their global footprint. Conversely, this heightened pressure could force the OTT communications providers to seek partnerships with mobile operators, as a tactical move designed to speed the commercial realisation of the service. This would represent a significant development in the communications marketplace and would start the realignment of mobile operators within the next-generation of (OTT) communications.

Mobilesquared believes this will result in a period of convergence between mobile operators and OTT communications providers. This will be driven by two factors.

Firstly, there has been a significant shift in mobile operator mindset regarding OTT communications. The perception that OTT communications is a threat has been replaced with a revenue-generating opportunity. Mobile operators have never been more open and receptive to the notion of partnering with OTT communications providers, and to this end, OTT communications providers must look to exploit this opportunity.

Secondly, the need for OTT communications providers to monetise their community. Driving this commercialisation will be a period of maturation throughout OTT communications providers as their

model evolves beyond pure community-driven user acquisition, to revenue generation and user acquisition. The need to partner is compounded by the fact OTT communications providers have little or no user information or data, and mobile operators have customer data in abundance, and limited or no billing capability.

WHAT THE RESEARCH TOLD USThe research revealed that 97.6% of mobile operators will potentially enter into an OTT communications partnership. By removing those mobile operators that have entered into a partnership already, this leaves 75% of mobile operators that are looking to enter into a partnership. Or an alternative view is that 59% of mobile operators looking to partner with an OTT communications provider do not want to partner with Facebook and/or WhatsApp, even though a similar number would like to provide a WhatsApp-like experience to their customers. Of the mobile operators who have partnered with OTT communications providers already (23.8%), 58% of these mobile operators have partnered with Facebook and/or WhatsApp, with the remaining 42% entered into partnerships with alternative OTT communications providers. In total, just under 40% of mobile operators would like to partner with Facebook and/or WhatsApp.

Not surprisingly, 58.5% of mobile operators said WhatsApp would be the OTT communication service they would most like to provide to their customers, primarily because of its scale. But mobilesquared research reveals that Facebook Messenger is the

PAGE 2 | EXECUTIVE SUMMARY

EXECUTIVE SUMMARY

most likely OTT messaging app to reach 1 billion users – days ahead of WhatsApp.

SOURCE: MOBILESQUARED

Although 80% of mobile operators said that decreasing revenues and margins on traditional offerings is their most pressing concern in 2014, the same figure believe they can generate revenue from OTT communication services. A breakdown of that figure reveals that 22% believe OTT will generate additional revenues, 27% believe the additional revenues will come at the expense of voice and SMS revenues, and 31% believe additional revenues will be generated via partnerships.

SOURCE: MOBILESQUARED

Yes – OTT will generate additional revenues for mobile operators

Yes – but at the expense of voice and SMS revenues

Yes – OTT will generate additional revenues for mobile operators via partnerships

No

Undecided

The primary expectation of mobile operators for partnering with an OTT service provider was to drive customer loyalty, according to 71% of respondents. Equally, 34% of mobile operators said it would be to develop an OTT subscription model and/or use as a marketing platform, while the up-sale of content would appeal to 16% of mobile operators.

More than two-thirds of mobile operators (69%) would be willing to assist OTT communications providers to verify private user information, with 37% of total respondents using the data to authenticate a user’s identity, and 31% to ensure compliance with the mobile operator provided a system was in place. Mobile operators would be willing to monetise gender, age, location, behaviour and preferences.

The majority of mobile operators believe that partnering with specific OTT providers to charge for data is the clearest OTT monetisation model. However, 42% of mobile operators believe that terminating IP traffic onto a mobile network also presents a clear monetisation opportunity. Mobile operators are a little more sceptical when it comes to monetising their own branded OTT app, appealing to 25% of respondents. But that was more popular than the rental of virtual mobile phone numbers (i.e. without SIM cards) (14%).

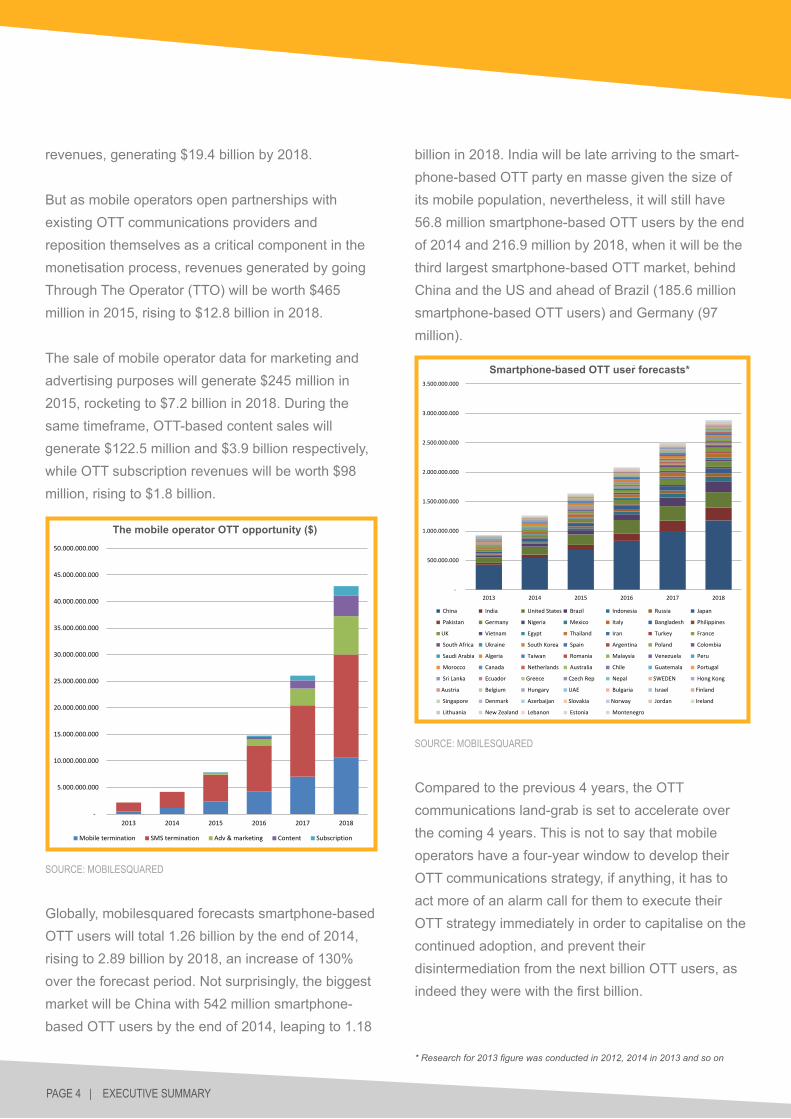

Mobilesquared forecasts that the global mobile operator opportunity for OTT communication will be worth $42.9 billion in 2018, an increase from $4.2 billion in revenues in 2014.

OTT off-net communication termination for voice and messaging will account for $4.2 billion in 2014, and leap to $30 billion in 2018 as mobile operators partner with OTT communications providers and open their networks to terminate traffic. OTT off-net messaging termination will represent the majority of

EXECUTIVE SUMMARY | PAGE 3

The race to 1 billion

Do you believe operators can generate revenue from OTT services?

22,2%

26,7%31,1%

11,1%

8,9%

revenues, generating $19.4 billion by 2018.

But as mobile operators open partnerships with existing OTT communications providers and reposition themselves as a critical component in the monetisation process, revenues generated by going Through The Operator (TTO) will be worth $465 million in 2015, rising to $12.8 billion in 2018.

The sale of mobile operator data for marketing and advertising purposes will generate $245 million in 2015, rocketing to $7.2 billion in 2018. During the same timeframe, OTT-based content sales will generate $122.5 million and $3.9 billion respectively, while OTT subscription revenues will be worth $98 million, rising to $1.8 billion.

