富邦金控簡介 - mzcan.com fhc... · 2 公司聲明 本 ... 獲利 能力及資產 ......

TRANSCRIPT

2015.2.9

富邦金控簡介

2

公司聲明

本文件可能包含「前瞻性陳述」,包括但不限於所有本公司對未來可能發生的業務活動、

事件或發展的陳述。該等陳述係基於本公司對未來營運之假設,及種種本公司無法控制之

政治、經濟、市場等因素所做成,故實際經營結果可能與該等陳述有重大差異。

本文件中所揭露之財務資訊未完全經會計師核閱。

本文件不得視為買賣有價證券或其他金融商品的要約或要約之引誘。

富邦金控競爭策略優勢

台灣地區業務領先

現金股利配發穩定

在競爭環境下股東權益報酬率穩定提升

唯一兩岸三地擁有銀行子行台資之金融機構

掌握佈局大中華地區保險及證券業務的機會

經驗豐富的團隊具堅定持續成長業務的信念

透過有紀律且成功的併購持續成長 業務持續成長

大中華區布局領先

股利配發穩定

3

旗下銀行、證劵、人壽、產險的業務排名皆領先同業

獲利能力及資產規模優於台灣上市櫃金控

國內版圖最完整的金控公司

• 2009年合併

安泰人壽

• 承保及投資皆

位居市場

領先地位

• 1992成立富邦銀行

• 2002年台北銀行換

股成為富邦金控子

公司

• 2005年台北銀行與

富邦銀行正式合併

• 大台北地區民營銀

行分行市占率第一

名

• 經紀業務市占率第三名

• 子公司富邦投信首家參股大陸基金公司

富邦金控

富邦證券

合併總資產: NT$5.4兆

股東權益: NT$4,085億

員工人數:33,938人

• 市場佔有率

第一名

• ECFA後首家

於大陸廈門設立財產保險子公司之台資企業

富邦人壽 富邦產險 1961 1993

台北富邦銀行 1992

• 首家併購香港地區銀行

• 首家參股大陸銀行 (2008參股廈門銀行)

富邦銀行(香港)

2003&2011 1988

2001年成立

富邦華一銀行 2014

• 首家台資金融機構併購大陸銀行

• 兩岸三地銀行佈局領先台灣金融同業

註:1. 合併總資產、股東權益計算至2014.12.31,員工人數更新至2014.11.30

2. 富邦金控除上述子公司外,尚有富邦金控創投、富邦行銷、富邦資產管理、富邦投信、富邦期貨、富邦投顧等子公司 4 4

發展歷程

2002 2004 2000 2009 2014 2008

富邦證券七合一

5

透過策略性併購拓展業務

• $803億台幣

• 2002年富邦金

控以換股方式

取得台北銀行

100%股權

• 2005年正式合

併成為台北富

邦銀行,分行

數達119家,

為當時資產最

大的民營銀行

• $4.15億美元

• 富邦金控以直

接收購的方式

取得港基銀行

75%股權,

2005年更名

為富邦銀行(

香港),成為

首家跨海至香

港併購銀行的

台灣金融機構

• $108億台幣

• 富邦證券以

換股方式合

併環球、中

日、金山、

世霖、華信

及快樂等六

家證券商,

「七合一」

案創下台灣

證劵史上最

大合併案

• $64.5億人民幣

• 台北富邦銀行與

富邦金控合計取

得華一銀行80%

控制性股權,

2014年1月份完

成交割

• 富邦為唯一兩岸

三地都有子行台

資金融機構,為

富邦金控在大陸

長期佈局跨出關

鍵性的一大步

• $6億美元

• 2008年宣布

取得安泰人

壽100%股權

• 2009年6月完

成合併,成

為台灣第二

大壽險公司

• $2.3億人民幣

• 透過富邦銀行(

香港)參股廈門

銀行,成為首

家參股登陸台

資金融機構

管理階層經驗豐富

Daniel Tsai

Chairman, Fubon Financial

• 34 years of industry experience

• Master of Comparative Law, Georgetown University

Richard Tsai

Vice Chairman, Fubon Financial

• 34 years of industry experience

• MBA, New York University

• 資深管理階層皆於金融服務產業領域有超過三十年的經驗

Oliver Cheng

President, Fubon Life

• 42 years of industry

experience

• Joined Fubon in 1973

• BA of Law, National

Taiwan University

Life Insurance Financial Holding Company

Jerry Harn

President, Taipei Fubon Bank

• 26 years of industry

experience

• Joined Fubon in 2005

• MBA, Ohio State University

Taipei Fubon Bank

Victor Kung

Chairman, Fubon Insurance

• 34 years of industry

experience

• Joined Fubon in 2000

• MBA, New York

University / M.A. in

Economics, New York

University

P&C Insurance

6

Vivien Hsu

President, Fubon Funancial

• 37 years of industry experience

• Joined Fubon in 2013

• MBA, University of New South

Wales

Fubon Securities

Samuel Hsu

Chairman, Fubon Securities

• 34 years of industry experience

• Joined Fubon in 2013

• MBA, Chinese Culture

University

公司治理廣獲肯定

獨立董事架構: 13席董事中4席為獨立董事、7席為非執行董事

公司治理獲獎紀錄:

「亞洲地區最佳公司治理」, 亞洲公司治理雜誌 , 2009~2014

富邦金控董事長蔡明忠: 「亞洲企業領袖成就獎」, 亞洲公司治理雜誌, 2010~2014

「台灣最佳企業社會責任」, 亞洲公司治理雜誌, 2011~2014

「公司治理白金獎」, 財資雜誌 , 2011~2014

「台灣企業永續獎-企業社會責任報告書-金融業金獎」, 2014

「天下企業公民-大型企業組前十名, 」 天下雜誌, 2014

「綠色品牌大調查─金融服務業特優」, 數位時代, 2014

7

注: (1) 為民營銀行排名 (2) 前十大發卡行排名;以有效卡為基礎

(3) 房貸餘額統記時間為2014年1~11月,其他資料統計時間為2014年1~12月

市場排名 市占率/金額

聯貸金額 (1) 1 9.2%

匯率類衍生性金融商品名目本金餘額 2 11.7%

房貸餘額 (1) 2 5.1%

信用卡每月簽帳金額 (2) 2 NT$8,102

市場排名 市占率

銀保通路 (首年度保費基礎) 1 17.3%

經代通路 (首年度保費基礎) 1 19.5%

首年度保費 2 16.3%

總保費收入 2 15.3%

業務通路 (首年度保費基礎) 3 14.6%

市場排名 市占率

IPO承銷募資金額 1 24.2%

證券經紀單點 2 0.1%

興櫃交易金額 2 18.6%

證券經紀業務 3 5.7%

市場排名 市占率/金額

直接簽單保費收入 1 22.10%

個人保險業績 1 21.30%

企業保險業績 1 24.10%

員工每人生產力 1 NT$11.7百萬元

市場地位名列前茅

人壽 銀行

產險 證劵

8

5.0

10.3 4.2

4.4

1.0 4.3

台北富邦銀行 富邦人壽 富邦產險 富邦證劵 重疊客戶 富邦金控

金融百貨模式提供多元產品與通路

多元通路提供良好跨售帄台

服務台灣客戶數超過一千萬

註: 台北富邦銀行共127家分行、富邦銀行(香港)共25家分行、 華一銀行共14家分行 (上述資料日期為 2014/12/31)

電子帄台: Fubon.com, Fubon e01電子下單系統, 518fb產險電子帄台等

(百萬人)

台北富邦銀行 富邦人壽 富邦產險 富邦證劵

328 個業務通訊處

30,712 位業務員

72 個業務通訊處

57 個證劵營業據點

616 個ATM

845 位理財顧問

127 家分行

1,016 位業務員 45 家合作保代

16,681 位業務員

海外佈局

註:富邦金控旗下子公司於大陸、菲律賓、馬來西亞、印尼等地設有

辦事處

香港

重慶

越南

福建

台灣

遼寧

泰國

印尼

江蘇

北京

廣東

公司 服務據點

銀行

台北富邦銀行 5處海外分行:香港、洛杉磯、胡志明市、帄陽及河內

富邦銀行(香港) 香港23間分行、 2間證劵服務中心、1間私人貸款中心

廈門銀行 48 間分支行:廈門、福建及重慶

富邦華一銀行 14 間分支行:上海、蘇州、天津及深圳

保險

富邦財險 31處據點: 廈門、福建、重慶、大連、遼寧

越南富邦產險 6處據點: 胡志明市、河內、峴港、帄陽、同奈及海防

越南富邦人壽 2處據點: 河內和胡志明市

證劵

富邦證劵 香港子公司

方正富邦基金 北京

天津

上海

10

菲律賓

臺北富邦銀行,

18.0 , 30%

富邦人壽,

35.5 , 59%

富邦產險,

2.8 , 5%

富邦證劵,

1.4 , 2%

富邦銀行

(香港), 2.3 ,

4% 其他, 0.2 , 0%

11

金控及各子公司獲利成長 獲利貢獻

註:富邦金控和臺北富邦銀行合計持有富邦華一銀行80%股權;

富邦華一銀行獲利貢獻約佔金控2.4%

NT$十億元 NT$十億元

11

註: 2013為反映投資性不動產採公允價值之擬制性數據

各子公司獲利表現

38.5

12.2

25.0

3.2 1.4 1.6

60.2

18.00

35.47

2.8 1.4 2.3

富邦

金控

台北富邦

銀行

富邦

人壽

富邦

產險

富邦

證劵

富邦銀行

(香港)

2013 2014

60,192

49,800

40,547

30,199

16,538 14,076 13,191 12,968 10,850 10,501 10,374 7,794 2,441 1,733 1,570

富邦金 國泰金 中信金 兆豐金 元大金 第一金 華南金 永豐金 開發金 玉山金 合庫金 新光金 日盛金 國票金 台新金

5.88

3.94

2.66 2.43

1.63 1.55 1.52 1.45 1.41 1.13 0.76 0.73 0.69 0.66

0.08

富邦金 國泰金 中信金 兆豐金 元大金 玉山金 第一金 永豐金 華南金 合庫金 日盛金 開發金 新光金 國票金 台新金

12

2014年稅後淨利

2014年每股盈餘

NT$百萬元

獲利表現超越同業

NT$/元

註: 為各家金控公布之全年自結獲利

獲利表現持續領先同業

13 13

每股盈餘

2009 2010 2011

2012 2013 2014

Note: Based on top 5 FHCs of average EPS during 2009 to 2014. 2014 data are preliminary basis.

