working capital,credit and accounts receivable management

TRANSCRIPT

8/6/2019 Working Capital,Credit and Accounts Receivable Management

http://slidepdf.com/reader/full/working-capitalcredit-and-accounts-receivable-management 1/31

Working Capital, Credit andWorking Capital, Credit and

Accounts ReceivableAccounts ReceivableManagementManagement

8/6/2019 Working Capital,Credit and Accounts Receivable Management

http://slidepdf.com/reader/full/working-capitalcredit-and-accounts-receivable-management 2/31

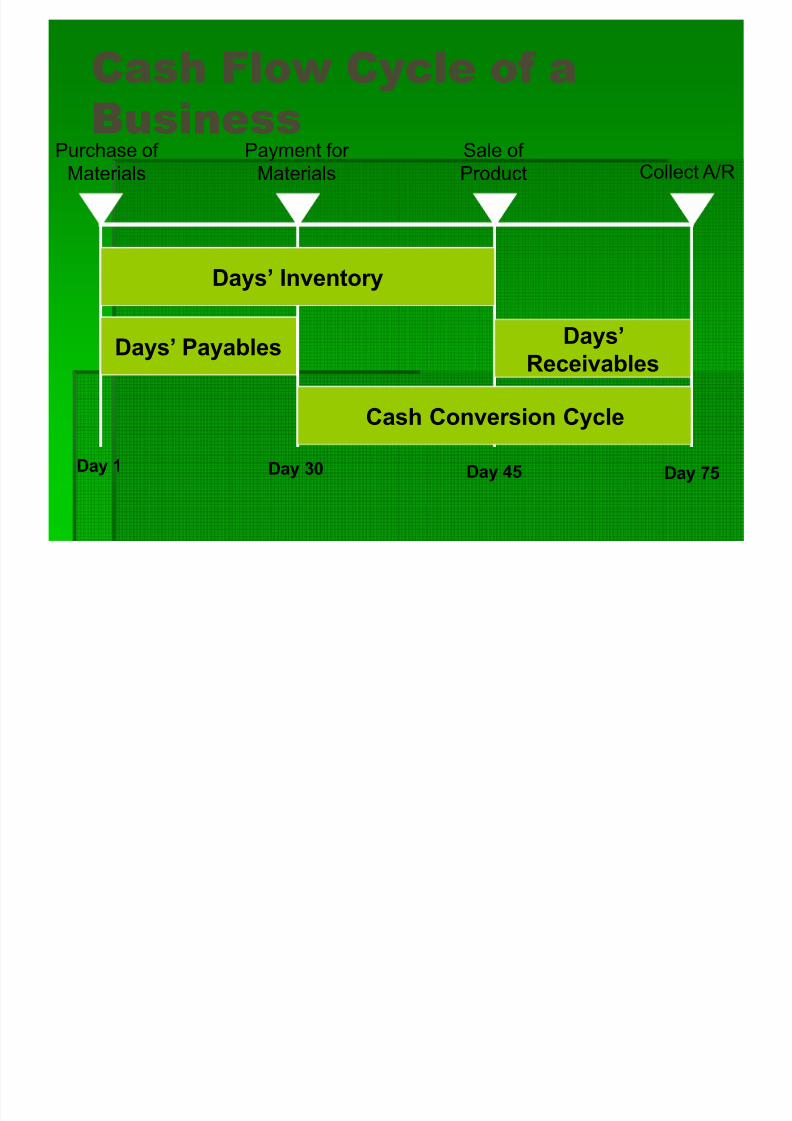

Cash Flow Cycle of aCash Flow Cycle of a

BusinessBusinessPurchase of

Materials

Payment for

Materials

Sale of

Product Collect A/R

Days¶ Inventory

Cash Conversion Cycle

Days¶Receivables

Days¶ Payables

Day 1 Day 30 Day 45 Day 75

8/6/2019 Working Capital,Credit and Accounts Receivable Management

http://slidepdf.com/reader/full/working-capitalcredit-and-accounts-receivable-management 3/31