SOURCE: MOBILESQUARED

Globally, mobilesquared forecasts smartphone-based OTT users will total 1.26 billion by the end of 2014, rising to 2.89 billion by 2018, an increase of 130% over the forecast period. Not surprisingly, the biggest market will be China with 542 million smartphone- based OTT users by the end of 2014, leaping to 1.18

billion in 2018. India will be late arriving to the smart-phone-based OTT party en masse given the size of its mobile population, nevertheless, it will still have 56.8 million smartphone-based OTT users by the end of 2014 and 216.9 million by 2018, when it will be the third largest smartphone-based OTT market, behind China and the US and ahead of Brazil (185.6 million smartphone-based OTT users) and Germany (97 million).

SOURCE: MOBILESQUARED

Compared to the previous 4 years, the OTT communications land-grab is set to accelerate over the coming 4 years. This is not to say that mobile operators have a four-year window to develop their OTT communications strategy, if anything, it has to act more of an alarm call for them to execute their OTT strategy immediately in order to capitalise on the continued adoption, and prevent their disintermediation from the next billion OTT users, as indeed they were with the first billion.

PAGE 4 | EXECUTIVE SUMMARY

-

5.000.000.000

10.000.000.000

15.000.000.000

20.000.000.000

25.000.000.000

30.000.000.000

35.000.000.000

40.000.000.000

45.000.000.000

50.000.000.000

2013 2014 2015 2016 2017 2018

Chart Title

Mobile termination SMS termination Adv & marketing Content Subscription

The mobile operator OTT opportunity ($)

* Research for 2013 figure was conducted in 2012, 2014 in 2013 and so on

-

500.000.000

1.000.000.000

1.500.000.000

2.000.000.000

2.500.000.000

3.000.000.000

3.500.000.000

2013 2014 2015 2016 2017 2018

Smartphone-based OTT user forecast

China India United States Brazil Indonesia Russia Japan

Pakistan Germany Nigeria Mexico Italy Bangladesh Philippines

UK Vietnam Egypt Thailand Iran Turkey France

South Africa Ukraine South Korea Spain Argentina Poland Colombia

Saudi Arabia Algeria Taiwan Romania Malaysia Venezuela Peru

Morocco Canada Netherlands Australia Chile Guatemala Portugal

Sri Lanka Ecuador Greece Czech Rep Nepal SWEDEN Hong Kong

Austria Belgium Hungary UAE Bulgaria Israel Finland

Singapore Denmark Azerbaijan Slovakia Norway Jordan Ireland

Lithuania New Zealand Lebanon Estonia Montenegro

Smartphone-based OTT user forecasts*

In 2014, every mobile operator included in the research said OTT communications were now being used by at least 1% of their customer base. In fact, 56% of respondents said that between 1% and 50% of their customer base were using OTT communi-cations, with 26% of respondents claiming that over 51% of their customer base was using OTT communications.

Mobilesquared predicts it will takes less than 2 years until over 50% of mobile operators will experience 80% of their customer base using OTT communications.

SOURCE: MOBILESQUARED

0,0% 5,0% 10,0% 15,0% 20,0% 25,0%

0%

1-5%

6-10%

11-20%

21-30%

31-40%

41-50%

51-60%

61-70%

71-80%

>81%

Don’t know

2015

2014

EXECUTIVE SUMMARY | PAGE 5

What percentage of your customers will be using OTT communications in 2014 and 2015

subscription rate is attached. At $0.99 per year applicable after the first year, WhatsApp’s annual cost is negligible to the user.

SOURCE: MOBILESQUARED

But the WhatsApp subscription model has severe revenue-generating limitations compared to alternative OTT messaging apps. Japan-based OTT messaging app LINE’s 300 million users generated revenues of $338 million in 2013 from games, stickers and advertising. In 1Q2014 its revenues were $145 million up from $64 million for the same period the previous year.

Similarly, WeChat generated $330 million in revenues in 2013 from games, stickers and commerce. While Kakao generated revenues of $203 million in 2013 from games (84%) and advertising (14%).

Kakao moved into mobile money in June 2014, allowing users to send and receive money following partnerships with the South Korean banks. In October 2014, LINE also jumped on the mobile money bandwagon as part of a broader initiative to extend its engagement with users.

0

200.000.000

400.000.000

600.000.000

800.000.000

1.000.000.000

1.200.000.000

1.400.000.000

1.600.000.000

Jun

Oct

Feb

Jun

Oct

Feb

Jun

Oct

Feb

Jun

Oct

Feb

Jun

Oct

Feb

Jun

Oct

Feb

Jun

Oct

Feb

Jun

Oct

Feb

Jun

Oct

2009 2010 2011 2012 2013 2014 2015 2016 2017

WhatsApp users and revenues ($)

Revenues

TOTAL USERS

PART 1: THE NOW

THE EXPONENTIAL GROWTH OF OTT COMMUNICATIONSOver the last 12 months OTT communications has become a numbers game with WhatsApp heading the field. On its existing growth trajectory of 800,000 new users per day, it is on course to join Facebook in the Billionaire’s Club in January 2016. Rival OTT messaging app LINE too has ambitions of hitting 1 billion users, but its 510 million users trails WhatsApp’s 660 million users and its daily uptake is considerably lower. Then there is LINE with 490 million global users, WeChat with 440 million, as well as the likes of Snapchat with over 100 million users, to name just a few of the OTT messaging apps available. And they all have one thing in common: becoming the next WhatsApp. Or, becoming what WhatsApp could have become if it had developed a monetisation model beyond just subscriptions, such as advertising, or commerce (content and games). The industry baulked at the $45 Cost Per User (CPU) Facebook paid WhatsApp, but that figure is already towered by Snapchat’s CPU of $100 CPU based on no revenues. This is just the beginning.

Given that Facebook paid a staggering $19 billion for a company that generated revenues of $133.1 million in 2013 and is not expected to generate in excess of $1 billion annual revenues until 2017, the OTT communications playing field has become community driven over monetisation.

As WhatsApp can testify, it is significantly easier to build a community when a product or service is free, or perceived to be free, than it is when a monthly

PAGE 6 | PART 1: THE NOW

Fig 1. WhatsApp users and revenues ($) 1

1 Mobilesquared estimates

LINE Pay allows users to make purchases via their mobile or PC using either a credit card or prepaid card, as well as letting users split the purchase across LINE friends via a Share Payment facility. Users will also be able to send payments to other users. The LINE app will also soon be able to book and pay for cab rides, not to mention the launch of the LINE WOW food delivery service in conjunction with South Korean food delivery app Woowa Brothers.

Like Kakao and WeChat, LINE too is evolving into more of a social media platform, a closed community, or as more commonly referred to in the mobile industry, a walled garden, designed to keep as many people engaged on the platform for as long a period as possible, with the ultimate goal of spending more money.

Over the last 10-15 years, the majority of mobile operators deployed a walled garden content model, but the only truly successful model was Japanese mobile operator NTT DoCoMo’s i-mode platform. Walled gardens have since become synonymous with mobile operators and failure. Yet, iTunes is effectively a walled garden that has served Apple very well. Walled gardens can be a success with scale. iTunes has a global footprint, as indeed, do the majority of OTT messaging apps. But as the mobile operators found out to their detriment, creating a model that overcomes language and cultural barriers, local content, price differentiation, to name a few of the hurdles, is going to be one of the challenges facing the global OTT communications platform providers moving forward.

Nevertheless, LINE is intent on growing its business and pushing up its existing market capitalisation of $30 billion, a figure which starts to add context to the WhatsApp deal in line with the rest of the

marketplace. But then Snapchat, some 12 months after rejecting Facebook’s offer of $3 billion, is now reportedly worth $10 billion, based on its 100 million users and zero revenues. Snapchat’s cost per user (CPU) of $100 is more than double the $42 CPU Facebook paid WhatsApp. Snapchat’s CPU could be set to receive a significant injection following the company’s introduction of advertising in October 2014.

This is perhaps the first step for the OTT communications community to move towards a revenue generation model as opposed to capturing high-market capitalisation, and could be conceived as being representative of a maturing of the marketplace. This means in the near term, greater pressure will be exerted on OTT communications providers to drive revenues, and not just increasing their global footprint. Conversely, this heightened pressure could force the OTT communications providers to seek partnerships with mobile operators, as a tactical move designed to speed the commercial realisation of the service. This would represent a significant development in the communications marketplace and would start the realignment of mobile operators within the next- generation of (OTT) communications.

