working with bdo salt best opportunities to serve …...page 1 client name - event - presentation...

TRANSCRIPT

Page 1Page 1Page 1Client name - Event - Presentation titlePage 1Client name - Event - Presentation titlePage 1Client name - Event - Presentation titlePage 1

Working with BDO SALTBest Opportunities to Serve your Clients

Tom SmithPartner – State and Local Tax

[email protected] (Mobile)[email protected]

Page 2Page 2Page 2

Thomas A. Smith, CPA

• 24 years of SALT Experience• Texas Sales and Use Tax Auditor• Coopers & Lybrand, Tulsa• Ernst & Young (Memphis and Atlanta)• KPMG, LLP (Tulsa and Dallas)• HoganTaylor LLP• BDO USA, LLP

Page 2

Page 3Page 3Page 3

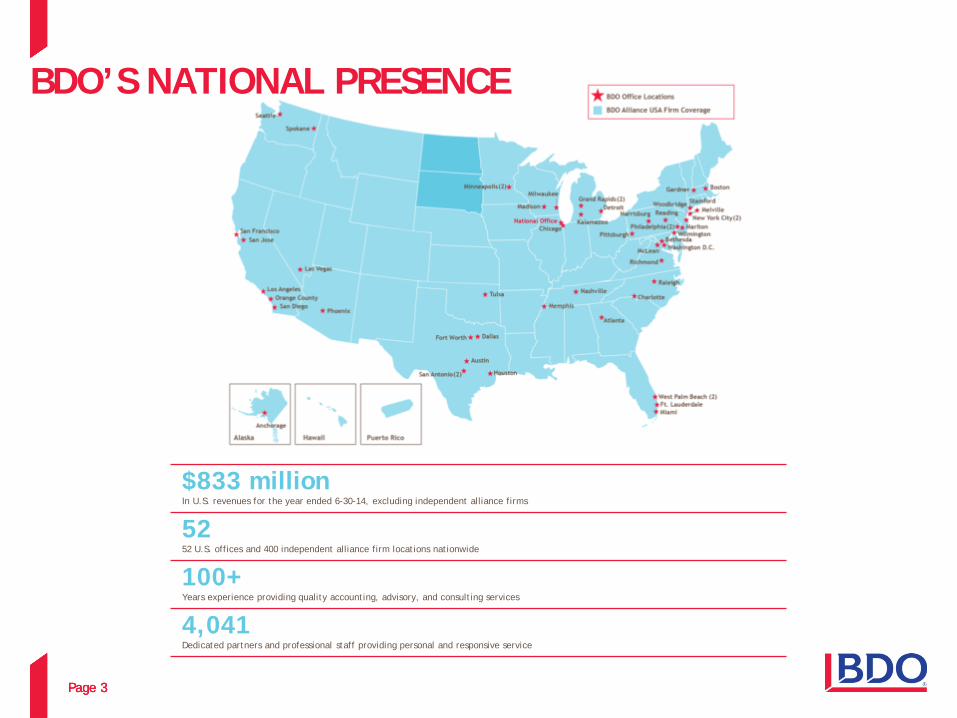

BDO’S NATIONAL PRESENCE

$833 millionIn U.S. revenues for the year ended 6-30-14, excluding independent alliance firms

5252 U.S. offices and 400 independent alliance firm locations nationwide

100+Years experience providing quality accounting, advisory, and consulting services

4,041Dedicated partners and professional staff providing personal and responsive service

Page 4Page 4Page 4

BDO’S GLOBAL REACH5thLargest

Accountancy Network

$6.45BRevenues in FY13

56,389Total

Personnel

1,264Offices

144Countries

Page 5Page 5Page 5Page 5

State and Local Tax (SALT)

Escheat(unclaimed property)

Credits & Incentives

Sales and Use Tax

Property Tax

Income /Franchise Tax

Page 6Page 6Page 6

Local Property Tax Updates Washington County reappraisal – an example

• Court ordered reappraisal• Tax Equalization Division indicated too many properties were under and over

assessed.• Last reappraisal was early effective in 1981• 121,000 parcels reappraised• Likely significant increases and potential over-assessments.

Page 7Page 7Page 7

Interesting proposal in Pittsburgh• They’ve had 3 reappraisals in 15 years• Value appeals by city is common after sale – resolution would limit this

ability until two years after sale.• Limits city to appealing value to once every three years.• Generate list of properties with assessments 50% over market value and city

would appeal values downward. City traditionally defended values.• City could be fighting reappraisals against school districts and municipalities

on behalf of property owner.• The proposal was pushed into committee – likely too many obstacles for

implementation

City of Baltimore has recently become more engaged in tracking sales and appealing assessments for value increases.

Local Property Tax Updates

Page 8Page 8Page 8

Property Tax – Value In Use Vs Value In Exchange• “Dark Store” theory for big box retailers (successful lawsuits in mid-west

spreading to other states) - properties are unique and few alternatives if the space goes vacant. Therefore current use value is not actual market value (value in exchange).

• Recent Harley Davidson case in York County has brought this issue recently to Pennsylvania. Other issues with pollution stigma muddies the water.

• A property is to be assessed at its actual value. 53 Pa.C.S. § 8842. Actual value means a parcel's fair market value, which is the price which a purchaser, willing but not obliged to buy, would pay an owner, willing but not obliged to sell, taking into consideration all uses to which the property is adapted and might in reason be applied. In that regard, a parcel's market value is distinct from its value as it is currently being used; the Commonwealth Court of Pennsylvania has reasoned that a property's use and its resulting value-in-use, value unique to a particular owner, is not to be considered in assessing the fair market value of property for tax assessment purposes.

Page 9Page 9Page 9

Property Tax - Department Stores

• It’s estimated about 800 stores, or about 1/5 of mall anchor space, would need to close to return market to 2006 levels of sales per square foot.

• Competition from online retailers (Amazon) and discount retailers ( Walmart) are hurting Sears, JC Penney, and Macy’s. Department stores were expanding fairly rapidly before recession.

• Average mall in America generated $165 in sales per square foot last year (24% decline over last decade). There were an estimated 35 million visits to malls in 2010. The number of visits are estimated at 17 million in 2013.

• Problem of decreasing mall values is a problem for pensions and other large investors. They have to invest billions of dollars and reach targeted returns for their members. A commercial real estate bubble is brewing.

Page 10Page 10Page 10

Unclaimed Property

• Generally intangible personal property for which there has been no owner activity for a specified period of time (“dormancy period”).

• Examples of unclaimed property:

• Uncashed payroll or commission checks• Uncashed payable/vendor checks• Gift certificates/gift cards• Customer merchandise credits, layaways, deposits, refunds or rebates• Overpayments/unidentified remittances• Unused/outstanding benefits (non-ERISA)• Miscellaneous income/bad debt expense accounts

Page 11Page 11Page 11

Unclaimed Property

• All 50 states and the District of Columbia have enacted unclaimed property laws.

• The purpose of unclaimed property laws is to ensure the protection of abandoned property until the rightful owner is located. Moreover, states use any derivative funds earned on such property for the public good.

• The Supreme Court of the United States in Texas v. New Jersey, established the following unclaimed property sourcing rule:

• First, to the state of the rightful owner’s last known address, if known, or

• Second, to the state of the holder’s incorporation (commercial domicile for unincorporated entities).

