1h2017 financial results analyst & media...

TRANSCRIPT

1H2017 Financial Results

Analyst & Media Briefing

Datuk Seri TajuddinAtanChief Executive Officer

Rosidah BaharomChief Financial Officer

26 July 2017

2

Agenda

Key Financial Highlights & Market Performance

Financial Review

Highlights & Conclusion

Appendices

3

Key Financial Highlights & Market Performance

Financial Highlights for 1H2017

Half Yearly Financial Trend

Securities Market Overview

Derivatives Market Overview

Islamic Capital Market Overview

4

Financial Highlights for 1H2017Stellar financial results driven by better performance from Securities Market

Higher operating revenue contributed by higher trades in the Securities Market.

Higher operating expenses mainly due to increase in staff cost and technology cost.

Interim and special dividends of 20 sen and 15 sen respectively. The entitlement and

payment dates for the dividends are 10th and 23rd August 2017.

1H2017 vs. 1H2016:

Financial Items 1H2017 1H2016

1H2017

vs.

1H2016

Operating Revenue (RM million) 269.4 248.4 8.5%

Operating Expenses (RM million) 124.9 123.6 1.0%

PATAMI (RM million) 116.2 99.4 16.9%

EPS (sen) 21.7 18.6 16.7%

Cost to Income Ratio 44% 47% 3 percentage points

Annualised ROE 26% 25% 1 percentage point

5

18

16

18

17

21

19

23

27

25 26

25

22

26

50

52

48

50

45

52

48

44

46 46 47

46

44

200

181 197 191

224 216

231 241

240 247 248

225

269

77 67

78 72

93

80

92 106

97 102 99 95

116

1H2011 2H2011 1H2012 2H2012 1H2013 2H2013 1H2014 2H2014 1H2015 2H2015 1H2016 2H2016 1H2017

Half Yearly Financial TrendHighest first half operating revenue since listing

Operating Revenue

(RM mil)

PATAMI

(RM mil)

Cost to Income

Ratio (%)ROE (%)

6

965

1,383

413

593532

522

1H2016 1H2017

1,910

2,498

28

35

1,660

1,838

1H2016 1H2017

10.7%

Securities Market OverviewHigher trades backed by improved market sentiments

Average Daily Value (“ADV”)

(OMT)(RM mil)

Market Capitalisation (RM bil) Fund Raised from New Listings &

Secondary Market (RM bil)

Velocity (%)

1,654

1,764

FBMKLCI

0.4

3.5

7.0

5.0

1H2016 1H2017

7.4

8.5

No. of New Listing

Fund raised from new listings

Fund raised from secondary market

ADV - Domestic Institutions

ADV - Retail

ADV - Foreign Institutions Market Capitalisation

5

8

14.9%30.8%

7

12,057 9,095

47,475

50,482

258 241

1H2016 1H2017

ADC - Crude Palm Oil Futures

Volatility of Crude Palm Oil

Prices

Derivatives Market Overview6% growth in FCPO contracts Y-o-Y

ADC - OthersADC – FBMKLCI Futures

Volatility of FBMKLCI

11%7%

79%

20%

Average Daily Contracts (“ADC”)

& VolatilityOpen Interest (No. of Contract)

84%

15%

0.1%

30 June

2016

292,81731 Mar

2017

262,155

30 June

2017

263,260

1 Sept 2010

111,548

31 Dec 2015

230,376

1%

59,81859,790

1%

19%20%

8

Islamic Capital Market OverviewStronger growth in trade value from foreign participants

24.1 24.5

29.230.6

30 JUNE 2016 30 JUNE 2017

53.355.1

14.4 14.3

2.63.8

1H2016 1H2017

17.0

18.1

6.5%

116

135

No. of Shariah Compliant

Stocks (%)

No. of Trading

Participants

Bursa Suq Al-Sila’ (“BSAS”)

ADV (RM bil)

Market Capitalisation of

Shariah Compliant Stocks

(RM bil)

No. of Sukuk

Value of Listed Sukuk (USD bil)

