© the mcgraw-hill companies, inc., 2001 irwin/mcgraw-hill chapter 10 reporting and interpreting...

Post on 21-Dec-2015

217 views

TRANSCRIPT

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Chapter 10

Reporting and Interpreting Bonds

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Significant debt needs of a company are often filled

by issuing bonds.

Significant debt needs of a company are often filled

by issuing bonds.

Business BackgroundCapital Structure - Bonds

Bonds Cash

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Business Background

Bonds can be traded on

established exchanges that

provide liquidityliquidity to

bondholders.

Bonds can be traded on

established exchanges that

provide liquidityliquidity to

bondholders.

As liquidity increases . . .

. . . Cost of borrowing decreases.

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Business Background

Advantages of bonds:• Bonds are debt, not equity, so the

ownership and control of the company are not diluted.

• Interest expense is tax-deductible.• The low interest rates on bonds

allow for positive financial leverage.

Advantages of bonds:• Bonds are debt, not equity, so the

ownership and control of the company are not diluted.

• Interest expense is tax-deductible.• The low interest rates on bonds

allow for positive financial leverage.

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Business Background

Disadvantages of bonds:• The scheduled interest

payments are legal obligations and must be paid each period.

• A single, large principal payment is required at the maturity date.

Disadvantages of bonds:• The scheduled interest

payments are legal obligations and must be paid each period.

• A single, large principal payment is required at the maturity date.

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Key Ratio Analysis

The debt-equity ratio is an important measure of the balance between debt and

equity.

High debt-equity ratios(Greater than 1 to 1) indicate more leverage and risk.

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

1. Face Value = Maturity or Par Value, Principal2. Maturity Date3. Stated Interest Rate 4. Interest Payment Dates5. Bond Date

Characteristics of Bonds Payable

Other Factors:6. Market Interest Rate7. Issue Date

BOND PAYABLE

Face Value $1,000 Interest 10%

6/30 & 12/31

Maturity Date 1/1/10Bond Date 1/1/01

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

• Senior Debt Senior Debt receives preference over other creditors in the event of bankruptcy or default.

• Subordinated Debt Subordinated Debt is riskier than senior debt.

• Senior Debt Senior Debt receives preference over other creditors in the event of bankruptcy or default.

• Subordinated Debt Subordinated Debt is riskier than senior debt.

Bond Classifications

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

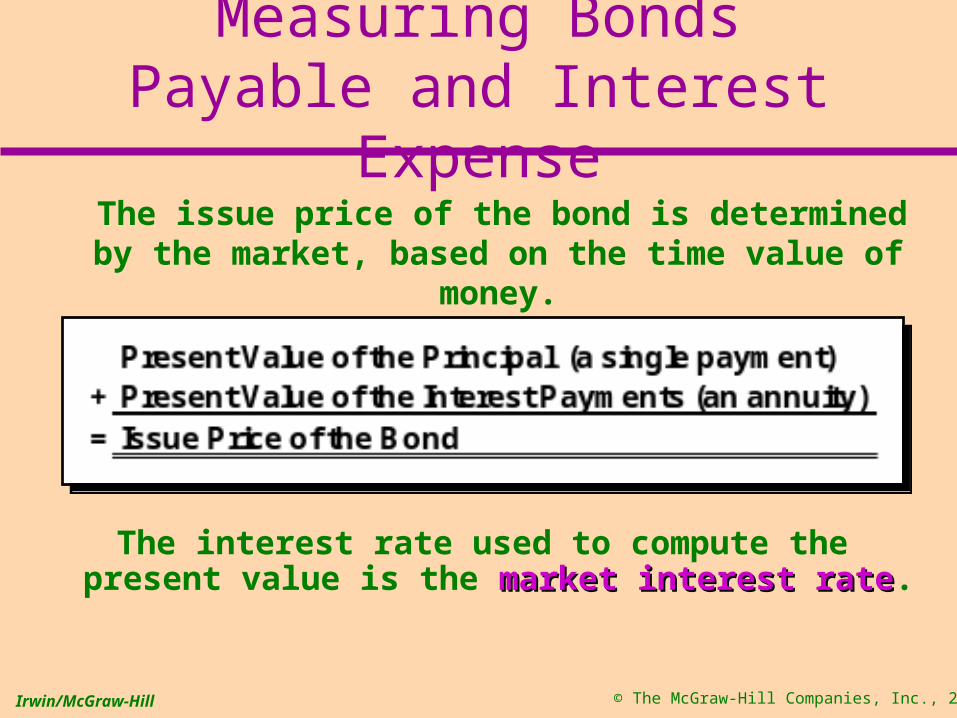

Measuring Bonds Payable and Interest Expense

The issue price of the bond is determined by the market, based on the time value of money.

