© 2004 the mcgraw-hill companies, inc. mcgraw-hill/irwin chapter 22 statement of cash flows...

Post on 20-Dec-2015

214 views

TRANSCRIPT

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Chapter 22

Statement of Cash Flows Revisited

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-2

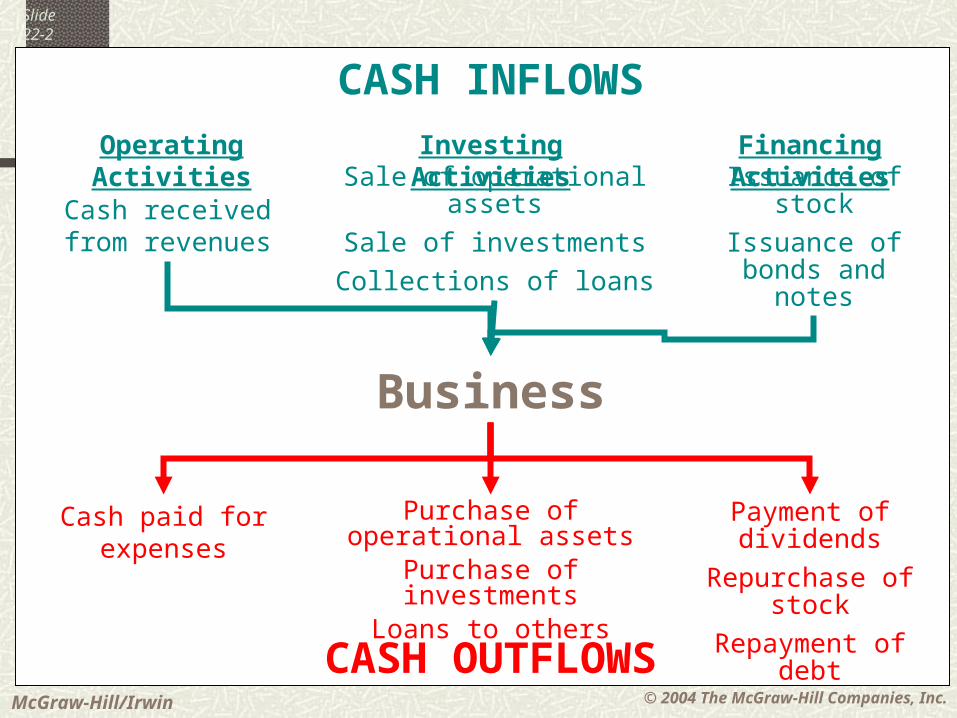

Investing ActivitiesOperating Activities Financing ActivitiesSale of operational assets

Sale of investments

Collections of loans

Cash received from revenues

Issuance of stock

Issuance of bonds and notes

CASH INFLOWS

Business

CASH OUTFLOWS

Purchase of operational assets

Purchase of investmentsLoans to others

Cash paid for expenses

Payment of dividends

Repurchase of stock

Repayment of debt

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-3 Role of the Statement of Cash

Flows

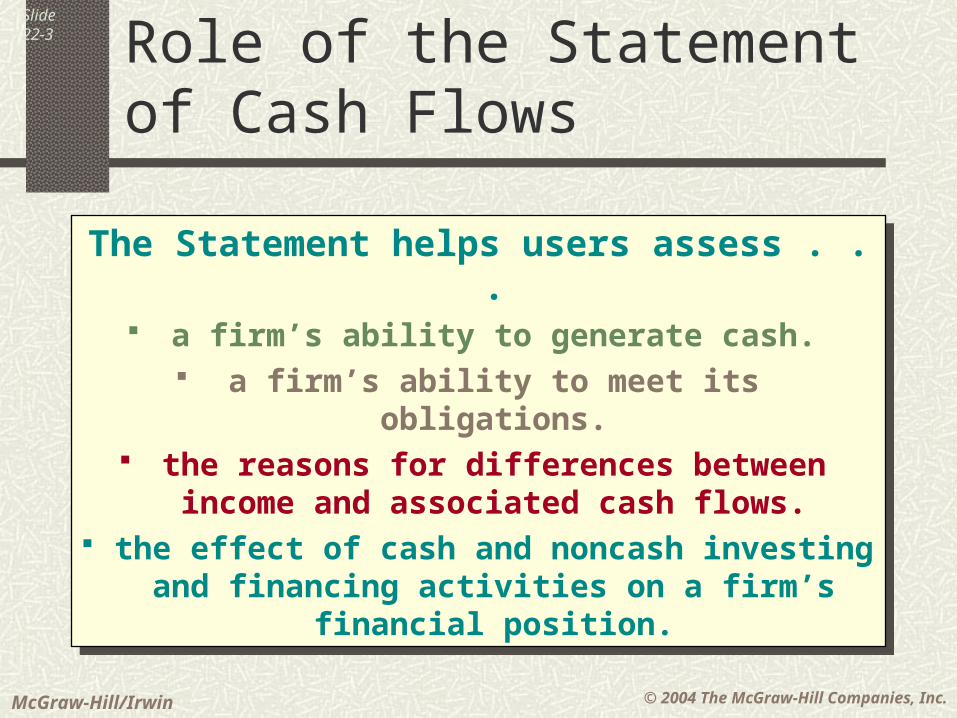

The Statement helps users assess . . . a firm’s ability to generate cash.

a firm’s ability to meet its obligations. the reasons for differences between

income and associated cash flows. the effect of cash and noncash investing

and financing activities on a firm’s financial position.

The Statement helps users assess . . . a firm’s ability to generate cash.

a firm’s ability to meet its obligations. the reasons for differences between

income and associated cash flows. the effect of cash and noncash investing

and financing activities on a firm’s financial position.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-4

Statement of Cash Flows . . .

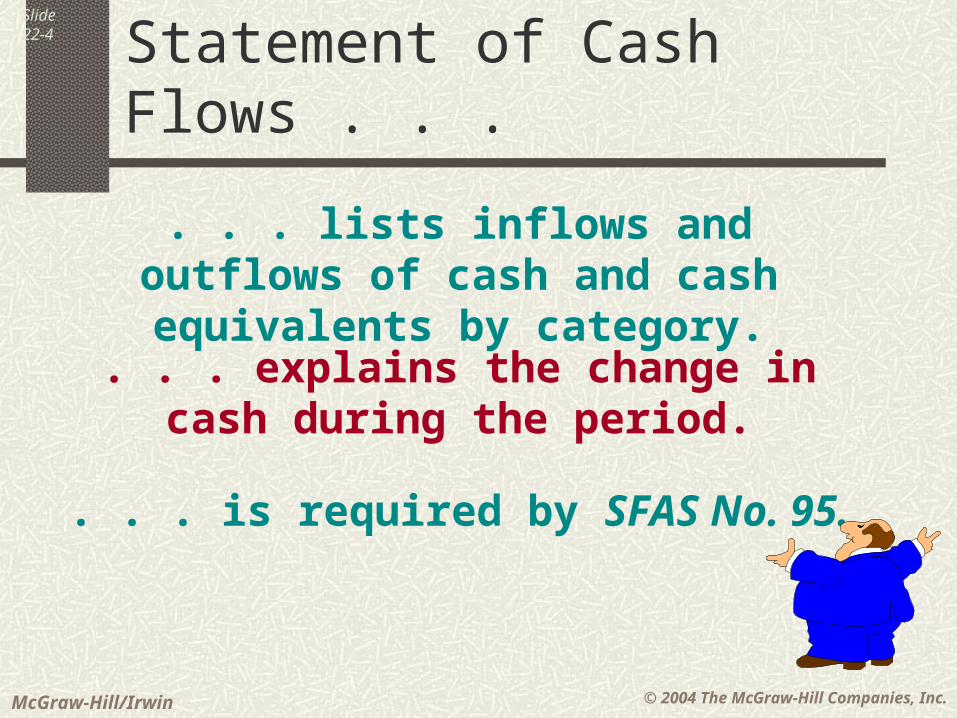

. . . is required by SFAS No. 95.

. . . lists inflows and outflows of cash and cash equivalents by category.

. . . explains the change in cash during the period.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-5

Cash and Cash Equivalents

Resources immediately available to

pay obligations.

Resources immediately available to

pay obligations.

Short-term, highly liquid investments. Readily convertible into known, fixed amounts of cash. So near maturity that there is insignificant risk of market value fluctuation from interest rate changes.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-6 Primary Elements of the

Statement of Cash Flows (SCF)

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

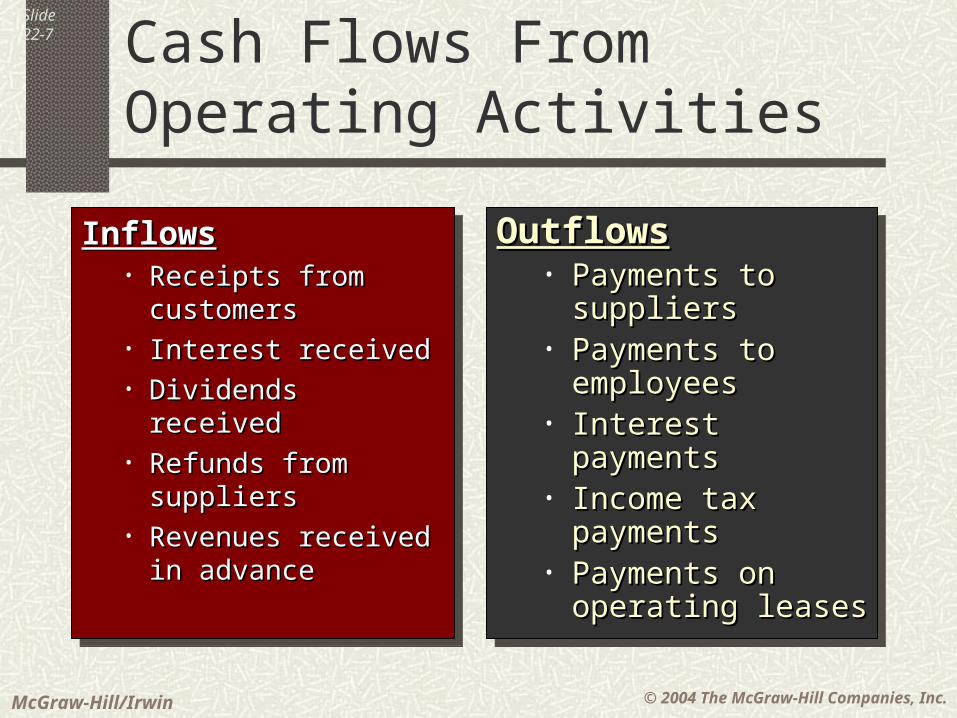

Slide22-7 Cash Flows From Operating

Activities

InflowsInflows• Receipts from Receipts from

customerscustomers• Interest receivedInterest received• Dividends receivedDividends received• Refunds from Refunds from

supplierssuppliers• Revenues received Revenues received

in advancein advance

InflowsInflows• Receipts from Receipts from

customerscustomers• Interest receivedInterest received• Dividends receivedDividends received• Refunds from Refunds from

supplierssuppliers• Revenues received Revenues received

in advancein advance

OutflowsOutflows• Payments to Payments to

supplierssuppliers• Payments to Payments to

employeesemployees• Interest paymentsInterest payments• Income tax Income tax

paymentspayments• Payments on Payments on

operating leasesoperating leases

OutflowsOutflows• Payments to Payments to

supplierssuppliers• Payments to Payments to

employeesemployees• Interest paymentsInterest payments• Income tax Income tax

paymentspayments• Payments on Payments on

operating leasesoperating leases

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

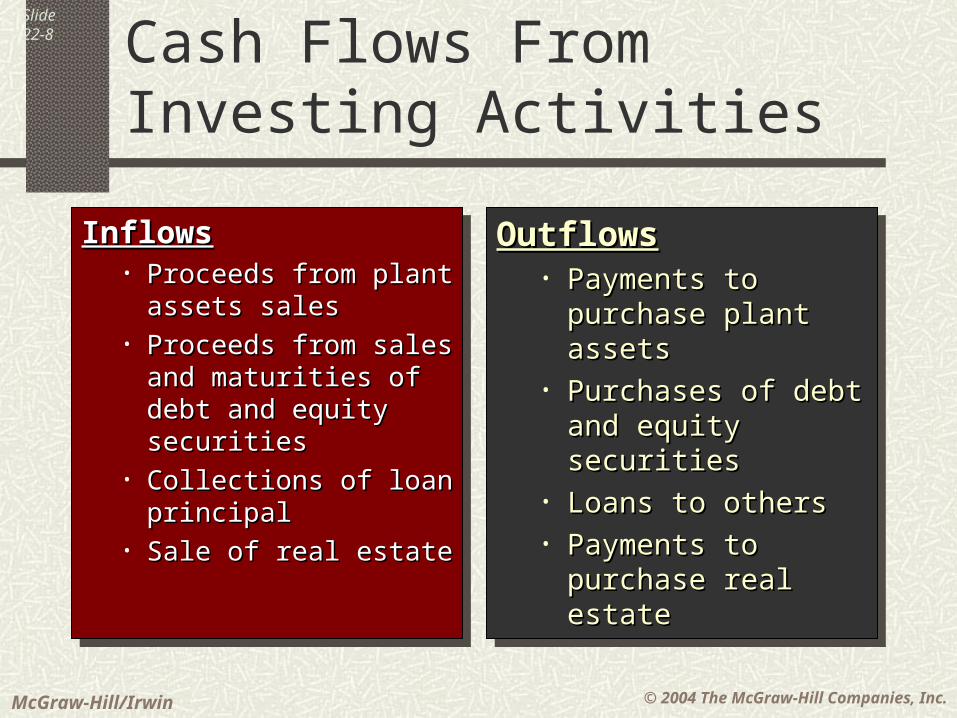

Slide22-8 Cash Flows From Investing

Activities

InflowsInflows• Proceeds from plant Proceeds from plant

assets salesassets sales• Proceeds from sales Proceeds from sales

and maturities of and maturities of debt and equity debt and equity securitiessecurities

• Collections of loan Collections of loan principalprincipal

• Sale of real estateSale of real estate

InflowsInflows• Proceeds from plant Proceeds from plant

assets salesassets sales• Proceeds from sales Proceeds from sales

and maturities of and maturities of debt and equity debt and equity securitiessecurities

• Collections of loan Collections of loan principalprincipal

• Sale of real estateSale of real estate

OutflowsOutflows• Payments to Payments to

purchase plant purchase plant assetsassets

• Purchases of debt Purchases of debt and equity securitiesand equity securities

• Loans to othersLoans to others• Payments to Payments to

purchase real estatepurchase real estate

OutflowsOutflows• Payments to Payments to

purchase plant purchase plant assetsassets

• Purchases of debt Purchases of debt and equity securitiesand equity securities

• Loans to othersLoans to others• Payments to Payments to

purchase real estatepurchase real estate

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

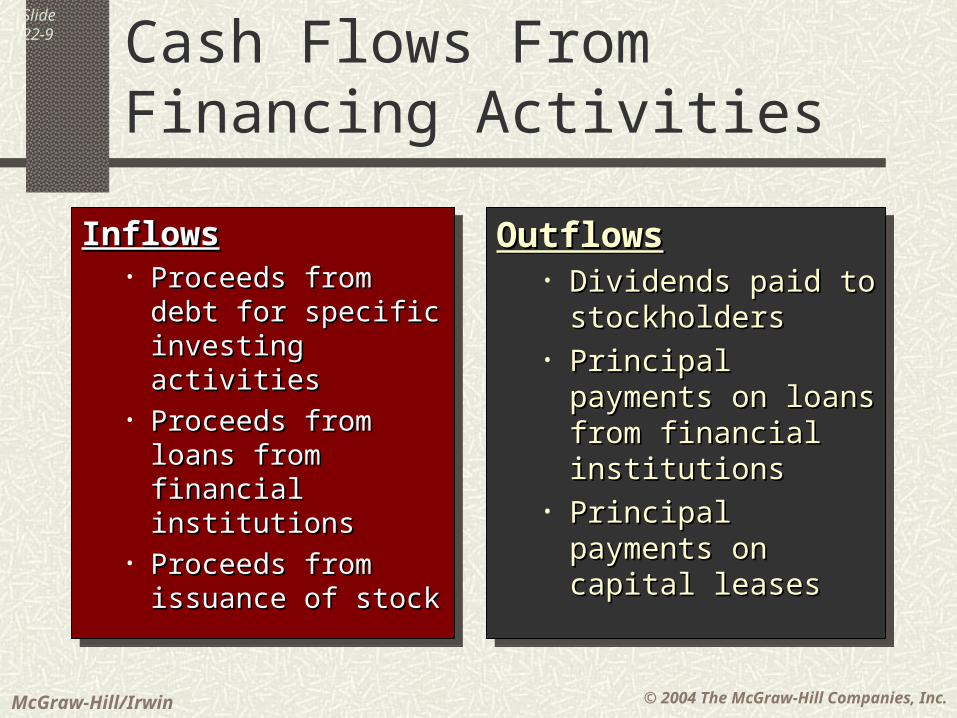

Slide22-9 Cash Flows From Financing

Activities

InflowsInflows• Proceeds from debt Proceeds from debt

for specific for specific investing activitiesinvesting activities

• Proceeds from Proceeds from loans from financial loans from financial institutionsinstitutions

