2017 t. rowe price global economic outlook

TRANSCRIPT

GLOBAL ECONOMY

Alan Levenson

Chief U.S. Economist

November 17, 2016

2017 Global Market Outlook Press Briefing

2

48

50

52

54

56

58

2011 2012 2013 2014 2015 2016

Net

Pe

rce

nt

Inc

rea

sin

g

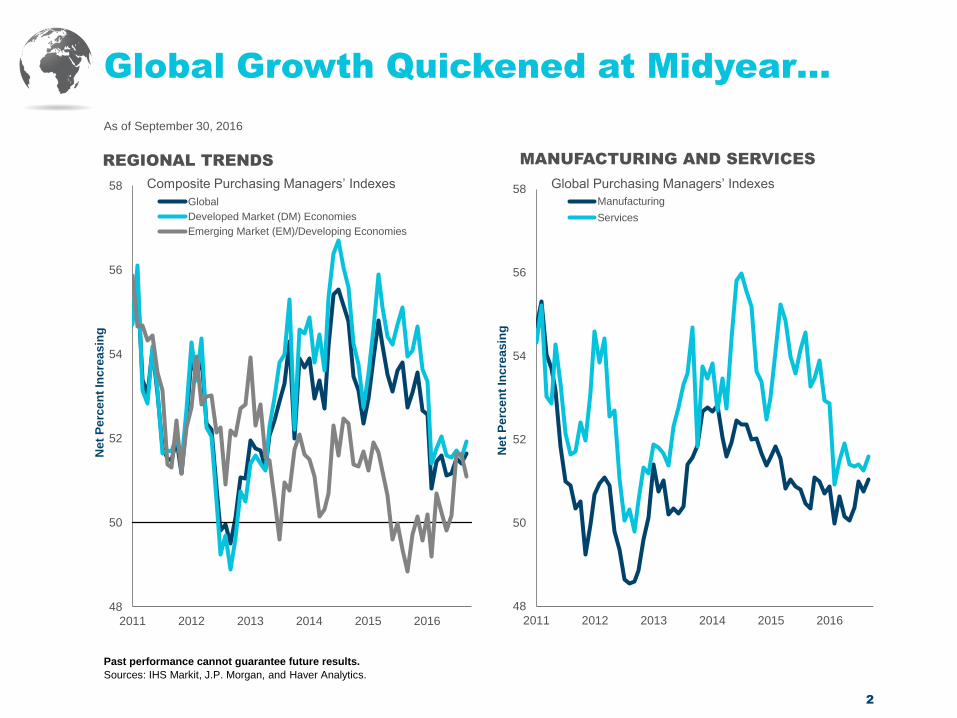

MANUFACTURING AND SERVICES

Manufacturing

Services

Global Purchasing Managers’ Indexes

As of September 30, 2016

Past performance cannot guarantee future results.

Sources: IHS Markit, J.P. Morgan, and Haver Analytics.

