winners and losers - carnegie endowment for international peace

TRANSCRIPT

IMPACT OF THE DOHA ROUND ON DEVELOPING COUNTRIES

Sandra Polaski

Winners and Losers

IMPACT OF THE DOHA ROUND ON DEVELOPING COUNTRIES

Sandra Polaski

Winners and Losers

© 2006 Carnegie Endowment for International Peace. All rights reserved.

No part of this publication may be reproduced or transmitted in any form or by any means withoutpermission in writing from the Carnegie Endowment.

The Carnegie Endowment normally does not take institutional positions on public policy issues; theviews presented here do not necessarily reflect the views of the Endowment, its staff, or its trustees.

For electronic copies of this report, visit www.CarnegieEndowment.org/trade. Limited printcopies are also available. To request a copy, send an e-mail to [email protected].

Carnegie Endowment for International Peace

1779 Massachusetts Avenue, N.W.Washington, D.C. 20036202-483-7600Fax 202-483-1840www.CarnegieEndowment.org

About the Author

Sandra Polaski is senior associate and director of the Trade, Equity, and Development project atthe Carnegie Endowment. Before joining the Endowment, she served as the U.S. Secretary ofState’s special representative for international labor affairs, the senior State Department officialdealing with such matters. She played a leading role in the development of U.S. government policyon international labor issues, and integrated those issues into U.S. trade and foreign policy. Prior tothat, she was the director of research for the North American Commission on Labor Cooperation, aNAFTA-related intergovernmental body.

Cover photo: Tomasz Tomaszewski/National Geographic Image Collection

Table of Contents

Acknowledgments iv

List of Tables, Figures, and Boxes v

Overview of the Report vii

Chapter 1Introduction: A Changing World of Trade 1

Chapter 2 A Description of the Model 3

Chapter 3The Results of Doha Round Trade Simulations 21

Chapter 4A Comparison of Models and Simulation Results 57

Chapter 5Policy Implications and Recommendations 67

AppendixesA. Technical Specifications of the Model 75B. Sensitivity Analysis 97

Notes 101

Carnegie Endowment for International Peace 104

This report is the product of a team organizedby the Trade, Equity, and Development Projectof the Carnegie Endowment for InternationalPeace, which included external experts as wellas Carnegie staff. It was led by project directorSandra Polaski. The team consisted of chiefmodeler Zhi Wang, expert advisor ShermanRobinson, researchers Kate Vyborny andJennifer Maul, program assistants GretchenSmith and Nicole Brown, copyeditor Alfred F.Imhoff, designers Laurie Rosenthal and PeteLindeman, and production manager Phyllis Jask.

We are deeply grateful to the RockefellerFoundation and its Global Inclusion Program forgenerous funding and continuous engagementand support throughout the project.

We benefited greatly from the comments,criticisms, and questions of numerous policymakers, modelers, and other economists as wepresented early versions of the model resultsand implications at meetings in Geneva,Washington, Brussels, and Paris.

The work of external modelers and experts doesnot imply any responsibility for the contents ofthe final report or for any remaining errors,which rests with the main author, Sandra Polaski.The policy conclusions and recommendationsare also those of Sandra Polaski, and they donot necessarily represent the views of theCarnegie Endowment for International Peace orthose of the external experts or the institutionswith which they are affiliated.

Acknowledgments

iv Winners and Losers: Impact of the Doha Round on Developing Countries

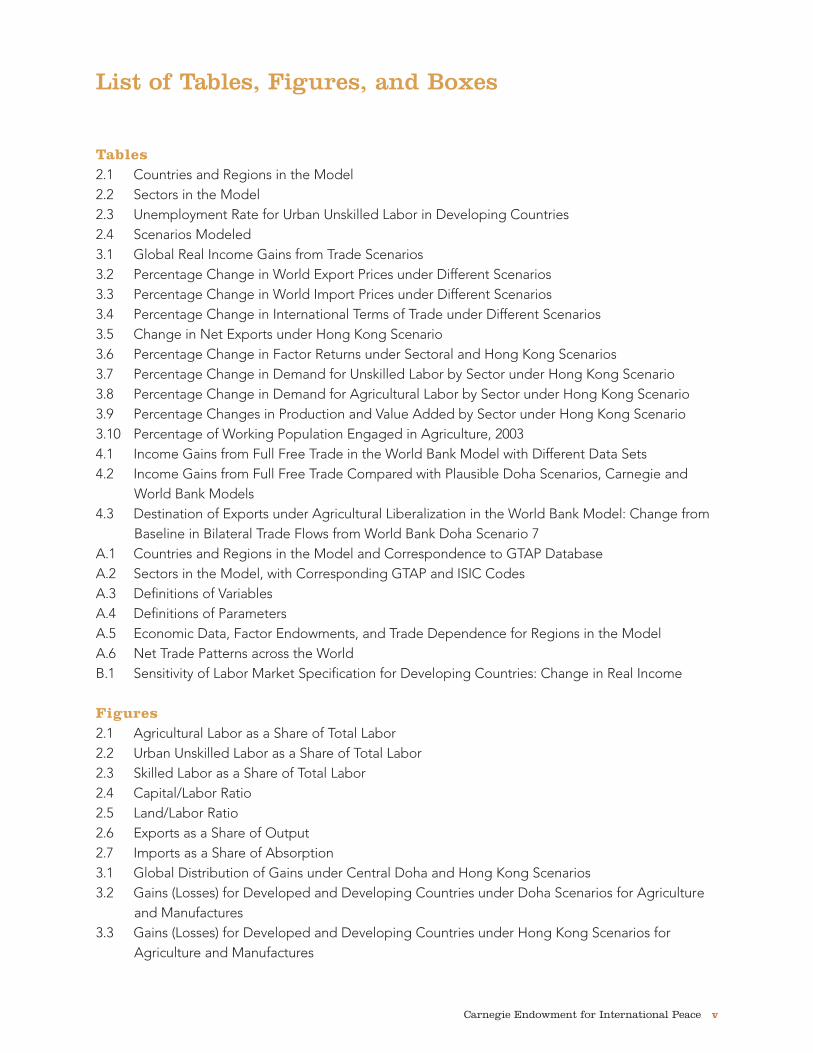

List of Tables, Figures, and Boxes

Tables2.1 Countries and Regions in the Model2.2 Sectors in the Model2.3 Unemployment Rate for Urban Unskilled Labor in Developing Countries2.4 Scenarios Modeled3.1 Global Real Income Gains from Trade Scenarios3.2 Percentage Change in World Export Prices under Different Scenarios3.3 Percentage Change in World Import Prices under Different Scenarios3.4 Percentage Change in International Terms of Trade under Different Scenarios3.5 Change in Net Exports under Hong Kong Scenario3.6 Percentage Change in Factor Returns under Sectoral and Hong Kong Scenarios3.7 Percentage Change in Demand for Unskilled Labor by Sector under Hong Kong Scenario3.8 Percentage Change in Demand for Agricultural Labor by Sector under Hong Kong Scenario3.9 Percentage Changes in Production and Value Added by Sector under Hong Kong Scenario3.10 Percentage of Working Population Engaged in Agriculture, 20034.1 Income Gains from Full Free Trade in the World Bank Model with Different Data Sets4.2 Income Gains from Full Free Trade Compared with Plausible Doha Scenarios, Carnegie and

World Bank Models4.3 Destination of Exports under Agricultural Liberalization in the World Bank Model: Change from

Baseline in Bilateral Trade Flows from World Bank Doha Scenario 7A.1 Countries and Regions in the Model and Correspondence to GTAP DatabaseA.2 Sectors in the Model, with Corresponding GTAP and ISIC CodesA.3 Definitions of VariablesA.4 Definitions of ParametersA.5 Economic Data, Factor Endowments, and Trade Dependence for Regions in the ModelA.6 Net Trade Patterns across the World B.1 Sensitivity of Labor Market Specification for Developing Countries: Change in Real Income

Figures2.1 Agricultural Labor as a Share of Total Labor2.2 Urban Unskilled Labor as a Share of Total Labor2.3 Skilled Labor as a Share of Total Labor2.4 Capital/Labor Ratio2.5 Land/Labor Ratio2.6 Exports as a Share of Output2.7 Imports as a Share of Absorption3.1 Global Distribution of Gains under Central Doha and Hong Kong Scenarios3.2 Gains (Losses) for Developed and Developing Countries under Doha Scenarios for Agriculture

and Manufactures3.3 Gains (Losses) for Developed and Developing Countries under Hong Kong Scenarios for

Agriculture and Manufactures

Carnegie Endowment for International Peace v

vi Winners and Losers: Impact of the Doha Round on Developing Countries

3.4 Manufacturing Liberalization: Developing Country Winners and Losers under Doha Scenario forManufactures

3.5 Manufacturing Liberalization: Developing Country Winners and Losers under Modest Scenariofor Manufactures

3.6 Gains (Losses) of World Export Market Share for Developing Countries’ Manufactures Exportsunder Hong Kong Scenario, by sub-sector

3.7 Gains (Losses) of World Export Market Share for Developing Countries’ Manufactures Exportsunder Hong Kong Scenario

3.8 Agricultural Liberalization: Developing Country Winners and Losers under Doha Scenario forAgriculture

3.9 Agricultural Liberalization: Developing Country Winners and Losers under Limited Scenario forAgriculture

3.10 Gains (Losses) of World Export Market Share for Developing Countries’ Agriculture Exportsunder Hong Kong Scenario, by sub-sector

3.11 Impact of Flexibility for “Special Products” on Real Income Gains for Developed andDeveloping Countries

3.12 Impact of Flexibility for “Special Products” on Real Income Gains for Selected Countries3.13 Poorest Countries Lose Income under All Doha Scenarios3.14 Sectoral Composition of Real Income Gains for Developing Countries 3.15 Real Income Gains (Losses) for Developing Countries under Overall Scenarios3.16 Real Income Gains for Developed Countries under Overall Scenarios3.17 Sectoral Composition of Real Income Gains for Developed Countries3.18 Gains (Losses) of World Export Market Share for Developed Countries’ Agriculture Exports

under Hong Kong Scenario, by sub-sector3.19 Gains (Losses) of World Export Market Share for Developed Countries’ Manufactures Exports

under Hong Kong Scenario, by sub-sector3.20 Developing Country Real Income Gains (Losses) as a Percentage of GDP under Central Doha

and Hong Kong Scenarios3.21 Developed Country Real Income Gains as a Percentage of GDP under Central Doha and Hong

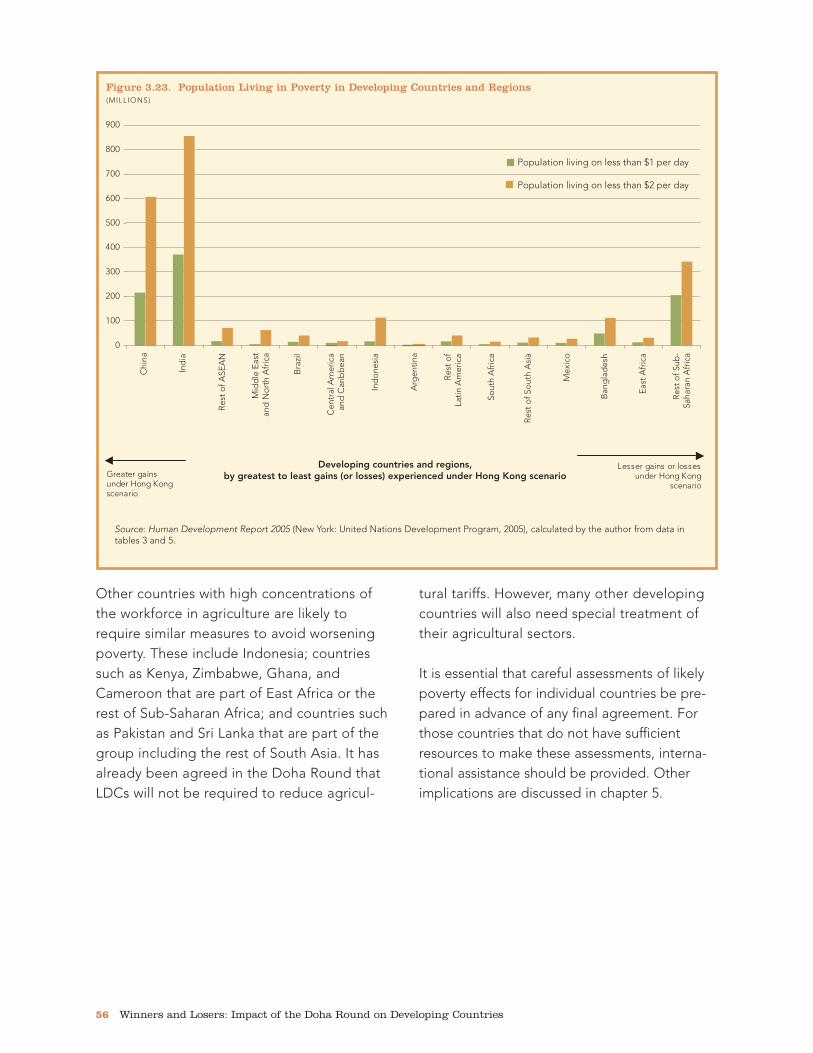

Kong Scenarios3.22 Impact of Hong Kong Scenario on Global Prices 3.23 Population Living in Poverty in Developing Countries and Regions4.1 Sectoral Gains (Losses) for Developed and Developing Countries under World Bank Scenarios

for Agriculture and Manufactures4.2 Global Real Income Gains from Agricultural Liberalization: Comparison of Major Models4.3 Agricultural Liberalization: Developing Country Winners and Losers under Carnegie Doha

Scenario for Agriculture and World Bank Scenario 2A.1 Structure of ProductionA.2 Structure of DemandA.3 Price System in the Model

Boxes5.1 RecommendationsA.1 Equations

Carnegie Endowment for International Peace vii

World trade negotiationsappear to be stalemated.Meeting in Hong Kong inDecember 2005, tradeministers from World

Trade Organization (WTO) member countrieswere unable to bridge major disagreements inthe Doha Round negotiations, so calledbecause they were launched in Doha, Qatar, in2001. Why are these negotiations so difficult?The answers lie mainly in the developing world.