The interest rate used to compute the present value is the market interest ratemarket interest rate.

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Measuring Bonds Payable and Interest Expense

The stated ratestated rate is only used to compute the periodic interest payments.

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Bond Premium and Discounts (See-Saw Diagram)

=

>

<

>

<

=

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Issuing Bonds

On May 1, 2001, Harrah’s issues $1,000,000 in bonds having a stated rate of 6% annually. The bonds mature in 10 years and interest is paid semiannually.

The market rate is 8% annually.

On May 1, 2001, Harrah’s issues $1,000,000 in bonds having a stated rate of 6% annually. The bonds mature in 10 years and interest is paid semiannually.

The market rate is 8% annually.

Are Harrah’s bonds issued at par, at a discount, or at a premium?

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

On May 1, 2001, Harrah’s issues $1,000,000 in bonds having a stated rate of 6%

annually. The bonds mature in 10 years and interest is paid semiannually. The

market rate is 8% annually.

On May 1, 2001, Harrah’s issues $1,000,000 in bonds having a stated rate of 6%

annually. The bonds mature in 10 years and interest is paid semiannually. The

market rate is 8% annually.

Issuing Bonds

< <

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Issuing Bonds

On May 1, 2001, Harrah’s issues $1,000,000 in bonds having a stated rate of 6%

annually. The bonds mature in 10 years and interest is paid semiannually. The

market rate is 8% annually.

On May 1, 2001, Harrah’s issues $1,000,000 in bonds having a stated rate of 6%

annually. The bonds mature in 10 years and interest is paid semiannually. The

market rate is 8% annually.

Compute the issue price of Harrah’s bonds.

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

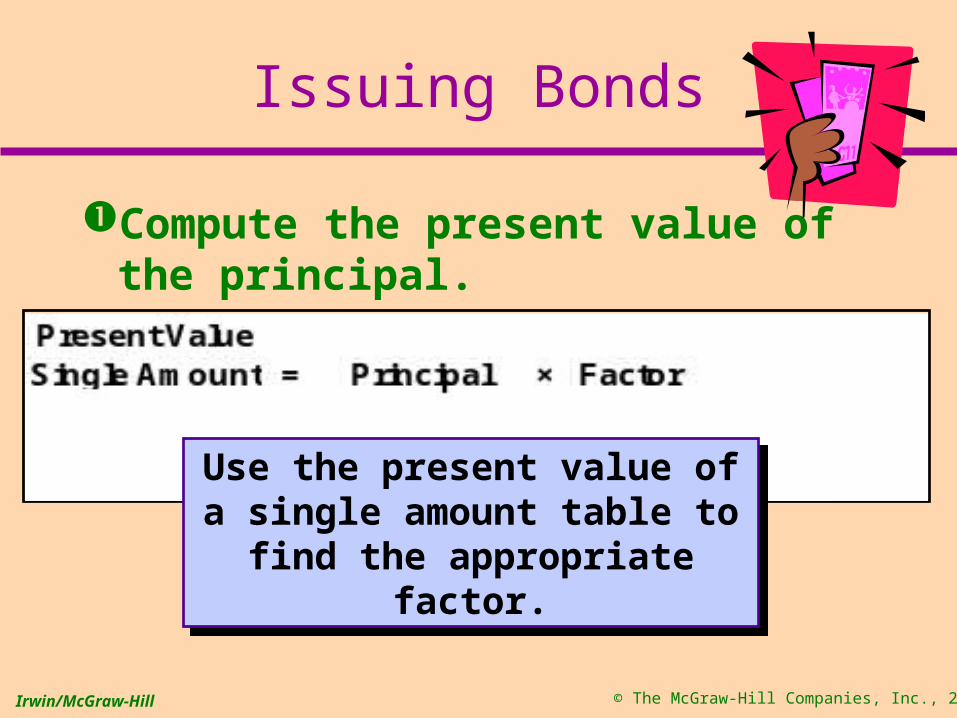

Issuing Bonds

Compute the present value of the principal.