NT$元

2.5

1.3 1.3 1.1

0.2

Fubon Mega Taishin Cathay CTBC

2.3

1.4 1.3 1.1

0.5

Fubon Mega CTBC Taishin Cathay

3.4

1.6 1.6 1.3 1.1

Fubon CTBC Mega Taishin Cathay

3.1

1.9 1.7 1.6

1.3

Fubon Mega CTBC Cathay Taishin

3.3

2.5

2.0 1.7

1.5

Fubon Cathay Mega Taishin CTBC

5.9

3.9

2.7 2.4

0.1

Fubon Cathay CTBC Mega Taishin

1.2

1.6 1.7

1.2 1.0

1.5

0.0

2.0

1.0 1.0 1.0

1.5

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

現金股利與股東權益報酬率

14 14

現金股利

NT$元

股東權益報酬率

6.3%

9.8% 9.9%

6.8% 5.3%

8.8%

7.0%

11.3%

9.3%

13.5%

10.8% 10.1%

16.2%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 6M14

2014.11.27

富邦金控2014年前九月

法人說明會

16

公司聲明

本文件可能包含「前瞻性陳述」,包括但不限於所有本公司對未來可能發生的業務活動、

事件或發展的陳述。該等陳述係基於本公司對未來營運之假設,及種種本公司無法控制之

政治、經濟、市場等因素所做成,故實際經營結果可能與該等陳述有重大差異。

本文件中所揭露之財務資訊未完全經會計師核閱。

本文件不得視為買賣有價證券或其他金融商品的要約或要約之引誘。

17

子公司營運摘要

• 富邦人壽

• 富邦證劵

富邦金控營運摘要

• 富邦產險

簡報大綱

• 台北富邦銀行

• 海外銀行業務

18

富邦金控 - 2014年前9月營運摘要

台北富邦銀行

富邦人壽

富邦產險

富邦證券

稅後獲利NT$536億元,年成長率78%

初年度等價保費成長率超越市場,來自分期繳貢獻提升

投資績效持續優異

簽單保費市佔率業界第一

承保績效持續優異

收益來源均持續成長

財富管理表現優異,帶動手續費收入成長

各項業務市佔穩定提升

30.1

53.6

9M13 9M14

3.39 3.07

3.90

2011 2012 2013

30.7 29.1

38.5

2011 2012 2013

3.09

5.24

9M13 9M14

19

富邦金控 - 獲利摘要

稅後淨利

每股盈餘

NT$

+78%

+70%

NT$bn

註: (1) *投資性不動產於2014年9月採公允價值模式,9M13和2013年以擬制性基礎反映其影響

(2) 2011年和2012年分別認列出售富邦媒體科技獲利NT$80億和NT$8億

(3) 2012~2014年財務數字為T-IFRS基礎,2011年為ROC GAAP基礎

1.8 5.8

3.2

0.33

0.18 0.59

*

*

*

*

20

富邦金控 - 各子公司獲利表現

金控及各子公司獲利成長 獲利貢獻

註: 9M13為反映投資性不動產採公允價值之擬制性數據,對富邦金控、

台北富邦銀行、富邦人壽、富邦產險、富邦證劵的影響數分別為

32億、0.3億、33億、2億、0.1億

NT$bn NT$bn

註:富邦金控和台北富邦銀行合計持有富邦華一銀行80%股權;

富邦華一銀行獲利貢獻約佔金控2%

台北富邦銀行,

16.6 , 31%

富邦人壽,

31.3 , 58%

富邦產險, 2.4 ,

5%

富邦證劵, 1.2 ,

2%

其他, 2.1 ,

4%

30.1

9.2

19.9

2.7 1.1

53.6

16.6

31.3

2.4 1.2

富邦

金控

台北富邦

銀行

富邦

人壽

富邦

產險

富邦

證劵

9M13 9M14

3,623 4,106

4,597

2011 2012 2013

4,440

5,207

9M13 9M14

324

371

9M13 9M14

21

富邦金控 - 資產與淨值

總資產

淨值

+17%

+14%

NT$bn

NT$bn

註: * 9M13和2013年為反映投資性不動產採公允價值之擬制性數據

234

306 342

2011 2012 2013

23.7

22.6

29.0

27.3

26.4

25.2

*

*

*

*

22

富邦金控 - 資產報酬率與股東權益報酬率

資產報酬率 (ROA)

股東權益報酬率 (ROE)

0.94%

1.46%

9M13 9M14

12.36%

20.05%

9M13 9M14

0.87%

0.75%

0.88%

2011 2012 2013

13.54%

10.71% 11.54%

2011 2012 2013

0.10%

0.57%

0.04%

0.87%

0.13%

1.04%

註: *9M13和2013年為反映投資性不動產採公允價值之擬制性數據

*

*

*

*

不動產增值利益影響數

23

對淨值和損益影響數

對 ROA、ROE和每股淨值的影響數 (2014/9/30)

NT$m 淨值 (2014/9/30) 稅後淨利 (2014年1~9月)

調整前 調整後 差異數 調整前 調整後 差異數

富邦金控 343,752 371,074 27,322 51,786 53,582 1,796

台北富邦銀行 147,975 149,009 1,034 16,537 16,577 40

富邦人壽 168,667 192,537 23,870 29,803 31,253 1,450

富邦產險 20,682 26,235 5,553 2,272 2,372 100

富邦證劵 30,714 31,080 366 1,254 1,246 (8)

ROE ROA 每股淨值

調整前 調整後 差異數 調整前 調整後 差異數 調整前 調整後 差異數

富邦金控 20.92% 20.05% -0.87% 1.42% 1.46% 0.04% 33.59 36.26 2.67

台北富邦銀行 15.68% 15.61% -0.07% 1.14% 1.15% 0.01% 16.59 16.71 0.12

富邦人壽 25.11% 22.98% -2.13% 1.57% 1.64% 0.07% 38.35 43.78 5.43

富邦產險 13.91% 11.59% -2.32% 4.11% 3.97% -0.14% 65.07 82.54 17.47

富邦證劵 5.50% 5.40% -0.10% 2.70% 2.67% -0.03% 18.45 18.67 0.22

註:已扣除合併主體間沖銷金額

24

子公司營運摘要

• 富邦人壽

• 富邦證劵

富邦金控營運摘要

• 富邦產險

簡報大綱

• 台北富邦銀行

• 富邦華一銀行

13.9 14.6 15.8

8.1 8.3 8.4

3.4

6.3

9.4

2011 2012 2013

* Note: Disposal gains of NT$984m from VISA and MasterCard investment in 2Q13

25

台北富邦銀行 - 營收成長

台北富邦銀行營收組成

NT$bn

註: 合併基礎;富邦華一銀行自2014年1月7日計入

營收多元成長

財富管理業務帶動淨手續費收入強勁成長

25.5

29.2

33.6

11.6 12.9

6.1

8.2

7.9

9.2

3.8

9M13 9M14

富邦華一銀行

衍生性商品、外匯與其他收入

淨手續費收入

淨利息收入 34.2

25.5

182.7 140.0

518.5 565.1

39.9 65.6

356.5 376.0

47.0 43.9 7.2 6.9

Sep-13 Sep-14

信用卡循環餘額

其他消金放款

房貸

遠期信用狀買斷及應收帳款承購

企業放款

政府

26

台北富邦銀行 - 授信組成

放款及應收帳款餘額組成

NT$bn YoY +4.0% (放款及應收帳款)

YoY +1.8% (放款)