• Dormancy Periods

Page 12Page 12Page 12

Unclaimed Property • Temple-Inland, Inc. v. Cook

• Temple-Inland, Inc., a Delaware incorporated entity, was audited by Kelmar Associates on behalf of the State of Delaware beginning in 2008, and subsequently filed an administrative appeal regarding Kelmar’s “Report of Examination.”

• On June 28, 2016 The Court entered summary judgement in favor of Temple-Inland on the substantive due process claims. There was no suggested remedy published at the time.

• The case was settled out of court on August 5, 2016.

• DE SOS update to VDA Program • In late August the DE SOS issued a letter for all companies in the DE VDA program. The highlights are as follows:

• The Court’s ruling in Temple-Inland is limited to the specific facts and circumstances of the unclaimed property audit issue in the case.

• DE SOS VDA program is different than Audit at issue in Temple-Inland.• Extrapolation formula requires “reasonable estimation” and bright line test (expected to remain as “gross

approach method” and avoids multiple state extrapolations in their view);• Extrapolation method is same or substantially similar method used by other states;• DE VDA 2 Release Form - state agrees to indemnify the holder for all future claims by another state on

the estimated unclaimed property that was reported (application of this must be made clear as part of the settlement, with additional language by legal counsel where warranted);

• Reduced look-back to 10 years plus 5 year dormancy period = 15 years from date of enrollment

• Legislature will convene in January 2017 and is expected to make certain statutory changes to unclaimed property law.

Page 13Page 13Page 13

In most organizations, tax is a reactionto events that have already occurred.

I’m usually called to find a solution during an unexpected audit, that could have went much better

had a simple strategy been in place.

Page 13

Page 14Page 14Page 14

The Result Is:Limited opportunities for improvementLimited opportunities to manage risk

Page 14

Page 15Page 15Page 15

Companies have all sorts of marketing plans but very rarely have a state tax plan or

strategy.

Page 15

Page 16Page 16Page 16

Not talking about the tax tail wagging the dog.

Tax Tail

Page 16

Page 17Page 17Page 17

But proactively managing the tax destiny by design

Instead of allowing a client’s tax destiny to be created

by default

Page 17

Page 18Page 18Page 18

Identify Key Triggers

Establish clear triggers that will cause the company to establish itself in a state.

Know the questions you need answered.

For Example:- Employee Living in a State- Sales Person Entering a State- Preforming a Service in a State- Sales Level or Volume within a State

Client name - Event - Presentation titlePage 18

Page 19Page 19Page 19

Type of Taxes

• Sales Tax• Transaction Taxes imposed on transfers of

tangible personal property and taxable services

• Use tax • Tax imposed on “USE” of property in State

Page 20Page 20Page 20

Type of Taxes

• Intrastate Sales• Transactions completed in the SAME state• If Seller and Purchaser are in same state and

the sale is consummated in same state, sales tax generally applies

• Interstate Sales • Transaction involving multiple states, use tax

generally applies

Page 21Page 21Page 21

Type of Taxes

Page 22Page 22Page 22

Responsibility for Tax

• Seller• Fiduciary responsibility to collect and remit

tax legally due to state• Technically, not seller’s tax

• Buyer• Legally obligated to pay sales tax

Page 23Page 23Page 23

Responsibility for Tax

If the Seller is making a taxable sale in the state, they must charge tax or obtain the proper documentation to support a tax-free sale.

What is the proper documentation to be maintained by the seller?

Page 24Page 24Page 24

Responsibility for Tax

• Resale and Exemption Certificates• States differ on what is acceptable• Generally, must have the following to be valid

• Name and address of Purchaser• Purchaser’s Retail Permit Number• Purchaser’s Statement

• Reseller of item purchased• Items are purchased for resale

• Signature of Purchaser

Page 25Page 25Page 25

Responsibility for Tax

• Multi-state Tax Commission• Created Uniform Sales and Use Tax Certificate

• For use in Multiple Jurisdictions• 37 states and the District of Columbia accept

the Multijurisdictional Resale Certificate• Each retailer is responsible for determining

the validity of a purchaser’s claim for exemption

Page 26Page 26Page 26

Responsibility for TaxMultijurisdictional: Uniform Sales and Use Tax Certificate

Page 27Page 27Page 27

Responsibility for Tax

• Good Faith Acceptance of Resale Certificates• Latitude for taxpayers

• May use as a defense• However, Seller must ask questions!

• Seller with actual knowledge that Purchaser is unlikely to resell MUST ask questions to ascertain facts to support Resale Certificate

Page 28Page 28Page 28

Responsibility for Tax

• Retailers • Fiduciary duty to collect and remit tax

• Must register with state, timely collect, self-assess and remit tax

• Proper documentation• Invoices, purchase orders, contracts, bills

of lading, credit and bad debt write-offs, past returns, exemption and resale certificates

Page 29Page 29Page 29

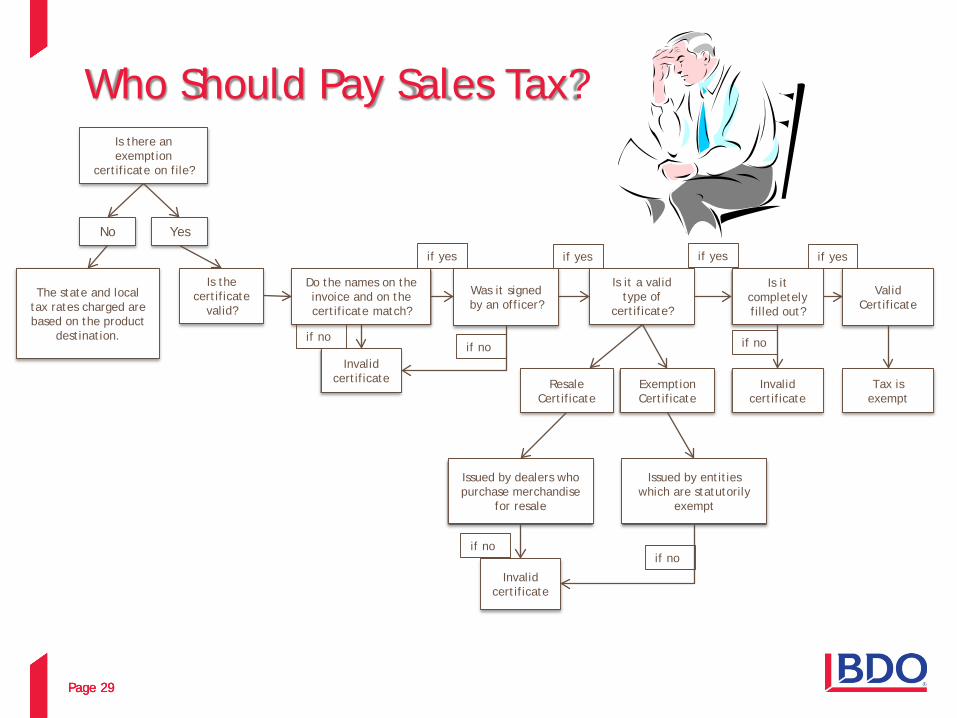

Who Should Pay Sales Tax?Is there an exemption

certificate on file?

No Yes

The state and local tax rates charged are based on the product

destination.

Is the certificate

valid?

Do the names on the invoice and on the certificate match?

