xp investimentos 11° xp latam - imf meetings brazil’s economic

TRANSCRIPT

April 09, 2021

XP Investimentos 11° XP Latam - IMF Meetings

Brazil’s Economic Outlook and Agenda BC#

Roberto Campos NetoGovernor of Banco Central do Brasil

2

COVID-19Covid-19: new cases and new deathsGlobal scenario

Source: Our World in Data. Last data available: Apr 07, 2021.

New cases/million(7-day rolling average)

UK

US

Brazil

Europe ex UK

Lat. Am. ex Brazil

New deaths/million(7-day rolling average)

0

100

200

300

400

500

600

700

800

900

Mar-20 May-20 Jul-20 Sep-20 Nov-20 Jan-21 Mar-21

0

2

4

6

8

10

12

14

16

18

20

0

2

4

6

8

10

12

14

16

18

20

Mar-20 May-20 Jul-20 Sep-20 Nov-20 Jan-21 Mar-21

GLOBAL ECONOMYCovid-19 vaccinationVaccination

The biggest vaccination campaign in history

*UN initiative to support vaccination in low- and middle-income countries.Sources: Airfinity, FT, economic Times. BNP Paribas

3

Millions of administered doses(in millions and in % of population*)

Vaccine doses purchased(per capita)

Note: * The number of administered doses is less than or equal to the number of people vaccinated. In some countries, some people have already taken the second dose. Therefore, the percentage in relation to the population should be understood as “maximum percentage of the vaccinated population”.

709.9 MM (9.1%)

171.5 MM (51.8%)

149.1 MM (10.4%)

90.2 MM (6.5%)

84.9 MM (19.1%)

37.4 MM (55.1%)

24.2 MM (11.4%)

17.7 MM (21%)

13.5 MM (4.9%)

13 MM (8.9%)

108.5 MM (3.2%)

World

United States

China

India

European Union

United Kingdom

Brazil

Turkey

Indonesia

Russia

Rest of the world

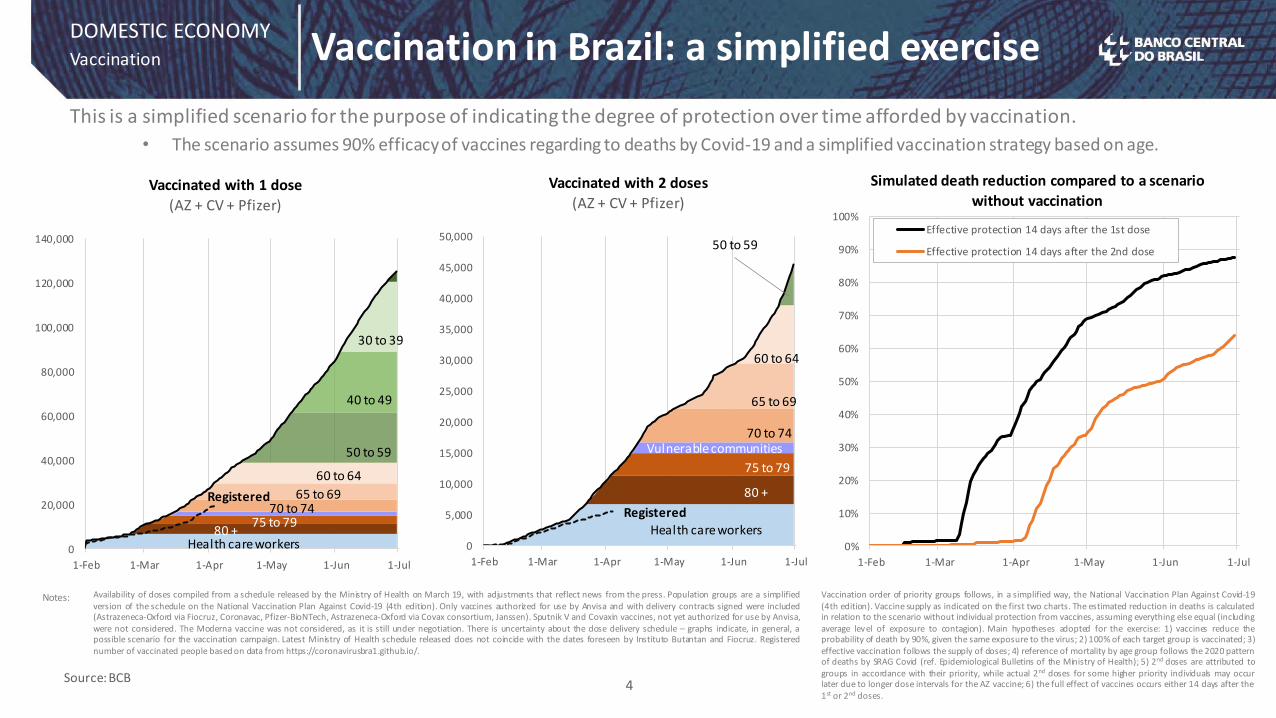

DOMESTIC ECONOMYVaccination in Brazil: a simplified exerciseVaccination

4

Availability of doses compiled from a schedule released by the Ministry of Health on March 19, with adjustments that reflect news from the press. Population groups are a simplifiedversion of the schedule on the National Vaccination Plan Against Covid-19 (4th edition). Only vaccines authorized for use by Anvisa and with delivery contracts signed were included(Astrazeneca-Oxford via Fiocruz, Coronavac, Pfizer-BioNTech, Astrazeneca-Oxford via Covax consortium, Janssen). Sputnik V and Covaxin vaccines, not yet authorized for use by Anvisa,were not considered. The Moderna vaccine was not considered, as it is still under negotiation. There is uncertainty about the dose delivery schedule – graphs indicate, in general, apossible scenario for the vaccination campaign. Latest Ministry of Health schedule released does not coincide with the dates foreseen by Instituto Butantan and Fiocruz. Registerednumber of vaccinated people based on data from https://coronavirusbra1.github.io/.

This is a simplified scenario for the purpose of indicating the degree of protection over time afforded by vaccination.

• The scenario assumes 90% efficacy of vaccines regarding to deaths by Covid-19 and a simplified vaccination strategy based on age.

Notes: Vaccination order of priority groups follows, in a simplified way, the National Vaccination Plan Against Covid-19(4th edition). Vaccine supply as indicated on the first two charts. The estimated reduction in deaths is calculatedin relation to the scenario without individual protection from vaccines, assuming everything else equal (includingaverage level of exposure to contagion). Main hypotheses adopted for the exercise: 1) vaccines reduce theprobability of death by 90%, given the same exposure to the virus; 2) 100% of each target group is vaccinated; 3)effective vaccination follows the supply of doses; 4) reference of mortality by age group follows the 2020 patternof deaths by SRAG Covid (ref. Epidemiological Bulletins of the Ministry of Health); 5) 2nd doses are attributed togroups in accordance with their priority, while actual 2nd doses for some higher priority individuals may occurlater due to longer dose intervals for the AZ vaccine; 6) the full effect of vaccines occurs either 14 days after the1st or 2nd doses.

