wwc india retail

TRANSCRIPT

8/8/2019 WWC India Retail

http://slidepdf.com/reader/full/wwc-india-retail 1/24

2007

World Winning Cities Series

Emerging City Winners Proles

8/8/2019 WWC India Retail

http://slidepdf.com/reader/full/wwc-india-retail 2/24

8/8/2019 WWC India Retail

http://slidepdf.com/reader/full/wwc-india-retail 3/24

The Geography of Opportunity

The “India 50”EXECUTIVE SUMMARY

India’s Retail AwakeningIndia’s retail sector is evolving at breakneck speed, uelled by a strong economy, avourable demographics, rising wealth levels, and

the rapidly changing liestyles and consumer aspirations o an ever growing middle class. Rarely a week goes by without major

announcements by retailers and property developers committing to aggressive programmes o retail expansion and shopping mall

development; or announcements about the arrival o new market entrants or the orging o new joint ventures with oreign retailers,

all eager to participate in an increasingly dynamic sector. India’s cities are witnessing a paradigm shi rom traditional orms o

retailing into a modern organised sector; a transormation that will no doubt accelerate over the coming decade. Te booming retail

sector is oering signicant new property opportunities, but also many challenges or a new market that is going through structural

change at an unprecedented rate.

Te demographic and economic statistics that underpin the growth o India’s retail sector are truly impressive, but in order to get

a realistic perspective on property opportunities, we need to comprehend how Indian consumer behaviour is changing; and to

understand how new retail geographies and retail ormats are likely to evolve in a country characterised by enormous cultural and

regional diversity. So to help uncover the potential o the Indian retail property market, Jones Lang LaSalle Meghraj has embarked on

a programme o in-depth research to better understand the current and uture landscape o retail property in India.

A New Geography o Opportunity t

Tis report is the rst in a series on India Retail Futures. It reviews in brie the drivers o India’s booming retail market, and how

both retailers and the property sector are responding to the massive changes in the Indian retail environment. Te report’s primary

ocus, however, is to explain and predict the emerging geography o Indian retail activity and property opportunities. Most organised

retailing and retail property activity is still overwhelmingly concentrated in India’s two largest metros – Delhi/NCR (National

Capital Region) and Mumbai. Whilst the report concludes that there are considerable property opportunities in these two vast

cities, increasing competition combined with the growing opportunities in India’s regional markets is encouraging both retailers and

property developers to move into new and potentially more rewarding markets urther a eld. Organised retailing in India’s other

main cities, such as Bangalore, Kolkata, Hyderabad, Pune and Chennai is growing rapidly, but such is the pace o change, that many

smaller third tier cities are now rmly on the radar screen o the retail sector and mall developers.

With around 50 cities o over one million population, many o which are still largely untapped, there are clearly substantial

opportunities or the retail property sector. Domestic retailers and shopping mall developers are moving aggressively into India’s

smaller cities in order to gain rst mover advantage, to capture growing consumer markets and to respond to the strong demand or

branded goods. Tere is clearly a signicant requirement rom both the retail sector and the property industry to know where India’s

next growth opportunities are likely to be concentrated. W i n n i n g C i t i e s : I N D I A R E T A I L

8/8/2019 WWC India Retail

http://slidepdf.com/reader/full/wwc-india-retail 4/24

INDIAN OCEAN

JAMMU AND KASHMIR

HIMACHAL

PRADESH

UTTRAKHANDPUNJAB

HARYANA

RAJASTHAN UTTAR PRADESH

MADHYA PRADESHGUJARAT

MAHARASHTRA

Arabian Sea

CHHATTISGARH

ORISSA

JHARKHAND

BIHAR

MEGHALAYA

MANIPUR

NAGALAND

MIZORAMTRIPURA

Bay of Bengal

ASSAM

SIKKIM

ARUNACHA PRADESH

WEST BENGAL

ANDHRA

PRADESH

KARNATAKA

TAMIL NADU

KERALA

GOA

Pune

BengaluruChennai

Kochi

Hyderabad Vizag

Mangalore

Mysore

Coimbatore

Vijayawada

Madurai

Mumbai

KolkataVadodara

Surat

Nashik

Nagpur

Jamshedpur

Bhubaneshwar

Goa

Dhanbad AsansolBhopal

Jabalpur

Solapur

Kolhapur

Ahmedabad

Delhi

LudhianaChandigarh

Jaipur Lucknow

Amritsar

Agra

Kanpur

Indore

Allahabad

Meerut

PatnaVaranasi

GuwahatiJodhpur

Aurangabad

Srinagar

Panipat

India’s Emerging Retail Hierarchy

Maturing NCR/Delhi Mumbai

Transitional Bangalore Kolkata Hyderabad Chennai

Pune Ahmedabad

High Growth Chandigarh Ludhiana Jaipur Lucknow

Kochi Vadodara Surat

Emerging Indore Amritsar Jalandhar Mangalore

Nashik Bhubaneshwar Agra Vizag

Coimbatore Kanpur Nagpur Goa

Allahabad Mysore Jamshedpur Thiruvananthapuram

Nascent Jodhpur Patna Varanasi Meerut

Rajkot Aurangabad Bhopal Sonipat

Vijayawada Madurai Ranchi Guwahati

Jabalpur Asansol Dhanbad Panipat

Kolhapur Srinagar Solapur

The India 50

8/8/2019 WWC India Retail

http://slidepdf.com/reader/full/wwc-india-retail 5/24

8/8/2019 WWC India Retail

http://slidepdf.com/reader/full/wwc-india-retail 6/24

India’s Retail Hierarchy-Characteristics

No oCities

Typical MetroPop’n (Mills)

Shopping MallDevelopment

Since:

% o NationalOrganised

Retailing (by 2008)

Typical no oshopping malls

(by 2008)

Format Opportnities

Matring 2 20 1999 0% 50-150

Large Mixed Use Malls

Speciality & Luxury Brands

Big Box

Neighbourhood Malls

†

†

†

†

Transitional 6 5-16 200 2% 20-0

Large Mixed Use Malls

Speciality & Luxury Brands

Big Box

Neighbourhood Malls

†

†

†

†

High Growth 7 2.5 2006 11% 5-10

Mixed Use Malls

Large Department Stores

Branded StoresBig Box

†

†

†

†

Emerging 16 1.5 2007-09 1% 2-5

Mixed Use Malls

Department Stores

Branded Stores

†

†

†

Nascent

19 < 1.5 2010 % 1-2

First Mover Advantage

100k + Shopping Malls

Supermarkets/Hypermarkets

†

†

†

Source: Jones Lang LaSalle Meghraj Research

The Future: Promises and ProblemsTis report shows that the Indian retail market oers signicant opportunities or domestic and international retailers and property

developers/investors across a broad range o geographies and ormats. Rapidly changing consumer behaviour, new market entrants

and changing government policy will urther transorm the sector, and open up yet more opportunities. Te organised retail sector is

developing at breathtaking speed, and the insatiable demand or modern retail is ar outpacing supply. Te market has entered a very

exciting phase o evolution, but undoubtedly there will be losers as well as winners…

In the rush to expand retail ormats and build new malls, many retailers and developers have lacked strategic vision, and in a

booming market they have oen lost sight o the “end game”. Tere is also a huge amount o market hype, and a widening gap

between developers’ claims and what is actually happening on the ground. Te reality will be that many planned retail schemes will

not get built, and most o those that do eventually become operational will all well below international standards. As more choice

becomes available or the Indian consumer, many malls and retail concepts will ail the test o time.

