wojciech misiĄg revenue and expenditure of local governments

TRANSCRIPT

WOJCIECH MISIĄG *

REVENUE AND EXPENDITURE OF LOCAL GOVERNMENTS

IN POLAND – RECOMMENDATIONS AND WARNINGS

* INSTITUTE FOR FINANCIAL RESEARCH AND ANALYSIS – UNIVERSITY OF IT & MANAGEMENT IN RZESZOW

SUPREME AUDIT OFFICE

PLAN OF THE PRESENTATION

1. HISTORY – KEY DATES 1989−2015

2. ORGANISATION AND STRUCTURE OF LOCAL & REGIONAL SELF-GOVERNMENT IN POLAND

3. REVENUE AND EXPENDITURE OF LOCAL GOVERNMENT ENTITIES (LGE)

4. FINANCIAL SITUATION OF LOCAL GOVERNMENTS

5. WHAT’S GOOD, WHAT’S WRONG – RECOMMENDATIONS AND WARNINGS

POLAND IN 1989

Centrally-planned, socialist-type economy

Small private sector outside agriculture

Large foreign debt (49 billion $)

Unbalanced state budget

Leading position of the communist party stated in the Constitution

Hierarchical system of state public administration

Communes without legal personality and without ownership rights

Non-democratic elections to the communes’ councils

Territorial organisation of the state: 49 voivodships, almost 2,500 communes

KEY DATES 1989−2015

1990 Self-government act – reactivation of the self-government in Poland (March) First elections (June) Self-government revenue act (December)

1991 Establishment of regional audit chambers

1997 New Constitution – new guarantees for the LGE

1998 Establishment of poviats (counties) and self-governed voivodships (regions)

2003 New Self-government revenue act – still in force

2004 Poland becomes the member of EU – new opportunities for LGs

2007 Voivodships become the managing authorities for the regional operational programmes

2009 New public finance act – budget procedures – still in force

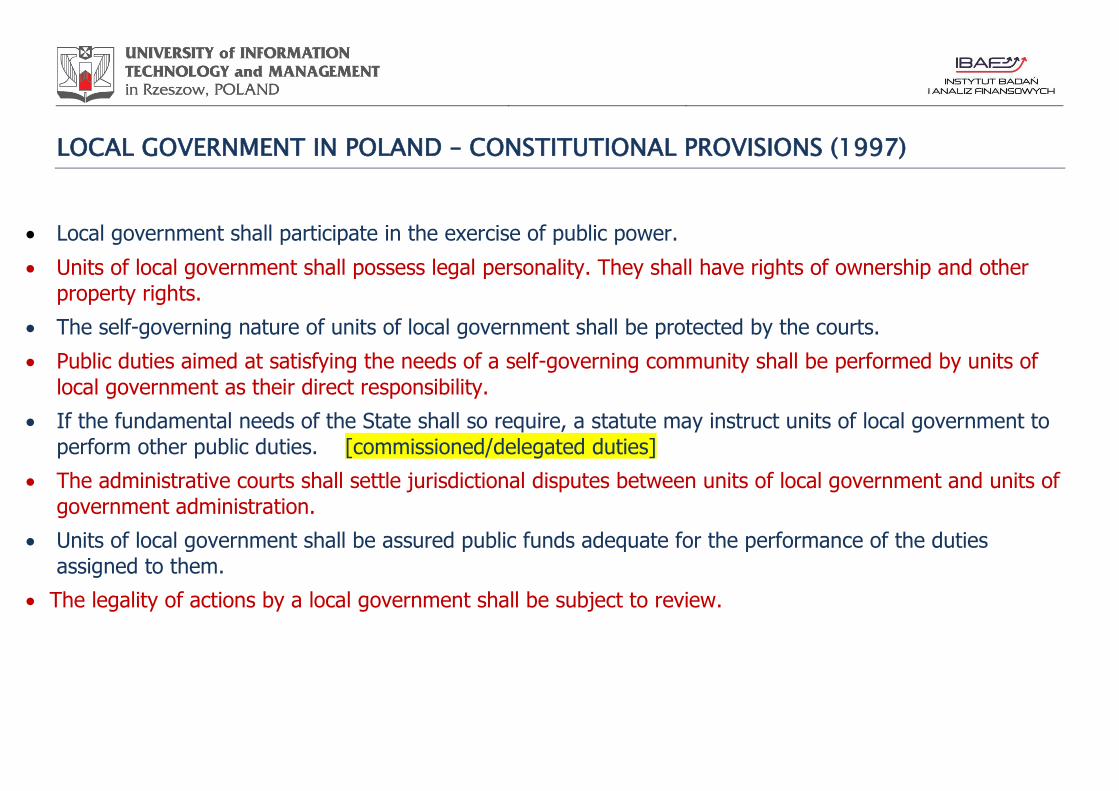

LOCAL GOVERNMENT IN POLAND – CONSTITUTIONAL PROVISIONS (1997)

Local government shall participate in the exercise of public power.

Units of local government shall possess legal personality. They shall have rights of ownership and other

property rights.

The self-governing nature of units of local government shall be protected by the courts.

Public duties aimed at satisfying the needs of a self-governing community shall be performed by units of

local government as their direct responsibility.

If the fundamental needs of the State shall so require, a statute may instruct units of local government to

perform other public duties. [commissioned/delegated duties]

The administrative courts shall settle jurisdictional disputes between units of local government and units of

government administration.

Units of local government shall be assured public funds adequate for the performance of the duties

assigned to them.

The legality of actions by a local government shall be subject to review.

