wine market value chain profile 2011-12. · pdf filea profile of the south african wine market...

TRANSCRIPT

A PROFILE OF THE SOUTH AFRICAN WINE MARKET VALUE CHAIN

2011

Directorate Marketing Private Bag X 15

Arcadia 0007

Tel: 012 319 8455 Fax: 012 319 8131

E-mail: [email protected] www.daff.gov.za

2

RECENT DEVELOPMENTS For the most part of the first decade of the second millennium, the wine industry in South Africa experienced a significant swing towards red wine production – moving from 18% of planting in 1996 to 44% in 2008. This gave rise to a surplus production position putting downward pressure on producer prices. Given that the local demand for wine, red wine in particular, did not match the increased supply, the local industry was forced to enter the export market in a much more aggressive way than ever before. No wonder then the export, as percentage of local production increased from 21% in 1999 to 54% in 2008. Despite fluctuations in the rand exchange rates over this period, the general trend was downwards, helping to maintain export profitability. The inflationary conditions coupled with pressure on disposable income have resulted in consumers trading down. This obviously became much more price conscious. The South African wine consumer in general is regarded as more price conscious and less likely to venture into the higher priced products. In 2008 the demand for white wine has weakened whilst red wine sales showed a moderate increase. However, as far as red wine is concerned, the supply / demand position has since moved into equilibrium.

3

Table of Contents

1. DESCRIPTION OF THE INDUSTRY 5

1.1 Production areas 6

1.2 Production 13

1.3 Deregulation of markets and re-regulation of labor 15

1.4 Consumption 16

2. MARKET STRUCTURE 17

2.1 Domestic markets and prices 19

3. EXPORTS VOLUMES 21

3.1 Provincial and district export values of South African wines 25

3.2 Share analysis 40

4. MARKET INTELIGENCE 47

4.1 Competitiveness of South African wine exports 55

5. MARKET ACCESS 67

5.1 Tariff, quotas and the price entry system 67

5.2 The EU-South Africa wine agreement and its implications 87 5.2.1 Rules on additives, processes and what is natural wine 88 5.2.2 Voluntary standards 89 5.2.3 British Retailer Consortium (BRC) Global Standard – Food 90 5.2.4 The Integrated Production of Wine (IPW) Scheme 91

5.3 Entry barriers and rules of participation in the UK retail market 91 5.3.1 Elements of an industrial convention: Delivering basic quality 91 5.3.2 Elements of a market convention: Delivering price and promotions 93

5.4 Entry barriers and rules of participation in other end-markets 93

5.4.1 Netherlands 93 5.4.2 Sweden 93 5.4.3 Germany 94 5.4.4 USA 94

4

6. REGULATORY FRAMEWORKS 95

6.1 The wine of Origin Scheme 95 6.1.1 Origin 95 6.1.2 Cultivar 98 6.1.3 Certification system 98

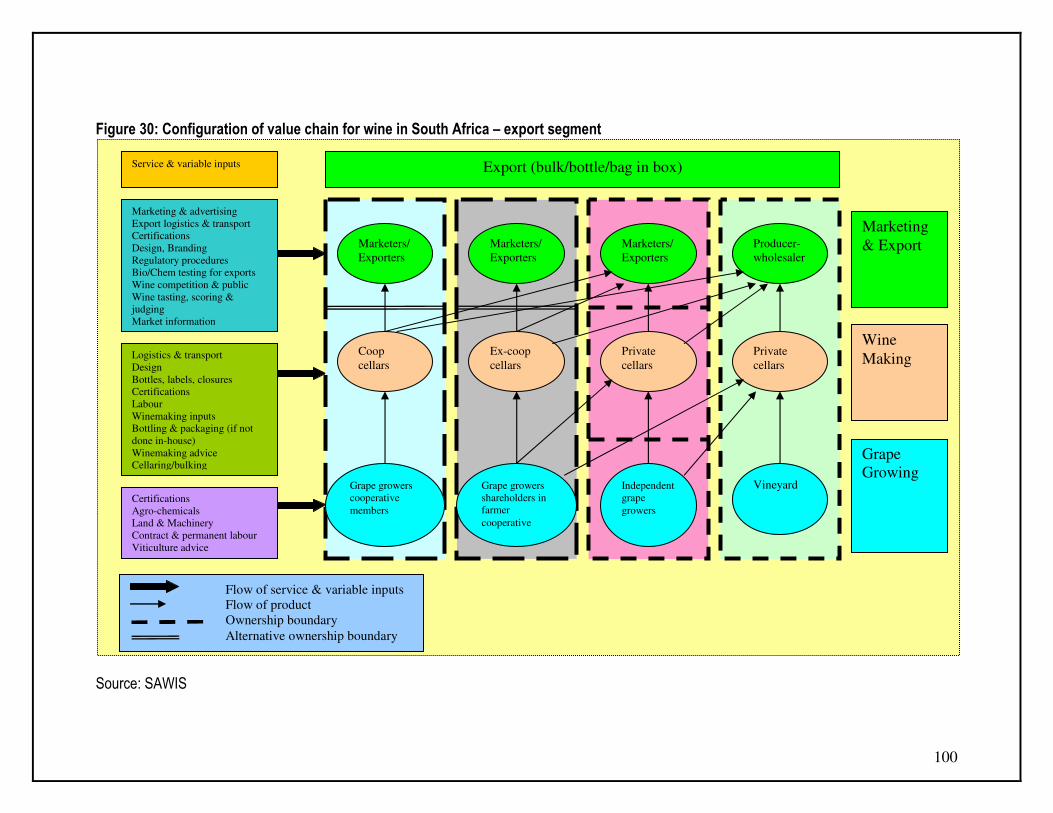

7. THE VALUE CHAIN FOR WINE IN SOUTH AFRICA 99

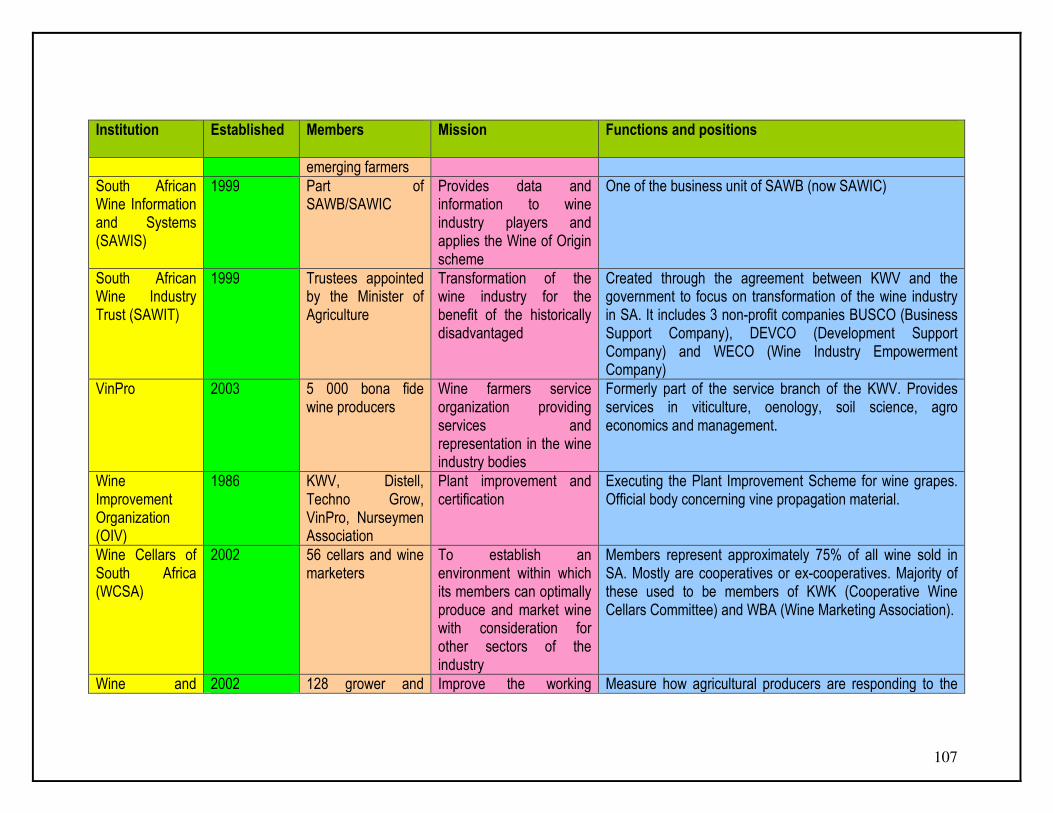

8. ORGANIZATIONAL ANALYSES 104

8.1 FORMAL INSTITUTIONS AND ORGANIZATIONS 104

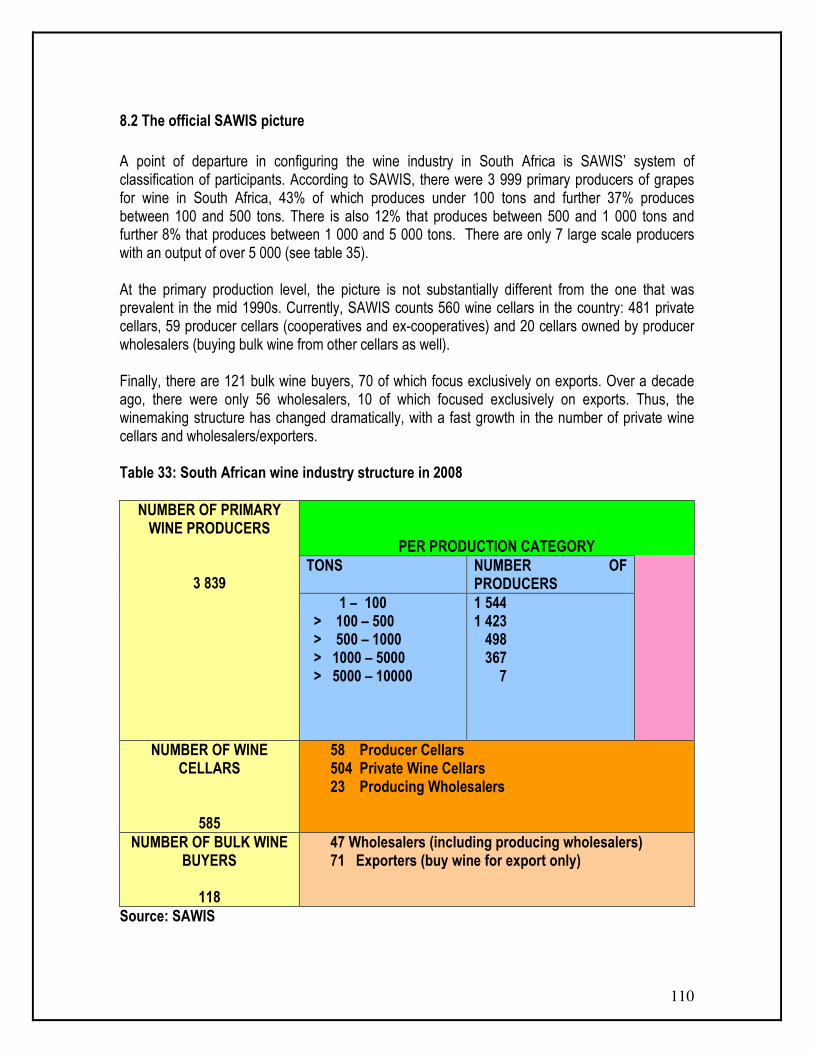

8.2 The Official SAWIS picture 110

8.3 Strengths, Weaknesses Opportunities and Threats (SWOT) analysis 112

8.4 Business opportunities and challenges 113

9. EMPOWERMENT & TRANSFORMATION IN THE SECTOR 113

9.1 The transformation of the industry 113

9.2 BEE in the wine industry 115

10. ACKNOWLEDGEMENTS 118

5

1. DESCRIPTION OF THE INDUSTRY The wine industry in South African context is much wider than signified by the ordinary meaning of the word “wine”. Brandy and its building blocks (wine for brandy and distilling wine) have always formed a significant part of South African wine industry. In recent years, grape juice concentrate for use in non-alcoholic beverages, and not just for sweetening of wine, have come to the fore. The South African wine industry thus encompasses wine (natural, fortified and sparkling), wine for brandy, distilling wine, brandy and other spirits distilled from distilling wine, and grape juice and grape juice concentrate for use in non-alcoholic products. Wine products includes the following

• Natural wine is a non fortified and non sparkling wine, including perle wine which is wine carbonated to the extend that the pressure in the container in which it is sold is between 75 and 300 kPa. It includes any grape juice or must and grape juice or must concentrate used in the sweetening of such natural wine.

• Fortified wine is a non-sparkling wine which has been fortified with wine spirit. It includes the volume of wine spirit used in the fortification process.

• Sparkling wine is carbonated (either by fermentation or by impregnation with carbon dioxide) to the extent that the pressure in the container in which it is sold is more than 300 kPa. It includes any grape juice or must and grape juice or must concentrate used in the sweetening of such sparkling wine.

Wine for brandy is wine specially prepared for double distillation in a pot still and then, as distillate, matured for a period of at least three years in oak casks with capacity of more than 340 litres. Distilling wine is wine specially prepared for distillation of spirits intended for use in brandy or other spirits, for fortification of wine for industrial purposes. Grape juice concentrate and grape juice refers to unfermented, undiluted or concentrated juice from grapes destined for use in non-alcoholic products such as fruit juices. The wine industry in the Western Cape (excluding tourism) supported almost 200 000 jobs in 2008. The industry contributed R14, 214 billion to the Western Cape economy. This amounted to approximately 7.3% of the total provincial Gross Domestic Product of the Western Cape. When assessing the contribution that was made to the national economy’s GDP, an amount of R26, 223 billion or 1,95% was added to the South African economy. The wine industry is an important contributor to the economy of the Western Cape region of South Africa. Perhaps, even more important than the direct economic impact of employment and foreign exchange generation is the unique position of wine (and to some extend wine tourism) in generating images of South Africa abroad.

6

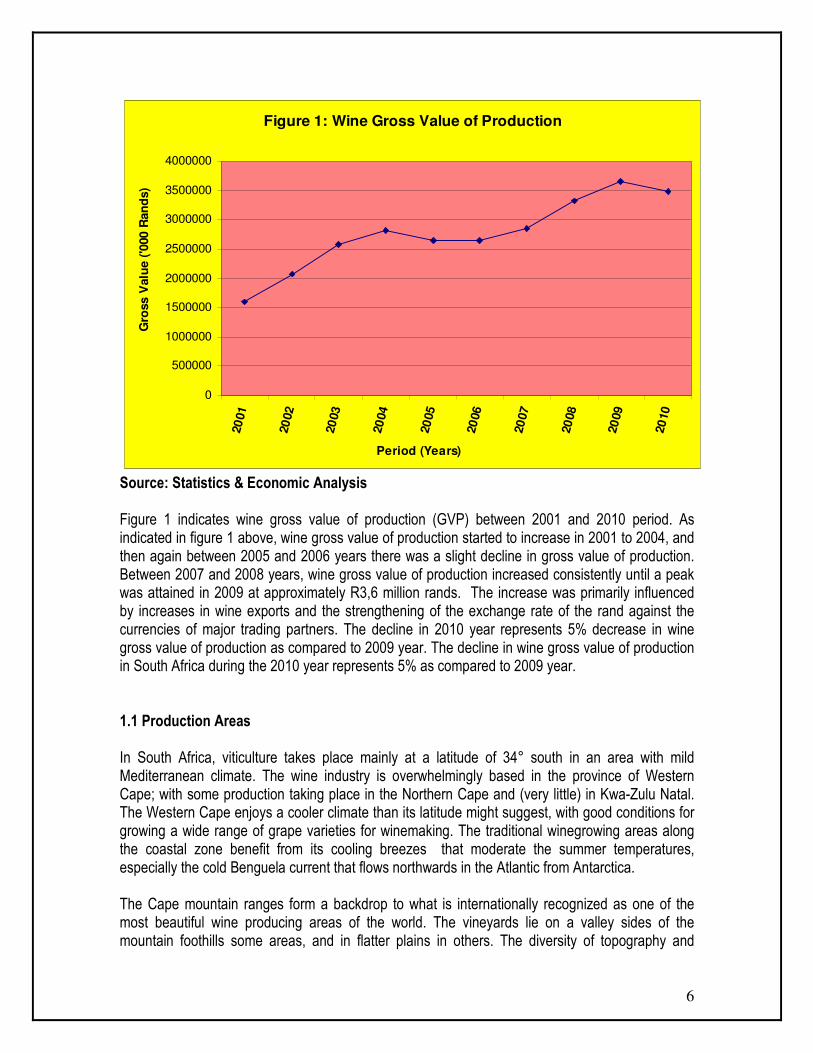

Figure 1: Wine Gross Value of Production

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

4000000

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Period (Years)