• Proceeds from Proceeds from issuance of stockissuance of stock

InflowsInflows• Proceeds from debt Proceeds from debt

for specific for specific investing activitiesinvesting activities

• Proceeds from Proceeds from loans from financial loans from financial institutionsinstitutions

• Proceeds from Proceeds from issuance of stockissuance of stock

OutflowsOutflows• Dividends paid to Dividends paid to

stockholdersstockholders• Principal payments Principal payments

on loans from on loans from financial institutionsfinancial institutions

• Principal payments Principal payments on capital leaseson capital leases

OutflowsOutflows• Dividends paid to Dividends paid to

stockholdersstockholders• Principal payments Principal payments

on loans from on loans from financial institutionsfinancial institutions

• Principal payments Principal payments on capital leaseson capital leases

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

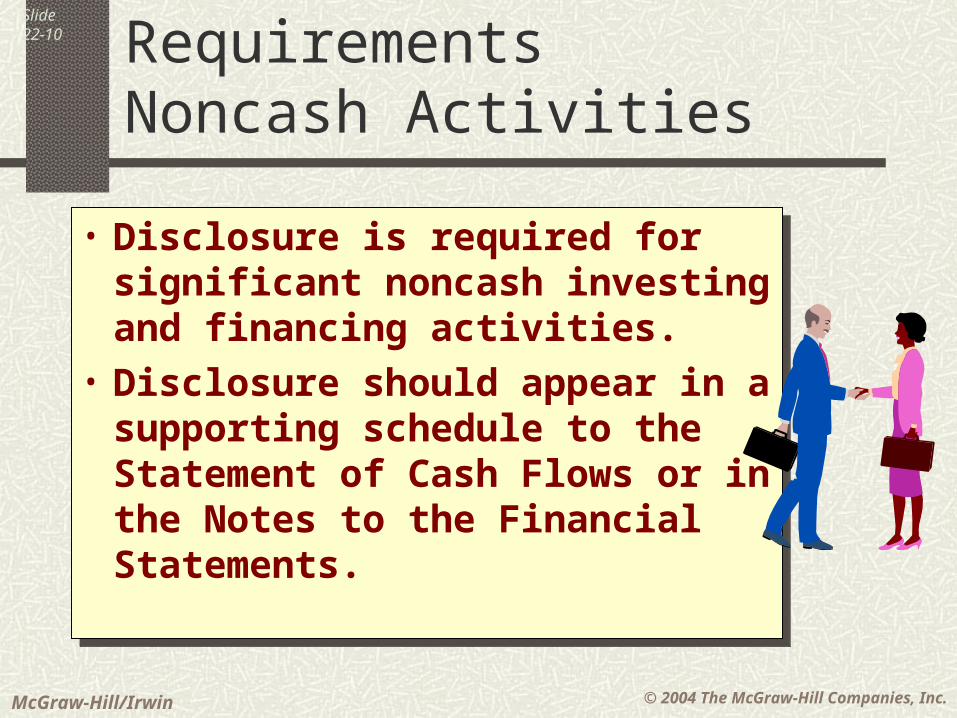

Slide22-10 SFAS No. 95 Requirements

Noncash Activities

• Disclosure is required for significant noncash investing and financing activities.

• Disclosure should appear in a supporting schedule to the Statement of Cash Flows or in the Notes to the Financial Statements.

• Disclosure is required for significant noncash investing and financing activities.

• Disclosure should appear in a supporting schedule to the Statement of Cash Flows or in the Notes to the Financial Statements.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

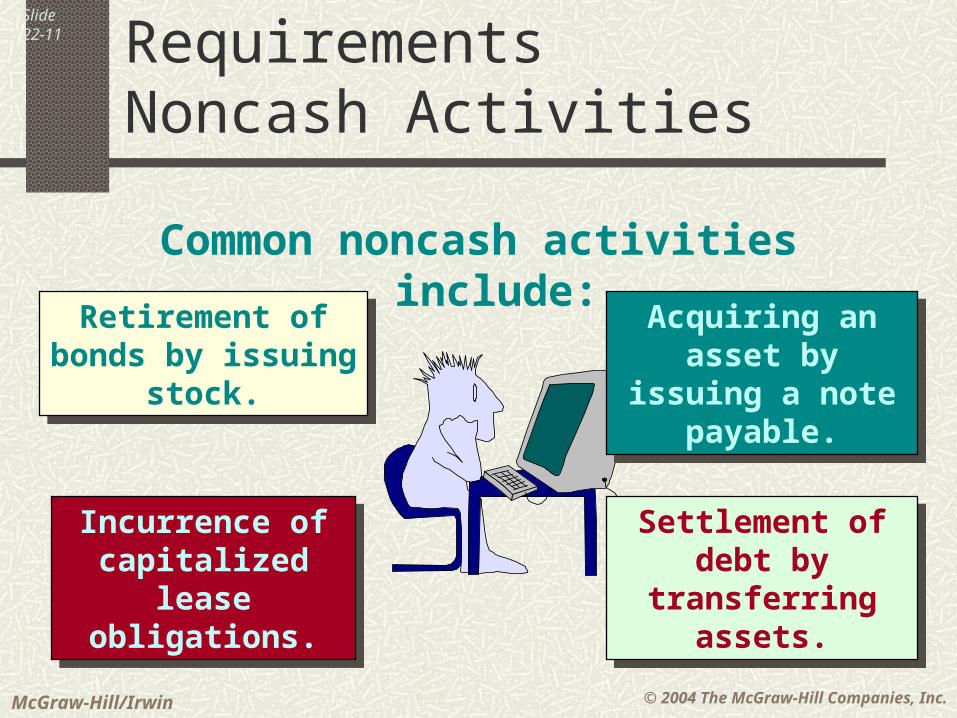

Slide22-11 SFAS No. 95 Requirements

Noncash Activities

Common noncash activities include:

Retirement of bonds by issuing

stock.

Retirement of bonds by issuing

stock.

Settlement of debt by transferring

assets.

Settlement of debt by transferring

assets.

Acquiring an asset by issuing a note

payable.

Acquiring an asset by issuing a note

payable.

Incurrence of capitalized lease

obligations.

Incurrence of capitalized lease

obligations.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

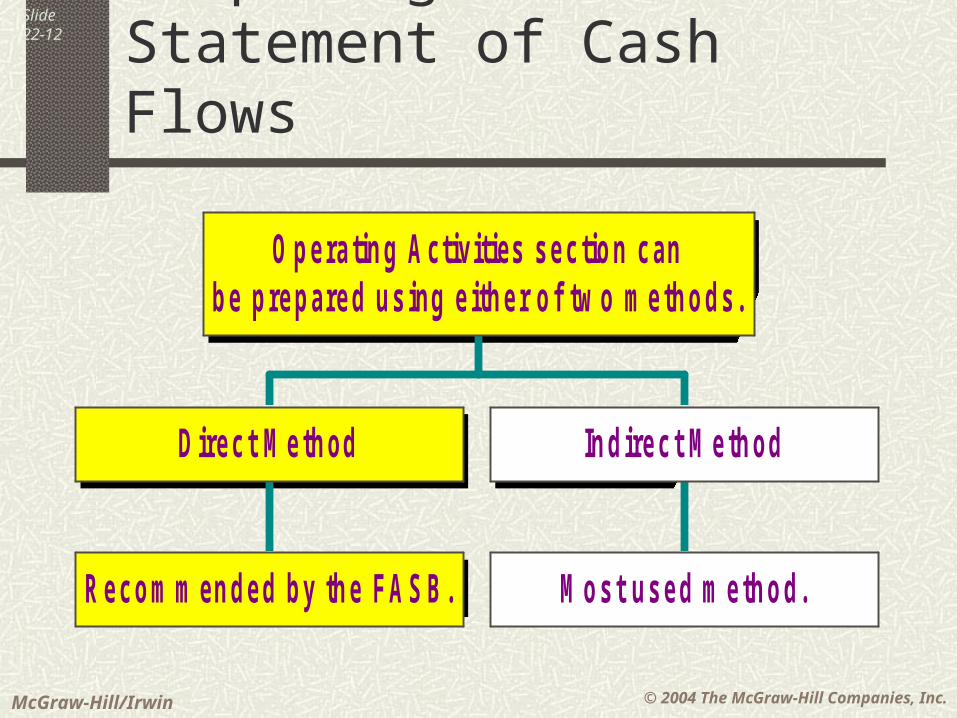

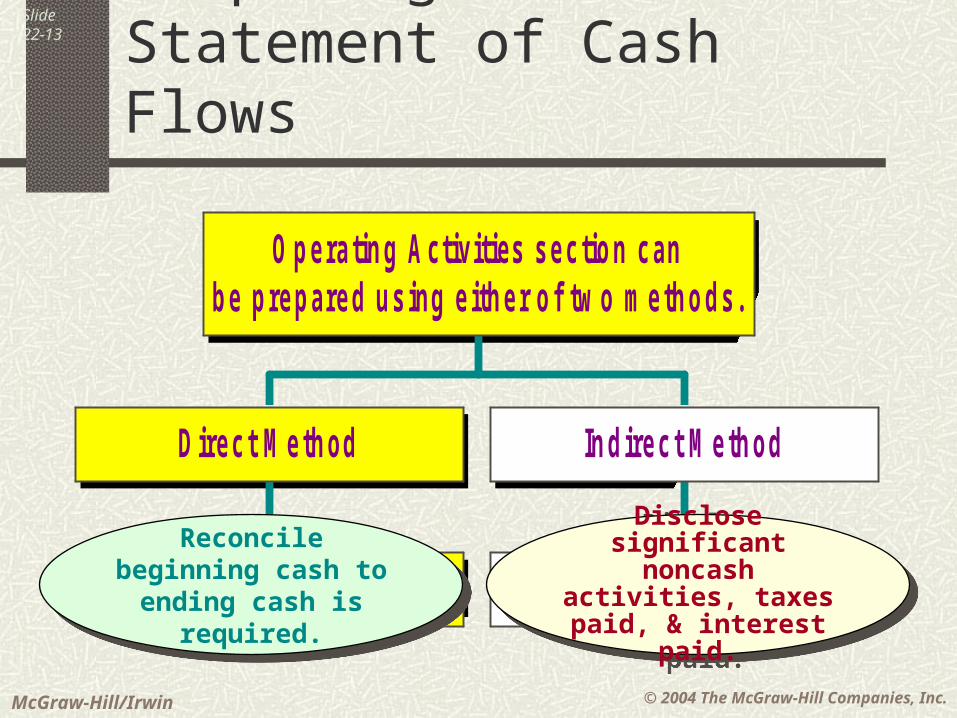

Slide22-12 Preparing the Statement of Cash

Flows

Recom m ended by the FASB.

Direct M ethod

M ost used m ethod.

Indirect M ethod

Operating Activities section canbe prepared using either of tw o methods.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-13 Preparing the Statement of Cash

Flows

Recom m ended by the FASB.

Direct M ethod

M ost used m ethod.

Indirect M ethod

Operating Activities section canbe prepared using either of tw o methods.

Reconcile beginning cash to ending cash

is required.

Reconcile beginning cash to ending cash

is required.

Disclose significant noncash activities,

taxes paid, & interest paid.

Disclose significant noncash activities,

taxes paid, & interest paid.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-14

Let’s look at the Direct Method for

preparing the Cash Flows from

Operating Activities section.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-15 Direct Method

Analyzing Sales Revenue

The key information is cash collected from customers.

Can be computed two ways: Obtained from cash receipts journal. Obtained from accrual sales information.

Collections Accrual-basis + Decrease in net A/Ron Account Revenues - Increase in net A/R= {

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

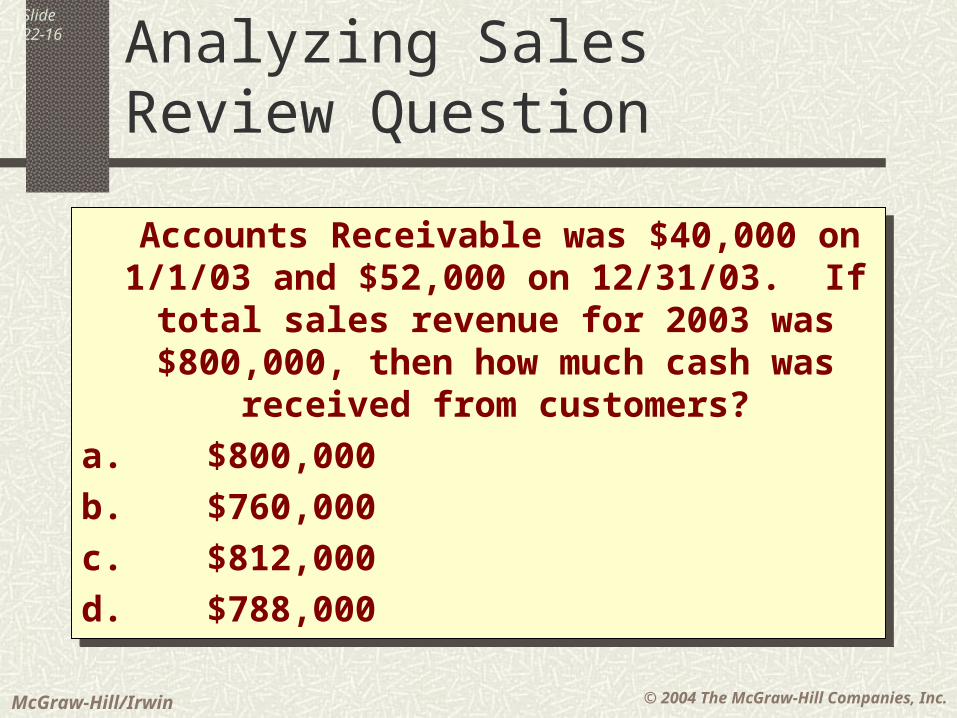

Slide22-16 Analyzing Sales

Review Question

Accounts Receivable was $40,000 on 1/1/03 and $52,000 on 12/31/03. If total sales

revenue for 2003 was $800,000, then how much cash was received from customers?

a.$800,000

b.$760,000

c.$812,000

d.$788,000

Accounts Receivable was $40,000 on 1/1/03 and $52,000 on 12/31/03. If total sales

revenue for 2003 was $800,000, then how much cash was received from customers?

a.$800,000

b.$760,000

c.$812,000

d.$788,000

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

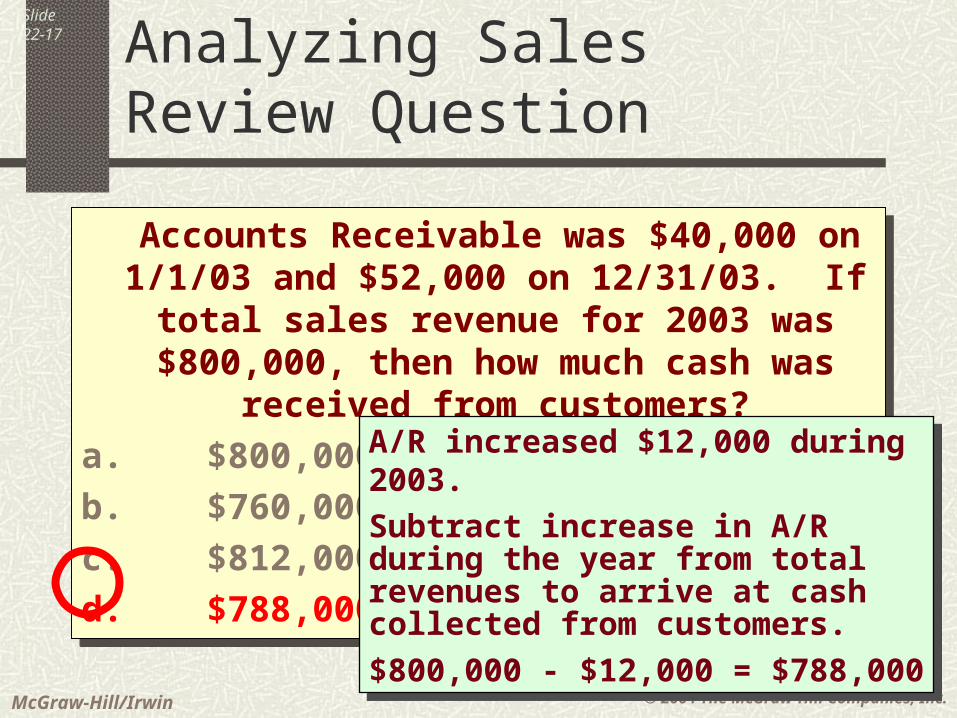

Slide22-17 Analyzing Sales

Review Question

Accounts Receivable was $40,000 on 1/1/03 and $52,000 on 12/31/03. If total sales

revenue for 2003 was $800,000, then how much cash was received from customers?

a.$800,000

b.$760,000

c.$812,000

d.$788,000

Accounts Receivable was $40,000 on 1/1/03 and $52,000 on 12/31/03. If total sales

revenue for 2003 was $800,000, then how much cash was received from customers?

a.$800,000

b.$760,000

c.$812,000

d.$788,000

A/R increased $12,000 during 2003.

