wooden furniture industry in vietnam

TRANSCRIPT

NATIONAL SECTOR EXPORT STRATEGY Wooden Furniture Industry in Vietnam

Prepared by: VIETRADE/ITC

Executive Summary.

Vietnam has a long tradition of producing traditional style furniture but is a relative

newcomer to the world of internationally tradeable lifestyle furniture for outdoor and indoor

use.

A very substantial production has developed very rapidly over the past 7 to 8 years kick

started by a number of fairly substantial FDI’s seeking lower labour costs. They have moved

from such East Asian locations as Taiwan, Philippines, Malaysia, Thailand and more recently

even China. This production arising from the influx of FDI’s has been further added to by the

arrival of the very large trading houses such as IKEA, Carrefours, B & Q, Walmart etc. They

are seeking bargain basement furniture at low cost as a hedge against over exposure to China

. This in turn has given rise to a very substantial number of Vietnamese start ups in furniture

to meet the demand. On the face of it all seems to be going well. Exports are rising at a

dramatic rate, employment is rising, industry appears to be on a roll. But is it ?.

The dramatic rise of the furniture industry is on poor foundations. A strategy to correct

direction and create an environment in which the furniture industry can become a real

economic success is essential if there is to any security for its contribution in the long term.

The current success is being achieved against a background of :

shortage of skilled workers

serious under capacity in training facilities

poor and outdated equipment

lack of environmentally certified forests in Vietnam

lack of an adequate home produced supply of raw materials

lack of trained and experienced marketing personnel.

weakness in design and

under-capacity of infrastructure

Taking into account these limitations of the indigenous industry and the fact that a very

considerable volume of the exports achieved are produced by foreign invested companies the

projected expansion of the industry’s exports clearly needs a defined strategy to enhance

sector competitiveness, boost the sector’s export value to meet government prtojections and

put it on a sustainable basis for long term development.

The strategy put forward in this report is designed to achieve a long term sustainably invested

industry, delivering real value to the Vietnamese economy, over the long term is essentially

to analyse the current value chain at every step and seek to capture the maximum benefit

for the Vietnamese economy while laying the foundations for a long term sustainable

industry

This strategy will be achieved by:

developing the indigenous capability to supply as much raw material as possible to

feed the industry and where this not possible ensuring that the infrastructure is put in

place to handle the imported material needs of the industry

through design and product development maximize the use of non timber natural

materials such as bamboo, rattan, and natural fibres such as water hyacinth etc

putting in place the training facilities at artisanal level, engineering level, design and

managerial level to provide the trained personnel where needed

bridging the gap in current availability of training facilities by giving direct assistance

to enterprises to employ outside expertise in technical, design, marketing, managerial

and financial expertise

at every opportunity promoting Vietnam as a realistic destination for sourcing

furniture and assisting attendance at International Trade Fairs as Vietnamese suppliers

while ensuring that those who do exhibit on national stands are capable of upholding

and enhancing the good name of Vietnamese furniture.

commencing branding of companies products as early as possible in a company’s

development

providing state of the art exhibition facilities to allow Vietnamese companies

showcase their products in a pleasant and credible venue

encouraging and incentivising FDI companies to put down roots so that they do not

easily move on to the next ‘cheap’ destination.

Using all opportunities presented by Information Technology to enhance Vietnam’s

access to international markets and optimise real returns on product delivered

ultimately achieving more efficient means of delivering furniture to the end user

while emphasising at every step the use of sustainable materials, clean manufacturing

environments and minimum carbon footprint in delivery to the customer.

The sustainable development of the furniture industry in Vietnam requires a long term

commitment from government. Ideally it should be assisted by a ‘one stop shop’1 under the

appropriate Ministry that can provide all the inputs and advise on all the facilities available

for assistance on management, marketing, training, grant aid, fiscal incentives etc.

1 A ‘one stop shop’ is a facility whereby investors in a given industry may seek advice on all aspects of

government policy towards that industry inclusive of the legislative framework, the fiscal framework and the

availability of incentives.

1 Introduction

1.1 Rationale

Traditional wooden furniture manufacture has a long tradition in Vietnam. Recently,

furniture manufacture has been booming. It has become one of the top 5 exported turnover

earners after crude oil, garment and textile, shoes and seafood.

The wooden furniture of Vietnam has been well recognized in international markets with

exports growing from $135 million in 1998, to US$1 billion in 2004 and reaching US$1.98

billion in 2006. By 2006, Vietnamese wooden furniture had already penetrated into 167

countries and territories in the world. This is up significantly from 58 countries in 1998, of

which United States of America, European Union and Japan are major ones with export

turnover in 2006 of US$774 million, US$400 million and US$280 million, respectively.

From 2000 - 2006, the export turnover of the industry increased with an annual growth rate

of 30%. By 2006, Vietnam had already overtaken Indonesia and Thailand to become one of

the top two woodwork exporting countries in the Southeast Asian region.

There are about 2,000 wood processing enterprises nationwide, creating jobs for almost

170,000 workers. The industry has contributed considerably to the improvement of living

standards for people in many rural areas of Vietnam. Not yet fully recognised, let alone

exploited, the development of the wooden furniture industry also brings about opportunities

for the development of other supporting industries in the country like hardware, accessories,

finishing materials, adhesives, veneers, machinery etc. and service industries in consultancy,

software, marketing, shipping, financing etc. All of these are yet to be fully captured in the

Value Chain.

There are still a lot of difficulties for the development of the wooden furniture industry in

Vietnam. It comes from both internal and external factors which are:

shortage of skilled workers

serious under capacity in training facilities and lack of higher education opportunities

in design and engineering for entrants to the industry

poor and outdated equipment in many factories

lack of certified forests in Vietnam and difficulties in sourcing timber, certified and

uncertified from world markets.

lack of trained and experienced marketing personnel and remoteness from the main

markets seriously limits the options for profitable sales.

weakness in design and engineering of furniture has led to a ‘sameness’ of product

seeking similar markets and thus pushing price as the first competitive advantage which

of course forces down profitability and therefore the ability to invest in design, product

development and engineering.

under-capacity of infrastructure both in surface transport and in port facilities will

increasingly limit efficient exports unless addressed in a coordinated fashion

Taking into account these limitations that impact all the sector, and particularly the

indigenous industry, and the fact that a very considerable volume of the exports achieved are

produced by foreign invested companies ( FDI’s) the projected expansion of the industry’s

exports clearly needs a defined strategy to enhance sector competitiveness, boost the

sector’s export value and shape up private enterprises to be viable and strong

competitors in the world furniture industry for the coming years. It has to be stressed it

is value that is the key not volume.

A strategy is particularly pertinent as the Ministry of Trade has set a target of US$ 5.56

billion by 2010 and the Prime Minister has set a target of US$ 7 billion by 2020.

1.2 Approach

The wooden furniture sector export strategy aims at developing a framework to meet the

objectives of promoting exports and advancing the development of the industry. Building on

a comprehensive assessment of the current value chain, export performance, export

competitiveness, critical success factors, related government policies and strategies and the

sector’s support network. This proposed strategy sets out a long-term vision and proposes

actions and measures that should be taken into account and implemented within the next 5

years.

The main tools applied are Value Chain Analysis and the Four - Wheel Gear Interactive

Frame provided by the ITC. A value chain consists of all the individuals or enterprises that

buy and sell from each other in order to supply a particular product or set of products

including vertical and horizontal linkages.

In the wooden furniture sector, the value chain can be described as a set of connected raw

material producers/suppliers (both wood and accessories), manufacturers, exporters on the

domestic side and importers, wholesalers, retailers and end-users in the international part of

the chain.

The Four - Wheel Gear Interactive Frame is used to create a comprehensive sector export

strategy by having a closer look at four categories of value chain development issues:

Border-In: This deals with issues related to:

(1) Capacity development that involves the sector’s production capacity. It deals with

improvement in productivity, increase in volume, improvement in quality and most

importantly, increased value;

(2) Diversification and product development such as producing new product lines and/or

related products;

(3) Human capital development that includes the development and training of human

resources and the encouragement and fostering of entrepreneurship within the sector.

