© the mcgraw-hill companies, inc., 2005 mcgraw-hill/irwin chapter 6 reporting and analyzing cash...

TRANSCRIPT

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

Chapter 6Chapter 6

Reporting and Analyzing Cash and Internal Controls

6-1

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-2

Purpose of Internal ControlPurpose of Internal Control

Policies and procedures Policies and procedures managers use to . .managers use to . . . .

Protect assets.Protect assets. Ensure reliable Ensure reliable

accounting. accounting. Promote efficient Promote efficient

operations. operations. Urge adherence to Urge adherence to

company policies. company policies.

Policies and procedures Policies and procedures managers use to . .managers use to . . . .

Protect assets.Protect assets. Ensure reliable Ensure reliable

accounting. accounting. Promote efficient Promote efficient

operations. operations. Urge adherence to Urge adherence to

company policies. company policies.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-3

Principles of Internal ControlPrinciples of Internal Control

Establish responsibilities.Establish responsibilities.

Maintain adequate records.Maintain adequate records.

Insure assets and bond key employees.Insure assets and bond key employees.

Separate recordkeeping from custodySeparate recordkeeping from custodyof assets.of assets.

Divide responsibility for related Divide responsibility for related transactions.transactions.

Apply technological controls.Apply technological controls.

Perform regular and independent Perform regular and independent reviews.reviews.

Establish responsibilities.Establish responsibilities.

Maintain adequate records.Maintain adequate records.

Insure assets and bond key employees.Insure assets and bond key employees.

Separate recordkeeping from custodySeparate recordkeeping from custodyof assets.of assets.

Divide responsibility for related Divide responsibility for related transactions.transactions.

Apply technological controls.Apply technological controls.

Perform regular and independent Perform regular and independent reviews.reviews.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-4

