1 ceist limited school finances – challenging times october 2009

Post on 19-Dec-2015

214 views

TRANSCRIPT

11

CEISTCEIST Limited Limited School Finances – School Finances – Challenging TimesChallenging Times

October 2009

22

Welcome!Welcome!

Welcome to everyone and thank you for Welcome to everyone and thank you for being here today.being here today.

IntroductionIntroduction

Mike Higgins, Director of Finance, Mike Higgins, Director of Finance, CEISTCEIST Limited. Limited.

Bernadette McKeown, Accountant, Bernadette McKeown, Accountant, CEISTCEIST Limited. Limited.

33

School Finances - Challenging Times

44

Current SituationCurrent Situation

D.E.S. Grant Cutbacks.D.E.S. Grant Cutbacks.

Current Economic Climate.Current Economic Climate.

Reduction in Household Income.Reduction in Household Income.

Disadvantaged Schools – Non-DEIS.Disadvantaged Schools – Non-DEIS.

Smaller Schools.Smaller Schools.

55

School Finances – Challenging TimesSchool Finances – Challenging Times

SchoolSchool

IncomeIncome

66

School IncomeSchool Income

There are 3 Main Areas of There are 3 Main Areas of

School IncomeSchool Income::

1.1. D.E.S.D.E.S.

2.2. School Generated Income School Generated Income

3.3. Other IncomeOther Income

77

School IncomeSchool Income

D.E.S. Grants are fixedD.E.S. Grants are fixed

The options remaining are:The options remaining are:

(a) Maximise School Generated Income(a) Maximise School Generated Income

and/or and/or

(b) Maximise Other Income(b) Maximise Other Income

88

School Income contd.School Income contd.The Main Areas of The Main Areas of School Generated IncomeSchool Generated Income that that

can be maximised:can be maximised:

Bus IncomeBus Income Charges for PhotocopyingCharges for Photocopying T.Y. to T.Y. to cover all T.Y. costscover all T.Y. costs School Tours must always be School Tours must always be self-financingself-financing School canteens, tuck shops, book shops, uniform School canteens, tuck shops, book shops, uniform

sales sales must always be at least break-evenmust always be at least break-even Rental of School Premises – potentially a major Rental of School Premises – potentially a major

source of income (source of income (caution on insurancecaution on insurance).).

99

School Income contd.School Income contd.

The Main Areas of The Main Areas of Other IncomeOther Income that can be that can be maximised:maximised:

Voluntary Subscriptions / Income from ParentsVoluntary Subscriptions / Income from Parents

FundraisingFundraising

Donations – all Donations – all CEISTCEIST schools have charitable schools have charitable status. Tax reclaimable on donations > €250 per status. Tax reclaimable on donations > €250 per annum (hope to have this reduced to > €100 p.a.)annum (hope to have this reduced to > €100 p.a.)

Collecting money from any of these Collecting money from any of these sources is becoming increasingly difficult sources is becoming increasingly difficult in the current economic climatein the current economic climate

1010

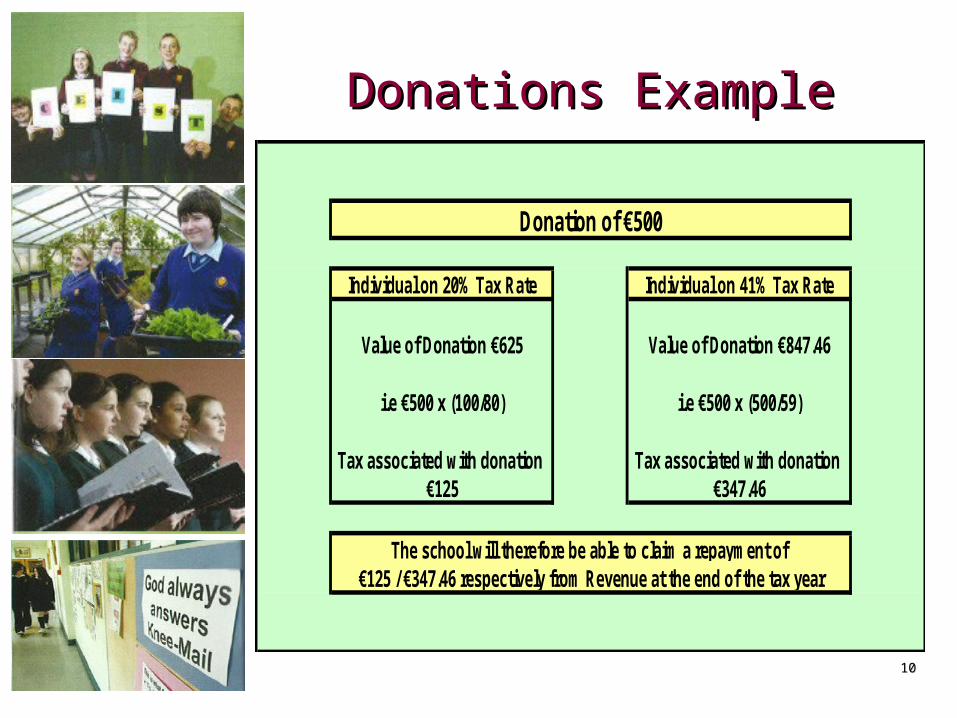

Donations ExampleDonations Example

€125 / €347.46 respectively from Revenue at the end of the tax yearThe school will therefore be able to claim a repayment of

Donation of €500

Individual on 41% Tax RateIndividual on 20% Tax Rate

Value of Donation €625

i.e €500 x (100/80)

Tax associated with donation €125

Value of Donation €847.46

i.e €500 x (500/59)

Tax associated with donation €347.46

1111

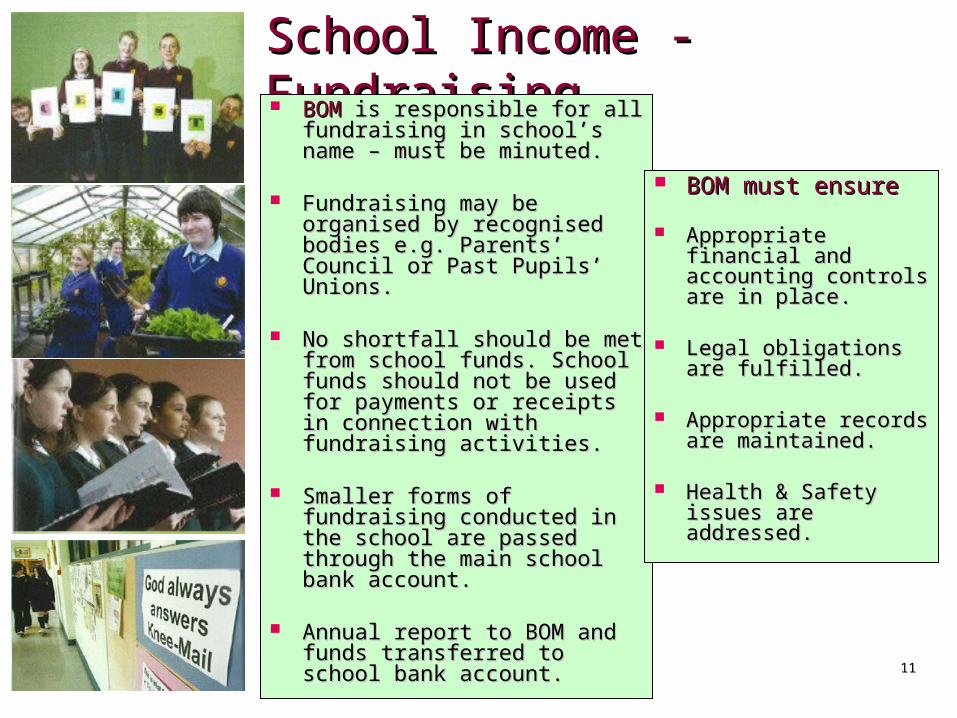

School Income - FundraisingSchool Income - Fundraising BOMBOM is responsible for all is responsible for all

fundraising in school’s name – fundraising in school’s name – must be minuted.must be minuted.

Fundraising may be organised Fundraising may be organised by recognised bodies e.g. by recognised bodies e.g. Parents’ Council or Past Pupils’ Parents’ Council or Past Pupils’ Unions.Unions.

No shortfall should be met from No shortfall should be met from school funds. School funds school funds. School funds should not be used for should not be used for payments or receipts in payments or receipts in connection with fundraising connection with fundraising activities.activities.

Smaller forms of fundraising Smaller forms of fundraising conducted in the school are conducted in the school are passed through the main passed through the main school bank account.school bank account.

Annual report to BOM and Annual report to BOM and funds transferred to school funds transferred to school bank account.bank account.

BOM must ensureBOM must ensure

Appropriate financial Appropriate financial and accounting and accounting controls are in placecontrols are in place..

Legal obligations are Legal obligations are fulfilled.fulfilled.

Appropriate records Appropriate records are maintained.are maintained.

Health & Safety Health & Safety issues are addressedissues are addressed..

1212

School Finances – Challenging TimesSchool Finances – Challenging Times

School School ExpenditureExpenditure

1313

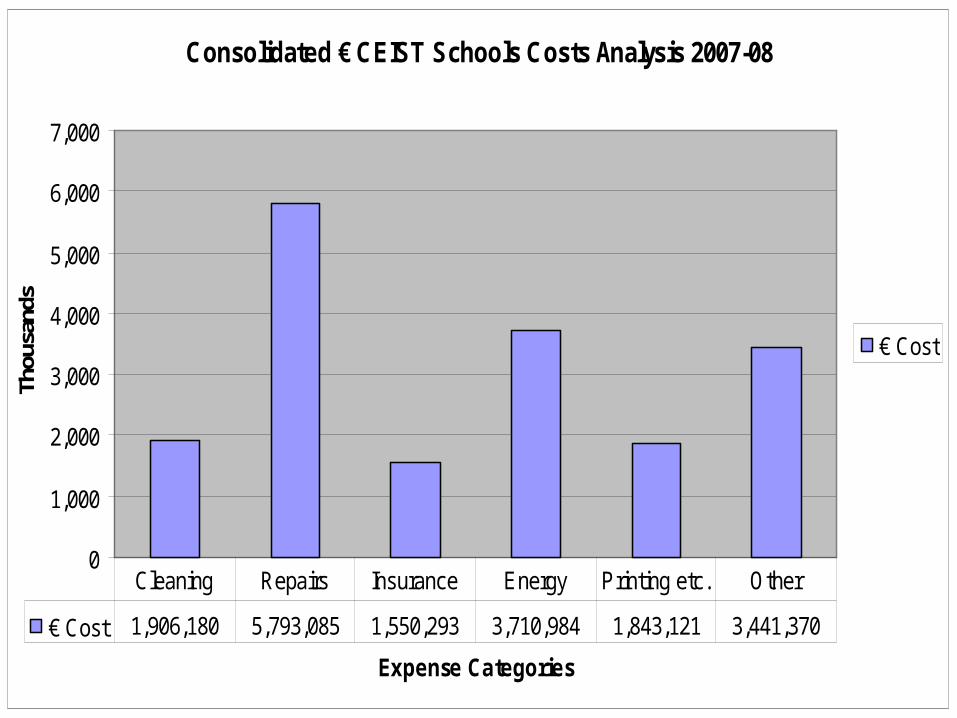

Consolidated € CEIST Schools Costs Analysis 2007-08

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Thou

sand

s

Expense Categories

€ Cost

€ Cost 1,906,180 5,793,085 1,550,293 3,710,984 1,843,121 3,441,370

Cleaning Repairs Insurance Energy Printing etc. Other

1414

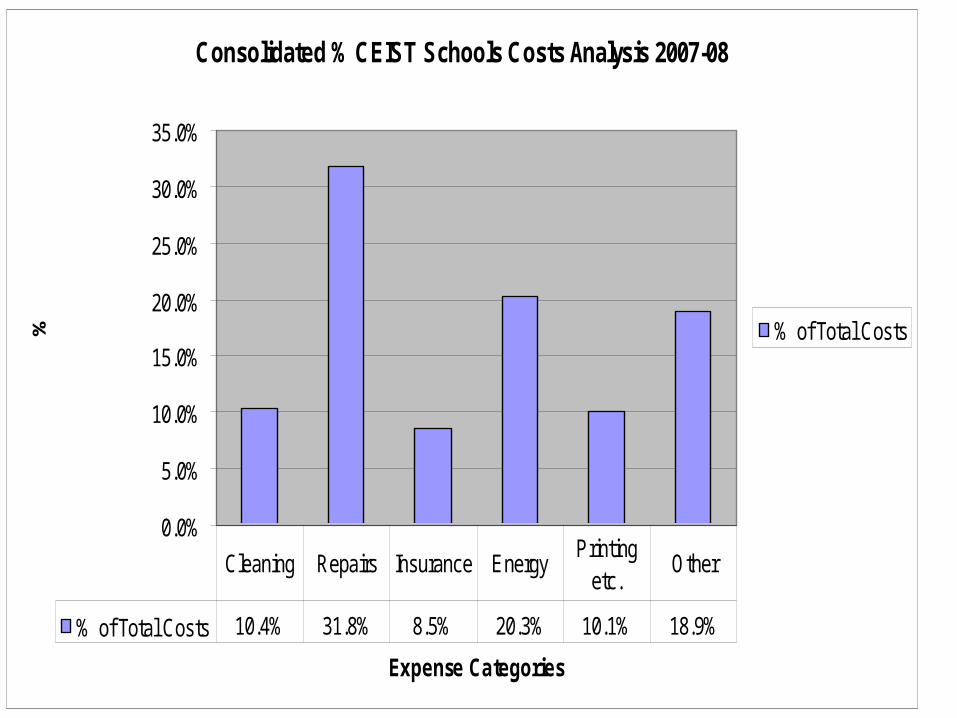

Consolidated % CEIST Schools Costs Analysis 2007-08

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

Expense Categories

% % of Total Costs

% of Total Costs 10.4% 31.8% 8.5% 20.3% 10.1% 18.9%

Cleaning Repairs Insurance Energy Printing

etc.Other

1515

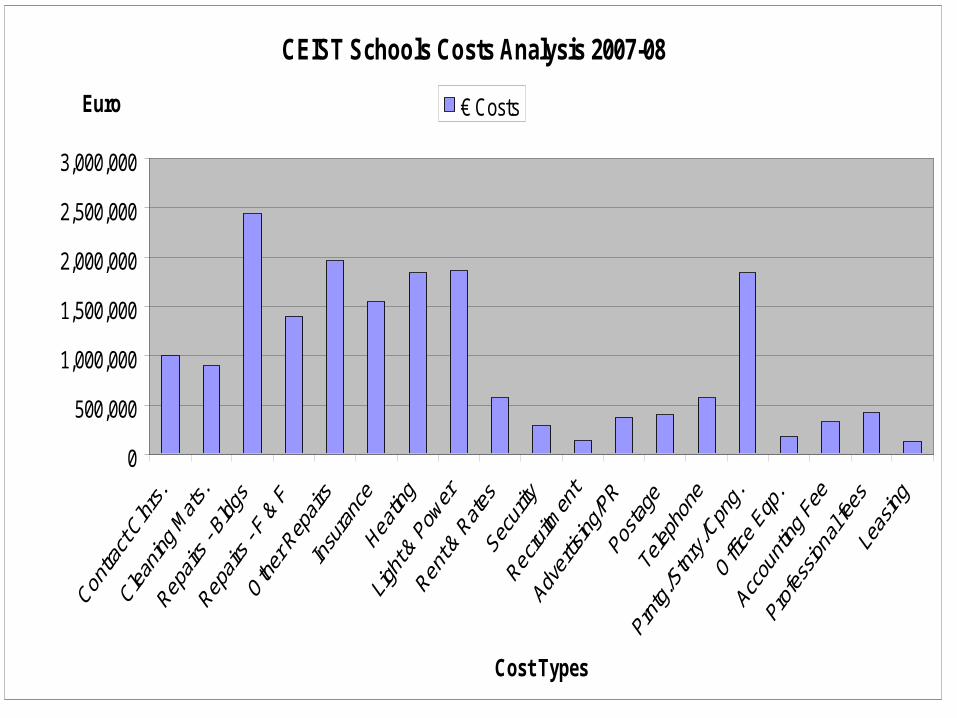

School Expenditure School Expenditure CEIST Schools Costs Analysis 2007-08

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

Cost Types

Euro € Costs

1616

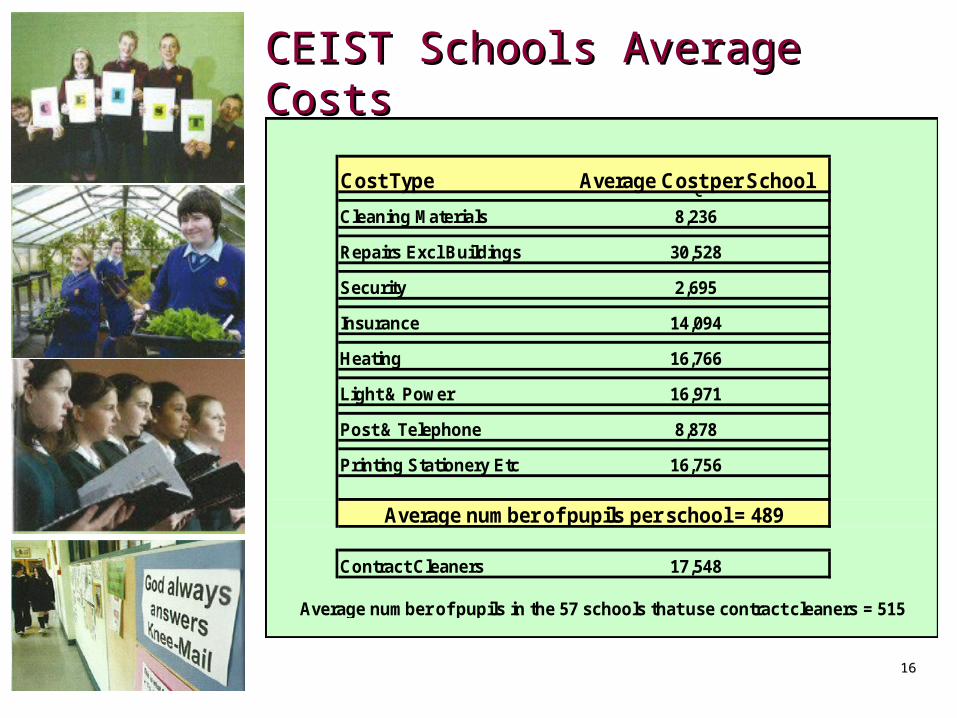

CEIST Schools Average CostsCEIST Schools Average Costs

Cost Type Average Cost per School €

Cleaning Materials 8,236

Repairs Excl Buildings 30,528

Security 2,695

Insurance 14,094

Heating 16,766

Light & Power 16,971

Post & Telephone 8,878

Printing Stationery Etc 16,756

Contract Cleaners 17,548

Average number of pupils per school = 489

Average number of pupils in the 57 schools that use contract cleaners = 515

1717

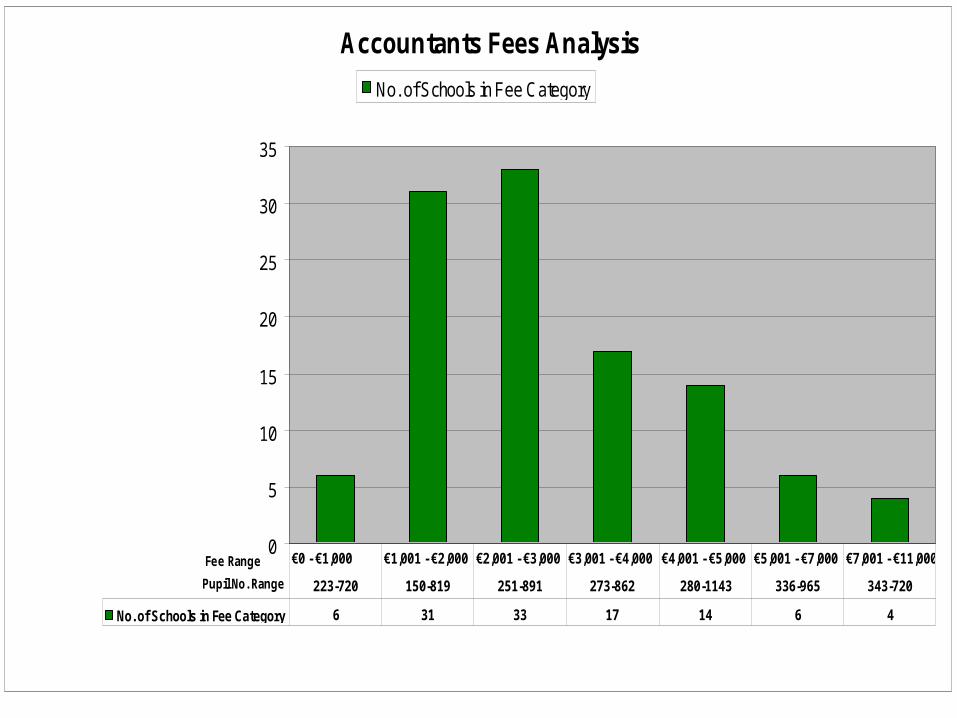

Accountant’s FeesAccountant’s FeesAccountants Fees Analysis

0

5

10

15

20

25

30

35

Fee Range

Pupil No. Range

No. of Schools in Fee Category

No. of Schools in Fee Category 6 31 33 17 14 6 4

€0 - €1,000 €1,001 - €2,000 €2,001 - €3,000 €3,001 - €4,000 €4,001 - €5,000 €5,001 - €7,000 €7,001 - €11,000

223-720 150-819 251-891 273-862 280-1143 336-965 343-720

1818

School Income contd.School Income contd.

Rigorous Control is required inRigorous Control is required in - -

Salaries & WagesSalaries & Wages Secretaries, Caretakers, Supervisors, Games Coaches Secretaries, Caretakers, Supervisors, Games Coaches Please Contact JMB/FSSU for Current Salary ScalesPlease Contact JMB/FSSU for Current Salary Scales

Part-time Teaching HoursPart-time Teaching HoursAvoid at all costs!Avoid at all costs!

Repairs & MaintenanceRepairs & MaintenanceCaretaking, Cleaning, Repairs, EnergyCaretaking, Cleaning, Repairs, Energy

Administration CostsAdministration CostsPostage, Telephone, Photocopying, Advertising/PRPostage, Telephone, Photocopying, Advertising/PR

1919

Initiative underway by TrusteesInitiative underway by Trustees

The Trustees have carried out a pilot study of 10 The Trustees have carried out a pilot study of 10 schools on certain cost areas that could be schools on certain cost areas that could be managed through a facility management function:managed through a facility management function:

Utility Installations Utility Installations (ESB meters, Oil Tanks)(ESB meters, Oil Tanks)

Telecomms, IT & Office Equipment (phones, Telecomms, IT & Office Equipment (phones, computer equipment, faxes, copiers)computer equipment, faxes, copiers)

Security Systems Equipment Security Systems Equipment (intruder & fire alarms, CCTV equipment) (intruder & fire alarms, CCTV equipment)

2020

Essential Financial ControlsEssential Financial Controls

Record KeepingRecord Keeping

Accounting for Cash IncomeAccounting for Cash Income

Banking ControlsBanking Controls

Purchase Order ProceduresPurchase Order Procedures

Segregation of DutiesSegregation of Duties

Financial Reports to B.O.M Financial Reports to B.O.M (each meeting)(each meeting)

2121

Cost Savings Cost Savings Some Practical Tips - EnergySome Practical Tips - Energy

1. Make sure you are 1. Make sure you are on the correct on the correct electricity tariff. Your electricity tariff. Your energy supplier will energy supplier will be able to advise you.be able to advise you.

2. Laser printers are 2. Laser printers are very high energy very high energy users. Turn them off users. Turn them off when not in use.when not in use.

3. Don’t leave non-3. Don’t leave non-essential equipment essential equipment running overnight. running overnight. Powersave mode is Powersave mode is not as cheap as not as cheap as switching it off.switching it off.

4. If you have air 4. If you have air conditioners, use them conditioners, use them only when necessary only when necessary e.g. P.E Halls.e.g. P.E Halls.

5. Energy-efficient 5. Energy-efficient bulbs, dimmer and bulbs, dimmer and timer switches all lower timer switches all lower electricity costs.electricity costs.

6. A heat increase of 1 6. A heat increase of 1 degree will add up to degree will add up to 8% to your heating 8% to your heating costs. Keep windows & costs. Keep windows & doors closed whenever doors closed whenever practical.practical.

2222

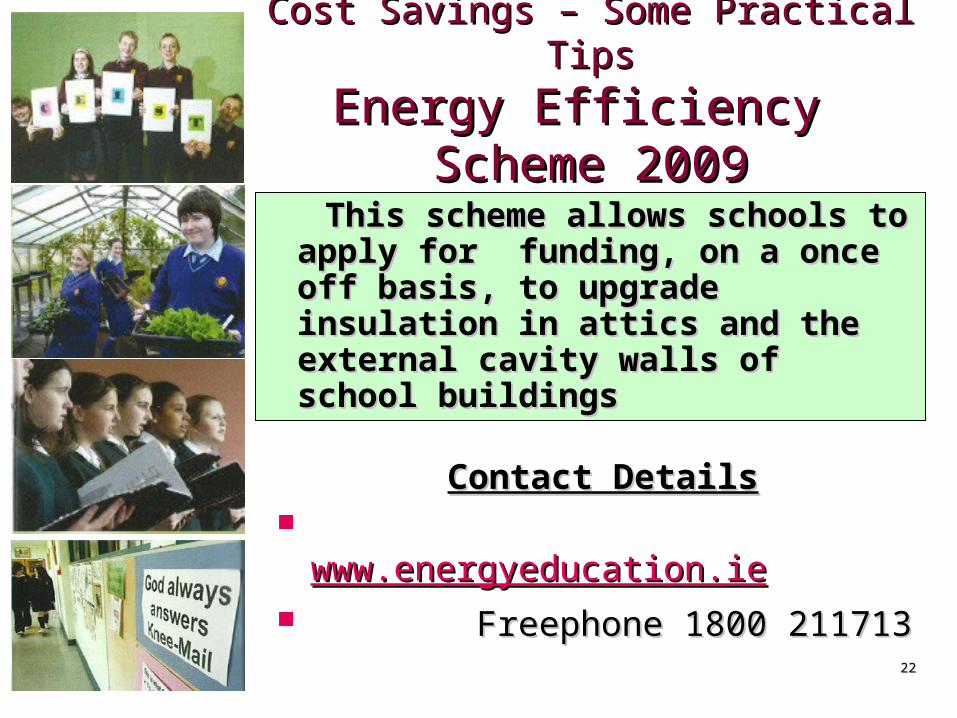

Cost Savings – Some Practical TipsCost Savings – Some Practical Tips

Energy Efficiency Energy Efficiency Scheme 2009Scheme 2009

This scheme allows schools to This scheme allows schools to apply for funding, on a once off apply for funding, on a once off basis, to upgrade insulation in basis, to upgrade insulation in attics and the external cavity walls attics and the external cavity walls of school buildingsof school buildings

Contact DetailsContact Details www.energyeducation.iewww.energyeducation.ie Freephone 1800 211713Freephone 1800 211713

2323

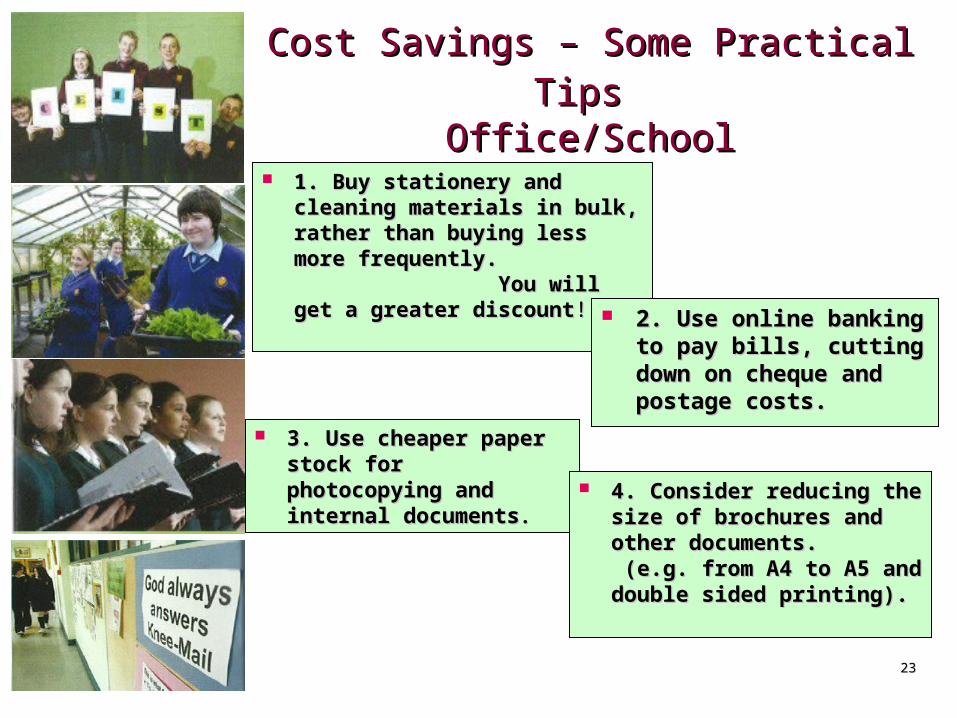

Cost Savings – Some Practical TipsCost Savings – Some Practical Tips Office/SchoolOffice/School

1. Buy stationery and 1. Buy stationery and cleaning materials in bulk, cleaning materials in bulk, rather than buying less more rather than buying less more frequently. frequently. You will get a greater You will get a greater discountdiscount!!

2. Use online banking to 2. Use online banking to pay bills, cutting down pay bills, cutting down on cheque and postage on cheque and postage costs.costs.

3. Use cheaper paper 3. Use cheaper paper stock for photocopying stock for photocopying and internal documentsand internal documents.. 4. Consider reducing the 4. Consider reducing the

size of brochures and size of brochures and other documents. other documents. (e.g. from A4 to A5 and (e.g. from A4 to A5 and double sided printing).double sided printing).

2424

Cheque or EFT Payment?Cheque or EFT Payment?

Cheque Charge 0.50€ Cheque Charge 0.06€

Postage 0.55€ Time (5mins est.) 1.77€

Envelope 0.04€ Email Remittance -€

Time (10mins est.) 3.53€

Comp. Slip 0.22€

Total Cost 4.84€ Total Cost 1.83€

Time is calculated based on Point 16 of the Clerical Officer Salary Scale III

Analysis of Cheque Cost - V- EFT Cost

Cheque Cost EFT Cost

2525

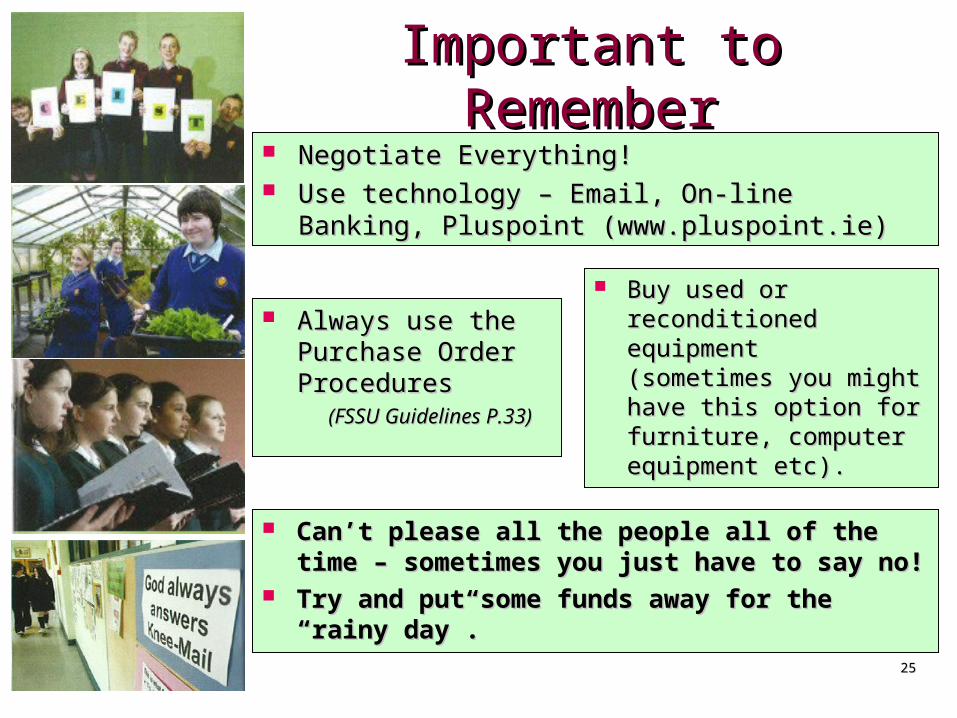

Important to RememberImportant to Remember Negotiate Everything!Negotiate Everything! Use technology – Email, On-line Banking, Pluspoint Use technology – Email, On-line Banking, Pluspoint

(www.pluspoint.ie)(www.pluspoint.ie)

Always use the Always use the Purchase Order Purchase Order Procedures Procedures (FSSU Guidelines P.33)(FSSU Guidelines P.33)

Buy used or Buy used or reconditioned equipment reconditioned equipment (sometimes you might (sometimes you might have this option for have this option for furniture, computer furniture, computer equipment etc).equipment etc).

Can’t please all the people all of the time – Can’t please all the people all of the time – sometimes you just have to say no!sometimes you just have to say no!

Try and put some funds away for the “rainy day”.Try and put some funds away for the “rainy day”.

2626

Finance Sub-Committee

2727

Finance Sub-Committee Assists Finance Sub-Committee Assists the Principal with:the Principal with:

Articles of Articles of ManagementManagement

Annual Budget Annual Budget (see (see www.ceist.iewww.ceist.ie for for templates and templates and instructions)instructions)

Ensure finalising of Ensure finalising of School Accounts School Accounts (see suggested (see suggested timetable).timetable).

School Asset School Asset Register Register (FSSU Appendix 3, (FSSU Appendix 3, Pg 67)Pg 67)

Requirement of Requirement of Trustees, D.E.S., Trustees, D.E.S., F.S.S.U.F.S.S.U.

Regular financial Regular financial reports to B.O.M. reports to B.O.M. (FSSU Appendix 5, (FSSU Appendix 5, Pgs. 70 & 71)Pgs. 70 & 71)

2828

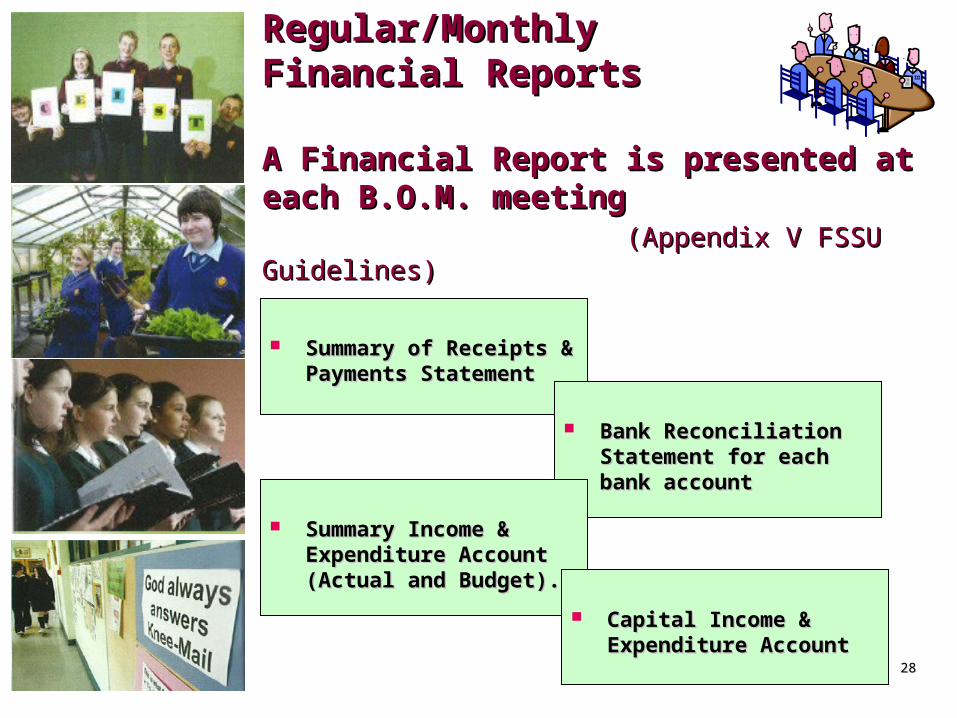

Regular/Monthly Regular/Monthly Financial ReportsFinancial Reports

A Financial Report is presented at each A Financial Report is presented at each B.O.M. meetingB.O.M. meeting (Appendix V FSSU Guidelines)(Appendix V FSSU Guidelines)

Summary of Receipts & Summary of Receipts & Payments StatementPayments Statement

Bank Reconciliation Bank Reconciliation Statement for each bank Statement for each bank accountaccount

Summary Income & Summary Income & Expenditure Account Expenditure Account (Actual and Budget).(Actual and Budget).

Capital Income & Capital Income & Expenditure AccountExpenditure Account

2929

The End!The End!

Q & AQ & A

3030

NotesNotes__________________________________________________________________________________________________

________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________