Global Growth Quickened at Midyear…

48

50

52

54

56

58

2011 2012 2013 2014 2015 2016

Net

Pe

rce

nt

Inc

rea

sin

g

REGIONAL TRENDS

Global

Developed Market (DM) Economies

Emerging Market (EM)/Developing Economies

Composite Purchasing Managers’ Indexes

3

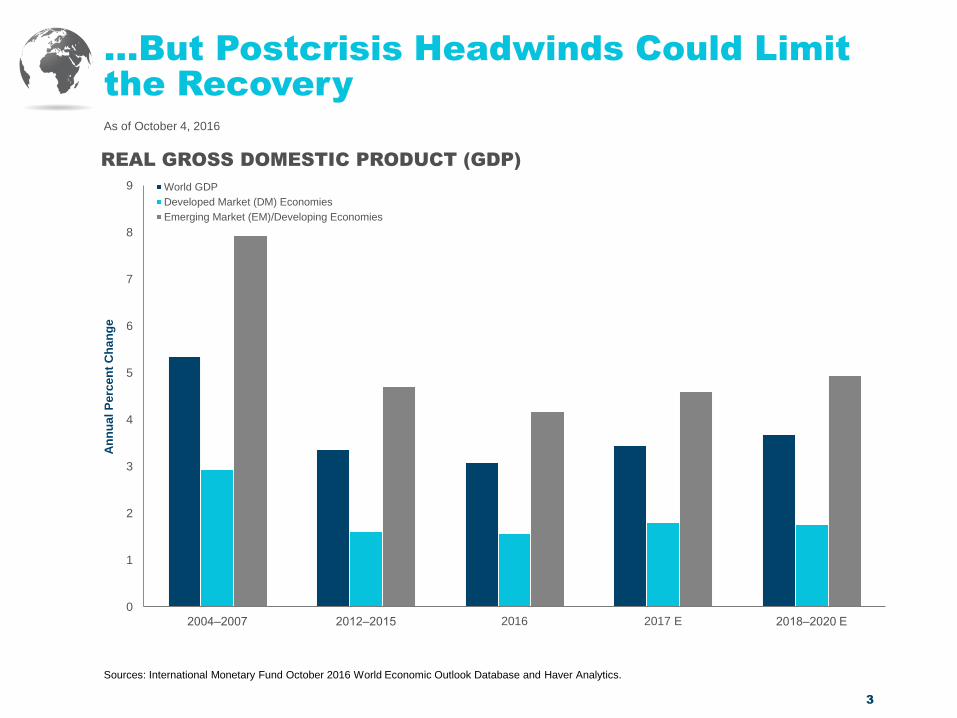

…But Postcrisis Headwinds Could Limit

the Recovery

0

1

2

3

4

5

6

7

8

9

2004‒2007 2012‒2015 2016 2017 E 2018‒2020 E

An

nu

al

Pe

rce

nt

Ch

an

ge

REAL GROSS DOMESTIC PRODUCT (GDP)

World GDP

Developed Market (DM) Economies

Emerging Market (EM)/Developing Economies

As of October 4, 2016

Sources: International Monetary Fund October 2016 World Economic Outlook Database and Haver Analytics.

4

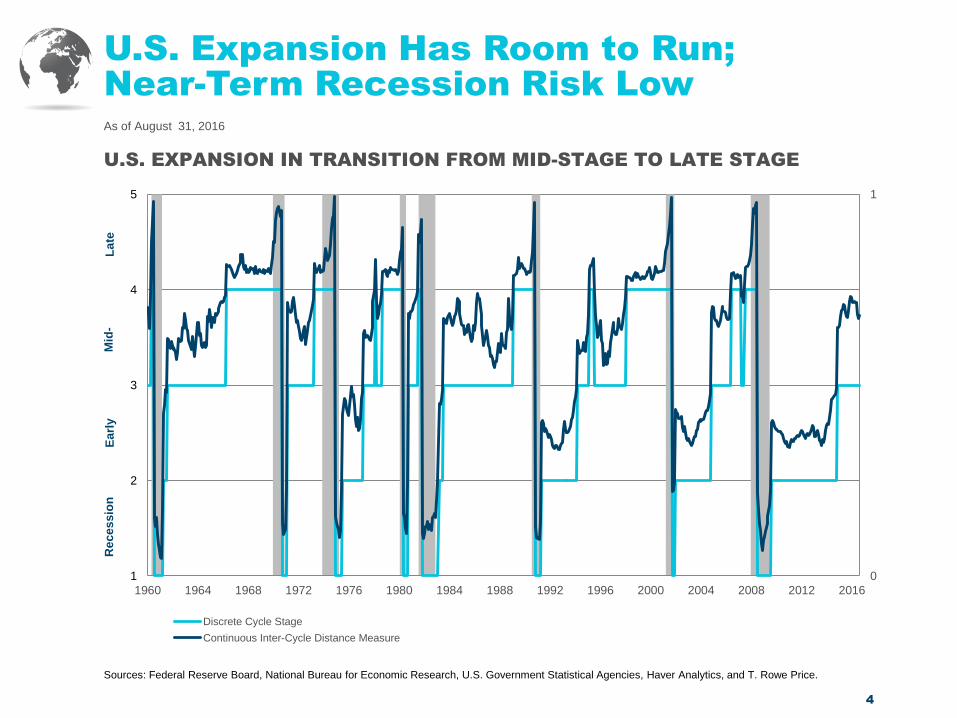

U.S. Expansion Has Room to Run;

Near-Term Recession Risk Low

As of August 31, 2016

Sources: Federal Reserve Board, National Bureau for Economic Research, U.S. Government Statistical Agencies, Haver Analytics, and T. Rowe Price.