Source: BCB

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

1-Feb 1-Mar 1-Apr 1-May 1-Jun 1-Jul

Vaccinated with 1 dose

(AZ + CV + Pfizer)

40 to 49

50 to 59

30 to 39

60 to 64

65 to 6970 to 74

75 to 7980 +

Health care workers

Registered

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

1-Feb 1-Mar 1-Apr 1-May 1-Jun 1-Jul

Vaccinated with 2 doses

(AZ + CV + Pfizer)

60 to 64

65 to 69

70 to 74

75 to 79

80 +

Health care workers

50 to 59

Registered

Vulnerable communities

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1-Feb 1-Mar 1-Apr 1-May 1-Jun 1-Jul

Simulated death reduction compared to a scenario

without vaccination

Effective protection 14 days after the 1st dose

Effective protection 14 days after the 2nd dose

80 +

75

80

85

90

95

100

105

110

T12019

T2 T3 T4 T12020

T2 T3 T4

Ave

rage

201

9 =

100

USA Euro area UK Japan China Asia ex Japan and China

5

GLOBAL ECONOMYGlobal Economic Activity

Global economic recovery continues to be directly linked to the evolution of the pandemic and containment measures.

Source: Bloomberg.

GDP*Average 2019 = 100

* Series at constant prices, seasonally adjusted. The series 'Asia ex. Japan and China' was calculated as a weighted average of Singapore, South Korea, Hong Kong, India, Indonesia, Philippines, Malaysia, Thailand, Taiwan and Turkey. The series of Singapore, India and Indonesia are not seasonally adjusted.

6

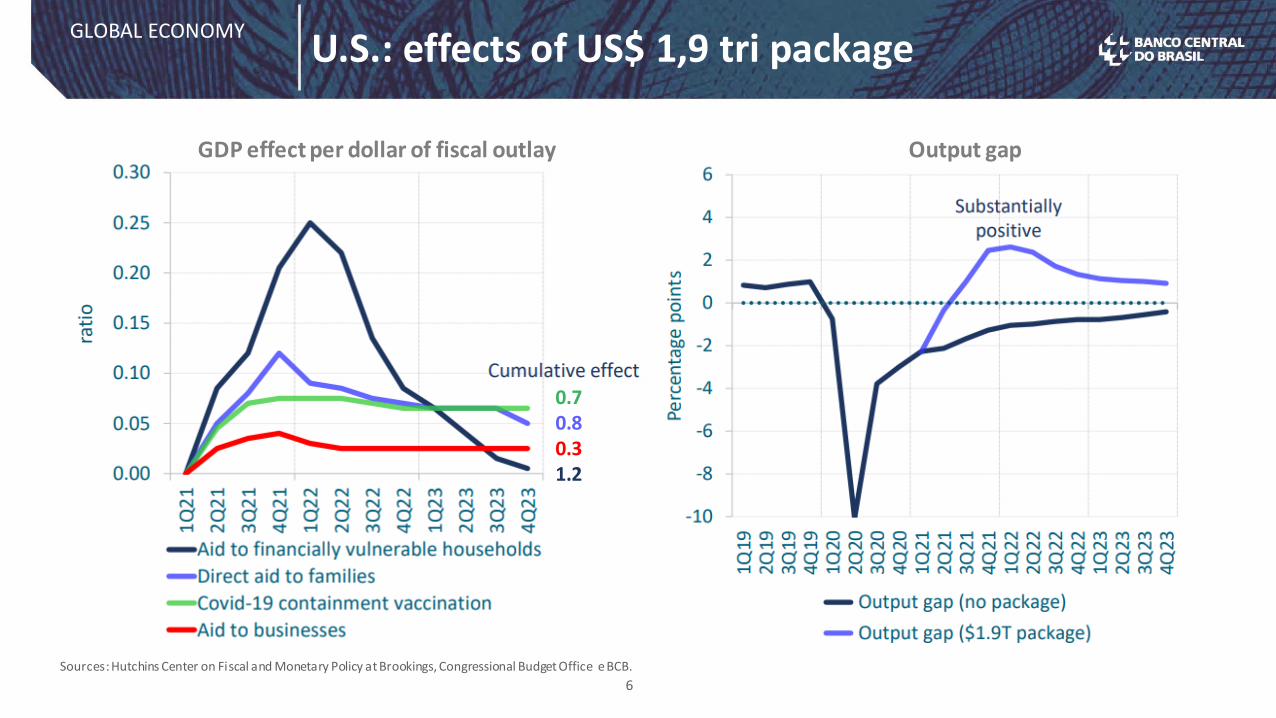

GLOBAL ECONOMYU.S.: effects of US$ 1,9 tri package

Sources: Hutchins Center on Fiscal and Monetary Policy at Brookings, Congressional Budget Office e BCB.

Output gapGDP effect per dollar of fiscal outlay

0.70.80.31.2

-50

-40

-30

-20

-10

0

10

20

30

Feb-20 Apr-20 Jun-20 Aug-20 Oct-20 Dec-20 Feb-21

Brazil Chile Colombia Mexico South Africa Russia

-12 -8 -4 0 4 8 12

Russia

South Africa

Brazil

Mexico

Argentina

Colombia

Chile

Malaysia

Peru

2022

2021

2020

7

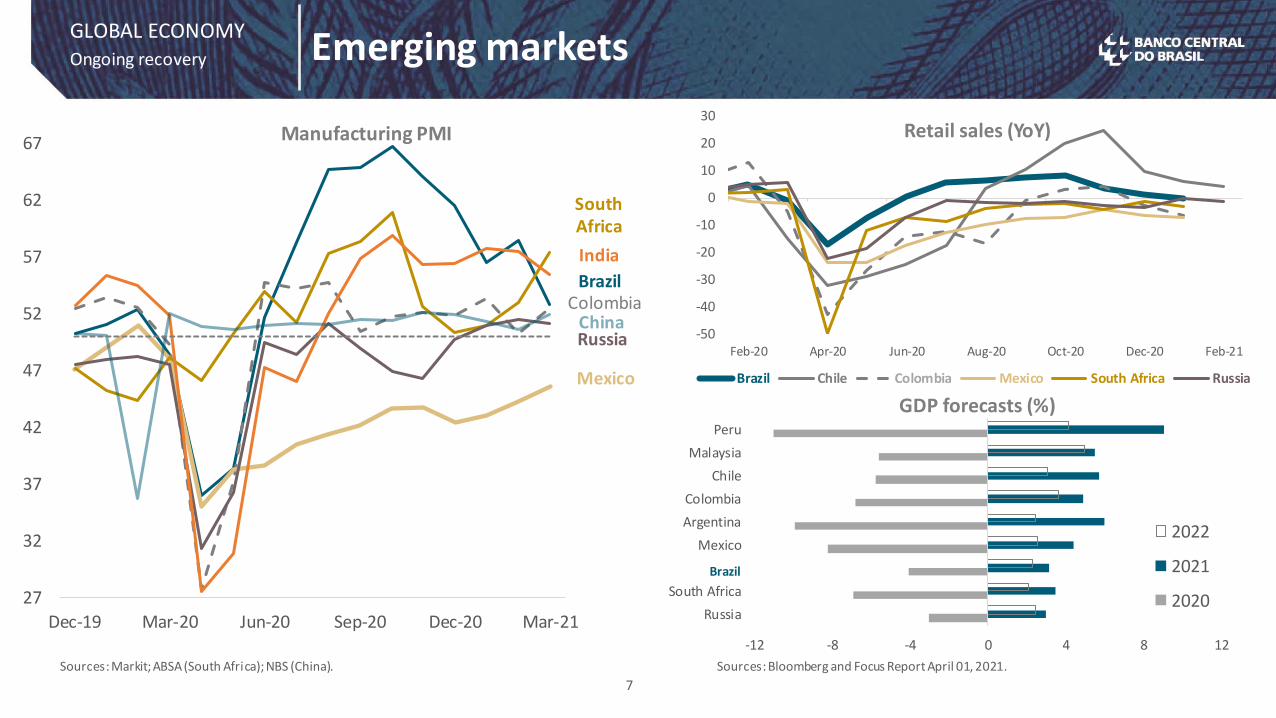

GLOBAL ECONOMYEmerging marketsOngoing recovery

Sources: Markit; ABSA (South Africa); NBS (China). Sources: Bloomberg and Focus Report April 01, 2021.