Yet this “shake-out” will provide even greater opportunities or an elite group o visionary developers, owners and retailers who have

the scalability, the teams, the processes and the logistics required to ourish in this rapidly growing retail environment. Tey will

go on to set new benchmarks, not only or India, but or the world. Subsequent reports in the Jones Lang LaSalle Meghraj series on

India Retail Futures will assess the ormulae or success in terms o retail ormats and asset management. Te Indian retail market is

ull o promise, but it is not or the aint hearted and success requires a deep understanding and knowledge o the Indian consumers

and their likely retail requirements.

8/8/2019 WWC India Retail

http://slidepdf.com/reader/full/wwc-india-retail 7/24

India Retail in

Brief The 21st Century Landscape:A Masterpiece o ModernisationRetailing is emerging as one o India’s most dynamic and ast

paced sectors. Te drivers o its upward growth trajectory hardly

need rehearsing, but they nonetheless help to explain why the

Indian retail market is seen by both domestic and international

retailers, as well as the property industry, as one o the globe’s

greatest untapped market:

Favourable Demographics – wo-thirds o India’s . billion

population is below 35. Te country’s median age is 24 years,comparing avourably with China where the median age is 33

years. India is home to 20% o the global population under

25 years. We are seeing a tidal wave o young adults entering

India’s consumer society with rising aspirations, new liestyle

requirements and an insatiable demand or consumer brands.

Rapid Urbanisation – Te country is urbanising at a rapid

rate, with almost 50 cities over one million population. India’s

“mega-cities” – Mumbai and Delhi – will be the world’s 2nd and

3rd largest cities by 205, providing massive concentrations o

retailing potential.

India’s Economy is Booming - Economic growth, currently

at circa 9% is supported by a rapidly expanding I/IES

sector, a deepening corporate base, growing FDI, economic

diversication and policy liberalisation. Most orecasters expect

7-9% annual growth over the next ve years, uelling strong

growth in consumer demand.

Growing Middle Classes – Estimates o the size o India’s

emerging middle classes vary enormously, but there is little

doubt that the numbers are large. Currently 70 million + earn

over $8,000 a year, a number that is expected to double by

20. We are also seeing the ascendancy o the “super rich”,with .6 million households bringing home over $00,000. Te

propensity o the middle classes to consume is rising, oiled

by easier availability o credit, income growth o around 5%

per annum, and a notable shi rom a “saving” to “spending”

mindset.

Te Emergence o Organised Retailing – A widely quoted

act is that 97% o retailing is still concentrated in traditional

neighbourhood “mom and pop” stores. In ew other countries

around the world is organised retailing so small. But India’s

cities are witnessing a paradigm shi rom traditional orms o

retailing into a modern organised sector requiring international

standard retail ormats, providing massive opportunities or the

property market. Tis pace o change will accelerate over the

coming decade.

India’s Vanguard ConsumersTe demographic and economic acts widely quoted are

undoubtedly impressive, but in order to assess the true nature

o property opportunities, we need to better understand the

deep and widespread transormation that is occurring in Indian

consumer behaviour due to changing liestyles, rising aspirations

and the emergence o a dynamic youth culture.

Working with Sociovision2

, experts in social change, Jones LangLaSalle Meghraj has looked at the changes in Indian society,

their impacts on consumerism and how this is eeding through

to shopping behaviour and property demand. Te research has

ocused on the emerging youthul, urban and relatively afuent

Vanguard Class that is the driving orce behind consumer

spending, new business activity, high-technology and workspace

innovations. Tis group includes circa 20 million people and

continues to expand. Hal o them are under 25 years, and most

have excellent education. Within the vanguard class, there

are couple o leading edge segments that are exerting a major

inuence on shopping behaviour:

Resourceul Young Women – Te growth in the emale

workorce has resulted in the emergence o “Resourceul Young

Women”, a group that are at the oreront o new India mores.

Tey are young, literate and resourceul; they place a heavy

emphasis on their careers and they have a very sel oriented

motivation or spending. Resourceul Young Women have a

signicant inuence on Indian retailing – and 46% o them see

shopping as a source o pleasure (compared to 36% globally).

For this inuential group, mall shopping is about “experience

and pleasure”, and not just about cost eciencies.

Young Urban Managers are the vibrant backbone o the Indianeconomy. Tey are highly entrepreneurial, hard working, money

ocused and are keen networkers. Teir shopping habits are

driven by a quest or status and economic advancement. With

their busy careers and limited leisure time, their shopping needs

are highly inuenced by accessibility and convenience. Te

demand or home delivery, particularly or convenience goods,

is very strong amongst this group.

2 See www.sociovision.com

8/8/2019 WWC India Retail

http://slidepdf.com/reader/full/wwc-india-retail 8/24

8/8/2019 WWC India Retail

http://slidepdf.com/reader/full/wwc-india-retail 9/24

Among the vanguard class, our research identies our dierent

mindsets described below, which are o prime interest or the

retail sector. Retailers and developers need create shopping

experiences that appeal to these groups:

Golden Boys and Girls – are young, university educated andurbanised. Mumbai and New Delhi are their avoured cities.

Tey are thirsty or new consumer goods and designer brands,

especially I products and services. Tey are the prime target

or international retailers, but interestingly they still have one

oot deeply implanted in traditional Indian amily values. Tis

group will increasingly avour “hybrid” retail concepts that oer

the best o Western models, but also strongly reect their Indian

cultures.

Cosmopolitans – are less “show o” than the Golden Boys

and Girls. Tey incarnate the values o globe-trotting travel

and proessional mobility. Tey are early adopters o newtechnologies and buy into global brands. Bangalore is the natural

home o the “Cosmopolitans” and because o its cosmopolitan

demographics is requently used as a test market or new retail

concepts.

Reactives – are older managers, who are modern and keen to

break away rom rigid hierarchies and social boundaries. Tey

seek new skills, knowledge and proessional success. However,

they are less at ease with change in Indian society. Kolkata is a

city in which the “Reactives” nd their place.

Peaceul India – or this group consumption is linked to

aesthetics and renement. Tey are modern in their openness

to gender equality and quest or reconciliation. Chennai is an

attractive place to live or the “Peaceul India”

Seven Drivers o ConsumptionOur research identies seven drivers o consumption, which are

important components o spending and retailing activity:

Trill Pleasures – Tere is a strong desire in Indian society or

emotionally rewarding experiences. Mall shopping in India is

currently viewed as an “experience”, a leisure pursuit and a orm

o entertainment, which has encouraged huge ootalls in new

shopping malls. However, the challenge or many mall retailers

and owners is converting the Indian “window shopper” rom

browser to purchaser. Complexes that oer other entertainment

opportunities, such as multiplexes, are avoured by consumers.