HAVEN’T WE HEARD THIS ALL BEFORE?Regardless of who will be driving the partnership between mobile operator and OTT communications provider, the immediate impact of OTT communications continues to reverberate throughout the mobile operator community. Four-fifths (80%) of mobile operators said that decreasing revenues and margins on traditional offerings is their most pressing concern in 2014. This was followed by exploring new revenue generating opportunities (33%), such as mHealth and connected devices, and regulatory issues (22%), like roaming and Net

PART 1: THE NOW | PAGE 7

Neutrality. The continued surging growth of OTTs was only a pressing concern for 19% of mobile operators, with 11% of respondents also stating their inability to partner with, and monetise, OTT communications.

SOURCE: MOBILESQUARED

In recent years, the OTT communications research by mobilesquared has not only tracked the exponential growth rate of OTT communication apps, but monitored the mobile operator mindset towards these rival services, ultimately replacing churn as their greatest concern. In 2014, the latest research suggests that the continued surging growth of OTTs has now become accepted within mobile operators, whom in turn, are now focused on addressing decreasing revenues and margins on traditional telecoms offering, albeit a direct result of OTT communications. But rather than just identifying the cause, by focusing on the impact – the decreasing revenues and margins on traditional telecoms offerings – the mobile operators are demonstrating a newfound understanding of what needs addressing. Indeed, included within the category of “exploring new revenue generating opportunities”, alongside mHealth and connected devices inevitably sits OTT communications and partnerships.

While OTT communications have started the deconstruction of traditional communications, it is

now incumbent on the mobile operators to reinvent themselves, and reinvigorate the communications marketplace by grappling communications control back from the start-ups and upstarts. After all, users pay the bulk of their communication fees to their mobile operators – something that has become overlooked among the hullabaloo surrounding OTT communications: If communications is becoming a subset of data, the logical next step for mobile operators would be to introduce a data communications package to complement the data package? Presently, the majority of OTT communications providers are yet to demonstrate a commanding monetisation model. So why can’t mobile operators make their move now? After all, their revenues have taken something of a pounding in recent years.

OPERATOR REVENUE As stressed in the 2013 research, mobile operators must act fast, and 12 months on is no different. Forty percent of mobile operators included in this year’s research said that OTT communications had attributed to a decrease in revenues over the last 12 months, 16% said revenues had increased and 44% said they didn’t know. Almost three quarters of those mobile operators that had experienced a decline in revenues over the last 12 months claimed that figure was between 0% and 10%, with the remaining mobile operators citing revenue declines of between 11% and 20%.

Compared to previous years when the research focused purely on decreases in mobile operator revenue, this latest data suggests mobile operators are starting to limit the impact OTT communications has on their revenues, or at least they are starting to manage the decreases more effectively. In 2013, 14% of mobile operators claimed revenues were down more than 21% as a direct consequence

PAGE 8 | PART 1: THE NOW

Fig 2. What is the most pressing concern for you as an operator? (Multiple choice)

PART 1: THE NOW | PAGE 9

of OTT communications, but this year the maximum reduction was between 16% and 20% for 5% of respondents. However, year-on-year, more mobile operators (33% of total respondents) are now being impacted by up to a 10% revenue decline, up from 21% of mobile operators in 2013, which does confirm the impact of OTT communications on mobile operators is becoming more far-reaching.

SOURCE: MOBILESQUARED

Despite an increasing number of mobile operators experiencing a decline in revenues as a direct result of OTT communications activity, the extent to which the declines are affecting their revenues appears to be diminishing. It is unlikely that the extent of the impact of OTT communications on mobile operator revenues has hit rock-bottom, but this does suggest that the impact has started to stabilise. How long this will last remains to be seen, but it is yet another indicator that mobile operators need to develop a strategy to respond to the situation urgently.

OTT SUBSCRIBERS BECOMING MORE PLENTIFULPerhaps the biggest indicator that mobile operators need to develop a strategy to respond to the rise of OTT communications rapidly is the fact that their customers are using OTT apps in their droves.

The cliché in business is that you need to be where

your customers are. The emergence of Facebook resulted in businesses developing Facebook pages. The rise of Twitter and Instagram have sparked businesses to open accounts on each respective service to connect with users. Yet the advent of OTT communications has prompted the majority of mobile operators to follow the much-maligned “Ostrich Movement” – and bury their head in the sand!

In 2014, every mobile operator included in the research said OTT communications were now being used by at least 1% of their customer base. In fact, 56% of respondents said that between 1% and 50% of their customer base were using OTT communications, with 26% of respondents claiming that over 51% of their customer base was using OTT communications.

When asked what percentage of their customer base would be using OTT communications in 2015, 37% of respondents expected between 6% and 50%, while 50% of respondents expected over 51% of their customer base. In 2014, 6.5% and 2.2% of respondents believed that 71-80% and over 81% respectively of their customer base was using OTT communications. Jump forward 12 months, and that figure is expected to leap to 11% and 22% respectively. That means more than one fifth of mobile operators anticipate over 80% of their customer base using OTT communications by the end of 2015.

Clearly mobile operators are not expecting the deepening penetration of OTT communications amongst their customer base to appease any time soon, and based on the trends emerging from the 2014 research, mobilesquared expects it will take less than 2 years until over 50% of mobile operators will experience 80% of their customer base using OTT communications.

5,4%

0,0%2,7% 2,7%

0,0%

27,0%26,3%

5,3%

10,5%

0,0%0,0%

26,3%

14,3%

7,1% 7,1%

14,3%

21,4%20,9%

11,6%

2,3%4,7%

0,0%

44,2%

0,0%

5,0%

10,0%

15,0%

20,0%

25,0%

30,0%

35,0%

40,0%

45,0%

50,0%

0-5% 6-10% 11-15% 16-20% >21% Don’t know

Fig. 3 Over the last 12 months what percentage of your operator revenues have decreased because of OTT

communications?

2011

2012

2013

2014

Fig 3. Over the last 12 months what percentage of your operator revenues have decreased because of

OTT communications?

communications alternative, and has to be taken as a serious emerging business model opportunity for mobile operators.

SOURCE: MOBILESQUARED

0,0%

10,0%

20,0%

30,0%

40,0%

50,0%

60,0%

0% 1-5% 6-10% 11-20% 21-30% 31-40% 41-50% >51%

Chart Title

2013 2014 2015

PAGE 10 | PART 1: THE NOW

Compared to the research findings from previous OTT communications research, there have been some dramatic changes in mobile operator expectations over the last 3 years.

When the research asked mobile operators in 2012 their expectations for 2013, they were clearly expecting between 6% and 30% of their customer base to be using OTT communications. The following year expectations altered to reflect a new wave of mobile operators’ customers adopting OTT communications (ie 36% of mobile operators expected 1% to 5% of their customers using the services), while 22% of mobile operators expected OTT communication penetration to surpass 50%.

SOURCE: MOBILESQUARED

The research conducted this year reveals that 50% of mobile operators expect over 51% of their customers using OTT communications by the end of 2015. It’s confirmation that OTT communications can no longer be viewed as a passing fad that will disappear over time, and now represents a truly global

Fig 5. What percentage of your subscribers will be using OTT communications next year?*

* Research for 2013 figure was conducted in 2012, 2014 in 2013 and so on

0,0% 5,0% 10,0% 15,0% 20,0% 25,0%

0%

1-5%

6-10%

11-20%

21-30%

31-40%

41-50%

51-60%

61-70%

71-80%

>81%

Don’t know

2015

2014

Fig 4. What percentage of your customers will be using OTT communications in 2014 and 2015

PART 2: THE NEXT BILLION

Connecting the next billion users to affordable internet access is the ambition of Internet.org, a global partnership between technology leaders, nonprofits, local communities and experts.

Mobile networks (2G/3G/4G) cover almost 80% of the world’s population, but only one-third of the population are connected, according to Internet.org. And with the $25 smartphone, devices have become significantly more affordable, which means mobile operators will be facing increased pressure on data plan pricing in the coming years to make internet access more affordable throughout the developing world and connect the next one, two, even three billion users. What’s interesting with the next 2 or 3 billion internet users, is that not only will their primary device for accessing the internet be mobile, but as a consequence of their internet education from the likes of Facebook and WhatsApp via Internet.org, OTT communications will realistically be their primary form of communication.