Retail sales (YoY)

GDP forecasts (%)

Brazil

BrazilColombia

Mexico

South Africa

Russia

India

China

27

32

37

42

47

52

57

62

67

Dec-19 Mar-20 Jun-20 Sep-20 Dec-20 Mar-21

Manufacturing PMI

8

GLOBAL ECONOMYEmerging markets: food pricesInflation

Increasing trend of food prices in international markets create upward pressure on inflation.

Sources: FAO, Bloomberg.

145

129

121

115

109

90

70

80

90

100

110

120

130

140

150D

ec-

19

Jan

-20

Feb

-20

Mar

-20

Ap

r-2

0

May

-20

Jun

-20

Jul-

20

Au

g-2

0

Sep

-20

Oct

-20

No

v-2

0

De

c-20

Jan

-21

Feb

-21

FAO Food Prices(Dec/2019 = 100)

Oils

Cereals

Sugar

Food Price Index

Dairy

Meat

121

120

108107107106106105102

100

95

100

105

110

115

120

125

Jan

-20

Feb

-20

Mar

-20

Ap

r-2

0

May

-20

Jun

-20

Jul-

20

Au

g-2

0

Sep

-20

Oct

-20

No

v-2

0

De

c-20

Jan

-21

Feb

-21

CPI Food (Jan/2020 = 100)

TurkeyBrazilRussiaChileMexicoSouth AfricaColombiaPeruIndiaChina

9

Covid-19 Government Fiscal Responses

Source: Bloomberg, IMF.

GLOBAL ECONOMY

EMMIEs* = emerging market and middle-income economies

Advanced Countries Emerging and Middle-Income Countries

1.8 3.0 3.4 4.1 4.2 4.2 4.5 5.3 5.4 6.8 7.2 7.711.0 12.7

14.6 15.6 16.2 16.3 16.3 16.719.1

2.6

8.8

4.37.0 10.2 14.4 5.3 4.4 8.3 6.0 15.5

35.5 11.9 15.8

27.811.3

4.028.4 1.8

4.7

16.1

2.4

2.7

0

10

20

30

40

50

Den

mar

k

Fin

lan

d

Kore

a

Spai

n

Swed

en

Nor

way

Net

her

lan

ds

Swit

zerl

an

d

Czec

h R

ep

Ital

y

Belg

ium

Fran

ce

Ger

man

y

AEs

Cana

da

Jap

an

Aus

tral

ia

Sin

gap

ore UK

USA

New

Zea

land

% G

DP

0.7 1.1 1.2 1.6 2.0 2.2 2.3 2.4 2.4 2.5 2.5 2.7 2.9 3.1 3.6 3.8 4.1 4.4 4.7 5.4 5.56.4

7.7 8.2 8.3 8.3

0.8

1.39.0 1.7

0.10.0 0.8 3.2 3.1 0.5 0.0 0.9 0.9

1.5 5.12.5 1.9 5.7 3.9 1.3

9.6 4.2

0.0

5.41.8 4.3

6.2

0

3

6

9

12

15

18

Mex

ico

Tu

rke

y

Alb

ania

Egyp

t

Paki

stan

Sau

di

Ara

bia

Rom

ania

Kaza

khst

an

Tuni

sia

UA

E

Ph

ilip

pin

es

Indo

nesi

a

Russ

ia

Indi

a

EM

MIE

s

Arg

enti

na

Colo

mbi

a

Bu

lga

ria

Chin

a

Peru

Sout

h A

fric

a

Ge

org

ia

Pola

nd

Ch

ile

Th

aila

nd

Bra

zil

% G

DP

0

14

28

42

56

70

84

98

112

126

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

201

9

202

0

202

1

Angola

Egypt

South Africa

Morocco

Algeria

Nigeria

India

Pakistan

China

Malaysia

Turkey

Kazakhstan

Azerbaijan

Russia

Thailand

Philippines

Croatia

Hungary

Ukraine

Romania

Belarus

Brazil

Uruguay

Bolivia

Colombia

Ecuador

Peru

Chile

Mexico

Dominican Rep.

Oman

Islamic Re. of Iran

Un. Arab Emirates

Source: IMF WEO oct/20.

GLOBAL ECONOMYFiscal responseFiscal Policy

10

Historical pattern of general government debt(% of GDP)

Advanced Emerging

140

120

100

80

60

40

20

0

Gross Debt – emerging markets(% of GDP)

AFR

ICA

ASI

A E

X M

IDD

LE E

AST

EUR

OP

ELA

TIN

AM

ERIC

AM

IDD

LE E

AST

Brazil

11

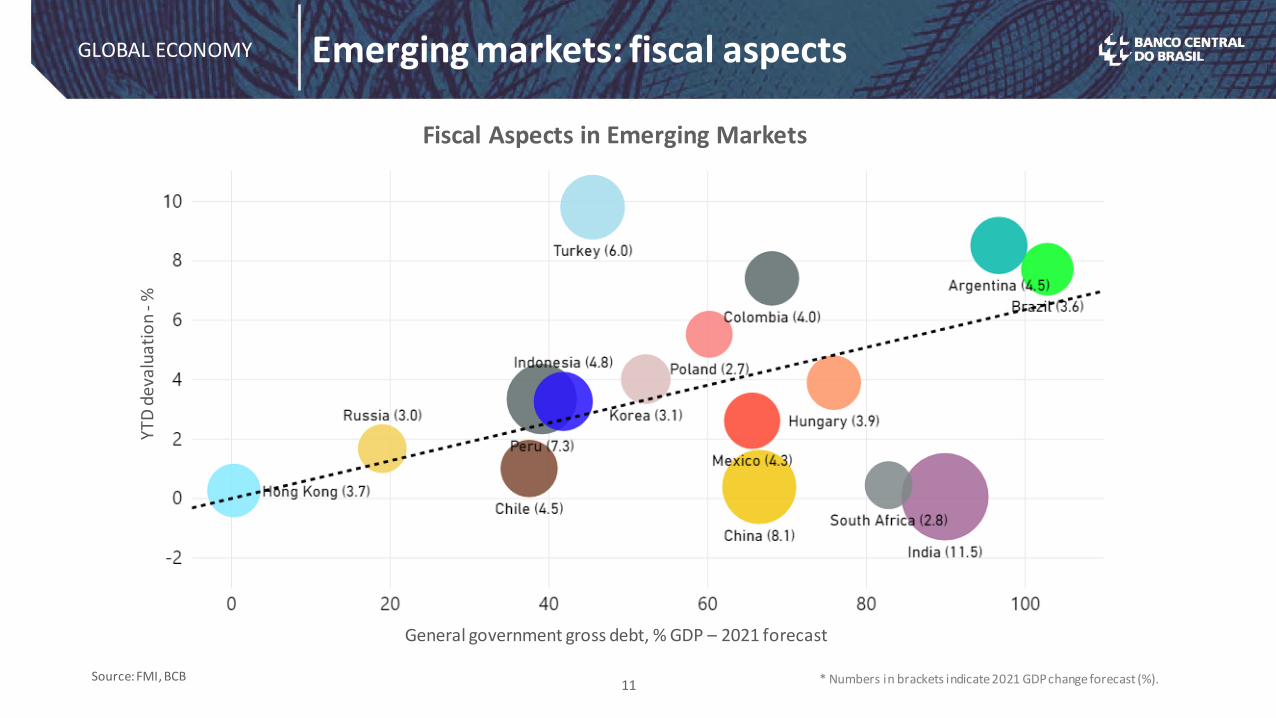

Emerging markets: fiscal aspects

Source: FMI, BCB

GLOBAL ECONOMY

* Numbers in brackets indicate 2021 GDP change forecast (%).