Indians are avid cinema-goers, reecting their thirst or evasion,

romance and new orms o vicarious consumption.

Fusion Fever - Whilst the Indian middle classes are attracted

to global brands, they are still committed to their traditions

and culture. We are seeing a usion o modernity and tradition,

and the hybridization o Indian and “western” cultures, re-

enorced by the strong “Indian Brand”. Tis hybridization willincreasingly translate into new retail concepts.

Aesthetics - Indian society has a deep sense o aesthetics,

and home aesthetics are especially top o the mind to India’s

vanguard class. Home urnishings are central to the concept o

a good quality o lie, and retailers catering or this segment will

see strong growth.

Novelty – Te thirst or novelty is a undamental characteristic

o the “New India”, which is not just conned to the young.

Te taste or novelty is also driven by the need or learningand advancement through education. Te current novelty

value o shopping malls is high, but over time this will wane as

choice increases, and Indian shoppers will become much more

discriminatory over their choice o venue.

echnology - A taste or technology is a dening characteristic

o Indian socio-cultural prole. Tis translates into strong

interest in internet retailing which is increasingly popular,

particularly or electronics and advanced consumer durables.

An interesting dynamic is emerging in India, whereby

internet retailing is evolving in tandem with modern store-

based retailing. Tis will raise the demand or concept stores,exhibition space and promotion zones within shopping malls.

Network Culture - Indian society has become increasingly

network based, and there is a strong urge to communicate,

interact and extend one’s mobility. Increasingly, malls are a ocal

point or interaction and social exchange.

Advertising – tops the global rank in terms o society’s

attraction to advertising and “inotainment” as a source o

inuence and inormation. Indian advertising is known or its

creativity and boldness.

India – Drivers o ConsumptionThrill Seeking

A desire or “thrill pleasures” and emotionally rewardingexperiences

†

Fsion Fever

Hybridization o Indian and “Western” cultures†

Aesthetics

Quest or aesthetics, especially home aesthetics†

InnovationTaste or novelty driven by need or learning†

Technology

Taste or technology is a dening eature o the Indiansocio-cultural prole

†

Network Cltre

New IT and communications interacting with a morefexible social abric

†

Stats

Quest or status is a key driver o the current consumer

boom

†

Source: Sociovision

W i n n i n g C i t i e s : I N D I A R E T A I L

9

8/8/2019 WWC India Retail

http://slidepdf.com/reader/full/wwc-india-retail 10/24

Deep Diversity, ExtremeExpectationsIndia is a vast and complex society – its huge population is

highly diverse in terms o language, customs, ethnicity, habitat

and way o lie. Even between India’s major cities there are

notable dierences in consumer behaviour. Mumbai, Delhi

and Bangalore with their money-making ethic are home to

many o India’s “Golden Boys and Girls”; whilst the older more

sophisticated “Cosmopolitans” are attracted to these cities’

global orientation. Kolkata is a city in which the “Reactives” are

prevalent– its balance and cultural richness is valued by this

group. Chennai with its balance between modern and traditional

is an attractive place to live or both the “Reactives” and the

“Peaceul India” groups.

Tere are also notable dierences in consumer habits,

preerences and loyalties by region. For example a number

o smaller northern Indian cities, such as Chandigarh and

Ludhiana, have developed relatively sophisticated consumer

markets and brand awareness, due to their high NRI (Non

Resident Indians) populations. In contrast consumers across

most o southern India continue to have relatively low exposure

to organised retailing.

Such regional diversity places an additional layer o challenges

or retailers and property developers that are seeking to create

pan-Indian operations. No single retail ormat is appropriate

or the whole o India, and ormats need to be adapted or local

requirements. Market knowledge o local tastes is absolutely

essential.

From Fragmentation to Unication:All in a Decade?Te rise o organised retailing – raditional neighbourhood

retailers have historically dominated the Indian retail

environment. Tis is now changing rapidly, with organised

retailing growing by around 30%3 per year. Sales growth o

leading domestic retailers o 50-00% per year suggests that the

market is on target to beat market predictions that organisedretailing will account or nearly 0% o total sales by 2003.

Existing domestic retailers are consolidating and expanding

– Te main retail players, that have traditionally been regional-

specic, are evolving into pan-India operations. Te rise o large

domestic players such as Pantaloon/Big Bazaar, Shoppers Stop

Group, RPG and rent/Westside are a key eature o today’s

market. All have very ambitious programmes o expansion

across the sub-continent, and are building up their management

expertise to support this growth.

New domestic entrants will be the companies to watch

– Existing retailers are being joined by numerous new marketentrants who are seeking a slice o India’s lucrative retail

business. Notably, several o India’s largest corporate houses,

such as Reliance, Bharti and the Aditya Birla Group are moving

3 KSA echnopak, 2005

into retail in a big way. Reliance Retail have a very aggressive

expansion programme and is reported to be planning to invest

nearly $6 billion in 5,000 shops across India, with annual sales

o $25 billion by 200. Also in late 2006, Bharti enterprises

announced its tie-up with Wal-Mart to roll out branded

stores across India. Both Reliance Retail and Bharti-Wal-Mart

will be the companies to watch – they are set to dominate

organised retail and could well become global operations. Teir

understanding o Indian consumers, their impressive track

record in business and their deep pockets places them in a

strong position vis-à-vis existing players.

RELIANCE – A Major Force in Retailing

Reliance, one o India’s largest corporate houses,

headed by Mukesh Ambani, has an aggressiveexpansion programme and is reported to be

planning to invest nearly $6 billion in 5,000 shops

across India. It is poised to become India’s

largest retailer, with aims o achieving annual

sales o $25 billion by 2010.

Reliance Retail opened their rst

“Reliance Fresh” stores in Hyderabad in late

2006 attracting considerable global attention.They are now rolling out stores at a rapid pace

across India through both organic expansion and

acquisitions o existing retailers. The company

also expect to debut their speciality stores and

hypermarkets during 2007. Reliance is also

ocusing on supply chain management –

“the arm to ork” logistics chain – with the aim

o strengthening its procurement and

supply chain networks.

Foreign retailers are slowly moving in – Foreign retailers are

still restricted rom ully participating in the retail boom. Partial

FDI relaxations in 2006 (allowing 5% investment in “single

brands”) are now enabling premium brands (such as Chanel,

LVMH, Gucci and Zegna) and mass brands (e.g. Starbucks) to

enter the market. While there is considerable pressure to allow

00% FDI, the local lobby to retain restrictions is strong, and

urther deregulation is likely to be slow and piecemeal. Tis is

providing a short term window o opportunity or domestic

players to embed and expand their operations.