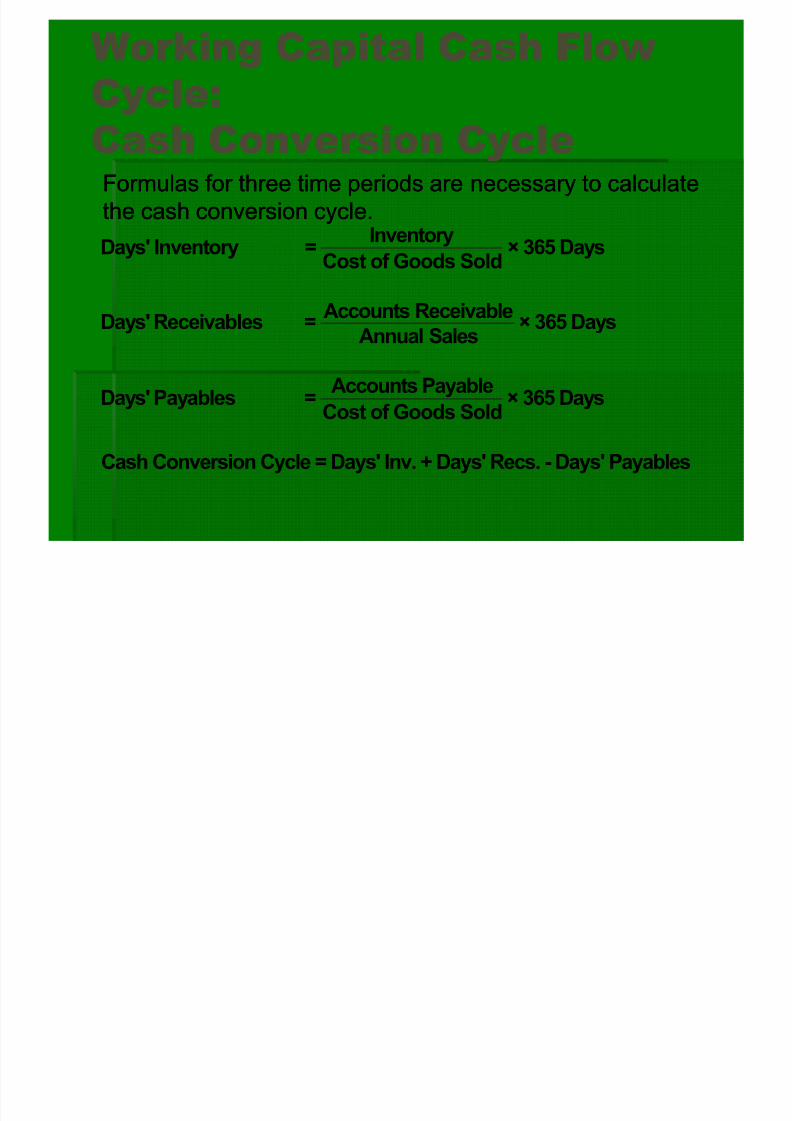

Working Capital Cash FlowWorking Capital Cash Flow

Cycle:Cycle:

Cash Conversion CycleCash Conversion Cycle

Inventory

Days' Inventory = × 365 DaysCost of Goods Sold

Accounts ReceivableDays' Receivables = × 365 Days

Annual Sales

Accounts PayableDays' Payables = × 365 DaysCost of Goods Sold

Cash Conversion Cycle = Days' Inv. + Days' Recs. - Days' Payables

Formulas for three time periods are necessary to calculateFormulas for three time periods are necessary to calculate

the cash conversion cycle.the cash conversion cycle.

8/6/2019 Working Capital,Credit and Accounts Receivable Management

http://slidepdf.com/reader/full/working-capitalcredit-and-accounts-receivable-management 4/31

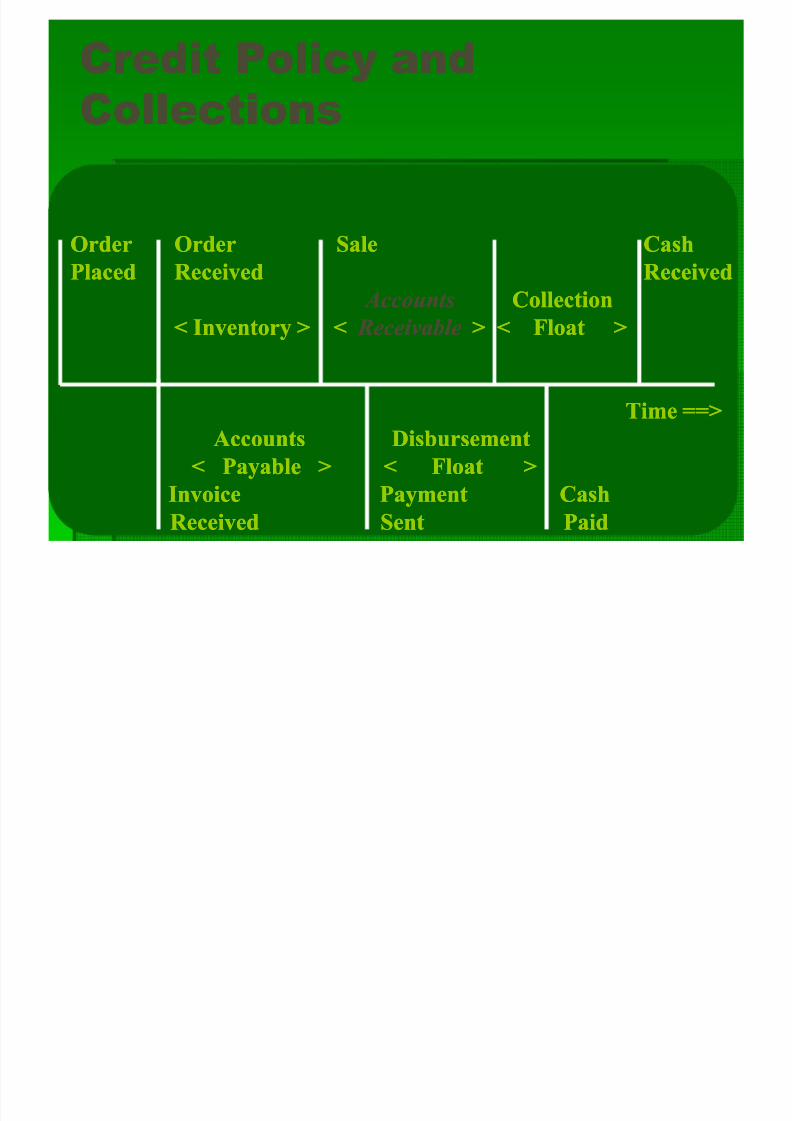

Credit Policy andCredit Policy and

CollectionsCollections

OrderOrder OrderOrder SaleSale CashCashPlacedPlaced ReceivedReceived ReceivedReceived

Accounts Accounts CollectionCollection

< Inventory > << Inventory > < Receivable Receivable > < Float >> < Float >

Time ==>Time ==>

Accounts DisbursementAccounts Disbursement

< Payable > < Float >< Payable > < Float >

InvoiceInvoice PaymentPayment CashCash

Received Sent PaidReceived Sent Paid

8/6/2019 Working Capital,Credit and Accounts Receivable Management

http://slidepdf.com/reader/full/working-capitalcredit-and-accounts-receivable-management 5/31

Objectives of Credit ManagementObjectives of Credit Management

Creating, preserving, and collecting A/R.Creating, preserving, and collecting A/R.

Establishing and communicating credit policies.Establishing and communicating credit policies.