This potentially means that the next 2-3 billion internet users could go directly onto OTT services for their communication, and ultimately create an even greater threat to mobile operator revenues than have been experienced to date. Unless of course, the mobile operators can get their OTT strategy aligned in the foreseeable future.

THE NEXT BILLION OTT COMMUNICATION USERSGlobally, mobilesquared forecasts smartphone-based OTT users will total 1.26 billion by the end of 2014,

rising to 2.89 billion by 2018, an increase of 130% over the forecast period. Not surprisingly, the biggest market will be China with 542 million smartphone- based OTT users by the end of 2014, leaping to 1.18 billion in 2018. India will be late arriving to the smartphone-based OTT party en masse given the size of its mobile population. Nevertheless, it will still have 56.8 million smartphone-based OTT users by the end of 2014 and 216.9 million by 2018, when it will be the third largest smartphone-based OTT market, behind China and the US and ahead of Brazil (185.6 million smartphone-based OTT users) and Germany (97 million).

SOURCE: MOBILESQUARED

Compared to the previous 4 years, the OTT communications land-grab is set to accelerate over the coming 4 years. This is not to say that mobile operators have a four-year window to develop their

PART 2: THE NEXT BILLION | PAGE 11

*Research for 2013 figure was conducted in 2012, 2014 in 2013 and so on

-

500.000.000

1.000.000.000

1.500.000.000

2.000.000.000

2.500.000.000

3.000.000.000

3.500.000.000

2013 2014 2015 2016 2017 2018

Smartphone-based OTT user forecast

China India United States Brazil Indonesia Russia Japan

Pakistan Germany Nigeria Mexico Italy Bangladesh Philippines

UK Vietnam Egypt Thailand Iran Turkey France

South Africa Ukraine South Korea Spain Argentina Poland Colombia

Saudi Arabia Algeria Taiwan Romania Malaysia Venezuela Peru

Morocco Canada Netherlands Australia Chile Guatemala Portugal

Sri Lanka Ecuador Greece Czech Rep Nepal SWEDEN Hong Kong

Austria Belgium Hungary UAE Bulgaria Israel Finland

Singapore Denmark Azerbaijan Slovakia Norway Jordan Ireland

Lithuania New Zealand Lebanon Estonia Montenegro

Fig. 6 Smartphone-based OTT user forecasts*

SOURCE: MOBILESQUARED

Interestingly, the impact on how mobile operators perceive WhatsApp lessens when associated with Facebook to the extent that Facebook’s purchase of WhatsApp has not sparked the seismic shift in the OTT communications landscape one might have expected.

The mobile operator research in 2013 revealed only 7% of mobile operators believed Facebook posed a challenge to their revenues, with almost two-thirds of mobile operators believing Facebook – and specifically Facebook Home – was just another OTT service provider to contend with. Facebook’s lack of a compelling consumer OTT communication offering was further compounded by the fact that not one of the mobile operators surveyed wanted to partner with its OTT service: a messaging failure that conceivably cost the company $19 billion to fix, even though it already had Messenger waiting in the wings. This is in stark contrast to the 36% of mobile operators that said WhatsApp would have the most impact on their revenues in 2013.

This year’s research reveals that 46% of mobile operators believe the combination of Facebook and WhatsApp represent a risk to mobile operator revenues. While that represents a significant leap on last year’s research, the reality is that when

10%2%

5%

17%

2%59%

5%

Chart Title

iMessenger

Facebook Messenger

Google +

Skype

Viber

Snapchat

KakaoTalk

ChatON

OTT communications strategy, if anything, it has to act more of an alarm call for them to execute their OTT strategy immediately in order to capitalise on the continued adoption, and prevent their disintermediation from the next billion OTT users, as indeed they were with the first billion.

ALL EYES ON WHATSAPPAs WhatsApp is viewed by the mobile industry – yet to read this White Paper – as the next platform to potentially reach 1 billion users, it continues to be viewed as the greatest challenge, according to the mobile operators taking part in the 2014 research. Sixty-two percent of respondents identified WhatsApp as the greatest challenge, up from 36% of mobile operators in 2013. Skype was viewed by 20% of mobile operators as the second greatest challenge to their revenues, but it is the messaging revenues that the mobile operators remain most protective of.

Only 4% of respondents identified Facebook Messenger as the greatest challenge to their revenues. Given Messenger’s meteoric rise in downloads since the summer of 2014, mobilesquared predicts mobile operators to label Messenger as the greatest challenge to mobile operator revenues in 2015, replacing WhatsApp.

As part of the 2014 research, when asked which of the OTT services they would most like to provide to their customers, 58.5% of respondents said WhatsApp. WhatsApp was considerably ahead of Skype in second (17% of mobile operators) and iMessenger (10%). The majority of mobile operators selecting WhatsApp cited its popularity as the primary reason.

Again, Facebook Messenger has been overlooked by the mobile operator community as a potential threat, but it really could become the telco industry’s Trojan Horse.

PAGE 12 | PART 2: THE NEXT BILLION

Fig 7. If you could choose any OTT service to provide to your customers, which of the following would you select?

45%

2%

25%

14%

14%The combination of Facebook andWhatsApp represent a risk tooperator revenues

We perceive the partnership ofFacebook and WhatsApp to beirrelevant to the telecom industry

We would like to find out how topartner with them

We already partner with Facebookand/or WhatsApp

We do not believe Facebook andWhatsApp to be any risk to operatorrevenues

combined, Facebook and WhatsApp accounted for 58% of mobile operator responses. If anything, the acquisition has actually nullified the revenue risk posed by the individual companies.

While 14% of respondents from this year’s research adopted the opposing view and selected “no risk”, most telling of all, was that 14% of respondents said that they have already entered a partnership with Facebook and/or WhatsApp, and a further 25% would like to. This means two-fifths of mobile operators would like to partner with Facebook and/or WhatsApp and that certainly fits within Facebook CEO Mark Zuckerberg’s vision of connecting the next billion people.

SOURCE: MOBILESQUARED

CAN MESSENGER BEAT WHATSAPP TO 1 BILLION USERS?One key development since Facebook acquired WhatsApp is that the number of new daily users has slowed considerably. In February 2014, WhatsApp was experiencing over 1 million new users per day, but this figure has subsequently fallen by 200,000 per day, placing the likelihood of the app achieving 1 billion users in January 2016, though if the download rate continues to subside, to push that milestone back until later into the year.

One of the reasons for the slowdown in WhatsApp downloads can be attributed to the sheer amount of choice. In the App Store and Google Play store, there are over 2,300 social networking apps, of which 490 are messaging-based apps. And new apps are emerging on a daily basis, which makes discoverabi-lity a major issue unless you already have over 1 billion users and need a platform to promote your app.

Facebook Messenger is one messaging app that is experiencing an incredible resurgence. When the company announced it was extricating its messaging service from its main app in June 2014, it was only a matter of time until the 1.07 billion Facebook Mobile users started downloading Messenger. In April 2014, Facebook had around 200 million Messenger users amassed in the 3 years since its launch. But from July 2014 the number of daily downloads on both the App Store and Google Play has rocketed past that of WhatsApp.

Mobilesquared estimates that Messenger now has around 350 million global users, growing by over 1 million per day and accelerating. Furthermore, mobilesquared forecasts that if Facebook Messenger can sustain its existing growth for the next 15 months, it will beat WhatsApp to the 1 billion user milestone by a couple of days. It is somewhat ironic that the next WhatsApp will in fact “just be Facebook.”

PART 2: THE NEXT BILLION | PAGE 13

Fig 8. Which of the following statements do you agree with regarding the acquisition of WhatsApp by Facebook and its

impact on mobile operator revenues and OTT usage?