Use the present value of a single amount table to find the

appropriate factor.

Use the present value of a single amount table to find the

appropriate factor.

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Issuing Bonds

Compute the present value of the principal.

Use the market rate of 8% to determine present value. Interest is

paid semiannually, so the rate is i=4% (8% ÷ 2 interest periods per year).

Use the market rate of 8% to determine present value. Interest is

paid semiannually, so the rate is i=4% (8% ÷ 2 interest periods per year).

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

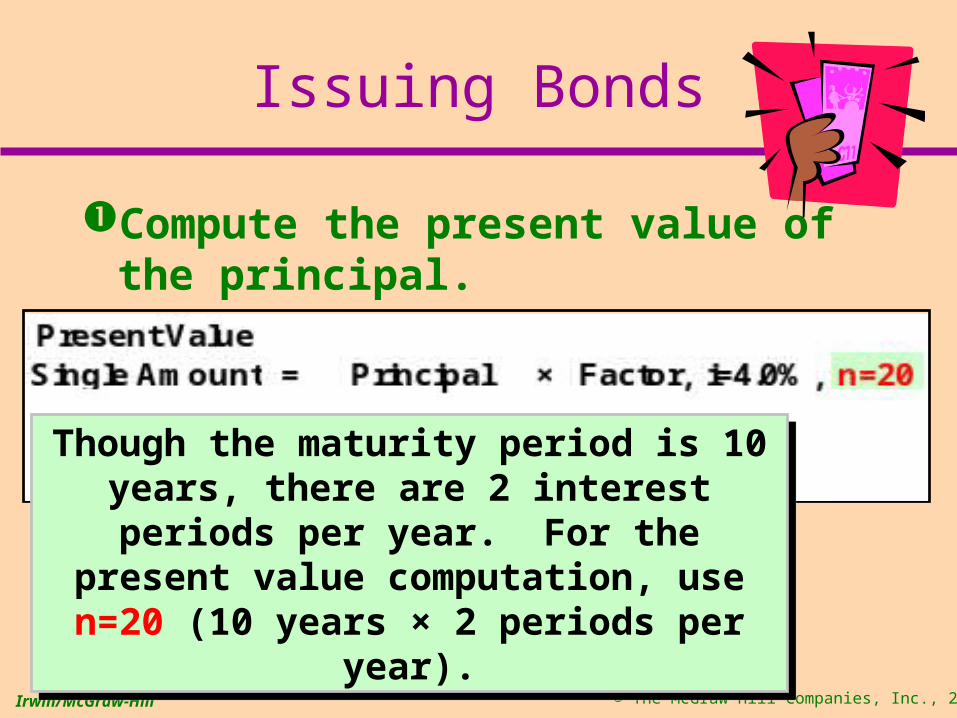

Issuing Bonds

Compute the present value of the principal.

Though the maturity period is 10 years, there are 2 interest periods per year. For the present value computation, use n=20

(10 years × 2 periods per year).

Though the maturity period is 10 years, there are 2 interest periods per year. For the present value computation, use n=20

(10 years × 2 periods per year).