0

1

1

2

3

4

5

1960 1964 1968 1972 1976 1980 1984 1988 1992 1996 2000 2004 2008 2012 2016

Discrete Cycle Stage

Continuous Inter-Cycle Distance Measure

Re

ce

ss

ion

E

arl

y

Mid

- L

ate

U.S. EXPANSION IN TRANSITION FROM MID-STAGE TO LATE STAGE

5

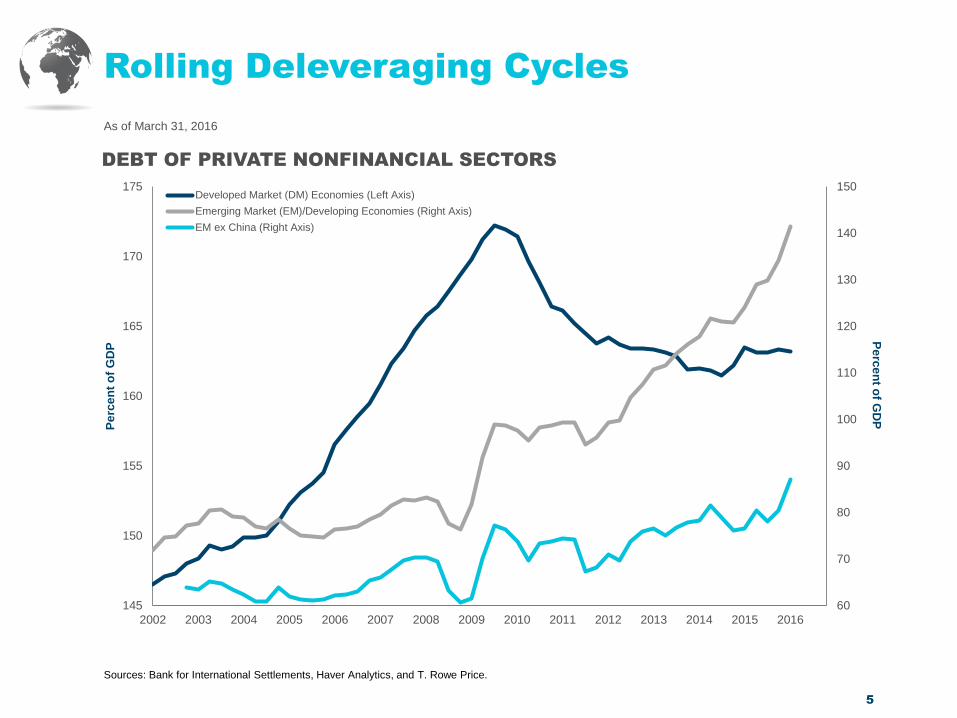

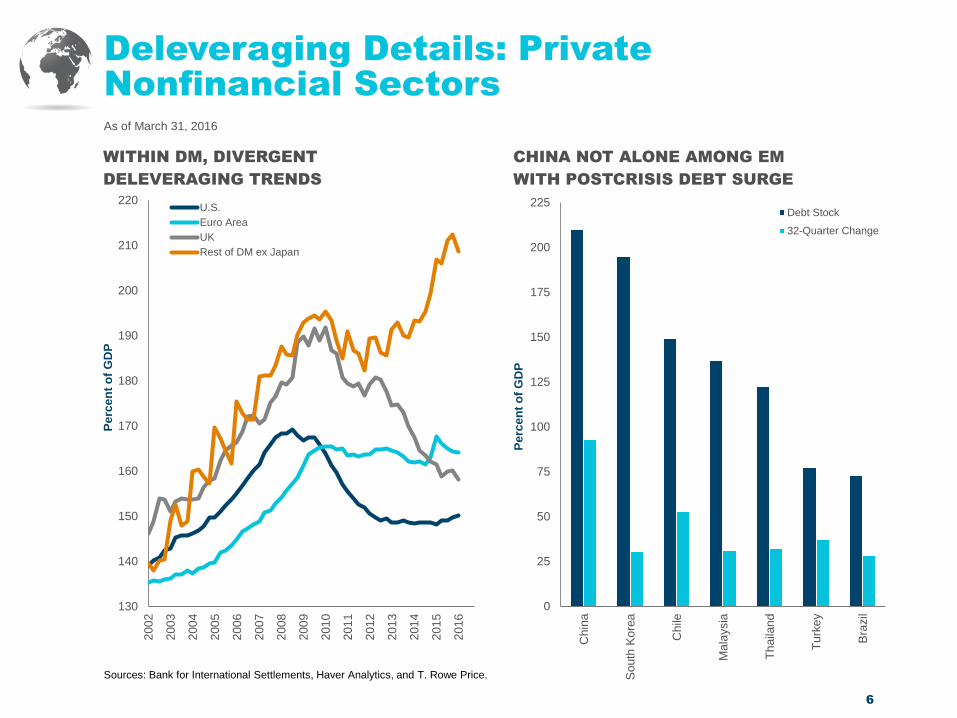

As of March 31, 2016

Sources: Bank for International Settlements, Haver Analytics, and T. Rowe Price.