Fiscal Aspects in Emerging Markets

General government gross debt, % GDP – 2021 forecast

YT

D d

eval

uat

ion

-%

Differentiation in risk appetite for emerging economies with unfavorable economic fundamentals remains.

12

EME Group 1:Chile, Indonesia, Malaysia and Russia.

Gross Debt/GDP (average 2017-21) = 34.9%

EME Group 2:Brazil, Colombia, India, Mexico, South Africa and Turkey.

Gross Debt/GDP (average 2017-21) = 65%

Risk Appetite

GLOBAL ECONOMYRisk AppetiteMarkets

Sources: BCB, Bloomberg, Refinitiv, IMF, Fed St Louis. Gross Debt: IMF. Data up to March 31st.

-7

-6

-5

-4

-3

-2

-1

0

1

2

2017 2018 2019

stan

dar

d d

evi

atio

ns

to a

vera

ge

0

20

40

60

80

2017 2018 2019 2020F 2021F

% G

DP

Debt/GDPGroup 1 Group 2

-7.0

-6.0

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

Jan Mar May Jul Sep Nov Jan Mar

2020

Advanced

EME (Group 1)

EME (Group 2)

0.90

0.55

-1.45

2021

13

GLOBAL ECONOMYFinancial conditions and yieldsMarkets

Financial conditions more stimulative in the US. Increase in long term yields, especially in the US and the UK.

*Accumulated change since January 1st, 2021.

Change in 10-year yield* (YTD b.p.)

98

99

100

101

102

103

Jan-20 Mar-20 May-20 Jul-20 Sep-20 Nov-20 Jan-21 Mar-21

US Euro Area UK Japan

GS Financial Conditions Index

Source: Bloomberg

-5

25

55

85

Jan-21 Feb-21 Mar-21 Apr-21

USA UK Germany Japan

14

Inflation expectations

Source: Bloomberg

Implicit inflation (5-years break-even)

GLOBAL ECONOMYMarkets

-1

0

1

2

3

4

Apr-20 Jul-20 Oct-20 Jan-21 Apr-21

USA UK Germany Japan Australia

15

GLOBAL ECONOMYEmerging markets: yield curves Markets

Source: Bloomberg

Rat

e (%

)Va

riat

ion

(b.p

.)

sinc

e Ja

n 20

th

South Africa

Brazil

Colombia

Indonesia

MexicoRussia

Chile

Tenure

Yield curves Slope for 2 x 5 years (b.p.)

Yields and food inflation

Yields and food CPI – Selected countries

Source: Bloomberg

16

GLOBAL ECONOMY

Food CPI

98

102

106

110

114

118

Jul-20 Aug-20 Sep-20 Oct-20 Nov-20 Dec-20 Jan-21 Feb-21

Chile Brasil Mexico Turkey

Russia South Africa Colombia Indonesia

Brazil

Change in 5-year yield (YTD b.p.)

-35

65

165

265

365

465

565

665

-35

65

165

265

365

Jan-21 Jan-21 Mar-21 Apr-21

Brazil Chile Colombia Indonesia

Mexico Russia South Africa Turkey (right)

17

GLOBAL ECONOMYStock marketsMarkets

Source: Bloomberg

Stock markets performance

50

70

90

110

130

150

Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20 Oct-20 Nov-20 Dec-20 Jan-21 Feb-21 Mar-21

S&P Eurostoxx Mexico Chile Colombia Nikkei

Shanghai Indonesia India Russia South Africa Ibovespa

117.22

100.81

Commodities price: disagreggated

Brent, metals, iron ore and grains

Source: Bloomberg

18

GLOBAL ECONOMY

240

159

147

172

90

135

180

225

270

Brent Metals Index Grains Subindex Iron Ore

17.5%

5.1%

9.1%

2.0%

3.6%

0.0%

11.4%

8.0%

0%

4%

8%

12%

16%

20%

Brazil India IndonesiaMalaysia Mexico TurkeyColombia Australia

20.0%

14.9%

1.1%

0.2%

16.1%

1.4%

18.4%

5.3%4.3%

0%

4%

8%

12%

16%

20%

24%

Brazil Australia RussiaMalaysia Korea TurkeyArgentina Mexico India

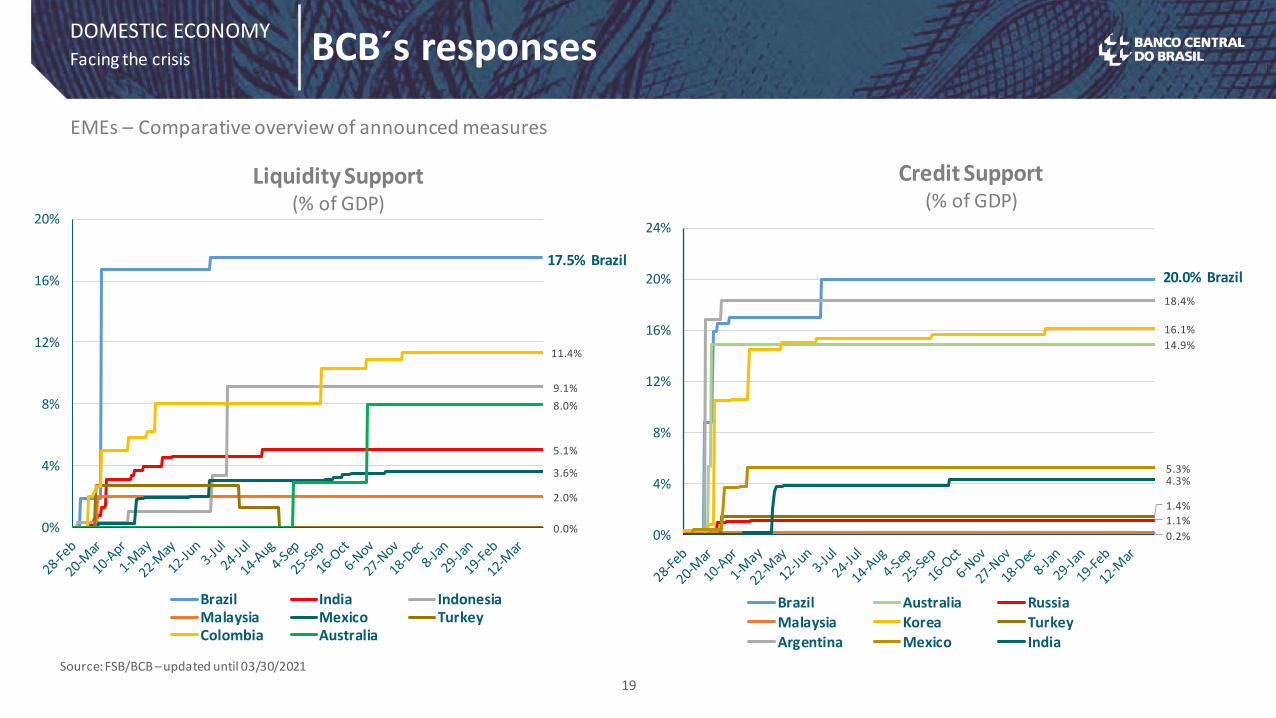

DOMESTIC ECONOMYBCB´s responsesFacing the crisis

EMEs – Comparative overview of announced measures

Source: FSB/BCB – updated until 03/30/2021

Liquidity Support(% of GDP)

Credit Support (% of GDP)

19

20.0% Brazil17.5% Brazil

86

88

90

92

94

96

98

100

102

I II III IV I II III IV I II III IV I II III IV I II III IV I II III IV I II III IV

2014 2015 2016 2017 2018 2019 2020

20

DOMESTIC ECONOMYBrazil: GDPEconomic Growth

Sources: IBGE and Focus Report (Apr 1st, 2021)

Forecast for 2021: +3.17%

(Median of market expectations; Focus report)

GDP(2019=100; s.a.)