Border: This deals with the issues related to:

(1) Infrastructure improvements necessary for the sector’s development;

(2) Trade facilitation which is necessary to improve trading effectiveness and value

capture;

(3) Reduction in the cost-of-doing business to maintain and improve the sector’s

competitiveness

Border-Out: This deals with the issues related to:

(1) Market access that includes tariff, non-tariff barriers and other related market entry

issues;

(2) In-market support services such as design, product development, exhibiting etc.

(3) Promotion and branding to build and reinforce the sector’s image in the target

markets

Development: This deals with issues related to the social and economic development of

the country that the sector contributes to.

2 The Sector’s Current Status

2.1 Product Groups

According to the present Harmonization System (HS), the wood furniture sector in Vietnam

can be classified into 8 basic groups, namely:

HS940161: Upholstered seats (wooden frame)

HS940169 : Non-upholstered seats, made of wood

HS940180 : Other chairs

HS940190 : Chair components

HS940330 : Home office furniture, made of wood

HS940340 : Built-in Kitchen furniture and Other Kitchen furniture, made of wood

HS940350 : Bedroom furniture, made of wood

HS940360 : Dining and living room furniture, made of wood

The products can be classified into indoor and outdoor as well. In many cases, it is classified

also into styles like Classic, Colonial, Rustic, Contemporary…

Wood furniture production in Vietnam is carried out in both craft villages and by industrial

processing (factory-based). There are 4 main centers for wood furniture production: In the

Red Delta river, in Binh Dinh province, Central Highlands (Gia Lai, Dak Lac) and Southern

Vietnam (Binh Duong, Hochiminh, Dong Nai and Long An)

In the red delta river, Ha Tay, Bac Ninh and Ha Noi is the first center where most of

traditional wooden carved furniture is produced. The famous centres are Dong Ky village

(Bac Ninh), Van Diem village (Ha Tay), Van Ha village (Ha Noi)… There are also many

other villages producing wooden furniture in Hai Duong, Vinh Phuc, Nam Dinh and Hung

Yen provinces. There are up to 342 craft villages making wooden furniture in Vietnam

creating jobs for 99,904 people2. Most of the carved wood furniture is for local use and it is

also exported to China, Laos, Taiwan and Hongkong market.

The big industrial production of wood furniture, other than traditional, in Vietnam is centered

in 3 main areas: Binh Dinh province, Central Highlands (Gia Lai, Dak Lac) and Southern

Vietnam (Binh Duong, Hochiminh, Dong Nai and Long An). The exports of wooden

furniture from Vietnam takes place mainly from these 3 areas, especially in the Southern

provinces of Vietnam and Binh Dinh province. From these areas various kinds of indoor and

outdoor furniture is made of natural forest wood, plantation wood or combinations of wood,

wood composites and other materials are manufactured. They are normally made and

exported to meet customer requirements. In addition woodchips are also exported in some

considerable volume from this area.

There is a large variation of enterprise within the industry. It ranges from mass production

with many machines and sophisticated CNC machinery ( mostly FDI’s ) to small family

production often with very poor machinery and relying largely on handwork. The production

of furniture products in family households is very common in the Vietnamese villages. This

family production can have major advantages. Typically, almost all production stages are

done by skilled handicrafts people. They use very simple machines. On the other hand it can

be difficult to achieve realistic volumes for bigger orders.

This allows for flexibility in meeting a variety of product and decoration and it is suitable for

those looking for specialties and sophisticated hand-made products. A problem arises when

larger orders are sought. There is not the organization to cope with volume. The quality

suffers, the producers miss delivery dates, the buyers are disappointed and the image of the

producers can be damaged.

2 JICA study, 2004

However, there are many companies that have quality certification and can manage

production properly to meet the quality and quantity demands of their customers. The better-

managed factories are well organised and there is a high degree of flow in production.

Workers have obtained specialised skills at defined functions. Managers are aware of how a

production facility should be set up in order to be efficient and productive. Many of the mass

producers in Vietnam are not focusing on a few series of products but instead they include a

broad array of products in their portfolios. This type of production needs a higher degree of

industrialisation and benefits greatly from the addition of modern CNC equipment and other

repetitive machinery and finishing environments.

2.2 The sector value chain

The value chain of wooden furniture is constituted with the participation of various

stakeholders. The major ones are; wood and board materials ( MDF, Particle board,

laminates, veneers ) finishing and adhesive materials, hardware and fittings, packaging,

equipment supply, selling agents, logistic agencies, research and development institutions,

wholesalers, retailers and consumers. ( See Value Chain below )

2.2.1 Wood from home sources:

Wood from home sources in Vietnam includes wood in natural forest, plantation wood and

artificial wood (MDF, Fiberboard, Particle board...)

The total natural forest in Vietnam is almost 8,2 million ha, of which 2,9 million ha is

classified as production forest3. The harvestable volume of wood from the natural forest is

strictly managed by the government. The harvesting quota is given on yearly basis for certain

provinces and the logging quantity is reducing year by year on a national scale. If in the

1990’s, the annual logging quantity was over 1 million M3, then it reduced to 300,000 M3 in

2000 and the quota for logging in 2006 is only 130,000 M3 nationwide.

Table 1: Logging quota in Vietnam

Year 1990s 2000 2003 2004 2005 2006

Harvesting

quota (m3)

Over 1

mil.

300,000 250,000 200,000 150,000 130,000

3 Data updated as 31 Dec., 2006 – MARD

* Services here refer to physical services such as kiln drying, tool maintenance and machine maintenance.

** Finishing Materials refers to consumable materials used for the preparation and finishing of the product such as adhesives, abrasives, diluents,

lacquers, paints etc The internal ‘Wood Furniture Manufacture’ for all its complexity is achieving only 25% of the Consumer Value. The

remaining 75% is in the External Value Chain. This highlights the opportunities for increasing retained value.

It should be noted that, the above yearly logging quantity from the natural forest is used for

various applications not only the processing of furniture but also wood for construction and

mining. It is estimated that about 60% of the wood from natural forest is used for production

of furniture (equal to 80,000 M3 in 2006).

The plantation forest in Vietnam is 2.2 million ha, of which area for production is 1.45

million ha (681,000 ha is matured forest). Harvesting quantities from plantation wood are

increasing year by year, from 800,000 M3 in 2000 to 1,950,000 M3 in 2004. Most of wood

from plantation forest in Vietnam is used for paper pulp production and the remaining is used

for mining stands, construction, man-made board materials and furniture production.

The volume for furniture production from plantation wood is estimated at 20% of the total

harvested volume. Total plantation wood for furniture production from 2003-2006 was about

1 million M3. The consumption of plantation wood for furniture in 2010 is estimated at 3.5

million M3. A similar volume of plantation wood for the production of man made board

materials is required in 20104. One of the weaknesses of plantation wood in Vietnam is its

small diameter. This means it cannot be used efficiently for furniture production. Most of it

goes to man made board materials and pulp chips. In addition there is still no FSC (certified)

wood in Vietnam either natural or plantation. for use in the furniture industry. (There is only

one company, OJI, a Japanese invested paper manufacturer, who has obtained FSC

certification for their plantation. This material is used for paper pulp. ).

In an effort to minimize the shortage of natural wood, the wood-based panel producers have

had much attention in terms of investment from the government. However, for whatever

reason, production has failed to meet projections. This has resulted in only 20% of total

processing capacity being achieved, of which:

Plywood production: 12 factories and 10 small-scale units with a designed capacity of

150,000 M3 of product per year; actually only achieving 60,000 M3 product per year

Particleboard, fiberboard production: 6 factories with a designed capacity of 88,000

m3 product per year have actual capacity of 45,000 M3 product per year

Laminated board production: 9 units with a designed capacity of 26,000 M3 of

product per year have actual capacity of 15,000 M3

This in general terms is an underachievement of 50%. And requires immediate and

determined analysis followed by appropriate technical assistance to improve the position.