Yes – OTT will generate additional revenues for mobile operators

Yes – but at the expense of voice and SMS revenues

Yes – OTT will generate additional revenues for mobile operators via partnerships

No

Undecided

SOURCE: MOBILESQUARED

For Facebook, Messenger becomes yet another channel boasting more inventory to monetise via advertising. In 2014, mobilesquared predicts Facebook will generate mobile advertising revenues in excess of $6.4 billion, and could account for one-third of total global mobile advertising spend for the year. What does this mean for WhatsApp which remains insistent of its mantra of being an advertising free platform? Well, to date, Zuckerberg has been respectful of WhatsApp’s business model, though he did say at Mobile World Congress 2014 that “the vision is to keep the business exactly the same”; while adding that he wanted to “build a more profitable model”; something of an oxymoron.

For example, LINE and Kakao are monetising their platform at $2-3 per person, and Zuckerberg is confident of achieving similar levels with WhatsApp. How is this possible when the subscription model is $0.99 per user?

It is conceivable, that were Facebook to integrate the WhatsApp platform with Messenger, it could insert an ad into a WhatsApp-to-Messenger-bound message, and maintain its commitment of keeping WhatsApp’s vision of an advertising-free zone and building a more

profitable model. Alternatively, the subscription model is increased to $2-3 per user per annum.

MOBILE OPERATOR OTT EPIPHANYLike Zuckerberg, the mobile operators appear to have had an OTT communications business epiphany, and are now confident of monetising OTT services. The 2014 research has revealed that a staggering 80% of mobile operators believe they can generate revenue from OTT communication services. A breakdown of that figure reveals that 22% believe OTT will generate additional revenues, 27% believe the additional revenues will come at the expense of voice and SMS revenues, and 31% believe additional revenues will be generated via partnerships. Only 11% of respondents said OTT services will not generate revenue for mobile operators, leaving 9% undecided.

SOURCE: MOBILESQUARED

The optimism expressed by mobile operators in 2013 has abated somewhat 12 months later when it comes to OTT services generating additional revenues, with 22% of respondents believing the above statement as compared to 36% last year. However, the concern over the impact of OTT services on voice and messaging revenue appears to be diminishing, with

PAGE 14 | PART 2: THE NEXT BILLION

Fig 9. The race to 1 billion

Fig 10. Do you believe operators can generate revenue from OTT services?

22,2%

26,7%31,1%

11,1%

8,9%

0,0%

10,0%

20,0%

30,0%

40,0%

50,0%

60,0%

Chart Title

2011

2012

2013

2014

27% of mobile operators believing OTT service- based revenues will come at the expense of existing voice and messaging revenues, compared to 29% of respondents in 2013, and significantly lower than the 63% from 2012.

This suggests time has provided something of a healing process for mobile operators since the initial furore of the impact of OTT services on their revenues.

This response also reveals consistency throughout the research by also reiterating the lower-than- expected revenue loss highlighted earlier in this White Paper.

MOBILE OPERATORS EMBRACING OTTBut it is the extent to which mobile operators are starting to embrace OTT communications that is one of the clear findings of the research. Some 87% of mobile operators have recognised upsides associated with increased OTT communication activity of their subscribers. Fifty-six percent of respondents identified an increase in billable data usage, followed by 18% experiencing increased messaging and data usage. Although 11% said they had seen an increase in messaging, data and voice usage, only 2% of respondents selected an increased in messaging only, an increase in voice usage only was not selected.

Increased data usage is, perhaps obviously, the key driver for mobile operators when it comes to OTT services, and subsequently having an increase on messaging and voice. But as standalone services, the positive impact on voice and messaging appears negligible.

There certainly is a sea-change in mindset regarding OTT communications among the mobile operators taking the research this year compared to 2013. Although the amount of mobile operators that experience an increase in messaging has dropped from 7% in 2013 to 2% this year, the remaining comparable responses listed above are possibly the first indicators that mobile operators are not only coming to terms with OTT communications, but starting to capitalise on the opportunity.

SOURCE: MOBILESQUARED

Over the last 12 months the number of mobile operators experiencing an increase in billable data usage as a result of OTT activity has increased from 43% to 56%. Those mobile operators that have experienced an increase in messaging and data usage has increased from 7% to 18%. While most tellingly of all, the number of mobile operators that are yet to identify any upsides from OTT activity fell from 36% to 4%.

In fact, 64% of mobile operators said that the upsides from increased OTT activity by their subscribers were driving their OTT strategy. Presently, 74% of mobile operators have an OTT communications strategy, 21% are without an OTT strategy (based on 14%

PART 2: THE NEXT BILLION | PAGE 15

Fig 11. What is your OTT communications strategy?

2%

29%

12%33%

7%

17%

Chart Title

Yes

Yes, but it’s taken too long and has too few adopters

Yes, we will explore Joyn but wewill also explore partnering withan existing OTT provider

No, I don’t believe that it will ever be successfully launched or adopted

No

Don’t know

without an OTT strategy and 7% claiming not to know how to develop an OTT strategy), and 5% intent on not developing an OTT strategy.

Not one mobile operator included in this year’s research is blocking or imposing a subscriber surcharge for OTT services. This development must be viewed as yet another indication of the mobile operators’ softening stance towards the potential threat of OTT communications. This could be down to the fact that 42% of mobile operators said that they were making money from OTT services.

JOYN REMAINS MOBILE OPERATOR ENIGMAOne quarter of mobile operators are rolling out IMS/LTE to offer RCS/RCSe, and 14% said that they have or intend to launch Joyn – just over half of the mobile operators that are rolling out IMS/LTE to offer RCS/RCSe have launched or intend to launch Joyn. And of those mobile operators that have or intend to launch Joyn, half have also partnered with at least one OTT service provider. This suggests that while RCS/RCSe will help maintain the mobile operators’ relevance as a communications provider, doubts remain whether Joyn is the best application to achieve this.

Joyn is the GSMA’s OTT initiative and continues to be something of an enigma to mobile operators. This year, only 2% of mobile operators believed that Joyn is the ideal OTT communications countermeasure, with a further 29% also believing Joyn could be the solution but has taken too long to develop and has too few adopters. Nevertheless 12% of respondents said that they would explore Joyn while also look to partner with OTT service providers. Forty percent of mobile operators believe that Joyn will not be a success and is not an OTT countermeasure.

SOURCE: MOBILESQUARED

Since 2013, the number of mobile operators yet to formulate a view regarding Joyn has decreased from 36% to 17% this year. Overall, those that are positive, or could be positive towards Joyn (ie those respondents that said “yes, but ...”), account for 43% of mobile operators compared to 40% that have adopted an outright negative stance. This compares to 36% positive and 21% negative in 2013. The research highlights that negativity has increased within the mobile operator community surrounding Joyn as a viable combatant to OTT over the last 12 months, and will be another element used in the justification of partnering with third-party OTT communications providers.

One possible casualty from the emergence of mobile operators embracing OTT communications could be advanced messaging services, such as SMS 2.0. There is a clear shift in mobile operator strategy away from SMS 2.0, with only 5% of mobile operators offering their own messaging application or feature, compared to 43% in 2013. Up until last year, the appeal of advanced messaging services experienced a year-on-year increases since 2011. The appeal of advanced messaging services has most likely receded as mobile operators start to

PAGE 16 | PART 2: THE NEXT BILLION

Fig 12. Do you believe the prospect of the GSMA’s Joyn initiative can be an OTT countermeasure for

mobile operators?

understand and explore ways of capitalising on OTT communications, especially partnering. But it could also be attributed to the ascent of A2P traffic.

MOBILE OPERATOR GROWTH POINT: A2P TRAFFICBrands and businesses alike are starting to understand the benefit of communicating with their customer base via messaging. Anything from appointment reminders, to sales confirmation, to quickfire surveys, are helping companies gain a greater understanding of their customer’s experience and delivering greater efficiencies and cost savings in the process.

What’s more, while OTT communications focuses primarily on smartphone users, A2P traffic provides total mobile ubiquity and is device agnostic. Not surprisingly, this wave of A2P activity is starting to register with the mobile operators.

Thirty percent of respondents said that A2P traffic accounted for up to 10% of their overall messaging traffic during the last 12 months (between Sept 2013-2014), compared to 20% of respondents that said A2P accounted for between 11% and 30% of overall messaging traffic. Eleven percent of respondents claimed A2P accounted for over 41% of total messaging traffic.