2020: -4.1%

21

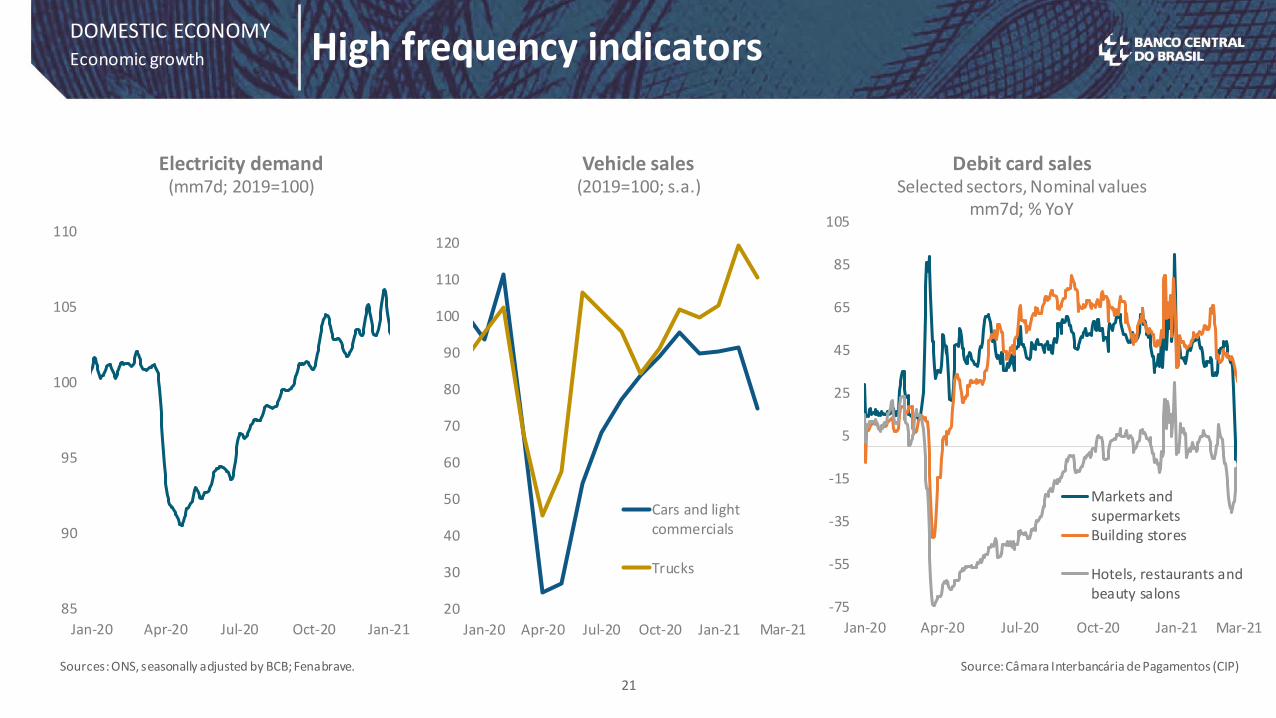

DOMESTIC ECONOMYHigh frequency indicatorsEconomic growth

Sources: ONS, seasonally adjusted by BCB; Fenabrave. Source: Câmara Interbancária de Pagamentos (CIP)

Vehicle sales(2019=100; s.a.)

20

30

40

50

60

70

80

90

100

110

120

Jan-20 Apr-20 Jul-20 Oct-20 Jan-21

Cars and lightcommercials

Trucks

Electricity demand(mm7d; 2019=100)

85

90

95

100

105

110

Jan-20 Apr-20 Jul-20 Oct-20 Jan-21

F -75

-55

-35

-15

5

25

45

65

85

105

Jan-20 Apr-20 Jul-20 Oct-20 Jan-21

Markets andsupermarketsBuilding stores

Hotels, restaurants andbeauty salons

Mar-21 Mar-21

Debit card salesSelected sectors, Nominal values

mm7d; % YoY

DOMESTIC ECONOMYConfidence indicators

Sources: FGV. Seasonally adjusted data.

22

< R$ 2.1 thousand

Business confidence X consumer confidence Consumer confidenceBy income range (in BRL thousand)

55

60

65

70

75

80

85

90

95

100

105

110

115

120

Sep-19 Mar-20 Sep-20 Mar-21

ManufacturingConstruction

Commerce

Services

Average 2018-2019=

100

55

60

65

70

75

80

85

90

95

100

105

110

115

120

Sep-19 Mar-20 Sep-20 Mar-21

Average 2018-2019= 100

> R$ 9.6 thousand

R$ 4.8 to 9.6 thousand

R$ 2.1 to 4.8 thousandConsumer

(6)

1

8

15

22

Feb-14 Feb-15 Feb-16 Feb-17 Feb-18 Feb-19 Feb-20 Feb-21Food at home Administered prices

Industrials goods Services

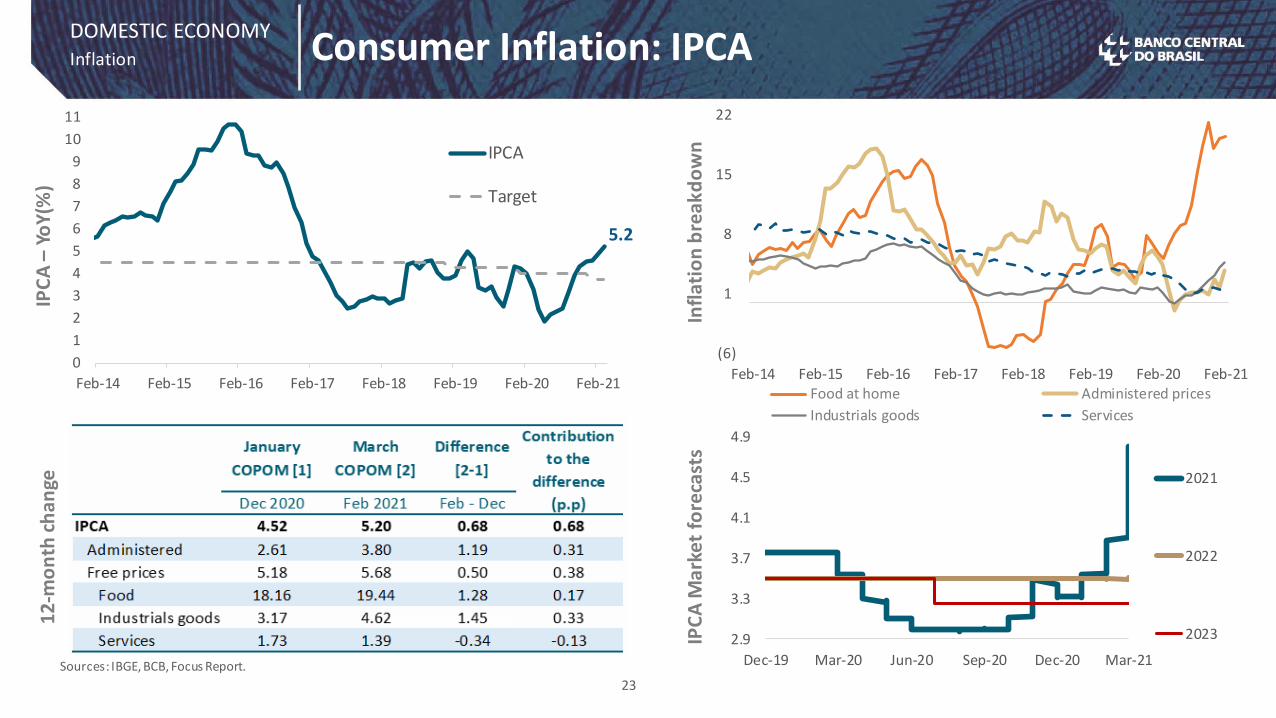

DOMESTIC ECONOMYConsumer Inflation: IPCAInflation

Sources: IBGE, BCB, Focus Report.