Was it signed by an officer?

Is it a valid type of

certificate?

Is it completely filled out?

Valid Certificate

Invalid certificate Resale

CertificateExemption Certificate

Invalid certificate

Tax is exempt

Issued by dealers who purchase merchandise

for resale

Issued by entities which are statutorily

exempt

Invalid certificate

if yes if yes if yes if yes

if noif no if no

if noif no

Page 30Page 30Page 30

Imposition of Tax

• Sale• Transaction resulting in passage of title or

possession or both of tangible personal property from the seller to buyer, or which results in the provision of a service, in exchange for consideration

Page 31Page 31Page 31

Imposition of Tax

• Service• Task performed by one person for another – can be

professional or personal• Generally exempt unless specifically designated as

taxable

Page 32Page 32Page 32

Imposition of Tax• Tangible Personal Property (“TPP”)

• Property, other than real property, that can be • Held• Smelled• Touched• Seen • Tasted• Otherwise perceptible to the human senses

• Typically subject to tax unless specifically exempted or excluded by statute

Page 33Page 33Page 33

Imposition of Tax

• Lease of Tangible Personal Property• Taxability of leases may vary

• Type of lease: Operational, Capital or Financing• State’s definition of Taxable Lease• Tax Base of Lease• Lease Period• Bargain Purchase Options• Right to Ownership at End of Lease Term

Page 34Page 34Page 34

Imposition of Tax

• Lease of Tangible Personal Property with Operator• Depends on whether the lessee has possession or

control over the tangible personal property• For tax to be due, the lessee must have possession

or use of the tangible personal property• Person must legally be able to exercise dominion

over the property

Page 35Page 35Page 35

Why didn’t that vendor charge tax?

Page 36Page 36Page 36

Nexus

• Vendor didn’t charge tax because vendor may not have nexus

• DO NOT ADD TAX TO INVOICE• Vendor likely has no way to remit that tax to

the State• Adding tax to invoice will not hold up under

audit

Page 37Page 37Page 37

Nexus

• Nexus is defined as the minimum contact an entity must have in order for a state to impose a tax.

• Nexus requires sufficient contact between the state and the business it wants to tax.

• Nexus standards vary depending on the type of tax involved, therefore it is possible to have nexus for one tax and not another.

Quill Corp. v. N.D., 504 U.S. 298 (1992).

Page 38Page 38Page 38

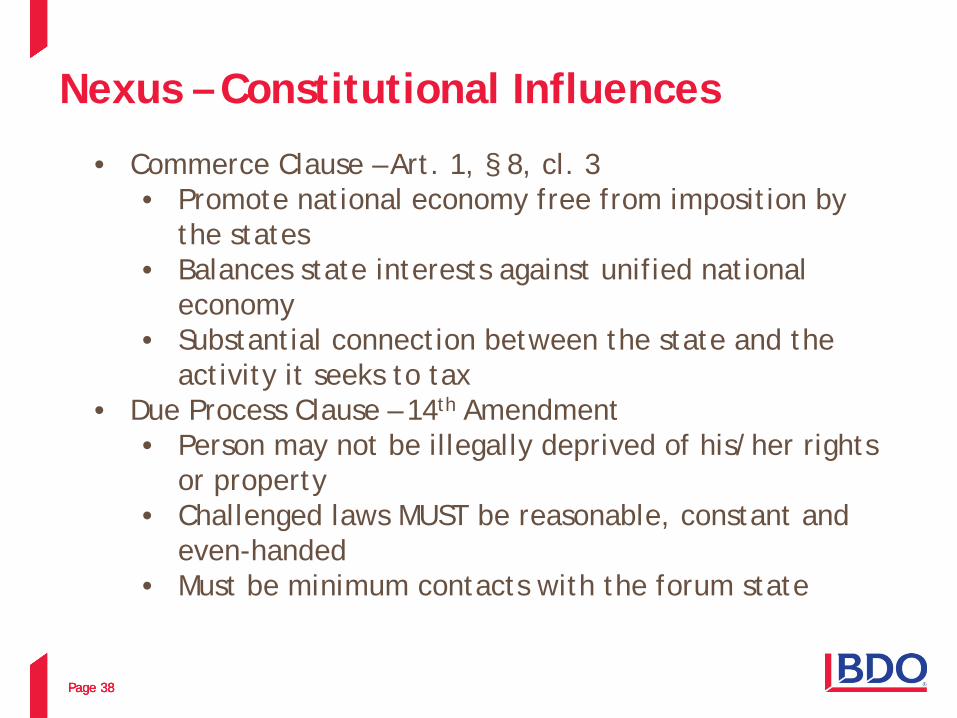

Nexus – Constitutional Influences

• Commerce Clause – Art. 1, § 8, cl. 3• Promote national economy free from imposition by

the states• Balances state interests against unified national

economy• Substantial connection between the state and the

activity it seeks to tax• Due Process Clause – 14th Amendment

• Person may not be illegally deprived of his/her rights or property

• Challenged laws MUST be reasonable, constant and even-handed

• Must be minimum contacts with the forum state

Page 39Page 39Page 39

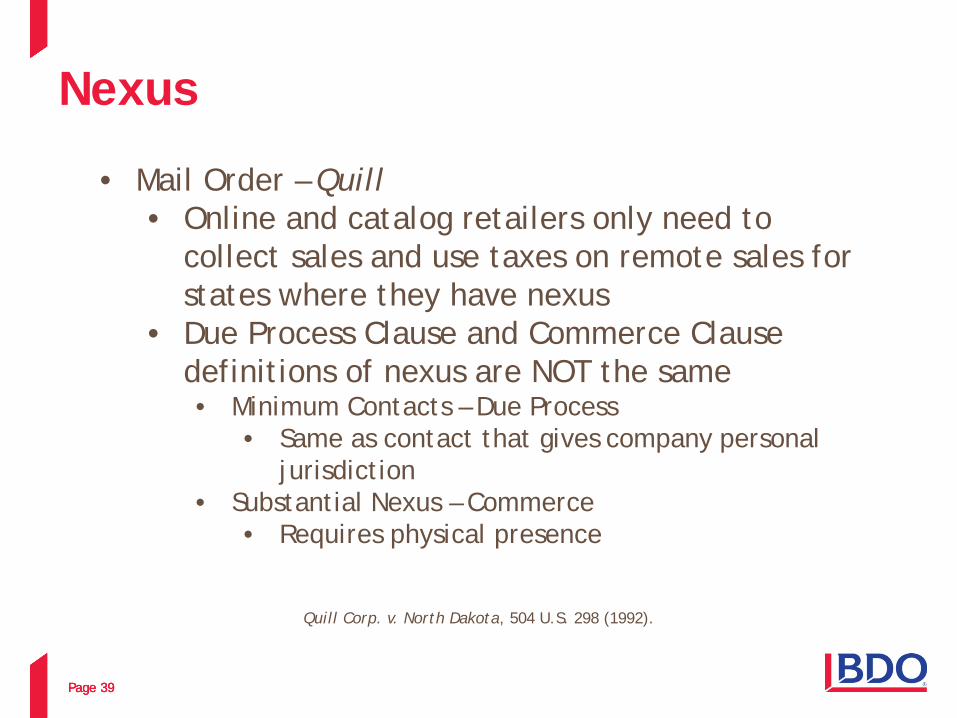

Nexus

• Mail Order – Quill• Online and catalog retailers only need to

collect sales and use taxes on remote sales for states where they have nexus

• Due Process Clause and Commerce Clause definitions of nexus are NOT the same• Minimum Contacts – Due Process

• Same as contact that gives company personal jurisdiction

• Substantial Nexus – Commerce • Requires physical presence

Quill Corp. v. North Dakota, 504 U.S. 298 (1992).