Gro

ss V

alu

e (

'000 R

an

ds)

Source: Statistics & Economic Analysis Figure 1 indicates wine gross value of production (GVP) between 2001 and 2010 period. As indicated in figure 1 above, wine gross value of production started to increase in 2001 to 2004, and then again between 2005 and 2006 years there was a slight decline in gross value of production. Between 2007 and 2008 years, wine gross value of production increased consistently until a peak was attained in 2009 at approximately R3,6 million rands. The increase was primarily influenced by increases in wine exports and the strengthening of the exchange rate of the rand against the currencies of major trading partners. The decline in 2010 year represents 5% decrease in wine gross value of production as compared to 2009 year. The decline in wine gross value of production in South Africa during the 2010 year represents 5% as compared to 2009 year. 1.1 Production Areas In South Africa, viticulture takes place mainly at a latitude of 34° south in an area with mild Mediterranean climate. The wine industry is overwhelmingly based in the province of Western Cape; with some production taking place in the Northern Cape and (very little) in Kwa-Zulu Natal. The Western Cape enjoys a cooler climate than its latitude might suggest, with good conditions for growing a wide range of grape varieties for winemaking. The traditional winegrowing areas along the coastal zone benefit from its cooling breezes that moderate the summer temperatures, especially the cold Benguela current that flows northwards in the Atlantic from Antarctica. The Cape mountain ranges form a backdrop to what is internationally recognized as one of the most beautiful wine producing areas of the world. The vineyards lie on a valley sides of the mountain foothills some areas, and in flatter plains in others. The diversity of topography and

7

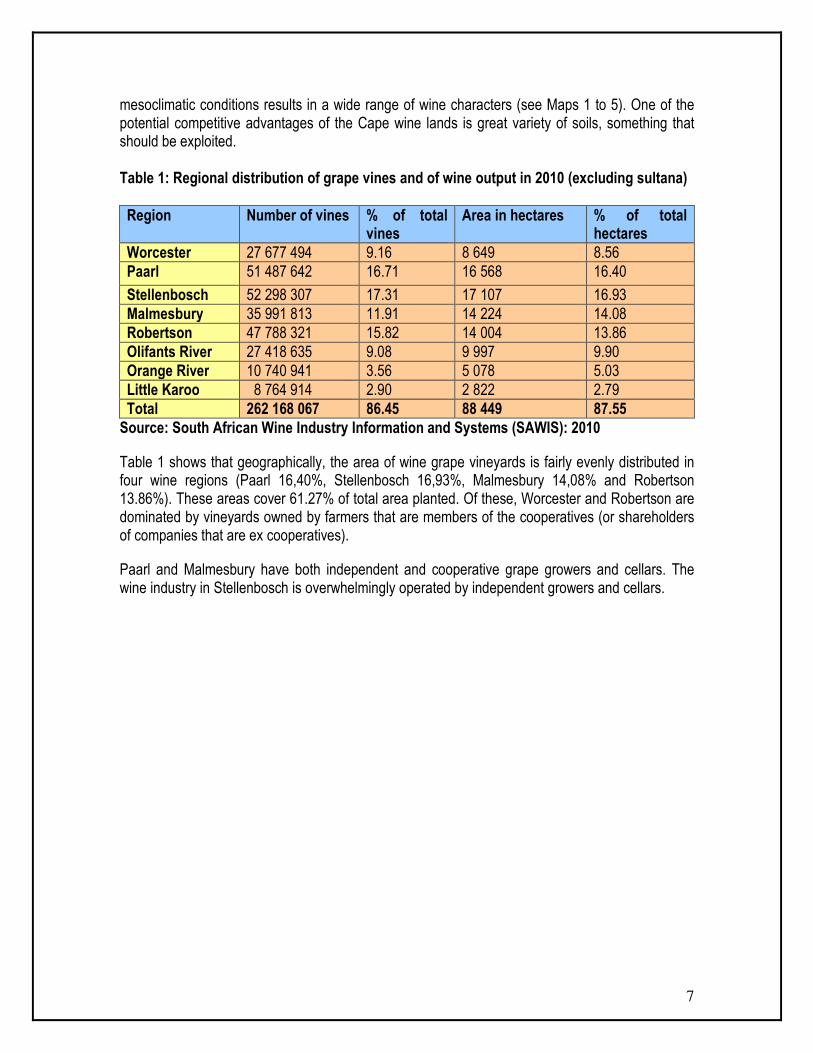

mesoclimatic conditions results in a wide range of wine characters (see Maps 1 to 5). One of the potential competitive advantages of the Cape wine lands is great variety of soils, something that should be exploited. Table 1: Regional distribution of grape vines and of wine output in 2010 (excluding sultana) Region Number of vines % of total

vines Area in hectares % of total

hectares Worcester 27 677 494 9.16 8 649 8.56 Paarl 51 487 642 16.71 16 568 16.40

Stellenbosch 52 298 307 17.31 17 107 16.93 Malmesbury 35 991 813 11.91 14 224 14.08 Robertson 47 788 321 15.82 14 004 13.86 Olifants River 27 418 635 9.08 9 997 9.90 Orange River 10 740 941 3.56 5 078 5.03 Little Karoo 8 764 914 2.90 2 822 2.79 Total 262 168 067 86.45 88 449 87.55 Source: South African Wine Industry Information and Systems (SAWIS): 2010

Table 1 shows that geographically, the area of wine grape vineyards is fairly evenly distributed in four wine regions (Paarl 16,40%, Stellenbosch 16,93%, Malmesbury 14,08% and Robertson 13.86%). These areas cover 61.27% of total area planted. Of these, Worcester and Robertson are dominated by vineyards owned by farmers that are members of the cooperatives (or shareholders of companies that are ex cooperatives).

Paarl and Malmesbury have both independent and cooperative grape growers and cellars. The wine industry in Stellenbosch is overwhelmingly operated by independent growers and cellars.

8

Map 1: Production areas of South Africa – Geographical Units

Source: SAWIS Map 2: Production areas of South Africa – Regions

9

Source: SAWIS

10

Map 3: Production areas of South Africa – Districts

11

Source: SAWIS Map 4: Production areas of South Africa – Wards (Western Cape)

Source: SAWIS

12

Map 5: Production areas of South Africa – Wards (Northern Cape) Source: SAWIS

13

1.2 Production

Figure 2: Area under wine grape vineyards (excluding sultana)

Figure 2: Total area under wine grape vineyards

(Excluding Sultana)

90000

92000

94000

96000

98000

100000

102000

104000

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Period (Years)

Are

a p

lan

ted

(h

a)

Source: SAWIS Figure 2 illustrates total area under wine grape vineyards (excluding sultana) between 2001 and 2010 period. The graph further illustrates that the total area planted under wine grape vineyards (excluding sultana) has increased dramatically in the last decade, from 94 500 ha in 2001 to 102 00 ha in 2006 year and 101 000 ha in 2010 year. The figure also illustrates that between 2007 and 2010 years, there was a slight decline in the total area under wine grape vineyards. The figure further illustrates that in 2006 a peak was attained in total area under wine grape vineyards at approximately 102 000 ha. The decline in total area under wine grape vineyards during the 2010 year represents 0.24% as compared to 2009 year.

14

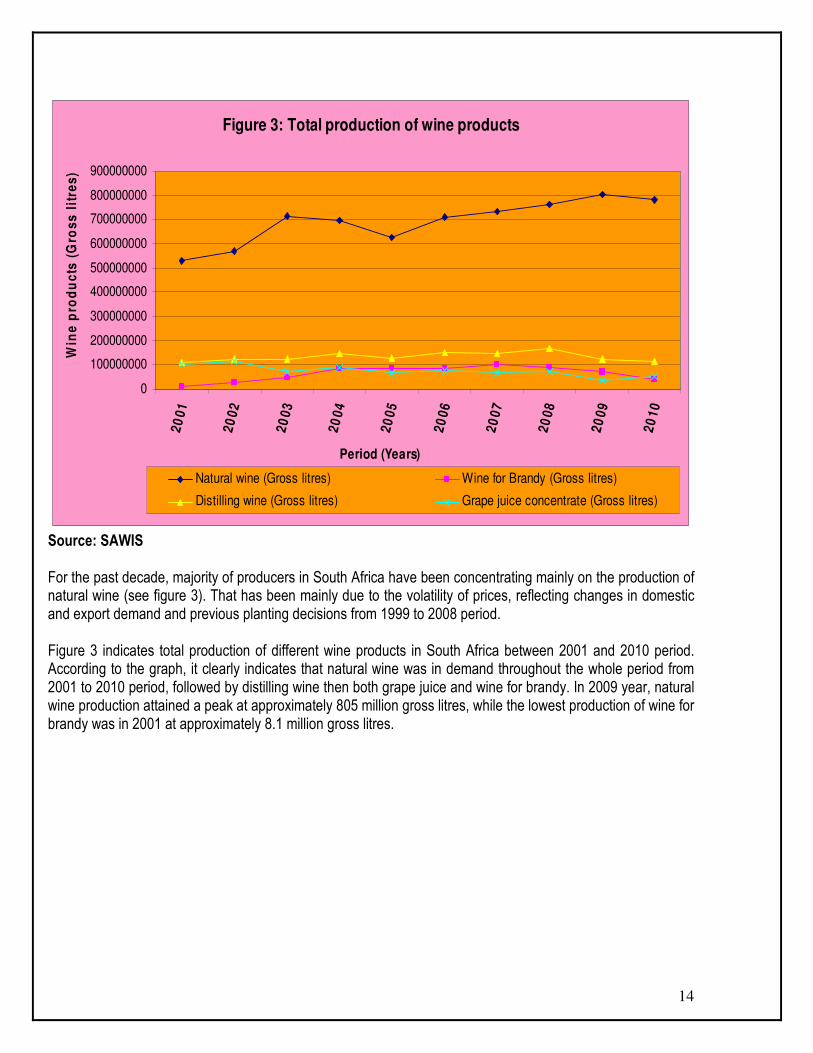

Figure 3: Total production of wine products

0

100000000

200000000

300000000

400000000

500000000

600000000

700000000

800000000

9000000002

00

1

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Period (Years)

Win

e p

rod

uc

ts (

Gro

ss

lit

res

)

Natural wine (Gross litres) Wine for Brandy (Gross litres)

Distilling wine (Gross litres) Grape juice concentrate (Gross litres)

Source: SAWIS For the past decade, majority of producers in South Africa have been concentrating mainly on the production of natural wine (see figure 3). That has been mainly due to the volatility of prices, reflecting changes in domestic and export demand and previous planting decisions from 1999 to 2008 period. Figure 3 indicates total production of different wine products in South Africa between 2001 and 2010 period. According to the graph, it clearly indicates that natural wine was in demand throughout the whole period from 2001 to 2010 period, followed by distilling wine then both grape juice and wine for brandy. In 2009 year, natural wine production attained a peak at approximately 805 million gross litres, while the lowest production of wine for brandy was in 2001 at approximately 8.1 million gross litres.

15

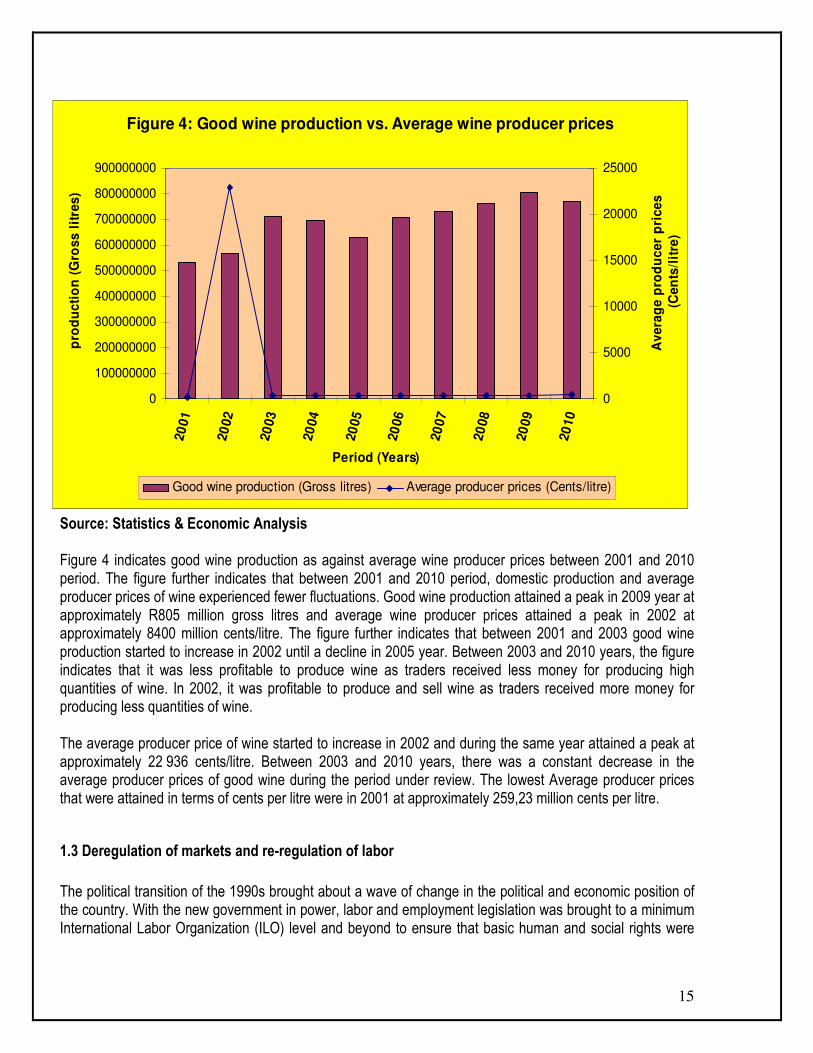

Figure 4: Good wine production vs. Average wine producer prices

0

100000000

200000000

300000000

400000000

500000000

600000000

700000000

800000000

90000000020

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Period (Years)

pro

du

cti

on

(G

ros

s l

itre

s)

0

5000

10000

15000

20000

25000

Av

era

ge

pro

du

ce

r p

ric

es

(Ce

nts

/lit

re)

Good wine production (Gross litres) Average producer prices (Cents/litre)

Source: Statistics & Economic Analysis Figure 4 indicates good wine production as against average wine producer prices between 2001 and 2010 period. The figure further indicates that between 2001 and 2010 period, domestic production and average producer prices of wine experienced fewer fluctuations. Good wine production attained a peak in 2009 year at approximately R805 million gross litres and average wine producer prices attained a peak in 2002 at approximately 8400 million cents/litre. The figure further indicates that between 2001 and 2003 good wine production started to increase in 2002 until a decline in 2005 year. Between 2003 and 2010 years, the figure indicates that it was less profitable to produce wine as traders received less money for producing high quantities of wine. In 2002, it was profitable to produce and sell wine as traders received more money for producing less quantities of wine. The average producer price of wine started to increase in 2002 and during the same year attained a peak at approximately 22 936 cents/litre. Between 2003 and 2010 years, there was a constant decrease in the average producer prices of good wine during the period under review. The lowest Average producer prices that were attained in terms of cents per litre were in 2001 at approximately 259,23 million cents per litre.

1.3 Deregulation of markets and re-regulation of labor The political transition of the 1990s brought about a wave of change in the political and economic position of the country. With the new government in power, labor and employment legislation was brought to a minimum International Labor Organization (ILO) level and beyond to ensure that basic human and social rights were

16

afforded to all the workers under the law. The extension of Labor Relations Act of 1995 and the free movement of unions in the sector led to bursts of union activity in agriculture. The extension of basic human, social and economic rights to farm workers resulted, inter alia, in increased levels of casualization and externalization – which were carried out to mitigate the consequences of increased labour costs and the costs of complying with labour legislation. This did not take place overnight, by the mid-1990s, farmers had developed new technologies as a result of industry restructuring (deregulation, opening of the export market), but that labour practices had remained unchanged. It was also found out that employment had grown in wine farms (due to the major new plantings that took place in the 1990s) and that there was no apparent decrease in the size of permanent labour force, despite the passing of new labour legislation. At that time, wine farms were said to be still stuck in a low productivity and low wage model, with no formal contracts between farm workers and owners, no middle management (except in larger farms), and very low levels of unionization. The first signs of labour restructuring had emerged in some farms, where owners had cut their permanent work force, adopted technologies that minimized the need for such workforce, and were restricting the security of occupation on farms by hiring younger workers. These practices were to become the norm of labour management in wine farms in the following decade. In the mid-2000s, they characterized the changes in the wine industry resulting from deregulation, opening of export markets and regulation of labour a ‘double divide’. The first divide entails the winners and losers among cellars and farmers, depending on how positioned they are to make use of global export opportunities. The second divide is among the workers that remain in the permanent workforce (usually skilled ones) and those who have been casualized and externalized, and are now hired through labour contractors. This movement towards the minimization of a permanent labour force and the casualization of unskilled and low-skilled labour is not confined to the wine industry, but it is part of a wider process taking place in the Western Cape and elsewhere in South Africa, especially in labour-intensive farms. These casual workers are excluded from the basic entitlements that permanent workers have now gained. Despite reporting wages that may not be lower than permanent workers, casual workers face higher livelihood vulnerability and insecurity.