Subtract increase in A/R during the year from total revenues to arrive at cash collected from customers.

$800,000 - $12,000 = $788,000

A/R increased $12,000 during 2003.

Subtract increase in A/R during the year from total revenues to arrive at cash collected from customers.

$800,000 - $12,000 = $788,000

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-18

Direct MethodGains and Losses on Sale of Assets

Gains and losses do not appear on the Statement of Cash

Flows using the Direct Method.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-19 Direct Method

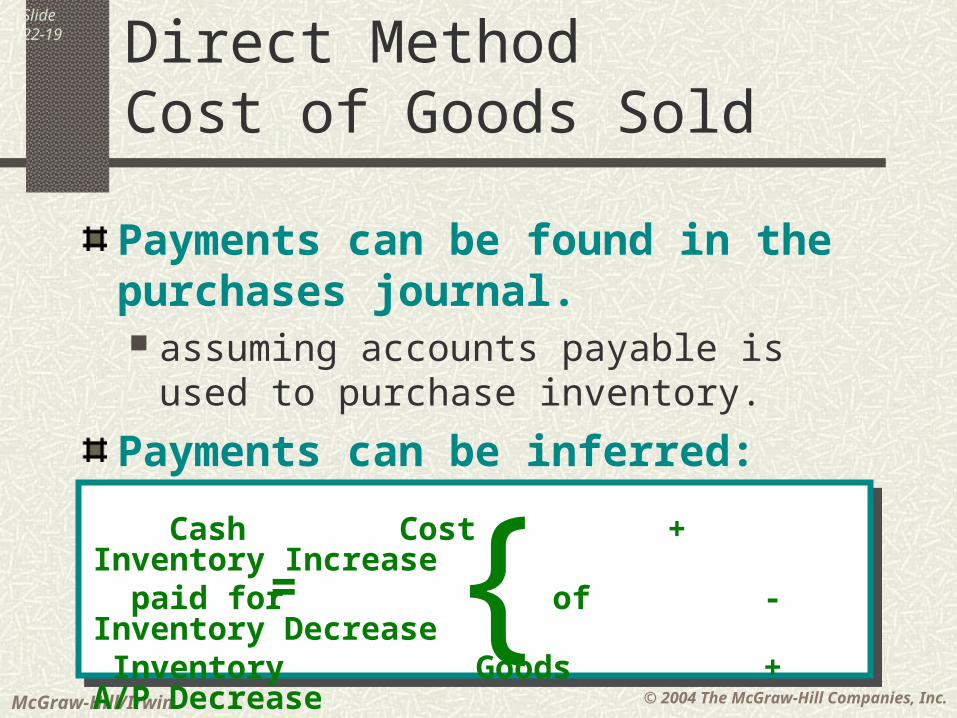

Cost of Goods Sold

Payments can be found in the purchases journal. assuming accounts payable is used to

purchase inventory.

Payments can be inferred:

{ Cash Cost + Inventory Increase paid for of - Inventory Decrease Inventory Goods + A/P Decrease Purchases Sold - A/P Increase

=

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-20 Cost of Goods Sold

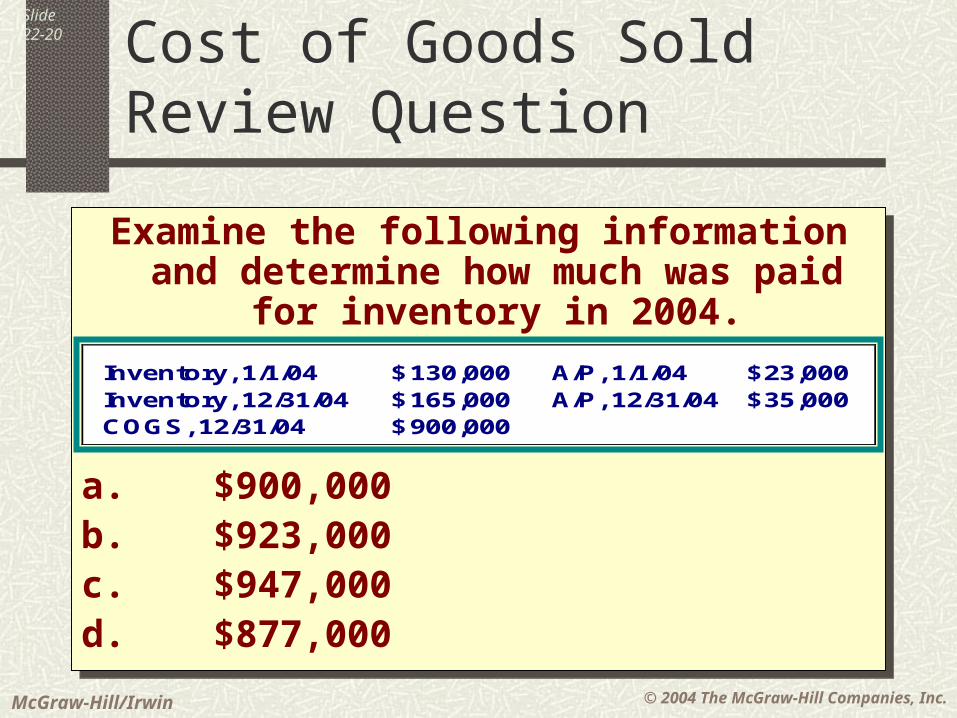

Review Question

Examine the following information and determine how much was paid for

inventory in 2004.

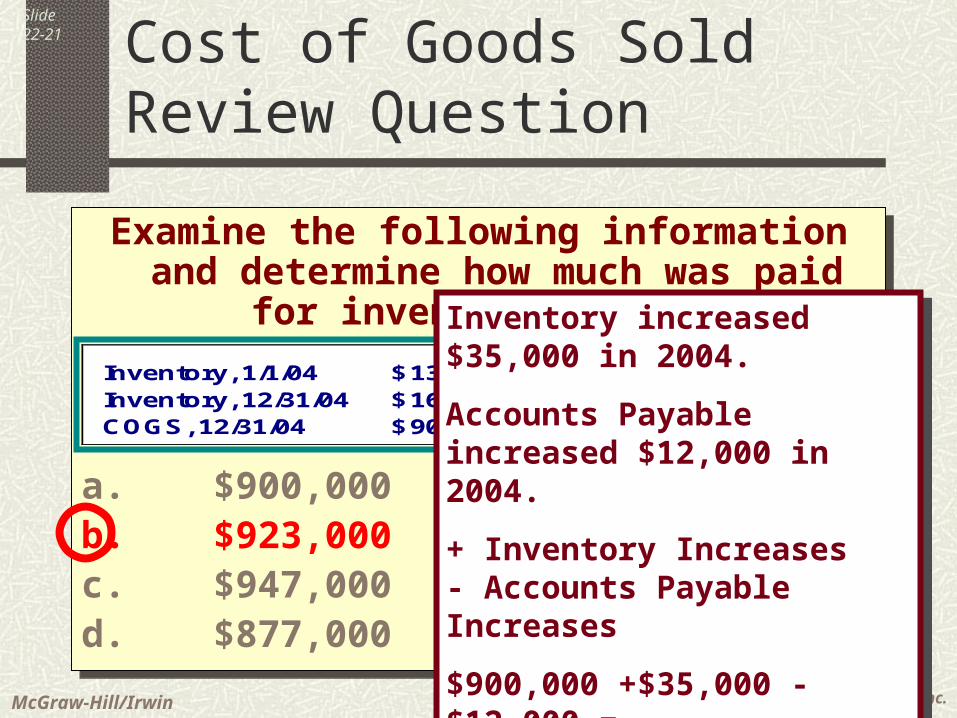

a.$900,000b.$923,000c.$947,000d.$877,000

Examine the following information and determine how much was paid for

inventory in 2004.

a.$900,000b.$923,000c.$947,000d.$877,000

Inventory, 1/1/04 130,000$ A/P, 1/1/04 23,000$ Inventory, 12/31/04 165,000$ A/P, 12/31/04 35,000$ COGS, 12/31/04 900,000$

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-21

Examine the following information and determine how much was paid for

inventory in 2004.

a.$900,000b.$923,000c.$947,000d.$877,000

Examine the following information and determine how much was paid for

inventory in 2004.

a.$900,000b.$923,000c.$947,000d.$877,000

Cost of Goods SoldReview Question

Inventory, 1/1/04 130,000$ A/P, 1/1/04 23,000$ Inventory, 12/31/04 165,000$ A/P, 12/31/04 35,000$ COGS, 12/31/04 900,000$

Inventory increased $35,000 in 2004.

Accounts Payable increased $12,000 in 2004.

+ Inventory Increases- Accounts Payable Increases

$900,000 +$35,000 - $12,000 =$923,000

Inventory increased $35,000 in 2004.

Accounts Payable increased $12,000 in 2004.

+ Inventory Increases- Accounts Payable Increases

$900,000 +$35,000 - $12,000 =$923,000

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

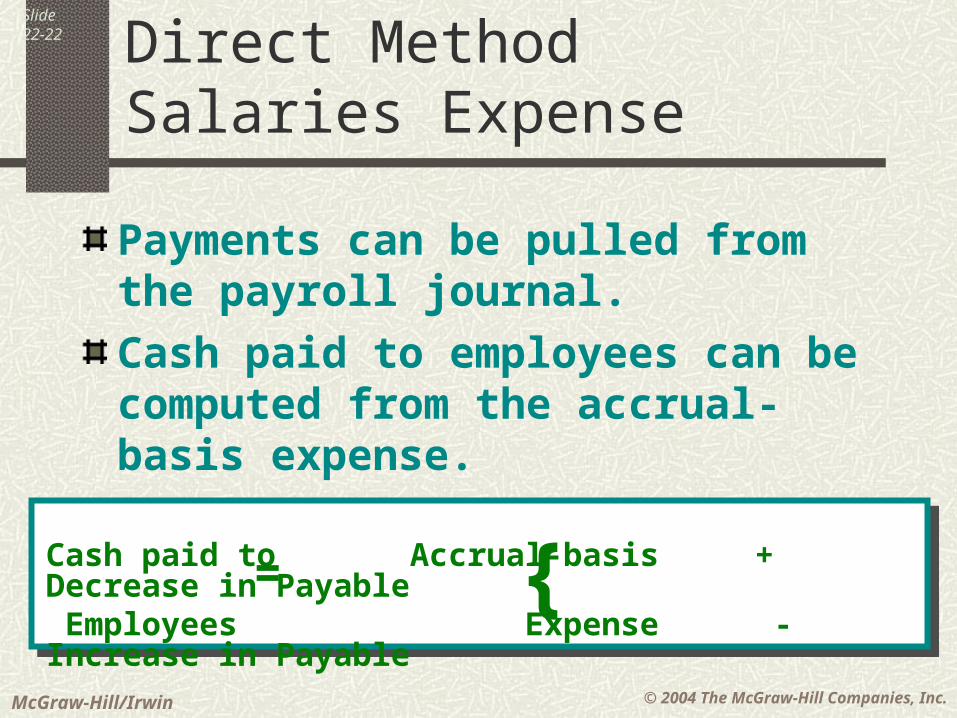

Slide22-22 Direct Method

Salaries Expense

Payments can be pulled from the payroll journal.

Cash paid to employees can be computed from the accrual-basis expense.

Cash paid to Accrual-basis + Decrease in Payable Employees Expense - Increase in Payable= {

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

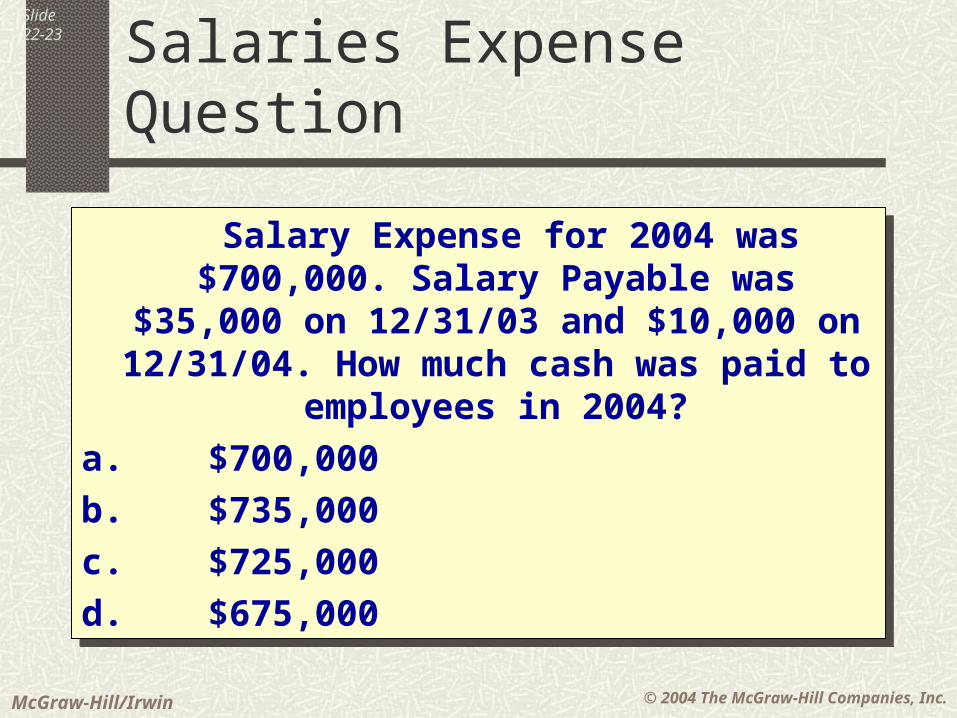

Slide22-23 Salaries Expense

Question

Salary Expense for 2004 was $700,000. Salary Payable was $35,000 on 12/31/03

and $10,000 on 12/31/04. How much cash was paid to employees in 2004?

a.$700,000

b.$735,000

c.$725,000

d.$675,000

Salary Expense for 2004 was $700,000. Salary Payable was $35,000 on 12/31/03

and $10,000 on 12/31/04. How much cash was paid to employees in 2004?

a.$700,000

b.$735,000

c.$725,000

d.$675,000

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-24

Salary Expense for 2004 was $700,000. Salary Payable was $35,000 on 12/31/03

and $10,000 on 12/31/04. How much cash was paid to employees in 2004?

a.$700,000

b.$735,000

c.$725,000

d.$675,000

Salary Expense for 2004 was $700,000. Salary Payable was $35,000 on 12/31/03

and $10,000 on 12/31/04. How much cash was paid to employees in 2004?

a.$700,000

b.$735,000

c.$725,000

d.$675,000

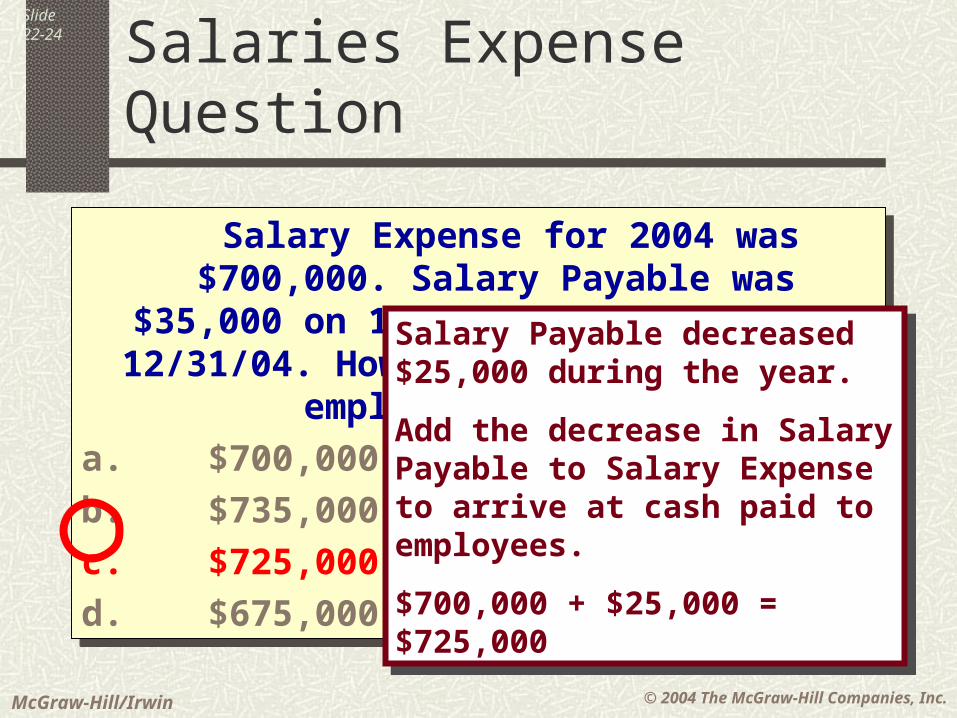

Salaries ExpenseQuestion

Salary Payable decreased $25,000 during the year.