Page 40Page 40Page 40

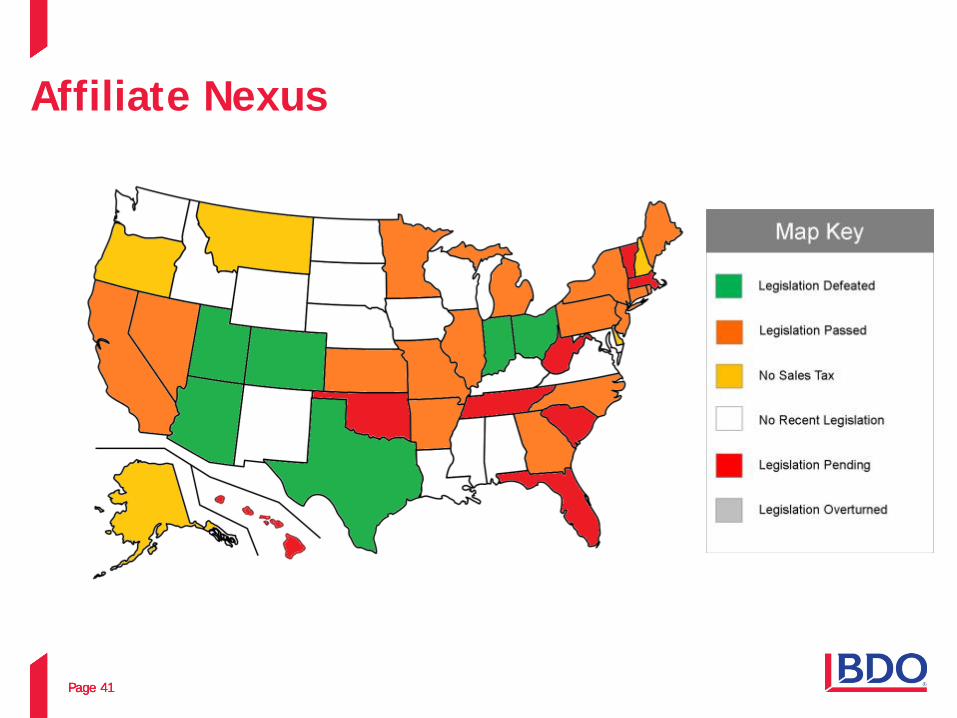

Nexus – Developments• Affiliate Nexus

• Applies generally to any out-of-state person, typically a vendor or subsidiary, under the control of a dealer or corporation

• Applies unitary approach to the entire group of companies

Page 41Page 41Page 41

Affiliate Nexus

Page 42Page 42Page 42

Why Out of State Auditors?

Page 43Page 43Page 43

Nexus Developments

• Click-Through Nexus• Originated in New York : Law enacted on April 23, 2008, that requires out-of-state

sellers to collect sales tax if they enter into an agreement with a NY resident for website referrals/links and pay a commission based on sales generated there from (i.e. click-thru nexus) N.Y. Tax Law § 1101(b)(8)(vi).• Presumption – A seller that makes taxable sales of TPP or services in a state has nexus when a

state resident’s website clicks through potential customers to the seller.• Rationale – Link on the website in New York creates a physical presence for the seller when

the owner of the website is a resident of New York and acts as a sales agent for the seller.

• Amazon and Overstock.com challenged the constitutionality of NY’s vendor nexus law.• Does not violate the U.S. Constitution: Overstock.com, Inc. v. New York State Department of

Taxation and Finance, New York State Court of Appeals, Nos. 33 and 34, March 28, 2013.• Court reasoned that following the Quill case, physical presence in the state itself does not

need to be substantial, but must be more than a “slightest presence” that solicitation in a state that produces a significant amount of revenue qualifies as more than a “slightest presence” in the state.

Page 44Page 44Page 44

The Marketplace Fairness Act

• Proposed legislation in the United State Congress that would enable state governments to collect sales taxes and use taxes from remote retailers with no physical presence in their state

• Legislative history• Bill was originally passed by the Senate in 2013, but never made it out of the House of

Representatives• The Act was introduced again in 2015, but is still in limbo

• Supported by a large number of people• 90 members of Congress (30 Senators and 67 Representatives)• 26 Governors (13 Republican, 12 Democrat, and 1 Independent)• 80 National Trade Associations• 122 State and Local Trade Associations

Page 45Page 45Page 45

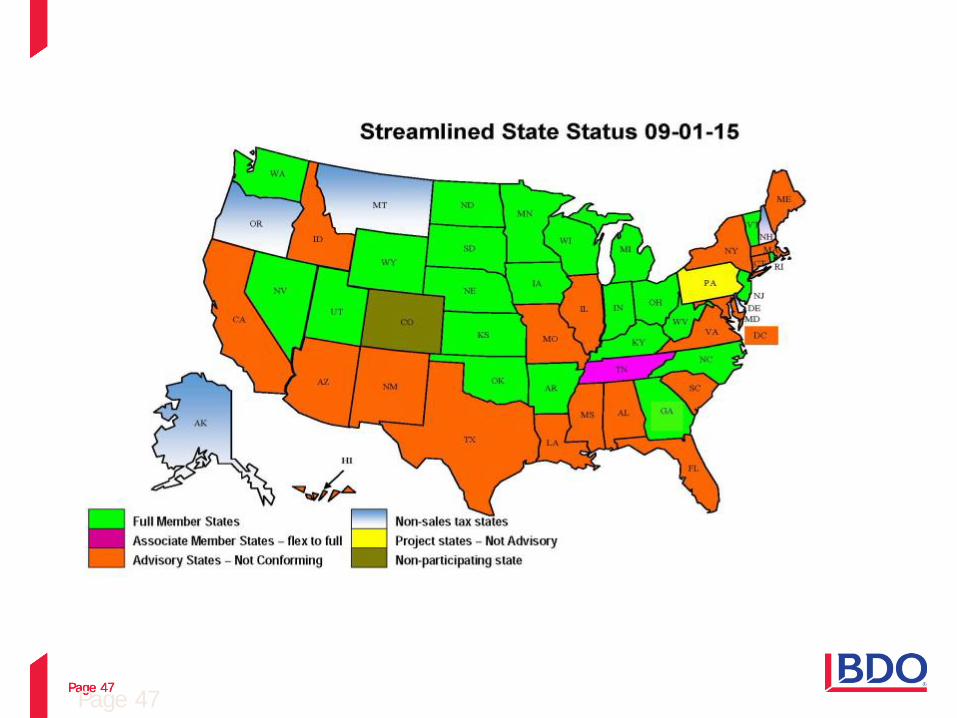

Streamlined Sales Tax

• 23 full member states

• Local tax sourced based on destination

• Texas is not a member, due to the fact they will not change their sourcing rules