1.4 Consumption

17

Table 2: Per capita consumption of wine products on the domestic markets in 2010 year Year

Wine consumption – litres per capita

Natural wine Sparkling wine Fortified wine Total

2001 8.19 0.15 0.66 9.00 2002 8.03 0.17 0.68 8.88 2003 7.00 0.18 0.68 7.86 2004 6.73 0.18 0.68 7.59 2005 6.40 0.18 0.68 7.26 2006 6.31 0.19 0.71 7.21 2007 6.53 0.21 0.71 7.45 2008 6.43 0.21 0.69 7.33 2009 6.04 0.17 0.68 6.89 2010 6.18 0.18 0.67 7.03 Source: SAWIS Table 2 depicts per capita consumption of wine products in the domestic markets during the 2010 year. The table further depicts that the local consumption of wine has slightly declined in 2010 despite a rapid growth in the volume of exports in the last couple of years. South Africans have continued to consume all types of alcohol and have consumed increasing amounts of beer and spirits. At the same time the consumption of wine is hardly growing. The wine industry will therefore struggle to maintain a share in the market for alcoholic beverages in both the global and local markets.

2. MARKET STRUCTURE

The South African wine industry has gone through a tough period of major changes over the past decade, as largely reflected by the changes in its economic structure and institutional framework. Its re-introduction into the world trade setup has brought huge opportunities, as reflected by the increase in exports but on the other hand has brought pressure on its competitiveness, both locally and abroad. Table 3: Extend of the total South African wine industry Grapes crushed in tons

2008 2009 2010 2010/2009 TREND

White varieties 885 044 864 933 812 894 94.0 Red varieties 454 833 427 650 375 236 87.7 Table grapes 85 735 55 037 73 179 133.0 Total 1 425 612 1 347 620 1 261 309 3 147

18

Production in million litres

2008 2009 2010 2010/2009 TREND

Natural wine 763.30 805.1 780.7 97.0

Wine for brandy 86.6 71.4 39.6 55.5 Distilling wine 166.6 122.1 113.3 92.8 Grape juice concentrate and grape juice

72.5 34.8 51.2 147.1

Total 1 089.00 1 033.4 984.8 95.3 Domestic sales (wine) in million litres

2008 2009 2010 2010/2009 TREND

Natural wine 312.30 296.8 304.4 102.7 Fortified wine 33.70 33.4 33.1 99.1 Sparkling wine 10.1 8.5 8.9 104.7 Brandy @ absolute alcohol

19.3 18.1 17.0 93.9

Total 375.40 356.8 363.4 400.4 Exports (wine) in million litres

2008 2009 2010 2010/2009 TREND

Natural wine 407.4 389.1 371.0 95.3 Fortified wine 0.40 0.3 0.4 133.3 Sparkling wine 4.00 6.2 7.2 116.1 Total 411.80 395.6 378.6 95.7 Source: SAWIS Table 3 shows the extent of the total South African wine industry between 2008 and 2010 period. Out of a total of 1.26 million tons of grapes crushed in 2010 year, the trend in terms of percentages was 94.0% of white varieties, 87.7% were red varieties and 133% were table grapes. Total production was slightly over 1 billion litres, of which 97.0% was natural wine and the brandy was (55.5%), distilling wine (92.8%) and Grape juice concentrate and grape juice (147.1%). Natural wine sales constitute the vast majority of sales in both the domestic market (102.7%) and in the export market (95.3%). Reds make up 93.3% of domestic sales, even though they account for 55.5% of production. Fortified wines and sparkling wines are relatively small niches and sell almost exclusively on the domestic market.

By comparison, the industry in 2008 exhibited similar levels of grape production and similar make up in terms of production wine; rebate/distilling wine and non-alcoholic. However, natural wine exports represented approximately 95.5% of total sales (by volume) as the industry had just started to gear up for the international wine markets following the end of sanctions.

19

2.1 Domestic markets and prices

There is an extensive distribution of wholesalers and retailers, as well as producer cellars, estates and other organizations which market wine directly. They ensure that the product reach consumers around the country. The opposite picture applies to private cellars and producing wholesalers. Table 4: Varieties utilized for total wine making purposes during 2010

% of variety crushed by Variety Total Tons Private Wine

Cellars Producer Cellars

Producing Wholesalers

Chenin Blanc 270 391 9.2 88.1 2.7 Colombar(d) 266 504 3.9 95.7 0.4 Muscat dÁlexandrie

30 021 9.1 `90.3 0.6

Sauvignon Blanc 85 025 32.4 52.4 15.2 Cape Riesling 8 123 12.5 84.9 2.6 Chardonnay 71 543 21.8 69.9 8.4 Weisser Riesling 998 46.7 39.5 13.8 Semillon 14 620 22.9 69.8 7.3 Other white varieties

65 668 17.4 79.4 3.2

Table grapes 52 286 13.2 81.0 5.8 Total white varieties

865 180 12.0 84.0 3.9

Cabernet Sauvignon

84 863 27.8 52.0 20.1

Cinsaut 26 140 9.8 86.8 3.4

Pinotage 53 473 21.9 68.5 9.5 Merlot 58 479 28.8 52.7 18.4 Shiraz 87 882 25.2 59.8 15.0 Ruby Cabernet 30 396 6.9 91.7 1.3 Cabernet Franc 6 429 44.2 34.2 21.6 Pinot Noir 4 053 63.8 6.0 30.2 Other red varieties

23 520 42.3 45.4 12.3

Table grapes 20 893 0.1 99.9 - Total red varieties 396 129 23.8 62.8 13.4 Total white and red

1 261 309 15.7 77.4 6.9

Source: SAWIS Table 4 illustrates that cooperatives and ex-cooperatives (producer cellars) still crush approximately 80% of all grapes used for wine making locally. Along with a few producing wholesalers, they are the ones that can

20

provide economies of scale, competitive pricing and large volumes. These are essential requirements for supermarket chains to place wines on the shelf. The fact that cooperatives focus on run of the mill wines is an open secret, although it is perhaps insufficiently remarked in industry publications how much they have improved in the last decade in terms of quality – the result of technical improvements in both wine making and viticulture. Cooperatives crush a much higher proportion of white varieties than red, and a much lower proportion of their average share of highly sought varieties such as Sauvignon Blanc, Cabernet Sauvignon and Shiraz. Yet, they are still responsible for crushing over half of the production of these varieties, with the exception of Sauvignon Blanc. This is mainly due to climatic reasons as well as many cooperative farmers are located in warmer areas that are not friendly to this grape variety Table 5: Average prices of wine sold in bulk in South Africa

Varieties Cent per litre 2005 2006 2007 2008 2009 2010

All varieties 338.35 338.42 334.87 340.67 384.21 413.48 Cabernet Sauvignon 596.76 476.23 430.49 451.74 539.66 583.72 Merlot 471.33 426.29 396.68 417.67 495.26 556.81 Pinotage 443.73 392.88 396.68 410.15 472.69 535.38 Shiraz 548.21 514.37 458.12 471.89 560.82 601.86 All red varieties 440.49 406.02 374.41 386.75 459.08 502.97 Chardonnay 494.22 495.11 474.14 481.54 523.90 530.75 Sauvignon Blanc 522.11 547.53 517.21 519.00 546.06 538.00 Colombar 277.70 293.68 297.46 297.23 314.72 328.17 Chenin Blanc 304.43 317.27 323.17 321.45 350.23 367.89 All white varieties 297.57 310.51 314.46 314.71 345.44 364.98 NB. Price excludes added wine spirit

Cent per litre Concentrate/Sweet must for sweetening

2005 2006 2007 2008 2009 2010 240.21 236.43 262.13 293.28 362.17 365.57

Cent per litre @ 10% ALC/VOL

Wine for brandy 2005 2006 2007 2008 2009 29010 207.30 210.59 222.43 225.45 236.33 261.14

Cent per litre @ 10% ALC/VOL

Distilling wine 2005 2006 2007 2008 2009 2010 97.43 94.10 93.36 95.50 97.83 109.66

Table 5 shows average prices of wine sold in bulk in South Africa between 2005 and 2010 period. Table 5 further shows the global red wine glut that started in 2005 and has continued in the following 5 years. Chenin Blanc in 2009 was trading at 367.89 cents per litre as compared to 350.23 cents per litre in 2009. The price of wine for brandy has increased at an increasing rate from 2005 to 2010 and the price of distilling wine declined in 2006, 2007. In 2008 the price of distilling wine started to increase to 95.50 cents per litre until a peak was

21

attained in 2010 at approximately 109.66 cents per litre. Some cooperatives indicated that in 2010, they were profiting more from a hectare of vineyard that was being managed to produce distilling wine than from a hectare managed for table wine production. Globally, the wine industry is generally highly price responsive. Price movements, especially in global context, characterized by over production, high subsidized regimes, surplus removal schemes and export promotion support, fluctuate considerably, causing uncertainty and instability.

3. EXPORTS OF WINE OF FRESH GRAPES

This is a review of world level trade data for wines of fresh grapes, including fortified wines by South Africa between 2002 and 2010 period.

Figure 5: Exports volumes of wine of fresh grapes

(including fortfied wines) to various regions

0

1000000

2000000

3000000

4000000

5000000

Period (Years)

Exp

ort

s V

olu

mes

('000 l

itre

s)

Africa 1393702 751594 944000 961411 886602 1689415 2878630 3901246 3989565

Americas 93845 99752 144357 203269 174805 175863 194361 359172 333890

Asia 62165 92295 96295 98875 130751 1176662 270321 2317799 514215

Europe 871863 1643881 863465 941060 851457 1476093 962457 2798610 2826065

Oceania 39403 59410 25529 22356 12350 67639 103718 333004 294430

2002 2003 2004 2005 2006 2007 2008 2009 2010

Source: Quantec Figure 5 depicts exports volumes of wines of fresh grapes (including fortified wines) from South Africa to various regions between 2002 and 2010 period. The figure further depicts that the major export market for wines of fresh grapes from South Africa to the world was Africa followed by Europe and Asia. Exports of wine of fresh grapes from South Africa to Africa started to increase in 2002, with a slight decline between 2003 and 2006 years. In 2007 to 2009 years, exports of wine of fresh grapes from South Africa to Africa experienced an increase until a peak was attained in 2010 year at approximately 3.9 million litres. The figure also depicts that exports of wine of fresh grapes from South Africa to Europe attained a peak in 2010 year at approximately 2.8 million litres. The increase in exports of wines of fresh grapes from South Africa to Africa in the year 2010 represents 2.2% as compared to 2009 year.

22

Natural wine as a category makes up almost 99% of exports with the rest accounted by sparkling wine and fortified wines. Given the small size of exports of fortified wine, it is curious that the European Union (EU) forcefully insisted that South Africa drop the use of names ‘port’ and ‘sherry’ from exported products and that almost brought down the negotiations with South Africa on a bilateral trade agreement. Table 6: Types of exported wine and other liquor products (2010) in litres Types of wines and spirits

Bottled Bulk Total litres Litres AS % of

total per variety

Litres AS % of total per variety

2010

Chardonnay 14 827 514 63.07 8 681 086 36.93 23 508 600 Sauvignon Blanc 17 104 738 78.77 4 610 663 21.23 21 715 401 Chenin Blanc 18 693 288 40.41 27 562 503 59.59 46 255 791 Other white wine 39 911 240 57.37 29 658 367 42.63 69 569 607 Blanc de Noir and Rose

13 343 179 51.32 12 657 825 48.68 26 001 004

Cabernet Sauvignon

14 710 723 73.48 5 309 867 26.52 20 020 590

Shiraz 15 389 874 81.78 3 428 003 18.22 18 817 877 Pinotage 9 021 816 60.93 5 784 561 39.07 14 806 377 Merlot 9 521 362 82.05 2 082 310 17.95 11 603 672 Other red wine 69 808 694 58.82 48 865 714 41.18 118 674 408 Subtotal natural wine

222 332 428 59.93 148 640 899 40.07 370 973 327

Fortified wine 401 700 100.00 - - 401 700 Sparkling wine 7 174 873 100.00 - - 7 174 873 Total wine 229 909 001 60.73 148 640 899 39.27 378 549 900

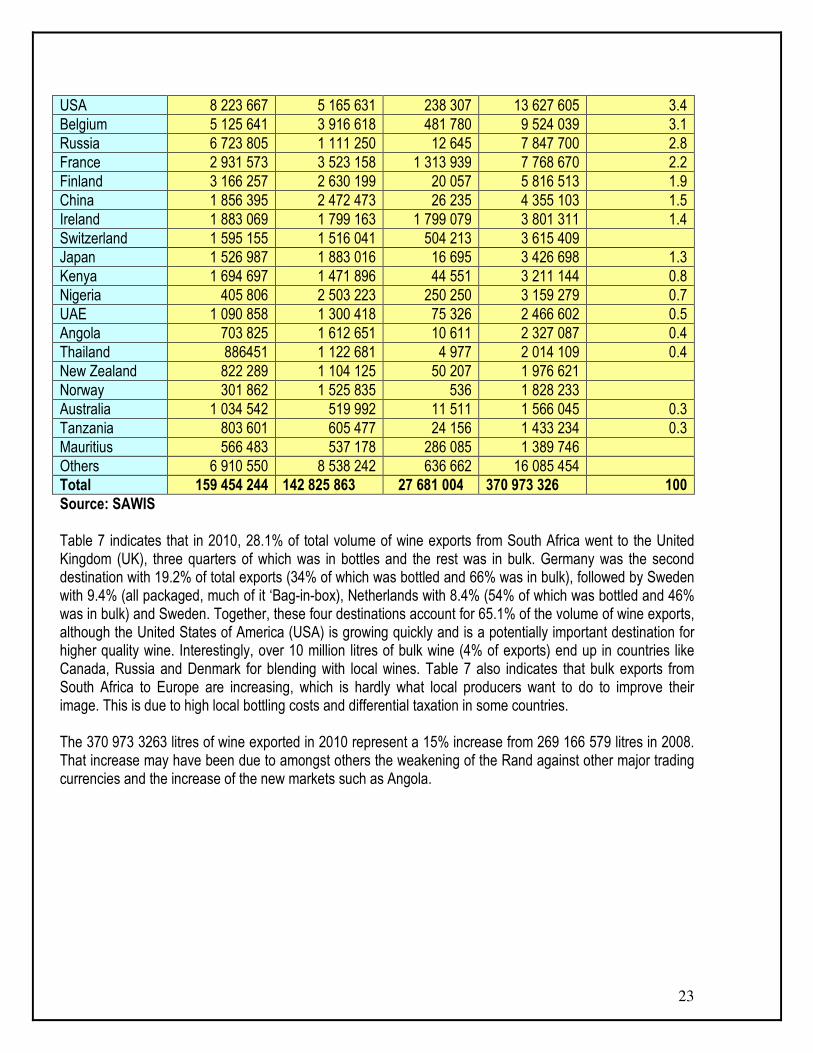

Source: SAWIS According to table 6, of the total exports in 2010, 60.73% was bottled wine and 39.27% was bulk wine. The varieties with the highest bottled-to-bulk export ratio are not surprisingly, noble varieties such as Shiraz, Cabernet Sauvignon, Sauvignon Blanc, Merlot and Chardonnay. The highest proportion of bulk exports is under ‘other red wines’. Table 7: Bottled and bulk natural wine exports by country in litres (2010)