SOURCE: MOBILESQUARED

Over the last 12 months 50% of respondents said that they have seen an increase in A2P messaging traffic, compared to just 6% of respondents experiencing a decline. Mobilesquared research has revealed that the A2P messaging traffic is increasing by 25% every 6 months, and stands to represent the biggest growth for mobile operators in terms of traffic and revenue in the near-term. Understandably, given what’s happening to their messaging and voice traffic and revenues, mobile operators will become highly-protective of the A2P sector. After all, while the A2P space remains a corporate, enterprise and small business domain, the mobile operators remain in control.

But as pressure mounts on OTT communications service providers to monetise their user footprint and increase their cost per user (CPU), it is perhaps inevitable that they will explore ways of entering the A2P marketplace.

Presently, mobile operators are the gateway to mobile customers for A2P traffic, and they must position themselves as the gatekeeper if they are to safeguard and secure their long term future in the A2P space, especially as the number of partnerships with OTT communications providers increases.

PARTNERINGWhen asked about partnering as part of a broader question regarding OTT strategy, 37% of mobile operators said they were partnering with OTT service providers. But when specifically asked about partnering, the number of mobile operators that said they were already partnering with an OTT provider (or providers) dropped to 24%. This discrepancy could be attributed to the fact mobile operators are in discussions with OTT providers and yet to launch.

PART 2: THE NEXT BILLION | PAGE 17

Fig 13. Over the last 12 months, what percentage of your messaging traffic was A2P?

For example, 31% of respondents said they were very open and receptive to partnering with an OTT provider, with a further 26% stating that they were open to the possibility of partnering but unsure how to begin the process.In total, 81% of mobile operators are already engaged with OTT providers or looking to enter into a partnership. Twelve percent remain undecided, leaving 5% waiting for commercial business models to emerge and 2% claiming there is no value in partnering.

Certainly in emerging markets – and to a lesser extent in developed markets – the research revealed that mobile operators are using brands such as WhatsApp, Facebook, WeChat, and LINE to convert customers onto smartphones and drive data package adoption, spend and usage. A number of mobile operators believe this is generating a sustainable business model, while other mobile operators said they continue to search for clear monetisation models of OTT.

When asked, 45% of mobile operators said that they would include OTT for free as part of the standard data bundle, while 21% would look to monetise the partnership via advertising and marketing, 16% selling content or through a monthly subscription model (10%).

PRIVACY ISSUESWith a growing number of mobile operators exploring the possibility of partnering with an OTT service provider to extend their marketing platform, it introduces additional concerns. For instance, 53% of mobile operators have expressed their concern with data privacy issues regarding OTTs, with 32% claiming they were not concerned with data privacy issues relating to OTT, or that they had already implemented the monetisation of this (15%).

More than two-thirds of mobile operators (69%) would be willing to assist OTT communications providers to verify private user information, with 37% of total respondents using the data to authenticate a user’s identity, and 31% to ensure compliance with the mobile operator provided a system was in place.Mobile operators would be willing to monetise gender, age, location, behaviour and preferences. A number of mobile operators said they have an open API platform that can provide a variety of subscriber data, and were looking to expand the data that this provided.

The primary expectation of mobile operators for partnering with an OTT service provider was to drive customer loyalty, according to 71% of respondents. Equally, 34% of mobile operators said it would be to develop an OTT subscription model and/or use as a marketing platform.

The majority of mobile operators believe that partnering with specific OTT providers to charge for data is the clearest OTT monetisation model. However, 42% of mobile operators believe that terminating IP traffic onto a mobile network also presents a clear monetisation opportunity. Mobile operators are a little more sceptical when it comes to monetising their own branded OTT app, appealing to 25% of respondents. But that was more popular than the rental of virtual mobile phone numbers (ie without SIM cards) (14%).

Entering into a partnership with an OTT provider does not hold any challenges for 21% of mobile operators, but for the majority a number of reasons were cited. Sixty four percent of mobile operators said that business reasons were the primary motive it had not forged a partnership with an OTT provider, followed by infrastructure complexities (26%) and regulatory issues (23%).

PAGE 18 | PART 2: THE NEXT BILLION

Not only are there challenges, but mobile operators have also expressed their concerns of entering a collaborative model with an OTT provider. Almost one-third of mobile operators said that they would have no idea what the contractual agreements would look like, based on margin split, staffing levels, setting KPIs and measuring the success of the partnership, for example. One fifth of respondents believe a partnership could be too complicated from an operational standpoint, based on the processes and systems, while 6% cited cultural differences as a likely concern. One fifth of mobile operators said their concerns were addressed when they entered the partnership, leaving 18% having no concerns whatsoever.

THE CHANGING FACE OF COMMUNICATIONSConcerns or not, mobile operators are being left with very little option other than to develop an OTT communications strategy, primarily because of the exponential adoption of OTT communications by their customers. As highlighted by this year’s research, increased data usage, lower-than-expected revenue losses, coupled with a more general upbeat positioning towards OTT is the first indication that mobile operators are starting to come to terms with their new rivals. Not to mention a growing belief that OTT apps represent just another rival company fighting for market share in a highly competitive marketplace. Telecoms is merely the latest industry to undergo an incredibly disruptive force. The airline industry underwent similar turbulence when budget airlines like Easyjet launched in the mid 1990s and forced the national incumbent airlines to reassess their pricing model in order to compete. The likes of BA, Lufthansa and American Airlines all survived to tell the tale.

To a large extent, the telecoms industry is no different, though it has a clear advantage over the airlines in that it has an established customer base in terms of subscribers, compared to a loyal customer base of repeat flyers.

A LEVEL PLAYING FIELDSo while investment communities are cock-a-hoop about the hundreds of millions of users on OTT messaging apps, the mobile operators have inadvertently become overlooked and even sidelined in the communications marketplace. Vodafone has over 400 million customers around the world, Telefonica has over 250 million, Orange has 236 million and T-Mobile 143 million customers. Not to mention China Mobile with over 791 million customers. These numbers are comparable with the major OTT messaging apps. What’s more, mobile operators generate substantial revenues. To make this a level playing field, OTT messaging apps must be viewed from a national perspective, which is, on the whole, how mobile operators are viewed and held accountable. Mobile operators have a very strong customer footprint, but have become restricted and segmented by geographical boundaries and cultural differences. In Germany, for instance, there are almost 40 million WhatsApp users (6% of total WhatsApp users), which is three-times the number of Twitter users (about 12 million). Yet Telefonica Deuschland, following its successful acquisition of E-Plus, now has 41 million subscribers. T-Mobile has 39 million subscribers, and in financial year 2013, it generated revenues of €7.7 billion in Germany, and €15.67 billion globally. The combined global revenue of WhatsApp, WeChat, LINE and Kakao in 2013 was $1.04 billion.

PART 2: THE NEXT BILLION | PAGE 19

PAGE 20 | PART 2: THE NEXT BILLION

Elsewhere, Snapchat has come from nowhere to amass 80 million users in the US, overtaking WhatsApp’s 75 million users in the process. Messenger has around 62 million users and LINE has 12 million. But all of these figures are overshadowed by AT&T’s 117 million mobile subscribers and Verizon Wireless’s 105 million customers, while T-Mobile also has a very respectable 50 million customers. For 2Q2014, AT&T posted wireless consolidated revenues of $17.9 billion.

In the UK, WhatsApp has just over 10 million users, with 8 million users on Snapchat, and 5 million on Facebook Messenger. While EE has 27 million mobile customers in the UK, Telefonica has 23.7 million and Vodafone has 19.5 million.

Mobilesquared data reveals that the US, UK and Germany have 137.6 million, 32.1 million and 44.1 million smartphone-based OTT users respectively in 2014. These figures are expected to more than double by 2018, when OTT smartphone penetration is forecasted to be close to 100% of the smartphone user base in each of the three markets. An emerging trend that mobilesquared has identified across all developed mobile markets.