Page 45

Page 46Page 46Page 46

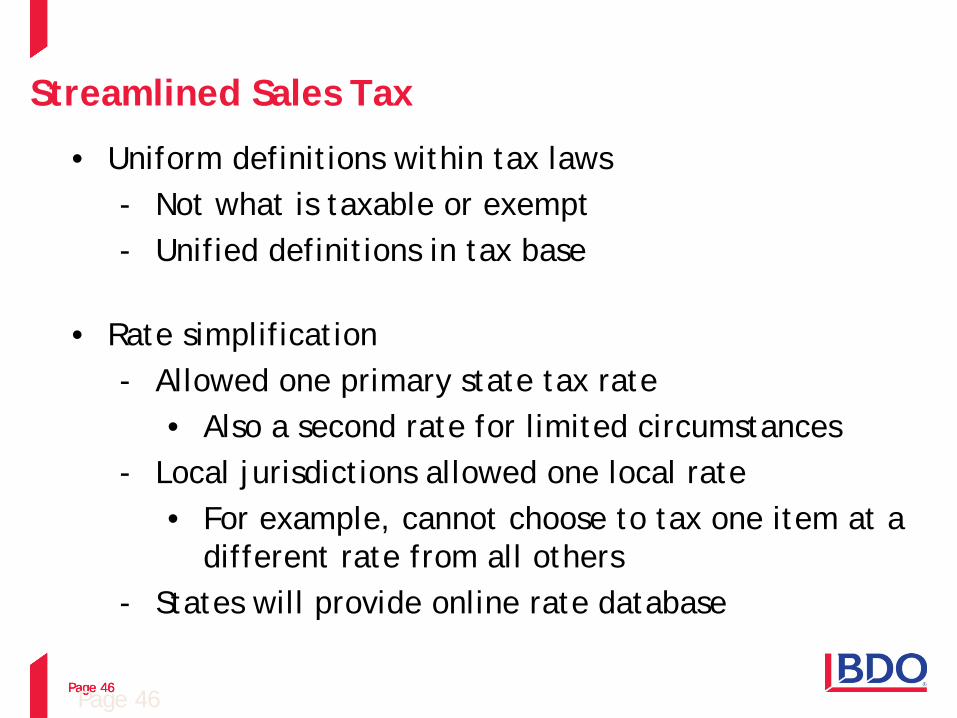

Streamlined Sales Tax

• Uniform definitions within tax laws- Not what is taxable or exempt- Unified definitions in tax base

• Rate simplification- Allowed one primary state tax rate

• Also a second rate for limited circumstances- Local jurisdictions allowed one local rate

• For example, cannot choose to tax one item at a different rate from all others

- States will provide online rate database

Page 46

Page 47Page 47Page 47Page 47

Page 48Page 48Page 48

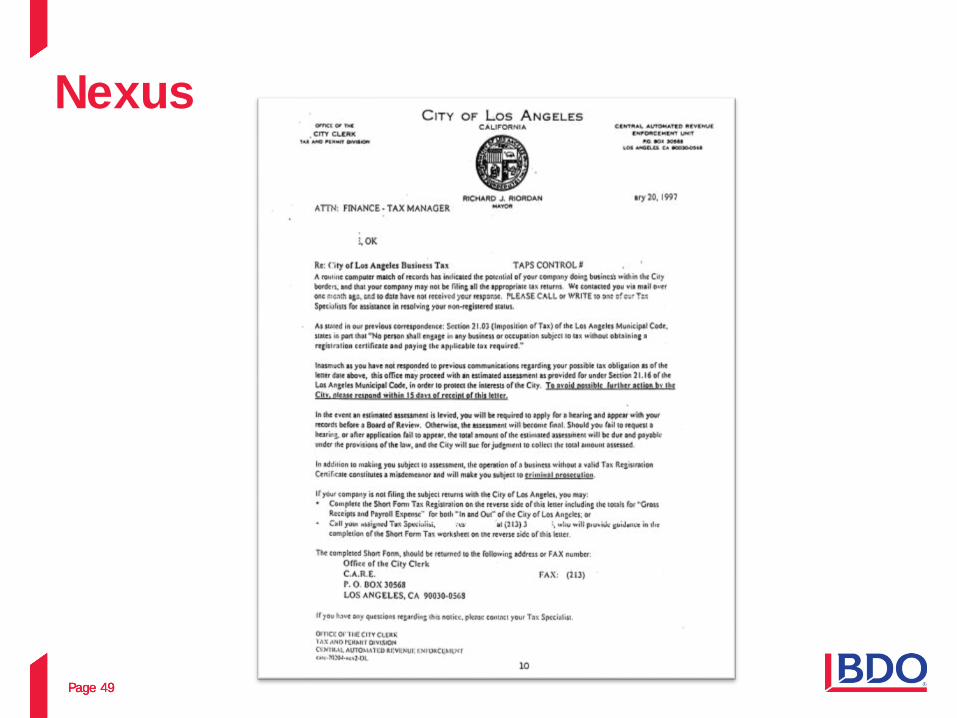

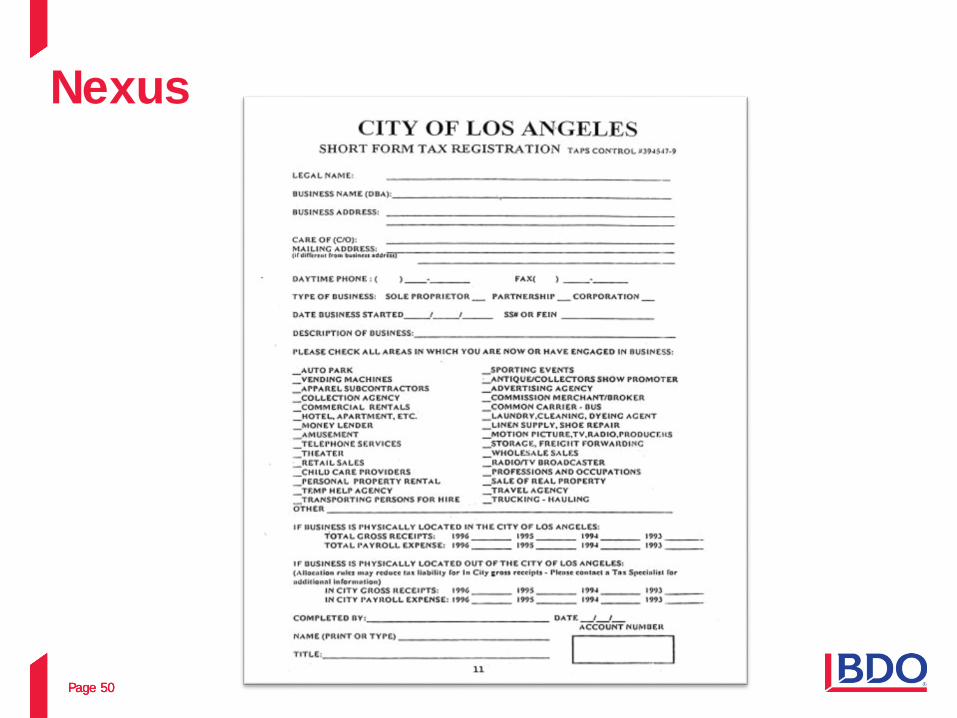

Nexus

• Nexus Questionnaire• “Nexus Units”

• Sole purpose is to find non-filers• Often send questionnaire

Page 49Page 49Page 49

Nexus

Page 50Page 50Page 50

Nexus

Page 51Page 51Page 51

Disregarded Entities

Disregarded entities are not disregarded for purposes of state property taxes and sales and use taxes.