Technology and Internal ControlTechnology and Internal Control

ReducedProcessing

Errors

ReducedProcessing

Errors

MoreExtensive Testing

of Records

MoreExtensive Testing

of Records

LimitedEvidence ofProcessing

LimitedEvidence ofProcessing

CrucialSeparation of

Duties

CrucialSeparation of

Duties

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-5

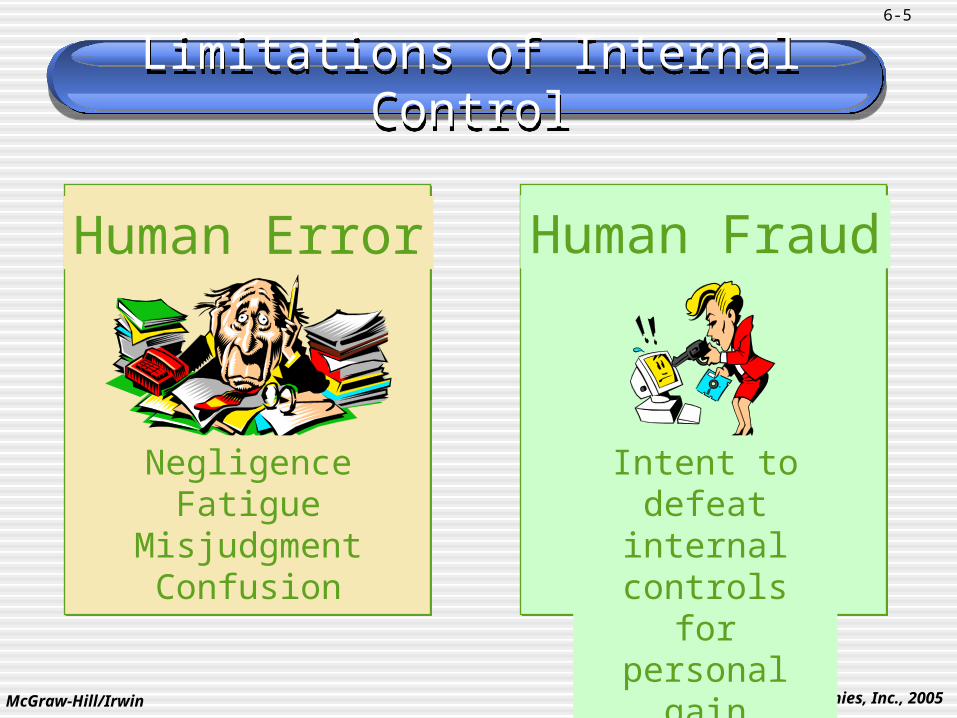

Limitations of Internal ControlLimitations of Internal Control

Human Error

NegligenceFatigue

MisjudgmentConfusion

Human Fraud

Intent todefeat internal

controls forpersonal gain

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-6

Limitations of Internal ControlLimitations of Internal Control

The costs of internal controls must not exceed their benefits.The costs of internal controls must not exceed their benefits.

CostsBenefits

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-7

Control of CashControl of Cash

An effective system of internal control that protects cash and cash equivalents should meet

three basic guidelines:

An effective system of internal control that protects cash and cash equivalents should meet

three basic guidelines:

Handling cash is separated from

recordkeeping of cash.

Handling cash is separated from

recordkeeping of cash.

Cash receipts are promptly deposited

in a bank.

Cash receipts are promptly deposited

in a bank.

Cash disbursements are made by check.Cash disbursements are made by check.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-8

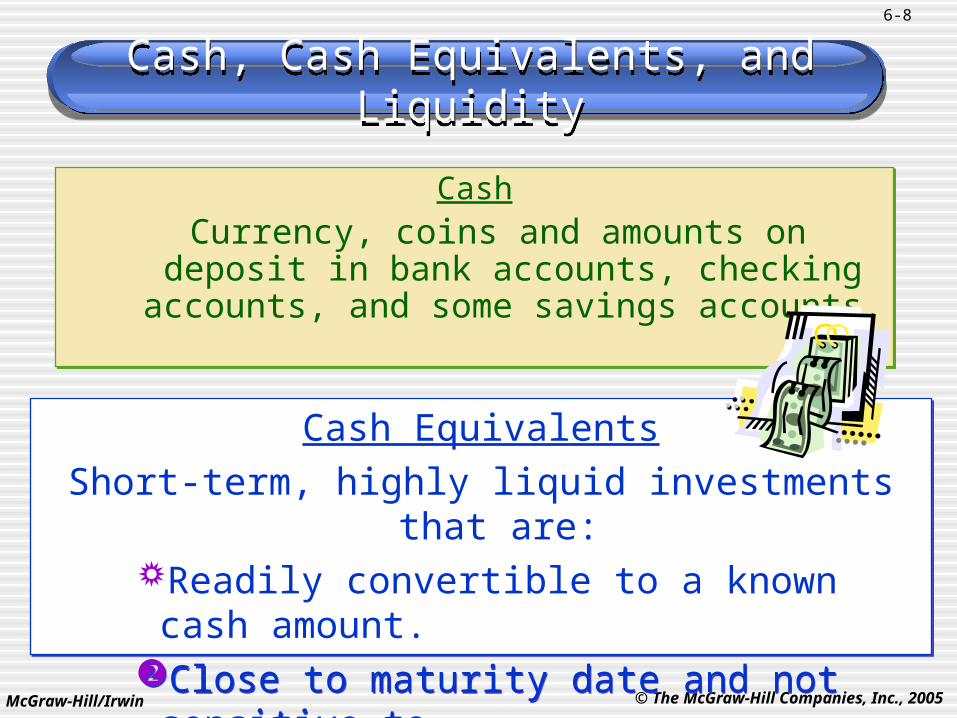

Cash, Cash Equivalents, and LiquidityCash, Cash Equivalents, and Liquidity

Cash

Currency, coins and amounts on deposit in bank accounts, checking accounts, and some

savings accounts.

Cash

Currency, coins and amounts on deposit in bank accounts, checking accounts, and some

savings accounts.

Cash Equivalents

Short-term, highly liquid investments that are:Readily convertible to a known cash amount.Close to maturity date and not sensitive to

interest rate changes.

Cash Equivalents

Short-term, highly liquid investments that are:Readily convertible to a known cash amount.Close to maturity date and not sensitive to

interest rate changes.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-9

Cash, Cash Equivalents, and LiquidityCash, Cash Equivalents, and Liquidity

Liquidity

How easily an asset can be converted into another asset or be used in paying for services

or obligations.

Liquidity

How easily an asset can be converted into another asset or be used in paying for services

or obligations.

InventoryInventory CashCash

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-10

Control of Cash ReceiptsControl of Cash Receipts

Over-the-Counter Cash Receipts

• Cash register with locked-in record of transactions.

• Compare cash register record with cash reported.

Over-the-Counter Cash Receipts

• Cash register with locked-in record of transactions.

• Compare cash register record with cash reported.

Cash Receipts By Mail

• Two people open the mail.Money to cashier’s

office.List to accounting dept.Copy of list filed.

Cash Receipts By Mail

• Two people open the mail.Money to cashier’s

office.List to accounting dept.Copy of list filed.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-11

Control of Cash DisbursementsControl of Cash Disbursements

• All expenditures made by check. The only exception is for small payments from petty cash.

• Separate authorization, check signing and recordkeeping duties.

• Use a voucher system.

• All expenditures made by check. The only exception is for small payments from petty cash.

• Separate authorization, check signing and recordkeeping duties.

• Use a voucher system.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-12

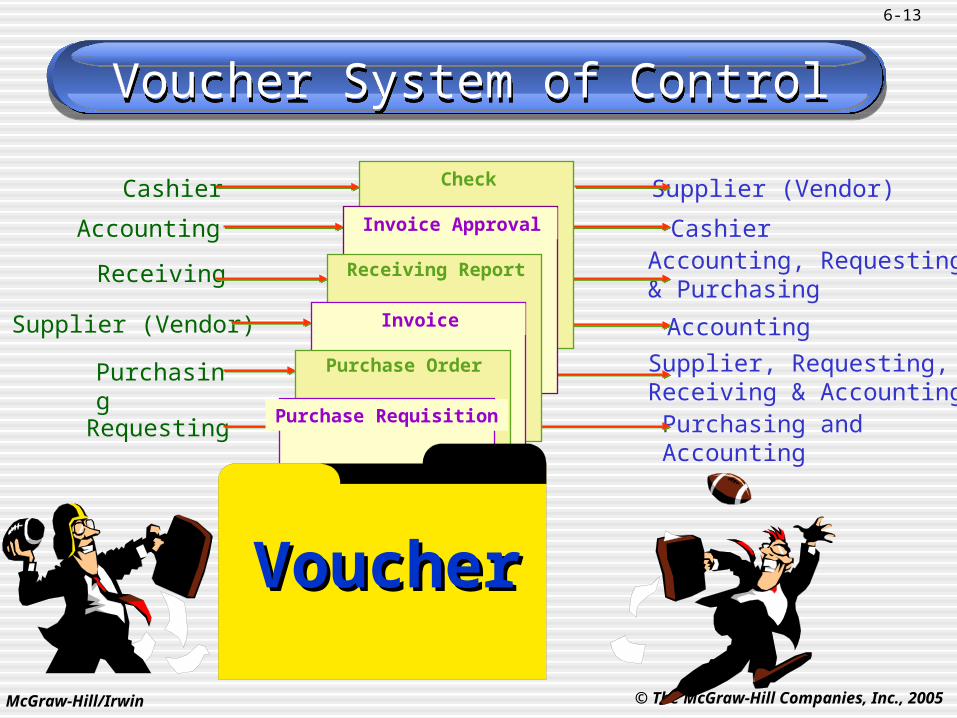

Voucher System of ControlVoucher System of Control

A voucher system establishes procedures for:

Verifying, approving and recording obligations for eventual cash disbursement.

Issuing checks for payment of verified, approved and recorded obligations.

A voucher system establishes procedures for:

Verifying, approving and recording obligations for eventual cash disbursement.

Issuing checks for payment of verified, approved and recorded obligations.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-13

Voucher System of ControlVoucher System of Control

Cashier

Accounting

Receiving

Supplier (Vendor)

Purchasing

Requesting

CashierAccounting, Requesting& Purchasing

Accounting

Supplier (Vendor)

Purchasing andAccounting

Supplier, Requesting, Receiving & Accounting

Check

Invoice Approval

Receiving Report

Invoice

Purchase Order

Purchase Requisition

VoucherVoucher

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-14

Petty Cash System of ControlPetty Cash System of Control

Small payments required in most companies for items such as postage, courier fees, repairs

and supplies.

Small payments required in most companies for items such as postage, courier fees, repairs

and supplies.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-15

Petty Cash

Operating a Petty Cash FundOperating a Petty Cash Fund

CompanyCompanyCashierCashier

Petty Petty CashierCashier

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-16

Petty Cash

Operating a Petty Cash FundOperating a Petty Cash Fund

CompanyCompanyCashierCashier

Petty Petty CashierCashier

May 1 Petty cash 400 Cash 400

AccountantAccountant

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-17

Petty Cash

Operating a Petty Cash FundOperating a Petty Cash Fund

Petty Petty CashierCashier

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-18

37¢

Stamps$45

Courier$80

Operating a Petty Cash FundOperating a Petty Cash Fund

Petty Petty CashierCashier

A petty cash fund is used only for

business expenses.

A petty cash fund is used only for

business expenses.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-19

Operating a Petty Cash FundOperating a Petty Cash Fund

Receipts

Petty cash receipts with

either no signature or a

forged signature usually indicate misuse of petty

cash.

Petty cash receipts with

either no signature or a

forged signature usually indicate misuse of petty

cash.

Petty Petty CashierCashier

37¢

Stamps$45

Courier$80

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-20

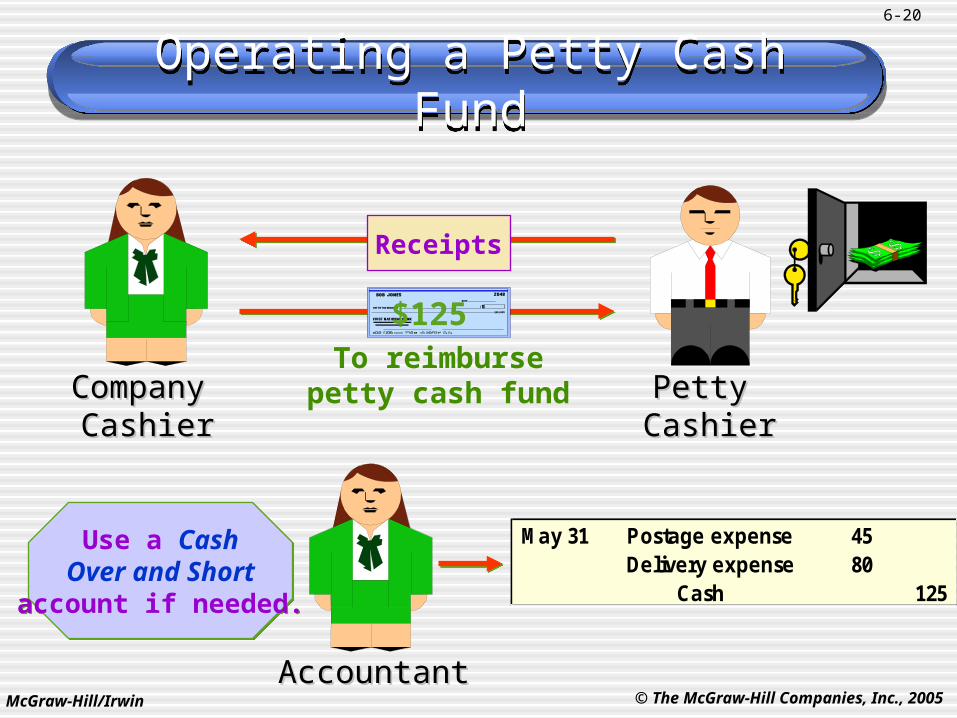

Receipts

Company Company CashierCashier

$125To reimburse

petty cash fund

Use a CashOver and Short

account if needed.

Use a CashOver and Short

account if needed.

Operating a Petty Cash FundOperating a Petty Cash Fund

Petty Petty CashierCashier

May 31 Postage expense 45 Delivery expense 80

Cash 125

AccountantAccountant

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-21

Petty Cash ExamplePetty Cash Example

Tension Co. maintains a petty cash fund of $400. The following summary information was taken

from petty cash vouchers for July:

Travel Expenses $79.30

Customer Business Lunches 93.42

Express Mail Postage 55.00

Miscellaneous Office Supplies 32.48

Let’s look at replenishing the fund if the balance on July 31 was $137.80.

Tension Co. maintains a petty cash fund of $400. The following summary information was taken

from petty cash vouchers for July:

Travel Expenses $79.30

Customer Business Lunches 93.42

Express Mail Postage 55.00

Miscellaneous Office Supplies 32.48

Let’s look at replenishing the fund if the balance on July 31 was $137.80.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-22

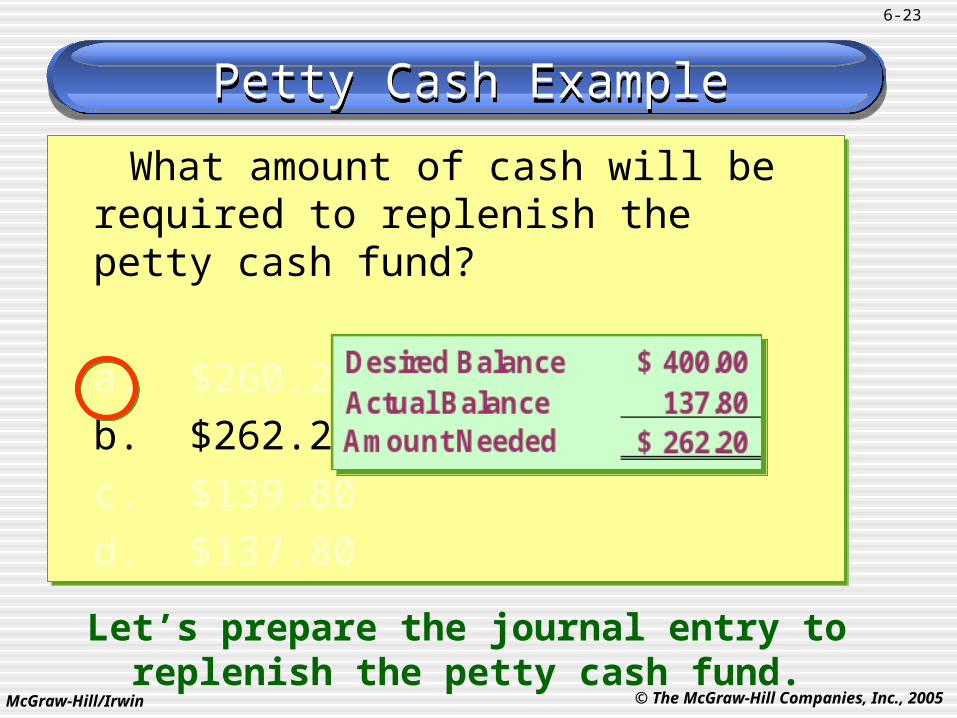

Petty Cash ExamplePetty Cash Example

What amount of cash will be required to replenish the petty cash fund?

a. $260.20

b. $262.20

c. $139.80

d. $137.80

What amount of cash will be required to replenish the petty cash fund?

a. $260.20

b. $262.20

c. $139.80

d. $137.80

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-23

Petty Cash ExamplePetty Cash Example

What amount of cash will be required to replenish the petty cash fund?

a. $260.20

b. $262.20

c. $139.80

d. $137.80

What amount of cash will be required to replenish the petty cash fund?

a. $260.20

b. $262.20

c. $139.80

d. $137.80

Let’s prepare the journal entry to replenish the petty cash fund.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-24

Petty Cash ExamplePetty Cash Example

Travel Expense 79.30

Entertainment Expense 93.42

Postage Expense 55.00

Office Supplies Expense 32.48

Cash Over and Short 2.00

Cash 262.20

July 31

Here is the journal entry to replenish the petty cash fund.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-25

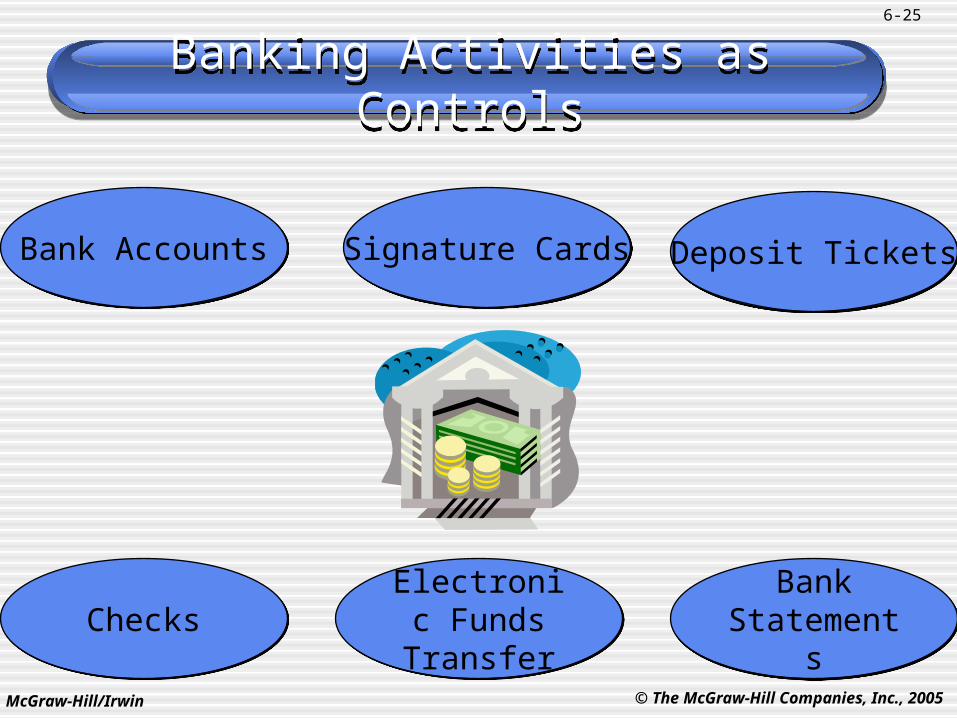

Banking Activities as ControlsBanking Activities as Controls

Bank AccountsBank Accounts Signature CardsSignature Cards Deposit TicketsDeposit Tickets

ChecksChecksElectronic

Funds Transfer

Electronic Funds

Transfer

Bank Statements

Bank Statements

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-26

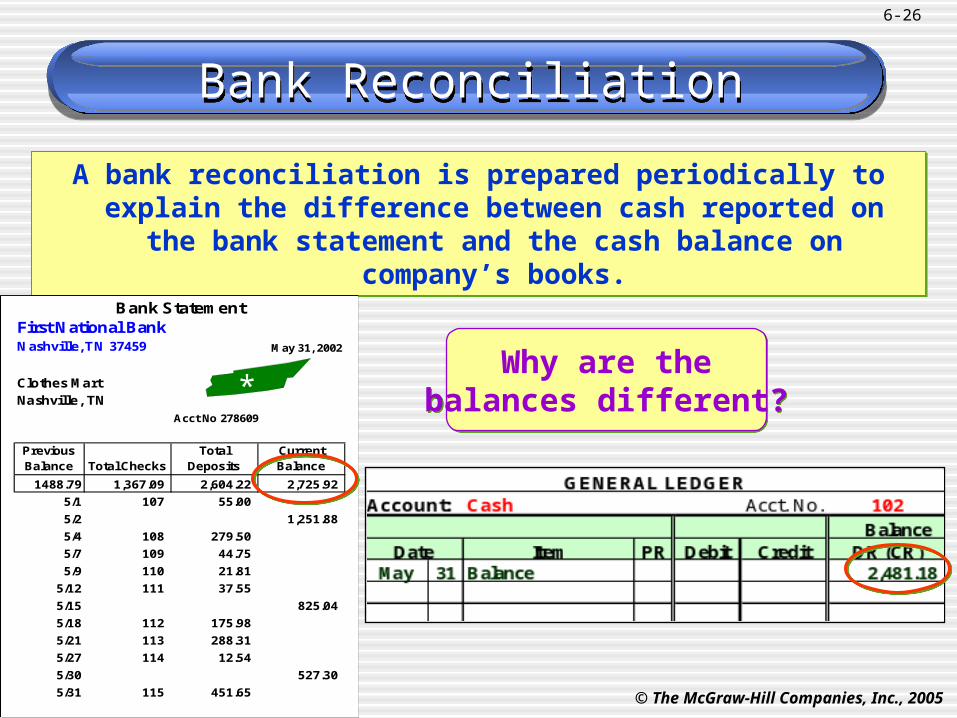

Bank ReconciliationBank Reconciliation

A bank reconciliation is prepared periodically to explain the difference between cash reported on the bank

statement and the cash balance on company’s books.

A bank reconciliation is prepared periodically to explain the difference between cash reported on the bank

statement and the cash balance on company’s books.

First National BankNashville, TN 37459 May 31, 2002

Clothes MartNashville, TN

Acct No 278609

Previous Balance Total Checks

Total Deposits

Current Balance

1488.79 1,367.09 2,604.22 2,725.92

5/1 107 55.00

5/2 1,251.88

5/4 108 279.50

5/7 109 44.75

5/9 110 21.81

5/12 111 37.55

5/15 825.04

5/18 112 175.98

5/21 113 288.31

5/27 114 12.54

5/30 527.30

5/31 115 451.65

Bank Statement

Why are thebalances different?

Why are thebalances different?*

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-27

Reconciling ItemsReconciling Items

Bank Statement Balance

Deduct: Outstanding checks.

Add: Deposits in transit.

Add or Deduct: Bank errors.

Bank Statement Balance

Deduct: Outstanding checks.

Add: Deposits in transit.

Add or Deduct: Bank errors.

Book Balance

Deduct: Nonsufficient funds check (NSF).

Deduct: Bank service charge.

Add: Interest earned on checking account.

Add: Collections made by the bank.

Add or Deduct: Book errors.

Book Balance

Deduct: Nonsufficient funds check (NSF).

Deduct: Bank service charge.

Add: Interest earned on checking account.

Add: Collections made by the bank.

Add or Deduct: Book errors.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-28

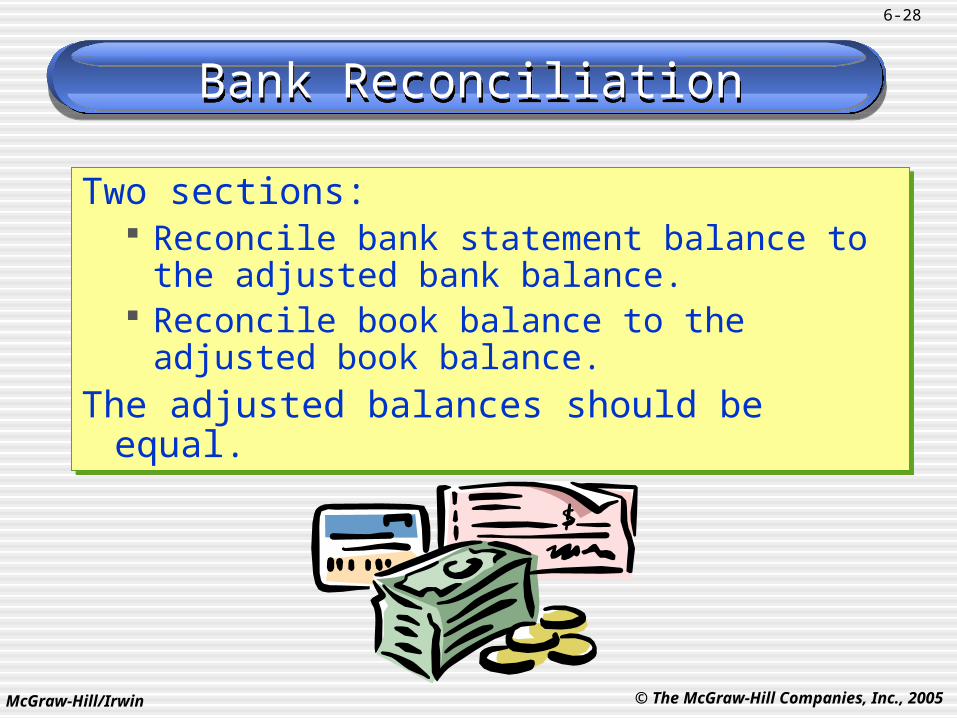

Bank ReconciliationBank Reconciliation

Two sections: Reconcile bank statement balance to the

adjusted bank balance. Reconcile book balance to the adjusted

book balance.

The adjusted balances should be equal.

Two sections: Reconcile bank statement balance to the

adjusted bank balance. Reconcile book balance to the adjusted

book balance.

The adjusted balances should be equal.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-29

Bank Reconciliation ExampleBank Reconciliation Example

Let’s prepare a July 31 bank reconciliation statement for the Simmons Company.

• The July 31 bank statement indicated a

balance of $9,610. • The cash general ledger account on that

date shows a balance of $7,430.

Additional information necessary for the reconciliation is shown on the next screen.

Let’s prepare a July 31 bank reconciliation statement for the Simmons Company.

• The July 31 bank statement indicated a

balance of $9,610. • The cash general ledger account on that

date shows a balance of $7,430.

Additional information necessary for the reconciliation is shown on the next screen.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-30

Bank Reconciliation ExampleBank Reconciliation Example

Outstanding checks totaled $2,417.

A $500 check mailed to the bank for deposit had not reached the bank at the statement date.

The bank returned a customer’s NSF check for $225 received as payment on account receivable.

The bank statement showed $30 interest earned during July.

Check No. 781 for supplies expense cleared the bank for $268 but was erroneously recorded in our books as $240.

A $486 deposit by Acme Company was erroneously credited to our account by the bank.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-32

July 31 Cash 30 Interest revenue 30

July 31 Supplies expense 28 Accounts receivable 225

Cash 253

Recording Adjusting Entries from a Bank Reconciliation

Recording Adjusting Entries from a Bank Reconciliation

Only amounts shown on the book portion of the reconciliation require an adjusting entry.

Only amounts shown on the book portion of the reconciliation require an adjusting entry.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-33

Recording Adjusting Entries from a Bank Reconciliation

Recording Adjusting Entries from a Bank Reconciliation

After posting the reconciling entries the cash account looks like this . . .

After posting the reconciling entries the cash account looks like this . . .

Adjusted balance on July 31.Adjusted balance on July 31.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-34

Days’ Sales UncollectedDays’ Sales Uncollected

Days’Sales

Uncollected

Accounts Receivable Net Sales

× 365=

How much time is likely to pass beforewe receive cash receipts from credit sales.

How much time is likely to pass beforewe receive cash receipts from credit sales.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

6-35

End of Chapter 6End of Chapter 6