Rolling Deleveraging Cycles

60

70

80

90

100

110

120

130

140

150

145

150

155

160

165

170

175

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Pe

rce

nt o

f GD

P P

erc

en

t o

f G

DP

DEBT OF PRIVATE NONFINANCIAL SECTORS

Developed Market (DM) Economies (Left Axis)

Emerging Market (EM)/Developing Economies (Right Axis)

EM ex China (Right Axis)

6

As of March 31, 2016

Sources: Bank for International Settlements, Haver Analytics, and T. Rowe Price.

Deleveraging Details: Private

Nonfinancial Sectors

130

140

150

160

170

180

190

200

210

220

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

Pe

rce

nt

of

GD

P

WITHIN DM, DIVERGENT

DELEVERAGING TRENDS

U.S.

Euro Area

UK

Rest of DM ex Japan

0

25

50

75

100

125

150

175

200

225

Ch

ina

So

uth

Ko

rea

Chile

Ma

laysia

Th

aila

nd

Tu

rke

y

Bra

zil

Pe

rce

nt

of

GD

P

CHINA NOT ALONE AMONG EM

WITH POSTCRISIS DEBT SURGE

Debt Stock

32-Quarter Change

7

0

2

4

6

8

10

12

14

16

18

20

2008 2009 2010 2011 2012 2013 2014 2015 2016

Pe

rce

nt

Ch

an

ge

, Y

ea

r A

go

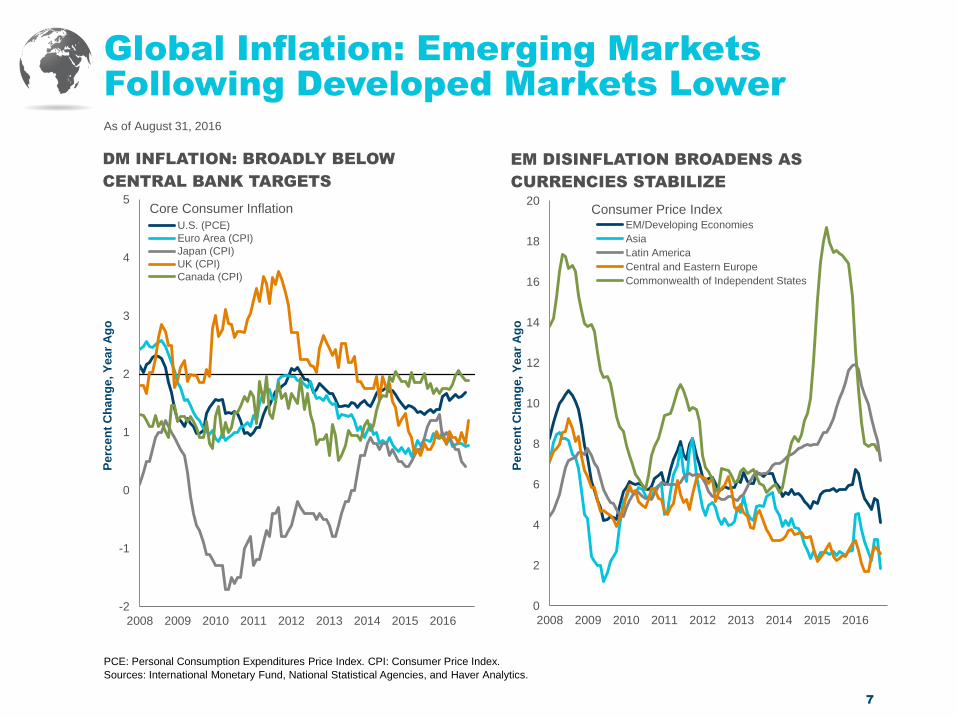

EM DISINFLATION BROADENS AS

CURRENCIES STABILIZE

EM/Developing Economies

Asia

Latin America

Central and Eastern Europe

Commonwealth of Independent States

Consumer Price Index

As of August 31, 2016

PCE: Personal Consumption Expenditures Price Index. CPI: Consumer Price Index.