Evaluation of customers and setting creditEvaluation of customers and setting creditlines.lines.

Ensuring prompt and accurate billing.Ensuring prompt and accurate billing.

Maintaining upMaintaining up--toto--date records of accountsdate records of accounts

receivables.receivables. Initiating collection procedures on overdueInitiating collection procedures on overdue

accountsaccounts..

8/6/2019 Working Capital,Credit and Accounts Receivable Management

http://slidepdf.com/reader/full/working-capitalcredit-and-accounts-receivable-management 6/31

Reasons to Offer CreditReasons to Offer Credit

CompetitionCompetition

Market ShareMarket Share

PromotionPromotion

Credit Availability to CustomersCredit Availability to Customers

Customer ConvenienceCustomer Convenience

ProfitProfit

8/6/2019 Working Capital,Credit and Accounts Receivable Management

http://slidepdf.com/reader/full/working-capitalcredit-and-accounts-receivable-management 7/31

Credit and A/R Management:Credit and A/R Management:Fit Into the Financial OrganizationFit Into the Financial Organization

A credit manager or a captive finance company A credit manager or a captive finance companyis the administrator of credit policies.is the administrator of credit policies.

Credit policies and collections will impact cashCredit policies and collections will impact cashflows so credit and cash managers must workflows so credit and cash managers must worktogether.together.

Reasons for credit and cash manager Reasons for credit and cash manager

interaction include the accuracy of cash flowinteraction include the accuracy of cash flowforecast, banking network management, andforecast, banking network management, andaccounts receivable updating.accounts receivable updating.

8/6/2019 Working Capital,Credit and Accounts Receivable Management

http://slidepdf.com/reader/full/working-capitalcredit-and-accounts-receivable-management 8/31

Cost Associated With aCost Associated With a

Credit PolicyCredit Policy

Credit Department CostsCredit Department Costs

Credit Evaluation CostsCredit Evaluation Costs A/R Carrying Cost A/R Carrying Cost

Discounted PaymentsDiscounted Payments

Selling and Production CostSelling and Production Cost

Collection ExpensesCollection Expenses

Bad DebtsBad Debts

8/6/2019 Working Capital,Credit and Accounts Receivable Management

http://slidepdf.com/reader/full/working-capitalcredit-and-accounts-receivable-management 9/31

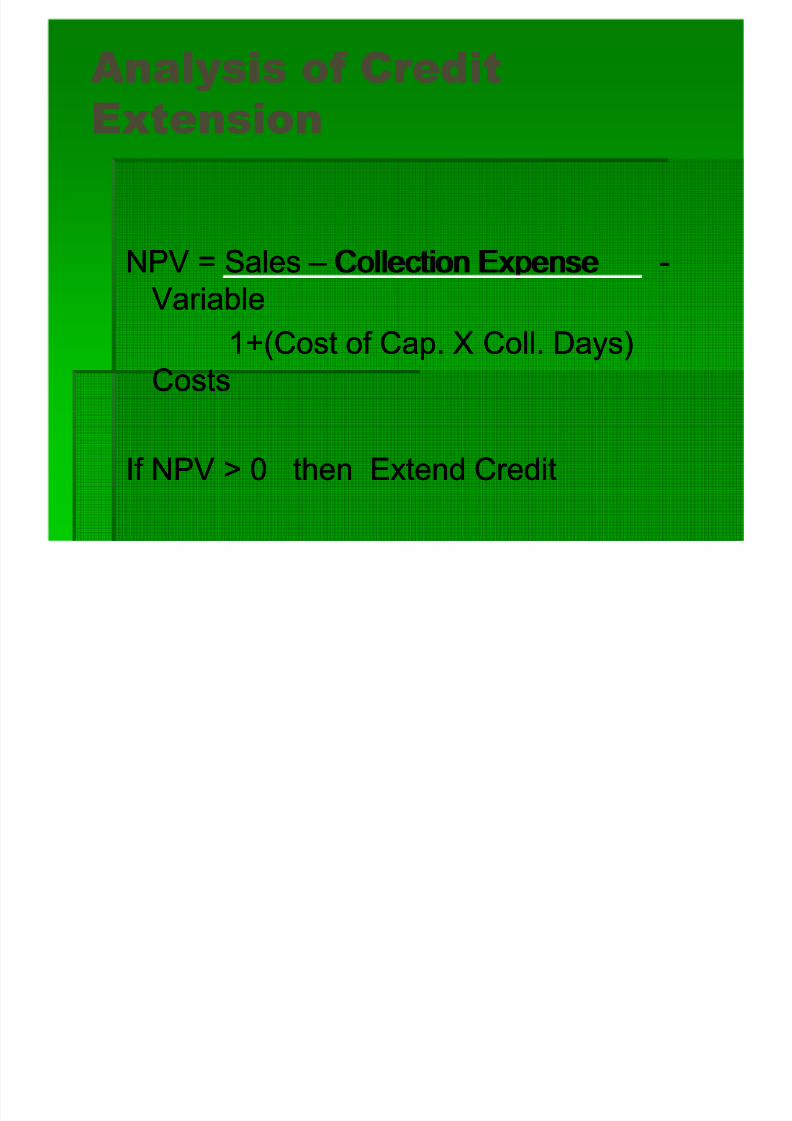

Analysis of CreditAnalysis of Credit

ExtensionExtension

NPV =NPV = SalesSales ± ± Collection ExpenseCollection Expense --VariableVariable

1+(Cost of Cap. X Coll. Days)1+(Cost of Cap. X Coll. Days)

CostsCosts

If NPV > 0 then Extend CreditIf NPV > 0 then Extend Credit

8/6/2019 Working Capital,Credit and Accounts Receivable Management

http://slidepdf.com/reader/full/working-capitalcredit-and-accounts-receivable-management 10/31