Country Total (Bottled and bulk) White Red Blanc de

Noir/Rosé Total % of total

exports

UK 48 224 807 45 663 402 11 044 246 104 932 455 28.1 Germany 28 307 937 38 352 301 5 651 713 72 311 951 19.2 Sweden 13 484 770 24 104 596 687 540 38 276 906 9.4 Netherlands 10 729 053 12 339 834 3 771 053 26 839 940 8.4 Denmark 3 980 170 12 751 177 602 080 17 333 427 4.3 Canada 8 069 149 5 852 346 116 550 14 038 045 4.2

23

USA 8 223 667 5 165 631 238 307 13 627 605 3.4 Belgium 5 125 641 3 916 618 481 780 9 524 039 3.1 Russia 6 723 805 1 111 250 12 645 7 847 700 2.8 France 2 931 573 3 523 158 1 313 939 7 768 670 2.2 Finland 3 166 257 2 630 199 20 057 5 816 513 1.9 China 1 856 395 2 472 473 26 235 4 355 103 1.5 Ireland 1 883 069 1 799 163 1 799 079 3 801 311 1.4 Switzerland 1 595 155 1 516 041 504 213 3 615 409 Japan 1 526 987 1 883 016 16 695 3 426 698 1.3 Kenya 1 694 697 1 471 896 44 551 3 211 144 0.8 Nigeria 405 806 2 503 223 250 250 3 159 279 0.7 UAE 1 090 858 1 300 418 75 326 2 466 602 0.5 Angola 703 825 1 612 651 10 611 2 327 087 0.4 Thailand 886451 1 122 681 4 977 2 014 109 0.4 New Zealand 822 289 1 104 125 50 207 1 976 621 Norway 301 862 1 525 835 536 1 828 233 Australia 1 034 542 519 992 11 511 1 566 045 0.3 Tanzania 803 601 605 477 24 156 1 433 234 0.3 Mauritius 566 483 537 178 286 085 1 389 746 Others 6 910 550 8 538 242 636 662 16 085 454 Total 159 454 244 142 825 863 27 681 004 370 973 326 100 Source: SAWIS Table 7 indicates that in 2010, 28.1% of total volume of wine exports from South Africa went to the United Kingdom (UK), three quarters of which was in bottles and the rest was in bulk. Germany was the second destination with 19.2% of total exports (34% of which was bottled and 66% was in bulk), followed by Sweden with 9.4% (all packaged, much of it ‘Bag-in-box), Netherlands with 8.4% (54% of which was bottled and 46% was in bulk) and Sweden. Together, these four destinations account for 65.1% of the volume of wine exports, although the United States of America (USA) is growing quickly and is a potentially important destination for higher quality wine. Interestingly, over 10 million litres of bulk wine (4% of exports) end up in countries like Canada, Russia and Denmark for blending with local wines. Table 7 also indicates that bulk exports from South Africa to Europe are increasing, which is hardly what local producers want to do to improve their image. This is due to high local bottling costs and differential taxation in some countries. The 370 973 3263 litres of wine exported in 2010 represent a 15% increase from 269 166 579 litres in 2008. That increase may have been due to amongst others the weakening of the Rand against other major trading currencies and the increase of the new markets such as Angola.

24

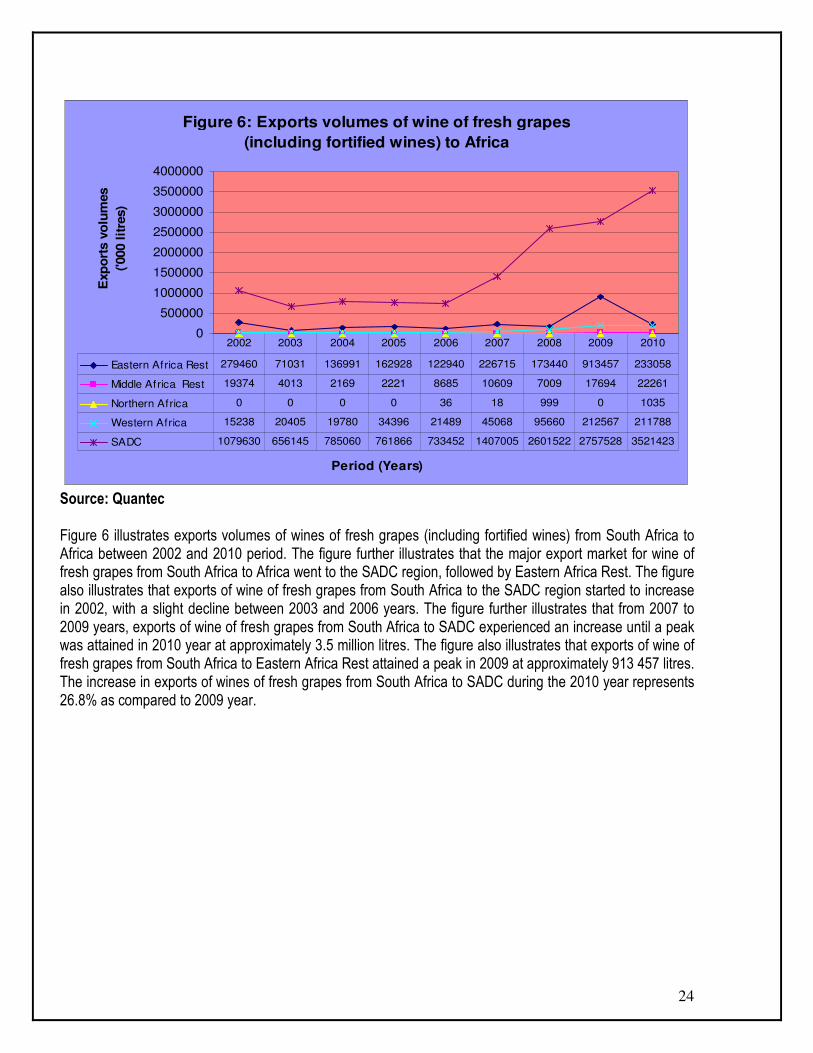

Figure 6: Exports volumes of wine of fresh grapes

(including fortified wines) to Africa

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

4000000

Period (Years)

Exp

ort

s v

olu

mes

('000 l

itre

s)

Eastern Africa Rest 279460 71031 136991 162928 122940 226715 173440 913457 233058

Middle Africa Rest 19374 4013 2169 2221 8685 10609 7009 17694 22261

Northern Africa 0 0 0 0 36 18 999 0 1035

Western Africa 15238 20405 19780 34396 21489 45068 95660 212567 211788

SADC 1079630 656145 785060 761866 733452 1407005 2601522 2757528 3521423

2002 2003 2004 2005 2006 2007 2008 2009 2010

Source: Quantec Figure 6 illustrates exports volumes of wines of fresh grapes (including fortified wines) from South Africa to Africa between 2002 and 2010 period. The figure further illustrates that the major export market for wine of fresh grapes from South Africa to Africa went to the SADC region, followed by Eastern Africa Rest. The figure also illustrates that exports of wine of fresh grapes from South Africa to the SADC region started to increase in 2002, with a slight decline between 2003 and 2006 years. The figure further illustrates that from 2007 to 2009 years, exports of wine of fresh grapes from South Africa to SADC experienced an increase until a peak was attained in 2010 year at approximately 3.5 million litres. The figure also illustrates that exports of wine of fresh grapes from South Africa to Eastern Africa Rest attained a peak in 2009 at approximately 913 457 litres. The increase in exports of wines of fresh grapes from South Africa to SADC during the 2010 year represents 26.8% as compared to 2009 year.

25

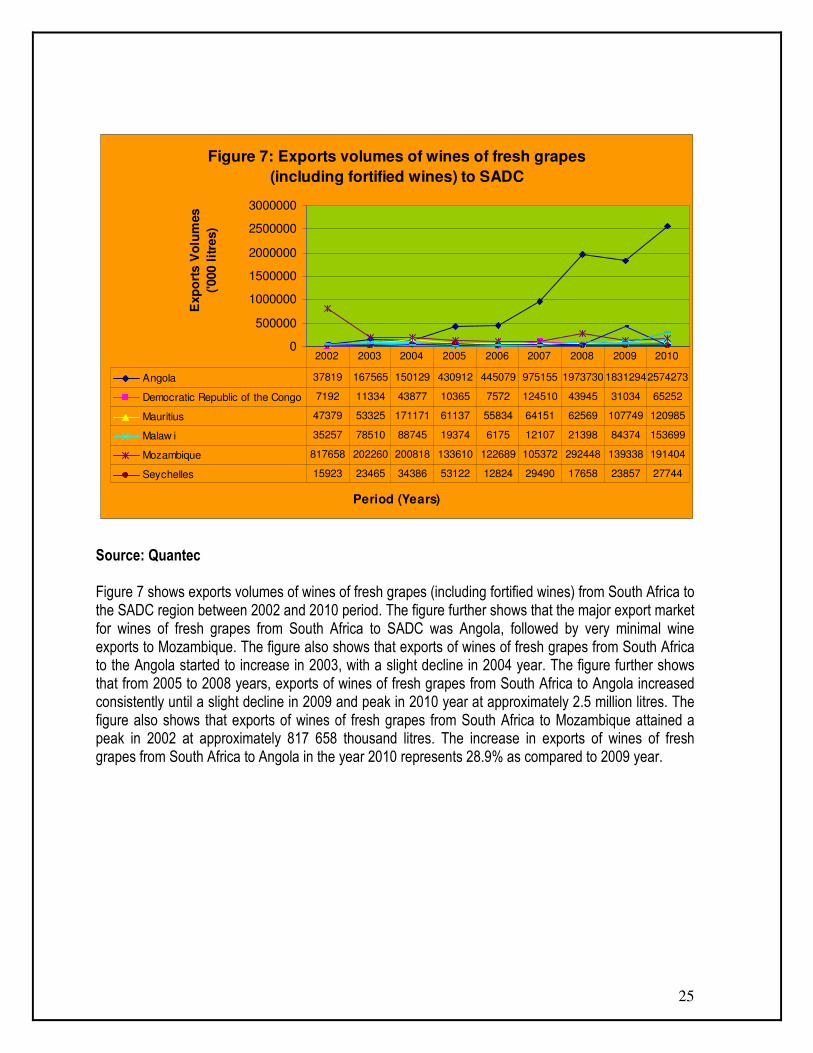

Figure 7: Exports volumes of wines of fresh grapes

(including fortified wines) to SADC

0

500000

1000000

1500000

2000000

2500000

3000000

Period (Years)

Exp

ort

s V

olu

mes

('000 l

itre

s)

Angola 37819 167565 150129 430912 445079 975155 1973730 18312942574273

Democratic Republic of the Congo 7192 11334 43877 10365 7572 124510 43945 31034 65252

Mauritius 47379 53325 171171 61137 55834 64151 62569 107749 120985

Malaw i 35257 78510 88745 19374 6175 12107 21398 84374 153699

Mozambique 817658 202260 200818 133610 122689 105372 292448 139338 191404

Seychelles 15923 23465 34386 53122 12824 29490 17658 23857 27744

2002 2003 2004 2005 2006 2007 2008 2009 2010

Source: Quantec Figure 7 shows exports volumes of wines of fresh grapes (including fortified wines) from South Africa to the SADC region between 2002 and 2010 period. The figure further shows that the major export market for wines of fresh grapes from South Africa to SADC was Angola, followed by very minimal wine exports to Mozambique. The figure also shows that exports of wines of fresh grapes from South Africa to the Angola started to increase in 2003, with a slight decline in 2004 year. The figure further shows that from 2005 to 2008 years, exports of wines of fresh grapes from South Africa to Angola increased consistently until a slight decline in 2009 and peak in 2010 year at approximately 2.5 million litres. The figure also shows that exports of wines of fresh grapes from South Africa to Mozambique attained a peak in 2002 at approximately 817 658 thousand litres. The increase in exports of wines of fresh grapes from South Africa to Angola in the year 2010 represents 28.9% as compared to 2009 year.

26

Figure 8: Exports volumes of wines of fresh grapes

(including fortified wines) to the Americas

0

50000

100000

150000

200000

250000

300000

350000

Period (Years)

Exp

ort

s v

olu

mes

('000 l

itre

s)

Caribbean 16568 23958 34627 42691 24750 46276 46395 29588 40410

Central America 81 18 9 316 0 9 22 0 0

Northern America 0 45 90 0 0 0 0 0 0

South America 13396 10495 13055 73360 2717 1683 2483 11520 14433

NAFTA 63800 65236 96576 86902 147338 127895 145461 318064 279047

2002 2003 2004 2005 2006 2007 2008 2009 2010

Source: Quantec Figure 8 illustrates exports volumes of wines of fresh grapes (including fortified wines) from South Africa to the Americas between 2002 and 2010 period. The figure further illustrates that the major market for wines of fresh grapes from South Africa to the Americas was mainly NAFTA, followed by South America. The figure also illustrates that exports of wines of fresh grapes from South Africa to NAFTA has been generally increasing between 2002 and 2010 period, a peak was attained in 2009 at approximately 318 064 litres. The figure also illustrates that exports of wines of fresh grapes from South Africa to South America attained a peak in 2005 at approximately 73 360 litres. The decline in exports of wines of fresh grapes from South Africa to NAFTA in the year 2010 represents 14.8% as compared to 2009 year.

27

Figure 9: Exports volumes of wines of fresh grapes

(including fortified wines) to Asia

0

500000

1000000

1500000

2000000

2500000

Period (Years)

Exp

ort

s v

olu

mes

('000 l

itre

s)

Eastern Asia 54951 63709 65269 65121 75792 1114614 173855 2188709 395609

South-central Asia 1876 9538 4039 3740 10867 11172 12863 12674 17112

South-eastern Asia 2633 3592 5018 5556 7322 8643 24775 49586 26375

Western Asia 2705 15456 21969 24458 36770 42233 58828 66830 75119

2002 2003 2004 2005 2006 2007 2008 2009 2010

Source: Quantec Figure 9 indicates exports volumes of wines of fresh grapes (including fortified wines) from South Africa to Asia between 2002 and 2010 period. The figure further indicates that the major market for wines of fresh grapes from South Africa to Asia was mainly Eastern Asia. The three other Asia regions had very minimal exports of wines of fresh grapes from South Africa during the period under review. The figure also indicates that exports of wines of fresh grapes from South Africa to Eastern Asia attained a peak in 2009 at approximately 2.1 million litres. The figure further indicates that in 2010 year, there was a dramatic decline in wine exports of fresh grapes from South Africa to Eastern Asia. The dramatic decline in exports of wines of fresh grapes from South Africa to Eastern Asia in the year 2010 represents 453% as compared to 2009 year.

28

Figure 10: Exports volumes of wines of fresh grapes

(including fortified wines) to Europe

0

500000

1000000

1500000

2000000

2500000

3000000

Period (Years)

Exp

ort

s v

olu

mes

('000 l

itre

s)

Eastern Europe 5625 9729 10203 25209 39447 45743 71896 48150 90778

Northern Europe 45 810 1233 720 855 738 3217 6462 3601

Southern Europe 0 0 0 5 0 0 792 515 0

Western Europe Rest 9770 31972 20956 39225 18491 19694 26269 30435 24693

European Union 856423 1601370 831073 875901 792664 1409918 860283 2713048 2706993

2002 2003 2004 2005 2006 2007 2008 2009 2010

Source: Quantec Figure 10 depicts exports volumes of wines of fresh grapes (including fortified wines) from South Africa to Europe between 2002 and 2010 period. The figure further depicts that the major market for wines of fresh grapes from South Africa to Europe was mainly European Union. The other four European regions had very low levels of wine exports from South Africa during the period under scrutiny. The figure also depicts that exports of wines of fresh grapes from South Africa to the European Union attained a peak in 2009 at approximately 2.7 million litres. The figure also depicts that in 2010, there was a slight decline in wine exports of fresh grapes from South Africa to the European Union. The slight decline in exports of wines of fresh grapes from South Africa to the European Union in the year 2010 represents 0.2% as compared to 2009 year.