YoY -4.2%

YoY -6.6%

YoY +5.5%

YoY +9.0%

YoY +64.4%

YoY -23.4%

註: 第12-17頁均為個體基礎

1,151.9 1,197.5

放款成長趨緩主因政府部門還款

排除政府相關之放款年成長率6.8%,含應收帳款類年成長率9.1%

27

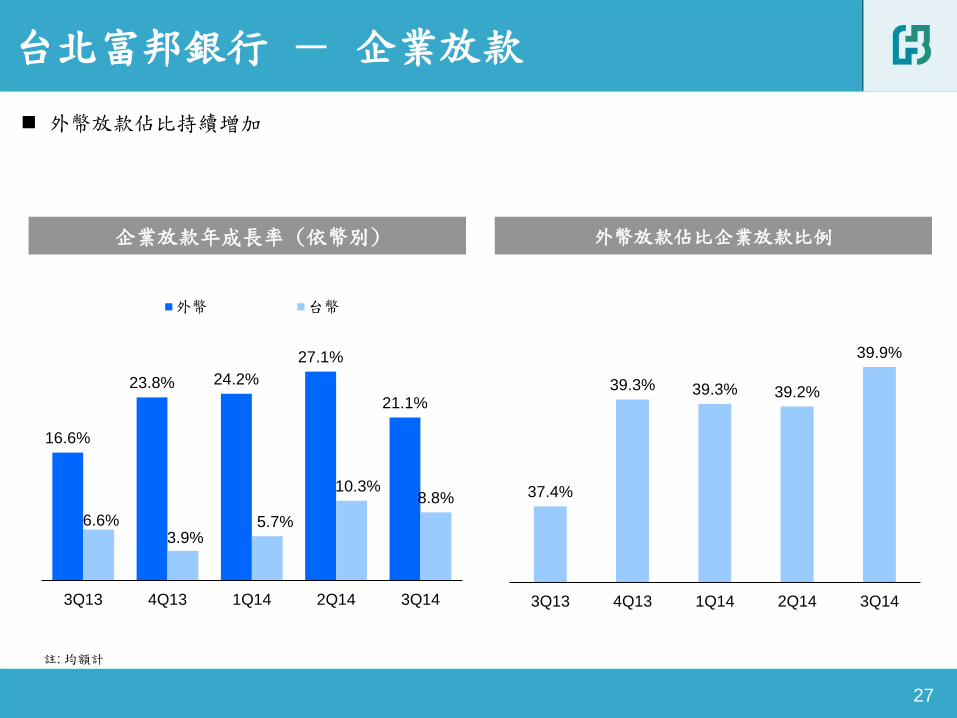

台北富邦銀行 - 企業放款

企業放款年成長率 (依幣別) 外幣放款佔比企業放款比例

註: 均額計

16.6%

23.8% 24.2%

27.1%

21.1%

6.6% 3.9%

5.7%

10.3% 8.8%

3Q13 4Q13 1Q14 2Q14 3Q14

外幣 台幣

37.4%

39.3% 39.3% 39.2%

39.9%

3Q13 4Q13 1Q14 2Q14 3Q14

外幣放款佔比持續增加

28

台北富邦銀行 - 放款利率與收益率

淨利差與存放利差

放款利率與存款利率

註: 放款利率計算包含信用卡循環息

1.98% 2.06% 2.04%

0.64% 0.73% 0.71%

2011 2012 2013

放款利率 存款利率

0.99% 1.01% 1.05%

1.34% 1.33% 1.33%

2011 2012 2013

淨利差 (NIM) 存放利差

1.04% 1.10%

1.34% 1.27%

9M13 9M14

2.04% 2.06%

0.71% 0.79%

9M13 9M14

29

台北富邦銀行 - 存款與存放比

台幣存放比與淨利差 台幣存款組合

外幣存款組合

NT$bn

NT$bn

1,014 988

308 376

註: 期末餘額計

外幣存放比與淨利差

1.02% 1.02%

1.12% 1.30%

NIM

NIM

89.2% 91.0%

Sep-13 Sep-14

70.7% 63.5%

Sep-13 Sep-14

48.9% 53.3%

51.1% 46.7%

Sep-13 Sep-14

定存

活存

46.6% 38.4%

53.4% 61.6%

Sep-13 Sep-14

定存

活存

708 663 774 984 1,007 986 1,290 87 80 79

85 90 71

65 806 831 514

616 797 807

875 197 204 423 228

268 393

373

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14

結構式商品與其他

共同基金

信託

銀行保險

30

台北富邦銀行 - 手續費收入與財富管理業務

手續費收入來源

財管業務收益

1,778 1,789 1,912

2,162

NT$m

NT$m

財管業務成長動能強勁,帶動全行手續費收入年成長31.5%

註: 資料包含台北富邦銀行及北富銀人身保代

2,256

1,798

6,269

4,526

813 314

8,249

6,408

862 438

手續費收入 財富管理 信用卡 聯貸

9M13 9M14

2,603

3,639

41

9M13 9M14

福聚能放款提列50%呆帳準備(10

月底達80%),為其他放款回收所抵消

為達正常放款1%提存,增加NT$37億元提存

0.0%

0.2%

0.4%

0.6%

Sep-11 Mar-13 Sep-14

企業放款 房貸

31

台北富邦銀行 - 資產品質

逾放比

法金放款與房貸逾放比 提存金額

備抵呆帳覆蓋率

0.30%

0.02%

1068.2%

589.5%

Sep-13 Sep-14

0.11%

0.20%

Sep-13 Sep-14

福聚能NT$11.4億元放款轉列逾放

NT$m

32

子公司營運摘要

• 富邦人壽

• 富邦證劵

富邦金控營運摘要

• 富邦產險

簡報大綱

• 台北富邦銀行

• 富邦華一銀行

222.8 249.7

212.9

145.4

171.0 207.2

2011 2012 2013

初年度保費 續年度保費

33 33

368.2

420.7

NT$bn

富邦人壽 - 總保費收入

420.1

初年度續年度保費成長帶動總保費年成長9%

149.8 160.2

150.3 167.0

9M13 9M14

300.1 327.3