8/8/2019 WWC India Retail

http://slidepdf.com/reader/full/wwc-india-retail 11/24

Nonetheless, several international retailers are already

operational through dierent routes:

Franchises – e.g. M&S, Pizza Hut, McDonalds and Nike are

already operational.

Wholesaling – Metro (Germany) and Shop Rite (South Arica)

are already operational through the wholesale “cash and carry”

route (where 00% FDI allowed).

100% FDI in manufacturing – e.g. LG Electronics and Levis are

permitted to sell directly.

However, the attractions o India retailing are so strong, that

despite restrictions, many international retailers are seeking

market entry through JVs with local players, and are stepping

up sourcing operations. Companies such as esco and IKEA are

all targeting the market and exploring business opportunities.

Te eventual arrival o major international retailers will create amuch more competitive environment or retailers, and through

knowledge transer will lead to greater eciencies and the

introduction o higher international standards.

The Property Response –Accepting a Steep Learning CurveShopping mall development - reality vs hype? Since the

completion o India’s rst mall in 999, India has seen the steady

migration o retailing rom traditional ormats into retail malls.

As recently as 2002 there was barely one million sq o space in

only a handul o shopping malls. By the close o 2006, this hadrisen to around 90 malls totalling 9 million sq across seven

cities4.

Based on domestic developers’ intentions, the stock could more

than double to over 40 million sq by the end o 2007 and

to up to 60 million sq by 2008. However, there is a

widening gap between developers’ claims and

what is actually happening on the ground,

and we estimate that the end 2007 stock

could be between 5-25% below

“ocial” developer estimates.

Even i all the space iscompleted on time, in

per capita terms stock

levels by 2008

will still be

signicantly

below all

main

4 Bangalore, Chennai, Delhi, Hyderabad, Mumbai, Kolkata and Pune.

property markets in Asia, Europe and North America. China,

or example currently has over 300 million sq o completed

shopping malls.

Indian Shopping Mall Development

7 cities: NCR, Mumbai, Bangalore, Kolkata, Hyderabad, Pune and ChennaiSource: Jones Lang LaSalle Meghraj Research

Emergence o a new breed o pan Indian developers – Te

retail development market has so ar been highly ragmented,

with each region dominated by a dierent set o local

developers. Most local developers have lacked both expertise

and strategic vision, which has consequently compromised on

the quality o malls that are being built. However, the recent

and planned activities o leading developers such as DLF,

Emaar-MGF, Unitech, Prestige Group and Raheja points to

2000 2001 2002 200 200 2005 2006 2007 2008

60,000

70,000

50,000

0,000

0,000

20,000

10,000

0

‘000 sq t

W i n n i n g C i t i e s : I N D I A R E T A I L

11

8/8/2019 WWC India Retail

http://slidepdf.com/reader/full/wwc-india-retail 12/24

8/8/2019 WWC India Retail

http://slidepdf.com/reader/full/wwc-india-retail 13/24

the emergence o a select group pan-Indian developers with a

strategic vision and ambitious national expansion plans; that

are raising capital using various methods including domestic

and oreign public listings and private equity; diversiying their

ormats and gaining the necessary management expertise. For

example, DLF, which is planning listing in 2007 is aggressively

targeting national growth, with the reported aim o developing

up to 00 malls across 60 cities within the next 8-0 years.

DLF – A Pioneering Developer

DLF, India’s largest real estate developer

was among the rst movers into shopping mall

development, when it launched the 250,000 sq t

City Centre Mall in Gurgaon in 2000. The company

has a very strong presence in the NCR.

DLF is planning a listing in 2007 with aggressive

plans to become a truly pan Indian player.

They already have portolio in most o India’s

main cities, but now are also targeting Tier

III cities o Punjab viz. Ludhiana, Jalandhar,

Chandigarh and Amritsar, alongwith Jaipur and

Kochi. They have a reported aim

o developing up to 100 malls across 60 cities

within the next 8-10 years.

DLF are broadening their ormats to include

speciality malls, big box retailing and integrated

malls within SEZs. They are also moving into

“lease models” and “revenue share model”.

Poor quality shopping malls – In the competitive rush to build

shopping malls, we assess that over 90% o the current and

planned shopping mall stock alls below international standards,

in terms o specication and design:

Most malls developed earlier in the decade were strata titled.Currently circa 80% o mall units are strata title versus only 20% leased. A recent survey by Jones Lang LaSalle Meghrajindicates that three-quarters o domestic branded retailerspreer to lease rather than purchase retail units. Developersare beginning to respond to this trend, with more malldevelopers are now holding on to their properties. Local

amily retailers still preer to buy rather than lease.Construction standards are inherently poor, with developers’urther compromising standards due to rising constructioncosts.

†

†

Mall congurations are poor in terms o pedestrianaccess, corridor width, linkages between oors and theamount o space allocated or ood courts, entertainmentareas, promotion zones, etc. Service areas or delivery andmovement o merchandise are oen inadequate.

Many malls have a severe lack o parking provision, which iscompounded by poor linkages with the road inrastructure.

No emphasis on tenant and trade mix

But the biggest challenge or most Indian malls is the poor

quality o the surrounding inrastructure and lack o integration

with neighbouring residential areas, which oen leads to

signicant congestion. A combination o poor inrastructure

(both transport and utilities), planning and zoning legislation

makes it inherently dicult or developers to provide an

attractive retail destination.

Despite their inerior quality, most shopping malls stillcommand large ootalls. But, many will fail the test of time as

more choice becomes available or the Indian consumer, who

will become increasingly discerning over their choice o retail

destination.

India: Lease Preerences

Choice o Lease Model

Inadequate asset management – Most malls are poorly

managed at both an operational/tactical and strategic level.

Tis translates into problems ranging rom low maintenance

and cleaning, and various health & saety risks, through toinappropriate tenant mixes. Most owners continue to struggle

with translating high ootalls into higher revenue. But this is

gradually starting to change with the introduction o outsourced

proessional mall management to manage tenant mix, acilities,

promotion, etc.