29

Figure 11: Exports volumes of wines of fresh grapes

(including fortified wines) to Oceania

0

50000

100000

150000

200000

250000

300000

350000

Period (Years)

Exp

ort

s v

olu

mes (

'000 l

itre

s)

Australia and New Zealand 39403 59410 25529 22356 12350 67639 103718 333004 293962

Melanesia 0 0 0 0 0 0 0 0 468

2002 2003 2004 2005 2006 2007 2008 2009 2010

Source: Quantec

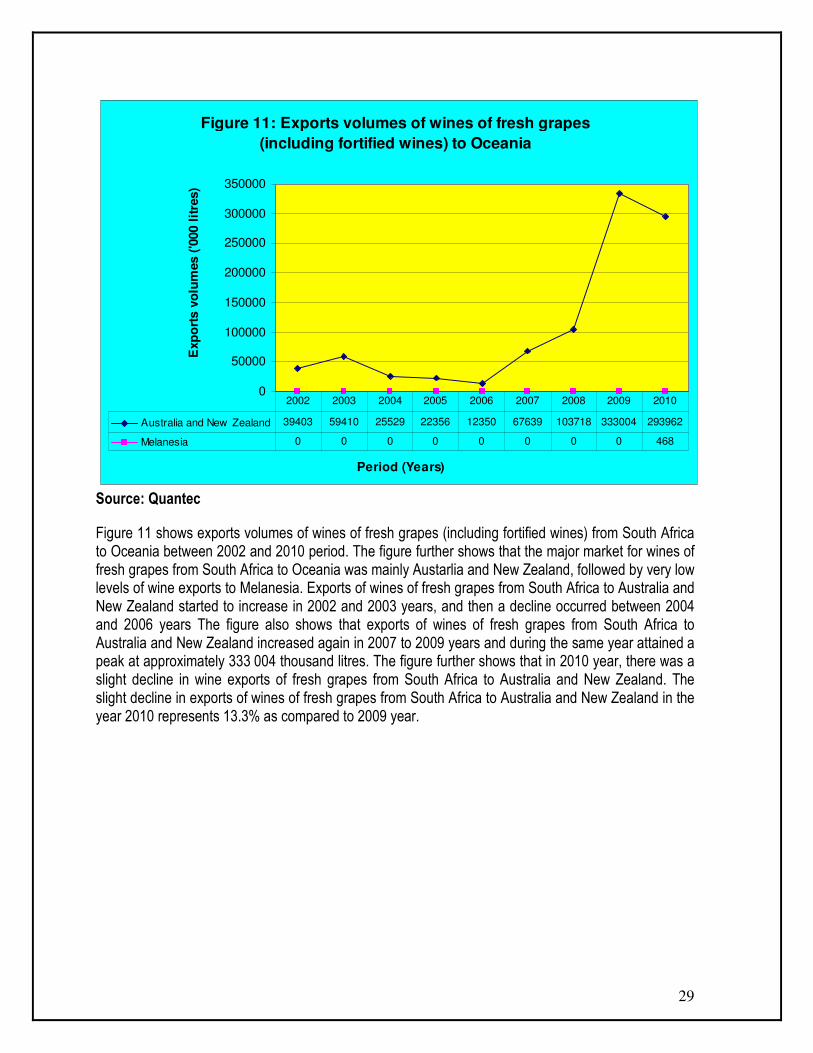

Figure 11 shows exports volumes of wines of fresh grapes (including fortified wines) from South Africa to Oceania between 2002 and 2010 period. The figure further shows that the major market for wines of fresh grapes from South Africa to Oceania was mainly Austarlia and New Zealand, followed by very low levels of wine exports to Melanesia. Exports of wines of fresh grapes from South Africa to Australia and New Zealand started to increase in 2002 and 2003 years, and then a decline occurred between 2004 and 2006 years The figure also shows that exports of wines of fresh grapes from South Africa to Australia and New Zealand increased again in 2007 to 2009 years and during the same year attained a peak at approximately 333 004 thousand litres. The figure further shows that in 2010 year, there was a slight decline in wine exports of fresh grapes from South Africa to Australia and New Zealand. The slight decline in exports of wines of fresh grapes from South Africa to Australia and New Zealand in the year 2010 represents 13.3% as compared to 2009 year.

30

3.1 Provincial and district export values of South African wines A review of provincial level trade data shows that the Western Cape Province had high export values over the past decade. This can be attributed to the fact that the province is firstly the leader in both the production and export of the wine. Secondly, the registered exporters are based in the province and thirdly, the province has the Cape Town harbour that serves as an exit point for wine products. Figure 5 below depicts the value of wine exports from each province of South Africa.

Figure 12: Value of wine exports by Provinces

0

2000000000

4000000000

6000000000

8000000000

10000000000

12000000000

14000000000

Period (Years)

Ex

po

rt V

alu

e (

Ra

nd

s)

Western Cape 3821713735 5791908707 6145611294 6696146174 7326168443 6966343604 9194101729 122255948381182021285811102800919

Eastern Cape 8223271 15691922 16407118 14180636 8648680 12051222 16922156 12545574 15089793 22082640

Northern Cape 719164 6146720 3086187 8459123 13490440 3202212 4728185 7417316 2269996 5713192

Free State 11658 198476 90874 1354226 397086 2835833 287851 911565 578 1470

Kw azulu-Natal 10860663 13460852 13268941 14129983 19708725 21352378 33498644 37761478 28309107 45644345

North West 109751 3179 800924 73936 410524 879842 708414 345299 3248665 2686491

Gauteng 98846763 173123292 122128937 139047537 239621909 119584708 210859906 173421635 133542430 189174221

Mpumalanga 124270 69086 213066 457068 1470594 0 127722 53432 781767 154110

Limpopo 1983462 19235 1600 107933 3642950 756261 2649352 2089 27420488 75377503

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Source: Quantec Figure 12 shows the value of wine exports by provinces of South Africa to the world between 2001 and 2010 period. The graph further shows that between 2001 and 2010 period, Western Cape Province was the top wine exporting province in South Africa followed by Gauteng and KwaZulu-Natal Provinces. During the same period under examination, exports of wine from the Western Cape Province attained a peak in 2008 at approximately R122 billion. The graph also shows that there were fewer fluctuations in terms of the exports of wine by the Western Cape Province during the period

31

under review. Other provinces featured intermittently but usually registered very low values in terms of trade. The slight decline in exports of wine from the Western Cape Province to the world in the year 2010 represents 6.5% as compared to 2009 year. The Western Cape Province is generally a major producer and exporter of wine in South Africa.

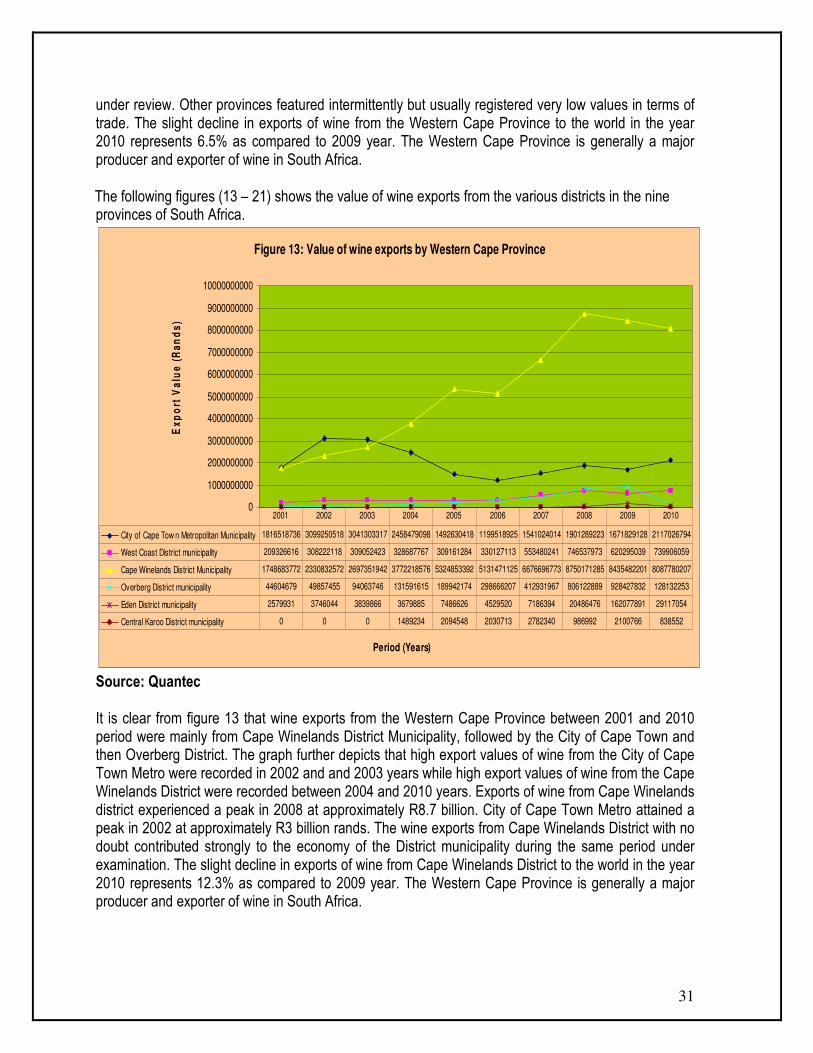

The following figures (13 – 21) shows the value of wine exports from the various districts in the nine provinces of South Africa.

Figure 13: Value of wine exports by Western Cape Province

0

1000000000

2000000000

3000000000

4000000000

5000000000

6000000000

7000000000

8000000000

9000000000

10000000000

Period (Years)

Ex

po

rt V

alu

e (

Ra

nd

s)

City of Cape Tow n Metropolitan Municipality 1816518736 3099250518 3041303317 2458479098 1492630418 1199518925 1541024014 1901289223 1671829128 2117026794

West Coast District municipality 209326616 308222118 309052423 328687767 309161284 330127113 553480241 746537973 620295039 739906059

Cape Winelands District Municipality 1748683772 2330832572 2697351942 3772218576 5324853392 5131471125 6676696773 8750171285 8435482201 8087780207

Overberg District municipality 44604679 49857455 94063746 131591615 189942174 298666207 412931967 806122889 928427832 128132253

Eden District municipality 2579931 3746044 3839866 3679885 7486626 4529520 7186394 20486476 162077891 29117054

Central Karoo District municipality 0 0 0 1489234 2094548 2030713 2782340 986992 2100766 838552

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Source: Quantec It is clear from figure 13 that wine exports from the Western Cape Province between 2001 and 2010 period were mainly from Cape Winelands District Municipality, followed by the City of Cape Town and then Overberg District. The graph further depicts that high export values of wine from the City of Cape Town Metro were recorded in 2002 and and 2003 years while high export values of wine from the Cape Winelands District were recorded between 2004 and 2010 years. Exports of wine from Cape Winelands district experienced a peak in 2008 at approximately R8.7 billion. City of Cape Town Metro attained a peak in 2002 at approximately R3 billion rands. The wine exports from Cape Winelands District with no doubt contributed strongly to the economy of the District municipality during the same period under examination. The slight decline in exports of wine from Cape Winelands District to the world in the year 2010 represents 12.3% as compared to 2009 year. The Western Cape Province is generally a major producer and exporter of wine in South Africa.

32

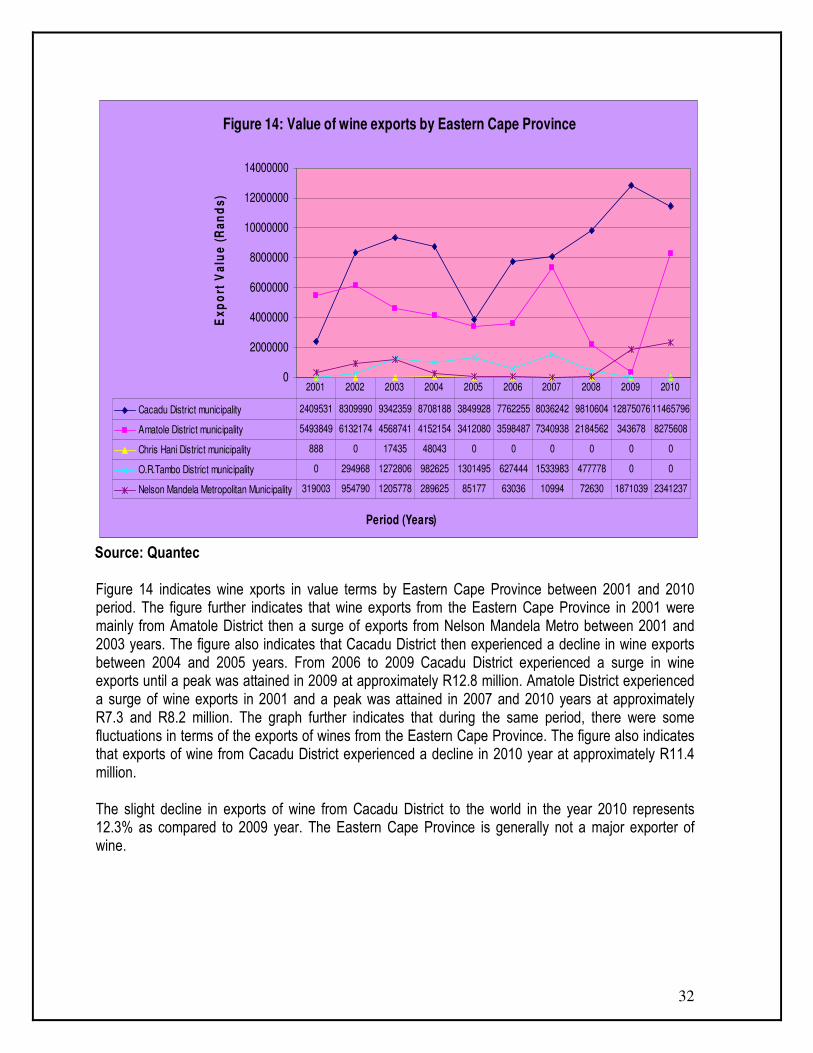

Figure 14: Value of wine exports by Eastern Cape Province

0

2000000

4000000

6000000

8000000

10000000

12000000

14000000

Period (Years)

Ex

po

rt V

alu

e (

Ra

nd

s)

Cacadu District municipality 2409531 8309990 9342359 8708188 3849928 7762255 8036242 9810604 12875076 11465796

Amatole District municipality 5493849 6132174 4568741 4152154 3412080 3598487 7340938 2184562 343678 8275608

Chris Hani District municipality 888 0 17435 48043 0 0 0 0 0 0

O.R.Tambo District municipality 0 294968 1272806 982625 1301495 627444 1533983 477778 0 0

Nelson Mandela Metropolitan Municipality 319003 954790 1205778 289625 85177 63036 10994 72630 1871039 2341237

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Source: Quantec Figure 14 indicates wine xports in value terms by Eastern Cape Province between 2001 and 2010 period. The figure further indicates that wine exports from the Eastern Cape Province in 2001 were mainly from Amatole District then a surge of exports from Nelson Mandela Metro between 2001 and 2003 years. The figure also indicates that Cacadu District then experienced a decline in wine exports between 2004 and 2005 years. From 2006 to 2009 Cacadu District experienced a surge in wine exports until a peak was attained in 2009 at approximately R12.8 million. Amatole District experienced a surge of wine exports in 2001 and a peak was attained in 2007 and 2010 years at approximately R7.3 and R8.2 million. The graph further indicates that during the same period, there were some fluctuations in terms of the exports of wines from the Eastern Cape Province. The figure also indicates that exports of wine from Cacadu District experienced a decline in 2010 year at approximately R11.4 million. The slight decline in exports of wine from Cacadu District to the world in the year 2010 represents 12.3% as compared to 2009 year. The Eastern Cape Province is generally not a major exporter of wine.

33

Figure 15: Value of wine exports by Northern Cape Province

0

2000000

4000000

6000000

8000000

10000000

12000000

14000000

Period (Years)

Exp

ort

Valu

e (

Ran

ds)

Pixley ka Seme District municipality 0 2226149 0 383552 411315 1019 0 0 0 1361381

Siyanda District municipality 440840 3271354 2644739 8075571 13079125 3201193 4728185 7417316 2269996 4351811

Frances Baard District municipality 278324 649216 441449 0 0 0 0 0 0 0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Source: Quante It is clear from figure 15 that wine exports from the Northern Cape Province were mainly from Siyanda District Municipality between 2001 and 2010 period. The figure further illustrates that high export values of wine for the leading municipality were recorded in 2002, 2005, 2008 and 2010 years. The figure also illustrates that exports of wine from Siyanda District attained a peak in 2005 year at approximately R13 million rands. The graph also illustrates that Pixley ka Seme District was the second with higher values of wine exports during the period under scrutiny. The graph further illustrates that there were a number of declines in exports of wine from Siyanda District in 2003, 2006 and 2009 years. In 2010 year, exports of wine from Siyanda District started to increase again at approximately R4.3 million rands. The increase in exports of wine from Siyanda District to the world in the year 2010 represents 47.8% as compared to 2009 year. The Northern Cape Province is generally not a major wine exporter.