23

5.2

0

1

2

3

4

5

6

7

8

9

10

11

Feb-14 Feb-15 Feb-16 Feb-17 Feb-18 Feb-19 Feb-20 Feb-21

IPCA

Target

IPC

A –

YoY

(%)

2.9

3.3

3.7

4.1

4.5

4.9

Dec-19 Mar-20 Jun-20 Sep-20 Dec-20 Mar-21

2021

2022

2023

12-m

on

th c

ha

nge

Infl

ati

on

bre

akd

ow

nIP

CA

Mar

ket

fore

cast

s

24

Implicit inflation

Sources: BCB. Rates estimated from DAP.

Inflation expectations – Brazil

DOMESTIC ECONOMYInflation

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

Break-even 2023 Break-even 2024

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

Break-even 2021 Break-even 2022

Implicit Inflation

0%

1%

2%

3%

4%

5%

6%

-100%

-50%

0%

50%

100%

150%

200%

05/0

2/2

0

05/2

3/2

0

06/1

3/2

0

07/0

4/2

0

07/2

5/2

0

08/1

5/2

0

09/0

5/2

0

09/2

6/2

0

10/1

7/2

0

11/0

7/2

0

11/2

8/2

0

12/1

9/2

0

01/0

9/2

1

01/3

0/2

1

02/2

0/2

1

03/1

3/2

1

100%

70%

40%

10%

-20%

-50%

25

Implicit inflation and commodities

Source: Bloomberg.

DOMESTIC ECONOMY

CRB Food and WTI vs. implicit inflation 12 months ahead

WTI (BRL) _% change (y/y) CRB Food (BRL)_% change (y/y) Implicit inflation (right)

Bre

ak-e

ven

infl

atio

n –

12 m

on

ths

ahe

ad (

% y

/y)

CR

B F

oo

d (

BR

L) %

ch

ange

(y/

y)

WTI

(B

RL)

% c

han

ge (

y/y)

30

32

34

36

38

40

Feb-17 Aug-17 Feb-18 Aug-18 Feb-19 Aug-19 Feb-20 Aug-20 Feb-21

Caged PNADC-CC

11.4

14.2

61.9

56.9

54

55

56

57

58

59

60

61

62

63

64

10.0

10.5

11.0

11.5

12.0

12.5

13.0

13.5

14.0

14.5

15.0

jan-17 jul-17 jan-18 jul-18 jan-19 jul-19 jan-20 jul-20 jan-21

Unemployment rate

Participation rate (right axis)

DOMESTIC ECONOMYLabor market: formal vs informalLabor market

Source: IBGE (PNAC-C mensalizada). Data is seasonally adjusted by BCB. Source: Ministry of Economy (CAGED). Data is seasonally adjusted by BCB.

26

-135

-75

-15

45

105

Feb-18 Aug-18 Feb-19 Aug-19 Feb-20 Aug-20 Feb-21

Manufacturing

Building

Commerce

Accommodation and maintenance

Unemployment and participation rate (%)

Net formal job creation by sector(3-month-moving average, in thousands of jobs)

Formal Jobs – Caged vs PnadC(millions of workers)

DOMESTIC ECONOMY

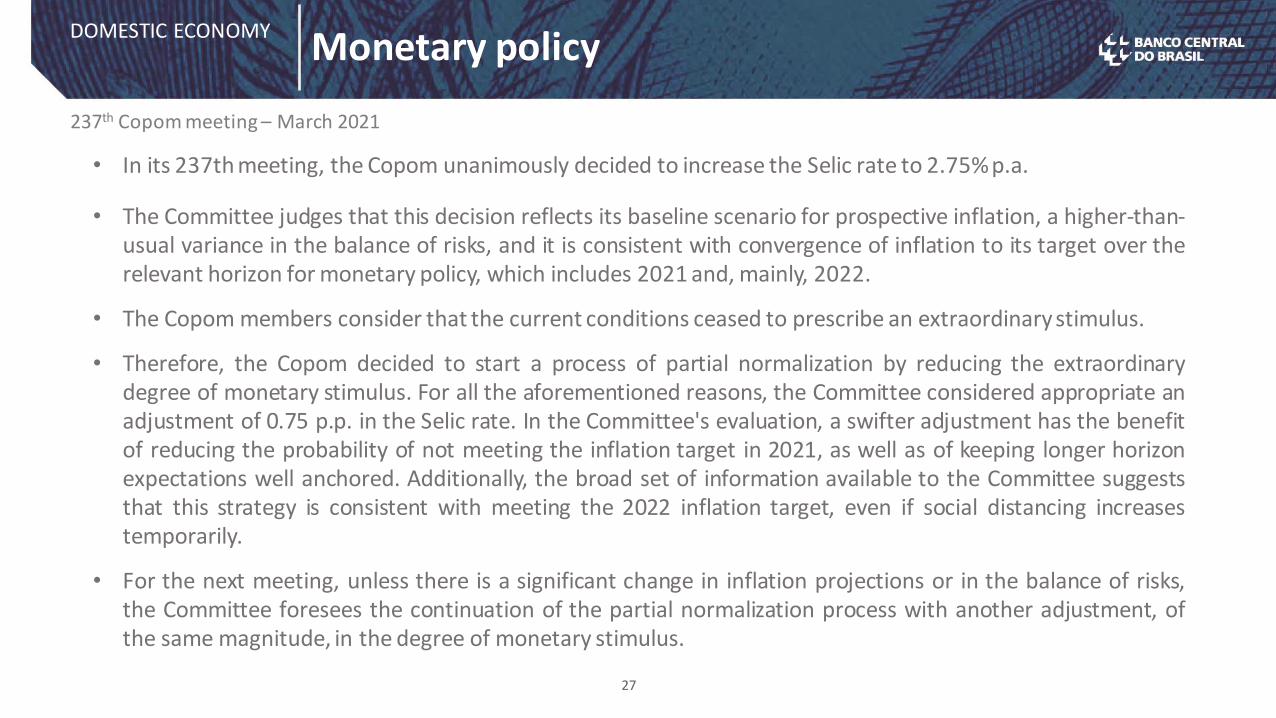

27

• In its 237th meeting, the Copom unanimously decided to increase the Selic rate to 2.75%p.a.

• The Committee judges that this decision reflects its baseline scenario for prospective inflation, a higher-than-usual variance in the balance of risks, and it is consistent with convergence of inflation to its target over therelevant horizon for monetary policy, which includes 2021 and, mainly, 2022.

• The Copom members consider that the current conditions ceased to prescribe an extraordinary stimulus.