Te benchmark shopping malls – Tere are nonetheless a ew

trophy malls, such as the Prestige Forum (in Bangalore) and

Inorbit (in Mumbai), which have been particularly successul,

and are closer to the standards expected by international

investors. Tey are large, well planned and constructed malls,

actively managed and promoted, incorporating entertainmentand adequate parking. Select City Walk (in South Delhi)

which is expected to become operational during 2008, a large

multi use scheme, will set a new benchmark or shopping mall

development in India. A revenue share model is being adopted

†

†

†

Lease model

74%

Ownership

model

26%

Fixed rent model

65%

Revenue-share

model35%

Source: Jones Lang LaSalle Meghraj Research

W i n n i n g C i t i e s : I N D I A R E T A I L

1

8/8/2019 WWC India Retail

http://slidepdf.com/reader/full/wwc-india-retail 14/24

8/8/2019 WWC India Retail

http://slidepdf.com/reader/full/wwc-india-retail 15/24

8/8/2019 WWC India Retail

http://slidepdf.com/reader/full/wwc-india-retail 16/24

8/8/2019 WWC India Retail

http://slidepdf.com/reader/full/wwc-india-retail 17/24

raditional “High Streets” will adapt – While the property

market is rmly ocused on new shopping mall ormats,

traditional “high streets” will continue to be the mainstay o

the Indian retail scene. Te pull o traditional neighbourhood

retailers, particularly or local brands will remain very strong;

“High Street” retailers have the advantages o proximity,

amiliarity and high personal service. Culturally Indian

consumers expect and receive rst class personal service rom

local retailers, and are oen better positioned to respond to

the huge demand or home delivery. But competition will

increase, particularly as some local retailers move into malls

and it will become a credible alternative to shop or local retail

in newer ormats. raditional retailers will ght back, and the

“high streets” will be orced to adapt, which will provide new

opportunities or the property market to cater or this important

local component o the Indian retail scene. Moreover, many

traditional retailers still occupy illegal premises, and the policy adopted by the Delhi government to close/demolish illegal stores

is likely to be rolled out to other Indian cities, orcing traditional

retailers into the organised sector.

Retail property market is expanding into new geographies– Many retailers and mall developers are looking beyond India’smajor cities, and selectively ocusing on smaller cities whichoer huge potential. Tese cities oer avourable opportunitiesor retailers due to growing consumer markets, considerablelatent demand or branded goods and lower property costs. Tey are also less saturated than India’s main metros, and are lesslikely to ace uture competition rom international players.

In the ollowing section we look at India’s emerging retailgeography, and assess current property market conditions anduture prospects in both the major cities and those smalleremerging cities that are starting to appear on the radar screen o the retail property market.

The New Retail

Hierarchy and Property OpportunitiesAssessing City Retail Potentialo create a view o the where, how and when each o India’s

cities with a million + population will emerge as interesting

locations or property development, we have consolidated all

the intelligence, inormation and views we have on 50 Indiancities in order to create a new retail city classication. Te

classication is based on an analysis o three sets o indicators:

Retail Potential Indicator – based on a basket o indicators

including metropolitan area population and total income; per

capita income, savings and expenditure; household prole

and economic growth measures. Tese indicators enable a

quantitative appraisal o each city’s demographic and economic

undamentals, and provide an indicator o their potential to

develop as vibrant retail locations.

Retailer Demand Indicator – based on the operational and

planned presence o a basket o major domestic retailers (such as

Pantaloon, Westside and Shoppers Stop) as well as domestic and

international niche (“vanilla”) retailers.

Retail Supply Indicator – based on the number o current and

planned shopping malls.

City Retail Potential Model

Our analysis has identied a ve-level classication o cities:

1. Maturing CitiesTe National Capital Region (Delhi) and Mumbai dominate

India’s organised retailing sector. Malls have been a eature

o these two metros since 999, but it is only since 2003 that

volumes have increased markedly. Tese two vast metro regions

currently account or around hal o all o India’s organised

retailing. By 2008, they will still contribute over 40% o national

organised retail activity; although this proportion is expected

to decline over the longer term as retailing opportunities grow

elsewhere (see page 2-23).

Te NCR and Mumbai have by ar the highest number o

shopping malls in operation and planned. Most pan-Indian

CITIES HIERARCHY

NASCENT

MATURING

EMERGING

HIGH GROWTH

TRANSITIONAL

50 CITIES

Socio-EconomicFundamentals

Size: Total City Income

Wealth: Income,Savings, Expenditure

Socio-EconomicProle (% in SEC A/B)

GDP Growth

†

†

†

†

RetailerDemand

Basket o 20Retailers

ExistingStores

PlannedStores

†

†

Retail Supply

Shoppingmall stock

Shoppingmallconstruction

RETAIL POTENTIAL SCORE RETAIL ACTIVITY SCORE

Source: Jones Lang LaSalle Meghraj Research

W i n n i n g C i t i e s : I N D I A R E T A I L

17

8/8/2019 WWC India Retail

http://slidepdf.com/reader/full/wwc-india-retail 18/24

retailers have a multiple presence, they are the launch pads or

most new retailer entrants and with by ar the largest number o

“super-rich”, and these cities are the hubs o luxury brands. Tey

are rmly on the radar o screen o international retailers and

property investors.

Competition within the NCR and Mumbai will intensiy as

supply grows and there is risk o saturation in some market

segments by 2008. Strong asset price growth and diculties in

land procurement make or a challenging environment or both

retailers and developers. Nonetheless, there are notable market

gaps and both metros are suciently large to accommodate a

wide variety o new ormats.

Opportunities are likely to arise in:

Developing large one-stop malls that combine mixed useconcepts, integrating retail, entertainment, eating and

residential uses.Catering or the numerous luxury brand retailers that arenow targeting India’s two main metros. Currently, luxury brands are only largely present in major ve star hotels (suchas Te Oberoi and Imperial in Delhi and the aj MahalPalace in Mumbai), but there is strong demand rom theseretailers or showrooms in both large shopping malls andspeciality malls.

Responding to the requirement or “Big Box” ormats; aormat that is likely to emerge over the next couple o years.

Developing more accessible neighbourhood malls andhypermarkets within the cities. Most current and planned

schemes are remote rom the main residential areas, and lowcar penetration makes shopping malls inaccessible to many consumers.

argeting the booming middle class residential suburbs, suchas Greater NOIDA (NCR) and Navi Mumbai and Tane(Mumbai) where many o the I/IES companies are based;and ocusing in particular on those suburbs that have yet to

see signicant mall development.

National Capital Region

Te National Capital Region has been and continues to be the

leader in mall culture in India. Organised retailing in the NCR is

twice the size o Mumbai, both in terms o shopping mall stock and retailer presence. Rising income levels, increasing demand

or branded products and wider acceptance o mall culture (than

elsewhere in India) has led to massive growth in the shopping

mall stock. Retailers are also attracted by the consumer prole o

the NCR, with over 40% o households in SEC groups A and B.

At present the total mall stock stands at 8.2 million sq , o

which 2.6 million sq is within the city o Delhi. Most stock,

however, is concentrated in the main suburban regions o

Gurgaon (at 2.6 million sq ), Ghaziabad (.2 million sq ) and

NOIDA (. million sq ).

Organized retailing rst came to the city with the constructiono Ansal Plaza in South Delhi in 999. However, it wasn’t until

200 that the NCR saw the rst shopping mall development

boom, ocused on the suburban market o Gurgaon, due to

its booming I/IES sector and the availability o larger plots

†

†

†

†

†

Source: Jones Lang LaSalle Meghraj Research

o cheap land. Gurgaon saw the development o several large

ormat malls by developers such as DLF and MGF. NOIDA

ollowed Gurgaon into the retail boom in 2003, and more

recently Ghaziabad and Faridabad have both emerged as major

retail sub-markets. Te city o Delhi is also witnessing large scale

mall development, which has been made possible by the release

and auction o land by the Delhi Development Authority.