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

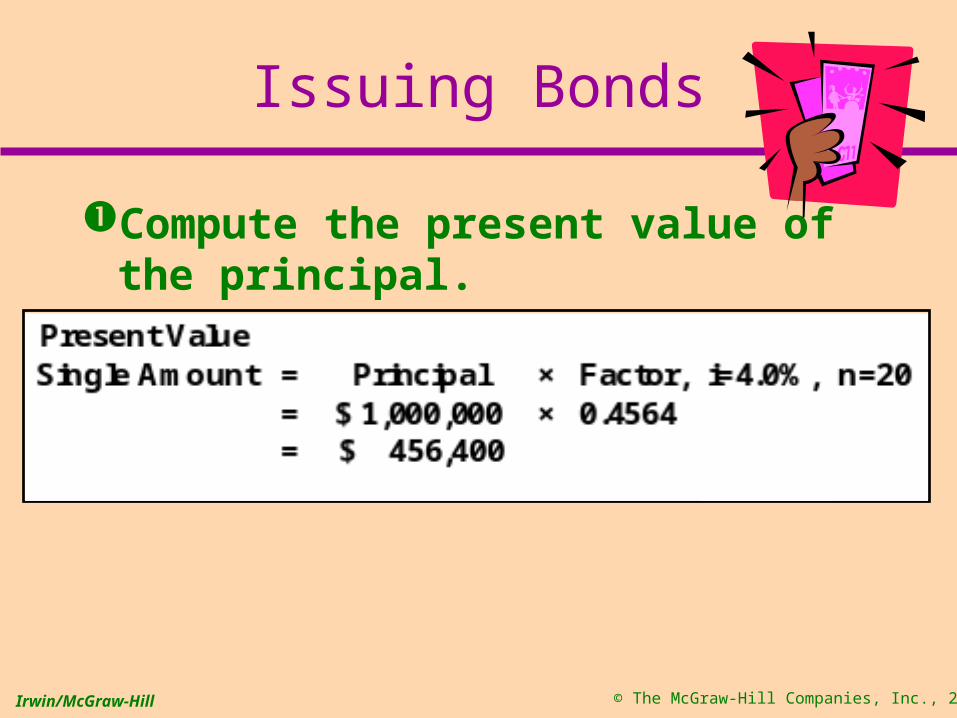

Issuing Bonds

Compute the present value of the principal.

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Issuing Bonds

Compute the present value of the interest payments.

The interest payment is computed as:

$1,000,000 × 6% × 6/12

= $30,000

The interest payment is computed as:

$1,000,000 × 6% × 6/12

= $30,000

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Issuing Bonds

Compute the present value of the interest payments.

Use the same i=4.0% and n=20 used for the present value of the principal,

but use the present value of an annuity table.

Use the same i=4.0% and n=20 used for the present value of the principal,

but use the present value of an annuity table.

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Issuing Bonds

Compute the present value of the interest payments.

Now, the issue price of the bonds can be computed.

Now, the issue price of the bonds can be computed.

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Issuing Bonds

Compute the issue price of the bonds.

456,400$ Present Value of the Principal

+ 407,709 Present Value of the Interest

= 864,109$ Present Value of the Bonds

456,400$ Present Value of the Principal

+ 407,709 Present Value of the Interest

= 864,109$ Present Value of the Bonds

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

456,400$ Present Value of the Principal

+ 407,709 Present Value of the Interest

= 864,109$ Present Value of the Bonds

456,400$ Present Value of the Principal

+ 407,709 Present Value of the Interest

= 864,109$ Present Value of the Bonds

Issuing Bonds

Compute the issue price of the bonds.

The $864,109 is less than the face amount of

$1,000,000, so the bonds are issued at a discount of

$135,891.

The $864,109 is less than the face amount of

$1,000,000, so the bonds are issued at a discount of

$135,891.

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Recording BondsIssued at a Discount

Prepare the journal entry to record the issuance of the bonds.

This is a contra-liability account and appears in the liability section of the balance sheet.

This is a contra-liability account and appears in the liability section of the balance sheet.

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Bonds Issued at a DiscountFinancial Statement Presentation

The discount The discount will be will be

amortizedamortized over the 10-over the 10-

year life of the year life of the bonds.bonds.

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Straight-Line Amortization of Bond Discount

Identify the amount of the bond discount.

Divide the bond discount by the number of interest periods.

Include the discount amortization amount as part of the periodic interest expense entry.

The discount will be reduced to zero by the maturity date.

Identify the amount of the bond discount.

Divide the bond discount by the number of interest periods.

Include the discount amortization amount as part of the periodic interest expense entry.

The discount will be reduced to zero by the maturity date.

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Straight-Line Amortization of Bond Discount

Harrah’s issued their bonds on May 1, 2001. The discount was $135,891. The bonds have a 10-year maturity

and $30,000 interest is paid semiannually.

Compute the periodic discount amortization using the straight-line method.

Harrah’s issued their bonds on May 1, 2001. The discount was $135,891. The bonds have a 10-year maturity

and $30,000 interest is paid semiannually.

Compute the periodic discount amortization using the straight-line method.