• Therefore, the Copom decided to start a process of partial normalization by reducing the extraordinarydegree of monetary stimulus. For all the aforementioned reasons, the Committee considered appropriate anadjustment of 0.75 p.p. in the Selic rate. In the Committee's evaluation, a swifter adjustment has the benefitof reducing the probability of not meeting the inflation target in 2021, as well as of keeping longer horizonexpectations well anchored. Additionally, the broad set of information available to the Committee suggeststhat this strategy is consistent with meeting the 2022 inflation target, even if social distancing increasestemporarily.

• For the next meeting, unless there is a significant change in inflation projections or in the balance of risks,the Committee foresees the continuation of the partial normalization process with another adjustment, ofthe same magnitude, in the degree of monetary stimulus.

Monetary policy

237th Copom meeting – March 2021

Sources: B3, Anbima, Demab.

28

LFT

DOMESTIC ECONOMYFiscal riskFiscal policy

Risk premia in government bonds

LTN

-5

0

5

10

15

20

25

30

35

40

Bas

e p

oin

ts

Jul-21 Oct-21 Oct-22 Jul-23 Jan-24

0

5

10

15

20

25

30

35

40

45

Bas

e po

ints

Sep-21 Mar-22 Mar-23 Mar-24 Mar-25 Mar-26

DOMESTIC ECONOMY

29

Debt and nonresident participationFiscal policy

Federal Domestic Public Debt

Sources: B3, BCB.

0

50

100

150

200

250

300

350

400

450

500

550

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

R$

bill

ion

% o

f FD

PD

FDPD

NTN-F LTN NTN-B LFT Non resident participants

DOMESTIC ECONOMY

30

Govnt. bonds: cost and maturity structureFiscal policy

Sources: B3, BCB.

Issuance cost - FDPDMaturity structure

Feb

-11

Aug

-11

Feb-

12

Aug

-12

Feb

-13

Aug

-13

Feb

-14

Aug

-14

Feb-

15

Aug

-15

Feb

-16

Aug

-16

Feb

-17

Aug

-17

Feb-

18

Aug

-18

Feb

-19

Aug

-19

Feb-

20

Aug

-20

Feb

-21

14%

17%

20%

23%

26%

29%

32%

35%

% maturity in 12 months % maturity over 5 years

Feb

-11

Aug

-11

Feb

-12

Aug

-12

Feb

-13

Aug

-13

Feb

-14

Aug

-14

Feb

-15

Aug

-15

Feb

-16

Aug

-16

Feb

-17

Aug

-17

Feb

-18

Aug

-18

Feb

-19

Aug

-19

Feb

-20

Aug

-20

Feb

-21

4

6

8

10

12

14

16

Ra

tes

% p

.y.

Issue Cost FDPD in 12 months

Average Cost FDPD acc. 12 months

26.8%

18.6%

31

DOMESTIC ECONOMYStock marketsMarkets

Source: B3

Accumulated flows into the stock market

-100

-80

-60

-40

-20

0

20

40

60

80

100

Jan-20 Mar-20 May-20 Jul-20 Sep-20 Nov-20 Jan-21 Mar-21

Individuals Institutionals Foreigners

BRL billions

BRL -18.4 bi

BRL -31.5 bi

BRL +67.1 bi

62%

47%

53%

31%

43%40%

51%58%

38%

27%29%

0%

10%

20%

30%

40%

50%

60%

70%

80%

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

IPO/Follow-on - Foreign Investors’ share

32

DOMESTIC ECONOMYStock marketsMarkets

Source: B3, Anbima

33

DOMESTIC ECONOMYForeign exchange derivativesMarkets

Source: B3

Investors’ position change in foreign exchange derivatives at B3

-45

-35

-25

-15

-5

5

15

25

35

45

Mar-20 Jun-20 Sep-20 Dec-20 Mar-21

Institucionals Non-residents Banks Central Bank

USD Bln

External sector

34

Current account12 month accumulated, % of GDP

-6.0%

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

Feb-08 Feb-10 Feb-12 Feb-14 Feb-16 Feb-18 Feb-20

Trade balance Services Income Current account

DOMESTIC ECONOMY

Fonte: BCB, Bloomberg.

Effective foreign exchange rate and terms of trade

-15

-10

-5

0

5

10

15

200

1

2

3

4

5

Mar-07 Mar-09 Mar-11 Mar-13 Mar-15 Mar-17 Mar-19 Mar-21

20%

12%

25%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Feb-17 Feb-18 Feb-19 Feb-20 Feb-21

Cen

ten

as35

16.1%

22.9%

11.3%

-11%

-6%

-1%

4%

9%

14%

19%

24%

Feb-17 Feb-18 Feb-19 Feb-20 Feb-21

DOMESTIC ECONOMYCredit in the National Financial SystemCredit Market

Credit increase amid the crisis. Interest rates at historically low levels.

Source: BCB

Households Corporate Total

Interest rates(% per year)

Outstanding credit(YoY)

TechnologyAgenda

36

37

INCLUSION

COMPETITIVENESS

TRANSPARENCY

EDUCATION

InnovationMarket efficiencyInternational reserves

Rural creditHousing creditRelationship with CongressTransparency of Monetary PolicyCommunication plan for BCB actionsRelationship with foreign investors

Financial education

Cooperative creditMicrocreditCurrency convertibilityInitiatives for capital market

SUSTAINABILITYBCB’s S&E responsibilityRegulationSupervisionPartnerships

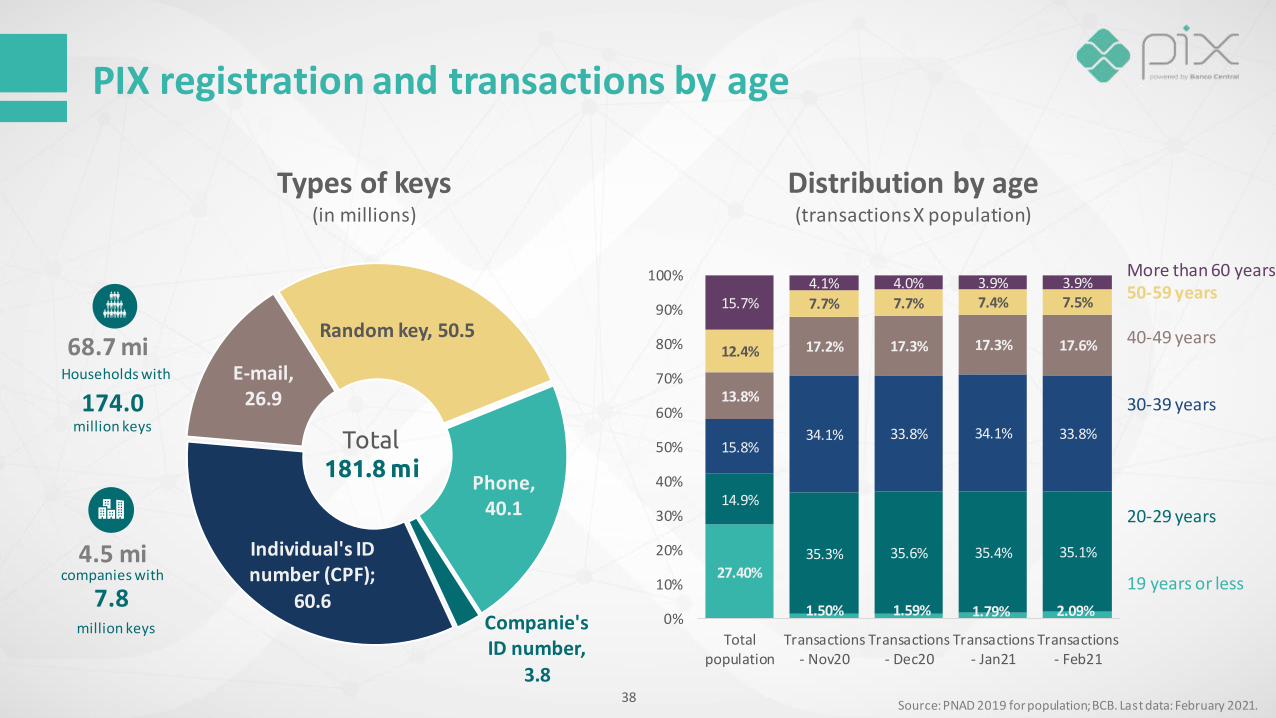

Random key, 50.5

Phone, 40.1

Companie's ID number,

3.8

Individual's ID number (CPF);

60.6

E-mail, 26.9

PIX registration and transactions by age

38Source: PNAD 2019 for population; BCB. Last data: February 2021.