Add the decrease in Salary Payable to Salary Expense to arrive at cash paid to employees.

$700,000 + $25,000 = $725,000

Salary Payable decreased $25,000 during the year.

Add the decrease in Salary Payable to Salary Expense to arrive at cash paid to employees.

$700,000 + $25,000 = $725,000

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

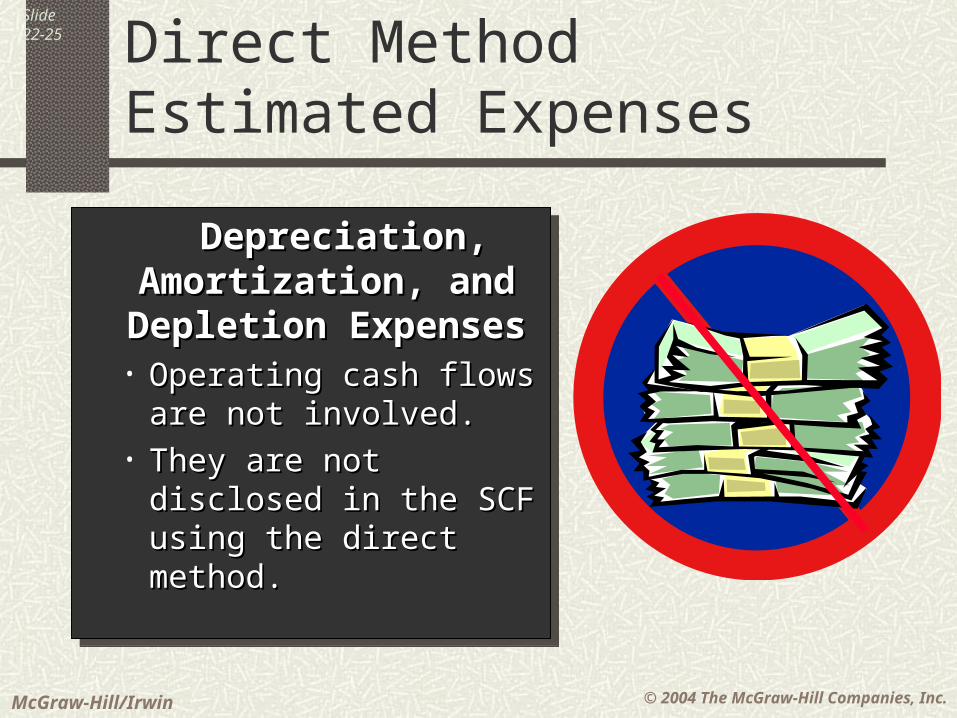

Slide22-25 Direct Method

Estimated Expenses

Depreciation, Depreciation, Amortization, and Amortization, and

Depletion ExpensesDepletion Expenses• Operating cash flows Operating cash flows

are not involved.are not involved.• They are not disclosed They are not disclosed

in the SCF using the in the SCF using the direct method.direct method.

Depreciation, Depreciation, Amortization, and Amortization, and

Depletion ExpensesDepletion Expenses• Operating cash flows Operating cash flows

are not involved.are not involved.• They are not disclosed They are not disclosed

in the SCF using the in the SCF using the direct method.direct method.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

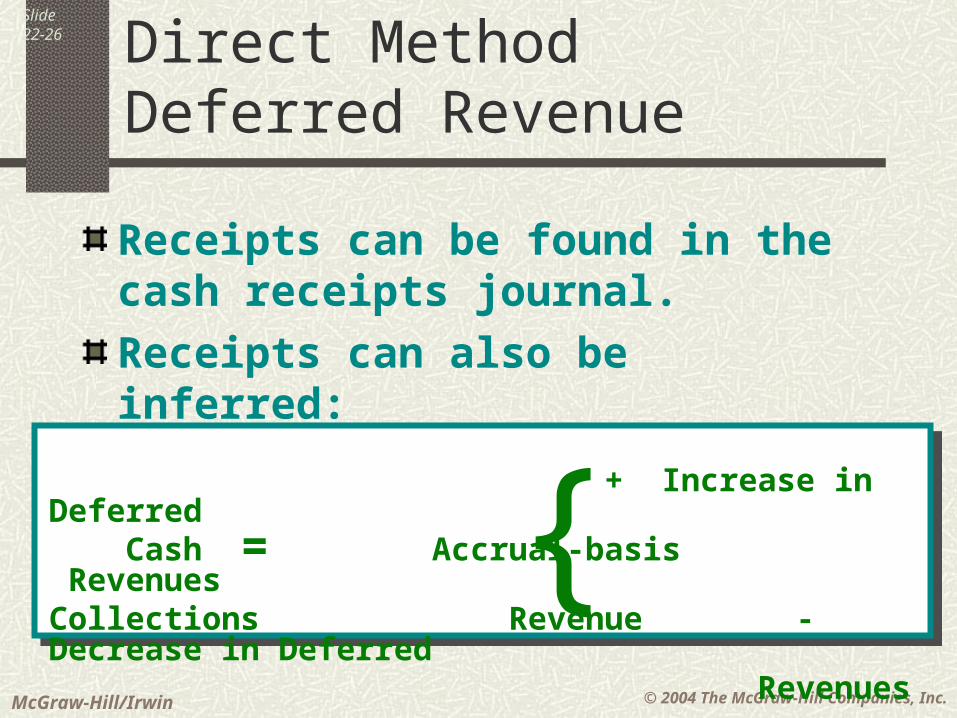

Slide22-26 Direct Method

Deferred Revenue

Receipts can be found in the cash receipts journal.

Receipts can also be inferred:

+ Increase in Deferred Cash Accrual-basis RevenuesCollections Revenue - Decrease in Deferred

Revenues= {

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

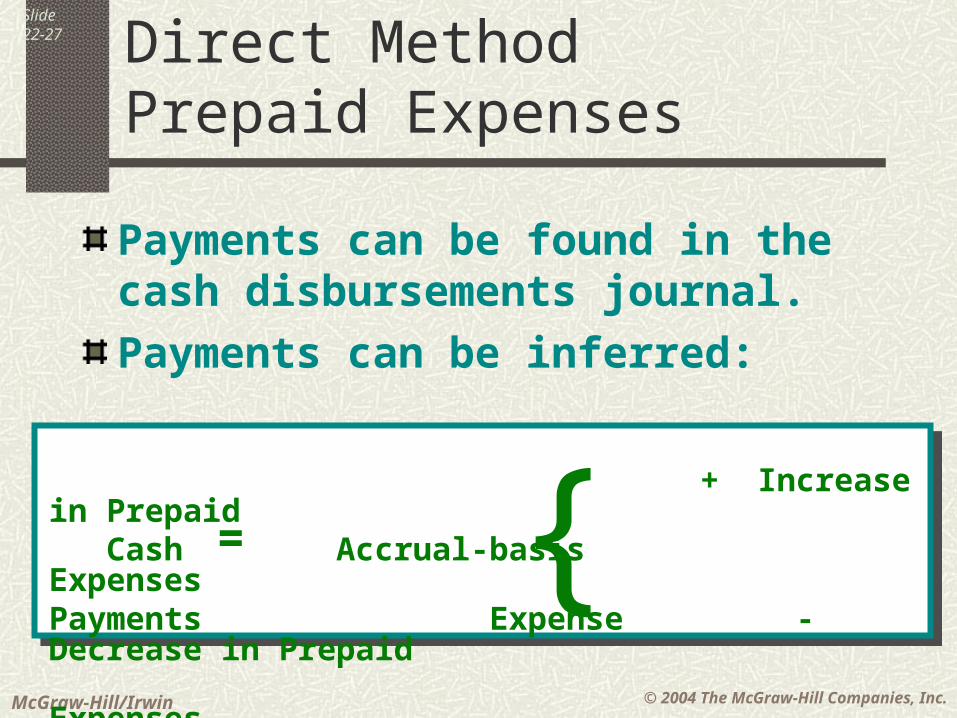

Slide22-27 Direct Method

Prepaid Expenses

Payments can be found in the cash disbursements journal.

Payments can be inferred:

+ Increase in Prepaid Cash Accrual-basis ExpensesPayments Expense - Decrease in Prepaid Expenses

= {

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-28

Let’s do an example of a

direct method Statement of Cash Flows.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-29 Statement of Cash Flows

Direct Method Example

Using the direct method, prepare a Statement of Cash Flows for the year

ended 2003.

Examine the following information . . .

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-30

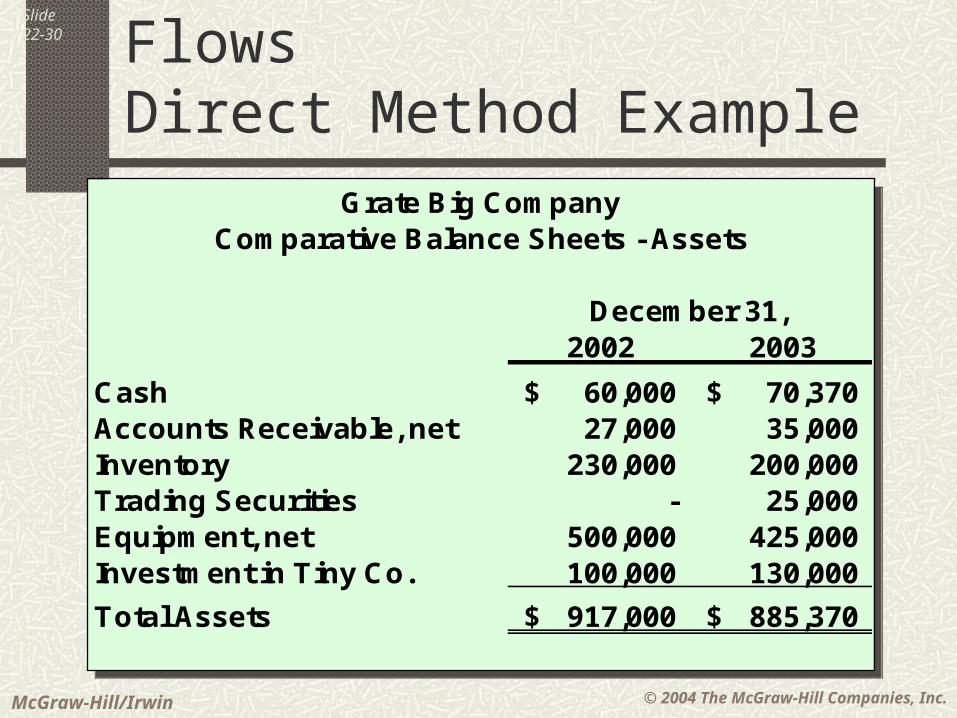

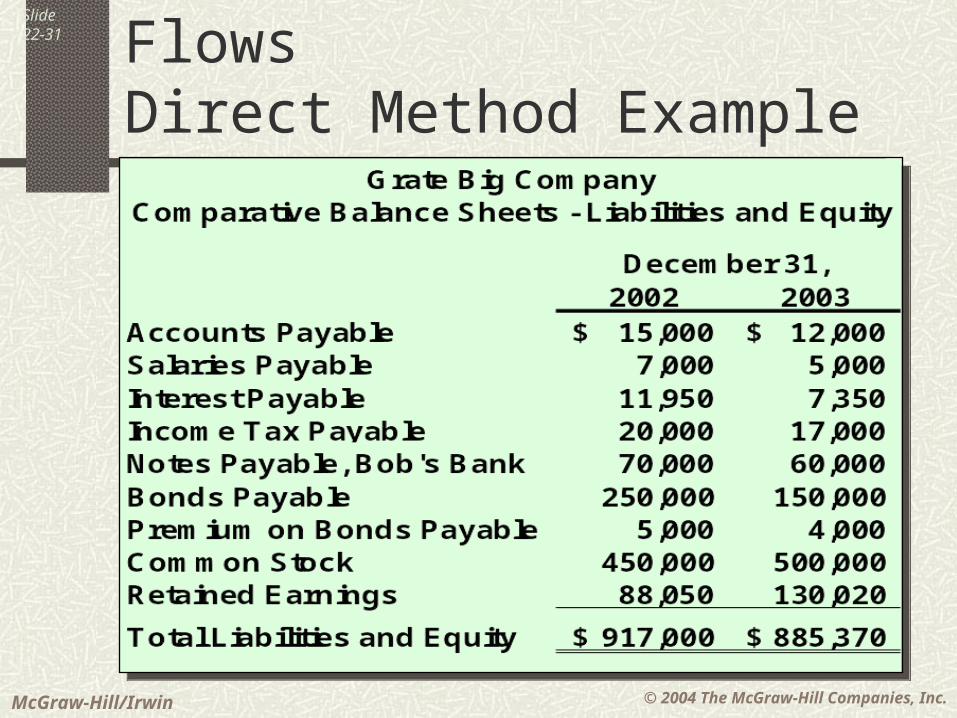

Grate Big CompanyComparative Balance Sheets - Assets

December 31, 2002 2003

Cash 60,000$ 70,370$ Accounts Receivable, net 27,000 35,000 Inventory 230,000 200,000 Trading Securities - 25,000 Equipment, net 500,000 425,000 Investment in Tiny Co. 100,000 130,000

Total Assets 917,000$ 885,370$

Grate Big CompanyComparative Balance Sheets - Assets

December 31, 2002 2003

Cash 60,000$ 70,370$ Accounts Receivable, net 27,000 35,000 Inventory 230,000 200,000 Trading Securities - 25,000 Equipment, net 500,000 425,000 Investment in Tiny Co. 100,000 130,000

Total Assets 917,000$ 885,370$

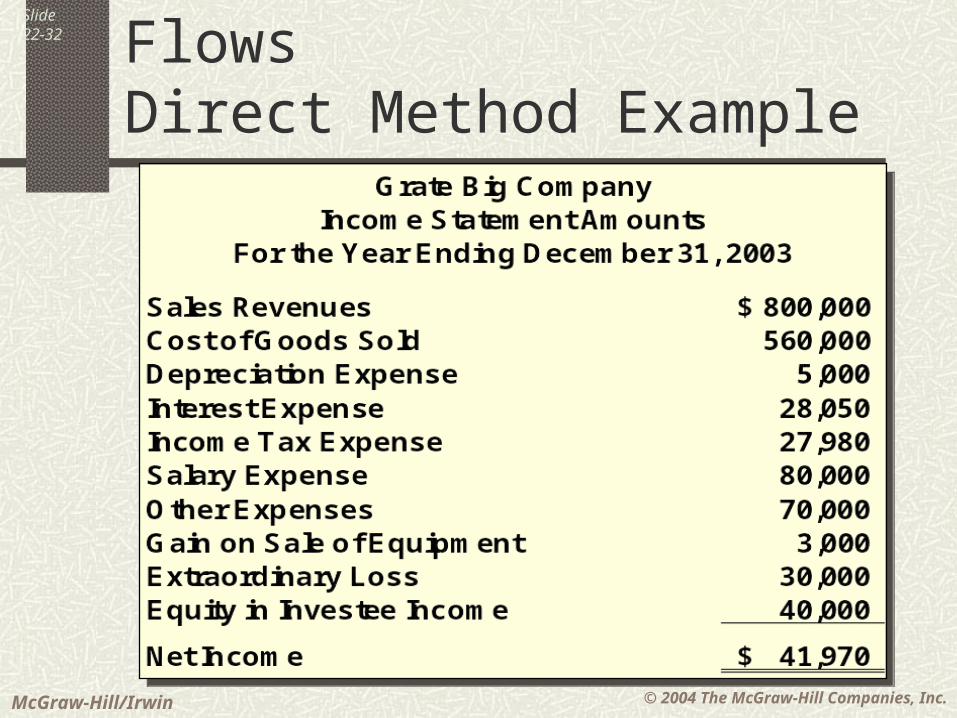

Statement of Cash FlowsDirect Method Example

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-31 Statement of Cash Flows

Direct Method Example

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-32 Statement of Cash Flows

Direct Method Example

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-33 Statement of Cash Flows

Direct Method Example

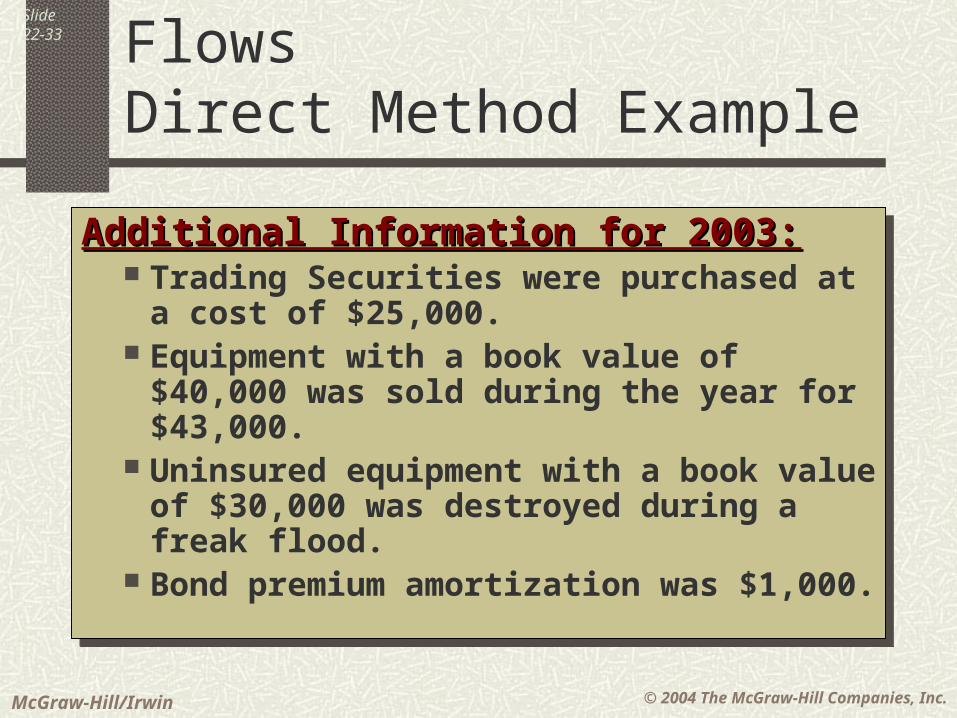

Additional Information for 2003:Additional Information for 2003: Trading Securities were purchased at a

cost of $25,000. Equipment with a book value of $40,000

was sold during the year for $43,000. Uninsured equipment with a book value

of $30,000 was destroyed during a freak flood.