Forms of Credit ExtensionForms of Credit Extension

Installment CreditInstallment Credit Revolving CreditRevolving Credit

Letters of CreditLetters of Credit

Open AccountOpen Account

8/6/2019 Working Capital,Credit and Accounts Receivable Management

http://slidepdf.com/reader/full/working-capitalcredit-and-accounts-receivable-management 11/31

Common Terms of SalesCommon Terms of Sales

Cash Before Delivery (CBD)Cash Before Delivery (CBD)

Cash on Delivery (COD)Cash on Delivery (COD)

Cash TermsCash Terms Net TermsNet Terms

Discount TermsDiscount Terms

Monthly BillingMonthly Billing

Bill of Lading or Documentary CollectionBill of Lading or Documentary Collection Seasonal DatingSeasonal Dating

ConsignmentConsignment

8/6/2019 Working Capital,Credit and Accounts Receivable Management

http://slidepdf.com/reader/full/working-capitalcredit-and-accounts-receivable-management 12/31

The Five C·s of CreditThe Five C·s of Credit Character Character

CapacityCapacity

CapitalCapital

CollateralCollateral

ConditionsConditions

8/6/2019 Working Capital,Credit and Accounts Receivable Management

http://slidepdf.com/reader/full/working-capitalcredit-and-accounts-receivable-management 13/31

Cost of Trade CreditCost of Trade Credit

From a seller¶s viewpoint, the cost of theFrom a seller¶s viewpoint, the cost of thediscount must be weighted against the benefitdiscount must be weighted against the benefitof receiving early payment.of receiving early payment.

From buyer¶s viewpoint, the cost of tradeF

rom buyer¶s viewpoint, the cost of tradecredit is an opportunity cost.credit is an opportunity cost.

A buyer should take the discount if its cost of A buyer should take the discount if its cost of borrowing is less than the cost of foregoingborrowing is less than the cost of foregoing

the discount.the discount. Alternatively, a buyer should forego the Alternatively, a buyer should forego the

discount if investment rates are higher thandiscount if investment rates are higher thanthe cost of foregoing the discount.the cost of foregoing the discount.

8/6/2019 Working Capital,Credit and Accounts Receivable Management

http://slidepdf.com/reader/full/working-capitalcredit-and-accounts-receivable-management 14/31

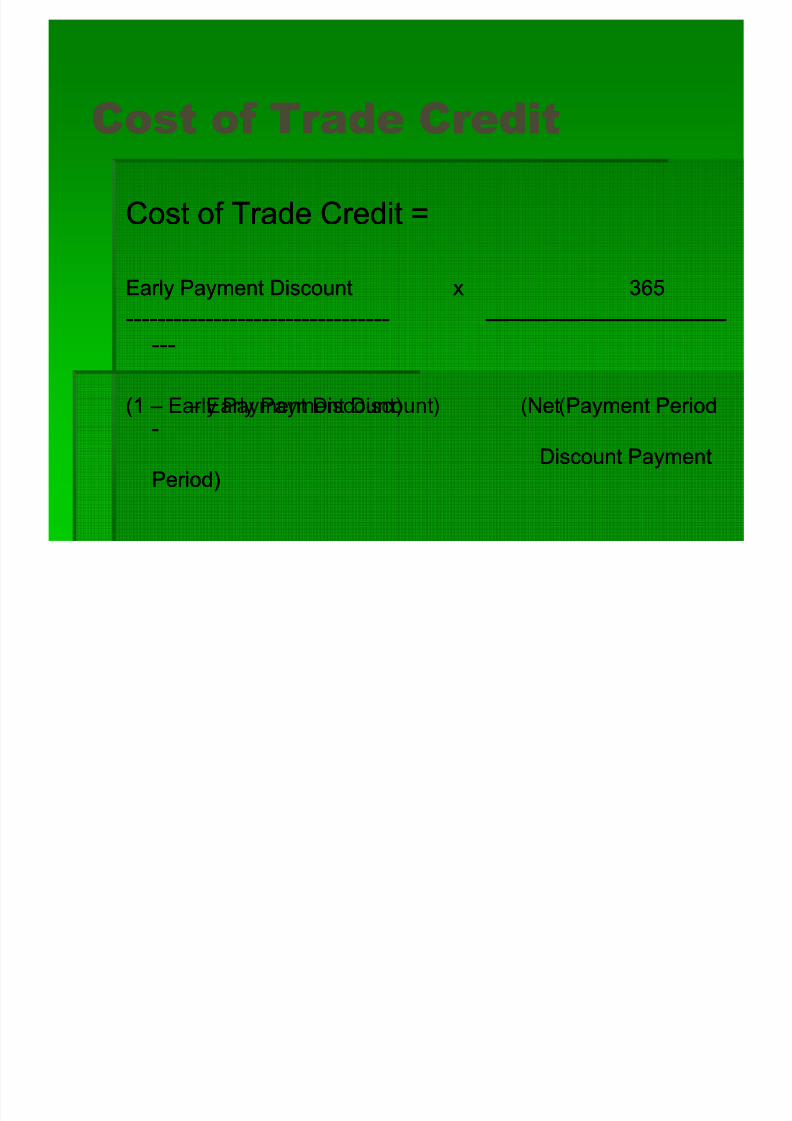

Cost of Trade CreditCost of Trade Credit

Cost of Trade Credit =Cost of Trade Credit =

Early Payment Discount x 365Early Payment Discount x 365

------------------------------------------------------------------ ------------------------------------------------------------------

(1(1 ± ± Early Payment Discount) (Net Payment PeriodEarly Payment Discount) (Net Payment Period--

Discount PaymentDiscount PaymentPeriod)Period)

8/6/2019 Working Capital,Credit and Accounts Receivable Management

http://slidepdf.com/reader/full/working-capitalcredit-and-accounts-receivable-management 15/31