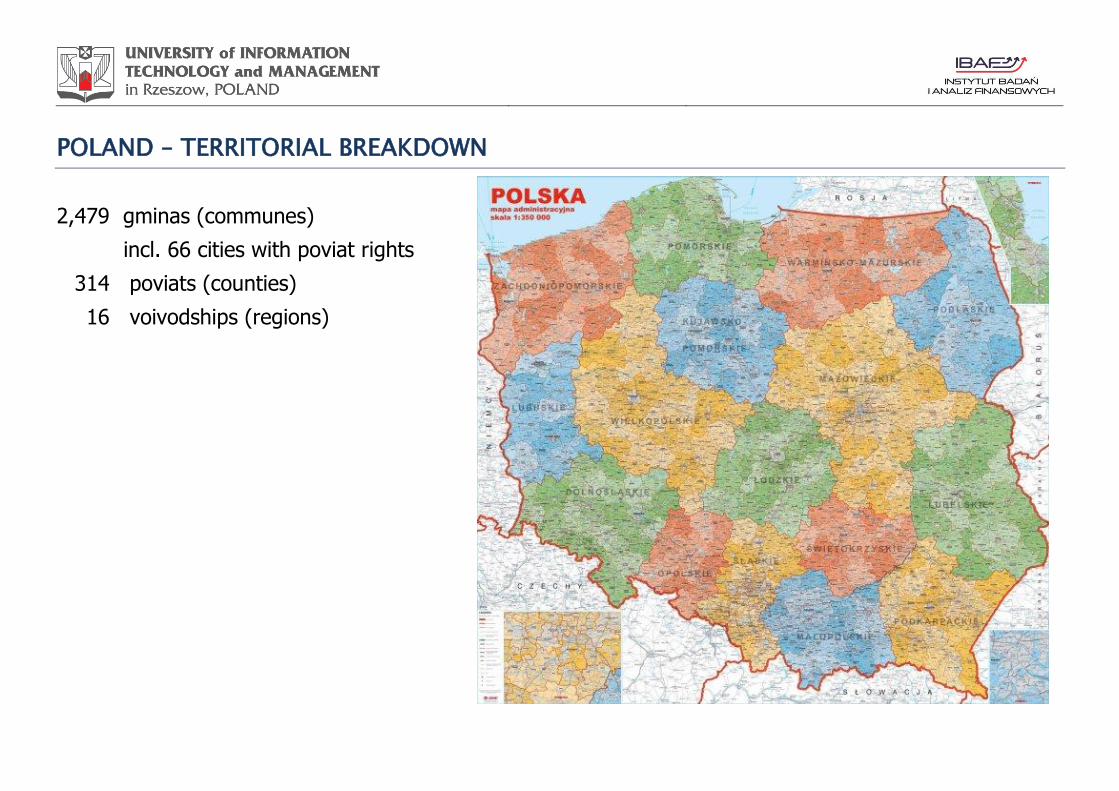

POLAND – TERRITORIAL BREAKDOWN

2,479 gminas (communes)

incl. 66 cities with poviat rights

2,314 poviats (counties)

2,416 voivodships (regions)

REVENUE OF LOCAL GOVERNMENT ENTITIES (1)

SIX TYPES OF REVENUE

1. LOCAL TAXES AND FEES

2. SHARES IN PERSONAL INCOME TAX (PIT) AND CORPORATE INCOME TAX (CIT)

3. GENERAL SUBSIDIES FROM THE STATE BUDGET

4. APPROPRIATED SUBSIDIES FROM THE STATE BUDGET (incl. EU FUNDS)

5. OTHER SUBSIDIES

6. OTHER OWN REVENUE

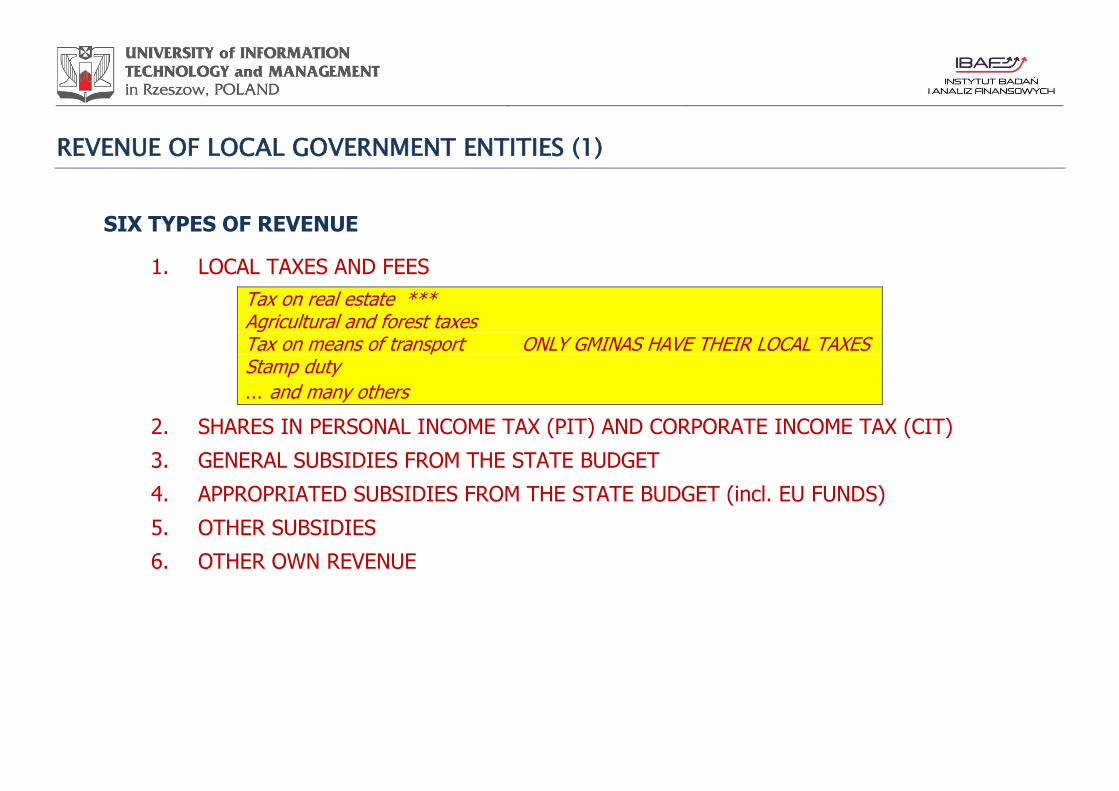

REVENUE OF LOCAL GOVERNMENT ENTITIES (1)