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Harrah’s issued their bonds on May 1, 2001. The discount was $135,891. The bonds have a 10-year maturity

and $30,000 interest is paid semiannually.

Compute the periodic discount amortization using the straight-line method.

Harrah’s issued their bonds on May 1, 2001. The discount was $135,891. The bonds have a 10-year maturity

and $30,000 interest is paid semiannually.

Compute the periodic discount amortization using the straight-line method.

Straight-Line Amortization of Bond Discount

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

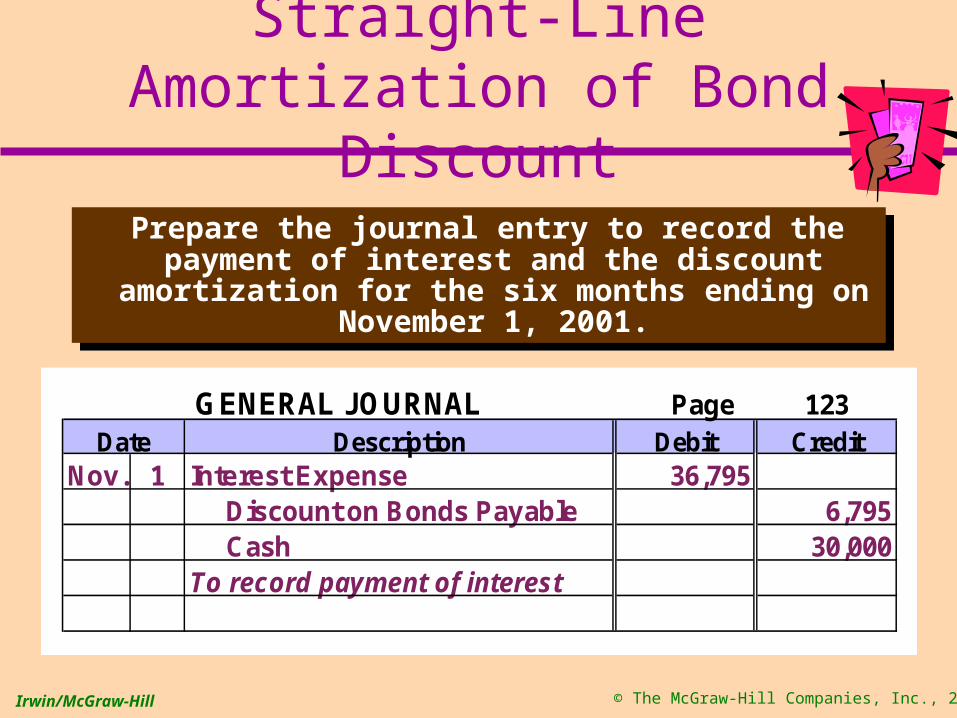

Straight-Line Amortization of Bond Discount

Prepare the journal entry to record the payment of interest and the discount amortization for the six months ending on November 1, 2001.

Prepare the journal entry to record the payment of interest and the discount amortization for the six months ending on November 1, 2001.

GENERAL JOURNAL Page 123Date Description Debit Credit

Nov. 1 Interest Expense 36,795 Discount on Bonds Payable 6,795 Cash 30,000To record payment of interest

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Bonds Issued at a DiscountFinancial Statement Presentation

As the discount is

amortized, the carrying

amount of the bonds

increases.

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Zero Coupon Bonds

• Zero coupon bonds do not pay periodic interest.

• Because there is no interest annuity . . .

• This is called a deep discount bonddeep discount bond.• Discount is amortized using

straight line method

PV of the Principal = Issue Price of the BondsPV of the Principal = Issue Price of the Bonds