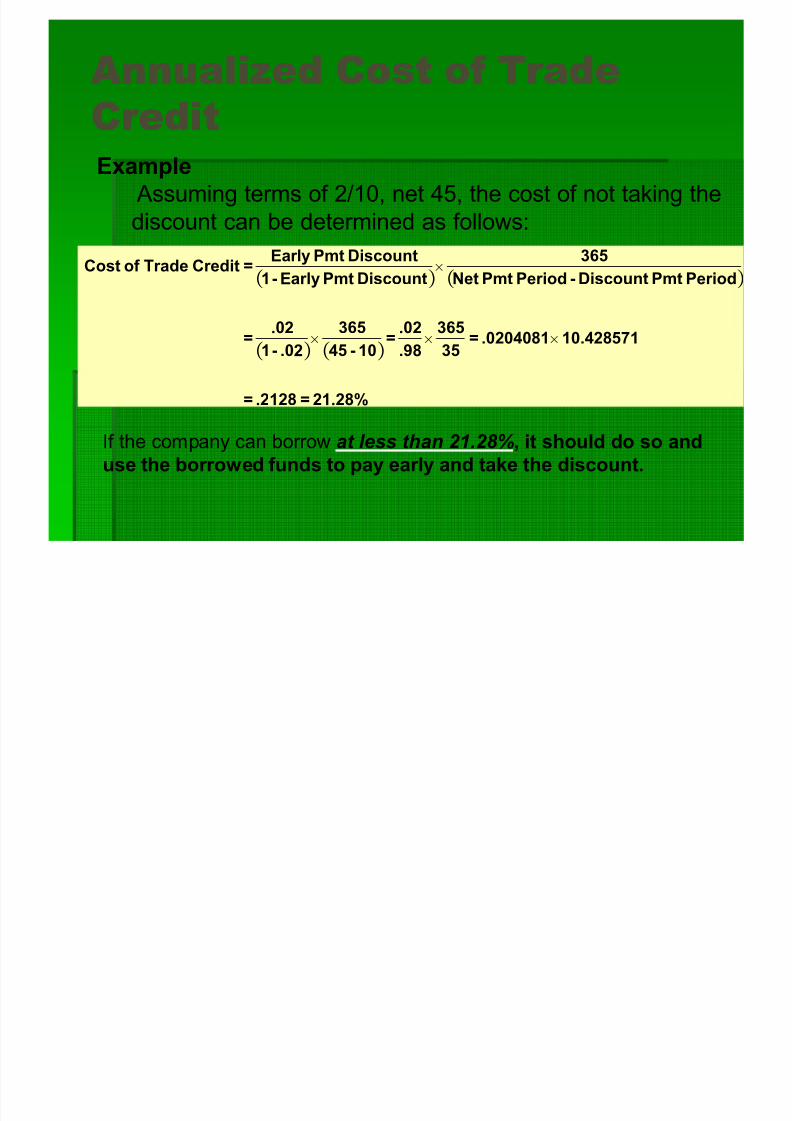

Annualized Cost of TradeAnnualized Cost of Trade

CreditCreditExample

Assuming terms of 2/10, net 45, the cost of not taking the

discount can be determined as follows:

21.28%=.2128=

10.428571.0204081=35

365

.98

.02 =

10-45

365

.02-1

.02 =

PeriodPmtDiscount-PeriodPmtNet365

DiscountPmtEarly-1DiscountPmtEarly =CreditTradeof Cost

vvv

v

If the company can borrow at less than 21.28%, it should do so anduse the borrowed funds to pay early and take the discount.

8/6/2019 Working Capital,Credit and Accounts Receivable Management

http://slidepdf.com/reader/full/working-capitalcredit-and-accounts-receivable-management 16/31

Account ReceivableAccount Receivable

Monitoring and ControlMonitoring and Control

Monitoring and control is the responsibility of Monitoring and control is the responsibility of the credit manager.the credit manager.

Receivables turnover Receivables turnover

least favored techniqueleast favored technique

Monitoring conducted on individual accountsMonitoring conducted on individual accountsthroughthrough aging schedulesaging schedules..

Monitoring conducted at the aggregate levelMonitoring conducted at the aggregate level

usingusing days¶ sales outstandingdays¶ sales outstanding (DSO).(DSO).

8/6/2019 Working Capital,Credit and Accounts Receivable Management

http://slidepdf.com/reader/full/working-capitalcredit-and-accounts-receivable-management 17/31

DSODSO

Can give an indication of overallCan give an indication of overallcollection efficiency.collection efficiency.

Changes in sales volume, paymentChanges in sales volume, payment

patterns, or strong seasonality in salespatterns, or strong seasonality in sales

can distort DSO.can distort DSO.

8/6/2019 Working Capital,Credit and Accounts Receivable Management

http://slidepdf.com/reader/full/working-capitalcredit-and-accounts-receivable-management 18/31

Days· SalesDays· Sales

Outstanding (DSO) Outstanding (DSO)

Assume that a company has outstanding receivables of Assume that a company has outstanding receivables of Rs350,000 at the end of the first quarter and credit sales of Rs350,000 at the end of the first quarter and credit sales of Rs425,000 for the quarter. Using a 90Rs425,000 for the quarter. Using a 90--day averagingday averagingperiod, the DSO for this company can be computed asperiod, the DSO for this company can be computed asfollows:follows: Sales During Period $425,000Avg. Daily Credit Sales = = = $4,722.22

Number of Days in Period 90

Outstanding A/R $350,000DSO = = = 74.11 Days

Avg. Daily Credit Sales $4,722.22

Average Past Due = DSO - Avg. Days of Credit Terms

= 74.11 Days - 60 Days = 14.11 Days

If the company¶s credit terms are net 60, the average past due iscomputed as follows:

8/6/2019 Working Capital,Credit and Accounts Receivable Management

http://slidepdf.com/reader/full/working-capitalcredit-and-accounts-receivable-management 19/31

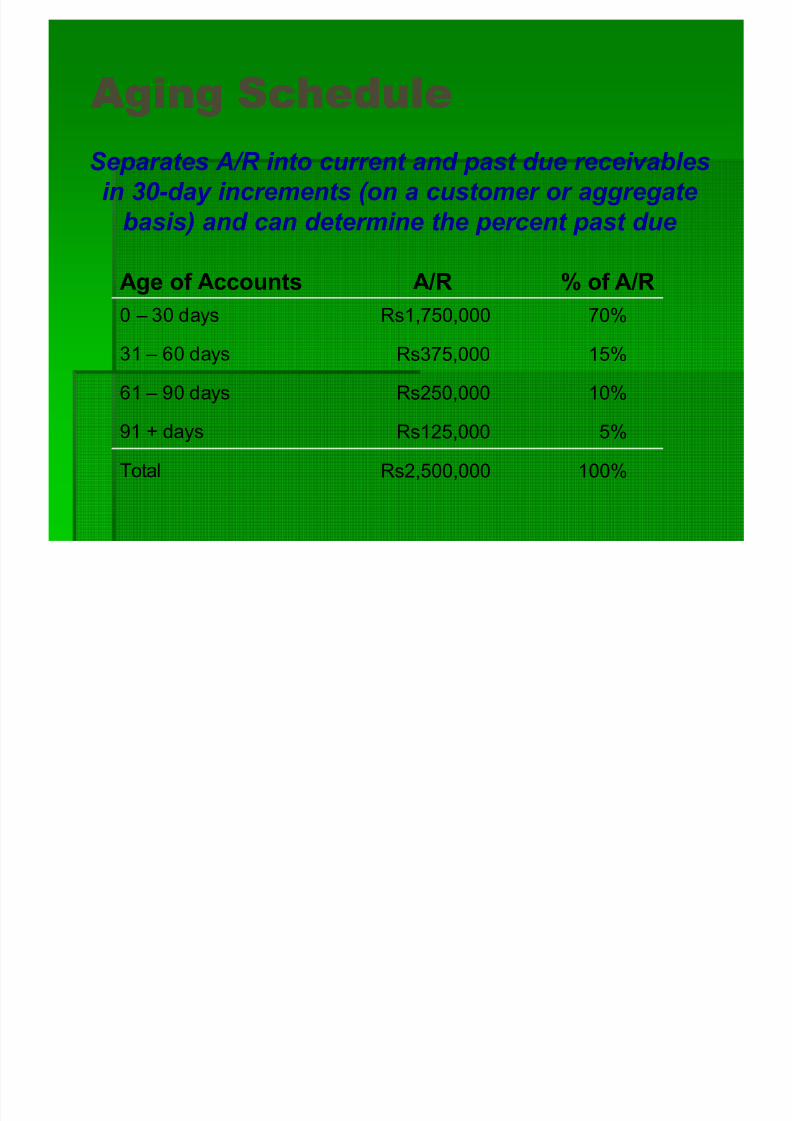

Aging ScheduleAging Schedule

Is a list of the percentage and/or amounts of Is a list of the percentage and/or amounts of

outstanding A/R classified as current or pastoutstanding A/R classified as current or past

due.due.

Used primarily to identify past due accounts.Used primarily to identify past due accounts.

Can be prepared at the aggregate level or Can be prepared at the aggregate level or

customer customer--byby--customer.customer.

Subject to distortions due to sales variations.Subject to distortions due to sales variations.

8/6/2019 Working Capital,Credit and Accounts Receivable Management

http://slidepdf.com/reader/full/working-capitalcredit-and-accounts-receivable-management 20/31

Aging ScheduleAging Schedule

Age of Accounts A/R % of A/R

0 ± 30 days

31 ± 60 days

61 ± 90 days

91 + days

Total

Rs1,750,000

Rs375,000

Rs250,000

Rs125,000

Rs2,500,000

70%

15%

10%

5%

100%

S eparates A/R into current and past due receivables

in 30-day increments (on a customer or aggregate

basis) and can determine the percent past due

8/6/2019 Working Capital,Credit and Accounts Receivable Management

http://slidepdf.com/reader/full/working-capitalcredit-and-accounts-receivable-management 21/31

A/R Balance PatternA/R Balance Pattern

Gives the percent of credit sales in a timeGives the percent of credit sales in a timeperiod that remains outstanding at the end of period that remains outstanding at the end of each time period.each time period.

Based on aging schedules.Based on aging schedules.

It is not directly affected by sales variations.It is not directly affected by sales variations.

A useful tool in cash flow forecasting because it A useful tool in cash flow forecasting because it

can be used to project A/R levels andcan be used to project A/R levels andcollections.collections.

8/6/2019 Working Capital,Credit and Accounts Receivable Management

http://slidepdf.com/reader/full/working-capitalcredit-and-accounts-receivable-management 22/31