They are subject to reporting, payment and penalty provisions at the entity level just like any other business entity. Thus, sales between disregarded entities and their owners, while disregarded for federal income tax purposes, can be subject to sales or use tax.

Page 51

Page 52Page 52Page 52

FAS 5 Considerations

•FAS 5 states that an estimated loss from a loss contingency shall be accrued by a charge to income if both of the following conditions are met:

- Information indicates that it is probable that an asset had been impaired or a liability had been incurred at the date of the financial statements; and,

- The amount of loss can be reasonably estimated.

- Accrue the best estimate in a range or lowest amount in the range.

Page 52

Page 53Page 53Page 53

Stre

ngth

When a loss contingency exists, the likelihood that the future event or events will confirm the loss or impairment of an asset or the incurrence of a liability can range from probable to remote.

• Probable - The future event or events are likely to occur

• Reasonably Possible - The chance of the future event or events occurring is more than remote but less than likely

• Remote - The chance of the future event or events occurring is slight

FAS 5 Reserve: Definitions

Page 53

Page 54Page 54Page 54

Taxability

Page 55Page 55Page 55

Exemptions and Exclusions

• Exemption• Transaction that is within the general scope of

the statutes imposing tax, but is the subject of special provisions removing it from taxation

• Exclusion• Transaction that is outside the general scope

of the statutes imposing the sales and use tax• Real estate, stocks, bonds

• Amount that is not included in the measure of sales and use taxes• Freight, discounts, etc.

Institute for Professionals in Taxation, Sales Tax School I (Ga. 2013).

Page 56Page 56Page 56

Exemptions and Exclusions

University is purchasing polo shirts in bulk from a local vendor. The majority of these shirts are being

sold through the University’s bookstore. However, a small percentage of the shirts are being

given to the bookstore staff to wear as their uniforms on game days to promote school spirit.

Must the University pay sales tax or tax on any or all of the shirts?

Page 57Page 57Page 57

Exemptions and Exclusions

• “Status” Exemptions from Tax• Free from tax because purchaser is exempt

• Government agencies• Charitable organization• Not-for-profits• Educational institutions

• Sales made by these organizations are NOT generally exempt

Page 58Page 58Page 58

Exemptions and Exclusions

• “Transactional” Exemptions from Tax• Free from tax because item being purchased is

exempt• Focuses on what purchaser intends to do with

property or service purchased• Sales for resale• Material and component parts of finished

product• Manufacturing and processing machinery

and equipment

Page 59Page 59Page 59

Exemptions and Exclusions

• Service Exemption• Most states specifically enumerate taxable services

• If service is not enumerated, it is not taxable• Generally, service providers must pay tax when

purchasing property to be consumed while performing nontaxable service

• Several states have provision for providers to purchase services for resale

Page 60Page 60Page 60

Exemptions and Exclusions

Natural Foods Store purchases fruits and vegetables in bulk with a resale certificate. Natural Foods also

conducts cooking demonstrations for free for its customers.

During these demonstrations, Natural Foods employees remove fruits and vegetables from the store shelves and use them as ingredients in the

dishes.

Is there an issue here? If so, what is the issue and how is it remedied?

Page 61Page 61Page 61

Manufacturing Exemptions

• Raw material/resale• Materials acquired to be incorporated into

manufactured product• Machinery and equipment used in manufacturing

process• Direct use vs. integrated plant theory

• Exemption or resale certificates required• Exemption – used for purchasers made by an

exemption entity• Resale – used for purchases bought to be resold

Page 62Page 62Page 62

Manufacturing Exemptions

G.T. Manufacturing, LLC has a problem. G.T. purchases paint thinner for multiple uses within the manufacturing process, however, some uses are not

for manufacturing purposes. G.T. comes to you under the impression that because paint thinner is used to

thin paints, which become part of the finished product, all of their purchases of paint thinner are

exempt, regardless of use. G.T. has not been identifying the paint thinners use as it is consumed.

How would you advise them?

Page 63Page 63Page 63

Real Property Construction

• Generally, construction contractor is ultimate user or consumer of all materials purchased for use in project and incorporated into realty• Liable for tax to material vendor

• Type of construction contract matters• Custom building or speculative building• Materials are permanent or consumable• Contractor is prime or subcontractor• New construction or remodel• Lump sum or separately stated

Page 64Page 64Page 64

Computer Hardware,Software and Service Agreements

• Hardware – Taxable as TPP• Canned (prewritten) vs. Custom Software• Load and Leave vs. Electronic Download• Mandatory vs. Optional Agreements

Page 65Page 65Page 65

Computer Hardware,Software and Service Agreements

You recently expanded your practice into an area that your current software suite does not cover. After

much research, you have decided to purchase a new system from Virus, Inc. Virus is located in California

and will deliver the software to you via tangible media and electronic download. The tangible media

being delivered is completely custom and the electronically downloaded software is canned.

Do you owe tax on any of the software? If yes, which items?

Page 66Page 66Page 66

Bundled Transactions

• Retail sale of two or more product where products are otherwise distinct and identifiable, and the products are sold for one non-itemized price

• Typically subject to sales tax without any deduction for the value of the nontaxable products or service

• Predominant use

Page 67Page 67Page 67

Freight Charges

• Typically separately stated delivery charges are not taxable

• Typically delivery charges included in selling price of TPP are taxable

• Third Party Common Carriers• USPS, FedEx, UPS, etc.

• F.O.B. - Free on Board• Origin• Destination

Page 68Page 68Page 68

Drop Shipments

• A Third Party Sale involving the purchaser, the retailer, and the wholesale distributor• Purchaser submits a PO to a retailer, who then

submits its own PO to the wholesale distributor

• The retailer instructs the wholesale distributer to ship the purchased product directly to the purchaser – in effect “dropping” the shipment on behalf of the retailer

Page 69Page 69Page 69

Sales Tax Compliance

Page 70Page 70Page 70

Sales and Use Tax Research

• Case Law• Court of last resort that interprets or declares law

unconstitutional has highest authority • Statutes

• Highest authority of statutory law• Rules and Regulations

• State agency’s interpretation of statutes• Letter Rulings

• Written by taxing agency in response to requests for guidance

• Newsletter, Tax Advisories, News Releases, Other Publications

Page 71Page 71Page 71

Local Taxes

• Many states allow the imposition of sales and use tax by counties and cities parallel to the state sales and use tax

• Local tax rates may vary from jurisdiction to jurisdiction

• Items exempt from state tax are typically exempt from local tax

Page 72Page 72Page 72

Basic Compliance

• Tax Decision Matrix (TDM)• Tool that indicates taxability for multiple

products • Generally for several jurisdictions

• Can be integrates into billing system or use tax accrual system

• Should be updated periodically

Page 73Page 73Page 73

Basic Compliance

• Tax Decision Matrix (TDM)• Needs to be industry specific

• Healthcare• Energy• Manufacturing

• Needs to be a reference as to what supports the answer

• Different version for different users• AP should be on a single frame

• Color• Laminated• Does not need all the support

Page 74Page 74Page 74

Basic Compliance Example:

Page 75Page 75Page 75

Basic Compliance

• Tax Decision Matrix (TDM)• Different version for

different users• Decision Maker Copy

• Tabbed by state• All sources included• Three ring binder

Page 76Page 76Page 76

Basic Compliance

• Benefits of Training• Use of the matrix as part of training process

• After any training, questions always arise as to taxability of items

• Matrix may be used as part of training as a “cheat sheet”

Page 77Page 77Page 77

Basic Compliance

• Spreadsheets and Databases• Build simple database to help accrue tax

• Often occurs when AP staff is resistant to training

• Makes more sense to outsourced or do within tax department

• Tax decisions may be too complex

Page 78Page 78Page 78

Basic Compliance Example:

Page 79Page 79Page 79

Basic Compliance

• Using a Database• Trapped all of the AP data in a database• Sorted by Vendor in groups

• Always Taxable• Sometimes Taxable• New Vendors• Vendors issued a direct pay permit

• Allowed us to focus time on the vendors that required attention

• Allowed us to review approximately 10,000 invoices in less than 40 hours

Page 80Page 80Page 80

Basic Compliance

• Manual Accruals• If AP can handle the task…

• Most AP systems have an option to accrue tax within the AP screen

• Write a “hard line of accrual” into the tax payable account

• Pull out the questionable invoices for a decision maker to review• Use a spreadsheet• Use a database• Make copies or scans of invoices

Page 81Page 81Page 81

Sales Tax Automation

• Electronic Data Interchange• Electronic transmission of standard business

information between two companies in machine readable format

• Automated Accrual System• Automate taxability determinations and

eliminate errors that are often problem in manual systems

Page 82Page 82Page 82

Sales Tax Planning

• Single State v. Multistate • Do not be reactive, BE PROACTIVE• Identify key nexus triggers

• Employee living in a state• Sales person entering a state• Sales level or volume within a state

• Different types of taxes have different nexus requirements• Sales Tax v. Income Tax

Page 83Page 83Page 83

Sales Tax Planning

• Risk/Exposure• Quantify amount of what is present by failure

to take action• How much risk are you willing to take?• What is your threshold of pain?

• Once trigger occurs, next steps:• Certificate of Authority • Register for applicable taxes

Page 84Page 84Page 84

Requirements

• Registration• Must do if you have nexus

• Permits• Every state where you have nexus

• Sales and Use Permits• Reporting Requirements

• Monthly, quarterly, bi-annually, annually• Often depends on amount of tax remitted

to state

Page 85Page 85Page 85

Direct Pay Permits

• Allows purchasers to pay tax directly to state• Oil & gas companies• Healthcare• Some manufacturing companies• Allows use of TDM’s

Pros and Cons?

Page 86Page 86Page 86

Liability for Deficiency

Page 87Page 87Page 87

Audits and Assessments

• State and Local Audits • Audit Period

• Statute of Limitations• Generally 3-4 years• Waiver/Extension

What is the Audit Period if Company Never Registered for Sales and Use Tax

Permits?

Page 88Page 88Page 88

Audits and Assessments

• Records Retention• Records and books of all sales and all purchases of

TPP• Must maintain complete books and records covering

receipts from all sales and distinguishing taxable from nontaxable receipts

• Notice • Initial notification of audit from the State

• Confirmation Letter• Documents requested from auditor • Official audit period

Page 89Page 89Page 89

Audits and Assessments

• Big Issues in Audits• Transactions within a corporate group• Items brought in from out-of-state• Hardware/software maintenance• Contractor issues

Page 90Page 90Page 90

Audits and Assessments

Your audit is completed and you STRONGLY disagree with the assessment against your company.

Where do you go from here?

Page 91Page 91Page 91

Audits and Assessments

• Taxpayer Relief• Usually will write a timely “petition for review”

or submit a similar request• Typically a conference is scheduled if requested

by the taxpayer or deemed necessary by the state

• Appeal to an outside court

Page 92Page 92Page 92

Sampling Techniques

There are seven basic steps involved in an audit:1. Determine the objectives of the test2. Define the deviation conditions3. Define the population4. Determine the method of sample selection5. Determine the sample size6. Perform the sampling plan7. Evaluate the sample results

Page 93Page 93Page 93

Sampling Techniques

• Sampling Methods• Random Sampling• Systematic Sampling• Block or Cluster Sampling• Judgmental• Stratified

• Sample Evaluation• Variance• Ratio Analysis• Mean Estimation

Page 94Page 94Page 94

Liability Issues

• Common Issues Resulting from Audits• Successor Liability

• Any person who directly or indirectly purchases, acquires, or succeeds to the business or the stock of goods of any person quitting, selling, or otherwise disposing of a business or stock of goods.

• Officer and Director Liability• Any person required to collect sales tax as a trustee

for the state will be held personally liable for the sales tax due. In the case of a corporation each "principal" officer will be held personally liable for the sales tax due.