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

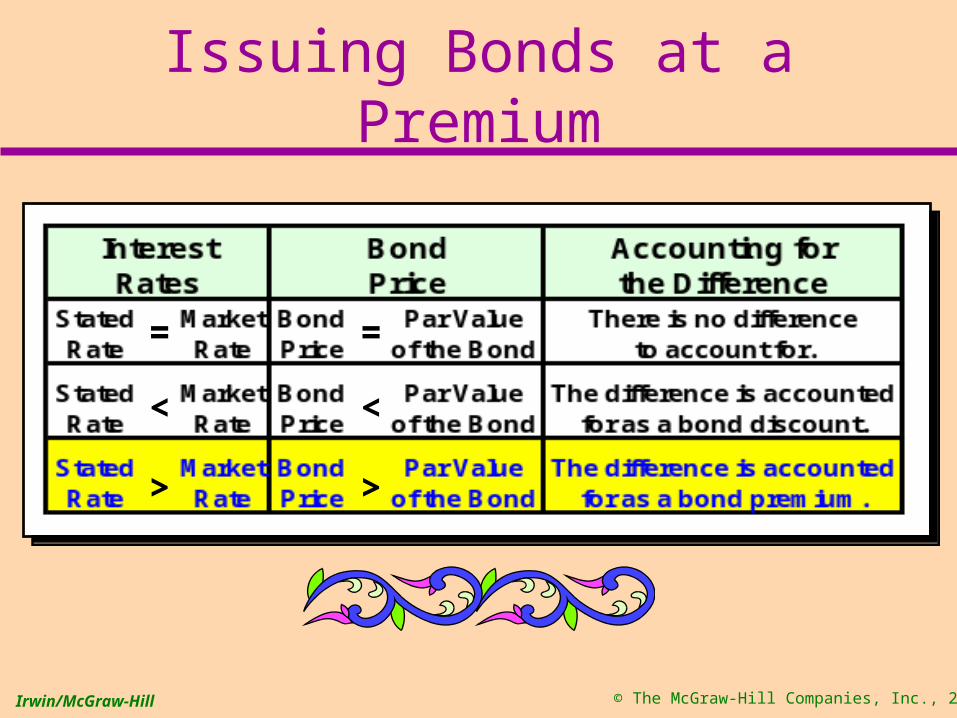

Issuing Bonds at a Premium

=

>

<

>

<

=

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Issuing Bonds at a Premium

On May 1, 2001, Harrah’s issues $1,000,000 in bonds having a stated rate of 10% annually. The bonds mature in 10 years and interest is

paid semiannually. The market rate is 8% annually.

On May 1, 2001, Harrah’s issues $1,000,000 in bonds having a stated rate of 10% annually. The bonds mature in 10 years and interest is

paid semiannually. The market rate is 8% annually.

Are Harrah’s bonds issued at par, at a discount, or at a premium?

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

On May 1, 2001, Harrah’s issues $1,000,000 in bonds having a stated rate of 10% annually. The bonds mature in 10 years and interest is

paid semiannually. The market rate is 8% annually.

On May 1, 2001, Harrah’s issues $1,000,000 in bonds having a stated rate of 10% annually. The bonds mature in 10 years and interest is

paid semiannually. The market rate is 8% annually.

Issuing Bonds at a Premium

> >

Let’s compute the issue price of the bonds.