With a very large number o malls in the pipeline (the mall

stock could potentially more than double to 22 million sq by

2008-09) the NCR will continue to lead India’s organized retail

market. We expect the suburbs o Faridabad, Ghaziabad and

Greater NOIDA to be the ocus o uture retail development.

Manesar on National Highway 8 connecting the NCR to the city

o Jaipur is also likely to witness high retail interest. HSIDC has

approved large commercial projects, and several major MNCs

have commenced operations. wo Special Economic Zones by

DLF (NCR’s largest developer) and Reliance are also proposed.

Tese new suburban areas have large tracts o low cost land, and

will attract high developer interest or mixed use development.

Connaught Place, South Extension, Khan Market and Greater

Kailash are Delhi’s prime “high street” locations. Tey are

vibrant retail destinations with recognised brands; and they

will continue to attract signicant consumer activity. Lack

o expansion space in prime “high streets” is likely to lead

to urther price rises. Te Delhi government’s policy o

demolishing/closing illegal stores will re-enorce the migration

towards organised retailing.

National Capital RegionShopping Mall Development, 2000-2008

Mumbai

Mumbai’s rst mall was completed in 999 in the Central

Business District (CBD). Since 2003 mall development has

increased massively, expanding rom the CBD to all parts o the

island city and suburbs. Currently, Mumbai has a shoppingmall stock o 4.0 million sq , a gure that could rise to around

5 million sq by 2008-09.

SBD Central (Worli, Prabhadevi and Mahalaxmi) and SBD

North (Bandra, Andheri, Juhu and Santacruz) were the

6,000

7,000

8,000

9,000

10,000

5,000

4,000

3,000

2,0001,000

0

‘000 sq ft

Delhi

2000 2001 2002 2003 2004 2005 2006 2007 2008

Gurgaon NOIDA Ghaziabad Faridabad

Existing Stock Future Supply

WinningCities:INDIARETAIL

8

8/8/2019 WWC India Retail

http://slidepdf.com/reader/full/wwc-india-retail 19/24

8/8/2019 WWC India Retail

http://slidepdf.com/reader/full/wwc-india-retail 20/24

8/8/2019 WWC India Retail

http://slidepdf.com/reader/full/wwc-india-retail 21/24

Shopping Mall Development, 2000-2008

Source: Jones Lang LaSalle Meghraj Research

2000 2001 2002 2003 2004 2005 2006 2007 2008

6,000

7,000

8,000

9,000

5,000

4,000

3,000

2,000

1,000

0

‘000 sq ft

CBD SBD-North SBD-Central

Suburbs-Navi Mumbai & Thane Suburbs-Others

Existing Stock Future Supply

12,000

14,000

20,000

22,000

18,00016,000

10,000

8,000

6,000

4,000

2,000

0

‘000 sq ft

NCR Mumbai Bangalore Kolkata Pune Chennai Hyderabad

2000 2001 2002 2003 2004 2005 2006 2007 2008

Delhi/NCR 41%

Mumbai 20%

Kolkata 10%

Pune 6%

Bangalore 8%

Hyderabad 4%

Chennai 3%

Ahmedabad 8%

45 milion sq t

Source: Jones Lang LaSalle Meghraj Research

rst micro-markets outside the CBD to see signicant mall

development in 2002-2003. Since then there has been steady

growth in the number o malls and several new developments

are slated or completion by 2008 in the western suburban

regions.

Another hot retail market is likely to be in the Parel area (in SBD

Central), where the sale o mill lands has created considerable

opportunities or mixed use development.

Other western suburban regions such as Malad and Goregaon

have seen the development o integrated townships such as

Mindspace. o cater or these residential townships, Raheja

built the In-Orbit mall, which has become one o India’s most

successul malls.

Te central suburban regions o Powai, Mulund, Navi Mumbai

and Tane are emerging as Mumbai’s next hot retail markets,

boosted by the growing activities o the I/IES sector and

rapidly expanding residential areas. Both Navi Mumbai and

Tane are set to witness huge mall development in the near

uture. We expect that the central suburbs o Powai, Mulund,

Navi Mumbai and Tane will overtake the western suburbs in

terms o mall space.

Mumbai’s “high streets” such as Bandra Linking Road, Colaba

Causeway, Breach Candy and Lokhandwala will continue to

attract the Mumbai-ites.

Mmbai, Shopping Mall Development

2000-2008

2. Transitional CitiesBangalore, Kolkata, Hyderabad, Pune, Chennai, Ahmedabad

India’s transitional retail cities o Bangalore, Kolkata, Hyderabad,

Pune, Chennai and Ahmedabad are now rmly making their

mark on the retail sector. Whilst organised retailing is a more

recent phenomenon than in the NCR and Mumbai, they are

catching up as both retailers and developers tap into their largemiddle classes. By 2008, these six transitional cities will account

or one-third o India’s organised retailing. Retailers are attracted

by their increasingly vibrant corporate sectors, high economic

growth rates, above average incomes and large middle classes.

Property, construction and labour costs are also well below the

NCR and Mumbai.

Te majority o major domestic retailers and new market

entrants, irrespective o their business models, are already

expanding in these cities or have plans to open new stores.estimony to the strength o ier II cities, Reliance Retail chose

to open its rst concept store in Hyderabad. As with ier I cities,

the key opportunities are in large one-stop malls, speciality

malls, neighbourhood malls and hypermarkets and “Big Box”

retailing.

Kolkata, Pune and Hyderabad currently have the largest

shopping mall oorspace o the transitional cities. But Bangalore

has the most aggressive mall construction programme, with

a wide variety o retailers attracted to the city’s increasingly

cosmopolitan population. Chennai has so ar lagged the other

transitional cities in terms o mall development, but is expectedto start to catch up by 2008.