Bond premium amortization was $1,000.

Additional Information for 2003:Additional Information for 2003: Trading Securities were purchased at a

cost of $25,000. Equipment with a book value of $40,000

was sold during the year for $43,000. Uninsured equipment with a book value

of $30,000 was destroyed during a freak flood.

Bond premium amortization was $1,000.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-34 Statement of Cash Flows

Direct Method Example

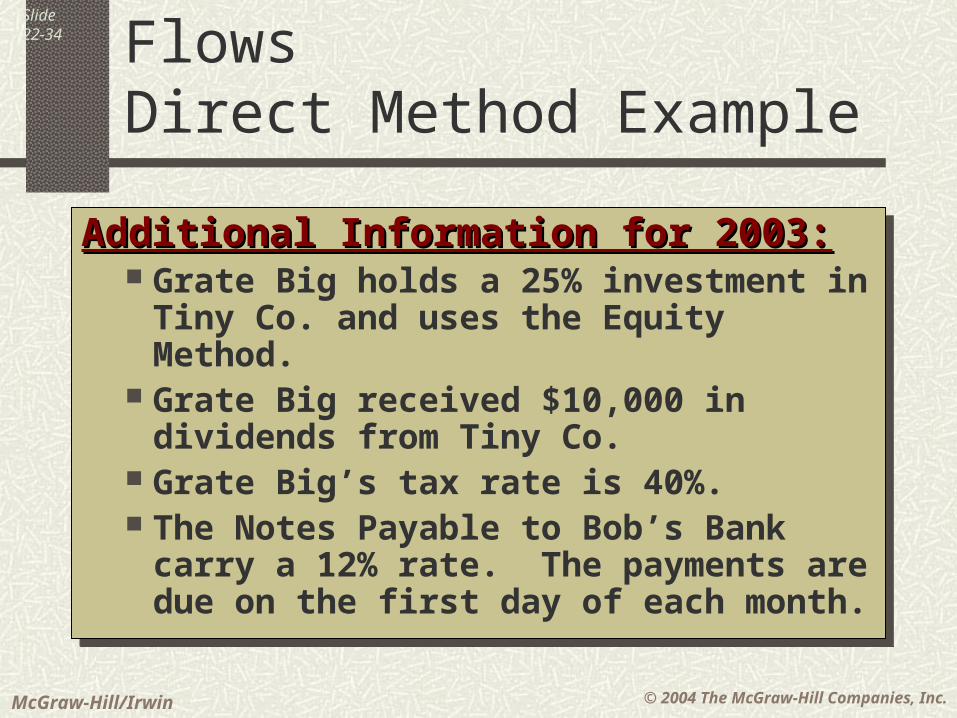

Additional Information for 2003:Additional Information for 2003: Grate Big holds a 25% investment in

Tiny Co. and uses the Equity Method. Grate Big received $10,000 in dividends

from Tiny Co. Grate Big’s tax rate is 40%. The Notes Payable to Bob’s Bank carry

a 12% rate. The payments are due on the first day of each month.

Additional Information for 2003:Additional Information for 2003: Grate Big holds a 25% investment in

Tiny Co. and uses the Equity Method. Grate Big received $10,000 in dividends

from Tiny Co. Grate Big’s tax rate is 40%. The Notes Payable to Bob’s Bank carry

a 12% rate. The payments are due on the first day of each month.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

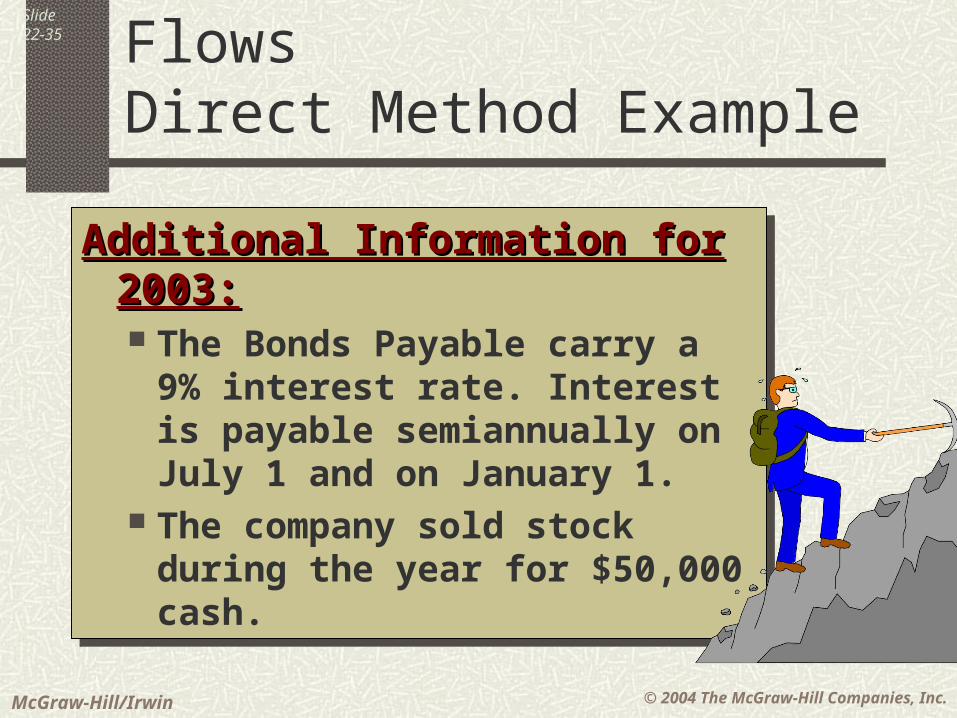

Slide22-35 Statement of Cash Flows

Direct Method Example

Additional Information for 2003:Additional Information for 2003: The Bonds Payable carry a 9%

interest rate. Interest is payable semiannually on July 1 and on January 1.

The company sold stock during the year for $50,000 cash.

Additional Information for 2003:Additional Information for 2003: The Bonds Payable carry a 9%

interest rate. Interest is payable semiannually on July 1 and on January 1.

The company sold stock during the year for $50,000 cash.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-36 Statement of Cash Flows

Direct Method Example

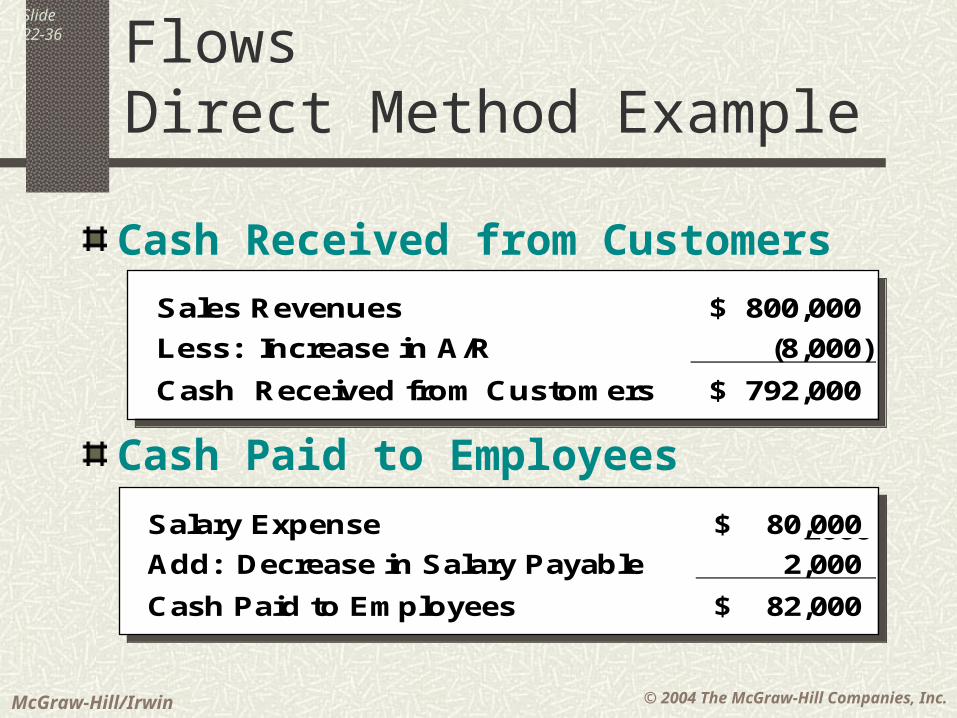

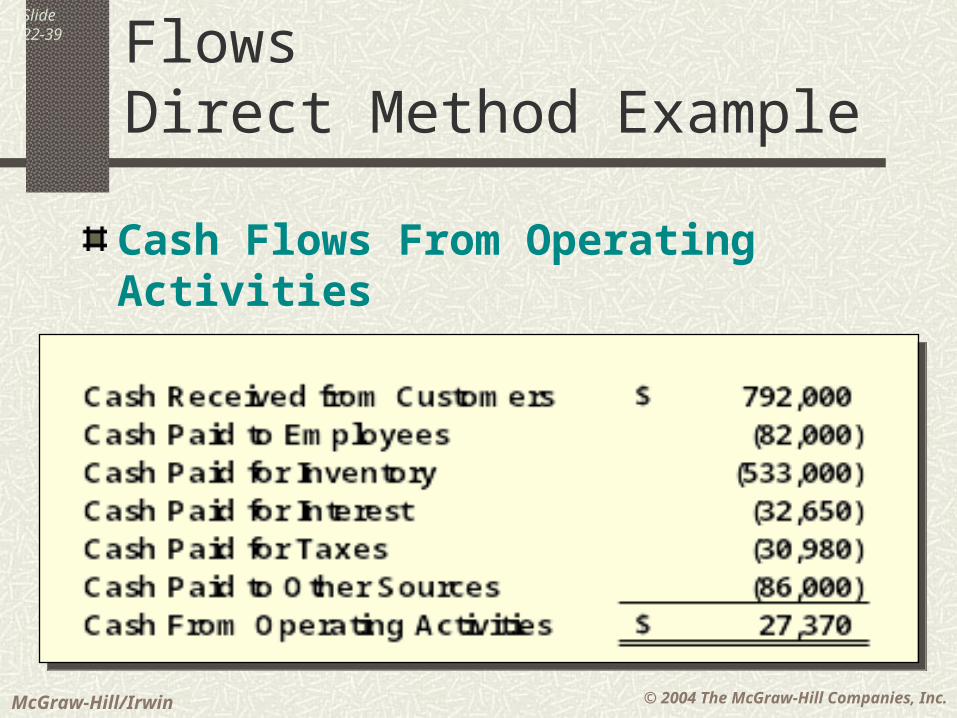

Cash Received from Customers

Cash Paid to Employees

Salary Expense 80,000$ 2000Add: Decrease in Salary Payable 2,000

Cash Paid to Employees 82,000$

Salary Expense 80,000$ 2000Add: Decrease in Salary Payable 2,000

Cash Paid to Employees 82,000$

Sales Revenues 800,000$

Less: Increase in A/R (8,000)

Cash Received from Customers 792,000$

Sales Revenues 800,000$

Less: Increase in A/R (8,000)

Cash Received from Customers 792,000$

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-37 Statement of Cash Flows

Direct Method Example

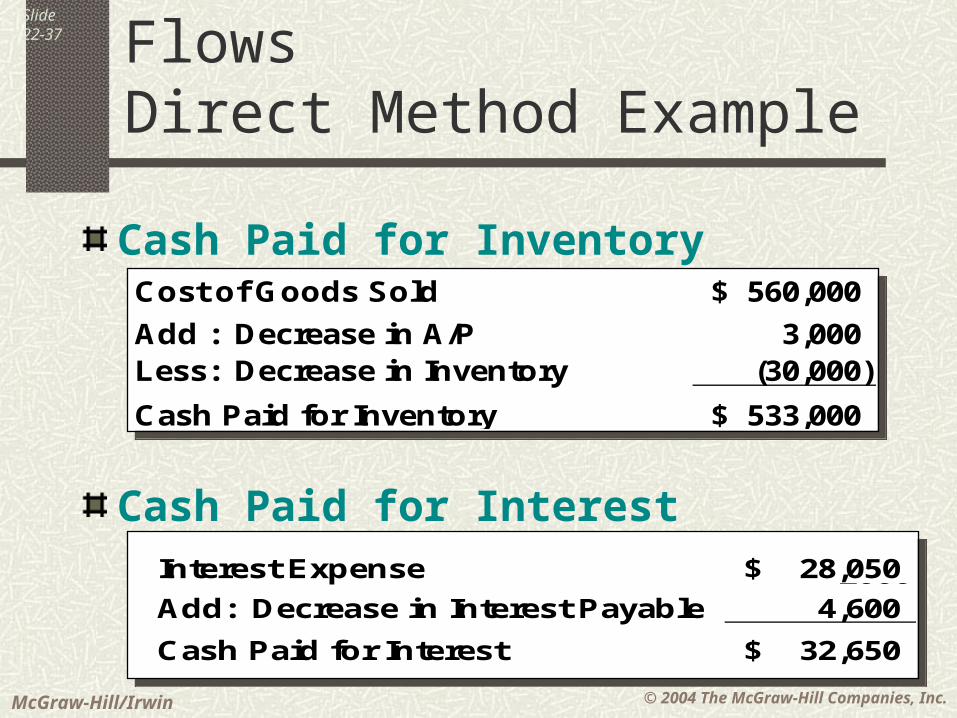

Cash Paid for Inventory

Cash Paid for Interest

Interest Expense 28,050$ 2000Add: Decrease in Interest Payable 4,600

Cash Paid for Interest 32,650$

Interest Expense 28,050$ 2000Add: Decrease in Interest Payable 4,600

Cash Paid for Interest 32,650$

Cost of Goods Sold 560,000$

Add : Decrease in A/P 3,000 Less: Decrease in Inventory (30,000)

Cash Paid for Inventory 533,000$

Cost of Goods Sold 560,000$

Add : Decrease in A/P 3,000 Less: Decrease in Inventory (30,000)