A Changing World of Trade

The global trade regime expanded during thepast two decades to encompass most devel-oping countries, including China, which wasoutside the capitalist trading system in earlierrounds of trade talks. Countries like India wereless engaged in earlier rounds, reflectingeconomies that were largely closed at the time.Now, however, these fast-growing countrieshave become major players in the globaleconomy and global trade regime. As they joinglobal trade negotiations, they bring their ownoffensive and defensive concerns. Some wantto liberalize sectors in which they are competi-tive, such as agriculture, textiles, and apparel—the same sectors that are the most protected inwealthy countries, reflecting strong domesticconstituencies resistant to change. Developingcountries also have defensive concerns. Manyof them have agricultural sectors that employ

large shares of their population but are notcompetitive in global markets. And many wantto maintain trade barriers to nurture fledglingdomestic manufacturing and service sectors.The different priorities of developed and devel-oping countries make it inevitable that currentand future bargaining rounds will be morecomplex and difficult than past negotiations.

What would it take to produce a global tradeagreement that addresses the interests of bothdeveloped and developing countries? Toanalyze the underlying economic interests ofthe WTO’s diverse members and the potentialeffects of the Doha Round negotiations, theTrade, Equity, and Development Project of theCarnegie Endowment for International Peacecommissioned a model of global trade as a toolto estimate the impact of different trade policyscenarios. It is one of the newest in a series ofmodels built to analyze the Doha Round, usingthe latest global trade data.

In comparison with other models, the Carnegiemodel makes several improvements. Mostnotable are more accurate representations ofthe way labor markets function in developingcountries. Most models assume that all labor,including unskilled labor, is fully employed. Yetthis assumption is far from the reality of devel-oping countries. The Carnegie model incorpo-rates actual unemployment rates. Most modelstreat agricultural labor as identical to urban

Overview of the Report

unskilled labor, an inaccurate assumption thatcan produce inaccurate results. The Carnegiemodel treats agricultural labor markets sepa-rately from urban unskilled labor markets indeveloping countries. These innovations makethe Carnegie model more accurate in gaugingthe impact of trade policies on countries withlarge unskilled and agricultural labor forces.

The Carnegie model was used to simulate arange of plausible outcomes from the DohaRound. The central scenario anticipates anambitious expansion of market access for man-ufactured goods, a more modest expansion foragricultural products, reductions of domesticsubsidies and elimination of export subsidiesfor agricultural products. It requires lessermeasures by developing countries and none bythe least developed countries (LDCs), based onguidelines already agreed. A second main sce-nario was constructed after the Hong Kongmeeting to simulate agreements reachedthere. In this scenario, the same level of tariffcuts is applied to both agriculture and manu-facturing. The reductions are set at levels closeto proposals that are now on the negotiatingtable.

Findings That Defy ConventionalWisdom about the Doha Round

The most important finding at the aggregate,global level is that any of the plausible tradescenarios will produce only modest gains, onthe order of a one-time increase in worldincome of $40 to $60 billion. This represents anincrease of less than 0.2 percent of currentglobal gross domestic product (GDP). Thelimited nature of the gains from the DohaRound goes far in explaining the lack ofurgency demonstrated by WTO negotiators.Given relatively low gains, the adjustment coststo which countries expose themselves whenthey change trade policies may loom largerthan in the past. Losses of existing jobs and

firms are often more painful politically thanpotential gains in future growth. Major coun-tries are likely to insist that any agreement mustaccommodate their main defensive interests. Asa result, the Doha Round will probably achieveonly modest changes in any sector.

The modest overall gains would have quite dif-ferent economic effects on different countriesand regions. There are both net winners andnet losers under different scenarios, and thepoorest countries are among the net losersunder all likely Doha scenarios. At the countrylevel, maximum gains or losses are about 1percent of GDP for the most affectedeconomies. The biggest gainer is China, withgains ranging from 0.8 to 1.2 percent of GDPunder different scenarios. The biggest losersare some Sub-Saharan African countries, whichsee a reduction in income of just under 1percent. Most countries’ gains or losses rangefrom 0 to 0.5 percent of current GDP.

Among developing countries, about 90 percentof the gains from Doha scenarios would comefrom liberalization of trade in manufacturedgoods. Most developing countries gain fromliberalization of trade in manufactured goods,with China gaining the most and Asian coun-tries gaining more than Latin American andAfrican countries.

The benefits of agricultural trade liberalizationflow overwhelmingly to rich countries, whiledeveloping countries actually suffer slight lossesas a group. There are great differences in theimpact on different developing countries. A fewcountries gain, notably Brazil, Argentina, andThailand, but more suffer small losses from agri-cultural liberalization. The losers include manyof the poorest countries in the world, includingBangladesh and the countries of East Africa andthe rest of Sub-Saharan Africa. Middle Easternand North African countries, Vietnam, Mexico,and China also experience losses.

viii Winners and Losers: Impact of the Doha Round on Developing Countries

These results run counter to a commonly heldview about the Doha Round, that agriculturalliberalization benefits developing countries andwill augment their growth and development.Instead, agricultural liberalization benefits onlya relatively small subset of developing coun-tries, whereas manufacturing liberalization ismore important to most developing countries.

There are several reasons why the developingworld does not gain broadly from agriculturalliberalization. Many poor countries are net foodimporters. Many lose relative advantages theynow enjoy under special preference programs.However, a more fundamental problem arisesfrom the reality that low-productivity, small-scalesubsistence farming makes up a large portion ofagricultural activity in many developing coun-tries. The products of subsistence farmers aregenerally not competitive on global markets.

The pervasiveness of noncompetitive, small-scale farming in many developing countries hasled them to demand special consideration fortheir agricultural sectors in the Doha Round. Totest the impact on other countries of takingaccount of these agricultural concerns, we simu-lated a scenario in which developing countriesare allowed to shield agricultural products fromtariff liberalization. The results of this scenarioare surprising and important. Special treatmentcould be extended with only minor reductionsin other countries’ gains from the Doha Round,even for countries that are major agriculturalexporters. As for the developing countriesthemselves, India and Vietnam experienceslightly greater overall income gains under thisscenario, despite some loss of efficiency in theireconomies from continued tariffs. Bangladeshand the East African countries experiencesmaller losses if these exceptions are allowed.

Another striking result from the model is thepossibility that the poorest countries may losefrom any agreement unless additional special

measures are taken on their behalf. The resultsshow that Bangladesh, East Africa, and the restof Sub-Saharan Africa are adversely affected inalmost every scenario.

Although the Carnegie model was constructedprimarily to assess the impact of the DohaRound on developing countries, interestingresults also emerge for the developed world.All high-income countries and regions experi-ence small gains from the main scenarios, andthe gains come mainly from the liberalization ofmanufactured rather than agricultural goods.The United States gains more from liberaliza-tion of manufacturing than of agriculture. Forthe fifteen Western and Central Europeanmembers of the European Union (EU) and forJapan, manufacturing accounts for most gains,but agriculture contributes a greater share ofgains than in the United States, as higher levelsof distortions are removed in the EU and Japan.The gains are not without a cost, however.Income from farmland declines dramatically, by26 percent in the EU and 23 percent in Japan.

World export and import prices for all agricul-tural products increase under the main sce-narios. By contrast, liberalization ofmanufactured goods intensifies competition inseveral manufacturing sectors—includingapparel, metal products, and motor vehiclesand parts—and world prices decline slightly.These price trends are at odds with a long-standing historical pattern of declining pricesfor agricultural commodities relative to manu-factured goods.

Trade liberalization for manufactured goodsincreases demand for unskilled labor in mostof the developing world. However, wages donot increase, due to the abundant supply oflabor and the fact that liberalized trade inlabor-intensive manufactures drives downworld prices for such goods. Under the mainscenarios, employment of unskilled labor

Carnegie Endowment for International Peace ix

increases by about 1 percent in the manufac-turing sector for developing countries as agroup, although the gain is unevenly distrib-uted among countries and across manufac-turing subsectors. Increases in unskilledemployment of 1 percent or more are realizedby China, Indonesia, the other members of theAssociation of Southeast Asian Nations(ASEAN), and India. Once again, the threepoorest countries/regions in the model(Bangladesh, East Africa, and the rest of Sub-Saharan Africa) actually lose unskilled jobs inmanufacturing industries. Income for agricul-tural labor and land increases in developingcountries, except in Mexico, India,Bangladesh, and Vietnam. For developingcountries as a group, agricultural employmentbarely increases (0.17 percent) under the mainscenarios, but is somewhat more robust underthe special scenario for developing countryagriculture (0.3 percent).

Global trade models do not capture the costsincurred as economies adjust to trade reform,with some labor and capital idled by changes intrade patterns. At least in the short term, thiswill subtract from overall income gains and havea potentially large negative impact on theaffected individuals and households. As a resultof omitting these costs, models tend to system-atically overstate the gains from trade or under-state the losses. The effects are likely to berelatively greater in developing countries,because they have less diversified economies,with fewer alternative sources of employmentthan developed countries.

From the Perspectives of Equity and Poverty, a Complicated Picture Emerges

The overall gains to the world are dividedfairly evenly between the developed anddeveloping worlds. The big winner in thedeveloping world, China, is also home to large

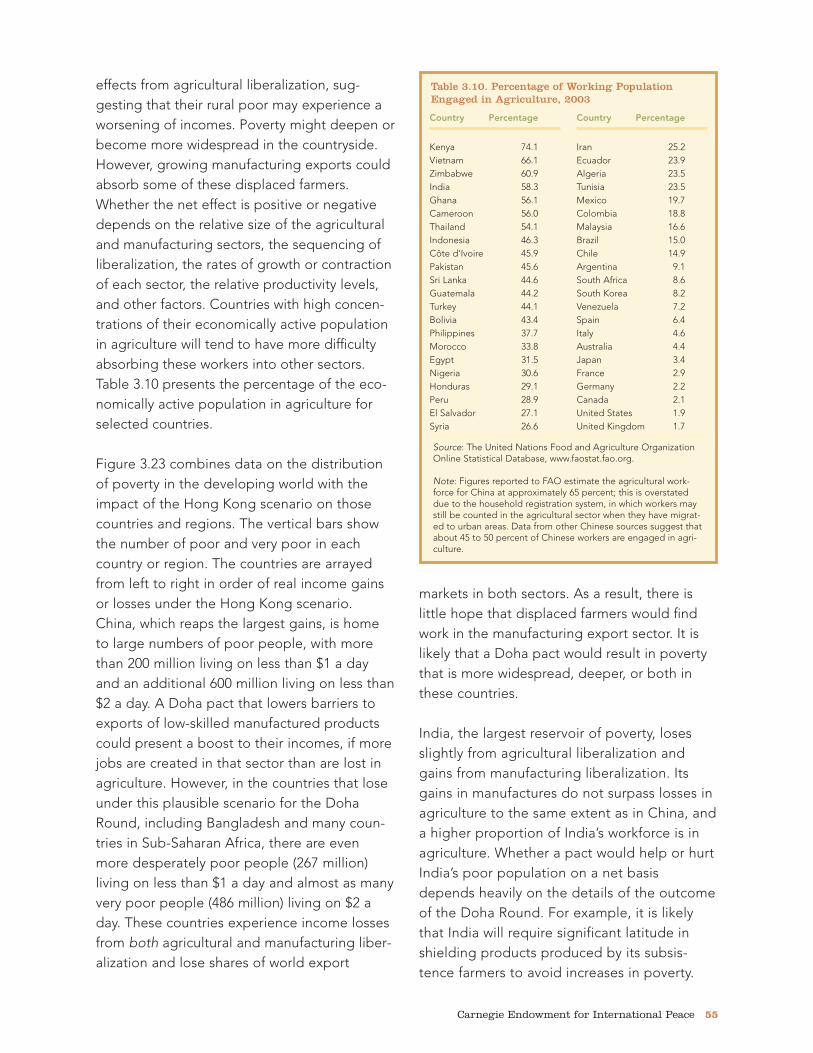

numbers of poor people, with more than 200million living on less than $1 per day and anadditional 600 million living on less than $2 perday. A Doha pact that lowers tariffs in low-skilled manufactured products could increaseemployment there and boost the incomes ofthe poor. However, in the countries that losefrom the Doha Round, including Bangladeshand many countries in Sub-Saharan Africa,there are even more desperately poor people(267 million) living on less than $1 per day andalmost as many very poor people (486 million)living on less than $2 per day. Most of theworld’s poor people are concentrated in ruralareas and depend on agriculture for theirincomes. This is true in China, Bangladesh,and Sub-Saharan Africa, as well as in othercountries that have large numbers of poorpeople, most notably India. All of these coun-tries lose from agricultural liberalization.Whether a pact would help or hurt their poorcitizens on a net basis depends heavily on thedetails of the outcome. For example, countrieslike India, Indonesia, and Kenya will requireexceptions for the products produced by theirsubsistence farmers if they are to avoidincreases in poverty.

Comparison with Other Trade Models

This report compares results from theCarnegie model with several other models,including the newest World Bank model. Onsome of the most surprising results, othermodels show similar patterns, although theseresults often are not highlighted in reports onthose models.

Conclusions and Recommendations

It is important not to overstate the possiblegains from the Doha Round, as has been doneby many political leaders, commentators, andactivists. It has been fashionable to state thattrade can do more than development aid to lift

x Winners and Losers: Impact of the Doha Round on Developing Countries

Carnegie Endowment for International Peace xi

people out of poverty in developing countries.Though this may be theoretically true, it is clearfrom the Carnegie model and a close study ofmost other recent models that trade is not apanacea for poverty alleviation or for develop-ment more generally. Trade is one factor amongmany that can contribute to economic growthand rising incomes, but its contribution is likelyto be very modest. At the same time, changesin existing trade policies can also cause eco-nomic contraction and must be designed andimplemented with great care. An unrealisticexpectation of gains can lead to pressure forinappropriate policies and could create a band-wagon effect where the very legitimate defen-sive concerns of developing countries areignored to achieve illusory gains. Errors inanalysis can lead to increases in poverty, not thehoped-for reductions, in a broad range ofdeveloping countries. For the poorest coun-tries, where there is little margin for error, therisks are particularly acute.

The report concludes with a set of recommen-dations meant to address the interests andproblems of the developing world in the DohaRound. These include:

■ Many developing countries will require verylong phase-in periods and a carefulsequencing of sectoral liberalizationmeasures, to take account of the impact oftrade changes on their less diversifiedeconomies.

■ Special treatment for developing countryagricultural sectors will be needed becauseof the high concentrations of employment inthose sectors and the long and difficultprocess of raising productivity levels anddeveloping new skills among the hundredsof millions of subsistence farmers in theworld.

■ The Doha Round should include additionaldevelopment assistance for agriculture in

developing countries, because the transitionto more modern sectors will require resourcesbeyond what is domestically available in poorcountries. Major new aid commitments bymultilateral development agencies andbilateral donors are needed.

■ For the LDCs, additional measures will beneeded to ensure that they are not net losersfrom the Doha Round. In Hong Kong,developed countries agreed to extend duty-free and quota-free market access for mostexports of LDCs; however, their mostcompetitive products can be excluded. Theagreement should be extended to include allproducts of LDCs by a firm future date. Thefinal plan should also eliminate cumbersomerules of origin that block imports of someproducts from LDCs and reduce theiropportunity to achieve economies of scale.

■ Middle-income countries should also extendthis access to the LDCs. China established apositive precedent by offering preferentialaccess to many products of the leastdeveloped ASEAN members as part of aregional free trade agreement, althoughthere are many exceptions. Preferentialaccess should be extended by other middle-income developing countries and by China toLDCs in other regions.

■ A solution must also be found for the groupof low-income countries that are just abovethe threshold for LDC status, because theymay be made worse off by the effort to helpthe poorest. Some access to the specialbenefits should be extended to thesecountries as well.

■ Trade adjustment assistance programs forpoor people in low-income countries shouldbe part of a Doha package. This can be donethrough multilateral development agencies,such as the World Bank, or through bilateralassistance. To date, such programs have notbeen adopted or even discussed. Theyshould be added to the Doha agenda.

Carnegie Endowment for International Peace 1

Efforts to liberalize global tradethrough the World TradeOrganization (WTO) have madelimited progress since thecurrent round of negotiations

was launched in Doha, Qatar, in 2001. Meetingin Hong Kong in December 2005, trade minis-ters from the 149 WTO member countriesresolved only a few issues, while postponingthe deadline for resolution of the main contro-versies until April 30, 2006. Despite the pres-ence of the most senior negotiators and theglare of media attention, member countrieswere unable to break stalemates that exist invirtually every major area of the negotiations.

Why are these negotiations so difficult? Theanswers lie mainly in the developing world.Earlier trade rounds primarily involved devel-oped countries and addressed their priorities.During the past twenty years, however, theglobal trade regime has expanded to includemost of the developing world, including commu-nist countries such as China, which were outsidethe capitalist trading system in earlier rounds oftrade talks. India and a number of smaller coun-tries were less engaged in earlier rounds,reflecting economies that were largely closed atthe time. The relative weight of these countriesin the global economy has grown enormouslyover the same period, and it will continue toexpand due to higher rates of growth in thesecountries compared with mature economies.

As developing countries join global trade nego-tiations, they bring their own offensive anddefensive concerns. Offensively, they want toliberalize sectors in which they are competitive,such as agriculture, textiles, and apparel. Thesesectors were liberalized least in earlier traderounds, due to strong domestic constituenciesin developed countries. The developing coun-tries also have their own defensive concerns,often involving agricultural sectors that employlarge shares of their population but are notcompetitive in global markets, or even indomestic markets in the absence of tariffs.Many are also concerned defensively aboutmanufacturing and service sectors, where theyhope to nurture domestic industries behindtrade barriers. In most developing countries,growing manufacturing and service sectors areseen as essential to absorb growing laborforces and large numbers of low-income, low-productivity farmers.

The different priorities of developed and devel-oping countries make it inevitable that currentand future bargaining rounds will be even morecomplex and difficult than past negotiations. Atthe same time, the size and high growth ratesof many developing economies mean that theirpresence in the global trading system iswelcome. In recognition of the new reality, thecurrent negotiations were named the “DohaDevelopment Round” and were launched witha commitment by wealthy countries to pay

C H A P T E R 1

Introduction: A Changing World of Trade

2 Winners and Losers: Impact of the Doha Round on Developing Countries

special attention to the needs and interests ofdeveloping countries. Arguably, without thiscommitment to redress perceived imbalances inthe global trading system that favored richcountries, the launch of negotiations would nothave been possible. After 2001, however, theinterests of developing countries did notreceive the promised prioritization. The summitof trade ministers held in Cancún, Mexico, in2003 broke down in acrimony, largely due tothese countries’ perception of their continuedmarginalization in the negotiations. At theHong Kong ministerial, at least some progresswas made on the demands of the poorestcountries, although most of these concessionswill take effect only if the talks produce anoverall agreement, an achievement that stillappears out of reach.1

What would it take to reach a global tradeagreement that addresses the interests ofdeveloping countries and holds the potential tolift their incomes, while at the same timeoffering sufficiently expanded opportunities fordeveloped countries to win their assent?Answering this question is not a simple matter.Global trade is carried out through myriad two-way trade relationships between countries thathave different sets of assets, capabilities, andvulnerabilities. Differences in the size and skillsof workforces, suitability for cultivating differentagricultural crops, and amount of capital avail-able for investment mean that a particular traderule change will affect countries differently.Finding a mix of trade policy changes thatoffers opportunities for all, or even for most, iscomplex and difficult.

To analyze the underlying economic interests of

the WTO’s diverse members and to identifycombinations of trade policies that wouldproduce widely distributed benefits, the Trade,Equity, and Development Project of theCarnegie Endowment for International Peacecommissioned an applied general equilibrium(AGE) model of global trade.2 AGE models arecomputer-based simulations of how economieswork. In the case of global trade models, theentire world economy is modeled, including themaze of bilateral trade relationships.

Once such a model is built, it can be used as alaboratory for policy experiments in whichvarious policies are changed and the results aretraced through the model for their impact ondifferent sectors, different economic actors, andthe overall welfare of countries and the globaleconomy. The Carnegie model was used tosimulate the impact on different countries andregions of various trade proposals that approxi-mate those under consideration in the DohaRound. Scenarios were constructed that captureplausible outcomes from the round.

This report presents the results of these tradepolicy simulations. The model and a descrip-tion of how it represents the world’s economiesare presented in chapter 2, with a moredetailed specification of the model provided inappendix A and a sensitivity analysis inAppendix B. In chapter 3, the main results ofthe trade policy simulations are reported.Chapter 4 provides an overview of severalother important models and a comparison oftheir structures and results. In chapter 5, theconclusions and implications that can be drawnfrom the Carnegie model results are discussedand policy recommendations are presented.

Carnegie Endowment for International Peace 3

The Carnegie model is one of thenewest in a series of models builtfor the purpose of analyzing andprojecting possible impacts of theDoha Round. Applied general

equilibrium (AGE) trade models create a simula-tion of the workings of actual economies as theyengage in trade, represented through an exten-sive series of equations that establish the rela-tionships between economic variables. The AGEmodel used in this analysis shares many basicfeatures with other current models. The impor-tant distinguishing features of this model are dis-cussed below.

The Carnegie model is a multicountry, multi-sector general equilibrium model. It uses datafrom the Global Trade Analysis Project (GTAP)database Version 6.0, the newest compilation ofglobal trade data, which is used in most recentmajor models.3 Additional data are drawn fromvarious national and intergovernmental sources,as noted where the data appear. The data areused to construct a baseline representation ofthe current global economy. This serves as abasis for comparison with the impact of simula-tions of different trade policy scenarios, such asthose that might be agreed in the World TradeOrganization (WTO). The scenarios are describedbelow. The results of the simulations showchanges in prices, terms of trade, and net tradevolumes induced by different trade policychanges, along with changes in returns to factors

of production (land, labor, and capital) andemployment. The model also captures gainsfrom the more efficient use of resources and fromthe transfer of technology, which increases astrade barriers are lowered. Technology transfer isassumed to flow in one direction—from moredeveloped regions to less developed regions.

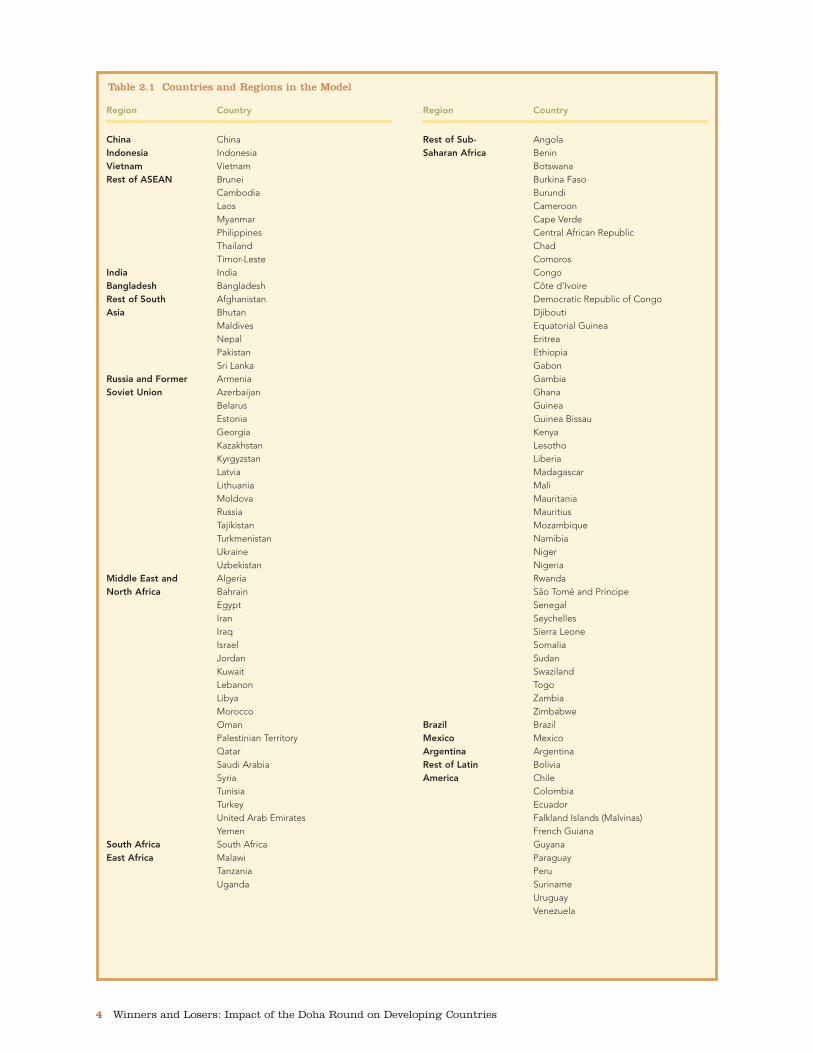

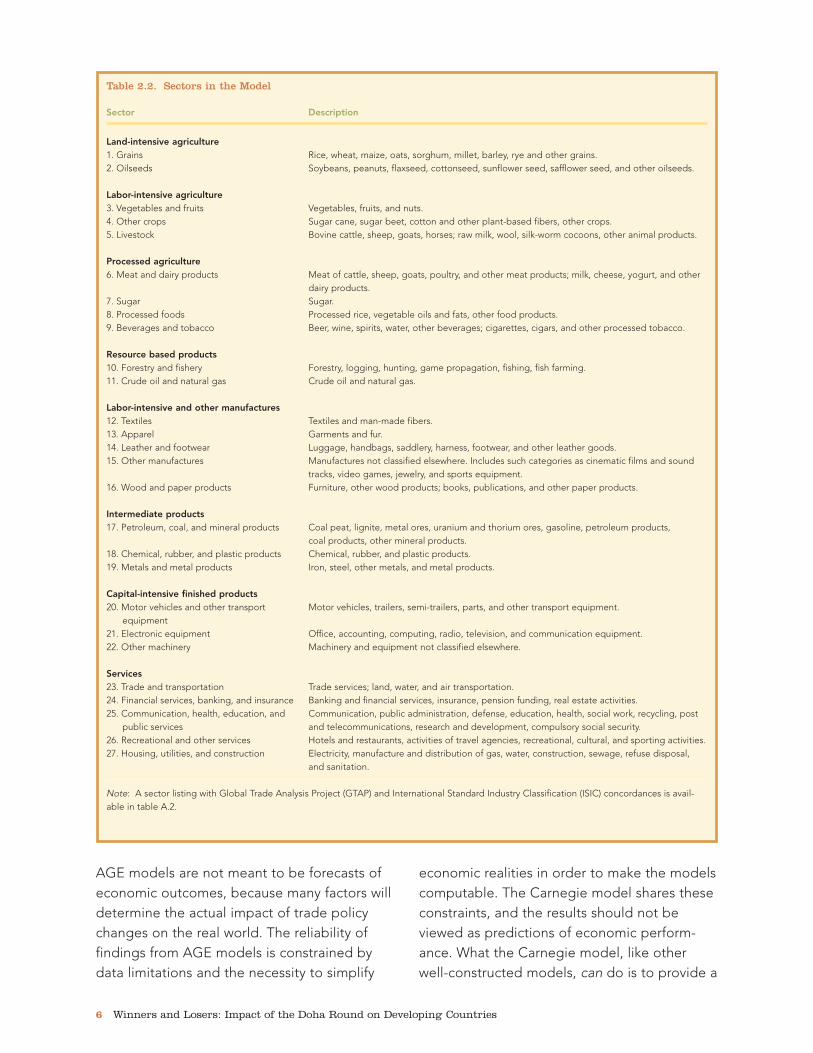

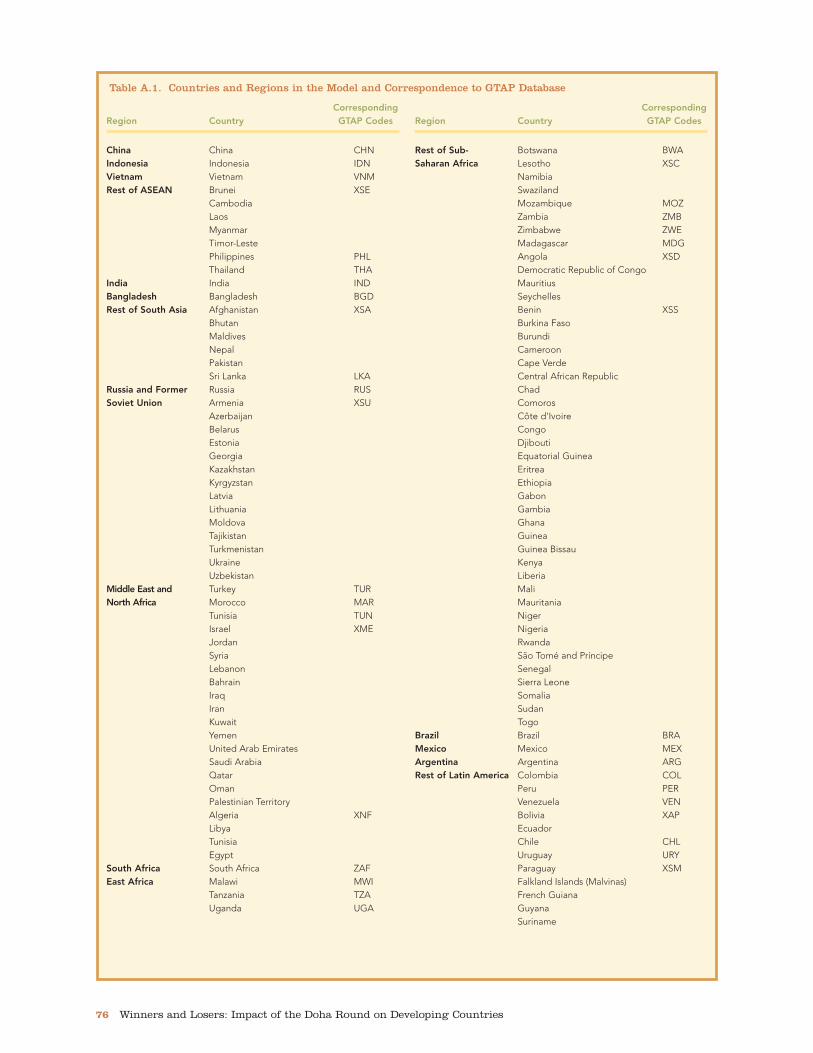

The model is global in scope, covering all coun-tries (including nonmembers of the WTO). Tomake global models computable (and becauseof data limitations) it is necessary to aggregatesmaller countries. In the Carnegie model,eleven large countries, including nine devel-oping countries, are modeled separately, andthe remaining countries are aggregated intothirteen regions (table 2.1). The model coversall sectors, including agriculture, manufacturing,and services. Again, due to the technical limita-tions of models, sectors must be aggregatedinto a workable number. In the Carnegie model,there are twenty-seven sectoral aggregations(table 2.2). There are six factors of production:agricultural land, natural resources, capital, agri-cultural labor, unskilled labor, and skilled labor.The way labor is modeled for developing coun-tries, which is unique to the Carnegie model, isdiscussed below. The model incorporates con-siderable detail on domestic production andconsumption within each country or region aswell as international trade flows at the bilateraland global levels. A fuller technical discussionof the model is found in appendix A.

C H A P T E R 2

A Description of the Model

4 Winners and Losers: Impact of the Doha Round on Developing Countries

Region Country

China ChinaIndonesia IndonesiaVietnam VietnamRest of ASEAN Brunei

CambodiaLaosMyanmarPhilippinesThailandTimor-Leste

India IndiaBangladesh BangladeshRest of South AfghanistanAsia Bhutan

MaldivesNepalPakistanSri Lanka

Russia and Former ArmeniaSoviet Union Azerbaijan

BelarusEstoniaGeorgiaKazakhstanKyrgyzstanLatviaLithuaniaMoldovaRussiaTajikistanTurkmenistanUkraineUzbekistan

Middle East and AlgeriaNorth Africa Bahrain

EgyptIranIraqIsraelJordan Kuwait LebanonLibyaMoroccoOmanPalestinian TerritoryQatarSaudi ArabiaSyriaTunisiaTurkeyUnited Arab EmiratesYemen

South Africa South AfricaEast Africa Malawi

TanzaniaUganda

Region Country

Rest of Sub- AngolaSaharan Africa Benin

BotswanaBurkina FasoBurundiCameroonCape VerdeCentral African RepublicChadComorosCongoCôte d'IvoireDemocratic Republic of CongoDjiboutiEquatorial GuineaEritreaEthiopiaGabonGambiaGhanaGuineaGuinea Bissau KenyaLesothoLiberiaMadagascarMaliMauritaniaMauritiusMozambiqueNamibiaNigerNigeriaRwandaSão Tomé and Príncipe SenegalSeychellesSierra LeoneSomaliaSudanSwazilandTogoZambiaZimbabwe

Brazil BrazilMexico MexicoArgentina ArgentinaRest of Latin BoliviaAmerica Chile

ColombiaEcuadorFalkland Islands (Malvinas)French GuianaGuyanaParaguayPeruSurinameUruguayVenezuela

Table 2.1 Countries and Regions in the Model

Carnegie Endowment for International Peace 5

Region Country

Central America Anguillaand Caribbean Antigua and Barbuda

ArubaBahamasBarbadosBelizeBritish Virgin IslandsCayman IslandsCosta RicaCubaDominicaDominican RepublicEl SalvadorGrenadaGuadeloupeGuatemalaHaitiHondurasJamaicaMartiniqueMontserratNetherlands AntillesNicaraguaPanamaPuerto RicoSaint Kitts and NevisSaint LuciaSaint Vincent and the GrenadinesTrinidad and TobagoTurks and CaicosU.S. Virgin Islands

Rest of the World AlbaniaAmerican SamoaAndorraBermudaBosnia and HerzegovinaBulgariaCook IslandsCroatiaFaroe IslandsFijiFormer Yugoslav Republic of MacedoniaFrench PolynesiaGibraltarGreenlandGuamKiribatiMacauMarshall IslandsMicronesia, Federated States ofMonacoMongoliaNauruNew CaledoniaNiue

Region Country

Norfolk IslandNorth KoreaNorthern Mariana IslandsPalauPapua New GuineaRomaniaSaint Pierre and MiquelonSamoaSan MarinoSerbia and MontenegroSolomon IslandsTokelauTongaTuvaluVanuatuWallis and Futuna

Asian Newly Hong KongIndustrialized Economies Malaysia

SingaporeSouth KoreaTaiwan

United States United StatesEuropean Union 15 Austria

BelgiumDenmarkFinlandFranceGermanyGreeceIrelandItalyLuxembourgNetherlandsPortugalSpainSwedenUnited Kingdom

European Union 10 CyprusCzech RepublicHungaryMaltaPolandSlovakiaSloveniaEstoniaLatviaLithuania

Japan JapanRest of OECD Australia

CanadaIcelandLichtensteinNew ZealandNorwaySwitzerland

Table 2.1 (continued) Countries and Regions in the Model

Note: ASEAN = Association of Southeast Asian Nations. OECD = Organization for Economic Cooperation and Development.

AGE models are not meant to be forecasts ofeconomic outcomes, because many factors willdetermine the actual impact of trade policychanges on the real world. The reliability offindings from AGE models is constrained bydata limitations and the necessity to simplify

economic realities in order to make the modelscomputable. The Carnegie model shares theseconstraints, and the results should not beviewed as predictions of economic perform-ance. What the Carnegie model, like otherwell-constructed models, can do is to provide a

6 Winners and Losers: Impact of the Doha Round on Developing Countries

Table 2.2. Sectors in the Model

Sector Description

Land-intensive agriculture1. Grains Rice, wheat, maize, oats, sorghum, millet, barley, rye and other grains.2. Oilseeds Soybeans, peanuts, flaxseed, cottonseed, sunflower seed, safflower seed, and other oilseeds.

Labor-intensive agriculture3. Vegetables and fruits Vegetables, fruits, and nuts.4. Other crops Sugar cane, sugar beet, cotton and other plant-based fibers, other crops.5. Livestock Bovine cattle, sheep, goats, horses; raw milk, wool, silk-worm cocoons, other animal products.

Processed agriculture6. Meat and dairy products Meat of cattle, sheep, goats, poultry, and other meat products; milk, cheese, yogurt, and other

dairy products.7. Sugar Sugar.8. Processed foods Processed rice, vegetable oils and fats, other food products.9. Beverages and tobacco Beer, wine, spirits, water, other beverages; cigarettes, cigars, and other processed tobacco.

Resource based products10. Forestry and fishery Forestry, logging, hunting, game propagation, fishing, fish farming.11. Crude oil and natural gas Crude oil and natural gas.

Labor-intensive and other manufactures12. Textiles Textiles and man-made fibers.13. Apparel Garments and fur.14. Leather and footwear Luggage, handbags, saddlery, harness, footwear, and other leather goods.15. Other manufactures Manufactures not classified elsewhere. Includes such categories as cinematic films and sound

tracks, video games, jewelry, and sports equipment.16. Wood and paper products Furniture, other wood products; books, publications, and other paper products.

Intermediate products17. Petroleum, coal, and mineral products Coal peat, lignite, metal ores, uranium and thorium ores, gasoline, petroleum products,

coal products, other mineral products.18. Chemical, rubber, and plastic products Chemical, rubber, and plastic products.19. Metals and metal products Iron, steel, other metals, and metal products.

Capital-intensive finished products20. Motor vehicles and other transport Motor vehicles, trailers, semi-trailers, parts, and other transport equipment.

equipment21. Electronic equipment Office, accounting, computing, radio, television, and communication equipment.22. Other machinery Machinery and equipment not classified elsewhere.

Services23. Trade and transportation Trade services; land, water, and air transportation.24. Financial services, banking, and insurance Banking and financial services, insurance, pension funding, real estate activities.25. Communication, health, education, and Communication, public administration, defense, education, health, social work, recycling, post

public services and telecommunications, research and development, compulsory social security.26. Recreational and other services Hotels and restaurants, activities of travel agencies, recreational, cultural, and sporting activities.27. Housing, utilities, and construction Electricity, manufacture and distribution of gas, water, construction, sewage, refuse disposal,

and sanitation.

Note: A sector listing with Global Trade Analysis Project (GTAP) and International Standard Industry Classification (ISIC) concordances is avail-able in table A.2.

comparison of the relative effects of alternativetrade policy proposals when all other factorsare held constant. This capacity makes themodel an extremely useful tool for policymakers and the public in deciding betweencompeting proposals.

Distinguishing Features of the Model

AGE models can be extended or adapted invarious ways to provide greater detail on partic-ular aspects of economic activity or to attemptgreater accuracy in the representation of eco-nomic reality. The approaches taken in differentmodels will differ according to the trade andeconomic policy issues that are of greatestinterest to those constructing the models anddesigning policy simulations.

In the case of the Carnegie model, importantobjectives were to explore the impact of pos-sible trade policy changes on economic growth,employment, agriculture, and low-skilled manu-facturing in developing countries. Because themajority of the world’s population lives in thosecountries, and the vast majority of livelihoodsthere depend on the agricultural sector orunskilled urban occupations, the impact ofglobal trade policies on these individuals andhouseholds will have an important effect onglobal economic activity, stability, and growth. Ifglobal trade extends opportunities to theseindividuals and households—the globalmajority—the global trading system can realizeits potential to contribute to poverty alleviation,equity, and broad-based growth. If these indi-viduals and households do not benefit, or ifthey face worse economic circumstances as aresult of global trade rules, the impact of tradewill be to concentrate wealth in a relativelysmall number of countries, firms, and house-holds. This would call into question both thelegitimacy and sustainability of an open globaltrade regime.

Trade policy changes tend to affect individualsand households more through effects on earn-ings, such as changes in employment or wagesor the prices of agricultural products sold, thanthrough effects on consumption, such aschanges in the prices of goods purchased.4 Theimpact of trade policies on demand in the agri-cultural sector and in labor markets of eachcountry is an important factor in gauging thewelfare results for the poor and for others whosemain asset is their labor. AGE models are wellsuited for probing these effects, because theycapture the gains or losses to both producersand consumers, through wage and pricechanges that are induced by trade liberalization.

The importance of agriculture and unskilledlabor demand for the livelihoods of the globalmajority makes it imperative to represent themarkets for agricultural and unskilled labor indeveloping countries as accurately as possiblein the model. The Carnegie model makesseveral important innovations in this regardcompared with other models.5

Most general equilibrium models include onlytwo classes of labor, skilled and unskilled,without distinguishing between unskilled laborin urban and agricultural labor markets. In manydeveloping countries, however, a large share ofthe economically active population is engagedin small-scale agriculture. The labor market inthat sector is quite distinct from urban labormarkets. To reflect this reality, the Carnegiemodel disaggregates labor into three types:agricultural labor, urban unskilled labor, andurban skilled labor.

Most models assume that all labor, includingunskilled labor, is fully employed.Unemployment is not taken into account. Anyincreases (or decreases) in demand for laborcaused by trade policy changes will be shown inthe model results as rising (or declining) wages.This assumption is highly inaccurate for the

Carnegie Endowment for International Peace 7

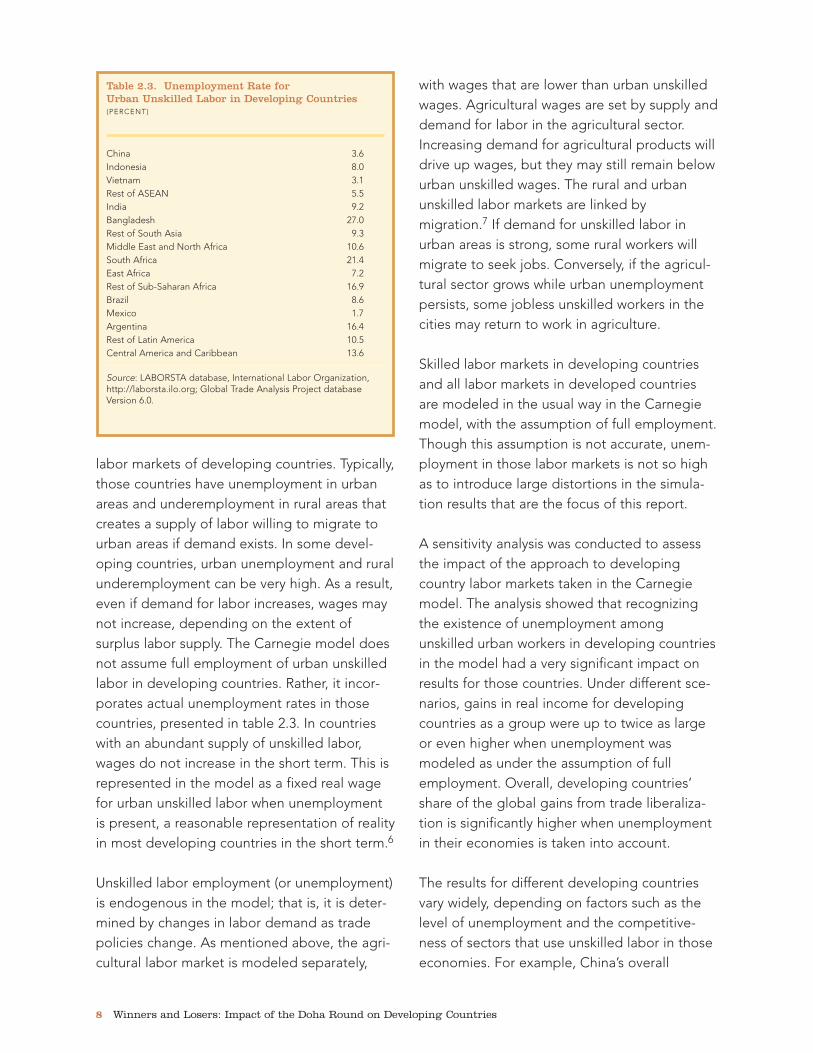

labor markets of developing countries. Typically,those countries have unemployment in urbanareas and underemployment in rural areas thatcreates a supply of labor willing to migrate tourban areas if demand exists. In some devel-oping countries, urban unemployment and ruralunderemployment can be very high. As a result,even if demand for labor increases, wages maynot increase, depending on the extent ofsurplus labor supply. The Carnegie model doesnot assume full employment of urban unskilledlabor in developing countries. Rather, it incor-porates actual unemployment rates in thosecountries, presented in table 2.3. In countrieswith an abundant supply of unskilled labor,wages do not increase in the short term. This isrepresented in the model as a fixed real wagefor urban unskilled labor when unemploymentis present, a reasonable representation of realityin most developing countries in the short term.6

Unskilled labor employment (or unemployment)is endogenous in the model; that is, it is deter-mined by changes in labor demand as tradepolicies change. As mentioned above, the agri-cultural labor market is modeled separately,

with wages that are lower than urban unskilledwages. Agricultural wages are set by supply anddemand for labor in the agricultural sector.Increasing demand for agricultural products willdrive up wages, but they may still remain belowurban unskilled wages. The rural and urbanunskilled labor markets are linked bymigration.7 If demand for unskilled labor inurban areas is strong, some rural workers willmigrate to seek jobs. Conversely, if the agricul-tural sector grows while urban unemploymentpersists, some jobless unskilled workers in thecities may return to work in agriculture.

Skilled labor markets in developing countriesand all labor markets in developed countriesare modeled in the usual way in the Carnegiemodel, with the assumption of full employment.Though this assumption is not accurate, unem-ployment in those labor markets is not so highas to introduce large distortions in the simula-tion results that are the focus of this report.

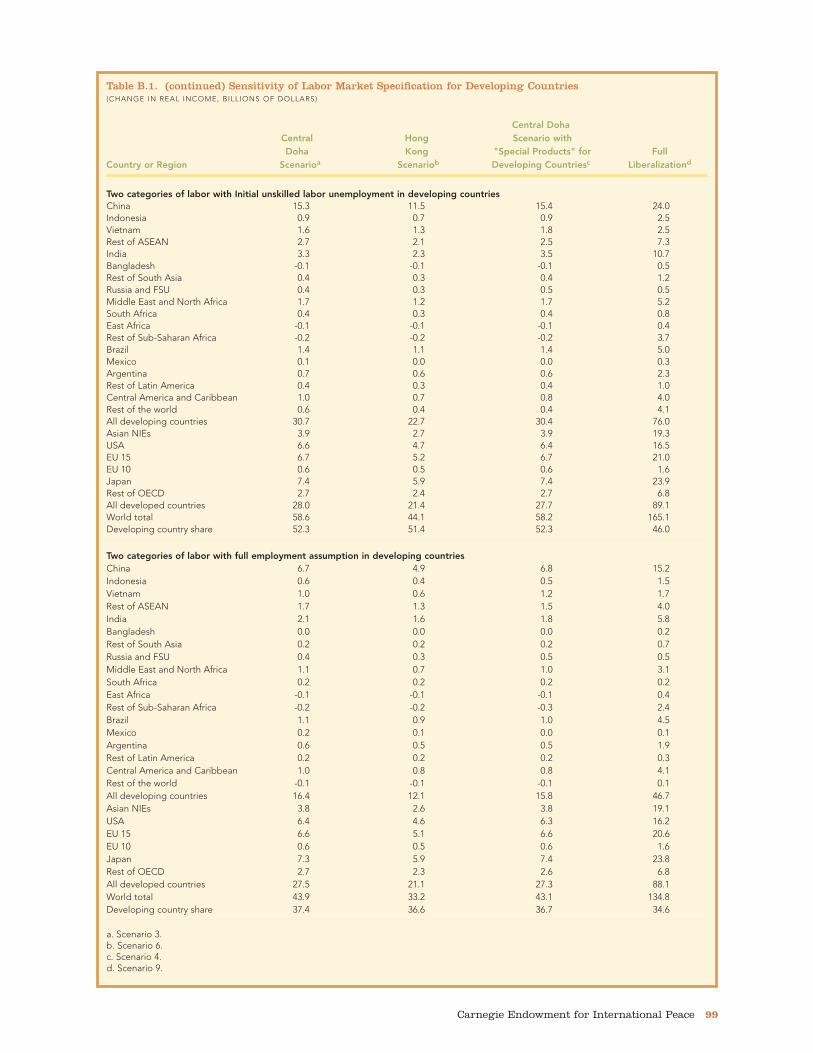

A sensitivity analysis was conducted to assessthe impact of the approach to developingcountry labor markets taken in the Carnegiemodel. The analysis showed that recognizingthe existence of unemployment amongunskilled urban workers in developing countriesin the model had a very significant impact onresults for those countries. Under different sce-narios, gains in real income for developingcountries as a group were up to twice as largeor even higher when unemployment wasmodeled as under the assumption of fullemployment. Overall, developing countries’share of the global gains from trade liberaliza-tion is significantly higher when unemploymentin their economies is taken into account.

The results for different developing countriesvary widely, depending on factors such as thelevel of unemployment and the competitive-ness of sectors that use unskilled labor in thoseeconomies. For example, China’s overall

8 Winners and Losers: Impact of the Doha Round on Developing Countries

Table 2.3. Unemployment Rate for Urban Unskilled Labor in Developing Countries(PERCENT)

China 3.6Indonesia 8.0Vietnam 3.1Rest of ASEAN 5.5India 9.2Bangladesh 27.0Rest of South Asia 9.3Middle East and North Africa 10.6South Africa 21.4East Africa 7.2Rest of Sub-Saharan Africa 16.9Brazil 8.6Mexico 1.7Argentina 16.4Rest of Latin America 10.5Central America and Caribbean 13.6

Source: LABORSTA database, International Labor Organization,http://laborsta.ilo.org; Global Trade Analysis Project databaseVersion 6.0.

income gains are more than twice as largewhen unemployment is included in the model.At the same time, a few developing countriesthat are less competitive would see smallergains or larger losses because of the extraadvantage that their more competitive counter-parts enjoy when wages are constrained byunemployment. Mexico and Central Americagain less and Bangladesh loses more in the faceof competition from more efficient countrieswith reserves of unemployed labor.

The sensitivity analysis suggests that modelsthat do not acknowledge unemployment indeveloping countries probably understate gainsfor countries that have competitive manufac-turing sectors to a significant degree, whileminimizing the negative effects on less compet-itive developing countries.

Separating unskilled labor into agricultural andurban unskilled labor forces has a lesser effecton the results. However, the effect is in theopposite direction from that of unemployment.Depending on the scenario, the gains to devel-oping countries as a group are about 2 to 6percent less if these labor forces are modeledseparately rather than as a single unskilledlabor group. This suggests that models thatcombine these two distinct groups into one willtend to overstate the gains to developing coun-tries, although the overstatement will be small.

The results are reported in greater detail inappendix B.

Characteristics of the Global Economy as Represented in the Model

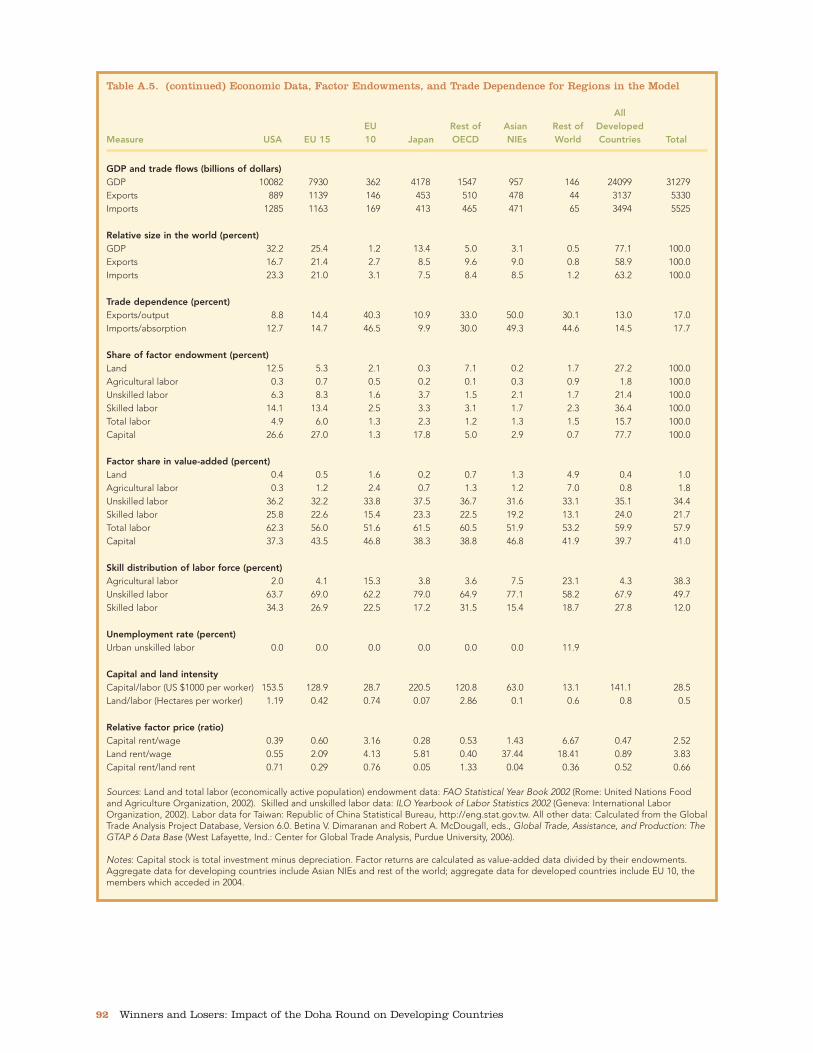

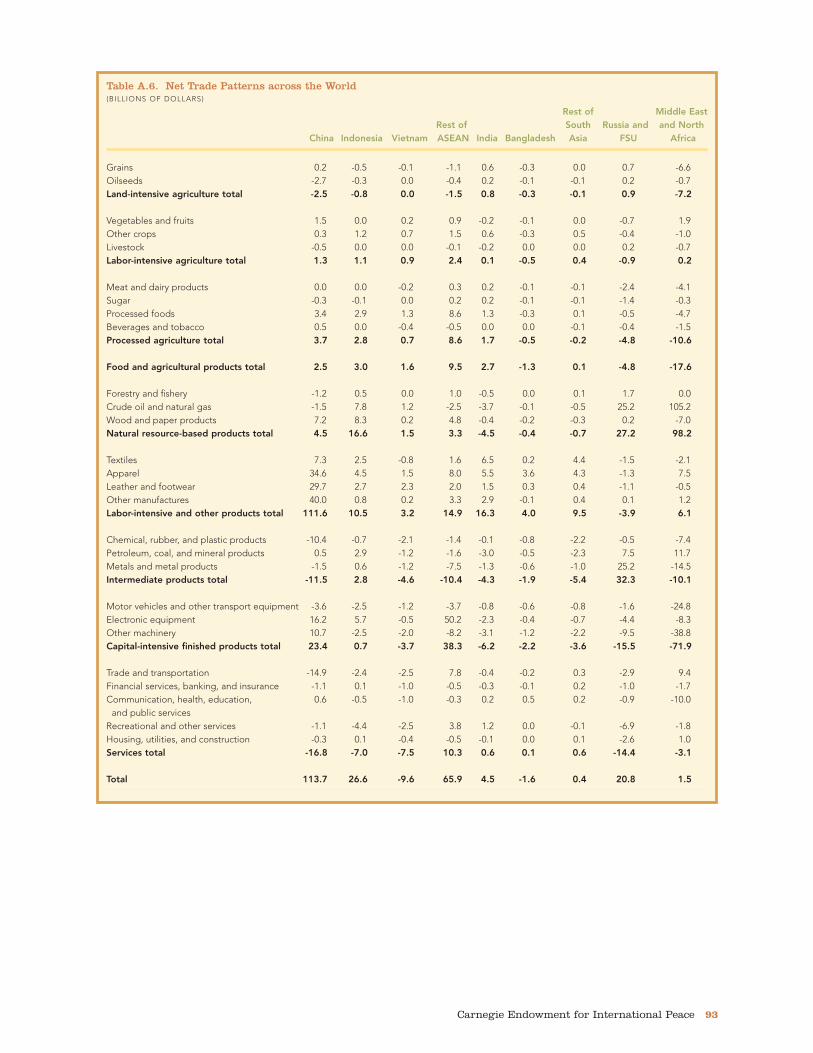

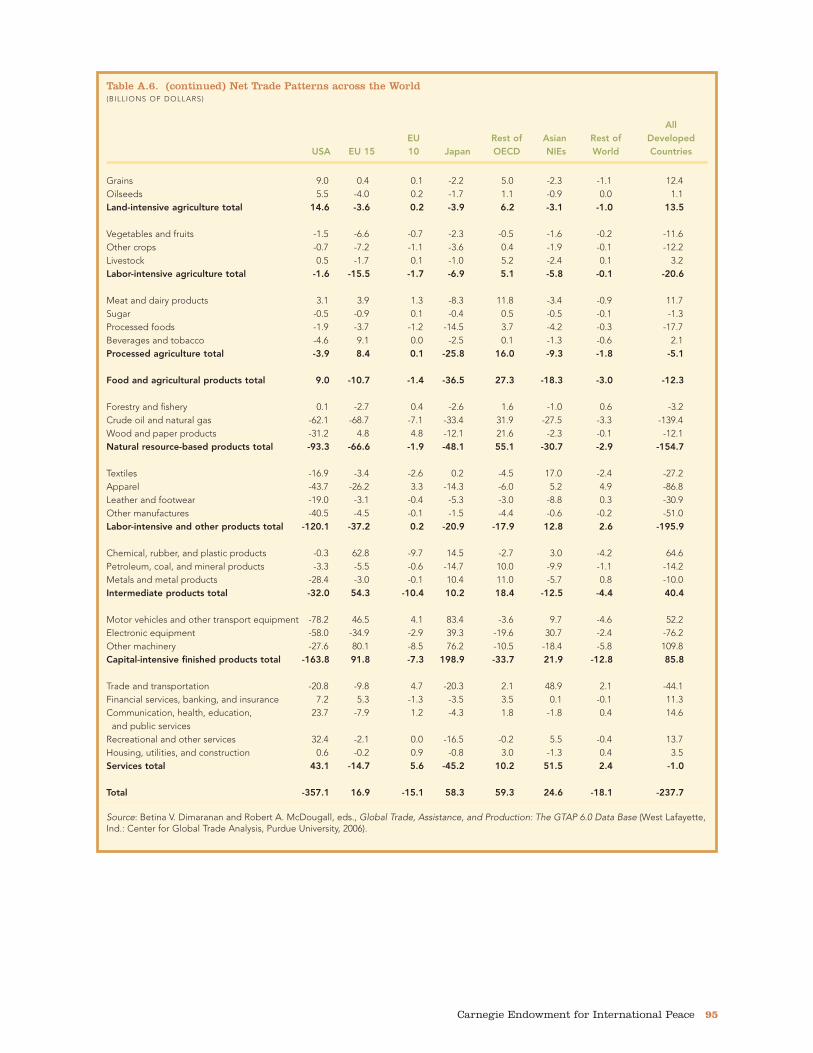

The main data used in the Carnegie model torepresent the existing global economy are pre-sented in tables A.5 and A.6 of appendix A.Table A.5 covers measures such as grossdomestic product (GDP), trade flows, trade

dependence, and factor endowments for eachcountry and region. These variables help toexplain both existing patterns of trade and thepotential impact of trade policy changes. TableA.6 presents the existing net trade patternsacross the world.

A key factor in understanding existing tradepatterns is the distribution of land, labor, andcapital in the global economic system. Thecombination of these factors of production ineach country’s endowment determines its com-parative advantage relative to others in theworld economy. Because these endowmentsare distributed unevenly, countries have dif-ferent relative strengths and costs of produc-tion. For example, if a country has a largesupply of unskilled labor but little capital, itscost of labor will be lower relative to its cost ofcapital. Goods that it produces using unskilledlabor intensively will be relatively inexpensive,both domestically and if exported to countriesthat have relatively scarce (and therefore moreexpensive) supplies of such labor. Similarly, acountry that has abundant land and capital butrelatively scarce labor will tend to produce agri-cultural crops that can be farmed in mecha-nized ways and export them to other countrieswith differing factor endowments and costs.

The data presented in table A.5 show that thehigh-income regions—the United States,European Union (EU), Japan, other high-incomemembers of the Organization for EconomicCooperation and Development (OECD), and thenewly industrialized economies (NIEs) of Asia—are home to only about 16 percent of the globallabor force but possess 78 percent of the world’scapital stock. In contrast, developing regions arehome to more than 84 percent of the globallabor force but possess just 22 percent of theworld’s capital stock. The high-income regionsare also relatively abundant in skilled labor, with36 percent of the world’s skilled labor, more thantwice their share of the total global labor force.

Carnegie Endowment for International Peace 9

Land is more abundant in the developing world,which accounts for 73 percent of the worldendowment of agricultural land.

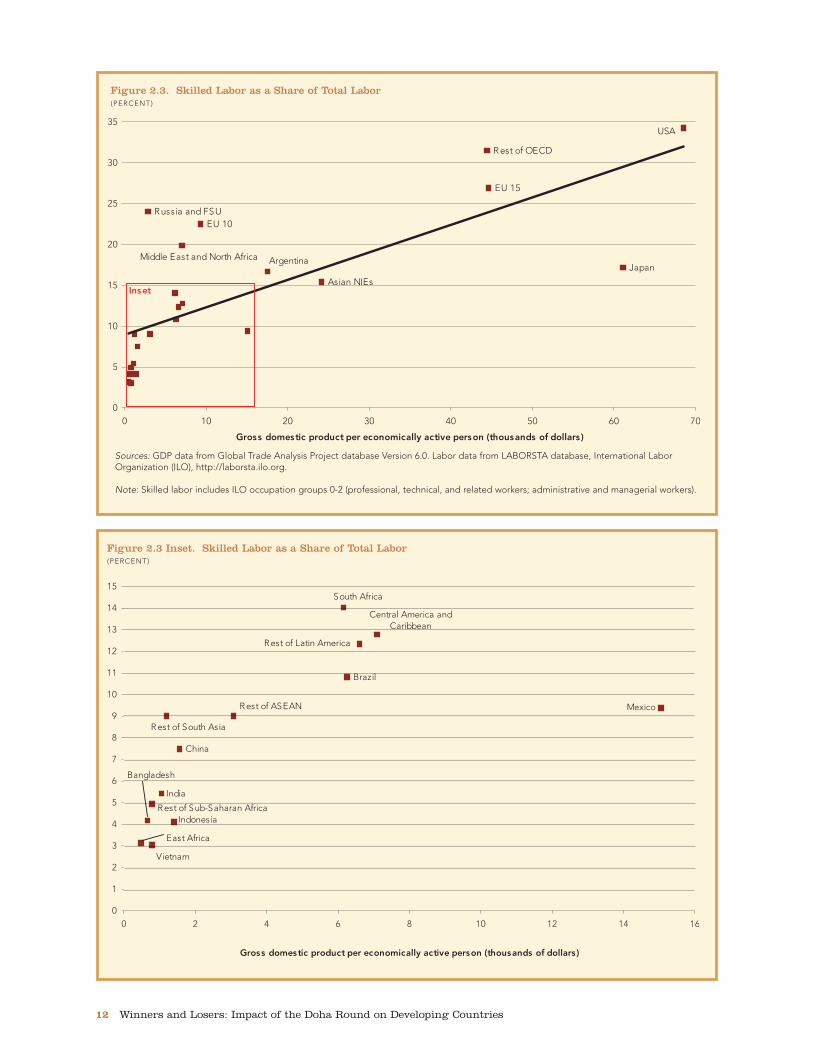

Figures 2.1 through 2.3 present the proportionof each class of labor (agricultural, urbanunskilled, and skilled) in the total economicallyactive population for each country or region.The x (horizontal) axis shows the level of GDPper economically active person, which is ameasure of how much wealth is created by eachparticipant in the labor force.8 Figure 2.1 indi-cates that economies with large proportions oftheir labor force in agriculture have relativelylow levels of GDP per worker. The trend lineindicates that wealth per worker increases asthe share of agricultural labor declines. It alsoshows that some of the most populous coun-tries in the world, including China, India,Bangladesh, and Indonesia, continue to havevery high proportions of their labor force inagriculture. Figure 2.2 suggests that countriesbecome richer as their share of unskilled laborin sectors other than agriculture increases.

Figure 2.3 and the detailed inset show an evenstronger correlation between the endowment ofskilled labor in an economy and its ability to gen-erate higher levels of GDP per worker. Countriessuch as China and India, notwithstanding recentgrowth and diversification, still have low sharesof skilled labor (7.5 and 5.4 percent, respectively)in their total labor endowment.

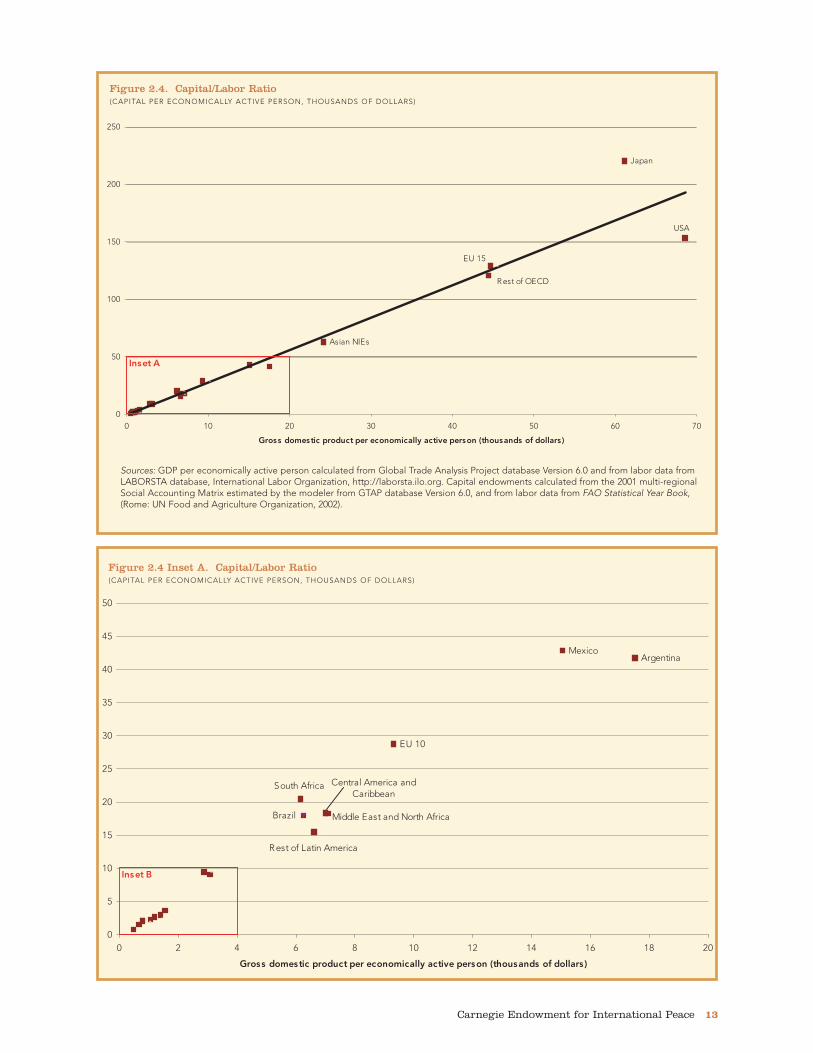

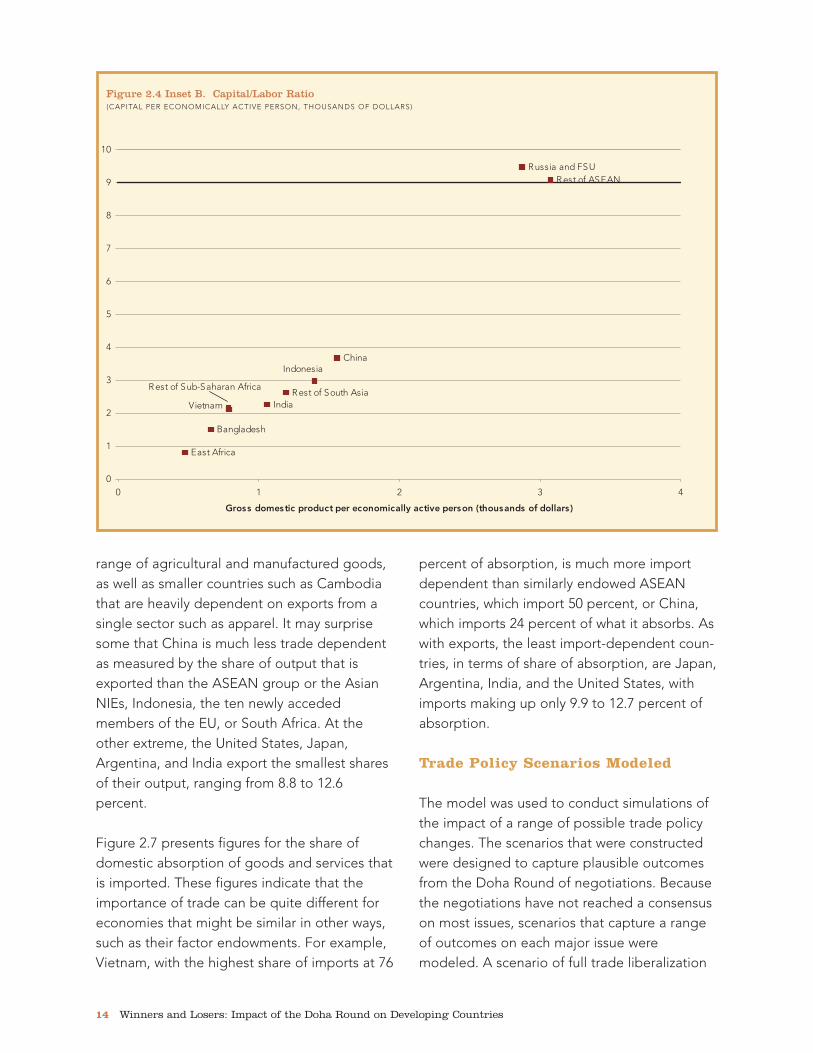

The ratio of capital to labor, which is the accu-mulated capital per worker measured in dollars,is shown in figure 2.4 and the two related insets.Japan has the highest capital intensity, with$220,500 of accumulated capital per worker,while the U.S. ratio is $153,500 per worker. Inthe fifteen pre-2004 members of the EU (EU 15),the ratio is $128,900 per worker. In China,despite high inflows of capital in recent years,the ratio is $3,700 of accumulated capital perworker. The figure for India is $2,300. The

lowest capital/labor ratios are found in the leastdeveloped countries (LDCs), includingBangladesh ($1,500) and East Africa, whichincludes Tanzania, Malawi, and Uganda ($800).

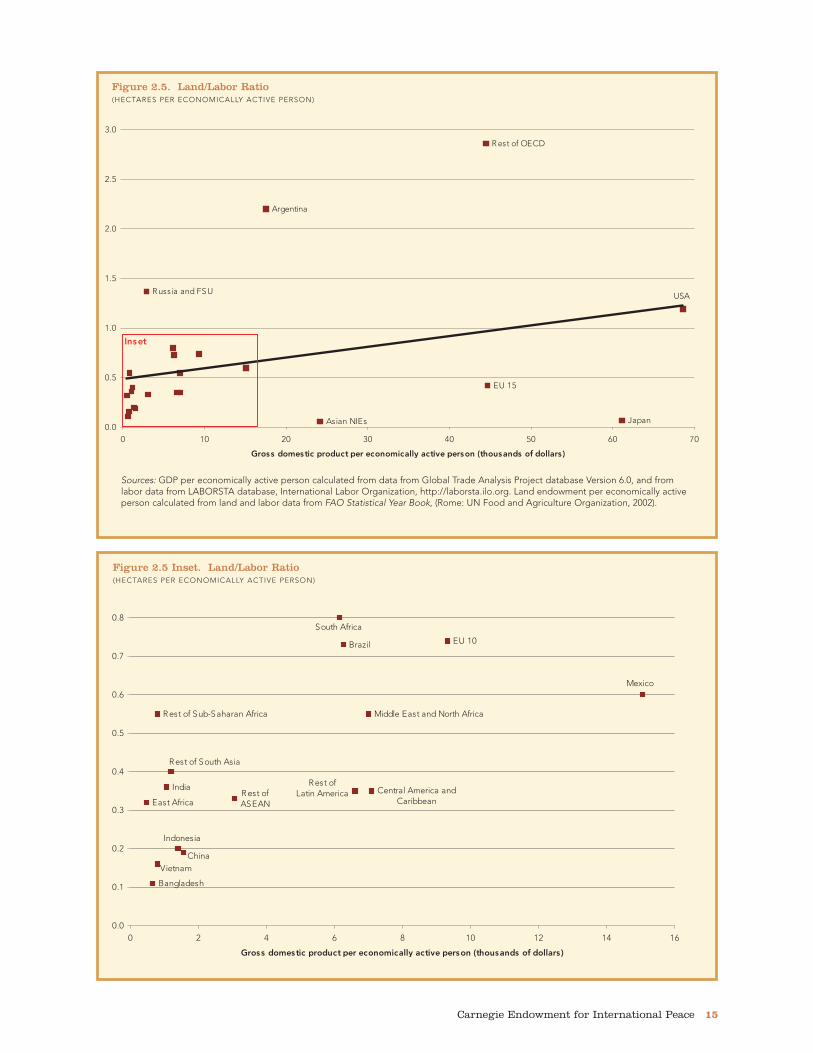

Figure 2.5 and the inset present the ratio of landto labor. With respect to land, Japan, the AsianNIEs, China, Indonesia, Vietnam, andBangladesh are poorly endowed with arable landrelative to the size of their labor force. Theirlabor share is much greater than their land sharein the total world endowment (see table A.5).Conditions are just the opposite in the UnitedStates, other high-income OECD countries(including Canada, Australia, and New Zealand),Argentina, Brazil, South Africa, Russia, and therest of the former Soviet Union, where land is rel-atively abundant compared with labor. The EU,India, both North Africa and Sub-Saharan Africa,the Middle East, and Mexico have intermediateamounts of arable land relative to the size oftheir labor force (their land share and labor sharein total world endowment are roughly the same).The relative abundance of land and the ratio ofland to labor are not as strongly correlated withoverall GDP per worker as is the abundance ofskilled labor or the capital/labor ratio. Thisreflects the fact that the productivity of agricul-tural land varies widely, depending on inherentfactors such as fertility and climate as well as thelevel of technology used.

Another important characteristic of economiesis their level of dependence on trade. This is afunction of the share of their economic outputthat is exported and the share of consumptionby households, investment by firms, andspending by government that is imported.Figure 2.6 presents the share of output that isexported by each economy, arrayed from themost trade dependent to the least. By far themost trade-dependent region in terms ofexports is the Association of Southeast AsianNations (ASEAN) region, which includesThailand and the Philippines, which export a

10 Winners and Losers: Impact of the Doha Round on Developing Countries

Carnegie Endowment for International Peace 11

-

-

-

-

-

-

-

-

-

-

-

-

--

-

-

-

-

-

-

-

-

-

anihC

01 UE

aisenodnI

aidnI

ocixeM

sEIN naisA

manteiVacirfA narahaS-buS fo tseR

acirfA tsaE

anitnegrA

hsedalgnaB

lizarB

naebbiraC dna aciremA lartneC

51 UEnapaJDCEO fo tseR

USF dna aissuR

NAESA fo tseR

tsaE elddiMacirfA htroN dna

aisA htuoS fo tseR

aciremA nitaL fo tseR

acirfA htuoS

0

01

02

03

04

05

06

07

08

09

070605040302010

)srallod fo sdnasuoht( nosrep evitca yllacimonoce rep tcudorp citsemod ssorGa

USA

Figure 2.1. Agricultural Labor as a Share of Total Labor(PERCENT)

Sources: GDP data from Global Trade Analysis Project database Version 6.0. Betina V. Dimaranan and Robert A. McDougall, eds., GlobalTrade, Assistance, and Production: The GTAP 6 Data Base, (West Lafayette, Ind.: Center for Global Trade Analysis, Purdue University, 2006).Labor data from LABORSTA database, International Labor Organization, http://laborsta.ilo.org.

a. Gross Domestic Product in 2001 US Dollars.

-

-

-

-

-

-

-

-

-

-

-

-

-

--

-

-

-

-

-

-

-

-

acirfA tsaE

anitnegrAlizarB

51 UE

sEIN naisA

DCEO fo tseR

acirfA htuoS

hsedalgnaB

aciremA lartneCnaebbiraC dna

anihC

01 UE

aisenodnI

aidnI

napaJ

ocixeMaissuRUSF dna USA

manteiV

NAESA fo tseR

acirfA htroN dna tsaE elddiM

aisA htuoS fo tseR

fo tseRaciremA nitaL

acirfA narahaS-buS fo tseR

0

01

02

03

04

05

06

07

08

09

070605040302010

)srallod fo sdnasuoht( nosrep evitca yllacimonoce rep tcudorp citsemod ssorG

Figure 2.2. Urban Unskilled Labor as a Share of Total Labor(PERCENT)

Sources: GDP data from Global Trade Analysis Project database Version 6.0. Labor data from LABORSTA database, International LaborOrganization (ILO), http://laborsta.ilo.org.

Note: Urban unskilled labor includes ILO occupation groups 3-5 (clerical and related workers; sales workers; service workers) and 7-9, (produc-tion and related workers, transport equipment operators, and laborers).

12 Winners and Losers: Impact of the Doha Round on Developing Countries

01 UE

51 UE

napaJ

sEIN naisA

DCEO fo tseR

USF dna aissuR

anitnegrA

USA

acirfA htroN dna tsaE elddiM

0

5

01

51

02

52

03

53

070605040302010

)srallod fo sdnasuoht( nosrep evitca yllacimonoce rep tcudorp citsemod ssorG

tesnI

Figure 2.3. Skilled Labor as a Share of Total Labor(PERCENT)

Sources: GDP data from Global Trade Analysis Project database Version 6.0. Labor data from LABORSTA database, International LaborOrganization (ILO), http://laborsta.ilo.org.

Note: Skilled labor includes ILO occupation groups 0-2 (professional, technical, and related workers; administrative and managerial workers).

-

-

-

-

-

-

-

-

-

--

-

-

-

lizarB

anihC

acirfA tsaE

hsedalgnaB

dna aciremA lartneCnaebbiraC

aisenodnI

aidnI

ocixeM

manteiV

NAESA fo tseR

aisA htuoS fo tseR

aciremA nitaL fo tseR

acirfA narahaS-buS fo tseR

acirfA htuoS

0

1

2

3

4

5

6

7

8

9

01

11

21

31

41

51

6141210186420

)srallod fo sdnasuoht( nosrep evitca yllacimonoce rep tcudorp citsemod ssorG

Figure 2.3 Inset. Skilled Labor as a Share of Total Labor(PERCENT)

Carnegie Endowment for International Peace 13

-

-

-

-

-

-

--

-

-

-

-

-

-

-

-

-

anitnegrA

01 UE

ocixeM

lizarB

dna aciremA lartneCnaebbiraC

acirfA htroN dna tsaE elddiM

aciremA nitaL fo tseR

acirfA htuoS

0

5

01

51

02

52

03

53

04

54

05

02816141210186420

)srallod fo sdnasuoht( nosrep evitca yllacimonoce rep tcudorp citsemod ssorG

B tesnI

Figure 2.4 Inset A. Capital/Labor Ratio(CAPITAL PER ECONOMICALLY ACTIVE PERSON, THOUSANDS OF DOLLARS)

-

-

-

- -

-

-

-

--

-

-

-

-

-

-

--

-

-

-

-

-

napaJ

sEIN naisA

51 UE

DCEO fo tseR

USA

0

05

001

051

002

052

070605040302010

)srallod fo sdnasuoht( nosrep evitca yllacimonoce rep tcudorp citsemod ssorG

A tesnI

Figure 2.4. Capital/Labor Ratio(CAPITAL PER ECONOMICALLY ACTIVE PERSON, THOUSANDS OF DOLLARS)

Sources: GDP per economically active person calculated from Global Trade Analysis Project database Version 6.0 and from labor data fromLABORSTA database, International Labor Organization, http://laborsta.ilo.org. Capital endowments calculated from the 2001 multi-regionalSocial Accounting Matrix estimated by the modeler from GTAP database Version 6.0, and from labor data from FAO Statistical Year Book,(Rome: UN Food and Agriculture Organization, 2002).

range of agricultural and manufactured goods,as well as smaller countries such as Cambodiathat are heavily dependent on exports from asingle sector such as apparel. It may surprisesome that China is much less trade dependentas measured by the share of output that isexported than the ASEAN group or the AsianNIEs, Indonesia, the ten newly accededmembers of the EU, or South Africa. At theother extreme, the United States, Japan,Argentina, and India export the smallest sharesof their output, ranging from 8.8 to 12.6percent.

Figure 2.7 presents figures for the share ofdomestic absorption of goods and services thatis imported. These figures indicate that theimportance of trade can be quite different foreconomies that might be similar in other ways,such as their factor endowments. For example,Vietnam, with the highest share of imports at 76

percent of absorption, is much more importdependent than similarly endowed ASEANcountries, which import 50 percent, or China,which imports 24 percent of what it absorbs. Aswith exports, the least import-dependent coun-tries, in terms of share of absorption, are Japan,Argentina, India, and the United States, withimports making up only 9.9 to 12.7 percent ofabsorption.

Trade Policy Scenarios Modeled

The model was used to conduct simulations ofthe impact of a range of possible trade policychanges. The scenarios that were constructedwere designed to capture plausible outcomesfrom the Doha Round of negotiations. Becausethe negotiations have not reached a consensuson most issues, scenarios that capture a rangeof outcomes on each major issue weremodeled. A scenario of full trade liberalization

14 Winners and Losers: Impact of the Doha Round on Developing Countries

-

-

-

-

-

-

-

-

-

-

acirfA tsaE

hsedalgnaB

anihC

aidnI

USF dna aissuRNAESA fo tseR

aisA htuoS fo tseR

aisenodnI

manteiV

acirfA narahaS-buS fo tseR

0

1

2

3

4

5

6

7

8

9

01

43210

)srallod fo sdnasuoht( nosrep evitca yllacimonoce rep tcudorp citsemod ssorG

Figure 2.4 Inset B. Capital/Labor Ratio(CAPITAL PER ECONOMICALLY ACTIVE PERSON, THOUSANDS OF DOLLARS)

Carnegie Endowment for International Peace 15

acirfA tsaE

hsedalgnaB

lizarB 01 UE

aidnI

acirfA htroN dna tsaE elddiMacirfA narahaS-buS fo tseR

dna aciremA lartneCnaebbiraC

anihC

aisenodnI

ocixeM

manteiV

fo tseRNAESA

aisA htuoS fo tseR

fo tseRaciremA nitaL

acirfA htuoS

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

6141210186420

)srallod fo sdnasuoht( nosrep evitca yllacimonoce rep tcudorp citsemod ssorG

anitnegrA

51 UE

napaJsEIN naisA

DCEO fo tseR

USF dna aissuR USA

0.0

5.0

0.1

5.1

0.2

5.2

0.3

070605040302010

)srallod fo sdnasuoht( nosrep evitca yllacimonoce rep tcudorp citsemod ssorG

tesnI

Sources: GDP per economically active person calculated from data from Global Trade Analysis Project database Version 6.0, and fromlabor data from LABORSTA database, International Labor Organization, http://laborsta.ilo.org. Land endowment per economically activeperson calculated from land and labor data from FAO Statistical Year Book, (Rome: UN Food and Agriculture Organization, 2002).

Figure 2.5. Land/Labor Ratio(HECTARES PER ECONOMICALLY ACTIVE PERSON)

Figure 2.5 Inset. Land/Labor Ratio(HECTARES PER ECONOMICALLY ACTIVE PERSON)

16 Winners and Losers: Impact of the Doha Round on Developing Countries

0

01

02

03

04

05

06

07

08

Res

t o

f ASE

AN

Asi

an N

IEs

Ind

one

sia

Vie

tnam

EU

10

Sout

h A

fric

a

Chi

na

Res

t o

f OE

CD

Res

t o

f Sub

-Sah

aran

Afr

ica

Mid

dle

Eas

t an

d N

ort

h A

fric

a

Mex

ico

Cen

tral

Am

eric

an a

nd C

arib

bea

n

Res

t o

f So

uth

Asi

a

Res

t o

f Lat

in A

mer

ica

Ban

gla

des

h

Eas

t A

fric

a

EU

15

Bra

zil

Ind

ia

Arg

entin

a

Jap

an

USA

Rus

sia

and

FSU

Fgure 2.7. Imports as a Share of Absorption(PERCENT)

Source: Calculated from the 2001 multiregional Social Accounting Matrix estimated by the modeler from GTAP database Version 6.0. Betina V.Dimaranan and Robert A. McDougall, eds., Global Trade, Assistance, and Production: The GTAP 6 Data Base (West Lafayette, Ind.: Center forGlobal Trade Analysis, Purdue University, 2006).

0

01

02

03

04

05

06

07

Res

t o

f ASE

AN

Asi

an N

IEs

Ind

one

sia

Vie

tnam

EU

10

Sout

h A

fric

a

Chi

na

Res

t o

f OE

CD

Res

t o

f Sub

-Sah

aran

Afr

ica

Mid

dle

Eas

t an

d N

ort

h A

fric

a

Mex

ico

Cen

tral

Am

eric

an a

nd C

arib

bea

n

Res

t o

f So

uth

Asi

a

Res

t o

f Lat

in A

mer

ica

Ban

gla

des

h

Eas

t A

fric

a

EU

15

Bra

zil

Ind

ia

Arg

entin

a

Jap

an

USA

Rus

sia

and

FSU

Figure 2.6. Exports as a Share of Output(PERCENT)

Source: Calculated from the 2001 multiregional Social Accounting Matrix estimated by the modeler from GTAP database Version 6.0. Betina V.Dimaranan and Robert A. McDougall, eds., Global Trade, Assistance, and Production: The GTAP 6 Data Base (West Lafayette, Ind.: Center forGlobal Trade Analysis, Purdue University, 2006).

was also modeled as a reference point. Themain scenarios are described below and addi-tional details are provided in table 2.4.

In all the scenarios, reductions in tariffs andother forms of border protection are made fromapplied, rather than bound, rates.9 Appliedrates are the tariffs that are actually charged bycountries, while bound rates are the maximumtariffs that may be charged by a country underits WTO commitments. Negotiations on tariffreductions at the WTO usually take the form ofagreements to reduce bound tariffs. We choseto model reductions from applied rather thanbound rates for two reasons. First, and mostimportant, we wanted to capture the impact ofactual changes in tariffs on production, trade,demand for labor, and other economic meas-ures. Reductions in bound tariffs may notproduce any reduction in applied tariffs if thegap between bound and applied is large. Wewanted to use the model to simulate theimpact on the real world economy of realchanges in trade policies.

Second, a number of other models use scenariosthat take reductions from bound tariffs, oftenusing the bands or thresholds for different levelsof reductions that have been proposed in pastnegotiating sessions. This is a useful exercise,but there was no particular value in repeating ithere. In addition, the precision of using very spe-cific thresholds coupled with specific levels oftariff reductions within each band, or particularcoefficients for the size of cuts, means that thesescenarios quickly lose relevance if other bandsare proposed or agreed to in the negotiations.By contrast, the method we chose, reductions toapplied tariffs, can be thought of as an end pointthat would be achieved by any of various for-mulas of reductions in bound rates. When newproposals are made, their proponents (andothers) often calculate the resulting impact onapplied tariffs, which can be used for comparisonwith our scenarios.

The same approach was taken to reductions ofsubsidies and domestic support, which werereduced from applied rather than boundrates.10

The central Doha scenario that we constructedentails an ambitious expansion of market accessfor manufactured goods (50 percent reductionsin applied tariffs and other border protection bydeveloped countries and 33 percent reductionsby developing countries); a modestly ambitiousexpansion of market access for agriculturalproducts (36 percent reductions in appliedtariffs and other border protection by devel-oped countries and 24 percent reductions bydeveloping countries); reductions of domesticsubsidies for agricultural products by one-thirdby all countries except LDCs; and the elimina-tion of agricultural export subsidies by all coun-tries except LDCs. The scenario does notinclude market access liberalization by theLDCs, in line with agreements already made inthe Doha Round.11

The scenario was constructed separately foragricultural measures (scenario 1) and manufac-turing measures (scenario 2) and then cumu-lated (scenario 3). The results are sometimespresented for the separate components, todraw attention to the contribution of that sectorfor each country or group of countries. It shouldbe noted that the combined results for theoverall scenario differ slightly from the sum ofthe two sectoral scenarios. Because of the pres-ence of initial unemployment in unskilled labormarkets, if the overall scenario generates ahigher level of demand for either agricultural orunskilled labor or both, it may generate furtherincreases in total production and wage incomedue to general equilibrium effects.

We then varied different elements of thiscentral scenario to simulate other plausible out-comes of the Doha Round. First, we alloweddeveloping countries to exclude an unlimited

Carnegie Endowment for International Peace 17

18 Winners and Losers: Impact of the Doha Round on Developing Countries

Tab

le 2

.4.

Sce

nar

ios

Mod

eled

(4

)C

entr

al D

oha

Sc

enar

io w

ith

(8)

"Sp

ecia

l Sc

enar

io w

ith

(1)

(2)

(3)

Pro

duc

ts"

for

(5)

(6)

(7)

Lim

ited

Ag

ricu

ltur

e (9

) D

oha

Sce

nari

o f

or

Do

ha S

cena

rio

fo

r C

entr

al D

oha

D

evel

op

ing

M

od

est

Scen

ario

H

ong

Ko

ng

Lim

ited

Sce

nari

o

and

Am

bit

ious

Fu

ll P

olic

y M

easu

reA

gri

cult

ure

Man

ufac

ture

sSc

enar

ioC

oun

trie

sfo

r M

anuf

actu

res

Scen

ario

for

Ag

ricu

ltur

eM

anuf

actu

ring

Lib

eral

izat

ion

Red

ucti

on

in A

pp

lied

Tar

iffs

and

Oth

er B

ord

er P

rote

ctio

n (A

VE

s)a

Ag

ricul

tura

l pro

duc

tsD

evel

op

ed c

oun

trie

sR

educ

ed b

y 36

%N

o c

hang

eR

educ

ed b

y 36

%R

educ

ed b

y 36

%N

o c

hang

eR

educ

ed b

y 36

%R

educ

ed b

y 25

%R

educ

ed b

y 25

%R

educ

ed t

o z

ero

Dev

elo

pin

g c

oun

trie

sR

educ

ed b

y 24

%N

o c

hang

eR

educ

ed b

y 24

%N

o c

hang

eN

o c

hang

eR

educ

ed b

y 24

%R

educ

ed b

y 15

%R

educ

ed b

y 15

%R

educ

ed t

o z

ero

Man

ufac

ture

d p

rod

ucts

Dev

elo

ped

co

untr

ies

No

cha

nge

Red

uced

by

50%

Red

uced

by

50%

Red

uced

by

50%

Red

uced

by

36%

Red

uced

by

36%

No

cha

nge

Red

uced

by

50%

Red

uced

to

zer

oD

evel

op

ing

co

untr

ies

No

cha

nge

Red

uced

by

33%

Red

uced

by

33%

Red

uced

by

33%

Red

uced

by

24%

Red

uced

by

24%

No

cha

nge

Red

uced

by

33%

Red

uced

to

zer

o

Exp

ort

sub

sid

ies

Dev

elo

ped

co

untr

ies

Elim

inat

edN

o c

hang

eE

limin

ated

Elim

inat

edN

o c

hang

eE

limin

ated

Elim

inat

edE

limin

ated

Elim

inat

edD

evel

op

ing

co

untr

ies

Elim

inat

edN

o c

hang

eE

limin

ated

Elim

inat

edN

o c

hang

eE

limin

ated

Elim

inat

edE

limin

ated

Elim

inat

ed

Do

mes

tic

sup

po

rtD

evel

op

ed c

oun

trie

sR

educ

ed b

y 1/

3N

o c

hang

eR

educ

ed b

y 1/

3R

educ

ed b

y 1/

3N

o c

hang

eR

educ

ed b

y 1/

3R

educ

ed b

y 25

%R

educ

ed b

y 25

%E

limin

ated

Dev

elo

pin

g c

oun

trie

sR

educ

ed b

y 1/

3N

o c

hang

eR

educ

ed b

y 1/

3N

o c

hang

eN

o c

hang

eR

educ

ed b

y 1/

3R

educ

ed b

y 15

%R

educ

ed b

y 15

%E

limin

ated

Spec

ial t

reat

men

tb

Leas

t D

evel

op

ed C

oun

trie

s d

o n

ot

mak

e re

duc

tions

in s

cena

rios

1–8

No

ne

a. T

rad

e-w

eig

hted

ad

val

ore

m e

qui

vale

nt (A

VE

) pro

tect

ion.

An

ad v

alo

rem

eq

uiva

lent

is a

co

nver

sio

n o

f a s

pec

ific

tarif

f (a

spec

ific

amo

unt

per

uni

t tr

aded

) int

o a

n ad

val

ore

m t

ariff

(a p

erce

ntag

e o

f the

val

ue o

f the

go

od

) with

an

equi

vale

nt v

alue

.b

. Bec

ause

of a

gg

reg

atio

n, s

pec

ial t

reat

men

t fo

r le

ast

dev

elo

ped

co

untr

ies

in t

he m

od

el a

pp

lies

to t

he fo

llow

ing

co

untr

ies

or

reg

ions

: Ban

gla

des

h, E

ast

Afr

ica,

and

the

res

t o

f Sub

-Sah