74%75%

23 25

3.4%

Domestic ForeignMarket Capitalisation of

Shariah Compliant Stocks

Domestic Foreign

1,0341,131

9.4%

30 JUNE 2016 30 JUNE 2017

9

Financial Review

Financial Snapshot

Operating Revenue

Operating Expenses

Dividends

10

49.559.5

99.4

116.2

2Q2016 2Q2017 1H2016 1H2017

122.2134.8

248.4

269.4

2Q2016 2Q2017 1H2016 1H2017

16.9%

8.5%

10.3%

60.3 61.1

123.6 124.9

2Q2016 2Q2017 1H2016 1H2017

1.3%

Financial SnapshotImproved performance for first half of 2017

Operating revenue (RM mil) Operating expenses (RM mil)

PATAMI (RM mil)

46

43

47

44

2Q2016 2Q2017 1H2016 1H2017

Cost to income ratio (%)

3 percentage points

1.0%

3 percentage points

20.3%

11

Operating RevenueGrowth contributed by higher securities trading revenue

Increase in securities trading revenue mainly contributed by domestic trades.

Decrease in derivatives trading revenue was due to lower FKLI trades and also the

downward revision in the guarantee fee rate from 0.5% to 0.3%.

Lower BSAS trading revenue despite growth in its ADV due to volume discount

incentives given.

(RM mil)

112.6138.8

46.1

40.78.8

7.827.0

28.319.6

20.317.9

17.110.6

10.45.8

6.0

1H2016 1H2017

8.5%

Total

RM269.4mil

Total

RM248.4 milGrowth contribution by revenue streams:

248.4

269.4

+ 26.2 - 5.4

- 1.0

4.9%

+ 0.7 - 0.8 - 0.2 + 0.2

1H2016 1H2017

+ 1.3

23.3%

11.9%

3.7%11.7% 1.8%

4.5%4.4%

Securities Trading Revenue

Derivatives Trading Revenue

Listing & Issuer Services

Depository Services

Market Data

Member Services & Connectivity

BSAS Trading Revenue

Conference Fee & Exhibition

Related Income

12

66.6 68.5

12.1 12.1

6.5 5.58.4 9.8

11.813.4

18.2 15.6

1H2016 1H2017

Total

RM123.6 mil

Total

RM124.9 mil

1.0%

(RM mil)

Operating Expenses1H2017 operating expenses increased marginally by 1%

Movement of expenses:

Note^ - Other operating expenses include building maintenance, administrative expenses and CDS expenses.

Increase in staff cost due to annual salary increment.

Increase in service fees due to higher exchange rate.

Higher IT maintenance subsequent to commencement of maintenance for new

enterprise systems.

Lower other operating expenses as 1H2016 included a one-off consultancy fees.

1H2016 1H2017

123.6

+ 1.9 - 1.0 + 1.4 124.9

+ 1.6 - 2.6

2.8%15.5% 16.0%

13.3% 13.8%

Staff costs

Depreciation & amortisation

Marketing & development

IT maintenance

Service fees

Other operating expenses^

13

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

YT

L C

orp

Bri

tish

Am

eri

can T

obacco

Mala

yan B

ankin

g

KLC

CP S

taple

d G

roup

DiG

i.C

om

HA

P S

eng C

onso

lidate

d

West

port

s H

old

ings

Ast

ro M

ala

ysi

a H

old

ings

Maxis

AM

MB H

old

ings

Petr

onas

Gas

CIM

B G

roup H

old

ings

Tele

kom

Mala

ysi

a

Petr

onas

Dagangan

MIS

C

Sim

e D

arb

y

Tenaga N

asi

onal

Petr

onas

Chem

icals

Gro

up

Public B

ank

Hong L

eong B

ank

RH

B B

ank

IJM

Corp

Hong L

eong F

inancia

l G

roup

PPB G

roup

Kuala

Lum

pur

Kepong

IOI C

orp

Axia

ta G

roup

Genti

ng M

ala

ysi

a

Genti

ng

IHH

Healt

hcare

BU

RSA

MA

LA

YSIA

Dividend Yield (annualised) – Bursa vs. FBMKLCI Constituents

@ 30 June 2017

5.4

Source: Bloomberg and Bursa Malaysia

16.0 16.0 16.5 17.0 20.0

16.0 18.0 18.0 17.0

20.020.0

15.0

2013 2014 2015 2016 1H2017

Payout

98% *

Special Dividend (sen)Final Dividend (sen)

* Exclude special dividend

Payout

94%

Payout

92% *

Payout

93%

Interim and special dividend of 20 sen and 15 sen respectively. The entitlement and payment dates for the

dividends are on the 10th and 23rd of August 2017.

Interim Dividend (sen)

DividendsSpecial dividend for our valued shareholders

%

Payout

93%*

14

Highlights & Conclusion

Highlights of 1H2017 Initiatives

Moving Forward

15

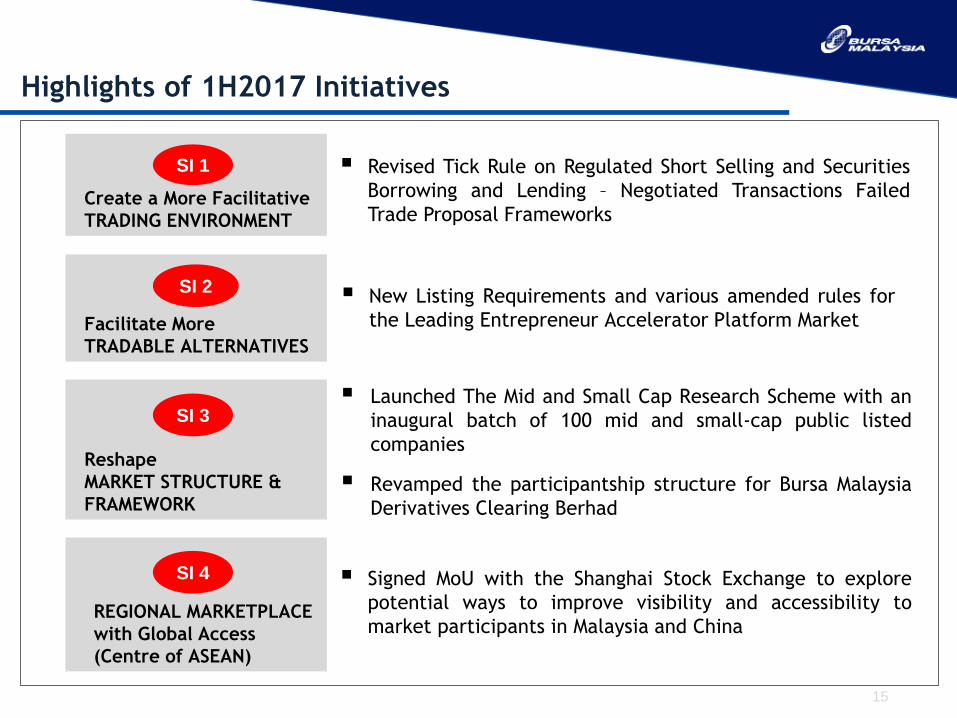

Highlights of 1H2017 Initiatives

Create a More Facilitative

TRADING ENVIRONMENT

SI 1

REGIONAL MARKETPLACE

with Global Access

(Centre of ASEAN)

Revised Tick Rule on Regulated Short Selling and Securities

Borrowing and Lending – Negotiated Transactions Failed

Trade Proposal Frameworks

Facilitate More

TRADABLE ALTERNATIVES

New Listing Requirements and various amended rules for

the Leading Entrepreneur Accelerator Platform Market

Launched The Mid and Small Cap Research Scheme with an

inaugural batch of 100 mid and small-cap public listed

companies

Revamped the participantship structure for Bursa Malaysia

Derivatives Clearing Berhad

Reshape

MARKET STRUCTURE &

FRAMEWORK

SI 2

SI 3

SI 4 Signed MoU with the Shanghai Stock Exchange to explore

potential ways to improve visibility and accessibility to

market participants in Malaysia and China

16

Moving Forward

SECURITIES MARKET• The Securities Market trading activities for the first half of 2017 registered strong Average Daily Trading

Value.

• The momentum of Securities Market performance is forecasted to continue with the expected

improvements in the global as well as domestic economic conditions.

DERIVATIVES MARKET• Improved oil palm fruit harvest and volatility in the FBMKLCI will continue to underpin trading and

hedging of FCPO and FKLI contracts respectively.

ISLAMIC CAPITAL MARKET• Bursa Suq Al-Sila’ continues to show progress with new participants from financial institutions in Africa,

Central Asia and South America. Bursa Malaysia will continue with its efforts to expand its niche in these

regions and globally.

• Bursa Malaysia-i will further intensify its efforts to promote Shariah investing and to focus on forging

collaborations with capital market participants to spur the growth and vibrancy of Islamic Capital Market

domestically and regionally.

Bursa Malaysia will continue its efforts to make the Malaysian capital markets attractive and anticipates an

improved performance for the current financial year.

17

1H2017 Financial Results Analyst & Media Briefing

Q&A

18

Appendices

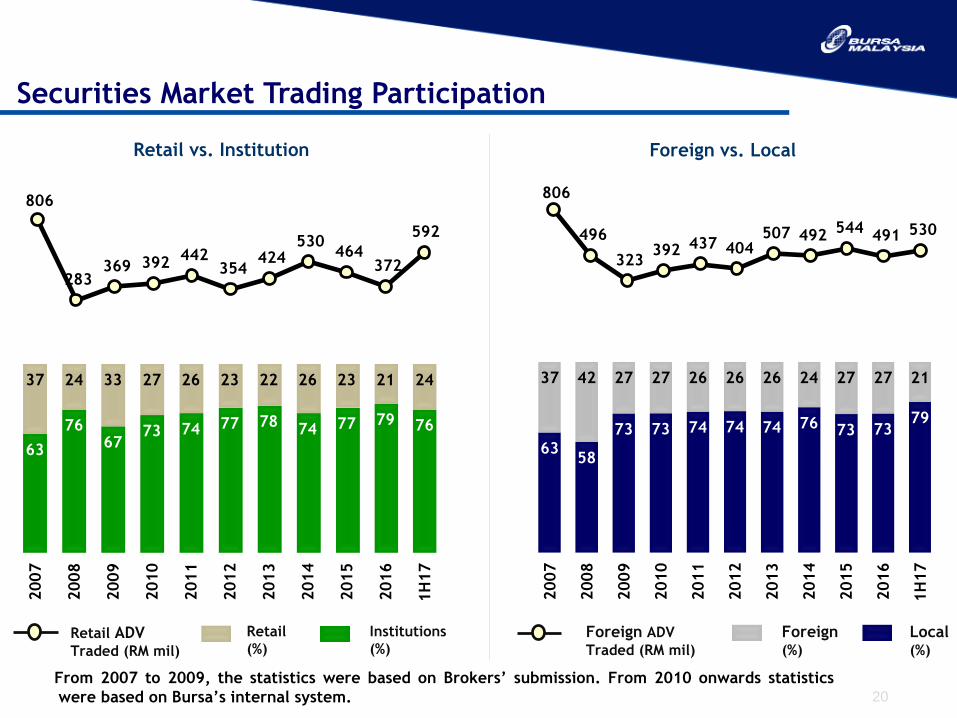

Securities Market Trading Activity

Securities Market Trading Participation

Securities Market Foreign Ownership

Foreign Inflow/Outflow

Derivatives Market Activity

Derivatives Market Demography

Islamic Capital Market Activity

19

1,435

1,209 1,387

1,793

2,161

1,579 1,732

1,341

1,841

1,439 1,595

1,430

1,643

2,308

2,002

1,686

2,068 2,053 2,196

1,901 2,081

1,913 1,933 2,042 1,981

1,842 1,740 1,690

2,378

2,621

1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17

35

2831

3742

3034

27

34

27 2825

28

3731

2530 29 30 28 30 28 29 30 29 27 26 25

34 35

53

34 34 33 3328 30 29 30 27

35

2,179

1,181 1,129 1,454

1,699 1,573 1,915

2,053 1,991 1,812

2,498

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 1H17

Turnover Velocity (%)

Quarterly ADV Traded & Velocity

Average Daily Value Traded (OMT, RM mil)

Average Daily Value Traded (OMT, RM mil)Turnover Velocity (%)

Annual ADV Traded & Velocity

Securities Market Trading Activity

20

806

283 369 392

442 354

424 530

464 372

592

63

7667

73 74 77 7874 77 79 76

37 24 33 27 26 23 22 26 23 21 24

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

1H

17

6358

73 73 74 74 74 76 73 7379

37 42 27 27 26 26 26 24 27 27 21

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

1H

17

From 2007 to 2009, the statistics were based on Brokers’ submission. From 2010 onwards statistics

were based on Bursa’s internal system.

Retail

(%)

Institutions

(%)Local(%)

Foreign(%)

Retail ADVTraded (RM mil)

Foreign ADV

Traded (RM mil)

Retail vs. Institution Foreign vs. Local

Securities Market Trading Participation

806

496

323 392 437 404

507 492 544

491 530

21

Securities Market Foreign Ownership

22.3

23.1

24.4

24.0

24.3

22.8

22.3

22.5

23.0 23.0 23.022.8

23.023.1

22.8 22.8

22.6

22.3 22.3 22.3 22.4

22.7

22.923.0

Based on Market Capitalisation (%)

22

Foreign Inflow/Outflow

Monthly foreign inflow/outflow from 2012 to June 2017

-1,760

1,021 1,605

-315-450

-3,934

-972

420 942

4,355

2,6101,977

359

-5,000

-4,000

-3,000

-2,000

-1,000

0

1,000

2,000

3,000

4,000

5,000Monthly foreign inflow/outflow from June 2016 to June 2017(RM mil)

2016

TNFO: RM3.2 bil

-10,000

-5,000

0

5,000

10,000

2015

TNFO: RM19.7 bil

2012

TNFI: RM13.6 bil

2013

TNFI: RM2.6 bil2014

TNFO: RM6.9 bil

TNFI: Total Net Foreign Inflow

(RM mil)

TNFO: Total Net Foreign Outflow

1H2017

TNFI: RM10.7 bil

23

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

1H

17

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

15

%

129

115 114

132

136

162

171

152

174

146

172

214

196

213204

196

218

239

288

196

207

229235

283

293

226237

262263

230

40

Quarterly Average Daily Contracts (’000)

31

42

35

60

Total Annual Contract (mil)

Crude Palm Oil FuturesOthersOpen Interest (’000)

15%

84%

6.2 6.1 6.1 6.2

8.4

9.6

FMBKLCI Futures

37

`

`

84

%32

34

444542

4642

10.7

50

12.5

44

54

Derivatives Market Activity

55

14.2

62

51

62

56

7.2

5856

62

55

as

125

156

123132

152

214196 196

230237

263

14.1

2423

2528

57

1%

1%

24

15 15 20 21 19 15 18 20 18 14 11

4146

5244

42

2828 24

23

1917

2

2

3

22

21 2

5

3

3

4237

2633

37

55 53 54 55

6469

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 1H17

(%)FKLI

25 27

36 34 34 36 33 34 31 28 26

3438

2726 24 19

17 1515

16 17

11

11

1 11

1

22 15 17

1513

12

10 15 2121 22

18 20 1925 28

3239

35 32 34 34

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 1H17

(%)FCPO

1

Local

Domestic Retail

Domestic

Institutions

Foreign Institutions Local

Domestic RetailDomestic

Institutions

Foreign Institutions Foreign Retail

Derivatives Market Demography

25

2011 2012 2013 2014 2015 2016 1H2017

BSAS Annual Average Daily Value

Local ADV Foreign ADV

1.22.3 3.9

6.9

15.2 16.3 18.1

14.3

3.8

13.3

(RM bil)

13.413.5

1.61.0

2.91.7

1.4

1.20.70.2

BSAS ADV (RM bil)

13.5

0.9

0.8 0.9 1.1 1.1 1.3 1.5 1.6 1.8 2.6 2.4 2.7 3.2 3.7 3.7 5.9

8.5 10.4

12.0 14.4

16.9 16.1

12.7 12.2 12.6 13.6 15.1

0.2 0.2 0.2 0.3 0.3 0.7 0.9 1.2

1.1 1.0 1.1 1.5 1.4 1.5

1.4

1.4

1.5

1.6

1.6

2.1 2.6

2.7 3.0 3.2 3.8

3.7

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

BSAS Quarterly Average Daily Value(RM bil)

5.5

2.7

Islamic Capital Market Activity

DISCLAIMER:

Bursa Malaysia and its Group of Companies (the Company) reserve all proprietary rights to the contents of this presentation. Whilst the company endeavors to ensure that

the contents in this presentation are accurate, complete or have been obtained from sources believed by the Company to be accurate and reliable, neither the Company

nor the presenter make any warranty, express or implied, nor assume any legal liability or responsibility for the accuracy, completeness or currency of the contents of this

presentation. In no event shall the Company be liable for any claim, howsoever arising, out of or in relation to this presentation.

Copyright Bursa Malaysia Berhad 2017 (30632-P)

www.bursamalaysia.com

RASMONA ABDUL RAHMAN

603-2034 7175

E-mail : [email protected]

RAFIDAH AZIZ

603-2034 7262

ADAM ISKANDAR AHMAD ZAHAR

603-2034 7351

INVESTOR RELATIONS CONTACT INFORMATION