Page 95Page 95Page 95

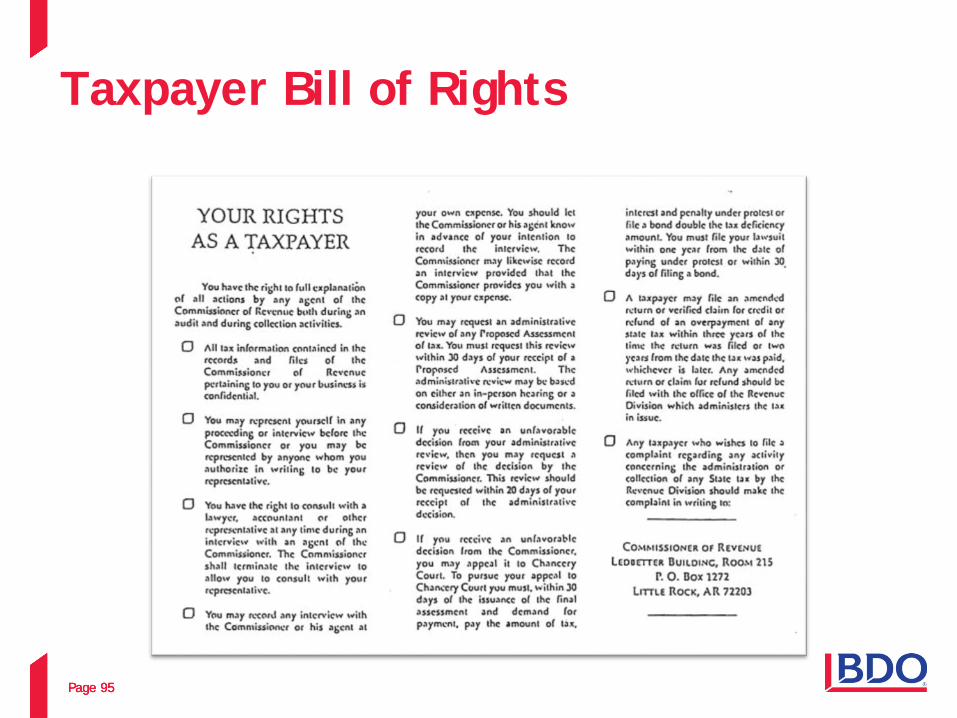

Taxpayer Bill of Rights

Page 96Page 96Page 96

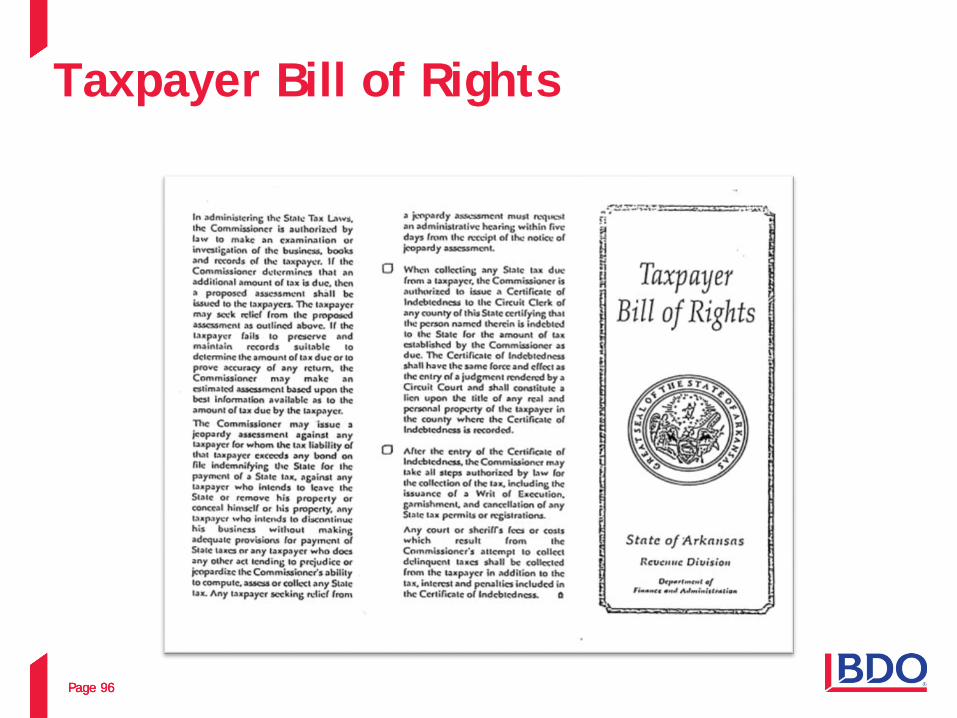

Taxpayer Bill of Rights

Page 97Page 97Page 97

Voluntary Disclosure Agreements

• Contract between Taxpayer and State • Taxpayer makes Voluntary Disclosure through

Third Party• State may waive penalty and/or interest• Usually initiated when deficiency is discovered• Cannot be made if Taxpayer is under audit

Pros and Cons?

Page 98Page 98Page 98

What happens when you have overpaid tax?

Is it lost forever?

Page 99Page 99Page 99

Reverse Audits (Refunds)

• Recovering tax that was not legally due• Statute of Limitations – Generally 3-4 years

• The State must grant or deny all petitions for refund within a certain amount of time from the date of submission (generally the deadline can be extended)

Page 100Page 100Page 100

Reverse Audits (Refunds)

• Reverse Audit Techniques• Gather Documentation

• Invoices• Proof of Payment• Use Tax Accruals• Correspondence with State• Correspondence with Vendors

• Review Documentation• Purchase Transactions • Corporate Structure • Audit History

Page 101Page 101Page 101

Reverse Audits (Refunds)

• Reverse Audit Techniques• Determine Taxability

• Overpayments• Exposure

• Data Entry• Access or Excel Spreadsheet

• Submit to State• Correspondence• Citations (justification for refund)• Refund Schedule• Invoices• Supporting Documentation

Page 102Page 102Page 102

Reverse Audits (Refunds)

• If refund is denied, the taxpayer can appeal the denial• Must be within a prescribed time from the

date of petition was denied• Typically refunds are appealed to an outside

court

Page 103Page 103Page 103

Reverse Audits (Refunds)

You have been making purchases or years from ABC, Corp. After completing an internal audit, you discovered that you paid sales tax on certain

purchases that was not legally due. You file for a refund with the state, only to learn that ABC, Corp. has not remitted your paid sales tax to the state.

What now?

Page 104Page 104Page 104

Advanced Topics

• Mergers, Acquisitions & Corporate Reorganizations• Intercompany Transactions• Bulk Sales• Occasional Sales

• Purchasing Cards• Simplification• Cost Reduction• Improved Efficiency

Page 105Page 105Page 105Client name - Event - Presentation titlePage 105Client name - Event - Presentation titlePage 105Client name - Event - Presentation titlePage 105

Participant Questions

Page 105

Page 106Page 106Page 106

Thank You!

Tom Smith, Partner

918-640-4306 (Mobile) 918-281-4081 (Fax)[email protected]

BDO8908 South Yale Avenue, Suite 450Tulsa, OK 74137-3557 UNITED STATES918-281-4080www.bdo.com

Stay Connected with BDO USA, LLP

Page 106

Page 107Page 107Page 107@BDO_USA_Tax

STATE AND LOCAL TAXATION –SALES AND USE TAXES

BDO Specialized Tax Services107

Relevant Issue: Companies don’t collect tax on the correct items or at the correct rate.

Planning Idea: Provide Taxability Studies on the products and services sold into the jurisdictions where the company has a reporting responsibility.

What is it: Taxability / Nexus Studies

Who needs it: Companies selling into multiple states or seeing growth outside their home state.

When do they need it:

What is the sales pitch: Sales taxes vary by state, have you researched your transactions to see if you charge tax properly.

Who is the buyer: CFO / Controller / VP Tax

Questions you might ask: Do your customers ever tell you your taxability on your invoices is incorrect?

How do you make certain your taxability is correct?

How do you update your tax rates in your invoicing system?

Do you file sales tax returns in all the jurisdictions where you have sales people traveling?

Do you expect to go through due diligence in the next couple years?

Page 108Page 108Page 108@BDO_USA_Tax

STATE AND LOCAL TAXATION –SALES AND USE TAX

BDO Specialized Tax Services108

Relevant Issue: Companies overpay sales tax all the time.

Planning Idea: Sales and use tax refund study.

What is it: We basically come in and review the companies transactions for overpayments of sales tax, if we find them we take the necessary steps to secure the refund with the states.

Who needs it: Manufacturing companies, for-profit hospitals, E&P Companies (in Texas).

When do they need it: Every three years at least.

What is the sales pitch: You don’t pay us unless we find you savings.

Who is the buyer: CFO / VP Tax / Controller

Questions you might ask: Has anyone ever looked to see if you are overpaying sales tax?

How confident are you in your accounts payable department to catch errors on sales tax?

Page 109Page 109Page 109@BDO_USA_Tax

STATE AND LOCAL TAXATION –SALES AND USE TAXES

BDO Specialized Tax Services109

Relevant Issue: Companies routinely get audited by the states.

Planning Idea: Provide audit management services.

What is it: We basically run the audit, handle all the questions from the auditor and help get records.

Who needs it:

When do they need it:

What is the sales pitch:

• We are former auditors, who better to deal with the state then someone from the state.

• Your staff is already stressed, how can they do their job and deal with an auditor.

• Auditors find a lot of information just hanging out at a company.

• Sometimes the best answer is “I don’t know, let me find out”.

Who is the buyer: CFO / Controller / VP Tax

Questions you might ask: • Do you have any sales tax audits going on?

• When was the last time you were audited? How did it go?