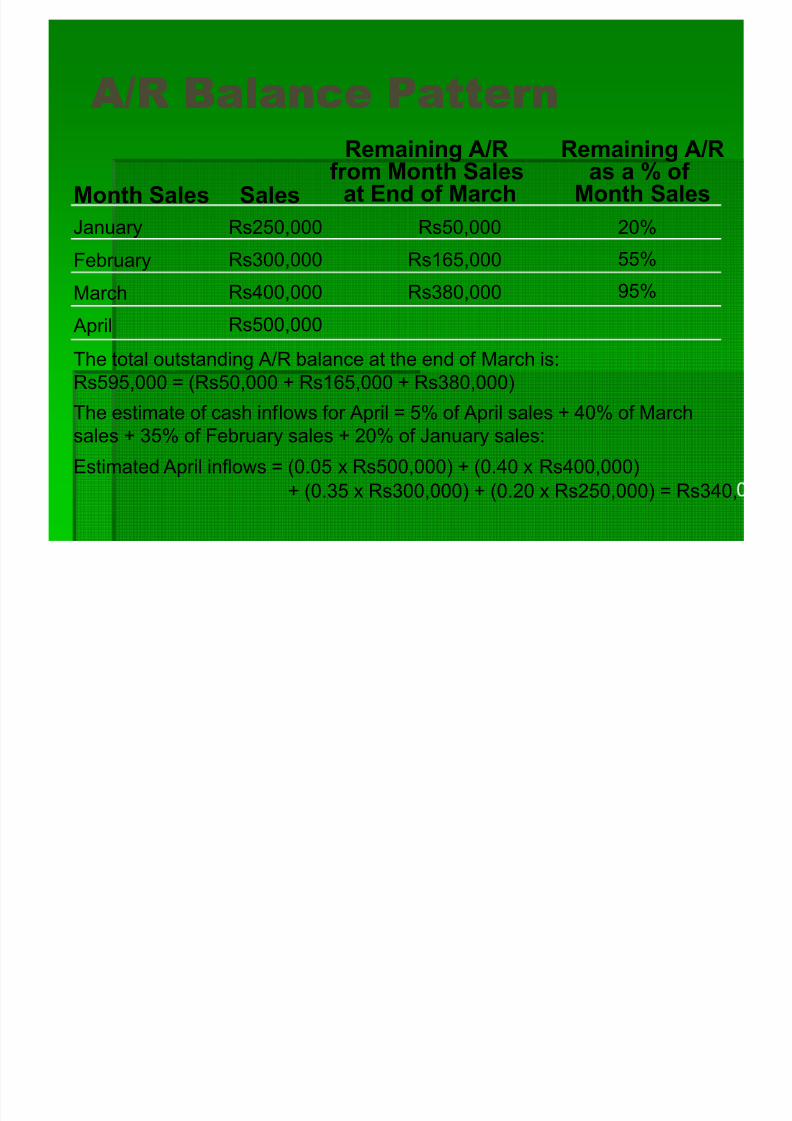

A/R Balance PatternA/R Balance Pattern

Month Sales Sales

Remaining A/Rfrom Month Sales

at End of March

February

January

March

April

Rs250,000

Rs300,000

Rs400,000

Rs500,000

20%

55%

95%

Remaining A/Ras a % of

Month Sales

Rs50,000

Rs165,000

Rs380,000

The total outstanding A/R balance at the end of March is:

Rs595,000 = (Rs50,000 + Rs165,000 + Rs380,000)The estimate of cash inflows for April = 5% of April sales + 40% of March

sales + 35% of February sales + 20% of January sales:

Estimated April inflows = (0.05 x Rs500,000) + (0.40 x Rs400,000)

+ (0.35 x Rs300,000) + (0.20 x Rs250,000) = Rs340,

8/6/2019 Working Capital,Credit and Accounts Receivable Management

http://slidepdf.com/reader/full/working-capitalcredit-and-accounts-receivable-management 23/31