India’s Shopping Mall Stock (est. by end 2007)Primary and Secondary Cities

Source: Jones Lang LaSalle Meghraj Research

W i n n i n g C i t i e s : I N D I A R E T A I L

21

8/8/2019 WWC India Retail

http://slidepdf.com/reader/full/wwc-india-retail 22/24

Indian Tertiary Cities – Retail Activity v Potential

GROWTH

EMERGING

NASCENT

Jaipur

Ludhiana

Chandigarh

Lucknow

Kochi

Vadodara

Surat

IndoreAmritsar

Jalandhar

MangaloreNashikBhubaneshwarAgra

VizagCoimbatore

Nagpur KanpurGoaAllahabad

Thiruvananthapuram

Mysore

Jamshedpur

JodphurVaranasi Patna MeerutRajkot

Aurangabad Bhopal

Kolhapur

Guwahati

MaduraiRanchi

SonipatSrinagar

Solapur

Asansol

DhanbadPanipat

VijayawadaJabalpur

1.2

1.0

0.8

0.6

0.4

0,2

0

0.4 0.6 0.8 1.0 1.2 1.4

Retail Activity Score

Retail Potential Score

2000 2001 2002 2003 2004 2005 2006 2007 2008

6,000

5,000

4,000

3,000

2,000

1,000

0

‘000 sq ft

Prime SecondarySecondary Suburbs

Existing Stock Future Supply

Bangalore, Shopping Mall Development2000-2008

Source: Jones Lang LaSalle Meghraj Research

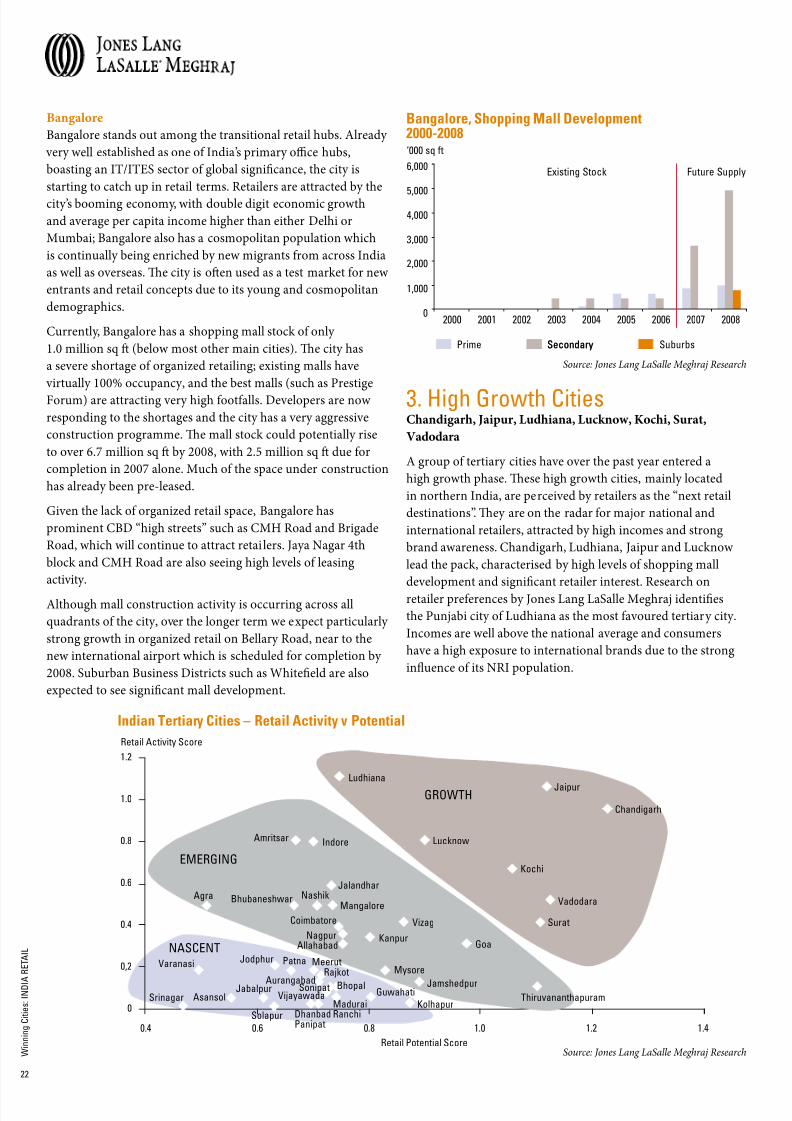

. High Growth CitiesChandigarh, Jaipur, Ludhiana, Lucknow, Kochi, Surat,

Vadodara

A group o tertiary cities have over the past year entered a

high growth phase. Tese high growth cities, mainly located

in northern India, are perceived by retailers as the “next retail

destinations”. Tey are on the radar or major national and

international retailers, attracted by high incomes and strong

brand awareness. Chandigarh, Ludhiana, Jaipur and Lucknow

lead the pack, characterised by high levels o shopping mall

development and signicant retailer interest. Research on

retailer preerences by Jones Lang LaSalle Meghraj identies

the Punjabi city o Ludhiana as the most avoured tertiary city.

Incomes are well above the national average and consumers

have a high exposure to international brands due to the strong

inuence o its NRI population.

Bangalore

Bangalore stands out among the transitional retail hubs. Already

very well established as one o India’s primary oce hubs,

boasting an I/IES sector o global signicance, the city is

starting to catch up in retail terms. Retailers are attracted by the

city’s booming economy, with double digit economic growth

and average per capita income higher than either Delhi or

Mumbai; Bangalore also has a cosmopolitan population which

is continually being enriched by new migrants rom across India

as well as overseas. Te city is oen used as a test market or new

entrants and retail concepts due to its young and cosmopolitan

demographics.

Currently, Bangalore has a shopping mall stock o only

.0 million sq (below most other main cities). Te city has

a severe shortage o organized retailing; existing malls have

virtually 00% occupancy, and the best malls (such as Prestige

Forum) are attracting very high ootalls. Developers are now

responding to the shortages and the city has a very aggressive

construction programme. Te mall stock could potentially rise

to over 6.7 million sq by 2008, with 2.5 million sq due or

completion in 2007 alone. Much o the space under construction

has already been pre-leased.

Given the lack o organized retail space, Bangalore has

prominent CBD “high streets” such as CMH Road and Brigade

Road, which will continue to attract retailers. Jaya Nagar 4th

block and CMH Road are also seeing high levels o leasing

activity.

Although mall construction activity is occurring across all

quadrants o the city, over the longer term we expect particularly

strong growth in organized retail on Bellary Road, near to the

new international airport which is scheduled or completion by

2008. Suburban Business Districts such as Whiteeld are also

expected to see signicant mall development.

Source: Jones Lang LaSalle Meghraj Research

WinningCities:INDIARETAIL

2

8/8/2019 WWC India Retail

http://slidepdf.com/reader/full/wwc-india-retail 23/24

Most high growth cities are located in northern India wherethere is strong brand awareness. Te exception is Kochi insouthern India, a avoured destination or the I/IES sector.A sharp rise in mall development is expected in 2007/2008in Kochi, with schemes by both the Kshitij Fund (a retail

investment und o the Future Group) and Lulu (a division o EMKE Group o Dubai) in the pipeline.

. Emerging CitiesAmritsar, Indore, Jalandhar, Mangalore, Nashik,

Bhubaneshwar, Agra, Vizag, Nagpur, Coimbatore, Kanpur,

Goa, Allahabad, Mysore, Jamshedpur, Tiruvananthapuram

On the basis o the uture plans o major hypermarkets and

department stores, a group o 6 emerging cities are likely to

be the next growth markets over a three year horizon. Factors

such as growing incomes, rising aspirations, scarcity o branded

stores and growing corporate activity are increasing the demandor organised retailing. In cities such as Nagpur, Indore, Nashik,

Bhubaneshwar, Vizag, Coimbatore, Mangalore, Mysore and

Tiruvananthapuram, I/IES companies are rapidly expanding

their workorces, which in turn is stimulating retailer activity.