From now to 2020, the government will focus on 2 main product types of man made board

materials, particle board and medium density fibre board (MDF) using plantation materials.

Wood-based panel production capacity of 540,000M3 product per year is projected,

4 According to forestry plan 2006-2010

320,000M3 of particle board product per year and 220.000M3 of fiber board product per

year. As a matter of fact, the quality of plantation forest in Vietnam is still poor resulted

from the quality of seedling, caring condition… therefore, most of wood are only suitable for

paper industry (wood chip) and material for artificial wood.

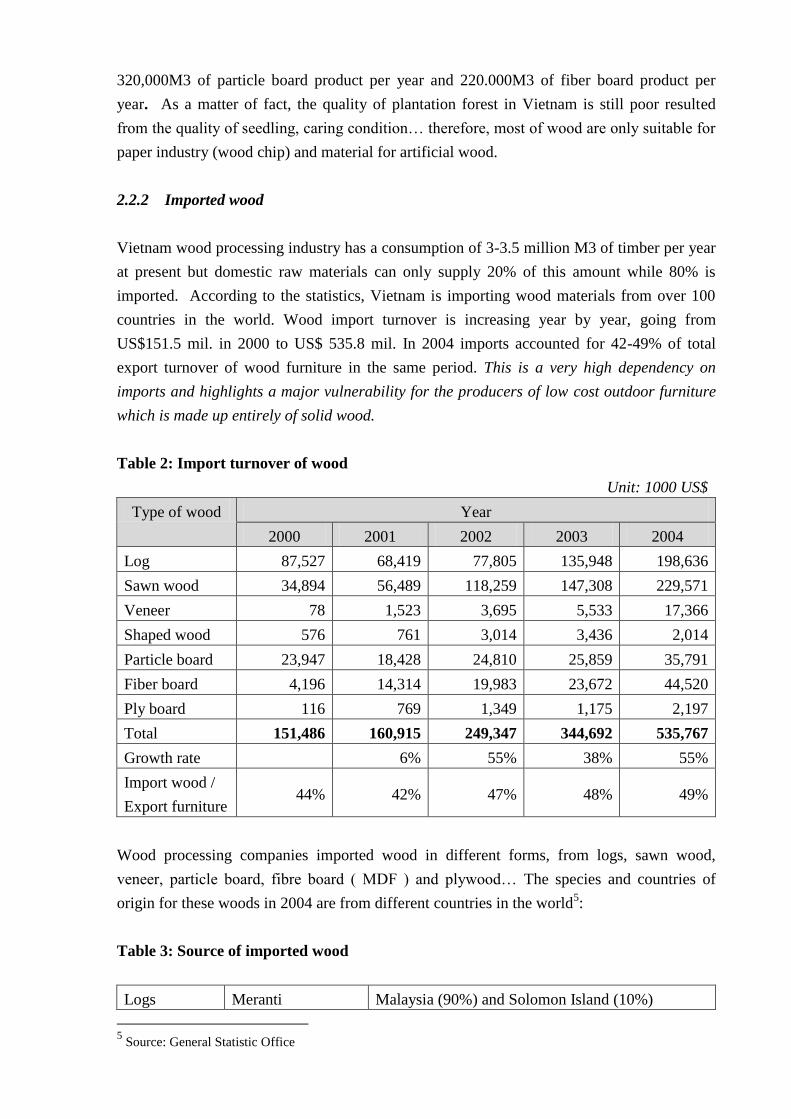

2.2.2 Imported wood

Vietnam wood processing industry has a consumption of 3-3.5 million M3 of timber per year

at present but domestic raw materials can only supply 20% of this amount while 80% is

imported. According to the statistics, Vietnam is importing wood materials from over 100

countries in the world. Wood import turnover is increasing year by year, going from

US$151.5 mil. in 2000 to US$ 535.8 mil. In 2004 imports accounted for 42-49% of total

export turnover of wood furniture in the same period. This is a very high dependency on

imports and highlights a major vulnerability for the producers of low cost outdoor furniture

which is made up entirely of solid wood.

Table 2: Import turnover of wood

Unit: 1000 US$

Type of wood Year

2000 2001 2002 2003 2004

Log 87,527 68,419 77,805 135,948 198,636

Sawn wood 34,894 56,489 118,259 147,308 229,571

Veneer 78 1,523 3,695 5,533 17,366

Shaped wood 576 761 3,014 3,436 2,014

Particle board 23,947 18,428 24,810 25,859 35,791

Fiber board 4,196 14,314 19,983 23,672 44,520

Ply board 116 769 1,349 1,175 2,197

Total 151,486 160,915 249,347 344,692 535,767

Growth rate 6% 55% 38% 55%

Import wood /

Export furniture 44% 42% 47% 48% 49%

Wood processing companies imported wood in different forms, from logs, sawn wood,

veneer, particle board, fibre board ( MDF ) and plywood… The species and countries of

origin for these woods in 2004 are from different countries in the world5:

Table 3: Source of imported wood

Logs Meranti Malaysia (90%) and Solomon Island (10%)

5 Source: General Statistic Office

Keruing and Kapur Malaysia (70%), Laos (12%), Papua New Guinea

and Australia.

Oak6 Malaysia (50%), Papua New Guinea (11%), Laos

(6%), Myanmar (5%), Uruguay (3%), USA (2%)

Sawnwood

Redwood:

Malaysia 48%, Laos 42%...

Kapu, Kempas,

Keruing, Ramin,

Teak, Balau

Cambodia (58%), Malaysia (10%), USA (7%),)

Indonesia (5%), Brazil (4%), New Zealand (3%)...

Oak USA (58%), Italy (15%), Ukraine (7%), Romania

(4%)

Other sawn wood Laos (20%), Cambodia (15%), Brazil (9%),

Malaysia (8%), Finland (6%)...

Veneer Taiwan (52%), China (12%), USA (10%)...

Particle

board

Malaysia (45%), Indonesia (25%), USA (10%),

Thailand, China...

Fiber board,

MDF

Malaysia (30%), Thailand (25%), Australia

(25%)...

Plywood China (35%), Japan (25%), Malaysia (20%)...

The cost of wood and man made board materials accounts for a very high percentage of the

product cost structure (40-65%+), therefore, looking for solutions to minimize the cost of

wood material as a percentage of selling price plays a very important role in improving the

competitiveness of the manufacturers. The fact that Malaysia supplied almost 50% of Oak

logs for Vietnamese wood manufacturers, while there’s no Oak in Malaysia but it is sourced

from the USA, Germany, Russia and Romania highlights the weakness of Vietnamese

companies in approaching appropriate sources of wood supply. The wood traders of Malaysia

were able to find better sources of wood supply to trade with Vietnamese manufacturers. The

same case happens when many US wood suppliers source wood from Canada and supply to

Vietnamese companies. The involvement of intermediaries, together with the increasing price

of wood recently, make the production costs of Vietnamese furniture less and less profitable

and seriously threatens competitiveness. This is major issue that has to be addressed.

At the same time, the main traditional suppliers of wood for Vietnam like Laos, Myanmar,

Indonesia, have already banned the exportation of logs. Therefore, Vietnamese companies

must import processed wood at higher prices. Moreover, most of the companies importing

wood independently in small quantity also make the CIF Vietnam price of wood higher. In

addition to these pressures, the rapidly rising demand for wood and wood products in

6 Oak is not necessarily indigenous to these countries but is cited here as these are the countries who are acting

as intermediaries in Oak supply, This highlights the current lack of expertise in sourcing.

China will put increasing pressure on the wood inventory of neighbouring exporting

countries. This has been highlighted by the World Wild Fund (WWF) who say the

demand of wood consumption in China will increase quickly.

In 2003, China imported about 42 million M3 of wood, of which over 50% came from

Malaysia, Indonesia and Russia. It is forecasted that the wood consumption of China will

reach 125 million M3/year in 2010. This will undoubtedly put pressure on prices.