34

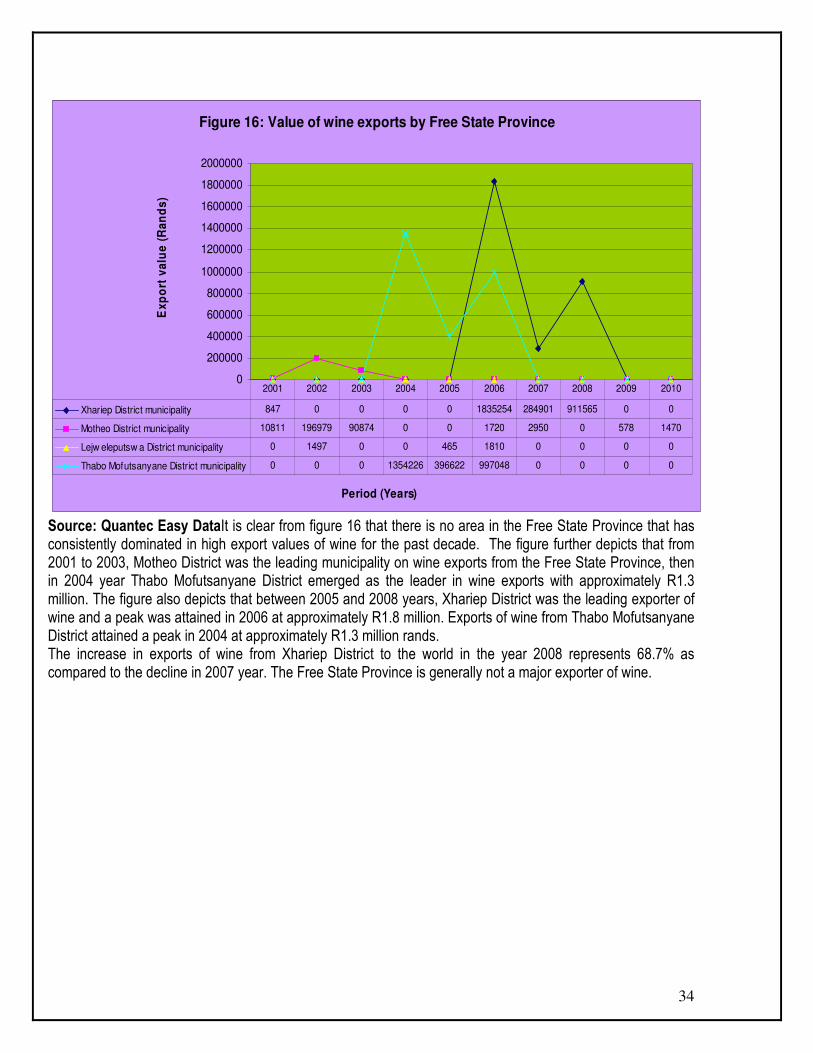

Figure 16: Value of wine exports by Free State Province

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

1800000

2000000

Period (Years)

Ex

po

rt v

alu

e (

Ra

nd

s)

Xhariep District municipality 847 0 0 0 0 1835254 284901 911565 0 0

Motheo District municipality 10811 196979 90874 0 0 1720 2950 0 578 1470

Lejw eleputsw a District municipality 0 1497 0 0 465 1810 0 0 0 0

Thabo Mofutsanyane District municipality 0 0 0 1354226 396622 997048 0 0 0 0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Source: Quantec Easy DataIt is clear from figure 16 that there is no area in the Free State Province that has consistently dominated in high export values of wine for the past decade. The figure further depicts that from 2001 to 2003, Motheo District was the leading municipality on wine exports from the Free State Province, then in 2004 year Thabo Mofutsanyane District emerged as the leader in wine exports with approximately R1.3 million. The figure also depicts that between 2005 and 2008 years, Xhariep District was the leading exporter of wine and a peak was attained in 2006 at approximately R1.8 million. Exports of wine from Thabo Mofutsanyane District attained a peak in 2004 at approximately R1.3 million rands. The increase in exports of wine from Xhariep District to the world in the year 2008 represents 68.7% as compared to the decline in 2007 year. The Free State Province is generally not a major exporter of wine.

35

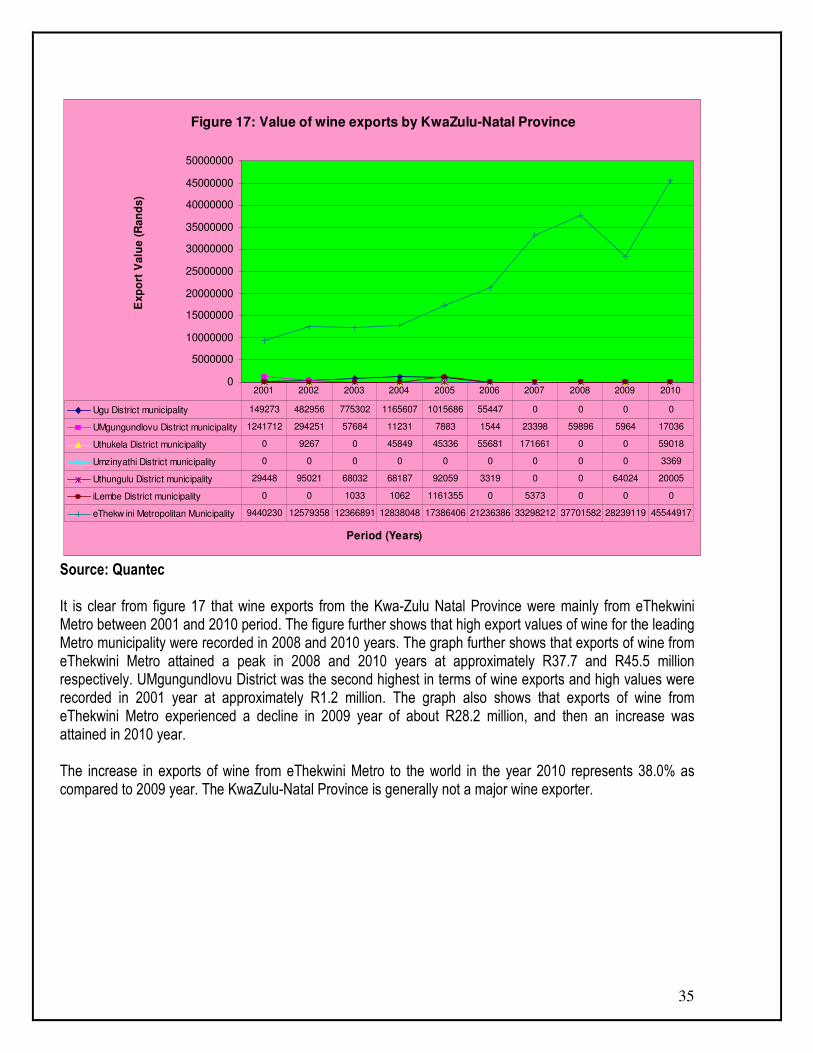

Figure 17: Value of wine exports by KwaZulu-Natal Province

0

5000000

10000000

15000000

20000000

25000000

30000000

35000000

40000000

45000000

50000000

Period (Years)

Exp

ort

Valu

e (

Ran

ds)

Ugu District municipality 149273 482956 775302 1165607 1015686 55447 0 0 0 0

UMgungundlovu District municipality 1241712 294251 57684 11231 7883 1544 23398 59896 5964 17036

Uthukela District municipality 0 9267 0 45849 45336 55681 171661 0 0 59018

Umzinyathi District municipality 0 0 0 0 0 0 0 0 0 3369

Uthungulu District municipality 29448 95021 68032 68187 92059 3319 0 0 64024 20005

iLembe District municipality 0 0 1033 1062 1161355 0 5373 0 0 0

eThekw ini Metropolitan Municipality 9440230 12579358 12366891 12838048 17386406 21236386 33298212 37701582 28239119 45544917

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Source: Quantec

It is clear from figure 17 that wine exports from the Kwa-Zulu Natal Province were mainly from eThekwini Metro between 2001 and 2010 period. The figure further shows that high export values of wine for the leading Metro municipality were recorded in 2008 and 2010 years. The graph further shows that exports of wine from eThekwini Metro attained a peak in 2008 and 2010 years at approximately R37.7 and R45.5 million respectively. UMgungundlovu District was the second highest in terms of wine exports and high values were recorded in 2001 year at approximately R1.2 million. The graph also shows that exports of wine from eThekwini Metro experienced a decline in 2009 year of about R28.2 million, and then an increase was attained in 2010 year. The increase in exports of wine from eThekwini Metro to the world in the year 2010 represents 38.0% as compared to 2009 year. The KwaZulu-Natal Province is generally not a major wine exporter.

36

Figure 18: Value of wine exports by North West Province

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

Period (Years)

Ex

po

rt v

alu

e (

Ra

nd

s)

Bojanala District municipality 109512 1909 381967 4297 409167 85447 0 35601 0 49618

Central District municipality 0 0 418857 69639 0 790149 685773 305703 0 0

Southern District municipality 239 1270 101 0 1358 4246 22641 3995 3248665 2636873

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Source: Quantec

Figure 18 indicates values of wine exports from North West Province between 2001 and 2010 period. During the same period under examination, the graph indicates that exports of wine from North West were mainly from Southern District, followed by Central and Bojanala Districts. The figure also indicates that exports of wine from Southern District started to increase in 2009 year, and during the same year attained a peak at approximately R3.2 million. High export values for the leading municipality were recorded in 2009 and 2010 years. Exports of wine from Central District started to increase in 2003, and then a decline occurred in 2004 and 2005 years until a peak was attained in 2006 at approximately R790 149. In 2010 year, exports of wine from Southern District experienced a decline of about R2.6 million.

The sharp decline in exports of wine from Southern District to the world in the year 2010 represents 23.2% as compared to 2009 year. The North West Province is generally not a major wine exporter.

37

Figure 19: Value of wine exports by Gauteng Province

0

20000000

40000000

60000000

80000000

100000000

120000000

140000000

160000000

180000000

200000000

Period (Years)

Ex

po

rt V

alu

e (

Ra

nd

s)

Sedibeng District municipality 1921431 29609347 772757 702933 273337 551 60141 1200000 36003 198

Metsw eding District Municipality 0 4707 278696 0 31638 0 100 0 822005 17324

West Rand District Municipality 611775 265874 354958 348765 570856 310475 423550 1320486 5077630 787670

Ekurhuleni Metropolitan Municipality 59480308 94908832 64428088 46019445 178256077 52717999 148404961 63287571 67519719 82628321

City of Johannesburg Metropolitan Municipality 35124295 46876826 55310749 90399592 55620462 65012561 61014040 105752354 59077655 102952611

City of Tshw ane Metropolitan Municipality 1708955 1457705 983690 1576802 4869539 1543122 957113 1861225 1009417 2788098

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Source: Quantec

Figure 19 illustrates values of wine exports by Gauteng Province between 2001 and 2010 period. Wine exports as illustrated in figure 19 originated mainly from Ekurhuleni Metro followed closely by the City of Johannesburg Metro. During the period under scrutiny, wine exports from Ekurhuleni Metro attained a peak in 2005 at approximately R178 million. City of Johannesburg Metro also contributed strongly to the economy of Gauteng Province during the same period under examination. The figure further illustrates that wine exports from the City of Johannesburg Metro attained a peak in 2005 at approximately R105 million. The figure also illustrates that there was a decline in wine exports from Ekurhuleni Metro to the world in 2003, 2004, 2006 and 2008 years. The graph also illustrates that in 2009 and 2010 years, wine exports started to increase again to approximately R82 million. The increase in exports of wine from Ekurhuleni Metro to the world in the year 2010 represents 18.3% as compared to 2009 year. The Gauteng Province is generally not a major wine exporter.

38

Figure 20: Value of wine exports by Mpumalanga Province

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

Period (Years)

Ex

po

rt V

alu

e (

Ra

nd

s)

Gert Sibande District municipality 0 0 94590 0 0 0 0 0 7798 2198

Nkangala District municipality 200 0 0 3334 126137 0 0 698 773322 0

Ehlanzeni District municipality 124070 69086 118477 453734 1344457 0 127722 52734 647 151912

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Source: Quantec Figure 20 indicates values of wine exports from Mpumalanga Province to the world between 2001 and 2010 period. It is further clear from figure 20 that wine exports from the Mpumalanga Province were mainly from Ehlanzeni District during the period under examination. The graph also indicates that Nkangala District came second in terms of wine exports from Mpumalanga Province. Exports of wine from Ehlanzeni District attained a peak in 2005 at approximately R1.3 million, while exports of wine from Nkangala district attained a peak in 2009 at approximately R773 322. The graph also indicates that there was a surge of wine exports from 2004 to 2005 years. Exports of wine from Ehlanzeni district declined dramatically in 2009, and a slight increase occurred in 2010 year. The increase in exports of wine from Ehlanzeni District to the world in the year 2010 represents 99.6% as compared to 2009 year. The Mpumalanga Province is generally not a major wine exporter.

39

Figure 21: Value of wine exports by Limpopo Province

0

10000000

20000000

30000000

40000000

50000000

60000000

70000000

80000000

Period (Years)

Ex

po

rt V

alu

e (

Ra

nd

s)

Mopani District municipality 0 2401 1600 0 88671 0 0 2089 0 0

Vhembe District municipality 1983462 11657 0 0 4226 756261 2352185 0 26961717 74422047

Capricorn District municipality 0 0 0 105321 3550054 0 0 0 0 0

Waterberg District municipality 0 5176 0 2612 0 0 297167 0 451236 955457

Greater Sekhukhune District Municipality 0 0 0 0 0 0 0 0 7535 0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Source: Quantec Figure 21 depicts values of wine exports by Limpopo Province between 2001 and 2010 period. The figure further depicts that wine exports from Limpopo Province were mainly from Vhembe District followed by very low levels of wine exports from Capricorn District. The graph also depicts that Vhembe District attained a peak in wine exports in 2010 at approximately R74 million. However, Capricorn District has emerged as a second wine exporter in the province between 2001 and 2010 period. The increase in exports of wine from Vhembe District to the world in the year 2010 represents 63.7% as compared to 2009 year. The Limpopo province is generally not a major wine exporter.

40

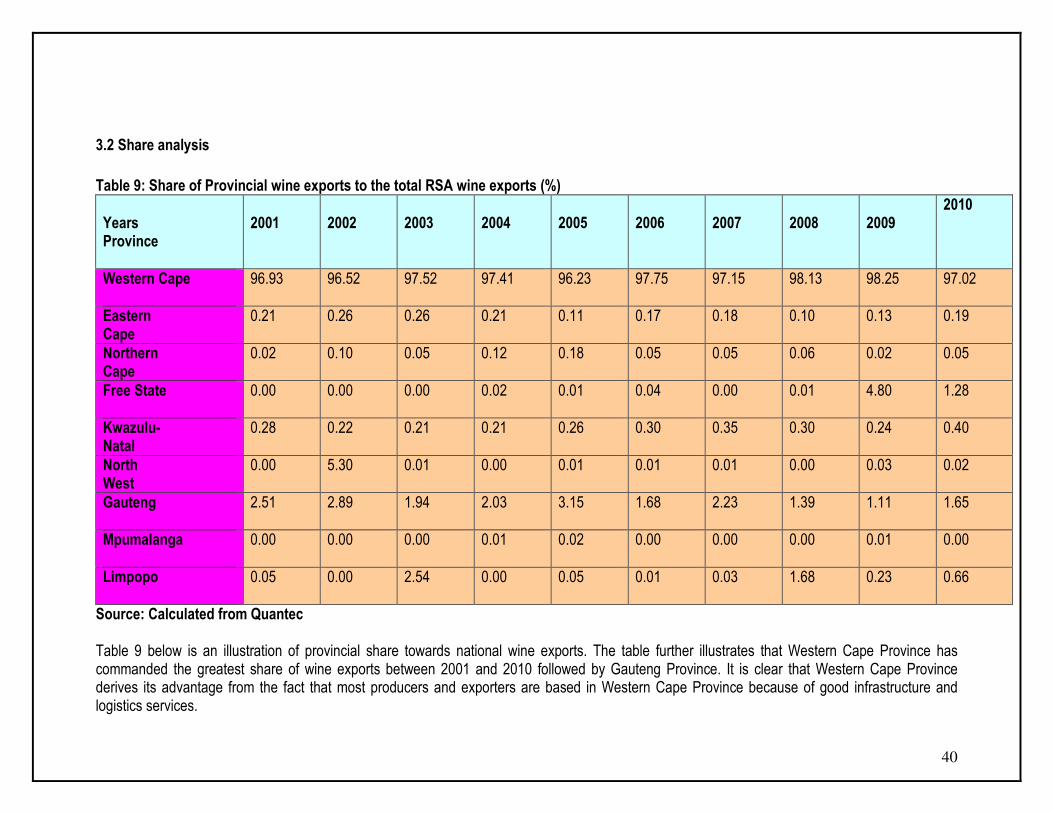

3.2 Share analysis

Table 9: Share of Provincial wine exports to the total RSA wine exports (%) Years Province

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Western Cape

96.93 96.52 97.52 97.41 96.23 97.75 97.15 98.13 98.25 97.02

Eastern Cape

0.21 0.26 0.26 0.21 0.11 0.17 0.18 0.10 0.13 0.19

Northern Cape

0.02 0.10 0.05 0.12 0.18 0.05 0.05 0.06 0.02 0.05

Free State

0.00 0.00 0.00 0.02 0.01 0.04 0.00 0.01 4.80 1.28

Kwazulu- Natal

0.28 0.22 0.21 0.21 0.26 0.30 0.35 0.30 0.24 0.40

North West

0.00 5.30 0.01 0.00 0.01 0.01 0.01 0.00 0.03 0.02

Gauteng

2.51 2.89 1.94 2.03 3.15 1.68 2.23 1.39 1.11 1.65

Mpumalanga

0.00 0.00 0.00 0.01 0.02 0.00 0.00 0.00 0.01 0.00

Limpopo

0.05 0.00 2.54 0.00 0.05 0.01 0.03 1.68 0.23 0.66

Source: Calculated from Quantec Table 9 below is an illustration of provincial share towards national wine exports. The table further illustrates that Western Cape Province has commanded the greatest share of wine exports between 2001 and 2010 followed by Gauteng Province. It is clear that Western Cape Province derives its advantage from the fact that most producers and exporters are based in Western Cape Province because of good infrastructure and logistics services.