初年度保費收入組成

34

富邦人壽 - 初年度保費(FYP)收入

初年度保費收入年成長7%

傳統型分期繳貢獻提升

NT$bn 9M13 % 9M14 % YoY

傳統壽險:分期繳 22.9 15.3% 40.8 25.4% 77.7%

傳統壽險:躉繳 77.1 51.5% 98.0 61.2% 27.1%

利變年金險 38.6 25.8% 5.8 3.6% -85.0%

投資型保單 7.3 4.9% 11.6 7.2% 58.1%

健康險、傷害險和其他 3.8 2.5% 4.0 2.5% 7.0%

合計 149.8 100.0% 160.2 100.0% 7.0%

8.2% 8.2% 9.5%

4.3% 2.7% 10.3% 1.0% 0.8%

1.8%

22.6% 25.2% 20.1%

63.9%

63.1%

58.3%

2011 2012 2013

傳統壽險:分期繳

傳統壽險:躉繳

投資型保單

利變年金險

健康險、傷害險和其他

35

54.2

68.6

62.3

NT$bn

富邦人壽 - 初年度等價保費(FYPE)收入

39.1

46.9

初年度等價保費收入成長20.1%, 超越市場同期成長率12.9%

追求分期繳儲蓄型商品及高利潤商品持續成長

初年度保費依通路別

36

NT$bn

富邦人壽 - 銷售通路分佈

銀行通路 – 初年度保費收入

NT$bn

業務員人數

14,800

16,297

Sep-13 Sep-14

89.2 70.7

8.3 23.5

9M13 9M14

分期繳壽險

躉繳壽險 & 利變年金

業務員通路保費收入穩定成長,組織人數持續增加

銀行通路持續加強傳統型商品銷售,分期繳比重大幅提升

34.1 47.2

71.2 67.1

26.4 27.2

18.3 18.7

9M13 9M14

其他

銀行保代:台北富邦銀行

銀行保代:外部銀行

業務員通路

37 37

經常性收益為投資收益主要來源

利得收益創造佳績

富邦人壽 - 投資收益組成

NT$bn 9M13 9M14 YoY 2011 2012 2013

經常性投資收益 57.2 67.5 18.0% 52.0 62.7 74.4

債劵類投資利得 7.8 10.6 36.3% 2.6 7.9 8.0

股票類投資利得 3.3 12.1 264.6% 5.2 4.7 4.0

外匯及其他 -4.3 -5.9 36.5% -5.1 -6.6 -6.3

投資性不動產公允價值變動 * 2.9 1.3 -56.3%

總投資收入 66.9 85.6 28.0% 54.7 68.6 80.2

總投資資產 2130.3 2466.1 15.8% 1573.2 1932.3 2203.7

註: *9M13為反映投資性不動產採公允價值之擬制性數據

38 38

投資資產規模年成長15.8%

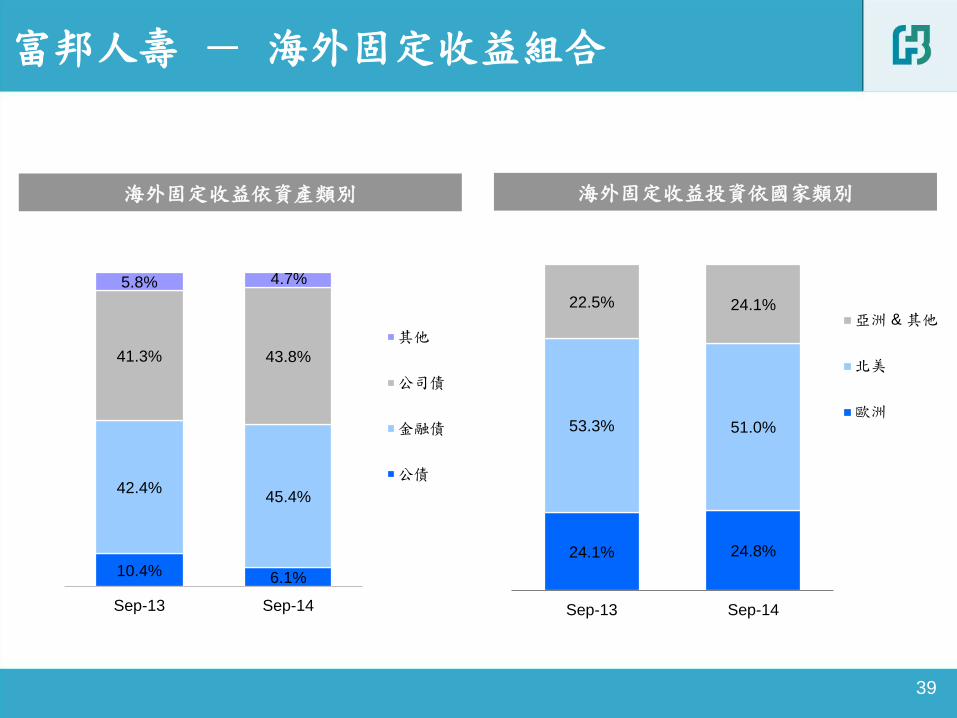

海外股債佔比提升

國際板債劵投資達總投資資產2.1%

富邦人壽 - 投資組合

2013/9/30 2014/9/30

NT$bn

現金及約當現金 112.2 5.3% 132.8 5.4%

國內債券 612.2 28.7% 631.5 25.6%

國外債券 897.8 42.1% 1,072.9 43.5%

國內股票 233.2 10.9% 256.2 10.4%

國外股票 63.7 3.0% 119.3 4.8%

房貸 48.9 2.3% 65.9 2.7%

保單貸款 48.0 2.3% 50.3 2.0%

不動產 114.2 5.4% 137.1 5.6%

總投資資產 2,130.3 100.0% 2,466.1 100.0%

國內 1,168.8 54.9% 1,273.9 51.7%

國外 961.5 45.1% 1,192.2 48.3%

39

海外固定收益依資產類別

富邦人壽 - 海外固定收益組合

海外固定收益投資依國家類別

10.4% 6.1%

42.4% 45.4%

41.3% 43.8%

5.8% 4.7%

Sep-13 Sep-14

其他

公司債

金融債

公債

24.1% 24.8%

53.3% 51.0%

22.5% 24.1%

Sep-13 Sep-14

亞洲 & 其他

北美

歐洲

40 40

避險成本 & 外匯損益 外幣資產

67 bps 72 bps

持續性收益 (避險前)