Cash Paid for Inventory 533,000$

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-38 Statement of Cash Flows

Direct Method Example

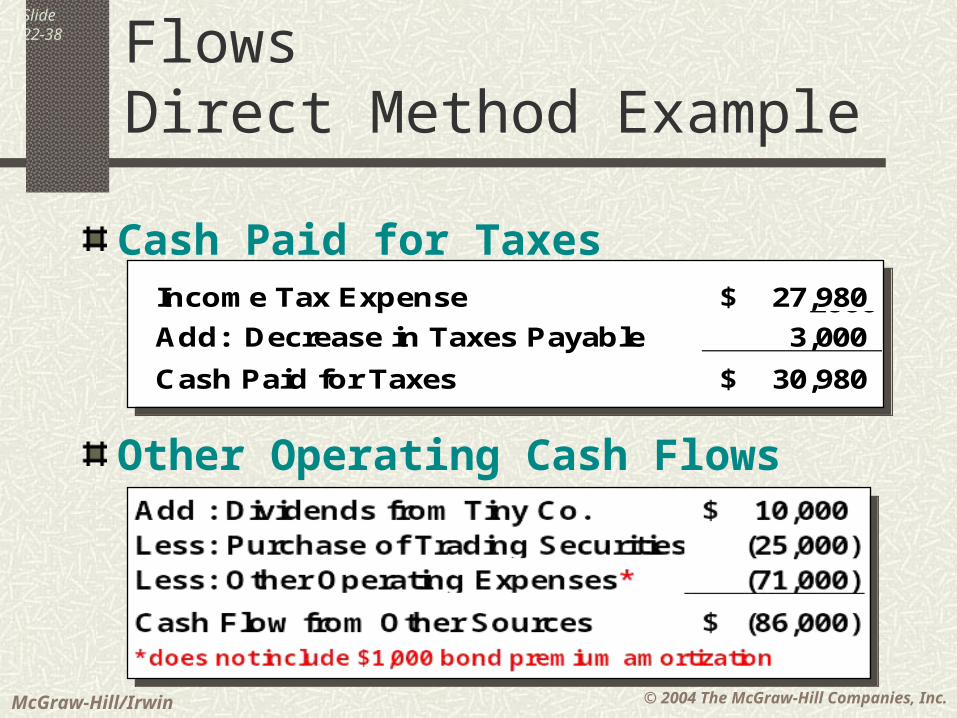

Cash Paid for Taxes

Other Operating Cash Flows

Income Tax Expense 27,980$ 2000Add: Decrease in Taxes Payable 3,000

Cash Paid for Taxes 30,980$

Income Tax Expense 27,980$ 2000Add: Decrease in Taxes Payable 3,000

Cash Paid for Taxes 30,980$

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-39 Statement of Cash Flows

Direct Method Example

Cash Flows From Operating Activities

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

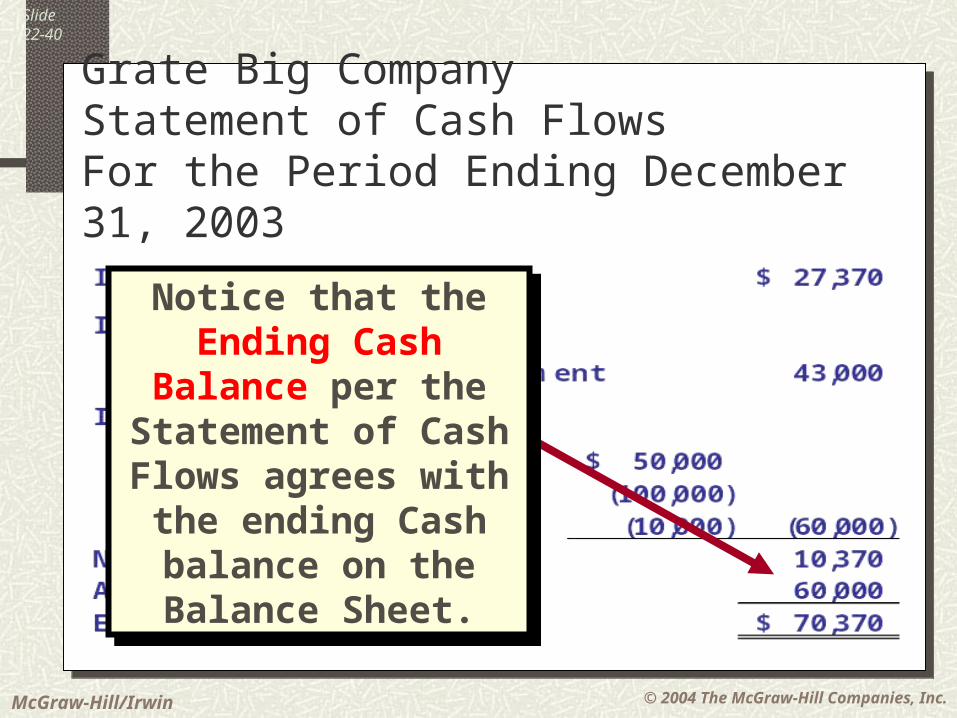

Slide22-40

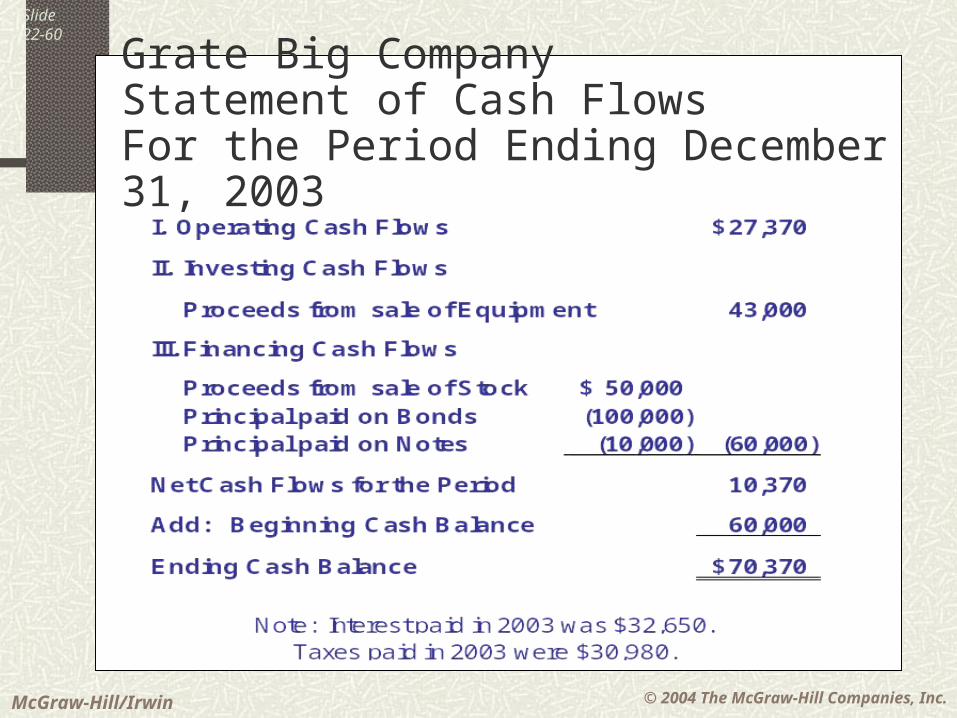

Grate Big CompanyStatement of Cash FlowsFor the Period Ending December 31, 2003

Notice that the Ending Cash Balance per the

Statement of Cash Flows agrees with the ending Cash balance on the Balance Sheet.

Notice that the Ending Cash Balance per the

Statement of Cash Flows agrees with the ending Cash balance on the Balance Sheet.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

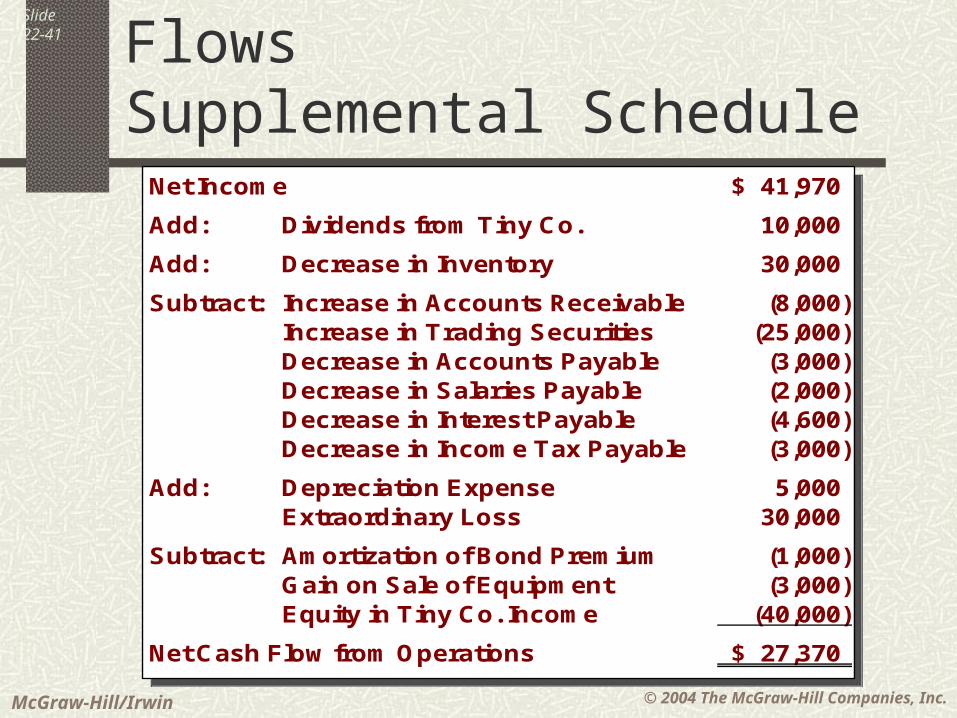

Slide22-41

Net Income 41,970$

Add: Dividends from Tiny Co. 10,000

Add: Decrease in Inventory 30,000

Subtract: Increase in Accounts Receivable (8,000) Increase in Trading Securities (25,000) Decrease in Accounts Payable (3,000) Decrease in Salaries Payable (2,000) Decrease in Interest Payable (4,600) Decrease in Income Tax Payable (3,000)

Add: Depreciation Expense 5,000 Extraordinary Loss 30,000

Subtract: Amortization of Bond Premium (1,000) Gain on Sale of Equipment (3,000) Equity in Tiny Co. Income (40,000)

Net Cash Flow from Operations 27,370$

Net Income 41,970$

Add: Dividends from Tiny Co. 10,000

Add: Decrease in Inventory 30,000

Subtract: Increase in Accounts Receivable (8,000) Increase in Trading Securities (25,000) Decrease in Accounts Payable (3,000) Decrease in Salaries Payable (2,000) Decrease in Interest Payable (4,600) Decrease in Income Tax Payable (3,000)

Add: Depreciation Expense 5,000 Extraordinary Loss 30,000

Subtract: Amortization of Bond Premium (1,000) Gain on Sale of Equipment (3,000) Equity in Tiny Co. Income (40,000)

Net Cash Flow from Operations 27,370$

Statement of Cash FlowsSupplemental Schedule

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-42

Now, let’s look at the Indirect Method

for preparing the Cash Flows from

Operating Activities section.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

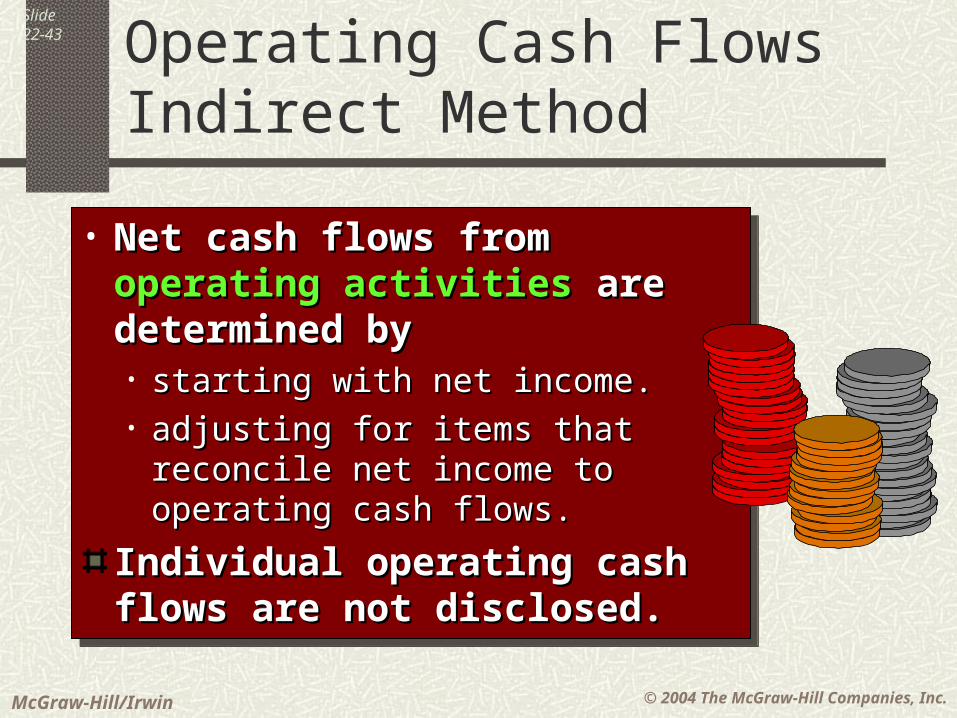

Slide22-43 Operating Cash Flows

Indirect Method

• Net cash flows from Net cash flows from operating operating activitiesactivities are determined by are determined by• starting with net income.starting with net income.• adjusting for items that reconcile adjusting for items that reconcile

net income to operating cash net income to operating cash flows.flows.

Individual operating cash Individual operating cash flows are not disclosed.flows are not disclosed.

• Net cash flows from Net cash flows from operating operating activitiesactivities are determined by are determined by• starting with net income.starting with net income.• adjusting for items that reconcile adjusting for items that reconcile

net income to operating cash net income to operating cash flows.flows.

Individual operating cash Individual operating cash flows are not disclosed.flows are not disclosed.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

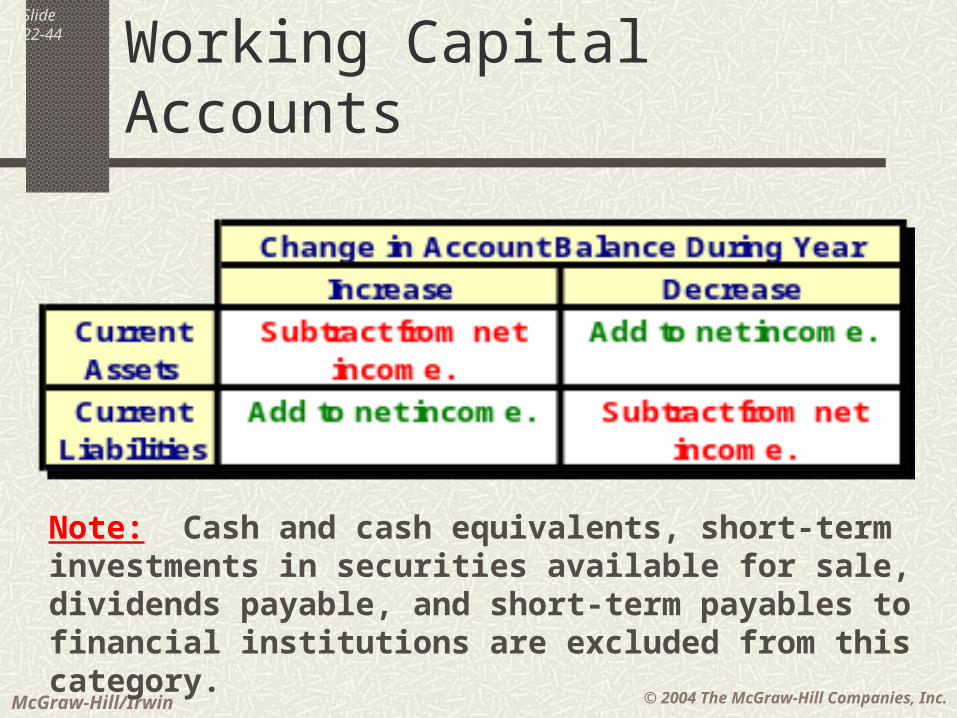

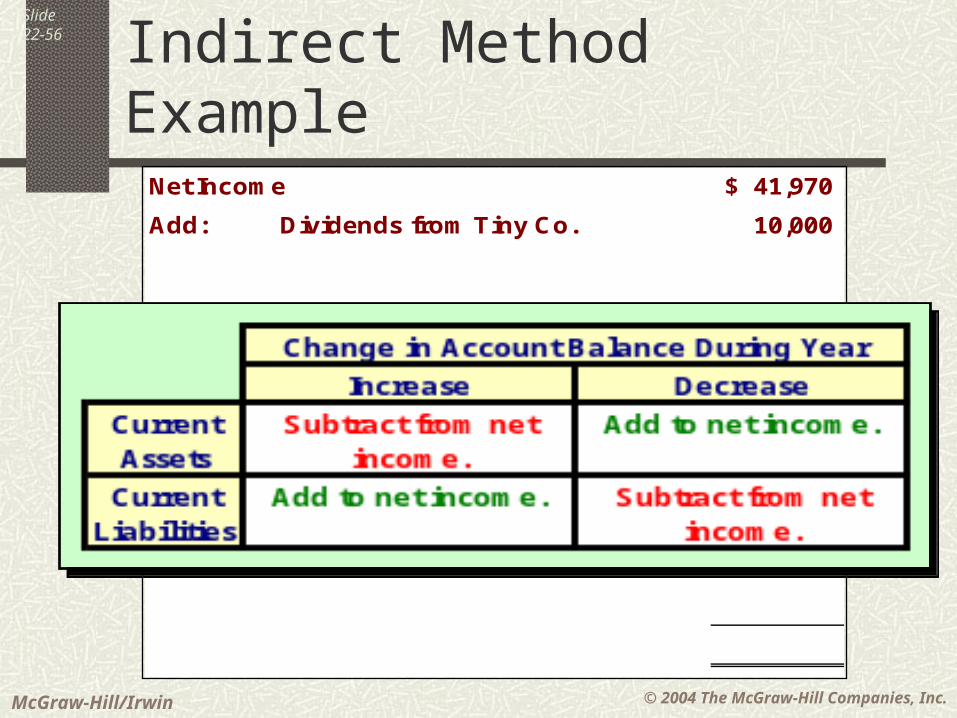

Slide22-44 Indirect Method

Working Capital Accounts

Note: Cash and cash equivalents, short-term investments in securities available for sale, dividends payable, and short-term payables to financial institutions are excluded from this category.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