41

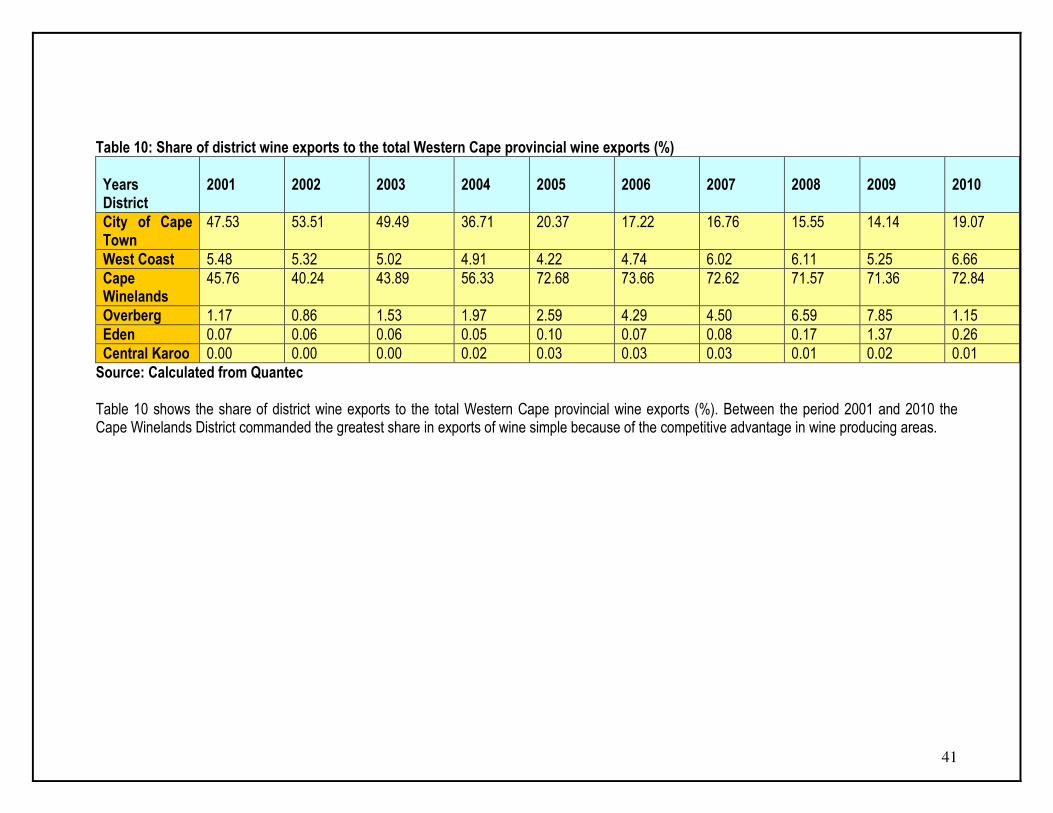

Table 10: Share of district wine exports to the total Western Cape provincial wine exports (%) Years District

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

City of Cape Town

47.53 53.51 49.49 36.71 20.37 17.22 16.76 15.55 14.14 19.07

West Coast 5.48 5.32 5.02 4.91 4.22 4.74 6.02 6.11 5.25 6.66 Cape Winelands

45.76 40.24 43.89 56.33 72.68 73.66 72.62 71.57 71.36 72.84

Overberg 1.17 0.86 1.53 1.97 2.59 4.29 4.50 6.59 7.85 1.15 Eden 0.07 0.06 0.06 0.05 0.10 0.07 0.08 0.17 1.37 0.26 Central Karoo 0.00 0.00 0.00 0.02 0.03 0.03 0.03 0.01 0.02 0.01 Source: Calculated from Quantec Table 10 shows the share of district wine exports to the total Western Cape provincial wine exports (%). Between the period 2001 and 2010 the Cape Winelands District commanded the greatest share in exports of wine simple because of the competitive advantage in wine producing areas.

42

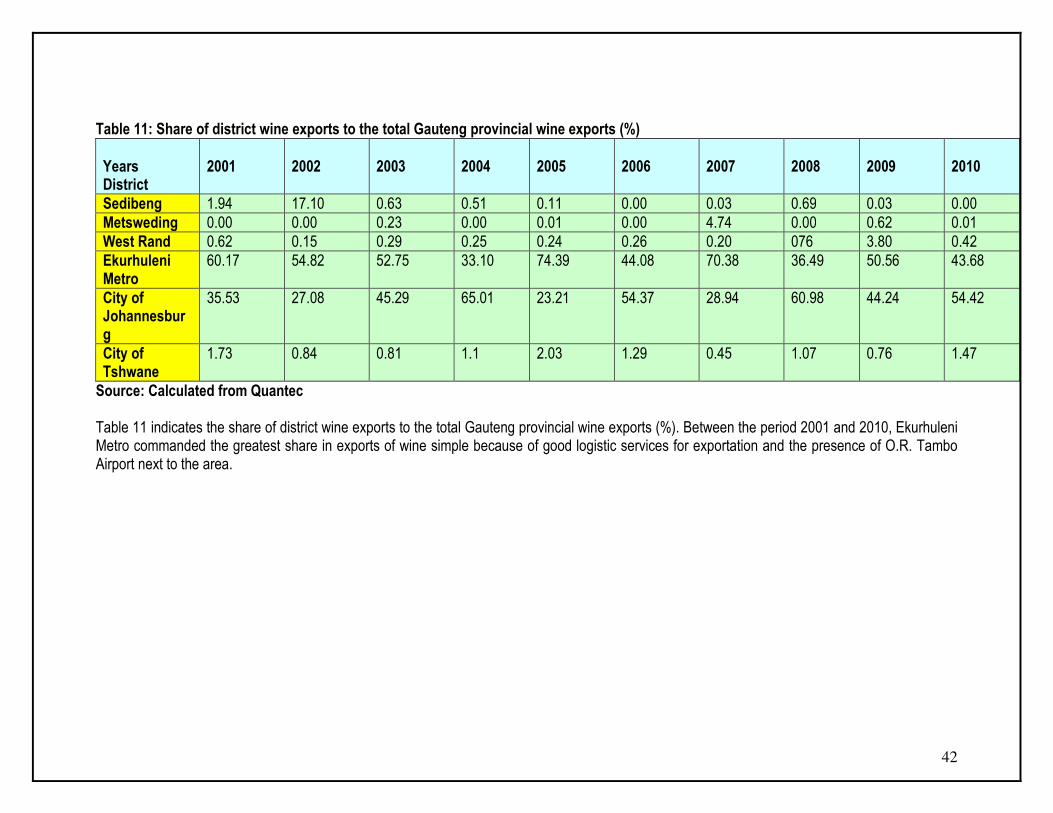

Table 11: Share of district wine exports to the total Gauteng provincial wine exports (%) Years District

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Sedibeng 1.94 17.10 0.63 0.51 0.11 0.00 0.03 0.69 0.03 0.00 Metsweding 0.00 0.00 0.23 0.00 0.01 0.00 4.74 0.00 0.62 0.01 West Rand 0.62 0.15 0.29 0.25 0.24 0.26 0.20 076 3.80 0.42 Ekurhuleni Metro

60.17 54.82 52.75 33.10 74.39 44.08 70.38 36.49 50.56 43.68

City of Johannesburg

35.53 27.08 45.29 65.01 23.21 54.37 28.94 60.98 44.24 54.42

City of Tshwane

1.73 0.84 0.81 1.1 2.03 1.29 0.45 1.07 0.76 1.47

Source: Calculated from Quantec Table 11 indicates the share of district wine exports to the total Gauteng provincial wine exports (%). Between the period 2001 and 2010, Ekurhuleni Metro commanded the greatest share in exports of wine simple because of good logistic services for exportation and the presence of O.R. Tambo Airport next to the area.

43

Table 12: Share of district wine exports to the total Kwa-Zulu Natal provincial wine exports (%) Years District

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Ugu District 1.37 3.59 5.84 8.25 5.15 0.26 0.00 0.00 0.00 0.00 Umgungundlovu

11.43 2.19 0.43 0.08 0.04 0.01 0.01 0.16 0.02 0.04

Uthukela 0.00 0.07 0.00 0.32 0.23 0.26 0.51 0.00 0.00 0.13 Umzinyathi 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.01 Uthungulu 0.27 0.71 0.51 0.48 0.47 0.02 0.00 0.00 0.23 0.04 Ilembe District

0.00 0.00 0.01 0.01 5.89 0.00 0.02 0.00 0.00 0.00

eThekwini 86.92 93.45 93.20 90.86 88.22 99.46 99.40 99.84 99.75 99.78 Source: Calculated from Quantec Table 12 illustrates the share of district wine exports to the total Kwazulu-Natal provincial wine exports (%). Between the period 2001 and 2010, the eThekwini Metro commanded the greatest share in exports of wine simple because of the competitive advantage in exportation and the presence of Durban harbour.

44

Table 13: Share of district wine exports to the total Eastern Cape provincial wine exports (%) Years District

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Cacadu 29.30 52.96 56.94 61.41 44.51 64.41 47.49 78.20 85.32 51.92 Amatole 66.81 39.08 27.85 29.28 39.45 29.86 43.38 17.41 2.28 37.48 Chris Hani 0.01 0.00 0.11 0.34 0.00 0.00 0.00 0.00 0.00 0.00 OR Tambo 0.00 1.88 7.76 6..93 15.05 5.21 9.06 3.81 0.00 0.00 Nelson Mandela

3.88 6.08 7.35 2.04 0.98 0.52 0.06 0.58 12.40 10.60

Source: Calculated from Quantec Table 13 illustrates the share of district wine exports to the total Eastern Cape provincial wine exports (%). Between the period 2001 and 2010, Cacadu District commanded the greatest share in exports of wine simple because of the presence of Port Elizabeth harbour that makes it easy to ship the wine products. Table 14: Share of district wine exports to the total Northern Cape provincial wine exports (%) Years District

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Pixley ka Seme

0.00 36.22 0.00 4.53 3.05 0.03 0.00 0.00 0.00 23.83

Siyand District

61.30 53.22 85.70 95.47 96.95 99.97 100 100 100 76.17

Frances Baard

38.70 10.56 14.30 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Source: Calculated from Quantec Table 14 illustrates the share of district wine exports to the total Northern Cape provincial wine exports (%). Between the period 2001 and 2010, Siyanda District commanded the greatest share in exports of wine in the Northern Cape Province.

45

Table 15: Share of district wine exports to the total Limpopo provincial wine exports (%) Years District

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Mopani 0.00 12.48 100 0.00 2.43 0.00 0.00 100 0.00 0.00 Vhembe 100 60.61 0.00 0.00 0.12 100 88.78 0.00 98.33 98.73 Capricorn 0.00 0.00 0.00 97.58 97.45 0.00 0.00 0.00 0.00 0.00 Waterberg 0.00 26.91 0.00 2.42 0.00 0.00 11.22 0.00 1.65 1.27 Greater Sekhukhune

0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.01 0.00

Source: Calculated from Quantec Table 15 illustrates the share of district wine exports to the total Limpopo provincial wine exports (%). Between the period 2001 and 2010, Vhembe District commanded the greatest share in exports of wine in that province. Table 16: Share of district wine exports to the total Mpumalanga provincial wine exports (%) Years District

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Gert Sibande 0.00 0.00 44.39 0.00 0.00 0.00 0.00 0.00 0.99 1.43 Nkangala 0.16 0.00 0.00 0.73 8.58 0.00 0.00 1.31 98.92 0.00 Ehlanzeni 99.83 100 55.61 99.27 91.42 0.00 100 98.69 0.08 98.57 Source: Calculated from Quantec Table 16 illustrates the share of district wine exports to the total Mpumalanga provincial wine exports (%). Between the period 2001 and 2010, Ehlanzeni District commanded the greatest share in exports of wine in that province.

46

Table 17: Share of district wine exports to the total North West provincial wine exports (%) Years District

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Bojanala 99.78 60.05 47.69 5.81 99.67 9.71 0.00 10.31 0.00 1.85 Central District 0.00 0.00 52.30 94.19 0.00 89.81 96.80 88.53 0.00 0.00 Southern District

0.22 39.95 0.01 0.00 0.33 0.48 3.20 1.16 100 98.15

Source: Calculated from Quantec Table 17 shows the share of district wine exports to the total North West provincial wine exports (%). Between the period 2001 and 2010, Bojanala District commanded the greatest share in exports of wine in that province. Table 18: Share of district wine exports to the total Free State provincial wine exports (%) Years District

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Xhariep 7.27 0.00 0.00 0.00 0.00 64.72 98.98 100 0.00 0.00 Motheo 92.73 99.25 100 0.00 0.00 0.06 1.02 0.00 100 100 Lejweleputswa

0.00 0.75 0.00 0.00 0.12 0.06 0.00 0.00 0.00 0.00

Thabo Mofutsanyane

0.00 0.00 0.00 100 99.88 35.16 0.00 0.00 0.00 0.00

Source: Calculated from Quantec

47

Table 18 depicts the share of district wine exports to the total Free State provincial wine exports (%). Between the period 2001 and 2010, Motheo District commanded the greatest share in exports of wine in that province. 4. IMPORTS OF WINES OF FRESH GRAPES

Figure 22: Imports volumes of wines of fresh grapes (including

fortified wines) from various regions

0

100000

200000

300000

400000

500000

Period (Years)

Imp

ort

s v

olu

mes

('000 l

itre

s)

Africa 1265 3229 42 28 321 329 4081 1937 63726 4558

Americas 877 107 470 336 266 424 255 213 426 1831

Asia 5 73 2 22520 111 704 2102 17 2160 85

Europe 117778 134155 171972 203854 351772 409769 423807 426344 333571 375788

Oceania 99 101 131 852 1099 180 325 146 123 187

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Source: Quantec Figure 22 depicts imports volumes of wines of fresh grapes (including fortified wines) from various regions into South Africa between 2001 and 2010 period. The figure further depicts that the major import market for wines of fresh grapes from the world into South Africa originated from Europe, followed by minimal imports of wines from Africa and Asia. The figure also depicts that imports of wines of fresh grapes from Europe into South Africa started to increase in 2002 with a dramatic increase between 2005 and 2008 years. The graph further depicts that in 2008 year, imports of wines of fresh grapes from Europe into South Africa experienced a peak in 2008 at approximately 426 344 litres. In 2009 imports of wines of fresh grapes from Europe experienced a slight decline, and then in 2010 wine imports slightly increased to approximately 375 788 litres. The increase in imports of wines of fresh grapes from Europe into South Africa in the year 2010 represents 11.2% as compared to 2009 year.