Sources: International Monetary Fund, National Statistical Agencies, and Haver Analytics.

Global Inflation: Emerging Markets

Following Developed Markets Lower

-2

-1

0

1

2

3

4

5

2008 2009 2010 2011 2012 2013 2014 2015 2016

Pe

rce

nt

Ch

an

ge

, Y

ea

r A

go

DM INFLATION: BROADLY BELOW

CENTRAL BANK TARGETS

U.S. (PCE)

Euro Area (CPI)

Japan (CPI)

UK (CPI)

Canada (CPI)

Core Consumer Inflation

8

As of August 31, 2016

Sources: National Central Banks and Statistical Agencies, and Haver Analytics.

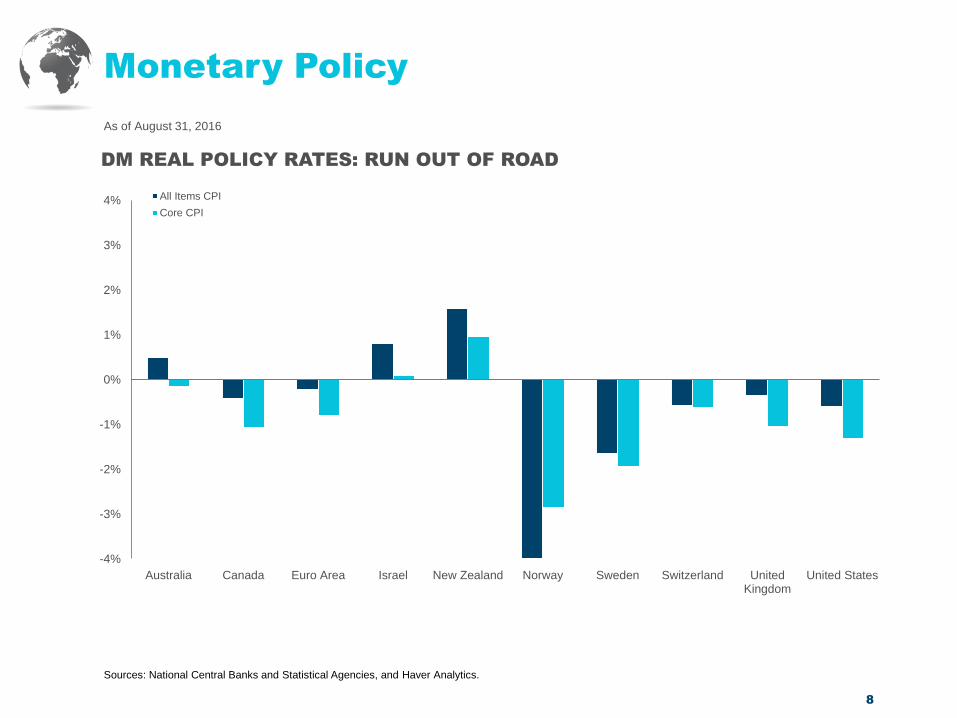

Monetary Policy

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

Australia Canada Euro Area Israel New Zealand Norway Sweden Switzerland UnitedKingdom

United States

DM REAL POLICY RATES: RUN OUT OF ROAD

All Items CPI

Core CPI

9

As of August 31, 2016

Sources: National Central Banks and Statistical Agencies, and Haver Analytics. Details available on request.