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

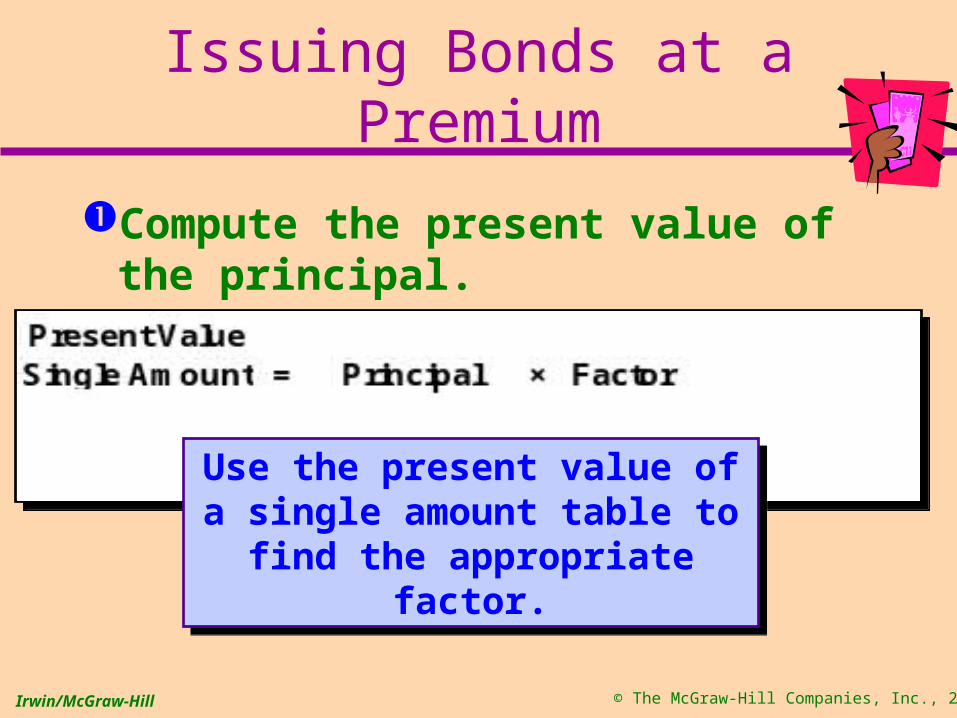

Issuing Bonds at a Premium

Compute the present value of the principal.

Use the present value of a single amount table to find the

appropriate factor.

Use the present value of a single amount table to find the

appropriate factor.

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

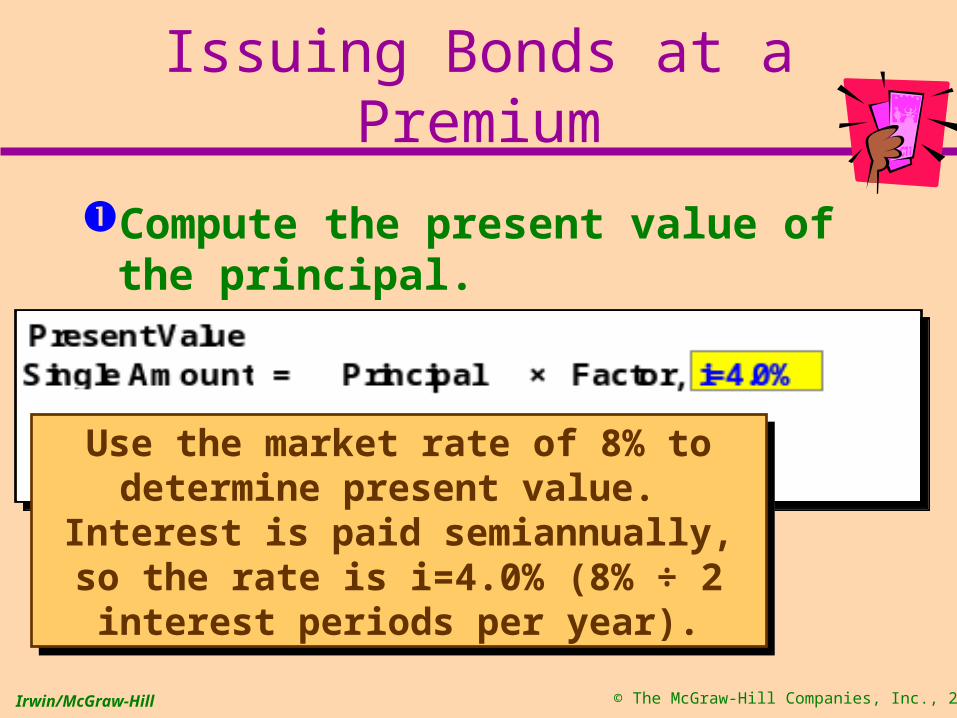

Issuing Bonds at a Premium

Compute the present value of the principal.

Use the market rate of 8% to determine present value. Interest is paid

semiannually, so the rate is i=4.0% (8% ÷ 2 interest periods per year).

Use the market rate of 8% to determine present value. Interest is paid

semiannually, so the rate is i=4.0% (8% ÷ 2 interest periods per year).

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Issuing Bonds at a Premium

Compute the present value of the principal.

The maturity period is 10 years, there are 2 interest periods per year. For the present value computation, use n=20

(10 years × 2 periods).

The maturity period is 10 years, there are 2 interest periods per year. For the present value computation, use n=20

(10 years × 2 periods).

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Issuing Bonds at a Premium

Compute the present value of the principal.

Next, we compute the present value of the interest payments.

Next, we compute the present value of the interest payments.

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Issuing Bonds at a Premium

Compute the present value of the interest payments.