48

Figure 23: Imports volumes of wines of fresh grapes (including

fortified wines) from Africa

0

10000

20000

30000

40000

50000

60000

70000

Period (Years)

Imp

ort

s v

olu

mes

('000 l

itre

s)

Eastern Africa Rest 0 0 0 18 0 1 0 0 0 16

Middle Africa Rest 0 0 0 0 0 0 0 0 0 18

Western Africa 0 16 0 0 68 185 100 101 17 0

SADC 1265 3213 42 10 253 143 3981 1836 63709 4524

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

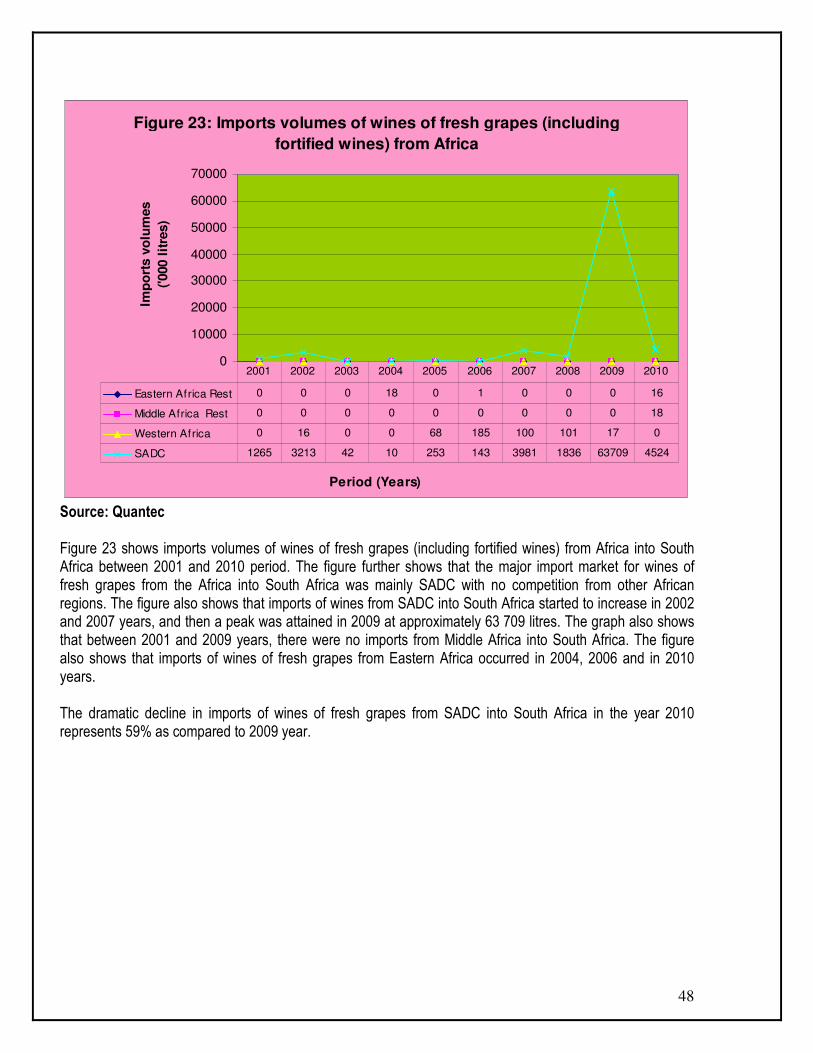

Source: Quantec Figure 23 shows imports volumes of wines of fresh grapes (including fortified wines) from Africa into South Africa between 2001 and 2010 period. The figure further shows that the major import market for wines of fresh grapes from the Africa into South Africa was mainly SADC with no competition from other African regions. The figure also shows that imports of wines from SADC into South Africa started to increase in 2002 and 2007 years, and then a peak was attained in 2009 at approximately 63 709 litres. The graph also shows that between 2001 and 2009 years, there were no imports from Middle Africa into South Africa. The figure also shows that imports of wines of fresh grapes from Eastern Africa occurred in 2004, 2006 and in 2010 years. The dramatic decline in imports of wines of fresh grapes from SADC into South Africa in the year 2010 represents 59% as compared to 2009 year.

49

Figure 24: Imports volumes of wines of fresh grapes (including

fortified wines) from SADC region

0

500

1000

1500

2000

Period (Years)

Imp

ort

s v

olu

mes

('000 l

itre

s)

Angola 0 0 0 0 0 0 3 4 0 0

Mauritius 157 0 0 0 0 7 460 0 36 0

Malaw i 0 0 0 0 0 1 0 0 0 0

Mozambique 0 0 0 0 0 2 0 0 0 0

United Republic of Tanzania 0 0 0 0 0 0 0 0 0 6

Zimbabw e 0 57 3 4 0 34 0 1800 0 0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

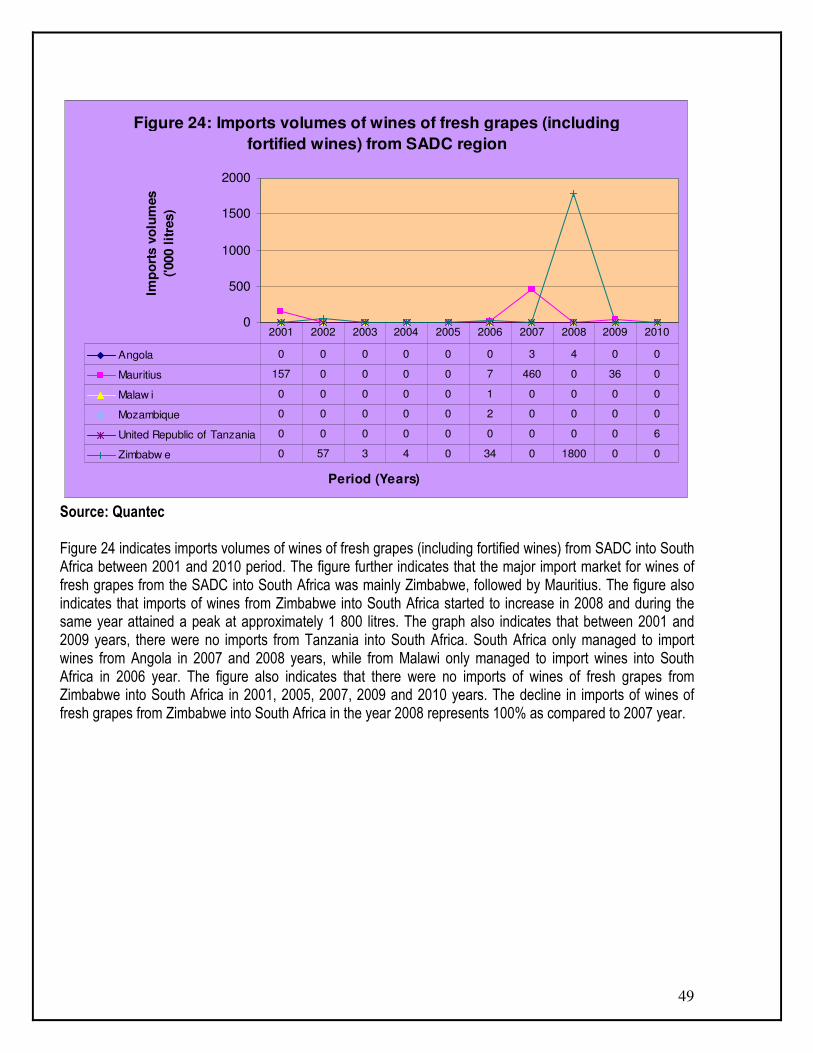

Source: Quantec Figure 24 indicates imports volumes of wines of fresh grapes (including fortified wines) from SADC into South Africa between 2001 and 2010 period. The figure further indicates that the major import market for wines of fresh grapes from the SADC into South Africa was mainly Zimbabwe, followed by Mauritius. The figure also indicates that imports of wines from Zimbabwe into South Africa started to increase in 2008 and during the same year attained a peak at approximately 1 800 litres. The graph also indicates that between 2001 and 2009 years, there were no imports from Tanzania into South Africa. South Africa only managed to import wines from Angola in 2007 and 2008 years, while from Malawi only managed to import wines into South Africa in 2006 year. The figure also indicates that there were no imports of wines of fresh grapes from Zimbabwe into South Africa in 2001, 2005, 2007, 2009 and 2010 years. The decline in imports of wines of fresh grapes from Zimbabwe into South Africa in the year 2008 represents 100% as compared to 2007 year.

50

Figure 25: Imports volumes of wines of fresh grapes (including

fortified wines) from the Americas

0

200

400

600

800

1000

1200

1400

1600

Period (Years)

Imp

ort

s v

olu

mes

('000 l

itre

s)

Caribbean 0 0 0 0 0 0 0 0 13 9

Central America 0 0 10 0 0 0 0 0 0 2

South America 36 6 252 275 134 141 50 41 41 1340

NAFTA 841 101 208 61 132 283 205 172 372 480

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

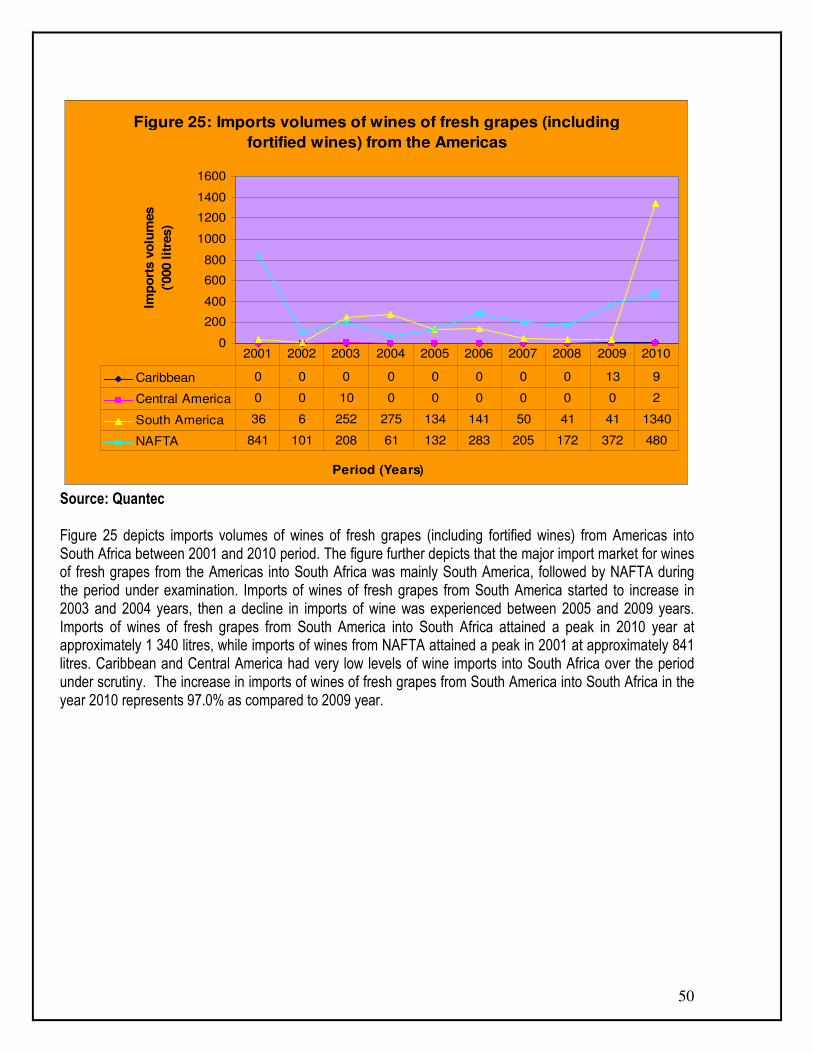

Source: Quantec Figure 25 depicts imports volumes of wines of fresh grapes (including fortified wines) from Americas into South Africa between 2001 and 2010 period. The figure further depicts that the major import market for wines of fresh grapes from the Americas into South Africa was mainly South America, followed by NAFTA during the period under examination. Imports of wines of fresh grapes from South America started to increase in 2003 and 2004 years, then a decline in imports of wine was experienced between 2005 and 2009 years. Imports of wines of fresh grapes from South America into South Africa attained a peak in 2010 year at approximately 1 340 litres, while imports of wines from NAFTA attained a peak in 2001 at approximately 841 litres. Caribbean and Central America had very low levels of wine imports into South Africa over the period under scrutiny. The increase in imports of wines of fresh grapes from South America into South Africa in the year 2010 represents 97.0% as compared to 2009 year.

51

Figure 26: Imports volumes of wines of fresh grapes (including

fortified wines) from Asia

0

5000

10000

15000

20000

25000

Period (Years)

Imp

ort

s v

olu

mes

('000 l

itre

s)

Eastern Asia 5 72 0 22511 12 650 1135 0 810 83

South-central Asia 0 0 0 0 0 0 48 0 0 0

South-eastern Asia 0 1 2 0 1 54 19 6 0 0

Western Asia 0 0 0 9 98 0 900 11 1350 2

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

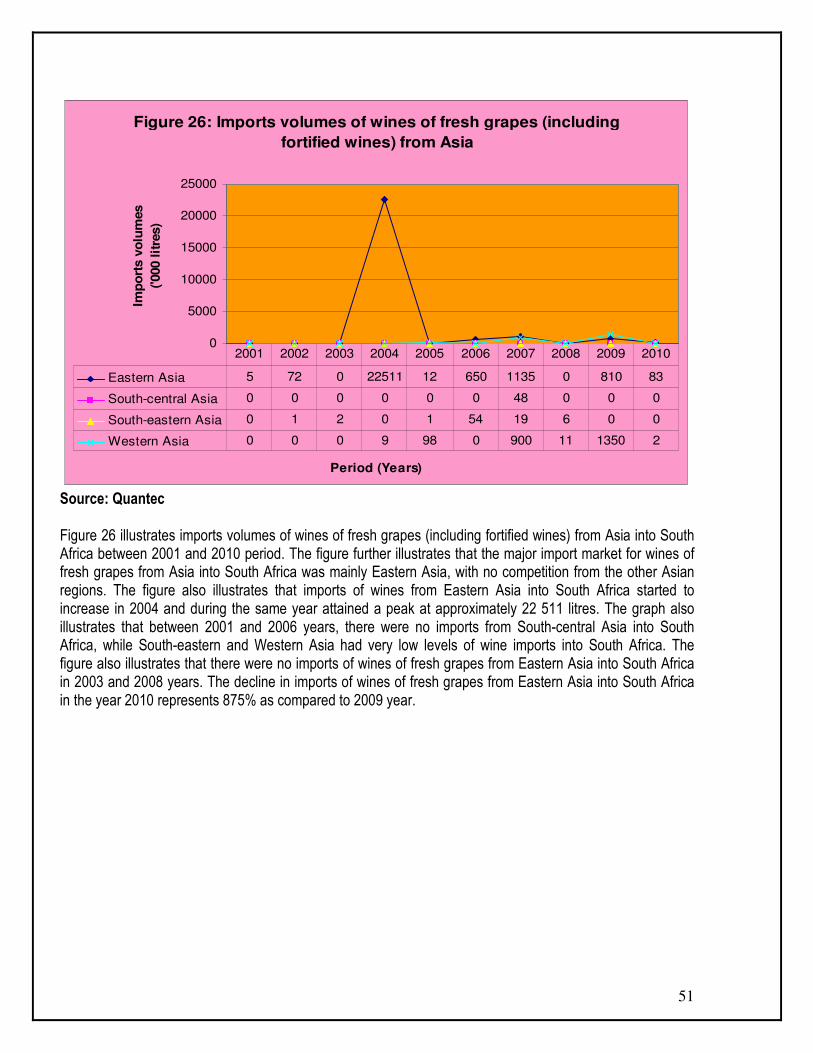

Source: Quantec Figure 26 illustrates imports volumes of wines of fresh grapes (including fortified wines) from Asia into South Africa between 2001 and 2010 period. The figure further illustrates that the major import market for wines of fresh grapes from Asia into South Africa was mainly Eastern Asia, with no competition from the other Asian regions. The figure also illustrates that imports of wines from Eastern Asia into South Africa started to increase in 2004 and during the same year attained a peak at approximately 22 511 litres. The graph also illustrates that between 2001 and 2006 years, there were no imports from South-central Asia into South Africa, while South-eastern and Western Asia had very low levels of wine imports into South Africa. The figure also illustrates that there were no imports of wines of fresh grapes from Eastern Asia into South Africa in 2003 and 2008 years. The decline in imports of wines of fresh grapes from Eastern Asia into South Africa in the year 2010 represents 875% as compared to 2009 year.

52

Figure 27: Imports volumes of wines of fresh grapes (including

fortified wines) from Europe

0

100000

200000

300000