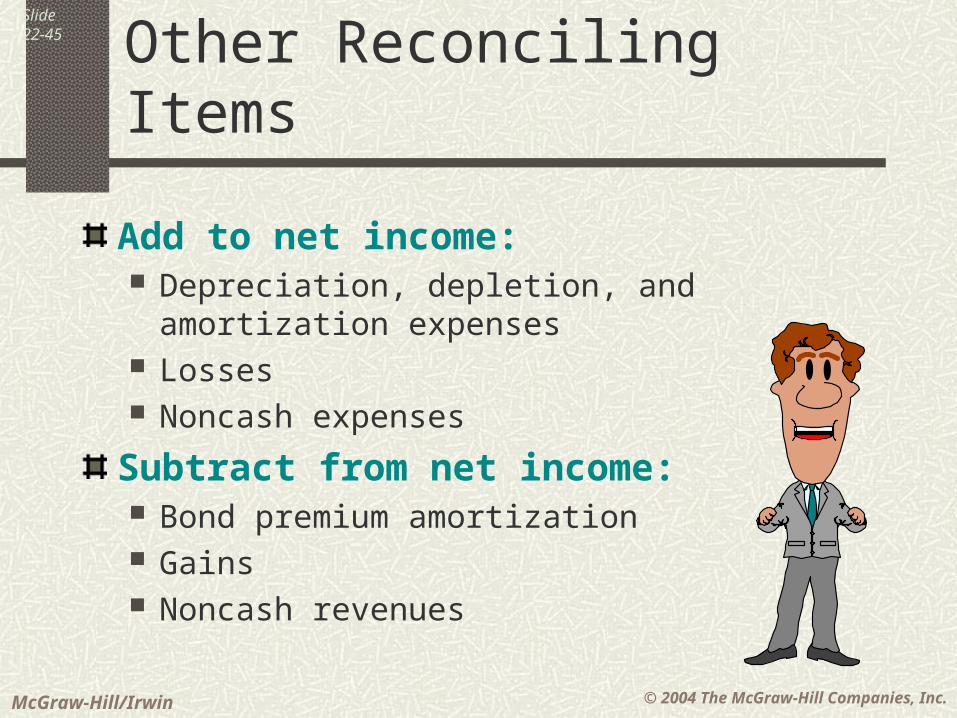

Slide22-45 Indirect Method

Other Reconciling Items

Add to net income: Depreciation, depletion, and amortization

expenses Losses Noncash expenses

Subtract from net income: Bond premium amortization Gains Noncash revenues

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-46

Let’s do an Indirect Method

Statement of Cash Flows.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-47 Statement of Cash Flows

Indirect Method Example

Prepare a Statement of Cash Prepare a Statement of Cash Flows for the period ending Flows for the period ending

December 31, 2003, using the December 31, 2003, using the Indirect Method.Indirect Method.

Refer to the following Refer to the following information . . .information . . .

Prepare a Statement of Cash Prepare a Statement of Cash Flows for the period ending Flows for the period ending

December 31, 2003, using the December 31, 2003, using the Indirect Method.Indirect Method.

Refer to the following Refer to the following information . . .information . . .

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

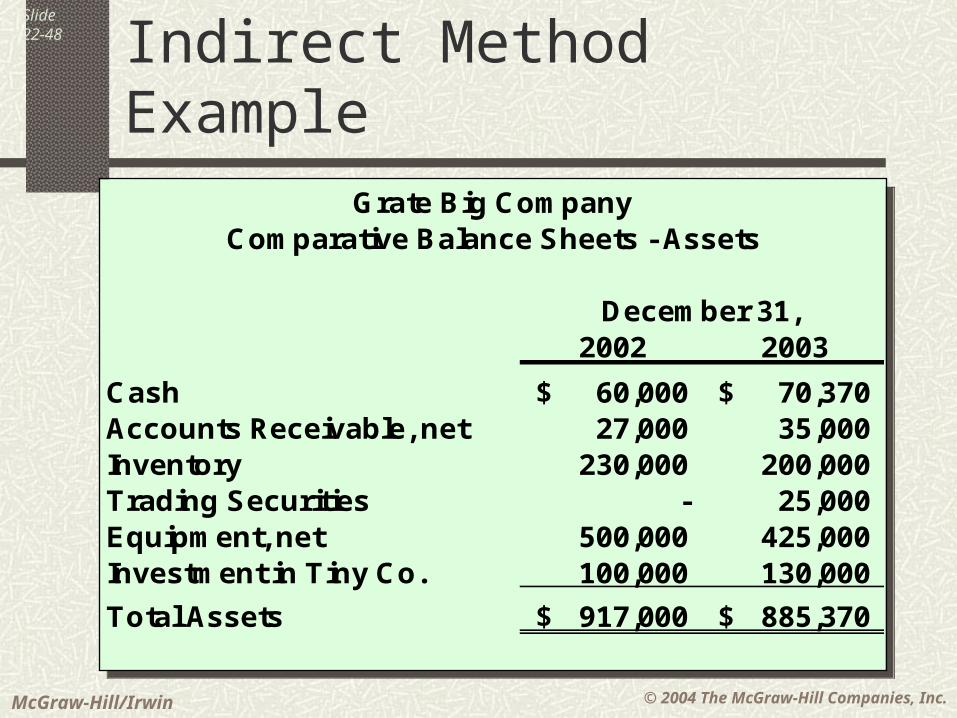

Slide22-48 Statement of Cash Flows

Indirect Method Example

Grate Big CompanyComparative Balance Sheets - Assets

December 31, 2002 2003

Cash 60,000$ 70,370$ Accounts Receivable, net 27,000 35,000 Inventory 230,000 200,000 Trading Securities - 25,000 Equipment, net 500,000 425,000 Investment in Tiny Co. 100,000 130,000

Total Assets 917,000$ 885,370$

Grate Big CompanyComparative Balance Sheets - Assets

December 31, 2002 2003

Cash 60,000$ 70,370$ Accounts Receivable, net 27,000 35,000 Inventory 230,000 200,000 Trading Securities - 25,000 Equipment, net 500,000 425,000 Investment in Tiny Co. 100,000 130,000

Total Assets 917,000$ 885,370$

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

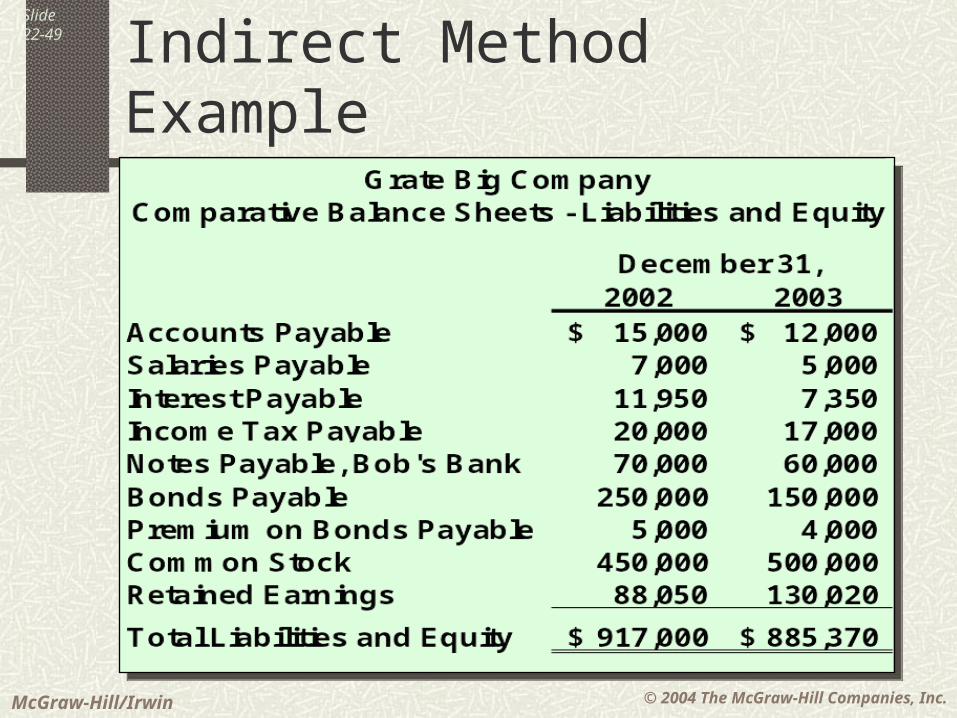

Slide22-49 Statement of Cash Flows

Indirect Method Example

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

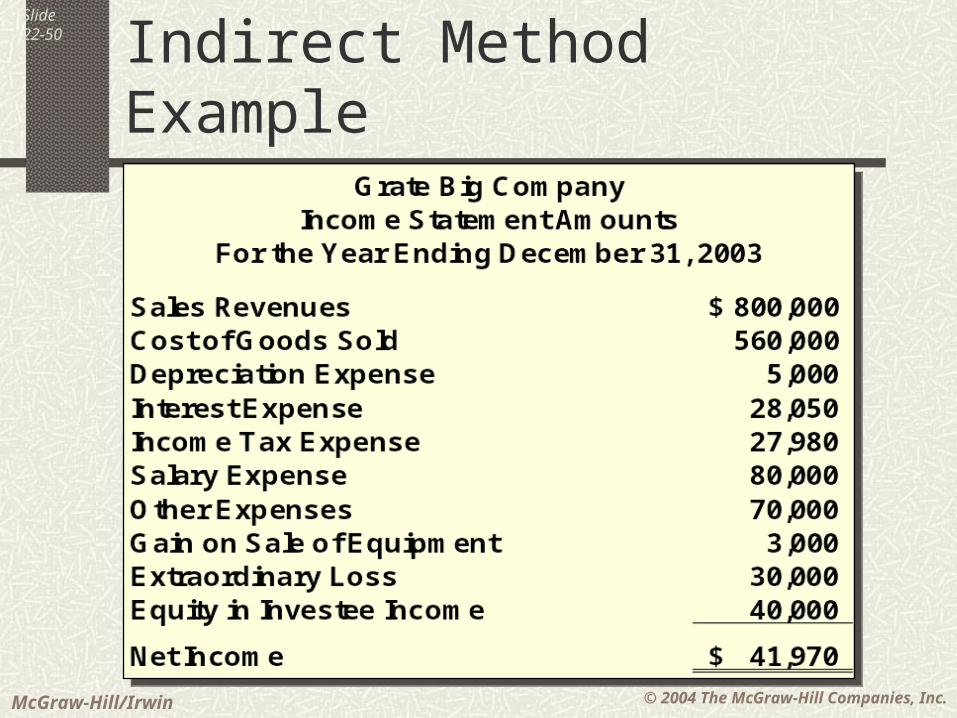

Slide22-50 Statement of Cash Flows

Indirect Method Example

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-51 Statement of Cash Flows

Indirect Method Example

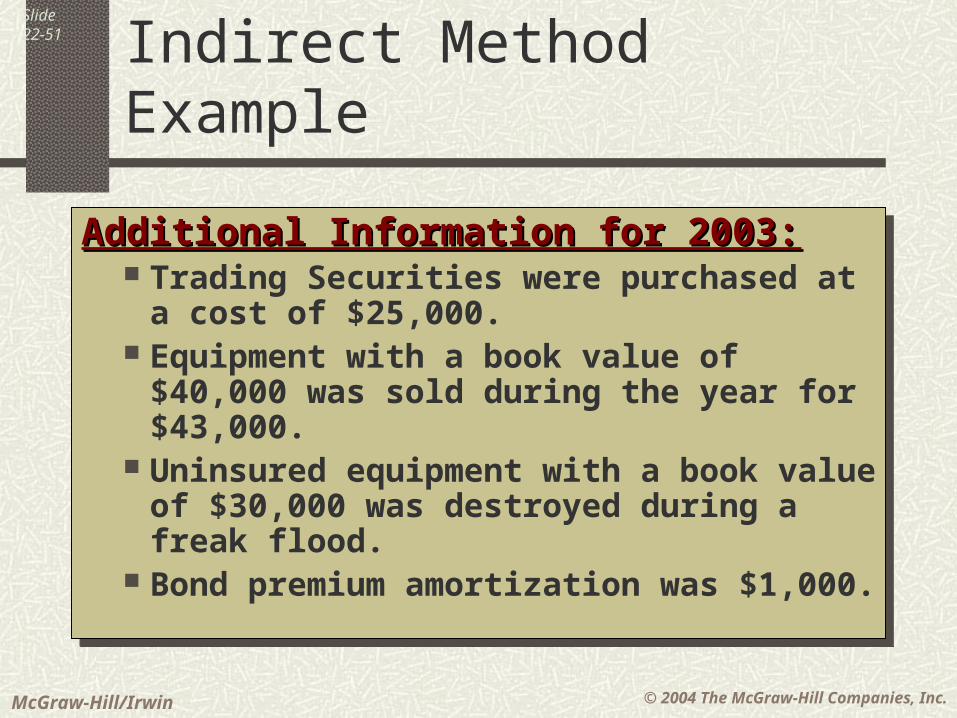

Additional Information for 2003:Additional Information for 2003: Trading Securities were purchased at a

cost of $25,000. Equipment with a book value of $40,000

was sold during the year for $43,000. Uninsured equipment with a book value

of $30,000 was destroyed during a freak flood.

Bond premium amortization was $1,000.

Additional Information for 2003:Additional Information for 2003: Trading Securities were purchased at a

cost of $25,000. Equipment with a book value of $40,000

was sold during the year for $43,000. Uninsured equipment with a book value

of $30,000 was destroyed during a freak flood.

Bond premium amortization was $1,000.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

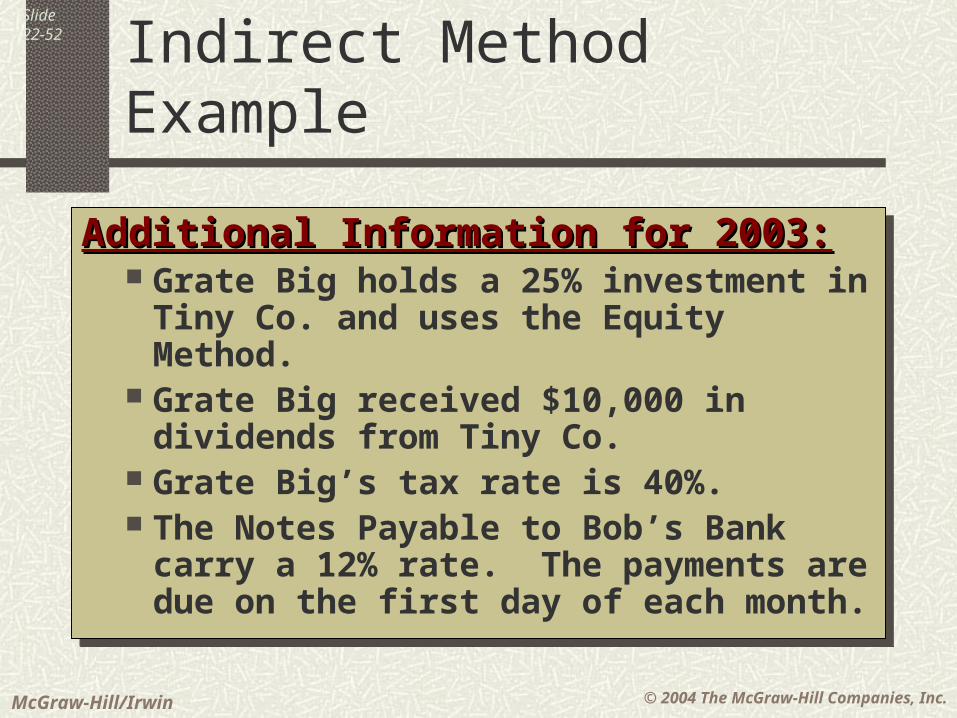

Slide22-52 Statement of Cash Flows

Indirect Method Example

Additional Information for 2003:Additional Information for 2003: Grate Big holds a 25% investment in

Tiny Co. and uses the Equity Method. Grate Big received $10,000 in dividends

from Tiny Co. Grate Big’s tax rate is 40%. The Notes Payable to Bob’s Bank carry

a 12% rate. The payments are due on the first day of each month.

Additional Information for 2003:Additional Information for 2003: Grate Big holds a 25% investment in

Tiny Co. and uses the Equity Method. Grate Big received $10,000 in dividends

from Tiny Co. Grate Big’s tax rate is 40%. The Notes Payable to Bob’s Bank carry

a 12% rate. The payments are due on the first day of each month.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

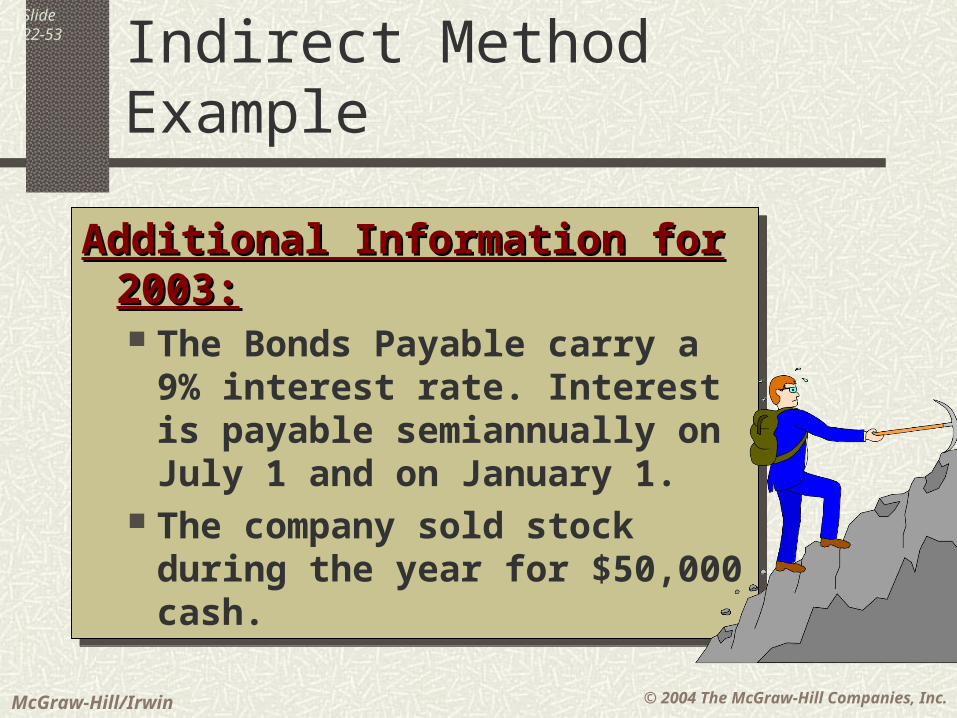

Slide22-53 Statement of Cash Flows

Indirect Method Example

Additional Information for 2003:Additional Information for 2003: The Bonds Payable carry a 9%

interest rate. Interest is payable semiannually on July 1 and on January 1.

The company sold stock during the year for $50,000 cash.

Additional Information for 2003:Additional Information for 2003: The Bonds Payable carry a 9%

interest rate. Interest is payable semiannually on July 1 and on January 1.

The company sold stock during the year for $50,000 cash.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

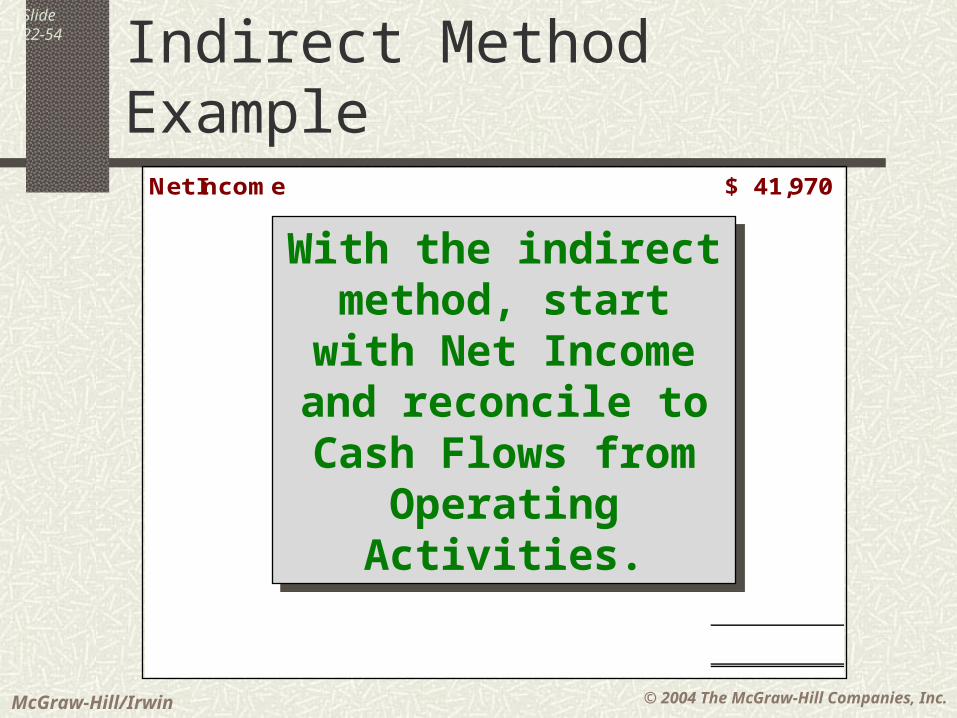

Slide22-54

Net Income 41,970$

With the indirect method, start with

Net Income and reconcile to Cash

Flows from Operating Activities.

With the indirect method, start with

Net Income and reconcile to Cash

Flows from Operating Activities.

Statement of Cash FlowsIndirect Method Example

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

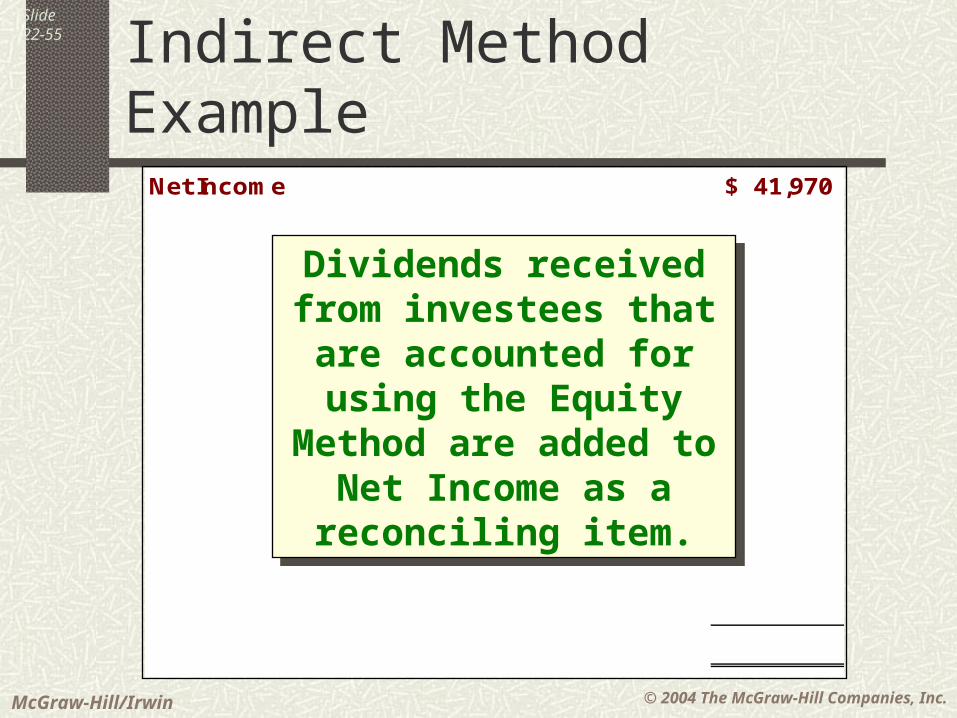

Slide22-55

Net Income 41,970$

Statement of Cash FlowsIndirect Method Example

Dividends received from investees that are

accounted for using the Equity Method are added

to Net Income as a reconciling item.

Dividends received from investees that are

accounted for using the Equity Method are added

to Net Income as a reconciling item.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-56

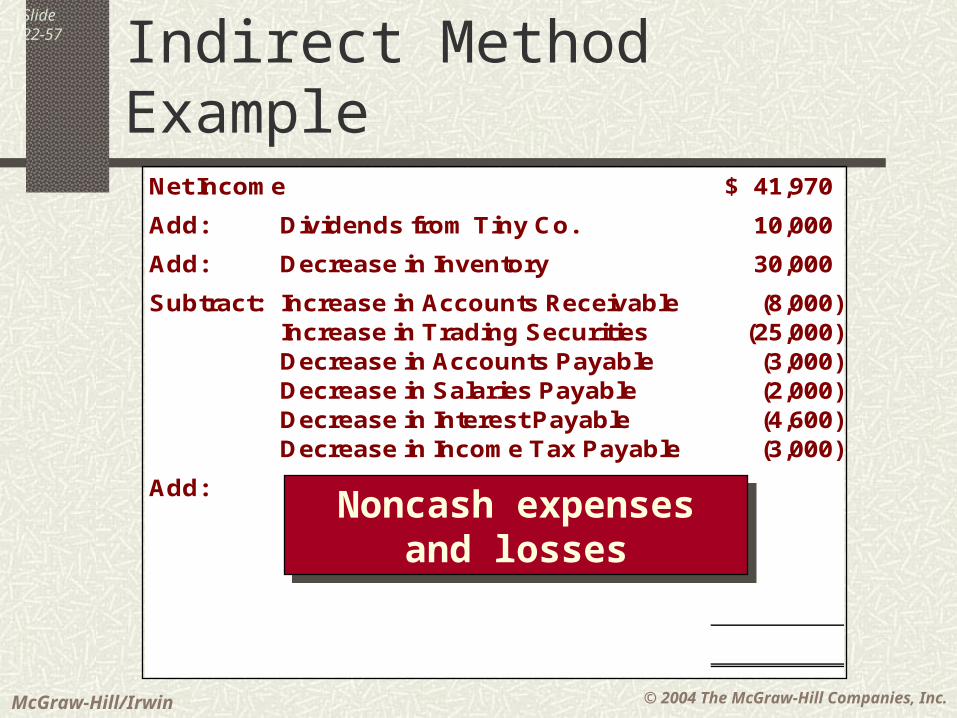

Net Income 41,970$

Add: Dividends from Tiny Co. 10,000

Statement of Cash FlowsIndirect Method Example

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-57

Net Income 41,970$

Add: Dividends from Tiny Co. 10,000

Add: Decrease in Inventory 30,000

Subtract: Increase in Accounts Receivable (8,000) Increase in Trading Securities (25,000) Decrease in Accounts Payable (3,000) Decrease in Salaries Payable (2,000) Decrease in Interest Payable (4,600) Decrease in Income Tax Payable (3,000)

Add:

Noncash expenses and losses

Noncash expenses and losses

Statement of Cash FlowsIndirect Method Example

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-58

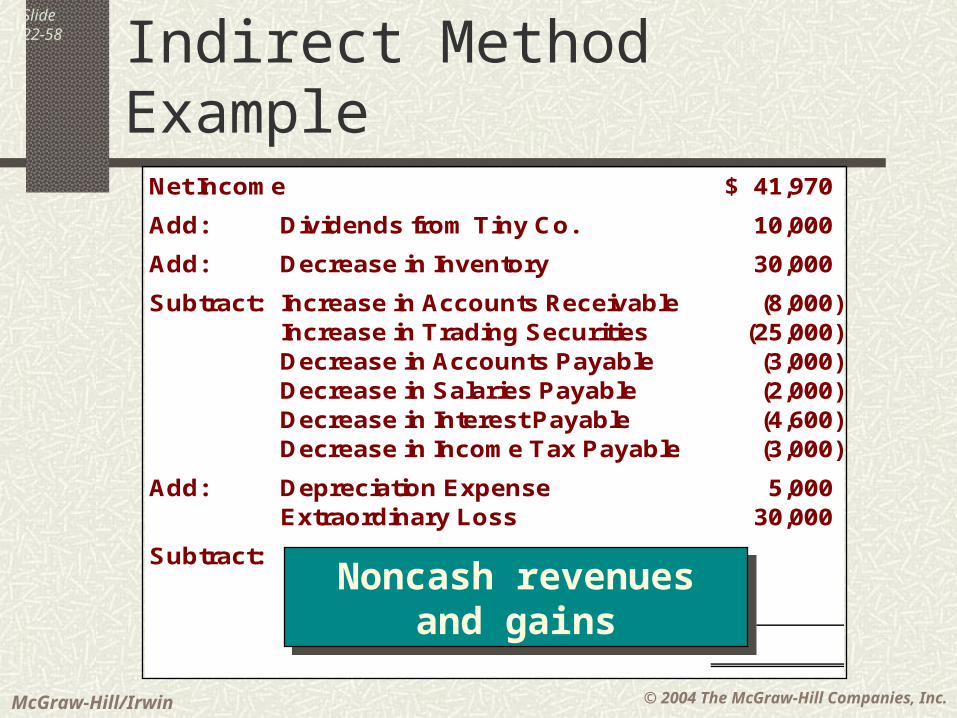

Net Income 41,970$

Add: Dividends from Tiny Co. 10,000

Add: Decrease in Inventory 30,000

Subtract: Increase in Accounts Receivable (8,000) Increase in Trading Securities (25,000) Decrease in Accounts Payable (3,000) Decrease in Salaries Payable (2,000) Decrease in Interest Payable (4,600) Decrease in Income Tax Payable (3,000)

Add: Depreciation Expense 5,000 Extraordinary Loss 30,000

Subtract:

Noncash revenues and gains

Noncash revenues and gains

Statement of Cash FlowsIndirect Method Example

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-59

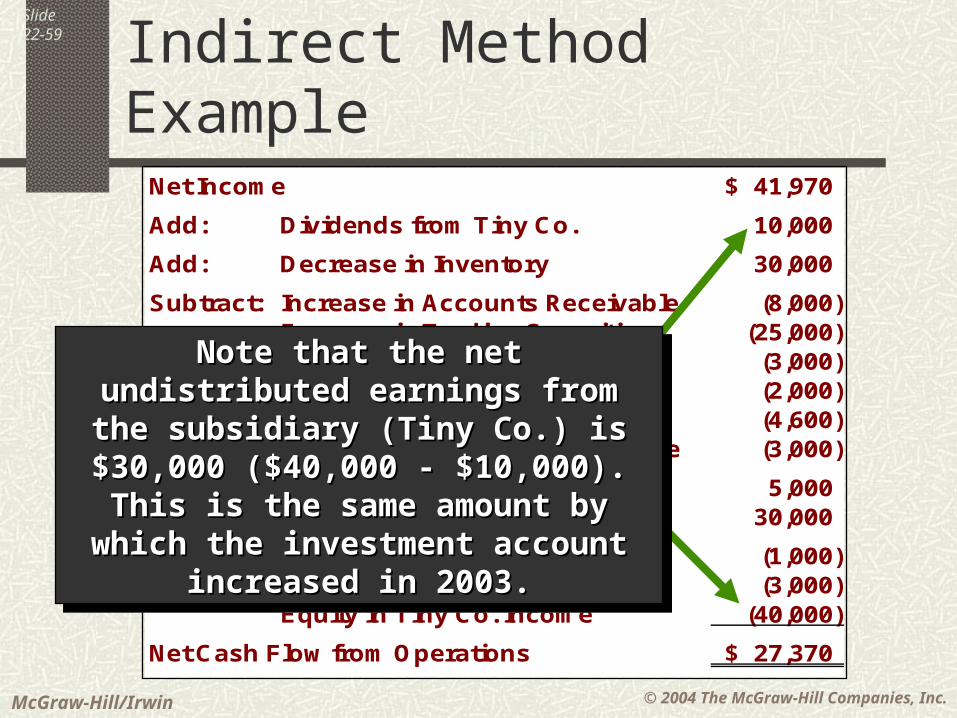

Net Income 41,970$

Add: Dividends from Tiny Co. 10,000

Add: Decrease in Inventory 30,000

Subtract: Increase in Accounts Receivable (8,000) Increase in Trading Securities (25,000) Decrease in Accounts Payable (3,000) Decrease in Salaries Payable (2,000) Decrease in Interest Payable (4,600) Decrease in Income Tax Payable (3,000)

Add: Depreciation Expense 5,000 Extraordinary Loss 30,000

Subtract: Amortization of Bond Premium (1,000) Gain on Sale of Equipment (3,000) Equity in Tiny Co. Income (40,000)

Net Cash Flow from Operations 27,370$

Statement of Cash FlowsIndirect Method Example

Note that the net undistributed Note that the net undistributed earnings from the subsidiary (Tiny earnings from the subsidiary (Tiny Co.) is $30,000 ($40,000 - $10,000). Co.) is $30,000 ($40,000 - $10,000).

This is the same amount by which the This is the same amount by which the investment account increased in 2003.investment account increased in 2003.

Note that the net undistributed Note that the net undistributed earnings from the subsidiary (Tiny earnings from the subsidiary (Tiny Co.) is $30,000 ($40,000 - $10,000). Co.) is $30,000 ($40,000 - $10,000).

This is the same amount by which the This is the same amount by which the investment account increased in 2003.investment account increased in 2003.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-60

Grate Big CompanyStatement of Cash FlowsFor the Period Ending December 31, 2003

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-61

End of Chapter 22I love this job!

Lots of cash flow!