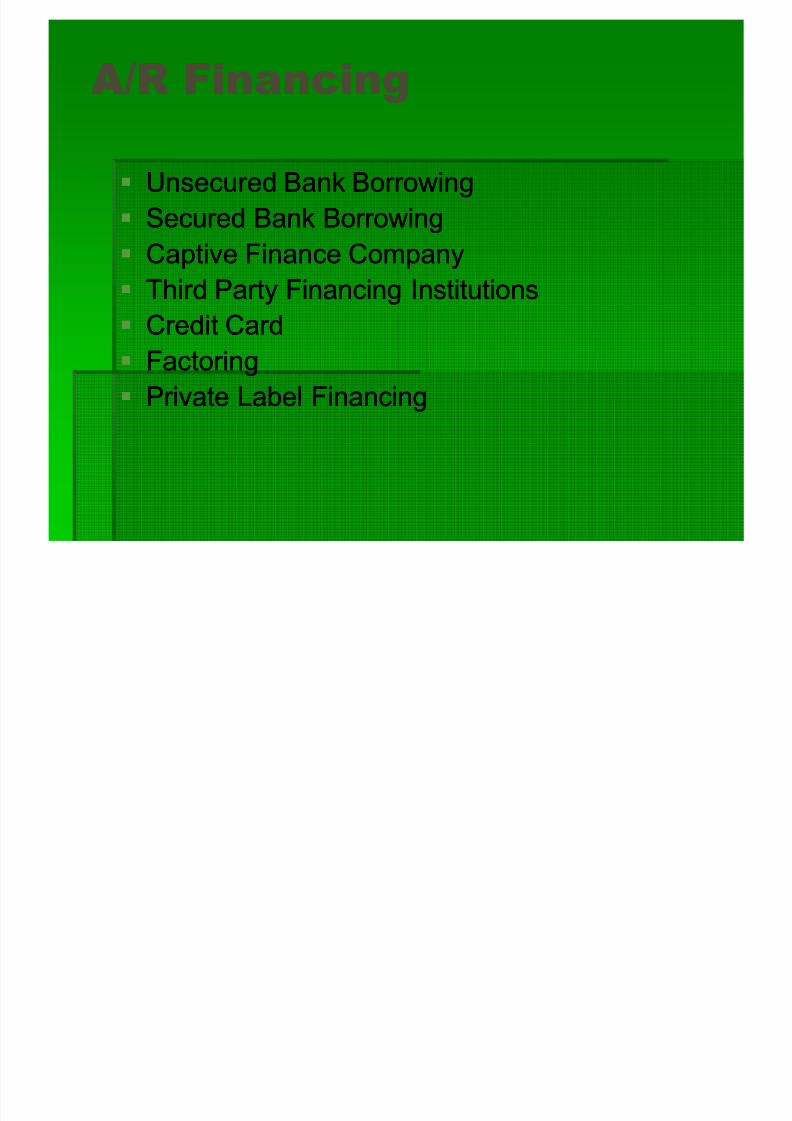

A/R FinancingA/R Financing

Unsecured Bank BorrowingUnsecured Bank Borrowing

Secured Bank BorrowingSecured Bank Borrowing

Captive Finance CompanyCaptive Finance Company

Third Party Financing InstitutionsThird Party Financing Institutions

Credit CardCredit Card

FactoringFactoring

Private Label FinancingPrivate Label Financing

8/6/2019 Working Capital,Credit and Accounts Receivable Management

http://slidepdf.com/reader/full/working-capitalcredit-and-accounts-receivable-management 24/31

Evaluate Changes inEvaluate Changes in

Credit PolicyCredit Policy Credit term change decision variablesCredit term change decision variables

effect on dollar profitseffect on dollar profits

sales effectsales effect

receivables effectreceivables effect

return on investment effectreturn on investment effect

default probabilitydefault probability

credit limitscredit limits

opportunity cost of funds invested in receivablesopportunity cost of funds invested in receivables

company¶s overall cost of capitalcompany¶s overall cost of capital

8/6/2019 Working Capital,Credit and Accounts Receivable Management

http://slidepdf.com/reader/full/working-capitalcredit-and-accounts-receivable-management 25/31

Cash ApplicationCash Application

Cash applicationCash application is the process of is the process of

matching and applying a customer¶smatching and applying a customer¶s

payment against accounts receivable.payment against accounts receivable.

Done via anDone via an Open ItemOpen Item or aor a BalanceBalance

ForwardForward system.system.

8/6/2019 Working Capital,Credit and Accounts Receivable Management

http://slidepdf.com/reader/full/working-capitalcredit-and-accounts-receivable-management 26/31

Open Item SystemOpen Item System

Used in commercial transactions.Used in commercial transactions. Each invoice is recorded separately inEach invoice is recorded separately in

an account receivable file.an account receivable file.

Payments are matched to the particular Payments are matched to the particular invoice in the file.invoice in the file.

8/6/2019 Working Capital,Credit and Accounts Receivable Management

http://slidepdf.com/reader/full/working-capitalcredit-and-accounts-receivable-management 27/31

Balance Forward SystemBalance Forward System

Used in retail applications.Used in retail applications.

Credit limits are established for eachCredit limits are established for each

individual.individual.

As purchases are made, A/R increase. As purchases are made, A/R increase.

Payments are applied against thePayments are applied against the

aggregate A/R outstanding.aggregate A/R outstanding.

8/6/2019 Working Capital,Credit and Accounts Receivable Management

http://slidepdf.com/reader/full/working-capitalcredit-and-accounts-receivable-management 28/31

Collection ProceduresCollection Procedures

Typical collection effortTypical collection effort initial contact within 10 days of delinquencyinitial contact within 10 days of delinquency

then reminder letter followed by phone callthen reminder letter followed by phone call

sales force notifiedsales force notified

last resort, reference to collection agency/legal actionlast resort, reference to collection agency/legal action

Collection agencyCollection agency Phase 1Phase 1 -- computer generated collection letter, whencomputer generated collection letter, when

accounts are 45 to 90 days past dueaccounts are 45 to 90 days past due Phase 2Phase 2 -- commissioned collectors usedcommissioned collectors used

8/6/2019 Working Capital,Credit and Accounts Receivable Management

http://slidepdf.com/reader/full/working-capitalcredit-and-accounts-receivable-management 29/31

Collection ProceduresCollection Procedures

Companies tend to be more aggressiveCompanies tend to be more aggressive

the larger the receivables balancethe larger the receivables balance

Companies understand the goodCompanies understand the good--willwilltradeoff when selecting collection methodstradeoff when selecting collection methods

8/6/2019 Working Capital,Credit and Accounts Receivable Management

http://slidepdf.com/reader/full/working-capitalcredit-and-accounts-receivable-management 30/31

International CreditInternational Credit

ManagementManagement Credit policy analysisCredit policy analysis

lengthening terms increases exchange rate risklengthening terms increases exchange rate risk

also increases default riskalso increases default risk

harder to get D&B reportsharder to get D&B reports

harder to get bank credit informationharder to get bank credit information

Modifying monitoring and collectionsModifying monitoring and collections legal remedies for late payment or nonpayment differ legal remedies for late payment or nonpayment differ

by countryby country

8/6/2019 Working Capital,Credit and Accounts Receivable Management

http://slidepdf.com/reader/full/working-capitalcredit-and-accounts-receivable-management 31/31

ATTENTION COMMERCEATTENTION COMMERCE

STUDENTSSTUDENTSACCOUNTING(FINANCIAL & COST) OFACCOUNTING(FINANCIAL & COST) OFICMAP STAGE 1,2,3,4ICMAP STAGE 1,2,3,4CA..MODULE B,C,DCA..MODULE B,C,DPIPFA (FOUNDATION,INTERMEDIATE,FINAL)PIPFA (FOUNDATION,INTERMEDIATE,FINAL)ACCAACCA--F1,F2,F3F1,F2,F3BBA,MBABBA,MBAB.COM(FRESH),M.COMB.COM(FRESH),M.COMMAMA--ECONOMICS..O/A LEVELSECONOMICS..O/A LEVELSKHALID AZIZ«..0322KHALID AZIZ«..0322--3385752..kARACHI3385752..kARACHI

JOIN GROUPJOIN GROUPhttp://finance.groups.yahoo.com/group/costhttp://finance.groups.yahoo.com/group/cost--accountantsaccountants