The imported woods are both FSC and Non-FSC. The need for FSC wood is increasing in all

companies even though the cost of FSC wood is often 20-25% higher than non-certified

wood. The raw material cost is often accounting for 35-60% in the product cost in case of

outdoor furniture and it is higher in case of indoor (50-70%). There is no import duty on

wood, except for 10% VAT, which is not paid if the final product is re-exported. However,

shipping costs may add additional 40-60% extra to the costs of the actual wood

The government of Vietnam has decided to preserve the natural forest for valid

environmental reasons. This is wise. When these and further plantations come on stream

Vietnam will become better positioned for materials but it will not be self sufficient.

Meantime importing timber is a real constraint on Vietnamese manufacturers for

which strategies need to be developed to alleviate this strain. eg. More metal and less

wood in outdoor furniture achieved by innovative design, more bamboo, more fibre etc.

2.2.3 Other materials

The availability and supply of other materials like bamboo, rattan, water-hyacinth,

aluminum/metal, leather, ceramics, lacquer, glass, plastic etc must also play an important role

in the design, development and diversification of wooden furniture products. This is true for

all strata of the market.

These materials are all available in Vietnam but at different competitive levels as compared

to other countries in the world. Vietnam has sometimes been named “the country of

bamboo”, and therein lies huge potential. Bamboo itself together with other bamboo-based

products like laminated bamboo and woven bamboo can be a good combination when placed

alongside wood in the design and manufacture of furniture. However, as with rattan, bamboo

sources in Vietnam are under threat of shortage and need seriously applied efforts to

preserve and cultivate the sources. Prices are increasing by the year and Vietnam is now

importing both bamboo and rattan from China, Laos and Indonesia.

Due to this situation, the Government of Vietnam has already approved a strategy for

development of Non-Timber Forest Products up to 2015, of which bamboo and rattan are

important components.

Wood furniture in combination with metal is getting more and more attention from exporters,

but there are only a few factories in Vietnam yet where metal parts like fabricated or cast

frames can be produced. This needs development. The quality and design is still very limited

and wood furniture exporters often still need to import these metal parts from China or

somewhere else for their export orders. The development of metal and other inputs to the

industry are both vital and profitable and lead a greater ‘capture’ in the Value Chain.

2.2.4 Hardwares & accessories

Hardware, fittings and accessories can be produced and supplied by local manufacturers, by

traders and from foreign sources. Hardware such as bolts, nuts, screws, nails etc are produced

locally but are still very limited as to quality and variety. This supply side is a major

opportunity for a vibrant furniture industry. Taiwan is the perfect model for development of

this sector and case studies should be prepared for study by the industry’s strategists. Where

specialized fittings are required they are still imported from Germany, Italy, Japan, China and

Taiwan. In many cases, the importers will provide suitable hardware and/or specify

accessories that manufacturers need to use to ensure the quality of products. The more of this

that can be supplied from within Vietnam the better.

Other accessories and supplies like lacquer, paint, adhesives, foils, fabrics etc can be

produced in Vietnam, but again the higher quality materials still need to be imported.

The supply of such hardware and accessories are mainly concentrated in Hochiminh city and

this can cause a lot of difficulties for wood manufacturers in the North as the distribution

infrastructure is weak.

In some cases foreign companies have either set up their production of hardware and

accessories in Vietnam or are working in partnership with local trading companies.

Investment in this area should be encouraged and producers should be assisted to identify

local production when it has the potential to replace imports. Some of these companies have

also set up representative outlets in Vietnam to promote their sale.

2.2.5 Machinery

Machinery and equipment play an important role in achieving competitiveness in the

furniture industry. Basic wood processing machinery is produced in Vietnam and supplied

locally to many of the smaller producers and to large companies too There are several

companies specialized in this business but most of them are still in small scale (about 80%)

and medium scale (20%) producing very basic low technology equipment. Most of the more

sophisticated machinery is imported either new or secondhand. There is a shortage of skilled

personnel capable of using such equipment and the supplies infrastructure for software,

tooling and maintenance is still very basic. Often, where secondhand machinery is purchased,

the buyer does not have adequate access to instruction manuals for operation and

maintenance and the equipment proves a disappointment. Many wood processing workshops

are located next to wood craft villages (in Ha Tay and Bac Ninh provinces) and these

workshops are sometimes at household scale to make simple equipment like bench saws,

bandsaws, lathes, spindles and simple boring machines. These machines greatly improve the

productivity of wood processing in the craft villages but where the accuracy is required to

produce series all the same they are not reliable. Safety is also an issue that should receive

attention. Many of these types of machine are inadequately guarded. They are dangerous to

use even by very experienced workers.

The centre for manufacturing of wood processing machines in Vietnam is around Hochiminh

and Da Nang cities. The majority are in Hochiminh where most of the machines for wood

processing can be either produced or assembled with a certain percentage of parts imported

from Taiwan, China, or Japan. Basically, these manufacturers can meet demand of wood

processing companies for equipment of rough and semi-finished stages and they are trying to

invest in equipment to improve efficiency of their production. They are investing in CNC

machine tools to replace old technology and to achieve improved quality. The industry can

now produce and supply such machines as Finger Jointing Lines, Automatic double end

tenoners, copy shapers as well as the basic saws, planers, thicknessers etc.

There is no exact data on the percentage of wood processing machines that are imported but

it is likely that it is over 80%. This, as said earlier, is a big opportunity for local producers.

In 2006, the total amount of wood processing machines imported by Vietnamese wood

manufacturers cost about US$57 million. They were purchased from Japan, Italy, Taiwan,

China and Germany. More high quality machines will be imported as the number of furniture

manufacturers moving to the production of indoor furniture increases

The imported machines are supplied by a network of traders. Most of them are local traders,

some of them are foreign representative offices. There are also many cases where furniture

manufacturers contact and import directly from manufacturers overseas.

2.2.6 Technical, managerial and vocational skills training

The wood processing industry in Vietnam is supported by a system of research institutes and

training schools to provide processing knowledge to managers and workers for the industry.

There are three institutes and various training schools (including universities, high schools,

secondary schools, vocational technical schools, management cadres’s schools) nationwide.

The forestry training system within the Ministry of Agriculture and Rural development

comprises the Institute of Forestry Sciences (post graduate training), Forestry College in

Xuan Mai – Ha Tay province, 2 schools for training management staff in Agriculture and

Rural development in Hanoi and Ho Chi Minh city, 3 Central forestry high schools in Quang

Ninh, Dong Nai and Gia Lai provinces; Vocational training School for wood processing in

Ha Nam province, Central School for training forestry workers No.1 in Lang Son, No. in

Binh Dinh, No.3 in Binh Duong, No.4 in Phu Tho provinces. 2 training centers for staff in

forest protection and forestry management in the North and the South have been established.

In general, these training system has provided considerably the human resources for the

sector, but the quality of training available now, particularly in relation to machine

technology, materials technology, design, and marketing… is still poor.

Annually, training institutions within MARD are recruiting 5,170 students and pupils of

which 70 are Ph.D and Master students, 800 are university students in formal training , 450

are undergraduates in in-service training, 50 students in college training, 850 pupils in formal

high school, 400 pupils in in-service training school, 2,550 pupils in formal vocational

training.

Besides colleges and training institutions within the MARD, there are Thu Duc Agriculture

and Forestry College, University of Central highlands, Thai Nguyen Agriculture and Forestry

College under the Ministry of Education and Training. Provincial People’s Committees are

managing 10 forestry training institutions including 1 college (Hong Duc College – Thanh

Hoa province), 8 Training High Schools and 1 Vocational School. These schools admits 800

students for both formal and in-service forestry training at university-college, high school and

technical worker levels.

The number of trained staff and forestry workers by those institutions are more than 80,000

of which post-graduate training are 13,000 (Doctor 110, Master 200), Training High School

are 27,000 and skilled workers are 40,000.