富邦人壽 - 避險組合

-41

-60

-26

-12

9M13 9M14

-41

-60

-26

-12

9M13 9M14

外匯損益 & 準備

金淨提存

經常性避險成本

-41

-60

-26

-12

9M13 9M14

外匯損益 & 準備

金淨提存

經常性避險成本

完全避險,

75.8%

美元部位,

9.9%

其他幣別

部位,

2.4%

股票/共同

基金,

11.9%

3.87% 3.97%

3.64% 3.62%

9M13 9M14

避險前

避險後

4.01% 3.89%

4.57%

5.02%

Sep-13 Sep-14

負債成本 投資報酬率

41 41

投資利差

投資利差持續改善,提升公司獲利

經常性投資收益率大於損益兩帄點,持續創造公司穩定獲利來源

富邦人壽 - 投資利差持續改善

損益兩帄點與經常性收益率

損益兩帄點 = (稅前淨利– 投資收入) / 帄均投資資產

*

註: *9M13為反映投資性不動產採公允價值之擬制性數據

3.05% 2.90%

3.64% 3.62%

Sep-13 Sep-14

損益兩帄點 經常性投資收益率

0.22%

0.07%

70.8

31.0

8.4 12.0

19.4

Jun-14 Sep-14

42 42

富邦人壽淨值

NT$bn

NT$bn

備供出售金融資產未實現損益變動 備供出售金融資產未實現損益

156.0 170.2 171.3

191.6 192.5

Sep-13 Dec-13 Mar-14 Jun-14 Sep-14

實現利得

股票投資之

股息收入 評價影響

19.8 22.4

23.9

* *

NT$bn

富邦人壽 - 資本水準

註: *9M13和2013年為反映投資性不動產採公允價值之擬制性數據

43

子公司營運摘要

• 富邦人壽

• 富邦證劵

富邦金控營運摘要

• 富邦產險

簡報大綱

• 台北富邦銀行

• 富邦華一銀行

52.5% 53.5%

34.7% 34.4%

9M13 9M14

淨費用率

淨損失率

9.7 10.3

4.2 4.3

1.4 1.3 0.9 0.8

2.8 3.1

2.0 2.1

9M13 9M14

其他

健康/傷害險

工程險

水險

火險

車險

44

自留綜合率

44

NT$bn

20.9 21.9

87.2% 87.9%

簽單保費市佔率業界第一

核保利潤表現優異

註:為個體報表基礎 註:不包括汽車強制險,強制險係為無盈無虧之經營

富邦產險 - 營運摘要

險種別直接簽單保費

45

子公司營運摘要

• 富邦人壽

• 富邦證劵

富邦金控營運摘要

• 富邦產險

簡報大綱

• 台北富邦銀行

• 富邦華一銀行

46

富邦證劵 - 營運摘要

市場排名

營業收入

NT$m

各項業務市佔穩定提升

承銷業務市佔率第一

稅後淨利

1,142

1,246

9M13 9M14

4,232

4,642

9M13 9M14

9M14 市場排名 9M13 市場排名

經紀市佔率 5.81% 第3名 5.48% 第3名

經紀單點市佔率 0.10% 第2名 0.09% 第3名

興櫃交易金額市佔率 18.94% 第2名 17.45% 第2名

承銷募資金額市佔率 7.37% 第4名 5.68% 第5名

初次上櫃承銷金額市佔率 29.29% 第1名 13.25% 第3名

47

子公司營運摘要

• 富邦人壽

• 富邦證劵

富邦金控營運摘要

• 富邦產險

簡報大綱

• 台北富邦銀行

• 富邦華一銀行

48

富邦華一銀行 - 資產負債摘要

資產

存款 放款

淨值

RMB$m

28,506

31,278

Sep-13 Sep-14

40,200 38,920

Sep-13 Sep-14

44,268

56,620

Sep-13 Sep-14

3,228

4,433

Sep-13 Sep-14

49

富邦華一銀行 - 營運摘要

資產報酬率 & 股東權益報酬率

淨利差 稅後淨利

逾放比 & 備抵呆帳覆蓋率

RMB$m

資產品質及淨利差均改善

416

329

Sep-13 Sep-14

1.25% 0.83%

18.29%

11.70%

Sep-13 Sep-14

ROAA ROAE

2.44%

1.74% 1.86%

Sep-13 Jun-14 Sep-14

0.37%

1.48%

0.94% 476.2%

154.8%

264.7%

Sep-13 Jun-14 Sep-14

逾放比 呆帳覆蓋率

2013年富邦人壽隱含價值

2013年彙整

項目 2012 2013 年增率 差異 影響

淨值 (帳面價值 ) 165.6 147.8 -10.8% -17.9

調整後淨值 101.1 133.8 32.4% 32.7

有效契約價值 (不含資本成本 ) 175.1 229.9 31.3% 54.8

資本成本 (58.4) (68.0) -16.5% -9.6

有效契約價值 (含資本成本 ) 116.8 161.9 38.7% 45.1

隱含價值 (Embedded Value) 217.9 295.7 35.7% 77.9

初年度保費 (FYP) 249.7 212.9 -14.8% -36.9

初年度等價保費 (FYPE) 68.6 54.2 -21.1% -14.5

新契約年化等價保費 (APE) 71.7 54.5 -24.0% -17.2

新契約價值 (VNB, V1NB) 31.7 31.8 0.3% 0.1

新契約價值利潤率 (VNB/FYP) 12.7% 15.0% 17.7% 2.2%

新契約價值利潤率 (VNB/FYPE) 46.2% 58.8% 27.1% 12.5%

新契約價值利潤率 (VNB/APE) 44.2% 58.4% 32.0% 14.2%

新契約乘數 8.84 8.84 0.0% 0.0

精算評估價值 (Appraisal Value) 498.4 577.2 15.8% 78.7

在外流通股數 (金控 ) 9.5 10.2 7.3% 0.7

每股隱含價值 22.8 28.9 26.5% 6.0

每股精算評估價值 52.3 56.4 7.9% 4.1

Inforce

Value Creation

New Sales

Value Creation

Appraisal Value

(20 year NB)

Value per FHC

share

NT$bn

51

Unit: NT$ BN

% of change + 0.8% -23.3% + 11.6% -10.8%

Adjust.% + 1.0% -10.3% -0.1% -9.4%

(38.5) (15.2) 133.8

(0.2)1.5165.6

1.3 19.2

147.8

- 40.0

10.0

60.0

110.0

160.0

Statutory Net

Worth@Dec.

31, 2012

IFRS adj Un-realized

capital gain

Earning Statutory Net

Worth@Dec.

31, 2013

Special

Reserve

(FX and RE

Appraisal)

Adjust Market

Value of

(AFS) Fixed

Income Asset

to Book

Value

Goodwill Adjusted Net

Worth@Dec.

31, 2013

因四捨五入,數字可能無法加總

價值變動分析: 從淨值 (帳面價值)至調整後淨值

52

價值變動分析: 有效契約價值 (不含資本成本)

Unit: NT$ BN

註:

2012年有效契約價值的等價投資報酬率為4.45% ,反映rolling over效果,增加為4.51%。

2013年有效契約價值的等價投資報酬率為4.57% 。

2013年新契約價值(含資本成本) 為 318 億元

% of change -9.6% + 12.2% + 2.0% + 5.1% + 1.0% + 20.6% + 31.3%

229.9

36.0

1.79.03.521.4

175.1 (16.9)

- 20.0

30.0

80.0

130.0

180.0

230.0

2012 VIF

(before CoC)

Existing

business -

transfer to net

worth

Required

return on

existing

business

Model & Data

Change

Eco.