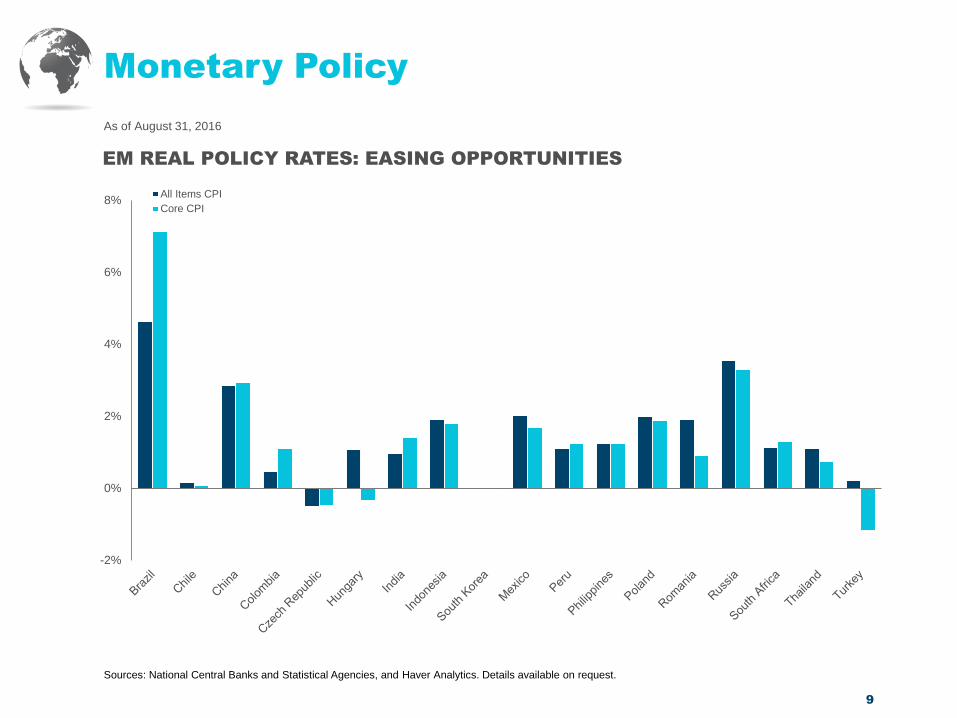

Monetary Policy

-2%

0%

2%

4%

6%

8%

EM REAL POLICY RATES: EASING OPPORTUNITIES

All Items CPI

Core CPI

10

As of October 4, 2016

Sources: International Monetary Fund October 2016 World Economic Outlook Database, Haver Analytics, and T. Rowe Price.

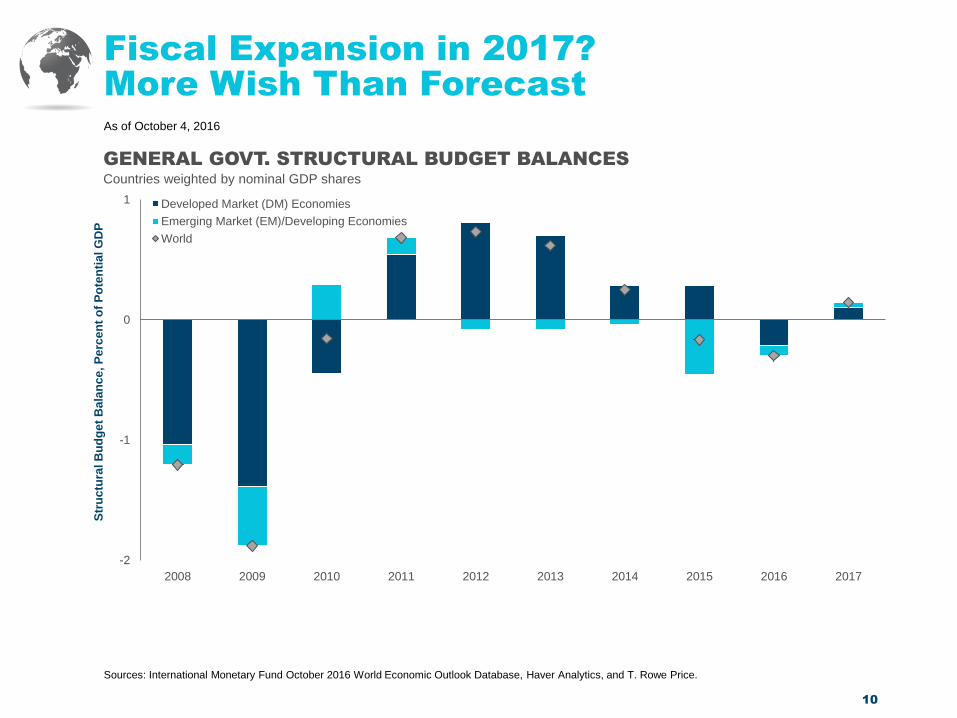

Fiscal Expansion in 2017?

More Wish Than Forecast

-2

-1

0

1

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Str

uc

tura

l B

ud

ge

t B

ala

nc

e, P

erc

en

t o

f P

ote

nti

al G

DP

GENERAL GOVT. STRUCTURAL BUDGET BALANCES

Countries weighted by nominal GDP shares

Developed Market (DM) Economies

Emerging Market (EM)/Developing Economies

World

11

Politics

ITALY: Constitutional referendum, December 4, 2016

U.S.: Continuing budget resolution expires December 9, 2016;

debt limit reinstated March 16, 2017

FRANCE: National elections, April‒May 2017

GERMANY: Federal elections, September 2017

CHINA: Communist Party Congress, autumn 2017

As of October 28, 2016

12

Global Outlook Summary

As of October 28, 2016

Growth improving in second half of 2016 as impact of commodity

price plunge fades

Slight improvement in 2017 on rebound in U.S., Canada, Brazil,

and Russia, but deleveraging and restructuring headwinds persist,

particularly in EM

Relative stability in currencies after 2014‒2015 rout fosters

disinflation in EM, contributes to modest U.S. inflation lift

Fed normalization creep to continue, while European Central

Bank (ECB) and Bank of Japan (BoJ) rethink quantitative

easing (QE); EM central bank outlooks mixed, though easing

predominates as inflation falls

13

Important Information

This material is being furnished by T. Rowe Price for general informational purposes only. Under no circumstances should the content, in whole or in part, be copied

or redistributed without consent from T. Rowe Price. The material does not constitute a distribution, an offer, an invitation, recommendation or solicitation to sell or

buy any securities in any jurisdiction. The material has not been reviewed by any regulatory authority in any jurisdiction. The material does not constitute advice of

any nature and prospective investors are recommended to seek independent legal, financial, and tax advice before making any investment decision.

The views contained herein are as of November 2016 and may have changed since that time.

Past performance cannot guarantee future results.

Australia—Issued in Australia by T. Rowe Price International Ltd (ABN 84 104 852 191), Level 50, Governor Phillip Tower, 1 Farrer Place, Suite 50B, Sydney, NSW

2000, Australia. T. Rowe Price International Ltd is exempt from the requirement to hold an Australian financial services licence in respect of the financial services it

provides in Australia. T. Rowe Price International Ltd is authorised and regulated by the UK Financial Conduct Authority under UK laws, which differ from Australian

laws. For Wholesale Clients only.

Canada—Issued in Canada by T. Rowe Price (Canada), Inc. T. Rowe Price (Canada), Inc.’s investment management services are only available to Accredited

Investors as defined under National Instrument 45-106. T. Rowe Price (Canada), Inc. enters into written delegation agreements with affiliates to provide investment

management services.

DIFC—Issued in the Dubai International Financial Centre by T. Rowe Price International Ltd. This material is communicated on behalf of T. Rowe Price International

Ltd by its representative office which is regulated by the Dubai Financial Services Authority. For Professional Clients only.

EEA—Issued in the European Economic Area by T. Rowe Price International Ltd, 60 Queen Victoria Street, London EC4N 4TZ which is authorised and regulated by

the UK Financial Conduct Authority. For Professional Clients only.

Hong Kong—Issued in Hong Kong by T. Rowe Price Hong Kong Limited, 21/F, Jardine House, 1 Connaught Place, Central, Hong Kong. T. Rowe Price Hong Kong

Limited is licensed and regulated by the Securities & Futures Commission. For Professional Investors only.

Singapore—Issued in Singapore by T. Rowe Price Singapore Private Ltd., No. 501 Orchard Rd, #10-02 Wheelock Place, Singapore 238880. T. Rowe Price

Singapore Private Ltd. is licensed and regulated by the Monetary Authority of Singapore. For Institutional and Accredited Investors only.

Switzerland—Issued in Switzerland by T. Rowe Price (Switzerland) GmbH ("TRPSWISS"), Talstrasse 65, 6th Floor, 8001 Zurich, Switzerland. For Qualified

Investors only.

USA (public)—Issued in the USA by T. Rowe Price Associates, Inc., and by T. Rowe Price Investment Services, Inc., 100 East Pratt Street, Baltimore, MD, 21202.

T. ROWE PRICE, INVEST WITH CONFIDENCE and the Bighorn Sheep design are, collectively and/or apart, trademarks or registered trademarks of T. Rowe Price

Group, Inc. in the United States, European Union, and other countries. This material is intended for use only in select countries.

77306

THANK YOU.