However, the output of these courses are not always furniture production related except some

at vocational school level. Besides, this apparently massive training input is still not

translating into competent technicians on the ground. Under the pressure of labour shortage,

several cooperation models have been formulated effectively. The Agro-Forestry University

in Ho Chi Minh City has invited wood manufacturers to locate in the precinct of the

university and employ students as trainees to participate in production activities. Besides, the

model of Public-Private Partnership for training workers on woodworking has been

implemented in Dak Lak province under the technical and financial support of GTZ

(Germany).

2.2.7 Wood furniture manufacturers

According to the figures of the Ministry of Agriculture and Rural Development, there are

about 1,600-2,000 enterprises that specialize in wood processing and trading nationwide.

Among these companies, there are 374 state-owned companies, 324 foreign-invested

companies with the registration capital of US$1.2 billion (up to 14 December 2006) and the

others are indigenous private enterprises.

The aggregate wood processing capacity of these units is estimated at 3 million M3/year

(combination of solid wood and man-made boards). Most of these state processing and

trading enterprises are based in the Binh Dinh, Ho Chi Minh City , Binh Duong, Dong Nai ...

The scale of wood processing companies can be divided into there main groups:

Group 1. Large companies with a monthly production capacity of about 100 to 350 x 40ft

containers.

Group 2. Medium companies with a monthly production capacity of about 20 to 100 x 40ft

containers.

Group 3. Smaller companies with a monthly production capacity of less than 20 x 40ft

containers

Among these companies, there were already 99 companies with a Chain of Custody

certificate (COC )and the number of certified companies will be increased in the future. Most

of the large companies and some of the medium ones have also obtained ISO 9001-2000 and

SA 8000.

The wood processing companies are also in the process of building clusters that can foster

growth through cooperation and strategic alliances. Already, some manufacturers act as sub-

contractors for those with limited capacity or for specialty items. The manufacturers are

slowly learning that each must find its core competency and concentrate on that. At the same

time some are trying to become more vertically integrated in such areas as veneer and

veneered top production in order to have more control over costs and quality. In addition,

they are serving as suppliers to smaller furniture manufacturers.

The foreign wood processing companies ( FDI’s) play an important role for the development

of the industry in Vietnam, not only in term of export turnover but also in awareness of

technology, human resource training, diversifying products and even promote images of

wood processing industry to the world market. As labor costs began to swell and a shortage

of workers developed in their own countries foreign manufacturers from the US, Europe and

Japan began looking offshore to Malaysia, Singapore, Thailand, the Philippines, and more

recently Vietnam to find a suitable manufacturing environment. At this very moment there is

tremendous momentum in Vietnam as Taiwanese entrepreneurs build or expand large

factories in Vietnam, especially around Ho Chi Minh City, as they gear up to compete head-

to-head with the Chinese in resolute determination to export to U.S. and European markets. It

is obvious there is great confidence and optimism in the potential here and thus huge

investments are being made to gain a solid footing in this emerging furniture manufacturing

cluster. These new factories are equipped with new machinery and incorporate the latest

equipment in some areas — such as finishing.

2.2.8 Agents and sourcing companies.

These are independent individuals or companies which negotiate and settle business on the

instructions of their principals and which act as intermediaries between buyer and seller.

They do not buy or sell on their own account and work on a commission basis. Most agents

represent more than one manufacturer, although competition is avoided. Often the buying

agent has his office in the supplying country

There are many agents and sourcing companies buying wood furniture in Vietnam. Most are

just sourcing like Carrefour, Ikea, Diamond Keystone Associates but some are involved in

both sourcing and production like Scancom. The sourcing agents play an important role for

the development of the sector, for instance, Carrefour has imported US$ 20 million of

furniture in 2006 while Scancom has exported from Vietnam over 40 million US$ in the

same year.

2.2.9 Freight forwarding and transport

Shipping and forwarding companies either belong to local or foreign companies and offer

various kinds of services, from customs declaration and clearance to hiring containers,

chartering vessels, inland transportation etc. Competition between forwarding and shipping

companies is fierce. Each company is often strong at a certain shipping route. Freight in

Vietnam is often higher in than China due to lower traffic density and poor seaport

infrastructure.

2.2.10 Importers/ Wholesalers/Buying Groups

By buying on his own account the importer or wholesaler takes title to the goods and is

responsible for their further sale and distribution in his country and/or in other markets.

He/she is familiar with local markets and can supply considerable information and guidance

to the overseas manufacturer in addition to the primary business of buying and selling, such

as the administration of import and export procedures and holding of stock. The development

of a successful working relationship between manufacturer and importer can lead to a high

level of co-operation with regard to appropriate designs for the market, new trends, use of

materials and quality requirements.

Buying groups are formed to assist small retailers get better terms. They usually buy for a

collection of small companies. The buying groups act somewhat like a cooperative and seek

to achieve a better price and a better service by virtue of their buying volume. However

typically they do not stock and require that the furniture is delivered to its destination retail

store. This requires a little more sophistication on behalf of the manufacturer to do the

necessary paperwork and manage the logistics.

2.2.11 Retailers

Retailing is the last step in the distribution chain from manufacturer to consumer. Retailers

come in many different sizes from the small single unit known in the US as ‘Mom & Pop’

stores to the giant leviathans such as Walmart, IKEA and Carrefours.

The small units are usually specialists either, by product or by service. They buy from

wholesalers and do not normally carry stock. The wholesaler charges them for his service of

importing, stocking and distributing. The mark-ups vary but usually will be in the region of

80 to 100%, and sometimes more, of the FOB price. The retailer in turn will add a further

100%, plus or inclusive of local taxes, and so the furniture sold to the consumer ends up at

something in the region of 4 times the FOB cost to the consumer.

The next stage up is the buying groups who buy collectively on behalf of a number of

independent retailers. They take a percentage of the price of the goods landed for their

service of sourcing and selection. Normally 10% to 12% but the retailer incurs all the

handling charges from factory to store and thus the retail price ends up similar to that of the

furniture bought from a wholesaler but the retailer may achieve a mark-up of more than

100%.

The small chain stores come next. These are where you have localized groups of stores under

one ownership operating in one city or one state but not usually nationwide. They usually act

as their own wholesalers buying into a central warehouse and distributing around their own

stores. Again the furniture usually finds its way to the consumer at 4 times the FOB price.

The next group is the giant retailers such as the IKEAs, Walmarts, Carrefours etc. These

groups are masters of globalisation and have enormous purchasing power. They buy directly

from the manufacturer and sell on directly to the end consumer. They seek to benefit from

economies of scale and negotiate very hard when purchasing. They offer huge volumes and

demand very low prices. Typically they pay 20 –22% of the ultimate selling price in their

stores and so to supply them the manufacturer must be super efficient if he is to make a

profit. More and more these enormous buying groups are achieving monopolies in their

respective markets. Due to globalisation they have a hegemony in the marketplace and their

suppliers are swamped with huge volumes giving them little or no space to seek out higher

prices from other buyers.

Such buying groups have huge costs and inefficiencies in their systems. While they often sell

at a discount to the consumer this discount is achieved by ruthless buying practices. These

practices can be very destructive of the manufacturing base. It is essential to understand that

supplying the retailing giants requires extreme efficiency on behalf of the manufacturer or

profitability will be sacrificed to volume and the manufacturing company will ultimately fail.

Supplying such outlets can be a strong learning curve and build strong industrial stamina but

the goal should be to get closer to the end user. Alongside supplying such leviathan

companies it is essential that the supplying companies develop strategies that will lead them

into more independent supply chains.

2.2.12 Consumers

The consumer is the end user, the person who pays his money and takes the product home.

This is the end of the value chain. The consumer is motivated to make his purchase by style

and design, by location and quality of product and of store, by fashion and peer pressure and

by functional necessity. The price the consumer will pay is dictated by availability,

affordability, quality and payment terms.

2.3 Assessment of wood furniture performance

The export turnover of wood and wood furniture has grown quickly in recent years. From

the turnover of $344,940,000 in 2000 it has reached $1.1 billion in 2004, $1.56 billion in

2005 and $1.98 billion in 2006. Vietnam has also set the target for the turnover of $5.5

billion in 2010 with the annual growth rate of 29.8%.

Table 4: Export turnover for wood and wood furniture in Vietnam

Unit: 1000 US$

Year

2000 2001 2002 2003 2004 2005 2006

HS940161 0 467 594 1,392 17,868

HS940169 0

1,225

4,906

47,026

165,930

HS940180 55,869 42,488 70,789 59,597 2,926

HS940190 4,251 7,497 10,061 11,104 14,915

HS940330 60,007

35,081

68,499

76,771

69,438

HS940340 311

1,802

6,936

8,806

19,642

HS940350 7,121

14,356

48,269

54,923

228,464

HS940360 76,567

127,028

135,317

278,117

362,442

HS44 140,814 155,434 188,107 173,271 220,127

Total 344,940 385,378 533,478 711,007 1,101,75

2

1,560,00

0

1,980,0

00

Growth rate 12% 38% 33% 55% 42% 27%

Source: General Statistic Office (2007)

It is noted from the above table that, the total export turnover is also included of both wood

furniture (HS44) and wood materials HS4401-4421(Various kinds of woods and material

boards) are also counted.

The EU, Japan, the US and Australia are the biggest markets for Vietnamese furniture.

Shipments to the U.S. market alone reached US$744 million in 2006, 39% of the total. The

figure is expected to leap to US$1.26 billion in 2007, around half the country’s total. Exports

to the EU and Japan amounted to US$500 million and US$286 million in 2006 respectively,

up 300% and 200% against 2003. However, so far the ratio of wood furniture in these

markets are still very small as compared to its actual consumption. The markets (in order of

export turnover, from high to low) for specific furniture categories are as follows:

Table 5: The market for Vietnamese furniture

HS940161 UK, Denmark, Germany, Australia, Taiwan, Canada, Holand, Belgium

HS940169 Germany, UK, Holland, Belgium, Australia, Denmark...

HS940180 UK, Germany, Denmark, Taiwan, France...

HS940190 USA, Taiwan, Malaysia...

HS940330 USA, Japan, France, UK, S.Korea, Denmark.. (Most of these markets did

not show growth in recent years)

HS940340 USA, Japan, S.Korea, Taiwan, UK.... (US, Japan and S.Korea market

increased quickly).

HS940350 USA, Japan, UK, China, S.Korea, Australia... (US and Japan market

increased sharply, other ones were also grown stably at high rate)

HS940360 USA, Japan, France, Holland, UK, Germany, Australia... (US market

grown 100-300%/year, Japan market also grown stably)

The export turnover generated by foreign invested companies is a very big share of Vietnam

wood furniture processing industry. More than half the 2006 export revenue of US$1.93

billion came from the foreign-invested sector. The southern province of Binh Duong, which

accounts for around 40% of the country’s annual woodwork exports, now has 369 wood

processing enterprises, including 194 foreign-invested companies with combined investment

capital of more than US$700 million. Also, according to a statistic figure from a US

Consulting firm in Hochiminh which is specializing in promoting wood furniture for US

market, about 80% of wood furniture export turnover in Vietnam destined for the US market

is from the Chinese and Taiwanese invested companies in Hochiminh, Binh Duong, Dong

Nai as well as other traders in the third countries. This statistic alone underpin the need to

ensure that these companies put down roots.

Since Vietnam became an official member of the World Trade Organization in January 2007,

more foreign investors have been paying greater attention to the domestic wood processing

industry and operational foreign-invested enterprises also plan to expand their business in

Vietnam. For example, Taiwan’s Kaizer Wood Industry Co. has quadrupled its processing

capacity so that it can export 1,000 container loads a month, targeting export turnover of

US$60 million this year. According to the source of Vietnam Economic News, the export

turnover of top foreign invested wood furniture companies in 2006 are as follows:

Table 6: The export turnover of top foreign invested wood furniture companies in 2006

Company Export turnover (US$)

Scancom Vietnam 41.637.887

Green River Wood & Lumber 40.800.000

Theodore Alexander 34.591.588

Poh Huat Viet Nam 34.561.159

San Lim Furniture Vietnam 34.126.261

Latitude Tree (Vietnam) 29.844.014

Kaiser Vietnam 28,807,267

Great Veca Vietnam 26.148.977

Koda International 25,826,033

Standart Furniture Vietnam 21.023.016

RK Resources 19.656.991

Johnson Wood 18.620.162

FuTa (Vietnam) 18.373.433

Marumitsu-Vietnam 17.722.557

Chien Furniture Vietnam 17.622.965

The case of Kaiser expansion looks great but if looking at the math, one can find that the

value per container based on these figures is extremely low and may be not really economic

for Vietnam whatever about the company. About all that can be said is that it is keeping

people in jobs though probably for very low wages where it is more worthwhile to improve

the economic worth to the economy of Vietnam and not the volume.

2.4 Performance against Critical Success Factors

There are a number of critical success factors that determine competitiveness in the wood

furniture sector :

2.4.1 Government level:

Government must engage with industry, empower development in the industry and

provide the platform from which an innovative approach to the market is undertaken. It is

vital to the economic success of the furniture industry that companies get as far long the

value chain to the end consumer as possible. The efforts of government should at all

times bear this in mind.

The training facilities must be put in place at all levels, craft skills, technological skills,

design and innovation skills and marketing management skills.

The long term development of ‘homegrown’ timber supplies must be actively undertaken

to ensure maximum security of raw materials in the longer term and thus sustainability of

the industry.

A suitably qualified team should be selected/recruited to lead the industry and manage its

adaptation to the international market, manage its image and its value growth.

Sufficient companies must be encourages buy into proposed innovative approaches to the

marketing and branding of furniture from Vietnam and they must be prepared to

contribute to a ‘directorate’ to manage the operation.

2.4.2 Industry level:

2.4.2.1 Availability of wood material

Currently, as much as 42-49% of the export value of furniture from Vietnam goes out of the

country paying for wood and panel imports. This is an extremely high ratio and one that

should raise concerns for the overall viability of the industry long term.

Meanwhile, the supply sources in Vietnam’s neighboring countries like Laos and Cambodia

are depleting. The price of wood in Malaysia, Vietnam’s largest material provider, is rising

sharply and other exporters like Russia have increased export duties on wood materials. The

price of wood material imported by Vietnam in 2006 rose from 40 to 100 percent compared

to 2003. In addition, there does not exist a good plan for material import. Vietnam is also yet

to have long-term agreements at Governmental level with its major material exporters like

Russia, New Zealand, the US and South American countries.

According to the “New 5 million hectare forest-planting” programme, Vietnam will have 2

million hectares of protective forest and 3 million hectares of production forest in 2010. It

will be difficult for the Vietnamese forestry sector to reach this goal, so it is expected that

Vietnam must import around 75% of its timber in the coming years. There is no import duty

on wood, except for 10% VAT, which is not paid if the final product is re-exported.

However, shipping costs may add 60% extra to the costs of the actual wood.

Local wood supplies are not catching up and in many cases plantation timber is not being left

long enough to be really useful.“The Acacia logs are harvested too soon (6 years ) to allow

mature logs and thus logs with a more cost effective yield. It is preferable that suppliers

have access to larger diameter logs 10 to 12 years old. The problem is that the farmer and

the government want their money sooner and will not wait. Without larger logs higher

quality products cannot be made here in Vietnam”7

Species of wood to be planted in Vietnam, for instance, eucalyptus urophylla often provide

low quality wood while in other countries that have similar conditions like Vietnam, for

instance, Solomon Islands, South Africa, Uruguay and Brazil grow other planted eucalyptus

species like Deglupta, Saligna and Grandis. This provides much better wood quality. The

species to be planted and cultivation technique are still weak points of the forestry sector in

Vietnam.

The demand for certified wood is increasing and will soon become the norm due to pressures

from environmentalists and reinforced by acceptance of global warming as a reality.

However, there are still no certified forests in Vietnam yielding wood for furniture. The

government is moving towards certification of state managed forests and it is the generally

held opinion that sustainable exploitation of the forests is the best option to preserve the

forests from piracy and develop good management practice but natural forest will not yield

the necessary volumes.

As much as 42-49% of the cost of exported outdoor furniture is raw material cost. This leaves

very little value to be distributed to labour, overheads and profit. At this percentage for raw

material companies cannot make worthwhile profits or fund sustainable development of the

enterprises. This situation can only be made better by improved marketing, improved design

and product development and consistently good quality in product and service. All of these

are critical success factors.

2.4.2.2 Cluster Development and Supporting industries

The wood processing furniture sector is now facing the pressing problem of poor supporting

industries. Despite impressive growth over the past few years, the Vietnamese wood

processing sector is not harmoniously coordinated with related industries which produce

auxiliary materials and components for wood products. The accessories and auxiliary

7 Opinion of a big buyer for furniture in Vietnam

materials account for 5-10% (sometime up to 15-19% - the case of Forexco, 15-25%

Savimex) of the total product value (but it is only 3-5% in China as reported by some

companies).

Most of metal parts for furniture are being imported, even though there are already several

manufacturers in the South. The other ones like polyurethane (PU), adhesive, fabric,

leather... are being distributed by traders who are also importing from different countries.

PU lacquer and adhesive are the items that are largely consumed by both indoor and outdoor

manufacturers. They are being imported from Akzo Nobel (the Netherlands), Jowat

(Germany), Kony Bond (Japan) and some other local manufacturers like Inchem (Malaysia),

Duy Hoang... Auxiliary materials for the timber sector are not only highly priced but also of

low quality and sometimes hard to have delivered on time. The supply of textiles in

particular poses difficulties for wood processing and exporting enterprises. For example, a

textile enterprise agreed to produce cloth of a certain colour and pattern as required by

furniture manufacturer, but the cloth eventually delivered was not of the colour and pattern

agreed to, thus severely undermining the relationship between furniture manufacturer and its

customers and even leading to the cancellation of orders and claims for compensation.

2.4.2.3 Labor force

The universities and colleges can only provide a small percentage of the necessary labour to

the wood processing industry. The vocational training dedicated to wood processing has also

failed to meet enterprise demand, therefore, the wood processing industry is suffering from a

lack of skilled labour. Recent figures from Vietnam Forestry and Wood Products Association

(VIFORES) show that the industry needs around 122,400 workers, including almost 120,000

manual workers and 2,400 technical engineers and there is a shortage of about 20.000

workers now.

Because of the shortage of skilled labour, many companies have tried to attract the labour

from the other companies, especially the ones in the same areas (this is popularly happened

in Phu Tai IP of Binh Dinh province or industrial parks in Binh Duong province). Fighting

over good labour between the companies often happens and many companies have incurred

delays in delivery because of this issue.

Productivity in the bulk of enterprises visited was low. This was mainly due to poor product

engineering because the necessary trained middle management just did not exist. It was

found in interviews that lack of training presented one of the biggest obstacles to the long

term development of the industry. “ Labour turnover is a big problem you have them trained

and they leave. Quality perceptions are low and you have to train from scratch. Training of

supervisory management is vital. They would like short term training 2 to 3 times a year.

They would release staff for this training”

2.4.2.4 Equipment and Processing technologies

Most of the machinery used in production is locally made or imported from China, Taiwan,

Japan or Germany. Machines from Japan and Germany are typically second hand. The

machinery which is locally made, or imported from China or Taiwan, is often of poor quality

and outdated. This underdevelopment is due to the fact that the industry lacks sufficient

capital to invest in more sophisticated technology. However, as more and more companies

enter the Vietnamese market, the demand for more advanced machineries is expected to rise.

2.4.2.5 Product range

There are essentially four product groups making up the furniture exports of Vietnam.

Outdoor furniture; made from local and imported Acacia, Teak , Beech, Balau and

Eucalyptus.

Indoor furniture; made from imported Pine, Rubberwood and also hardwoods like

Ironwood, Rosewood, Mahogany and Redwoods.

Reproduction furniture; and ornate indoor furniture made largely from imported redwood .

A good trend that many wood furniture manufacturers are pursuing, is the combining of

wood and other natural materials or metal for unique designs.

Traditional carved furniture; this is made from imported wood from Laos and Cambodia

and some locally harvested wood. It is mostly aimed at local markets and those of China and

Taiwan.

Table 7: The popular species of wood for wood furniture in Vietnam

Indoor Outdoor

Products:

Dining set (tables, chair...), sofas and coffee

table, saloon chair, beds (King/Queen...),

bookcases, cabinets, buffets, cupboards...

Imported wood

Oak, Cherry, Walnut, Black Cedar, Pine,

Beech, Soft Maple..., Ebony, Rosewood,

mahogany,

Local wood (both natural and plantation)

Gioi/ Talauma Gioi A.Chev; Ebony,

Rosewood, mahogany, Re/ Cinamomum

albiflorum Eces;Thông nàng/ Podocarpus

Products:

Armchair, bench, rocking chair, coffee

table, table with extension, hammock,

steamer chair, sun lounge, swing, trolley,

footrest...

Imported wood

Meranti, Merbau, Manni, Keruing, Kapur,

Kempas, Pyinma, Pyinkado, Teak (white

and Yellow), Yellow Balau; Eucalyptus;

Acacia

Local wood (both natural and plantation)

Cho chi/ Parashorea stellata Kury;Acacia,

imbricatus B1; Rubber, Cherry, MDF,

Plywood & Veneer...

Eucalyptus...

2.4.2.6 Production costs

Labor costs per hour for Vietnamese workers range from 0.2-0.6 US$, for Indonesia from

0.3-0.4 US$, for China from 0.5-0.75 US$, for Malaysia from 1.25-1.40US$, for Thailand

from 1.5 US$ onwards and are about 5 US$ in Taiwan).

2.4.2.7 Product quality

Outdoor furniture is generally produced for the middle to lower end markets and sold to bulk

buyers at weak prices.

Indoor furniture produced for export by local companies is usually made from imported Pine

or Rubberwood and is directed to low end markets. Indoor furniture produced by FDI

companies is generally of better quality made largely from imported woods. They come to

Vietnam for cheap labour and a stable environment.

Reproduction furniture is made mostly for the local market but there are a few very large FDI

companies exporting strongly drawing on the ‘handicraft’ skills of the local workers and

using overseas designers and technicians. ( Theo Alexander is an excellent example )

Hand carved furniture produced in the North (Bac Ninh, Hanoi, Ha Tay) is underachieving

due to lack of design and markets are confined to China and Taiwan as well as the home

market at present. Consultation at government level for this resource has been limited as has

consultation with training institutions.

A major issue here too relative to quality is the need to ensure that wood is properly dried

before it is manufactured into furniture. Adequate kiln drying facilities to service industry’s

needs is critical to success in exporting.

2.4.2.8 Branding of Vietnam wood furniture

The branding of Vietnamese wood furniture in the world marketplace is not well recognized.

This is understandable as there is little or no joint national exhibits by Vietnamese companies

and few indigenous Vietnamese companies have extensive overseas exposure as individually

named / branded companies.

An example that the Vietnamese wood producers could usefully learn from is the model of

Taiwan. Taiwan started out into the furniture industry as lowest cost producer with little or

no locally available raw materials and little expertise. They gradually built up strength and

manufacturing know how from their close cooperation with the US market. The quickly

recognised there was a need to specialise to be competitive and that led them down the road

of forming very effective clusters and of developing the whole supply chain into their

industry. Now Taiwan has become a relatively high labour cost area an it is moving its

furniture manufacture off shore to such venues as China and more recently Vietnam.

However in the intervening years since it commencement in the mid 70’s Taiwan has

developed a huge supply side in fittings, hardware, machinery etc and it is now a major

supplier not just of furniture but of the ancillary materials and accessories for furniture

manufacture. Thus, the trademarks of Taiwanese furniture is the excellent quality of finish

relative to value, accomplished with good equipment, knowledge, and the use of good

finishing materials. In addition, excellent quality control measures are being implemented to

assure the appearance and durability meet or exceed customer expectations.

2.4.2.8 Design and Intellectual property.

Vietnam still lacks a national policy on the protection of trademarks and brands. Such policy

does need to be developed. However furniture design is notoriously difficult to protect. The

emphasis in the short term should be for enterprises to invest in good design and get that

design on to the market at a quality level that is difficult to copy cost effectively. This

process will be greatly assisted by determined efforts to improve productivity and by having

a policy of “no compromise” on quality.

2.4.2.9 Ability to supply larger quantities

Here the whole issue of ‘globalisation’ comes up. The bulk of outdoor furniture exports from

Vietnam are purchased by large multinational groups who require certified ( FSC or similar)

wood and whose purchasing policies leave little room for profits to the producers. The

supplying companies are often so busy with the ‘day to day’ pressures. Management does

not take time to think strategically about direction till it is too late. It must be stressed again

value addition is what profitable manufacture must achieve assisted by focused marketing

and good logistics.

Quoting one large international buyer “ we have 10 – 12 suppliers here in Vietnam on the

furniture side. All are supplying Acacia, garden furniture sourced strictly from plantations.

We are here for cheap labour but unless productivity improves it will not stay cheap and we

will move on”

Quoting another large multinational buyer; Yes, our prices are very tight but we give the

factories very big volumes. If they cannot meet those volumes reliably we cannot do business

with them. We left Indonesia to come to Vietnam because the Indonesians did not satisfy our

volumes.

This can be described as the ‘Hegemony’ of the giant multinational trading groups such as

Walmart, Sears, IKEA, Carrefours, Mitsui, Isetan, METRO, GB, B & Q etc brought about by

globalisation. These Leviathans now dominate the markets of the developed world. They

buy in vast quantities at punitive prices. They ‘imprison’ the producers with quantity but

leave no room for profit and typically they lock in the manufacturers to their ‘model’ of

trading leaving no room for exploration of other possible outlets.

Such business can have short term benefits for manufacturers seeking to build up

manufacturing stamina but in general companies who remain supplying such companies are

doomed to failure unless they take time to develop an alternative model of trading and build

up their own market presence through design, branding and service.

2.4.2.10 Product design and innovation

An estimated 90% of Vietnam’s production is based on customer specification. Little product

development and innovation is made on the industry’s own initiative, exporters lack design

competence. This is a major weakness and one which this strategy must address.

Vietnamese products have a highly uniform appearance, especially for outdoor furniture.

Vietnam lacks adequate research and development support for the production of furniture.

The market potential in the US, EU and Japan for low-cost, mass market suppliers is huge

however as the entire distribution chain upgrades to higher quality, better designed products

it still demands that pricing is held low and continually squeezes the manufacturer to meet

the lowest prices. At the moment Vietnamese suppliers are currently competing almost

entirely on the lowest price and are still being outbid by Chinese factories. This is a bad place

to be.

To supply a higher market, producers will need to upgrade their designs, quality, and

finishing techniques, and constantly stay on top of current design and consumer trends. They

must also commence ‘branding’ both individually as companies establishing their own brand

name but also as VIETNAM establishing VIETNAM as a source of well designed, well made

and affordable product. The objective has to be to get closer to the market and to have as

little ‘interference’ as possible between the producer and the end user. There is greater

long-term export potential for mid-sized companies that determinedly brand to supply better

products to mid-level international markets.

Recently, some big companies have set up their own design departments and, there is also a

trend towards hiring foreign designers to develop their products. Design is a must and design

training has to be a component of any strategy to upgrade and develop the industry.

2.4.2.11 Access to Financing

Access to financing sources plays a very important role for industry. The wood producers and

furniture manufacturers are no exception. They need finance to upgrade their equipment,

store enough materials for stable production and to finance sales. There are many different

sources of finance providers that wood producers can approach, from the commercial banks,

and the development banks to the capital and investment funds. In general, the procedures for

getting loans are very time-consuming even though it has been much improved in recent

times. Besides that, the high interest from the banks (about 12 to 15% a year) is the biggest

problem that causes difficulties for the producers and it reduces the competitiveness of the

sector. Further support to reduce the interest burden needs to be done to promote wood sector.

The Chinese government ordered its banks to offer lowest rates to wood manufacturers

several years ago.

2.4.2.12 Trade promotion

Vietnam’s competitors from other Asian countries, and from European countries too, have

more advanced trade promotion systems. They have important international trade fairs at

home and they attend the leading International Fairs collectively. Good information systems,

attract more foreign business visitors. Properly organized trade fair participation is vital to

the development of the industry.

Many international buyers report problems in identifying suitable suppliers in Vietnam and at

the same time, exporters report poor access to market related information and have little

knowledge about international market structures.

2.4.2.13 Entrepreneurial skills

Vietnam’s wood furniture sector is still a very young industry with many companies having

emerged during the last 2-5 years only. As a result, entrepreneurial skills, know-how on

marketing, financial planning, company organization, command of foreign languages etc are

still weak. Business managers manage everything from product development, marketing, and

quality management to financial management. There is no organizational hierarchy with

delineated functions within furniture enterprises. Hence, the structure of enterprises is

significantly weak, as business operation stops in the absence of the business manager.

2.4.2.14 Infrastructure

Shipping from Vietnam to markets in the US or Europe does not, generally, present any

logistical problems but costs of shipping tend to be more expensive. Compared with China,

Vietnamese exporters incur relatively high overseas transport costs for both sea and air

transport. Recent findings from the Georgetown University, USA8 on ocean freight from

China and Vietnam to the States show that “Ocean freight and delivery time from Vietnam to

the States for 50 containers are 322,000 US$ and 17-35 days, while those figures from China

are 136,000 US$ and 11 days, respectively”. International importers indicate that there are

10-30% hidden subsidies for Chinese exporters

Infrastructure, especially the availability of suitable seaports, has become a major concern for

the development of the furniture industry in several provinces. For the time being, there is a

trend towards moving processing factories from the Central Highlands provinces to the wood

processing centers like Hochiminh, Binh Duong and Binh Dinh. This is done to reduce the

transportation cost to the port and increase the sourcing capacity of supporting accessories

(fabric, metal parts, finishes etc. ). The processing factories in the provinces are then just

specialized in parts and accessories production for the final assembly factory in the wood-

centered areas. (Wood furniture manufacturers in Gia Lai is an example, they have to pay

between US$300 and US$650 for a 40’ container to Quy Nhon and Saigon port, respectively

while the cost from Binh Duong to Saigon is just US$100)

The road condition in the Southern provinces is another issue. Most of the roads in this area

only allow trucks of less than 25 tons, but containers of imported wood usually weigh more

than 30 tons. To transport the wood to the factories, wood processing companies must divide

the volume of imported wood into smaller loads, which further increases the production cost.

2.4.2.15 Other logistical issues

Other logistics and commercial issues for woodwork export activities cover payment through

banks, warehousing, customs declaration and related services. All of these issues are

acceptable, except storage facilities, which are still poor. For many years, the Ministry of

Trade (now the Ministry of Industry and Trade) has been asking the association to call for

member enterprises to establish wood import and storage hubs in three regions of Vietnam,

but its effort has not borne fruit and every woodwork enterprise still has its own plans for

importing wood, which unintentionally pushes up the cost of input materials.

2.4.2.16 Summary of Critical Success factors.

1. Government should be pro active in providing an enabling environment for industry to

thrive. Raw material security, training facilities, financing and infrastructure are the

8 Workshop in Binh Dinh, organized by MPDF-IFC.

critical issues.

2. Industry must be managed profitably to ensure adequate funding is in place to fuel

development and attract the investment necessary. Value not volume is the critical issue.

3. Branding of product must be established and nurtured to ensure customer satisfaction and

customer loyalty.

4. Marketing, Design , Innovation and Product Development must be actively pursued to

ensure value addition to products and market take-up of production.

5. Quality and value for money must be relentlessly pursued.

6. Employee attraction and retention is vital to the long term success of individual