Assumption

Change

Non-eco.

Assumption

Change

2013

VNB(before

CoC)

2013

VIF(before

CoC)

53

Unit: NT$ BN

註:

2012年新契約價值的等價投資報酬率為4.41%,反映rolling over效果及2013年新銷售保單,等價投資報酬率下降為4.23% 。

2013年新契約價值的等價投資報酬率為4.50%。

價值變動分析: 新契約價值

% of change -24.0% + 7.9% + 12.6% + 3.8% + 0.3%

VNB/APE 44.2% 0.0% + 4.6% + 7.3% + 2.2% 58.4%

31.7

1.2

(7.6)

2.5

4.0

31.8

- 8.0

- 6.0

- 4.0

- 2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

22.0

24.0

26.0

28.0

30.0

32.0

34.0

36.0

38.0

40.0

2012 VNB Sales Volume Product Mix Econ. Change Non-Econ. Change 2013 VNB

54

經濟假設

• 外匯價格準備金於2012年3月實施,其相關成本反映於投資報酬率假設。

Year 2012 Year 2013

投資報酬率假設

有效契約價值

台幣保單:

2013年 至 2051年為3.88%~5.32%(2052+)

美元保單 :

2013年 至 2017年為5.16%~5.18%(2018+)

一年新契約價值

台幣保單:

2013年 至 2051年為3.39%~5.32%(2052+)

美元保單 :

2013年 至 2020年為4.83%~5.18%(2021+)

利變年金

帄均利差益約為 100bps

有效契約價值

台幣保單 :

2014年 至 2051年為3.94%~5.32%(2052+)

美元保單 :

2014 至 2036年為5.16%~5.94%(2037+)

一年新契約價值

台幣保單:

2014年 至 2048年為3.74%~5.32%(2049+)

美元保單 :

2014年 至 Year 2032年為5.14%~5.94%(2033+)

利變年金

帄均利差益約為 100bps.

貼現率 11% for VIF; 10.5% for V1NB 11% for VIF; 10.5% for V1NB

等價投資報酬率 有效契約價值 : 4.45% (rolling over to 2013: 4.51%)

新契約價值 : 4.41% (rolling over to 2013: 4.23%)

有效契約價值 : 4.57%

新契約價值 : 4.50 %

評價日之殖利率

(10 年期)期初 / 長期

台幣: 1.29% / 3.50%

美元 : 1.84% / 5.25%

台幣: 1.72% / 3.50%

美元 : 3.09% / 5.25%

55

經濟假設: 有效契約投資報酬率

56

經濟假設: 一年新契約投資報酬率

57

經濟假設: 貼現率

富邦人壽 2012/12/31 2013/12/31

無風險利率 1.29%~3.5% 1.72%~3.5%

股票及國家風險溢酬 7.00% 6.50%

BETA值 1.2 1.2

風險貼現率估計 9.7%~11.9% 9.5%~11.3%

價值評估使用之風險貼現率 有效契約價值:11.0%

一年新契約價值:10.5% 有效契約價值:11.0%

一年新契約價值:10.5%

• 風險貼現率: 依資本資產定價模型 (CAPM, Capital Asset Pricing Model)訂定;

風險貼現率 = 無風險利率 + BETA值 * 股票及國家風險溢酬。

58

資本成本

資本成本估算

資本成本主要係依據法定最低要求200%RBC之計算基礎估算而來, 並考慮下述因子:

1) K 值: 2013年貣上升至0.5,之後維持不變;

2) 加計前一年度傳統型商品C3調整後之風險資本額總計的10%

(除了投資型商品以外之所有商品) ;

3) 反映公司目前經營狀況以及未來營運策略。

2013年風險資本(RBC)法規變動與調整:

1) 修改C1集中度風險計算基礎(將國外投資總額拆分至六項分類)

2) 調整C1s分類(將股票型基金併入C1s)

3) 修改投資性不動產素地展延次數之計算基礎。

59

敏感度分析: 投資報酬率

註:調整後淨值不受投資報酬率假設影響

-17.5% 17.5% -26.6% 26.6%

-14.6% 14.6% -13.6% 13.6%

(40.2)

229.9

40.2

Return - 0.25% Base Return + 0.25%

43.1(43.1)

295.7

Return - 0.25% Base Return + 0.25%

43.1

161.9

(43.1)

Return - 0.25% Base Return + 0.25%

4.3

(4.3)

31.8

Return - 0.25% Base Return + 0.25%

VIF (before CoC) VIF

EV VNB

NT$bn

60

8.2% -6.9% 14.3% -12.0%

7.8% -6.6% 13.9% -11.8%

18.8

229.9

(15.8)

RDR - 1% Base RDR + 1%

23.1

295.7

(19.4)

RDR - 1% Base RDR + 1%

(19.4)

161.9

23.1

RDR - 1% Base RDR + 1%

31.8

4.4(3.8)

RDR - 1% Base RDR + 1%

VIF (before CoC) VIF

EV VNB

敏感度分析: 貼現率

註:調整後淨值不受貼現率假設影響

NT$bn

61

7.2%

8.7%8.0%

12.7%12.6%

15.0%

EV2008 EV2009 EV2010 EV2011 EV2012 EV2013

CAGR: 16% (2.1x)

11.8

17.9

24.8

28.031.831.7

EV2008 EV2009 EV2010 EV2011 EV2012 EV2013

CAGR: 22% (2.7x)

38.552.5

73.688.7

116.8

161.9

EV2008 EV2009 EV2010 EV2011 EV2012 EV2013

CAGR: 33% (4.2x)

77.7

128.8155.5

176.0

217.9

295.7

EV2008 EV2009 EV2010 EV2011 EV2012 EV2013

CAGR: 31% (3.8x)

2013彙整: 富邦人壽歷年隱含價值相關數值

新契約價值

有效契約價值

新契約獲利率 (VNB / FYP)

隱含價值

NT$bn

62

允當的投資報酬率假設

3.68

3.87 3.883.97

4.06

3.78 3.80

4.01 4.05

EV2009 EV2010 EV2011 EV2012 EV2013

Assumption Actual

63

德勤精算顧問審閱意見

The Engagement

• Deloitte Actuarial and Insurance Solutions (Hong Kong) Limited (“Deloitte Actuarial”) were retained by Fubon

Life to perform an independent review of the Embedded Value (EV) as at 31 December 2013 and the Value

of One Year’s New Business (V1NB) written over the period of 1 January 2013 to 31 December 2013.