PART 3: THE MOBILE OPERATOR OPPORTUNITY

PART 3: THE MOBILE OPERATOR OPPORTUNITY | PAGE 21

With voice and messaging revenues in continual decline for a significant proportion of mobile operators and an imminent eventuality for the rest how long can mobile operators pin their hopes on data to redress declining revenues and thwart its inevitable commoditisation? Although the cost of 1GB of data on 4G today is significantly lower compared to 1GB on 3G five years ago, 4G usage is significantly higher, with an increasing number of data users exceeding their data bundles, even though more users are trading up to higher data plans.

SOURCE: VODAFONE

OTT is not an epidemic but a fundamental paradigm shift in the way consumers communicate. The disruptive innovation of OTT communications has altered the economics of mobile telecoms forever. And because OTT providers do not operate under the shadow of million or billion dollar spectrum investments, network roll-out costs and extensive network maintenance spend, they can enjoy the agility of a small team adjusting and tweaking their product. The cost for WhatsApp to deliver a message is three-to-four orders of magnitude less than what it costs a mobile operator. If the cost structure of OTT communications applied to the car industry, everyone would be driving round in Rolls Royces, Aston Martins and Lamborghinis. OTT communications is a model of massive volume at minimal cost, which has also become the framework in which the mobile operators must compete.

ANALYSISThe research included a number of different questions associated with mobile operators partnering with third-party OTT communications providers. The percentage of respondents “partnering” changed with the wording of each question. The highest response was based on a mobile operator’s OTT strategy, in which 37.2% said they were “partnering”. But when asked outright about their partnering strategy on a separate question, only 23.8% of mobile operators claimed to have already partnered. This implies that 13.4% of mobile operators are in the process of partnering with third-party OTT providers now.

2 Based on the assumption that “Don’t know” implies that the respondent was not aware of the extent of OTT penetration within their customer base, otherwise they would have responded “0%”

When specifically asked about the role of Facebook and WhatsApp, 13.6% of mobile operators said they have partnered with one or both companies, and a further 25% of mobile operators would be interested in partnering with them.

Of the mobile operators to have partnered with OTT communications providers already (23.8%), 58% of these mobile operators have partnered with Facebook and/or WhatsApp, with the remaining 42% entered into partnerships with alternative OTT communications providers. In total, just under 40% of mobile operators would like to partner with Facebook and/or WhatsApp.

Then there are the 14% of mobile operators that have launched Joyn, half of which are looking to enter partnerships with third-party OTT communications providers as well, as a contingency plan should Joyn fail.

Overall, 97.6% of mobile operators will potentially enter into an OTT communications partnership provided their concerns are addressed. By removing those mobile operators that have entered into a partnership already, this leaves 75% of mobile operators that are looking to enter into a partnership. Or an alternative view is that 59% of mobile operators looking to partner with an OTT communications provider do not want to partner with Facebook and/or WhatsApp, even though a similar number would like to provide a WhatsApp-like experience to their customers.

BUSINESS MODELSThis newfound optimism coursing through mobile operator veins is best encapsulated by the fact a number of mobile operators are now exploring what tools they can provide to OTT communication providers to help them monetise their service.

Already, 55.6% of mobile operators have experienced an increase in billable data usage as a direct result of OTT communications over their network, and 29% of mobile operators have experienced an increase in messaging, data and messaging, or data, messaging and voice.

For 71% of mobile operators, offering an OTT communications-based service is about driving customer loyalty, which in turn will potentially boost messaging and voice usage, and most notably data, with 66% of mobile operators expecting to charge for data following a partnership with specific OTT communications companies. Whereas opening up APIs and connecting platforms to allow mobile operators to terminate IP traffic on their network appeals to 40% of respondents. As with the data regarding partnerships, there is some inconsistency across the responses when it comes to business models. The percentage of mobile operators intending to develop an OTT subscription model is 35% in one question focusing on collaboration, but drops to 11% when specifically asked about business models for the OTT partnership. It’s the same with the ability to monetise the partnership via advertising and marketing, which drops from 35% in the collaboration question to 21.6% when linked to business models.

Analysis of the research implies mobile operators are significantly more comfortable with the notion of partnering than they are talking about specific business models associated with partnering, which after all, is a completely unknown discussion for them. Mobilesquared believes the fact that the percentage of mobile operators looking to monetise an OTT offering drops when the phrase “collaboration” is swapped with “business model”,

PAGE 22 | PART 3: THE MOBILE OPERATOR OPPORTUNITY

-

5.000.000.000

10.000.000.000

15.000.000.000

20.000.000.000

25.000.000.000

30.000.000.000

35.000.000.000

40.000.000.000

45.000.000.000

50.000.000.000

2013 2014 2015 2016 2017 2018

Chart Title

Mobile termination SMS termination Adv & marketing Content Subscription

PART 3: THE MOBILE OPERATOR OPPORTUNITY | PAGE 23

suggests that mobile operators feel restricted or limited when it comes to discussing business models with OTT third parties. Presently, the notion of negotiating a contract with an OTT service provider remains something of a dark art to mobile operators. After all, as highlighted by this year’s research, 26% of mobile operators need advice when it comes to commencing discussions with a third-party OTT communications provider, while an additional 30% said they have no idea what the contractual agreements would look like.

Clearly light needs to be shed on how to craft a mobile operator and OTT service provider partnership contract. There is an opportunity for a company to create a “What does a mobile operator and OTT communications company contractual agreement look like” document to speed up the collaborative effort now being entertained.

OTT COMMUNICATION FORECASTSMobilesquared forecasts that the global mobile operator opportunity for OTT communication will be worth $42.9 billion in 2018, an increase from $4.2 billion in revenues in 2014.

OTT off-net communication termination for voice and messaging will account for $4.2 billion in 2014, and leap to $30 billion in 2018 as mobile operators partner with OTT communications providers and open their networks to terminate traffic. OTT off-net messaging termination will represent the majority of revenues, generating $19.4 billion by 2018.

But as mobile operators open partnerships with existing OTT communications service providers and reposition themselves as a critical component in the monetisation process, revenues generated by going Through The Operator (TTO) will be worth $465 million in 2015 rising to $12.8 billion in 2018.

The sale of mobile operator data for marketing and advertising purposes will generate $245 million in 2015 rocketing to $7.2 billion in 2018. During the same timeframe, OTT-based content sales will generate $122.5 million and $3.9 billion respectively, while OTT subscription revenues will be worth $98 million, rising to $1.8 billion.

SOURCE: MOBILESQUARED

Fig 14. The mobile operator OTT communication opportunity ($)

CONCLUSIONIt is not coincidental that almost every mobile operator included in the research is open to the concept of partnering with an OTT communications provider, and around 80% of mobile operators now believe they can generate revenues from OTT communications. Clearly, mobile operators now believe that partnering will unlock the revenue generating potential of OTT communications.

Rather than develop their own OTT service, mobile operators are now intent on capitalising on what is already available and pursuing partnerships. Ironically, Joyn has been trying to develop the ultimate RCS/RCSe communication experience, but almost two-thirds of mobile operators said they would like to provide the simplicity of a WhatsApp-like experience to their customers.

Mobilesquared believes this will result in a period of convergence between mobile operators and OTT communications service providers. This will be driven by two factors.

Firstly, there has been a significant shift in mobile operator mindset regarding OTT communications. The perception that OTT communications is a threat has been replaced with a revenue-generating opportunity. Mobile operators have never been more open and receptive to the notion of partnering with OTT communications service providers, and to this end, OTT communications providers must look to exploit this opportunity.

Secondly, the need for OTT communications providers to monetise their community. Driving this

commercialisation will be a period of maturation throughout OTT communications providers as their model evolves beyond pure community-driven user acquisition, to revenue generation and user acquisition. The need to partner is compounded by the fact OTT communications have little or no user information or data, and mobile operators have customer data in abundance, and limited or no billing capability.

To date mobile operators have been tentative and reluctant to partner with OTT communication providers. As this year’s research has highlighted, this is down to not knowing what elements to include in a contractual agreement, as well as the means by which to measure success, to not knowing how to start the process. Ultimately, it has come down to the fact that OTT communications is yet to have a clear business model.

Of course, the OTT communication (or social messaging) platforms emanating out of Asia are generating a cost per user of up to $3 – significantly lower than a mobile operators average revenue per user (ARPU). But from experience, only a select few companies have made the closed community, or walled garden model, work. This has resulted in the mobile operator questioning the justification for partnering with an OTT communications provider.

But mobilesquared believes partnering will overcome the lack of business model, and present clear monetisation opportunities. The functionality, customer data and billing capability of an operator, along with the potential of providing an open network API, when applied to the vast and engaged user

PAGE 24 | CONCLUSION

CONCLUSION

APPENDIXMobilesquared conducted the international mobile network operator (MNO) and mobile virtual network operator (MVNO) research between July and September 2014. The views of over 60 mobile operators have been included in the research. Companies include (in no particular order):

Essar Telecom Kenya, Yu Mobile, Bharti Airtel, PT Telekomunikasi Selular Indonesia, Telecom Italia, Juvo, Inc., A1 Telekom Austria, SK Telecom, Bouygues Telecom, Telecom Italia Mobile, Telecable, Warid Telecom, EE.DTAG, U.S. Cellular, BT PLC, Deutsche Telekom, T – mobile, Tele2 Lithuania, Telefonica, Cellcom Isael, Aircel, Croatian Telecom Inc., Wind Telecomunicazioni S.p.a., Polkomtel, COSMOTE GREECE, AT&T, Telekom Austria Group, EWA, Zain KSA, Airtel Africa, MegaFon, Smart Telecom, Movicel, Digicel, Tesco Mobile, Telenor, Telkomsel, du, mtel, TELE Greenland, Hrvatski Telekom d.d., BH Telecom

SOURCE: MOBILESQUARED

11% 2%

56%

13%

18%

Chart Title

Where are you based?

North America

Latin America

Europe

MEA

APAC

APPENDIX | PAGE 25

community of an OTT communications provider will create additional revenue opportunities for the mobile operator.

Business models to emerge on the back of these partnerships will be created by the re-intermediation of the mobile operator to a central role for the delivery of communications. For example, the sale of mobile operator customer data will provide enhanced targeting for advertising and marketing, as well as the up-selling of relevant content to OTT users. The mobile operator`s billing capability can also be applied to the up-sale of content, as well as to a monthly subscription fee for the OTT service. Mo-bilesquared believes mobile operators should also explore the opportunity of launching a flat-rate all-you-can-eat data communications tariff, to complement the existing data bundle, and to offset the decline in traditional communication revenues.

Mobilesquared forecasts that the global mobile operator opportunity for OTT communication will be worth $42.9 billion in 2018, up from $4.2 billion in revenues in 2014. The partnership model will be worth $465 million in 2015 to mobile operators, rising to $12.8 billion in 2018.

To put this opportunity into context, it has taken 10 years for the mobile advertising industry to generate $13 billion in global revenues. The mobile operator OTT partner model can achieve that in 4 years.

Mobile operators are back in the game.

APPENDIX

Fig 15. Where are you based?

Job titles of respondents partaking in the 2014 research include:

VAS, Voice & Data Product Manager; Core and VAS System Roadmap; Head, Future Centre; SVP Business Development; Lead Architect; Core Network and Value Added Services Engineering Director; Manager Data & Devices; Principal Strategist; VP Core Network & Services; Head of Product Management – Messaging; Senior Proposition Manager Voice & Messaging; Senior Engineer, RAN Rollout Manager, Internet & Mobile Application Area Manager; Head - Strategic Alliances; Proposition Manager; Marketing Manager; New Service Development Manager; Senior Software Engineer; CEO; International Marketing Consultant; Head of Marketing; Head of New Business Solutions; Senior User and Retention Manager; Marketing Analyst; Strategy Implementation; Lead Member of Technical Team; Director Data; International Director; Telecoms, Manager of Device Content; VAS & Broadband Marketing Communication; CTO Assistant; Head Value Added Service; CTO; Chief Marketing and Sales Officer; Head of Network Architecture; Customer Value Management and Customer Intelligence Specialist; Head of Research Department.

METHODOLOGYResearch was conducted by mobilesquared during July to September 2014. The project involved a multi-layered approach based on direct and indirect research.

Direct research involved two elements. Firstly, the mobile operator research used an online survey of agreed questions between mobilesquared and tyntec. The survey was pushed out to mobilesquared’s global mobile operator database. This was supported by mobilesquared’s proprietary LinkedIn research tool to drive responses.

Secondly, primary research based on 1-2-1 interviews with mobile operators and OTT service providers and vendors, extensive research and interviews at key industry events, such as Monetising OTT in London, was used to update market data, information and identify emerging trends. And indirect research, i.e. secondary and tertiary research (primarily online based).

Forecasts for this white paper have been constructed using a 6-step process.

1. mobilesquared forecasts are based on subscriptions, and not subscribers, which factor in consumers owning more than one smartphone device. This has been applied to 68 markets (see page 27).

2. The research then involved updating smartphone penetration as a percentage of subscriptions per market.

PAGE 26 | METHODOLOGY

METHODOLOGY

METHODOLOGY | PAGE 27

3. The next step was to identify OTT communication user penetration as a percentage of the smartphone user base in each market.

4. Key data points were extracted from the direct and indirect research to identify OTT communication users and usage trends for mobile voice and messaging, from providers such as Skype, Viber, WhatsApp, LINE, such as percentage of “OTT off-net communication” mobile calls compared to Skype-to-Skype calls for example, and repeat OTT communications user and usage trends for IP messaging.

5. Termination rates from the mobile operator research were applied to traffic projections to create revenue forecasts.

6. OTT communication revenue forecasts are based on a universal rate of $0.06 for OTT-to-mobile calls, and a flat-rate of $0.01 for all OTT off-net communication SMS traffic. These termination rates are based on actual numbers acquired during the research process.

7. The incremental revenue forecasts for Through The Operator (TTO)/mobile operator partnership opportunity are based on key data from the mobile operator research 2014, and applied to updated OTT smartphone forecasts.

Please note, the mobile forecasts included in this report focus only on the global mobile operator opportunity generated from traffic generated from an OTT communication service provider to a mobile phone using a traditional phone number. For the purposes of this report we call a Skype call to a mobile phone, for example, an “OTT off-net communication” call. Therefore, the forecasts in this report only cover the traffic and revenues generated by the termination of “OTT off-net communication” communications (mobile voice and messaging). The

forecasts only focus on the direct revenue generating potential for mobile operators from OTT communications (terminating voice and messaging traffic), the sale of customer data, the sale of content, and the introduction of a subscription model. Indirect revenue generating sources, such as an increase in data usage, has not been included.

The 68 countries researched are: Algeria, Argentina, Austria, Australia, Azerbaijan, Bangladesh, Belgium, Brazil, Bulgaria, Canada, China, Chile, Columbia, Czech Republic, Denmark, Ecuador, Egypt, Estonia, Finland, France, Greece, Germany, Guatemala, Hong Kong, Hungary, India, Indonesia, Iran, Ireland, Israel, Italy, Japan, Jordan, Lebanon, Lithuania, Malaysia, Mexico, Montenegro, Morocco, Nepal, Netherlands, New Zealand, Nigeria, Norway, Pakistan, Peru, Philippines, Poland, Portugal, Romania, Russia, South Africa, Saudi Arabia, Singapore, Slovakia, South Korea, Spain, Sri Lanka, Sweden, Taiwan, Thailand, Turkey, UAE, UK, Ukraine, USA, Venezuela and Vietnam.

Please note, this is the fourth year mobilesquared has run the mobile operator OTT research. The first wave of mobile operator research was conducted in 3Q2011 and repeated in 2Q2012 and 2Q2013.

ABOUT TYNTEC

tyntec is a mobile interaction specialist, enabling businesses to integrate mobile telecom services for a wide range of uses – from enterprise mission-critical applications to internet services. The company reduces the complexity involved in accessing the closed and complex telecoms world by providing a high quality, easy-to-integrate and global offering using universal services such as SMS, voice and numbers. Founded in 2002, and with more than 150 staff in six offices around the globe, tyntec works with 500+ businesses including mobile service providers, enterprises and internet companies.

For more information: www.tyntec.com

ABOUT MOBILESQUARED