The interest payment is computed as:

$1,000,000 × 10% × 6/12

= $50,000

The interest payment is computed as:

$1,000,000 × 10% × 6/12

= $50,000

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Issuing Bonds at a Premium

Compute the present value of the interest payments.

Use the same i=4.0% and n=20 that were used to compute the present

value of the principal. Now, however, the factor comes from the present value of an annuity table.

Use the same i=4.0% and n=20 that were used to compute the present

value of the principal. Now, however, the factor comes from the present value of an annuity table.

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Issuing Bonds at a Premium

Compute the present value of the interest payments.

Now, the issue price of the bonds can be computed.

Now, the issue price of the bonds can be computed.

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

456,400$ Present Value of the Principal

+ 679,515 Present Value of the Interest

= 1,135,915$ Present Value of the Bonds

456,400$ Present Value of the Principal

+ 679,515 Present Value of the Interest

= 1,135,915$ Present Value of the Bonds

Issuing Bonds at a Premium

Compute the issue price of the bonds.

The $1,135,915 is greater than the face amount of $1,000,000, so the bonds are issued at a premium of

$135,915.

The $1,135,915 is greater than the face amount of $1,000,000, so the bonds are issued at a premium of

$135,915.

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

GENERAL JOURNAL Page 97Date Description Debit Credit

May 1 Cash 1,135,915 Bonds Payable 1,000,000 Premium on Bonds Payable 135,915

Issuing Bonds at a Premium

Prepare the journal entry to record the issuance of the bonds.

This is called an adjunct account and appears in the liability section.

This is called an adjunct account and appears in the liability section.

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

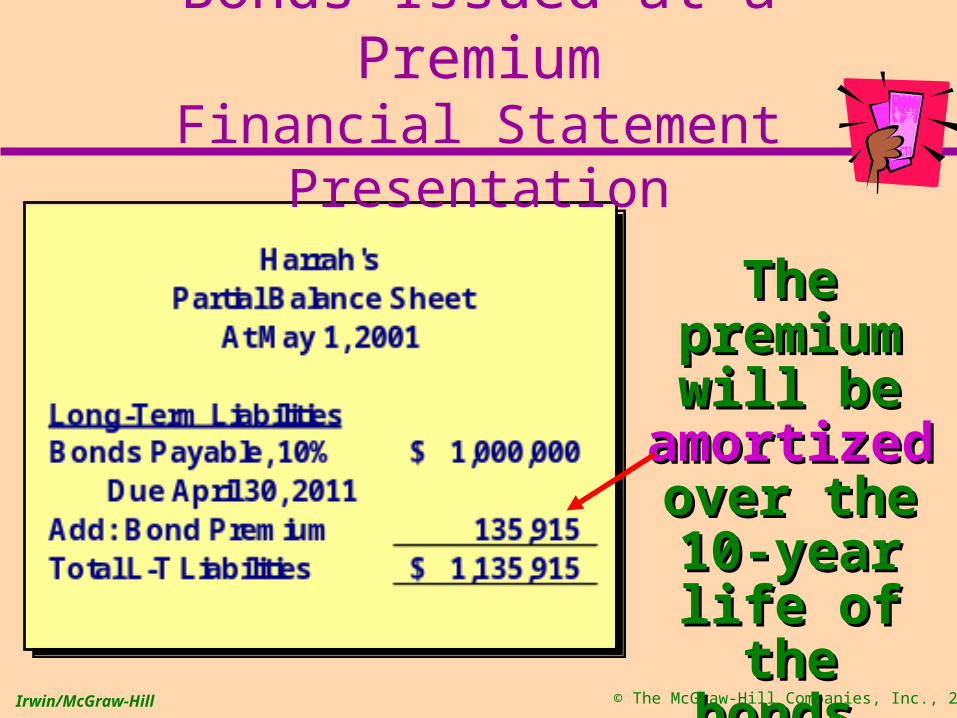

Bonds Issued at a PremiumFinancial Statement Presentation

The The premium premium

will be will be amortizedamortized

over the 10-over the 10-year life of year life of the bonds.the bonds.

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Recording Interest Expense

Amortization of Bond Preemium:

$135,915 / 20 = $6,795.75

Recording Interest Expense:

Bond Interest Expense $43,204

Premium on Bonds 6,796

Cash 50,000

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

End of Chapter 10