Scope of Deloitte Actuarial’s Involvement

• Review and opine on the reasonableness of the EV and V1NB as calculated by the Company;

• Review of the reasonableness of the assumptions used in the calculations, taking into consideration both the

Company’s recent experience and the experience of the Taiwanese life insurance market;

• Review, at a high-level, model changes to the actuarial projection model since the previous valuation date;

• Review of the Company’s projection approach of the Cost of Capital;

• Review of the data put through the model compared to the policy data on the Company’s policy

administration systems to judge the extent to which the business has been valued in the financial model and

to identify the portion (if any) omitted and how that was valued;

• Review of the approach used to determine the Adjusted Net Worth (“ANW”), in particular, the adjustments

made in deriving the ANW, and any other adjustments made outside of the actuarial projection model;

• Review of the Company's analysis of change in the Value of In-Force Business (“VIF”) between 31 December

2012 and 31 December 2013.

Deloitte Actuarial

64

65 65

Risk Adjusted Discount Rates

Fubon Life calculated the EV and V1NB at Risk Adjusted Discount Rates (“RDR”) of 11.0%

and 10.5% respectively.

RFR based on current government

bond yield

RFR based on Company’s long-

term view

Equivalent RFR for New Business

Equivalent RFR for In-Force Business

Risk Free Rate (“RFR”) 1.72% 3.50% 2.66% 2.78%

Equity and Country Risk Premium 6.50% 6.50% 6.50% 6.50%

Beta 1.20 1.20 1.20 1.20

Calculated Risk Discount Rate 9.52% 11.30% 10.46% 10.58%

Risk Discount Rate used in the Valuation for VIF

11.00%

Risk Discount Rate used in the Valuation for V1NB

10.50%

Reference – RDR based on Capital Asset Pricing Model (CAPM):

RDR = RFR + Beta * Equity and Country Risk Premium

66 66

Comments on the Risk Adjusted Discount Rates

Deloitte Actuarial independently derived a range of RDRs using the CAPM approach:

The low end of the RDR is developed based on the current yield on 10-year Taiwan government bonds.

The high end of the RDR is developed based on the Company’s view of the 10-year Taiwan government

bond in the future.

The equivalent RFR is the RFR equivalent to using a set of graded-up RFR from 1.72% to 3.50% that

derives the same VIF and V1NB.

The Equity and Country Risk Premium was developed based on the Country Default Spreads and Risk

Premiums research published by New York University.

The Beta of 1.2 was set using a risk profiling approach which considers risks related to the product range,

distribution diversification/vulnerability, regulatory intervention and investments. Note that this beta value

is consistent with that used in previous valuations.

The RDR assumption applied by Fubon Life in the valuation lies within the range of RDR that we derived.

In particular, we feel comfortable with different RDRs being used for the valuation of the in-force and new

business, given the specific market conditions in Taiwan: it is well-known that the legacy business has a

much riskier profile than the current new business, and hence it is reasonable for shareholders to be

expecting a higher rate of return for the higher risk level. We feel that Fubon Life has taken a good

approach in splitting up the RDR assumption for the two distinctively different blocks of business.

Deloitte Actuarial

67 67

Comments on Investment Return (1)

A set of rising investment return assumption has been used in this valuation which is

considered reasonable for the present market conditions.

Deloitte Actuarial

Fubon Life’s derivation of the investment return assumption is featured by the following:

• Derivation methodology is consistent with that applied in previous valuations;

• The methodology involves:

For VIF, the investment return assumption was derived from a combination of the investment

return generated by the run-off of the existing asset portfolio and of that from future purchases

of new assets;

For V1NB, the new business is not supported by returns on existing assets and the

investment return was derived from future purchases of new assets;

• New assets are purchased at the prevailing new money rates, which are set to equal to the expected

future risk free rates plus a risk margin for each asset type;

• Future risk free rates are set starting off with the actual yield curves as at the valuation date and are

assumed to rise to a long-term level over a 10-year period. For New Taiwan Dollar and US Dollar

respectively, the initial risk free rates are 1.72% and 3.09% and a long-term risk free rate of 3.50%

and 5.25% is assumed.

• Different assumptions were derived for different types of business, which were assumed to have a

different long-term asset allocation.

• For some business lines, the investment return assumption derived in the above-mentioned manner

was capped at a certain level for conservative reasons.

68 68

Comments on Investment Return (2)

It is in Deloitte Actuarial’s view that:

Methodology

• Fubon Life’s derivation methodology for the investment return assumption is reasonable and

consistent with the way that the ANW is calculated;

Economic Assumptions

• The expected long-term risk-free rate for New Taiwan Dollar yield and US Dollar yield are

maintained at 3.5% and 5.25% respectively.

• We note that taking a view on the future capital market is not uncommon under the traditional

Embedded Value methodology. On a macro-economic level the arguments put forward for

rising interest rates are plausible, and we note that the expected future rise in yields is spread

out over a reasonably long period of 10 years.

• Readers should be aware that capital market conditions are subject to the impact of many

forces. Yields and prices of financial instruments can move dramatically in a short period of

time. As a result, it is difficult to predict the interest rate level in the future with great certainty.

Readers should refer to the sensitivity tests to develop a broader understanding of the impact of

the investment return assumption on the assessment of the economic value of Fubon Life.

• Overall, the economic assumptions appear to be reasonable.

Deloitte Actuarial

69 69

Comments on EV and V1NB Results

Deloitte Actuarial

Deloitte Actuarial have reviewed the Embedded Value and Value of One

Year’s New Business results at a high-level under the generally accepted

method for calculating traditional embedded values in Taiwan:

•Review of the changes in the VIF relative to the assumption changes and model

changes from 2012 to 2013;

•Review of the changes in the new business profit margin relative to that in 2012 based

on information on changes in sales mix, sales volume and valuation assumptions;

•Review of the sensitivities relative to the base case results.

The Embedded Value and Value of One Year’s New Business results

appear to be reasonable within the above context.

Deloitte Actuarial’s detailed opinion can be found in their opinion letter.

70 70

Comments on Non-Economic Assumptions

Non-Economic Assumptions

• The non-economic assumptions reflect Fubon Life’s best estimate of future operating

experience, and are appropriately supported by the company’s historical operating experience.

Deloitte Actuarial

謝謝