Tese cities currently represent among the most interesting

locations or property developers - retailers are combing these

cities or opportunities, with demand exceeding supply. Tis

group also includes several major tourist destinations such as

Amritsar, Agra and Goa, as well as a number o southern Indian

cities which have so ar been less impacted by organised retail

than their northern Indian counterparts.Tese smaller cities have consistently outpaced the larger metros

in economic growth rates, and they are witnessing strong growth

in incomes. But even more signicant is the changing liestyles

and aspirations, and the undamental shi in the consumer

mindset in smaller cities.

Low property costs, lower operating costs and high brand

acceptance in smaller cities are enabling retailers to achieve

better margins than in India’s main cities. Retailers are

introducing contemporary retail ormats but at a smaller

scale, with mall sizes typically between 00,000-50,000 sq

compared to 500,000 sq in the larger metros.

5. Nascent Cities–The Next FrontierPatna, Bhopal, Meerut, Asansol, Varanasi, Kolhapur, Sonipat,

Madurai, Rajkot, Jabalpur, Dhanbad, Vijayawada, Srinagar,

Panipat, Aurangabad, Solapur, Ranchi, Jodhpur, Guwahati

A urther 9 smaller cities (most o which have populations

o between -.5 million) are classied as “nascent”, largely

reecting low incomes and limited corporate activity. Organised

retailing is currently very limited, but they are nonetheless on

the “watch list” o pioneering retailers and mall developers that

are seeking to benet rom “rst mover advantage”. Progress

towards the development o an active organised retail sector in

these cities is likely to be slow, although market conditions can

change rapidly should their local economies be boosted by new

corporate arrivals.

Jodhpur, Vijayawada and Varanasi are amongst the most popular

tourist destinations in India, and their potential or organised

retail is higher than other “nascent” cities. Others cities havesignicant manuacturing sectors, which have attracted

department stores and hypermarkets. Pantaloon’s agship brand

“Big Bazaar” is already present in the majority o these cities.

Developers like Prozone, are active in cities such as Aurangabad

and Rajkot.

Final ObservationsRetail Developers Must Fight or a

Place in the Modernisation ProcessTis report has shown how changes in consumer behaviour

and the rapid transormation o India’s retail scene have

bought the Indian retail real estate market to the point o

“li-o”. Signicant new opportunities across a broad range o

geographies and ormats are being captured by an increasing

number o domestic real estate developers and investors, all

eager to participate in a market that is still at an early stage o

evolution. However in the rush to expand retail ormats and

build new malls, many schemes all well below international

standards. As more choice becomes available or the Indian

consumer, a lot o malls and retail concepts will ail the testo time. Moreover, most retailers will struggle to implement

aggressive expansion plans due a lack o suitable and aordable

property, inecient logistics operations and shortages o

manpower skills. A rapidly growing, but highly challenging

retail environment will inevitably result in many losers as well as

winners.

The Next StageTe next stage in the evolution o the Indian retail market

will be when international developers and nanciers start to

change the shape o India retailing, joining an elite group o visionary domestic developers, owners and retailers who have

the scalability, the teams, the processes and the logistics required

to ourish in this rapidly growing retail environment. In the

next report in the Jones Lang LaSalle Meghraj series on India

Retail Futures, we will look at the state o Indian retailing on

the ground, and drawing on international best practice, we will

provide insights into how new retail development is likely to

evolve in terms o design, style and management, as the Indian

retail sector truly becomes part o the global real estate market.

W i n n i n g C i t i e s : I N D I A R E T A I L

2

8/8/2019 WWC India Retail

http://slidepdf.com/reader/full/wwc-india-retail 24/24

Reports on India rom Jones Lang LaSalle

World Winning Cities SeriesEmerging City Winners

“Emerging City Winners” is Phase IV o Jones Lang LaSalle’s WorldWinning Cities Research, a multi-year programme designed to draw together the essence o contemporary city competitiveness. WorldWinning Cities examines trends that are impacting on the business andeconomic landscape, and how these actors are coalescing to create the rising urban stars o the next decade.

Our Emerging Cities Winners research aims to identiy the winners andlosers amongst the world’s emerging cities in Asia, EMEA and Latin America. This phase o World WinningCities has evolved in response to the rapid changes that are occurring in the geography o business, wherenew opportunities are now emerging in cities that have not traditionally been on the radar screen o the

property sector. Cross-border occupiers and investors need to be able to spot the rising urban stars o theuture. Emerging City Winners aims to provide insights into the dynamics o the world’s emerging cities, tohelp real estate occupiers and investors understand the opportunities and complexities o a growing band orising urban stars.

Jones Lang LaSalle Ofces

SINGAPORE 9 Rafes Place

#9-00 Republic Plaza

Singapore 08619 tel +65 6220 888

ax +65 68 60

www.joneslanglasalle.com.sg

CHICAGO 200 East Randolph Drive

Chicago IL 60601

tel +1 12 782 5800ax +1 12 782 9

www.am.joneslanglasalle.com

LONDON

22 Hanover SquareLondon W1A 2BN

tel + 20 79 600

ax + 20 708 0220www.joneslanglasalle.co.uk

Jones Lang LaSalle Meghraj - India

NEW DELHI tel +91 11 21 7070

BANGALORE tel +91 80 118 2900

tel +91 80 112 1271

CHENNAI tel +91 212 9982

tel +91 2811 6789

CHANDIGARH

tel +91 172 07 651

COCHIN

tel +91 8 018 652

COIMBATORE tel +91 22 25

GuRGAON

tel +91 12 60 5000 tel +91 12 08 7

HYDERABAD

tel +91 0 668 716

tel +91 0 291 52

MuMBAI tel +91 22 6658 1000 tel +91 22 282 800

tel +91 22 297 2652

PuNE tel +91 20 058 600 tel +91 20 6601 0861

KOLKATA tel +91 200 26

tel +91 2227 29

Anj Pri Chairman & Country HeadJones Lang LaSalle Meghraj (Mumbai) tel +91 22 282 [email protected]

Vincent Lottefer Chie Executive Oicer

Jones Lang LaSalle Meghraj (New Delhi) tel +91 12 60 [email protected]

Vivek Kal Head o Retail & Leisure Advisory – IndiaJones Lang LaSalle Meghraj (New Delhi) tel +91 12 60 [email protected]

Marc TrevesBusiness Development Director –Retail & Leisure AdvisoryJones Lang LaSalle Meghraj (New Delhi) tel +91 12 60 [email protected]

Manisha Grover Head o Strategic Consulting & ResearchJones Lang LaSalle Meghraj (Bangalore)tel +91 80 118 2922

AuTHORS Jeremy Kelly Programme Director, World Winning CitiesJones Lang LaSalle (London) tel + 20 17 [email protected]

Abhishek Kiran Gpta

Senior Manager, ResearchJones Lang LaSalle Meghraj (Mumbai) tel + 91 22 658 [email protected]

Nitika Masih Assistant Manager, ResearchJones Lang LaSalle Meghraj (New Delhi) tel +91 12 [email protected]

For more inormation on India Retail and how Jones Lang LaSalle Meghraj can assist companies making highquality real estate decisions in India, please contact: