2016 depreciation study

TRANSCRIPT

2016 DEPRECIATION STUDY

CALCULATED ANNUAL DEPRECIATION ACCRUALS RELATED TO WATER PLANT

AS OF DECEMBER 31, 2016

Prepared by:

NEW JERSEY AMERICAN WATER COMPANY Voorhees, New Jersey

2016 DEPRECIATION STUDY

CALCULATED ANNUAL DEPRECIATION

ACCRUALS RELATED TO WATER PLANT

AS OF DECEMBER 31, 2016

GANNETT FLEMING VALUATION AND RATE CONSULTANTS, LLC

Camp Hill, Pennsylvania

TABLE OF CONTENTS

EXECUTIVE SUMMARY . . . . . . . . . . . . . . . . . . .. . ... . . . . . . . . . . . .. . . . . . . . . . . .... .. . . .. . . . . . . . . . . . . . . . . . . . . . . ........ iii

PART I. INTRODUCTION...................................................................................... 1-1 Scope .................................................................................................................... 1-2 Plan of Report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1-2 Basis of the Study . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1-3

Depreciation ................................................................................................ 1-3 Service Life Estimates and Net Salvage Normalization............................... 1-4

PART II. ESTIMATION OF SURVIVOR CURVES................................................. 11-1 Survivor Curves...................................................................................................... 11-2

Iowa Type Curves........................................................................................ 11-3 Retirement Rate Method of Analysis........................................................... 11-9 Schedules of Annual Transactions in Plant Records................................... 11-10 Schedule of Plant Exposed to Retirement................................................... 11-13 Original Life Table ...................................................................................... 11-15 Smoothing the Original Survivor Curve........................................................ 11-17

PART Ill. SERVICE LIFE CONSIDERATIONS..................................................... 111-1 Field Trips.............................................................................................................. 111-2 Service Life Analysis.............................................................................................. 111-2

PART IV. NET SALVAGE CONSIDERATIONS................................................... IV-1 Net Salvage Normalization..................................................................................... IV-2

PART V. CALCULATION OF ANNUAL AND ACCRUED DEPRECIATION......... V-1 Group Depreciation Procedures............................................................................. V-2

Single Unit of Property................................................................................. V-2 Group Depreciation Procedures.................................................................. V-3 Remaining Life Annual Accruals.................................................................. V-3 Average Service Life Procedure.................................................................. V-3

Calculation of Annual and Accrued Amortization.................................................... V-4

PART VI. RESULTS OF STUDY.......................................................................... Vl-1 Qualification of Results........................................................................................... Vl-2 Description of Detailed Tabulations........................................................................ Vl-2

~ 6annett Fleming New Jersey American Water Co - Water December 31, 2016

TABLE OF CONTENTS, cont.

Table 1. Summary of Estimated Survivor Curves, Original Cost, Book Depreciation Reserve, and Calculated Annual Depreciation Accrual Rates and Net Salvage Normalization as of December 31, 2016........ Vl-4

Table 2. Calculation of Net Salvage Normalization........................................... Vl-7

PART VII. SERVICE LIFE STATISTICS................................................................ Vll-1

PART VIII. DETAILED DEPRECIATION CALCULATIONS .................................. Vllll-1

~ 6annettF/eming ii New Jersey American Water Co - Water December 31, 2016

EXECUTIVE SUMMARY

Pursuant to New Jersey American Water Company's ("NJAWC") request, Gannett

Fleming Valuation and Rate Consultants, LLC ("Gannett Fleming") has conducted a

depreciation study related to NJAWC plant as of December 31, 2016. The purpose of

this study was to determine the annual depreciation accrual rates and amounts for book

and ratemaking purposes.

The depreciation rates are based on the straight line method using the average

service life ("ASL") procedure and were applied on a remaining life basis. The

calculations were based on attained ages and estimated average service life as well as

the net salvage normalization for each depreciable group of assets.

NJAWC's accounting policy has not changed since the previous depreciation study

was prepared, nor were there any significant policy changes that might affect the results

of the study presented here. However, some average service life estimates proposed in

this study have changed from the currently approved estimates. The overall depreciation

accrual rate has increased since the last study was performed.

Gannett Fleming recommends the calculated annual depreciation accrual rates

proposed herein apply specifically to NJAWC's plant in service as of December 31, 2016

as summarized in Table 1 of the study. The study sets forth a total annual depreciation

expense of $123.5 million as applied to the depreciable original cost of $4.38 billion as of

December 31, 2016.

Gannett Fleming iii New Jersey American Water Co - Water December 31, 2016

~ 6annettF/eming 1-1

PART I. INTRODUCTION

New Jersey American Water Co - Water December 31, 2016

NEW JERSEY AMERICAN WATER COMPANY

DEPRECIATION STUDY

PART I. INTRODUCTION

SCOPE

This report presents the results of the depreciation study prepared for the New

Jersey American Water Company as applied to water plant in service as of December 31,

2016. It relates to the concepts, methods, and basic judgments which underlie

recommended annual depreciation accrual rates related to current utility plant in service.

The service life estimates resulting from the study were based on informed

judgment which incorporated analyses of historical plant retirement data as recorded

through 2016; a review of Company practice and outlook as they relate to plant operation

and retirement; and consideration of current practice in the water industry, including

knowledge of service life estimates used for other water properties.

PLAN OF REPORT

Part I, Introduction, contains statements with respect to the plan of the report, and

the basis of the study. Part II, Estimation of Survivor Curves, presents descriptions of the

considerations and the methods used in the service life studies. Part Ill, Service Life

Considerations, presents the factors and judgment utilized in the average service life

analysis. Part IV, Net Salvage Considerations, presents the judgment utilized of the net

salvage study. Part V, Calculation of Annual and Accrued Depreciation, describes the

procedures used in the calculation of group depreciation. Part VI, Results of Study,

presents summaries by depreciable group of annual depreciation accrual rates and

amounts, as well as composite remaining lives. Part VII, Service Life Statistics presents

the statistical analysis of service life estimates, and Part VIII, Detailed Depreciation

Calculations presents the detailed tabulations of annual depreciation.

Gannett Fleming 1-2 New Jersey American Water Co - Water December 31, 2016

BASIS OF THE STUDY

Depreciation

Depreciation, in public utility regulation, is the loss in service value not restored by

current maintenance, incurred in connection with the consumption or prospective

retirement of utility plant in the course of service from causes which are known to be in

current operation and against which the utility is not protected by insurance. Among

causes to be given consideration are wear and tear, deterioration, action of the elements,

inadequacy, obsolescence, changes in the art, changes in demand, and the requirements

of public authorities.

Depreciation, as used in accounting, is a method of distributing fixed capital costs,

less net salvage, over a period of time by allocating annual amounts to expense. Each

annual amount of such depreciation expense is part of that year's total cost of providing

water utility service. Normally, the period of time over which the fixed capital cost is

allocated to the cost of service is equal to the period of time over which an item renders

service, that is, the item's service life. The most prevalent method of allocation is to

distribute an equal amount of cost to each year of service life. This method is known as

the straight-line method of depreciation.

For most accounts, the annual depreciation was calculated by the straight line

method using the average service life procedure and the remaining life basis. For certain

General Plant accounts, the annual depreciation is based on amortization accounting.

Both types of calculations were based on original cost, attained ages, and estimates of

service lives.

The straight line method, average service life procedure is a commonly used

depreciation calculation procedure that has been widely accepted in jurisdictions

throughout North America. Gannett Fleming recommends its continued use. Amortization

accounting is used for certain General Plant accounts because of the disproportionate

~ 6annettF/eming 1-3 New Jersey American Water Co - Water December 31, 2016

plant accounting effort required when compared to the minimal original cost of the large

number of items in these accounts. An explanation of the calculation of annual and

accrued amortization is presented beginning on page V-4 of the report.

Service Life Estimates and Net Salvage Normalization

The service life estimates used in the depreciation and amortization calculations

were based on informed judgment which incorporated a review of management's plans,

policies and outlook, a general knowledge of the water utility industry, and comparisons

of the service life and net salvage estimates from our studies of other water utilities. The

use of survivor curves to reflect the expected dispersion of retirement provides a

consistent method of estimating depreciation for water plant. Iowa type survivor curves

were used to depict the estimated survivor curves for the plant accounts not subject to

amortization accounting.

The procedure for estimating service lives consisted of compiling historical data

for the plant accounts or depreciable groups, analyzing this history through the use of

widely accepted techniques, and forecasting the survivor characteristics for each

depreciable group on the basis of interpretations of the historical data analyses and the

probable future. The combination of the historical experience and the estimated future

yielded estimated survivor curves from which the average service lives were derived.

The estimates of net salvage by account incorporated a review of experienced

costs of removal and salvage related to transactions over the last three years. Each

component of net salvage, i.e. cost of removal and salvage, was stated in dollars incurred

during the three-year period.

An understanding of the function of the plant and information with respect to the

reasons for past retirements and the expected causes of future retirements was obtained

through field trips and discussions with operating and management personnel. The

Gannett Fleming 1-4 New Jersey American Water Co - Water December 31, 2016

supplemental information obtained in this manner was considered in the interpretation

and extrapolation of the statistical analyses.

6annettF/eming 1-5 New Jersey American Water Co - Water December 31, 2016

~ Gannett Fleming 11-1

PART II. ESTIMATION OF SURVIVOR CURVES

New Jersey American Water Co - Water December 31, 2016

PART II. ESTIMATION OF SURVIVOR CURVES

The calculation of annual depreciation based on the straight line method requires

the estimation of survivor curves and the selection of group depreciation procedures. The

estimation of survivor curves is discussed below and the development of net salvage is

discussed in later sections of this report.

SURVIVOR CURVES

The use of an average service life for a property group implies that the various

units in the group have different lives. Thus, the average life may be obtained by

determining the separate lives of each of the units, or by constructing a survivor curve by

plotting the number of units which survive at successive ages.

The survivor curve graphically depicts the amount of property existing at each age

throughout the life of an original group. From the survivor curve, the average life of the

group, the remaining life expectancy, the probable life, and the frequency curve can be

calculated. In Figure 1, a typical smooth survivor curve and the derived curves are

illustrated. The average life is obtained by calculating the area under the survivor curve,

from age zero to the maximum age, and dividing this area by the ordinate at age zero.

The remaining life expectancy at any age can be calculated by obtaining the area under

the curve, from the observation age to the maximum age, and dividing this area by the

percent surviving at the observation age. For example, in Figure 1, the remaining life at

age 30 is equal to the crosshatched area under the survivor curve divided by 29.5 percent

surviving at age 30. The probable life at any age is developed by adding the age and

remaining life. If the probable life of the property is calculated for each year of age, the

probable life curve shown in the chart can be developed. The frequency curve presents

the number of units retired in each age interval. It is derived by obtaining the differences

between the amount of property surviving at the beginning and at the end of each interval.

6annett Fleming 11-2 New Jersey American Water Co - Water December 31, 2016

This study has incorporated the use of Iowa curves developed from a retirement

rate analysis of historical retirement history. A discussion of the concepts of survivor

curves and of the development of survivor curves using the retirement rate method is

presented below.

Iowa Type Curves

The range of survivor characteristics usually experienced by utility and industrial

properties is encompassed by a system of generalized survivor curves known as the Iowa

type curves. There are four families in the Iowa system, labeled in accordance with the

location of the modes of the retirements in relationship to the average life and the relative

height of the modes. The left moded curves, presented in Figure 2, are those in which

the greatest frequency of retirement occurs to the left of, or prior to, average service life.

The symmetrical moded curves, presented in Figure 3, are those in which the greatest

frequency of retirement occurs at average service life. The right moded curves, presented

in Figure 4, are those in which the greatest frequency occurs to the right of, or after,

average service life. The origin moded curves, presented in Figure 5, are those in which

the greatest frequency of retirement occurs at the origin, or immediately after age zero.

The letter designation of each family of curves (L, S, R or 0) represents the location of

the mode of the associated frequency curve with respect to the average service life. The

numbers represent the relative heights of the modes of the frequency curves within each

family.

The Iowa curves were developed at the Iowa State College Engineering

Experiment Station through an extensive process of observation and classification of the

ages at which industrial property had been retired. A report of the study which resulted

in the classification of property survivor characteristics into 18 type curves,

liannett Fleming 11-3 New Jersey American Water Co - Water December 31, 2016

[Bf

en ~ I

10

0

i ~I

90

l! ~

80

...

. I

~ I

70

O>

-~

60

>

>

s..

::,

- ~ .b.

I

(JJ

50

....

-C

~

G)

(J

s.. a>

40

a.

- - -

z 3

0

CD

-::: c:.

.. CD

..., en

~I

)>

20

3 ~ o·

o ~

I 10

~~

CD

DJ

3 -

O'"

~

~

()

(,J

0 ...

.>.

I

~~

0 DJ

.....

. -0

) ~

0

~ "'

\ '\

.....---s

urv

ivo

r C

urv

e

\-L.

.,-P

roba

ble

Life

Cu

rve

~ \

\ \

\ \

Ave

rag

e L

ife

\~

\ '-

~ I

I I

I '-

' M

axi

mu

m L

ife

,

\ \

~

Pro

ba

ble

Lif

e

' \

~

"" -=: ::

xpe

cta

ncy

~

Ag

e

Mod

e \.

~

\ \.

~

~ ~ "'

F

req

ue

ncy

Cu

rve

~ ,,,,

,.------

.... ~

~

/ ~ W

//~

~ ""'-

-~

~

~

'-ij//// ////,,

5 10

15

20

2

5

30

3

5

40

4

5

50

Ag

e I

n Y

ea

rs

Fig

ure

1.

A T

ypic

al S

urv

ivo

r C

urv

e an

d D

eriv

ed C

urv

es

~

55

60

:u ~ :.; a.

4 l

3 ~ c

2 1l :.; a.

~

g, ~ l'D

l"'to

l"'to :tl ~ 5· LC

:i I 01

z ~ c....

(1) iil

(1)

'<

)>

3 (1) £.

0::

J

(1) ~

@ Il

l

3 ro

C""

"'

(1)

()

""'0

~.

~ ::

E O

il>

mm

""'

10

0

--

90

1

~

ao

I I

70

I

I

C>

so I

C

I >

>

L

..

:::,

Cl)

5

0

-C Cl) 0 L..

C

l) 4

0

a..

30

20

10

0 2

5 -

--

-~

50

i:

> ,;;;

: ,. Ii:

: ,. ' "'

" I

I I

i45

~4

0

e ~3

5

0

/ L

5

/u \

r i\\

~ r:,

n

L1

~ ~

I>

..

~/ ~ ~

LO

' r-,.;::

'< ~

' \l

\

\ "

I I

I ::

30

I '

...

.g

,4'.

\I \

\\

j25

I I

e

I ~

\\I

I ~

20

,,:;

I g

15

I C

l :, f1

0

IL

5

0 2

5

50

7

5

10

0

12

5

15

0

17

5

20

0

22

5

25

0

27

5

30

0

Ag

e, P

erc

en

t o

f A

vera

ge

Life

50

7

5

10

0

12

5

15

0

17

5

20

0

22

5

25

0

27

5

30

0

Ag

e,

Pe

rce

nt

of

Ave

rag

e L

ife

Fig

ure

2.

Le

ft M

od

al

or

"L"

Iow

a T

yp

e S

urv

ivo

r C

urv

es

[e

~ 5 rn ~ lJ ~ 5· IQ

I 0)

z ~ c:_

(D

iil ~

)>

3 (D @"

0::

J

~~

(D

Ill

3 ro

CT

-,

(D

(")

-,

0 ~.

~~

mar -,

10

0

90

I

ao I

70

I

C>

ao I

C

: > "> L

..

::::,

(f)

50

-C: Q

) 0 L

..

Q)

40

a..

30

20

10

0

--

--

--

-6

0

.!!

I ""~

''\\\

I I

~ 4

5

-<

~ ~

-..

. I

~ ~ 4

0

• f 35

I

.,

I'<

'<

3\-1>

.t \

\I

11.

I I

I ~ 3

0

~ 2

5

C .,

I I

'-.I

~ .. ,\\

\\ I

I

~ 2

0

I 11

. ~1

5

I I

I I

I ]

I I

S8

I I

J 1

I .

~ L---1

--+--t

----rr

li ,, -

~, -

~

~, s,

1\

I I

1,\\

\\1

.. I

I ~

10

e IL

5

8 S

_

/,,.

s-

'-

/ I

J\,~

"~

I

I J

....

....

..-:

:~r.

.i

"-0

25

5

0

75

1

00

1

25

1

50

1

75

2

00

2

25

2

50

2

75

3

00

Ag

a.

Pe

rce

nt

of

Ave

rag

e L

ife

25

5

0

75

1

00

1

25

1

50

1

75

2

00

2

25

2

50

2

75

3

00

Ag

e,

Pe

rce

nt

of

Ave

rag

e L

ife

Fig

ure

3.

Sym

me

tric

al

or

"S"

Iow

a T

yp

e S

urv

ivo

r C

urv

es

re

&11

10

0

5 l'b

I ,....

9

0

,.... ,, rr

I 8

0

:3 5· lQ I

70

O>

C ·s:

60

-~

:::

:,

C/J

50

-C Q

) (.

)

.!_i I

<ii 4

0

a.

30

20

z (1

) :E

c.... !!l

I 1

0

en

(1)

'<

)>

3 !)l

o~

· 0

(1) ~

£ Q

) 3

.....

O"

!)l

!)l

()

vJ

0 ...

>.

I

N~

0

Q)

........

.. O

l !)l

25

5

0

75

1

00

1

25

1

50

,o5

0

"ii 145

1

:40

~ l35

0 ::

30

.e 1

:25

~ :20

~1

5

:i ::, e1

0 u.

5

~

c:.

- ~ ,/

'/

R6 j\

I ~, ,1 R3

' i/

~

,:,

•'-

-R1

,,..._ _

\.

~ ~ ....

......

0 2

5

50

7

5

10

0

12

5

15

0

17

5

20

0

22

5

25

0

27

5

30

0

Ag

e,

Pe

rce

nt

of

Ave

rag

e L

ife

17

5

20

0

22

5

25

0

27

5

Ag

e,

Pe

rce

nt

of

Ave

rag

e L

ife

Fig

ure

4.

Rig

ht

Mo

da

l o

r "R

" Io

wa

Typ

e S

urv

ivo

r C

urv

es

30

0

en ! I

10

0

:::J

~I

90

""" :ti ~I

80

5· ~I

70

C)

C:

·s;

60

·s;

L

..

::::,

en

50

.....

C

: <

I)

co I

0 L..

4

0

<I)

a..

30

z 2

0

CD

::E

c...

CD

-, ~I

'<

10

)>

3 CD

o~

· 0

25

~ ~

CD

Ill

3 r+

O" ~

~o

w

o

_..

I

-N ~

Olll

....

..

r+

0) ~

50

7

5

10

0

12

5

15

0

•20

! .!

18

.!:

j 1

6

e ~1

4

0 :: 1

2

.g

E1

0

~ ~ 8

r; 6

C " g.

4 I!! IL

2

..

~

04

DI. .....

.. 0

3

~2

I

~

01

' ~

_::

, '

..........

.. L~

,._

1 ....

......

...

L I

o ~ ~

n 10

0 1

~

1~

1

n ~ ~ ~ ~ ~

Ag

e,

Pe

rce

nt

of

Ave

rag

e L

ife

17

5

20

0

22

5

25

0

27

5

Ag

e,

Pe

rce

nt

of

Ave

rag

e L

ife

Fig

ure

5.

Ori

gin

Mo

da

l o

r "O

" Io

wa

Typ

e S

urv

ivo

r C

urv

es

30

0

which constitute three of the four families, was published in 1935 in the form of the

Experiment Station's Bulletin 125. These curve types have also been presented in

subsequent Experiment Station bulletins and in the text, "Engineering Valuation and

Depreciation."1 In 1957, Frank V. B. Couch, Jr., an Iowa State College graduate student

submitted a thesis presenting his development of the fourth family consisting of the four

0 type survivor curves.

Retirement Rate Method of Analysis

The retirement rate method is an actuarial method of deriving survivor curves using

the average rates at which property of each age group is retired. The method relates to

property groups for which aged accounting experience is available and is the method

used to develop the original stub survivor curves in this study. The method (also known

as the annual rate method) is illustrated through the use of an example in the following

text, and is also explained in several publications, including "Statistical Analyses of

Industrial Property Retirements,"2 "Engineering Valuation and Depreciation,"3 and

"Depreciation Systems. "4

The average rate of retirement used in the calculation of the percent surviving for

the survivor curve (life table) requires two sets of data: first, the property retired during a

period of observation, identified by the property's age at retirement; and second, the

property exposed to retirement at the beginning of the age intervals during the same

period. The period of observation is referred to as the experience band, and the band of

years which represent the installation dates of the property exposed to retirement during

the experience band is referred to as the placement band. An example of the calculations

used in the development of a life table follows. The example includes schedules of annual

1Marston, Anson, Robley Winfrey and Jean C. Hempstead. Engineering Valuation and Depreciation, 2nd Edition. New York, McGraw-Hill Book Company. 1953.

2Winfrey, Robley, Statistical Analyses of Industrial Property Retirements. Iowa State College Engineering Experiment Station, Bulletin 125. 1935.

3Marston, Anson, Robley Winfrey, and Jean C. Hempstead, Supra Note 1. 4Wolf, Frank K. and W. Chester Fitch. Depreciation Systems. Iowa State University Press. 1994.

6annettF/eming 11-9 New Jersey American Water Co - Water December 31, 2016

aged property transactions, a schedule of plant exposed to retirement, a life table and

illustrations of smoothing the stub survivor curve.

Schedules of Annual Transactions in Plant Records

The property group used to illustrate the retirement rate method is observed for

the experience band 2007-2016 during which there were placements during the years

2002-2016. In order to illustrate the summation of the aged data by age interval, the data

were compiled in the manner presented in Schedules 1 and 2 on pages 11-11 and 11-12.

In Schedule 1, the year of installation (year placed) and the year of retirement are shown.

The age interval during which a retirement occurred is determined from this information.

In the example which follows, $10,000 of the dollars invested in 2002 were retired in 2007.

The $10,000 retirement occurred during the age interval between 4% and 5% years on

the basis that approximately one-half of the amount of property was installed prior to and

subsequent to July 1 of each year. That is, on the average, property installed during a

year is placed in service at the midpoint of the year for the purpose of the analysis. All

retirements also are stated as occurring at the midpoint of a one-year age interval of time,

except the first age interval which encompasses only one-half year.

The total retirements occurring in each age interval in a band are determined by

summing the amounts for each transaction year-installation year combination for that age

interval. For example, the total of $143,000 retired for age interval 4%-5% is the sum of

the retirements entered on Schedule 1 immediately above the stair step line drawn on the

table beginning with the 2007 retirements of 2002 installations and ending with the 2016

retirements of the 2011 installations. Thus, the total amount of 143 for age interval 4%-

5% equals the sum of:

10 + 12 + 13 + 11 + 13 + 13 + 15 + 17 + 19 + 20.

6annettF/eming 11-10 New Jersey American Water Co - Water December 31, 2016

[Bf g, I

SC

HE

DU

LE

1.

RE

TIR

EM

EN

TS

FO

R E

AC

H Y

EA

R 2

007-

2016

S

UM

MA

RIZ

ED

BY

AG

E I

NT

ER

VA

L

s FD

I E

xpe

rie

nce

Ban

d 20

07-2

016

Pla

cem

ent

Ban

d 20

02-2

016

,....

,.... :0

Ret

irem

ents

, T

hous

ands

of D

olla

rs

~ Y

ea

r D

urin

g Y

ear

Tot

al D

urin

g A

ge

Pla

ced

2007

20

08

2009

20

10

2011

20

12

2013

20

14

2015

20

16

Ag

e I

nter

val

Inte

rval

s· LC

5 (1

) (2

) (3

) (4

) (5

) (6

) (7

) (8

) (9

) (1

0)

(11)

(1

2)

(13)

2002

10

11

12

13

14

16

23

24

25

26

26

13

Yz-

14Y

z 20

03

11

12

13

15

16

18

20

21

22

19

44

12Y

z-13

Yz

2004

11

12

13

14

16

17

19

21

22

18

64

11

Yz-

12Y

z 20

05

8 9

10

11

11

13

14

15

16

17

83

1 OYz

-11

Yz

2006

9

10

11

12

13

14

16

17

19

20

93

9Yz-

10Y

z

~, 20

07

4 9

10

11

12

13

14

15

16

20

105

8Yz-

9Yz

2008

5

11

12

13

14

15

16

18

20

113

7Yz-

8Yz

2009

6

12

13

15

16

17

19

19

124

6Yz-

7Yz

2010

6

13

15

16

17

19

19

131

5Yz-

6Yz

2011

7

14

16

17

19

20

143

4Yz-

5Yz

2012

8

18

20

22

23

146

3Yz-

4Yz

z 20

13

9 20

22

25

15

0 2Y

z-3Y

z CD

20

14

11

23

25

151

1 Yz-2

Yz

:E

c:_

20

15

11

24

153

Yz-1

Yz

CD in

2016

13

80

0-

Yz

CD

'<

)>

3 ~. I

Tot

al

53

68

86

106

128

157

196

231

273

308

1,60

6 ('

)

0~

CD

@~

3

-0

-~

~o

w

o

...>

. I

~~

0 Q

l

~{

SC

HE

DU

LE

2.

OT

HE

R T

RA

NS

AC

TIO

NS

FO

R E

AC

H Y

EA

R 2

00

7-2

01

6

en I

SU

MM

AR

IZE

D B

Y A

GE

IN

TE

RV

AL

QJ

~I

Exp

eri

en

ce B

an

d 2

00

7-2

01

6

Pla

cem

en

t B

and

20

02

-20

16

l'D

.....

.....

Acq

uis

itio

ns,

Tra

nsf

ers

an

d S

ales

, T

ho

usa

nd

s o

f D

olla

rs

;o D

uri

ng

Ye

ar

~ Y

ea

r T

otal

Dur

ing

Ag

e

s· P

lace

d

20

07

2

00

8

20

09

2

01

0

2011

2

01

2

20

13

2

01

4

20

15

2

01

6

Ag

e I

nter

val

Inte

rval

IQ

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10)

(1

1)

(12)

(1

3)

20

02

-

--

--

-60

8 -

--

-13

%-1

4%

20

03

-

--

--

--

--

--

12%

-13%

20

04

-

--

--

--

--

--

11%

-12%

20

05

-

--

--

--

(5l

--

60

10

%-1

1%

20

06

-

--

--

--

6a

--

-9%

-10%

fl

20

07

-

--

--

--

--

-(5

) 8%

-9%

20

08

-

--

--

--

--

6 7%

-8%

20

09

-

--

--

--

--

6%-7

%

20

10

-

--

-(1

2l

--

-5%

-6%

2011

-

--

-22

8 -

-4%

-5%

z 2

01

2

--

(19

l -

-10

3%

-4%

(D

20

13

2%

-3%

:t:

--

--

-c.

.. (1

02

t (D

2

01

4

--

(121

) 1%

-2%

iil

(D

2

01

5

%-1

%

'<

--

-)>

2

01

6

0-%

3

-Ql o·

0

§1

T

ota

l -

--

--

-60

(3

0)

22

(102

) (5

0)

~~

(D

Dl

3-

0-

Ql a

Tra

nsf

er

Affe

ctin

g E

xpos

ures

at

Beg

inni

ng o

f Ye

ar

Ql ()

b

Tra

nsf

er A

ffec

ting

Exp

osur

es a

t E

nd o

f Ye

ar

c...

,O

......

' c

Sal

e w

ith C

ontin

ued

Use

N

~

0 D

l P

aren

thes

es D

enot

e C

redi

t Am

ount

. .....

. -0

)

Ql

In Schedule 2, other transactions which affect the group are recorded in a similar

manner. The entries illustrated include transfers and sales. The entries which are credits

to the plant account are shown in parentheses. The items recorded on this schedule are

not totaled with the retirements, but are used in developing the exposures at the beginning

of each age interval.

Schedule of Plant Exposed to Retirement

The development of the amount of plant exposed to retirement at the beginning of

each age interval is illustrated in Schedule 3 on page 11-14.

The surviving plant at the beginning of each year from 2007 through 2016 is

recorded by year in the portion of the table headed "Annual Survivors at the Beginning of

the Year." The last amount entered in each column is the amount of new plant added to

the group during the year. The amounts entered in Schedule 3 for each successive year

following the beginning balance or addition are obtained by adding or subtracting the net

entries shown on Schedules 1 and 2. For the purpose of determining the plant exposed

to retirement, transfers-in are considered as being exposed to retirement in this group at

the beginning of the year in which they occurred, and the sales and transfers-out are

considered to be removed from the plant exposed to retirement at the beginning of the

following year. Thus, the amounts of plant shown at the beginning of each year are the

amounts of plant from each placement year considered to be exposed to retirement at

the beginning of each successive transaction year. For example, the exposures for the

installation year 2012 are calculated in the following manner:

Exposures at age O = amount of addition Exposures at age% = $750,000 - $ 8,000 Exposures at age 1% = $742,000 - $18,000 Exposures at age 2% = $724,000 - $20,000 - $19,000 Exposures at age 3% = $685,000 - $22,000

= $750,000 = $742,000 = $724,000 = $685,000 = $663,000

~ 6annettFleming 11-13 New Jersey American Water Co - Water December 31, 2016

[8

i S

CH

ED

ULE

3.

PLA

NT

EX

PO

SE

D T

O R

ET

IRE

ME

NT

JA

NU

AR

Y 1

OF

EA

CH

YE

AR

200

7-20

16

5 S

UM

MA

RIZ

ED

BY

AG

E I

NT

ER

VA

L l'D

I"

"; '1

I Exp

erie

nce

Ban

d 20

07-2

016

Pla

cem

ent

Ban

d 20

02-2

016

rr 3 E

xpos

ures

, T

hous

ands

of D

olla

rs

Tot

al a

t 5·

Ye

ar

Ann

ual

Sur

vivo

rs a

t the

Beg

inni

ng o

f the

Ye

ar

Beg

inni

ng o

f A

ge

~

Pla

ced

2007

20

08

2009

20

10

2011

20

12

2013

20

14

2015

20

16

Age

Int

erva

l In

terv

al

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10)

(1

1)

(12)

(1

3)

2002

25

5 24

5 23

4 22

2 20

9 19

5 23

9 21

6 19

2 16

7 16

7 13

Yz-

14Y

z 20

03

279

268

256

243

228

212

194

174

153

131

323

12Y

z-13

Yz

2004

30

7 29

6 28

4 27

1 25

7 24

1 22

4 20

5 18

4 16

2 53

1 11

Yz-

12Y

z 20

05

338

330

321

311

300

289

276

262

242

226

823

10Y

z-11

Yz

i I 20

06

376

367

357

346

334

321

307

297

280

261

1,09

7 9Y

z-10

Yz

2007

42

0a

416

407

397

386

374

361

347

332

316

1,50

3 8Y

z-9Y

z 20

08

460a

45

5 44

4 43

2 41

9 40

5 39

0 37

4 35

6 1,

952

7Yz-8

Yz

2009

51

0a

504

492

479

464

448

431

412

2,46

3 6Y

z-7Y

z 20

10

580a

57

4 56

1 54

6 53

0 50

1 48

2 3,

057

5Yz-

6Yz

z (l)

2011

66

0a

653

639

623

628

609

3,78

9 4Y

z-5Y

z :E

(_

2012

75

0a

742

724

4,33

2 3Y

z-4Y

z (l

) 68

5 66

3 -,

en

(l

)

2013

85

0a

841

821

799

4,95

5 2Y

z-3Yz

'<

)>

3

2014

96

0a

949

926

5,71

9 1 Y

z-2Y

z (l

) :::

!. ()

2015

1,

080a

1,

069

6,57

9 Yz

-1 Yz

0

~

~ ~

2016

1,

220a

7,

490

0-Yz

(l

) Il

l 3

.....

C" ~

(l)

0 ;

<; I T

otal

1,

975

2,38

2 2,

824

3,31

8 3,

872

4,49

4 5,

247

6,01

7 6,

852

7,79

9 _

44

,78

0

N~

Olll

ml

I 8A

dditi

ons

durin

g th

e ye

ar

For the entire experience band 2007-2016, the total exposures at the beginning of

an age interval are obtained by summing diagonally in a manner similar to the summing

of the retirements during an age interval (Schedule 1 ). For example, the figure of 3,789,

shown as the total exposures at the beginning of age interval 4%-5%, is obtained by

summing:

255 + 268 + 284 + 311 + 334 + 374 + 405 + 448 + 501 + 609.

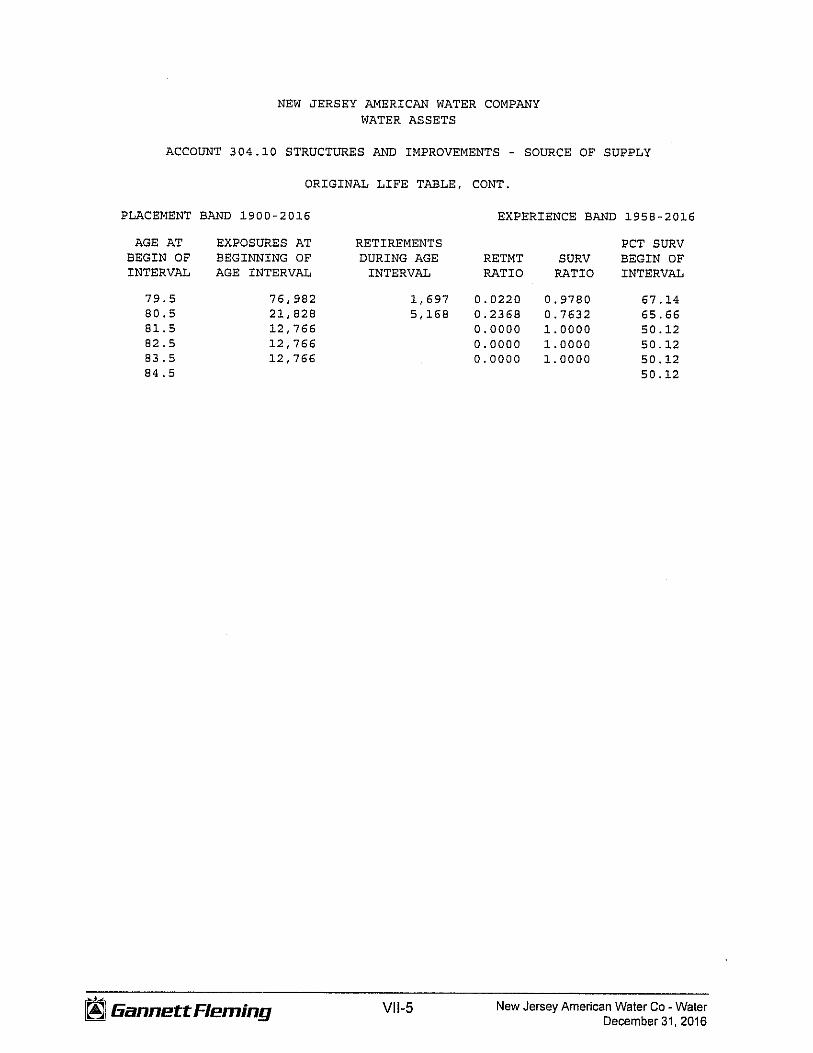

Original Life Table

The original life table, illustrated in Schedule 4 on page 11-16, is developed from

the totals shown on the schedules of retirements and exposures, Schedules 1 and 3,

respectively. The exposures at the beginning of the age interval are obtained from the

corresponding age interval of the exposure schedule, and the retirements during the age

interval are obtained from the corresponding age interval of the retirement schedule. The

retirement ratio is the result of dividing the retirements during the age interval by the

exposures at the beginning of the age interval. The percent surviving at the beginning of

each age interval is derived from survivor ratios, each of which equals one minus the

retirement ratio. The percent surviving is developed by starting with 100% at age zero

and successively multiplying the percent surviving at the beginning of each interval by the

survivor ratio, i.e., one minus the retirement ratio for that age interval. The calculations

necessary to determine the percent surviving at age 5% are as follows:

Percent surviving at age 4% = 88.15 Exposures at age 4% = 3,789,000 Retirements from age 4% to 5% = 143,000 Retirement Ratio = 143,000 + 3,789,000 = 0.0377 Survivor Ratio = 1.000 - 0.0377 = 0.9623 Percent surviving at age 5% = (88.15) X (0.9623) = 84.83

The totals of the exposures and retirements (columns 2 and 3) are shown for the

purpose of checking with the respective totals in Schedules 1 and 3. The ratio of the total

retirements to the total exposures, other than for each age interval, is meaningless.

~ liannett Fleming 11-15 New Jersey American Water Co - Water December 31, 2016

SCHEDULE 4. ORIGINAL LIFE TABLE CALCULATED BY THE RETIREMENT RATE METHOD

Experience Band 2007-2016 Placement Band 2002-2016

(Exposure and Retirement Amounts are in Thousands of Dollars)

Age at Exposures at Retirements Beginning of Beginning of During Age Retirement Survivor

Interval Age Interval Interval Ratio Ratio

(1) (2) (3) (4) (5)

0.0 7,490 80 0.0107 0.9893 0.5 6,579 153 0.0233 0.9767 1.5 5,719 151 0.0264 0.9736 2.5 4,955 150 0.0303 0.9697 3.5 4,332 146 0.0337 0.9663 4.5 3,789 143 0.0377 0.9623 5.5 3,057 131 0.0429 0.9571 6.5 2,463 124 0.0503 0.9497 7.5 1,952 113 0.0579 0.9421 8.5 1,503 105 0.0699 0.9301 9.5 1,097 93 0.0848 0.9152

10.5 823 83 0.1009 0.8991 11.5 531 64 0.1205 0.8795 12.5 323 44 0.1362 0.8638 13.5 167 ~ 0.1557 0.8443

Total 44,780 1.606

Column 2 from Schedule 3. Column 12. Plant Exposed to Retirement. Column 3 from Schedule 1, Column 12, Retirements for Each Year. Column 4 = Column 3 Divided by Column 2. Column 5 = 1.0000 Minus Column 4.

Percent Surviving at Beginning of Age Interval

(6)

100.00 98.93 96.62 94.07 91.22 88.15 84.83 81.19 77.11 72.65 67.57 61.84 55.60 48.90 42.24 35.66

Column 6 = Column 5 Multiplied by Column 6 as of the Preceding Age Interval.

~ tiannett Fleming 11-16 New Jersey American Water Co - Water December 31, 2016

The original survivor curve is plotted from the original life table (column 6, Schedule

4). When the curve terminates at a percent surviving greater than zero, it is called a stub

survivor curve. Survivor curves developed from retirement rate studies generally are stub

curves.

Smoothing the Original Survivor Curve

The smoothing of the original survivor curve eliminates any irregularities and

serves as the basis for the preliminary extrapolation to zero percent surviving of the

original stub curve. Even if the original survivor curve is complete from 100% to zero

percent, it is desirable to eliminate any irregularities, as there is still an extrapolation for

the vintages which have not yet lived to the age at which the curve reaches zero percent.

In this study, the smoothing of the original curve with established type curves was used

to eliminate irregularities in the original curve.

The Iowa type curves are used in this study to smooth those original stub curves

which are expressed as percents surviving at ages in years. Each original survivor curve

was compared to the Iowa curves using visual and mathematical matching in order to

determine the better fitting smooth curves. In Figures 6, 7, and 8, the original curve

developed in Schedule 4 is compared with the L, S, and R Iowa type curves which most

nearly fit the original survivor curve. In Figure 6, the L 1 curve with an average life between

12 and 13 years appears to be the best fit. In Figure 7, the SO type curve with a 12-year

average life appears to be the best fit and appears to be better than the L 1 fitting. In

Figure 8, the R1 type curve with a 12-year average life appears to be the best fit and

appears to be better than either the L 1 or the SO.

In Figure 9, the three fittings, 12-L 1, 12-SO and 12-R 1 are drawn for comparison

purposes. It is probable that the 12-R 1 Iowa curve would be selected as the most

representative of the plotted survivor characteristics of the group.

~ Gannett Fleming 11-17 New Jersey American Water Co - Water December 31, 2016

w

~ ~ l"f, l! ~ 5· U::3 ~, I z CD

::E L

. CD

in CD

'<

)>

3 CD

:::

i. n 0

gi CD

gi

3 ....

O

" !l;

!l;

()

c..

,O

->.

I

is.,

~

Olll

........

(J

) !l;

FIG

UR

E

6.

ILL

US

TR

AT

ION

O

F TH

E M

AT

CH

ING

O

F A

N

OR

IGIN

AL

SU

RV

IVO

R

CU

RV

E W

ITH

A

N

Ll

IOW

A

TY

PE

CU

RV

E O

RIG

INA

L

AN

D

SMO

OTH

SU

RV

IVO

R

CU

RV

ES

(!J

z >

>

0:: :::>

en

I- z w

(.)

0:: w

a.

100

~

2007

-201

6 E

XP

ER

IEN

CE

: O

RIG

INAL

CU

RV

E•

2002

-201

6 P

LA

CE

ME

NT

S

90+--~~~~1--~~~--i~~~~--+~~~~-+~~~~-+-~~~~-1-~~~~-1--~~~~+-~~~---i

80

-1

--~

~~

~t--"r~

,--~

--1

,---~

~~

--t~

~~

~--1

-~

~~

~--1

-~

~~

~-t-~

~~

~-i--~

~~

~-t--~

~~

---1

70

60

50

40

5 10

15

20

25

A

GE

IN

YE

AR

S

30

35

40

45

re

~ ~ l'D ~ ;c ~ 5· LO ~I

zl

~ c;_

CD .., (J

) ~

)>

3 CD 5·

otl

) CD

::J

@i

3 (D

0

-..

,

~o

(,

.)

0 _

,.

I

~i

0) C

D ..,

FIG

UR

E

7.

ILL

US

TR

AT

ION

O

F TH

E M

ATC

HIN

G

OF

AN

O

RIG

INA

L

SUR

VIV

OR

C

UR

VE

WIT

H

AN

SO

IO

WA

T

YPE

C

UR

VE

OR

IGIN

AL

A

ND

SM

OO

TH

SUR

VIV

OR

C

UR

VES

C, z > >

a:

:::,

(/J I- z w

(.) a:

w

a.

20

07

-20

16

EX

PE

RIE

NC

E:

10

0--

=--

---r

----

--ir

---,

----

1--

--l-

---1

1~

;~~

;;:~

:~~

~~

~~

~

OR

IGIN

AL

CU

RV

E •

20

02

-20

16

PL

AC

EM

EN

TS

90+

----

--l~

l---

----

lrl"

"l""

tT"l

ll"'M

<,.

..-:

:;""

"'li.

.,..

..,,

..--

--+

----

-+--

----

+--

----

+--

---+

----

---l

80

-1--

----

-,t-

--a ....

.... 'r

------t,-...-----+

------r-----+

------+

------1

------+

-------1

5 10

15

20

25

A

GE

IN

YE

AR

S

30

35

40

45

i1 5 l'D ""' ""' :t! ~ s· LO ~I

I z CD

:!::

c..

. CD

in CD

'<

)>

3 !ll o·

o§

CD

@~

3

-C

T

!]l

!ll ()

c.

vO

..... '

~~

Oll

l .....

-0

) !ll

FIG

UR

E

8.

ILL

US

TR

AT

ION

O

F TH

E M

ATC

HIN

G

OF

AN

O

RIG

INA

L

SUR

VIV

OR

C

UR

VE

WIT

H

AN

R

l IO

WA

T

YPE

C

UR

VE

OR

IGIN

AL

A

ND

SM

OO

TH

SUR

VIV

OR

C

UR

VE

S

(!J z > >

a::

:::,

Cl) I- z w

CJ

a::

UJ

a. 1

00

----

----

----

----

----

----

--.-

----

-.--

----

-,--

~~

~~

~~

~~

~~

~~

~--

.,

OR

IGIN

AL

CU

RV

E•

2007

-201

6 E

XP

ER

IEN

CE

: 20

02-2

016

PLA

CE

ME

NT

S

90

+----~

~1

-------l------+

-----t------+

------+

------1

------+

------1

so-1

----

--1-

-....

,,....

,,__-

---!

-........

----

+--

---+

----

-+--

----

+--

----

+--

---+

----

~

70

60

50

5 10

15

20

25

A

GE

IN

YE

AR

S

30

35

40

45

g, s I'll

l"'ti

l"'ti :tl ~ 5· IQ

~I

zl

CD

:if

(_

CD cil CD

'<

)>

3 ~ o·

oil)

CD

::J

g~

3

.....

C'"

CD

CD

,

,0

c,

.)

0 ....

' ~~

Oll

l mm

,

FIG

UR

E

9.

ILL

US

TR

AT

ION

O

F TH

E M

ATC

HIN

G

OF

AN

O

RIG

INA

L

SUR

VIV

OR

C

UR

VE

WIT

H

AN

L

l,

SO

AN

D

Rl

IOW

A

TY

PE

CU

RV

E O

RIG

INA

L

AN

D

SMO

OTH

SU

RV

IVO

R

CU

RV

ES

C, z > >

a:

:::, en

I- z w

()

a:

w

a.

10

0-:::::-----,------,.-----,-----r------,------,-,---------------,

5 10

15

20

25

A

GE

IN

YE

AR

S

30

2007

-201

6 E

XP

ER

IEN

CE

: O

RIG

INA

L C

UR

VE •

20

02-2

016

PLA

CE

ME

NTS

35

40

45

PART Ill. SERVICE LIFE CONSIDERATIONS

~ EiannettF/eming 111-1 New Jersey American Water Co - Water December 31, 2016

PART Ill. SERVICE LIFE CONSIDERATIONS

FIELD TRIPS

In order to be familiar with the operation of the Company and observe

representative portions of the plant, field trips were conducted for the study. A general

understanding of the function of the plant and information with respect to the reasons for

past retirements and the expected future causes of retirements are obtained during field

trips. This knowledge and information were incorporated in the interpretation and

extrapolation of the statistical analyses.

The following is a list of the locations visited during the recent field trips.

June 28, 2017 Delaware River Water Treatment Plant Delaware River Pump Station and Reservoir Mansfield Treatment Plant Homestead Water Treatment Plant Homestead Wastewater Treatment Plant

June 16. 2017 Canoe Brook Water Treatment Plant Raritan Millstone Water Treatment Plant Canal Road Water Treatment Plant EDC Wastewater Treatment Plant Pump Station #206 Schley Pump Station

Service Life Analysis

The service life estimates were based on judgment which considered a number of

factors. The primary factors were the statistical analyses of data; current company

policies and outlook as determined during field reviews of the property and other

conversations with management; and the survivor curve estimates from previous studies

of this company and other water companies.

liannett Fleming 111-2 New Jersey American Water Co - Water December 31, 2016

For most of the mass plant accounts and subaccounts, the statistical analyses

resulted in good to excellent indications of significant survivor patterns. These accounts

represent 91 percent of depreciable plant. Generally, the information external to the

statistics led to no significant departure from the indicated survivor curves for the accounts

listed below.

Account No.

304.10 304.20 304.20 304.30 304.30 304.50 304.60 304.70 304.80 306.00 307.00 309.00 310.00 311.20 311.30 311.40 311.50 320.10 320.10 320.20 330.00 331.01 331.10 331.20 331.30 331.40 333.00 334.10 335.00 341.10 341.20 341.40 345.00

Account Description Structures and Improvements - Source of Supply Structures and Improvements - Pumping - Major Structures and Improvements - Pumping - Other Structures and Improvements - Treatment - Major Structures and Improvements - Treatment - Other Structures and Improvements - General Structures and Improvements - Office Buildings Structures and Improvements - Stores, Shops and Garage Buildings Structures and Improvements - Miscellaneous Lake, River and Other Intakes Wells and Springs Supply Mains Power Generation Equipment Pumping Equipment - Electrical Pumping Equipment - Diesel Pumping Equipment - Hydraulic Pumping Equipment - Other Water Treatment Equipment - Non-Media Water Treatment Equipment - Other Water Treatment Equipment - Filter Media Distribution Reservoirs and Standpipes Mains - Other Mains - 4 Inch and Less Mains - 6 Inch to 8 Inch Mains -10 Inch to 16 Inch Mains - 18 Inch and Greater Services Meters Hydrants Transportation Equipment - Light Duty Trucks Transportation Equipment - Heavy Duty Trucks Transportation Equipment - Other Power Operated Equipment

~ 6annettFleming 111-3 New Jersey American Water Co - Water December 31, 2016

The combined Accounts 331.01 through 331.4, Mains, is used to illustrate the

manner in which the study was conducted for the accounts in the preceding list. Aged

plant accounting data have been compiled for the years through 2016. These data have

been coded according to account or property group, type of transaction, year in which the

transaction took place, and year in which the utility plant was placed in service. The

retirements, other plant transactions and plant additions were analyzed by the retirement

rate method.

The survivor curve estimate for this account is the 120-R2.5 and is based on the

statistical indication for the period 1958-2016. The 120-R2.5 is an excellent fit of the

significant portion of the original survivor curve as set forth on page Vll-111, is consistent

with management outlook for a continuation of the historical experience and is at the

upper end of the typical service life range of 75 to 120 years for water mains.

Amortization accounting is proposed for certain General Plant accounts that

represent numerous units of property, but a small portion of the depreciable plant in

service. These accounts represent approximately 5 percent of total utility plant. A

discussion of the basis for the amortization periods is presented in the section

"Calculation of Annual and Accrued Amortization".

Generally, the estimates for the remaining accounts of the total depreciable plant

in service were based on judgments which considered the nature of the plant and

equipment, the previous estimate for this company and a general knowledge of service

lives for similar equipment in other water companies.

~ 6annettF/eming 111-4 New Jersey American Water Co - Water December 31, 2016

PART IV. NET SALVAGE CONSIDERATIONS

Gannett Fleming IV-1 New Jersey American Water Co - Water December 31, 2016

PART IV. NET SALVAGE CONSIDERATIONS

NET SALVAGE NORMALIZATION

The estimates of net salvage by account were based on historical data compiled

from 2014 through 2016. Cost of removal and gross salvage by account were averaged

over the 3-year period and included by account as the total amount to be recovered. In

cases in which removal costs are expected to exceed salvage receipts, a negative net

salvage amount is estimated which is added to the annual depreciation amount to achieve

the total annual depreciation amount by account.

Although this method is not considered appropriate for full service value recovery,

the Company has previously agreed to use the historical normalized experience of net

salvage. The utilization of this method is inconsistent with sound depreciation practices.

The analyses of historical cost of removal and salvage data are presented by plant

account on Table 2, pages Vl-7 and Vl-8.

~ Gannett Fleming IV-2 New Jersey American Water Co - Water December 31, 2016

6annettFleming

PART V. CALCULATION OF ANNUAL AND

ACCRUED DEPRECIATION

V-1 New Jersey American Water Co - Water December 31, 2016

PART V. CALCULATION OF ANNUAL AND

ACCRUED DEPRECIATION

GROUP DEPRECIATION PROCEDURES

A group procedure for depreciation is appropriate when considering more than a

single item of property. Normally the items within a group do not have identical service

lives, but have lives that are dispersed over a range of time. There are two primary group

procedures, namely, average service life and equal life group. In the average service life

procedure, the rate of annual depreciation is based on the average life or average

remaining life of the group, and this rate is applied to the surviving balances of the group's

cost. A characteristic of this procedure is that the cost of plant retired prior to average life

is not fully recouped at the time of retirement, whereas the cost of plant retired subsequent

to average life is more than fully recouped. Over the entire life cycle, the portion of cost

not recouped prior to average life is balanced by the cost recouped subsequent to

average life.

Single Unit of Property

The calculation of straight line depreciation for a single unit of property is

straightforward. For example, if a $1,000 unit of property attains an age of four years

and has a life expectancy of six years, the annual accrual over the total life is:

$1,000 = $100 per year. (4 + 6)

The accrued depreciation is:

$1,000 (1 - 1~) = $400.

~ 6annettFleming V-2 New Jersey American Water Co - Water December 31, 2016

Group Depreciation Procedures

When more than a single item of property is under consideration, a group

procedure for depreciation is appropriate because normally all of the items within a group

do not have identical service lives, but have lives that are dispersed over a range of time.

There are two primary group procedures, namely, average service life and equal life

group.

Remaining Life Annual Accruals

For the purpose of calculating remaining life accruals as of December 31, 2016,

the depreciation reserve for each plant account is allocated among vintages in proportion

to the calculated accrued depreciation for the account. Explanations of remaining life

accruals and calculated accrued depreciation follow. The detailed calculations as of

December 31, 2016, are set forth in the Results of Study section of the report.

Average Service Life Procedure

In the average service life procedure, the remaining life annual accrual for each

vintage is determined by dividing future book accruals (original cost less book reserve)

by the average remaining life of the vintage. The average remaining life is a directly

weighted average derived from the estimated future survivor curve in accordance with the

average service life procedure.

The calculated accrued depreciation for each depreciable property group

represents that portion of the depreciable cost of the group which would not be allocated

to expense through future depreciation accruals, if current forecasts of life characteristics

are used as the basis for such accruals. The accrued depreciation calculation consists

of applying an appropriate ratio to the surviving original cost of each vintage of each

Gannett Fleming V-3 New Jersey American Water Co - Water December 31, 2016

account, based upon the attained age and service life. The straight line accrued

depreciation ratios are calculated as follows for the average service life procedure:

Ratio = 1 _ Average Remaining Life Average Service Life

CALCULATION OF ANNUAL AND ACCRUED AMORTIZATION

Amortization is the gradual extinguishment of an amount in an account by

distributing such amount over a fixed period, over the life of the asset or liability to which

it applies, or over the period during which it is anticipated the benefit will be realized.

Normally, the distribution of the amount is in equal amounts to each year of the

amortization period.

The calculation of annual and accrued amortization requires the selection of an

amortization period. The amortization periods used in this report were based on judgment

which incorporated a consideration of the period during which the assets will render most

of their service, the amortization period and service lives used by other utilities, and the

service life estimates previously used for the asset under depreciation accounting.

Amortization accounting is proposed for certain General Plant accounts that

represent numerous units of property, but a very small portion of depreciable utility plant

in service. The accounts and their amortization periods are as follows:

6annettF/eming V-4 New Jersey American Water Co - Water December 31, 2016

340.10 340.20 340.30 340.31 340.40 340.50 342.00 343.00 344.00 346.00 347.00 348.00

Account

Office Furniture Computers and Peripheral Equipment Computer Software Computer Software - Mainframe Data Handling Equipment Other Office Equipment Stores Equipment Tools, Shop and Garage Equipment Laboratory Equipment Communication Equipment Miscellaneous Equipment Other Tangible Equipment

Amortization Period, Years

20 5

10 8

10 15 25 25 20 15 25 25

The calculated accrued amortization is equal to the original cost multiplied by the

ratio of the vintage's age to its amortization period. The annual amortization amount is

determined by dividing the original cost by the period of amortization for the account.

~ liannett Fleming V-5 New Jersey American Water Co - Water December 31, 2016

6annettFJeming

PART VI. RESULTS OF STUDY

Vl-1 New Jersey American Water Co - Water December 31, 2016

PART VI. RESULTS OF STUDY

QUALIFICATION OF RESULTS

The calculated annual and accrued depreciation are the principal results of the

study. Continued surveillance and periodic revisions are normally required to maintain

continued use of appropriate annual depreciation accrual rates. An assumption that

accrual rates can remain unchanged over a long period of time implies a disregard for the

inherent variability in service lives and salvage and for the change of the composition of

property in service. The annual accrual rates were calculated in accordance with the

straight line remaining life method of depreciation, using the average service life

procedure based on estimates which reflect considerations of current historical evidence

and expected future conditions.

The annual depreciation accrual rates are applicable specifically to the water plant

in service as of December 31, 2016. For most plant accounts, the application of such

rates to future balances that reflect additions subsequent to December 31, 2016, is

reasonable for a period of three to five years.

DESCRIPTION OF DETAILED TABULATIONS

Summary schedules of the results of the study, as applied to the original cost of

water plant in service as of December 31, 2016, are presented on pages Vl-4 through VI

S of this report. The schedules set forth the original cost, the book depreciation reserve,

future accruals, the calculated annual depreciation rate and amount, and the composite

remaining life related to water plant. Table 1 sets forth the total annual depreciation

accrual rates for water plant assets as of December 31, 2016. Table 2 sefs forth the net

salvage normalization amounts by account based on the period 2014 through 2016.

~ 6annettF/eming Vl-2 New Jersey American Water Co - Water December 31, 2016

The service life estimates were based on judgment that incorporated statistical

analysis of retirement data, discussions with management and consideration of estimates

made for other water utilities. The results of the statistical analysis of service life are

presented in the section beginning on page Vll-2, within the supporting documents of this

report.

For each depreciable group analyzed by the retirement rate method, a chart

depicting the original and estimated survivor curves is followed by a tabular presentation

of the original life table(s) plotted on the chart. The survivor curves estimated for the

depreciable groups are shown as dark smooth curves on the charts. Each smooth

survivor curve is denoted by a numeral followed by the curve type designation. The

numeral used is the average life derived from the entire curve from 100 percent to zero

percent surviving. The titles of the chart indicate the group, the symbol used to plot the

points of the original life table, and the experience and placement bands of the life tables

which where plotted. The experience band indicates the range of years for which

retirements were used to develop the stub survivor curve. The placements indicate, for

the related experience band, the range of years of installations which appear in the

experience.

The tables of the calculated annual depreciation applicable to depreciable assets

as of December 31, 2016 are presented in account sequence starting·on page Vlll-2 of

the supporting documents. The tables indicate the estimated survivor curve for the

account and set forth, for each installation year, the original cost, the calculated accrued

depreciation, the allocated book reserve, future accruals, the remaining life, and the

calculated annual accrual amount.

~ Gannett Fleming Vl-3 New Jersey American Water Co - Water December 31, 2016

w

ij l""t,

l""t, ll ~ 5· lCj <

.h z ~ c

_

CD cil CD

'<

)>

3 CD ~l

0 :J

~ :§:

CD

Il

l 3

ro C

T -,

CD

()

-,

0 ~. N

:§:

Olll

en~

DE

PR

EC

IAB

LE

GR

OU

P

(1)

INT

AN

GIB

LE

PL

AN

T

30

1.0

0

30

2.0

0

OR

GA

NIZ

AT

ION

F

RA

NC

HIS

ES

AN

D C

ON

SE

NT

S

TO

TA

L IN

TA

NG

IBL

E P

LA

NT

NO

ND

EP

RE

CIA

BL

E P

LA

NT

LAN

D A

ND

LA

ND

RIG

HT

S

303.

20

SU

PP

LY

30

3.30

P

UM

PIN

G

303.

40

TR

EA

TM

EN

T

303.

50

TR

AN

SM

ISS

ION

AN

D D

IST

RIB

UT

ION

3

03

.60

G

EN

ER

AL

TO

TA

L N

ON

DE

PR

EC

IAB

LE

PL

AN

T

DE

PR

EC

IAB

LE

PL

AN

T

ST

RU

CT

UR

ES

AN

D I

MP

RO

VE

ME

NT

S

304.

10

SO

UR

CE

OF

SU

PP

LY

ST

RU

CT

UR

ES

304.

20

PU

MP

ING

ST

RU

CT

UR

ES

30

4.3

0

304.

40

304.

50

304.

60

30

4.7

0

30

4.8

0

30

5.0

0

30

6.0

0

30

7.0

0

30

8.0

0

30

9.0

0

31

0.0

0

31

0.2

0

DE

LA

WA

RE

RIV

ER

RE

GIO

NA

L S

WIM

MIN

G R

IVE

R

CA

NO

E B

RO

OK

C

AN

AL

RO

AD

R

AR

ITA

N M

ILL

ST

ON

E

OT

HE

R

TO

TA

L P

UM

PIN

G

TR

EA

TM

EN

T S

TR

UC

TU

RE

S

DE

LA

WA

RE

RIV

ER

RE

GIO

NA

L S

WIM

MIN

G R

IVE

R

JUM

PIN

G B

RO

OK

C

AN

OE

BR

OO

K

CA

NA

L R

OA

D

RA

RIT

AN

MIL

LST

ON

E

OT

HE

R

TO

TA

L T

RE

AT

ME

NT

TR

AN

SM

ISS

ION

AN

D D

IST

RIB

UT

ION

G

EN

ER

AL

O

FF

ICE

BU

ILD

ING

S

ST

OR

ES

, S

HO

P A

ND

GA

RA

GE

BU

ILD

ING

S

MIS

CE

LL

AN

EO

US

TO

TA

L S

TR

UC

TU

RE

S A

ND

IM

PR

OV

EM

EN

TS

CO

LL

EC

TIN

G A

ND

IM

PO

UN

DIN

G R

ES

ER

VO

IRS

LA

KE

, R

IVE

R A

ND

OT

HE

R I

NT

AK

ES

W

EL

LS

AN

D S

PR

ING

S

INF

ILT

RA

TIO

N G

AL

LE

RIE

S A

ND

TU

NN

ELS

S

UP

PL

Y M

AIN

S

PO

WE

R G

EN

ER

AT

ION

EQ

UIP

ME

NT

O

TH

ER

PO

WE

R G

EN

ER

AT

ION

EQ

UIP

ME

NT

NE

W J

ER

SE

Y A

ME

RIC

AN

WA

TE

R C

OM

PA

NY

W

AT

ER

AS

SE

TS

TA

BL

E 1

, S

UM

MA

RY

OF

ES

TIM

AT

ED

SU

RV

IVO

R C

UR

VE

S,

OR

IGIN

AL

CO

ST

, B

OO

K D

EP

RE

CIA

TIO

N R

ES

ER

VE

AN

D

CA

LC

UL

AT

ED

AN

NU

AL

DE

PR

EC

IAT

ION

AC

CR

UA

L R

AT

ES

AN

D N