Households with

million keysTotal

181.8 mi

Types of keys(in millions)

Distribution by age(transactions X population)

27.40%

1.50% 1.59% 1.79% 2.09%

14.9%

35.3% 35.6% 35.4% 35.1%

15.8%34.1% 33.8% 34.1% 33.8%

13.8%

17.2% 17.3% 17.3% 17.6%12.4%

7.7% 7.7% 7.4% 7.5%15.7%4.1% 4.0% 3.9% 3.9%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Totalpopulation

Transactions- Nov20

Transactions- Dec20

Transactions- Jan21

Transactions- Feb21

68.7 mi

174.0

4.5 mi

7.8companies with

million keys

More than 60 years50-59 years

40-49 years

30-39 years

20-29 years

19 years or less

33.5 mi 144.5 mi 200.3 275.3

R$29.6 bi

R$121.5 bi

R$160.1

R$197.7

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

200.0

220.0

- 10.0 20.0 30.0 40.0 50.0 60.0 70.0 80.0 90.0

100.0 110.0 120.0 130.0 140.0 150.0 160.0 170.0 180.0 190.0 200.0 210.0 220.0 230.0 240.0 250.0 260.0 270.0 280.0 290.0

nov-20 dez-20 jan-21 fev-21

Number of transactions (millions) Volume (R$ billions)

Pix transactions

39Fonte: BCB.

PIX average value

Pix versus other instruments(in million of transactions and% of total)

R$ 778.4 /PIX

Number of transactions and volume(in million of transactions and BRL billions)

(19%)

(60%)

(21%)33.5 (22.2%)

144.5 (41.2%)

200.3 (59.4%)

275.3 (71%)

95.1 (63%)

189.3 (54%) 122.7 (36.4%)

104.5 (27%)

22.4 (14.8%)

16.8 (4.8%) 14.5 (4.3%)

7.8 (2%)

-

49

98

147

196

245

294

343

392

16 - 30Nov20

Dec20 Jan21 Feb21

Pix TED DOC

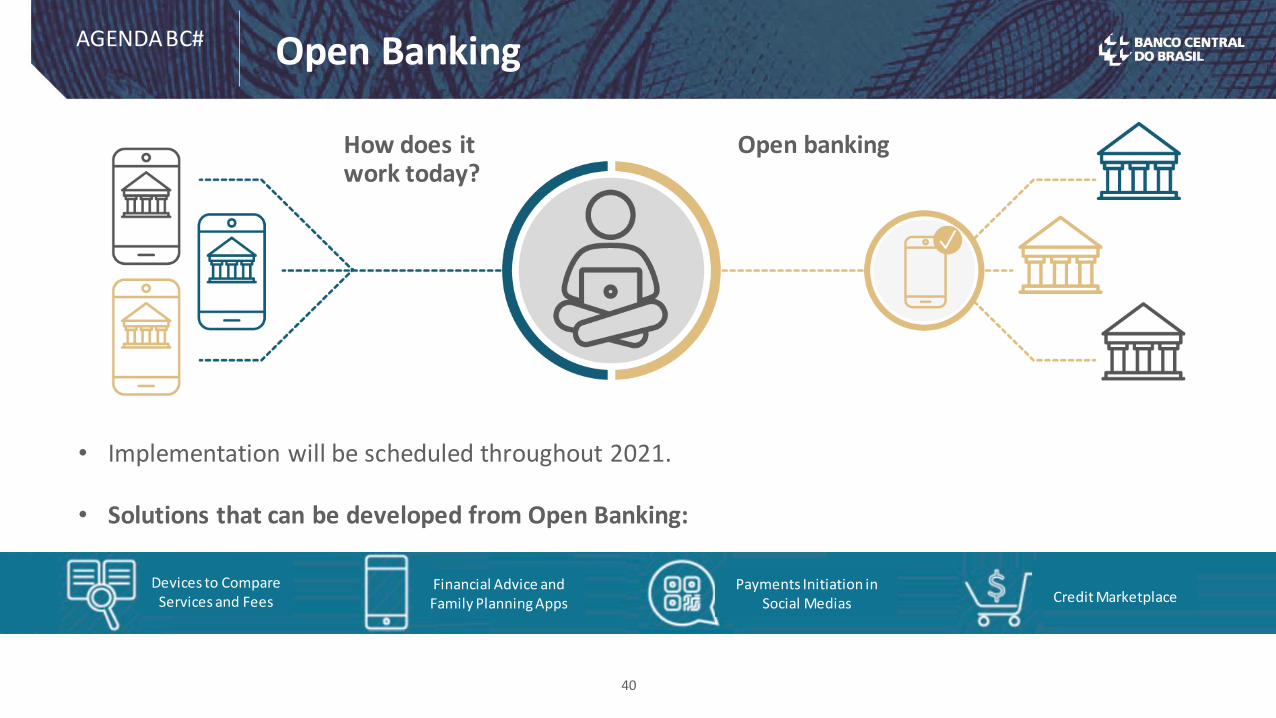

How does it work today?

Open banking

40

Open BankingAGENDA BC#

Devices to Compare Services and Fees

Financial Advice and Family Planning Apps

Payments Initiation in Social Medias Credit Marketplace

• Implementation will be scheduled throughout 2021.

• Solutions that can be developed from Open Banking:

41

Regulatory SandboxAGENDA BC#

BCB’s Regulatory Sandbox starts in 2021 with the Cycle 1.

During the sandbox licensing process, BCB will assess whether the submitted projects comply with the definition of innovative project and whether their development is under the regulatory scope of BCB and CMN, among other criteria.

Legal persons, notary and registration service providers, public companies, and semi-public companies can participate, even when not yet fully licensed by BCB.

Simplified monitoring procedures will be adopted, considering the complexity and risks associated to each innovative project and, should BCB deems appropriate, additional limits and criteria may be applied.

By the end of cycle 1, participants may obtain a permanent license from BCB to operate. The projects may be a stepping stone for the improvement of the regulation issued by BCB and CMN.

TO UNDERSTAND THE REGULATORY SANDBOX

42

Text

Payments

Content

Financial Innovation

Intensive use of clouding

ConvergenceAGENDA BC#

43

Digital currencyOpen Banking

• Simplification• Internationalization• Convertibility

Innovation in the currency

2021/2022

Innovation in the financial systemAGENDA BC#

Measures:

• BCB’s S&E Responsibility

• Partnerships

• Policies

• Supervision

• Regulation

Sustainability

Common factors in recoveryMore sustainable and more inclusive growth

More technologyThe epidemic has accelerated technological change

in medicine, education, finance, communication

Low interest rates and high liquidity in the world

There are challenges, but also opportunities to reinvent the economy with private resources

Changes in global value chains

World trade

Vision for the future

Impact of possible reflation global conditions on EMEs

Thank you!

Roberto Campos NetoGovernor of Banco Central do Brasil

April 09, 2021