SIX TYPES OF REVENUE

1. LOCAL TAXES AND FEES

Tax on real estate *** Agricultural and forest taxes Tax on means of transport ONLY GMINAS HAVE THEIR LOCAL TAXES Stamp duty … and many others

2. SHARES IN PERSONAL INCOME TAX (PIT) AND CORPORATE INCOME TAX (CIT)

3. GENERAL SUBSIDIES FROM THE STATE BUDGET

4. APPROPRIATED SUBSIDIES FROM THE STATE BUDGET (incl. EU FUNDS)

5. OTHER SUBSIDIES

6. OTHER OWN REVENUE

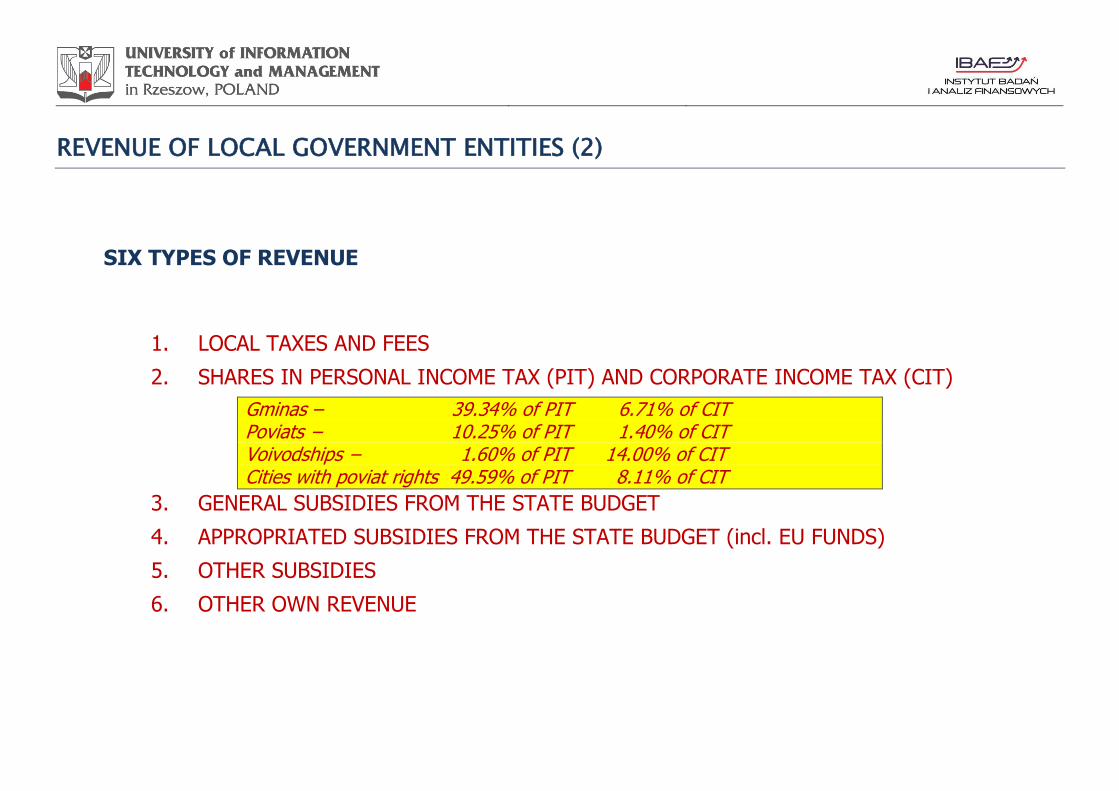

REVENUE OF LOCAL GOVERNMENT ENTITIES (2)

SIX TYPES OF REVENUE

1. LOCAL TAXES AND FEES

2. SHARES IN PERSONAL INCOME TAX (PIT) AND CORPORATE INCOME TAX (CIT)

Gminas – 39.34% of PIT 6.71% of CIT Poviats − 10.25% of PIT 1.40% of CIT Voivodships − 1.60% of PIT 14.00% of CIT Cities with poviat rights 49.59% of PIT 8.11% of CIT

3. GENERAL SUBSIDIES FROM THE STATE BUDGET

4. APPROPRIATED SUBSIDIES FROM THE STATE BUDGET (incl. EU FUNDS)

5. OTHER SUBSIDIES

6. OTHER OWN REVENUE

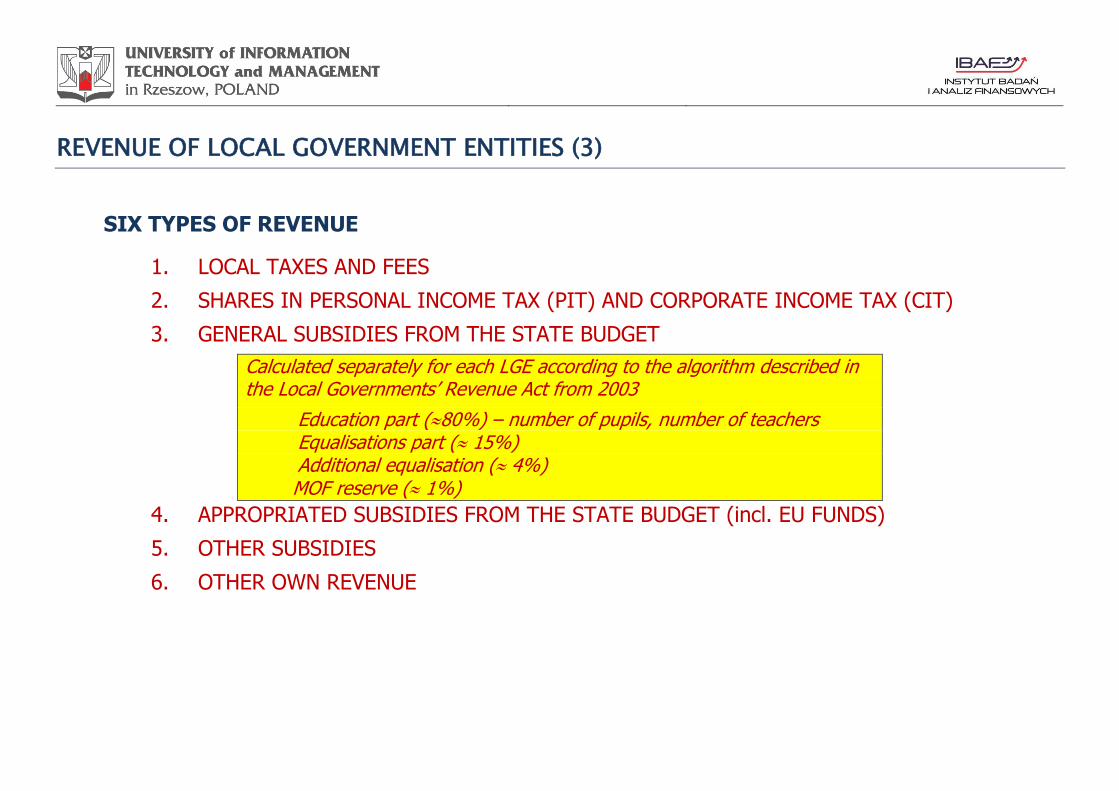

REVENUE OF LOCAL GOVERNMENT ENTITIES (3)

SIX TYPES OF REVENUE

1. LOCAL TAXES AND FEES

2. SHARES IN PERSONAL INCOME TAX (PIT) AND CORPORATE INCOME TAX (CIT)

3. GENERAL SUBSIDIES FROM THE STATE BUDGET

Calculated separately for each LGE according to the algorithm described in the Local Governments’ Revenue Act from 2003

Education part (80%) – number of pupils, number of teachers Equalisations part ( 15%) Additional equalisation ( 4%) MOF reserve ( 1%)

4. APPROPRIATED SUBSIDIES FROM THE STATE BUDGET (incl. EU FUNDS)

5. OTHER SUBSIDIES

6. OTHER OWN REVENUE

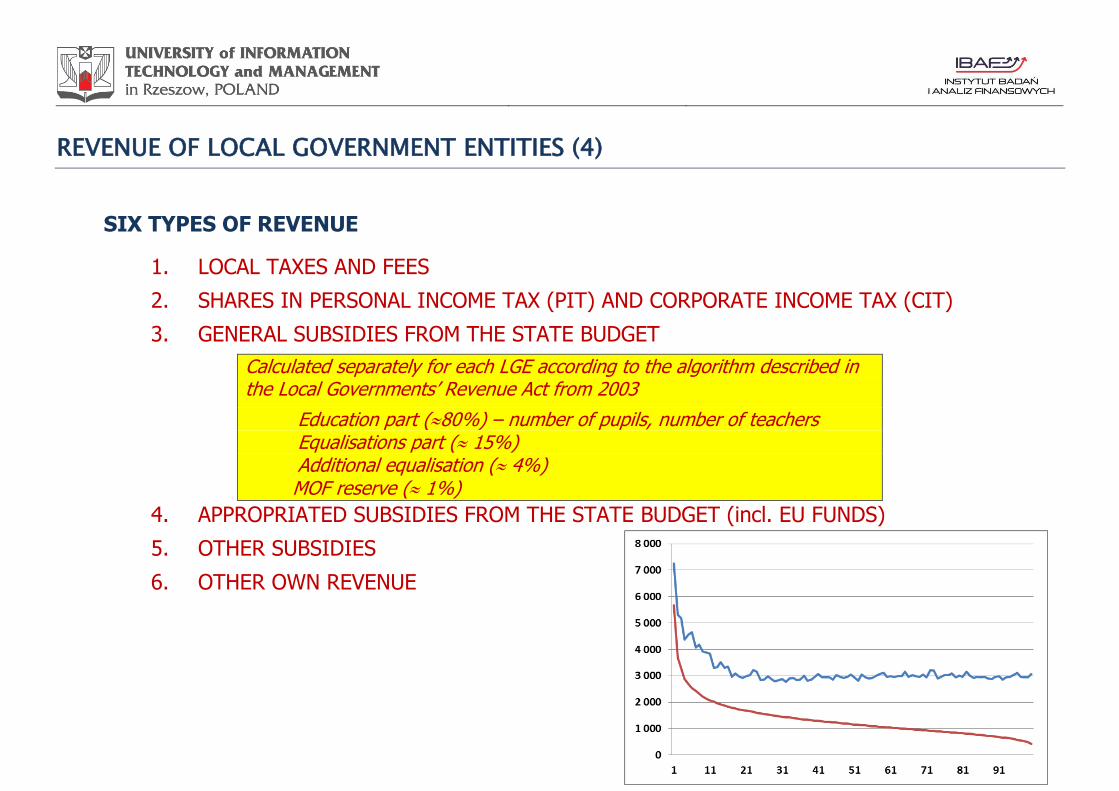

REVENUE OF LOCAL GOVERNMENT ENTITIES (4)

SIX TYPES OF REVENUE

1. LOCAL TAXES AND FEES

2. SHARES IN PERSONAL INCOME TAX (PIT) AND CORPORATE INCOME TAX (CIT)

3. GENERAL SUBSIDIES FROM THE STATE BUDGET

Calculated separately for each LGE according to the algorithm described in the Local Governments’ Revenue Act from 2003

Education part (80%) – number of pupils, number of teachers Equalisations part ( 15%) Additional equalisation ( 4%) MOF reserve ( 1%)

4. APPROPRIATED SUBSIDIES FROM THE STATE BUDGET (incl. EU FUNDS)

5. OTHER SUBSIDIES

6. OTHER OWN REVENUE

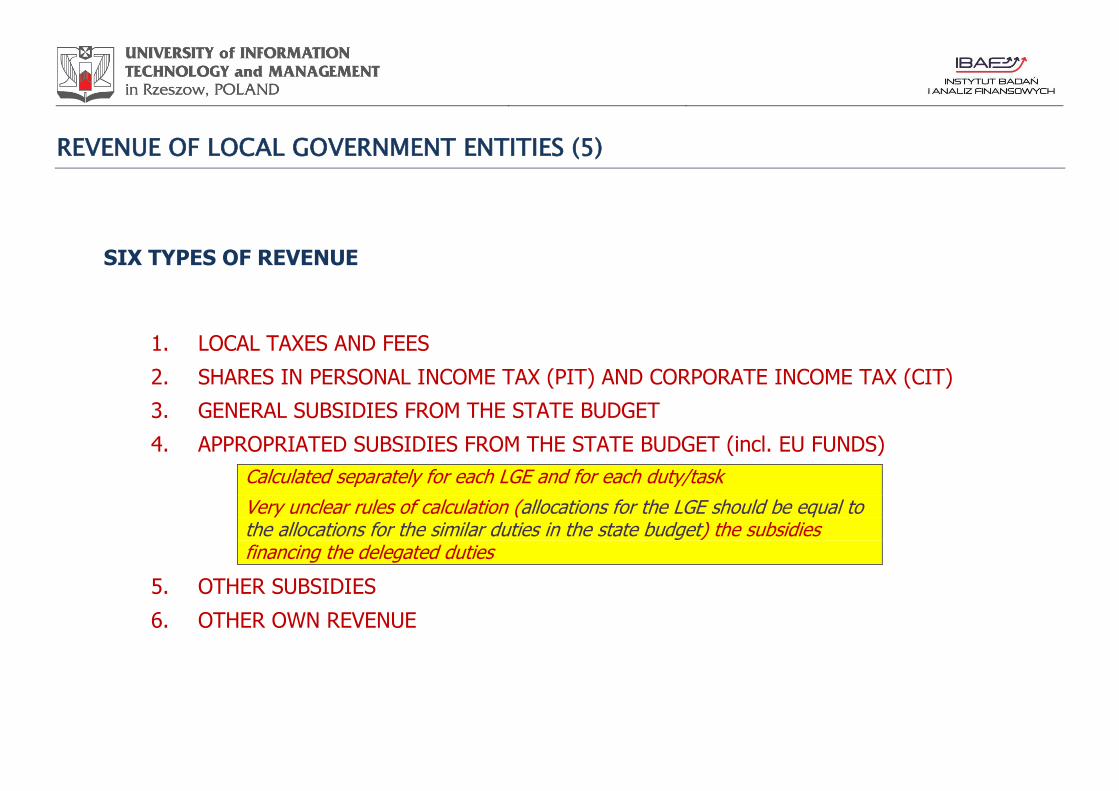

REVENUE OF LOCAL GOVERNMENT ENTITIES (5)

SIX TYPES OF REVENUE

1. LOCAL TAXES AND FEES

2. SHARES IN PERSONAL INCOME TAX (PIT) AND CORPORATE INCOME TAX (CIT)

3. GENERAL SUBSIDIES FROM THE STATE BUDGET

4. APPROPRIATED SUBSIDIES FROM THE STATE BUDGET (incl. EU FUNDS)

Calculated separately for each LGE and for each duty/task

Very unclear rules of calculation (allocations for the LGE should be equal to the allocations for the similar duties in the state budget) the subsidies financing the delegated duties

5. OTHER SUBSIDIES

6. OTHER OWN REVENUE

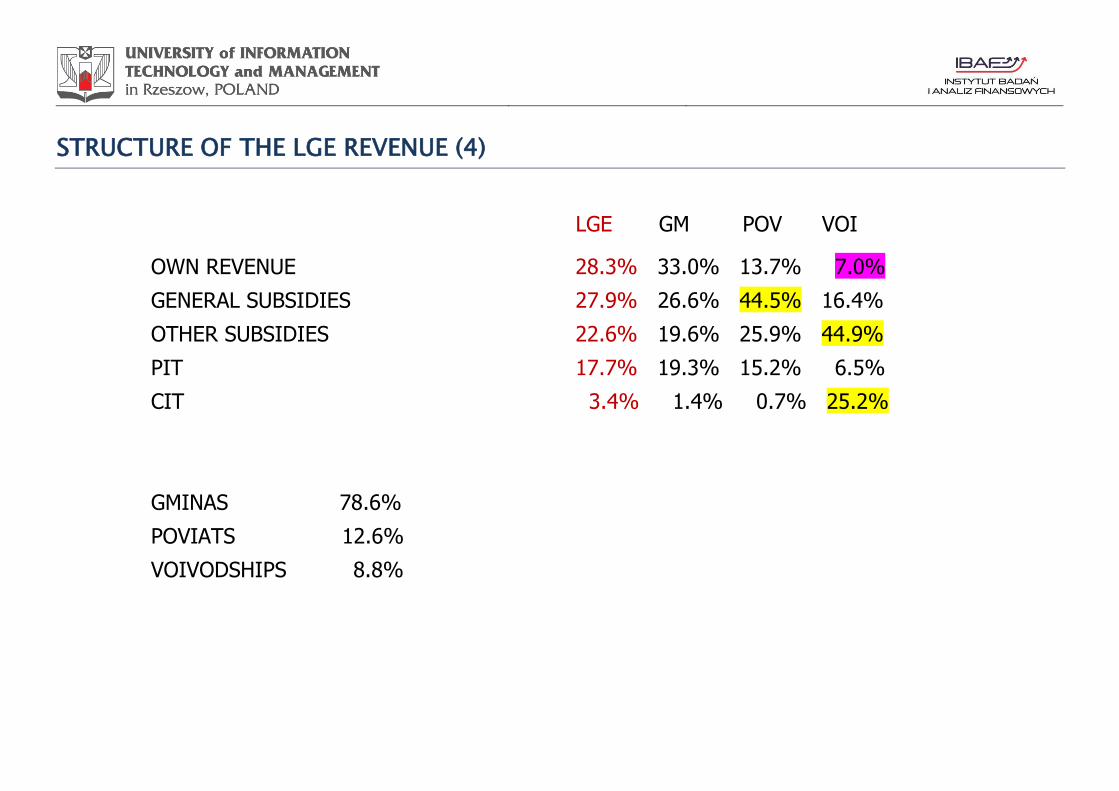

STRUCTURE OF THE LGE REVENUE (4)

LGE GM POV VOI

OWN REVENUE 28.3% 33.0% 13.7% 7.0%

GENERAL SUBSIDIES 27.9% 26.6% 44.5% 16.4%

OTHER SUBSIDIES 22.6% 19.6% 25.9% 44.9%

PIT 17.7% 19.3% 15.2% 6.5%

CIT 3.4% 1.4% 0.7% 25.2%

GMINAS 78.6%

POVIATS 12.6%

VOIVODSHIPS 8.8%

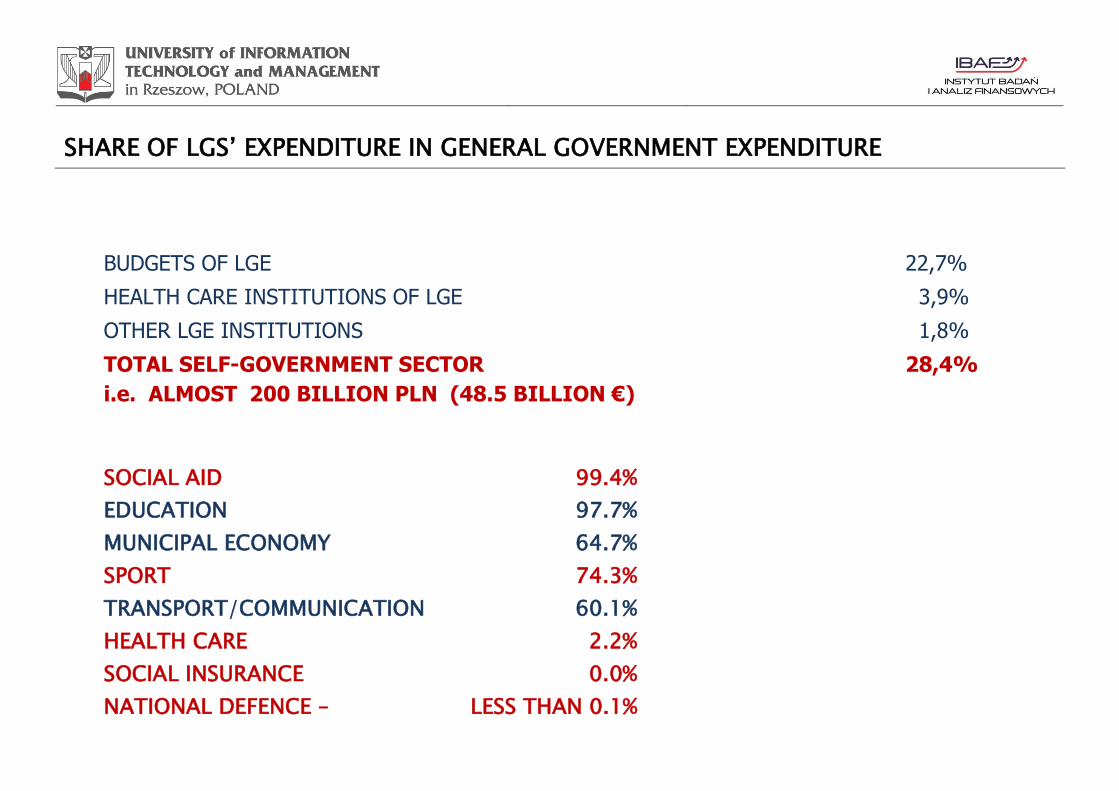

SHARE OF LGS’ EXPENDITURE IN GENERAL GOVERNMENT EXPENDITURE

BUDGETS OF LGE 22,7%

HEALTH CARE INSTITUTIONS OF LGE 3,9%

OTHER LGE INSTITUTIONS 1,8%

TOTAL SELF-GOVERNMENT SECTOR 28,4%

i.e. ALMOST 200 BILLION PLN (48.5 BILLION €)

SOCIAL AID 99.4%

EDUCATION 97.7%

MUNICIPAL ECONOMY 64.7%

SPORT 74.3%

TRANSPORT/COMMUNICATION 60.1%

HEALTH CARE 2.2%

SOCIAL INSURANCE 0.0%

NATIONAL DEFENCE – LESS THAN 0.1%

ASYMMETRIC DISTRIBUTION OF LGE REVENUE

LGE REVENUE PER CAPITA (3764,8 zł, OF WHICH OWN REVENUE– 2015,0 zł)

LGE REVENUE BY VOIVODSHIPS (2013, AVERAGE FOR POLAND =100)

CITIES WITH POVIAT RIGHTS 5067,1 zł OTHER CITIES 2941,9 zł URBAN-RURAL GMINAS – 3052,3 zł RURAL GMINAS – 3223,0 zł POVIATS – 893,5 ZŁ

DO 95% 95 – 100% 100 – 105% 105 – 110% PONAD 110%

ONLY 10% OF GMINAS HAVE THE REVENUES (PER CAPITA) HIGHER THEN AVERAGE FOR POLAND

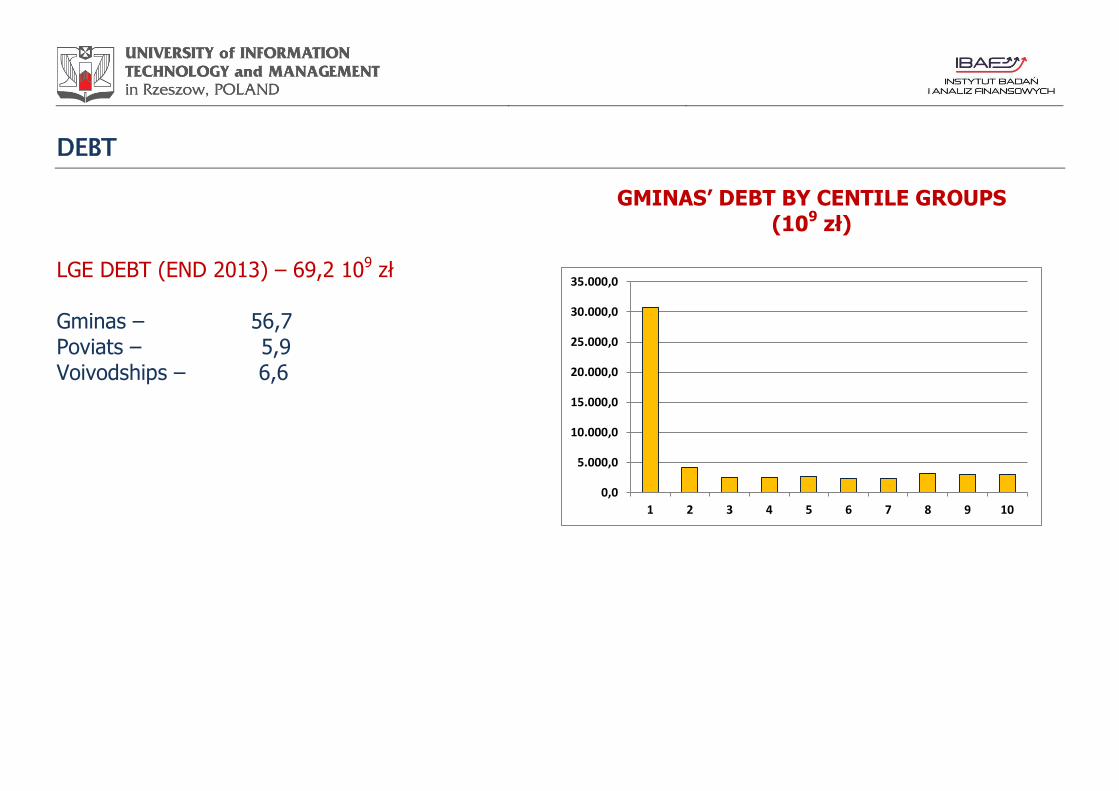

DEBT

GMINAS’ DEBT BY CENTILE GROUPS

(109 zł)

LGE DEBT (END 2013) – 69,2 109 zł Gminas – 56,7 Poviats – 5,9 Voivodships – 6,6

0,0

5.000,0

10.000,0

15.000,0

20.000,0

25.000,0

30.000,0

35.000,0

1 2 3 4 5 6 7 8 9 10

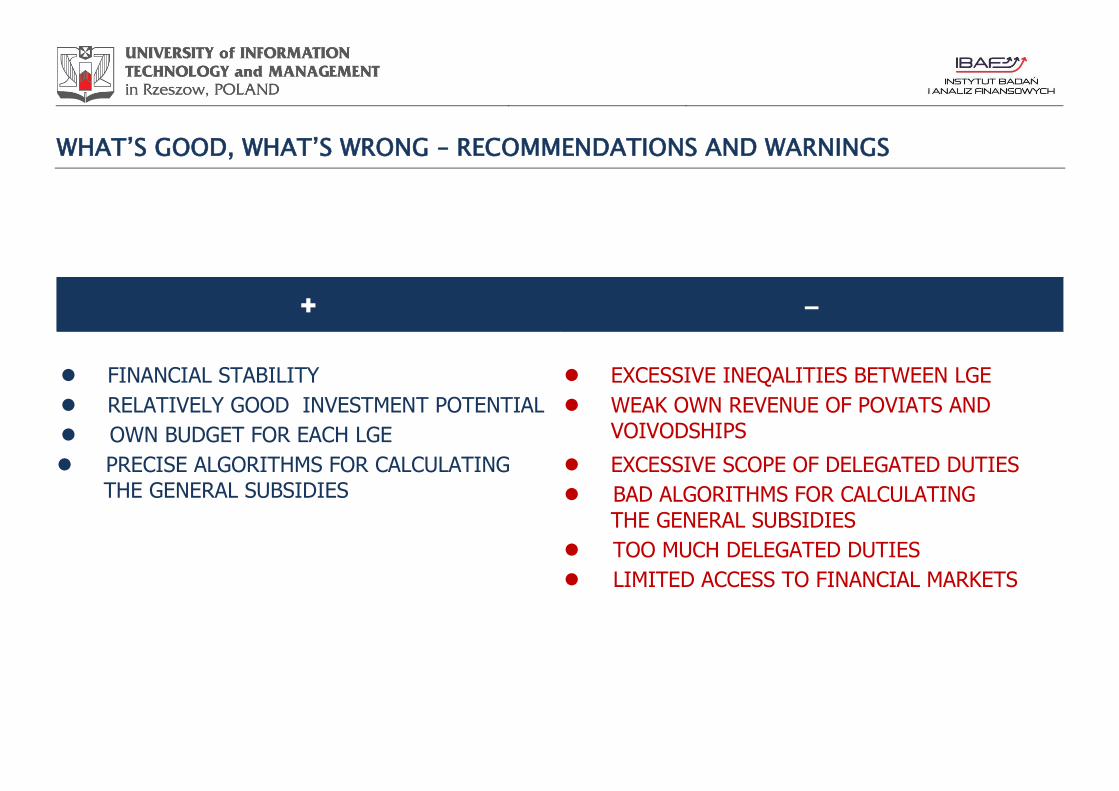

WHAT’S GOOD, WHAT’S WRONG – RECOMMENDATIONS AND WARNINGS

+ –

FINANCIAL STABILITY

RELATIVELY GOOD INVESTMENT POTENTIAL

OWN BUDGET FOR EACH LGE

EXCESSIVE INEQALITIES BETWEEN LGE

WEAK OWN REVENUE OF POVIATS AND VOIVODSHIPS

PRECISE ALGORITHMS FOR CALCULATING THE GENERAL SUBSIDIES

EXCESSIVE SCOPE OF DELEGATED DUTIES

BAD ALGORITHMS FOR CALCULATING

THE GENERAL SUBSIDIES

TOO MUCH DELEGATED DUTIES

LIMITED ACCESS TO FINANCIAL MARKETS

OUR PROPOSALS FOR POLAND

NEW OWN REVENUE

NEW ALGORITHM FOR THE GENERAL SUBSIDIES

CANCELLATION OF DELEGATED DUTIES

SIMPLIFICATION OF SUPERVISION PROCEDURES

VERIFICATION OF LG ENTITIES’ DUTIES

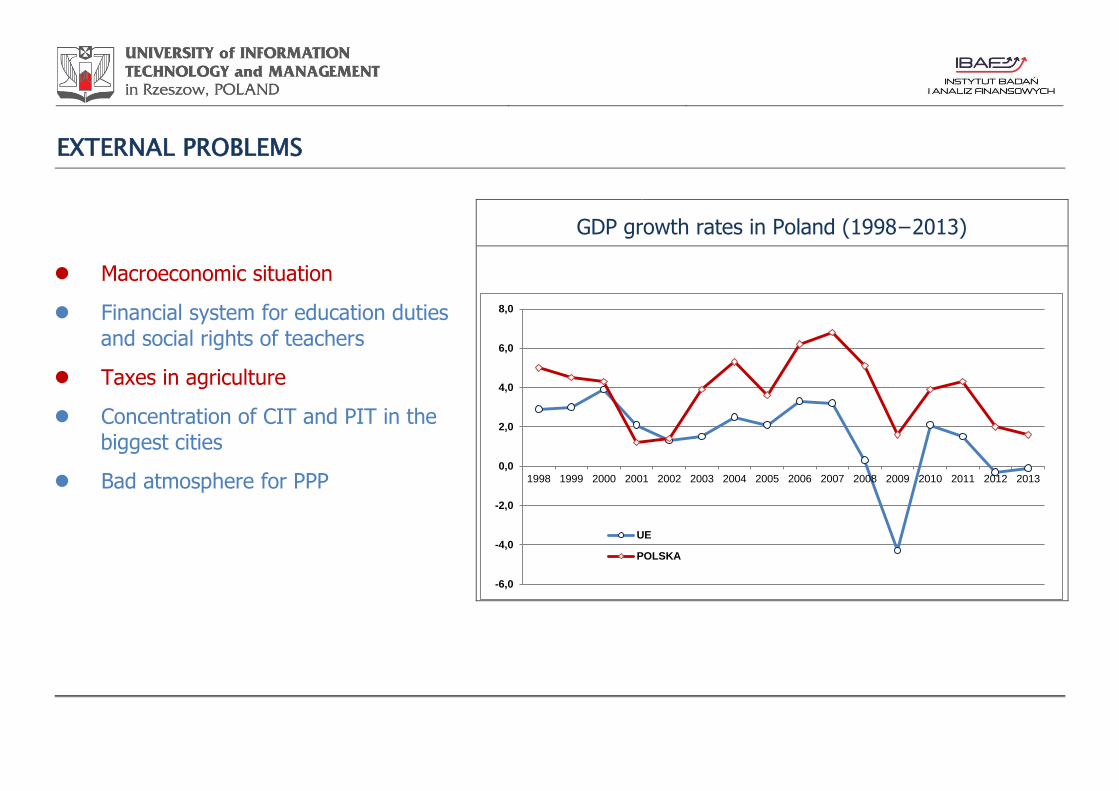

EXTERNAL PROBLEMS

GDP growth rates in Poland (1998−2013)

Macroeconomic situation

Financial system for education duties

and social rights of teachers

Taxes in agriculture

Concentration of CIT and PIT in the biggest cities

Bad atmosphere for PPP

-6,0

-4,0

-2,0

0,0

2,0

4,0

6,0

8,0

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

UE

POLSKA

INTERNAL WEAKNESSES OF LGE

LACK OF „TRUE” MULTI-YEAR STRATEGIC PLANNING

VERY TRADITIONSAL APPROACH TO BUDGET PLANNING

LOW ADMINISTRATIVE POTENTIAL

WEAK CONTACTS WITH INHABITANTS

TOO HIGH EXPENDITURE FOR ADMINISTRATION

LACK OF ACTIONS TOWARDS THE INCREASE OF OWN REVENUE

THANK YOU FOR YOUR ATTENTION